To Estimate the Biscuits Industry and identify the critical success factors OBJECTIVE OF THE STUDY To determine the key players operating in the industry by estimating their volumes and critically evaluate their distribution practices. Scope of the study: The study shall entail the following: Complete understanding of the category and industry. - The key players with brand wise volumes - Availability & Visibility figures of key players by channels Understanding of the distribution process and the components of the distribution chain: - The players: Distributor, trade (Wholesale & retail), Salesman. - Various channels and their dynamics (wholesale, convenience, grocer, tea stall/restaurant…).

Report Distribution Biscuits

Nov 19, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

To Estimate the Biscuits Industry and identify the critical success factors

OBJECTIVE OF THE STUDY

To determine the key players operating in the industry by estimating their

volumes and critically evaluate their distribution practices.

Scope of the study: The study shall entail the following:

Complete understanding of the category and industry.

- The key players with brand wise volumes

- Availability & Visibility figures of key players by channels

Understanding of the distribution process and the components of the

distribution chain:

- The players: Distributor, trade (Wholesale & retail), Salesman.

- Various channels and their dynamics (wholesale, convenience,

grocer, tea stall/restaurant…).

- Distribution infrastructure (vehicle, sales force…)

- Distribution norms and practices: (inventory, billing, credit, delivery,

frequency of service…)

- Strengths and weaknesses of various players as regard distribution.

Understanding of various trade schemes in the market.

To Estimate the Biscuits Industry and identify the critical success factors

- Critically analyze the schemes as regards their design and

effectiveness.

Recommendations for ITC to formulate a distribution strategy to align

with industry needs.

Location of the Study: Saharanpur.

Duration of the Study: 6 weeks

Methodology:

The project be broadly divided into 3 parts:

Part 1: Understanding of the distribution systems at different WD point

(across companies).

Part 2: Collection of data regarding industry figures, key players,

availability, schemes etc by carrying out a detailed market survey.

Part 3: Collation of data and preparation of recommendations.

Part 1 and Part 2 should be carried out simultaneously.

To Estimate the Biscuits Industry and identify the critical success factors

L I T E R A T U R E R E V I E W

MARKETING CHANNEL

Marketing channel are sets of interdependent organizations, involved in the

process of making a product or service available for use or consumption.

From the outset, it should be recognized that not only do marketing channels

satisfy demand of supplier goods and services at right place, quantity,

quality and price, but they also stimulate demand through the potential

activities of the unit (e.g., retailer, manufacturer, representative, sales officer,

wholesaler comprises them. Therefore the channel should be viewed as an

orchestrated network that creates value for the use of consumers through

the generation of firm, possession, time and place utilities. Members of

marketing channel perform a number of key functions. Some of the functions

are:

1. Information

2. Promotion

3. Negotiation

4. Ordering

5. Financing

6. Risk taking

7. Physical possession

To Estimate the Biscuits Industry and identify the critical success factors

8. Payment

1. Information: the collection and dissemination of marketing research

information about potential and current customer, competitors and the

other forces in market environment.

2. Promotion: The development and pervasive communication design to

attract customer to its offer.

3. Negotiation: The attempt to reach the final agreement on price and

other form so that transfer of ownership or possession can be

affected.

4. Ordering: Marketing channel member’s communication of intervention

to buy to the manufacturer goods.

5. Financing: the acquisition and allocation of funds required to finance

inventories at different links of marketing channel.

6. Physical possession: The successive storage and movement of

physical product from raw materials to the final customers.

7. Payment: Buyers payment of the bill to the seller through banks and

other financial institutions.

To Estimate the Biscuits Industry and identify the critical success factors

DISTRIBUTION STRATEGIES

Companies have to decide on the number of intermediaries to use in their

channel. The various strategies that are available are as follows:

Exclusive distribution

Selective distribution

Intensive distribution

Exclusive distribution: It involves severely limiting the number of

intermediaries handling the company goods or services. It is used when the

producer wants to maintain a great deal of control over the source level and

service output offered by the reseller. Often it involves exhaustive dealer

agreement in which dealer agrees not to carry competitive brand. By

generating exclusive distribution, the product hopes to obtain more

aggressive and knowledge selling. Exclusive distribution tends to enhance

the product image and attain larger markups. It requires greater partnership

between the seller and the reseller and it is found in major industrial

products, automobiles sector etc.

Selective distribution: It involves more than a few and less than all of the

intermediaries who are willing to carry a particular product. It is use both by

established companies and by new companies seeking to obtain distributors.

In this distribution the company does not have to dissipate its effort over

To Estimate the Biscuits Industry and identify the critical success factors

many outlet, rather it can develop a good working relation with its selected

intermediaries and expect a better than average selling effort with more

control and less cost than intensive distribution.

Intensive distribution: This involves placing the goods or services in as

many outlets as possible. When the consumers require a great deal of

location convenience. This strategy is generally used for consumer items like

tobacco products, soap, snacks and cosmetics.

To Estimate the Biscuits Industry and identify the critical success factors

DISTRIBUTION CHANNEL

Distribution issues come into play heavily in deciding brand level strategy. In

order to secure a more exclusive brand label, for example, it is usually

necessary to sacrifice volume—it would do no good for Mercedes-Benz to

create a large number of low priced automobiles. Some firms can be very

profitable going for quantity where economies of scale come into play and

smaller margins on a large number of units add up—e.g., McDonald’s

survives on much smaller margins than upscale restaurants, but may make

larger profits because of volume. Some firms choose to engage in a niching

strategy where they forsake most customers to focus on a small segment

where less competition exists (e.g., clothing for very tall people).

Distribution Objectives

Interrelated objectives: A firm’s distribution objectives will ultimately be highly

related—some will enhance each other while others will compete. For

example, as we have discussed, more exclusive and higher service

distribution will generally entail less intensity and lesser reach. Cost has to

be traded off against speed of delivery and intensity (it is much more

expensive to have a product available in convenience stores than in

supermarkets, for example).

Narrow vs. wide reach: The extent to which a firm should seek narrow

(exclusive) vs. wide (intense) distribution depends on a number of factors.

To Estimate the Biscuits Industry and identify the critical success factors

One issue is the consumer’s likelihood of switching and willingness to

search. For example, most consumers will switch soft drink brands rather

than walking from a vending machine to a convenience store several blocks

away, so intensity of distribution is essential here. However, for sewing

machines, consumers will expect to travel at least to a department or

discount store, and premium brands may have more credibility if they are

carried only in full service specialty stores.

Retailers involved in a more exclusive distribution arrangement are likely to

be more “loyal”—i.e., they will tend to

Recommend the product to the customer and thus sell large quantities;

Carry larger inventories and selections; and

Provide more services

Thus, for example, Compaq in its early history instituted a policy that all

computers must be purchased through a dealer. On the surface, Compaq

passed up the opportunity to sell large numbers of computers directly to

large firms without sharing the profits with dealers. On the other hand,

dealers were more likely to recommend Compaq since they knew that

consumers would be buying these from dealers. When customers came in

asking for IBMs, the dealers were more likely to indicate that if they really

wanted those, they could have them—“But first, let’s show you how you will

get much better value with a Compaq.”

To Estimate the Biscuits Industry and identify the critical success factors

Distribution opportunities: Distribution provides a number of opportunities for

the marketer that may normally be associated with other elements of the

marketing mix. For example, for a cost, the firm can promote its objective by

such activities as in-store demonstrations/samples and special placement

(for which the retailer is often paid). Placement is also an opportunity for

promotion—e.g., airlines know that they, as “prestige accounts,” can get very

good deals from soft drink makers who are eager to have their products

offered on the airlines. Similarly, it may be useful to give away, or sell at low

prices, certain premiums (e.g., T-shirts or cups with the corporate logo.) It

may even be possible to have advertisements printed on the retailer’s bags

(e.g., “Got milk?”)

Other opportunities involve “parallel” distribution (e.g., having products sold

both through conventional channels and through the Internet or factory outlet

stores). Partnerships and joint promotions may involve distribution (e.g.,

Burger King sells clearly branded Hershey pies).

Deciding on a strategy. In view of the need for markets to be balanced, the

same distribution strategy is unlikely to be successful for each firm. The

question, then, is exactly which strategy should one use? It may not be

obvious whether higher margins in a selective distribution setting will

compensate for smaller unit sales. Here, various research tools are useful.

In focus groups, it is possible to assess what consumers are looking for and

which attributes are more important. Scanner data, indicating how frequently

various products are purchased and items whose sales correlate with each

To Estimate the Biscuits Industry and identify the critical success factors

other may suggest the best placement strategies. It may also, to the extent

ethically possible, be useful to observe consumers in the field using products

and making purchase decisions.

Here, one can observe factors such as:

How much time is devoted to selecting a product in a given category,

How many products are compared,

What different kinds of products are compared or are substitutes (e.g.,

frozen yogurt vs. cookies in a mall), and

What are “complementing” products that may cue the purchase of others

if placed nearby?

Channel members—both wholesalers and retailers—may have valuable

information, but their comments should be viewed with suspicion as they

have their own agendas and may distort information.

Direct Marketing

We consider direct marketing early in the term as a “contrast” situation

against which later channels can be compared. In general, you cannot save

money by “eliminating the middleman” because intermediaries specialize in

performing certain tasks that they can perform more cheaply than the

manufacturer. Most grocery products are most efficiently sold to the

consumer through retail stores that take a modest mark-up—it would not

To Estimate the Biscuits Industry and identify the critical success factors

make sense for manufacturers to ship their grocery products in small

quantities directly to consumers.

Intermediaries perform tasks such as

Moving the goods efficiently (e.g., large quantities are moved from

factories or warehouses to retail stores);

Breaking bulk (manufacturers sell to a modest number of wholesalers in

large quantities—quantities are then gradually broken down as they

make their way toward the consumer);

Consolidating goods (retail stores carry a wide assortment of goods from

different manufacturers—e.g., supermarkets span from toilet paper to

catsup); and

Adding services (e.g., demonstrations and repairs).

Direct marketers come in a variety of forms, but their categorization is

somewhat arbitrary. The main thing to consider here is each firm’s functions

and intentions. Some firms sell directly to consumers with the express

purpose of eliminating retailers that supposedly add cost (e.g., Dell

Computer). Others are in the business not so much to save on costs, but

rather to reach groups of consumers who are not easily reached through the

stores. Others—e.g., online travel agents or check printers—provide heavily

customized services where the user can perform much of the work.

Telemarketers operate by making the promotion an integral part of the

To Estimate the Biscuits Industry and identify the critical success factors

process—you are explained the benefits of the product in an advertisement

or infomercial and you then order directly in response to the promotion.

Finally, some firms combine these roles—e.g., Geico is a customizer, but

also claims, in principle, to cut out intermediaries.

There are certain circumstances when direct marketing may be more useful

—e.g., when absolute margins are very large (e.g., computers) or when a

large inventory may be needed (e.g., computer CDs) or when the customer

base is widely dispersed (e.g., bee keepers).

Direct marketing offers exceptional opportunities for segmentation because

marketers can buy lists of consumer names, addresses, and phone-numbers

that indicate their specific interests. For example, if we want to target auto

enthusiasts, we can buy lists of subscribers to auto magazines and people

who have bought auto supplies through the mail. We can also buy lists of

people who have particular auto makes registered.

To Estimate the Biscuits Industry and identify the critical success factors

CHANNEL STRUCTURE

Paths to the customer

For most products and situations, it is generally more efficient for a

manufacturer to go through a distributor rather than selling directly to the

customer. This is especially the case when consumers need to have variety

and assortment (e.g., consumer would like to buy not just toothpaste but

also other personal hygiene products, and even other grocery products at

the same place), when products are bought in small volumes or at low value

(e.g., a candy bar sells for less than Rs. 20), or even intermediaries have

skills or resources that the manufacturer does not (a sales force,

warehousing, and financing). Nevertheless, there are situations when these

conditions are not met—most typically in industrial settings. As an extreme

case, most airlines are perfectly happy only being able to buy aircraft and

accessories from Boeing and would prefer not to go through a retailer—

particularly since the planes are often highly customized. More in the "gray"

area, it may or may not be appropriate to sell microcomputers directly to

consumers rather than going through a distributor—the costs of providing

those costs may be roughly comparable to the margin that a distributor

would take.

Potential channel structures

To Estimate the Biscuits Industry and identify the critical success factors

Channel structures can assume a variety of forms. In the extreme case of

Boeing aircraft or commercial satellites, the product is made by the

manufacturer and sent directly to the customer’s preferred delivery site. The

manufacturer, may, however, involve a broker or agent who handles

negotiations but does not take physical possession of the property. When

deals take on a smaller magnitude, however, it may be appropriate to

involve retailer--but no other intermediary. For example, automobiles, small

planes, and yachts are frequently sold by the manufacturer to a dealer who

then sends directly to the customer. It does not make sense to deliver these

bulky products to a wholesaler only to move them again. On the other hand,

it would not make sense for a Mumbai customer to fly to Delhi, buy a car

there, and then drive it home. As the need for variety increases, a

wholesaler may then be introduced. For example, an office supply store

needs to sell more merchandise than any one manufacturer can produce.

Therefore, a wholesaler will buy a very large quantity of binders, file folders,

staplers, reams of paper, glue sticks, and similar products and sell this in

smaller quantities—say 200 staplers at a time—to the office supply store,

which, in turn, may go to another wholesaler who has acquired telephones,

typewriters, and photocopiers. Note that more than one wholesaler level may

be involved—a local wholesaler serving the Inland Empire may buy from

each of the two wholesalers listed above and then sell all, or most, of the

products needed by local office supply stores. Finally, even in longer

channels, agents or brokers may be involved. This, in particular, will happen

when the owner of a small, entrepreneurial company has more experience

To Estimate the Biscuits Industry and identify the critical success factors

with technology than with businesses negotiations. Here, the manufacturer

can be freed, in return for paying the agent, from such tasks, allowing him or

her to focus on what he or she does well.

Criteria in selecting channel members

Typically, the most important consideration whether to include a potential

channel member is the cost at which he or she can perform the required

functions at the needed level of service. For example, it will be much less

expensive for a specialty foods manufacturer to have a wholesaler get its

products to the retailer. On the other hand, it would not be cost effective for

Procter & Gamble and Wal-Mart to involve a third party to move their

merchandise—Wal-Mart has been able to develop, based on its information

systems and huge demand volumes, a more efficient distribution system.

Note the important caveat that cost alone is not the only consideration

—premium furniture must arrive in the store on time in perfect condition, so

paying more for a more dependable distributor would be indicated. Further,

channels for perishable products are often inefficiently short, but the

additional cost is needed in order to ensure that the merchandise moves

quickly. Note also that image is important—Wal-Mart could very efficiently

carry Rolex watches, but this would destroy value from the brand.

"Piggy-backing." A special opportunity to gain distribution that a

manufacturer would otherwise lack involves "piggy-backing." Here, a

manufacturer enlists another manufacturer that already has a channel to a

To Estimate the Biscuits Industry and identify the critical success factors

desired customer base, to pick up products into an existing channel. For

example, a manufacturer of rhinoceros and hippopotamus shampoo might

be able to reach zoos by approaching a manufacturer of crocodile teeth

cleaning supplies that already reaches this target. In the case of reciprocal

piggy-backing, the shampoo manufacturer might then, in turn, bring the teeth

cleaning supplies through its existing channel to exotic animal veterinarians.

Parallel Distribution. Most manufacturers find it useful to go through at

least one wholesaler in order to reach the retailer, and it is simply not

efficient for Colgate to sell directly to pathetic little "mom and pop"

neighborhood stores. However, large retail chains such as K-Mart and

Ralph’s buy toothpaste and other Colgate products in such large volumes

that it may be efficient to sell directly to those chains. Thus, we have a

"parallel" distribution network whereby some retailers buy through a

distributor and others do not. Note that we may also be tempted to add a

direct channel—e.g., many clothing manufacturers have factory outlet

stores. However, note that the full service retailers will likely object to being

"undercut" in this manner and may decide to drop or give less emphasis to

the brand. It may be possible to minimize this contract by precautions such

as (1) having outlet stores located in vacation areas not within easy access

of most people, (2) presenting the merchandise as being slightly irregular,

and/or (3) emphasizing discontinued brands and merchandise not sold in

regular stores.

To Estimate the Biscuits Industry and identify the critical success factors

Evaluating Channel Performance. The performance of channel members

should be periodically monitored—a channel member may have looked

attractive earlier but may not, in practice be able to live up to promises. (This

can be either because of complacency or because the channel member

simply did not realize the skills and resources needed to perform to

standards). Thus, performance level (service outputs) and costs should be

evaluated. Further, changes in technology or in the market place may make

it worthwhile to shift certain functions to another channel member (e.g., a

distributor has expanded its coverage into another region or may have

gained or lost access to certain retail chains). Finally, the extent to which

compensation is awarded in proportion to performance should be

reassessed—e.g., a distributor that ends up holding inventory longer or

taking on more returns may need additional compensation.

To Estimate the Biscuits Industry and identify the critical success factors

DISTRIBUTION OPPORTUNITIES

First of all, we must consider what is realistically available to each firm. A

small manufacturer of potato chips would like to be available in grocery

stores nationally, but this may not be realistic. We need to consider, then,

both who will be willing to carry our products and whom we would actually

like to carry them. In general, for convenience products, intense distribution

is desirable, but only brands that have a certain amount of power—e.g., an

established brand name—can hope to gain national intense distribution.

Note that for convenience goods, intense distribution is less likely to harm

the brand image—it is not a problem, for example, for Haagen Dazs to be

available in a convenience store along with bargain brands—it is expected

that people will not travel much for these products, so they should be

available anywhere the consumer demands them. However, in the category

of shopping goods, having Rolex watches sold in discount stores would be

undesirable—here, consumers do travel, and goods are evaluated by

customers to some extent based on the surrounding merchandise.

Distribution Options

Major brand standard convenience good

Moderately intense distribution inappropriate; selective distribution

Premium brand shopping good

To Estimate the Biscuits Industry and identify the critical success factors

Selective distribution

Niche brand

National moderately intense distribution unrealistic; local or "invited"

national distribution

Minor brand shopping good

Moderately intense distribution (e.g., TVs in discount store)

Major brand shopping good

National regional intense distribution unrealistic; local or "invited" national

distribution

Minor brand convenience good

Intense distribution possible but not appropriate; selective preferred

Upscale brand convenience good

Intense distribution (limiting distribution would mean forfeiting brand

status)

To Estimate the Biscuits Industry and identify the critical success factors

PRODUCT TYPE

The product life cycle. In general, a brand can expect lesser distribution in

its early stages—fewer retailers are motivated to carry it. Similarly, when a

product category is new, it will be available in fewer stores—e.g., in the early

days, computer disks were available only in specialty stores, but now they

can be found in supermarkets and convenience stores as well. Certain

products that are not well established may have to get their start on

"infomercials," only slowly getting entry into other types out outlets. (Please

see PowerPoint chart).

Brief review of distribution intensity issues:

Full service retailers tend dislike intensive distribution.

Low service channel members can "free ride" on full service sellers.

Manufacturers may be tempted toward intensive distribution—

appropriate only for some; may be profitable in the short run.

Market balance suggests a need for diversity in product categories where

intensive distribution is appropriate.

Service requirements differ by product category.

To Estimate the Biscuits Industry and identify the critical success factors

CHOOSING DISTRIBUTION METHODS

Once you have selected and developed a unique product or business idea,

correctly positioned and targeted it to buyers, and developed your packaging

and pricing, the selection of distribution channels and sales representation is

key to successful marketing.

It's fairly easy to change many of your marketing tactics and strategies on a

periodic basis; pricing, packaging, and product mix are among these flexible

choices. However, distribution and sales decisions, once made, are much

more difficult to change. And distribution affects the selection and utilization

of all other marketing tools.

There is a wide variety of possible distribution channels, including:

Retail outlets owned by your company or by an independent merchant

or chain

Wholesale outlets of your own or those of independent distributors or

brokers

Sales force compensated by salary, commission, or both

Direct mail via your own catalog or flyers

Telemarketing on your own or through a contract firm

Cybermarketing, surfing the newest frontier

To Estimate the Biscuits Industry and identify the critical success factors

TV and cable direct marketing and home shopping channels

Distribution choices for a service business follow the same lines as those for

a physical product. For example, financial planning services may be offered

from printed material, sold at retail by consultants, delivered electronically by

computer, or relayed by phone, fax or mail.

Steps for selecting distribution and sales force representation include:

Identify how competitors' products are sold.

Analyze strengths, weaknesses, opportunities, and threats for your

business.

Examine costs of channels and sales force options.

Determine which distribution options match your overall marketing

strategy.

Prioritize your distribution choices.

This exercise is applicable for both large and small businesses.

Matching Distribution to Your Goals

A small company must work harder at focusing limited resources, especially

with distribution and sales force options. In some cases, the only sales force

option is for the owner to do it himself or herself, as in a small retail shop, or

consulting/service businesses.

To Estimate the Biscuits Industry and identify the critical success factors

Some distribution channels and sales force options may be attractive, but

off-strategy for the small company. A list of all possible distribution channels

and accompanying sales force options should be matched against company

marketing objectives.

For example, a company selling gourmet cooking equipment has many

options for distribution and sales force representation, including:

Company retail stores, with company sales personnel

Specialty food stores, with sales brokers

Department stores, with sales brokers

Hardware stores, with sales brokers

Specialty chains (e.g., Williams-Sonoma, Crate & Barrel), with sales

brokers

Direct mail, with company personnel

Distributors, with company sales managers, brokers, distributor sales

reps

The company's products are positioned as the highest-quality cookware,

used by celebrity chefs and guaranteed for the life of the end user/buyer.

Target end users/buyers are upscale, well-educated, urban consumers who

read upscale food magazines (e.g., Gourmet, Food & Wine), dine out at

gourmet restaurants, drink wine, travel, drive expensive cars, and spend

To Estimate the Biscuits Industry and identify the critical success factors

heavily on luxury purchases. Ideally, the company wants their products

distributed through every upscale channel that caters to this exclusive target

group.

Because of the positioning of the gourmet cookware, the company believed

that hardware stores and direct mail were not consistent with the image and

reputation that they were trying to establish with their positioning. Company

retail stores, while desirable, were financially risky and too expensive at the

early stage of development. Distributors were also eliminated because of the

time and knowledge required of distributor sales personnel, coupled with the

belief that distributors could not be encouraged to learn enough or devote

enough time to the product line. In addition, the estimated 35 percent to 40

percent discount with shipping expense to distributors was financially

unattractive.

The company decided the best distribution channels were direct sales to

specialty stores and upscale department stores such as Marshall Field's,

Bloomingdale's, and Nieman-Marcus. Their sales force consisted of three

regional managers with professional cooking experience, who also did

demos in stores with the cookware. In addition, the company had the extra

margin available to afford this highly trained and motivated sales force since

distributors were not utilized.

To Estimate the Biscuits Industry and identify the critical success factors

Costs of Distribution Channels

Obviously, financial resources and cost-effectiveness are important in

considering distribution and sales force options. What can you afford, and

what will give you the most bang for your buck?

For example, Life Designs, an independent architect specializing in

residential work, has identified three primary distribution channels for its

residential design services and estimated costs for each one:

Media sales: This channel is composed of competitors who advertise in

local city and county magazines, newspapers, and real-estate flyers,

subdivided by home-design only firms and home-design and industrial-

design firms. Ad inquiries are referred by the various media groups

carrying the ads. This quasi-sales force is paid on commission for

referrals that turn into jobs.

Contractors and developers: This distribution channel is composed of

referrals from contractors and developers who receive a commission

from home owners and buyers. The contractors and developers are the

"sales" personnel, who expect a commission and entertainment.

University design department: This is a closed distribution channel for

architectural students and professors only. It is not open to any other

architects. However, this architect's reputation may be enhanced by

occasional lectures at the university.

To Estimate the Biscuits Industry and identify the critical success factors

Life Designs knows from talking with media suppliers, competitors, and

contractors that the least expensive distribution channel is sales from

contractors and developers. However, the frequency of sales referrals and

volume of business is unpredictable. It is also somewhat out of the

architect's control because the business is dependent upon many outside

variables such as the economy, style of home wanted by buyers, etc.

Life Designs decides to work with two distribution channels concurrently —

both media and the contractor/developer channels, since most of the

spending commitment is for media. The contractor/developer channel

requires personal time and some minor entertainment expenses (wining and

dining the contractors). This one-man architect firm cannot spare much free

time, and media spending will provide a good alternative when he is busy

with a project.

Prioritizing Distribution Options

In some cases, a small business can pursue distribution into several

different channels. However, most small businesses must prioritize

distribution channel and sales force options over several years of growth and

evolving resources for the company. For example, food supplements and

vitamins are sold through a multitude of channels, including:

multi-level "network" organizations, with company and independent sales

reps

To Estimate the Biscuits Industry and identify the critical success factors

Health food stores, with company reps and sales brokers

Department stores, with company reps and sales brokers

Drug stores, with company reps and sales brokers

Grocery stores, with company reps and sales brokers

Mass merchandise stores, with company reps and sales brokers

Club member warehouse stores, with company reps and sales brokers

Direct mail, with company personnel

Distributors, with company sales managers, brokers, distributor sales

reps

Doctors’ offices, with company sales managers, brokers, distributor sales

reps

It is not always possible for a company, small or large, to take advantage of

all possible channels that match the marketing strategy it wants to achieve.

Financial considerations aside, it may be wise to prioritize the orderly

development and attack each distribution channel in order of easiest entry

and least competitive resistance, for example.

Other factors such as geographic proximity, ability and availability of

management to control many different channels simultaneously, availability

of experienced sales reps, marketing experience by channel, competitive

To Estimate the Biscuits Industry and identify the critical success factors

strengths by channel, manufacturing capacities, and product life cycles by

channel should be considered.

For small companies, key factors to prioritize your choice of channels

include a shorter list:

Financial resources and risks ("How much money do we have to risk

against our objectives and marketing programs?")

Competitors’ strengths and market share ("Are they big enough and

mean enough to hurt us, and what are their objectives?")

Management experience by channel ("What do we know about each

channel's opportunities and threats?")

Product positioning to target buyers ("Will the strengths of our product

uniqueness help sell it to interested buyers and can we communicate our

uniqueness effectively?")

To Estimate the Biscuits Industry and identify the critical success factors

INTRODUCTION

The Indian bakery market is still in a nascent stage. In a country where

average per capita income hovers around US$ 450 per annum, bakery items

are not very high on the list of priorities for the masses. Low margins, and a

high level of fragmentation characterize the bakery segment. Awareness is

nearly 100%, however, penetration is lower in rural areas at 15-20% and at

60% in urban areas. This is mainly because these products are consumed

as snacks, and do not form part of the main course meal.

However, over the past few years’ bakery products have shown a marked

improvement in volumes and customer base. But this growth has mainly

come from bread and biscuits segment. Infact one can safely say that bread

and biscuits constitute around 75% of the Rs 70 bn Indian bakery market.

Bread and biscuits have grown largely because these products are

characterized by the huge presence of unorganized sector (60%), as they

were reserved for the small-scale industry earlier. Also, bread to some

extent is consumed as a food supplement in the urban areas.

The Pie

Product Market size

(Rs m)

Market size

( '000

tonnes)

Growt

h

(%)

Penetratio

n

Urba Rur

To Estimate the Biscuits Industry and identify the critical success factors

n al

Bakery Items 70,000 - 8% 60% 20%

Biscuits 35,000 1,100 7%

Cakes 750 70 4-5%

Bread 11,000 1,400 3-4%

Other bakery products like cakes and pastries are also on the growth mode,

but the growth rates leave much to be desired. These products do not yet

have a mass appeal and are basically centred on the urban areas. In these

two categories also local manufacturers hold a sizeable chunk of the market.

Over the last few years, branded companies like Parle and Britannia have

upped their ante and introduced new products with slick packaging in order

to grow the market. These companies’ prospects were also buoyed post

deregulation of the biscuit industry in April 1997. Before that, the biscuit

segment was reserved for the small-scale industries.

Realising the mental block against premium bakery products these

companies employed a two-pronged strategy, especially in biscuits. To gain

volumes these companies continued to back glucose biscuits aimed at the

mass, and for margins they continued to stack up their portfolios with new

brands and variants. As a result, the unorganised segment that dominated

To Estimate the Biscuits Industry and identify the critical success factors

over 60% of the biscuit market in 1995-96, now sees its share shrunk to

around 50% levels.

The biscuit market is now estimated to be 1.1 m tonnes, valued at over 35

bn. Britannia and Parle control 38% and 29% respectively of the organised

biscuits market. Volumes, brand loyalty and strong distribution networks

drive this market, which is growing at 6-7% annually.

On the other hand, the 1.4 m tonnes bread market valued at Rs 11 bn, is

dominated by local manufacturers (80%). Market growth is 3-4%, but it is

much higher for organised sector (brands). Brands like Modern and Britannia

are major players in the bread market (10% and 5% market share

respectively), and together they account for 90% of the organised bread

market.

With Hindustan Lever’s acquisition of Modern Foods, this segment is likely to

see increased market penetration and rivalry in the years to come. HLL

plans to enter the bakery segment in a big way and this should be a key

driver for the industry’s growth.

According to estimates, the bakery market is poised to touch Rs 100 bn by

the year 2005 (a CAGR growth of 9.3% from current levels). However, with

the current slowdown faced by the FMCG sector as whole, the growth rates

have hit a speed breaker. It is only when the recent good monsoons give

impetus to demand, the segment would see its fortunes reviving. But in the

near term such relief looks unlikely.

To Estimate the Biscuits Industry and identify the critical success factors

In the longer term the bakery segment is likely to see competition getting

even more intense with new entrants especially MNC’s. Marketing wars

would get even more cut throat as players try to convert consumers of

unbranded products to branded products. The urban areas are likely to

continue seeing new high end products in all categories of the bakery

industry. But the road for this segment’s growth would be slow and steady.

ADVERTISING IN THE BISCUITS

Biscuit advertising on television is pretty seasonal with the spends

peaking in the first and last quarter each year.

Britannia industries and Parle products top the advertiser list with

nearly 68 per cent of the advertising in this category in 2003.

Biscuit advertisers prefer advertising in drama/soap, feature films and

comedies which make up for 54 per cent of the spends in this

category in 2003.

To Estimate the Biscuits Industry and identify the critical success factors

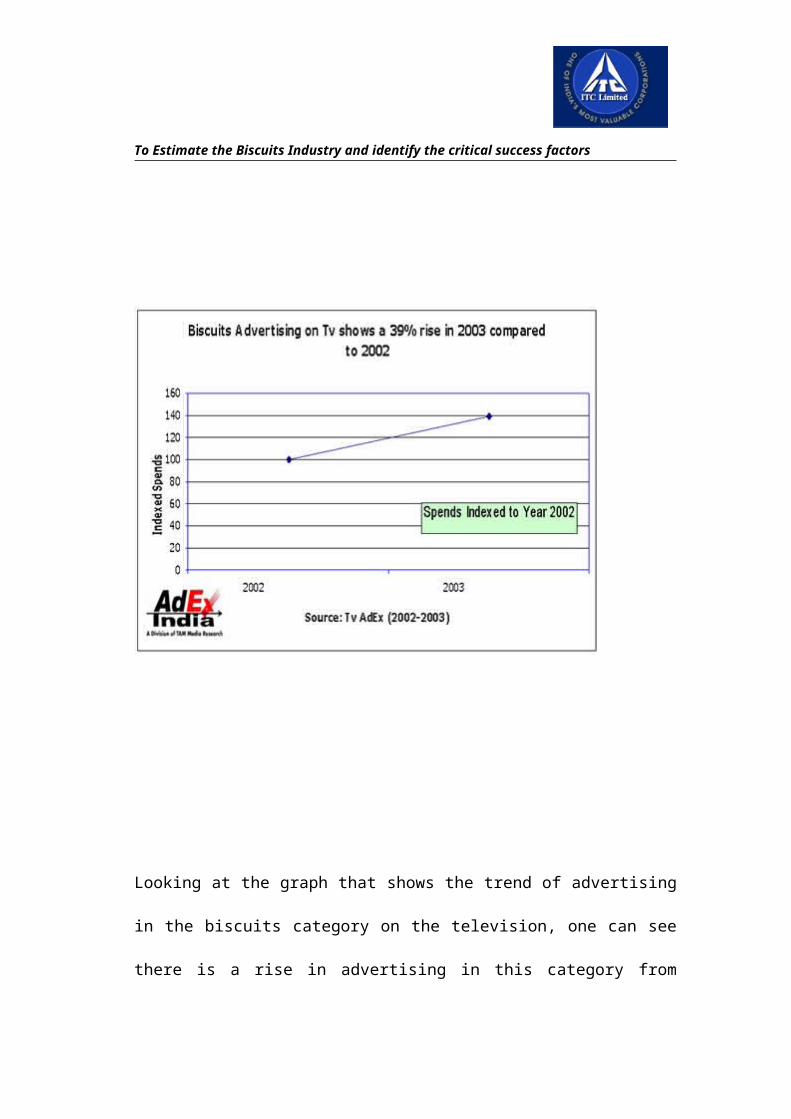

Looking at the graph that shows the trend of advertising in the biscuits

category on the television, one can see there is a rise in advertising in this

category from 2000 onwards. The graph shows the indexed spends of the

biscuits category on television advertising since 2000.

To Estimate the Biscuits Industry and identify the critical success factors

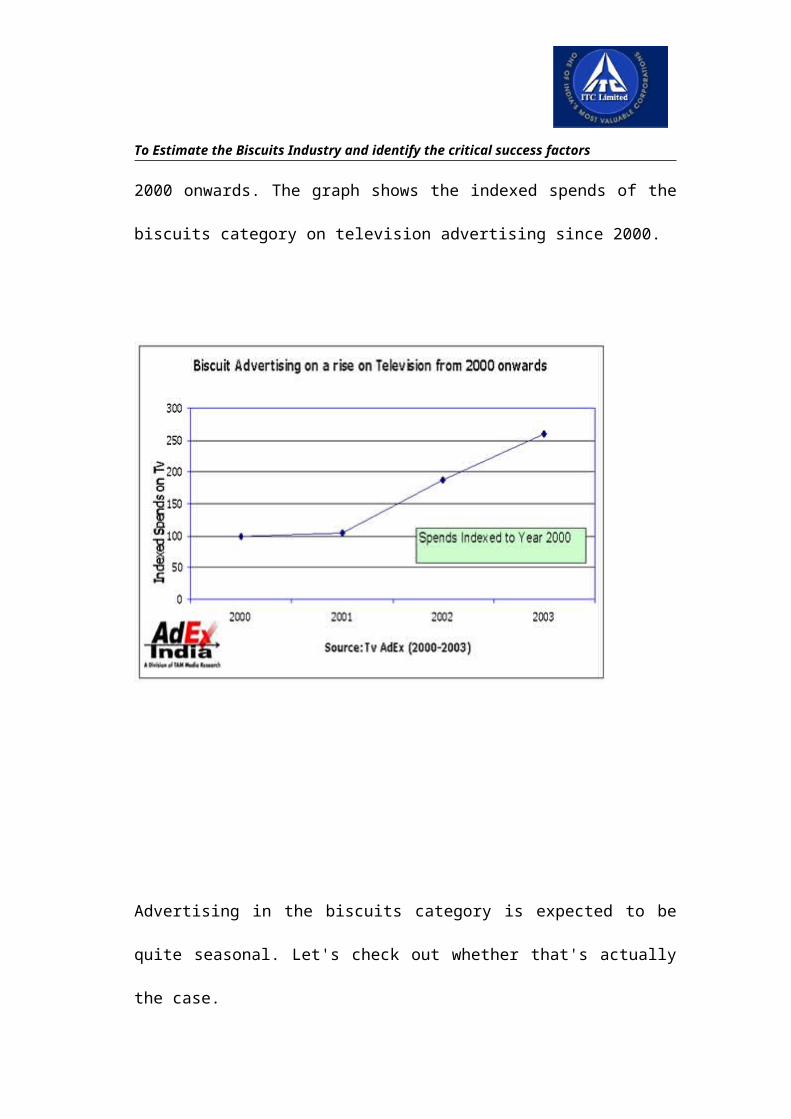

Advertising in the biscuits category is expected to be quite seasonal. Let's

check out whether that's actually the case.

To Estimate the Biscuits Industry and identify the critical success factors

The graph confirms that biscuit advertising on television is pretty seasonal

with the spends peaking in the first and the last quarter each year.

Let's look at the advertisers, which dominate in this category. The graph

shows that Britannia Industries ltd and Parle products tops the advertiser list

with nearly 35 per cent and 33 per cent of the advertising respectively. Surya

food and Agro pvt ltd at the third position, ITC ltd at the fourth position,

Hindustan Lever ltd at the fifth position, Heinz at the sixtrh position with

nearly 15.6 per cent, 4.7 per cent, 4.4 per cent and 1.7 per cent of the

To Estimate the Biscuits Industry and identify the critical success factors

advertising share. Other advertisers are Anmol Biscuit pvt ltd, Lancer food

products, Dukes biscuits and Apsara food industries pvt ltd.

Are there any particular program genres, which biscuit advertisers prefer?

Let's look at the chart below for answers.

To Estimate the Biscuits Industry and identify the critical success factors

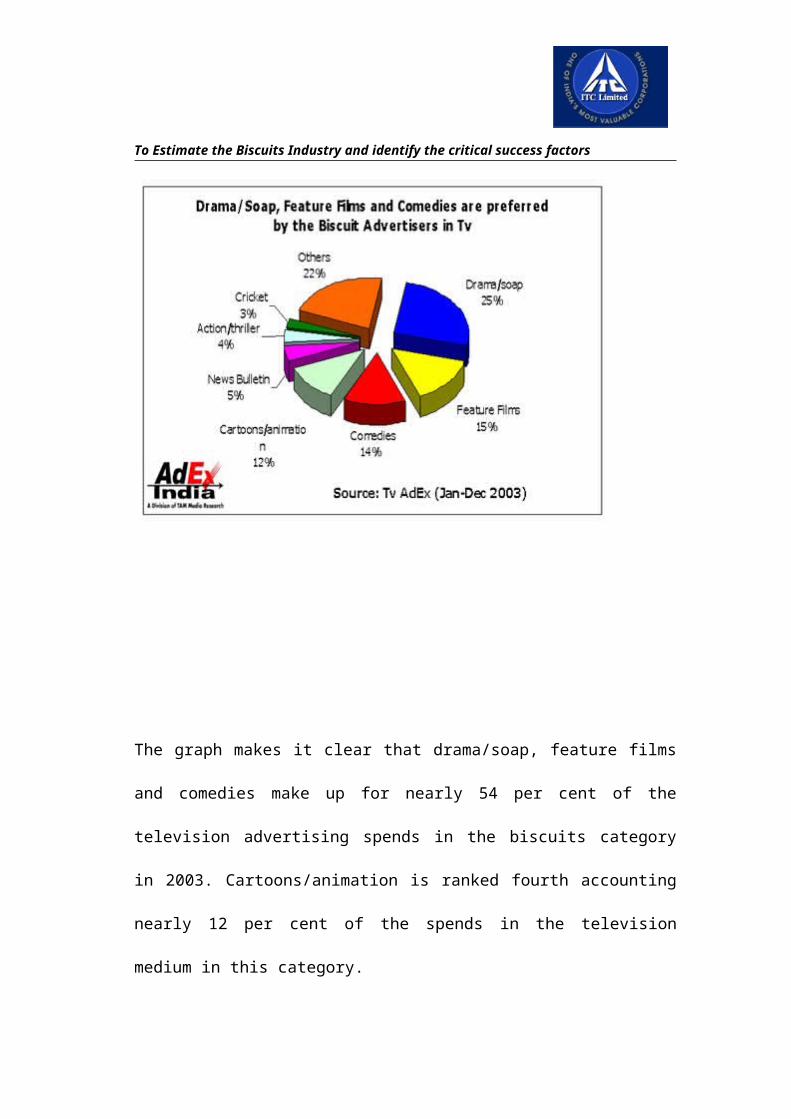

The graph makes it clear that drama/soap, feature films and comedies make

up for nearly 54 per cent of the television advertising spends in the biscuits

category in 2003. Cartoons/animation is ranked fourth accounting nearly 12

per cent of the spends in the television medium in this category.

To Estimate the Biscuits Industry and identify the critical success factors

MAJOR PLAYERS IN BISCUIT INDUSTRY

BRITTANNIA

Britannia was incorporated in 1918 as Britannia Biscuits Co Ltd in Calcutta.

In 1924, Pea Frean UK acquired a controlling stake, which later passed on

to the Associated Biscuits International (ABI) a UK based company. During

the ’50s and’ 60s, Britannia expanded operations to Mumbai, Delhi and

Chennai. Exports of sea foods started in the ’70s. In 1987, Nabisco, a well

known European food company, acquired ABI. In 1989, J M Pillai, a

Singapore based NRI businessman along with the Groupe Danone acquired

Asian operations of Nabisco, thus acquiring controlling stake in Britannia.

Later, Grop Danone and Nusli Wadia took over Pillai’s holdings.

In 1977, the Government reserved the industry for small scale sector, which

constrained Britannia's growth. Britannia adopted a strategy of engaging

contract packers (CP) in the small scale sector. This led to several

inefficiencies at the operating level. In April ’97, the Government dereserved

the biscuit sector from small scale. Britannia has expanded captive

manufacturing facilities and has modernized and upgraded its facilities in the

last five years. It has also forayed into the Dairy Business with the launch of

Cheese, Butter, Ghee, Dairy whitener and flavored milk products.

Parent Group

To Estimate the Biscuits Industry and identify the critical success factors

Britannia's controlling stake is jointly with Groupe Danone and Nusli Wadia.

Groupe Danone is one of the leading players in the world in bakery products

business. It acquired interest in Britannia Industries in 1989 and acquired

controlling stake in 1993..Nusli Wadia group is one of the leading industrial

houses in the country, with interests mainly in textiles and petrochemicals.

Plant locations

Britannia's plants are located in the 4 major metro cities - Kolkatta, Mumbai,

Delhi and Chennai. A large part of products are also outsourced from third

party producers. Dairy products are out sourced from three producers -

Dynamix Dairy based in Baramati, Maharashtra, Modern Dairy at Karnal in

Haryana) and Thacker Dairy Products at Howrah in West Bengal.

Business

Britannia core businesses constitute of Bakery and Dairy products. Bakery

products account for 90% of the revenues and include Biscuits, Bread and

Cake & Rusk. Dairy products contribute to 10% of Britannia’s annual

turnover of Rs13.38bn.

To Estimate the Biscuits Industry and identify the critical success factors

Over the years, Britannia has introduced and developed a full line of brands

in all segments of the biscuit market. The company's Tiger range of glucose

biscuits have been a runaway success, enabling the company to expand its

presence in the largest gluco category of the biscuit market. In salty-sweet

segment Parle’s Krackjack and Britannia’s Fifty-Fifty compete very closely.

Britannia’s other major brands include Marie, Thin Arrowroot, Bourbon, Milk-

bikis, Nice, Snax, Coconut Crunchies, Pure Magic, Good Day, Jim-Jam and

Chekkers. It has also launched biscuits like Vita MarieGold, Nutri-Choice etc,

under the health positioning.

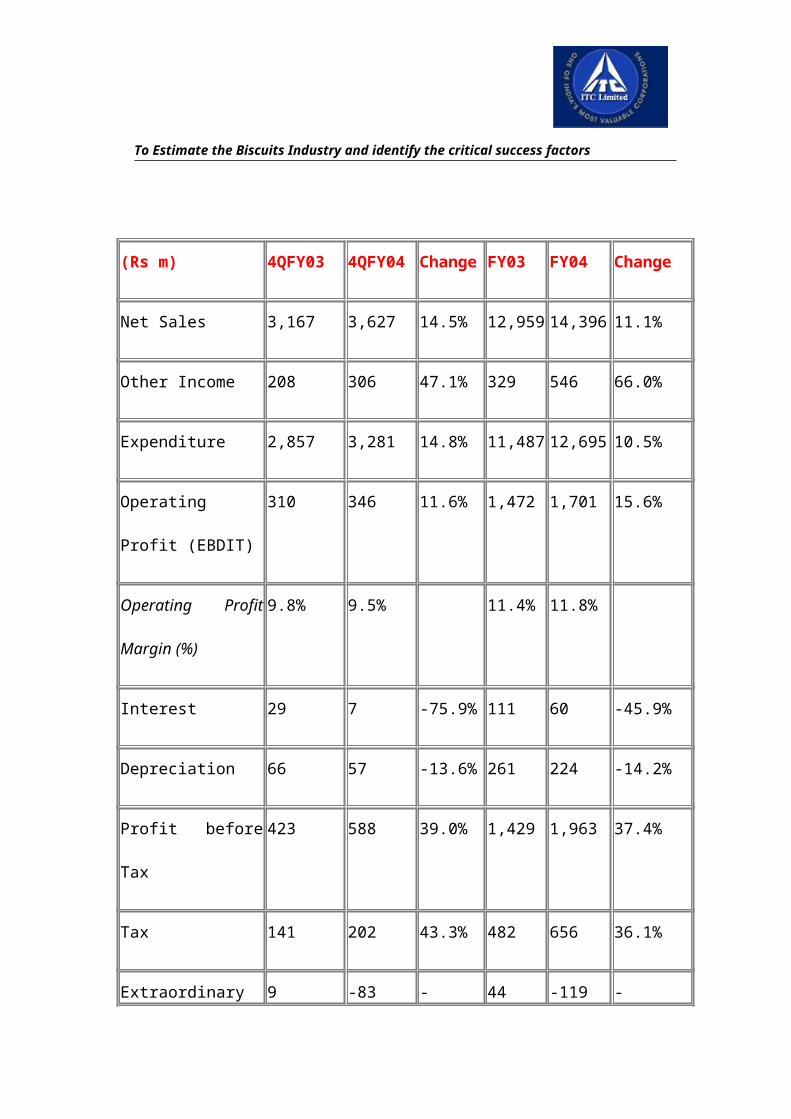

Bakery products major, Britannia Industries, had a brilliant FY04. The

company reported over 11% topline growth during the year, where most of

its FMCG peers found it tough to grow the topline. Focus on improving cost

efficiencies aided operating margin expansion. The company finished FY04

with nearly 20% bottomline growth.

To Estimate the Biscuits Industry and identify the critical success factors

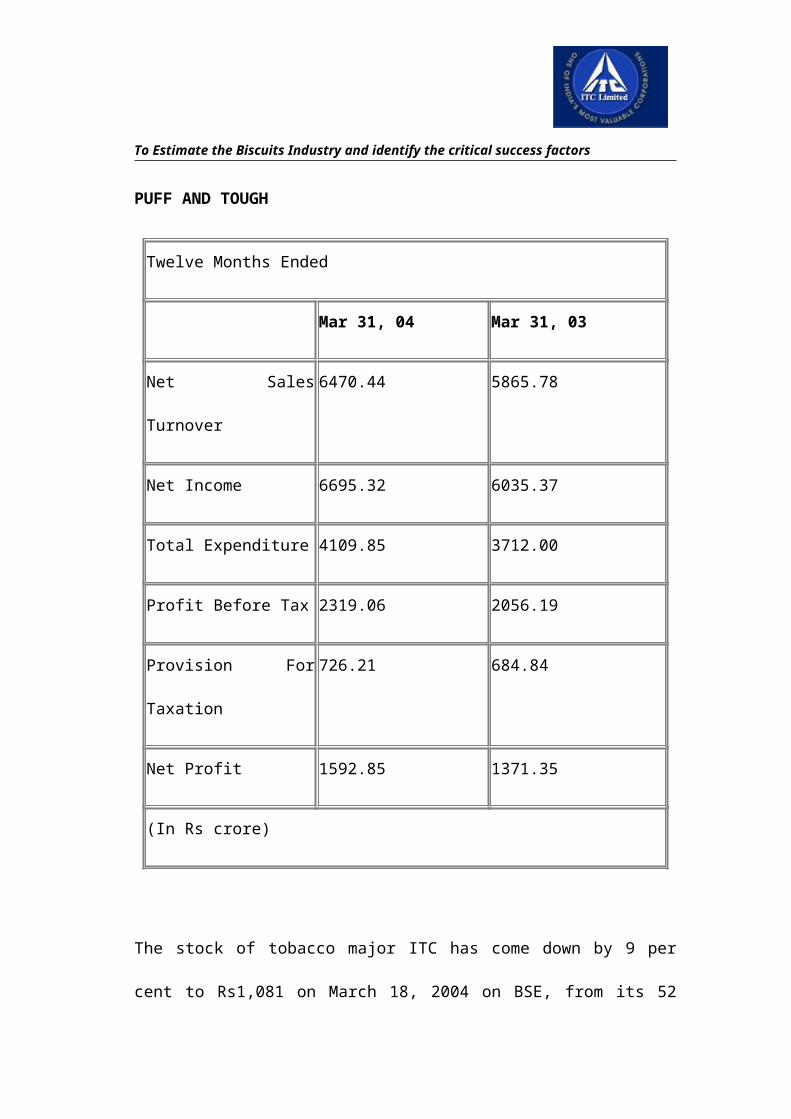

(Rs m) 4QFY03 4QFY04 Change FY03 FY04 Change

Net Sales 3,167 3,627 14.5% 12,959 14,396 11.1%

Other Income 208 306 47.1% 329 546 66.0%

Expenditure 2,857 3,281 14.8% 11,487 12,695 10.5%

Operating Profit

(EBDIT)

310 346 11.6% 1,472 1,701 15.6%

Operating Profit

Margin (%)

9.8% 9.5% 11.4% 11.8%

Interest 29 7 -75.9% 111 60 -45.9%

Depreciation 66 57 -13.6% 261 224 -14.2%

Profit before Tax 423 588 39.0% 1,429 1,963 37.4%

Tax 141 202 43.3% 482 656 36.1%

Extraordinary items 9 -83 - 44 -119 -

Profit after Tax 291 303 4.1% 991 1,188 19.9%

Net profit margin 9.2% 8.4% 7.6% 8.3%

To Estimate the Biscuits Industry and identify the critical success factors

(%)

Effective tax rate

(%)

33.3% 34.4% 33.7% 33.4%

No. of Shares (m) 25.9 25.1 25.9 25.1

Diluted earnings per

share* (x)

46.4 48.3 39.5 47.3

P/E ratio (x) 13.0 13.3

(* annualised)

The key reason for the strength in topline is believed to be the increasing

affordability of branded biscuits that aided volume growth. Moreover, the

company's repackaged and relaunched most of its biscuit brands. This

seemed to have kept the momentum going for Britannia. Apart from this,

Britannia continued to focus on ways to bring down its costs. VRS and lower

cost of debt has helped the company improve profitability.

The hiving off of properties has led to lower depreciation provisioning. The

company also received an order in favour of closure of its Mumbai plant. The

matter though is still sub-judice. After the break away from the dairy

business, the company's cash flows seemed to have improved significantly.

The company reported a strong 66% growth in other income, seemingly led

To Estimate the Biscuits Industry and identify the critical success factors

by sale of the company's mutual fund investments. All this led to a 36%

growth in profit before tax and extraordinary items.

Threat from competition

The key threats for the company are the growing competition in the biscuit

segment and the possibility of pricing pressures in the mass market.

Competitors such as Parle-G and Surya Foods have already carved out a

significant share in the mass market through aggressive pricing, where

Britannia's brand, Tiger, is trying to enlarge its share. At the higher end of

the market too, competition is hotting up, with players such as ITC rolling out

new extensions.

Britannia's profits in 2003-04 received a one-time boost from the cut in

excise duty on biscuits. This may not be repeated this fiscal.

To Estimate the Biscuits Industry and identify the critical success factors

However, the company's new cost-reduction measures may help alleviate

these pressures to some extent. The company has recently initiated

proceedings to close down its Mumbai unit and set up new manufacturing

facilities at Uttaranchal, which will significantly lower its excise and tax

burden.

The cost savings from the Mumbai unit closure, if it proceeds as planned,

could help lower the company's cost structure and put it in a better position

to compete in the mass market.

To Estimate the Biscuits Industry and identify the critical success factors

Britannia Industries Ltd. (BIL) is one of the leading producers of biscuits and

bakery products in the country. BIL’s marketing campaigns riding on the

cricket mania especially during the World Cup, have probably been the most

successful, which have added to its growth and visibility. The findings of a

recent study conducted by a private channel have also rated Britannia as

the most liked biscuit brand among kids.

Union Budget 2003-04 halved the excise duty on biscuits from 16% to

8%. Excise duty of 16% on biscuits was quite high and hence, BIL was

be the biggest beneficiary of this excise duty reduction. This also took

away some of the pricing advantage from the unorganized sector and

the pricing differential between the organised and the unorganized

sectors would also be bridged.

BIL HIGHLIGHTS:

BIL’s biscuit volume growth has outpaced the segment driven by the

various initiatives taken by the management. Tiger biscuits launch in July

1997 led Britannia’s foray into the glucose category. Tiger now

contributes about 40% to the biscuits turnover and has been Britannia’s

biggest success.

BIL has decided to focus on seven core brands in the biscuits and

bakerycategory. The brands include Good Day, Tiger, 50-50, Snax, and

the Cream Treat brands, among others. Last year, the company acquired

Kwality biscuits. Maska Chaska, the snack biscuit extension of Britannia's

To Estimate the Biscuits Industry and identify the critical success factors

50-50, is selling more than the mother brand in certain markets like north

Karnataka. And in doing so, Maska Chaska is contributing nearly 30% to

the mother brand 50-50's total sales across the country.

To establish a presence at various points of consumer visits, the

company is now in talks with specialty coffee outlets and petrol pumps to

place its products at strategic sites.

Britannia, which has agreed in-principle to acquire a 49% stake in Kwality

Biscuits and Snacko Bisc, has the option of hiking the holding in the two

companies to 100%. The company had acquired Kwality Biscuits and

Snacko Bisc to increase its presence in the southern market. Britannia is

expected to complete the acquisition of the 49% stake in Kwality Biscuits

and Snacko Bisc by the end of the current fiscal.

The effect of a poor monsoon last year is not likely to affect growth

significantly. Though, Britannia derives close to 40% of its sales from the

rural markets, the biscuit category is likely to be more resilient compared

Other factors, which support its higher-than-market growth are the

existence of relatively smaller players like Bakeman’s and Nutrine within

the organised sector that continue to be soft targets and the

aggressiveness of Britannia.The company is likely to better its operating

margins through greater volume sales as well as increasing productivity.

Volumes are expected to increase as company may pass on some of the

excise duty cut benefit to the customers.

To Estimate the Biscuits Industry and identify the critical success factors

PARLE

A long time ago, when the British ruled India, a small factory was set up in

the suburbs of of Mumbai city, to manufacture sweets and toffees. The year

was 1929 and the market was dominated by famous international brands

that were imported freely. Despite the odds and unequal competition, this

company called Parle Products, survived and succeeded, by adhering to

high quality and improvising from time to time.

A decade later, in 1939, Parle Products began manufacturing biscuits, in

addition to sweets and toffees. Having already established a reputation for

quality, the Parle brand name grew in strength with this diversification. Parle

Glucose and Parle Monaco were the first brands of biscuits to be introduced,

which later went on to become leading names for great taste and quality.

The strength of the Parle Brand

Over the years, Parle has grown to become a multi-million US Dollar

company. Many of the Parle products - biscuits or confectionaries, are

market leaders in their category and have won acclaim at the Monde

Selection, since 1971. Today, Parle enjoys a 40% share of the total biscuit

market and a 15% share of the total confectionary market, in India. The

Parle Biscuit brands, such as, Parle-G, Monaco and Krackjack and

confectionery brands, such as, Melody, Poppins, Mangobite and Kismi,

enjoy a strong imagery and appeal amongst consumers.

To Estimate the Biscuits Industry and identify the critical success factors

Be it a big city or a remote village of India, the Parle name symbolizes

quality, health and great taste! And yet, we know that this reputation has

been built, by constantly innovating and catering to new tastes. This can be

seen by the success of new brands, such as, Hide & Seek, or the single

twist wrapping of Mango bite. In this way, by concentrating on consumer

tastes and preferences and emphasizing Research & Development, the

Parle brand grows from strength to strength.

The Quality Commitment

Parle Products has one factory at Mumbai that manufactures biscuits &

confectioneries while another factory at Bahadurgarh, in Haryana

manufactures biscuits. Apart from this, Parle has manufacturing facilities at

Neemrana, in Rajasthan and at Bangalore in Karnataka. The factories at

Bahadurgarh and Neemrana are the largest such manufacturing facilites in

India. Parle Products also has 14 manufacturing units for biscuits & 5

manufacturing units for confectioneries, on contract. All these factories are

located at strategic locations, so as to ensure a constant output & easy

distribution. Each factory has state-of-the-art machinery with automatic

printing & packaging facilities.

All Parle products are manufactured under the most hygienic conditions.

Great care is exercised in the selection & quality control of raw materials,

packaging materials & rigid quality standards are ensured at every stage of

the manufacturing process. Every batch of biscuits & confectioneries are

To Estimate the Biscuits Industry and identify the critical success factors

thoroughly checked by expert staff, using the most modern equipment.

The Marketing Strength

The extensive distribution network, built over the years, is a major strength

for Parle Products. Parle biscuits & sweets are available to consumers, even

in the most remote places and in the smallest of villages with a population of

just 500.

Parle has nearly 1,500 wholesalers, catering to 4,25,000 retail outlets

directly or indirectly. A two hundred strong dedicated field force services

these wholesalers & retailers. Additionally, there are 31 depots and C&F

agents supplying goods to the wide distribution network.

The Parle marketing philosophy emphasizes catering to the masses. They

constantly endeavour at designing products that provide nutrition & fun to

the common man. Most Parle offerings are in the low & mid-range price

segments. This is based on their cultivated understanding of the Indian

consumer psyche. The value-for-money positioning helps generate large

sales volumes for the products.

However, Parle Products also manufactures a variety of premium products

for the up-market, urban consumers. And in this way, caters a range of

products to a variety of consumers.

Import-Export

To Estimate the Biscuits Industry and identify the critical success factors

The immense popularity of Parle products in India was always a challenge

to their production capacity. Now, using more modern techniques for

capacity expansion, they have begun spreading their wings and are going

global. Parle bisuits and confectionaries are fast gaining acceptance in

international markets, such as, Abu Dhabi, Africa, Dubai, South America

and Sri Lanka. Even the more sophisticated markets like USA & Australia,

now relish Parle products. As part of the efforts towards a larger share of the

global market, Parle has initiated the process of getting ISO 9000

certification. Many Parle Products have also won Gold, silver and

bronze medals at the Monde Selection.

To Estimate the Biscuits Industry and identify the critical success factors

PRIYA GOLD BISCUITS

TOUGH cookie. The term sits well on the shoulders of Shekhar Agarwal,

Director of the Rs 150-crore, Delhi-based Surya Food & Agro Ltd, the

company behind the Priyagold brand of biscuits. Unfazed by the muscle of

big-ticket competitors such as Britannia and Parle, Agarwal modestly tells

Catalyst that the reactive strategies adopted by his competitors speak for

themselves.

A decade of being in the business has got Priyagold the perception of being

a brand name to reckon with in the Northern region, a distribution network

that has helped the brand chart its way in Western India as well, and

recognition for quality production from Surya Food & Agro's manufacturing

plant at Surajpur (Greater Noida) in Uttar Pradesh. And while all these

factors have played significant roles in getting Priyagold where it is today, is

its competitive pricing that remains his brand's main strength.

A fact acknowledged by FMCG analysts. "It is a matter of concern that

regional players such as Priyagold offer products at retail prices that are

almost half that of established players such as Britannia. The product

offerings from such regional players may not necessarily be innovative on

taste, but are priced very aggressively and do not compromise on quality,"

observes an FMCG analyst. Some of Britannia's products such as Marie,

Good Day and Milk Bikis, for example, have been the victims of this strategy,

To Estimate the Biscuits Industry and identify the critical success factors

registering some decline in market share in recent months, according to an

AC Nielsen report.

This trend is highlighted more in semi-urban and rural markets, known to

occupy a significant share of the overall Rs 3,000-crore domestic biscuit

market. In fact, close to 70 per cent of Priyagold's sales are accounted for by

semi-urban rural markets, and the skew is expected to continue in favour of

these markets.

On the other hand, intensified competition from regional players has led the

established Britannia and Parle to squeeze their profit margins, offer

products at various price points, introduce small pack sizes, and offer

aggressive marketing promotions. And even as the battle royale continues

between Britannia and Parle on a national level, Surya Agro now claims

market leadership in the non-glucose biscuit segment, which, according to

industry estimates, accounts for 30 per cent of the overall biscuits market.

For all practical purposes then, Priyagold is hot property, especially for first

time entrants in the biscuits category. Surya Food & Agro has been

approached several times by FMCG multinationals, with proposals of either

acquiring the Priyagold brand, or forging strategic alliances with the

company.

It is very difficult for any company to enter the domestic biscuits market.

First, consider the competition. Britannia and Parle are very aggressive

nationally, in the East Priya Biscuits is tough competition for any new player,

To Estimate the Biscuits Industry and identify the critical success factors

while Duke is strong in the South. Then, of course, there is Priyagold. Yet

another player is Bakeman's. The second reason is that margins have to be

incurred at dealer, distributor and stockist levels. Then there are other

factors such as large investments involved in manufacturing and brand

building. It makes it easier for any company wanting to enter this segment,

therefore, to buy out an existing brand.

Recent times have thrown up examples of several established FMCG

players going slow on biscuits. Kellogg's recently stopped active production

of biscuits, Dabur has ruled out an entry and Nestle SA sold off the assets of

Excelsia Foods some months ago. There has been talk of Hindustan Lever,

too, extending its Modern brand to biscuits, but nothing has been announced

yet.

Surya Food & Agro, meanwhile, appears to be going full steam ahead. The

company now proposes to take on Britannia on its own turf. Their

strongholds are Uttar Pradesh, Punjab and Haryana, but they plan to foray

into the Southern market by the end of the current calendar year, beginning

with Karnataka. Surya Food intends to subsequently set up a manufacturing

unit in the State.

Up North, plans to set up a fresh manufacturing facility in Greater Noida next

financial year are currently being finalised. The proposed investment in this

plant will be about Rs 20 crore,. Production in full swing is expected to begin

by the end of this month at the company's third manufacturing base, in

To Estimate the Biscuits Industry and identify the critical success factors

Lucknow. The Lucknow plant, set up on an investment of Rs 5 crore,

commenced production about two months ago. Consolidation of production

is obviously a significant strategy for the company now, with its existing

manufacturing bases in Surajpur with seven biscuit lines and Faizabad, a

franchisee unit, in place. On the product front, 23 varieties of biscuits are

currently being produced by the company, and there is a plan to foray into

salty biscuits next year.

In the current fiscal, meanwhile, expect more of last year's Hak se maango

advertising, complete with its small-town appeal. Surya Food plans to hike

its consolidated ad spend to Rs 8 crore this fiscal, against the Rs 5 crore

spent on advertising last year.

On the exports front, the company plans to take its Priyagold brand to

markets such as Dubai, Muscat and Oman.

The Priyagold story, which began in late 1993 as a family business led by

entrepreneur B. P. Agarwal on an investment of Rs 1.5 crore, doesn't seem

to be playing second fiddle to anyone. With a target of doubling sales

turnover to Rs 300 crore in the current fiscal, the cookie certainly isn't

crumbling for Priyagold.

To Estimate the Biscuits Industry and identify the critical success factors

Other prominent players:

Ampee Industries Pvt. Ltd

Ampro Biscuits

Bakewal

Dalmia Biscuits

Delta Foods

Real Foods

Super Snacks

Tashi Commercial Corporation

To Estimate the Biscuits Industry and identify the critical success factors

COMPANY PROFILE - ITC LIMITED

ITC is one of India's foremost private sector companies with a market

capitalisation of around US $ 6 billion and a turnover of US $ 2.6 billion.

Rated among the World's Leading Companies by Forbes magazine, ITC

ranks fourth in net profit among India's private sector corporations . ITC has

a diversified presence in Cigarettes, Hotels, Paperboards & Specialty

Papers, Packaging, Agri-Business, Branded Apparel, Packaged Foods &

Confectionery, Greeting Cards and other FMCG products. While ITC is an

outstanding market leader in its traditional businesses of Cigarettes, Hotels,

Paperboards, Packaging and Agri-Exports, it is rapidly gaining market share

even in its nascent businesses of Branded Apparel, Greeting Cards and

Packaged Foods & Confectionery.

As one of India's most valuable and respected corporations, ITC is widely

perceived to be dedicatedly nation-oriented. Chairman Y C Deveshwar calls

this source of inspiration "a commitment beyond the market". In his own

words: "ITC believes that its aspiration to create enduring value for the

nation provides the motive force to sustain growing shareholder value. ITC

practises this philosophy by not only driving each of its businesses towards

international competitiveness but by also consciously contributing to

enhancing the competitiveness of the larger value chain of which it is a part."

ITC's diversified status originates from its corporate strategy aimed at

creating multiple drivers of growth anchored on its time-tested core

To Estimate the Biscuits Industry and identify the critical success factors

competencies: unmatched distribution reach, superior brand-building

capabilities, effective supply chain management and acknowledged service

skills in hoteliering. Over time, the strategic forays into new businesses are

expected to garner a significant share of these emerging high-growth

markets in India.

ITC's Agri-Business is one of India's largest exporters of agricultural

products. ITC is one of the country's biggest foreign exchange earners (US $

2 billion in the last decade). The Company's 'e-Choupal' initiative is enabling

Indian agriculture significantly enhance its competitiveness by empowering

Indian farmers through the power of the Internet. This transformational

strategy, which has already become the subject matter of a case study at

Harvard Business School, is expected to progressively create for ITC a huge

rural distribution infrastructure, significantly enhancing the Company's

marketing reach.

ITC's wholly owned Information Technology subsidiary, ITC Infotech India

Limited, is aggressively pursuing emerging opportunities in providing end-to-

end IT solutions, including e-enabled services and business process

outsourcing.

ITC's production facilities and hotels have won numerous national and

international awards for quality, productivity, safety and environment

management systems. ITC was the first company in India to be rated for

Corporate Governance by ICRA, an associate of Moody's Investors Service,

To Estimate the Biscuits Industry and identify the critical success factors

which accorded it the second highest rating, signifying "a high level of

assurance on the quality of corporate governance."

ITC employs over 15,000 people at more than 60 locations across India.

Ranked among the top five sustained value creators in India by 'Business

Today-Stern Stewart' in their studies conducted between 2000 and 2003,

ITC continuously endeavors to enhance its wealth generating capabilities in

a globalising environment to consistently reward its 1,47,035 shareholders,

fulfil the aspirations of its stakeholders and meet societal expectations. This

over-arching vision of the company is expressively captured in its corporate

positioning statement: "Enduring Value. For the nation. For the

Shareholder."

LEADERSHIP

Flowing from the concept and principles of Corporate Governance adopted

by the Company, leadership within ITC is exercised at three levels. The

Board of Directors at the apex, as trustee of shareholders, carries the

responsibility for strategic supervision of the Company. The strategic

management of the Company rests with the Corporate Management

Committee comprising the wholetime Directors and members drawn from

senior management. The executive management of each business division

is vested with the Divisional Management Committee (DMC), headed by the

To Estimate the Biscuits Industry and identify the critical success factors

Chief Executive. Each DMC is responsible for and totally focused on the

management of its assigned business.

This three-tiered interlinked leadership process creates a wholesome

balance between the need for focus and executive freedom, and the need

for supervision and control.

To Estimate the Biscuits Industry and identify the critical success factors

ITC's Core Values are aimed at developing a customer-focused, high-

performance organisation which creates value for all its stakeholders:

Trusteeship

As professional managers, we are conscious that ITC has been given to us

in "trust" by all our stakeholders. We will redeem the trust reposed in us by

continuously adding value to ITC.

Customer Focus

We will always be customer focused. We will deliver what the customer

needs in terms of value, quality and satisfaction.

Respect For People

We will respect and value people and uphold humanness and human

dignity.

We will value differences in individual perspectives. We want individuals to

dream, create and experiment in pursuit of opportunities and achieve

leadership through teamwork.

Excellence

We will strive for excellence in whatever we do. We will do what is right, do it

well and win.

To Estimate the Biscuits Industry and identify the critical success factors

Innovation

We will constantly innovate and strive to better our processes, products,

services and management practices.

Ethical Corporate Citizenship

We will pursue exemplary standards of ethical behaviour. We will at all times

comply with the laws of the land.

Preamble

Over the years, ITC has evolved from a single product company to a multi-

business corporation. Its businesses are spread over a wide spectrum,

ranging from cigarettes and tobacco to hotels, packaging, paper and

paperboards and international commodities trading. Each of these

businesses is vastly different from the others in its type, the state of its

evolution and the basic nature of its activity, all of which influence the choice

of the form of governance. The challenge of governance for ITC therefore

lies in fashioning a model that addresses the uniqueness of each of its

businesses and yet strengthens the unity of purpose of the Company as a

whole.

Since the commencement of the liberalisation process, India's economic

scenario has begun to alter radically. Globalisation will not only significantly

heighten business risks, but will also compel Indian companies to adopt

international norms of transparency and good governance. Equally, in the

To Estimate the Biscuits Industry and identify the critical success factors

resultant competitive context, freedom of executive management and its

ability to respond to the dynamics of a fast changing business environment

will be the new success factors. ITC's governance policy recognises the

challenge of this new business reality in India.

DEFINITION AND PURPOSE

ITC defines Corporate Governance as a systemic process by which

companies are directed and controlled to enhance their wealth generating

capacity. Since large corporations employ vast quantum of societal

resources, we believe that the governance process should ensure that these

companies are managed in a manner that meets stakeholders aspirations

and societal expectations.

CORE PRINCIPLES

ITC's Corporate Governance initiative is based on two core principles. These

are :

Management must have the executive freedom to drive the enterprise

forward without undue restraints; and

This freedom of management should be exercised within a framework of

effective accountability.

ITC believes that any meaningful policy on Corporate Governance must

provide empowerment to the executive management of the Company, and

To Estimate the Biscuits Industry and identify the critical success factors

simultaneously create a mechanism of checks and balances which ensures

that the decision making powers vested in the executive management is not

only not misused, but is used with care and responsibility to meet

stakeholder aspirations and societal expectations.

Cornerstones

From the above definition and core principles of Corporate Governance

emerge the cornerstones of ITC's governance philosophy, namely

trusteeship, transparency, empowerment and accountability, control and

ethical corporate citizenship. ITC believes that the practice of each of these

leads to the creation of the right corporate culture in which the company is

managed in a manner that fulfíls the purpose of Corporate Governance.

Trusteeship

ITC believes that large corporations like itself have both a social and

economic purpose. They represent a coalition of interests, namely those of

the shareholders, other providers of capital, business associates and

employees. This belief therefore casts a responsibility of trusteeship on the

Company's Board of Directors. They are to act as trustees to protect and

enhance shareholder value, as well as to ensure that the Company fulfils its

obligations and responsibilities to its other stakeholders. Inherent in the

concept of trusteeship is the responsibility to ensure equity, namely, that the

rights of all shareholders, large or small, are protected.

To Estimate the Biscuits Industry and identify the critical success factors

Transparency

ITC believes that transparency means explaining Company's policies and

actions to those to whom it has responsibilities. Therefore transparency must

lead to maximum appropriate disclosures without jeopardising the

Company's strategic interests. Internally, transparency means openness in

Company's relationship with its employees, as well as the conduct of its

business in a manner that will bear scrutiny. We believe transparency

enhances accountability.

Empowerment and Accountability

Empowerment is an essential concomitant of ITC's first core principle of

governance that management must have the freedom to drive the enterprise

forward. ITC believes that empowerment is a process of actualising the

potential of its employees. Empowerment unleashes creativity and

innovation throughout the organisation by truly vesting decision-making