Platts European Steel Summit, London, 23rd May, 2013 1 Remaining Competitive in a Challenging Climate Actual outlook on steel market development with a focus on plates Günter Luxenburger Director Sales & Marketing Member of the Board

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Platts European Steel Summit, London, 23rd May, 2013 1

Remaining Competitive in a Challenging Climate

Actual outlook on steel market development

with a focus on plates

Günter Luxenburger Director Sales & Marketing

Member of the Board

Platts European Steel Summit, London, 23rd May, 2013 2

• Short profile of Dillinger Hütte Group

• Raw materials

• Trends and developments in the steel market

• Specific view to the quarto plate market / Linepipe market

• Other important external conditions

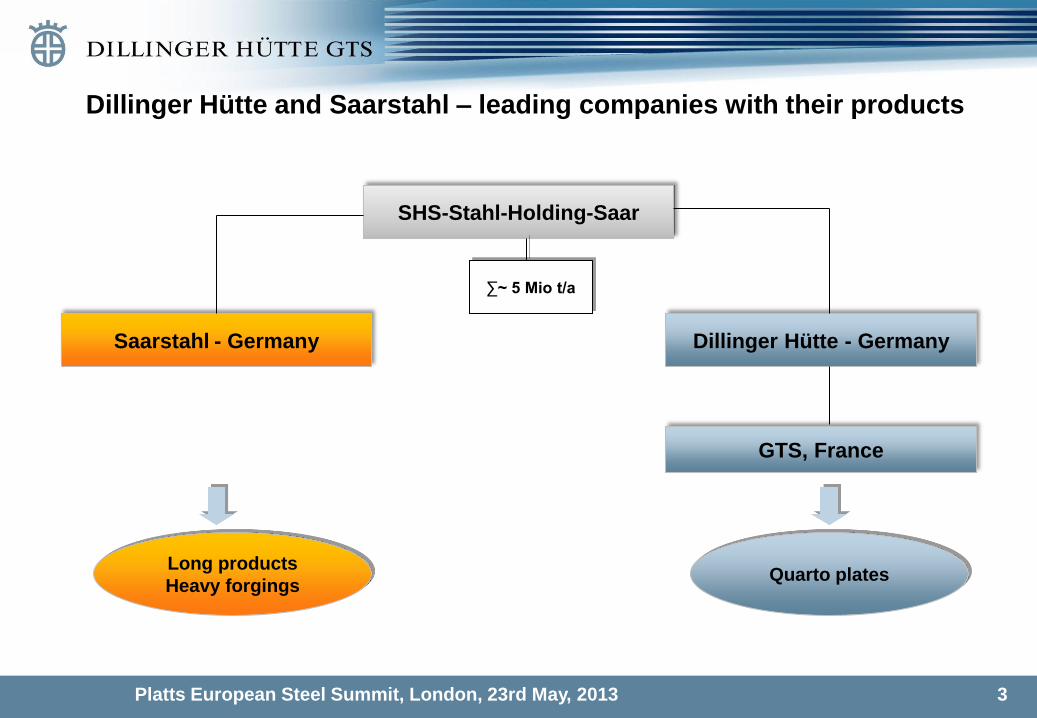

Platts European Steel Summit, London, 23rd May, 2013 3

Dillinger Hütte and Saarstahl – leading companies with their products

SHS-Stahl-Holding-Saar

Saarstahl - Germany Dillinger Hütte - Germany

GTS, France

Long products

Heavy forgings Quarto plates

∑~ 5 Mio t/a

Platts European Steel Summit, London, 23rd May, 2013 4

ArcelorMittal SHS - Stahl-Holding-Saar Saarstahl

26,17% 33,75%

DHS - Dillinger Hütte Saarstahl (DHS holds 10% of its own shares) Private Shareholders 95,28% 4,72%

* direct and indirect

Production Steel Service Centres

30,08%

ROGESA Roheisengesellsch.

Zentralkokerei Saar

50% *

50% *

Saarstahl AG

Europipe

25,1%

50%

Jebens

Ancofer Stahlhandel

Dillinger Middle East (AE)

90%

100%

100%

AncoferWaldram Steelplates (NL)

Eurodécoupe (F)

100%

100%

Dillinger-GTS Ventes (F)

Dillinger Hütte Vertrieb

Dillinger Nederland (NL)

100%

100%

100%

Dillinger UK (GB)

Dillinger Italia (I)

100%

100%

Sales Companies Logistics

Dillinger Sverige (S)

Dillinger Norge (N)

100%

100%

Dillinger Espana (E)

Dillinger America (US)

100%

100%

Satrans

Trans-Saar (NL)

Saar-Rhein Transport- gesellschaft

100%

40%

100%

60%

DILLINGER HÜTTE

Share holding structure of the Dillinger Hütte

GTS Industries (F)

100%

MSG Mineralstoffgesellsch.

100%

Platts European Steel Summit, London, 23rd May, 2013 5

Dunkerque (France)

Dillingen (Germany)

Dillinger Hütte - The leading European plate maker

Platts European Steel Summit, London, 23rd May, 2013 6

Key data of Dillinger Hütte Group

• Plate capacity: 2.300 kt/a

Dillingen, Germany: 1.600 kt/a

GTS, France: 700 kt/a

• Focus on: - thick, large, heavy plates

- stringent specifications

- top services

• Employees in the group: 8.200

Dillingen 5.300

GTS, France 600 (using slabs of DH)

Platts European Steel Summit, London, 23rd May, 2013 7

Grand Stade Lille Métropole

• The stadium for the 2016 European Soccer Cup in France

• Plate thickness: up to 260 mm

• DH-deliveries: 5,400 t

• Steel grades: S355K2+N, S355N, S355NL, S460ML

Platts European Steel Summit, London, 23rd May, 2013 8

Hydroelectric power generating plant Santo Antônio

• Santo-Antônio-barrage fix at the river of Madeira in the northwest of Brazil

• Output: 3,150 MW

• Plate thickness: up to 210 mm

• DH-deliveries: 5,800 t

• normalised

steel grades: S235J0

S355J0

S355J2

S355J2G3

Platts European Steel Summit, London, 23rd May, 2013 9

• 250 sunshades reaching up to a height of 20 m protect pilgrims in Medina from the rays of the sun

• Plate thickness: up to 70 mm

• DH-deliveries: 2,600 t

• Steel grades: DILLIMAX 690 and DILLIMAX 965

Sunshades for Medina

Platts European Steel Summit, London, 23rd May, 2013 10

200 DS super heavy-lift crane

• Type: PTC 200 DS

• Plate thickness: up to 120 mm

• DH-deliveries: 12,500 t

• Steel grades: DILLIMAX high-tensile steels

Platts European Steel Summit, London, 23rd May, 2013 11

• Output: 367 MW

• Number: 102 towers

• Plate thickness: up to 105 mm

• DH-deliveries: 35,700 t

• Steel grades: S355NL, S355ML,

S355G10+M, S355G9+M

Offshore wind farm Walney, off the west coast of England

Quelle: RWE Innogy GmbH

Platts European Steel Summit, London, 23rd May, 2013 12

Installation vessel „Innovation“

• „Innovation“ of HGO InfraSea Solutions

• DH-deliveries: Racks 1,400 t Chords 1,050 t

• Plate thickness: Racks 190 mm Chords 55 mm

• Steel grade: DILLIMAX 690 E

Platts European Steel Summit, London, 23rd May, 2013 13

• Course: from Vyborg (Russia) to Greifswald (Germany)

• Length: 1,200 km

• Plate thickness: 26.7 - 34.6 mm

• DH-GTS-deliveries: 495,000 t

• Steel grade: SAWL-485-I-FD

Gas pipeline „Nordstream 2“, Baltic Sea

Platts European Steel Summit, London, 23rd May, 2013 14

One of the big innovation steps – the new continuous casting plant

Platts European Steel Summit, London, 23rd May, 2013 15

Capacity extension for super-heavy plates

New ingot casting stands in the extension of hall 5.

Platts European Steel Summit, London, 23rd May, 2013 16

Monopiles for Offshore Wind Power Stations !

Platts European Steel Summit, London, 23rd May, 2013 17

Weser

Nordenham

Nordsee

OTB Industrial estate

Blexen

Fabrication site at the north sea shore

Short distance to the north sea and offshore erection sides

Platts European Steel Summit, London, 23rd May, 2013 18

Construction of halls and quay (end of April 2013)

Weser river

(2 km to the North sea)

Platts European Steel Summit, London, 23rd May, 2013 19

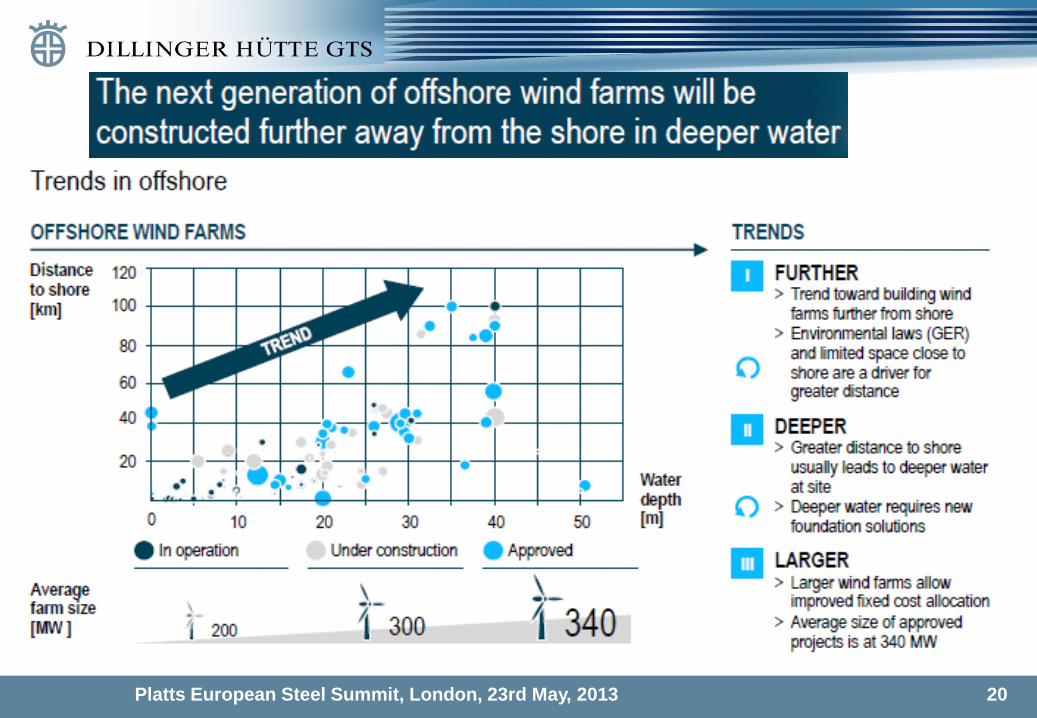

Platts European Steel Summit, London, 23rd May, 2013 20

Platts European Steel Summit, London, 23rd May, 2013 21

Platts European Steel Summit, London, 23rd May, 2013 22

• Trends and developments in the steel market

• Raw materials

• Short overview about Dillinger Hütte Group

• Specific view to the quarto plate market

• Other important external conditions

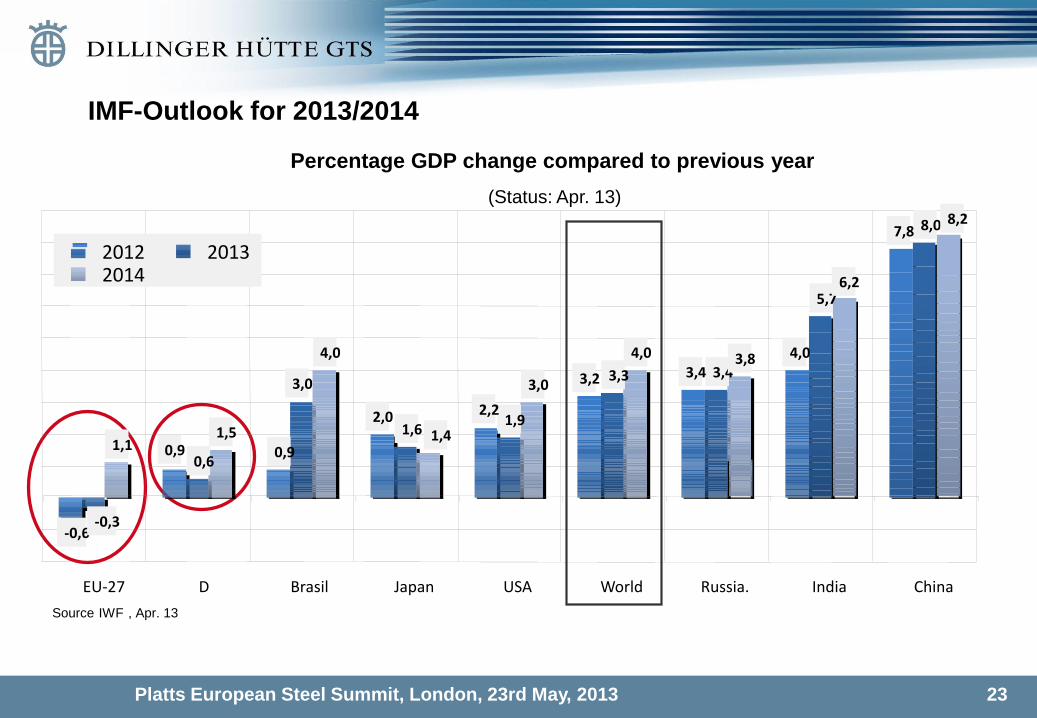

Platts European Steel Summit, London, 23rd May, 2013 23

IMF-Outlook for 2013/2014

(Status: Apr. 13)

Percentage GDP change compared to previous year

-0,6

0,9 0,6

1,6 1,9

3,3 3,4

5,7

8,0

1,1 1,5

4,0

3,0

4,0 3,8

6,2

0,9

2,0 2,2

3,2 3,4

4,0

7,8

-0,3

3,0

1,4

8,2

EU-27 D Brasil Japan USA World Russia. India China

2012 2013 2014

Source IWF , Apr. 13

Platts European Steel Summit, London, 23rd May, 2013 24

Quelle: CPB

Economic situation in industrial countries with little impetus

80

85

90

95

100

105

110

115

2011 2008 2009 2010

Industrieproduktion und Welthandel (2008=100, gl. 3-MD)

Jan--Feb 13: +1%

Jan-Feb 13: +2%

2012

Welthandel 2011: +6% 2012: +2%

Globale Industrieprod. 2011: +6% 2012: +3%

2013 80

85

90

95

100

105

110

115

120

125

130

135

140

2011 2008 2009 2010

Schwellenländer 2011: +7% 2012: +5%

Industrieländer 2011: +2%

2012: +0,4%

Industrieproduktion (Jan. 2008=100)

2012

Jan-Feb 13: +4%

Jan-Feb 13: -1%

2013

Global

industrial production

World trade

Emerging countries

Industrial Countries

Industrial production Industrial production and world trade

Platts European Steel Summit, London, 23rd May, 2013 25

0

200

400

600

800

1000

1200

1400

1600

1800

1950 1960 1970 1980 1990 2000 2010

Worldwide production of crude steel – up!

Average growth rates

(% per annum)

Years Growth

2000-12 5,3 %

1975-00 1,1 %

1950-75 5,0 %

I. II. III. II.

III.

2009 : 1,236 Mio t

2010 : 1,430 Mio t

2011 : 1,524 Mio t

2012: 1,548 Mio t

Outlook 2013: 1,596 Mio t *

Outlook 2014: 1,665 Mio t *

I.

*) Estimation Source: Worldsteel, WV, DH calculations

Development: 1950 - 2012

+5,3 %

+1,1 %

+5,0 %

Platts European Steel Summit, London, 23rd May, 2013 26

Eurofer Forecast: EU-steel market actually stagnating

192 201

185

121

148 157

142 139 144

0

50

100

150

200

250

06 07 08 09 10 11 12 13f 14f

Marktversorgung EU-27 (Mio. t)

Quelle: Eurofer Konjunkturkommission, Apr. 13

-10% -2% +3%

40

50

60

70

80

90

100

110

120

06 07 08 09 10 11 12 13f 14f

Deutschland

EU 27

Italien

Spanien

Marktversorgung Walzstahl in ausgewählten Ländern der EU-27 (2006=100)

Quelle: Eurofer Konjunkturkommission, Apr. 2013

Market supply EU-27 (Mio t) Market supply rolled steel in selected

EU-27 countries (2006=100)

Platts European Steel Summit, London, 23rd May, 2013 27

• Specific view to the quarto plate market

• Raw materials

• Short overview about Dillinger Hütte Group

• Trends and developments in the steel market

• Other external conditions

Platts European Steel Summit, London, 23rd May, 2013 28

Deliveries of Eurofer mills into EU 27 *)

Q1/2013 = Jan-March 2013; % variation y-o-y

into EU 27; Pre-material for large dia pipe excluded

1.000 t.p.m.

400

450

500

550

600

650

700

750

800

850

900

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

deliveries

orders

per year

Eurofer deliveries into EU 27 are recovering slowly in 2013

Orders

IV-12 597

I-13 636

Deliveries

IV-12 511

I-13 624

Platts European Steel Summit, London, 23rd May, 2013 29

*) = extrapolated from statistical figures for the German market; inventory at end of period; partly estimated Q1/13 = End of March 2013

2006 2007 2008 2009 2010 2011 2012

Inventory in kt Stock variation in kt

accumulated investory increase:

1,35 million tons or 50 % from beginning of

2006 till Q2/08

stockpiling: 28 months de-stocking 18 months

13

EU QP stock – continuous buying activity in 2013 expected

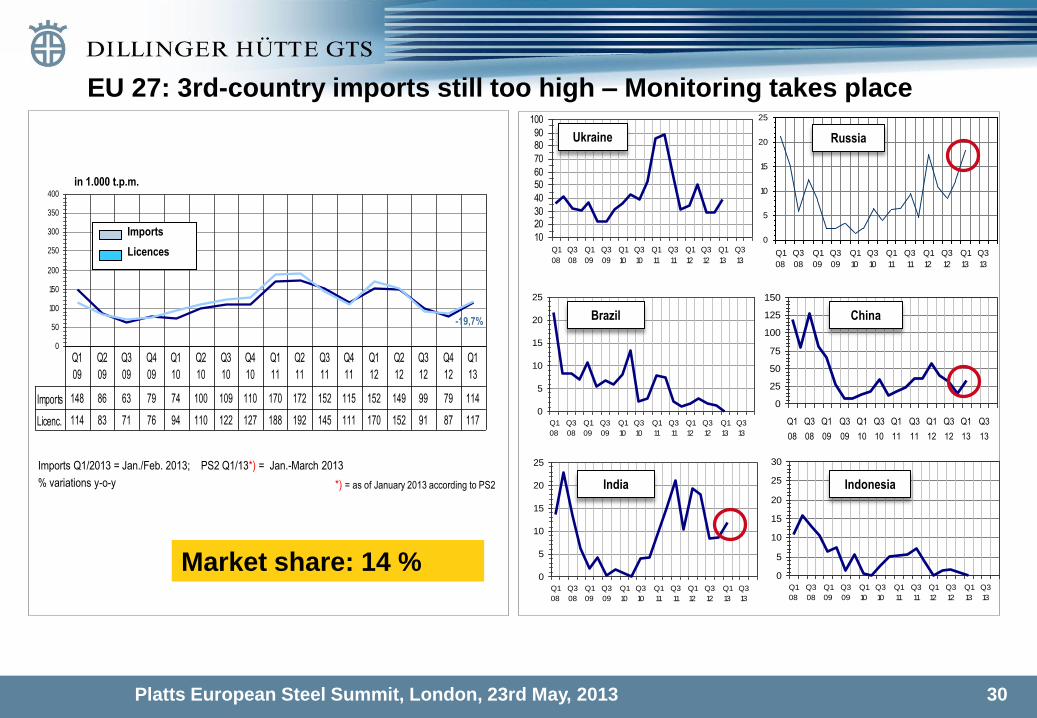

Platts European Steel Summit, London, 23rd May, 2013 30

Imports Q1/2013 = Jan./Feb. 2013; PS2 Q1/13*) = Jan.-March 2013

% variations y-o-y

EU 27: 3rd-country imports still too high – Monitoring takes place

0

5

10

15

20

25

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

0

5

10

15

20

25

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

10

2030

40

5060

70

8090

100

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

Ukraine Russia

Brazil

0

25

50

75

100

125

150

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

China

0

5

10

15

20

25

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

India

0

5

10

15

20

25

30

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

Indonesia

0

50

100

150

200

250

300

350

400

Imports 148 86 63 79 74 100 109 110 170 172 152 115 152 149 99 79 114

Licenc. 114 83 71 76 94 110 122 127 188 192 145 111 170 152 91 87 117

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Q4

10

Q1

11

Q2

11

Q3

11

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

in 1.000 t.p.m.

-19,7%

Imports

Licences

*) = as of January 2013 according to PS2

Market share: 14 %

Platts European Steel Summit, London, 23rd May, 2013 31

Consumer segments for QP - 2013 vs 2012: mixed picture

*** **

2012

****

*****

***/*

***

**** ****

*** **

**** ***

2013

**** ****

Yellow goods

Heavy machinery

Shipbuilding Asia

Offshore Oil & Gas

Linepipe

Wind-Energy

Pressure Equipment

Trend

(QIII, QIV)

Platts European Steel Summit, London, 23rd May, 2013 32

Quo vadis – plate market:

1. Many plate consuming segments still in good shape

2. Demand for (non line pipe) plates - improvement expected in QIV-13

3. Demand for shipbuilding plates low pressure to producers in Asia

4. Demand for line pipe plates actually low improvement expected in QIV-13

5. Stock inventories in healthy conditions continuous buying activity over the year

6. Prices too low compared to cost situation price hikes as soon as the market

allows it

Platts European Steel Summit, London, 23rd May, 2013 33

• Raw materials

• Specific view to the quarto plate market

• Short overview about Dillinger Hütte Group

• Trends and developments in the steel market

• Other important external conditions

Platts European Steel Summit, London, 23rd May, 2013 34

Stand: 21.05.13

2010 2011 2012 2013

USD/t

Brasilien

Referenzsorte SSFT ab 12/2009

IODEX and FOB-prices Brazil

ROGESA & ZKS/Beschaffung

Price development Iron Ore (world market) - high volatility!

Platts European Steel Summit, London, 23rd May, 2013 35

0

50

100

150

200

250

300

350

400

450

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2. Q. 2

013

US

D/t

FO

B A

US

Quarterly prices Hard Coking Coal

“Quarter”- Benchmark 2013/14: Q2: 172 USD/t * 2012/13: Q2: 210 USD/mt * Q3: 225 USD/mt * Q4: 170 USD/mt * Q1: 165 USD/mt *

ROGESA & ZKS/Beschaffung

(*): FOB QLD/AUS

Stand: 21.05.13

Platts European Steel Summit, London, 23rd May, 2013 36

• High volatility of raw material prices

• High volatility of steel prices

• Project contracts with a validity of several quarters

Price quotations based on unknown costs!

Huge risks for the steel maker to work with fixed prices

Solution by price adjustment formulas – to be agreed with the customers

raw material clause steel price indexation

or in combination including capping rules

Challenging Conditions for long lead time projects

Platts European Steel Summit, London, 23rd May, 2013 37

• Other important external conditions

• Specific view to the quarto plate market

• Short overview about Dillinger Hütte Group

• Trends and developments in the steel market

• Raw materials

Platts European Steel Summit, London, 23rd May, 2013 38

Quelle: VIK, 2012

Canada

USA

Brasil

Argentina

Australia

India

China

Indonesia

Malaysia

South

Korea

Russia

Russia

Turkey

Finland

Norway

Great Britain

France

Spain

Romania

Italy

1

2

3 4

5

6

7

1. Netherlands

2. Belgium

3. Switzerland

4. Austria

5. Czech

Republic

6. Hungrier

7. Bulgarian

Sweden

Poland

Power prices for the industry - huge disadvantages in Europe!

►

Platts European Steel Summit, London, 23rd May, 2013 39

Cost based on renewable energy law in Germany (EEG-Gesetz) has

quadrupled since 2009 one reason for high energy cost

Platts European Steel Summit, London, 23rd May, 2013 40

►

Platts European Steel Summit, London, 23rd May, 2013 41

Remaining Competitive in a Challenging Climate – means:

- frame conditions in EU have to be supportive, reliable and stable for the (steel) -

industry EU administration and national governments bear a high responsibility! - keep steel (consuming) industry in the EU – keep the jobs in EU!

- yes: to fair trade

- no: to unfair trade, dumping or unfair trade barriers!

- the steel companies in EU have still a lot of chances by marketing innovative

and customer oriented products & services!

- adjusting capacities is an issue not only in Europe – a general political solution is not realistic.

- Give the good companies the chance to win the race!

Related Documents