Relevant Information for Special Decisions Chapter 13 McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Relevant Information for

Special Decisions

Chapter 13

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

13-2

Learning Objectives1. Identify the characteristics of relevant

information.2. Distinguish between unit-level, batch-

level, product-level, and facility-level costs and understand how these costs affect decision making.

3. Make appropriate special order decisions.

4. Make appropriate outsourcing decisions.5. Make appropriate segment elimination

decisions.6. Make appropriate asset replacement

decisions.

13-3

Relevant Information

Two primary characteristics distinguish relevant from useless

information:

1.Relevant information differs among the alternatives under consideration.

2.Relevant information is future oriented.

Two primary characteristics distinguish relevant from useless

information:

1.Relevant information differs among the alternatives under consideration.

2.Relevant information is future oriented.

13-4

Sunk CostA sunk cost has been incurred in a past

transaction and cannot be changed, it is not relevant for making current decisions.

Why are you complaining? Why are you complaining? You have two offers at or You have two offers at or near the market value, so near the market value, so

the $25,000 is not the $25,000 is not relevant – it’s a sunk cost.relevant – it’s a sunk cost.

Why are you complaining? Why are you complaining? You have two offers at or You have two offers at or near the market value, so near the market value, so

the $25,000 is not the $25,000 is not relevant – it’s a sunk cost.relevant – it’s a sunk cost.

Wish I hadn’t Wish I hadn’t bought that car! It bought that car! It cost me $25,000, cost me $25,000, and now its worth and now its worth

only $19,000. I only $19,000. I really don’t want to really don’t want to take a loss on it but take a loss on it but

I need the cash I need the cash more than I need more than I need

the car!the car!

Wish I hadn’t Wish I hadn’t bought that car! It bought that car! It cost me $25,000, cost me $25,000, and now its worth and now its worth

only $19,000. I only $19,000. I really don’t want to really don’t want to take a loss on it but take a loss on it but

I need the cash I need the cash more than I need more than I need

the car!the car!

13-5

Opportunity CostAn opportunity cost is the sacrifice that is incurred in

order to obtain an alternative opportunity.

Your opportunity Your opportunity cost of ownership is cost of ownership is

$19,000 or the $19,000 or the highest value of the highest value of the

available available alternatives.alternatives.

Your opportunity Your opportunity cost of ownership is cost of ownership is

$19,000 or the $19,000 or the highest value of the highest value of the

available available alternatives.alternatives.

Even though the car Even though the car cost me $25,000, I can cost me $25,000, I can

sell it to my relative sell it to my relative for $18,000 or for for $18,000 or for

$19,000 to my $19,000 to my neighbor. So what is neighbor. So what is

my opportunity cost of my opportunity cost of keeping the car rather keeping the car rather than getting the cash? than getting the cash?

Even though the car Even though the car cost me $25,000, I can cost me $25,000, I can

sell it to my relative sell it to my relative for $18,000 or for for $18,000 or for

$19,000 to my $19,000 to my neighbor. So what is neighbor. So what is

my opportunity cost of my opportunity cost of keeping the car rather keeping the car rather than getting the cash? than getting the cash?

13-6

Relevance – Other Issues

Relevance is context-sensitive.

A particular cost that is relevant in one context may be irrelevant in another.

Relevance versus Accuracy.

Information need not be exact to be relevant.

13-7

Quantitative vs. Qualitative Data

Relevant information can have both quantitative and qualitative characteristics.

Features such as company reputation, welfare of employees, and customer satisfaction

Numbers or amounts used in decision making

Both quantitative and qualitative data are relevant to decision making.

13-8

Relevant (Avoidable) CostsBusinesses seek to minimize costs. Managers avoid costs whenever possible.

Relevant costs are frequently called avoidable or differential costs. They are costs managers can eliminate by making specific choices.

13-9

Differential Revenue• Revenue that differs between alternatives

is called differential and is relevant to decision making.

• Peck’s Department Store sells clothes for women, men and children and is considering eliminating the children’s.• The revenue from selling children’s is relevant

to this decision because it differs based on alternative chosen.

13-10

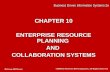

Cost Avoidance & Cost Hierarchy

Unit-levelUnit-levelActivitiesActivities

Batch-levelBatch-levelActivitiesActivities

Product-levelProduct-levelActivitiesActivities

Facility-levelFacility-levelActivitiesActivities

Avoided by eliminating oneAvoided by eliminating oneunit of product.unit of product.

Avoided when a batch ofAvoided when a batch ofwork is eliminated.work is eliminated.

Avoided if a product lineAvoided if a product lineis eliminated.is eliminated.

Avoided if the company is Avoided if the company is dissolved; some costs may be dissolved; some costs may be

avoided if a business segment is avoided if a business segment is eliminated.eliminated.

13-11

Relevant Information and Special Decisions

Occasionally, a company receives an offer to sell Occasionally, a company receives an offer to sell its product at a price significantly below its normal its product at a price significantly below its normal selling price. The company must make a selling price. The company must make a special special order decisionorder decision about whether to accept or reject about whether to accept or reject

the offer.the offer.

Occasionally, a company receives an offer to sell Occasionally, a company receives an offer to sell its product at a price significantly below its normal its product at a price significantly below its normal selling price. The company must make a selling price. The company must make a special special order decisionorder decision about whether to accept or reject about whether to accept or reject

the offer.the offer.

13-12

Opportunity CostsThe sacrifice represented by a lost opportunity is an opportunity cost. Opportunity costs that are (1) future oriented and (2) differ between the alternatives are relevant for decision making, but are extremely difficult to measure.

If Premier can lease its excess capacity for $15,000 but instead uses excess capacity to make additional computers, then it foregoes the opportunity to lease the excess capacity. Sacrificing the potential leasing revenue is an opportunity cost of $15,000.

It factors into the decision in the following manner.

13-13

Outsourcing DecisionsCompanies can sometimes purchase products

needed in the manufacturing process for less than it would cost to make them. Buying goods and

services from other companies rather than producing them internally is commonly called

outsourcingoutsourcing.

That test was so That test was so easy. Why is your easy. Why is your

score so low?score so low?

That test was so That test was so easy. Why is your easy. Why is your

score so low?score so low?

I outsourced I outsourced my homework!!my homework!!

I outsourced I outsourced my homework!!my homework!!

13-14

Qualitative FeaturesA company that uses vertical integration controls

the full range of activities from acquiring raw materials to distributing goods and services. An oil company, like Exxon, is a good example of vertical

integration.Outsourcing reduces the level of vertical integration,Outsourcing reduces the level of vertical integration,passing some of a company’s control over its passing some of a company’s control over its production to outside suppliers. But is the supplier production to outside suppliers. But is the supplier reliable? What about quality, timely delivery, reliable? What about quality, timely delivery, future prices and other qualitative considerations?future prices and other qualitative considerations?

Outsourcing reduces the level of vertical integration,Outsourcing reduces the level of vertical integration,passing some of a company’s control over its passing some of a company’s control over its production to outside suppliers. But is the supplier production to outside suppliers. But is the supplier reliable? What about quality, timely delivery, reliable? What about quality, timely delivery, future prices and other qualitative considerations?future prices and other qualitative considerations?

13-15

13-16

End of Chapter Thirteen

Related Documents