Relevance of corporate governance practices in charitable organisations A case study of registered charities in New Zealand Krishna Reddy, Stuart Locke and Fitriya Fauzi Department of Finance, Waikato Management School, University of Waikato, Hamilton, New Zealand Abstract Purpose – The purpose of this paper is to examine whether the registered charities in New Zealand have adopted the principle-based corporate governance practices similar to those adopted by the publicly-listed companies and the effect corporate governance practices have on their financial performance measured by technical efficiency, allocative efficiency and quick ratio. The paper addresses four important questions: how registered charities in New Zealand are managed and controlled; whether the funds donated to registered charities are utilised effectively; the nature of the corporate governance practiced by registered charities in New Zealand; and the nature of compliance to the Charities Act 2005. Design/methodology/approach – Panel data for the registered charities over the period 2008-2010 are analysed using ordinary least squares (OLS) regression and Tobit model regression. Technical efficiency, allocative efficiency and quick ratio are used as the dependent variables. Findings – The findings indicate that there is no reporting requirement for the registered charities under the Charities Act 2005 to report detailed information regarding the board make-up, board committees, board meetings, etc. and therefore, registered charities have not reported such information. The results show also that board gender diversity is an important corporate governance mechanism to mitigate agency problem in charitable organisations in New Zealand. However, large board size and large donors have potential to increase agency costs in charitable organisations in New Zealand. Research limitations/implications – Caution should be exercised when interpreting and generalising the paper’s results, as this study is a case study of registered charities in New Zealand and data comprised only large charities that have revenue over NZ$20 m. It should also be noted that there was a small sample size, which may have had a bearing on the results. Practical implications – This study offers insights for policy makers and practitioners interested in adopting similar corporate governance practices within their country. Social implications – Within New Zealand, issues relating to management and control of charitable organisations are better understood and as a consequence, development of sector-wise standards could be initiated. Originality/value – This research is novel as it investigates the nature of corporate governance practices relating to the registered charities in New Zealand. The availability of data provided by Charities Commission made this research possible. Keywords New Zealand, Charities, Corporate governance, Financial performance, Charitable organizations, Charities Commission, Technical efficiency, Allocative efficiency, Quick ratio Paper type Research paper 1. Introduction Large corporate failures that occurred at the beginning of the twenty-first century in America and Europe and the Asian financial crisis of 1997 have highlighted the The current issue and full text archive of this journal is available at www.emeraldinsight.com/1743-9132.htm International Journal of Managerial Finance Vol. 9 No. 2, 2013 pp. 110-132 r Emerald Group Publishing Limited 1743-9132 DOI 10.1108/17439131311307547 110 IJMF 9,2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Relevance of corporategovernance practices incharitable organisations

A case study of registered charities inNew Zealand

Krishna Reddy, Stuart Locke and Fitriya FauziDepartment of Finance, Waikato Management School, University of Waikato,

Hamilton, New Zealand

Abstract

Purpose – The purpose of this paper is to examine whether the registered charities in New Zealandhave adopted the principle-based corporate governance practices similar to those adopted by thepublicly-listed companies and the effect corporate governance practices have on their financialperformance measured by technical efficiency, allocative efficiency and quick ratio. The paperaddresses four important questions: how registered charities in New Zealand are managed andcontrolled; whether the funds donated to registered charities are utilised effectively; the nature of thecorporate governance practiced by registered charities in New Zealand; and the nature of complianceto the Charities Act 2005.Design/methodology/approach – Panel data for the registered charities over the period 2008-2010are analysed using ordinary least squares (OLS) regression and Tobit model regression. Technicalefficiency, allocative efficiency and quick ratio are used as the dependent variables.Findings – The findings indicate that there is no reporting requirement for the registered charitiesunder the Charities Act 2005 to report detailed information regarding the board make-up, boardcommittees, board meetings, etc. and therefore, registered charities have not reported suchinformation. The results show also that board gender diversity is an important corporate governancemechanism to mitigate agency problem in charitable organisations in New Zealand. However, largeboard size and large donors have potential to increase agency costs in charitable organisations inNew Zealand.Research limitations/implications – Caution should be exercised when interpreting andgeneralising the paper’s results, as this study is a case study of registered charities in New Zealand anddata comprised only large charities that have revenue over NZ$20 m. It should also be noted that therewas a small sample size, which may have had a bearing on the results.Practical implications – This study offers insights for policy makers and practitioners interested inadopting similar corporate governance practices within their country.Social implications – Within New Zealand, issues relating to management and control of charitableorganisations are better understood and as a consequence, development of sector-wise standards couldbe initiated.Originality/value – This research is novel as it investigates the nature of corporate governancepractices relating to the registered charities in New Zealand. The availability of data provided byCharities Commission made this research possible.

Keywords New Zealand, Charities, Corporate governance, Financial performance,Charitable organizations, Charities Commission, Technical efficiency, Allocative efficiency, Quick ratio

Paper type Research paper

1. IntroductionLarge corporate failures that occurred at the beginning of the twenty-first century inAmerica and Europe and the Asian financial crisis of 1997 have highlighted the

The current issue and full text archive of this journal is available atwww.emeraldinsight.com/1743-9132.htm

International Journal of ManagerialFinanceVol. 9 No. 2, 2013pp. 110-132r Emerald Group Publishing Limited1743-9132DOI 10.1108/17439131311307547

110

IJMF9,2

importance of investor protection and good corporate governance practices. Thefinancial crisis of 2007-2009 have also been attributed to the failures and weaknesses incorporate governance practices (OECD, 2009). Deficient risk management practices,weaknesses in board composition and the failure of non-executive directors andshareholders to effectively monitor and scrutinise the decisions of the boardsare highlighted as key areas requiring reform to avoid future failures (Brown andCaldwell, 2009). Some argue that boards’ lack of monitoring and lack of understandingof the nature and impact of risks undertaken has caused the financial crisis (OECD,2009), while others argue that it is the result of lack of shareholder monitoring (Icahn,2009). The widespread concern is that how boards’ and shareholders’ could let thishappen and more specifically, why did the corporate governance system failed somassively.

Although failures of the magnitude reported in the financial sector have notoccurred in the charities sector, there are still concerns of accountability andtransparency issues relating to the sector. Lack of publicly available information aboutthe charitable organisations, its management and how donated funds are utilisedmakes it difficult for the donor organisations as well as general public to selectcharities, which they would prefer to support. Furthermore, there has been an increasein the number of reported cases of theft in charitable organisations involving peopleboth internal (officers, employees, volunteers) and as well as external to theorganisation. Since 2009 courts have prosecuted individuals who in total have stolenmore than $3 million from New Zealand charities, which is equivalent to losing wellover NZ$30,000 each week as a result of fraud (Grant Thornton, 2011; New ZealandHerald, 2011; Personal Verification Limited, 2011). Also there are problems in regard tothe frequency and quality of financial statements provided by charitable organisations.Newbury (1992) reported that “[y] more than half of the sample of 29 charitiesfinancial accounts displayed basic accounting failures and three quarters showedapparent audit failures”. Baskerville (2006) identified commonalities in recentdishonest practice problem areas in not-for-profit organisations in New Zealand andalso evidence of “dominant” executives influencing trustees (Martyn and Gousmett,2011). These practices signal that the way in which charitable organisations aremanaged and controlled need to be improved. The view prevailed among many is thatcharities seeking funds from stakeholders needs to demonstrate transparency andaccountability of the funds received (Abraham, 2007). According to Newbury (1992,1994), there is a need for greater accountability, increased government regulation andas well as self-regulation by the charitable organisations themselves.

Although New Zealand Securities Commission (hereafter NZSC) in 2004promulgated nine high-level principles and guidelines with an aim of improvingcorporate governance practices especially in publicly listed companies as well as in allbusiness entities across all sectors in New Zealand, there is no evidence exists thatindicate that it has been adopted by the charitable organisations. It is evident that thecorporate governance issues that NZSC tried to resolve in the publicly listed companiesare also present in the charities sector and therefore, adoption of the principles andguidelines by charitable organisations will enhance accountability and transparencyissues relating to the sector. However, lack of regulation and also no regulatory bodyexisted that monitored compliance of the charities organisations (Cordery andBaskerville-Morley, 2005). Therefore, entities deemed charitable by the Inland RevenueDepartment (hereafter IRD) were not required to file financial reports whichcontributed towards the reduction in transparency and accountability in the sector.

111

Registeredcharities in

New Zealand

New Zealand government enacted New Zealand Charities Act 2005 and the Actestablished the Charities Commission[1], [2] which came to being from 1 July 2005. Themain functions of the Charities Commission are to establish and maintain a registrationand monitoring system for charitable organisations; and to provide support andeducation to the charitable sector on good governance and management (CharitiesCommission, 2011b). This development was intended to promote public trust andconfidence in the charitable sector and encourage effective use of charitable resources.There are no studies been undertaken that investigate: how registered charities inNew Zealand are managed and controlled; whether the funds donated to registeredcharities are utilised effectively; the nature of the corporate governance practiced byregistered charities in New Zealand; and the nature of compliance to the Charities Act2005. This study is an attempt to fulfill the gap in the literature.

The rest of this paper is organised as follows: Section 2 presents background of thedevelopment and the regulations relating of the charities sector in New Zealand.Section 3 provides literature review and Section 4 presents research method employed,describes variables and data sources. Section 5 reports empirical findings and Section 6provides conclusion.

2. BackgroundPrior to the western colonisation in 1840, there was no relevance for the existence of thecurrent construct of charitable organisational activities in New Zealand. The extendedMaori families (whanau) or wider descent groups (hapu[3]) mainly provided the socialneeds. Individual participation into group activities was more of an obligation ratherthan choice. Therefore, the roots of the current charities organisational forms inNew Zealand can be traced back to the UK where models of similar institutions(patriotic and charitable societies, lodges, clubs and sporting groups) existed thatunderwent vast expansion in Britain since the late eighteen century (Tennant et al.,2008). For example, Oddfellows and Friendly Societies[4] established in New Zealand(Cordery and Baskerville-Morley, 2005) were recognisably the modern form of thoseinstitutions that existed in Britain. Over the years charitable organisations grew innumber, complexity and size[5], as the need and demand for services increased with anincrease in the population (Tennant et al., 2006). In early twentieth century a number ofinternational charitable organisations also extended their branches to New Zealand,including Red Cross (established in 1859 but operations started in 1914), Barnados,Girls Guides, Scout movements and the Royal Society for the Protection of Animals.Myriad of factors have shaped the development of the charitable sector in New Zealand(Tennant et al., 2006). Survival and importance of Maori organisations based on tribaltraditions demonstrate vigour and adaptability of the indigenous social formationswithin the diversified and complex charities sector in New Zealand.

Since inception, charitable organisations in New Zealand have been playing animportant role in supporting disadvantage members of the society (Cullen and Dunne,2006; Fisher, 2006). However, reduction in government expenditure since 1984 toimprove efficiency and effectiveness of government bureaucracy has led to theweakening of the political involvement, where services previously provided by thegovernment are now being provided by the charitable organisations (New ZealandWorking Party on Charities and Sporting Bodies, 1989). This development has ledto a growing importance of the charitable sector in New Zealand as it replacedthe State as the provider of some of the social and welfare services (Nelson, 2000).As a consequence, number of charitable organisations increased considerably which

112

IJMF9,2

represent diverse sector of the economy and provides charitable, religious, health,education and leisure among others services to the community and marginalisedgroups. The estimated number of charities in 2005 was 90,000 (Cullen and Dunne,2006) and the key funding sources for the charitable organisations were biddingfor government contracts[6], donor organisations[7] and directly calling on generalpublic with pleas for funding for their worthwhile causes. Total donationsreceived by charitable organisations has increased from an estimated NZ$356million in 2005 (Cullen and Dunne, 2006) to NZ$5.1 billion in 2009 andNZ$14.3 billion in 2010 (Charities Commission, 2011a). The importance of thecharities sector is further emphasised by the fact that it contributes to the grossdomestic product. In 2004, charitable sector contributed 2.6 per cent towards NewZealand’s gross domestic product (Best et al., 2008) and therefore, in New Zealandgovernment’s view charities sector assists them in furthering their own socialobjectives (Cullen and Dunne, 2006; Fisher, 2006). Initially central governmentplayed a role of the philanthropist to favored organisations and in 1990s onwards,a contractual culture developed where government agencies played an important rolein shaping the activities of the charitable organisation in a more directive way thanever before. This development to some extent blurred the boundary betweengovernment control and self-governance.

Charitable organisations in New Zealand face a dual regulatory structuredepending on which structure they use and whether or not they are a charity (TheTreasury, 2008). Charitable organisation could register themselves as an IncorporatedSociety, under the Incorporated Societies Act 1908, or Charitable Trust, under theCharitable Trust Act 1957, or as a company under the Companies Act 1993. Allorganisations (irrespective of their legal structure) have to register with the NewZealand Companies Office[8], which keeps registers of the various types oforganisations and makes them available for public search. The Charitable TrustAct 1957 did not have any requirement for financial reporting, while IncorporatedSocieties Act 1908 and Companies Act 1993 require respective entities to file financialaccounts with the appropriate registrar. However, audit of financial reports arecompulsory only for the companies that provide protection of limited liability to officebearers (s196 of the Companies Act 1993). Although s58 of the Charitable Trusts Act1957 give powers to the attorney general to examine and inquire into the nature andobjects, administration, management and results thereof, utilisation of these powersappear to be rare (Martyn and Gousmett, 2011). Under the Income Tax Act 1994 anyorganisation in New Zealand can be classified as a charity irrespective of its legal form,provided it meet the definition of a charitable organisation. Section KC 5(1) of theIncome Tax Act 1994 defines charitable organisation as “a society, institution,association, organisation, or trust which is not carried on for the private pecuniaryprofit of any individual and the funds of which are, in the opinion of the Commissioner,applied wholly or principally to any charitable, benevolent, philanthropic, or culturalpurpose within New Zealand”. Since mid-2008 IRD require organisations seekingcharitable status to register with the Charities Commission. To qualify for a “taxcharity” status, charitable organisations must carry out one of the four purposesdrawn from the Preamble to the Statute of Elizabeth 1601 (also known as four headsof charity), that is: the relief of poverty; the advancement of education; theadvancement of religion; and/or other purposes beneficial to the community(Charities Commission, 2011b). Charitable organisation need to demonstrate thatthey fulfill at least one of the objectives and judgement regarding eligibility is based

113

Registeredcharities in

New Zealand

on a case-by-case basis. Charities Commission advises the IRD regarding theregistration of the charity only and the responsibility for income tax exemptionseligibility for organisations is retained by the IRD. Charities registration under the Act2005 began on 1 February 2007 and currently there are 25,785 registered charities and21,535 charities have provided annual returns (Charities Commission, 2011c). CharitiesCommission established under the Charities Act 2005 to promote public trust andconfidence in the charitable sector, to educate and support charities, and to registerand monitor charities that wish to be exempt from income tax. The Commission hasenforcement powers and can impose administrative penalties, issue warning notices,publicise instances of non-compliance to the register, initiate formal investigationsand re-register an organisation that persistently or seriously fails to meet its obligationunder the Act, including failure to fulfill its charitable purposes (Sections 10, 31and 32 of the Act).

However, it has been questioned that reporting requirement for the charitableorganisations is not stringent and far reaching enough as compared to disclosuresrequired for the listed companies under the principle-based corporate governanceapproach (Martyn and Gousmett, 2011). Under the Charities Act 2005, charitableorganisations have to notify the Charities Commission of changes made in particulars(Section 40) and filing of annual reports (Section 41). To some, information providedby charities is not substantive enough (Gousmett, 2011). Reporting requirement ofCharities Commission does not require registered charities to disclose:

. remuneration, benefits and fees paid to trustee;

. terms of office or lack of any such restrictions on trustees;

. terms of reference for its committees, members and their suitability for sittingon such committees;

. succession planning, recruitment practices and trustee appointment criteria;

. remuneration bands of staff over $75,000 including bonus payments; and

. average salary increases of all employees for the preceding 12 months (Martynand Gousmett, 2011).

In addition, Charities Act 2005 do not allow for any creative or more informativeexplanation of the activities of a charity to be reported, as well as financial reportingare also prescriptive which is inconsistent in itself with the nature of charitiesactivities (Gousmett, 2011). The Companies Act 1993 (Sections 131-137) sets out theresponsibilities and obligations[9] of the company directors, however, those common-sense responsibilities are not found in the legislation relating to the charitableorganisations (von Dadelszen, 2011). Furthermore, evidence show that charitiessector in New Zealand is replicating problems experienced in the UK, with over61 per cent of filings of annual returns to the Charities Commission contain errors andomissions (Patel, 2011). Therefore, information provided by charities does not seemto be meaningful and relevant under “comply or explain” approach of corporategovernance practices.

Where stakeholders of charitable organisations are widely distributed, onlydisclosing financial reports and glowing reports by the chair and CEO of the charitableorganisations regarding goals achieved makes it difficult for the beneficialstakeholders to monitor and difficult to make those responsible to be accountable.It is of interest to all stakeholders to know how organisations that are given special tax

114

IJMF9,2

status as a charity are governed and managed. Ongoing onus of accountability andtransparency rests with the trustees.

3. Literature reviewAlthough a plethora of theoretical and empirical studies has been undertaken thatrelate to for-profit organisations’ governance, less is known about the governancepractices of the charities sector (Dyl et al., 2000, p. 335). The economics- and finance-based literature is silent about the governance arrangement of the charitiesorganisations (Eldenburg et al., 2004, p. 5). However, both anecdotal (Ingley andMcCaffrey, 2009) and empirical evidence (Brown and Caylor, 2006a, b; Larcker et al.,2007; MacAvoy and Milstein, 2003; Millstein and MacAvoy, 1998) relating to for-profitorganisations support the view that good governance lead to improved financialperformance. It is acknowledged that good governance practices will not eliminatecompany failures or but if implemented, monitored and updated regularly, will reducefraud and assist organisations to maximise use of scarce resources. The same rationalesuggests that improved corporate governance practices in charitable organisationswould also lead to lower risk and maximisation of the use of scare resources.

Although many different definitions of corporate governance exist in the literature,none is suitable for charitable organisations. According to Tirole (2001, p. 4), corporategovernance (is) the design of institutions that induce or force management tointernalise the welfare of all stakeholders. More specifically, corporate governance isthe system by which organisations are directed and controlled (Anheier, 2005). Sincecharitable organisations are managed by the managers and monitored by the board oftrustees, Jensen and Meckling (1976) state that the separation of the decision-makingrole (managers) from the control role (trustees) leads to the agency problem. Agencyproblem arises when one or more persons (the principal(s)) engage another person(the agent) to perform some service on their behalf which involves delegating somedecision-making authority to the agent ( Jegers, 2009). Jensen and Meckling (1976,p. 308) argue that when both parties are (individual welfare) maximisers there isa good reason to believe that the agent will not always act in the best interest of theprincipal. Also, different stakeholders (principals) do not have identical objectives, oridentical perceptions of effectiveness, there is a possibility that agency problemcould also arise because of these differences, thus, leading to principal-principalagency problem.

Claessens et al. (2002) argue that good corporate governance practices alloworganisations to have easier access to funds, lower costs of capital, improvestakeholder reputation and improve organisational performance. Fisman and Hubbard(2005) report that poor corporate governance practices lead to a reluctance by majordonors to contribute non-targeted funds to not-for-profit organisations. Fisman andHubbard also suggest that poor governance equates to poor monitoring ofmanagement and thus, give rise to agency costs. Others have also reported that lackof monitoring leads to lower performance and higher executive compensation,which is analogous to the for-profit sector (Barros and Nunes, 2008; de Andres-Alonsoet al., 2006).

A number of studies have also investigated the relationship between boardcomposition and organisational performance (Callen et al., 2003; Chabotar, 1989;Chaganti et al., 1985; de Andres et al., 2005; Erhardt et al., 2003; Kang et al., 2007;Kiel and Nicholson, 2003; Rose, 2007; Sheridan and Milgate, 2005; Wan and Ong, 2005;Zahra and Pearce, 1989). Board composition consists of board size, board

115

Registeredcharities in

New Zealand

demographics (gender and age), board recruitment, board education and evaluation.Findings relating to board composition and performance remain inconclusive. Somereported board composition is positively related to company financial performance(Callen et al., 2003; Erhardt et al., 2003; Kang et al., 2007; Kiel and Nicholson, 2003;Sheridan and Milgate, 2005), while others report board composition is inverselyrelated to performance (de Andres et al., 2005; Rose, 2007; Sheridan and Milgate, 2005;Wan and Ong, 2005; Garg, 2007; Yermack, 1996). Furthermore, Chaganti et al. (1985)compared board size of failed and non-failed companies and reported that boards ofnon-failed companies tend to be larger compared to boards of failed companies.Therefore, it is argued that larger boards are likely to be more vigilant becausethere are a greater number of people reviewing managerial actions. Larger boards arelikely to be more knowledgeable and have skills to enhance cognitive conflicts.According to Singh and Harianto (1989), larger board size leads to more effectivemonitoring of management by reducing the domination of the CEO and Hillman andDalziel (2003) argue that organisations may increase board size in order to maximiseprovision of resources for the organisation. In not-for-profit organisations, boardshave a higher proportion of trustees that deal with operational issues and exert moreinfluence over operating functions of the organisation (Oster, 1995). Tinkelman (1996)suggest that charities with larger boards tends to be more efficient. Therefore,we propose our first hypothesis as:

H1. Large board size leads to lower operating costs in charitable organisations.

Gender arguably is the most debated issue, not only in terms of diversity but also inregard to politics and general societal situations. The debate relating to gender inboard diversity is especially timely given that the current movement in Europe andAustralia to increase the number of women on boards.

The concept of gender diversity is supported by the theoretical literature, forexample, Hampel (1998) argue that an increase in diversity provide a balance thatensures that no individual dominate the board decision-making processes. Keasey et al.(1997) state that an increase in board diversity provides linkages to additionalresources and representation for different stakeholders. Huse and Solberg (2006)suggest that diversity improves organisational value and performance throughadditional perspectives. Carter et al. (2003) examined the relationship between boarddiversity and firm value for Fortune 1000 firms and reported statistically significantpositive relationship between the fraction of women or minorities on the board andfirm value. Jurkus et al. (2008) investigated gender diversity in the top managementof Fortune 500 firms and reported that gender diversity is positively associated withboth performance and stock valuation. In the not-for-profit context, Siciliano (1996)investigated board diversity of 240 YMCA organisations and reported gender diversityhad a positive impact on social performance but a negative relationship with theamount of funds raised.

Brennan and McCafferty (1997) suggest that there are two advantages of havingwomen on the board. First, women are not part of the “old boys” network, which allowsthem to be more independent and second, they may have a better understanding ofconsumer behaviour, needs of customers and opportunities for companies in meetingthose needs. Women currently make up only 12.5 per cent of the members of the boardsin the UK and Australia, whereas New Zealand has 8.65 per cent of women directors(McGregor, 2008; Rotherham, 2009). Furthermore, other countries have taken various

116

IJMF9,2

actions to increase participation of women in boards. Norway, Iceland and Spain haveintroduced quotas of 40 per cent female representation on boards, and France hasproposed a similar quota. Meanwhile, New Zealand has also joined internationaltrend to have more female directors on the listed companies’ boards. Based on thefindings stated above, we argue that in charitable organisations boards are likely tohave a high level of diversity. Therefore, we propose our second hypothesis as:

H2. Gender diversity leads to lower operating costs in charitable organisations.

According to de Andres-Alonso et al. (2006), large donors act in similar way toblockholders in for-profit sector in evaluating not-for-profit organisations’ performanceto ensure resources are used in an efficient manner. Large donors have skills, powerand also have access to information to become efficient monitors (Frumkin and Kim,2001; Herman and Renz, 2000; O’Regan and Oster, 2002) because they demand detailedplans, financial budgets and information for each project they finance (Frumkin andKim, 2001). Major donors in New Zealand also demand detailed plans regarding theprojects they finance and where government is the major donor, quality audits are alsobeing undertaken. Therefore, we propose our third hypothesis:

H3. The presence of large donors is positively related to operational efficiency.

Using principle-agency theoretic literature it is argued that agency problem also existsbetween voluntary principals and voluntary agents. Preston and Brown (2004) reportthat boards in numerous not-for-profit organisations consist exclusively of volunteers.Also there are a number of volunteers in different charities providing services for freeas well. Handy (1995) modelled the decision of volunteers to join boards, takingconsideration of wealth and reputation. However, no research has been conducted onhow or the extent to which, volunteers affects charitable organisations’ performance.It is argued that volunteers (who tends to be retired professionals) regularly monitorthe actions of the decision makers against the outcomes of the charitable organisationsto ensure their effort is utilised in a productive manner in terms of deliveringorganisational outcomes. Therefore we propose our fourth hypothesis as:

H4. Presence of volunteers is positively associated with operational efficiency.

Both theoretical and empirical studies undertaken in for-profit sector provide supportfor using debt to discourage overinvestment of free cash flows by self-servingmanagers. Debt acts as a corporate governance mechanism that can voluntarily beused to transfer the functions of monitoring and evaluating managerial performance tothe participants of the capital market (debtholders) (Agrawal and Knoeber, 1996;Begley and Feltham, 1999; Jensen, 1986). According to the governance literatureincreased debt means a large part of the firm’s cash flows will be returned to thedebtholders. Therefore, debt forces managers to consume fewer perquisites andbecome more efficient, thus lessening the probability of bankruptcy and loss of theircontrol and reputation (Grossman and Hart, 1982). Similar reasoning can also beapplied to the charitable organisations where bondholders can also provide externalmonitoring. Therefore we propose our fifth hypothesis as:

H5. Debt is positively associated with operational efficiency of charities.

117

Registeredcharities in

New Zealand

4. Research method4.1 Dependent variableAccording to de Andres-Alonso et al. (2006), defining what efficiency means forcharitable organisations is not an easy task. However, not-for-profit sector studiesundertaken by Callen and Falk (1993), Frumkin and Keating (2001), Sargeant andKaehler (1998) and some watchdog agencies, such as, Better Business Bureau’s WiseGiving Alliance and the American Institute of Philanthropy (Trussel and Parsons,2004) suggest that donors’ principal concern is to have the large portion of theircontribution dedicated to achieving principal organisations outcomes (mission).Therefore, by changing the focus of charitable organisations performance from insideof the organisation to the donors’ point of view, we can obtain meaningful proxies.Using similar method to that used by Weisbrod and Dominguez (1986), Posnett andSandler (1989), Callen (1994), Tinkelman (1996, 1998, 1999) and de Andres-Alonso et al.(2006) among others, we also measure charitable organisations’ efficiency usingcommonly applied proxies relating to financial efficiency, that is, technical efficiencyand allocative efficiency. We define technical efficiency (tEFF) as a ratio of totaloperating expenses to total revenue, where low value is favourable thus indicatingcharity is operating efficiently:

tEFF ¼ Total operating expenses=Total revenue

Allocative efficiency (aEFF) is defined as the ratio of total cost of service provision tototal donated revenue, where higher value indicates that charitable organisations areutilising most of the donated funds in servicing projects for which funds are providedfor, so indicates efficient use of donated funds:

aEFF ¼ Total costs of service provision=Total donated revenue

A survey of the managers of Charitable Trusts indicated that cash flow management isan important and challenging aspect of their operations and also reflected on theorganisations ability to survive as well. For this reason, we have also used quick ratio(QR) which is the proxy for measuring charitable organisations’ ability to generatecash flow on a short notice or demand. QR also reflects on the charitable organisations’policies regarding collection of account receivables, payables and cash management:

QR ¼ ðCurrent assets� InventoryÞ=Current liabilities

4.2 Control variablesWe use natural log of board size (Ln(BDS)) as a proxy for board size (BDS) andproportion of female board of directors (number of female directors/board size) as aproxy for board diversity (DIVERS). Leverage (LEV) is the proportion of the debtdefined as long-term liabilities plus short-term liabilities divided by the total assets.Large donor (LDONOR) is a dumpy variable equal to “1” if the proportion of fundingfrom a particular donor is X20 per cent of the total donated funds, otherwise “0”. Thenatural log of the number of volunteers (VOLUN) in each charity is the proxy volunteerrepresentation at the charity.

To investigate whether large donor(s) are active monitors of managerial decisionswe use proportion of each donor funding, that is, proportion of government grantsor contracts/total donor funding (PGGC2TDF) and other government grants andsponsorship funding/total donor funding (POGSF2TDF).

118

IJMF9,2

As charities are of different sizes in our sample, to control for the size effect on ourresults we use two control variables for organisational size, that is, natural log of totalassets (Ln(TA)) and natural log of total revenue (Ln(TINC)). Since charities belong tosix different sectors, we intend to examine the sectoral effect on charities operationalperformance. We use six sector dummy variables as follows: SECT1 is equal to “1” ifcharity belongs to education sector, otherwise “0”. SECT2 is equal to “1” if charitybelongs to health sector, otherwise “0”. SECT3 is equal to “1” if charity belongs toreligious sector, other “0”. SECT4 is equal to “1” if charity belongs to sport, art andculture sector, otherwise “0”. SECT5 is equal to “1” if charity belongs to community,social services and fundraising sector, otherwise “0”. SECT6 is equal to “1” if charityother sectors than ones mentioned above, otherwise “0”.

4.3 Data and data sourcesData for this research was obtained from the New Zealand Charities Commission.Under the Charities Act 2005 all registered charities are required to submit theiraudited annual financial report and also other relevant information includinggovernance. Not all charities provided all the information, so we focused on charitiesthat were registered between 2008 and 2010 and have total annual revenue 4NZ$20million. Charities that did not provide all the information were excluded and ourfinal sample includes 881 charity-year data.

4.4 Model specificationUsing panel data for the years 2008-2010, ordinary least squares (OLS) regressionis used to measure the effect of governance and control variables on charitiesperformance measured by tEFF, aEFF and QR. Our model is formulated as follows:

PERF ¼ aþ b1BDS þ b2PFD þ b3LEV þ b4LDONOR

þ b5VOLUN þ b6PGGC2TDF þ b7OGSF2TDF

þ b8SizeþXT

i¼1

biSecti þ e

where PERF is the charities efficiency measured by tEFF, aEFF and QR; SIZE ¼Ln(TA) or Ln(TINC); T ¼ 6; I ¼ ranges from 1 to 6.

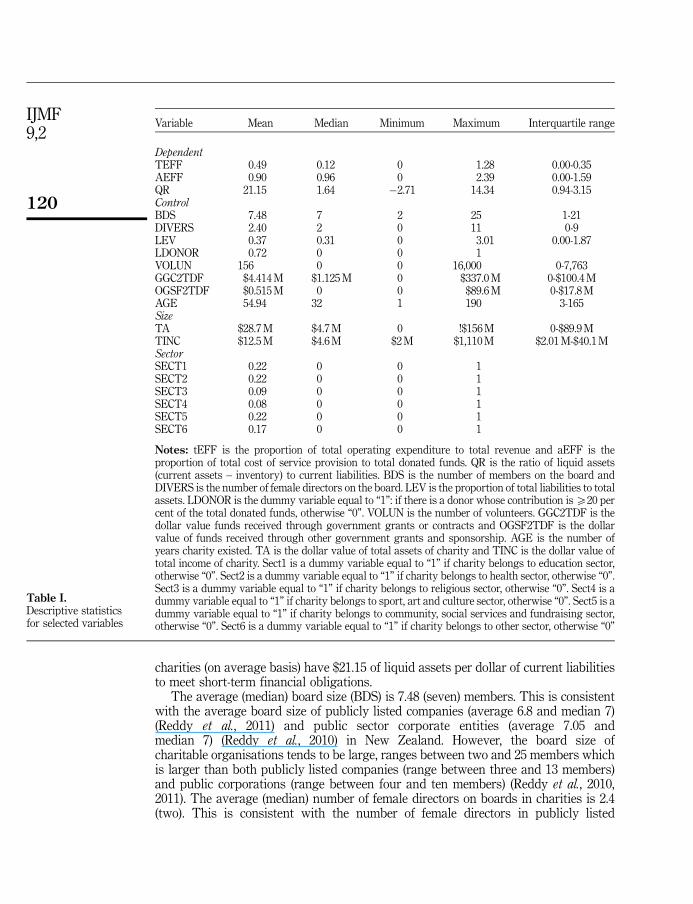

5. Empirical results5.1 Descriptive statisticsTable I provides a summary of descriptive statistics for the panel data, includingmeans, medians, minimums, maximums and interquartile ranges. The mean (median)of tEFF is 48 per cent (12 per cent) with the interquartile range of 0-35 per cent. Thisindicates that charities are operating efficiently as their overall expenditure on anaverage basis is 48 cents per dollar of total revenue. The mean (median) aEFF is 90 percent (96 per cent) and interquartile range of 0-159 per cent. This indicates that charitiesare spending 90 cents per dollar of donated funds in projects for which they gotfunding for. This indicates that the registered charities in New Zealand are utilisingtheir funds in an efficient manner. The QR is a proxy for measuring the short-termliquidity capacity of the company. The mean of QR is 21.15 (1.64), thus show that

119

Registeredcharities in

New Zealand

charities (on average basis) have $21.15 of liquid assets per dollar of current liabilitiesto meet short-term financial obligations.

The average (median) board size (BDS) is 7.48 (seven) members. This is consistentwith the average board size of publicly listed companies (average 6.8 and median 7)(Reddy et al., 2011) and public sector corporate entities (average 7.05 andmedian 7) (Reddy et al., 2010) in New Zealand. However, the board size ofcharitable organisations tends to be large, ranges between two and 25 members whichis larger than both publicly listed companies (range between three and 13 members)and public corporations (range between four and ten members) (Reddy et al., 2010,2011). The average (median) number of female directors on boards in charities is 2.4(two). This is consistent with the number of female directors in publicly listed

Variable Mean Median Minimum Maximum Interquartile range

DependentTEFF 0.49 0.12 0 1.28 0.00-0.35AEFF 0.90 0.96 0 2.39 0.00-1.59QR 21.15 1.64 �2.71 14.34 0.94-3.15ControlBDS 7.48 7 2 25 1-21DIVERS 2.40 2 0 11 0-9LEV 0.37 0.31 0 3.01 0.00-1.87LDONOR 0.72 0 0 1VOLUN 156 0 0 16,000 0-7,763GGC2TDF $4.414 M $1.125 M 0 $337.0 M 0-$100.4 MOGSF2TDF $0.515 M 0 0 $89.6 M 0-$17.8 MAGE 54.94 32 1 190 3-165SizeTA $28.7 M $4.7 M 0 !$156 M 0-$89.9 MTINC $12.5 M $4.6 M $2 M $1,110 M $2.01 M-$40.1 MSectorSECT1 0.22 0 0 1SECT2 0.22 0 0 1SECT3 0.09 0 0 1SECT4 0.08 0 0 1SECT5 0.22 0 0 1SECT6 0.17 0 0 1

Notes: tEFF is the proportion of total operating expenditure to total revenue and aEFF is theproportion of total cost of service provision to total donated funds. QR is the ratio of liquid assets(current assets – inventory) to current liabilities. BDS is the number of members on the board andDIVERS is the number of female directors on the board. LEV is the proportion of total liabilities to totalassets. LDONOR is the dummy variable equal to “1”: if there is a donor whose contribution is X20 percent of the total donated funds, otherwise “0”. VOLUN is the number of volunteers. GGC2TDF is thedollar value funds received through government grants or contracts and OGSF2TDF is the dollarvalue of funds received through other government grants and sponsorship. AGE is the number ofyears charity existed. TA is the dollar value of total assets of charity and TINC is the dollar value oftotal income of charity. Sect1 is a dummy variable equal to “1” if charity belongs to education sector,otherwise “0”. Sect2 is a dummy variable equal to “1” if charity belongs to health sector, otherwise “0”.Sect3 is a dummy variable equal to “1” if charity belongs to religious sector, otherwise “0”. Sect4 is adummy variable equal to “1” if charity belongs to sport, art and culture sector, otherwise “0”. Sect5 is adummy variable equal to “1” if charity belongs to community, social services and fundraising sector,otherwise “0”. Sect6 is a dummy variable equal to “1” if charity belongs to other sector, otherwise “0”

Table I.Descriptive statisticsfor selected variables

120

IJMF9,2

companies and public sector corporate entities in New Zealand (Reddy et al., 2010,2011). In total, 836 charities have at least one or more female members on boards. Thehighest number of female directors on boards is 11 members.

Leverage is the proxy for measuring the level of commitment provided by thebondholders. The mean (median) leverage ratio is 0.37 (0.31). This shows charitiesare borrowing 37 cent in every dollar of assets. The yearly analysis of data shows thatthe level of debt in charities has increased from 35 per cent in 2008 to 40 per cent in2010[10]. Since an increased number of charities are bidding for a small pool of fundsthat are available for distribution result being that each charity is receiving only afraction of the funds requested, thus forcing charities to borrow money to cover eithertheir operational costs and/or to service the contracts. Also, it is becoming difficult towin government contracts as government is cutting costs and attempting to improveefficiency as well. The results in Table I show that large registered charities aremanaged efficiently (see results for both tEFF and aEFF), thus makes it easier forcharities to borrow funds.

Charities have had a number of different sources of donated funds. On an averagebasis, 54 per cent ($4.41 M) of income came from government grants or contracts, 11.8per cent ($0.52 M) from other government grants and sponsorship, 42 per cent ($5.3 M)through income from service provision and the reminder through gifts, bequests andincome from interest and dividends. The average (median) age of the charitableorganisation is 55 (37) years with an interquartile range of 1-165 years. The resultshow that majority of the charities in our sample has been in existent for more than37 years. This indicates that these charities have gained knowledge relating to policyand procedures development, and have also gained experience in their business.

We have used two variables as proxies for size, that is, total assets and total income.The average (median) total assets are $28.7 M ($4.7 M). This result indicates thatmajoring of the charities has assets more than $4.7 M and the largest charity haveassets in excess of $156 M. The average (median) amount of income received bycharities is $12.5 M ($4.6 M). This result indicate that majority of the charities haveincome higher than $4.6 M with largest charity having income in excess of $1,110 M.

The sectoral analysis result show that 22 per cent of the charities belong toeducation sector, 22 per cent health, 9 per cent religious, 8 per cent sports, arts andculture, 22 per cent community, social services and fundraising and 17 per cent other.

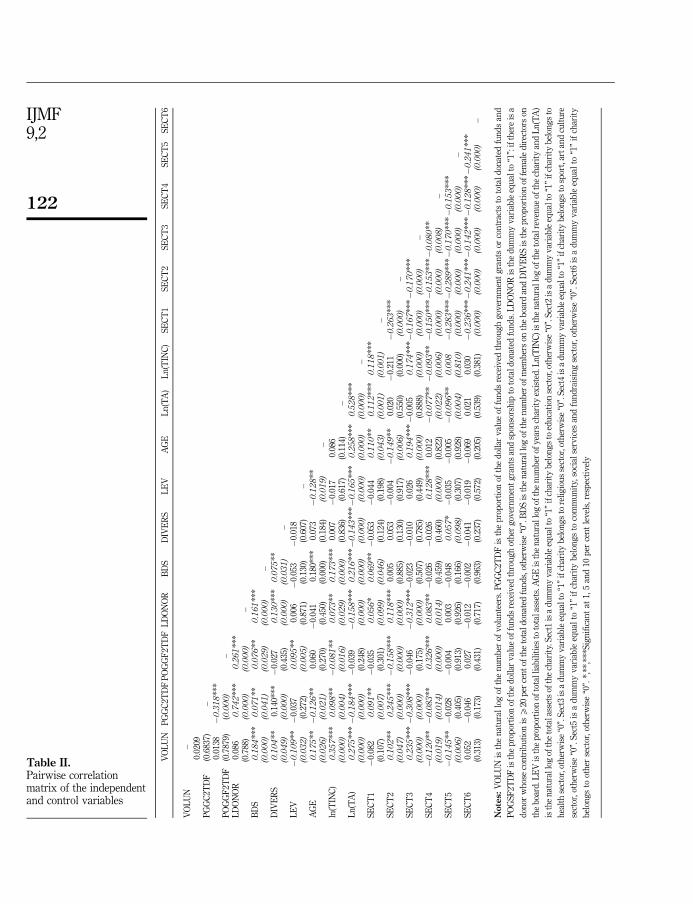

5.2 Pairwise correlationTable II report pairwise correlation matrices for the independent variables. The highestcorrelation is between LDONOR and PGGC2TDF at 0.74, indicating that a largeportion of charities revenue is generated from government grants and contracts. Thecorrelation between LnTA and LnTINC is 0.53 indicating that charities that have largeasset base also tend to have large total revenue. This result is not surprising ascharities with large assets base need more income to service fixed costs relating to theassets. Apart from these exceptions, other correlations range between 0.01 and 0.36.Since none of the coefficient of the correlations between independent variables isabove 0.75, the likelihood of multicollinearity issues arising from the OLS regressionanalysis is low.

5.3 OLS regression of tEFF, AEFF and QR, independent variablesTable III report the OLS regression results of the relationship between the dependentvariables (tEFF, aEFF, QR) and the independent variables. Results reported in

121

Registeredcharities in

New Zealand

VO

LU

NP

GG

C2T

DF

PO

GG

F2T

DF

LD

ON

OR

BD

SD

IVE

RS

LE

VA

GE

Ln

(TA

)L

n(T

INC

)S

EC

T1

SE

CT

2S

EC

T3

SE

CT

4S

EC

T5

SE

CT

6

VO

LU

N–

PG

GC

2TD

F0.

0209

(0.6

837)

–

PO

GG

F2T

DF

0.01

38(0

.787

9)�

0.3

18**

*(0

.000)

–L

DO

NO

R0.

086

0.7

42**

*0.2

61**

*(0

.788

)(0

.000)

(0.0

00)

–B

DS

0.1

84**

*0.0

71**

0.0

76**

0.1

61**

*(0

.000)

(0.0

41)

(0.0

29)

(0.0

00)

–D

IVE

RS

0.1

04**

0.14

0***

�0.

027

0.1

30**

*0.0

75**

(0.0

49)

(0.0

00)

(0.4

35)

(0.0

00)

(0.0

31)

–L

EV

�0.1

09**�

0.03

70.0

95**

0.00

6�

0.05

3�

0.01

8(0

.032)

(0.2

72)

(0.0

05)

(0.8

71)

(0.1

30)

(0.6

07)

–A

GE

0.1

75**�

0.1

26**

0.06

0�

0.04

10.

180*

**0.

073

�0.1

28**

(0.0

26)

(0.0

21)

(0.2

70)

(0.4

50)

(0.0

00)

(0.1

84)

(0.0

19)

–ln

(TIN

C)

0.3

57**

*0.0

98**

�0.0

81**

0.0

73**

0.1

73**

*0.

007

�0.

017

0.08

6(0

.000)

(0.0

04)

(0.0

16)

(0.0

29)

(0.0

00)

(0.8

36)

(0.6

17)

(0.1

14)

–L

n(T

A)

0.2

75**

*�

0.1

84**

*�

0.03

9�

0.1

58**

*0.2

16**

*�

0.1

43**

*�

0.1

65**

*0.2

58**

*0.5

28**

*(0

.000)

(0.0

00)

(0.2

48)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

–S

EC

T1

�0.

082

0.0

91**

�0.

035

0.0

56*

0.0

69**�

0.05

3�

0.04

40.1

10**

0.1

12**

*0.1

18**

*(0

.107

)(0

.007)

(0.3

01)

(0.0

99)

(0.0

46)

(0.1

24)

(0.1

98)

(0.0

43)

(0.0

01)

(0.0

01)

–S

EC

T2

0.1

02**

0.2

45**

*�

0.1

58**

*0.1

18**

*0.

005

0.05

3�

0.00

4�

0.1

49**

0.02

0�

0.21

1�

0.2

63**

*(0

.047)

(0.0

00)

(0.0

00)

(0.0

00)

(0.8

85)

(0.1

30)

(0.9

17)

(0.0

06)

(0.5

50)

(0.0

00)

(0.0

00)

–S

EC

T3

0.2

35**

*�

0.3

08**

*�

0.04

6�

0.3

12**

*�

0.02

3�

0.01

00.

026

0.1

94**

*�

0.00

50.1

74**

*�

0.1

67**

*�

0.1

70**

*(0

.000)

(0.0

00)

(0.1

75)

(0.0

00)

(0.5

07)

(0.7

85)

(0.4

49)

(0.0

00)

(0.8

88)

(0.0

00)

(0.0

00)

(0.0

00)

–S

EC

T4

�0.1

20**�

0.0

83**

0.3

26**

*0.0

83**�

0.02

6�

0.02

60.1

28**

*0.

012

�0.0

77**�

0.0

93**�

0.1

50**

*�

0.1

53**

*�

0.0

80**

(0.0

19)

(0.0

14)

(0.0

00)

(0.0

14)

(0.4

59)

(0.4

60)

(0.0

00)

(0.8

22)

(0.0

22)

(0.0

06)

(0.0

00)

(0.0

00)

(0.0

08)

–S

EC

T5

�0.1

45**�

0.02

8�

0.00

40.

003

�0.

048

0.0

57*�

0.03

5�

0.00

5�

0.0

96**

0.0

08

�0.2

83**

*�

0.2

89**

*�

0.1

70**

*�

0.1

53**

*(0

.006)

(0.4

05)

(0.9

13)

(0.9

26)

(0.1

66)

(0.0

98)

(0.3

07)

(0.9

28)

(0.0

04)

(0.8

10)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

–S

EC

T6

0.05

2�

0.04

60.

027

�0.

012

�0.

002

�0.

041

�0.

019

�0.

069

0.02

10.

030

�0.2

36**

*�

0.2

41**

*�

0.1

42**

*�

0.1

28**

*�

0.2

41**

*(0

.313

)(0

.173

)(0

.431

)(0

.717

)(0

.963

)(0

.237

)(0

.572

)(0

.205

)(0

.539

)(0

.381

)(0

.000)

(0.0

00)

(0.0

00)

(0.0

00)

(0.0

00)

–

Note

s:

VO

LU

Nis

the

nat

ura

llo

gof

the

nu

mb

erof

vol

un

teer

s.P

GG

C2T

DF

isth

ep

rop

orti

onof

the

dol

lar

val

ue

offu

nd

sre

ceiv

edth

rou

gh

gov

ern

men

tg

ran

tsor

con

trac

tsto

tota

ld

onat

edfu

nd

san

d

PO

GS

F2T

DF

isth

ep

rop

orti

onof

the

dol

lar

val

ue

offu

nd

sre

ceiv

edth

rou

gh

oth

erg

over

nm

ent

gra

nts

and

spon

sors

hip

toto

tal

don

ated

fun

ds.

LD

ON

OR

isth

ed

um

my

var

iab

leeq

ual

to“1

”:if

ther

eis

a

don

orw

hos

eco

ntr

ibu

tion

isX

20p

erce

nt

ofth

eto

tal

don

ated

fun

ds,

oth

erw

ise

“0”.

BD

Sis

the

nat

ura

llog

ofth

en

um

ber

ofm

emb

ers

onth

eb

oard

and

DIV

ER

Sis

the

pro

por

tion

offe

mal

ed

irec

tors

on

the

boa

rd.L

EV

isth

ep

rop

ort

ion

ofto

tall

iab

ilit

ies

toto

tala

sset

s.A

GE

isth

en

atu

ral

log

ofth

en

um

ber

ofye

ars

char

ity

exis

ted

.Ln

(TIN

C)i

sth

en

atu

rall

ogof

the

tota

lrev

enu

eof

the

char

ity

and

Ln

(TA

)

isth

en

atu

rall

ogof

the

tota

lass

ets

ofth

ech

arit

y.S

ect1

isa

du

mm

yv

aria

ble

equ

alto

“1”

ifch

arit

yb

elon

gs

toed

uca

tion

sect

or,o

ther

wis

e“0

”.S

ect2

isa

du

mm

yv

aria

ble

equ

alto

“1”

ifch

arit

yb

elon

gs

to

hea

lth

sect

or,o

ther

wis

e“0

”.S

ect3

isa

du

mm

yv

aria

ble

equ

alto

“1”

ifch

arit

yb

elon

gs

tore

lig

iou

sse

ctor

,oth

erw

ise

“0”.

Sec

t4is

ad

um

my

var

iab

leeq

ual

to“1

”if

char

ity

bel

ong

sto

spor

t,ar

tan

dcu

ltu

re

sect

or,o

ther

wis

e“0

”.S

ect5

isa

du

mm

yv

aria

ble

equ

alto

“1”

ifch

arit

yb

elon

gs

toco

mm

un

ity,

soci

alse

rvic

esan

dfu

nd

rais

ing

sect

or,o

ther

wis

e“0

”.S

ect6

isa

du

mm

yv

aria

ble

equ

alto

“1”

ifch

arit

y

bel

ong

sto

oth

erse

ctor

,ot

her

wis

e“0

”.*,

**,*

**S

ign

ific

ant

at1,

5an

d10

per

cen

tle

vel

s,re

spec

tiv

ely

Table II.Pairwise correlationmatrix of the independentand control variables

122

IJMF9,2

column 2 in Table III show that DIVERS (proportion of female directors on boards) hasa negative coefficient which is statistically significant at 5 per cent level, thus indicatethat presence of female directors improves technical efficiency in charities. An increasein female director by one leads to an increase in technical efficiency by 28.5 per cent.This finding is consistent with the findings reported by Huse and Solberg (2006),

tEFF SE aEFF SE QR SE

Constant 0.876** 0.299 �1.021 2.463 3.048** 1.197(2.93) (�0.41) (2.55)

BDS 0.066* 0.038 �0.149 �0.279 �0.413** 0.157(1.76) (�0.53) (�2.64)

DIVERS �0.113** 0.070 0.218 0.521 0.843** 0.282(�1.81) (0.420) (2.99)

PGGC2TDF �0.014 0.066 0.650 0.524 �0.312 0.263(�0.22) (1.24) (�1.18)

POGCF2TDF �0.151* 0.082 0.834 0.295 0.329(�1.84) (1.22) (0.90)

LDONOR 0.159** 0.068 �0.940* 0.566 �1.037*** 0.273(2.35) (�1.76) (�3.80)

VOLUN 0.010 0.008 �0.042 0.061 �0.060* 0.032(1.19) (�0.70) (�1.83)

LEV 0.023 0.022 0.068 0.141 �0.135 0.885(1.07) (0.48) (�1.52)

AGE 0.060*** 0.018 0.086 0.148 0.023 0.073(3.37) (0.58) (0.32)

Ln(TA) �0.020 0.014 0.196* 0.108 0.145** 0.058(�1.36) (1.79) (2.51)

Ln(TINC) �0.07 0.048 �0.191 0.193 �0.153 0.098(0.83) (�0.99) (�1.55)

Sector dummies Yes Yes YesF-value 2.73*** 0.67 5.56***( p-value) (0.001) (0.808) (0.000)Adjusted R2 0.14 0.31(R2) (0.22) (0.37)n 159 159 157

Notes: VOLUN is the natural log of the number of volunteers. PGGC2TDF is the proportion of thedollar value of funds received through government grants or contracts to total donated funds andPOGSF2TDF is the proportion of the dollar value of funds received through other government grantsand sponsorship to total donated funds. LDONOR is the dummy variable equal to “1”: if there is adonor whose contribution is X20 per cent of the total donated funds, otherwise “0”. BDS is the naturallog of the number of members on the board and DIVERS is the proportion of female directors on theboard. LEV is the proportion of total liabilities to total assets. AGE is the natural log of the number ofyears charity existed. Ln(TINC) is the natural log of the total revenue of the charity and Ln(TA) is thenatural log of the total assets of the charity. Sect1 is a dummy variable equal to “1” if charity belongs toeducation sector, otherwise “0”. Sect2 is a dummy variable equal to “1” if charity belongs to healthsector, otherwise “0”. Sect3 is a dummy variable equal to “1” if charity belongs to religious sector,otherwise “0”. Sect4 is a dummy variable equal to “1” if charity belongs to sport, art and culture sector,otherwise “0”. Sect5 is a dummy variable equal to “1” if charity belongs to community, social servicesand fundraising sector, otherwise “0”. Sect6 is a dummy variable equal to “1” if charity belongs toother sector, otherwise “0”. *,**,***Significant at 1, 5 and 10 per cent levels, respectively

Table III.OLS regression

of dependent andcontrol variables

123

Registeredcharities in

New Zealand

Carter et al. (2003), Jurkus et al. (2008), Reddy et al. (2008) and Siciliano (1996). Thisfinding suggest that female directors on boards do provide vigilance and monitoringon decision-making processes that lead to an improvement in technical efficiency; thussupporting our second hypothesis that diversity lowers operating costs in charities.

The coefficient of POGCF2TDF (proportion of other type of funders) is negativeand statistically significant at 10 per cent level. This finding suggests that somestakeholders (i.e. government and other type of funders) do have stringent monitoringrequirements to ensure funds donated are utilised in projects that was funded for. Thedownside of having stringent monitoring requirements is that it increases the costsof compliance. However, having stringent requirements for projects influences charitiesto use donated funds efficiently. This finding supports the proposition proposed byFrumkin and Kim (2001) that certain donors do have enough power and information toprovide monitoring and influence charities outcome.

The coefficient of board BDS (board size) is positive and statistically significant at10 per cent level, indicate that larger boards tend to increase the cost of monitoring andreduces efficiency. This finding is consistent with the findings reported by Eisenberget al. (1998), Hossain et al. (2001) and Reddy et al. (2008) that large boards leads to lowerfinancial performance. According to Forbes and Milliken (1999), large boards aredifficult to coordinate, have difficulty making value maximising strategic decisions,and as a consequence, fail to implement strategies that maximises value. The result forLDONOR (large donor) is surprising as its coefficient is positive and statisticallysignificant at 5 per cent level. This indicates that presence of large donors tends toincrease the total cost operating cost of charities. One plausible explanation could belarge donors have stringent reporting and quality audit requirements which increasesthe cost of compliance, thus increasing the overall compliance cost of charities. To meetthe large donors stringent requirements, charities have to hire additional expertise orconsultants which contributes to the total costs as well. The coefficient of the variableAGE is positive and statistically significant at 1 per cent level. This indicates thatas charities age increases, their costs also increase as well. A plausible explanationcould be that as charities get older, they increase in size which contributes to anincrease in overall costs. The analysis shows that correlation between AGE and SIZE(LnTA and LnTINC) is positive as well as the correlation between AGE and tEFF andAGE and aEFF. The sectoral analysis shows that those charities that belong to SECT5(community, social services and fundraising sector) seems to contribute towardsoverall costs as its coefficient is positive and statistically significant at 10 per cent level.

Results reported in column 6 in Table III for QR as the dependent variable areconsistent to that reported in column 2 using tEFF as the dependent variable. DIVERS(proportion of female directors on boards) have a positive coefficient which isstatistically significant at 5 per cent level, thus indicate that presence of femaledirectors on boards improves financial risk by having a close eye on the liquidityof charities (QR). This finding supports the view that female directors on boards doprovide vigilance and monitoring of financial risk of charities; thus supporting oursecond hypothesis that diversity lowers cost by managing liquidity risk of charities.

The coefficient of board BDS (board size) is negative and statistically significant at5 per cent level, indicate that larger boards tend to increase the cost of monitoring andthus, increase financial risk by not closely monitoring liquidity risk of the charities.The result for LDONOR (large donor) is surprising as its coefficient is negative andstatistically significant at 1 per cent level. This indicates that presence of large donorstends to divert the focus of the charities boards towards bigger picture that is, fulfilling

124

IJMF9,2

the requirements for the contracts rather than managing liquidity risk. The stringentreporting and quality audit requirements also contributes towards increasing theoverall costs of charities. Another plausible reason could be that charities become laxin monitoring liquidity risk as they know that large donors will bail them out if theyget into short-term financial problem. Since large donors have invested large sums offunds and they will ensure that the project is successfully completed, otherwise largedonors themselves have potential to come under scrutiny. The coefficient of thevariable VOLUN is negative and statistically significant at 10 per cent level. Thisindicates that charities that have many volunteers will result in having less liquidity.A plausible explanation could be that volunteers are reimbursed for petrol expenses orgiven allowances (cash) which have an impact on the liquidity of the charities. Thecoefficient of the variable LnTA is positive and statistically significant at 5 per centlevel, thus indicate that charities that have a large asset base tends to manage liquidityrisk better. A plausible explanation could be that charities with large asset base canprovide multiple services and therefore, increases their revenue which contributestowards lowing liquidity risk.

5.3.1 Robustness check. To check whether the dependent variables (tEFF, aEFF andQR) are correlated with the independent variables, we first performed pairwisecorrelations between the dependent and independent variables. Our results[11] showthat all the correlations are below 0.3 thus indicate that there is no concern formulticollinearity issues relating to the data[12].

Second, we tested all the independent variables whether they are endogenouslyrelated to the each of the dependent variable. Our test showed negative results;therefore we conclude that there is no endogeneity effect between dependent andindependent variables.

Third, we did Tobit model regression to check whether OLS regression resultsare biased. Results reported in Table IV for Tobit model regression are similar to theOLS regression results reported in Table III. Therefore, we conclude that OLSregression results reported in Table IV are not biased. However, standard errorsare bit smaller for the Tobit model regression for estimated coefficients of theindependent variables.

6. ConclusionThe major contribution of our study is to introduce agency theory perspective andempirical analysis to the corporate governance practices in charitable organisations inNew Zealand. This is a first study undertaken in New Zealand that analyses the effectof corporate governance practices on charitable organisations. The results highlightthe corporate governance mechanisms that have potential to mitigate agency costs incharities sector. A number of mechanisms are examined, including board size, boarddiversity (gender), types of donors, presence of large donor, volunteers and leverage.

Since charitable organisations have not reported and are not required under theCharities Act 2005 to report detailed information relating to the make-up of boards andboard committees (i.e. whether they are independent, have financial qualifications,appointment period and expiry and number of meeting attended, etc.), it is difficult toascertain from the data provided by the Charities Commission the extent to whichcharitable organisations have complied with to the principles-based corporategovernance practices. However, the empirical evidence supports the view that boarddiversity contributes positively towards financial performance of registered charitiesmeasured by both technical efficiency (tEFF) and QR. Our results also provide support

125

Registeredcharities in

New Zealand

tEFF SE aEFF SE QR SE

Constant 0.912** 0.287 0.789 0.773 2.768** 1.146(3.17) (1.02) (2.42)

BDS 0.068* 0.036 �0.160* 0.094 �0.412** 0.148(1.86) (�1.78) (�2.78)

DIVERS �0.114* 0.067 0.085 0.174 0.843** 0.267(�1.75) (0.49) (3.16)

PGGC2TDF �0.014 0.063 0.219 0.167 �0.311 0.249(�0.22) (1.31) (�1.25)

POGCF2TDF �0.150* 0.078 0.153 0.211 0.294 0.312(�1.93) (0.73) (0.95)

LDONOR 0.161** 0.064 �0.164 0.173 �1.037*** 0.258(2.49) (�0.95) (�4.01)

VOLUN 0.010 0.008 0.007 0.020 �0.060* 0.031(1.26) (0.350) (�1.95)

LEV 0.023 0.021 0.027 0.052 �0.135 0.083(1.12) (0.51) (�1.60)

AGE 0.060*** 0.017 0.110** 0.046 0.023 0.069(3.50) (2.36) (0.34)

Ln(TA) �0.019 0.014 0.036 0.035 0.145** 0.055(�1.44) (1.02) (2.65)

Ln(TINC) �0.007 0.023 �0.082 0.061 �0.152 0.092(�0.30) (�1.32) (�1.65)

SECTOR2 �0.022 0.0561 �0.009 0.146 0.192 0.225

(�0.40) (�0.07) (0.85)3 0.006 0.075 �0.196 0.197 �0.046 0.300

(0.09) (�0.99) (�0.15)4 �0.135** 0.067 0.047 0.172 0.186 0.266

(�2.03) (0.27) (0.70)5 0.038 0.045 �0.081 0.118 0.461** 0.183

(0.84) (�0.67) (2.52)6 �0.040 0.046 �0.198 0.121 0.279 0.183

(�0.88) (�1.63) (1.53)LR ch12 (15 ( p-value) 39.87*** 15.93 72.95***

(0.000) (0.386) (0.000)Pseudo R2 �1.046 0.0682 0.172Sigma 0.1867 0.011 0.462 0.033 0.741 0.042n 159 159 157

Notes: VOLUN is the natural log of the number of volunteers. PGGC2TDF is the proportion of thedollar value of funds received through government grants or contracts to total donated funds andPOGSF2TDF is the proportion of the dollar value of funds received through other government grantsand sponsorship to total donated funds. LDONOR is the dummy variable equal to “1”: if there is adonor whose contribution is X20 per cent of the total donated funds, otherwise “0”. BDS is the naturallog of the number of members on the board and DIVERS is the proportion of female directors on theboard. LEV is the proportion of total liabilities to total assets. AGE is the natural log of the number ofyears charity existed. Ln(TINC) is the natural log of the total revenue of the charity and Ln(TA) is thenatural log of the total assets of the charity. Sect1 is a dummy variable equal to “1” if charity belongs toeducation sector, otherwise “0”. Sect2 is a dummy variable equal to “1” if charity belongs to healthsector, otherwise “0”. Sect3 is a dummy variable equal to “1” if charity belongs to religious sector,otherwise “0”. Sect4 is a dummy variable equal to “1” if charity belongs to sport, art and culture sector,otherwise “0”. Sect5 is a dummy variable equal to “1” if charity belongs to community, social servicesand fundraising sector, otherwise “0”. Sect6 is a dummy variable equal to “1” if charity belongs toother sector, otherwise “0”. *,**,***Significant at 1, 5 and 10 per cent levels, respectively

Table IV.Tobit modelregression of dependentand control variables

126

IJMF9,2

to the view that certain donor types also lead to improvement in financial performancemeasured by tEFF.

However, the evidence also suggests that large boards and presence of largevolunteers increases agency costs of charities.

Caution should be exercised when interpreting results as our study is it is a casestudy of New Zealand environment and data comprised only large charities thathave revenue over NZ$20 M. It is also to be noted that we have a small sample size,which may have had a bearing on our results.

Finally, it is to be noted that this study is timely given the concerns relating to themanagement and reporting requirements for charities organisations. The extent towhich Charities Commission can work on improving reporting requirement of charitiesorganisations to lift corporate governance practices to that of publicly listed companiesand public sector corporations will provide research opportunities for the future.

Notes

1. Charities Commission is an autonomous Crown Entity, however, must have regard forgovernment policy when directed by the responsible minister (Charities Commission,2011b).

2. It is to be noted that the Government Administration Select Committee is due to report onthe Crown Entities Reform Bill to the Parliament on 29 February 2012. If passed, the Billwill disestablish the Charities Commission, and transfer its registration, education andmonitoring and investigations functions to the Department of Internal Affairs from 1 July2012 (Crown Entities Reform Bill, 2012).

3. Usually characterised as sub-tribes and iwi (tribes).

4. By 1884, there were 281 Friendly Societies in New Zealand with 21,000 members (Corderyand Baskerville-Morley, 2005).

5. Society for the Protection of Women and Children established a branch in Dunedin in 1884and Plunket Society (help for mothers with babies) was established in 1907.

6. Contract related.

7. Philanthropic trusts.

8. The New Zealand companies office supports the statutory office positions of Registrar ofCompanies and Registrar of Incorporated Societies (The Treasury, 2008).

9. Include requirements to act in good faith and in the interest of the company, to use powers fora proper purpose, not act in contravention of the Companies Act or the company’sconstitution, not run the company recklessly or at substantial risk to creditors, and toexercise reasonable care, diligence and skill, taking into account the nature of the company,the nature of the decision, the position of the director’s and the nature of the director’sresponsibilities (von Dadelszen, 2011).

10. Details of this analysis can be obtained from the authors on request.

11. Results not provided but can be obtained from the authors if required.

12. Results for the test are not provided but can be obtained from the authors on request.

References

Abraham, A. (2007), “Tsunami swamps aid agency accountability: governance waivesrequirements”, Australian Accounting Review, Vol. 17 No. 1, pp. 4-12.

127

Registeredcharities in

New Zealand

Agrawal, A. and Knoeber, C.R. (1996), “Firm performance and mechanisms to control agencyproblems between managers and shareholders”, Journal of Financial and QuantitativeAnalysis, Vol. 31 No. 3, pp. 377-97.

Anheier, H.K. (2005), Nonprofit Organisations: Theory, Management, Policy, Routledge, London.

Barros, C.P. and Nunes, F. (2008), “Social capital in non-profit organizations: a multi-disciplinaryperspective”, The Journal of Socio-Economics, Vol. 37 No. 4, pp. 1554-69.

Baskerville, R. (2006), “What mischief does this legislation week to cure?”, CharteredAccountants Journal, Vol. 85 No. 5, pp. 38-9.

Begley, J. and Feltham, G.A. (1999), “An empirical examination of the relation between debtcontracts and management incentives”, Journal of Accounting and Economics, Vol. 27No. 2, pp. 335-44.

Best, P., Buckby, S. and Bundesen, L. (2008), BDO Not-For-Profit Fraud Survey 2008, BDOInternational, Wellington.

Brennan, N. and McCafferty, J. (1997), “Corporate governance practices in Irish companies”,IBAR, Vol. 18 No. 1, pp. 116-35.

Brown, A. and Caldwell, S. (2009), “An update on corporate governance in the wake of the creditcrisis”, available at: www.bellgully.com/respources/resource.02244.asp (accessed 24 July2011).

Brown, L. and Caylor, M. (2006a), Corporate Governance and Firm Operating Performance,Georgia State University, Atlanta, GA.

Brown, L. and Caylor, M. (2006b), “Corporate governance and firm valuation”, Journal ofAccounting and Public Policy, Vol. 25 No. 4, pp. 409-34.

Callen, J.L. (1994), “Money donations, volunteering, and organizational efficiency”, The Journal ofProductivity Analysis, Vol. 5 No. 3, pp. 215-28.

Callen, J.L. and Falk, H. (1993), “Agency and efficiency in nonprofit organizations”, AccountingReview, Vol. 68 No. 1, pp. 48-65.

Callen, J.L., Klein, A. and Tinkelman, D. (2003), “Board composition, committees, andorganizational efficiency: the case of nonprofits”, Nonprofit and Voluntary SectorQuarterly, Vol. 32 No. 4, pp. 493-520.

Carter, D.A., Simkins, B.J. and Simpson, W.G. (2003), “Corporate governance, board diversity, andfirm value”, Financial Review, Vol. 38 No. 1, pp. 33-53.

Chabotar, K.J. (1989), “Financial ratio analysis comes to nonprofits”, The Journal of HigherEducation, Vol. 60 No. 2, pp. 188-208.

Chaganti, R.S., Mahajan, V. and Sharma, S. (1985), “Corporate board size, composition andcorporate failures retailing industries”, Journal of Management Studies, Vol. 22 No. 4,pp. 400-17.

Charities Commission (2011a), “A snapshot of New Zealand’s charitable sector: a profile ofregistered charities as at 28 February 2011”, available at: www.charities.govt.nz/Portals/0/docs/HOW_SNAP_APR_v3.pdf (accessed 20 July 2011).

Charities Commission (2011b), “Guide to the charities act”, available at: www.charities.govt.nz/Settingupcharity/RegistrationGuidelines/GuidetotheCharity (accessed 24 August 2011).

Charities Commission (2011c), “A snapshot of New Zealand’s charitable sector: a profile ofregistered charities as at 28 February 2011”, Charities Commission, Wellington.

Claessens, S., Djankor, S., Fan, J.P.H. and Lang, L.H.P. (2002), “Disentangling the incentive andentrenchment effects of large shareholders”, Journal of Finance, Vol. 57 No. 6, pp. 741-2771.

Cordery, C.J. and Baskerville-Morley, R.F. (2005), “Charity financial reporting regulation:a comparison of the United Kingdom and her former colony, New Zealand”, Working

128

IJMF9,2

Paper No. 20, Centre for Accounting, Governance and Taxation Research, School ofAccounting and Commercial law, Victoria University of Wellington, Wellington.

Crown Entities Reform Bill (2012), “Government Bill 332 – 1”, New Zealand Parliament, availableat: www.parliament.nz/en-NZ/legislation/Bills/5/a/b/00DBHOH_BILL11083 (accessed 10October 2011).

Cullen, M. and Dunne, P. (2006), “Tax incentives for giving to charities and other non-profitorganisations”, Inland Revenue Department, available at: www.taxpolicy.ird.govt.nz/publications/files/taxcharitiesdd.pdf (accessed 24 July 2011).

de Andres, P., Azofra, V. and Lopez, F. (2005), “Corporate boards in OECD countries: size,composition, functioning and effectiveness”, Corporate Governance, Vol. 13 No. 2,pp. 197-210.

de Andres-Alonso, P., Cruz, M.N. and Romero-Merino, M.E. (2006), “The governance of nonprofitorganizations: empirical evidence from nongovernmental development organizations inSpain”, Nonprofit and Voluntary Sector Quarterly, Vol. 35 No. 4, pp. 588-604.

Dyl, E.A., Frant, H.L. and Stephenson, C.A. (2000), “Governance and funds allocations in UnitedStates medical research charities”, Financial Accountability and Management, Vol. 16No. 4, pp. 335-52.

Eisenberg, T., Sundgren, S. and Wells, M.T. (1998), “Larger board size and decreasing firm valuein small firms”, Journal of Financial Economics, Vol. 48 No. 1, pp. 35-54.

Eldenburg, L., Hermalin, B.E., Weisbach, M.S. and Woskinska, M. (2004), “Governance,performance objectives and organizational form: evidence from hospitals”, Journal ofCorporate Finance, Vol. 10 No. 4, pp. 527-48.

Erhardt, N.L., Werbel, J.D. and Shrader, C.B. (2003), “Board of director diversity and firm financialperformance”, Corporate Governance, Vol. 11 No. 2, pp. 102-11.

Fisher, C. (2006), “Sector faces unique challenges”, Chartered Accountants Journal, Vol. 85 No. 5,pp. 27-9.

Fisman, R. and Hubbard, R.G. (2005), “Precautionary savings and the governance of nonprofitorganisations”, Journal of Public Economics, Vol. 89 Nos 11-12, pp. 2231-43.