Reinsurance Market Briefing Rendez - Vous de Septembre, Monte Carlo Greg Carter Managing Director, Analytics – EMEA & Asia Pacific Robert DeRose Senior Director, Global Reinsurance Ratings Nick Charteris - Black Managing Director, Market Development - EMEA 8 September 2019 Carlos Wong - Fupuy Senior Director

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Reinsurance Market Briefing

Rendez-Vous de Septembre, Monte Carlo

Greg CarterManaging Director,Analytics –EMEA & Asia Pacific

Robert DeRoseSenior Director,Global Reinsurance Ratings

Nick Charteris-BlackManaging Director,Market Development - EMEA

8 September 2019

Carlos Wong-FupuySenior Director

AM Best Delegates 2019

2

Preparing for Brexit

3

Preparing for Brexit... AM Best• AM Best Rating Services B.V. (AMB-EU) based in Amsterdam was registered with

ESMA on 3 December 2018

• Office is now fully staffed and operational

• EU27 clients migrated from London via a contractual novation process and analytical handover as required

• London will remain as the EMEA hub office, providing certain non analytical services to the Amsterdam office

• Common board and senior management working across both offices to ensure consistency and continuity

• AMBERS’ existing registration will convert to a new UK CRA registration with the UK FCA from Brexit date

• Both ESMA and the FCA have endorsement regimes in place even in a hard Brexit scenario to ensure mutual recognition of ratings for regulatory purposes

4

© AM Best Company, Inc. (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW ANDNONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED,REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANYMEANS WHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR WRITTEN CONSENT. All information contained herein is obtained by AMB from sources believed by it to beaccurate and reliable. AMB does not audit or otherwise independently verify the accuracy or reliability of information received or otherwise used and therefore all informationcontained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall AMB have any liability to any person or entity for (a) any loss or damage in wholeor in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of AMB or any of its directors,officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or(b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if AMB is advised in advance of thepossibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings, financial reporting analysis, projections, and other observations, ifany, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase,sell or hold any securities, insurance policies, contracts or any other financial obligations, nor does it address the suitability of any particular financial obligation for a specificpurpose or purchaser. Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. Credit ratings do not address any other risk,including but not limited to, liquidity risk, market value risk or price volatility of rated securities. AMB is not an investment advisor and does not offer consulting or advisory services,nor does the company or its rating analysts offer any form of structuring or financial advice. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS,COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN ORMADE BY AMB IN ANY FORM OR MANNER WHATSOEVER. Each credit rating or other opinion must be weighed solely as one factor in any investment or purchasing decisionmade by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security or other financialobligation and of each issuer and guarantor of, and each provider of credit support for, each security or other financial obligation that it may consider purchasing, holding or selling.

5

6

US Securities Laws explicitly prohibit the issuance or maintenance of a credit rating where a person involvedin the sales or marketing of a product or service of the CRA also participates in determining or monitoring thecredit rating, or developing or approving procedures or methodologies used for determining the credit rating.

No part of this presentation amounts to sales / marketing activity and AM Best’s Rating Divisionemployees are prohibited from participating in commercial discussions.

Any queries of a commercial nature should be directed to AM Best’s Market Development function.

Discussion Outline

7

Outlook

Capital

Developments

Performance

Global Reinsurance Market

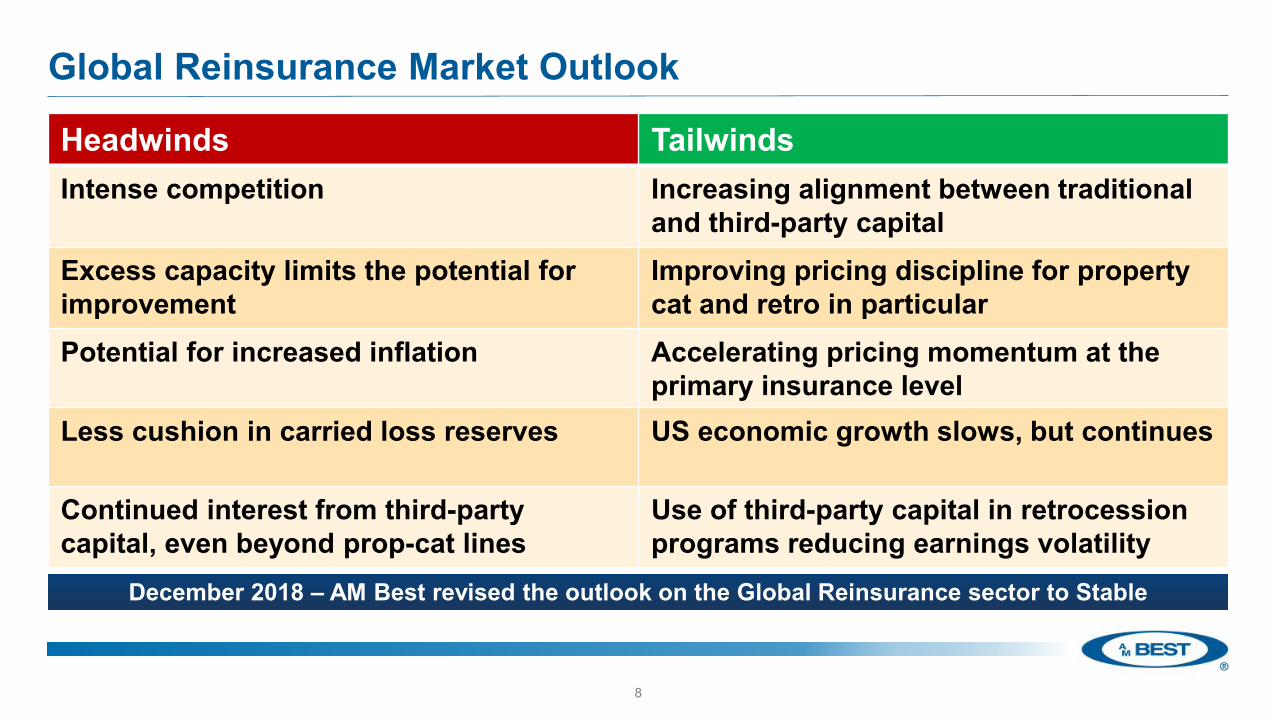

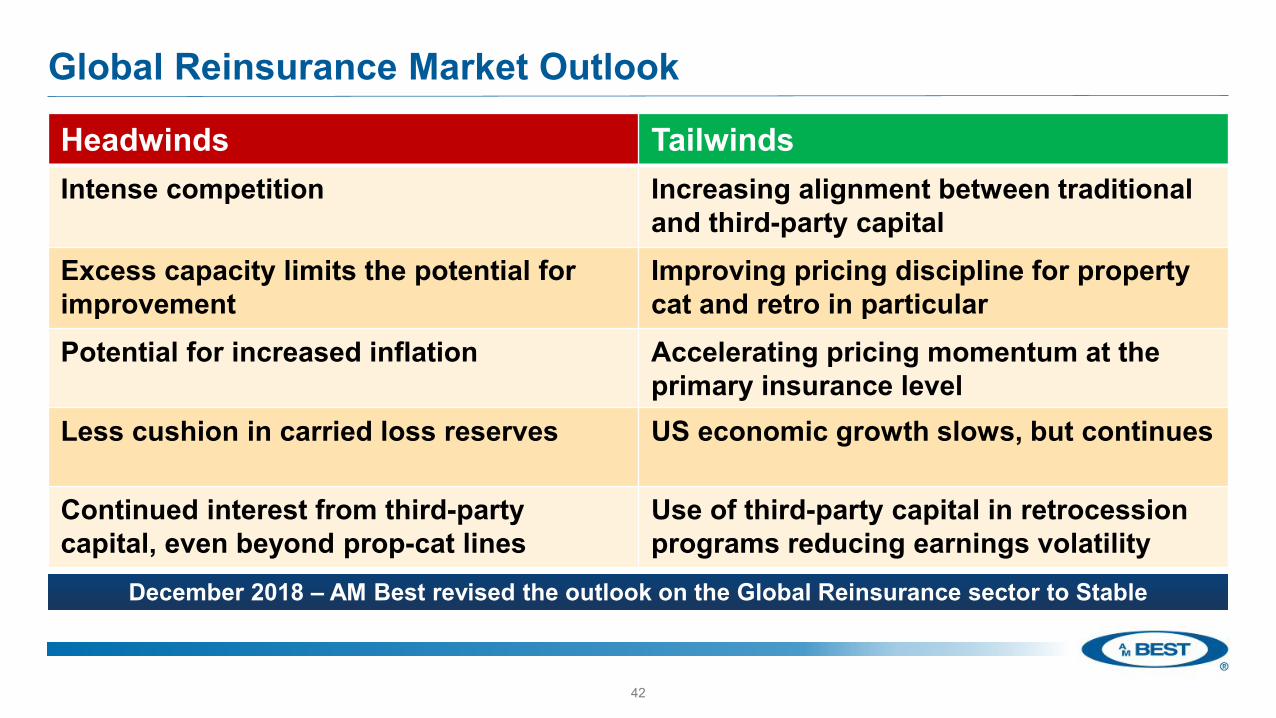

Global Reinsurance Market Outlook

8

Headwinds TailwindsIntense competition Increasing alignment between traditional

and third-party capitalExcess capacity limits the potential forimprovement

Improving pricing discipline for property cat and retro in particular

Potential for increased inflation Accelerating pricing momentum at the primary insurance level

Less cushion in carried loss reserves US economic growth slows, but continues

Continued interest from third-party capital, even beyond prop-cat lines

Use of third-party capital in retrocession programs reducing earnings volatility

December 2018 – AM Best revised the outlook on the Global Reinsurance sector to Stable

Global Reinsurance MarketPerformance

Global Reinsurance Market Performance

Source: AM Best data and research

Combined Ratio

10

89.7% 90.4% 95.2%

110.1%102.3% 97.6%

2014 2015 2016 2017 2018 Five Year Average

Global Reinsurance Market Performance

European “Big Four” U.S. & Bermuda Lloyd’s

Combined Ratios by Reinsurance Sector

11Source: AM Best data and research

92.4% 91.8% 96.3%108.9%

99.7%87.4% 88.9% 92.5%

109.2% 103.8%

88.1% 90.0%97.9%

114.0%104.6%

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Loss Ratio

Expense Ratio

11.6%

9.5%8.3%

-0.3% 1.0%

2014 2015 2016 2017 2018

Five Year Average 6.0%

Global Reinsurance Market Performance

Return on Equity

12Source: AM Best data and research

Global Reinsurance Market Performance

European “Big Four” U.S. & Bermuda Lloyd’s

Return on Equity by Reinsurance Sector

13Source: AM Best data and research

11.0% 11.5%9.7%

2.7%

5.8%

10.9%

7.5% 6.8%

-0.5% -1.5%

14.7%

8.9% 8.1%

-7.3%

-3.7%

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Five Year Average

6.0%

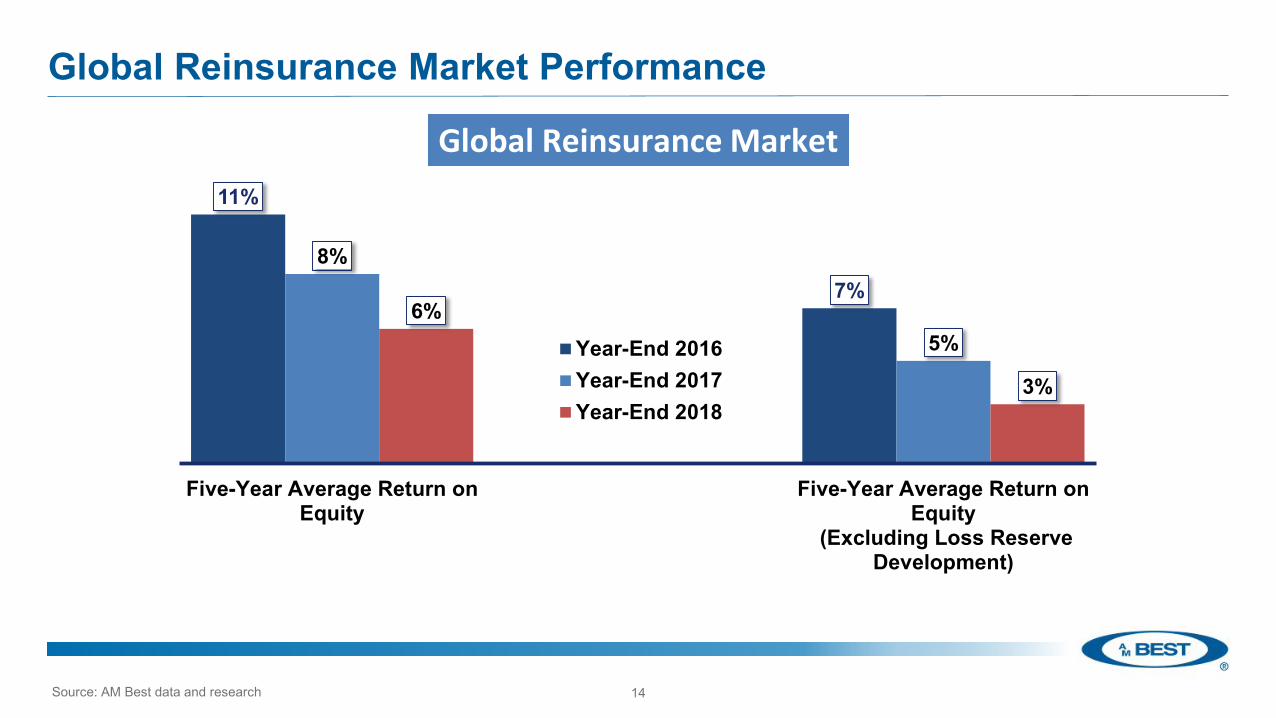

Global Reinsurance Market Performance

11%

7%8%

5%6%

3%

Five-Year Average Return onEquity

Five-Year Average Return onEquity

(Excluding Loss ReserveDevelopment)

Year-End 2016Year-End 2017Year-End 2018

Global Reinsurance Market

14Source: AM Best data and research

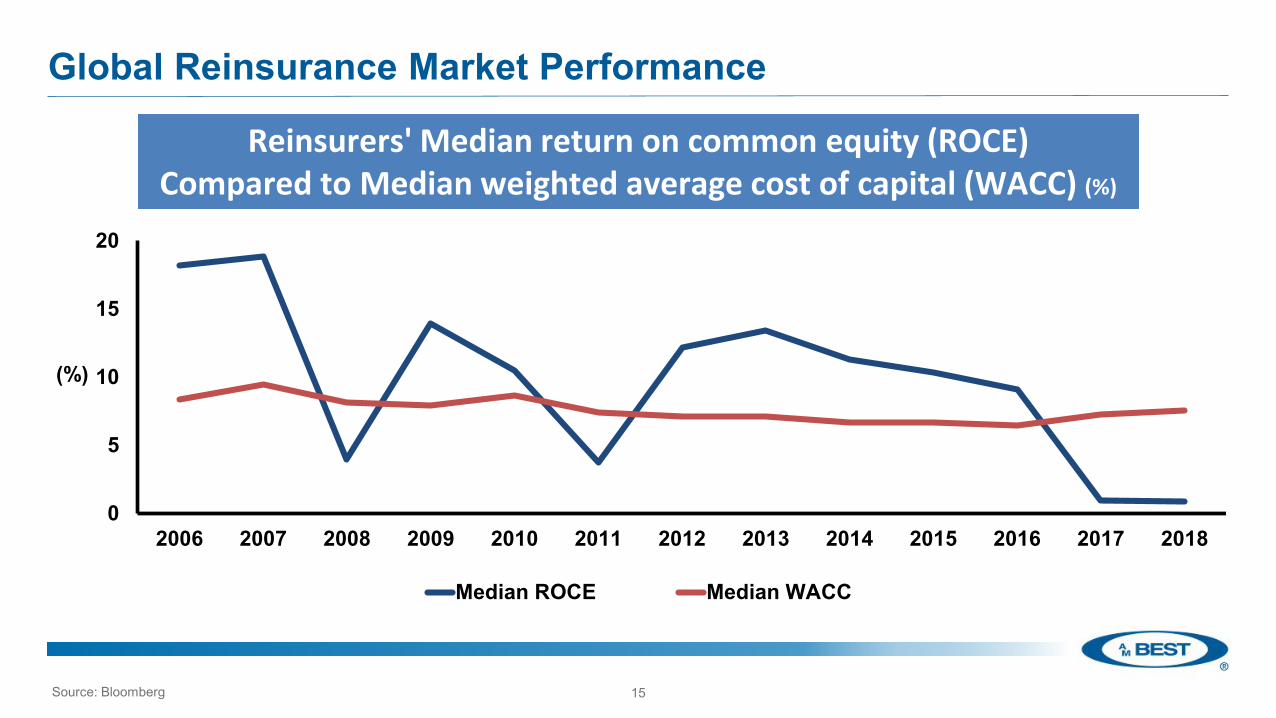

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

(%)

Median ROCE Median WACC

Global Reinsurance Market Performance

Reinsurers' Median return on common equity (ROCE)Compared to Median weighted average cost of capital (WACC) (%)

Source: Bloomberg 15

Global Reinsurance MarketCapital

Global Reinsurance Market Capital

17Notes and Sources: Estimates by Guy Carpenter and AM Best

Estimate - Total Dedicated Reinsurance Capital (USD billions)

292 320 340 332 345 345 341 346

19

48 60 68 75 87 95 92 311

368400 400 420 432 436 438

2012 2013 2014 2015 2016 2017 2018 2019E

Third-Party – Trapped Portion(High Estimate)

Third-Party – Trapped Portion(Low Estimate)

Third-Party

Traditional

Global Reinsurance Market Capital

18Notes and Sources: Estimates by Guy Carpenter and AM Best

2017 Reinsurance Market Briefing, Monte Carlo10 September 2017

Third-Party Capital (USD billions)

41 45 4962 56 53

1418 21

2034 345

55

55 6

6068

7587

95 92

2014 2015 2016 2017 2018 2019E

Direct InstitutionalInvestors

Reinsurance SponsoredManagers (includingsidecars)

Dedicated ILS Managers

Global Reinsurance - Top 15 ILS Funds (July 2019)

19Notes:Renaissance Re includes Top Layer, DaVinci, Langhorn, Vermeer and Medici.Source: Artemis

2017 Reinsurance Market Briefing, Monte Carlo10 September 2017

Assets Under Management

(AUM)(USD millions) Change in AUM Funds Location ILS Fund Managers Acquisitions

Nephila Capital 11,500 ▼ Bermuda Purchased by Markel 2018

RenaissanceRe Holdings Ltd. 8,200 ▲ Bermuda

Credit Suisse Insurance Linked Strategies Ltd. 8,000 ▼ Zurich, Switzerland

LGT ILS Partners Ltd. 7,100 ▼ Pfaeffikon, Switzerland

Markel CATCo Investment Management 6,800 ▼ Bermuda Purchased by Markel 2015

Fermat Capital Management, LLC 6,300 ▲ Westport, Connecticut, US

Stone Ridge Asset Management 5,930 ▼ New York

Securis Investment Partners LLP 5,900 ▼ London Northill bought out Swiss Re’s interest in 2012

Leadenhall Capital Partners LLP 5,500 ▲ London Purchased by Amlin 2014

AlphaCat Managers 4,200 ▲ Bermuda Purchased by AIG in 2018

Aeolus Capital Management Ltd 4,000 ● Hamilton, Bermuda Purchased by Elliott in 2016

Elementum Advisors, LLC 4,000 ● Chicago, IL White Mountain purchased 30% stake in 2019

Twelve Capital AG 4,000 ● Zurich, Switzerland

Schroder Investment Management 2,930 ▼ London

Amundi Pioneer 2,300 ▲ Boston, MA

Top 15 Fund Managers 86,660

What Would Turn the Market?

20Notes:Percentage of respondentsSource: Artemis

12.57%

16.17%

24.16%

13.17%

16.77%

5.99%

7.78%

3.39%

USD 150 billion+

USD 200 billion+

USD 250 billion+

Above USD 100 billion

Above USD 150 billion

USD 150 billion or greater

Nothing, the cycle is flat forever

Other

Capacity pressure could be a catalyst for a sustained uplift in prices

Event or Series of Events

Unmodelled Event

Liability Catastrophe Event

Global Reinsurance Market Capital

21

174 205 216 223 229

209 203

74% 71% 70% 73% 72% 72% 81%

2013 2014 2015 2016 2017 2018 2019E

Capital Depletion Needed to Reach 10% @ 99.6 Capital Utilisation

Capital Utilisation (USD billions)

Notes and Sources: Estimates by Guy Carpenter and AM Best

Global Reinsurance Market Capital

22

2017 Reinsurance Market Briefing, Monte Carlo10 September 2017

Top 10 World's Largest Reinsurance GroupsReinsurance

Premiums Written TotalLife & Non-Life (USD m) Non-Life Only (USD m) Shareholders’ Ratios (%)

Gross Net Gross Net Funds Loss Expense CombinedSwiss Re Ltd. 36,406 34,042 20,864 20,220 28,727 74.2 32.4 106.6

Munich Reinsurance Co. 35,814 34,515 23,395 22,570 30,336 65.2 34.2 99.4

Hannover Rück SE 21,952 19,791 13,709 12,368 10,923 66.9 29.5 96.4

SCOR S.E. 17,466 15,773 7,069 6,115 6,672 66.5 32.8 99.3

Berkshire Hathaway Inc. 15,376 15,376 9,930 9,930 352,500 88.6 21.9 110.4

Lloyd's 14,064 9,926 14,064 9,926 34,846 72.2 33.8 106.0

China Reinsurance (Group) Corp. 11,564 10,681 3,942 3,809 12,689 58.0 40.9 98.8

Reinsurance Group of America Inc. 11,341 10,544 – – 8,451 – – –

Great West Lifeco 7,737 7,647 – – 20,096 – – –

Korean Reinsurance Co. 6,803 4,786 5,972 4,058 2,014 83.7 17.8 101.5

Notes:Ranked by unaffiliated gross premium written in 2018.Source: AM Best data and research

Global Reinsurance Market Capital

23

Munich Reinsurance Co.

Swiss Re Ltd.

Lloyd's

Hannover Rück SE

Berkshire Hathaway Inc.

SCOR S.E.

Everest Re Group Ltd.

PartnerRe Ltd.

XL Bermuda Ltd.

Transatlantic Holdings, Inc.

Top 10 Global Reinsurance Groups Non-Life

Top 10 Global Reinsurance GroupsLife

Swiss Re Ltd.

Munich Reinsurance Co.

Reinsurance Group of America Inc.

SCOR S.E.

Hannover Rück SE

Great West Lifeco

Berkshire Hathaway Inc.

Pacific LifeCorp

Assicurazioni Generali SpA

PartnerRe Ltd.

Notes:Ranked by unaffiliated gross premium written in 2018.Source: AM Best data and research

Global Reinsurance Market Capital

24

Life and Non-Life Reinsurance GPW Distribution by Ranking

Rank 1-1067.9%

Rank 11-2017.2%

Rank 21-307.6%

Rank 31-404.8%

Rank 41-502.5%

Surviving Franchises of Today

• Arch• AXIS• Everest Re• Hannover Re• Lloyd’s• Munich Re• RenaissanceRe• SCOR• Swiss Re

ShelteredFranchises

• Allied World• Aspen• AXA-XL• Endurance(Sompo Intl)• General Re• MS Amlin• Odyssey Re• National Indemnity• Partner Re• TransRe• Validus

Franchises that are Gone

• Ariel Re• Flagstone• Harbor Point / Max (Alterra)• IPC Re• Maiden• Montpellier• New Castle Re• Paris Re• Platinum Re• Tokio Millennium Re

What does the Future Hold?

• Fidelis• Greenlight Re• Hamilton• Harrington Re• Third Point Re• Watford Re

Market Landscape ~10 Years In Time

25

Global Reinsurance Market Developments - Price/Book Value

40

60

80

100

120

140

160

180

200

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Pric

e/B

ook

Valu

e

Average

Current P/BV: 1.18x Average 1994-Present: 1.17x

Low Reached March 2009 (0.75x BV)

Peak reached February 2002 (1.83x BV)

1.0x P/BV

Announced Acquirer Acquiree Price (USD mm)

Tangible Price to BV

9-Jan-15 XL Group Catlin Group Limited 4,100 1.27x3-Aug-15 EXOR PartnerRe 6,900 1.19x5-Oct-16 Sompo Endurance 6,304 1.36x6-Jul-17 AXIS Novae 604 1.50x

26Notes:1996 to Present. Excludes accumulated other comprehensive income.Sources: AM Best data and research, Bloomberg, company reports and accounts

Announced Acquirer Acquiree Price (USD mm)

Tangible Price to BV

22-Jan-18 AIG Validus 5,560 1.53x4-Mar-18 AXA XL Group 15,300 1.96x

28-Aug-18 Apollo Aspen 2,600 1.08x31-Aug-18 Markel Nephila 975 –30-Oct-18 RenRe Tokio Millennium 1,469 1.02x

Global Reinsurance MarketDevelopments

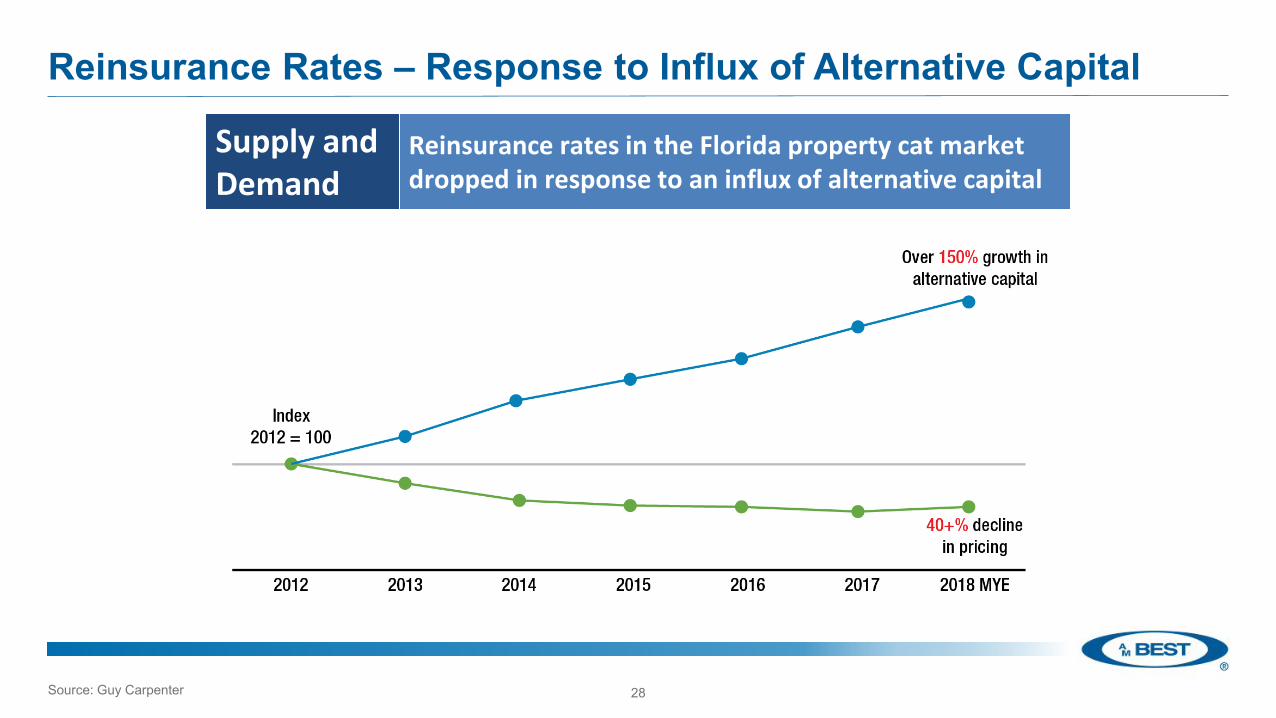

Reinsurance Rates – Response to Influx of Alternative Capital

28Source: Guy Carpenter

Supply and Demand

Reinsurance rates in the Florida property cat market dropped in response to an influx of alternative capital

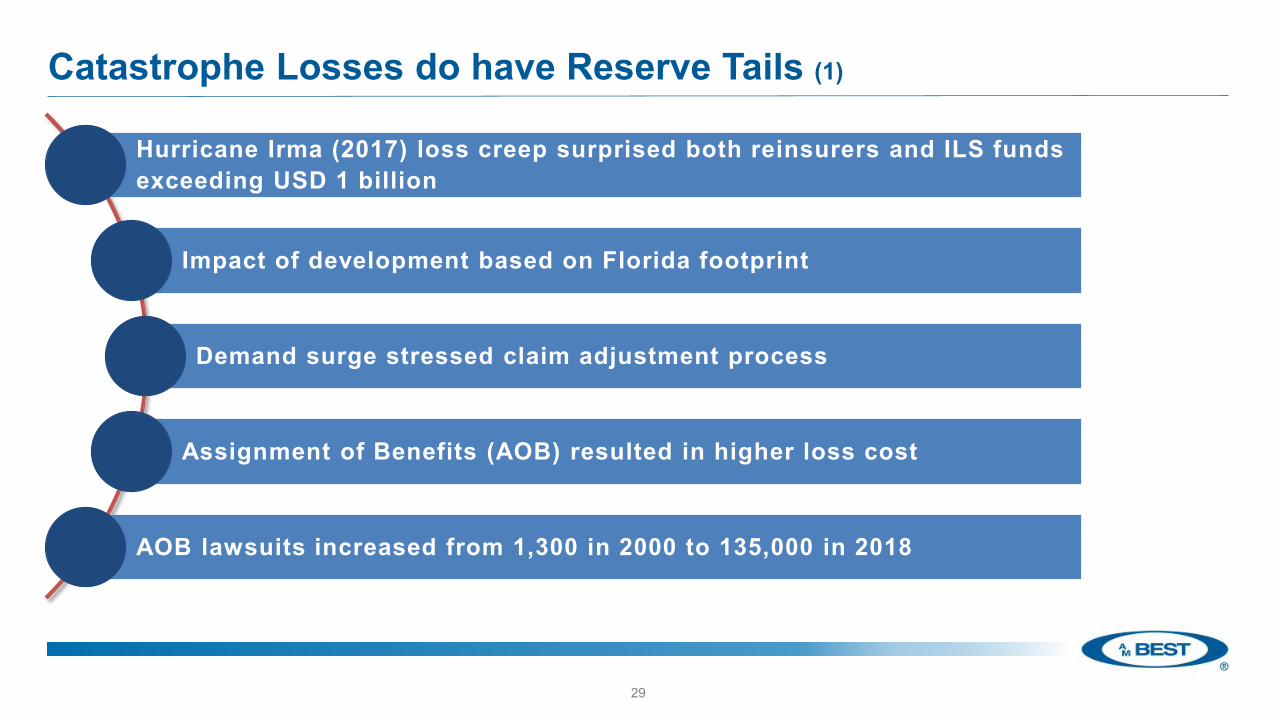

Catastrophe Losses do have Reserve Tails (1)

29

Hurricane Irma (2017) loss creep surprised both reinsurers and ILS funds exceeding USD 1 billion

Impact of development based on Florida footprint

Demand surge stressed claim adjustment process

Assignment of Benefits (AOB) resulted in higher loss cost

AOB lawsuits increased from 1,300 in 2000 to 135,000 in 2018

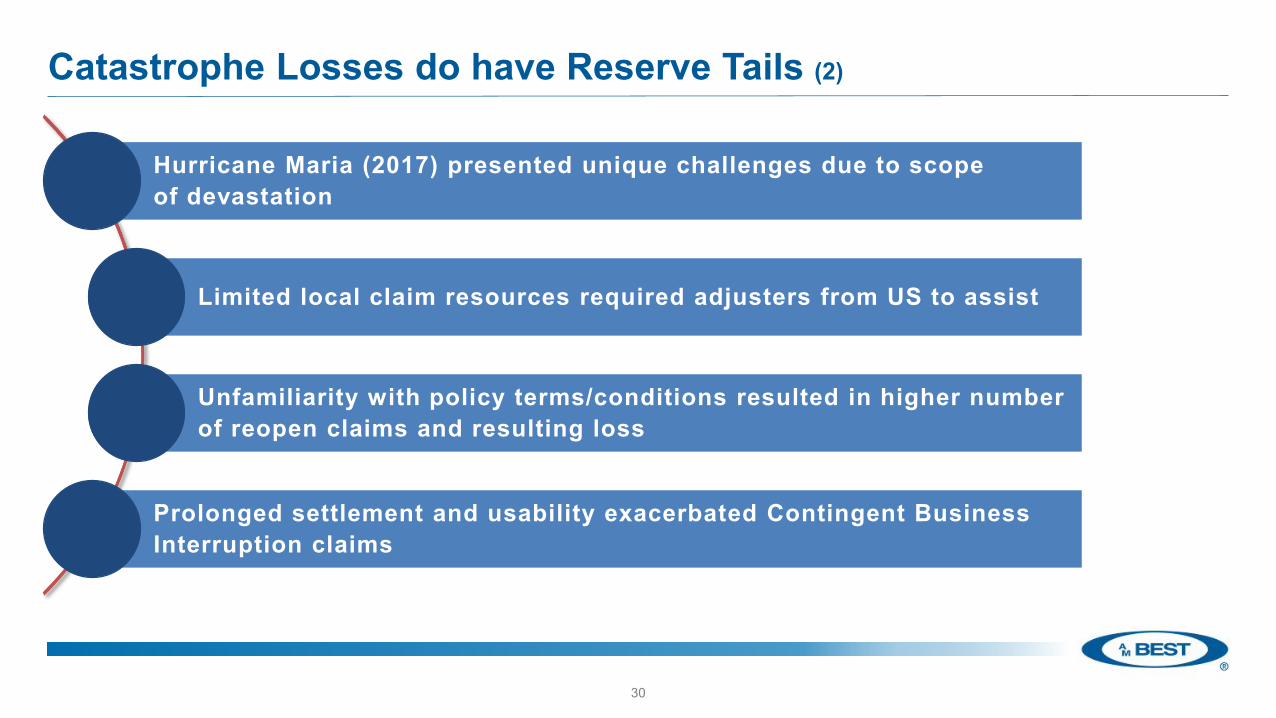

Catastrophe Losses do have Reserve Tails (2)

30

Hurricane Maria (2017) presented unique challenges due to scope of devastation

Limited local claim resources required adjusters from US to assist

Unfamiliarity with policy terms/conditions resulted in higher number of reopen claims and resulting loss

Prolonged settlement and usability exacerbated Contingent Business Interruption claims

Catastrophe Losses do have Reserve Tails (3)

31

Typhoon Jebi (2018) current loss estimates up to USD 16 billion vs original estimate of USD 2 - 3 billion. Some firm’s current loss pick of USD 8 - 10 billion

Japan fiscal year ends in March

Overlap with Typhoon Trami and a series of smaller losses, complicated claim and loss estimates

Preparation of Olympics stressed reconstruction resources driving up claims costs

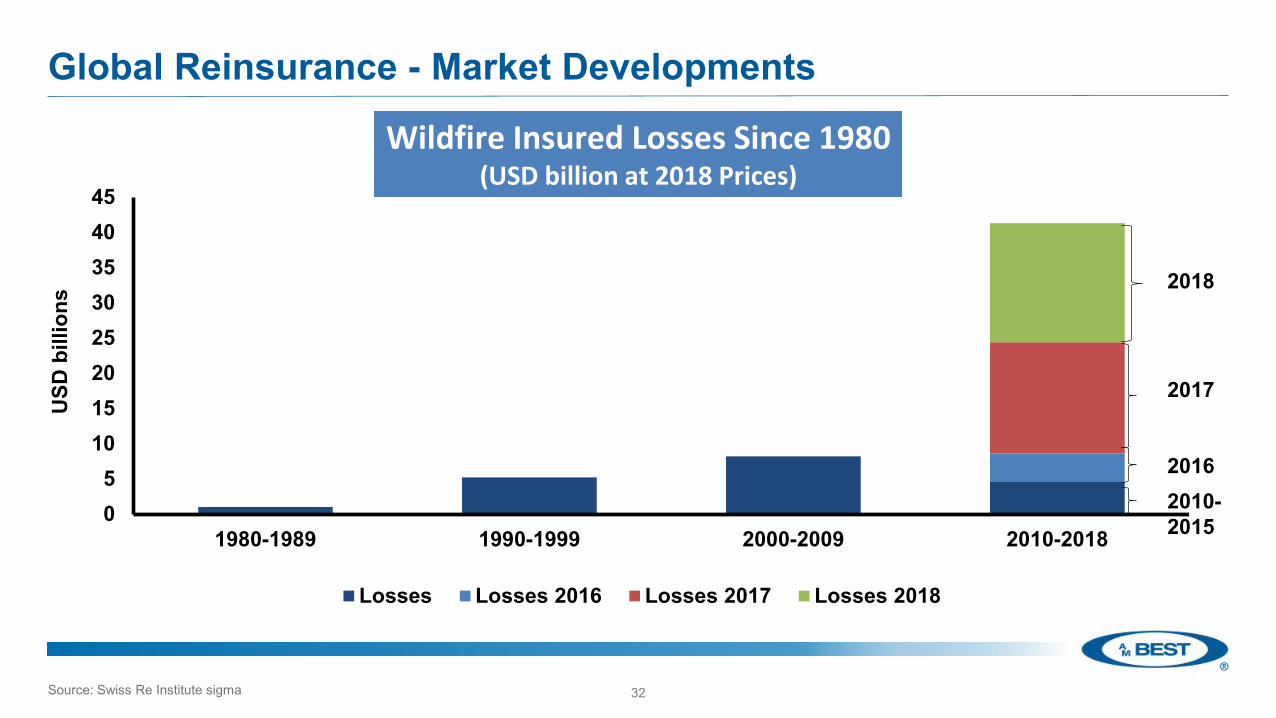

Global Reinsurance - Market Developments

32

2017 Reinsurance Market Briefing, Monte Carlo10 September 2017

05

1015202530354045

1980-1989 1990-1999 2000-2009 2010-2018

USD

bill

ions

Losses Losses 2016 Losses 2017 Losses 2018

Wildfire Insured Losses Since 1980(USD billion at 2018 Prices)

2018

2017

20162010-2015

Source: Swiss Re Institute sigma

Possible Turn in Trajectory

Capital elasticity has flattened the reinsurance market cycle

USD 219 billion in Cat losses over a

24 month period ending

December 2018

Capacity crunch in

retrocession markets

Earnings under

pressure Increased

demand for reinsurance

33

Continued Market Uncertainty

MARKET UNCERTAINTY

Upward rate

pressure

Trapped Collateral

Loss Uncertainty

Loss creep from hurricanes and wildfire uncertainty

New capacity being held on the sidelines

Aggregation of losses across ILS fund sector

34

What has transpired

Predominately European renewals

that were less affected by the 2017

and 2018 CATs

Rates did increase 30% for loss affected

programs(Lloyd’s and US)

Supply and Demand imbalance lead to

retro pricing increases of

15-20%

Casualty programs saw modest rate

improvement with ceding commissions

flat to down

Overall renewal pricing – flat to up

January and June renewal negotiationsran late

35

What to Expect?

Capital markets continue to be the key to sustained rate increases at the mid-year renewals

An abundance of capital waiting on the sideline

The evolving interest rate environment is a new variable within the pricing equation

36

Market Momentum - AIG

37

Recruiting proven talent to change culture from the top

Aggressive underwriting actions:• Pricing • Reducing both gross and net limits • Exit underperforming risks• Increasing utilisation of reinsurance to reduce

earnings volatility

Market Momentum – Lloyd’s

38

Address underperformance and

irrational underwriting behaviour

Implementation of risk-based oversight for

underwriting performance

Limited capacity for worst performing syndicates

Annual planreviews

Performance Management

Directive(PMD)

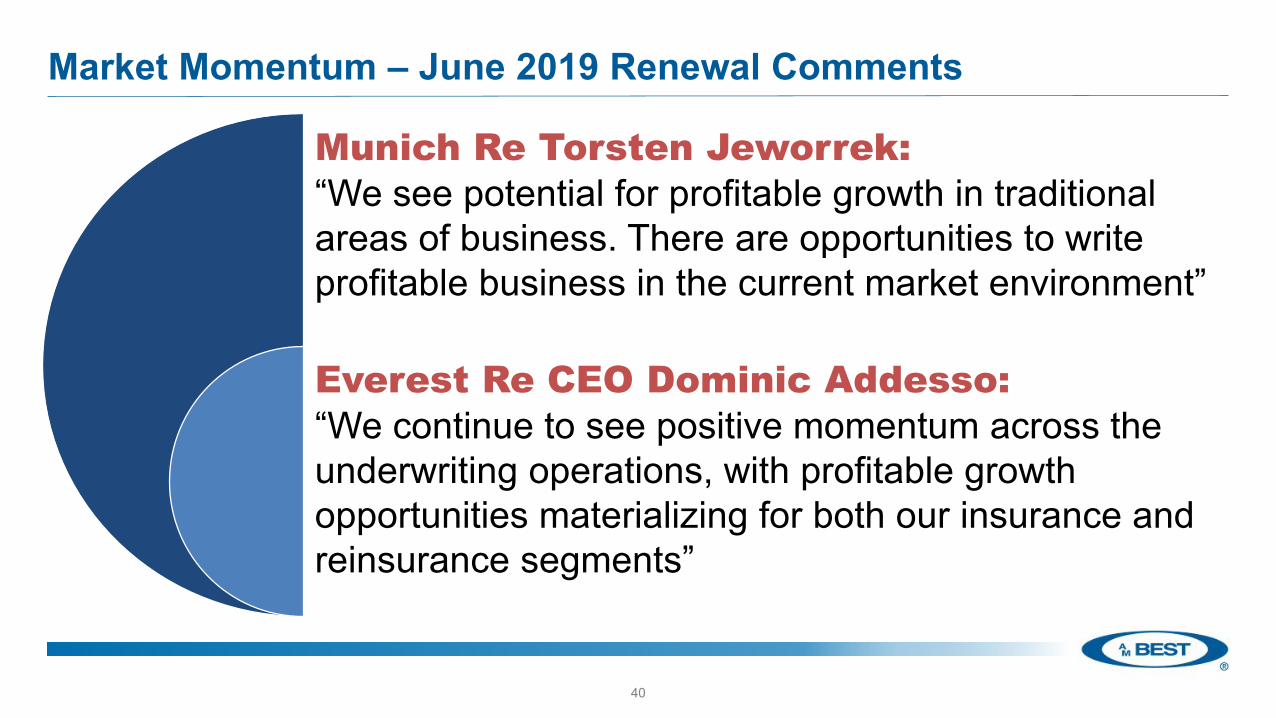

Market Momentum – June 2019 Renewal Comments

39

Travelers CEO Alan Schnitzer: “In business insurance, we achieved renewal premium change of 6.7%, including renewal rate change of 3.6% in both cases the highest levels in five years”

Chubb CEO Evan Greenberg: “Pricing continuing to tighten while spreading to more classes and business segments, particularly in the US and London wholesale market. Also seeing early signs of market firming spreading to more territories around the world”

Market Momentum – June 2019 Renewal Comments

40

Munich Re Torsten Jeworrek: “We see potential for profitable growth in traditional areas of business. There are opportunities to write profitable business in the current market environment”

Everest Re CEO Dominic Addesso: “We continue to see positive momentum across the underwriting operations, with profitable growth opportunities materializing for both our insurance and reinsurance segments”

Global Reinsurance - Market Trends

41

Potential Opportunities

Cyber Flood Mortgage Terrorism InsurTech

Global Reinsurance Market Outlook

42

Headwinds TailwindsIntense competition Increasing alignment between traditional

and third-party capitalExcess capacity limits the potential forimprovement

Improving pricing discipline for property cat and retro in particular

Potential for increased inflation Accelerating pricing momentum at the primary insurance level

Less cushion in carried loss reserves US economic growth slows, but continues

Continued interest from third-party capital, even beyond prop-cat lines

Use of third-party capital in retrocession programs reducing earnings volatility

December 2018 – AM Best revised the outlook on the Global Reinsurance sector to Stable

AM Best’s Forthcoming Events ‒ Register Now

43

Reinsurance Market Briefing - ZurichSept. 18, Zurich

Insurance Market Briefing - GulfOct. 2, Muscat

Insurance Market Briefing - MENAOct. 7, Dubai

Insurance Market Briefing - EuropeNov. 12, London

Insurance Market Briefing - CanadaSept. 13, Toronto

For further information, visit AM Best’s events webpage

Related Documents