Polarcus Limited, prospectus of 21 November 2014 Registration Document 1 of 37 Polarcus Limited Registration Document Oslo, 21 November 2014 Joint Lead Managers:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Polarcus Limited, prospectus of 21 November 2014 Registration Document

1 of 37

Polarcus Limited

Registration Document

Oslo, 21 November 2014

Joint Lead Managers:

Polarcus Limited, prospectus of 21 November 2014 Registration Document

2 of 37

Important information The Registration Document is based on sources such as annual reports and publicly available information and forward looking information based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for the Company's (including its subsidiaries and affiliates) lines of business. A prospective investor should consider carefully the factors set forth in chapter 1 Risk factors, and elsewhere in the Prospectus, and should consult his or her own expert advisers as to the suitability of an investment in the bonds. This Registration Document is subject to the general business terms of the Joint Lead Managers, available at their respective websites. The Joint Lead Managers and/or any of their affiliated companies and/or officers, directors and employees may be a market maker or hold a position in any instrument or related instrument discussed in this Registration Document, and may perform or seek to perform financial advisory or banking services related to such instruments. The Joint Lead Managers' corporate finance department may act as manager or co-manager for this Company in private and/or public placement and/or resale not publicly available or commonly known. Copies of this Registration Document are not being mailed or otherwise distributed or sent in or into or made available in the United States. Persons receiving this document (including custodians, nominees and trustees) must not distribute or send such documents or any related documents in or into the United States. Other than in compliance with applicable United States securities laws, no solicitations are being made or will be made, directly or indirectly, in the United States. Securities will not be registered under the United States Securities Act of 1933 and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements. The distribution of this Registration Document may be limited by law also in other jurisdictions, for example in Canada, Japan and in the United Kingdom. Verification and approval of this Registration Document by Finanstilsynet (the Norwegian FSA) implies that this Registration Document may be used in any EEA country. No other measures have been taken to obtain authorisation to distribute this Registration Document in any jurisdiction where such action is required. The Norwegian FSA has controlled and approved the Registration Document pursuant to the Norwegian Securities Trading Act, § 7-7. The Norwegian FSA has not controlled and approved the accuracy or completeness of the information given in the Registration Document. The control and approval performed by the Norwegian FSA relates solely to descriptions included by the Company according to a pre-defined list of content requirements. The Norwegian FSA has not undertaken any kind of control or approval of corporate matters described in or otherwise covered by the Registration Document. The Registration Document together with a Securities Note and any supplements to these documents constitutes the Prospectus. The content of the Prospectus does not constitute legal, financial or tax advice and potential investors should seek legal, financial and/or tax advice. Unless otherwise stated, the Prospectus is subject to Norwegian law. In the event of any dispute regarding the Prospectus, Norwegian law will apply.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

3 of 37

TABLE OF CONTENTS: 1 Risk factors .................................................................................................................... 4 2 Definitions ...................................................................................................................... 9 3 Persons responsible ....................................................................................................... 11 4 Statutory Auditors ......................................................................................................... 12 5 Information about the issuer ........................................................................................... 13 6 Business overview ......................................................................................................... 14 7 Organizational structure ................................................................................................. 23 8 Trend information .......................................................................................................... 27 9 Administrative, management and supervisory bodies .......................................................... 28 10 Major shareholders ...................................................................................................... 31 11 Financial information concerning the Company’s assets and liabilities, financial position and profits and losses ............................................................................................................. 32 12 Third party information and statement by experts and declarations of any interest ................ 34 13 Documents on display .................................................................................................. 34 Cross Reference List ......................................................................................................... 35 Joint Lead Managers’ disclaimer ......................................................................................... 36 Polarcus Limited Memorandum and Articles of Association ...................................................... 37

Polarcus Limited, prospectus of 21 November 2014 Registration Document

4 of 37

1 Risk factors Investing in bonds issued by Polarcus Limited involves inherent risks. Prospective investors should consider, among other things, the risk factors set out in the Prospectus, before making an investment decision. The risks and uncertainties described in the Prospectus are risks of which Polarcus Limited is aware and that Polarcus Limited considers to be material to its business. If any of these risks were to occur, Polarcus Limited’s business, financial position, operating results or cash flows could be materially adversely affected, and Polarcus Limited could be unable to pay interest, principal or other amounts on or in connection with the bonds. Prospective investors should also read the detailed information set out in this Registration Document and any accompanying Securities Note(s), and reach their own views prior to making any investment decision. An investment in the bonds is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of their investment.

1.1 Risk factors related to the industry in which Polarcus operates

1.1.1 Economic development trends The demand for the Company’s services will depend substantially on the level of activity and capital spending by oil and gas companies and specifically in relation to development and exploration expenditure. The activities of the oil and gas companies tend to follow the prices of oil and gas which have fluctuated widely over recent years. A decrease in oil and gas prices may have a negative impact on the expenditure on exploration activities which may affect demand for the services of the Company. Financial projections for and valuation of Polarcus’ assets are largely based on certain assumptions including those related to future conditions for the markets in which Polarcus will sell its services. Actual changes in market conditions may affect the accuracy of the assumptions and future prospects of Polarcus. Historically, the markets for oil and gas have been volatile and the current oil and gas prices worldwide have decreased to levels last seen in 2011.

1.1.2 Multi-jurisdictional operations Operations in international markets are subject to risks inherent in international business activities which might significantly affect the Company’s financial performance and competitiveness, including, but not limited to;

general economic conditions in each relevant country, changes in taxations and other fiscal regulations, unexpected changes in regulatory requirements, environmental protest activity, compliance with a variety of foreign laws and regulations, war, terrorist activities, piracy, political, civil or labour disturbances, embargos, border disputes, military

activity, restrictions in currency repatriation, and challenges in enforcing contractual rights

1.1.3 Government regulation and political risk Changes in the legislative and fiscal framework governing the activities of oil and gas business could have a material impact on exploration and development activities or affect Polarcus’ operations or financial results directly. Changes in political regimes might constitute a material risk factor for Polarcus‟ operations in foreign countries, including contract and bareboat chartering arrangements for the Polarcus‟ vessels. In a worst case scenario political authorities will in certain circumstances be in a position to seize the vessels when these are operating within or flagged under a particular jurisdiction. In certain countries there is an inherent risk of bribery, corruption and unethical work practices. The Company has developed clear policies and operating procedures to avoid these risks, and to the extent where reasonably possible, the Company will ensure that all external bodies that it is required to interact with, operate to the same high standards. Nevertheless, the Company’s operations could be impacted through the actions of these external bodies. The Company’s operations are subject to numerous international conventions as well as national, state and local law, and regulations in force in the jurisdictions in which the Company conducts, or will conduct, its business. These laws and regulations relate to, inter alia, the protection of the environment, natural resources, human health and safety, taxes, certification and visa regulations, licensing and permits for offshore blocks and other requirements. In particular, compliance with environmental regulations may require significant expenditures and breaches may result in fines and penalties, which could be material. Whereas the Company pays and has

Polarcus Limited, prospectus of 21 November 2014 Registration Document

5 of 37

paid particular attention to safety, conduct and the environment in its execution of business, stricter regulation or changes in the application of existing regulations may impose increased costs for operating the business of the Company, or otherwise impact the Company’s financial condition, operating results or future prospects. The Company also operates to strict international standards prohibiting unlawful commercial practices. The Company cannot predict the extent to which its future cash flow and earnings might be affected by mandatory compliance with any such new legislation or regulations.

1.1.4 Competition Polarcus operates in a highly competitive market. The Company may face competition from other seismic companies as well as other ship owners that introduce capacity into the market place. This, as well as overcapacity in the seismic market, could adversely affect the operating result of the Company. Polarcus’ revenue and operating results can vary significantly from quarter-to-quarter and year-to-year driven by competitor fleet size and global fleet distribution relative to market demand. Polarcus’ operating income is challenging to forecast due to changes in oil and gas company expenditures.

1.1.5 Commodity prices Any large fluctuations in oil price could materially impact the demand for seismic services.

1.2 Risk factors related to the Company

1.2.1 Service life and technical performance The service life of a modern seismic vessel is generally considered to be approximately thirty years, but could ultimately depend on its efficiency, vessel maintenance and demand for such vessels. There can be no guarantee that the vessels or equipment deployed by Polarcus will have a long service life. The vessels may have particular unforeseen technical problems or deficiencies, new environmental requirements might be enforced or new technical solutions or vessels might be introduced to the industry. The complex operations of the Company may lead to technical and operational difficulties that result in downtime for the vessel or inability of the vessel to complete a contract. Such risks may materially affect the operating result and reputation of the Company.

1.2.2 Fluctuating revenues from period to period The Company’s future revenues may fluctuate significantly from quarter to quarter and from year to year as a result of various factors including the following:

increases and decreases in industry-wide capacity to acquire seismic data; fluctuating oil and gas prices, which may impact customer demand for the Company’s services; different levels of activity planned by the customers; the timing of offshore lease sales and licensing rounds and the effect of such timing on the demand for

seismic data and geophysical services; the timing of award and commencement of significant contracts for geophysical data acquisition services; weather and other seasonal factors; seasonality and other variations in the licensing of geophysical data from the Company’s multi-client data

library; and reduced vessel utilization due to longer than scheduled yard stays, transit and delays in obtaining

necessary permits.

1.2.3 Access of personnel The Company’s development and business success are largely dependent upon senior management and other key personnel. Attracting and retaining qualified field and office based personnel is of significant importance for the operation of the Company’s business. The maritime and seismic industries are highly competitive for skilled personnel. There is no guarantee that the Company will be able to attract and retain the personnel required to continue its business and successfully execute the business strategy which might have negative effects on the Company’s operating results and financial performance.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

6 of 37

1.2.4 Insurance coverage Although the Company has taken out insurance coverage that the Company considers customary in the industry, such insurance arrangements will not carry full coverage of all its operating risks. Operation of the vessels represents a potential risk for loss of or damage to the vessels and equipment. In addition, the Group may not be able to maintain adequate insurance cover for its vessels and equipment in the future or do so at premiums that are considered reasonable. An accident involving any of the Group’s assets could result in loss of earnings, fines or penalties, higher insurance costs and damage to the reputation of the Company. The Group may not have sufficient insurance cover for the entire range of risks resulting in that particular losses may not be covered. Any significant loss or liability not insured could have a material adverse effect on its business, financial condition and results of operations. In addition, the loss of or continuing unavailability of one or several of the vessels could have an adverse effect on the Group even if effective insurance cover should be available.

1.2.5 Contractual and counter-party exposure The revenues of the Company are dependent on contract awards at competitive terms. Furthermore, the revenues of the Company will depend on the financial position of the customers and the willingness of these customers to honour their obligations towards Polarcus in a timely manner. There can be no guarantees that the financial position of the contract parties will be sufficient to adhere to the obligations under the contracts with the Company. The inability of one or more of the contractual parties to make payment under the contracts might have a significant adverse effect on the financial position of the Company. Polarcus is and will in the future be party to various contracts related to its business, most importantly seismic survey contracts and bareboat chartering arrangements. Consequently, the Company is and will be exposed to counter party risks. Any potential default by such counterparties or their inability or lack of willingness to fulfil their commitments may have a material adverse impact on the Company’s operating results and financial position. In a worst case scenario the counter party will under certain circumstances be in a position to seize the vessels for a period of time when these are operating within or flagged under a particular jurisdiction.

1.2.6 Multi-client investments The Company has made considerable investments in acquiring and processing seismic data that the Company owns (“multi-client data”). The multi-client data is being licensed to third parties for non-exclusive use in oil and gas exploration, development and production activities. However, the Company does not know with certainty how much of the multi-client data it will be able to license or at what price. There can be no assurance that the Company will be able to recover all costs and investments associated with acquiring and processing multi-client data. If there is a material adverse change in the general prospects for oil and gas exploration, development and production activities in areas where the Company acquires multi-client data, the value of such multi-client data could be impaired and the Company could be required to take a charge against its earnings. The value of multi-client data could also be impaired by technological or regulatory changes and by other industry or general economic developments. In general, the Company’s future sales of multi-client data licenses are uncertain and depend on a variety of factors, many of which will be beyond the Company’s control.

1.2.7 Operating risks The Company’s assets are concentrated in a single industry and the Group may be more vulnerable to particular economic, political, regulatory, environmental or other developments than a company with a more diversified portfolio of activities. It is not possible to give any guarantees that the vessels will be employed for the duration of their service life. There is an inherent exposure to technical risks, which may lead to operational problems, and increased operational costs and/or loss of earnings, additional investments, penalty payments, and other such costs which may have a material effect on the earnings and financial position of the Company. The seismic data acquisition operations are exposed to extreme weather and other hazardous conditions. In particular, a substantial portion of the Group’s operations are subject to perils that are customary for marine operations, including capsizing, grounding, collision, interruption and damage or loss from severe weather conditions, fire, explosions and environmental contamination from spillage. Any of these risks, whether in the marine or onshore operations, could result in damage to or destruction of vessels or equipment, personal injury and property damage, suspension of operations or environmental damage. In addition, the operations involve risks of a technical and operational nature due to the complex systems that are utilized. If any of these risks materialize, the Group’s business could be interrupted and the Group could incur significant liabilities. In addition, many similar risks may result in curtailment or cancellation of, or delays in exploration and production activities of the customers, which could in turn adversely impact the Group’s revenues.

1.2.8 Technology may become obsolete The Company’s technology could be rendered obsolete as new and enhanced products and services are introduced to the seismic market. The Group’ success depends to a significant extent on its ability to source develop and produce new and enhanced products and services on a cost effective and timely basis in accordance

Polarcus Limited, prospectus of 21 November 2014 Registration Document

7 of 37

with industry demands. While the Group commits resources to research and development, it may encounter resource constraints or technical or other difficulties that could delay introduction of new and enhanced products and services in the future. In addition, continuing development of new products and services inherently carries the risk of obsolescence of older products and services. New and enhanced products and services, if introduced, may not gain market acceptance or may be adversely affected by technological changes.

1.2.9 Commodity Prices Polarcus is exposed to the impact of market fluctuations in the price of certain key commodities and specifically, fuel and transportation costs. Any large fluctuations in these prices driven by the global economy, exacerbated further by exchange rate fluctuations, could materially impact future operating results.

1.2.10 Tax Operating internationally, Polarcus will be subject to taxation in several jurisdictions around the world. With increasingly complex and ever changing tax regulations and interpretation of these, the taxation on the Company could increase in certain jurisdictions. The Company may also in the future be subject to review of past years tax returns and be subjected to additional taxes and penalties. These conditions may have a material effect on the Company’s financial results. If Polarcus is controlled by Norwegian taxpayers, the Norwegian CFC-regulation (“NOKUS”- rules) may, on certain conditions, resulting in that the Company would be taxed under Norwegian law as if it had been a Norwegian company. Pursuant to the Company’s Articles of Association, the Company may refuse to accept shareholder positions leading to the CFC-regulations becoming applicable. Also, other amendments to applicable tax provisions may have negative impact on the return on the investment of Norwegian taxpayers.

1.3 Risk factors related to finance

1.3.1 Access to funding The Company may require additional capital in the future due to unforeseen liabilities or in order for it to take advantage of opportunities for acquisitions, joint ventures or other business opportunities that may be identified by the Company. Any negative development in sales, gross margins or sales processes, may lead to a strained liquidity position and the potential need for additional funding through equity financing, debt financing or other means. Any additional equity financing may be dilutive to existing shareholders. Should the current working capital and cash flow from operation not be sufficient to meet the Company’s financing needs, the Company may be forced to reduce or delay capital expenditures or research and development expenditures, or sell assets or businesses at unanticipated times and/or at unfavourable prices or other terms, or to seek additional equity capital or to restructure or refinance its debt. There can be no assurance that such measures would be successful or adequate to meet debt and other obligations as they fall due, or that such measures would not result in the Company being placed in a less competitive position.

1.3.2 Financial leverage and breach of covenants The financial leverage of the Company or any breach of covenants (or other circumstances which entail that loans fall due prior to the final maturity date) may have several adverse consequences, including the need to refinance, restructure or dispose of certain parts of the Company’s businesses in order to fulfill the Company’s financial obligations.

1.3.3 Defaults and insolvency of subsidiaries In the event of insolvency, liquidation or a similar event relating to one of the Company’s subsidiaries, all creditors of such subsidiary would be entitled to payment in full out of the assets of such subsidiary before the Company, as a shareholder, would be entitled to any payments. Defaults by, or the insolvency of, certain subsidiaries of the Company could result in the obligation of the Company to make payments under parent financial or performance guarantees in respect of such subsidiaries’ obligations under executed seismic survey contracts or the occurrence of cross defaults on certain borrowings of the Company or other Group companies. There can be no assurance that the Company and its assets would be protected from any actions by the creditors of any subsidiary of the Company, whether under bankruptcy law, by contract or otherwise.

1.3.4 Exchange rate fluctuations Currency exchange rates fluctuations and currency devaluation could have a material impact on the Company’s results of operations from time to time. Historically, most of the Company’s expenses have been denominated in USD, GBP, NOK, AED and EUR. The Company predominately sells its products and services in USD. A

Polarcus Limited, prospectus of 21 November 2014 Registration Document

8 of 37

depreciation of the USD will have an adverse effect on the Company’s financial performance as the Company will typically have higher revenues than expenses denominated in USD. The Company’s debt is predominately denominated in USD. Currency fluctuations relative to the NOK of an investor’s currency of reference may adversely affect the value of an investor’s investments.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

9 of 37

2 Definitions Annual Report 2012 The Company's annual report of 2012 Annual Report 2013 The Company's annual report of 2013 Company/Polarcus Limited/Issuer Polarcus Limited, a Cayman Islands tax exempted company with limited

liability Company Board or Company The board of directors of the Company Board of Directors EUR Euro GBP Pound Sterling Group The Company and its subsidiaries from time to time ICE-1A DNV GL class notation for ships operating in ice conditions of 0.5 – 1.0

meter level ice thickness ICE-1A* DNV GL class notation for ships operating in ice conditions above 1.0

meter level ice thickness IFRS International Financial Reporting Standards OHSAS 18001 An international occupational health and safety management system

specification ISIN International Securities Identification Number ISM Document of Compliance Document that verifies the Issuer’s compliance with the International

Safety Management (ISM) code for safe operation of ships and for pollution prevention

ISO 9001 A standard in the ISO 9000 family that sets out the requirements of a

quality management system ISO 14001 A standard in the ISO 14000 family that sets out the requirements of an

environmental management system ISPS standards A comprehensive set of measures to enhance the security of ships and

port facilities, developed in response to the perceived threats to ships and port facilities

NOK Norwegian kroner M&A Mergers and acquisitions Polarcus Limited The articles of association of the Company, as amended Articles of Association and currently in effect Share Listing Prospectus A prospectus written in conjunction with listing of 162,592,500 new

common shares on the Oslo Børs, dated 13 November 2014 Prospectus The Registration Document together with a Securities Note and any

supplements to these documents constitutes the Prospectus Registration Document This document dated 21 November 2014 Securities Note A document describing bonds to be offered and/or listed USD United States Dollars VPS or VPS System The Norwegian Central Securities Depository, Verdipapirsentralen

Polarcus Limited, prospectus of 21 November 2014 Registration Document

10 of 37

Polarcus Limited, prospectus of 21 November 2014 Registration Document

11 of 37

3 Persons responsible

3.1 Persons responsible for the information Persons responsible for the information given in this Registration Document are as follows: Polarcus Limited, c/o Intertrust Corporate Services (Cayman) Limited, 190 Elgin Avenue, George Town, Grand Cayman KYI - 9005, Cayman Islands.

3.2 Declaration by persons responsible Responsibility statement: Polarcus Limited confirms that, taken all reasonable care to ensure that such is the case, the information contained in this Registration Document is, to the best of our knowledge, in accordance with the facts and contains no omission likely to affect its import.

Dubai, United Arab Emirates, 21 November 2014

Rolf Rønningen Chief Executive Officer

Tom Henrik Sundby Chief Financial Officer

Eirin Inderberg General Counsel

Polarcus Limited, prospectus of 21 November 2014 Registration Document

12 of 37

4 Statutory Auditors

4.1 Names and addresses The Company’s auditor for 2012 and 2013 has been Ernst & Young AS, independent public accountants, located at Dronning Eufemias gate 6, NO-0191 Oslo, Norway. State Authorised Public Accountant Anders Gøbel has been responsible for the Auditor's report for 2012 and 2013. Ernst & Young AS is member of The Norwegian Institute of Public Accountants.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

13 of 37

5 Information about the issuer

5.1 History and development of the issuer

5.1.1 Legal and commercial name The legal name of the issuer is Polarcus Limited, the commercial name is Polarcus.

5.1.2 Place of registration and registration number The Company is registered with the Cayman Islands Registrar of Companies with registration number 201867.

5.1.3 Date of incorporation Polarcus Limited was incorporated on 17 December 2007.

5.1.4 Domicile and legal form The Company is Cayman Islands tax exempted company with limited liability validly incorporated in its jurisdiction. The Company is regulated by the Companies Law (2007 revision) of the Cayman Islands, as amended from time to time. See also section 7.1 (“Description of Group that Company is part of”). The Company's registered address is c/o Intertrust Corporate Services (Cayman) Limited, 190 Elgin Avenue, George Town, Grand Cayman KYI - 9005, Cayman Islands. The Company’s business address is c/o Polarcus DMCC, Almas Tower, level 32, Jumeirah Lakes Towers, Dubai, United Arab Emirates. The Company's telephone number is +971 4 43 60 800.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

14 of 37

6 Business overview

6.1 Business activities Polarcus is one of the five global providers of marine three dimensional (3D) towed streamer services. The seismic data acquired by the Company’s vessels is used by oil and gas companies to evaluate hydrocarbon plays and prospects ahead of drilling, and to determine size and structure of known reservoirs in order to maximize field recovery and production rates. Polarcus has two principal business activities currently; contract seismic services and multi-client projects.

6.1.1 Contract seismic services The Company’s range of contract seismic services include 3D, high-density 3D, 4D, multi-azimuth and wide azimuth data acquisition. The typical clients are independents, international and national oil and gas companies with a marine exposure. Contracts for seismic surveys are entered into directly with the client and priced and negotiated on a project by project or spot market basis, in light of the conditions and requirements of each individual project. A seismic survey may last anywhere from one to six months, with potential for seasonal and multi-year contract terms in some cases, especially with the national oil companies. Leads for seismic survey projects are typically identified three to twelve months before the projects are due to commence. An invitation to tender is issued by the relevant oil or gas company directly to the various potential service providers, normally around two to six months before the expected commencement of a project. There will rarely be direct awards of contracts. A project is typically awarded one to four months prior to its commencement and each project can run anywhere from one month duration to six months. The Company participates in seismic tenders globally, with activity hotspots being driven by license round activity, operational seasons (weather), new discoveries, and other market conditions supportive to investment by oil and gas companies in exploration activity. The Company has established four regional offices worldwide to gather market intelligence, drive marketing campaigns, and coordinate sales activity. These regional offices are located in Houston, London, Moscow, and Singapore. All these areas have consistent high activity with the exception of Russia where the market is seasonal, making it possible to build viable backlog within each region thereby minimizing inter-regional transits. The Company places a high focus on the Arctic in its marketing strategy, in line with the Company’s Arctic Frontiers Strategy and in order to generate value from the vessels significant differentiation that specifically benefits such operations. This includes the high ice class notations (ICE-1A and ICE-1A*), double hull construction, specialist de-icing equipment, ice radars, as well as the ballast water treatment systems. The Company’s first major Arctic project was offshore western Greenland in 2012 where the Company had three seismic vessels operating for two major oil companies, one a SuperMajor. The project endorsed the value of the investments made by Polarcus into Arctic differentiation and the comprehensive set of Arctic-specific operational procedures developed to support such activities. These procedures have been accredited by DNV-GL, the world's leading ship and maritime classification society. Polarcus continues to receive significant interest from major oil companies active in the Arctic and has demonstrated additional value benefits of the high ice class after successfully transiting the Northern Sea Route between Norway and the Pacific Ocean during summer 2013, a passage only available to vessels with ICE-1A or higher. The Company has subsequently undertaken successful contract and multi-client seismic operations in the Barents Sea, both offshore northern Norway and most recently in summer 2014, in the Russian Barents Sea. The Company continues to pursue similar projects to leverage its differentiation and most recently announced on 05 September 2014 a new contract award for 3D marine seismic acquisition services in summer 2015 for a major international energy company offshore Sakhalin, requiring two Polarcus vessels for a combined period of 8 months. The Company has established operational experience in several key markets globally including NW Europe (UK, Norway, Ireland), West Africa, East Africa, Australia and New Zealand, Uruguay, and the Falkland Islands. The Company is or is close to penetrating other important regional markets such as the Gulf of Mexico and Brazil. Polarcus announced on 22 September 2014 an award that will see the Company making its first entry into the US Gulf of Mexico in October 2014 having secured a contract award for a 6 month vessel charter. The Company is in the process of implementing an in-house processing capability through its recently established agreement with DUG under which Polarcus leases hardware and software for the seismic data quality control on-board its vessels and which also enables Polarcus to offer an high-end quality fast-track processing solution on-board the vessel. Polarcus will in connection with this new arrangement hire its own field personnel for these quality control and fast-track processing services. The arrangement will be implemented early 2015 and will replace the current arrangement with GX Technology Corporation. Under this new agreement DUG will furthermore provide onshore advanced seismic data processing services at one of DUG’s Data Processing Centres as and when such services are part of the scope of surveys awarded to or required by the Company.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

15 of 37

6.1.2 Multi-client projects Multi-client projects are surveys undertaken by seismic companies where the project deliverables comprise a suite of fully imaged seismic data that are subsequently licensed to oil and gas companies on a non-exclusive basis. The seismic company develops the seismic opportunity in much the same way as an exploration company and then seeks industry underwriting from oil and gas companies to reduce the upfront project risks. Subsequent multiple sales of data licenses over a long term period, typically up to 10 years, are expected to deliver returns in excess of contract seismic service rates. Such license sales arise both from first time sales to new clients, and from uplift fees contractually committed from existing licensees on trigger events such as formation of bidding groups for purposes of bidding for acreage, acreage awards, JOA’s (“Joint Operating Agreement), farm-ins, commencement of drilling operations, and M&A activity where an acquiring entity does not already possess a valid data license. Ownership of, or exclusive marketing rights to, the multi-client project deliverables remains with the seismic company and project risks are offset through meticulous business case planning supported by written pre-funding commitments from participating oil and gas companies in advance of vessel mobilization. Under this model oil and gas companies benefit from access to high quality data at less than the cost of acquiring the same data on contract seismic service rates, but forfeit their exclusivity of access to the data. In the majority of cases such data is typically acquired over open acreage, or acreage due for full or partial relinquishment, in anticipation of future licensing by relevant authorities. The project deliverables are used by oil and gas companies for risk evaluation and prospect identification prior to their making a bid for acreage or prior to making a field development plan. Seismic companies have the potential for multiple sales that in total exceed the revenue that would have been derived from a fixed price seismic services contract. During soft market conditions oil and gas companies seeking supply chain cost reductions sometimes reassign budgets in favour of such multi-client projects, providing the seismic companies the opportunity to secure revenues, which in aggregate, exceed prevailing market rates for standard contract seismic services. Multi-client projects constitute a viable and profitable business line when approached from a business rather than resource driven perspective. The Company applies a professional project management approach to the planning and delivery of multi-client projects, with each project being supported by a sound business case for success and with quality control of the deliverables in accordance with industry accepted practices. In July 2013, the Company entered into a three-year multi-client strategic operating alliance agreement with ION Geophysical Corporation under which the parties will together identify, develop and carry out 3D multi-client projects. Polarcus has furthermore entered into several service agreement under which various consultants assist Polarcus in identifying multi-client projects in the different regions. As of 30 September 2014 the company has a multi-client library with a book value of USD 116.8 million. The Company’s data library comprises multi-client surveys offshore Norway, UK, Ireland, North West Africa and Nigeria.

6.1.3 Vessel backlog The Company is dependent on obtaining contracts for seismic services and that the multi-client data is being licensed to third-parties. See also chaper 1 Risk factors. As per mid-October 2014, the Company had a USD 330 million backlog inclusive of bareboat charter of Vyacheslav Tikhonov to SCF.

6.1.4 Certifications Polarcus holds the ISM Document of Compliance and is certified to the ISPS standards. In addition its office and vessels have achieved DNV certification to ISO 9001, ISO 14001 and OHSAS 18001. No other geophysical company in the industry has undertaken such a project to have their Management System fully certified to the internationally recognized standards of ISM, ISPS, ISO and OSHAS. Uniquely in the seismic industry to date, the Company has secured the full suite of certification for the entire Polarcus Group, including both maritime and seismic across the full Polarcus fleet of vessels.

Figure 1: Polarcus Multi-Client Project Map

Polarcus Limited, prospectus of 21 November 2014 Registration Document

16 of 37

6.2 Data acquisition methods Modern marine seismic data is collected by emitting acoustic energy below the water’s surface from energy sources towed behind a survey vessel (see Figure 2). The energy source is typically formed by using high pressure air that is emitted through an array of source elements, typically called airguns. At rock layer boundaries beneath the seabed some of this acoustic energy is reflected back up to the seismic streamers, also towed behind the survey vessel. These streamers can be up to 12,000m long and have hydrophones within then that detect and convert this reflected energy into digital data, which in turn are recorded on-board the survey vessel. These data are processed both on-board and onshore and subsequently interpreted to provide an image of the earth beneath the survey vessel’s traverse. Geoscientists then analyse these images to identify potential hydrocarbon reservoirs. Figure 2: Collecting marine seismic data Several seismic techniques are in use today to provide such information to the geoscientists. At the highest level these can be categorized into 2-, 3- and 4-dimensional seismic surveys. The 2-dimensional (2D) seismic surveys represent the most cost efficient method, being conducted by a survey vessel towing a single streamer and one energy source. Such surveys will generate data which comprise individual cross-sections of the earth along the lines tracked by the vessel which can be kilometres apart, and is often used for large basin-wide analyses of frontier geologic regions. However, these 2D surveys cannot accurately define prospective hydrocarbon traps or the structural geometry of prospective oilfields. A more sophisticated method, termed 3D seismic, is to tow multiple streamers behind the survey vessel to produce in effect several parallel 2D cross-sections of data in each single traverse of the vessel (see Figure 3). When the area is covered with a number of traverses of this type, the data is processed to produce a 3-dimensional (3D) cube of the subsurface. Further improvements in data quality can be achieved by reducing the lateral spacing between the streamers, termed High Density 3D (or “HD3D”); by shooting the area from different directions to provide illumination of the target zone from a number of different perspectives, termed Multi-azimuth (or “MAZ”); or by laterally offsetting the source from the line of traverse to improve target illumination at depth and beneath sub-surface structures such as salt or basalt, termed Wide-azimuth (or “WAZ”). Naturally, these advanced techniques are more complex and more costly as they require additional streamer capacity and in the case of Wide-azimuth, additional vessels to tow the energy sources parallel to the primary survey vessel. Compared to classic 3D seismic, High Density 3D seismic can quadruple the streamer requirements, Wide-azimuth surveys are often shot with 2 vessels carrying streamers and sources as well as two additional vessels carrying sources only. In the case of Multi-azimuth, the same area can be shot up to six times from different directions. However, the benefits in terms of improved image quality and therefore better understanding of the reservoir are increasingly recognized to outweigh the higher costs. At the other end of the spectrum a market has also developed for a cost effective 3D exploration technique that is proving of high interest to oil and gas companies seeking to explore large frontier license blocks, often in deep water. Such acreage typically requires the licensee to undertake an initial exploration study prior to a more thorough appraisal or partial relinquishment, or to support an equity participation plan (farm-in/farm-out agreement). This technique requires expanding the lateral separation between streamers, commonly known as wide tow 3D acquisition, in order to provide much greater areal coverage without causing a significant loss of resolution in the imaging. New developments in drag reduction and in-sea deflector technology have allowed the Company to compete successfully in this growing market segment, with the Company’s vessels capable of towing ultra-wide spreads of 8 to 10 streamers with separations of up to 200m between parallel streamers.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

17 of 37

Figure 2: Plan views of four major types of 3D seismic acquisition that Polarcus is expected to employ

In 4-dimensional (4D) seismic programs, the 4th dimension is simply elapsed time, meaning that the same 3D survey may be reacquired in long period intervals of 1 year or sometimes greater. This method is used to observe the physical changes occurring in a reservoir as a result of hydrocarbon production, or injection of water or gas into the reservoir, by analysing the differences between models acquired over a number of years. Time-lapse or 4D seismic therefore involves comparing the results of 3D seismic surveys repeated at considerable time intervals (e.g. before a field starts producing versus various post-production stages) over the same geographic area. The picture below shows an example of a seismic 3D operation where the total lateral spread can exceed 1,350 meters, and the length of the seismic streamers typically are between 6 and 8 kilometres but can be as much as 12,000 meters.

Figure 3: An aerial schematic view of a 3D operation demonstrating size of the ‘spread’

Polarcus Limited, prospectus of 21 November 2014 Registration Document

18 of 37

6.3 The Polarcus fleet

6.3.1 Introduction The Polarcus fleet currently comprises seven ultra-modern seismic research vessels built to the ULSTEIN SX124, SX133 and SX134 designs. The vessels are ultra-modern and innovative seismic research vessels that have been designed for the most challenging offshore projects and operating conditions and carries class notations from the classification society, Det Norske Veritas (DNV) of Norway. The vessels combine the latest developments in maritime technology with the most advanced seismic systems commercially available. The first five Polarcus vessels, have been built in Dubai, UAE, by DWD and vessels six and seven have been built in Norway by Ulstein Verft AS. All vessels are high-end 3D seismic vessels where four of the vessels have the capability of towing up to 12 streamers and capable of a transit speed at 14 to 15 knots, two vessels have the capability of towing up to 14 sreamers and a transit speed of 15 knots, and one vessel is unique wide-tow 8 streamer 3D seismic vessel that is able to tow configurations comprising 200 metres lateral separation between streamers. The latter vessel is also capable of a transit speed of up to 18 knots making it especially suited for fast and safe transits to/from survey areas in the Arctic thereby maximizing time on prospect.

6.3.2 Design features All the vessels feature the latest innovative inverted bow design, the ULSTEIN X-BOW® hull. This has several benefits over traditional hull designs such as:

Improved transit performance in marginal or bad weather, giving the Company the option of either higher transit speeds or reduced fuel consumption according to operational requirements

Lower pitch and heave acceleration

No bow slamming

Reduced noise and vibration levels

Less spray, especially important in Arctic operations Other important features are increased systems redundancy, crew comfort, environmental impact mitigation and superior performance. The ULSTEIN SX133 and SX134 vessels also hold a DNV ICE-1A class notation (the two latest vessels an ICE-1A* class notation) that will enable safe access and an extended operations season in the Arctic Ocean, a region currently attracting significant industry attention. The new super-high ice class notation, ICE-1A*, verifies that the vessels have sufficient strength, engine power and equipment to transit through areas with ice floes of 1.0 m level ice thickness, potentially enabling the vessels to extend the otherwise short Arctic operating season. Compared to the other vessels in the market, the Company considers its own vessels to be environmentally sound. The Polarcus vessels are designed with i.a. exhaust catalysts for all main engine exhaust lines in order to reduce the emissions of NOx, HC, soot and sound. The environmental focused designs supersede any international requirements currently in force and are in accordance to DNV’s latest rules for CLEAN-DESIGN class. There are for instance no fuel tanks adjacent to the vessels external hull, which mitigates potential exposure of fuel to the environment, and the adopted bilge water cleaning system will reduce contaminants to less than 5 ppm in contrast to typical maritime shipping levels of 15 ppm or greater. All maritime and seismic equipment has been sourced from best-in-class suppliers including LMF, Rolls Royce (Odim), Wärtsilä, ABB, Schottel, Berg, Scana Volda, Furuno, Kongsberg, Sercel, ION, and Seamap. Polarcus believes that the expansion of the industry into new frontiers and environmentally sensitive regions of the world will require a much greater level of environmental compliance as new and projected legislation on emissions to air and water come into effect. Taxes on NOx emissions for instance have already been introduced in Norway and are expected to be implemented in other parts of the world in due course. The Company has seen that the environmental attributes of the vessels have become a significant service differentiator for Polarcus. In order to secure this differentiator, the Company is placing a strong emphasis on “green” investments, both for its seismic systems and its maritime technologies. The Company has an emission accreditation certificate from DNV that verifies that its fleet has on average only 1/5 of the environmental footprint of its peers.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

19 of 37

POLARCUS NADIA POLARCUS NAILA

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D Vessel ULSTEIN SX124 88.8m 19.0m 12 14.0 knots ICE-C 2009

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D Vessel ULSTEIN SX124 88.8m 19.0m 12 14.0 knots ICE-C 2010

POLARCUS ASIMA POLARCUS ALIMA

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D vessel ULSTEIN SX134 92.0m 21.0m 12 15.0 knots ICE-1A 2010

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D vessel ULSTEIN SX134 92.0m 21.0m 12 15.0 knots ICE-1A 2011

Polarcus Limited, prospectus of 21 November 2014 Registration Document

20 of 37

POLARCUS AMANI POLARCUS ADIRA

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D vessel ULSTEIN SX134 92.0m 21.0m 14 15.0 knots ICE-1A* 2012

Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D vessel ULSTEIN SX134 92.0m 21.0m 14 15.0 knots ICE-1A* 2012

VYACHESLAV TIKHONOV Type: Design: Length: (loa) Beam: Streamer capacity: Speed Ice class: Year delivered:

3D vessel ULSTEIN SX133 84.2m 17.0m 8 18.0 knots ICE-1A 2011

Polarcus Limited, prospectus of 21 November 2014 Registration Document

21 of 37

6.4 Market overview

6.4.1 Demand drivers The market for geophysical seismic surveys is mainly driven by the oil industry’s incentives to invest in exploration, development and production. The willingness to invest is a consequence of current revenues, acreage available for exploration and production combined with the global oil and gas demand/supply balance. These factors are in turn affected by various political and economic factors, such as global production levels, prices of alternative energy sources, government policies, and the political stability in the oil producing countries. In general the demand for geophysical services is therefore driven by:

The demand/supply balance for oil and gas

Oil and gas companies‟ exploration and production (“E&P”) spend After a decade of growth in E&P spending from 1999, the growth was capped by the economic recession that started in 2008. The result was a decrease in year-on-year global exploration and production spending in 2009. The recession had a significant short-term impact on the global energy demand, illustrated by the severe drop in oil prices. At USD 30.28 per barrel, the oil price trough was reached in December 2008. In 2009 oil prices recovered on OPEC’s above-average compliance to agreed-upon production targets, and trended upwards throughout the year. The positive trend in oil prices continued in 2010, with contract prices reaching USD 89 per barrel in December. Along with higher oil prices, oil companies invested more heavily in developing new resources, illustrated by a year-on-year increase in E&P spending for 2010. From 2011 to 2012 the oil price volatility has been significant, illustrated by contract values ranging from USD 74 to USD 114 during the period. Through 2013 and H1 2014 the oil price has been slightly less volatile with values ranging between USD 90 to 110 per barrel. However in the second half of 2014 the oil price has fallen back from highs of around USD 110 to USD 83 per barrel as supply fears waned with Opec production hitting a two-year high coupled with a decline in global demand on weak economic data. Consequently the short term outlook for the industry is challenging as exploration spend is deferred. In the longer perspective as over supply becomes constrained due to breakeven costs being above oil price and Opec members cut production to stabilize the market, the focus is expected to return to reserves replacement with new exploration provinces like Russia, Myanmar and Mexico providing comfort for an increase in demand of seismic services (source: US Energy Information Administration (“EIA”), International Energy Outlook 2014, International Energy Outlook 2014). Seismic market demand Seismic acquisition is the primary tool used by the oil companies both to explore for new reserves, and lately, for field appraisal and development programs of already discovered and in some cases, producing fields. The cost of such exploration programs has grown substantially which, combined with the historically delivered success rates of 20% - 25% on an exploration well, has fuelled the demand for more and higher quality 3D seismic surveys to better define the prospect and thereby reduce the oil company’s risk, and high cost, of drilling a dry hole. The search for hydrocarbons has also moved beyond the easy-to-find near surface reserves to much deeper and more complex geological places such as those found in the pre-salt geology present in the Gulf of Mexico, West Africa, offshore Brazil and most recently to frontier regions such as the Arctic. The high cost of exploration and drilling in these areas strongly favor the traditional high-end 3D seismic market that is utilized to improve the confidence of a successful discovery before the major investments in drilling and infrastructure are committed. The application of more advanced techniques such as 4D seismic (for time lapse studies of existing reservoirs) in the mature petroleum basins such as the North Sea, and wide- / multi- azimuth surveys of more complex structures offshore Brazil, Angola, and in the Gulf of Mexico, have become more commonplace. The use of 4D seismic in the North Sea has for example resulted in Statoil recognizing several direct benefits such as a 6% reduction in drilling costs and around 5% of additional reserves per field (Source: Offshore Technology / Statoil 13 October 2008). The use of towed marine seismic for both exploration and field appraisal / development programs has in the main resulted in a less volatile business environment than that present in the Nineties when the vast majority of seismic activity was driven by exploration and was consequently very susceptible to oil price movements. A trend in the recent years has been an increase in wide-azimuth projects as oil companies seek to explore more complex, ultra-deep reservoirs frequently located beneath large salt or carbonate deposits. Wide-azimuth surveys that to date have been primarily undertaken in the U.S. Gulf of Mexico are gaining acceptance outside of this area with projects being recently undertaken in West Africa and Brazil. The technique is proven to bring significant

Polarcus Limited, prospectus of 21 November 2014 Registration Document

22 of 37

seismic imaging benefits to sub-salt and sub-basalt plays globally. Polarcus expects the market for these surveys to continue to expand worldwide in areas where the geology supports the technique. The Arctic Region is projected by the US Geological Survey (“USGS”) to grow in significance as it remains one of the last remaining frontier opportunities open to the international oil and gas majors to help them rebuild their reserves portfolio. The Arctic, which comprises some 6% of the Earth‟s surface, is already known to hold around 10% of the known world reserves today (Source: USGS, www.sciencemag.org/content/324/5931/1175.full), with over 400 oil and gas fields discovered to date, mainly onshore Alaska and Russia. The USGS in their multi-year geologic appraisal of the Arctic potential published in July 2008 has estimated that there could be reserves of up to 412 billion barrels of oil equivalent (or 17% of the current known world oil reserves) yet to be found, with 84% of these undiscovered reserves expected to occur offshore, mostly on the existing (undisputed) shelf areas. Of these, the Arctic Alaska and Amerasia basins, both lying to the north of Alaska and Canada, are expected to be the most prolific for oil closely followed by offshore Greenland and the Barents Sea. The former disputed zone in the Arctic Barents Sea between Russia and Norway has additionally attracted considerable industry attention since the signing in September 2010 of an Arctic border agreement between the two countries. Under that agreement Russia and Norway have agreed to divide the 175,000 square kilometres disputed area, half the size of Germany, to the north off their coastlines ending a 40-year dispute over an area in the Barents Sea that contains potentially huge oil and gas reserves. Exploration activity in this area, on both sides of the border, has commenced in earnest. The Arctic region along with several other frontier regions worldwide has traditionally been covered by sparse 2D seismic data, with very little 3D coverage. Polarcus believes there is huge potential for the growth of both conventional 3D services in these areas as industry activity progresses through the exploration and development cycle, and for an exploration 3D solution such as the Company‟s First Pass™ 3D offering that aims to provide oil companies with a cost-effective „first look‟ at acreage prospectivity without the need to commit upfront to the significantly higher cost of a conventional 3D program. The 2014 pro-Russian unrest in Ukraine prompted a number of governments to apply sanctions against individuals and businesses from Russia and Ukraine. Sanctions were approved by the United States, the European Union (EU) and other countries and international organisations. Russia has responded with sanctions against a number of countries. The EU has banned the export of equipment and services suited to be used for Arctic oil exploration and production, deep-water oil exploration and production or shale oil projects in Russia, a move followed by Norway, and recently introduced further sanctions targeting the Russian energy industry. The Norwegian sanctions have to date however not included the seismic services. The US sanctions has banned the export of equipment and services suited to be used for Arctic oil and gas exploration and production, deep-water oil and gas exploration and production (greater than 500 feet depth) or shale projects in Russia. The sanctions are likely to impact seismic exploration activities in certain areas of Russia.

6.4.2 Seismic fleet overview During last month larger seismic companies announced that they would retire a number of older fleet vessels and in some instances, would postpone new build contracts. The Company maintains a comprehensive database of the global 3D seismic fleet, and estimates only limited growth in number of vessels through 2016. This is beneficial to Polarcus as it will help ensure a balanced supply / demand outlook for seismic in the short to medium term whilst the Company’s vessels, being all new build and incorporating many new and innovative features, will be amongst the most advanced in the global 3D seismic fleet. Consequently, Polarcus’ management now estimates that the Company will attain a market share of 10% in 2015.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

23 of 37

7 Organizational structure

7.1 Description of Group that Company is part of Polarcus Limited is the holding company of the Group. The corporate structure of the Polarcus Group is depicted below.

With the exception of Polarcus Nigeria Ltd. all subsidiaries are directly and indirectly 100% owned by Polarcus Limited. A description of the individual companies is given in section 7.1.1.

7.1.1 Description of the companies in the Group Polarcus Limited Polarcus Limited is a Cayman Islands tax exempted company with limited liability registered with the Cayman Islands Registrar of Companies with registration number 201867. The Company was incorporated on 17 December 2007. Polarcus Limited’s registered office is c/o Intertrust Corporate Services, 190 Elgin Avenue, George Town, Grand Cayman KY1 - 9005, Cayman Islands. Polarcus Limited is the holding company of the Polarcus Group. The business headquarter of the Company is in Dubai, UAE. The majority of the offshore crew of the Polarcus Group vessels are employed by Polarcus Limited. As of 30 June 2014, the Company had 422 employees. Polarcus Limited’s shares are registered on the Oslo Stock Exchange with ticker symbol “PLCS”. Polarcus DMCC Polarcus DMCC is a limited liability company incorporated in the free zone of Dubai Multi Commodities Centre under the laws of the United Arab Emirates. The registration number of Polarcus DMCC is 30852. The registered office is Almas Tower, Level 32, Jumeirah Lakes Towers, P.O. Box 283373, Dubai, UAE. Polarcus DMCC serves as the main administrative body of the Polarcus Group and provides services to the remaining group companies related to sales, marketing and operation of vessels as well as general administrative services. As of 30 June 2014, Polarcus DMCC had 125 employees.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

24 of 37

Polarcus UK Limited Polarcus UK Limited is a company with limited liability incorporated under the laws of England and Wales. The registration number of Polarcus UK Limited is 7068161 and its registered office is at St. James House, 13 Kensington Square, London W8 5HD, UK. Polarcus UK Limited carries out marketing and sales as well as multi-client activities and, in certain circumstances, carries out seismic projects in certain jurisdictions. As of 30 June 2014, the company had seven employees. Polarcus UK Limited is furthermore the parent company of Polarcus Shipholding AS. Polarcus Shipholding AS Polarcus Shipholding AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Shipholding AS is 995542846 and its registered office is at c/o Wikborg Rein & Co, Kronprinsesse Marthas Plass 1, 0160, Oslo, Norway. The company acts as the holding company for four Norwegian companies which own vessels. The company has no employees. Polarcus Nadia AS Polarcus Nadia AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Nadia AS is 994063901 and its registered office is at c/o Wikborg Rein & Co, Kronprinsesse Marthas Plass 1, 0160, Oslo, Norway. The company is the bareboat charterer of POLARCUS NADIA under the sale-leaseback arrangement established for this vessel. The company has no employees. Polarcus Naila AS Polarcus Naila AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Naila AS is 995097893 and its registered office is at c/o Wikborg Rein & Co, Kronprinsesse Marthas Plass 1, 0160, Oslo, Norway. The company is the bareboat charterer of POLARCUS NAILA under the sale-leaseback arrangement established for this vessel. The company has no employees. Polarcus Asima AS Polarcus Asima AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Asima AS is 998025877 and its registered office is at c/o RSM Hasner Kjelstrup & Wiggen AS, Filipstad Brygge 1, 0252, Oslo, Norway. The company owns POLARCUS ASIMA. The company has no employees. Polarcus Alima AS Polarcus Alima AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Alima AS is 995963426 and its registered office is at c/o Wikborg Rein & Co, Kronprinsesse Marthas Plass 1, 0160, Oslo, Norway. The company owns POLARCUS ALIMA. The company has no employees. Polarcus Amani AS Polarcus Amani AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Amani AS is 998025966 and its registered office is at c/o RSM Hasner Kjelstrup & Wiggen AS, Filipstad Brygge 1, 0252, Oslo, Norway. The company owns POLARCUS AMANI. The company has no employees. Polarcus Adira AS Polarcus Adira AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Asima AS is 998026016 and its registered office is at c/o RSM Hasner Kjelstrup & Wiggen AS, Filipstad Brygge 1, 0252, Oslo, Norway. The company owns POLARCUS ADIRA. The company has no employees. Polarcus Selma Ltd. Polarcus Selma Ltd. (formerly Polarcus 4) is a Cayman Islands tax exempted company with limited liability registered in the Cayman Islands Register of Companies with registration number 204020. Its registered office is the same as that of Polarcus Limited. Polarcus Selma Ltd. does not have any employees. Polarcus Selma Ltd. owns the vessel POLARCUS SELMA which in August 2011 was bareboat chartered to an OAO Sovcomflot company on a 5-year bareboat charter under the name VYACHESLAV TIKHONOV. Polarcus Multi-Client (CY) Limited Polarcus Multi-Client (CY) Limited is a company with limited liability incorporated under the laws of Cyprus. The registration number of Polarcus Multi-Client (CY) Limited is 267816 and its registered office is at c/o Ernst & Young, Spyrou Kyprianou 27, Ernst & Young House, P.C. 4001 Limassol, Cyprus. The company serves as a crewing company for part of the Polarcus Group’s offshore crew. As of 30 June 2014, the company had 20 employees. Polarcus Seismic Limited Polarcus Seismic Limited is a Cayman Islands tax exempted company with limited liability registered in the Cayman Islands Register of Companies with registration number is 213496. Its registered office is the same as that of Polarcus Limited. Polarcus Seismic Limited does not have any employees. Polarcus Seismic Limited

Polarcus Limited, prospectus of 21 November 2014 Registration Document

25 of 37

carries out certain contracts for seismic work on behalf of the Group as well as certain of the Group’s multi-client projects, and is the counterparty in various consultancy agreements entered into by the Polarcus Group. Polarcus MC Ltd. Polarcus MC Ltd. (formerly Polarcus 5) is a Cayman Islands tax exempted company with limited liability registered in the Cayman Islands Register of Companies with registration number 204065. Its registered office is the same as that of Polarcus Limited. The company carries out certain of the Group’s multi-client projects. The company has no employees. Polarcus Norway AS Polarcus Norway AS is a company with limited liability incorporated under the laws of Norway. The registration number of Polarcus Norway AS is 996798305 and its registered office is at c/o Wikborg Rein & Co, Kronprinsesse Marthas Plass 1, 0160, Oslo, Norway. The company is responsible for certain multi-client activities and seismic contracts in Norway. The company has no employees. Polarcus do Brasil Ltda Polarcus do Brasil Ltda. is a company limited by quotas incorporated under the laws of Brazil with registration number 11.428.425/0001-12. The registered office of the company is at Av Nilo Peçanha, 50 – group 2817, Centro, Rio de Janeiro, Brazil. The company is responsible for the Group’s sales and marketing activities in Brazil. As of 30 June 2014 the company had one employee. Polarcus Egypt Limited Polarcus Egypt Limited is a company limited by quotas incorporated under the laws of Egypt with registration number 41735. The registered office of the company is at 7 Al-Athary Mahmoud Akoush Street, Ard El-Golf, Nasr City Awal, Cairo, Egypt. The company is responsible for the Group’s sales and marketing activities in Egypt. As of 30 June 2014 the company had one employee. Polarcus US Inc. Polarcus US Inc. is a limited liability company incorporated under the state of Delaware in the U.S.A. The registered office of Polarcus US Inc. is c/o Capitol Services Inc., 615 South DuPont Highway, Dover, Kent County, Delaware 19901, U.S.A. The company is responsible for the marketing and business development activities of the Group in the Americas region. As of 31 December 2013 Polarcus US Inc. had one employee. Polarcus Nigeria Limited Polarcus Nigeria Limited is a limited liability company incorporated under the laws of Nigeria. The registration number of Polarcus Nigeria Limited in Nigeria Corporate Affairs Commission is 1024228 and its registered office is 196b, Awolowo Road, Ikoyi, Lagos, Nigeria. The company is owned 49/51 with Polarcus’ business partner in Nigeria, Ashbert Limited. The company is responsible for the marketing and business development activities of the Group in Nigeria. Polarcus Nigeria Limited does not currently have any employees. Polarcus Asia Pacific Pte. Ltd. Polarcus Asia Pacific Pte. Ltd. is a limited liability company incorporated in Singaore. The registration number of Polarcus Asia Pacific Pte. Ltd. is 201322670Z and its registered office is c/o Wikborg Rein & Co, 1 Fullerton Road, #02-01 One Fullerton, Singapore 049213. The company is responsible for the marketing and business development activities of the Group in South East Asia and Australia. As of 30 June 2014 Polarcus Asia Pacific Pte. Ltd had three employees. Polarcus France SAS Polarcus France SAS is a limited liability company incorporated in France with immatriculation number 804 999 902. The registered office of Polarcus France SAS is 121 avenue des Champ-Elysèes 75008 Paris, France. The company will be carrying out certain of the Group’s seismic surveys in Africa. The company has currently no employees. Other Polarcus Entities Polarcus has several shelf companies which currently have no activity including Polarcus 1 , Polarcus 2, Polarcus 6 and Polarcus Samur Ltd.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

26 of 37

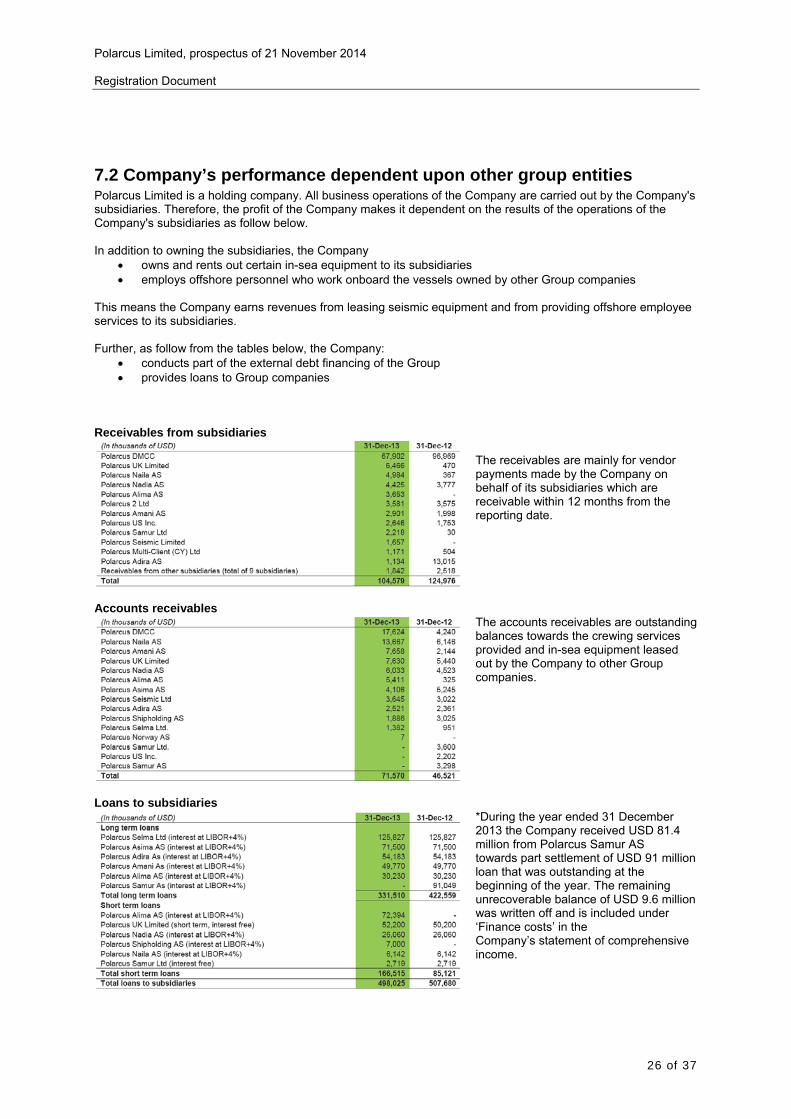

7.2 Company’s performance dependent upon other group entities Polarcus Limited is a holding company. All business operations of the Company are carried out by the Company's subsidiaries. Therefore, the profit of the Company makes it dependent on the results of the operations of the Company's subsidiaries as follow below. In addition to owning the subsidiaries, the Company

owns and rents out certain in-sea equipment to its subsidiaries employs offshore personnel who work onboard the vessels owned by other Group companies

This means the Company earns revenues from leasing seismic equipment and from providing offshore employee services to its subsidiaries. Further, as follow from the tables below, the Company:

conducts part of the external debt financing of the Group provides loans to Group companies

Receivables from subsidiaries

The receivables are mainly for vendor payments made by the Company on behalf of its subsidiaries which are receivable within 12 months from the reporting date.

Accounts receivables

The accounts receivables are outstanding balances towards the crewing services provided and in-sea equipment leased out by the Company to other Group companies.

Loans to subsidiaries

*During the year ended 31 December 2013 the Company received USD 81.4 million from Polarcus Samur AS towards part settlement of USD 91 million loan that was outstanding at the beginning of the year. The remaining unrecoverable balance of USD 9.6 million was written off and is included under ‘Finance costs’ in the Company’s statement of comprehensive income.

Polarcus Limited, prospectus of 21 November 2014 Registration Document

27 of 37

8 Trend information The demand for high end 3D seismic services has been stable over the past two years, however new builds entering the market with improved efficiency has had a negative impact on the rates. The short term outlook for the industry is challenging where the focus is on securing backlog rather than testing higher prices. If the current downturn in the oil price prevails, that may also have a negative impact on the demand. In the longer perspective, new exploration provinces like Russia, Myanmar and Mexico provides comfort for an increase in demand of seismic services. That coupled with an increasing number of vessels being retired lead the Company to believe that there will be an improved demand and supply balance resulting in improved pricing over time. Polarcus, with the benefit of a young and uniform fleet with its unique environmental features, is especially well positioned to take advantage of the positive development in the new frontier regions. There have been no significant changes to the operating costs in the industry other than those related to fuel costs which is derived from the prevailing oil price from time to time. The company has revised its EBITDA guidance for 2014 to USD 140 - 150 million. Global seismic opportunities for the next 12 months as per August 2014:

8.1 Statement of no material adverse change

There has been no material adverse change in the prospects of the issuer since the date of its last published audited financial statements. For further information, see section 11.6 (“Significant change in the Group’s financial or trading position”).

Polarcus Limited, prospectus of 21 November 2014 Registration Document

28 of 37

9 Administrative, management and supervisory bodies

9.1 Information about persons Board of Directors The table below set out the names of the members of the Board of Directors of the Company:

Name Position Business address

Peter Rigg Chairman

Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Carl-Gustav Zickerman

Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Hege Sjo Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Tore Karlsson Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Arnstein Wigestrand Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Karen El-Tawil Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E

Thomas Kichler Director Polarcus Limited, Almas Tower, Level 32, Jumeirah Lakes Towers, PO Box 283373, Dubai, U.A.E