INTRODUCTION As Zimbabwe's inclusive government, tasked with economic and political stabilization goes through its third year, the economy remains shaky whilst the outlook remains uncertain. The economy has stabilized, mainly due to the adoption of a basket of stable currencies but growth has remained sluggish due to a number of factors. On the back of slow growth in the productive sector, revenue authorities' reported growth in revenue collections in the first quarter of 2011 is still below adequate fiscal requirement. Zimbabwe's internal capacity to deal with its external debt, estimated to be $6.9 billion remains constrained in the short to medium term. Government of Zimbabwe (GoZ) has reportedly adopted what it calls a hybrid strategy, comprising of the 'best aspects' of the Highly Indebted Poor Country Initiative (HIPC) and pledging of the country's mineral resources. Under HIPC, a country receives cancellation of part of its debt if it meets certain sustainability criteria, and develops a Poverty Reduction Strategy Paper (PRSP) to link debt relief to poverty reduction. GoZ has also announced that a Debt Management Office (DMO) is being set up within the Ministry of Finance (MoF). Whilst Zimbabwe searches for a solution for its indebtedness, the issue of unsustainable public debt continues to played out in other economies, creating intriguing parallels globally. Of particular interest is the sovereign debt crisis of 2010 which involved some European states, notably Greece, 1 Ireland, Portugal, and Spain which are members of the Eurozone. Briefly, financial markets raised alarm over the rising government deficits and increasing debt levels in these countries. This caused Europe's finance ministers to facilitate a rescue package to maintain stability across Europe. Europe, in collaboration with the International Monetary Fund (IMF) also stepped in with financial assistance for the troubled countries, conditional on the implementation of harsh austerity measures similar to what developing countries went through under the structural adjustment programs. In this context, Jubilee UK and The Zimbabwe Coalition on Debt and Development (ZIMCODD) would like to offer stakeholders information on the state of play with the Eurozone debt, and identify key lessons for Zimbabwe to learn from this crisis and its possible implication for this struggling southern African country. It is hoped that this brief will help to broaden the knowledge of policymakers on matters of public finance, especially management of public debt. Investing in People for Social and Economic Justice Policy Brief June 2011 No. 1/2011 Zimbabwe Coalition on Debt and Development Reflections on the Euro-zone Debt Crisis and Lessons for Zimbabwe 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTRODUCTION

As Zimbabwe's inclusive government, tasked with economic and political stabilization goes through its third year, the

economy remains shaky whilst the outlook remains uncertain. The economy has stabilized, mainly due to the

adoption of a basket of stable currencies but growth has remained sluggish due to a number of factors. On the back of

slow growth in the productive sector, revenue authorities' reported growth in revenue collections in the first quarter

of 2011 is still below adequate fiscal requirement. Zimbabwe's internal capacity to deal with its external debt,

estimated to be $6.9 billion remains constrained in the short to medium term.

Government of Zimbabwe (GoZ) has reportedly adopted what it calls a hybrid strategy, comprising of the 'best aspects'

of the Highly Indebted Poor Country Initiative (HIPC) and pledging of the country's mineral resources. Under HIPC, a

country receives cancellation of part of its debt if it meets certain sustainability criteria, and develops a Poverty

Reduction Strategy Paper (PRSP) to link debt relief to poverty reduction. GoZ has also announced that a Debt

Management Office (DMO) is being set up within the Ministry of Finance (MoF). Whilst Zimbabwe searches for a

solution for its indebtedness, the issue of unsustainable public debt continues to played out in other economies,

creating intriguing parallels globally.

Of particular interest is the sovereign debt crisis of 2010 which involved some European states, notably Greece, 1Ireland, Portugal, and Spain which are members of the Eurozone. Briefly, financial markets raised alarm over the rising

government deficits and increasing debt levels in these countries. This caused Europe's finance ministers to facilitate a

rescue package to maintain stability across Europe. Europe, in collaboration with the International Monetary Fund

(IMF) also stepped in with financial assistance for the troubled countries, conditional on the implementation of harsh

austerity measures similar to what developing countries went through under the structural adjustment programs.

In this context, Jubilee UK and The Zimbabwe Coalition on Debt and Development (ZIMCODD) would like to offer

stakeholders information on the state of play with the Eurozone debt, and identify key lessons for Zimbabwe to learn

from this crisis and its possible implication for this struggling southern African country. It is hoped that this brief will

help to broaden the knowledge of policymakers on matters of public finance, especially management of public debt.

Investing in People for Social and Economic Justice

Policy Brief June 2011

No. 1/2011

Z i m b a b w e C o a l i t i o n o n D e b t a n d D e v e l o p m e n t

Reflections on the Euro-zone Debt Crisis and Lessons for Zimbabwe

1

1. The European private debt crisis

“The Irish state should have saved itself by drastic restructuring of bank liabilities. Bank debt

simply cannot be public debt. If bank debt is to be such debt, bankers should be viewed as

civil servants and banks as government departments. Surely, creditors must take the hit, 2instead.”

Martin Wolf, Financial Times

The root cause of the European debt crisis is private rather than public debt. It has its lineage in the global

financial crisis that hit the world from 2007. The collapse of major financial institutions in USA in 2007

triggered shocks that set the world markets in panic mode putting the whole world economy in distress.

Stock markets suffered, world output declined and the rate of bank failures was unprecedented.

Through the 2000s, deregulated private banks went on a lending spree, pushing up house prices and

increasing consumption and economic growth. As with all economic bubbles it was bound to burst. In

the Eurozone, a sovereign debt crisis has been one of the resultant effects of the crisis. Portugal, Ireland,

Greece and Spain otherwise referred to as the PIGS have been the worst affected, though not the only

ones.

3 Ireland's debt to the rest of the world increased by 35% in just three years between 2005 and 2008. This

increase was entirely due to borrowing by private banks. In the years preceding the financial crisis, the

Irish government was a net saver rather than borrower. The main lenders of this money were foreign

private banks. As of the end of 2010, British banks had lent Ireland €180 billion, and German banks €150 4billion. This lending fuelled a boom with the Irish economy growing by 5 percent a year in the 2000s. But

this growth was due to financial services, a phenomenon better known as financialisation rather than

increase in industrial output. Between 1996 and 2006, Irish house prices increased by between 200 and 5400 per cent.

Portugal was the most indebted European country going into the financial crisis, with a net debt to the 6

rest of the world in 2008 of 100 % of GDP. Again, most of this debt was due to borrowing by private

banks; around 8 out of every 10 Euros owed by Portugal to foreign lenders in 2008 was owed by the

private sector rather than the government. The largest outstanding loans to Portugal are from Spanish 7

(€86 billion), German (€40 billion), French (€37 billion) and British (€25 billion) banks. However, in

contrast to Ireland, the lending to Portugal did not fund unsustainable economic growth. The economy

grew by less than 2 per cent during the 2000s, though this has meant the Portuguese economy has 8shrunk by less than Ireland's since the financial crisis began. As of May 2011 Portugal's economy was

reported to be in a recession.

2

3

9Graph 1: European countries net external debt, 2008 (- surplus)

2. The response: Bailing out the lenders

“Ireland is now in its third year of austerity, and confidence just keeps draining away. And

you have to wonder what it will take for serious people to realize that punishing the 11

populace for the bankers' sins is worse than a crime; it's a mistake.”

Paul Krugman, noble prize winning economist

The global financial crisis, which began in 2007, was caused by too much debt within and between

countries. It was initially triggered when some borrowers in the US were unable to repay loans. Private

Banks across the world were exposed to these bad debts. As they entered financial crisis, the

deterioration accelerated, particularly in other countries with too much debt.

In the UK, the government took the decision to bailout private banks. In the US, multinational bank

Lehman Brothers was allowed to collapse, but this spread further confusion through the financial

system, as it was unclear which other banks had lent Lehman money, and so would lose out most.

Governments chose to give blanket bailouts to banks rather than risk further confusion. In Ireland, the

government decided to guarantee all the private bank loans owed to foreign lenders, effectively turning

all private debt into public debt.

-40

-20

0

20

40

60

80

100

120

Portu

gal

Spain

Greece

Irela

ndIta

ly UK

France

Netherla

nds

Ger

man

y

Per

cen

to

fG

DP

Box 1: The crisis and the EuroIn 1999 12 European countries created a common currency, the Euro, of which there are now 17 member

10countries. The Euro effectively fixes exchange rates between countries, and makes Central Bank interest rates the same. In the build-up to the financial crisis, Portugal, Spain, Greece and Ireland became heavily indebted because they imported more goods than they exported. These extra imports were paid for by borrowing. One way to try to import less, export more and so cut the borrowing would have been for the exchange rate to fall. But with the Euro this was impossible. Furthermore, interest rates were set by the European Central Bank to control inflation for the whole of the Eurozone countries. However inflation, particularly for assets such as house prices, was much higher in countries such as Ireland. Low interest rates helped fuel the borrowing in the heavily indebted European countries.

The bailing-out of banks directly turned private into public debt. But direct public debt also started to

increase dramatically because of shrinking economies. Tax receipts fell and spending on things such as

welfare payments increased. Governments effectively stepped in to keep more people in work and

provide basic benefits for those without. Public cushioning of the bust caused by private profligacy has

prevented the recession being even worse, but also transferred more debt from the private to public

sector.

Since 2008, the total foreign debts owed by Portugal, Spain, Greece and Ireland have continued to

increase.

12Graph 2: Selected European countries net external debt, 2008 and 2010

Ireland's initial response was to bring in government austerity; cuts in public spending and increases in

certain taxes. This sought to reduce the government deficit, even though this was a consequence rather

than cause of Ireland's financial and economic crisis. Yet, this led to Ireland's economy contracting more 13

– suffering the worst recession in Western Europe from 2008 to 2010 - thereby increasing the relative

size of the debt. In 2008 Ireland's GDP fell by 3.5 per cent, followed by a further drop of 7.6 per cent in 14

2009.

Ireland's foreign debt and that of the other crisis countries has continued to increase. Starting with

Greece, the standard prescription forced on the global South, Zimbabwe in particular during the ESAP

period began to be applied in Europe. The EU and IMF have given large new loans to Greece, Ireland and

Portugal. Whilst this is presented to the public as a 'bailout' for those countries, in reality the money is to

be used to ensure countries keep paying foreign private banks, primarily in other European countries

such as Germany, France and the UK. The net effect has not been different from the outcomes of other

creditor led debt relief strategies such as the Highly Indebted Poor Country Initiatives (HIPC) and the

Poverty Reduction Strategy Papers (PRSPs).

0

20

40

60

80

100

120

140

Portugal Spain Greece Ireland

Per

cen

to

fG

DP

2010

2008

4

5

As a condition of these loans, governments have to further increase austerity through cuts in public

spending and increases in certain taxes. By depressing the economy, this only serves to worsen the real

problem, the huge foreign owed debt of the countries concerned. As long as such large debts remain,

resources will continue to flow out of the country in debt repayments.

In the early 1980s Zambia, like many southern countries, suffered from a financial crisis after a decade of

lending by foreign banks and a sudden increase in US interest rates. The IMF bailed out the banks by

lending to keep Zambia from defaulting on its debts. But in return the IMF foisted a programme of cuts in

government spending and liberalisation on the Zambian economy.

Cuts in government spending contributed to Zambia suffering from a severe recession for much of the

1980s and 1990s. By 1995, the Zambian economy had declined by more than 30 percent to 1980 levels, 15

whilst government expenditure had been cut by half.

Yet the cuts in spending failed to reduce Zambia's debt. When the IMF intervened in Zambia in 1983 the

government's foreign debt was 75 per cent of GDP. By 1995 it had doubled to 150 per cent. At the same 16time Zambia reduced government expenditure at a rate “virtually unmatched in Africa” and was

17praised by the IMF and World Bank for doing so.

Zimbabwe has had an almost similar experience through the Structural Adjustments Programs (ESAP)

introduced in the early 1990s. ESAP saw a rapid rise in public debt not only through direct government

borrowing but also private publicly guaranteed debts. Upon independence in 1980 public debt stock

totalled US$786 million but by 1990 it had increased by 300% to US$3, 240 billion. Between 1990 and 181998 public debt increased by 50% to US$ 4,716 billion . Much of the debt now owed by Zimbabwe to

multilateral development banks and the Paris Club was originally borrowed under the auspices of the

ESAP.

But to only express the public costs of ESAP accrued debt in terms of repayments and actual figures owed

is in itself not enough. The social costs were enormous. By 2001 interest expenditure amounted to

1496% of the allocation to higher education. Expenditure on interest payments on external debt had

ballooned to forty times more than expenditure on social welfare by 2001. In 1980 1, 2% of gross

national product (GNP) went to debt servicing compared to 9% to education but by 1995 this had been

reversed with 10, 3% going toward debt servicing to 8, 5% toward education. By 2001 interest

expenditure amounted to 407% of primary and secondary education allocation. Further to this,

liberalisation and austerity measures prescribed by ESAP led to deindustrialisation, growing 20

unemployment and poverty . By 1999 external debt to GDP ratio stood at 82% . Zimbabwe was paying

more in debt servicing than it was receiving in aid. The deteriorating economic performance diminished

the state's capacity to repay its loans and Zimbabwe has been defaulting since 1999. As of October 2010

Zimbabwe's external debt stood at US$6, 9 billion of which US$4, 8 billion (70%) was in arrears.

19

2INTEREST EXPENDITURE AS % OF LABOUR & SOCIAL WELFARE ALLOCATIONS

Source: ZIMCODD Social Effects Study (2001)

3. The response: The power of creditors

“the more successful [Ireland] is at reducing wages and costs, the heavier its inherited debt

load becomes. Public spending then has to be cut even deeper. Taxes have to rise even

higher to service the debt of the government and of wards of the state like the banks. This in

turn implies the need for yet more internal devaluation, which further heightens the 24burden of the debt in a vicious spiral.”

Barry Eichengreen, Professor of Economics, University of California

The main creditors in the European debt crisis are foreign, mostly European, banks. The main creditor

within Europe is Germany. French and British banks are also large creditors, though as countries they are

in net debt to the rest of the world.

PERIOD PERCENTAGE

1996-97 929%

1997-98 412%

1999 1,771%

2000 2,304%

2001 3,948%

Box 2: Iceland The non-EU member country Iceland had an even larger boom in private borrowing, and subsequent bust, than Portugal, Ireland, Greece and Spain. But rather than guaranteeing all private bank loans, the government of Iceland let its private banks default on debt owed to foreign lenders. The IMF says that as a result “private sector bankruptcies have led to a marked decline in external debt.” At the same time, Iceland also imposed capital

21controls to prevent money rushing out of the country.

Iceland has still suffered from a severe recession, but now appears to be recovering, whilst the situation of the 22European crisis countries continues to get worse. Furthermore, its rate of unemployment is 7.5 per cent,

lower than that of the four European crisis countries.

The government of Iceland reached an agreement with the governments of the UK and Netherlands to repay some of the money owed by its bankrupt banks. This agreement linked debt repayments explicitly to its rate of growth; a useful mechanism which means lenders themselves lose out if they try to impose austerity measures on countries in recession. However, in a referendum in April 2011 the Icelandic people voted against this agreement, feeling that it was still landing them with debt they had no reason to repay.

Aditya Chakraborrty, economics correspondent at the UK Guardian newspaper, has said: “Iceland was a country wrecked by implementing free-market dogma crudely and quickly; it may yet became another such lesson of how an

23economy can ignore free-market dogma – and come out far better than its critics predicted.”

6

7

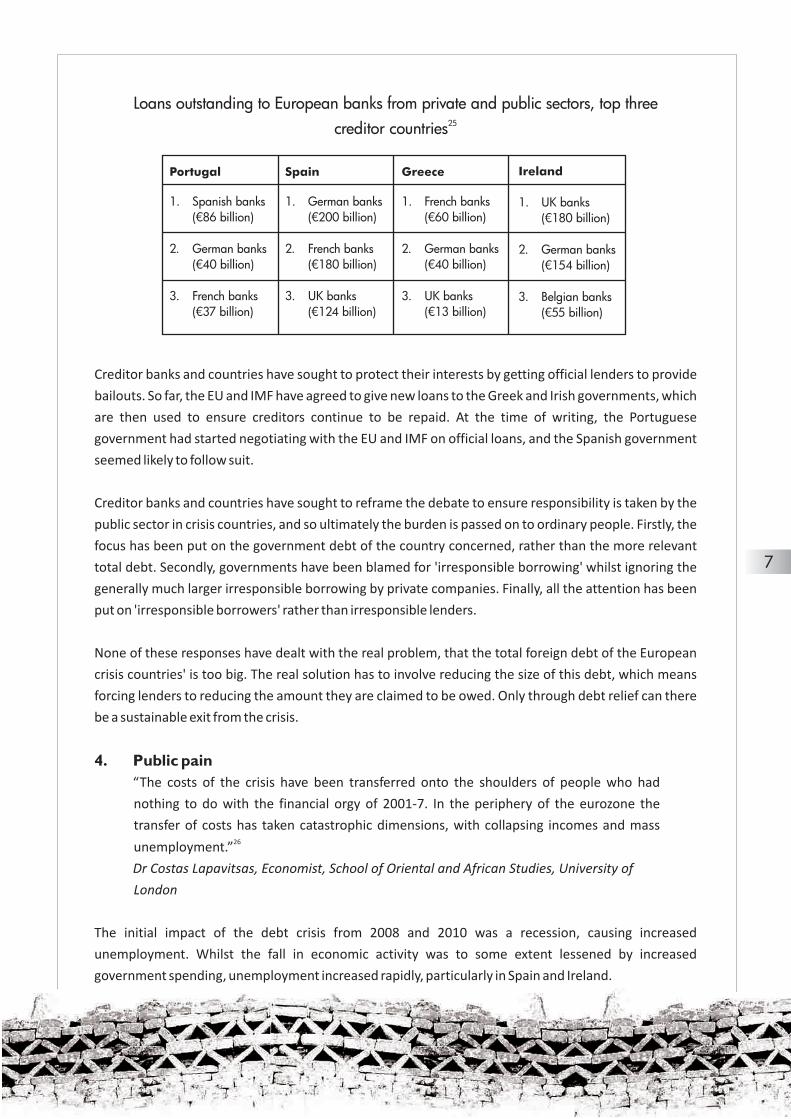

Loans outstanding to European banks from private and public sectors, top three 25

creditor countries

Creditor banks and countries have sought to protect their interests by getting official lenders to provide

bailouts. So far, the EU and IMF have agreed to give new loans to the Greek and Irish governments, which

are then used to ensure creditors continue to be repaid. At the time of writing, the Portuguese

government had started negotiating with the EU and IMF on official loans, and the Spanish government

seemed likely to follow suit.

Creditor banks and countries have sought to reframe the debate to ensure responsibility is taken by the

public sector in crisis countries, and so ultimately the burden is passed on to ordinary people. Firstly, the

focus has been put on the government debt of the country concerned, rather than the more relevant

total debt. Secondly, governments have been blamed for 'irresponsible borrowing' whilst ignoring the

generally much larger irresponsible borrowing by private companies. Finally, all the attention has been

put on 'irresponsible borrowers' rather than irresponsible lenders.

None of these responses have dealt with the real problem, that the total foreign debt of the European

crisis countries' is too big. The real solution has to involve reducing the size of this debt, which means

forcing lenders to reducing the amount they are claimed to be owed. Only through debt relief can there

be a sustainable exit from the crisis.

4. Public pain

“The costs of the crisis have been transferred onto the shoulders of people who had

nothing to do with the financial orgy of 2001-7. In the periphery of the eurozone the

transfer of costs has taken catastrophic dimensions, with collapsing incomes and mass 26

unemployment.”

Dr Costas Lapavitsas, Economist, School of Oriental and African Studies, University of

London

The initial impact of the debt crisis from 2008 and 2010 was a recession, causing increased

unemployment. Whilst the fall in economic activity was to some extent lessened by increased

government spending, unemployment increased rapidly, particularly in Spain and Ireland.

Portugal

1. Spanish banks

(€86 billion)

2. German banks

(€40 billion)

3. French banks

(€37 billion)

Spain

1. German banks

(€200 billion)

2. French banks

(€180 billion)

3. UK banks

(€124 billion)

Greece

1. French banks

(€60 billion)

2. German banks

(€40 billion)

3. UK banks

(€13 billion)

Ireland

1. UK banks

(€180 billion)

2. German banks

(€154 billion)

3. Belgian banks

(€55 billion)

27Unemployment rate in European crisis countries, 2001-2010

The EU and IMF are now forcing extreme austerity conditions on the crisis countries through cuts in

government spending. Public sector jobs and pay are being cut and welfare payments are being

reduced. Spending for services such as health and education are being cut.

A core condition of EU and IMF loans is also to increase taxes, usually sales taxes such as VAT. In Ireland

the government is increasing the rate of VAT from 21 per cent to 24 per cent over the next three years.

Greece, Portugal and Spain have or are all increasing VAT rates by 2 percentage points.

Whilst there have been increases in regressive taxes such as VAT, taxes on corporations have remained

unaffected. For example, Ireland has maintained its ultra-low 12.5 percent tax on company profits.

Despite not suffering from an external debt crisis, the UK is making large cuts in government spending.

And whilst UK VAT has been increased by 2.5 per percentage points at the start of 2011, corporation tax

has been cut by 2 percentage points and is to be reduced further.

One standard policy condition of the IMF is for a country to devalue its currency in order to reduce

imports, increase exports and thus stop creating more debt, and ultimately reduce debt. However, for

the European countries this is impossible without leaving the European single currency. Therefore, IMF

and EU conditions are attempting to 'internally devalue' a country's economy by cutting wages for

workers. There are three broad ways to do this:

! Cut public sector pay

! Reduce legal minimum wages (in Ireland the minimum wage is being cut by €1 an hour worked)

! Increase unemployment, so that workers will be willing to work for less money. Therefore,

unemployment is actually a goal of IMF and EU policy in the countries.

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

Per

cen

tag

eu

nem

plo

yed

Portugal

Ireland

Spain

Greece

8

9

The impact of austerity is set to increase unemployment, cut public spending on basic services and,

perhaps most importantly, increase inequality. In as much as it lowers economic growth, austerity will

also make the debt crisis worse, increasing the relative size of a country's debt compared to its economy.

5. The impact beyond Europe

“Financial globalisation has not generated increased investment or higher growth in

emerging markets. Countries that have grown most rapidly have been those that rely less on 28

capital inflows.”

Dani Rodrik, Harvard University, and Arvind Subramanian, IMF research department

The impact of the Western financial crisis and continuing debt crisis in Europe is passed on to the global

South through the direct effect on financial flows, and more indirectly through the impact of recession

on trade, remittance payments and aid. The IMF has calculated that economic growth in low income

countries has been 4 percent less over 2008-2010 than it was in the years immediately preceding the 29financial crisis.

Action Aid has found that the largest impact of the Northern debt crisis on the global South has been on

financial flows. The debt of the north has led to banks repatriating money back home to try to cover their

losses. The Institute of International Finance estimates that bank lending from the North to the South

dropped by more than 100 per cent between 2007 and 2009; there was a net outflow of banking money

from developing countries back to banks in the North. Action Aid conclude: “those countries that bought

most heavily into the rhetoric of financial liberalisation, and that were big enough to attract significant 30

amounts of capital from rich countries, will be most affected by the financial crisis”.

This experience again emphasises the importance of trying to use primarily domestically generated

capital to fund investment. Research by the likes of Dani Rodrik from Harvard University, and Arvind

Subramanian for the IMF research department, has shown that foreign capital inflows have a poor 31record in generating investment and growth. Foreign capital inflows can also lead to outflows as

interest and profits are taken out of a country. And it has now been seen that dependence on foreign

capital can make countries more vulnerable to financial crisis elsewhere in the world.

The Northern debt crisis has also impacted on the South by causing recession in the north, leading to a

fall in trade, remittances from migrants and aid. Action Aid say that overall for the South the losses due to

recession are less than those which are directly the result of financial crisis. But that for many countries,

the main impact has been on trade and remittances. This is true for the poorest countries which have

been less able to attract foreign finance, however much they have removed regulations on capital.

Action Aid and the New Economics Foundation have found that openness to international trade is the 32biggest factor for many countries in how vulnerable they are to the financial crisis.

For those most affected by the financial crisis and thus resorting to new loans and adjustment

programmes from the IMF, their experience mirrors that of European crisis countries.

Sierra Leone had 80 per cent of its foreign debts cancelled in 2007, but its debt to the rest of the world

has doubled during the financial crisis. Demand for its exports fell, along with remittances from Sierra

Leoneans living abroad. In 2011, 10 per cent of the government's revenue will be spent on debt 33repayments, more than is spent on healthcare (8 per cent).

At the start of 2010 prices for basic goods shot up across the West African country after a new IMF

inspired standard sales tax was introduced. The tax was meant to simplify a range of different sales taxes,

whilst increasing revenues. The IMF responded to higher inflation by telling Sierra Leone to increase 34interest rates, which will also hold back the economy.

Pakistan too is being made to increase VAT. The combined effect of the global financial crisis and 2010s

devastating floods have led the South Asian country's debt to increase by $10 billion in the last three

years; $60 per person in a country with a national income of just $1,000 per person a year. Shahid Hassan

Siddiqui from the Research Institute of Islamic Banking says IMF tax conditions in Pakistan will

Through the 1980s and 1990s Pakistan increased VAT at the behest of the IMF, whilst reducing taxes on

imports. As a percentage of tax revenue, sales taxes in Pakistan increased from 7 per cent in 1980 to

almost 30 per cent by 2000. Overall taxes for the poorest households, whilst

falling by 15 percent for the richest.

Jamaica's financial debt to the rest of the world has increased by a third during the financial crisis, and

now stands at more than $3,000 per person. The Jamaican government spends $400 per person in debt

repayments each year, more than it spends on education ($215) and health ($100) combined. With an

annual income per person of $4,800, Jamaica has never been considered for debt cancellation because it

'is not poor enough'.

Jamaica is now borrowing more money from the IMF to stay afloat. One of the IMF's conditions is a

three-year wage freeze for public sector workers, which the Jamaican Supreme Court has declared illegal

as it breaks previous commitments. Given current and predicted inflation rates in the Caribbean island,

the freeze is likely to amount to an effective 25 per cent cut in incomes. Public spending overall is to be

cut by 20 percent by 2012 of levels before the financial crisis.

6. Conclusion and recommendations

“Have politicians got the courage to make those who earn money share in the risk as well?

Or is dealing in government debt the only business in the world economy that involves no

risk.”35Angela Merkel, German Chancellor

"hurt the

poor".

increased by 7 percent10

11

Box 3: Surplus, deficits and debtA country ultimately comes to owe debt to the rest of the world if it imports more than it exports; it has a trade deficit. The extra imports are paid for by borrowing from other countries. On the flip side, countries which want to build-up their savings have to export more than they import; such countries have a trade surplus.

In the 1940s, the British economist John Maynard Keynes argued that the key to ensuring greater global financial stability, and preventing another depression such as that seen in the 1930s, was to stop countries having large surpluses and deficits. He proposed interventions which would prevent large recurring surpluses and deficits, and so limit crises from happening in the first place.

Keynes led the British delegation in negotiations with the US in 1944 on creating a new global financial system. As the world's largest surplus country, the US rejected Keynes' and the British argument. Instead the IMF was created to bailout deficit countries, rather than create a more well-functioning system which requires action from both surplus and deficit countries. Today, the US is a debtor country, whilst Japan, Germany and China are the main surplus countries. In fact because the US dollar is the reserve currency of the world, the US has an incentive to produce more dollars. US consumers spend more money and are essentially 'lent' the money very cheaply by many developing world countries. If world leaders are serious about reducing 'global imbalances' they need to re-examine some of Keynes' ground-breaking ideas.

History consistently shows that private lenders left to their own devices will be reckless, fuelling bubbles

which then burst, leaving the public to pick-up the bill. The fact lenders consistently get bailed out helps

to keep this system going, as lenders know they will not face the full consequences of their actions.

As well as creating a system where private banks do share in the costs of failed lending, there needs to be

far greater public control over the financial system. Banks need to be actively regulated to ensure that

they do not lend too much, as has happened in so many European countries. The flow of capital across

borders needs to be controlled, so that private money cannot flood in and out of countries to destabilise

them. Taxes on the richest and most powerful people and institutions need to be enforced to ensure

governments are not denied adequate funding.

High, middle and low income countries have huge disparities in wealth and income. But the people of all

suffer from debt crises', austerity and imbalances in global trade. We need to look to global responses if

true debt justice is to be achieved. With debt crisis reverberating across Europe, now is the time for all

campaigners against the scourge of debt to campaign for people to take back control of the financial

system, specifically:

! Lenders to be made responsible for the loans they give, rather than passing on all debts to the public.

! Care must also be taken to ensure that private borrowers do not pass on the risk to citizens through 36the process of publicly guaranteed private debt. In the context of Zimbabwe, this is important when

37one considers that Treasury recently raised concerns over the high loans default rate. The local

private sector has appealed for lines of credit to be reopened from external creditors. Parliamentary

oversight is therefore needed in the contraction of such loans, to ensure that private debt does not

become public debt.

! The experiences of Europe show that the costs of the crisis are really borne by ordinary citizens who

had nothing to do with the crisis. Mechanisms must therefore be adopted to ensure that debt service

does not crowd out spending on social sectors. In 2010 GoZ paid the IMF an amount that was

equivalent to the budget for anti-retroviral drugs by the Health and Child Welfare Ministry, according

to the 2010 budget estimates. Creditors still insist on debt repayments when it is clear that the

economy cannot cope with them at the moment.

! As illustrated above, it is extremely important to develop and depend primarily on domestically

generated capital to fund investment. In this view, GoZ must ensure transparency in the extraction

and marketing of minerals, in particular the recently discovered alluvial diamond deposits in South

Eastern Zimbabwe. Revenue from these sources must be channelled strategically to sectors that

ensure growth in the economy in the short to medium term.

! An independent debt commission must be created which in the future a) publicly audits all debts, b)

cancels unjust and corrupt debts, c) cancels or restructures all remaining debt on the basis of the

resources a government needs to provide essential services, d) treats all foreign creditors on an equal

basis.

! Greater public control of the financial system through tough regulation to ensure banks do not lend

recklessly and excessively.

! Giving governments the ability to regulate the flow of money across borders when needed ('capital

controls').

! Clamping down on tax dodging through applying reasonable corporation tax in all territories

including current 'tax havens', providing sufficient resources to revenue and customs authorities,

supporting companies reporting on a country-by-country basis to open up the tax system, and

supporting an automatic information exchange between countries.

! The experience of the Eurozone crisis shows that countries which had more trade liberalisation were

more vulnerable to the financial crisis. In this view, Zimbabwe needs to review its decision to sign the

Economic Partnership Agreement (EPA), with the EU. This will expose its ailing economy to

competition from stronger multinational corporations. Research done by Ha-Joon Chang of the

University of Cambridge shows that there is no leading economy that developed to its present status 38without tariffs, subsidies and other measures of intervention on their fledgling economies.

Zimbabwe must therefore take a leaf from the stance of Namibia, Malawi and Angola on EPAs.

The prospects for such changes may never have been closer, or further away. The European debt crisis

has also shown again the power of lenders to protect their interests through defining how issues are

debated and using powerful institutions such as the IMF and EU. But this has also brought home to the

people of Europe the danger of financial market power and uncontrolled debt. There is now a greater

chance of a global movement forming calling for debt justice.

12

13

Endnotes

1 The Eurozone is an economic and monetary union (EMU) of 17 European Union (EU) member states that have

adopted the euro (€) as their common currency and sole legal tender.2 Wolf, M. (2010). Why the Irish crisis is such a huge test for the Eurozone. Financial Times. London. 30/11/10.3 IMF. (2010). Ireland: Request for an extended arrangement. International Monetary Fund. Washington DC.

04/12/10.4 Stabe, M., Minto, R., Feeney, P. and Bernard, S. (2010). Bank exposure: The Eurozone risk. The Financial Times.

London. 13/12/10. http://www.ft.com/cms/s/0/9686c004-fca4-11df-bfdd-

00144feab49a.html#axzz1AdCzUOcd5 http://www.globalpropertyguide.com/Europe/Ireland/Price-History 6 IMF. (2009). IMF Executive Board concludes 2009 Article IV consultation with Portugal. International Monetary

Fund. Washington DC. 20/01/10.7 Stabe, M., Minto, R., Feeney, P. and Bernard, S. (2010). Bank exposure: The Eurozone risk. The Financial Times.

London. 13/12/10. http://www.ft.com/cms/s/0/9686c004-fca4-11df-bfdd-

00144feab49a.html#axzz1AdCzUOcd8 IMF. (2009). IMF Executive Board concludes 2009 Article IV consultation with Portugal. International Monetary

Fund. Washington DC. 20/01/10.9 IMF. (2009). IMF Executive Board concludes 2009 Article IV consultation with Portugal. International Monetary

Fund. Washington DC. 20/01/10. And (for UK stats) Whittard, D. and Khan, J. (2010). The UK's International

Investment Position. Office for National Statistics. June 2010.10 Some EU member states have not joined the Euro, such as the UK and Denmark. The current members are:

Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the

Netherlands, Portugal, Slovakia, Slovenia and Spain.11 Krugman, P. (2010). Eating the Irish. The New York Times. 25/11/10.

http://www.nytimes.com/2010/11/26/opinion/26krugman.html?_r=2&partner=rssnyt&emc=rss12 IMF. (2010/2011). IMF country documents, various. International Monetary Fund. Washington DC. 20/01/10.13 Data from Eurostat http://epp.eurostat.ec.europa.eu/portal/page/portal/eurostat/home/ 14 IMF. (2010). Ireland: Request for an extended arrangement. International Monetary Fund. Washington DC.

04/12/10.15 Situmbeko, L.C. and Zulu, J.J. (2004). Zambia: Condemned to debt. How the IMF and World Bank have

undermined development. World Development Movement. London. April 2004.16 Bigsten, A., Levin, J. and Persson, H. (2001). Debt relief and growth: A study of Zambia and Tanzania. Paper

prepared for the WIDER Development Conference on debt relief. 17-18 August 2001.17 Situmbeko, L.C. and Zulu, J.J. (2004). Zambia: Condemned to debt. How the IMF and World Bank have

undermined development. World Development Movement. London. April 2004.18 The Social Effects and Politics of Public Debt in Zimbabwe: the Impact of Public Debt Management on

Development, ZIMCODD, 2001.19 Zimbabwe's Plunge, Bond and Manyama, 200720 The Social Effects and Politics of Public Debt in Zimbabwe: the Impact of Public Debt Management on

Development, ZIMCODD, 2001.pg35 - 4021 Krugman, P. (2010). Eating the Irish. The New York Times. 25/11/10.

http://www.nytimes.com/2010/11/26/opinion/26krugman.html?_r=2&partner=rssnyt&emc=rss 22 Chakrabortty, A. (2011). Iceland broke the rules and got away with it. The Guardian. London. 12/04/11.23 Chakrabortty, A. (2011). Iceland broke the rules and got away with it. The Guardian. London. 12/04/11.

24 Eichengreen, B. (2010). Ireland's reparations burden.

http://www.irisheconomy.ie/index.php/2010/12/01/barry-eichengreen-on-the-irish-bailout/#more-883125 Stabe, M., Minto, R., Feeney, P. and Bernard, S. (2010). Bank exposure: The Eurozone risk. The Financial

Times. London. 13/12/10. http://www.ft.com/cms/s/0/9686c004-fca4-11df-bfdd-

00144feab49a.html#axzz1AdCzUOcd26 Lapavitsas, C. (2011). Support the campaign to audit Europe's public debt. The Guardian. London. 03/03/11.27 ILO. (2011). Labour market statistics. International Labour Organisation.28 Rodrik, D and Subramanian, A. (2008). Why did financial globalisation disappoint? March 2008.29 IMF. (2010). Emerging from the global crisis: Macroeconomic challenges facing low income countries.

International Monetary Fund. Washington DC. 05/10/10.30 Action Aid. (2009). Where does it hurt? The impact of the financial crisis on developing countries. Action Aid. 31 Rodrick, D and Subramanian, A. (2008). Why did financial globalisation disappoint? March 2008.32 Action Aid. (2009). Where does it hurt? The impact of the financial crisis on developing countries. Action Aid. 33 IMF. (2010). Staff Report for the 2010 Article IV Consultation, First Review Under the Three-

Year Arrangement Under the Extended Credit Facility, Request for Modification of

Performance Criterion, and Financing Assurances Review. International Monetary Fund. Washington DC.

18/11/10. http://www.imf.org/external/pubs/ft/scr/2010/cr10370.pdf 34 IMF. (2010). Staff Report for the 2010 Article IV Consultation, First Review Under the Three-

Year Arrangement Under the Extended Credit Facility, Request for Modification of

Performance Criterion, and Financing Assurances Review. International Monetary Fund. Washington DC.

18/11/10. http://www.imf.org/external/pubs/ft/scr/2010/cr10370.pdf 35 Reuters: 'Merkel:EU needs courage to make investors share risk', Wed, Nov 24 2010

http://www.reuters.com/article/idUSLDE6AN1612010112436 Publicly guarnateed private sector debt is an amount borrowed by a private debtor that is guaranteed for

repayment by government.37 Golden Sibanda “Biti Warns of Bank Crisis” in The Herald 28 April 2011 page B138 Ha-Joon Chang (ed.), Rethinking Development Economics (Anthem Press, London, 2003)

14

15

Notes

About ZIMCODD

The Zimbabwe Coalition on Debt and Development, ZIMCODD, is a socio-economic justice coalition established

in February 2000 to facilitate citizens' involvement in making public policy and practice pro-people and sustainable.

ZIMCODD views Zimbabwe's indebtedness, the unfair global trade regime and lack of democratic people-centered

economic governance as root causes of the socio-economic crises in Zimbabwe and the world at large. Drawing

from community-based livelihood experiences of its membership, ZIMCODD implements programs targeted at;

?Educating the citizen

?Facilitating policy dialogue among stakeholders

?Engaging and acting on socio-economic governance at local, regional and global levels

ZIMCODD's headquarters are in Harare with regional offices in Bulawayo and Mutare.

VisionSustainable socio-economic justice in Zimbabwe through a vibrant people based movement.

Mission

To develop capacities of Zimbabwean people to redress the debt burden and unjust trade practices, building and

promoting alternatives to neo-liberal agenda.

Ojectives

To raise the level of economic literacy among ZIMCODD members to include views and participation of grassroots

and marginalised communities;

?To facilitate research, lobbying and advocacy in order to raise the level of economic literacy on issues of

debt, trade and sustainable development;

?To formulate credible and sustainable economic and social policy alternatives;

?To develop a national coalition, and facilitate the building of a vibrant movement for social and economic

justice.

ZIMCODD is affiliated to the Southern Africa Peoples’ Solidarity Network (SAPSN), Africa Jubilee South (AJS), Jubilee South, the Zimbabwe Social Forum (ZSF) and the African Forum and Network on Debt and Development (AFRODAD).

Acknowledgements

ZIMCODD Contact DetailsHead Office Southern Region Office Mutare OfficeP. O Box 8840 , Harare 25A Jason Moyo Street, Cnr.1st Ave Suite 104 Old Mutual CenterTel/Fax:+263-4-776830/31/35 Bulawayo MutareEmail:[email protected] Tel/Fax : +263-9-62064 or Tel 020-68125Website: www.zimcodd.org.zw +263-9-886594/95

This policy brief was prepared by Tim Jones, (Jubilee Debt Campaign, UK), Showers Mawowa and Dakarayi Matanga, (Zimbabwe Coalition on Debt and Developmnet).

Project Supported by

Related Documents