Path Refinancing The www.totalmortgage.com © October 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

totalmortgage.com | 877-868-2503 1

PathRefinancing

The

www.totalmortgage.com © October 2012

totalmortgage.com | 877-868-2503 2

PathRefinancing

The

Over time, many things change and need adjustment, and the reality is your home financing

is no different. Regardless of whether you took your current home loan out 20 years ago, 10

years ago, five years ago, or even last year, your financial situation and the economic climate

may be vastly different than it was even a short time ago. For this very reason, it’s a good idea

to review your home financing and determine if your current loan still makes sense given your

current financial situation and needs.

Given today’s low rate environment and the wide range of refinancing options available to

borrowers, now is an excellent time to reevaluate your present mortgage. You may find a

tremendous opportunity to save a significant amount of money. To help make that determi-

nation, you’ll need to understand the steps of the refinance process and figure out if it’s the

right move for you at this time.

Refinancing Steps 1. Understanding Refinancing 2. Knowing Your Goals 3. Preparing Properly 4. Examining Your Options 5. Working with an Expert 6. Getting Through Closing 7. Managing Your Mortgage

totalmortgage.com | 877-868-2503 1

totalmortgage.com | 877-868-2503 3

When you engage in a refinance of your

mortgage loan you are agreeing to replace

your existing loan with a new one. This

means new terms, rates, and payments.

Typically those terms and rates should be

favorable to you, saving you money and

justifying the refinance process.

One of the first items you’ll want to review

are the terms of your current mortgage.

You should have an understanding of

what you are paying each month, your

current interest rate, how long you have

had your current mortgage loan, how

much you will pay over the life of the loan,

and if any pre-payment penalties apply.

This information will help you make a fair

comparison against new rate quotes and

programs that are being offered today and

will clearly show if it makes sound financial

sense for you to consider refinancing.

For example, here’s a basic look at what the

difference between paying a 6% interest

rate and a 3% interest rate could mean to

you on a 30-year loan of $300,000:

Understanding Refinancing1

CURRENT LOAN PROPOSED NEW LOANLoan Amount $300,000 $300,000Loan Term 30 years 30 yearsInterest Rate 6% 3%Payment 1798.65 1264.81Savings Per Month 533.84Total Payments $647,514 $455,331.60Total Savings 192,182,40

Of course there are many other factors

you’ll need to take into consideration. You’ll

want to determine the amount of equity

you have in your home, as that will help

narrow down what type of refinance loan

you may qualify for, and if you’ll need to pay

mortgage insurance. You may be required

to get an appraisal, which is simply a pro-

fessional estimate of your home’s current

worth. Understanding your home’s value

today is critical in helping to determine the

best financing options available to you.

As with any mortgage loan, a refinance

will also require completing paperwork,

including a loan application that will help

determine your eligibility. Depending

on the type of product you choose, your

totalmortgage.com | 877-868-2503 4

loan approval will be based on a variety of

personal financial factors. The good news

is that there are a variety of programs

available to meet the needs of different

types of borrowers and situations, including

traditional refinances, (where credit

scores, current debt and loan amounts

will weigh greatly on approvals), as well as

government programs designed to help

homeowners that may not have ideal credit.

Under the Making Homes Affordable Act,

there are even several programs that can

assist those underwater on their mortgage.

Also keep in mind that you will be required

to pay closing costs on your new loan, which

vary depending on your lender and location.

You will need to have a good understanding

of what these costs will be and factor them

in when determining if a refinance is right for

you. You should examine your break-even

point as well, which will clearly show you

the amount of time it will take you to recoup

the closing costs that you will incur with a

refinance. For a clearer picture of this, let’s

look at an example:

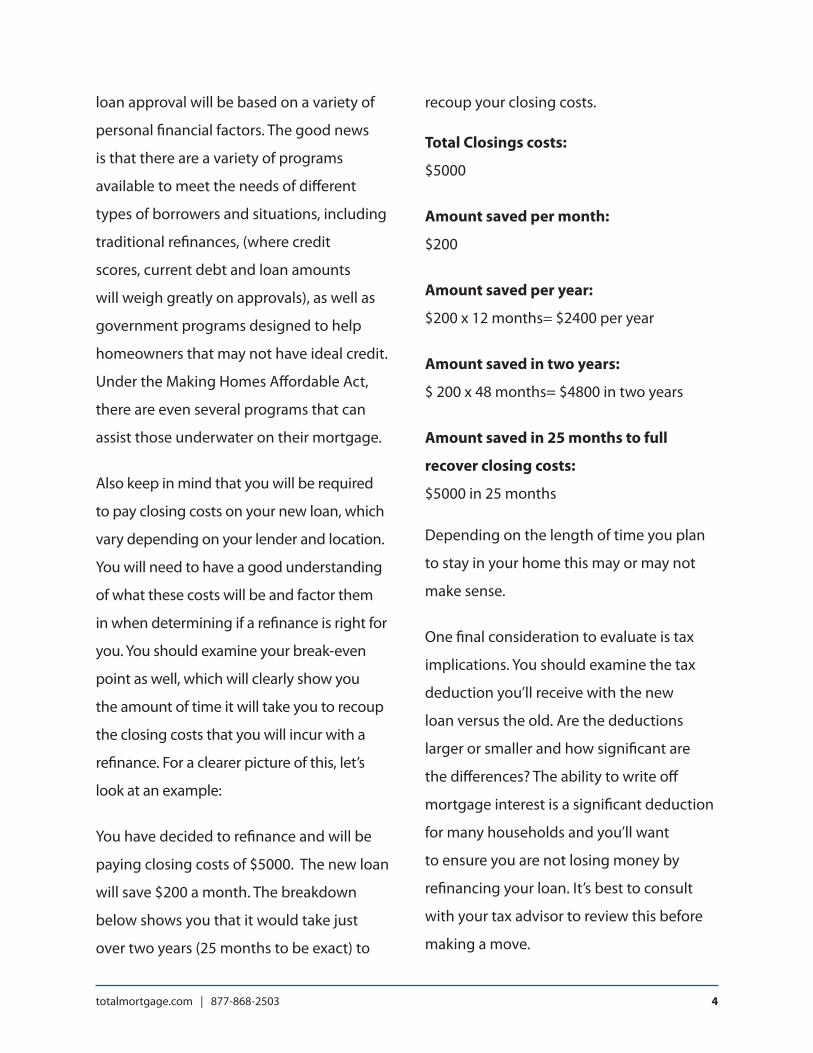

You have decided to refinance and will be

paying closing costs of $5000. The new loan

will save $200 a month. The breakdown

below shows you that it would take just

over two years (25 months to be exact) to

recoup your closing costs.

Total Closings costs:

$5000

Amount saved per month:

$200

Amount saved per year:

$200 x 12 months= $2400 per year

Amount saved in two years:

$ 200 x 48 months= $4800 in two years

Amount saved in 25 months to full

recover closing costs:

$5000 in 25 months

Depending on the length of time you plan

to stay in your home this may or may not

make sense.

One final consideration to evaluate is tax

implications. You should examine the tax

deduction you’ll receive with the new

loan versus the old. Are the deductions

larger or smaller and how significant are

the differences? The ability to write off

mortgage interest is a significant deduction

for many households and you’ll want

to ensure you are not losing money by

refinancing your loan. It’s best to consult

with your tax advisor to review this before

making a move.

totalmortgage.com | 877-868-2503 5

Knowing Your Goals2There are many reasons you may want to

consider a refinance and you should be clear

on your goals before you begin the process.

Be sure to share what you’d like to achieve

through refinancing with your mortgage

professional so they can help guide you

toward the best product to fit your current

needs. Below are just some of the key reasons

homeowners typically opt to refinance.

• Take advantage of lower interest rates.

Long term interest rates are close to

record lows, and the reality is that we

may never see them this low again. If

you are able to refinance now before

rates begin to climb you may not only

lower your monthly payment but you

could see tremendous savings over

the life of your loan.

• Tap into the equity in your home to pull

cash out.

If you have a good deal of equity

in your home, there may be an

opportunity for you to refinance and

use some of that equity for other

purposes. This may be a good option

if you need to use the money to pay

down high interest rate credit cards or

personal loans. You may even want to

opt for a cash-out refinance to help pay

for college tuition or even fund a new

business. Tapping one’s home equity is

not without risk, and you will definitely

want to consult your mortgage profes-

sional before doing so.

• Move out of an Adjustable Rate Mortgage.

Perhaps you are currently in an

Adjustable Rate Mortgage (ARM) that

is set to adjust very soon. Your rate may

Housing Facts • The median distance from the previous

residence was 12 miles

• To find their home, 88% use the Internet,

87% use real estate agents, 55% yard signs,

45% attend open houses and 30% review

print or newspaper ads.

totalmortgage.com | 877-868-2503 6

be set to adjust much higher than the

rate you could lock in today. Converting

to another type of loan could help

prevent you from seeing a large spike

in your monthly payment. You may also

simply choose to move to a more stable

fixed-rate mortgage product.

• Shorten or lengthen the period of your

mortgage loan to better meet your

financial situation.

If you are in a position to do so, you

may want to shorten the length of

your loan and move into a 15- or

20-year to help pay your mortgage off

sooner and save money over the life of

the loan. On the flip side, if your income

has recently decreased you may want

to consider a longer term, which can

help to keep payments lower and more

manageable each month.

• Move from two mortgage loans to one.

Perhaps you had a piggyback loan

on your original mortgage and are

currently paying two separate loans.

If that’s the case and you have one or

both loans with high interest rates,

you may be able to refinance into one

loan at a substantial savings.

• Take advantage of HARP if you have a

Fannie Mae or Freddie Mac owned loan.

This program allows you to take

advantage of today’s market and

reduce your monthly payments

regardless of whether or not you are

underwater on your mortgage. This

program also has a much greater level

of flexibility to qualify.

• Move out of a loan that requires Private

Mortgage Insurance (PMI).

If you purchased your home with

a conventional home loan and

put down less than 20% you were

required to pay PMI which helps

protect your lender against default

on your loan. In order to remove this

insurance you can have your house

appraised to show that you have

reached 20% equity in your home but

the problem is that in most cases you

must pay PMI for a certain period of

time. Another way to remove the PMI

payment is by refinancing. If the value

of your home has increased and you

have greater than 20% equity in your

home when you refinance, you won’t

be required to pay PMI which could

mean even more savings.

totalmortgage.com | 877-868-2503 7

Knowing Your Goals3Just as you did when you first applied for

your mortgage, you’ll want to ensure that

you are well prepared for what will be

needed to complete your refinance. You’ll

need to do some of your own research to

determine if in fact a refinance is the right

move for you and your current financial

situation. There are several items you’ll want

to make sure you have covered:

• Check your current mortgage.

You simply should not pursue a

refinance without a complete under-

standing of your current mortgage.

You will need to determine if you

would be saving enough money to

warrant pursuing a refinance. For

instance if you plan to move in the

next year or two, it probably would

not make sense. Also, if you will face a

pre-payment penalty on your current

mortgage and are just a few years into

the loan you’ll want to understand

that penalty and factor that into your

decision to proceed.

• Review your credit report.

You will absolutely need to ensure

there are no errors or issues on your

credit report. With lending require-

ments tighter than they were in the

past, you won’t want to hold up your

loan as you try and get something

squared away that could have been

resolved before submitting your

application. Visit www.annualcred-

itrpoert.com for a free copy of your

credit report. If you do find any errors

or issues, address them immediately

and then move forward with your

application. Although programs exist

today for a variety of borrowers, the

better your credit score the more

options you’ll have available to you.

Refinance Checklist

• Check your current mortgage

• Review your credit score

• Take a look at outstanding debt

• Have funds to cover closing costs

• Contact lenders and compare

totalmortgage.com | 877-868-2503 8

• Take a look at your current

outstanding debt.

Take a look at all of your outstanding

debt. In many cases lenders will

review your debt to income ratio to

determine if it is too high. This may

impact your ability to qualify for

certain products and some of the best

rates. Lenders will typically review

both your front-end ratio, which is the

difference between your income and

the mortgage loan you are applying

for and the back-end ratio which

is the ratio between your monthly

income of all your debt , including

your mortgage loan. Typically lenders

like to see your front end ratio under

30% and the back end ratio, which

is typically more closely looked at,

lower than 40%. Keep in mind though

under the federal Home Affordable

Refinancing Program some of these

requirements have been eased.

• Verify you have funds to cover

closing costs.

Your closing costs will vary depending

on the fees you are being charged by

the bank, lender or broker you work

with. You should be aware of these

costs up front. Keep in mind, you’ll

also want to review how long it will

take you to recoup your closing costs

through your monthly savings and

factor that into your determination

to refinance. After all, if it will take

you a few years to recoup the closing

costs you’ll need to pay and if you are

considering a move in the next five

years, it may not be the best decision

to refinance at this time. However, if

you will recoup your closing costs in

two years and you plan to stay in the

home for at least a decade or longer,

then the cost savings over that period

of time will be significant and more

than likely would be a good move.

• Contact lenders and compare.

Just as you would for any large

purchase, it’s always a good idea to

shop around and compare. Even if

you are working with a particular

mortgage professional that you have

worked with in the past, call some

additional lenders and feel confident

that you are getting the best rate,

service, and product you possibly

can. You can contact us here at Total

Mortgage Services and we can assist

with any questions you may have

totalmortgage.com | 877-868-2503 9

and put you in contact with a loan

officer in your area. We can work with

you to evaluate your current financial

situation and make recommendations

specific to your needs.

Just be sure to watch out for and steer

clear of anyone that mentions additional

fees but does not clarify what they are

for. Also be aware of any hidden costs

that may be rolled into your loan. Always

be sure you completely understand

the quotes you are getting. If you have

questions, don’t be afraid to ask for clear

explanations.

Examining Your Options4As you begin to explore your product

options, think about what you are looking

for in a loan. Do you prefer the stability of

a fixed rate mortgage? Are you concerned

about a low credit score and qualifying for

a conventional loan? Do you plan to move

in the next five to ten years? Are you late on

your payments or owing a great deal more

than your home is actually worth? Consider

your specific financial situation and needs

when evaluating the different types of

available products. Here’s a closer look at

just some of the programs you’ll find when

you look to refinance.

Fixed rate options:

As the name implies, a fixed-rate mortgage

product is one where the interest rate is

stable throughout the life of the loan. These

loans are among the most popular and are

typically offered in 30-year, 20-year and

15-year options. Some fixed –rate programs

also allow a cash-out option so you can pull

equity out of your home. There are a number

of benefits to each of these programs.

• A 30-year option may be ideal if you

plan to stay in your home for a long

period of time, prefer the stability of

a fixed rate and have a good credit

score and enough equity in your

home to avoid PMI. Your payments

may be lower as you are stretching

out the costs over a long period of

time. The downside of this is that

you will end up paying more interest

on the loan as it stretches out over

30-years.

• A 20-year fixed-rate option offers

similar benefits to a 30-year but for a

shorter period of time. Typically you’ll

see a better interest rate on a 20-year

as well and will have the ability to pay

totalmortgage.com | 877-868-2503 10

your loan off sooner, cutting down

on the amount of interest you’ll pay

over the life of the loan. Of course

since you are paying this loan off in

20-years you will see slightly higher

monthly payments than you would

with a 30-year option.

• A 15-year fixed-rate option will

allow you to pay your loan off in the

shortest period of time saving you a

substantial amount on interest over

the course of the loan. You may also

be able to secure the best rate for a

15-year loan and you will build equity

much more quickly, however, your

payments will be much higher since

you are opting to pay your loan off in

a shorter period of time.

• You may find some lenders also offer

ten-year fixed options and variations

of the above programs where you

pay the interest upfront on your

mortgage loan for a fixed period

of time and then the principal over

the remaining life of the loan. These

loans are known as interest-only

options. While not for everyone, they

may better meet your needs if you

expect your income to increase, are

looking for low monthly payments,

and don’t plan to be in your home

for a long period of time. For

example, a 30-year interest-only

fixed-rate allows you to only pay

interest upfront for the first ten

years. After that initial ten-year

period is up you will then need to pay

down the principal in just 20 years.

IF you plan to move in less than ten

years, you’d never even start paying

the principal. You should be clear

that you understand the advantages

and disadvantages of these types of

loans as they differ a great deal from

a traditional fixed-rate loan.

• An adjustable rate mortgage,

referred to as an ARM, offers a low

starter rate for a fixed period of time.

Once that period of time expires, the

ARM will readjust to a fully indexed

rate, which could be much higher

than your start rate. This could mean

your payments would increase at

that time. These refinance loans are

typically offered in a 30-year terms

and offer initial low, fixed starter rates

for 5, 7 or 10 years.

There are clear advantages to an ARM

for some types of borrowers. First, the

introductory rates are typically lower

totalmortgage.com | 877-868-2503 11

than those for fixed-rate options. So,

your initial payments may be lower.

This type of loan is also ideal for a

borrower that may only plan to be

in a home for a short time and plans

to leave before the ARM adjusts to

a higher rate. ARMs are also a good

option if you expect your income

to rise over time and want lower

payments to begin paying back your

loan. Keep in mind, there are inherent

risks with these types of loans.

Although you may plan to move

before the ARM adjusts your plans

may change or you may not be able

to sell your home in the timeframe

you imagined. Interest rates may rise

dramatically, impacting the rate your

ARM adjusts to and you could see

a tremendous spike in your actual

payment. You also may not see the

increase in salary that you thought

you might, which could make it

more difficult to keep up with higher

payments once your ARM adjusts.

Government options:

There are quite a few government

programs you may want to look into when

refinancing. Some of these programs have

less strict qualifications and are designed

to help the borrowers successfully manage

their mortgage.

• FHA

There are numerous refinance

programs available through the

FHA (Federal Housing Administra-

tion) from fixed rates to streamlined

programs designed specifically for

those holding a current FHA loan.

Even if you hold a conventional

mortgage an FHA refinance may

make sense as they typically have

less stringent qualifications.

• Fixed options

Similar to conventional fixed-rate

options, you can obtain an FHA fixed

rate loan in a 30-year or 15-year

option. The same benefits would

apply as a conventional fixed-rate—

the stability of a consistent rate over

the course of a loan. Also, credit

requirements may be less stringent if

you are concerned about qualifying

Consider your specific financial situation

and needs when evaluating the different

types of available products.

totalmortgage.com | 877-868-2503 12

under conventional guidelines.

The downside may be that FHA

does require mortgage insurance

if you do not have greater than

20% equity in your home so you’ll

need to factor that into your total

monthly payments and you will need

to go through the complete loan

application process if you are moving

from a conventional to an FHA.

• Streamline Refinance

The FHA Streamline Refinance may

be an excellent option if you have a

current FHA loan in good standing

and are looking for a quick refinance

program that can lower your interest

rate ad payment without the need for

an appraisal. This program typically has

much less stringent guidelines as it’s

only open to those that have already

been approved and gone through

the FHA qualification process when

obtaining their original home loan.

However, there is no cash–out option

with the FHA streamline program.

• VA

If you currently hold a VA Loan or are

eligible to move to one, there are also

several available refinance options

• Cash-out VA refinance

This program is designed to help you

tap into the equity in your home.

Perhaps your property has increased

in value since your purchase and

you’d like to take some of the equity

to help pay off other bills. This loan

will allow you to access up to 90% of

your home’s current value.

• Rate-Term Refinance

A rate-term refinance is for an eligible

borrower that may be currently in

a conventional or ARM that wishes

to move to a VA loan. This program

offers the ability to finance up to

100% of the property’s value and

never requires mortgage insurance.

This is a fixed- rate loan and provides

the same level of stability as other

fixed- rate products. This can

ultimately help a borrower save on

monthly payments while incurring

very minimal out-of pocket expenses.

• Interest Rate Reduction Refinance

Loan (IRRRL)

This is a streamlined program for

those borrowers currently in a VA

loan. It is designed to help lower

interest rates, change the overall

terms of the loan such as moving

totalmortgage.com | 877-868-2503 13

from an ARM to a fixed-rate. There

are typically no out-of-pocket

expenses and no appraisals are

required. Another great benefit of

this program is that documenta-

tion requirements are eased and

processing is usually quick.

Home Affordable Refinance

Program (HARP)

As part of the Making Homes Affordable

Program, borrowers that hold a Fannie Mae

or Freddie Mac home loan that are unable

to refinance under conventional methods

or are underwater on their mortgage can

take advantage of the HARP program. This

program has number of requirements so

you should be sure to check with your

lender, however overall it is designed to

help borrowers refinance to obtain lower

interest rates and reduce their payments.

If you are unsure if your loan is currently

held by Fannie Mae or Freddie Mac, you can

check here.

These are just some of the many programs

available to you. It’s best to contact a loan

officer to review your personal situation

and explore the best product to meet your

particular needs.

Housing Facts • Commuting costs continue to factor

strongly in decisions regarding location,

with 73% of buyers saying transportation

costs were important.

• Home buyers think the most important

services agents provide are helping find

the right house, and negotiating price and

sales terms.

totalmortgage.com | 877-868-2503 14

Working With an Expert5As you begin to determine that a refinance

makes sense and you start to narrow down

the products that best fit your needs, you’ll

want to begin working with a lender and

more specifically with a loan officer that you

can trust. As a refinance loan is a significant

financial decision, you should seek an

experienced, licensed loan officer who can

help you make the best decision for your

individual needs. You should have a level

of comfort with your loan officer as well as

the lending institution they represent. Your

loan officer must have the ability to provide

sound advice and successfully guide you

down the refinancing path.

If you’ve worked with someone in the

past you may want to start there. If it’s

been some time since you worked with a

loan officer, ask around for referrals from

friends and family. Our mortgage lending

professionals here at Total Mortgage

Services are always available to assist with

your needs as well. Our loan officers are

licensed, experienced, and looking to build

long-term relationships with each of their

clients. They have worked with borrowers

with a wide range of financial situations and

are extremely knowledgeable regarding

the variety of refinance programs available

today. You can feel confident they will be

able to guide you down the right path.

Still, don’t hesitate to contact several

different loan officers and interview them

for the job. This is one of the biggest

financial decisions of a lifetime for most

people, and you want the best. Don’t settle

for someone you are not comfortable with.

Here are some questions you may want

to consider when speaking with a lending

professional.

• Are you licensed?

Mortgage loan officers in all

states must be licensed. You may

verify licensing at the consumer

Nationwide Mortgage Licensing

System (NMLS) site at http://www.

nmlsconsumeraccess.org.

• How long have you been in business

Given the complexities of today’s

home financing requirements and

the myriad of programs available,

your best bet is to look for someone

well versed in dealing with a variety

of financial situations.

totalmortgage.com | 877-868-2503 15

• Do you have a former client

I may contact?

Reach out to former clients the loan

officer has worked with and ask them

how they liked working with that

particular individual. What were their

strengths and weaknesses? No one

is perfect but you’ll want to start out

on the right foot and know you are

working with someone that comes

highly recommended.

• Do you have referral partners that

may be able to help me with other

aspects of my financing (real estate

attorney, accountant, etc.)?

An experienced loan officer should

have a number of local profession-

al referral partners they work with

and recommend. This will assist

you in the process of refinancing

your loan should you need a real

estate attorney or accountant to ask

questions or assist with the process.

• Why should I choose to work

with you?

Although this may seem general, it’s

a great question to really understand

why a particular individual wants

your business. Are they just looking

to close a quick refinance, collect

their commission and move on,

or are they more focused in on

expanding their customer base,

building a relationship and working

with you for the long haul? Do they

talk about guiding you through your

mortgage refinance now and also

helping you in the future? Do you

believe they want to earn your trust

and business for a lifetime? That’s

the kind of loan officer you’ll want to

work with.

• What is your availability like?

Make sure you clearly understand

your loan officer’s availability from the

get go. If they work afternoons and

evenings and your free time is only in

the morning, it may not be the best fit.

Understanding these hurdles early on

will save you time and headaches later

on in the process.

• How would you describe your level

of service?

Get an overall feel for how they

view their own level of customer

service. As they answer this question

you should be able to tell just how

important keeping their customers

happy really is to them. Do you get

the impression they’ll work above

totalmortgage.com | 877-868-2503 16

and beyond for you? You should.

• How frequently will you update me

throughout the refinance process?

Gain an understanding on how

frequently the loan officer plans to

update you on your refinance. You’ll

want to make sure their responses

are clearly aligned with your desire

for updates. You’ll also want to cover

your preferred method of contact

and ensure your loan officer can relay

messages to you in the manner you’d

like. It’s not uncommon these days

to find customers preferring texts or

emails over phone calls.

You may recall what closing day was like

with your original home loan and with a

refinance it may not be very different. In

some cases, you will meet at the closing

agent or attorney’s office, however this may

vary. In other cases your attorney will work

with the closing agent to arrange signing

of all documentation without a formal

meeting. Regardless of the location of your

closing, the process will remain the same.

You will be required to:

Getting Through Closing6

• Carefully review and sign all

loan documents.

You should make sure all documents

you are signing reflect exactly the

loan terms, payments and information

you previously discussed with your

loan officer. If something is not correct

you should not sign and bring it to

your attorney’s attention immediately.

• Provide a certified or cashier’s

check to cover all closing costs.

You will need to obtain a certified or

cashier’s check; this cannot typically

be a personal check.

• Set up an escrow account, as

applicable, if you will be paying

your homeowner’s insurance and

taxes with your mortgage payment.

Your attorney should handle this

for you.

• Provide proof of homeowner’s

insurance

If something is not correct you should

not sign and bring it to your attorney’s

attention immediately.

totalmortgage.com | 877-868-2503 17

At the closing you will also receive copies of

and will need to sign the following:

• HUD-1 Settlement Statement

This is a line-by-line itemization of

your total closing costs.

• Deed of Trust or Mortgage

This documentation details the lien

on your property as security if you

should default on the loan.

• The Promissory Note

This is a document declaring your

agreement to all of the terms of

the loan, including your promise to

pay your mortgage payments on

time, in full and to the proper party

throughout the life of the loan.

Your attorney should guide you through

this process on closing day and explain each

and every document you are signing. Be

sure to address any questions or anything

you don’t understand immediately.

PathRefinancing

The That’s it! You have completed the TotalPath

to Refinancing. You have a made an

important step on another path—the one

that leads to the American Dream!

Managing Your Mortgage7

Once your refinance has been completed

and you have closed the loan, periodically

check in with your loan officer. It’s usually

best to plan a yearly mortgage review.

This is a good opportunity to verify that

the mortgage you are currently in remains

the right fit for your particular financial

needs. Just as a refinance may have been

right for you now, in the future your needs

may change and you may find your goals

have changed as well. Perhaps you’ll need

to tap into some equity in your home and

refinance again or you’ll decide to move

and will need to shop for a new mortgage.

Regardless of the situation, reviewing your

mortgage and how it fits your current

financial situation makes smart financial

sense and should be a commitment you

make sure to keep each year.

Related Documents