Realizing the Development Promise of the Doha Agenda 2004 Global Economic Prospects Global Economic Prospects 2004 Global Economic Prospects 2004 Realizing the Development Promise of the Doha Agenda

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Realizing the Development Promise of the Doha Agenda 2004

Global Economic Prospects

Global Economic Prospects

2004G

lobal Econom

ic Prospects2004

ISBN 0-8213-5582-1

THE WORLD BANK

Realizing the Development Promise of the Doha Agenda

The World Trade Organization(WTO) round of trade negotiations

initiated in November 2001 inDoha, Qatar, was intended to be a“development round.”Those good

intentions are now being tested.Trade ministers from all over the

world are discussing ways to reducetrade barriers—barriers that greatly

harm development and povertyreduction. Global Economic Prospects

2004 explores the tough issuesunder discussion—protection of

agriculture, trade in labor-intensivemanufactures, labor services, andspecial treatment for developing

countries, among others—to presentoptions that would indeed reduce

poverty and advance development.The global talks will not be easy and

may take time, but allowing poorpeople greater access to world

markets will offer them new opportunities to improve their living

standards. If agreements are to begenuinely pro-development, thesediscussions must be informed byclear analysis of measures that arelikely to benefit poor people themost.That is the purpose of this

Global Economic Prospects.

—Nicholas SternSenior Vice President and

Chief Economist

The Doha Development Agenda of the Fourth MinisterialConference of the WTO opened many contentious andimportant questions. Global Economic Prospects 2004:

Realizing the Development Promise of the Doha Agenda analyzes themost critical multilateral trade issues and suggests policy options that would raise living standards in developing countries and reduce global poverty.

The fourteenth annual edition of Global Economic Prospects

• explores the short-, medium-, and long-term outlook for the global economy, including driving forces, commodity prices,and capital flows, and their implications for major regions

• reviews recent trends in exports from developing countries,trade barriers that work to the disadvantage of poor people,and policies to reduce protection and other inequities in theworld trading system

• examines trade in agriculture—the most important and politicallycontentious sector for global poverty reduction—including keylessons from development experience, possible changes to the current system of subsidies and protection, and the potential for liberalization in both rich and poor countries

• investigates the temporary movement of labor—so-called Mode 4 of the General Agreement on Trade in Services—evaluating its advantages and disadvantages to both the home and the host countries

• discusses trade facilitation in light of post-9/11 concerns for security to suggest new policies that would promote greater and more-secure trade

• reviews the special treatment of developing countries in the world trading system and the role of trade preferences,exemptions from WTO rules, and technical assistance to implement WTO trade regulations.

Global Economic Prospects 2004 provides essential information forthose concerned with developments shaping today’s global economy.

GlobalEconomicProspects

Realizing the Development Promiseof the Doha Agenda

2004

© 2003 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433Telephone 202-473-1000Internet www.worldbank.orgE-mail [email protected]

All rights reserved.

1 2 3 4 04 03

This volume is a product of the staff of the World Bank. The findings, interpretations, andconclusions expressed herein do not necessarily reflect the views of the Board of ExecutiveDirectors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. Theboundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of the World Bank concerning the legal status of anyterritory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this work is copyrighted. Copying and/or transmitting portions or all of thiswork without permission may be a violation of applicable law. The World Bank encouragesdissemination of its work and will normally grant permission promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive,Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, e-mail [email protected].

ISBN 0-8213-5582-1 ISSN 1014-8906

Cover photo credit: AFP/CORBIS.

Workers at the Los Ausoles coffee plantation in Ahuachapan, El Salvador, clean coffee beans,August 14, 2002.

iii

Foreword ix

Acknowledgments xi

Overview xiii

Abbreviations and Data Notes xxxi

Chapter 1 Global Outlook and the Developing Countries 1The industrial countries: Deficits, confidence, capital spending, and the dollar 4The external environment for developing countries: Gradual improvement, but a

bumpy road ahead 19The developing countries: Back on track toward growth? 28Trade, growth, and poverty in developing countries 38Looking ahead to the Doha Round 47Annex 1 Historical trade dynamics for developing countries 55Notes 59References 60

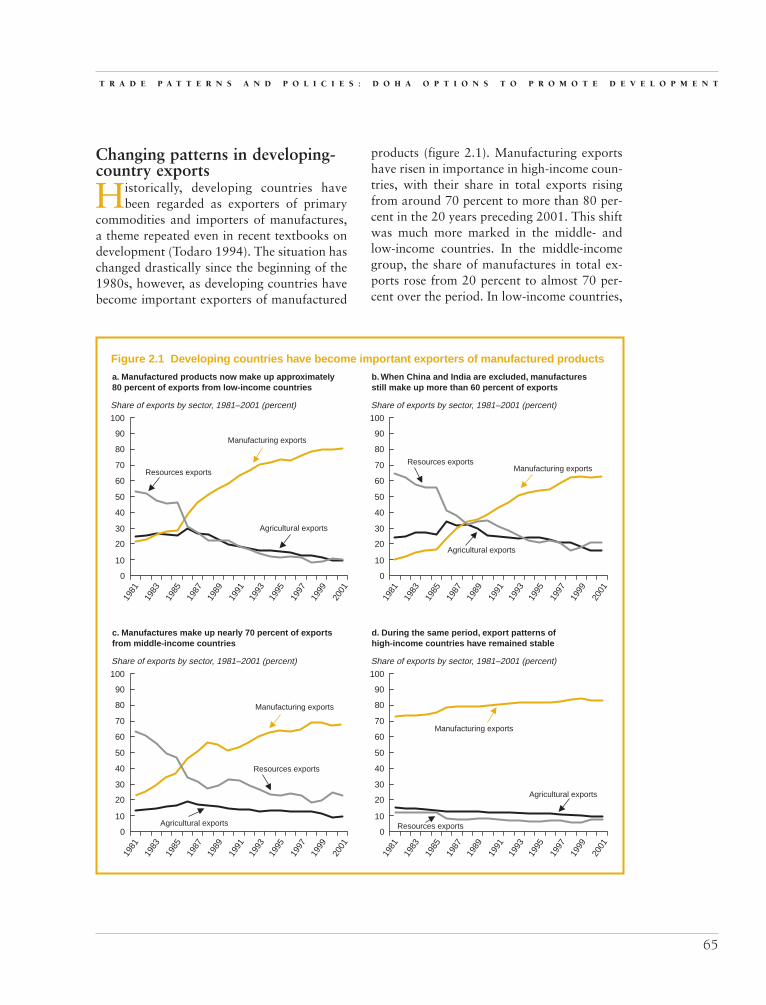

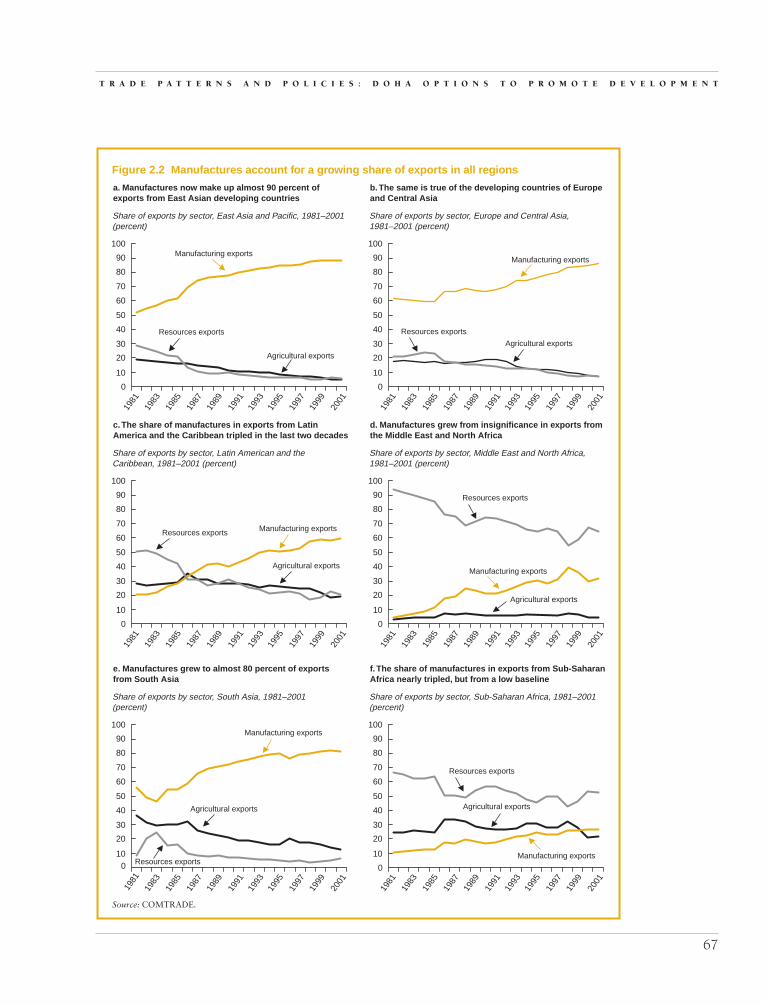

Chapter 2 Trade Patterns and Policies: Doha Options to Promote Development 63Changing patterns in developing-country exports 65Behind the patterns: Economic and policy determinants 73Market access for development: The agenda 78From Doha to Cancún and beyond: How should protection be reduced? 88Notes 98References 98

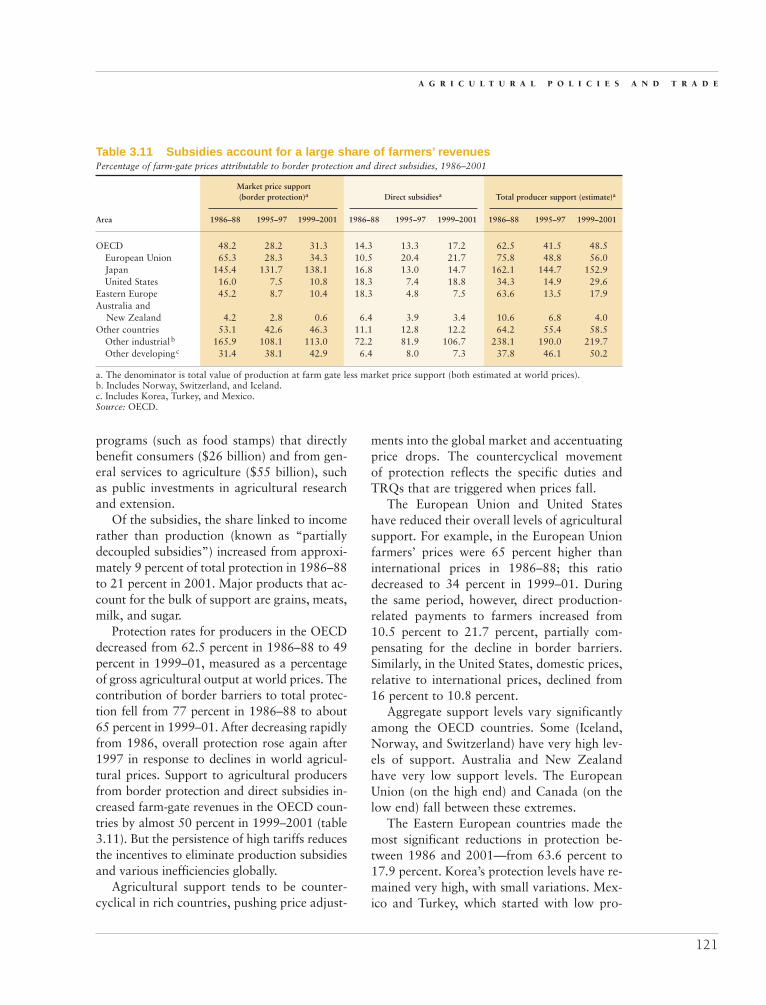

Chapter 3 Agricultural Policies and Trade 103Poverty, rural households, and trade in agriculture 105Trade and export growth in agriculture 109Global agricultural protection: The bias against development 114Proposals for reforms in the Doha Round 131Notes 138References 139

Contents

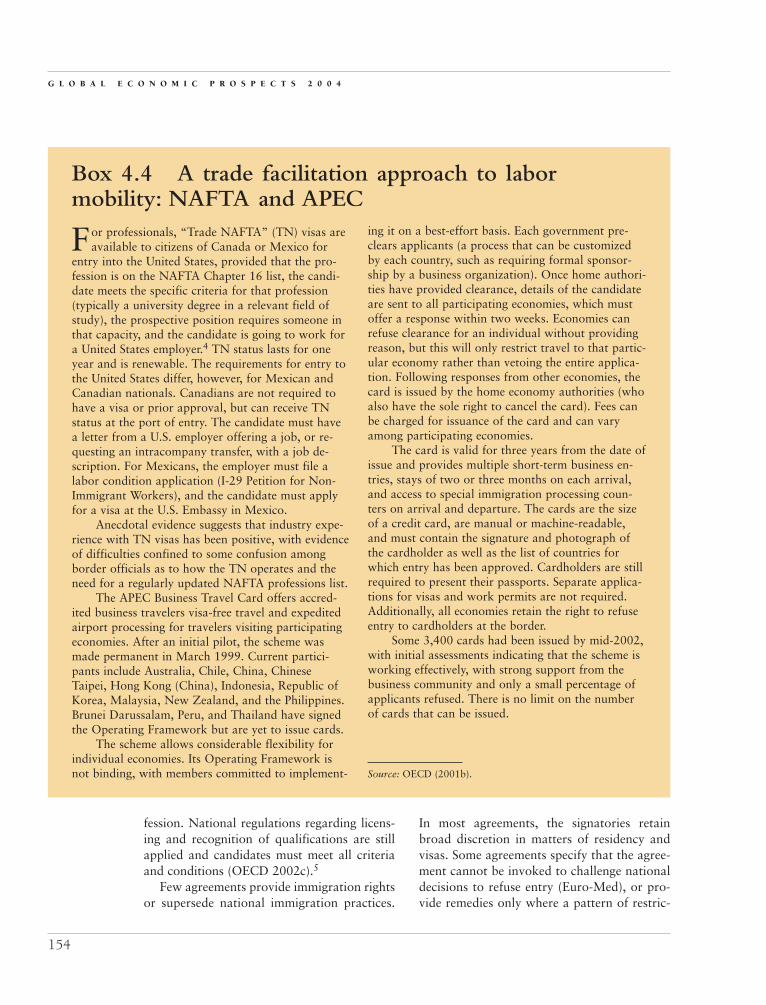

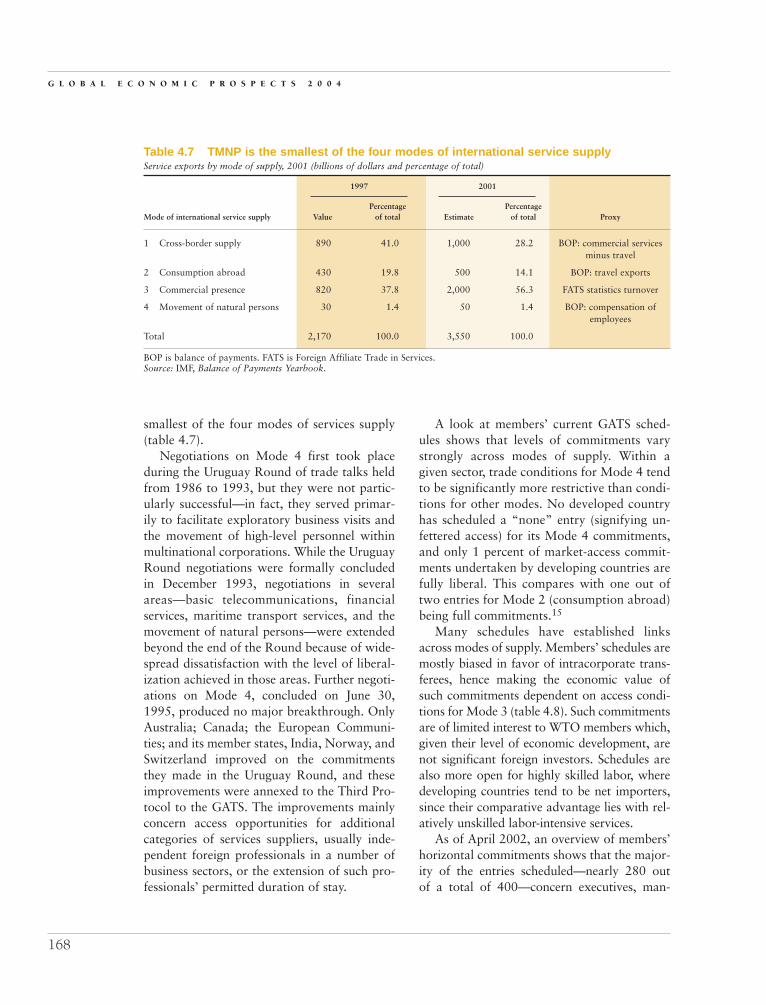

Chapter 4 Labor Mobility and the WTO: Liberalizing Temporary Movement 143The bigger picture: Global migration and remittance trends 145Temporary movement of workers 150Bilateral and regional approaches to labor mobility 152Understanding the impact of temporary foreign workers 155Mode 4 and the WTO 166Notes 172References 174

Chapter 5 Reducing Trading Costs in a New Era of Security 179Why transport, trade facilitation, and logistics matter 181The new international security dimension in trade 182The anticompetitive effects of international transport regulations 188Trade facilitation 191Trade facilitation and the WTO agenda 195Lowering transport costs, increasing security, and facilitating trade 198Notes 200References 202

Chapter 6 Development and the Doha Agenda 205Special and differential treatment and the WTO 207Market access for development 208Toward a new regime for WTO rules 220Putting development into the Doha agenda 227Notes 228References 229

Appendix 1 Regional Economic Prospects 233

Appendix 2 Global Commodity Price Prospects 257

Appendix 3 Global Economic Indicators 279

Figures1.1 Growth in the OECD countries falters 41.2 OECD manufacturing shows a distinct “double dip” 51.3 Consumer confidence recovers from pre-war lows 61.4 The drop in U.S. household net worth has been offset by real estate appreciation 81.5 Capital spending has been hesitant in all industrial countries 91.6 Corporate profits have risen moderately in the United States and Japan 91.7 Business confidence remains poor, but better in the United States than in Europe 101.8 The U.S. fiscal deficit is widening quickly 111.9a The U.S. current account deficit is at record levels 111.9b The U.S. current account deficit is at record levels 131.10 Market interest rates have dropped 141.11 Is deflation a danger for Europe and the United States? 15

G L O B A L E C O N O M I C P R O S P E C T S

iv

1.12 Output gaps are widening, bringing deflationary pressures to bear 161.13 The dollar has fallen sharply since early 2002 161.14 OECD recovery begins in the United States 181.15 OECD-area imports have declined sharply since April 2000 211.16 China’s share of East Asian exports keeps rising 211.17 The price of oil fell sharply before the war in Iraq 231.18 Agricultural prices have begun to decline as crop prospects improve 251.19 Emerging-market spreads rallied sharply after late 2002 261.20 Bond issuance dominates capital market flows in 2003 271.21a Regional trends in industrial production are mixed 29121b Inflation is moderating in the developing world 291.21c Major currencies in Latin America and East Asia are firming up 301.22 Developing countries are on track toward long-term growth 311.23 Growth rates in developing countries will rise through 2005 311.24 Before the SARS outbreak, East Asian GDP was growing robustly 321.25 Argentina, Brazil, and Chile see strong upturn in production 331.26 Growth will cool in CIS while picking up in Central and Eastern Europe 341.27 Middle East oil production has increased to prevent shortages 351.28 Indian production of food and automobiles recovered sharply in early 2003 371.29 Growth in Africa is expected to improve modestly 381.30 Income elasticity has risen globally, but particularly in the developing world 401.31 Export-to-GDP ratios have risen sharply in developing countries 411.32 Productivity will contribute more to GDP growth through 2015 than will capital or

labor 441.33 The pro-poor reform scenario promises substantial income gains 501.34 Exports should rise sharply 521.35 Millions of people would be moved out of poverty 521.36 Gains for most, but adjustment costs for some 531.37 Significant shifts in global output patterns 542.1 Developing countries have become important exporters of manufactured

products 652.2 Manufactures account for a growing share of exports in all regions 672.3 Technology-laden manufactures have increased as a share of exports from each group

of countries, while the share of resource-based exports has diminished 702.4 Global production sharing is increasingly important for China and India 712.5 Soaring exports from China and India had only a moderate effect on China’s and

India’s terms of trade 722.6 Many developing countries face an adjustment when quotas are lifted 802.7 Antidumping barriers by sector and by country group 883.1 Countries that produce more cash crops also produce more food 1093.2 Import growth rates of nontraditional export commodities decreased in industrial

countries but increased in developing countries 1123.3 Developing countries’ exports of nontraditional products have surged, but industrial

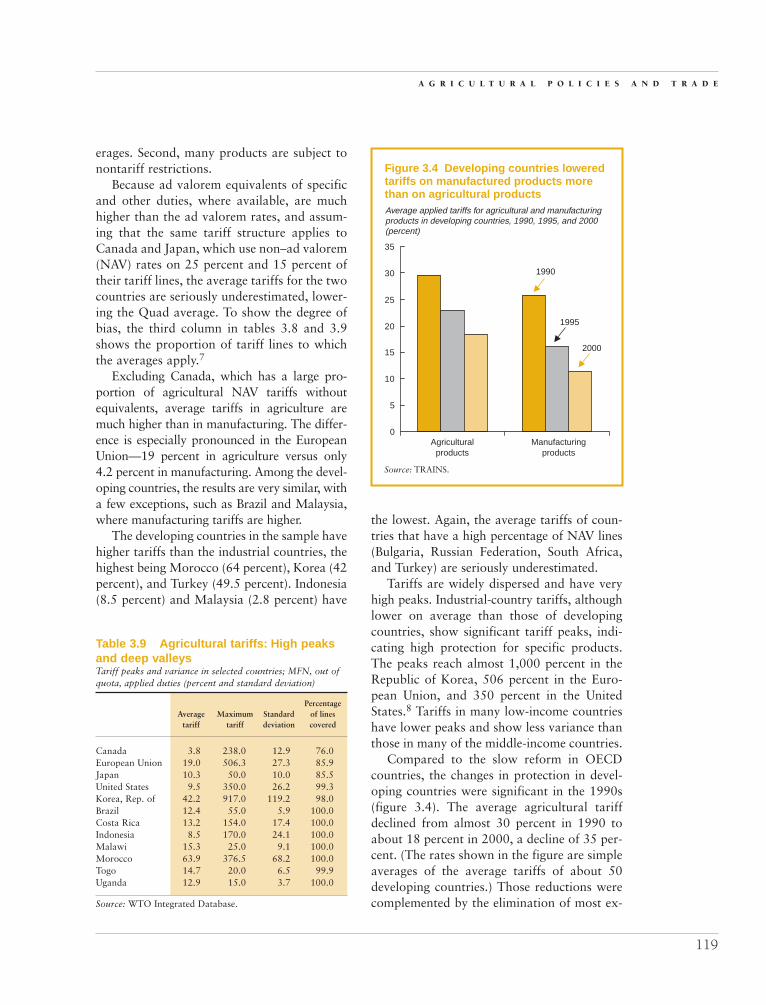

countries’ exports have changed little 1143.4 Developing countries lowered tariffs on manufactured products more than on

agricultural products 119

C O N T E N T S

v

3.5 Rich countries use non–ad valorem tariffs more often than do developingcountries 122

3.6 Throughout the world, tariff rates escalate with degree of processing 1233.7 The proportion of tariff lines containing non–ad valorem duties increases with degree

of processing 1253.8 Tariff rate quotas protect a substantial portion of output in many industrial

countries 1263.9 High protection of sugar and wheat has increased domestic production and reduced

net imports 1284.1 Workers’ remittances are an important source of income for many developing

countries 1495.1 Customs clearance takes longer in the developing world than in the OECD,

lowering the competitiveness of developing-country trade 1855.2 Higher trade costs reduce global welfare 1865.3 Facilitating trade in less-efficient countries would bring significant gains 1945.4 The impact of individual trade-facilitation measures differs significantly from region

to region 1955.5 Domestic reforms alone would produce many of the same gains as global

reform 1966.1 The benefits of U.S. trade preferences are distributed unequally 2116.2 Countries “graduating” from U.S. generalized system of preferences have better export

performance than those still in program 2126.3 Preferences have not increased the share of the least developed countries in imports

into the European Union and the United States 2156.4 Market shares of countries eligible for three U.S. “deep preference” programs have not

increased 2156.5 Preferred countries’ apparel exports to the United States have risen 2166.6 Agricultural exports from Mexico and Spain rose dramatically after the two countries

joined regional trade blocs 2176.7 The trade policies of countries in the U.S. generalized system of preferences are more

protectionist than those of countries not in the program 2186.8 Countries enjoying preferences have increased their exports of apparel to the

United States 219

Tables1.1 Global growth should accelerate, but risks persist 31.2 Weak fundamentals underlie sluggish growth in the rich countries 51.3 The difficult environment for developing-country growth should improve 201.4 Developing countries’ exports will grow faster than those of the high-income

countries 221.5 GDP per capita will grow faster in the developing world than in the OECD area 431.6 Global poverty will decrease significantly, but not uniformly across regions 461.7 Tariffs could be cut clearly and simply 481.8 The pro-poor tariff scenario would significantly lower protection 491.9 A large share of real income gains comes from lowering of barriers in agriculture and

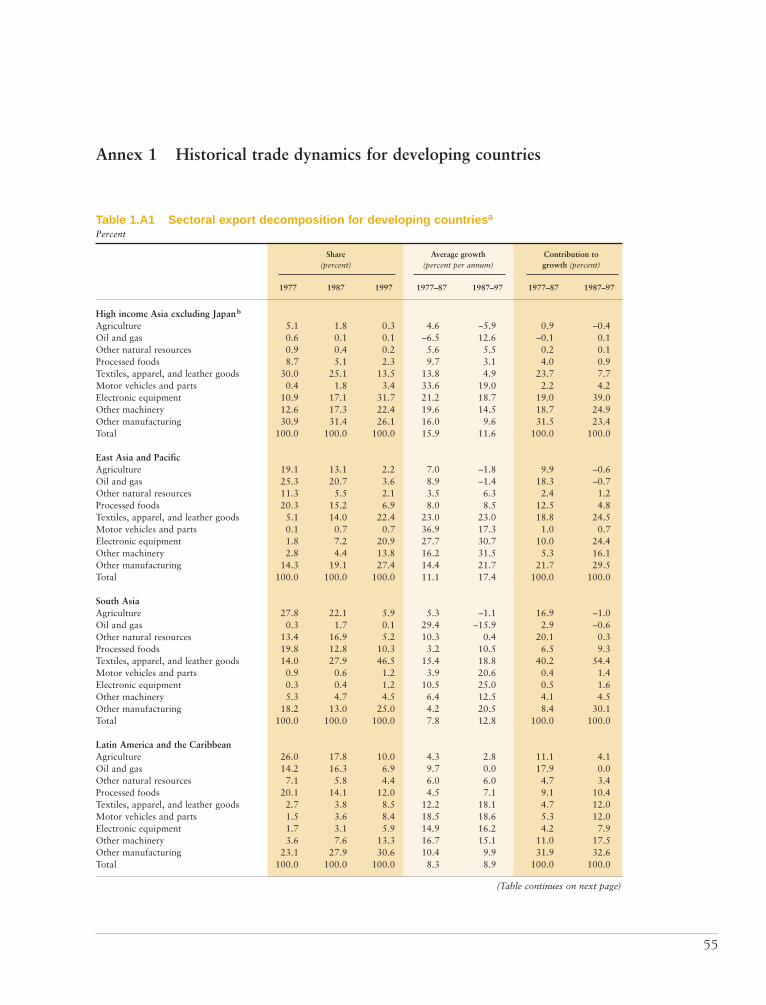

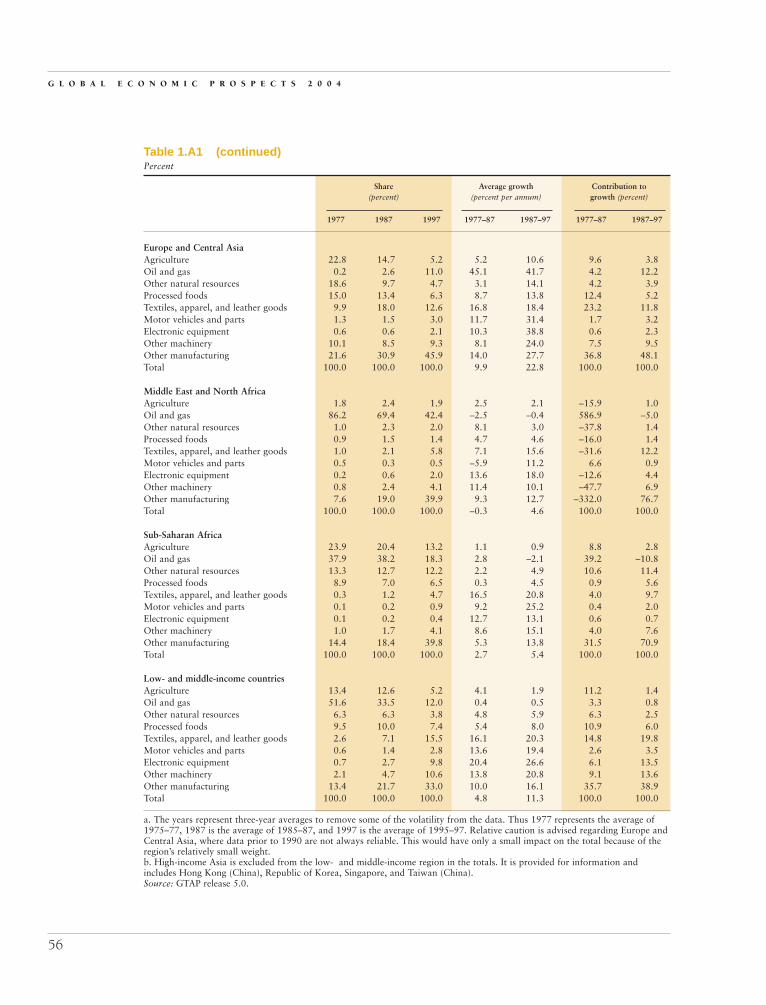

food 511.A1 Sectoral export decomposition for developing countries 55

G L O B A L E C O N O M I C P R O S P E C T S

vi

1.A2 Regional export decomposition for developing countries 572.1 Developing countries are becoming exporters of high-value products 682.2 Developing countries’ exports became more competitive in the 1990s 742.3 Investment in people and in capital grew rapidly 752.4 Tariffs hurt exports—but less so in the 1990s than in the 1980s 772.5 Quota abolition in China will move resources from other activities to textiles

and clothing 812.6 Industrial countries levy higher tariffs on imports from developing countries than from

other industrial countries—and some regions have high tariff walls 822.7 Developing countries pay large amounts in tariffs to their neighbors 832.8 Most antidumping actions are filed by developing countries against other developing

countries 862.9 Antidumping rates are much higher than tariff rates 862.10 Antidumping duties are high 872.11 Competing formulas make a big difference for tariffs 952A.1 The various liberalization proposals have very different features 973.1 Most of the world’s poor live in rural areas outside the least developed countries

1063.2 Rural poverty is higher in poorer countries 1073.3 Even in subsistence economies, cash is important 1073.4 U.S. farmers earn less from farming than from other sources 1073.5 Manufacturing exports grew much faster than agricultural exports 1103.6 South-South exports in agriculture are rising as South-North export shares fall 1103.7 Developing countries have shared unequally in export market gains 1173.8 Agricultural tariffs are higher than manufacturing tariffs in both rich and poor

countries 1183.9 Agricultural tariffs: High peaks and deep valleys 1193.10 Most subsidies go to producers—and come from border protection 1203.11 Subsidies account for a large share of farmers’ revenues 1213.12 Specific tariffs are higher than ad valorem rates 1233.13 Tariffs rise with level of processing 1243.14 The Harbinson proposals could greatly reduce applied tariffs in the European Union

and the United States 1333.15 The Harbinson proposals would not significantly reduce protection in the developing

world—if reductions were taken from bound rates 1333.16 U.S. trade preferences—a plethora of programs 1364.1 Migration is rising in many OECD countries 1474.2 Workers’ remittances are the second-largest source of external funding for developing

countries 1484.3 Remittances are a significant source of income in all regions of the developing

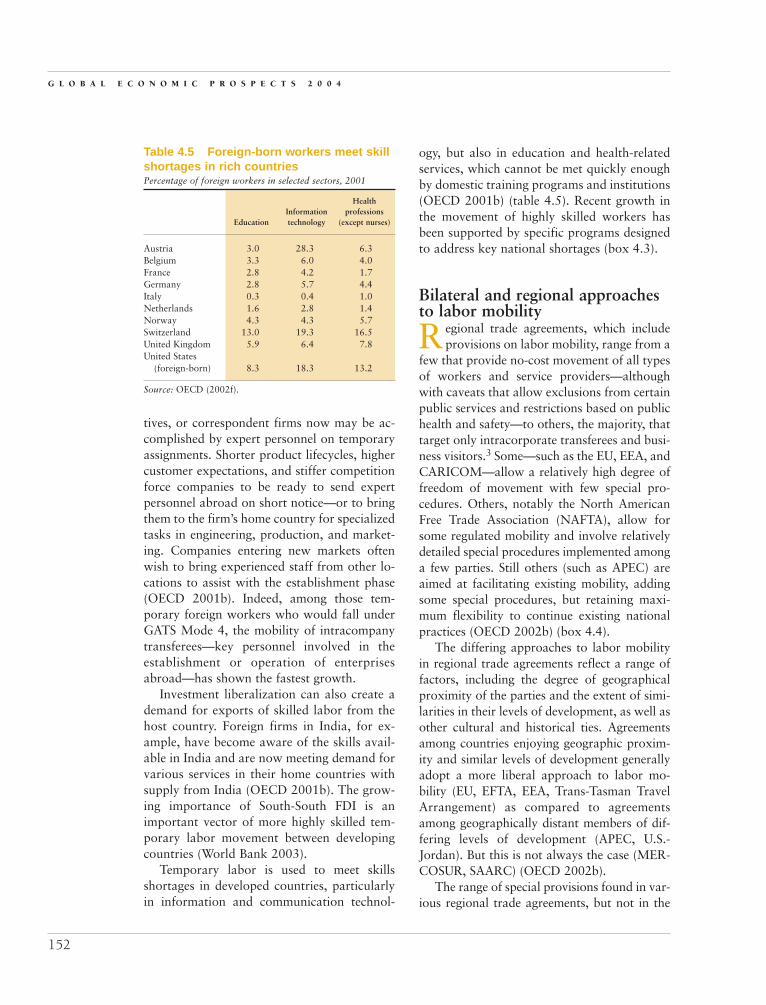

world 1494.4 Temporary movement is rising in rich countries 1504.5 Foreign-born workers meet skill shortages in rich countries 1524.6 The distribution of costs and benefits associated with Mode 4 trade 1574.7 TMNP is the smallest of the four modes of international service supply 1684.8 Most Mode 4 commitments by WTO members are in management categories 169

C O N T E N T S

vii

5.1 Elimination of anticompetitive private practices can cut costs drastically 1906.1 Developing countries rarely receive significant preferences in sectors in which they

would have a comparative advantage 2096.2 Utilization rates for preference-eligible products with high MFN tariffs are low 2106.3 Actual use of preference programs is declining 211

Boxes1.1 Consumer confidence and U.S. private consumption 71.2 Financing the U.S. current account deficit: From equity to debt 121.3 OPEC struggles to achieve higher prices amid growing supply competition 241.4 Economic effects of Severe Acute Respiratory Syndrome (SARS) 331.5 AIDS is taking a rising toll in Sub-Saharan Africa 392.1 Poor export performance in 43 countries 692.2 Swimming upstream: The case of Vietnamese catfish 852.3 The scourge of the specific 892.4 “Average cuts,” the cut you have when you’re not having a cut 922.5 The implications of five tariff-cutting proposals 933.1 The impact of national trade integration and reform on poverty 1063.2 Did agricultural exports slow down solely because of falling prices? 1113.3 Decomposing export growth in manufacturing 1133.4 Food safety standards: From barriers to opportunities 1153.5 Decoupling agricultural support from production decisions 1273.6 Fewer subsidies, stronger agricultural sector 1323.7 The potential impact of real preferences 1343.8 Rules of origin in preferential schemes are complicated—and often

contradictory 1363.9 Food aid principles 1374.1 Population aging and migration 1464.2 Temporary labor movement and the East Asian crisis of 1997–98 1514.3 Recent initiatives to facilitate temporary movement of highly skilled workers 1534.4 A trade facilitation approach to labor mobility: NAFTA and APEC 1544.5 Initiatives to encourage return migration 1604.6 Wages and conditions 1634.7 E-commerce and temporary movement 1644.8 Boosting intra-EU labor mobility 1654.9 Measuring Mode 4 is still imprecise 1674.10 Key impediments to Mode 4 trade 1694.11 Elements of a possible GATS visa/permit regime 1715.1 The evolving definition of trade facilitation 1815.2 The logistics needs of a German car part manufacturer in Tunisia 1925.3 Tackling corruption in customs: Peru 1975.4 Customs reform in Lebanon 1986.1 EU and U.S. preference programs 2136.2 Major WTO provisions allowing developing countries greater freedom to use

restrictive trade policies 2216.3 A “development box” for the Agreement on Agriculture? 223

G L O B A L E C O N O M I C P R O S P E C T S

viii

The international community finds itself at a crossroads as it goes into the last quar-ter of 2003. Will the Doha Agenda regenerate the multilateral consensus that has been thehallmark of successive rounds of trade liberalization since 1947 and in doing so provide

new impetus for global integration? Or will the Doha Agenda collapse in stalemate and perhapsbe viewed as the moment when the international community retreated from multilateralism andopened the floodgates for less desirable bilateral and regional arrangements?

The answers to these questions matter a great deal to the world’s poor. The round of tradetalks launched in November 2001 in Doha, Qatar, is the first negotiation focused primarily on is-sues of concern to developing countries, and the first trade round since the birth of the WorldTrade Organization (WTO). Moreover, the Doha round is the first trade round for many newWTO members, including the world largest developing economy, China. Consequently, the roundhas the opportunity to remove many of the inequities in the global trading system that put de-veloping countries—and poor people in particular—at a disadvantage in their trade.

Three trade barriers are of particular concern. Poor people work in agriculture, and agricul-tural products are subject to the highest barriers to trade. In addition, poor people produce labor-intensive manufactures, which are subject to peak tariffs in a world that has already reducedaverage tariffs in manufactures to historic lows. Poor people could benefit from greater tempo-rary migration.

Governments everywhere have worked hard to create the opportunity to reduce these andother barriers. And they will have to work hard to capitalize on that opportunity. To fulfill thedevelopment promise of the Doha Agenda, rich countries will have to reduce protection of their(relatively wealthy) farmers. Their tariff walls and huge subsidies depress global prices of theproducts that poor farmers produce throughout the developing world. These subsidies cost theaverage working family in the European Union, Japan, and the United States more than $1,000a year. Middle-income countries, though their protection is generally lower and less distorting inagriculture, have high average tariffs in all sectors, and are more restrictive in services. As south-south trade increases in importance, protection of sectors in middle-income countries underminestheir poorer trading partners and often undercuts the countries’ own productivity growth. Fi-nally, low-income countries should look to the international system to meet their very reasonabledemands—not for special preferences to some markets and exemptions from rules, but fornondiscriminatory market access to every market in products in which they have a comparativeadvantage, for appropriately phased introduction of international regulations, and for develop-ment assistance in implementing administratively costly WTO rules. Like other countries, low-

ix

Foreword

income countries will find it in their interest to reduce their own external levels of protection aspart of an integrated development strategy aimed at reducing poverty.

Reducing barriers to trade is not enough to fulfill the development promise of Doha. Trademust be part of a larger development strategy for each country, a strategy that includes attentionto macroeconomic policy, infrastructure, education, and health as well as to accountable andresponsible governance. These elements of investment climate take time to develop but are es-sential for growth and poverty reduction and are crucial to make a sound trade strategy pay itsgrowth and poverty reduction dividends.

The World Bank, working in partnership with the other international institutions and bilateraldonors, is committed to supporting a pro-poor Doha outcome. Our objectives in trade are two-fold: promoting a world trading system in which global, regional, and bilateral rules are con-ducive to development and poverty reduction, and helping individual developing countries lever-age trade to promote their own growth. The latter objective hinges on integrating appropriatelysequenced trade reforms into national development and poverty reduction strategies.

The Bank is increasing its investment in research, technical assistance, and lending for trade.A casual perusal of the bibliography in each chapter of this report will give the interested readeran idea of the scope of the Bank’s research program. Moreover, in the last two years, the Bankhas undertaken at the request of governments more than 20 diagnostic studies of obstacles totrade integration. In conjunction with six partner institutions, the Bank has led the IntegratedFramework program—studies of trade obstacles in a dozen least-developed countries to date. Ithas completed several regional studies of trade.

In addition to studies and policy advice, the Bank has provided technical assistance in the formof lending to improve trade-related institutions and transport logistics. The Bank has programsthat finance activities in 49 countries (approximately one-third of its active client countries).These projects span all regions and range from export competitiveness projects in Ghana andBangladesh, to transport and trade facilitation projects in Eastern Europe, to support for im-proving customs–border control agencies and training the trading community in Pakistan. TheBank is also implementing projects to improve quality standards and is leading the “Standardsand Trade Development Facility,” an interagency partnership with the WTO, the FAO, and theWorld Health Organization, to deliver technical assistance for food safety and related standards.Should trade ministers reach an agreement on the Doha Agenda, the Bank will expand its lend-ing and technical assistance to help countries take advantage of new market access, to use tradeto promote their domestic competitiveness, and to manage any transitional costs—such as thosearising from erosion of trade preferences, changes in prices of imports, or reallocation of domes-tic resources from inefficient sectors to more efficient ones.

A pro-poor outcome in the Doha Agenda is only one step toward a world more supportive ofdevelopment. But this step is an important one. And it can be achieved only if everyone under-stands what is at stake in this historical moment—and moves purposefully and together to seizethe opportunity.

Nicholas SternChief Economist and Senior Vice PresidentWorld Bank

G L O B A L E C O N O M I C P R O S P E C T S

x

THIS REPORT WAS prepared by the World Bank Development Prospects Group, drawing on re-sources throughout the Development Economics Vice Presidency and the World Bank’s op-erational units. Richard Newfarmer was the lead author and manager of the report, under

the direction of Uri Dadush. The principal chapter authors were Richard Newfarmer (Overview);Elliot Riordan and Dominique Van der Mensbrugghe (Chapter 1); William Martin and VladManole (Chapter 2); Ataman Aksoy (Chapter 3); Pierre Sauvé, drawing on work by the OECD(Chapter 4); John Wilson, Shweta Bagai, and Carsten Fink (Chapter 5); and Bernard Hoekmanand Caglar Ozden (Chapter 6). We are grateful for the ideas and insights of several peer reviewerswho provided comments at various stages: Bijit Bora (World Trade Organization); J. Michael Fin-ger (American Enterprise Institute); Gary Hufbauer (Institute for International Economics); MariPangestu (Center for Strategic and International Studies), Gary Horlick (Wilmer, Cutler, and Pick-ering), and Julia Nielson (OECD); Julio Nogues (United Nations Development Programme); andOlivier Cattaneo (Agence Française de Développement). The report was prepared under the gen-eral guidance of World Bank Chief Economist and Senior Vice President Nicholas Stern.

Many staff from inside and outside the World Bank contributed to the report. In the Overview,Aart Kraay contributed a note on trade and poverty, and Carsten Fink, Bernard Hoekman,William Martin, and Aaditya Mattoo provided helpful suggestions. In Chapter 1, Hans Timmer,Caroline Farah, Himmat Kalsi, Robert Keyfitz, Annette I. De Kleine, Robert Lynn, FernandoMartel Garcia, Mick Riordan, and Bert Wolfe contributed to the global trends analysis; Do-minique Van der Mensbrugghe provided the long-term analysis; Shaohua Chen and MartinRavallion contributed to the poverty analysis; and Katherine Rollins was the staff assistant.Chapter 2 benefited from background papers and other inputs from J. Michael Finger and AndriZlate. For Chapter 3, John Beghin, Donald Mitchell, John Baffes, Harry De Gorter, NdiameDiop, Paul Brenton, Steve Jaffee, and Mirvat Sewadeh provided background papers, and BarisSivri, Tarek Soueid, Konstantin Senyut, and Gaston Gohou undertook data collection and analy-sis. Chapter 4 drew on research papers prepared by the OECD Trade Directorate and on the an-nual OECD report Trends in International Migration; the chapter reflects insights from JeffreyLewis, Julia Nielson (OECD), and Olivier Cattaneo (AFD). Tsunehiro Otsuki and KatherineMann (IIE) worked closely with the team on Chapter 5, and Ranga Rajan Krishnamani providedresearch assistance. Chapter 6 draws on research by Bernard Hoekman, ConstantineMichalopoulos, and L. Alan Winters. The regional annexes benefited from the written input ofregional chief economists around the Bank and their staff, particularly Milan Brahmbhatt. JohnBaffes, Betty Dow, Donald Mitchell, and Shane Streifel prepared the commodity annex. The staffassistant for the report was Awatif Abuzeid. Steven Kennedy provided editorial assistance. Denis

xi

Acknowledgments

Medvedev provided research assistance. Dorota Nowak coordinated the report’s publication anddissemination activities, working closely with the World Bank’s Office of the Publisher.

Several experts provided written comments that have immeasurably improved the quality ofthe report at various stages: Paul Brenton, Robin Carruthers, Jean-Jacques Dethier, ShahrokhFardoust, Coralie Gevers, Ian Goldin, Gary Horlick, Elena Ianchovichina, Mark Juhel, HansPeter Lankes, Jeffrey Lewis, Patrick Low (WTO), Kunio Mikuriya (World Customs Organiza-tion), John Nash, David Rosenblatt, John Panzer, Luiz Perreira da Silva, Byungdoo Sohn, MarkSundberg, Helena Tang, Yvonne Tsikata, and L. Alan Winters.

G L O B A L E C O N O M I C P R O S P E C T S

xii

ON THE EVE of the World Trade Organi-zation’s (WTO) Fifth Ministerial Meet-ing in Cancún in September 2003, the

world’s trade ministers—and the governmentsthey represent—face enormous challenges. Theglobal trade talks are stalled in several policydomains vital to developing countries—agricul-ture, nonfarm trade, access to patented drugsfor countries without domestic drug industries,special and differential treatment, and disputesettlement. Nor is there much progress in othercontentious areas, such as the “Singapore is-sues” of investment, competition, trade facilita-tion, and government procurement.

At the same time, the global recovery con-tinues to sputter. Although some signs of aturnaround have been evident in the UnitedStates, Europe seems to be losing momentum,and Japan appears positioned for another dis-appointing year. The Chinese economy, rein-forced by a positive performance in East Asiain 2002, continues to bustle along, but con-cerns over Severe Acute Respiratory Syndrome(SARS) and lost export momentum in the faceof the world slowdown haunted the regionaloutlook. South Asia continues to grow morerapidly than the world average. Latin Americais showing signs of an upturn, driven in part byrenewed confidence in Brazil, a tentative re-bound in Argentina, and an increase in Mex-ico’s growth; however, the recession in theRepública Bolivariana de Venezuela, whencoupled with political difficulties in the An-

dean countries, continues to weigh down re-gional performance. Africa, suffering from lowcommodity prices, is growing slowly; althoughfaster than in the 1980s and 1990s, today’sgrowth is far short of the pace necessary tomake significant dents in the poverty head-count or to achieve the Millennium Develop-ment Goals in health and education. War hasadversely affected regional performance in theMiddle East and North Africa; sluggish per-formance in Europe, especially Germany, hasadversely affected many countries in Centraland Eastern Europe. Even though progress ontrade would undoubtedly boost investor confi-dence, politicians coping with slow growthand high unemployment at home have beenfinding it more difficult to risk alienating in-fluential constituencies by accepting bold pro-posals in the world trade talks.

The outlook for the remainder of this yearand for 2004, though somewhat improved, isunlikely to produce growth strong enough tocut sharply into unemployment rates (figure 1).Uncertainty in the global environment remainsunusually high. Structural problems persist—overcapacity in high-tech industries globally,rising twin deficits in the U.S. fiscal and cur-rent accounts, and lingering bad loans inJapanese and (to a lesser extent) Europeanbanks. Other problems may prove more tran-sitory. The cessation of conflict in Iraq has notyet produced complete calm, and the inabilityto reach consensus at the UN Security Council

xiii

Overview

xiv

has created a lingering distrust among multi-lateral partners that clouds the global businessenvironment. Nonetheless, policy responsesare promising. Governments in the UnitedStates and Europe reacted to weak economicconditions with fiscal and monetary policy tostimulate their economies. And at the globalpolitical level, the June meeting of the G-8, to-gether with several subsequent bilateral meet-ings, began to mend frayed multilateral rela-tions. It remains to be seen whether this newpositive momentum will extend into multilat-eral collaboration in trade.

The precarious international environment isonly one reason why the global trade talkshave progressed slowly. Deeper explanationscan also be found in the history of multilateraltrade talks themselves. With the incorporationof ever more countries—mainly from the de-veloping world—the sheer number of actorshas expanded, making coalitions more difficultto build and consensus more elusive. More-over, previous multilateral rounds producedagreements in areas of primary interest to therich countries that dominated these discus-sions, particularly in manufactured goods. Itwas only with the Uruguay Round, concluded

in 1994, that tentative steps toward freeing uptrade in products of particular interest to de-veloping countries—notably agriculture andtextiles—were included. Consequently, manyof the hardest issues for rich countries havebeen left to this negotiation.

Realizing the developmentpromise of the Doha agenda

The challenge is daunting. But so is the re-ward to success. With room for addi-

tional fiscal and monetary stimulus rapidlyvanishing, progress on structural reforms suchas trade is important. In addition to bolsteringinvestor confidence in the short term, a DohaRound agreement that slashed trade barriers,particularly in agriculture, would stimulatetrade and raise incomes around the world,leading to a substantial reduction in globalpoverty.

The open question is whether a new multi-lateral agreement will live up to the develop-ment promise of the Doha Agenda. Severalissues under discussion are pivotal to develop-ment outcomes. They are the focus of thisreport:

• Because most poor people live in rural areas,trade barriers in agriculture are among themost important to poverty reduction.

• Labor-intensive manufactures have been themost dynamic market segment for everymajor region, including Africa, yet manydeveloping countries find that their exportsmeet obstacles in foreign markets—hightariffs, quotas, specific duties, and “anti-development” tariff structures that discour-age adding value in poor countries.

• In services, the potential for development-promoting reciprocal gains is especially high.Regulations in some developing countriesstill protect some inefficient state monopo-lies from competition—a drag on growth.(To be sure, proper regulation in some sec-tors must precede liberalization to avoid po-tential disruptions in socially important mar-kets, such as finance or basic services.) Also,

G L O B A L E C O N O M I C P R O S P E C T S

Figure 1 The recovery is building . . . but slowlyGDP growth, percent per annum

Source: World Bank data and projections.

Developingeconomies

Forecast

�

High-incomeeconomies

�

02000 2001 2002 2003 2004 2005

1

2

3

4

5

xv

O V E R V I E W

access for developing countries’ services ex-ports to industrial countries has yet to befully bound in the General Agreement onTrade in Services (GATS) (World Bank2001). Finally, national laws prevent greaterlabor mobility that would otherwise con-tribute to higher standards of living in bothreceiving and sending countries.

• Reducing the costs of trading by improvinginternational transportation services, cus-toms and ports, and logistics management—trade facilitation—requires substantial newinvestment, additional technical assistance,and coordinated multilateral efforts. Tradefacilitation is fundamental to realizing theexpanded trade promise of Doha, but theWTO agenda constitutes a small part of the challenge.

• Finally, the issue of special treatment for de-veloping countries cuts across all of thesepolicy domains and affects trade preferencesand exemptions from WTO regulations.The pursuit of trade preferences and exemp-tions from multilateral rules have not al-ways served developing countries partic-ularly well, both because preferences have not proven reliable and because selec-tive coverage has often left productivity-detracting trade barriers in place. The resid-ual barriers sap growth in the protectedeconomies and in developing-country trad-ing partners that are denied access. Perhapsmost important, the majority of the world’spoor do not live in the least developed coun-tries (LDCs). Trade preferences targeted atthese countries do not benefit the three-quarters of the world’s poor that live onUS$1 per day in other countries. In imple-menting new WTO rules, new accords willbe most effective if they recognize differ-ences among individual countries’ capacityto undertake new, resource-intensive rules.These differences require a new approach tospecial and differential treatment.

These areas pose difficult political chal-lenges for all segments of the internationalcommunity—rich countries, middle-income de-

veloping countries, and low-income countriesalike. Rich countries account for two-thirds ofworld trade and comprise nearly three-quartersof world GDP, so their domestic policies—mostevident in agriculture—have the greatest effecton the global marketplace. Despite the fact thatagricultural protection, tariff peaks, and anti-dumping measures shield powerful lobbies,rich-country leadership in reducing this protec-tion is a prerequisite for a pro-poor develop-ment outcome.

Today’s middle-income developing coun-tries have increased their global market sharein the last two decades. Because they includemany of the most dynamic global economies,their domestic policies no longer have onlyminor consequences for trade. With protectionrates in manufactures three times the level ofthose in rich countries and with ubiquitous re-strictions on services, the middle-income coun-tries have ample scope for undertaking reduc-tions in protection that will accelerate theirgrowth and provide access and a growth im-pulse to neighboring countries. High protec-tion in these countries taxes their growth andtheir poor in much the same way as protectionin the North.

Low-income countries have a special inter-est in greater market access, but they cannotsuccumb to the siren calls of preferential mar-ket access nor opt out of reducing border pro-tections at home, which tax exports and cutinto productivity growth. Preferences forLDCs can help, but would be more effective ifthey were made less restrictive and more reli-able than at present—and if benefiting coun-tries take the necessary policy steps, includingreductions in border protection, to promote asupply response. Moreover, because other de-veloping countries are unlikely to be grantednew trade preferences, global reciprocal re-duction in trade barriers holds the mostpromise for the world’s poor.

Market access is not the whole develop-ment story. Even if developing countries suc-ceed in obtaining access to new markets, theywill have to adopt complementary policies—removing obstacles to private investment, im-

proving public investment in infrastructure,and providing education—to ensure that do-mestic firms respond to new opportunities as-sociated with greater integration, and that thebenefits of integration are transmitted to thepoor. Put differently, trade policies must beembedded in a coherent national developmentstrategy—they are not a substitute for it. Forall of these reasons, realizing the developmentpromise of the Doha Agenda requires the par-ticipation of all groups of the internationalcommunity.

This report: toward a pro-poor Doha outcomeThis report analyzes central elements of theDoha Agenda that are important to developingcountries. Chapter 1 describes the prospectsfor the global economy that form the back-drop to the Doha trade negotiations. Chapters2–6 focus on agriculture, nonagricultural trade,services, transport and trade facilitation, andspecial development provisions. In each area,we expand on themes that have received lessanalysis in previous World Bank reports—among them specific duties in agriculture, an-tidumping in manufactures trade, temporarymovement of labor in services, security issuesin trade facilitation, and trade preferences andexemptions from rules as part of special anddifferential treatment (SDT). The remainder ofthis overview weaves these findings togetherwith those of previous Bank studies1 to lay outthe principal elements of a pro-poor outcomefor the Doha Agenda.

A Doha deal for development

Agriculture is at the heart of a development roundAgriculture is central to the developmentpromise of this trade round for two reasons:most of the world’s poor work in agricultureand most of the world’s protection is directedat agriculture. Some 70 percent of the world’spoor live in rural areas and earn their incomefrom agriculture. Largely exempt from pre–

Uruguay Round trade agreements to reduceprotection, agriculture is among the most dis-torted sectors in international trade. Eventhough levels of average tariff protection arecomparable in rich and poor countries, the ex-tensive use of producer subsidies in the OECDcountries and the fact that the OECD consti-tutes two-thirds of world agricultural trade un-derscore the centrality of their policies to de-velopment outcomes. Reducing protection inagriculture alone would produce roughly two-thirds of the gains from full global liberaliza-tion of all merchandise trade.

A few facts are enough to establish the con-text: protection facing developing country ex-porters in agriculture is four to seven timeshigher than in manufactures in the North andtwo to three times higher in developing coun-tries (IMF-World Bank 2002). Tariff peaks areparticularly high in rich countries againstproducts from poor countries. Tariff escalationthat discourages development of further pro-cessing is more pronounced in agriculture inboth rich and poor countries (figure 2). Heftyspecific duties are particularly common in richcountries; they automatically increase protec-

G L O B A L E C O N O M I C P R O S P E C T S

xvi

Figure 2 Escalating tariff rates discouragedevelopmentTariff rates

Sources: World Bank staff.

Raw

�

Final

Intermediate

�

�

0QUAD Canada Japan United

StatesEuropean

Union

5

10

15

20

25

O V E R V I E W

xvii

tion when commodity prices fall, throwing theburden of adjustment onto global prices andpoor countries. Subsidies in OECD countriesamount to US$330 billion—of which someUS$250 billion goes directly to producers. Theeffect is to stimulate overproduction in high-cost rich countries and shut out potentiallymore competitive products from poor coun-tries. It is no wonder that agricultural exportsfrom developing countries to rich countriesgrew in the 1990s at just half the rate they didto other developing countries.

Consider how agricultural protection playsthrough individual commodity markets. Sugarin the European Union (EU), Japan, and theUnited States is commonly protected through a combination of quotas, tariffs, and subsidiesallowing domestic sugar producers in thosecountries to receive more than double theworld market price. OECD governments sup-port sugar producers at the rate of US$6.4 bil-lion annually—an amount nearly equal to alldeveloping country exports. Prices are so highthat it has become economic to grow sugarbeets in cold climates and to convert corn tohigh-fructose corn syrup. Sugar imports in theOECD have shrunk to next to nothing. U.S.subsidies to cotton growers totaled US$3.7 bil-lion last year, three times U.S. foreign aid toAfrica. These subsidies depress world cottonprices by an estimated 10–20 percent, reducingthe income of thousands of poor farmers inWest Africa, Central and South Asia, and poorcountries around the world. In West Africaalone, where cotton is a critical cash crop formany small-scale and near-subsistence farmers,annual income losses for cotton growers areabout US$250 million a year. Rice support inJapan amounts to 700 percent of production atworld prices, stimulating inefficient domesticproduction, reducing demand, and denying ex-port opportunities to India, Thailand, Vietnam,and other countries.

More than 70 percent of subsidies in richcountries are directed to large (often corporate)farmers. These farmers have incomes that arehigher—often substantially so—than averageincomes in Europe, Japan, and, to a lesser ex-

tent, the United States. The net effect of subsi-dizing the relatively rich in wealthy countries atthe expense of adverse price penalties for theproducts of the relatively poor in developingcountries is to aggravate global income inequal-ities. Said differently, subsidies make the rela-tively rich even richer and the poor even poorer.

Realizing the development potential ofDoha requires phased reductions of borderprotection and subsidies. Of these, border pro-tection is the most important. These reductionsought to be done in a way that cuts off anti-development tariff peaks, reduces tariff escala-tion, and phases out specific duties. A pro-poor reform also means reforming policies thatdistort particular commodities of importanceto developing countries—sugar, cotton, rice,wheat, and dairy products.

Because global prices may rise in some com-modities, the international community maywant to design—and help finance—a programof adjustment in vulnerable countries that suf-fer deterioration in their terms of trade. Theseeffects are likely to be confined to a few coun-tries for several reasons: many food importersalso export other agricultural products thatwill experience positive terms-of-trade changesfrom liberalization; others now have tariffs onthose same food imports, tariffs that can be re-duced to offset any increase in global prices;some food importers will gain access to newmarkets in nonagricultural products and beable to export; and, because prices will changerelatively slowly, some food importers will in-crease domestic production in response tohigher prices and become self-sufficient or evennet exporters. Nonetheless, even though thechanges are likely to be manageable at theglobal level, the issue requires study and insome countries may require action.

Because rich and poor countries alike willbenefit from liberalization, all must make thepolicy changes necessary to realize its develop-ment promise. The rich countries, whose poli-cies arguably distort international trade themost, cannot escape leadership on agriculture.Moreover, leadership among donors to fi-nance a program to cushion adjustment is

G L O B A L E C O N O M I C P R O S P E C T S

xviii

Countries that trade more grow faster, according toevidence emerging from case studies of trade liberal-

ization and from large cross-country and time-serieseconometric studies. Although the links from specifictrade policy instruments to trade outcomes and growthis less clear, the basic association between increased tradeand growth is clear (box figure 1).a

Even when trade raises average incomes, its effects on poverty will depend on whether poverty in a given country is sensitive to growth in average in-comes, and on how the increase in trade affects the dis-tribution of income in the country. The first of these is-sues is empirically well understood. The sensitivity ofpoverty to growth in average incomes depends in an im-portant way on initial inequalities in a country (Raval-lion 1997). When incomes and opportunities are distrib-uted relatively equally, the effect of growth on povertyis larger than when initial inequality is high. Thus,growth associated with increased trade (or from anyother source) is likely to have larger proportional effectson poverty in countries where initial inequality is low.

More interesting and potentially more importantare the effects of increased trade on the distribution ofincome. Almost by definition, if increased trade dispro-portionately benefits the poor, poverty will fall fasterthan if trade disproportionately benefits the nonpoor.Understanding the likely distributional consequences oftrade liberalization is therefore crucial to understandingthe overall effects of trade on poverty. In many cases,there are very direct channels through which trade liber-alization is likely to disproportionately benefit the poor.For example, agricultural trade liberalization that al-lows previously suppressed prices of agricultural goodsto rise to world levels will benefit farmers, who are netproducers, but will hurt consumers. If farmers are morelikely to be poor, the liberalization will be, on average,pro-poor. Similarly, reductions in tariffs on manufactur-ers will hurt previously protected urban workers, who

Box 1 Trade and poverty: what are the links?

in many developing countries are likely to be relativelywell off, but will benefit poorer consumers of theirproducts by lowering prices.

At the same time, however, the distributional conse-quences of trade liberalization can also work againstpoor people. For example, reductions in tariffs imply re-ductions in trade tax revenues that can be important indeveloping countries that rely disproportionately on thissource of revenue. To the extent that public spending dis-proportionately benefits poor people (and this is by nomeans universal), reductions in tax revenues that accom-pany trade liberalization can have adverse distributionalconsequences.

The likely distributional consequences of trade lib-eralization, therefore, are complex and country-specific.Determining whether a given action would be pro- oranti-poor requires careful analysis. Looking back acrosscountries, there is little evidence that increased trade issystematically associated with either increases or de-creases in inequality (box figure 2).

On average, trade can be a powerful force forpoverty reduction, especially over longer horizons wherethe cumulative effects of growth on incomes of the poorare large. But this will not be true for all countries at alltimes—underscoring the importance of complementarypro-poor policies at the country level to ensure maximumpositive effects in every situation.

Box Figure 1 Integration with globalmarkets is associated with faster growthAverage annual per capita growth, 1980–99

Source: World Bank (2001).

0Decreasing export

share in GDPIncreasing export

share in GDP

0.51

1.52

2.53

3.5

–4

–3

–2

–1

0

1

2

3

4

–0.08 –0.06 –0.04 –0.02 0 0.02 0.04 0.06 0.08

Box Figure 2 Changes in trade have little relation to inequalityAverage annual change in Gini coefficient

Note: This figure shows changes in trade as a fraction of GDP andchanges in the Gini measure of income inequality, for a large sample of growth episodes of at least five years in duration.Source: Dollar and Kraay (2001).

Average annual change in trade/GDP

Series 1

Linear(Series 1)

y = 2.5227x + 0.0139R2 = 0.0013

Trade and the Gini coefficient

�

�

a For contrasting views on the state of the evidence on trade,trade policies, and growth, see Srinivasan and Bhagwati (2000),Rodriguez and Rodrik (1997), Bernanke and Rogoff (2001).Source: World Bank staff.

essential; their technical assistance to helpimplement standards and facilitate trade isneeded to help developing countries take ad-vantage of new trade opportunities. Middle-income countries, whose own policy reformswould produce a large share of the benefit todeveloping countries from global liberaliza-tion in agriculture, have to move more as-sertively than in the past. Their high tariffshave an adverse impact on growing South-South trade, especially with neighboringcountries. In a pattern common to all regions,agricultural exporters in East Asia, for exam-ple, paid one-third of all their tariff duties toother East Asian governments (second only to tariffs paid to get into rich countries). Agri-cultural exporters in the Middle East paid 44 percent of their tariff duties to regionalneighbors.

Nonfarm trade is increasingly essential to growth in poor countriesOver the past two decades, developing coun-tries have increased their share of global tradefrom just under one-quarter to about one-third. As a group, they have moved beyondtheir traditional specialization in agriculturaland resource exports into manufactures trade.Exports of manufactures have grown at nearlytwice the rate of agriculture, and now consti-tute nearly 80 percent of exports from all de-veloping countries. Countries that were low in-come in 1980 managed to raise their exports ofmanufactures from roughly 20 percent of theirtotal exports to more than 80 percent (figure3). As a result, many grew quickly and enteredthe ranks of today’s middle-income countries.The middle-income group of 1980 also in-creased its manufactures share, but somewhatless rapidly, to reach nearly 70 percent. Thisdramatic change in trade magnitudes and com-position has given developing countries a newinterest—and a powerful voice—in the ongo-ing Doha Round.

One reason for this change was the dra-matic reduction in border barriers in develop-ing countries since the mid-1980s, in combi-nation with increased access to rich-country

markets. Because import tariffs indirectly taxexports, reducing trade barriers in developingcountries stimulated trade. The burden of im-port protection on all export activities in de-veloping countries declined, but more so formanufactures than for agriculture and naturalresources. At the same time, the fact that suc-cessive multilateral trade rounds liberalizedglobal manufactures, while rich countries con-tinued to protect their agriculture (and devel-oping countries eventually began to followsuit) meant that developing countries’ exportsof manufactures were free to grow morerapidly than those in agriculture.

Today, trade in manufactures is still im-peded. Although tariffs on manufacturing inrich countries are on average lower than in de-veloping countries, the tariffs rich countriescharge developing countries are substantiallyhigher than those they charge other industrialcountries. For example, exporters of manufac-tures from industrial countries face, on aver-age, a tariff of 1 percent on their sales to otherindustrial countries; exporters in developingcountries pay anywhere from 2 percent if theyare from Latin America (where NAFTA weighsheavily) to 8 percent if they are from SouthAsia. Overall, rich countries collect from de-veloping countries about twice the tariff rev-enues per dollar of imports that they collectfrom other rich countries. However, the prob-lem is not solely a North-South issue. LatinAmerican exporters of manufactures, for ex-ample, face tariffs in neighboring Latin Ameri-can markets that are seven times higher than inindustrial countries. In Sub-Saharan Africa, thesame multiple is six; in South Asia, two.

Protection takes forms other than tariffs—among them quotas, specific duties, and con-tingent protection measures such as antidump-ing duties. As with tariffs, these measures tendto be used more frequently against labor-intensive products from developing countries.The quota arrangements in the WTO Agree-ment on Textiles and Clothing (ATC) stillshackle the exports of many poor countries.Although these arrangements are scheduled tobe removed in only 15 months, rich countries

O V E R V I E W

xix

to date have freed up only 15 percent of thequotas, obliging them to implement majorchanges at the end of the phase-in period. Av-erage antidumping duties are seven to tentimes higher than tariffs in industrial coun-tries, and about five times higher in developingcountries. Today’s protection remains heavilyconcentrated in the most politically sensitiveareas—textiles, clothing, and other labor-in-tensive manufactures, as well as agriculture—in both rich and poor countries.

Realizing the development promise ofDoha depends particularly on three efforts.

• First, rich countries desirous of promotingdevelopment can do so by ensuring that thenow lagging phase-out of the ATC is com-pleted according to the agreement—and notreversed through antidumping actions. TheATC phase-out will also require reforms bysome exporters facing increased competi-tion, many of which are LDCs, to ensure a

G L O B A L E C O N O M I C P R O S P E C T S

xx

Figure 3 Developing countries have become important exporters of manufactures

0

10

20

30

40

50

60

70

80

1981 1982 1983 1984 1985

Manufacturing exports (%)

Agricultural exports (%)

Resources exports (%)

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001�

�

�

In middle-income countries, manufactures make up 70 percent of exports

Middle-income countries’ share of world exports, 1981–2001 (percent)

In low-income countries, manufactures make up 80 percent of exports

Low-income countries’ share of world exports, 1981–2001 (percent)

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Manufacturing exports (%)

Agricultural exports (%)

Resources exports (%)

0

10

20

30

40

50

60

70

80

90

�

�

�

Source: UN COMTRADE.

smooth adjustment; trade-related develop-ment assistance could play a role in easingthe transition.

• Second, in both rich and poor countries, ef-forts to cut back on antidumping measuresthat create a patchwork of ad hoc protectionare essential if market access granted by theright hand of quota elimination and tariff re-ductions is not to be withdrawn by the lefthand of antidumping suits. Developing coun-tries themselves have become accomplishedpractitioners of contingent protection.

• Third, moving forward in nonfarm trade re-quires a Swiss-type formula approach thatwill require disproportionately greater re-ductions in high tariffs so as to mitigate theantidevelopment bias embedded in mosttariff structures around the world. Thechoice of the formula, and of its coefficientsof reduction, is important. Applying thesecuts to bound rates will effectively credit de-veloping countries that have unilaterally re-duced their applied tariffs since the end ofthe Uruguay Round.

Services liberalization could raiseproductivity Services are the fastest-growing component ofthe global economy. Even in developing coun-tries, services exports grew more rapidly thanmanufactures in the 1990s (World Bank 2001,chapter 3). More efficient backbone services—in finance, telecommunications, domestic trans-portation, retail and wholesale distribution,and professional business services—improvethe performance of the whole economy becausethey have broad linkage effects. Yet most devel-oping regions trail the industrialized world inexposing service sectors to competition. Figure4 shows that only Latin American countries are beginning to approximate the high-incomecountries in their degree of competition. Esti-mates suggest that, after controlling for otherdeterminants of growth, countries that fully lib-eralized trade and investment in finance andtelecommunications grew on average 1.5 per-centage points faster than other countries overthe past decade (Mattoo, et al. 2001).

No less important, developing countrieshave an interest in locking in market access fortheir services exports to rich-country markets—exports that are growing more rapidly thanmerchandise exports. Examples include China’sincipient software industry as well as softwareand back-office services from India.

The Doha Round has the potential of lock-ing in access to foreign markets for servicesexports. Just as many rich countries have notyet bound access for developing countries’ ser-vices exports, many developing countries haveyet to schedule with the WTO liberalizing re-forms that have already been undertaken. Of-fering to bind unilateral reforms can be usedto lock in existing access to overseas servicesmarkets. Active participation in the servicesnegotiations could help accelerate these twinprocesses (Mattoo 2003).

The GATS process allows governments toliberalize services at their own pace. It does notrequire that a government forgo its regulatoryresponsibilities. Nor does the GATS frame-work require a cessation of subsidies or pre-empt pro-poor regulation on universal serviceaccess. The main requirement is that, once asector is scheduled, governments are requiredto have transparent regulations, treat domesticand foreign companies alike, and permit allforeign companies access to the domestic mar-ket on the same terms as domestic companies.In fact, many governments have chosen toliberalize—but not to make commitments with the GATS that would bind this opening.Some two-thirds of the WTO members havescheduled fewer than 60 sectors of the approx-imately 160 sectors covered by the GATS. Forexample, only 12 developing countries havemade commitments in education. None havemade commitments in the provision of water.

Why the reluctance? Liberalization in ser-vices is more complicated than in goods mar-kets. Privatization without competition andproper regulation may achieve nothing morethan transforming a public monopoly into aprivate monopoly—with no improvement inservices. And too many developing countrieshave been content to change ownership

O V E R V I E W

xxi

through privatization while retaining limits onentry that buttress monopolies.

Effective regulation is critical to ensure thatthe poor have access to basic services (WorldBank 2002a, 2002b). Some sectors, such asretail and wholesale services, can be openedexpeditiously because competition can be re-lied on to discipline firms’ pricing and invest-ment decisions. Others, however, require well-formulated regulations before liberalization toensure proper market functioning and ade-quate access for low-income groups to ser-vices. In China’s financial sector, for example,the World Bank recommended that financialmarkets be opened gradually to allow regula-tions and institutional developments to pre-cede liberalization. The goal was to avoiddestabilizing financial losses by state bankssaddled with poor portfolios as efficientbanks, domestic and foreign, entered the mar-ket (World Bank 1996). China’s WTO acces-sion agreement generally reflected this phasedapproach. In network sectors, such astelecommunications and water, ensuring ade-quate pricing and universal access are simi-larly important if the poor are to benefit fromthe expansion of the system (World Bank

2001, chapter 3). Trade ministers wishing toharness the reciprocal negotiating frameworkof the GATS to spur domestic reforms whileleveraging market access abroad must ensurethat sectoral ministries have properly se-quenced regulations to support liberalization.

Liberalized trade in labor services couldcontribute much more To date, virtually all GATS commitments havefocused on the first three “modes” of interna-tional service delivery. Most trade in serviceshas occurred through those same modes.Twenty-eight percent of the value of servicestrade, for example, has been in Mode 1, “cross-border supply of services.” Another 14 percenthas been in Mode 2, “consumption abroad,”such as tourism. Fifty-six percent has been in Mode 3, “commercial presence,” such asthrough foreign direct investment in services.

Mode 4, which involves the temporarymovement of labor to provide services, ac-counts for only 1.4 percent of services trade(figure 5). Temporary movement has some ad-vantages over permanent migration for bothdeveloped and developing countries. Richcountries can obtain workers whose skills are

G L O B A L E C O N O M I C P R O S P E C T S

xxii

Source: World Bank Global Economic Prospects 2002, based on data from Mattoo, et al. (2001).

Figure 4 Developing countries lag behind rich countries in services liberalization

0 2 4 6 8 10

South Asia

East Asia

Middle East and North Africa

Europe and Central Asia

Latin America and the Caribbean

High income

Middle East and North Africa

Europe and Central Asia

South Asia

East Asia

Latin America and the Caribbean

High income

Financial services

Telecommunications

Greater competitiveness

�

�

�

in short supply, with minimal disruption oflabor markets and without taxing social ser-vices. Temporary migration allows develop-ing countries to obtain access to new, higher-paying jobs without necessarily suffering the“brain drain” that would occur with perma-nent migration. Poor countries also gain fromremittances sent home by temporary migrants,and returning workers bring new skills back tothe sending country. In 2001, remittances frompermanent as well as temporary migrants pro-vided some US$71 billion to developing coun-tries, nearly 40 percent more than all officialdevelopment assistance and significantly morethan net debt flows to developing countries. Iftemporary movement of labor up to 3 percentof the total labor force in rich countries werepermitted, developing countries would standto gain as much as US$160 billion in addi-tional income (Walmsley and Winters 2003).

To date, however, even after the significantliberalization of trade in services during theUruguay Round, little has been done to loosenconditions governing the temporary movementof natural persons (TMNP) supplying services.Present commitments refer almost exclusively

to higher-level personnel. More than 40 per-cent of workers covered by existing Mode 4commitments are intracorporate transfereeswhose mobility is intimately related to foreigndirect investment (often in services); another50 percent are executives, specialists, and salespersonnel who are business visitors. To date,therefore, Mode 4 has been of limited signifi-cance for developing countries, whose compar-ative advantage lies in the export of mediumand low-skilled, labor-intensive services.

In addition to other concerns associatedwith broader migration issues, two fundamen-tal tensions hamper progress on Mode 4 tem-porary labor mobility. The first is that govern-ments are reluctant to undertake permanentcommitments when employment demand varieswith cyclical conditions. Wanting to maintainpolicy flexibility, immigration and labor marketofficials have made GATS commitments farbelow the degree of TMNP access already af-forded under domestic laws and regulations.TMNP liberalization has been greatest in sec-tors (and for categories of workers) where labordemand routinely exceeds supply—tourism, in-formation technology, health services. The sec-ond tension stems from the fact that regionalpatterns of migration create domestic politicalsupport for programs that favor neighboringcountries, whereas Mode 4 programs necessar-ily are open to all countries on a most-favored-nation (MFN) basis. Preferential migrationschemes are commonly negotiated at the bilat-eral and regional levels—and MFN-based liber-alization would undermine these. Becausemany bilateral labor agreements are usually nottied to trade policy or other agreements, theyafford governments a greater degree of flexibil-ity to adjust programs to evolving migrationtrends and labor-market needs.

Tensions notwithstanding, present levels ofMode 4 use fall far short even of Mode 4’s rel-atively modest potential. To rectify this, devel-oping countries should expand their requestsand offers in the Doha Round. Only six re-quests had been tabled by June 2003, and onlytwo from developing countries (India and Co-lómbia). Also, WTO members should adopt

O V E R V I E W

xxiii

Figure 5 Temporary labor mobility is anunderused mode of trade in service

Mode 4(movement of natural persons)1%

Value of world trade in services by mode, (percent)

Mode 1(cross-border

supply)28%

Mode 2(consumption

abroad)14%

Mode 3(commercialpresence)57%

Source: IMF, Balance of Payments Yearbook.

rules that would provide greater clarity andpredictability. To help regularize entry andexit while improving security, countries couldadopt a GATS visa system that would facili-tate national visas for up to one year, subjectto appropriate security checks and oversight(see Hatcher 2003 and Self and Zutshi 2003).

Reducing transport costs and facilitatingtrade can have a powerful effectThe cost of moving goods across internationalborders is often as important as formal tradebarriers in determining the cost of landedgoods—and ultimately of market share. Onestudy estimated that every day spent in cus-toms adds nearly 1 percent to the cost of goods(Hummels 2001). In developing countries,transit costs are routinely two to four timeshigher than in rich countries. Transparent cus-toms regimes, modern port facilities, densetransportation networks, and access to infor-mation and telecommunications systems—allcan help lower transit costs.

Since September 11, 2001, security has be-come a dominant issue in international trade.Border inspections, cargo review, and othermeasures have increased transport times anddriven up costs. Each 1 percent increase incosts to trade from programs to tighten bordersecurity reduces world income by US$75 bil-lion per year. Developing countries, too, arevulnerable to security threats and terrorism,but limited budgets, dependence on foreigntrade and investment, and outdated infrastruc-ture and technology present serious challengesfor these countries. New security protocolsbeing deployed at ports, customs offices, andborder posts around the world have the poten-tial to add costs and diminish market accessfor developing countries—at least in the shortterm. But managed correctly, the same mea-sures can streamline trade transactions whilepromoting safety and security. To achieve thistrade-expanding result, a global frameworkmust be established to ensure that the needs of developing countries are addressed as en-hanced security regimes take shape.

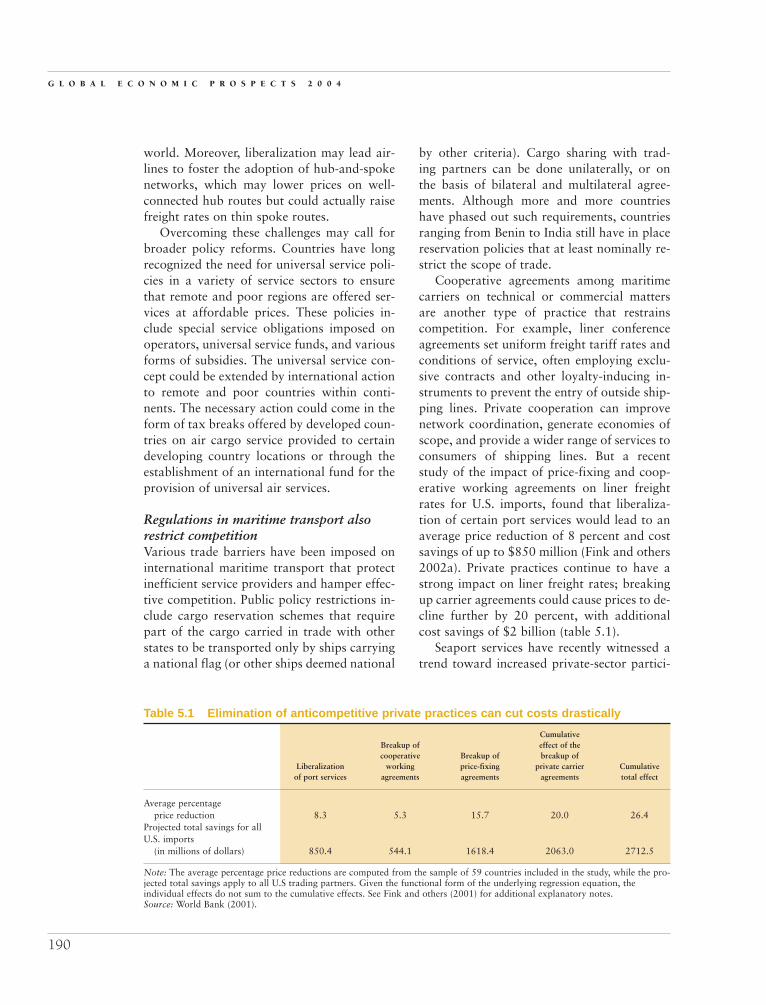

To counter any trade-reducing effects ofsecurity measures, every effort to cut trade-related costs in other areas is imperative. Reg-ulatory restrictions on international air andmaritime transport services inflate transportcosts—on some routes by amounts that dwarfthe value of tariffs. International air transport,which carries about 30 percent of developingcountries’ exports by value, is heavily pro-tected from international competition. Bilat-eral air service agreements commonly bar entryto efficient outside carriers, thereby raising ex-port costs for developing countries. City-pairroutes on which more than two passenger air-lines or dedicated freight airlines operate cancut costs by an average of 10.7 percent. Mar-itime transport, too, is often subject to prac-tices, such as cargo-reservation schemes andlimitations on port services, which protect in-efficient service providers. Such competition-restricting practices among shipping lines and port-terminal operators can increasefreight rates up to 25 percent on some routes.Rising concentration in the market for port-terminal services has increased the risk thatprivate firms may capture the benefits of gov-ernment reforms. Abusive practices by privateoperators are of special concern in develop-ing countries, where traffic volumes are lower and competitive forces inherently more limited.Regulations governing such practices are nowoutside the WTO mandate, but logically theyshould be reviewed for reformulation.

Facilitating trade by eliminating delays indeveloping countries would lower tradingcosts significantly, particularly if accompaniedby liberalization of transport and telecommu-nications, and streamlined regulations to pro-mote domestic competition. Trade facilitationrequires modernizing customs, improving portfacilities, and making investments in trade-related information technology—a huge insti-tutional and infrastructural agenda. Countriesdisplay wide variation in customs efficiencyand clearance times, for example (figure 6). Ifthose whose trade-facilitation capacity wasbelow average could be brought halfway up to

G L O B A L E C O N O M I C P R O S P E C T S

xxiv

the global average, international trade wouldincrease by US$380 billion annually.

Multilateral efforts are under way outsidethe WTO to promote—and in some cases fi-nance—institutional changes in trade facilita-tion. Key players include the World CustomsOrganization, the regional development banks,and the World Bank. Their efforts focus onpolicy reform, technical assistance, and infra-structure modernization.

Should trade facilitation, investment, andcompetition be the subject of newmultilateral disciplines in the WTO?As one of the four Singapore issues, tradefacilitation is under discussion in Geneva forpossible inclusion in the Doha Agenda. Al-ready the WTO, through the GATS, has a po-tentially important role to play in interna-tional transport and trade logistics—many ofthe transport service sectors could be immedi-ately scheduled with the GATS if countriessaw fit to do so. However, few countries havetaken advantage of its provisions.

Aspects of trade facilitation are part of theWTO’s trade-related disciplines, particularlythe provisions that encourage uniform treat-ment of transit trade and transparency of fees.Strengthening provisions related to transit,fees, and transparency, issues originally in theGeneral Agreement on Tariffs and Trade(GATT), would be helpful. However, bestpractice cannot be established in a vacuum; ithas to be gradually created in sound domesticlaws, regulations, and practices. A sustainedprogram of institutional reform must be tai-lored to each country, and it often requirestechnical assistance. The bilateral donors andmultilateral development banks and agen-cies are best positioned to provide the thor-ough diagnostics and technical assistancerequired to promote needed institutionalchange.

If the dynamics of the Doha negotiationspropel the WTO into a role in the broadertrade-facilitation agenda, any agreement, if it isto be effective, should recognize limitations indomestic capacity for implementation. Anagreement would be most effective if it in-cluded a serious commitment by developed na-tions to finance new trade-facilitation systems.Development assistance delivered under thecommitment could be provided by the WorldCustoms Organization, the multilateral devel-opment banks, and bilateral donors. The obli-gations of developing countries should be tai-lored to their implementation capacity. Andbecause the WTO’s dispute settlement provi-sions are largely inappropriate to promotinginstitutional changes, conventional enforce-ment of dispute settlement through trade sanc-tions ought to be set aside.

Other Singapore issues would stretch theWTO mandate into yet new areas, probablywith only marginal development benefits iftaken up in isolation. As discussed in GlobalEconomic Prospects 2003, there is no evidencethat an investment agreement would, by itself,promote new foreign investment. Similarly,adopting an agreement in competition policy—as currently framed in the negotiations—would

O V E R V I E W

xxv

Figure 6 Clearing customs takes longerin developing countriesAverage number of days to clear customs for sea cargo

Note: This is based on a sample of countries in each area;see figure 5.1 in chapter 5.Source: International Exhibition Logistics Associates.Available at http://www.iela.org.

Developed

East Asia andPacific

Latin Americaand the Caribbean

Africa

South Asia

0 2 4 6 8 10 12

have minimal effects on the terms of trade ofdeveloping countries, unless the agreementwere to establish new disciplines on nationalexport cartels and illegal international cartels(World Bank 2002a, chapter 4). Finally, a newagreement on government procurement thatfocuses on transparency is unlikely to improvemarket access substantially (Evenett 2002).Virtually all of the disciplines proposed in thesearrangements would require new policy actionsonly in developing countries. Although some ofthese may promote development, the main ben-efits of WTO agreements in these areas wouldbe in the market access that new agreementsleverage (Newfarmer 2003).

Securing the benefits of trade for thepoorest countriesMore favorable and differential treatment ofdeveloping countries is a prominent feature of multilateral trade rules. Selected subsets ofcountries have been granted trade preferences.Some countries were granted exemptions or al-lowed to defer implementing some multilateralagreements; many have benefited from techni-cal assistance to help implement mandates.

The present patchwork system has notworked especially well. Countries benefitingfrom trade preferences have generally under-performed in exports. One reason is that richcountries grant preferences voluntarily ratherthan as part of a binding multilateral negotia-tion. Those preferences often come laden withrestrictions, product exclusions, and adminis-trative rules that prevent beneficiaries from tak-ing full advantage of them. For example, only39 percent of potentially preferred importsunder the Generalized System of Preferences(GSP) into the Quad countries—Canada, theEU, Japan, and the United States—actuallytook advantage of preferential access—andusage rates are declining (figure 7). At times,protectionist lobbies have weighed in to pres-sure for reductions in the preference, either be-fore a country was deemed eligible or evenlater, when the first signs of export success fordeveloping countries become evident. BeyondGSP, the Quad countries sponsor their own