Real Estate in a Mixed-Asset Portfolio: The Role of the Investment Horizon Christian Rehring June 24 2009

Real Estate in a Mixed-Asset Portfolio: The Role of the Investment Horizon Christian Rehring June 24 2009.

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Real Estate in a Mixed-Asset Portfolio: The Role of the Investment HorizonChristian RehringJune 24 2009

2

Motivation

• Goal of the paper Explore the “term-structure of risk” for direct real estate in addition to

classic financial assets Quantify the influence of the investment horizon on the allocation to

real estate in a mixed asset portfolio By-product: Inflation-hedging abilities of assets depending on the

investment-horizon

• Factors inducing horizon effects addressed in the paper Predictable returns Illiquidity risk Transaction costs

3

Contributions of my paper

• Account for potential mean reversion effect using the cap rate as a state

variable Cap rate/Income return predicts real estate returns (Geltner and Mei,

1995; Fu and Ng, 2001; Plazzi et al., 2006) Prior research with direct real estate as an asset class (Geltner et al.

(1995), Porras Prado and Verbeek (2008), MacKinnon and Al Zaman

(2009)) does not include a state variable, which might capture mean

reversion in returns.

• Account for real estate market frictions in the form of illiquidity risk (Lin and

Vandell, 2007) and transaction costs Cheng (2008): Optimal holding period for a single property. Analytical

solution accounting for transaction costs, predictable returns (positive

autocorrelation) and illiquidity risk

4

Modeling approach

• Long-term mean variance analysis as in Campbell and Viceira (2005) Buy-and-hold investor with investment horizon of k years Investor concerned about real returns Predictable returns captured by VAR model induce horizon effects in

variances/covariances

• Augmented by Transaction costs Horizon dependent illiquidity risk (marketing period risk factor)

5

VAR(1) model

• zt+1 includes

Returns on asset classes

– Log real return on cash [r0,t+1]: basis asset

– Log excess returns on real estate, stocks and bonds: State variables

– Log nominal cash return

– Log excess return on property share returns

– Log cap rate

– Log dividend yield

– Log yield spread

zt1 0 1zt vt1,

vt1 ~ IIDN(0,v ).

xt1 rt1 r0,t1

6

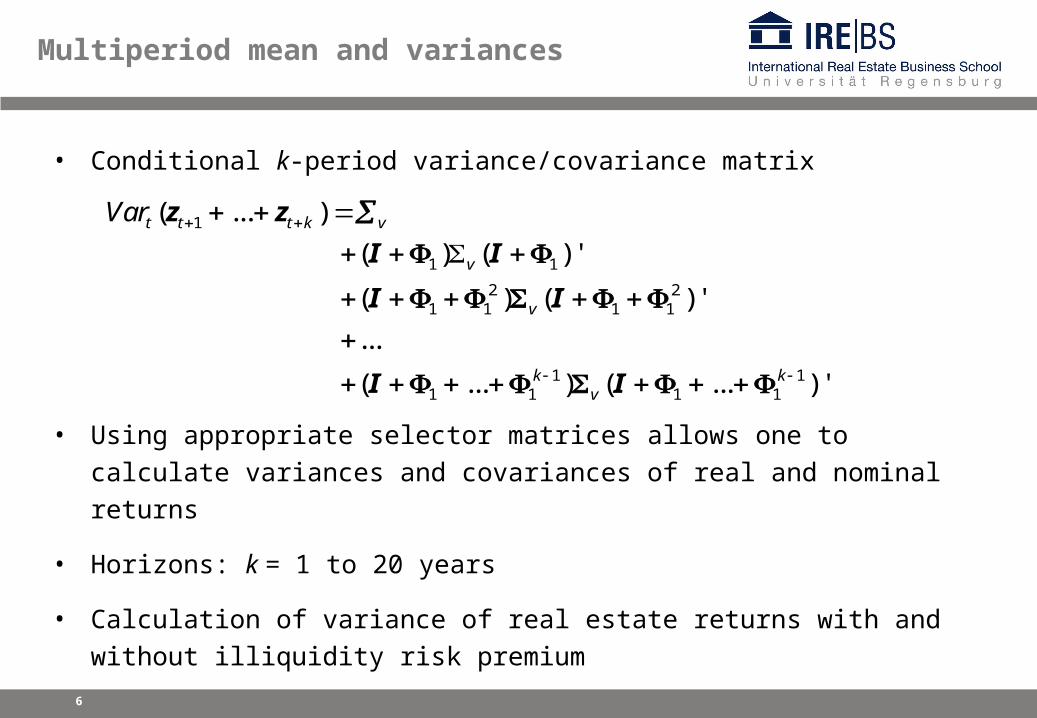

Multiperiod mean and variances

• Conditional k-period variance/covariance matrix

• Using appropriate selector matrices allows one to calculate variances and

covariances of real and nominal returns

• Horizons: k = 1 to 20 years

• Calculation of variance of real estate returns with and without illiquidity risk

premium

1

1 1

2 21 1 1 1

1 11 1 1 1

( ... )

( ) ( ) '

( ) ( ) '

...

( ... ) ( ... ) '

t t t k v

v

v

k kv

Var

z z

I I

I I

I I

7

Asset Allocation problem

• Approximation of log portfolio return (Campbell and Viceira, 2002):

where

• Mean-variance problem

costs ons transactiofvector :

))(()(

)()(

asset) basis(except htsasset weig ofVector :

2

)(,0

)(xx

c

σ

Σ

α

kdiagk

rrVark

xxx

kkt

kktt

)),()()()(('))((' 221)()(

,0)(

, kkkkkrr xxxkk

ktkktp ασαcα Σ k+tx

.)()(

subject to

,)(

2

1 ))( (w.r.t.min

)(,2

1)(,

)(,

k

rVarrE

k

rVark

kktpt

kktp

kktpt

α

8

Asset Allocation problem

• Expected log returns are assumed to take the values of their sample

counterparts• Horizon effects in log expected simple returns due to Jensen’s

inequality

• Round-trip transaction costs for real estate: ln(1+7.5%); 0% for other

assets

• Short-selling restriction on real estate

9

Data and sample statistics

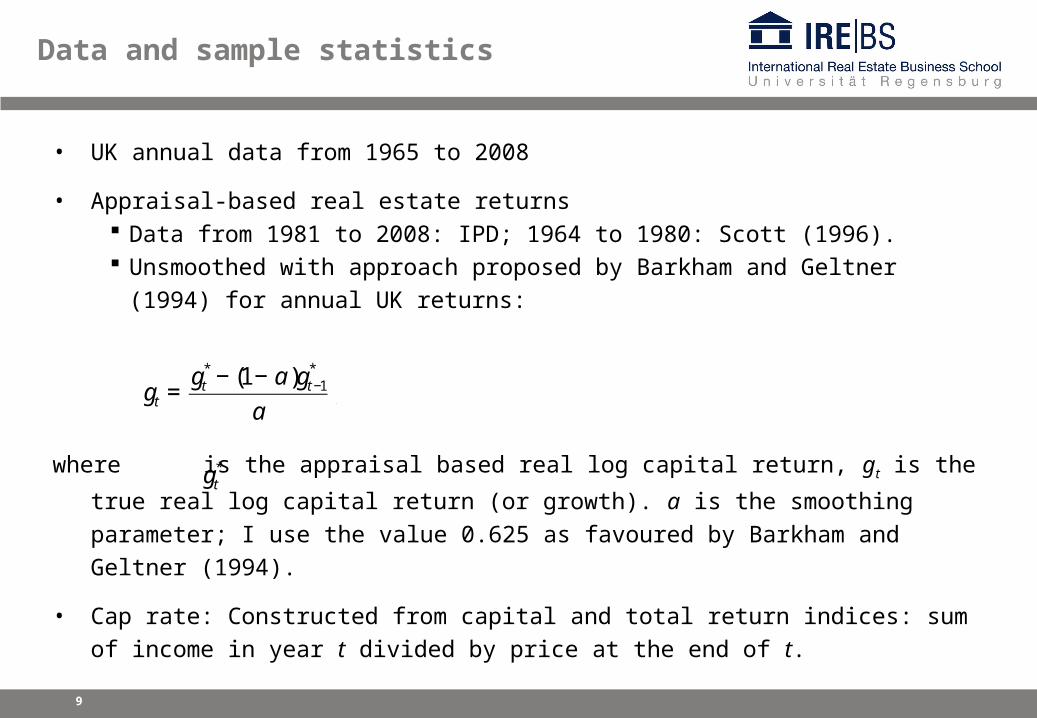

• UK annual data from 1965 to 2008

• Appraisal-based real estate returns Data from 1981 to 2008: IPD; 1964 to 1980: Scott (1996). Unsmoothed with approach proposed by Barkham and Geltner (1994) for

annual UK returns:

where is the appraisal based real log capital return, gt is the true real log capital

return (or growth). a is the smoothing parameter; I use the value 0.625 as favoured

by Barkham and Geltner (1994).

• Cap rate: Constructed from capital and total return indices: sum of income in year t

divided by price at the end of t.

€

gt =gt

* − (1− a)gt−1*

a,

€

gt*

10

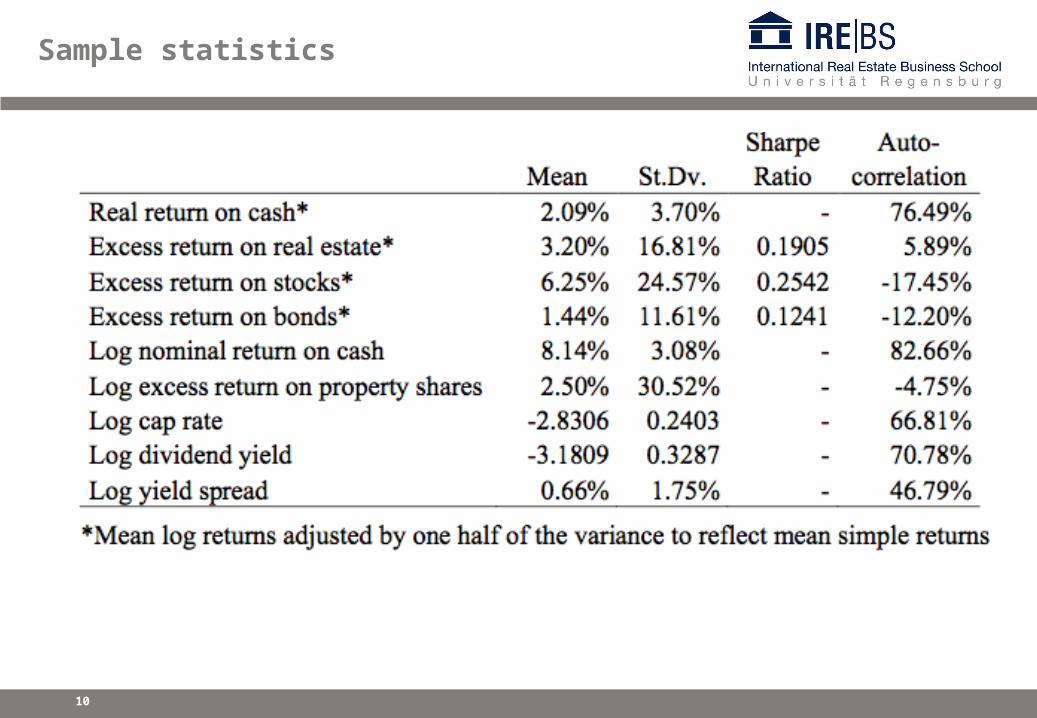

Sample statistics

11

VAR results

t-values in parantheses, values corresponding to p-values of 10% or below are highlighted Right most column: p-value of joint F-test in parantheses

VAR-Parameters

12

VAR results

Standard deviations (on diagonal) and correlations (on off-diagonals) of covariance matrix

13

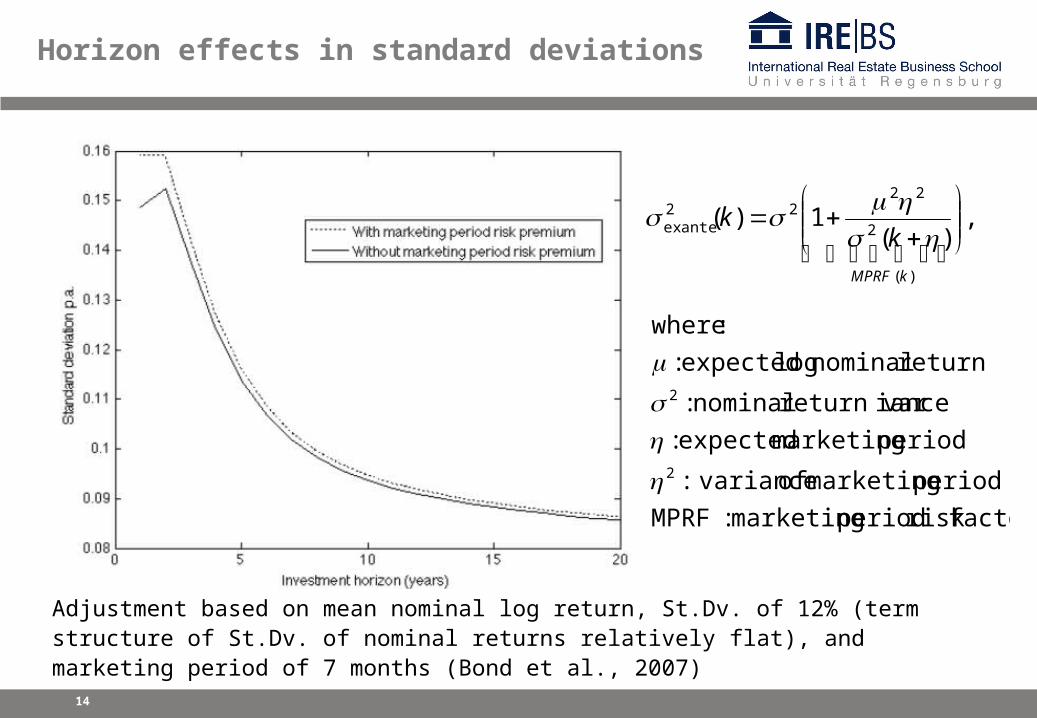

Horizon effects in standard deviations

The Figure shows conditional standard deviations of real returns and inflation depending on the investment horizon, as implied by the VAR model.

14

Horizon effects in standard deviations

Adjustment based on mean nominal log return, St.Dv. of 12% (term structure of St.Dv. of nominal returns relatively flat), and marketing period of 7 months (Bond et al., 2007)

factorrisk period marketing :MPRF

period marketing of variance:

period marketing expected :

iancereturn var nominal :

return nominal log expected :

:where

2

2

,)(

1)(

)(

2

2222

anteex

kMPRF

kk

15

Horizon effects in correlations

The Figure shows conditional asset correlations of real returns depending on the investment

horizon, as implied by the VAR model.

16

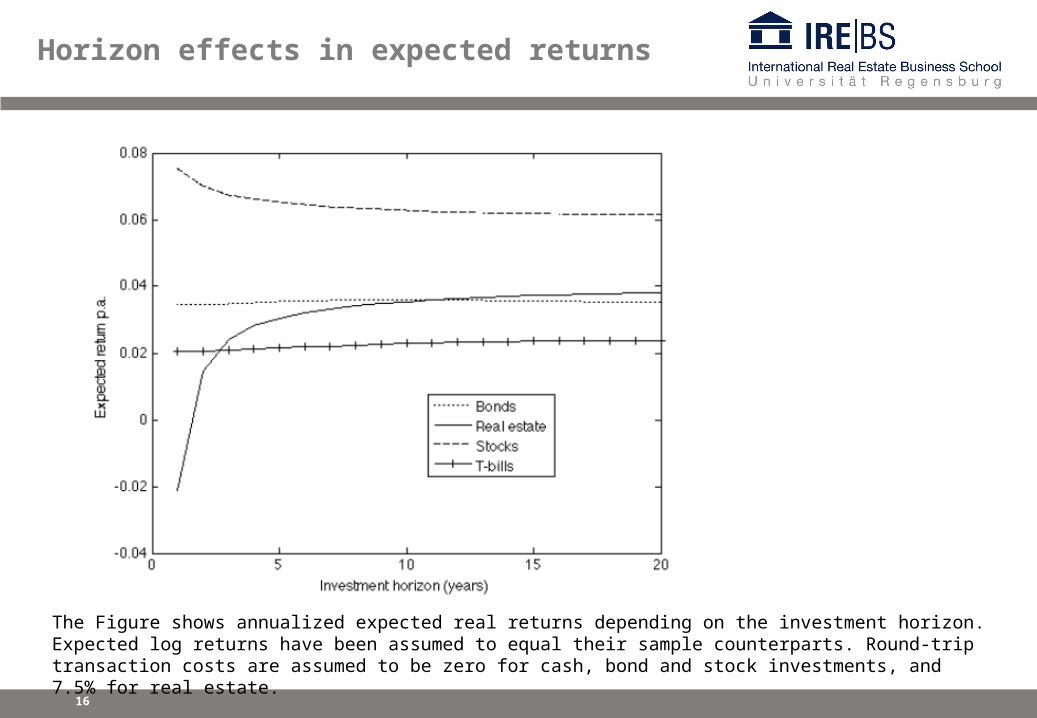

Horizon effects in expected returns

The Figure shows annualized expected real returns depending on the investment horizon. Expected log returns have been assumed to equal their sample counterparts. Round-trip transaction costs are assumed to be zero for cash, bond and stock investments, and 7.5% for real estate.

17

Asset allocation results

5-year horizon 10-year horizon 20-year horizon

This Figure shows optimized portfolio compositions for investment horizons of five, ten and twenty years for a

wide range of return expectations. The lower end of the return target is equal to the expected return of the

minimum-variance portfolio at the respective investment horizon. The upper end of the return target is equal to

the expected return of stocks at the respective investment horizon

18

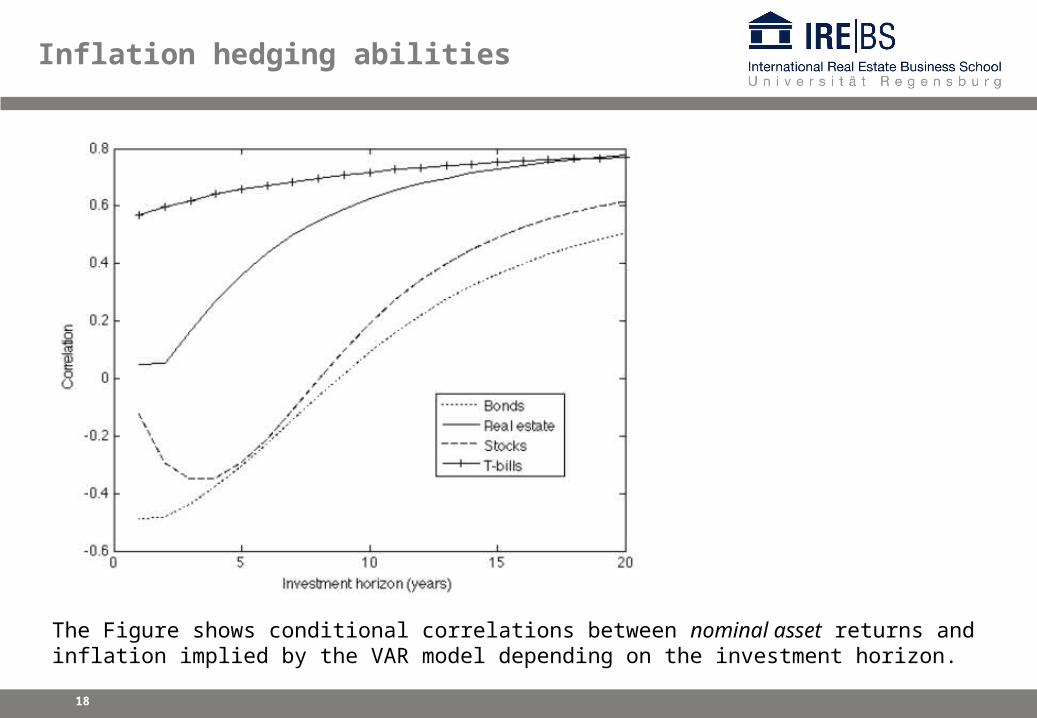

Inflation hedging abilities

The Figure shows conditional correlations between nominal asset returns and inflation implied by the VAR model depending on the investment horizon.

19

Conclusion

• UK real estate returns show slight mean aversion over short investment

horizons and strong mean reversion over medium and long horizons.

• An illiquidity risk premium accentuates the mean reversion effect.

• The return correlations of real estate with the other assets are relatively

favourable, even in the long run.

• The weight assigned to real estate is increasing with the investment

horizon. Over medium and long investment horizons, and over a wide

range of return targets, the weight allocated to real estate is between 13%

and 87%.

• Real estate appears to be a very good inflation hedge in the long run, but

not on a short-term basis.

20

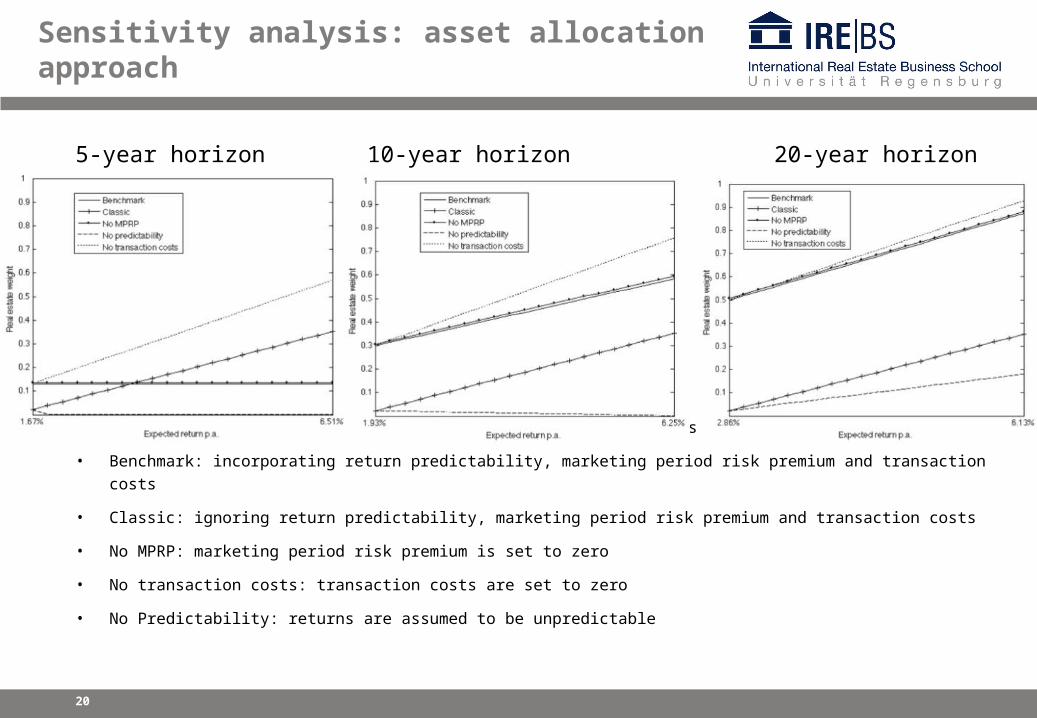

Sensitivity analysis: asset allocation approach

5-year horizon 10-year horizon 20-year horizon

This Figure shows the allocation to real estate under different asset allocation approaches.

• Benchmark: incorporating return predictability, marketing period risk premium and transaction costs

• Classic: ignoring return predictability, marketing period risk premium and transaction costs

• No MPRP: marketing period risk premium is set to zero

• No transaction costs: transaction costs are set to zero

• No Predictability: returns are assumed to be unpredictable

21

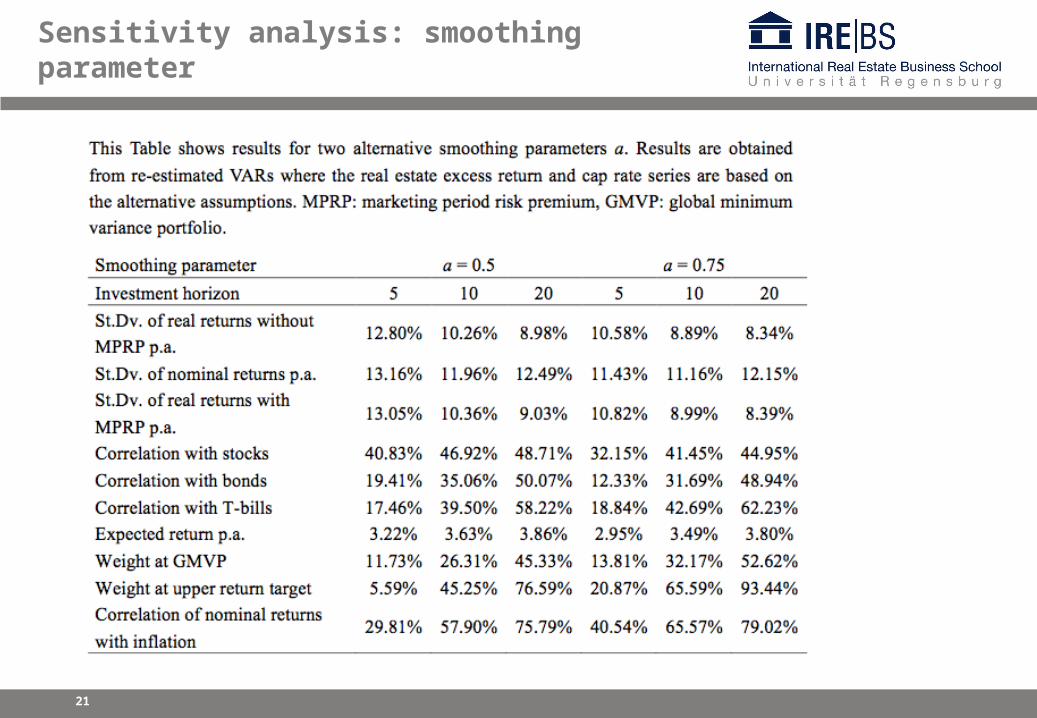

Sensitivity analysis: smoothing parameter

Related Documents