Real Estate Development Real Estate Development – Accounting Challenges Accounting Challenges By CA. Ramakrishna Prabhu

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Real Estate Development Real Estate Development ––Accounting ChallengesAccounting ChallengesAccounting ChallengesAccounting Challenges

By CA. Ramakrishna Prabhu

Agenda– Understanding the

industry

• What is real estate

development?

• Property development

cycle

2

cycle

• Development versus

construction

• Development business

risks

– Accounting considerations

– Auditing a real estate

developer

�Activity that is intended to create or add value to a real

estate asset

�A developer owns the asset during construction, sets the design,

provides development finance and arranges for the building works

�They may manage the project themselves and provide labour and

materials on site. However, many developers subcontract all or part

What do we mean by real estate development?

materials on site. However, many developers subcontract all or part

of the construction work.

�Developers range from high volume house builders to large single

project joint ventures

�Real estate developers may have land banks of undeveloped land,

held for strategic purposes to facilitate future developments

�This module considers development for sale (held as inventory)

and development to be held for long term capital appreciation or

rental income (held as investment property)

What do we mean by real estate development?

Accounting definitions

– In accounting terms real estate development can include a number of

alternatives The accounting approach depends on intentions for use of

the asset under development:

• Assets under development to be held by the developer for long-

term rental income and/or capital appreciation = Investment

property, accounted for under AS 13 (IndAS 40) Investment property, accounted for under AS 13 (IndAS 40) Investment

properties

• Assets under development for sale = Inventory (AS2)(IndAS2)

• Assets under development for use by the developer (owner-

occupied property) are accounted for under AS 10 (IAS 16

Property, Plant & Equipment). This is out of scope of this module.

– The above applies to new build (development of bare land) and to

redevelopments of existing buildings

Property development – critical

success factors

• Effective cost control

• Understanding government policies and their

implications

• Production of goods currently favoured by • Production of goods currently favoured by

the market

• Pre-development leases or sales

Difference between development

and construction– Developer exposed to both revenue and cost risk

– Construction is a service. Development is the sale of a good

– Constructor usually has no equity (i.e. ownership interest) in a project

– Developer usually has equity interest in project (i.e. own money at

risk)

– Developer engages constructor– Developer engages constructor

– Constructor is engaged to build a specific asset and their involvement

in a project is completed once the asset is completed and handed over

to their client

– Developer devises a strategy for the asset, commissions the

development works and markets the asset for sale and/ or lease to

tenants.

– Different risk profiles

Property development cyclePlan:

Execute:

Identify property

asset for development

Develop

concept

Initial

project

feasibility

7

Finalise:

Appoint architects,

project managers, other

consultants and

constructor

Acquire

property

Obtaining

funding

Secure approvals,

i.e. local council

and internal

Market for

sale/ lease

(pre-sale

targets for

residential)

ConstructionFinalise

sale

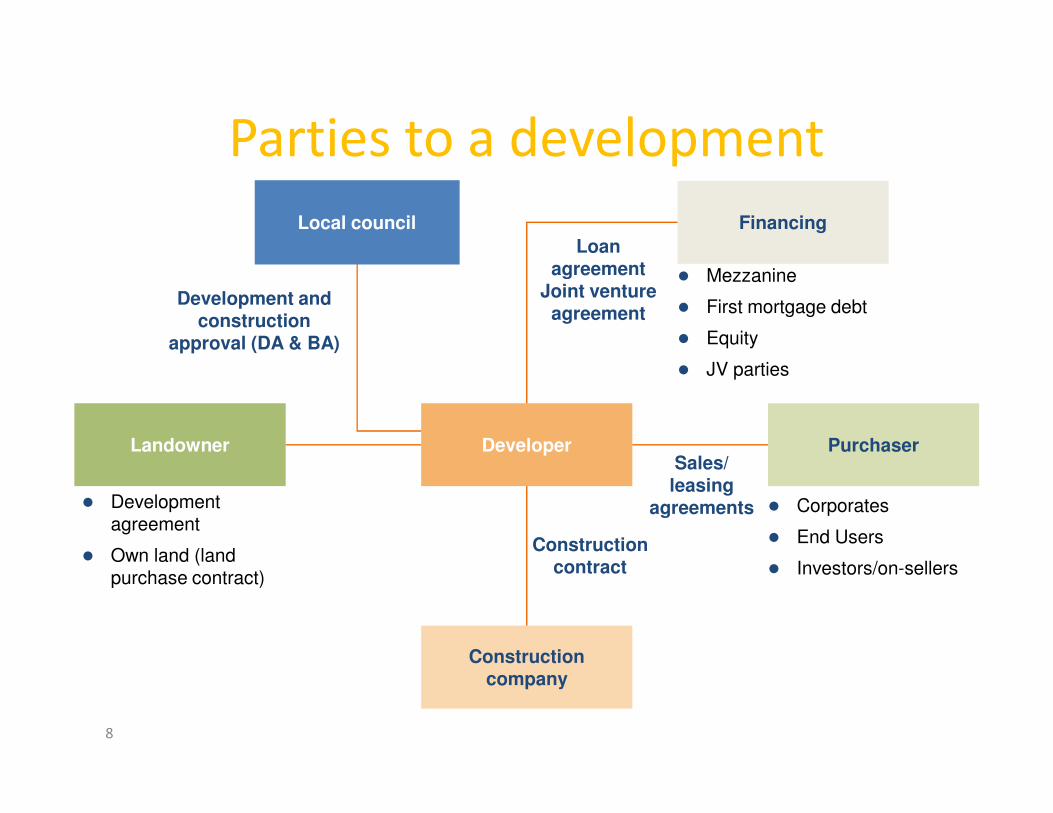

Parties to a development

Local council

Development and construction

approval (DA & BA)

Loan agreement

Joint venture agreement

Financing

� Mezzanine

� First mortgage debt

� Equity

� JV parties

8

DeveloperLandowner Purchaser

Construction company

Sales/leasing

agreements

Construction contract

� Development agreement

� Own land (land purchase contract)

� Corporates

� End Users

� Investors/on-sellers

Development business risk – often

speculative in nature

• What are the two main categories of risks?

Revenue Cost

� Realisation of value

− Market risk

� Risk of cost blow-

out

9

− Market risk

− Settlement risk� Funding risk

� Approval risk

� Completion risk

Development business risk –

risk of cost blow out

• Key risks

– Construction risk

– Design risk

– Schedule risk

– Finance and holding costs

10

– Finance and holding costs

• Developers risk management

– ‘Committing’ costs early

– Use of fixed price/lump sum contracts

– Updating and reviewing forecast costs and progress against

project feasibilities regularly

– Adequate project contingencies

Development business risk –

market risk– Most fundamental risk – matching timing and nature of developments with market

demand

– Fluctuations in property cycles

• Commercial

• Retail

• Industrial

11

• Residential

– Factors impacting property cycle

• Market sentiment

• Interest rates

• Competing supply (other developers)

• Legislation, e.g. Incentive under tax law

• Demographics

• Economics

– Developers risk management:

• Development lead time, i.e. Hold short/[med] term

• Pre-commitments, i.e. sales, leasing

Development business risk –

funding risk• Risk of not being able to fund the development or fund at a commercially viable rate

12

Increase in risk

Increase in interest rate

Development business risk –

funding risk (cont.)

• Lender requirements for debt

– Project viability (robust feasibility)

– Minimum level of developer equity

– Security

13

– Security

– Pre-commitments

– Interest rate

– Advances and covenants

• Developers risk management

– Pre-sale commitments

– Project feasibilities

Development business risk –

Approval risk

• Risk that approvals to commence the

development or a stage within the

development are not received

– Development approval (DA)

14

– Development approval (DA)

• Building design

• Property zoning

• Environment clearance

– Construction approval (CA)

Development business risk –

completion risk• Risk that development not ready for intended use by forecast completion

date

– Implications

• Potential fall over of pre-commitments

– Sunset dates in sales contracts

– Lease agreements, e.g. rental guarantees

15

– Lease agreements, e.g. rental guarantees

• Blow out of holding and financing costs

– Developers risk management

• Pass on to builder

– Early completion incentive

– Liquidated damages

– Program float (buffer between contracted completion and

sunset dates)

Development business risk –

settlement risk– The risk that sales

(exchanges) will not

complete (i.e. not

settled in cash)

– Developers risk

16

– Developers risk

management

• Exit strategy

• Enforceable sales

contracts

• Assessment of credit

risk

• Deposits (e.g. 10% cash

or deposits bonds)

Accounting challenges

– Which accounting standard – valuation?

– Cost accumulation and allocation

– Borrowing costs

– Which accounting standard - revenue?

17

– Which accounting standard - revenue?

– Revenue recognition

Accounting considerations

Which accounting standard – valuation?

• Valuation

– AS 2 Inventories – development for sale

• Inventory measured at lower of cost and NRV

– AS 13(IAS40) Investment Property – development to hold for long

term capital appreciation or rental income

• Asset measured at fair value OR depreciated historic cost

18

• Asset measured at fair value OR depreciated historic cost

• Revision to IAS 40 eliminated potential different treatment

between new development and redevelopment of existing

investment property

– AS 10/IAS 16 Property, Plant and Equipment – development by owner

occupiers

• Asset measured at fair value OR depreciated historic cost

Accounting considerations

Key questions Accounting impact/considerations

1. What is the nature of the entity’s

investment in the development?

− Asset

− Subsidiary

− Joint venture

� Inventory

� Consolidation

� Equity accounting/proportionate

The answer to

each of these

questions

19

− Joint agreement consolidation

� Proportional consolidation

2. How is the project funded? � Debt (on or off balance sheet)

� Equity

3. How does the developer acquire the

land?

� Upfront

� Instalments

� Land release/ related sale of lot/

property

4. What purpose is the property being

developed for?

� Outright sale (pre-commitment)

� Hold and lease

� Progressive sell down

questions

drives the

accounting

treatment

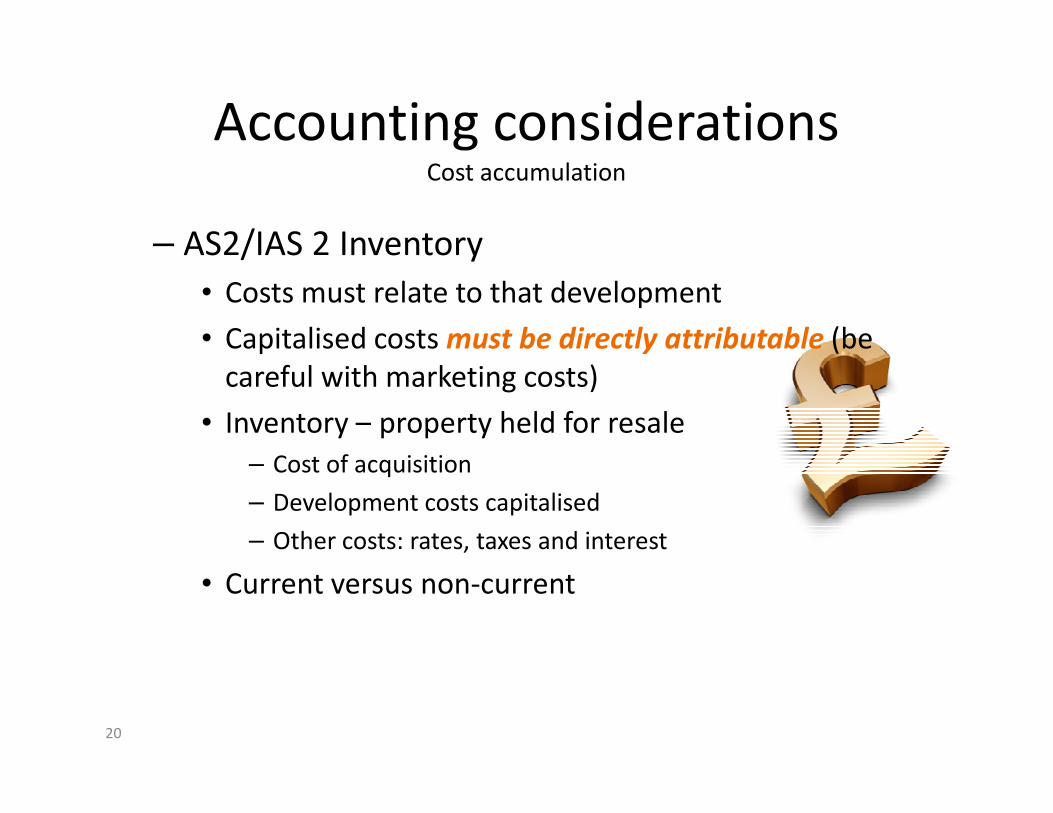

– AS2/IAS 2 Inventory

• Costs must relate to that development

• Capitalised costs must be directly attributable (be

careful with marketing costs)

• Inventory – property held for resale

Accounting considerationsCost accumulation

• Inventory – property held for resale

– Cost of acquisition

– Development costs capitalised

– Other costs: rates, taxes and interest

• Current versus non-current

20

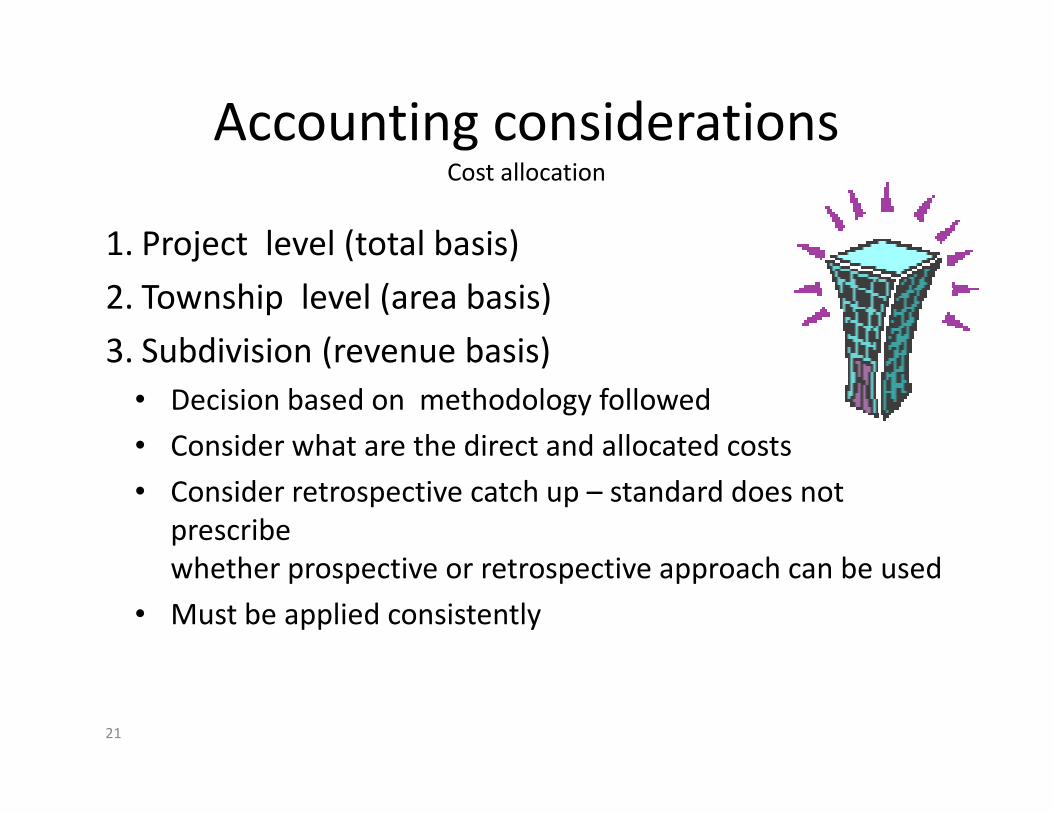

Accounting considerationsCost allocation

1. Project level (total basis)

2. Township level (area basis)

3. Subdivision (revenue basis)

• Decision based on methodology followed

21

• Decision based on methodology followed

• Consider what are the direct and allocated costs

• Consider retrospective catch up – standard does not

prescribe

whether prospective or retrospective approach can be used

• Must be applied consistently

Accounting considerations Borrowing costs

– AS 16 Borrowing Costs (revised)

• Attributable borrowing costs should be capitalised into the cost of the

project

• Includes interest

– amortisation of discounts or premiums and ancillary costs

– finance charges

22

– finance charges

– exchange differences

• Specific borrowings versus general borrowings (allocation on a reasonable

basis)

• Capitalisation

– commencement

– suspension

– Cessation

Accounting considerationsWhich accounting standard - revenue?

• IFRIC 15 Agreements for Construction of Real Estate

is applied to determine whether a contract is in

scope of either

– AS 7 Construction Contracts– AS 7 Construction Contracts

– AS 9 Revenue Recognition

– Guidance Note –Real Estate Revenue

Accounting considerationsRevenue recognition: IAS 18 Revenue

• Revenue recognition criteria – sale of a good

1. Significant risks and rewards have transferred

2. Does not retain continuing managerial involvement

usually associated with ownership

24

usually associated with ownership

3. Amount of revenue can be measured reliably

4. Probable economic benefit will flow

5. Costs can be measured reliably

If the above criteria are met then revenue can be

recognised

Accounting/Audit

Key considerations – revenue recognition matter of judgement

‘Assess who is exposed to majority

of risks and benefits of ownership

of asset’

Recognise revenue

� Cash collected

� Title transferred

� No terms/

conditions attached

to sale

� No continuing

Defer revenue

recognition

� Cash deferred and

25

� No continuing

involvement

� No bonding

� Cash deferred and

amount is contingent

� Title does not transfer

(is retained)

� Conditions attached to

sale, e.g. yield

guarantee

� Involved in asset’s

ongoing management

(continuing

involvement)

What if

� Seller of land is also

contracted to develop the

land for the purchaser?

Accounting considerations Revenue recognition – example

– Land sale Rs. 100 Crore being fair value of land

– Cash received at date of completion of contract

– Land sale contract cannot be rescinded based on

non performance of development agreement

26

non performance of development agreement

– Separate development agreement fee (is fixed

determined on budgeted cost plus normal

commercial margin (e.g. 10%))

– Seller can be terminated as developer if given 4

weeks notice, normal compensation under

agreement as opposed to large penalty for

termination

Accounting considerations Practical application of revenue recognition rules

Type of product Revenue recognised when:

Land /plot sale � Substantially complete (meaning sewer,

water and roads are complete)

� Title obtained from authorities

2

727

� Enforceable agreement entered in to for

sale and Settled (in cash by purchaser)

Built form residential, Commercial space

� Sold apartments on percentage completion

achieved (100% complete)

� Completion certificate from authorities.

Accounting considerations Disclosures

– Presentation as completed inventory or development work in progress

– Presentation as development property or investment property

– Investment property under construction – accounting policy choice under

AS 13/IAS 40 to hold at cost or fair value. But beware – if choose cost,

there is still a requirement to disclose fair value.

– Disclosure relating to the varying forms of joint ventures, joint

28

– Disclosure relating to the varying forms of joint ventures, joint

arrangements and other forms of collaboration among developers.

– Disclosure requirements relating to financing

Also:

– Large number of statutory financial statements common in many

jurisdictions due to structure of real estate development groups, where

each development project may be held in a separate statutory entity for

tax, organizational or other reasons.

Auditing a real estate developer

Inventory

– Recoverability of inventory is the most

fundamental audit consideration

• Requirements of AS 2 – Measure inventory at lower of

cost and NRV

– Also consider cost accumulation, cost allocation,

29

– Also consider cost accumulation, cost allocation,

capitalization of borrowing cost

– How do we assess this?

• Project reviews

Specific Issues

• Accounting for infrastructure cost in respect of

megha township project and working out its

impact on final product.

• Sale of land and construction under two • Sale of land and construction under two

separate agreements

• Perpetual ownership of infrastructure with

developer having continuous revenue stream

• Deferred payment facilities.

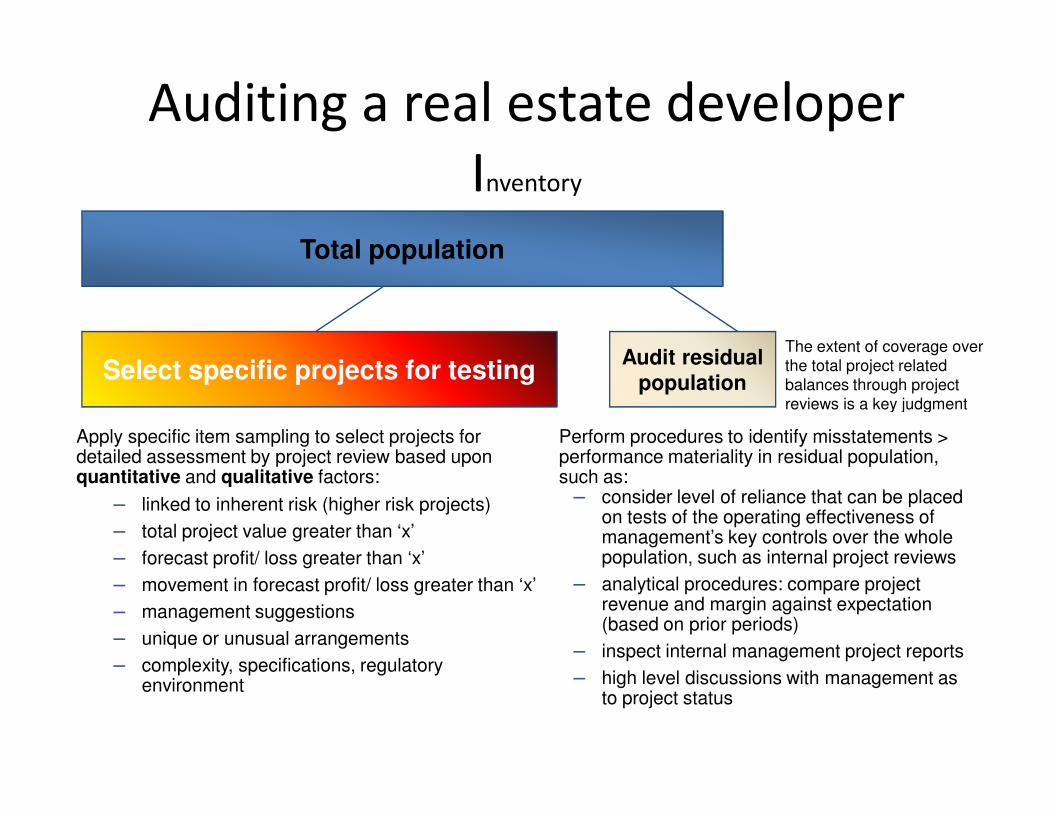

Auditing a real estate developer

Inventory

Total population

Select specific projects for testingAudit residual

population

The extent of coverage over

the total project related

balances through project

reviews is a key judgment

Apply specific item sampling to select projects for detailed assessment by project review based upon quantitative and qualitative factors:

− linked to inherent risk (higher risk projects)

− total project value greater than ‘x’

− forecast profit/ loss greater than ‘x’

− movement in forecast profit/ loss greater than ‘x’

− management suggestions

− unique or unusual arrangements

− complexity, specifications, regulatory environment

Perform procedures to identify misstatements > performance materiality in residual population, such as:

− consider level of reliance that can be placed on tests of the operating effectiveness of management’s key controls over the whole population, such as internal project reviews

− analytical procedures: compare project revenue and margin against expectation (based on prior periods)

− inspect internal management project reports

− high level discussions with management as to project status

reviews is a key judgment

Auditing a real estate developer Project reviews

• Understand the development and risks borne by developer through

– discussions with project and finance management

– Inspection of management reports (e.g. Project control group meeting minutes)

– detailed examination of all relevant contracts (including development agreement,

construction contract, financing and joint venture agreements)

– bank covenants

• Detailed analysis of the project feasibility, understanding movements and obtaining corroborative

32

• Detailed analysis of the project feasibility, understanding movements and obtaining corroborative

evidence for:

– sales rates and prices

– escalation applied

– time phasing

– forecast construction costs being in line with contract

– external valuations

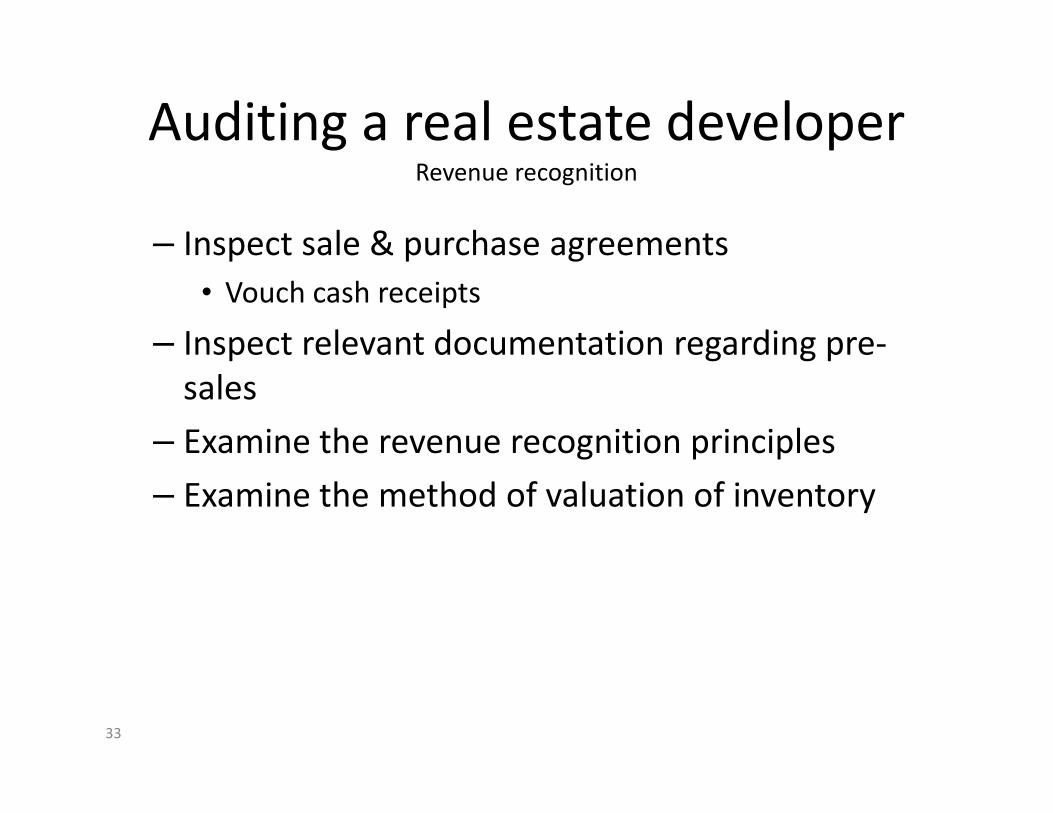

Auditing a real estate developer Revenue recognition

– Inspect sale & purchase agreements

• Vouch cash receipts

– Inspect relevant documentation regarding pre-

sales

33

– Examine the revenue recognition principles

– Examine the method of valuation of inventory

Any questions?

3

4

???

Related Documents