SARAS S.p.A. Platts 5th Annual Refining Conference 1 Platts 5 th Annual European Refining Markets Conference – 27 th Sep 2011 Dario Scaffardi – General Manager, Saras S.p.A. Reacting to structural changes in the EU refining industry

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SARAS S.p.A. Platts 5th Annual Refining Conference 1

Platts 5th Annual European Refining Markets Conference – 27th Sep 2011Dario Scaffardi – General Manager, Saras S.p.A.

Reacting to structural changes in

the EU refining industry

SARAS S.p.A. Platts 5th Annual Refining Conference 2

•• Structural changes in the oil marketsStructural changes in the oil markets

•• New competitors from Asia and Middle EastNew competitors from Asia and Middle East

•• Tightening EU environmental regulations Tightening EU environmental regulations

•• Consolidation process is unavoidable in OECDConsolidation process is unavoidable in OECD

•• Strategic relevanceStrategic relevance of the EU Refining sectorof the EU Refining sector

•• EU Governments should take appropriate actionsEU Governments should take appropriate actions

•• Companies should also pursue Companies should also pursue ““selfself--helphelp””

Agenda

SARAS S.p.A. Platts 5th Annual Refining Conference 3

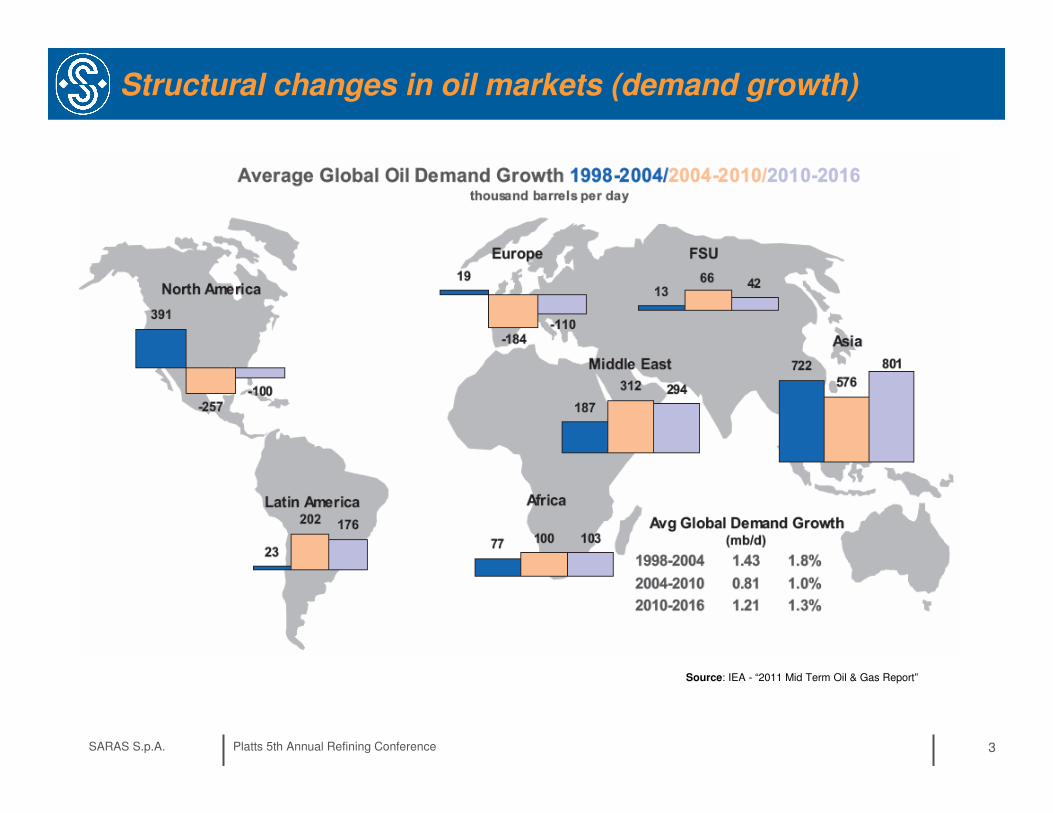

Structural changes in oil markets (demand growth)

Source: IEA - “2011 Mid Term Oil & Gas Report”

SARAS S.p.A. Platts 5th Annual Refining Conference 4

Incentives for new refineries in Asia & Middle East

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Asia Pacific Middle East North America Latin America Greater Europe FSU Sub-Saharan

Africa

Ad

dit

ion

al

CD

U C

ap

ac

ity

, M

bd

.

.

New Expansion

Additional Refinery

Capacity ('11-'15), kbd

New Expansion Total

Asia Pacific 2,572 1,028 3,600

Middle East 1,120 256 1,376

North America - 422 422

Latin America 651 252 903

Greater Europe - -163 -163

FSU 140 472 612

Sub-Saharan Africa 46 24 70

Total 4,529 2,290 6,819

Source: Wood Mackenzie

SARAS S.p.A. Platts 5th Annual Refining Conference 5

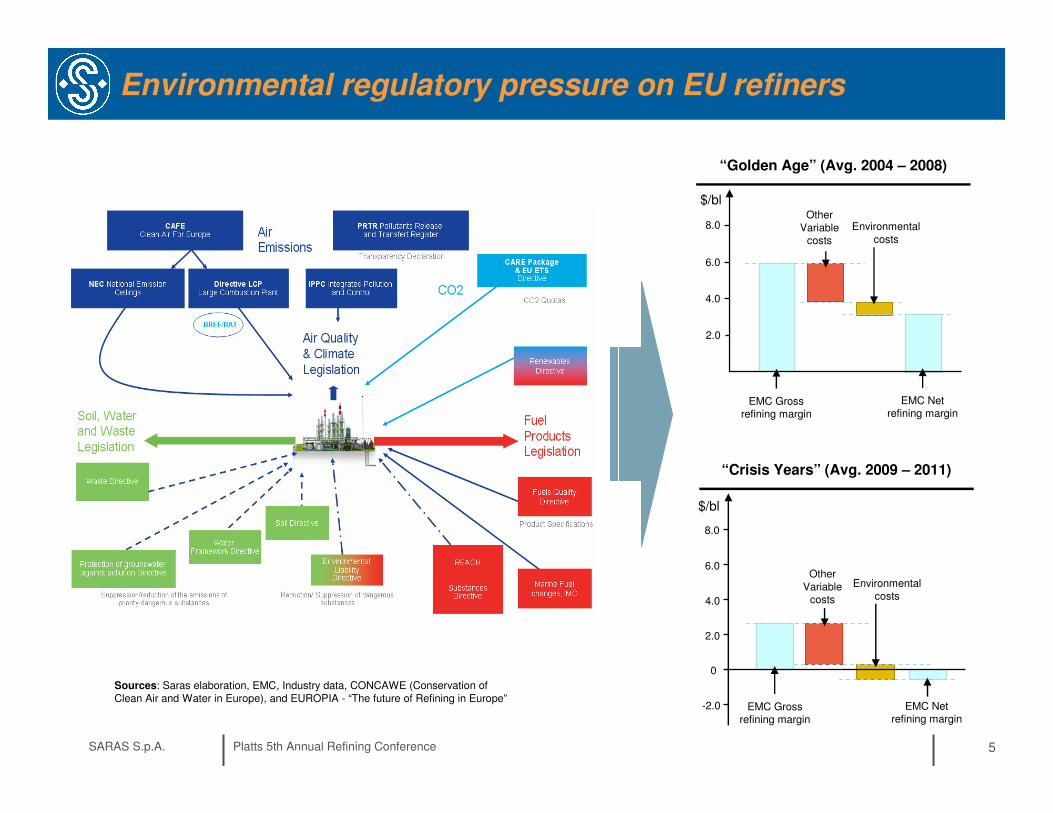

Environmental regulatory pressure on EU refiners

Sources: Saras elaboration, EMC, Industry data, CONCAWE (Conservation of Clean Air and Water in Europe), and EUROPIA - “The future of Refining in Europe”

$/bl

2.0

6.0

4.0

8.0

EMC Gross refining margin

Other Variable

costs

EMC Net refining margin

Environmental costs

“Golden Age” (Avg. 2004 – 2008)

$/bl

0

-2.0

2.0

6.0

4.0

8.0

EMC Gross refining margin

EMC Net refining margin

Other Variable

costs

Environmental costs

“Crisis Years” (Avg. 2009 – 2011)

SARAS S.p.A. Platts 5th Annual Refining Conference 6

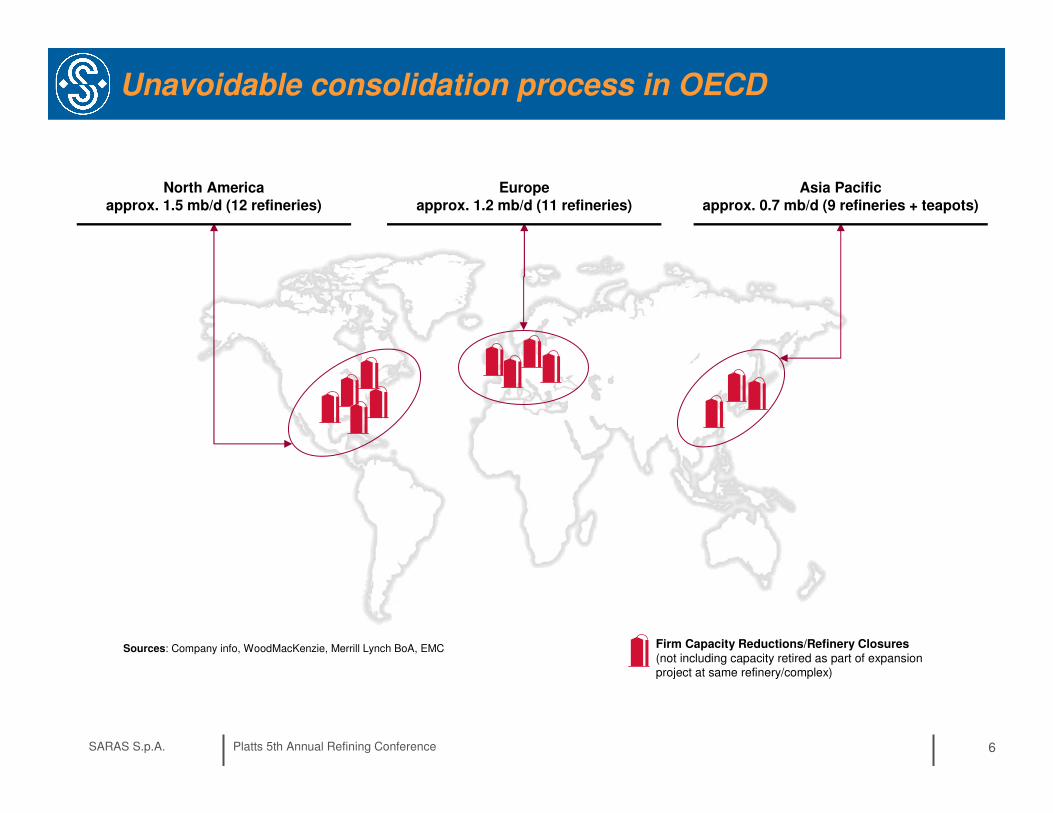

Unavoidable consolidation process in OECD

Sources: Company info, WoodMacKenzie, Merrill Lynch BoA, EMC

North America

approx. 1.5 mb/d (12 refineries)

Europe

approx. 1.2 mb/d (11 refineries)

Asia Pacific

approx. 0.7 mb/d (9 refineries + teapots)

Firm Capacity Reductions/Refinery Closures(not including capacity retired as part of expansion project at same refinery/complex)

SARAS S.p.A. Platts 5th Annual Refining Conference 7

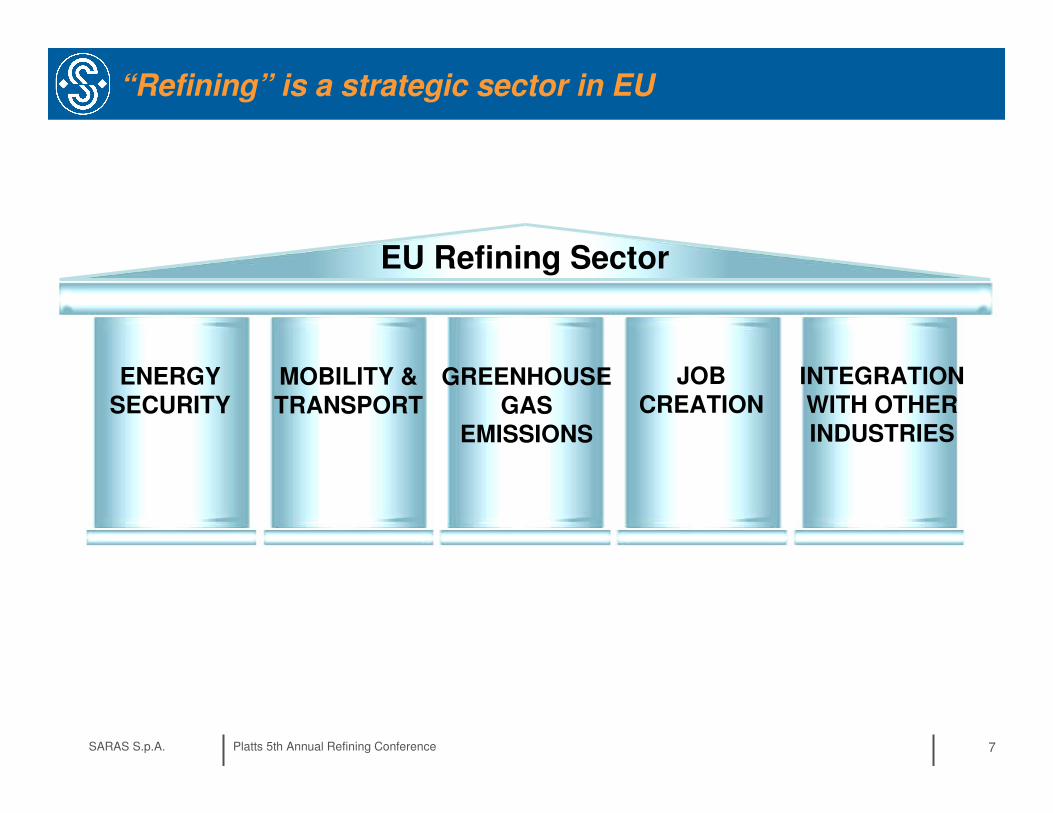

“Refining” is a strategic sector in EU

ENERGY

SECURITY

EU Refining Sector

MOBILITY &

TRANSPORTGREENHOUSE

GAS EMISSIONS

JOB

CREATIONINTEGRATION

WITH OTHER INDUSTRIES

SARAS S.p.A. Platts 5th Annual Refining Conference 8

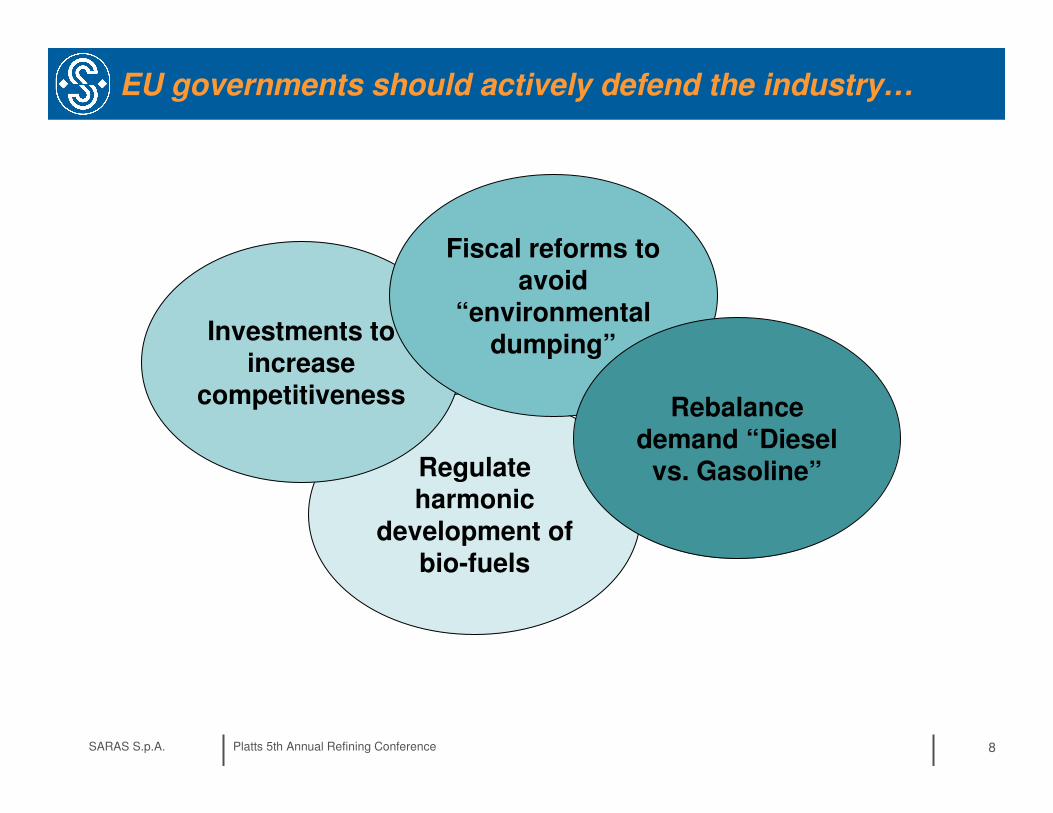

EU governments should actively defend the industry…

Regulate harmonic

development of bio-fuels

Investments to increase

competitiveness

Fiscal reforms to avoid

“environmental dumping”

Rebalance demand “Diesel

vs. Gasoline”

SARAS S.p.A. Platts 5th Annual Refining Conference 9SARAS S.p.A. 9

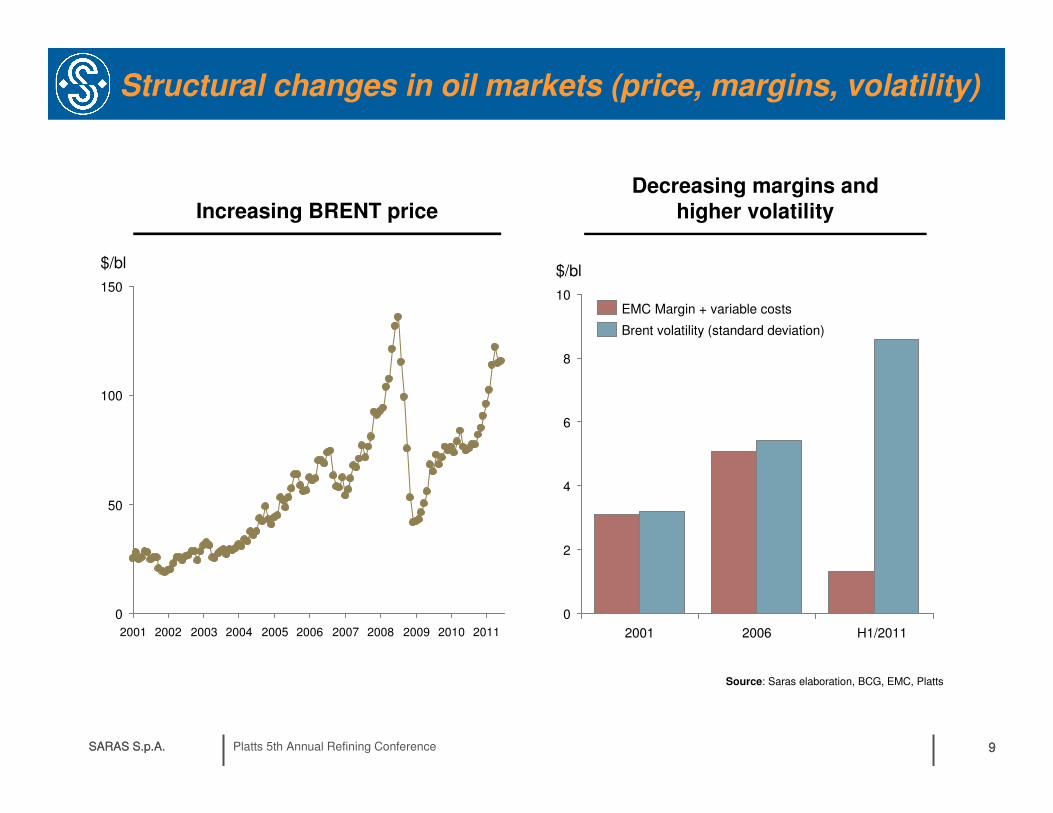

Structural changes in oil markets (price, margins, volatility)

Source: Saras elaboration, BCG, EMC, Platts

20052004200320022001

50

0

2006 20112010200920082007

$/bl

150

100

10

8

6

4

2

0

H1/201120062001

$/bl

Brent volatility (standard deviation)

EMC Margin + variable costs

Increasing BRENT priceDecreasing margins and

higher volatility

SARAS S.p.A. Platts 5th Annual Refining Conference 10

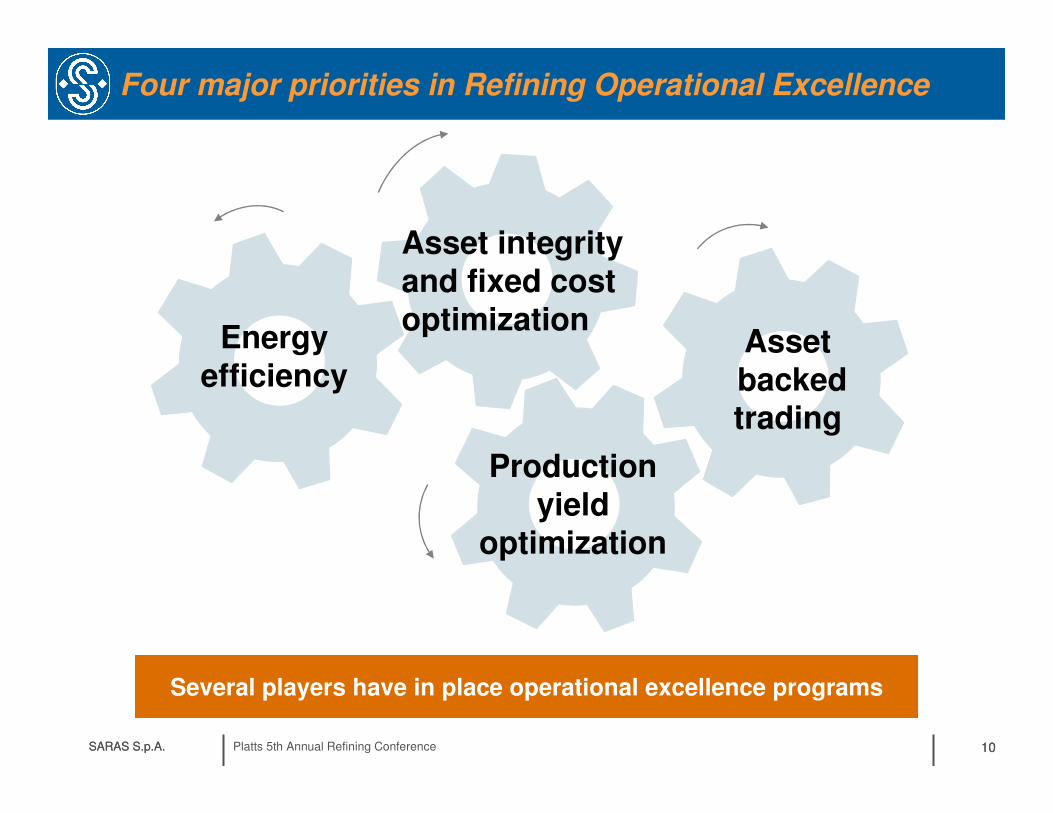

Four major priorities in Refining Operational Excellence

SARAS S.p.A. 10

Asset integrity and fixed cost optimization

Energy efficiency

Assetbacked trading

Production yield

optimization

Several players have in place operational excellence programs

SARAS S.p.A. Platts 5th Annual Refining Conference 11

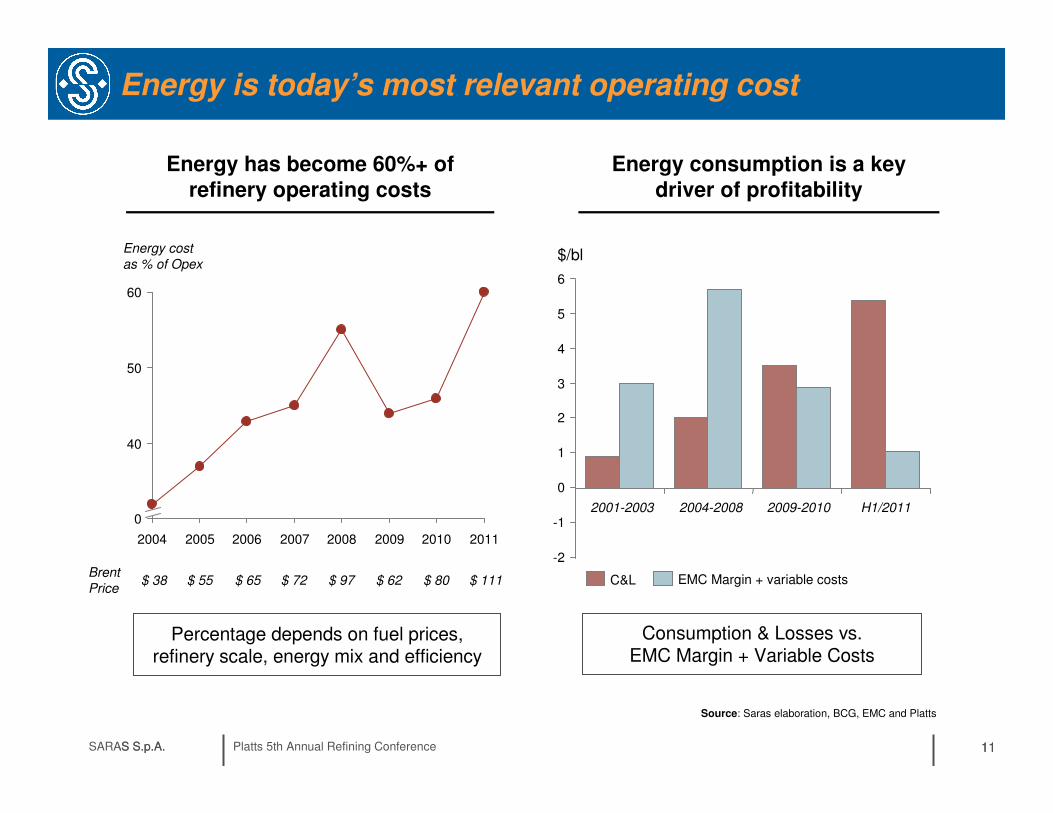

Energy is today’s most relevant operating cost

11

Energy has become 60%+ of

refinery operating costs

Percentage depends on fuel prices, refinery scale, energy mix and efficiency

60

50

40

0

2010200920082007200620052004

Energy costas % of Opex

$ 38 $ 55 $ 65 $ 72 $ 97 $ 62 $ 80BrentPrice

Energy consumption is a key

driver of profitability

11

Source: Saras elaboration, BCG, EMC and Platts

$ 111

$/bl

6

5

4

3

2

1

-2

EMC Margin + variable costsC&L

Consumption & Losses vs. EMC Margin + Variable Costs

SARAS S.p.A.

2011

0

-12001-2003 2004-2008 2009-2010 H1/2011

SARAS S.p.A. Platts 5th Annual Refining Conference 12

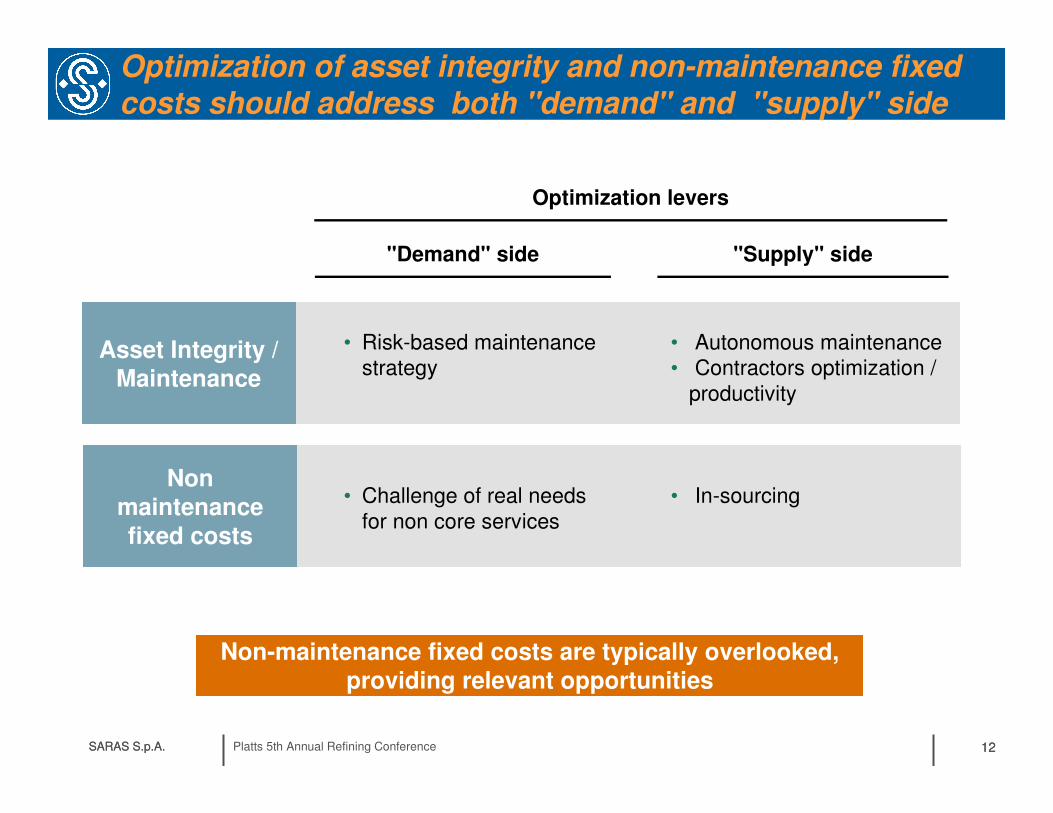

Optimization of asset integrity and non-maintenance fixed costs should address both "demand" and "supply" side

SARAS S.p.A. 12

Non-maintenance fixed costs are typically overlooked, providing relevant opportunities

"Demand" side "Supply" side

Optimization levers

• Autonomous maintenance• Contractors optimization /

productivity

• Risk-based maintenance strategy

• Challenge of real needs for non core services

• In-sourcing

Asset Integrity /

Maintenance

Non

maintenance

fixed costs

SARAS S.p.A. Platts 5th Annual Refining Conference 13

• Margin optimization of the whole supply chain

– Higher integration among Supply& Trading and Refinery Operations

• Exploit market volatility ...

• ... while hedging risk through refinery assets and flexibility

Asset backed trading to exploit volatility while hedging risk

SARAS S.p.A. 13

Leverage crude differentials

Proactive inventory management

• E.g. contango/ backwardation

Typical levers for asset backed trading

Dynamic forward trading

Complex refineries can fully enhance asset backed trading

Related Documents