This material has been produced by RBS sales and trading staff and should not be considered independent. The Round Up 10 November 2009 Issue No. 214 The Round Up is a comprehensive daily note produced by the RBS Warrants team providing an overview of market movements along with quality ideas for warrant traders and investors. In today’s issue Global Market Action Scoreboard, commentary Aussie Market Action SPI Comment, Events & Dividends DJS (DJSSZX) SFI Investment Buy – Upgrade QAN (QANKZJ) MINI Trading Buy – Beneficiary of high AUD QBE (QBESZX) SFI Investment Buy – Investor Update Round Up Corner RBS Monthly Market Review - October Equities Move Last % Move Range Volume ASX 200 +80.9 4674.9 +1.8% +81 to +81 $5.5 bn(A) SPI - yesterday +83.0 4684.0 +1.8% +14 to +92 32,842(A) Dow Jones +203.8 10227.2 +2.0% -3 to +205 Low S&P 500 +23.8 1093.1 +2.2% +3 to +24 Low Nasdaq +41.6 2154.1 +2.0% +16 to +42 Low FTSE +92.5 5235.2 +1.8% u.c to +97 Avg Commodities Move Last % Today % Past Month Oil-WTI spot +1.82 79.25 +2.4% +10.9% Gold Spot +8.00 1103.10 +0.7% +4.9% Nickel (LME) +3.45 787.40 +0.4% -7.1% Aluminium (LME) +1.85 87.02 +2.2% +2.4% Copper (LME) +2.15 295.60 +0.7% +4.8% Zinc (LME) -0.64 96.79 -0.7% +6.0% Silver +0.18 17.56 +1.0% -1.1% Sugar -0.05 21.79 -0.2% +5.4%

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 1/8

This material has been produced by RBS sales and trading staff and should not be considered independent.

The Round Up

10 November 2009Issue No. 214The Round Up is a comprehensive daily note produced by the RBS Warrants

team providing an overview of market movements along with quality ideas forwarrant traders and investors.

In today’s issue

Global Market Action Scoreboard, commentary

Aussie Market Action SPI Comment, Events & Dividends

DJS (DJSSZX) SFI Investment Buy – Upgrade

QAN (QANKZJ) MINI Trading Buy – Beneficiary of high AUD

QBE (QBESZX) SFI Investment Buy – Investor Update

Round Up Corner RBS Monthly Market Review - October

Equities

Move Last % Move Range Volume

ASX 200 +80.9 4674.9 +1.8% +81 to +81 $5.5 bn(A)

SPI - yesterday +83.0 4684.0 +1.8% +14 to +92 32,842(A)

Dow Jones +203.8 10227.2 +2.0% -3 to +205 Low

S&P 500 +23.8 1093.1 +2.2% +3 to +24 Low

Nasdaq +41.6 2154.1 +2.0% +16 to +42 Low

FTSE +92.5 5235.2 +1.8% u.c to +97 Avg

CommoditiesMove Last % Today % Past Month

Oil-WTI spot +1.82 79.25 +2.4% +10.9%

Gold Spot +8.00 1103.10 +0.7% +4.9%

Nickel (LME) +3.45 787.40 +0.4% -7.1%

Aluminium (LME) +1.85 87.02 +2.2% +2.4%

Copper (LME) +2.15 295.60 +0.7% +4.8%

Zinc (LME) -0.64 96.79 -0.7% +6.0%

Silver +0.18 17.56 +1.0% -1.1%

Sugar -0.05 21.79 -0.2% +5.4%

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 2/8

Dual Listed Companies (DLC’s)

Move %Move Last AUD Terms Diff to Aus

NWS (US) +0.37 +2.6% 14.52 15.62 +6.6 c

RIO (UK) +125.0 p +4.3% £30.42 54.79 -1095.7 c

BLT (BHP UK) +72.0 p +4.2% £17.755 31.98 -563.0 c

BXB (UK) +7.3 p +1.9% £3.970 7.15 -2.9 c

American Depository Receipts (ADR’s)

Move %Move Last AUD Terms Diff to Aus

BHP (US) +3.46 +5.1% 71.42 38.41 +79.6 c

AWC (US) +0.34 +5.8% 6.17 1.66 +1.9 c

TLS (US) +0.63 +4.3% 15.25 3.28 +5.0 c

ANZ (US) +0.92 +4.5% 21.33 22.94 +28.0 c

WBC (US) +5.25 +4.4% 124.16 26.71 +42.7 c

NAB (US) +1.58 +6.0% 27.78 29.88 +27.7 c

LGL (US) +1.11 +3.6% 31.91 3.43 +2.2 c

RMD (US) +1.72 +3.6% 49.15 5.29 -4.4 c JHX (US) +2.27 +6.9% 35.28 7.59 +17.9 c

PDN (CAN) +0.19 +4.8% 4.17 4.24 +5.3 c

Overnight Commentary

United States Commentary

A promise from the G20 to maintain stimulus had defence on the back burner overnight. A big showing from theheavyweight cyclicals and financials has the Dow heading toward c13month highs, up 180pts.The S&P around 2% higherand the Nasdaq up 1.7%.

Cyclicals - Anything leveraged to growth outperformed. Caterpillar up 4% and the biggest pt contributor, GE up 3.5%,Alcoa 3.2% higher, Boeing 3.1%, Dupont 3% and Intel heading toward a 2.5% gain. All of the aforementioned featuring inthe Dow's top10.

Financials - Comments from the Fed that fewer banks tightened lending standards in Q3, helped confirm liquiditycontinues to free-up. Amex and BofA both up over 4% and the Dow's best performers, Wells up 4%, Morgan Stanley puton 3.5%, Citi, US Bancorp and Regions all around 2-3% higher.

Retail - Radioshack up 15%(S&P500's best) along the way hitting 2 year highs post a broker upgrade and mgmt flaggingplans to sell iPhones in the US next year.

Retail - Abercrombie&Fitch nearly 8% higher after two broker upgrades. One upgrade from "neutral" to "outperform" andthe other, citing potential upside from international sales, saw the stock added to the brokers "Conviction Buy" list.

FX - The DXY index down 0.7c hitting a new 15month low and the AUD nearly 2c higher and back flirting with the 93clevel.

United Kingdom & Europe Commentary

The FTSE, up 1.8% or 92pts, hit its highest close in more than 2 weeks with the continued stimulus packages pledged atthe G20 helping investor sentiment. The FTSE Eurofirst 300 jumped 2%, the DAX was up 2.4% and the CAC ended 2.1%higher.

UK Banks - The G20 pledge to continue support until recovery was assured helped the banks. RBS soared 6.3%, Lloydswas up 0.5% and Standard Chartered climbed 0.8%. Positive 3Q trading statements from HSBC and Barclays, up 1.3%and 1.9% respectively, also helped.

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 3/8

Euro Banks - The G20 news also helped banks on the continent. Deutsche Bank jumped 3.4%, Commerzbank soared5.8%, BNP was up 2.8%, SocGen added 4.1$ and UniCredit ended 5.3% higher.

Insurers - The bid for AXA Aust by the parent saw traders highlight the value of Prudential's Asian business. Prudential jumped 5.2%, Aviva climbed 3%, L&G added 4.3%, Standard Life rose 3.7% and Old Mutual ended 3.8% higher.Germany's Allianz, up 4.3%, beat forecasts which helped the sector on the continent. Hannover Re was up 1.8% with thestock also benefiting from a broker upgrade and Munich Re rose 1.1%. AXA SA, up 0.4%, launched a €2bn rights issue tfund an "aggressive" acquisition strategy.

Eco - German Industrial Production surged 2.7% for the month vs 1% expected whilst the YoY number was -12.9% vs -14.4% expected. The Bank of France Business Sentiment climbed for the 8 consecutive month with the Bank saying theFrench economy will probably expand by 0.5% in Q4.

Commodiites Commentary

Miners - The sector added the most points to the index with a weak $US helping metal prices. BHP climbed 4.2%, Riowas up 4.3%, Anglo also rose 4.3%, Xstrata added 5% and Randgold ended 4% higher with gold hitting fresh all timehighs.

Energy - Crude climbed 3% rising above $80 briefly which helped the majors. Shell was up 2.3%, BP climbed 1.9%, BGroup added 0.8% and Tullow ended 2.8% higher. In Europe Total climbed 2.1%, Statoil was up 2.9% and Repsol ended1.3% higher.

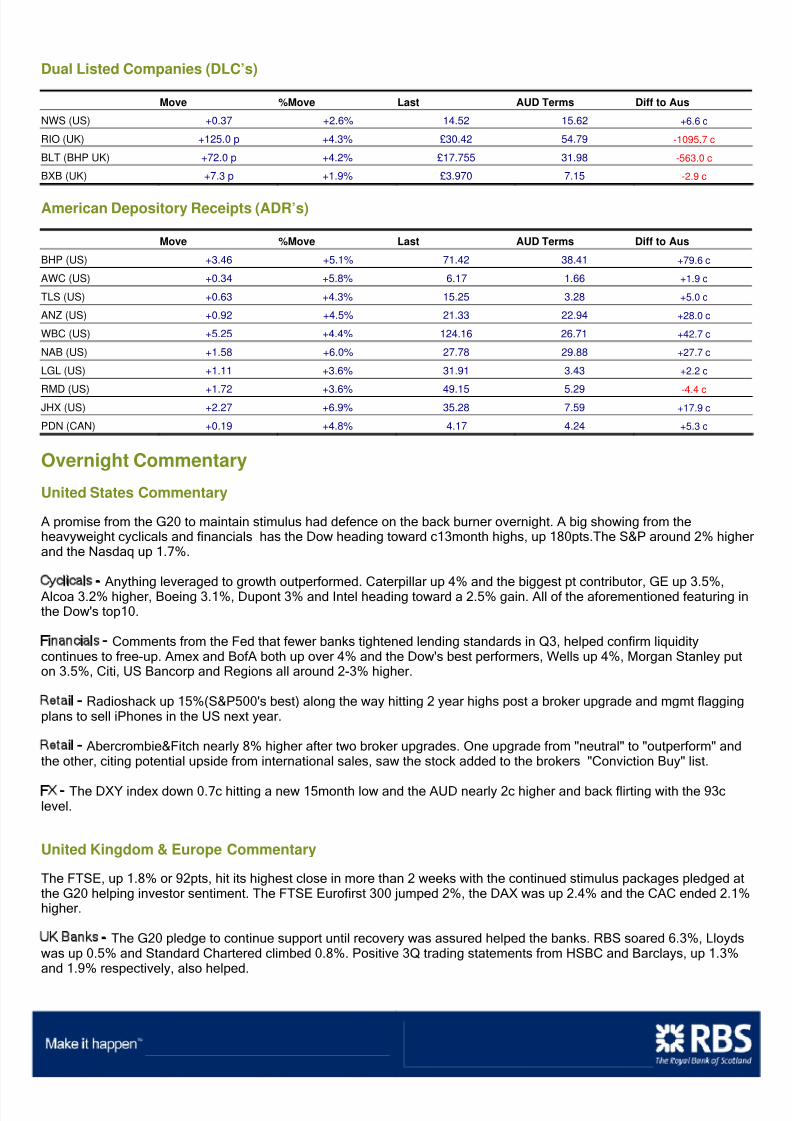

SPI Commentary

The SPI traded up 83pts or 1.8% to 4684. Open at 4615 with a low of 4615 and a high of 4693. Volume 31,306. Overnight the SPIclosed up 78 to 4762.

SPI Intraday SPI Daily

*SPI report taken from the 9:50am open to the 4:30pm close on the previous trading day. Charts taken from IRESS

Upcoming Economic Events for the Week

Monday AUS RBA Gov Lowe speaks, ANZ job ads, investor home loans, owner occ housing finance

US

Tuesday AUS RBA’s Broadbent speaks, NAB business confidence, NAB business conditions

US

Wednesday AUS WMI consumer confidence

US Veterans’ Day holiday

Thursday AUS Employment and unemployment

US

Friday AUS

US Trade balance, import prices, Michigan cons confidence

*Dates are indicative only and may change

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 4/8

SFI Investment Buy:

David Jones (DJSSZX) - Upgrade

RBS Research have upgraded DJS to a Buy, believing market forecasts do not sufficiently reflect the operationalleverage DJS should enjoy as consumer spending rebounds through FY11F and FY12F. Shorter term we see positivecatalysts in upgraded FY10 and 'aspirational through-the-cycle' operational guidance. Use the recent pullback to buy DJS

for a move back up through $6. Play through DJSSZX

Source: IRESS

RBS Research believe DJS is likely to surprise the market in FY10F with an increase to its through-the-cycle grossmargin guidance of 39.5-40.0% with upgraded FY10F guidance likely, from 0-5% to 5-10% underlying NPAT growth..

RBS research believe DJS can achieve a through-the-cycle sustainable gross margin of up to 41.0% (currently 39.6%)and a cash CODB of 27.5% (currently 28.1%)..

DJS is present in only 16 of Australia’s top-30 shopping centres by turnover. Excluding those to be entered as part of thepreviously disclosed store-rollout programme, RBS Research have identified a further six that we believe havedemographics attractive to DJS and that would be unlikely to significantly cannibalise the company’s existing store sales.

RBS Research upgrade NPAT forecasts as follows: FY10 +1.0% to A$170.5m; FY11 +0.4% to A$193.3m; FY12 +6.9% toA$220.5m. RBS now sit 5.5% and 10.4% above FY11F and FY12F consensus Bloomberg EPS forecasts, respectively.Target price to A$6.40

Buy DJSSZX

RBS SFIs over DJS

Security ExDate ExPrc CP ConvFac Delta Description

DJSSZX 4-Feb-19 169 Call 1 0 Rbs Feb19 169 I W

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 5/8

MINI Trading Buy:

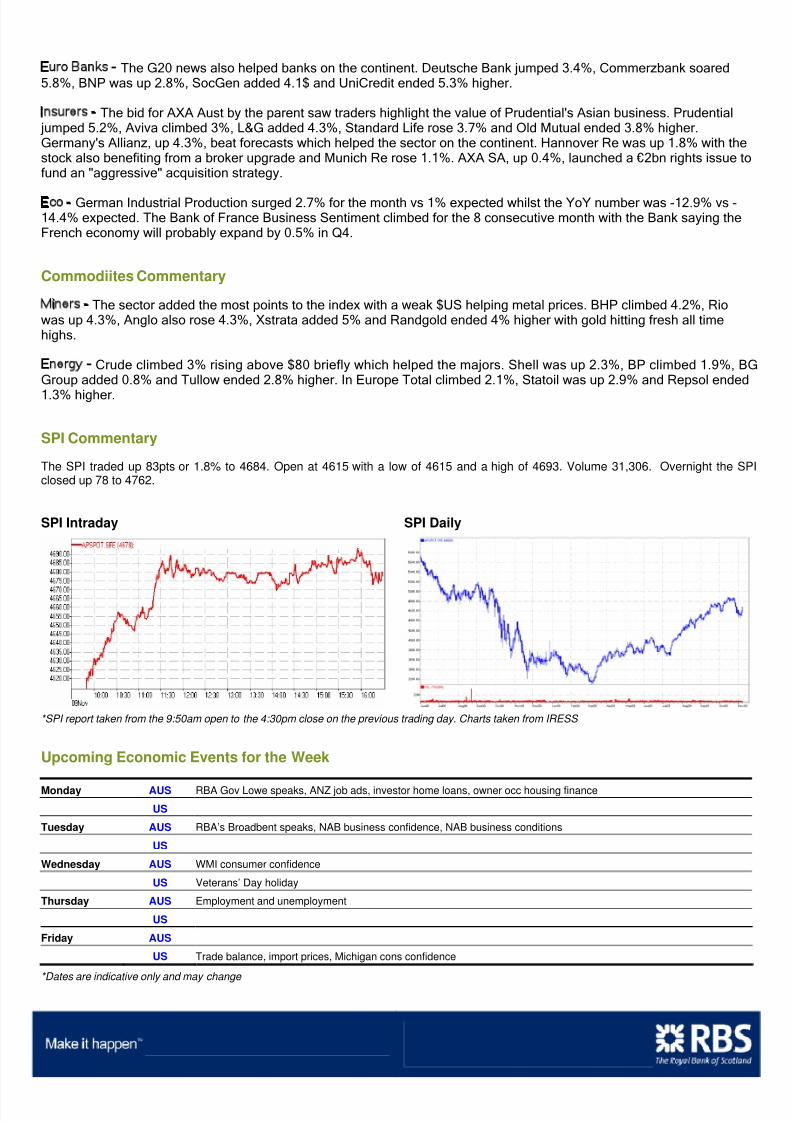

Qantas Airways (QANKZJ) – Load factor and yields improving

QAN is leveraged to an economic recovery and is a big beneficiary of the appreciating AUD/USD. Comments at QAN’sAGM suggest management is confident it has passed the worst. Updated currency forecasts result in earnings upgradesfor FY10-11F. Given strengthening economic conditions and higher currency, RBS Research maintain Buy

recommendation with $3.35 target price. September traffic statistics also highlighted increased load factors andimprovements to domestic yields. Use the recent pullback to buy QAN. Play thorugh QANKZJ

Source: IRESS

QAN management appears increasingly confident that the worst is behind the company. The next critical piece ofinformation is to see yield improvement, which RBS Research believe may become evident in 2H10 as demand hasstabilised and the worst of the discounting appears to have passed.

QAN is also a beneficiary of a rising AUD/USD. With an estimated 39% of QAN’s cost base exposed to the USD,earnings are positively impacted. Given the spot price sits at $0.92, further earnings upside potential exists. On RBSestimates a 1c increase in the AUD equates to a A$14m increase in NPAT (4.3%).

RBS Research has a Buy recommendation on QAN with a target price of $3.35. With the economic environmentstrengthening and currency movements positively impacting the cost base, we think there remains momentum behind theairlines.

Buy QANKZJ

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 6/8

SFI Investment Buy:

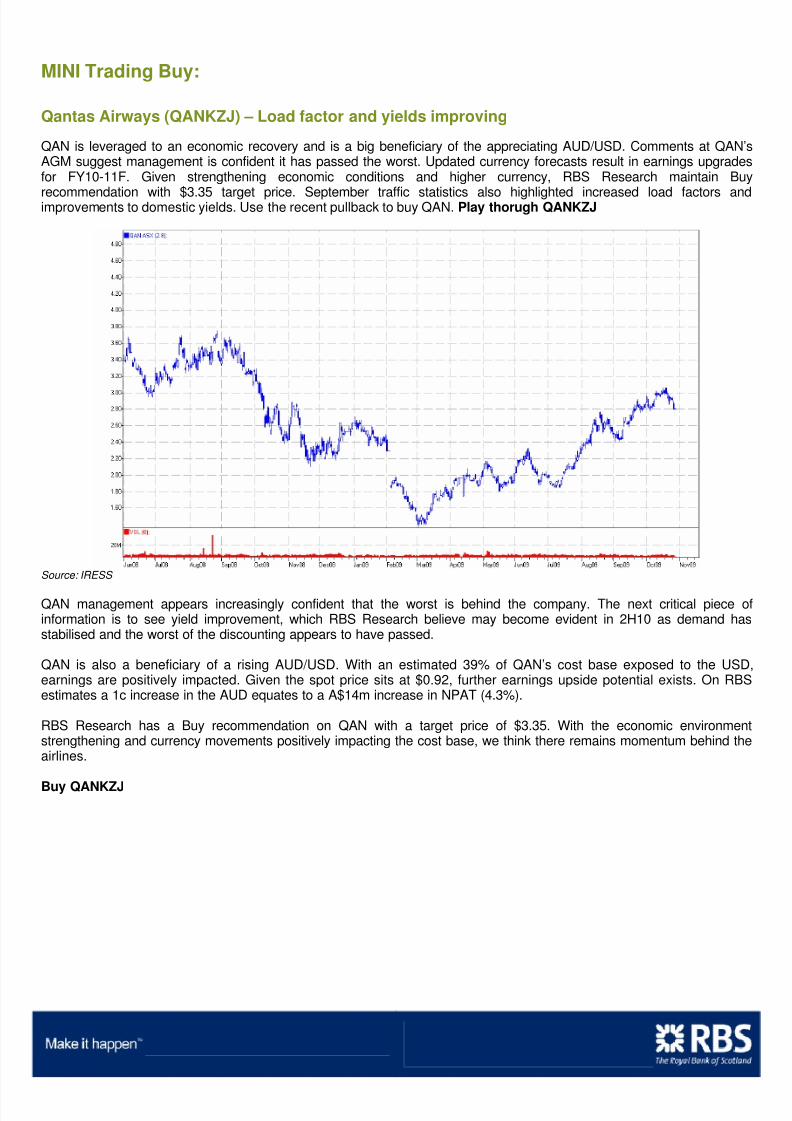

QBE Insurance Group (QBESZX) – Investor Update

We believe the recent pullback in QBE is a buying opportunity. QBE has reiterated its FY09 guidance for an insurancemargin of 17-18%. Management has also said it has additional debt capacity for cA$1bn in acquisitions. RBS Researchhave a target price of $26.11. Buy QBESZX

Source: IRESS

• QBE reaffirmed its full-year FY09 guidance for an insurance margin of 17-18%.• QBE says it has cA$1bn in debt capacity available for acquisitions with gearing currently only c30%. Bolt-on

acquisitions appear to remain the most attractive, while management has not ruled out further agency purchases.• QBE has said US and UK insurance markets remain soft, although they expect rates to harden in 2H10• QBE’s track record in underwriting and acquisition execution remains excellent. The company has reconfirmed its

FY09 guidance and has a strong balance sheet with cA$1bn of debt capacity available for acquisitions. At A$22.15the stock continues to trade at a discount to RBS price target of A$26.11. We see value in QBE at these levels

• Use the pullback to buy through QBESZX

RBS SFIs over QBE

Security ExDate ExPrc CP ConvFac Delta Description

QBESZX 4-Feb-19 1140.01 Call 1 1 Self Funding Instalment

RBS MINIs over QBE

Security ExPrc Stop Loss CP ConvFac Delta Description

QBEKZF 1219 Long 1 1 MINI Long

QBEKZK 1124.7 Long 1 1 MINI Long

QBEKZL 1792.43 Long 1 1 MINI Long

QBEKZR 3147.08 Short 1 1 MINI Short

QBEKZS 3376.24 Short 1 1 MINI Short

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 7/8

RBS Round Up Corner:

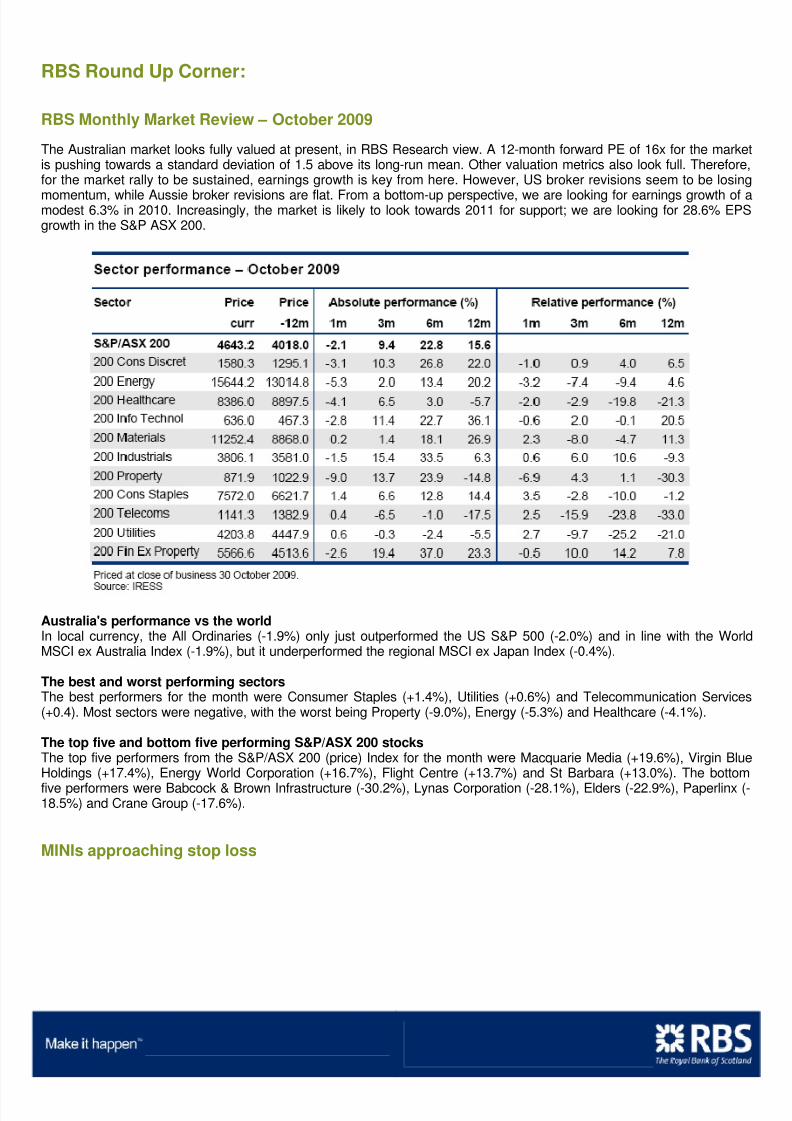

RBS Monthly Market Review – October 2009

The Australian market looks fully valued at present, in RBS Research view. A 12-month forward PE of 16x for the marketis pushing towards a standard deviation of 1.5 above its long-run mean. Other valuation metrics also look full. Therefore,for the market rally to be sustained, earnings growth is key from here. However, US broker revisions seem to be losing

momentum, while Aussie broker revisions are flat. From a bottom-up perspective, we are looking for earnings growth of amodest 6.3% in 2010. Increasingly, the market is likely to look towards 2011 for support; we are looking for 28.6% EPSgrowth in the S&P ASX 200.

Australia's performance vs the worldIn local currency, the All Ordinaries (-1.9%) only just outperformed the US S&P 500 (-2.0%) and in line with the WorldMSCI ex Australia Index (-1.9%), but it underperformed the regional MSCI ex Japan Index (-0.4%).

The best and worst performing sectorsThe best performers for the month were Consumer Staples (+1.4%), Utilities (+0.6%) and Telecommunication Services(+0.4). Most sectors were negative, with the worst being Property (-9.0%), Energy (-5.3%) and Healthcare (-4.1%).

The top five and bottom five performing S&P/ASX 200 stocksThe top five performers from the S&P/ASX 200 (price) Index for the month were Macquarie Media (+19.6%), Virgin BlueHoldings (+17.4%), Energy World Corporation (+16.7%), Flight Centre (+13.7%) and St Barbara (+13.0%). The bottomfive performers were Babcock & Brown Infrastructure (-30.2%), Lynas Corporation (-28.1%), Elders (-22.9%), Paperlinx (-18.5%) and Crane Group (-17.6%).

MINIs approaching stop loss

8/14/2019 RBS - Round Up - 101109

http://slidepdf.com/reader/full/rbs-round-up-101109 8/8

For further information please do not hesitate to contact us on the details below

Equities Structured Products & Warrants

Toll free 1800 450 005 www.rbs.com.au/warrantsTrading Products Team

Ben Smoker 02 8259 2085 [email protected]

Robbie Taylor 02 8259 2018 [email protected]

Ryan Corrigan 02 8259 2425 [email protected]

Investment Products Team

Elizabeth Tian 02 8259 2017 [email protected]

Tania Smyth 02 8259 2023 [email protected]

Robert Deutsch 02 8259 2065 [email protected]

Mark Tisdell 02 8259 6951 [email protected]

Disclaimer :

The information contained in this report has been prepared by RBS Equities (Australia) Limited (“RBS”) (ABN 84 002 768 701) (AFS Licence No240530) (“RBS Equities”) and has been taken from sources believed to be reliable. RBS Equities does not make representations that the information isaccurate or complete and it should not be relied on as such. Any opinions, forecasts and estimates contained in this report are the views of RBSEquities at the date of issue and are subject to change without notice. RBS Equities and its affiliated companies may make markets in the securitiesdiscussed. RBS Equities, its affiliated companies and their employees from time to time may hold shares, options, rights and warrants on any issuecontained in this report and may, as principal or agent, sell such securities. RBS Equities may have acted as manager or co-manager of a publicoffering of any such securities in the past three years. RBS Equities’ affiliates may provide, or have provided banking services or corporate finance tothe companies referred to in this report. The knowledge of affiliates concerning such services may not be reflected in this report. This report does notconstitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment. RBS Equities,in preparing this report, has not taken into account an individual client’s investment objectives, financial situation or particular needs. Before a clientmakes an investment decision, a client should, with or without RBS Equities’ assistance, consider whether any advice contained in this report isappropriate in light of their particular investment needs, objectives and financial circumstances. It is unreasonable to rely on any recommendationwithout first having consulted with your adviser for a personal securities recommendation. This information contained in this report is general adviceonly. RBS Equities, its officers, directors, employees and agents accept no liability for any loss or damage arising out of the use of all or any part of theinformation contained in this report. This Information is not intended for distribution to, or use by any person or entity in any jurisdiction or country wheresuch distribution or use would be contrary to local law or regulation. If you are located outside Australia and use this Information, you are responsiblefor compliance with applicable local laws and regulation. This report may not be taken or distributed, directly or indirectly into the United States, or toany U.S. person (as defined in Regulation S under the U.S. Securities Act of 1993, as amended.

The warrants contained in this report are issued by RBS Group (Australia) Pty Limited (ABN 78 000 862 797, AFS Licence No. 247013). The ProductDisclosure Statements relating to these warrants are available upon request from RBS Equities or on our website www.rbs.com.au/warrants

© Copyright 2009. RBS Equities. A Participant of the ASX Group.

Explanation of Warrant Tables :

Security – refers to the code ascribed to the warrant, ExDate – refers to the date on which the warrant expires or is reset, ExPrc – refers to theexercise price, or second instalment payment, CP – tells you whether the warrant is a call or a put, ConvFac – the conversion factor of the warrantwhich tells you how many warrants you need to exercise in order to take possession of 1 share, Delta – tells you how much the warrant will move for a

1c move in the underlying security, Description – Tells you the type of warrant.All charts taken from IRESS unless indicated otherwise

ContactContact

Related Documents