Raymond James Energy Group Raymond James Energy Group “Is The Stock Market or “Is The Stock Market or the Futures Market Correct?” the Futures Market Correct?” [email protected] [email protected] [email protected] [email protected] [email protected] [email protected] Raymond James Oilservice Group Raymond James Oilservice Group (800) 945-6275 (800) 945-6275 June 2006

Raymond James Energy Group “Is The Stock Market or the Futures Market Correct?” [email protected]@[email protected].

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Raymond James Energy GroupRaymond James Energy Group

“Is The Stock Market or “Is The Stock Market or the Futures Market Correct?”the Futures Market Correct?”

[email protected]@[email protected]@RaymondJames.com

[email protected]@RaymondJames.comRaymond James Oilservice GroupRaymond James Oilservice Group(800) 945-6275 (800) 945-6275 June 2006

Short-term Outlook (next 6 months)Short-term Outlook (next 6 months)Increasingly Bullish!Increasingly Bullish!

Investor sentiment: never been more bearish Investor sentiment: never been more bearish – U.S. gas fearsU.S. gas fears

Technical support levels have held firmTechnical support levels have held firm– Stocks bounced off their 200 day moving avg.Stocks bounced off their 200 day moving avg.

Fundamentals are strong & improvingFundamentals are strong & improving– Strong upward earningsStrong upward earnings– Gas storage situation is improvingGas storage situation is improving– No indication of a slow downNo indication of a slow down

2

Long-term Energy Outlook (6-18 months)Long-term Energy Outlook (6-18 months)Still Very Bullish! Still Very Bullish!

Gas resets in NovemberGas resets in November

Oil supply/demand remains tight Oil supply/demand remains tight – even with an economic slowdown & more drillingeven with an economic slowdown & more drilling

Supply response is anemicSupply response is anemic– Both U.S. gas & global oilBoth U.S. gas & global oil

Geopolitical issues are Geopolitical issues are NOTNOT going away going away

3

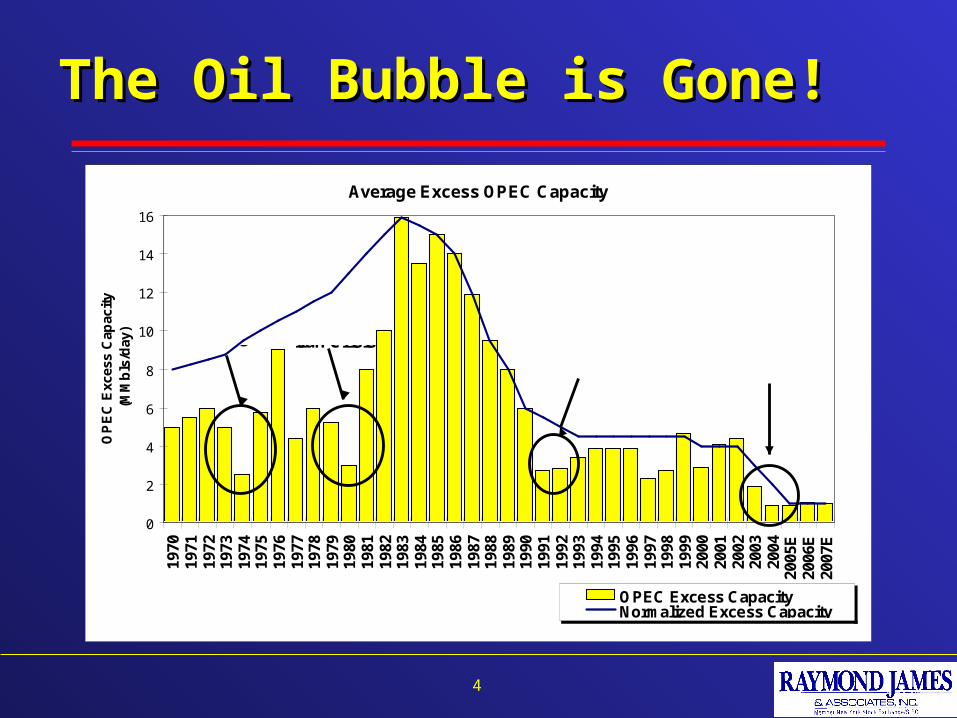

The Oil Bubble is Gone!The Oil Bubble is Gone!

4

Average Excess OPEC Capacity

0

2

4

6

8

10

12

14

16

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

E20

06E

2007

E

OP

EC

Exc

ess

Cap

acit

y(M

Mb

ls/d

ay)

OPEC Excess CapacityNormalized Excess Capacity

Sources: IEA, RJ&A, Bloomberg

Arab Embargo Iran Crisis

Kuwait WarDemand Growth

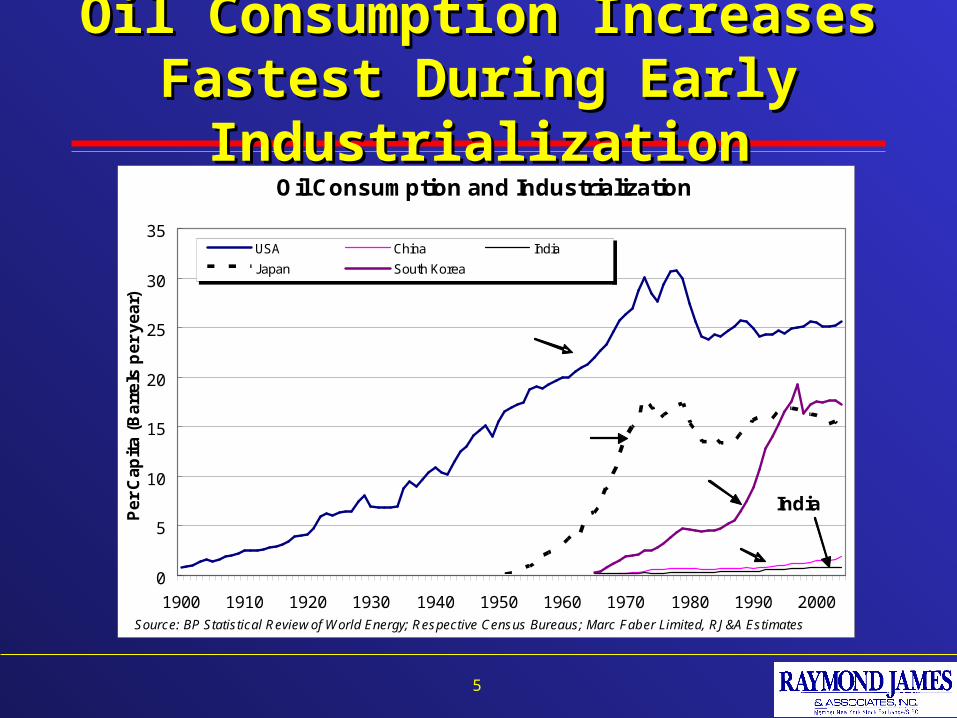

Oil Consumption Increases Fastest Oil Consumption Increases Fastest During Early IndustrializationDuring Early Industrialization

5

Oil Consumption and Industrialization

0

5

10

15

20

25

30

35

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Pe

r C

ap

ita

(B

arr

els

pe

r y

ea

r)

USA China India

Japan South Korea

USA

Japan

South Korea

China

India

Source: BP Statistical Review of World Energy; Respective Census Bureaus; Marc Faber Limited, RJ&A Estimates

Russian Oil Production Russian Oil Production GrowthGrowth Slowing Slowing

6

Russian Oil Production Growth (Year-Over-Year)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1998 1999 2000 2001 2002 2003 2004 2005 2006E 2007E

Mil

lio

n b

arre

ls p

er d

ay

Source: IEA, RJ&A Estimates

??

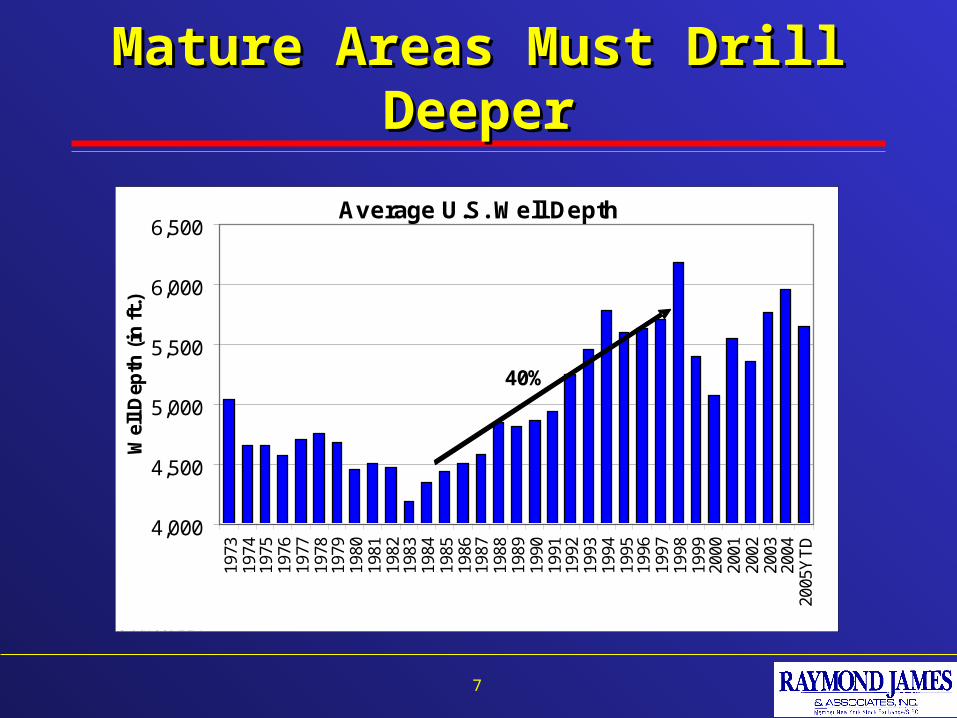

Mature Areas Must Drill DeeperMature Areas Must Drill Deeper

7

Average U.S. Well Depth

4,000

4,500

5,000

5,500

6,000

6,50019

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

05Y

TD

Wel

l Dep

th (

in f

t.)

Source: EIA

40%

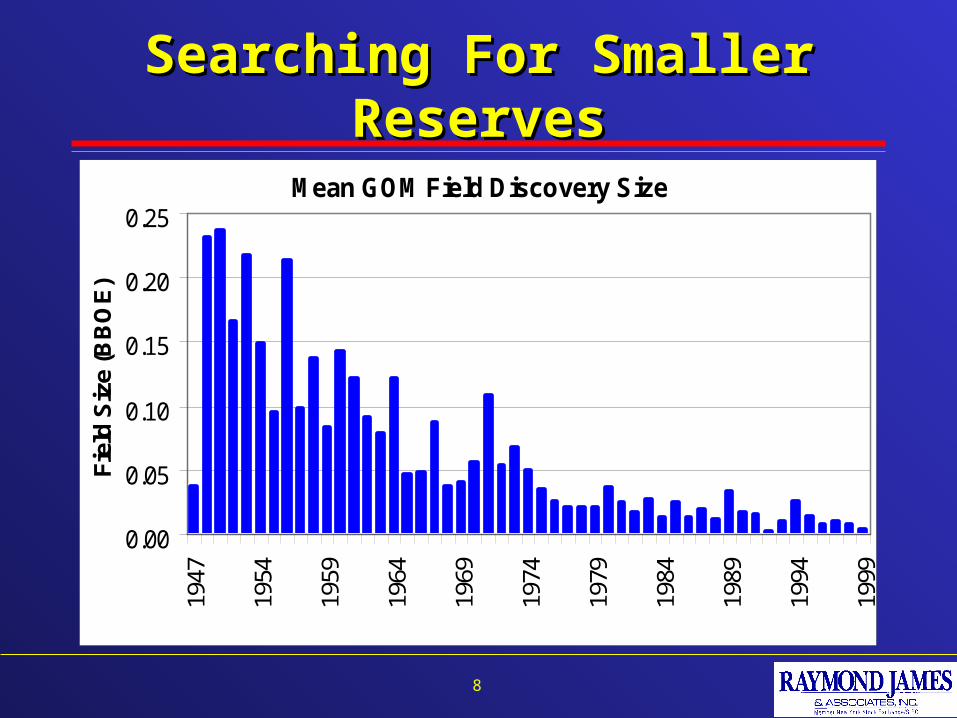

Searching For Smaller ReservesSearching For Smaller Reserves

8

Mean GOM Field Discovery Size

0.00

0.05

0.10

0.15

0.20

0.2519

47

1954

1959

1964

1969

1974

1979

1984

1989

1994

1999

Fiel

d S

ize

(BB

OE

)

Source: Minerals Management Service.

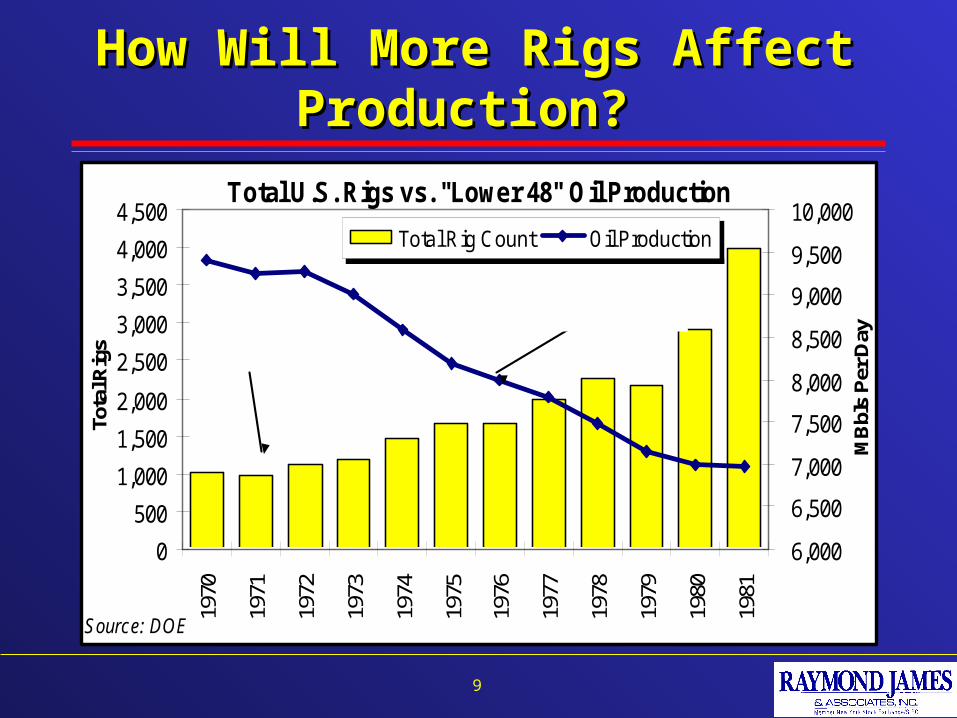

How Will More Rigs Affect Production?How Will More Rigs Affect Production?

9

Total U.S. Rigs vs. "Lower 48" Oil Production

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,50019

70

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

Source: DOE

Tota

l Rig

s

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

MB

bls

Per

Day

Total Rig Count Oil Production

Total Rigs

"Lower 48" Oil Production

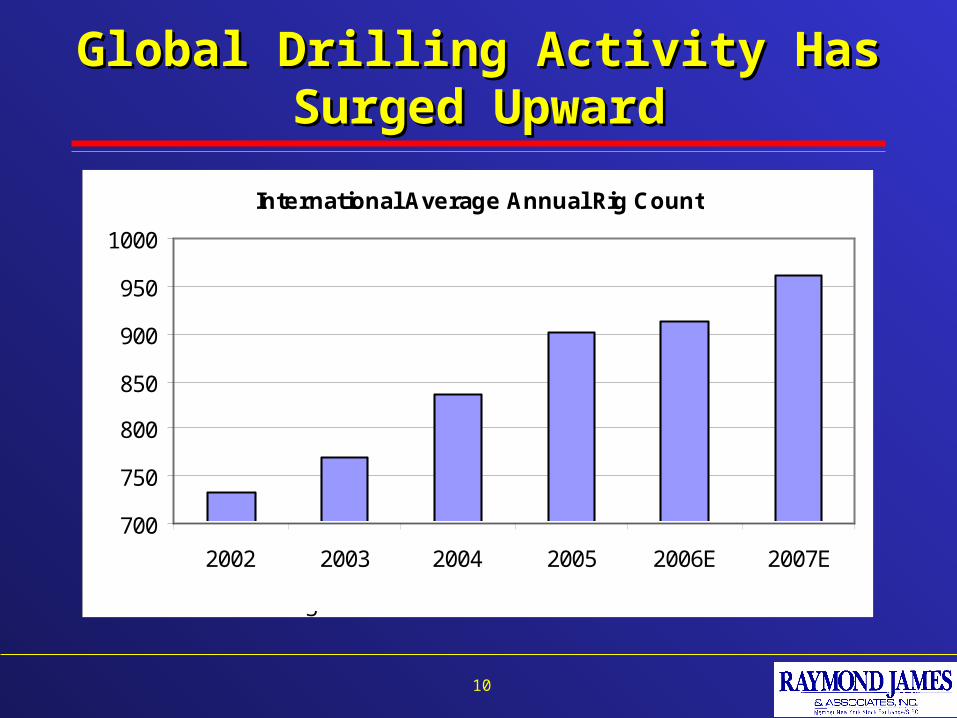

Global Drilling Activity Has Surged UpwardGlobal Drilling Activity Has Surged Upward

10

International Average Annual Rig Count

700

750

800

850

900

950

1000

2002 2003 2004 2005 2006E 2007E

Source: Baker Hughes

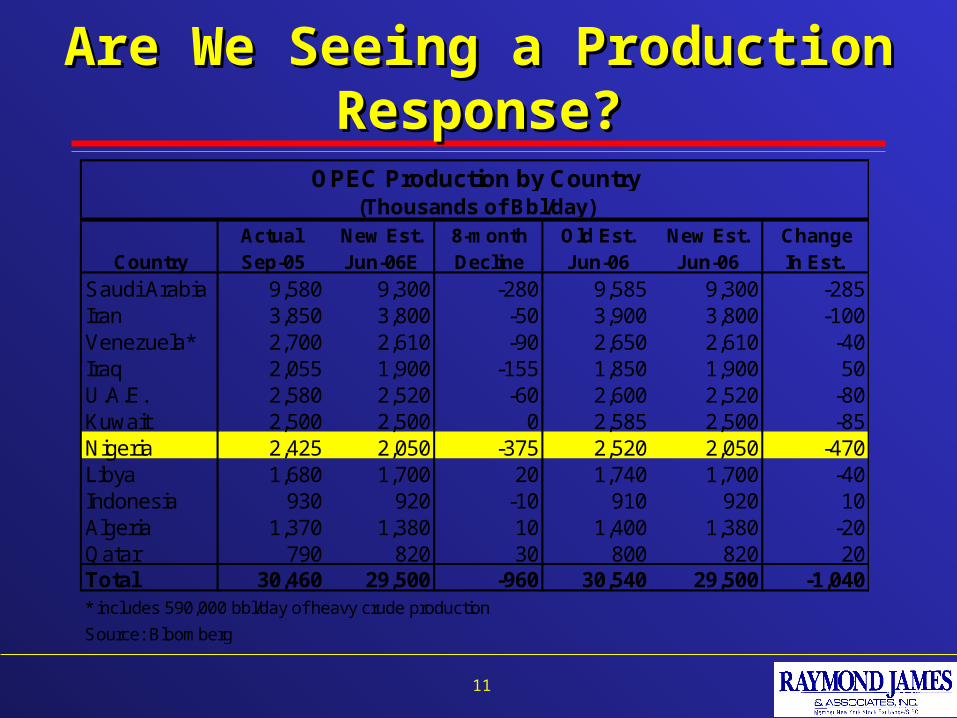

Are We Seeing a Production Response?Are We Seeing a Production Response?

11

Actual New Est. 8-month Old Est. New Est. ChangeCountry Sep-05 Jun-06E Decline Jun-06 Jun-06 In Est.

Saudi Arabia 9,580 9,300 -280 9,585 9,300 -285Iran 3,850 3,800 -50 3,900 3,800 -100Venezuela* 2,700 2,610 -90 2,650 2,610 -40Iraq 2,055 1,900 -155 1,850 1,900 50U.A.E. 2,580 2,520 -60 2,600 2,520 -80Kuwait 2,500 2,500 0 2,585 2,500 -85Nigeria 2,425 2,050 -375 2,520 2,050 -470Libya 1,680 1,700 20 1,740 1,700 -40Indonesia 930 920 -10 910 920 10Algeria 1,370 1,380 10 1,400 1,380 -20Qatar 790 820 30 800 820 20Total 30,460 29,500 -960 30,540 29,500 -1,040* includes 590,000 bbl/day of heavy crude production

Source: Bloomberg

OPEC Production by Country(Thousands of Bbl/day)

Today’s Oil OutlookToday’s Oil Outlook

12

Days of Supply (U.S.) New Estimate

29.0

31.0

33.0

35.0

37.0

39.0

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Da

ys

of

Su

pp

ly (

U.S

.)

5 Yr Range 5 Yr AVG 2005 2006 E 2006 Actual

Source: API.

Source: EIA, RJ&A Estimates

2006 E

2005 A

2006 A

Geo Area 03/'05 Avg. 2006E 2007ENorth America 1.8% 0.5% 1.0%

Europe 0.6% 0.8% 0.5%

Pacific 0.0% 0.5% 1.0%

FSU 3.0% 2.8% 0.0%China 10.1% 6.0% 5.0%

Other Asia 3.6% 1.8% 2.5%

Latin America 1.4% 1.9% 1.5%

Middle East 3.3% 6.2% 3.5%

Africa 2.5% 2.9% 1.0%

Source: IEA

Y/Y Demand Percentage Change

What if We Have a Global Slowdown?What if We Have a Global Slowdown?

13

Where is the Price Floor?Where is the Price Floor?(OPEC Will Defend $55 or Higher)(OPEC Will Defend $55 or Higher)

14

Rising Saudi infrastructure costsRising Saudi infrastructure costs

Higher shipping costsHigher shipping costs

Widening differential for poor quality crudesWidening differential for poor quality crudes

Devaluation of the U.S. $ Devaluation of the U.S. $

– Less OPEC purchasing powerLess OPEC purchasing power

• Cheaper international oil pricesCheaper international oil prices

OPEC wants highest price w/o demand destructionOPEC wants highest price w/o demand destruction

Discounts on Heavy Oil Have WidenedDiscounts on Heavy Oil Have Widened

15

Discount From WTI Price for Maya (Heavy) Crude

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Pri

ce p

er B

arre

l

Source: Bloomberg

Light/Heavy Spread

Historic Average Spread = ~$5

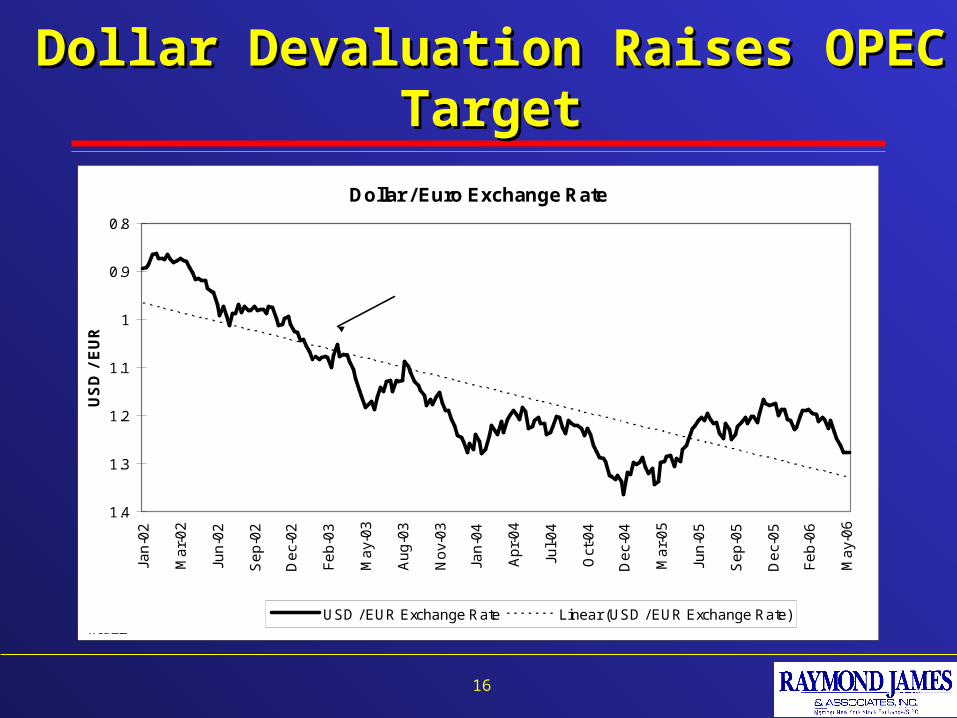

Dollar Devaluation Raises OPEC TargetDollar Devaluation Raises OPEC Target

16

Dollar / Euro Exchange Rate

0.8

0.9

1

1.1

1.2

1.3

1.4

Jan

-02

Ma

r-0

2

Jun

-02

Se

p-0

2

De

c-0

2

Fe

b-0

3

Ma

y-0

3

Au

g-0

3

No

v-0

3

Jan

-04

Ap

r-0

4

Jul-

04

Oct

-04

De

c-0

4

Ma

r-0

5

Jun

-05

Se

p-0

5

De

c-0

5

Fe

b-0

6

Ma

y-0

6

US

D /

EU

R

USD / EUR Exchange Rate Linear (USD / EUR Exchange Rate)Source: OANDA.com, Reuters

Dollar is down 42% since Dec 2001

USD/EUR

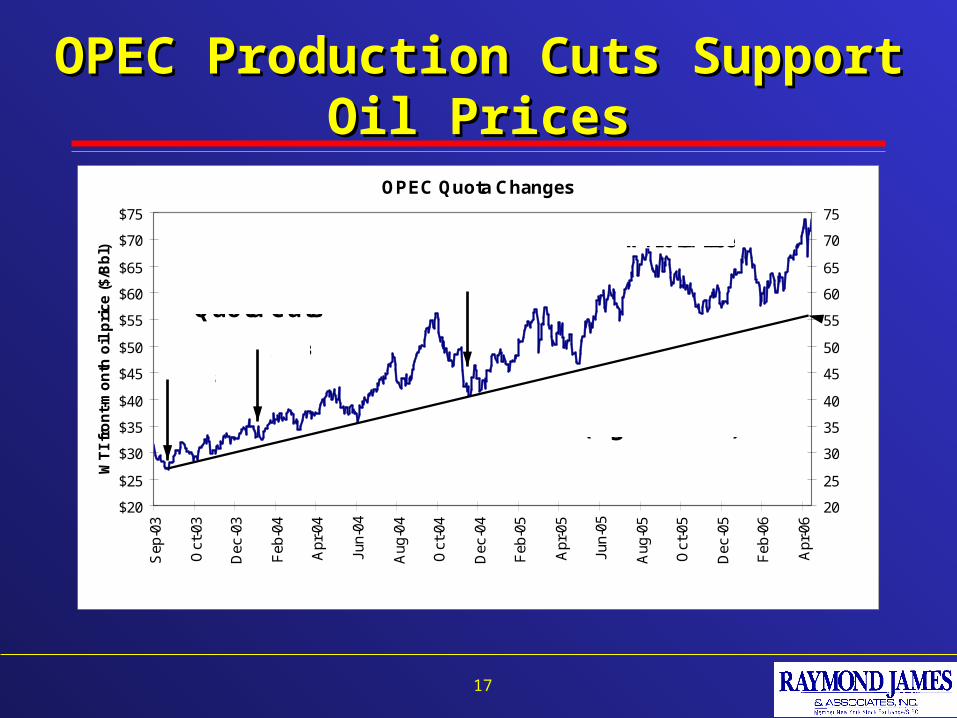

OPEC Production Cuts Support Oil PricesOPEC Production Cuts Support Oil Prices

17

OPEC Quota Changes

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

Sep

-03

Oct

-03

Dec

-03

Feb

-04

Apr

-04

Jun-

04

Aug

-04

Oct

-04

Dec

-04

Feb

-05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb

-06

Apr

-06

WT

I fr

on

t-m

on

th o

il p

rice

($/

Bb

l)

20

25

30

35

40

45

50

55

60

65

70

75

Quota Cuts

Source: Bloomberg

WTI Oil Price

(Higher Lows)

$26.93

$32.83

$42.53

Our Oil Price GuessOur Oil Price Guess

18

Q1 05A Q2 05A Q3 05A Q4 05A 2005AWTI $48.00 $52.00 $60.50 $61.15 $55.41

Estimate Q1 06A Q2 06E Q3 06E Q4 06E 2006EWTI First Call $62.50 $58.37 $58.68 $58.19 $59.44NYMEX Futures $62.50 $64.88 $68.83 $69.61 $66.46WTI Old RJ Oil $62.50 $54.00 $59.00 $62.00 $59.38WTI New RJ Oil $62.50 $65.00 $67.00 $68.00 $65.50

Estimate Q1 07E Q2 07E Q3 07E Q4 07E 2007EWTI First Call $58.00 $56.80 $57.20 $57.20 $57.30NYMEX Futures $69.75 $69.65 $69.62 $69.38 $69.60WTI Old RJ Oil $61.00 $59.00 $63.00 $65.00 $62.00WTI New RJ Oil $70.00 $70.00 $70.00 $70.00 $70.00

RJ&A Oil Price Estimates (as of April 2006)

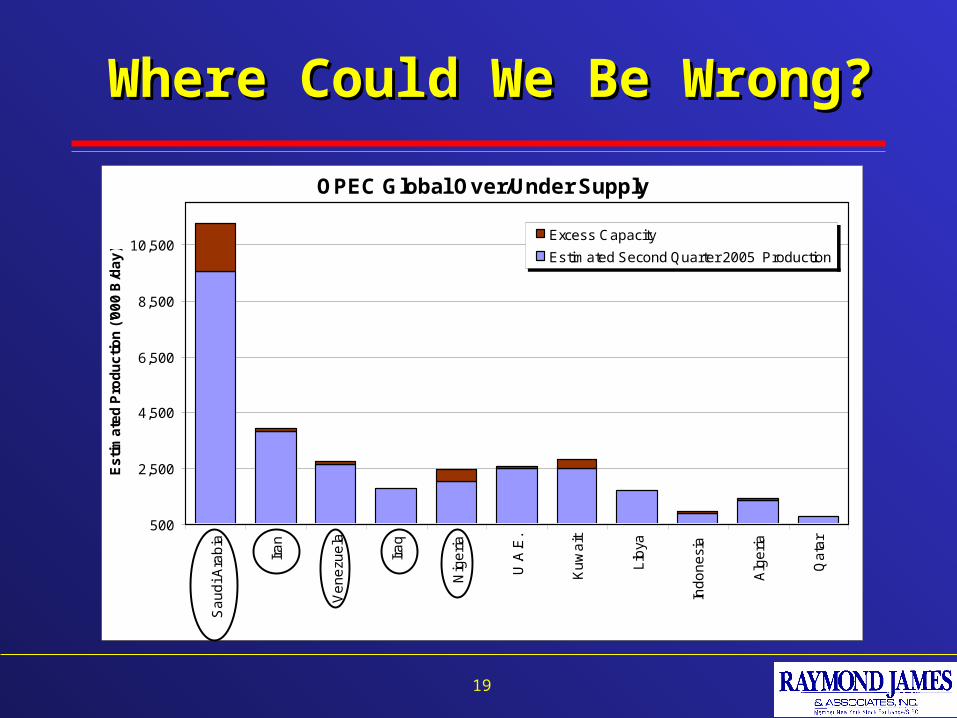

Where Could We Be Wrong?Where Could We Be Wrong?

19

OPEC Global Over/Under Supply

500

2,500

4,500

6,500

8,500

10,500

Sa

ud

i Ara

bia

Ira

n

Ve

ne

zue

la

Ira

q

Nig

eri

a

U.A

.E.

Ku

wa

it

Lib

ya

Ind

on

esi

a

Alg

eri

a

Qa

tar

Es

tim

ate

d P

rod

uc

tio

n (

'00

0 B

/da

y)

Excess Capacity

Estimated Second Quarter 2005 Production

Iran Has Changed the Game! Iran Has Changed the Game!

20

Iran has re-opened nuclear effortsIran has re-opened nuclear efforts

– New leader not backing downNew leader not backing down

U.S. & Israel will U.S. & Israel will NOTNOT let Iran get nuclear weapons let Iran get nuclear weapons

Iran’s 3.9 million Bpd is at riskIran’s 3.9 million Bpd is at risk

Situation should come to a head in 6 - 18 monthsSituation should come to a head in 6 - 18 months

80% probability Iran drives oil higher 80% probability Iran drives oil higher

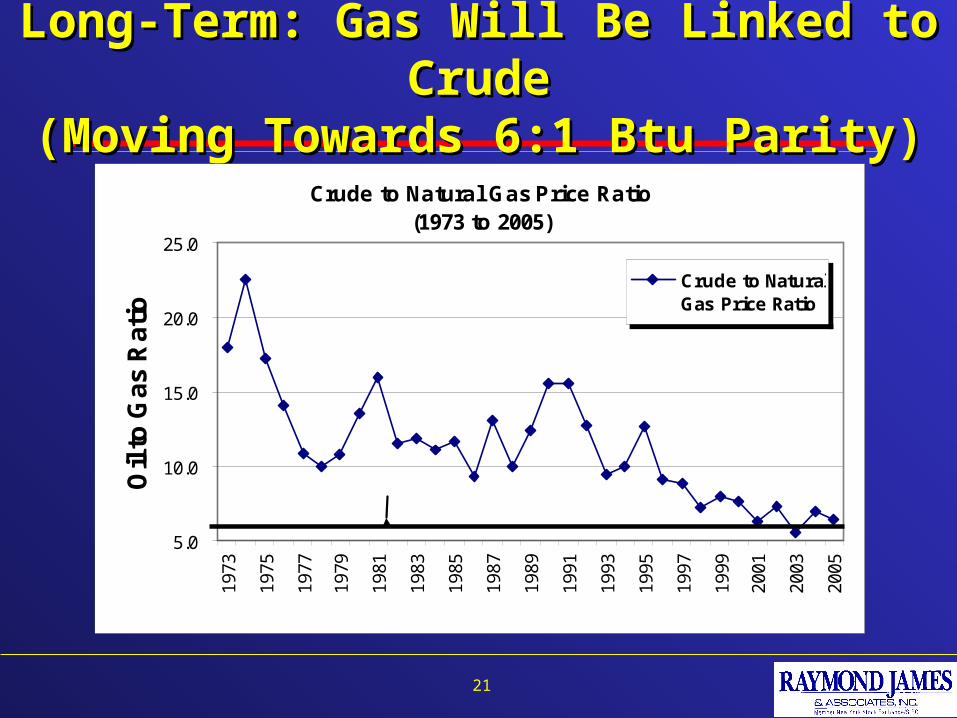

Long-Term: Gas Will Be Linked to CrudeLong-Term: Gas Will Be Linked to Crude(Moving Towards 6:1 Btu Parity)(Moving Towards 6:1 Btu Parity)

21

Crude to Natural Gas Price Ratio(1973 to 2005)

5.0

10.0

15.0

20.0

25.019

73

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Oil

to G

as

Ra

tio

Crude to NaturalGas Price Ratio

Source: Bloomberg, API, EIA

6:1 BTU Parity

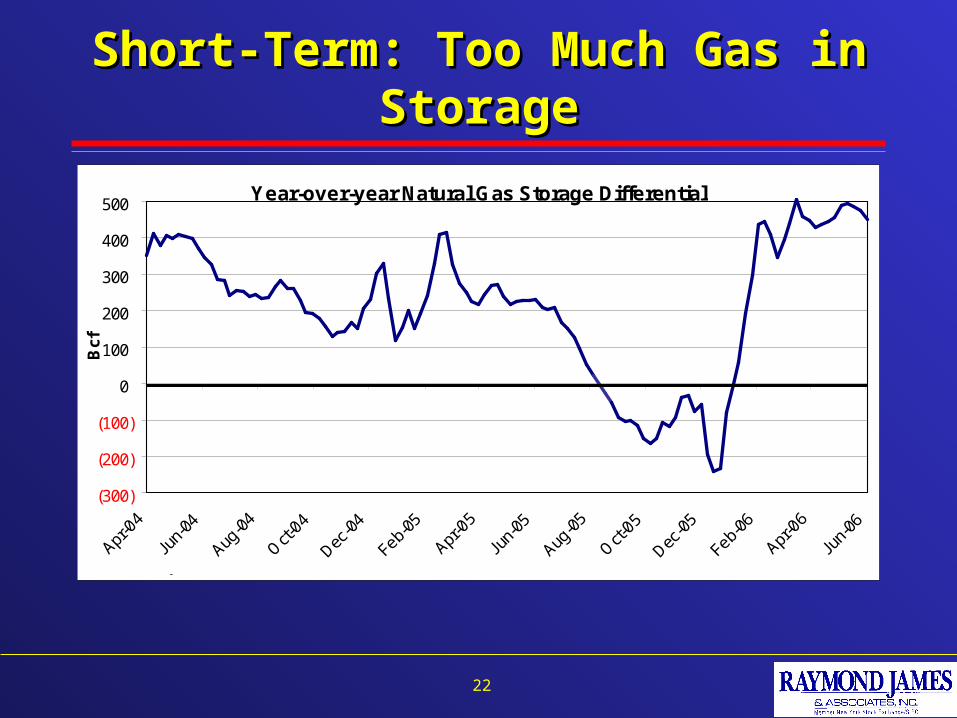

Short-Term: Too Much Gas in StorageShort-Term: Too Much Gas in Storage

22

Year-over-year Natural Gas Storage Differential

(300)

(200)

(100)

0

100

200

300

400

500

Apr-0

4

Jun-

04

Aug-0

4

Oct-

04

Dec-0

4

Feb-05

Apr-0

5

Jun-

05

Aug-0

5

Oct-

05

Dec-0

5

Feb-06

Apr-0

6

Jun-

06

Bcf

Source: EIA, RJ&A estimates

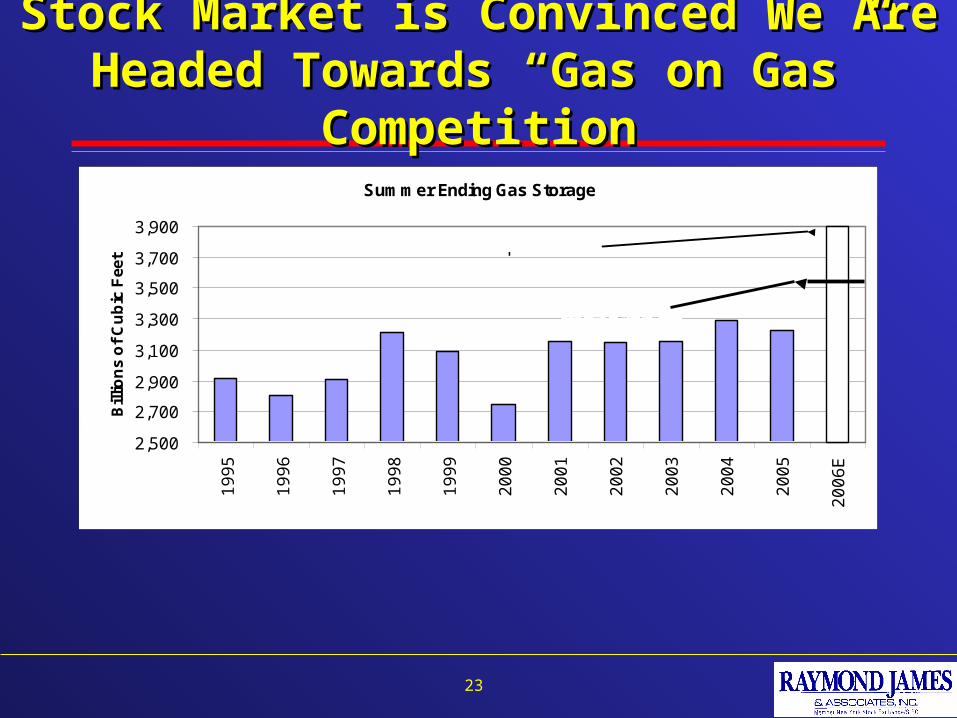

Stock Market is Convinced We Are Headed Stock Market is Convinced We Are Headed Towards “Gas on Gas” CompetitionTowards “Gas on Gas” Competition

23

Summer Ending Gas Storage

2,500

2,700

2,900

3,100

3,300

3,500

3,700

3,9001

99

5

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

E

Bill

ion

s o

f C

ub

ic F

eet

Source: EIA

RJ Estimate

Market Expectations

What Are Gas Bears Missing?What Are Gas Bears Missing?

24

Post hurricane Post hurricane demanddemand destruction was greater than destruction was greater than most people realizemost people realize

At current prices, demand is returningAt current prices, demand is returning– (or supply is falling)(or supply is falling)

Assuming normal weather & no hurricanes we are Assuming normal weather & no hurricanes we are headed towards 3,500 Bcf, not 3,900 Bcf ending storageheaded towards 3,500 Bcf, not 3,900 Bcf ending storage

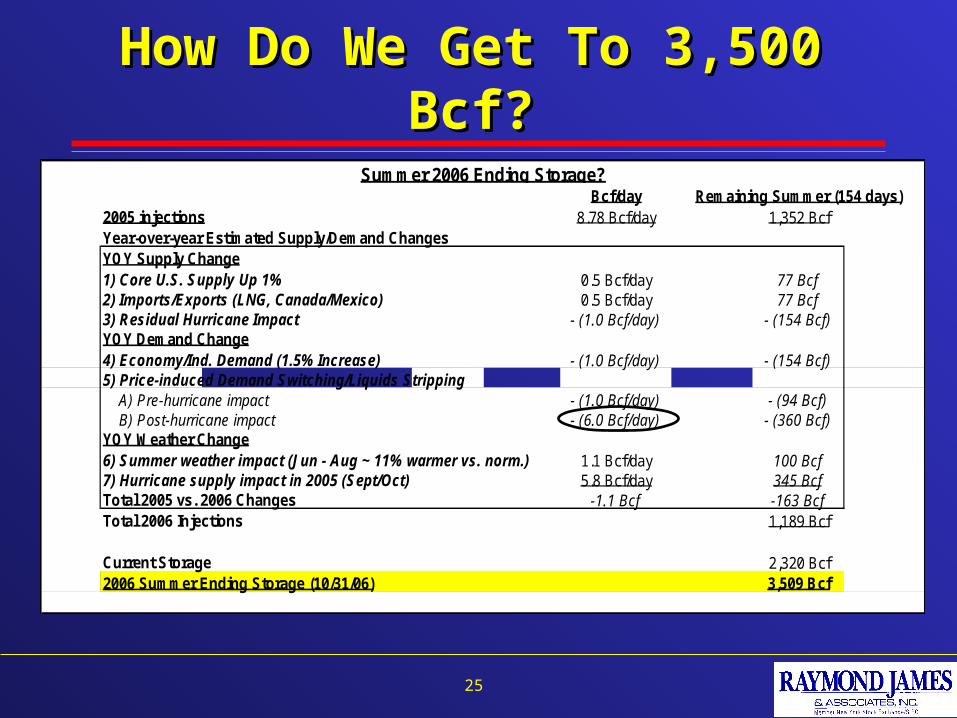

How Do We Get To 3,500 Bcf?How Do We Get To 3,500 Bcf?

25

Bcf/day Remaining Summer (154 days)2005 injections 8.78 Bcf/day 1,352 BcfYear-over-year Estimated Supply/Demand ChangesYOY Supply Change1) Core U.S. Supply Up 1% 0.5 Bcf/day 77 Bcf2) Imports/Exports (LNG, Canada/Mexico) 0.5 Bcf/day 77 Bcf3) Residual Hurricane Impact - (1.0 Bcf/day) - (154 Bcf)YOY Demand Change4) Economy/Ind. Demand (1.5% Increase) - (1.0 Bcf/day) - (154 Bcf)5) Price-induced Demand Switching/Liquids Stripping A) Pre-hurricane impact - (1.0 Bcf/day) - (94 Bcf) B) Post-hurricane impact - (6.0 Bcf/day) - (360 Bcf)YOY Weather Change6) Summer weather impact (Jun - Aug ~ 11% warmer vs. norm.) 1.1 Bcf/day 100 Bcf7) Hurricane supply impact in 2005 (Sept/Oct) 5.8 Bcf/day 345 BcfTotal 2005 vs. 2006 Changes -1.1 Bcf -163 BcfTotal 2006 Injections 1,189 Bcf

Current Storage 2,320 Bcf2006 Summer Ending Storage (10/31/06) 3,509 Bcf

Summer 2006 Ending Storage?

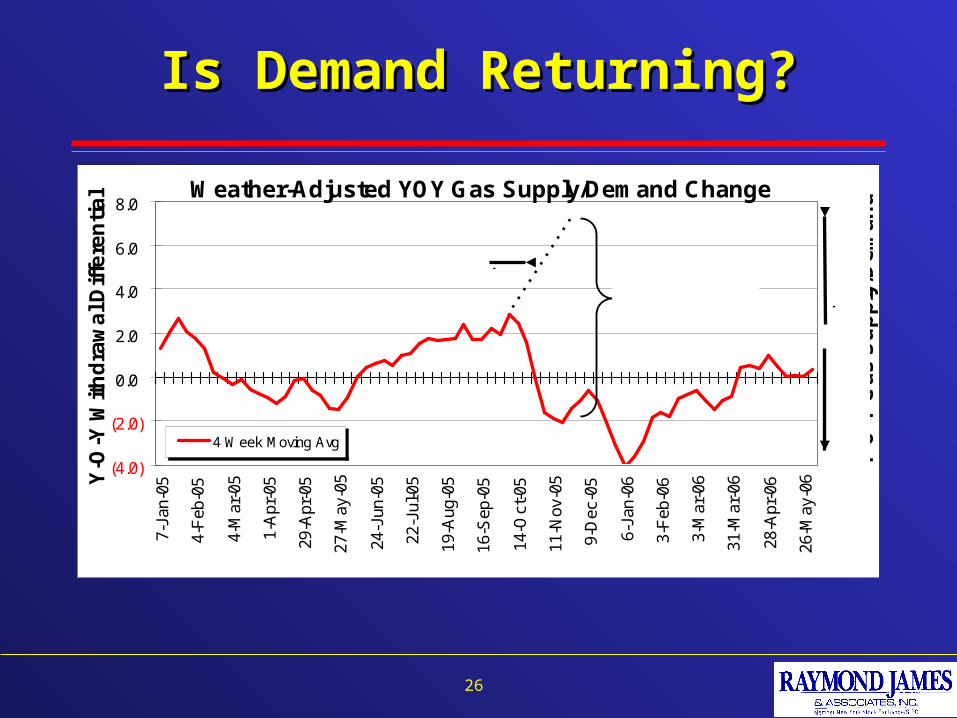

Is Demand Returning?Is Demand Returning?

26

Weather-Adjusted YOY Gas Supply/Demand Change

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

7-Ja

n-05

4-F

eb-0

5

4-M

ar-0

5

1-A

pr-0

5

29-A

pr-0

5

27-M

ay-0

5

24-J

un-0

5

22-J

ul-0

5

19-A

ug-0

5

16-S

ep-0

5

14-O

ct-0

5

11-N

ov-0

5

9-D

ec-0

5

6-Ja

n-06

3-F

eb-0

6

3-M

ar-0

6

31-M

ar-0

6

28-A

pr-0

6

26-M

ay-0

6Y-O

-Y W

ith

dra

wa

l Dif

fere

nti

al

4 Week Moving Avg

Source: EIA, RJ&A.

LO

OS

ER

TIG

HT

ER

Y-O

-Y G

as

Su

pp

ly/D

em

an

d

9 Bcf/day Demand Destruction?

5.5 Bcf/day supply lost

Even DOE’s Numbers Suggest Even DOE’s Numbers Suggest Big Demand DestructionBig Demand Destruction

27

Monthly Total Gas Demand, Excluding WeatherChange From Previous Year

(3.3)

0.61.5 1.2

(3.3)(4.0) (3.8)

(2.3)

(8.3)

(8.50)

(7.00)

(5.50)

(4.00)

(2.50)

(1.00)

0.50

2.00

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep

-05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Bcf

/Day

Source: EIA, DOE, RJ&A Estimates

~5 Bcf/day change in demand

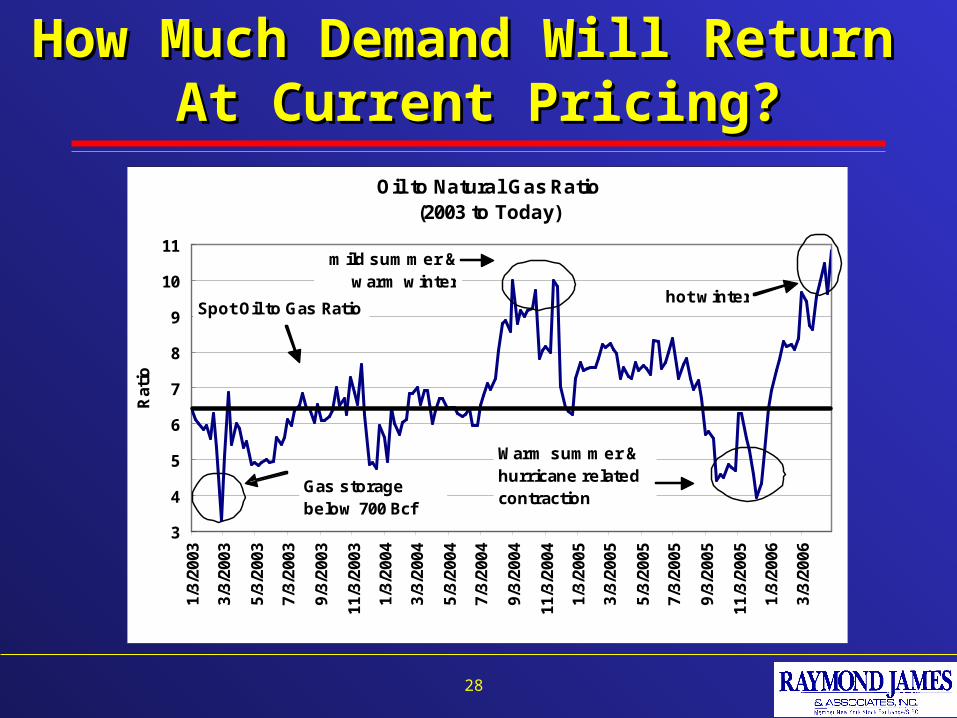

How Much Demand Will Return How Much Demand Will Return At Current Pricing?At Current Pricing?

28

Oil to Natural Gas Ratio(2003 to Today)

3

4

5

6

7

8

9

10

11

1/3/

2003

3/3/

2003

5/3/

2003

7/3/

2003

9/3/

2003

11/3

/200

3

1/3/

2004

3/3/

2004

5/3/

2004

7/3/

2004

9/3/

2004

11/3

/200

4

1/3/

2005

3/3/

2005

5/3/

2005

7/3/

2005

9/3/

2005

11/3

/200

5

1/3/

2006

3/3/

2006

Rat

io

Source: Bloomberg

Warm summer & hurricane related contraction

Gas storage below 700 Bcf

mild summer & warm winter

hot winterSpot Oil to Gas Ratio

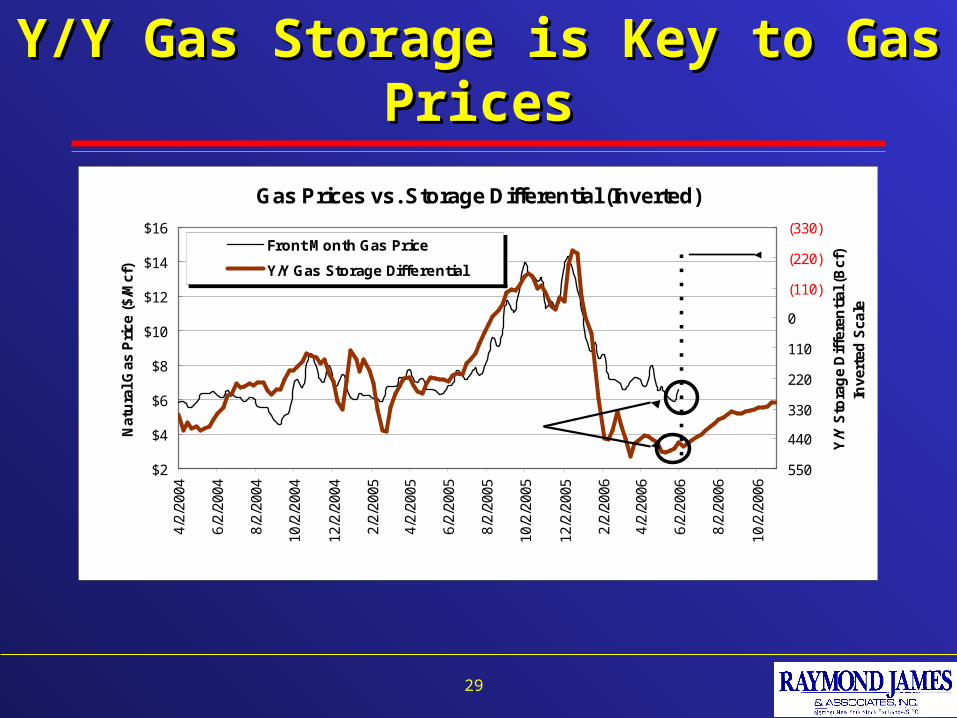

Y/Y Gas Storage is Key to Gas PricesY/Y Gas Storage is Key to Gas Prices

29

Gas Prices vs. Storage Differential (Inverted)

$2

$4

$6

$8

$10

$12

$14

$16

4/2/

2004

6/2/

2004

8/2/

2004

10/2

/200

4

12/2

/200

4

2/2/

2005

4/2/

2005

6/2/

2005

8/2/

2005

10/2

/200

5

12/2

/200

5

2/2/

2006

4/2/

2006

6/2/

2006

8/2/

2006

10/2

/200

6

Nat

ura

l Gas

Pri

ce (

$/M

cf)

(330)

(220)

(110)

0

110

220

330

440

550

Y/Y

Sto

rag

e D

iffe

ren

tial

(B

cf)

Inve

rted

Sca

le

Front Month Gas Price

Y/Y Gas Storage Differential

Source: Bloomberg, EIA

Inflection Point?

Estimate

Where Will Winter Storage End?Where Will Winter Storage End?

30

Bcf/day Full Winter (151 days)2005/2006 Withdrawals 9.56 Bcf/day 1,444 BcfYear-over-year Estimated Supply/Demand ChangesYOY Supply Change1) Core U.S. Supply Up 1% 0.50 Bcf/day 76 Bcf2) Imports/Exports (LNG, Canada/Mexico) 0 Bcf/day 0 Bcf3) Residual Hurricane Impact - (0.75 Bcf/day) - (113 Bcf)YOY Demand Change4) Economy/Ind. Demand (1.75% Increase) - (1.0 Bcf/day) - (151 Bcf)5) Price-induced Demand Switching/Liquids Stripping - (2.5 Bcf/day) - (378 Bcf)6) Hurricane Demand Recovery - (1.0 Bcf/day) - (151 Bcf)YOY Weather Change7) Winter weather impact (2005/2006 ~ 9% warmer vs. normal) - (2.4 Bcf/day) - (362 Bcf)8) Hurricane supply impact 2.1 Bcf/day 323 BcfTotal 2006/07 vs. 2005/06 Changes - (5.0 Bcf) - (757 Bcf)Total 2006/2007 Withdrawals 2,201 Bcf

2006 Summer Ending Storage 3,509 Bcf2006/2007 Winter Ending Storage (3/31/07) 1,308 Bcf

Winter 2006/2007 Ending Storage?

Long Term, U.S. Gas Will Be Linked to OilLong Term, U.S. Gas Will Be Linked to Oil

31

We are assuming 9:1 oil to gas ratio through summerWe are assuming 9:1 oil to gas ratio through summer– Currently we are at an 11:1 RatioCurrently we are at an 11:1 Ratio

Storage “resets” gas prices in NovemberStorage “resets” gas prices in November

Longer-term gas prices trend towards 6:1 Btu parityLonger-term gas prices trend towards 6:1 Btu parity

RJ estimate: 2006 = $7.81/McfRJ estimate: 2006 = $7.81/Mcf 2007 = $10.00/Mcf2007 = $10.00/Mcf

How Do Prospect Inventories Look & Are Higher How Do Prospect Inventories Look & Are Higher Service Costs Impacting Prospect Hurdle Rates?Service Costs Impacting Prospect Hurdle Rates?

32

Our Take:Our Take:

– 5 years ago 5 years ago “There aren’t enough prospects” “There aren’t enough prospects”

– Today Today “There aren’t enough rigs” “There aren’t enough rigs”

– Reality Reality LT gas prices above $6/Mcf generates LT gas prices above $6/Mcf generates

great revenues & more prospects despite higher costsgreat revenues & more prospects despite higher costs

Reinvestment Returns Reinvestment Returns Are Still OutstandingAre Still Outstanding

33

Major Assumptions:Year 1 2 3+Oil Price ($/Bbl) $60.00 $60.00 $60.00Gas Price ($/Mcf) $9.00 $9.00 VariesLOE and G&A Costs ($/Mcfe) $1.80Production Tax Rate 6.0%Net Revenue Interest 78%Percentage Gas 70%

IRR at Various Finding & Development (F&D) Costs

20%

30%

40%

50%

60%

70%

80%

90%

100%

$6.00 $7.00 $8.00 $9.00 $10.00

Long-term Gas Price ($ / Mcf)

Inte

rnal

Rat

e o

f R

etu

rn (

%) $1.75 $2.00 $2.25

Source: RJ&A Estimates

How Far Do Oil & Gas Prices Need to How Far Do Oil & Gas Prices Need to Fall Before Activity Slows?Fall Before Activity Slows?

34

Our Take:Our Take: Long-term price expectations (or 2 yr. strip) must fall Long-term price expectations (or 2 yr. strip) must fall

below $6 gas and $50 crudebelow $6 gas and $50 crude Short-term spike to $5 range will Short-term spike to $5 range will NOTNOT slow activity slow activity Most think gas pull-back will be short-livedMost think gas pull-back will be short-lived Many E&P companies have hedged @ higher pricesMany E&P companies have hedged @ higher prices E&P companies are flush with cash & prospectsE&P companies are flush with cash & prospects If E&P companies “lay down” a rig, they move to the If E&P companies “lay down” a rig, they move to the

“back of the line.”“back of the line.”

Will the Service Industry Over-Build Will the Service Industry Over-Build Rigs & Oilfield Equipment?Rigs & Oilfield Equipment?

35

Our Take:Our Take:

Global rig fleet will grow 10-15% per year over the Global rig fleet will grow 10-15% per year over the next 5 years.next 5 years.

Rig new build costs will rise & Rig new build costs will rise & demand will exceed demand will exceed supplysupply for the entire period for the entire period

History LessonHistory Lesson

36

Historic Average U.S. Rig Count

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

Rig

Co

un

t

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

21.0%

24.0%

27.0%

30.0%

33.0%Total U.S. Rigs AvailableRig Build Rate

Source: ReedHycalog, RJ&A

12.6% average growth rate

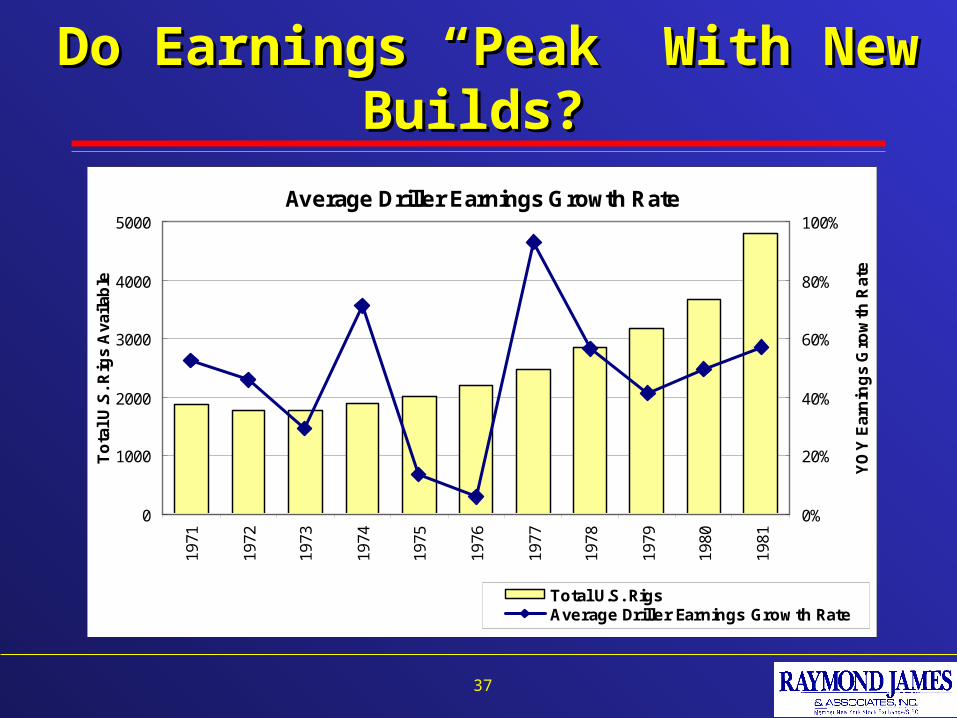

Do Earnings “Peak” With New Builds?Do Earnings “Peak” With New Builds?

37

Average Driller Earnings Growth Rate

0

1000

2000

3000

4000

5000

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

To

tal U

.S. R

igs

Ava

ilab

le

0%

20%

40%

60%

80%

100%

YO

Y E

arn

ing

s G

row

th R

ate

Total U.S. RigsAverage Driller Earnings Growth RateSource: Factset, Reedhycalog

Companies Included: GSF, RDC, HP, NBR, PKD

(10 yr. growth rate = 46%)

ConclusionConclusion

38

Longer-term bullish secular move is still intactLonger-term bullish secular move is still intact

Oil & gas supply is not responding to rigsOil & gas supply is not responding to rigs

Oil prices are signaling that demand Oil prices are signaling that demand must must slowslow

Oil wildcards are not going awayOil wildcards are not going away

Gas could be near a bottomGas could be near a bottom

DisclaimerDisclaimer

Important Investor Disclosures. Stock Ratings: Within our four-tiered rating system, Strong Buy means that the stock is expected to appreciate and produce

a total return of at least 15% and outperform the S&P 500 over the next six months; Outperform means the stock is expected to appreciate and outperform the S&P 500 over the next 12 months; Market Perform means the stock is expected to perform generally in line with the S&P 500 over the next 12 months and is potentially a source of funds for more highly rated securities; and Underperform means the stock is expected to underperform the S&P 500 or its sector over the next six to 12 months and should be sold.

Out of approximately 519 stocks in the Raymond James coverage universe, 52% have Strong Buy or Outperform ratings, 35% are rated Market Perform and 12% are rated Underperform. Within those rating categories, 25% of the Strong Buy- or Outperform-rated companies either currently are or have been Raymond James Investment Banking clients within the past three years; 17% of the Market Perform-rated companies are or have been clients and 9% of the Underperform-rated companies are or have been clients.

Analyst Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination including the analyst’s success in rating stocks versus an industry index, support effectiveness to the retail and institutional sales forces, traders, and investment bankers, institutional research votes, as well as overall productivity and revenue generated in covered stocks.

Raymond James Relationships: Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJA or its officers, employees, or affiliates may (1) currently own shares, options, rights or warrants and/or (2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report's conclusions.

Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available at www.rjcapitalmarkets.com/SearchForDisclosures_main.asp. Copies of research can be obtained by contacting any Raymond James & Associates or Raymond James Financial Services office (please see www.rjf.com for office locations) or by sending a written request to the Equity Research Library, Raymond James & Associates, Inc., Tower 3, 6th Floor, 880 Carillon Parkway, St. Petersburg, FL 33716.

Additional information is available on request. This document may not be reprinted without permission.

39

Related Documents