A PROJECT REPORT ON “RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED” AT NORTHERN COALFIELDS LIMITED SINGRAULI Submitted to SINHGAD INSTITUTE OF BUSINESS ADMINISTRATION & RESEARCH In Partial Fulfillment of Requirements for the Award of Post Graduate Diploma in Management BY SHRAWAN KUMAR DWIVEDI PGDM (Finance) IIIrd Semester Under the Guidance of PROF. SIDDHARTH KARALE ACADEMIC YEAR 2009-2011 SINHGAD INSTITUTE OF BUSINESS ADMINISTRATION & RESEARCH S.No. 40/4A + 4B/ 1, Near PMC Octroi Post, Kondhwa- Saswad Road, Kondhwa (Bk.), Pune – 411048

Ratio Analysis of Ncl by Shrawan Kumar Dwivedi

Apr 07, 2015

This Report is dealt with the ratio analysis of the Northern Coalfields limited which is a subsidiary company of Coal India Limited.I did my summer internship with this company and this analysis is done by me as a part of my PGDM course curriculum.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A PROJECT REPORT ON

“RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED”

AT

NORTHERN COALFIELDS LIMITED SINGRAULI

Submitted to SINHGAD INSTITUTE OF BUSINESS ADMINISTRATION & RESEARCH

In Partial Fulfillment of Requirements

for the Award of Post Graduate Diploma in Management

BY SHRAWAN KUMAR DWIVEDI

PGDM (Finance) IIIrd Semester

Under the Guidance of PROF. SIDDHARTH KARALE

ACADEMIC YEAR 2009-2011

SINHGAD INSTITUTE OF BUSINESS ADMINISTRATION & RESEARCH S.No. 40/4A + 4B/ 1, Near PMC Octroi Post, Kondhwa- Saswad Road,

Kondhwa (Bk.), Pune – 411048

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

2 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

3 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

4 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

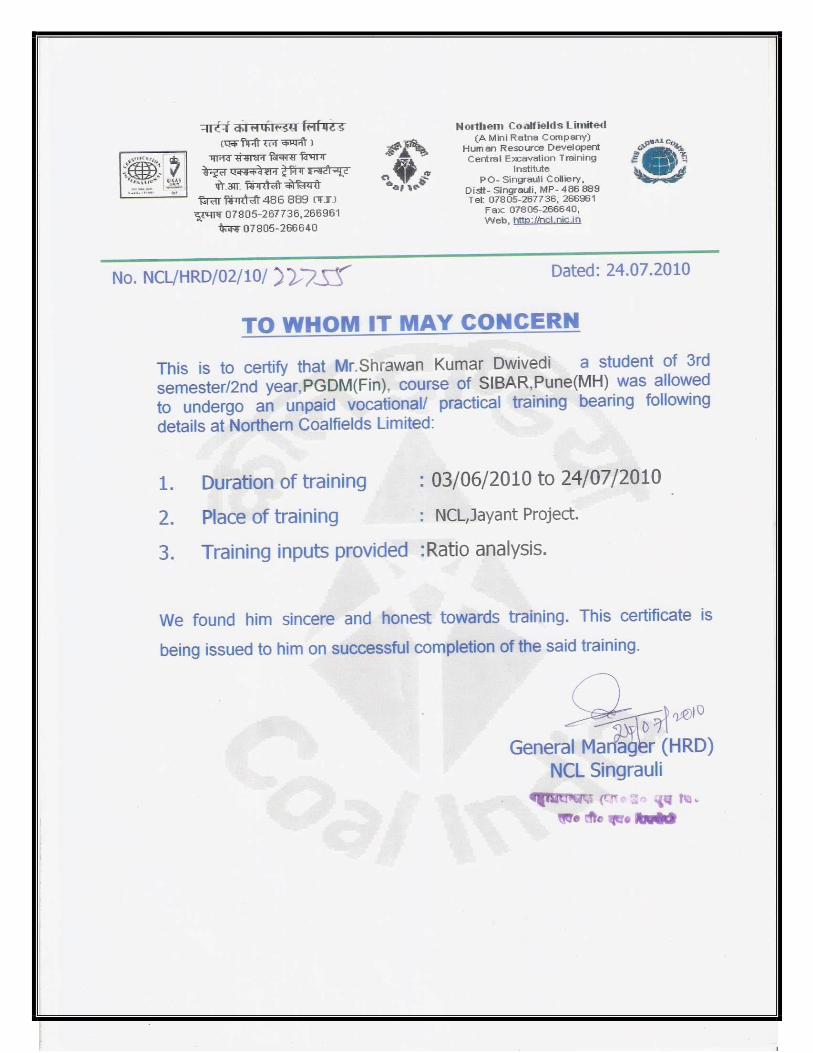

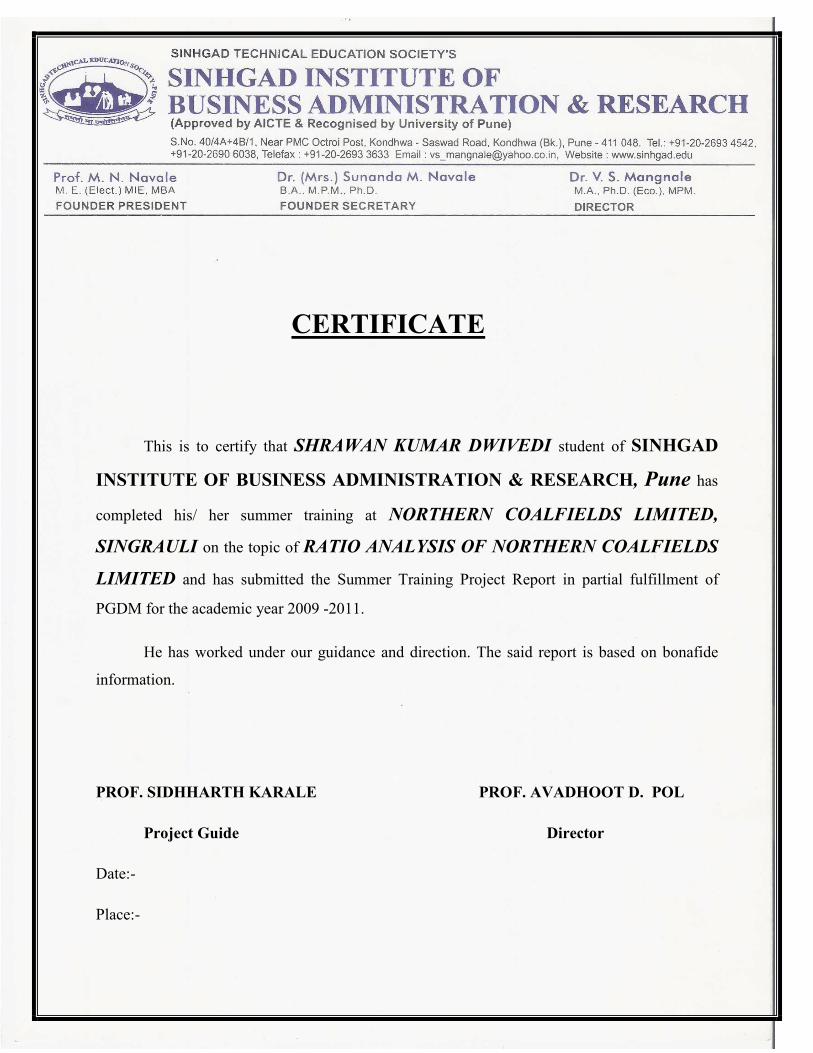

CERTIFICATE

This is to certify that SHRAWAN KUMAR DWIVEDI student of SINHGAD

INSTITUTE OF BUSINESS ADMINISTRATION & RESEARCH, Pune has

completed his/ her summer training at NORTHERN COALFIELDS LIMITED,

SINGRAULI on the topic of RATIO ANALYSIS OF NORTHERN COALFIELDS

LIMITED and has submitted the Summer Training Project Report in partial fulfillment of

PGDM for the academic year 2009 -2011.

He has worked under our guidance and direction. The said report is based on bonafide

information.

PROF. SIDHHARTH KARALE PROF. AVADHOOT D. POL

Project Guide Director

Date:-

Place:-

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

5 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

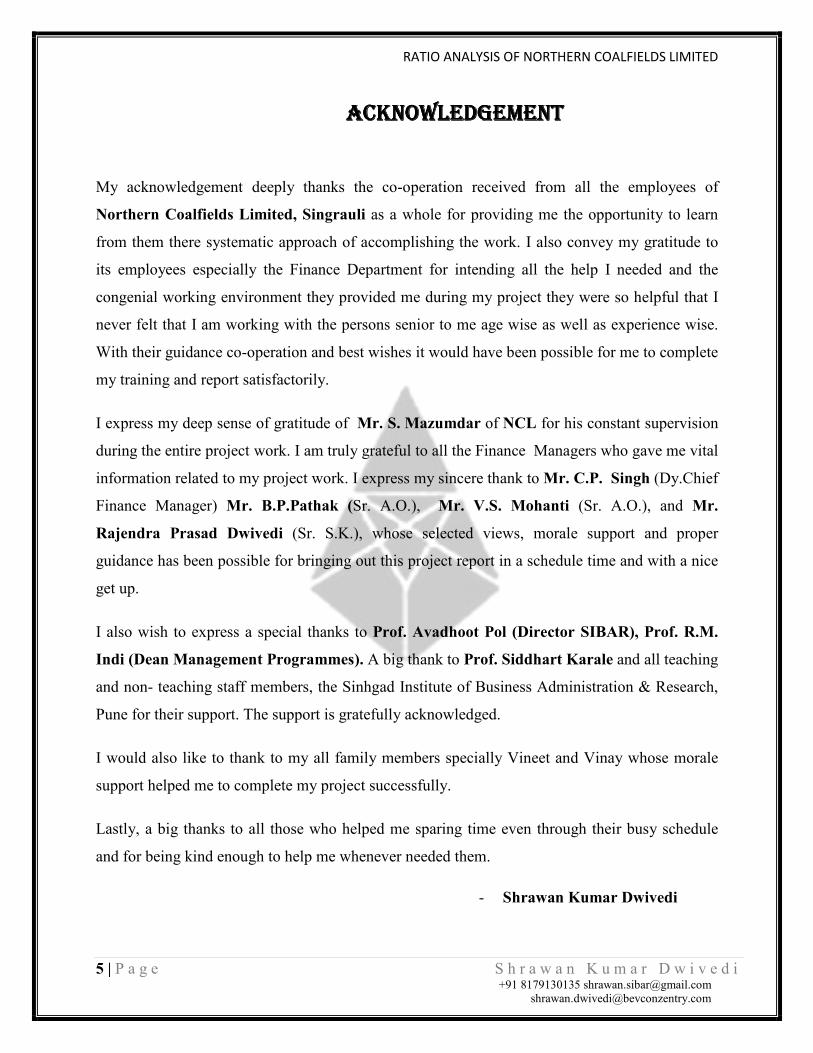

ACKNOWLEDGEMENTACKNOWLEDGEMENTACKNOWLEDGEMENTACKNOWLEDGEMENT

My acknowledgement deeply thanks the co-operation received from all the employees of

Northern Coalfields Limited, Singrauli as a whole for providing me the opportunity to learn

from them there systematic approach of accomplishing the work. I also convey my gratitude to

its employees especially the Finance Department for intending all the help I needed and the

congenial working environment they provided me during my project they were so helpful that I

never felt that I am working with the persons senior to me age wise as well as experience wise.

With their guidance co-operation and best wishes it would have been possible for me to complete

my training and report satisfactorily.

I express my deep sense of gratitude of Mr. S. Mazumdar of NCL for his constant supervision

during the entire project work. I am truly grateful to all the Finance Managers who gave me vital

information related to my project work. I express my sincere thank to Mr. C.P. Singh (Dy.Chief

Finance Manager) Mr. B.P.Pathak (Sr. A.O.), Mr. V.S. Mohanti (Sr. A.O.), and Mr.

Rajendra Prasad Dwivedi (Sr. S.K.), whose selected views, morale support and proper

guidance has been possible for bringing out this project report in a schedule time and with a nice

get up.

I also wish to express a special thanks to Prof. Avadhoot Pol (Director SIBAR), Prof. R.M.

Indi (Dean Management Programmes). A big thank to Prof. Siddhart Karale and all teaching

and non- teaching staff members, the Sinhgad Institute of Business Administration & Research,

Pune for their support. The support is gratefully acknowledged.

I would also like to thank to my all family members specially Vineet and Vinay whose morale

support helped me to complete my project successfully.

Lastly, a big thanks to all those who helped me sparing time even through their busy schedule

and for being kind enough to help me whenever needed them.

- Shrawan Kumar Dwivedi

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

6 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

SINHGAD INSTITUTE OF BUSINESS ADMINISTRATION AND RESEARCH, KONDHWA (BK)

DECLARATION

I herby declare that the project titled “RATIO ANALYSIS OF NORTHERN COALFIELDS

LIMITED” is an original piece of research work carried out by me under the guidance and

supervision of Prof. SIDDHARTH KARALE. The information has been collected from

genuine & authentic sources. The work has been submitted in partial fulfillment of the

requirement of PGDM .

Place:

Date: Shrawan Kumar Dwivedi

9595302505 [email protected]

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

7 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Executive Summary

India is the third largest coal producer in the world and the eighth largest importer. With annual production of 310 million tonnes and imports of almost 25 million tonnes, coal provides one-third of energy supply in India. The Indian government forecasts huge increases in electricity capacity based on coal, and a financially viable electricity industry will be necessary to support reforms in the coal industry. This report describes the Indian coal sector, and comments on government policies and the performance of India's largely state-owned coal companies. There is a substantial need for reforms in India's coal sector to improve efficiency and competitiveness.

With the growth of the Indian economy due to various factors like Industralization, Growth of Infrastructure, Institutional Development etc. the power is going to be the main key for any development so the Coal is wodely used by the power industries for generating the power.

Financial statement analysis is important to board of the Directors, Managers, Payers, Lenders, and others who make judgments about the financial health of organizations. One widely accepted method of assessing financial statements is ratio analysis, which uses data from the balance sheet and income statement to produce values that have easily interpreted financial meaning. The purpose of this project was to get awareness about how an organization works.

The project was carried out for study and analyzing the financial condition of Northern Coalfields Limited with special reference of Jayant Project. It was done to know that what is the current financial scenario of the company. In this project report I have made Ratio Analysis for analyzing that that what are the different ratios available in the organization and what is current growth comparing to the last year.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

8 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

TABLE OF CONTENTS

Chapter No. Sr. No. Particulars

Page No.

Chapter I Introduction 1.1 Introduction of the topic 9 1.2 Objectives of the study 11 1.3 Significance of te Study 11 1.4 Limitations & Future Scope 11

Chapter II Research Methodology 12

Chapter III Organizational Profile 14 3.1 About the Organization 16 3.2 Vision, Mission of the Organization 19

3.3 Historical Background of the Organization 20

3.4 Different Departments of the Organization 21

3.5 Organizational Structure of the Organization 23

3.6 Current Status of the Organization 26 3.7 Future Plans of the Organization 29 3.8 Awards and Achievements 30

Chapter IV Data Analysis 31

Chapter V Summary & Conclusions 45 5.1 Major Findings & Suggestions 46 5.2 Conclusions 47

Chapter VI Reference Section 48

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

9 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

LIST OF TABLES

TABLE NO. TITLE OF THE TABLE PAGE NO. Table no. 3.1 Projects of NCL 17 Table no. 3.2 Coal Resources in Northern

Coalfields Limited

26

Table no. 3.3 Payment to Central/ State Exchequer

44

LIST OF FIGURES

LIST OF FIGURES

TABLE NO. TITLE OF THE FIGURE PAGE NO. Figure no. 3.1 Consumer Profile 22 Figure no. 3.2 Cost of Production 27 Figure no. 3.3 Status of Outstanding Dues 28 Figure no. 3.4 Comparison of the

production between NCL and Jayant project

28

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

10 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CHAPTER I

INTRODUCTION

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

11 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

INTRODUCTION OF THE TOPIC

To analyze the financial position of NORTHERN COALFIELDS LIMITED, different tools are used, of Ratio Analysis. Financial analysis involves the use of various financial statements. These statements do several things. First the balance sheet and the second is income statement.

The Balance sheet summarizes the assets, liabilities, and owner’s equity of a business at a point in time, while the income statement summarizes revenues and expenses of a firm over a particular period of time. A conceptual framework for financial analysis provides the analyst with an interlocking means for structuring the analysis.

A financial ratio (or accounting ratio) is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there are many standard ratios used to try to evaluate the overall financial condition of a corporation or other organization. Financial ratios may be used by managers within a firm, by current and potential shareholders (owners) of a firm, and by a firm's creditors. Security analysts use financial ratios to compare the strengths and weaknesses in various companies. If shares in a company are traded in a financial market, the market price of the shares is used in certain financial ratios.

Values used in calculating financial ratios are taken from the balance sheet, income statement, statement of cash flows or (sometimes) the statement of retained earnings. These comprise the firm's "accounting statements" or financial statements. The statements' data is based on the accounting method and accounting standards used by the organization.

Financial ratios quantify many aspects of a business and are an integral part of financial statement analysis. Financial ratios are categorized according to the financial aspect of the business which the ratio measures. Liquidity ratios measure the availability of cash to pay debt. Activity ratios measure how quickly a firm converts non-cash assets to cash assets. Debt ratios measure the firm's ability to repay long-term debt.Profitability ratios measure the firm's use of its assets and control of its expenses to generate an acceptable rate of return. Market ratios measure investor response to owning a company's stock and also the cost of issuing stock.

Financial ratios allow for comparisons

• between companies • between industries • between different time periods for one company • between a single company and its industry average

Ratios generally hold no meaning unless they are benchmarked against something else, like past performance or another company. Thus, the ratios of firms in different industries, which face different risks, capital requirements, and competition are usually hard to compare.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

12 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

1.2 Objectives of the report

To get awareness about the financial techniques. To find out NCL’s ability to meet the current obligation. To analyze the financial statement of NCL. To understand how effectively NCL utilizes its assets in producing Coal.

1.3 Significance of the study:

The present study dealt with the current financial status of the Northern Coalfields

Limited. It provides a broad view regarding Coal Production in NCL as well as in India. And this

project also tells, what is the current financial condition of the NCL in India? And How they are

contributing towards the coal production?

. In this context, we will address the following questions:

1. To analyze the current financial condition of NCL, Singrauli

2. To know the contribution of the NCL in the Indian Coal Industry.

1.4 Limitations & Future Scope:

Limitations :

Less response by some of the staff members Due to new in the department some of the staff members not provided some kind of information.

Problems in collection of the data of past years because the database is maintained by the headquarter and they don’t allow to provide these information to the outsiders.

Two months period for understanding all the working procedure of any particular organization is not sufficient.

Scope :

In this project I have done the financial analysis of the company so the scope of the study is that this report can be used as a financial statement of the company. This report shows different financial aspects of the Northen Coalfields Limited. This report also contains the information related the various projects run by the NCL and what is their contribution in Coal production.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

13 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CHAPTER II

RESEARCH

METHODOLOGY

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

14 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

RESEARCH METHODOLOGY : Research in common parlance refers to a search for knowledge. One can also define

research as a scientific and systematic search for pertinent information on a specific topic.

Research methodology is a way to systematically solve the research problem. Research

methodology just does not deal research method but also consider the logic behind the method. It

facilitates the researcher with reason for evaluating the research problem.

Definition:

According to Redman and Mory

“Research is systematized effort to gain new knowledge”.

According to Clifford Woody

“Research comprises defining and redefining problems, formulating hypothesis or

suggested solutions, collecting organizing and evaluating data , making deductions and reaching

conclusions and at last carefully testing the conclusions to determine whether they fit the

formulating hypothesis”.

The research is done through :

Journals : I have used the the organizational journals published by the company for

collecting the data.

Annual Reports : Annual reports are the best way to collect the information about the

company. If we are going to conduct any research work in the field of Finance then we

must should have to refer the company’s Annual Report.

Plant visit : By visiting the Plant I came to know that what is the real scenario, what is

the position of the company? How the work flows ? etc. then I collected the relavent

information which I was needed to complete my project.

Personal discussion and interaction : I have Discussed with the concerned

people and thus collected information for the research.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

15 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CHAPTER III

ORGANIZATIONAL PROFILE

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

16 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

NORTHERN COALFIELDS LIMITED

(A Government of India’s Mini ratna Enterprise)

P.O.:Singrauli, Dist.:Singrauli (M.P.), PIN.:486889

EPABX-07805-266670, 266393 Fax - 07805-266640

E mail : [email protected], [email protected]

Website : http://www.ncl.nic.in

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

17 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

3.1 About the Company

Northern Coalfields Limited (NCL) – A Profile

NCL is a subsidiary of Coal India Limited (CIL). It was founded in

the year (1984). Earlier it was a subsidiary of Central Coalfields

Limited (CCL). It is among the top PSU's in India.

NCL is the only subsidiary of CIL producing 100% of coal from

opencast mines. There is steep rise in the coal demand on NCL to

meet the power and energy needs of the country . (44.43MT in 2002-

03 to 78.44MT in 2011-12). The major demand of coal on NCL is

from power sector, which contributes more than 96% of the total

demand.

The CILs production level in the year 2011-12 is projected as 619.67 million tones out of which NCLs

contribution will be 78 million tonnes.

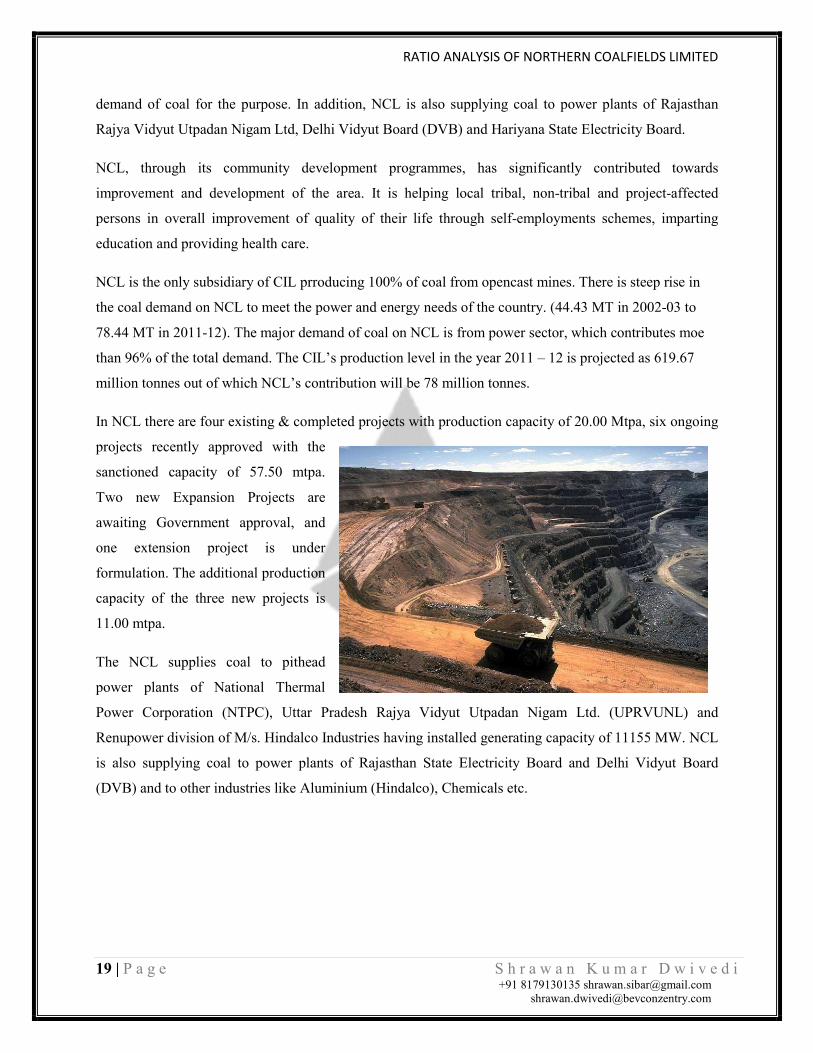

In NCL there are four existing & completed projects with production capacity of 20.00MTpa , six

ongoing projects recently approved with the sanctioned capacity of 57.50 mtpa. Two new expansion

projects are awaiting Government approval , and one extension project is under formulation .

The NCL supplies coal to pithead power plants of national thermal power corporation (NTPC), Uttar

Pradesh rajya vidyut utpadan nigam Ltd (UPRVUNL) and Renupower division of M/s. Hindalco

Industries having installed capacity of 11155MW. NCL is also supplying coal to power plants of

rajasthan state Electricity Board and Delhi Vidyut Board (DVB) and to other industries like Aluminium

(Hindalco), Chemicals etc.

In December 2008, NCL achieved its company-

wide ISO 9001:2000 certification. It is also

preparing to implement a company-level

Integrated Management System to

simultaneously comply with ISO 9001, ISO

14001, OHSAS 18001, and SA 8000; which will

cover all its mining establishments, other support

units, and all headquarters function .

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

18 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

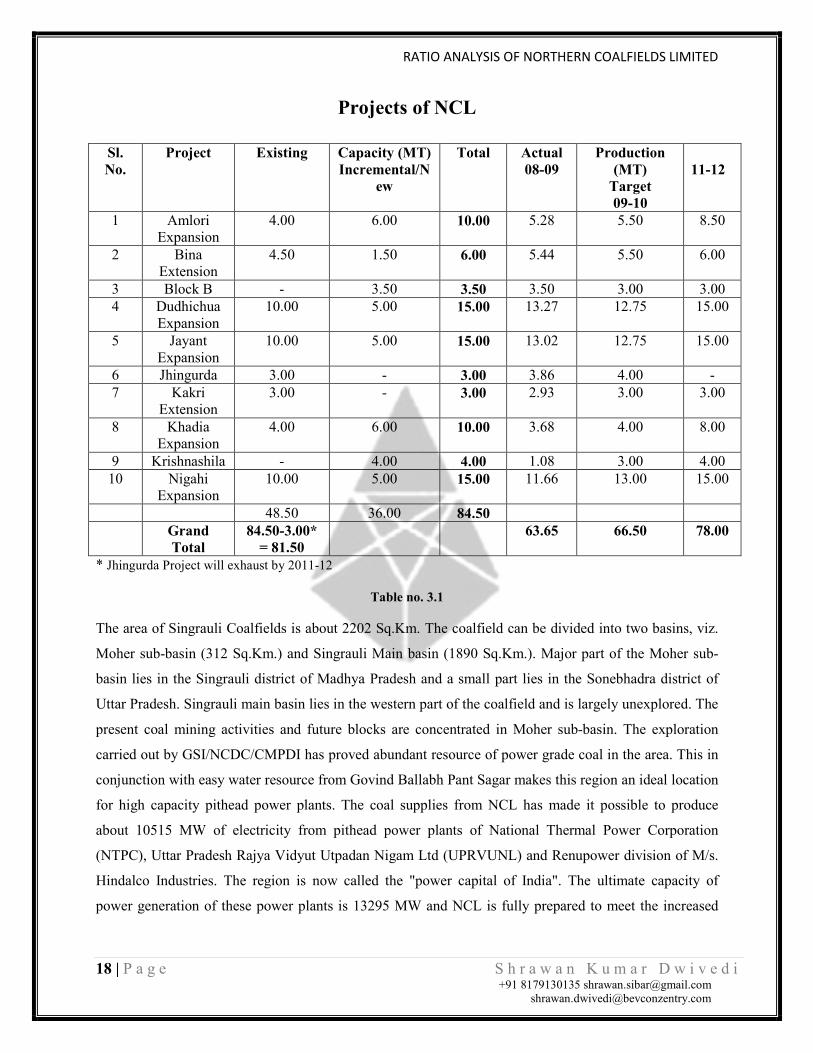

Projects of NCL

Sl. No.

Project Existing Capacity (MT) Incremental/N

ew

Total Actual 08-09

Production (MT) Target 09-10

11-12

1 Amlori Expansion

4.00 6.00 10.00 5.28 5.50 8.50

2 Bina Extension

4.50 1.50 6.00 5.44 5.50 6.00

3 Block B - 3.50 3.50 3.50 3.00 3.00 4 Dudhichua

Expansion 10.00 5.00 15.00 13.27 12.75 15.00

5 Jayant Expansion

10.00 5.00 15.00 13.02 12.75 15.00

6 Jhingurda 3.00 - 3.00 3.86 4.00 - 7 Kakri

Extension 3.00 - 3.00 2.93 3.00 3.00

8 Khadia Expansion

4.00 6.00 10.00 3.68 4.00 8.00

9 Krishnashila - 4.00 4.00 1.08 3.00 4.00 10 Nigahi

Expansion 10.00 5.00 15.00 11.66 13.00 15.00

48.50 36.00 84.50 Grand

Total 84.50-3.00* = 81.50

63.65 66.50 78.00

* Jhingurda Project will exhaust by 2011-12

Table no. 3.1

The area of Singrauli Coalfields is about 2202 Sq.Km. The coalfield can be divided into two basins, viz.

Moher sub-basin (312 Sq.Km.) and Singrauli Main basin (1890 Sq.Km.). Major part of the Moher sub-

basin lies in the Singrauli district of Madhya Pradesh and a small part lies in the Sonebhadra district of

Uttar Pradesh. Singrauli main basin lies in the western part of the coalfield and is largely unexplored. The

present coal mining activities and future blocks are concentrated in Moher sub-basin. The exploration

carried out by GSI/NCDC/CMPDI has proved abundant resource of power grade coal in the area. This in

conjunction with easy water resource from Govind Ballabh Pant Sagar makes this region an ideal location

for high capacity pithead power plants. The coal supplies from NCL has made it possible to produce

about 10515 MW of electricity from pithead power plants of National Thermal Power Corporation

(NTPC), Uttar Pradesh Rajya Vidyut Utpadan Nigam Ltd (UPRVUNL) and Renupower division of M/s.

Hindalco Industries. The region is now called the "power capital of India". The ultimate capacity of

power generation of these power plants is 13295 MW and NCL is fully prepared to meet the increased

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

19 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

demand of coal for the purpose. In addition, NCL is also supplying coal to power plants of Rajasthan

Rajya Vidyut Utpadan Nigam Ltd, Delhi Vidyut Board (DVB) and Hariyana State Electricity Board.

NCL, through its community development programmes, has significantly contributed towards

improvement and development of the area. It is helping local tribal, non-tribal and project-affected

persons in overall improvement of quality of their life through self-employments schemes, imparting

education and providing health care.

NCL is the only subsidiary of CIL prroducing 100% of coal from opencast mines. There is steep rise in

the coal demand on NCL to meet the power and energy needs of the country. (44.43 MT in 2002-03 to

78.44 MT in 2011-12). The major demand of coal on NCL is from power sector, which contributes moe

than 96% of the total demand. The CIL’s production level in the year 2011 – 12 is projected as 619.67

million tonnes out of which NCL’s contribution will be 78 million tonnes.

In NCL there are four existing & completed projects with production capacity of 20.00 Mtpa, six ongoing

projects recently approved with the

sanctioned capacity of 57.50 mtpa.

Two new Expansion Projects are

awaiting Government approval, and

one extension project is under

formulation. The additional production

capacity of the three new projects is

11.00 mtpa.

The NCL supplies coal to pithead

power plants of National Thermal

Power Corporation (NTPC), Uttar Pradesh Rajya Vidyut Utpadan Nigam Ltd. (UPRVUNL) and

Renupower division of M/s. Hindalco Industries having installed generating capacity of 11155 MW. NCL

is also supplying coal to power plants of Rajasthan State Electricity Board and Delhi Vidyut Board

(DVB) and to other industries like Aluminium (Hindalco), Chemicals etc.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

20 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

3.2 Vision and Mission of the organization

VISION

“Be the leading energy supplier in the country, through best practices from mine to market.”

MISSION

“The mission of Coal India Limited is to produce and market the planned quantity of coal and coal products efficiently and economically with due regard to safety, conservation, quality and environment.”

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

21 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

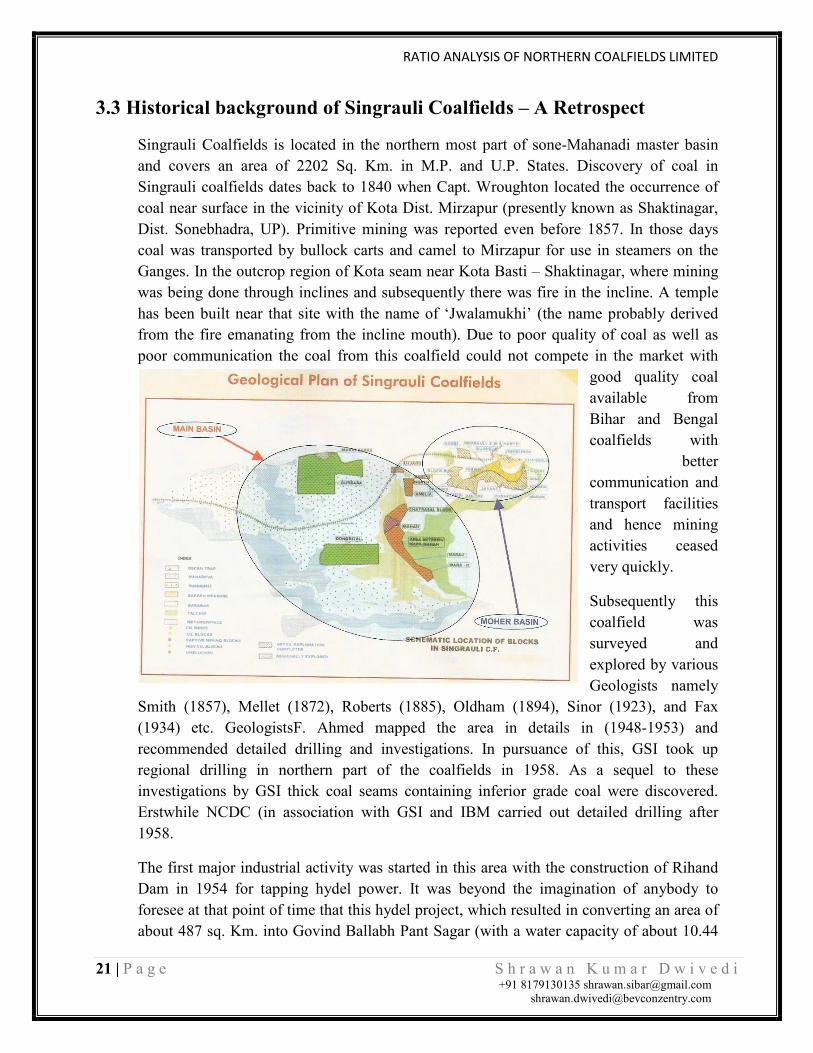

3.3 Historical background of Singrauli Coalfields – A Retrospect

Singrauli Coalfields is located in the northern most part of sone-Mahanadi master basin and covers an area of 2202 Sq. Km. in M.P. and U.P. States. Discovery of coal in Singrauli coalfields dates back to 1840 when Capt. Wroughton located the occurrence of coal near surface in the vicinity of Kota Dist. Mirzapur (presently known as Shaktinagar, Dist. Sonebhadra, UP). Primitive mining was reported even before 1857. In those days coal was transported by bullock carts and camel to Mirzapur for use in steamers on the Ganges. In the outcrop region of Kota seam near Kota Basti – Shaktinagar, where mining was being done through inclines and subsequently there was fire in the incline. A temple has been built near that site with the name of ‘Jwalamukhi’ (the name probably derived from the fire emanating from the incline mouth). Due to poor quality of coal as well as poor communication the coal from this coalfield could not compete in the market with

good quality coal available from Bihar and Bengal coalfields with

better communication and transport facilities and hence mining activities ceased very quickly.

Subsequently this coalfield was surveyed and explored by various Geologists namely

Smith (1857), Mellet (1872), Roberts (1885), Oldham (1894), Sinor (1923), and Fax (1934) etc. GeologistsF. Ahmed mapped the area in details in (1948-1953) and recommended detailed drilling and investigations. In pursuance of this, GSI took up regional drilling in northern part of the coalfields in 1958. As a sequel to these investigations by GSI thick coal seams containing inferior grade coal were discovered. Erstwhile NCDC (in association with GSI and IBM carried out detailed drilling after 1958.

The first major industrial activity was started in this area with the construction of Rihand Dam in 1954 for tapping hydel power. It was beyond the imagination of anybody to foresee at that point of time that this hydel project, which resulted in converting an area of about 487 sq. Km. into Govind Ballabh Pant Sagar (with a water capacity of about 10.44

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

22 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

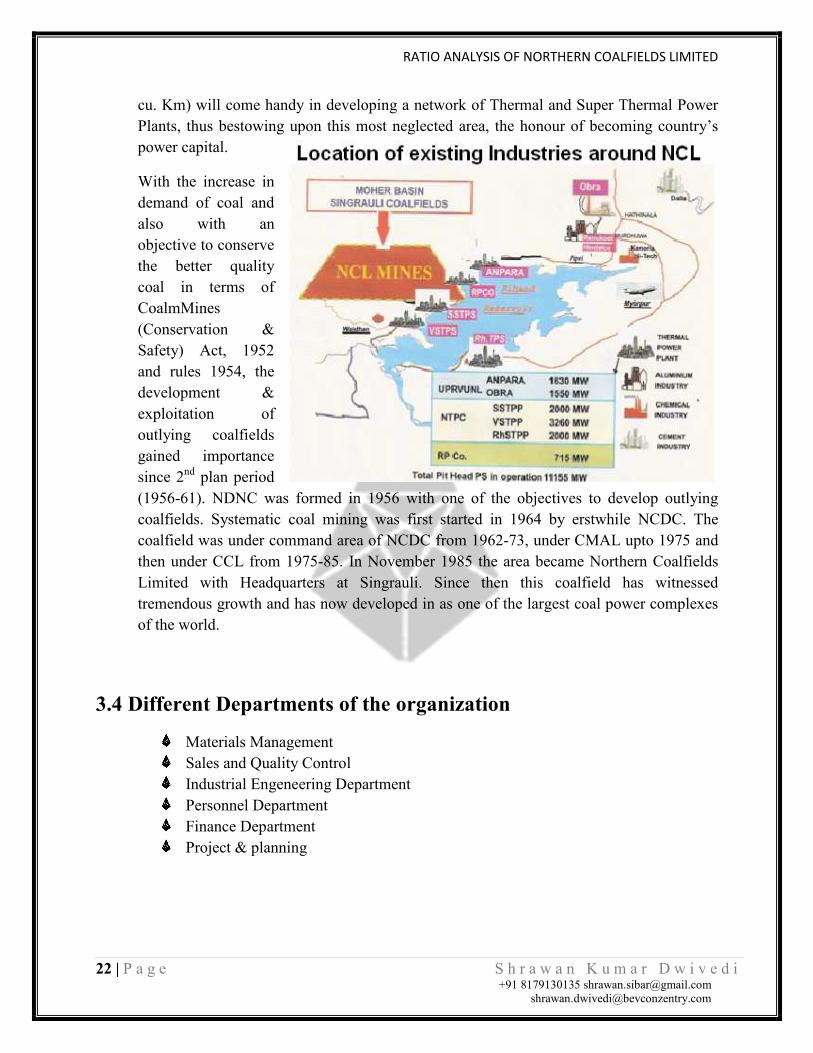

cu. Km) will come handy in developing a network of Thermal and Super Thermal Power Plants, thus bestowing upon this most neglected area, the honour of becoming country’s power capital.

With the increase in demand of coal and also with an objective to conserve the better quality coal in terms of CoalmMines (Conservation & Safety) Act, 1952 and rules 1954, the development & exploitation of outlying coalfields gained importance since 2nd plan period (1956-61). NDNC was formed in 1956 with one of the objectives to develop outlying coalfields. Systematic coal mining was first started in 1964 by erstwhile NCDC. The coalfield was under command area of NCDC from 1962-73, under CMAL upto 1975 and then under CCL from 1975-85. In November 1985 the area became Northern Coalfields Limited with Headquarters at Singrauli. Since then this coalfield has witnessed tremendous growth and has now developed in as one of the largest coal power complexes of the world.

3.4 Different Departments of the organization

Materials Management Sales and Quality Control Industrial Engeneering Department Personnel Department Finance Department Project & planning

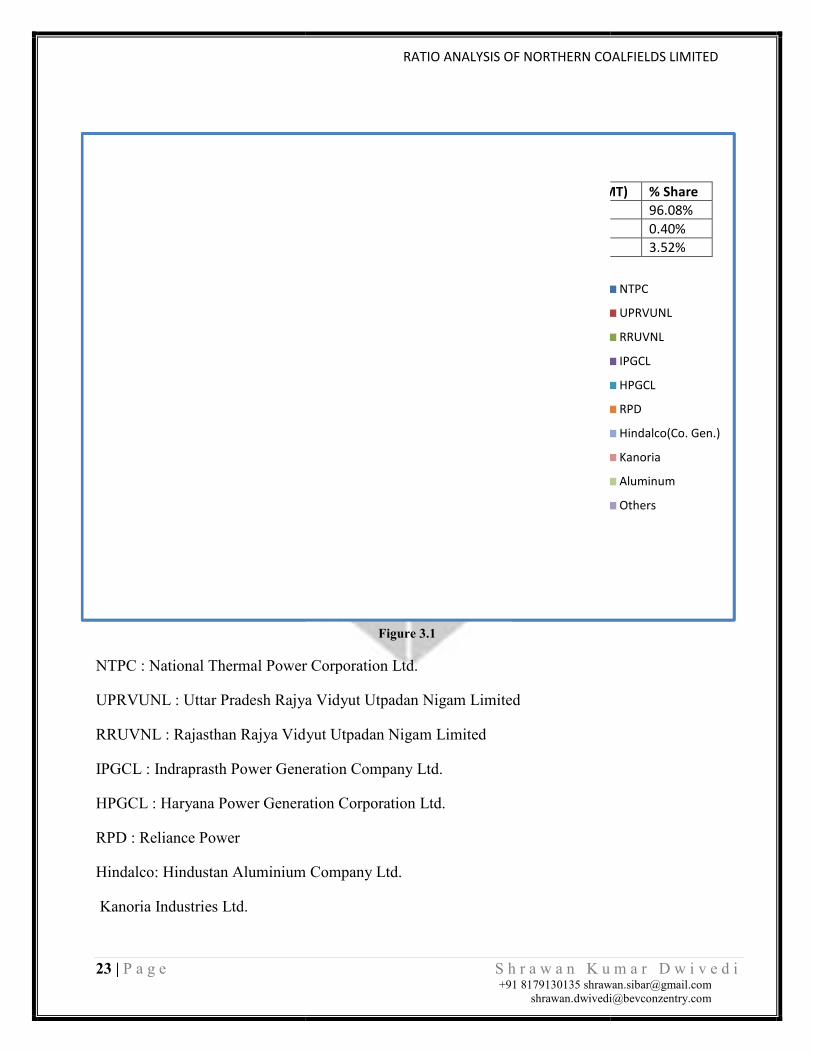

23 | P a g e

UPRVUNL21.90%

RRUVNL2.83%

IPGCL2.98% HPGCL

1.75%

RPD4.26%

Hindalco(Co. Gen.)0.37%

Kanoria0.41%

Consumer Profile (2009

NTPC : National Thermal Power Corporation Ltd.

UPRVUNL : Uttar Pradesh Rajya Vidyut Utpadan Nigam Limited

RRUVNL : Rajasthan Rajya Vidyut Utpadan Nigam Limited

IPGCL : Indraprasth Power Generation Company Ltd.

HPGCL : Haryana Power Generation Corporation Ltd.

RPD : Reliance Power

Hindalco: Hindustan Aluminium Company Ltd.

Kanoria Industries Ltd.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

NTPC61.58%

Hindalco(Co. Gen.)

Aluminum0.40% Others

3.52%

Consumer Profile (2009-10)Sector Coal Supplied (MT)Power 61.714 Aluminium 0.256 Other 2.260

Figure 3.1

NTPC : National Thermal Power Corporation Ltd.

UPRVUNL : Uttar Pradesh Rajya Vidyut Utpadan Nigam Limited

RRUVNL : Rajasthan Rajya Vidyut Utpadan Nigam Limited

Generation Company Ltd.

HPGCL : Haryana Power Generation Corporation Ltd.

Hindalco: Hindustan Aluminium Company Ltd.

Kanoria Industries Ltd.

ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected]

NTPC

UPRVUNL

RRUVNL

IPGCL

HPGCL

RPD

Hindalco(Co. Gen.)

Kanoria

Aluminum

Others

Coal Supplied (MT) % Share 96.08% 0.40% 3.52%

Kanoria Industries Ltd.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

24 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

3.5 Organizational Structure

Management Profile Board of Directors

Mr. Vinay Kumar Singh Chairman Cum Managing Director

FUNCTIONAL DIRECTORS

Ms. Shantilata Sahoo

Director ( Personnel)

Shri Niranjan Das

Director (Technical)

Project & Planning

Shri O. P. Mishra

Director (Technical) Operations

Shri S. K. Rawat

Director (Finance)

PART TIME OFFICIAL DIRECTOR

Shri Kailash Pati

Economic Advisor, Ministry of Coal

Dr. A. K. Sarkar

Director (Marketing), CIL

25 | P a g e

PART TIME NON

Mr.J.N.L. Shrivastava Mr.V.K. Bhalla

Mr. P. Parvathisem

Shri Chandan Roy

Company Secretary : Mr. D.H. Lalwani

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

PART TIME NON-OFFICIAL DIRECTORS

Mr.V.K. Bhalla Mr. B.N. Pan

Dr. B. B. Goel

PERMANENT INVITEES

Shri R. S. Pandey Shri M. K. Roy

: Mr. D.H. Lalwani

ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected]

Shri M. K. Roy

26 | P a g e

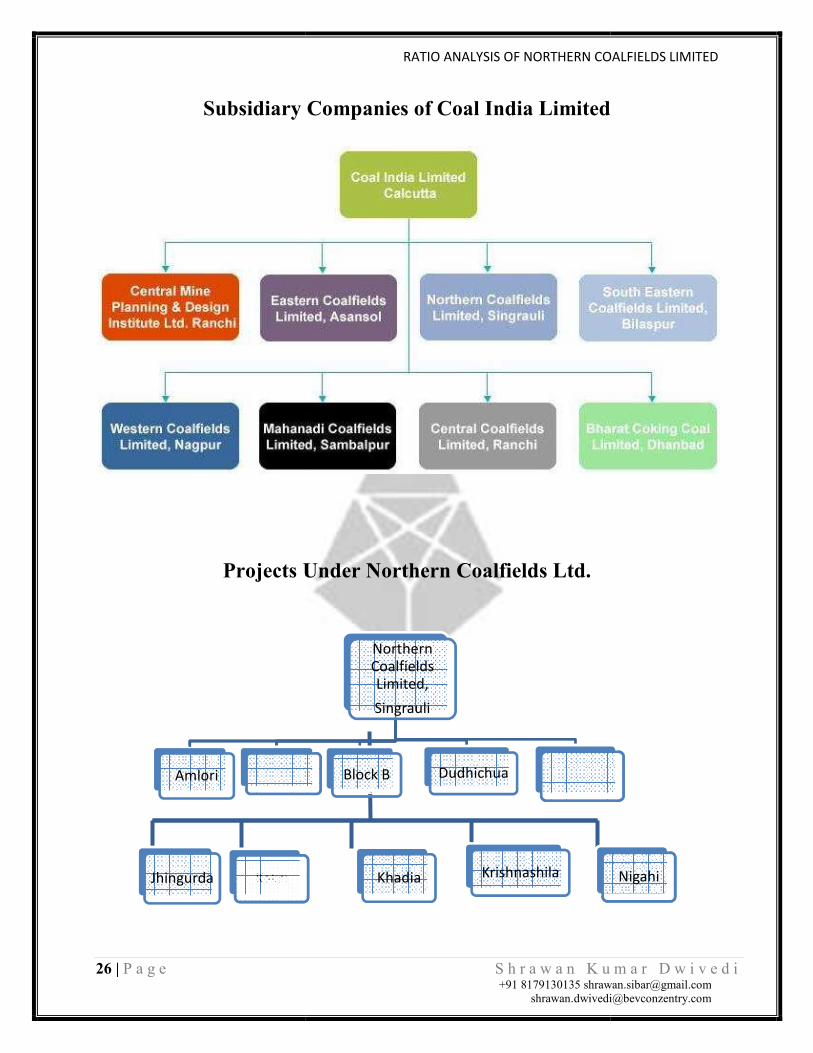

Subsidiary Companies of Coal India Limited

Projects Under Northern Coalfields Ltd.

Jhingurda Kakri

Amlori Bina

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Subsidiary Companies of Coal India Limited

Projects Under Northern Coalfields Ltd.

Northern Coalfields Limited,

Singrauli

Block B Dudhichua Jayant

Khadia Krishnashila

ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected]

Subsidiary Companies of Coal India Limited

Nigahi

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

27 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

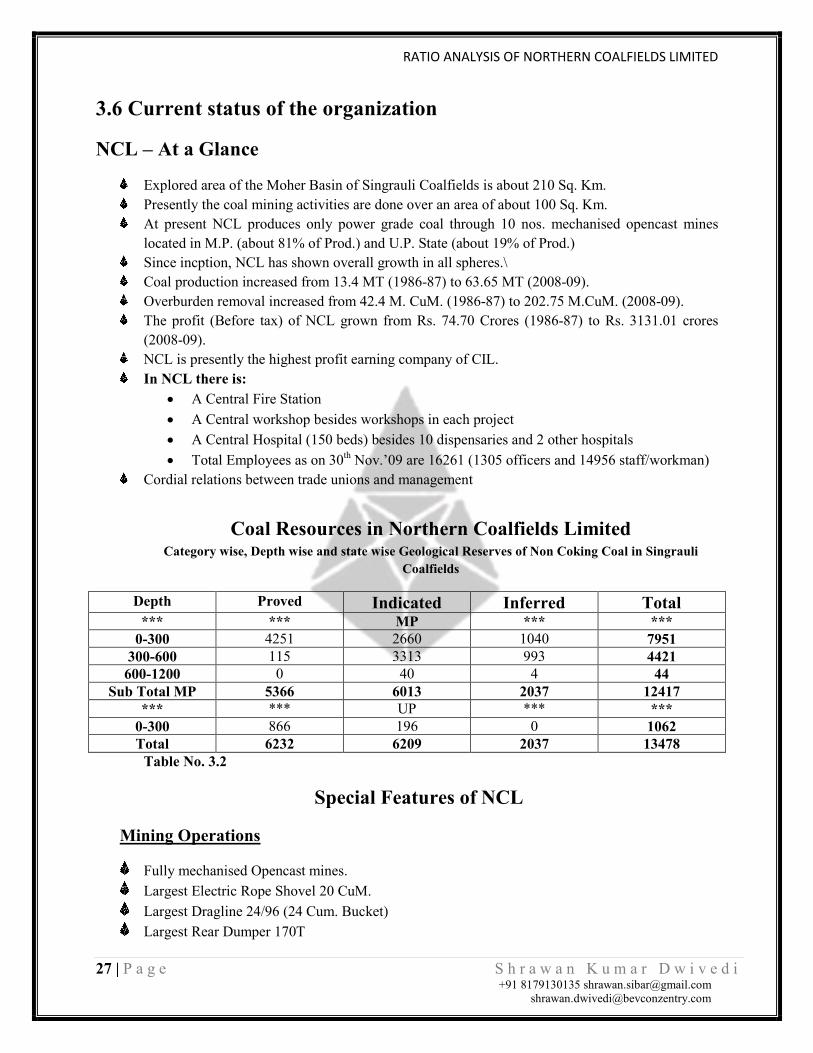

3.6 Current status of the organization

NCL – At a Glance

Explored area of the Moher Basin of Singrauli Coalfields is about 210 Sq. Km. Presently the coal mining activities are done over an area of about 100 Sq. Km. At present NCL produces only power grade coal through 10 nos. mechanised opencast mines

located in M.P. (about 81% of Prod.) and U.P. State (about 19% of Prod.) Since incption, NCL has shown overall growth in all spheres.\ Coal production increased from 13.4 MT (1986-87) to 63.65 MT (2008-09). Overburden removal increased from 42.4 M. CuM. (1986-87) to 202.75 M.CuM. (2008-09). The profit (Before tax) of NCL grown from Rs. 74.70 Crores (1986-87) to Rs. 3131.01 crores

(2008-09). NCL is presently the highest profit earning company of CIL. In NCL there is:

• A Central Fire Station • A Central workshop besides workshops in each project • A Central Hospital (150 beds) besides 10 dispensaries and 2 other hospitals • Total Employees as on 30th Nov.’09 are 16261 (1305 officers and 14956 staff/workman)

Cordial relations between trade unions and management

Coal Resources in Northern Coalfields Limited

Category wise, Depth wise and state wise Geological Reserves of Non Coking Coal in Singrauli Coalfields

Depth Proved Indicated Inferred Total *** *** MP *** *** 0-300 4251 2660 1040 7951

300-600 115 3313 993 4421 600-1200 0 40 4 44

Sub Total MP 5366 6013 2037 12417 *** *** UP *** *** 0-300 866 196 0 1062 Total 6232 6209 2037 13478 Table No. 3.2

Special Features of NCL

Mining Operations

Fully mechanised Opencast mines. Largest Electric Rope Shovel 20 CuM. Largest Dragline 24/96 (24 Cum. Bucket) Largest Rear Dumper 170T

28 | P a g e

Consumers’ Satisfaction

Supply of sized coal through CHP Electronically Weighed Coal Supplies Despatch through Merry-Go

Other Specialties

All employee’s salaries and wages are paid through Bank. Payment to all vendors through cheque with Bank name & Account Number Literacy of workforce, Free LPG to Employees, School Bus for Children, Supply of Drinking water Housing Satisfaction – 100% Land oustees Employed in NCl 25.92% of total workman (Land ous

out of total workman 14956)

Spares and other stores

12.18%

P.O.L.10.57%

Power5.14%

Repairs6.76%

Explosives4.43%

Others5.17%

Admin. Exp.4.16%

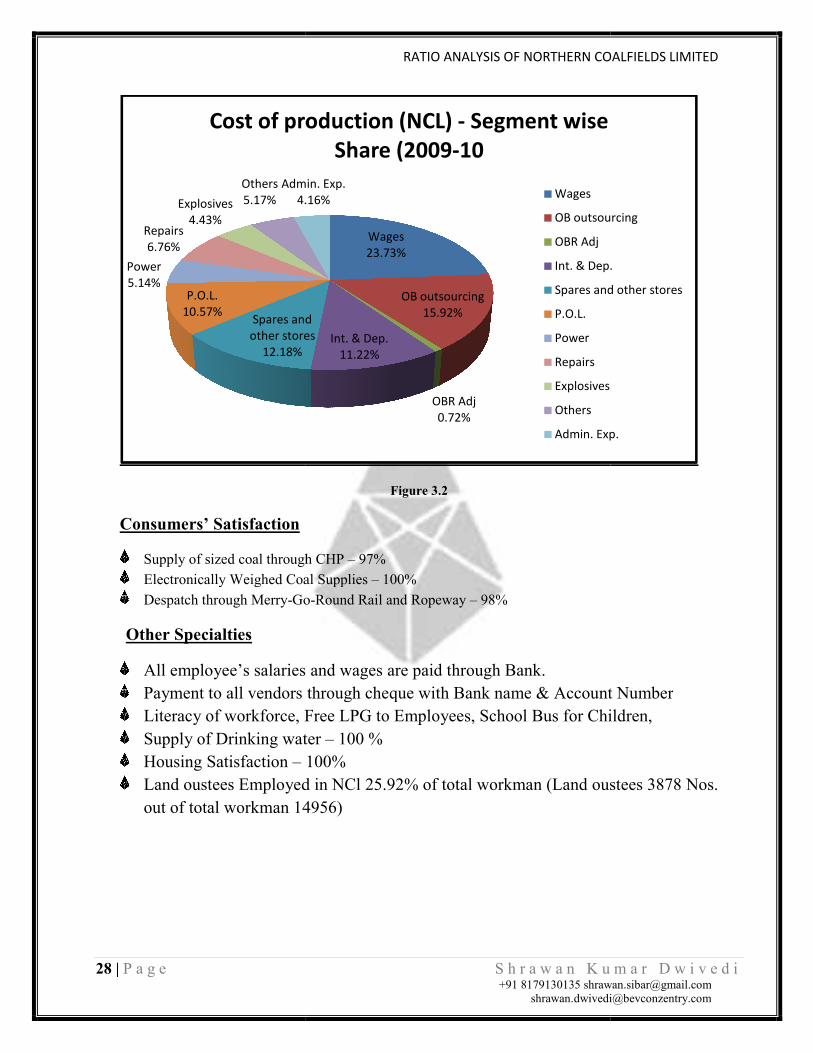

Cost of production (NCL)

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Figure 3.2

Supply of sized coal through CHP – 97% Electronically Weighed Coal Supplies – 100%

Go-Round Rail and Ropeway – 98%

All employee’s salaries and wages are paid through Bank. to all vendors through cheque with Bank name & Account Number

Literacy of workforce, Free LPG to Employees, School Bus for Children,Supply of Drinking water – 100 %

100% Land oustees Employed in NCl 25.92% of total workman (Land ousout of total workman 14956)

Wages23.73%

OB outsourcing15.92%

OBR Adj0.72%

Int. & Dep.11.22%

Spares and other stores

Admin. Exp.4.16%

Cost of production (NCL) - Segment wise Share (2009-10

Wages

OB outsourcing

OBR Adj

Int. & Dep.

Spares and other stores

P.O.L.

Power

Repairs

Explosives

Others

Admin. Exp.

ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected]

to all vendors through cheque with Bank name & Account Number Literacy of workforce, Free LPG to Employees, School Bus for Children,

Land oustees Employed in NCl 25.92% of total workman (Land oustees 3878 Nos.

Segment wise

OB outsourcing

Int. & Dep.

Spares and other stores

Admin. Exp.

29 | P a g e

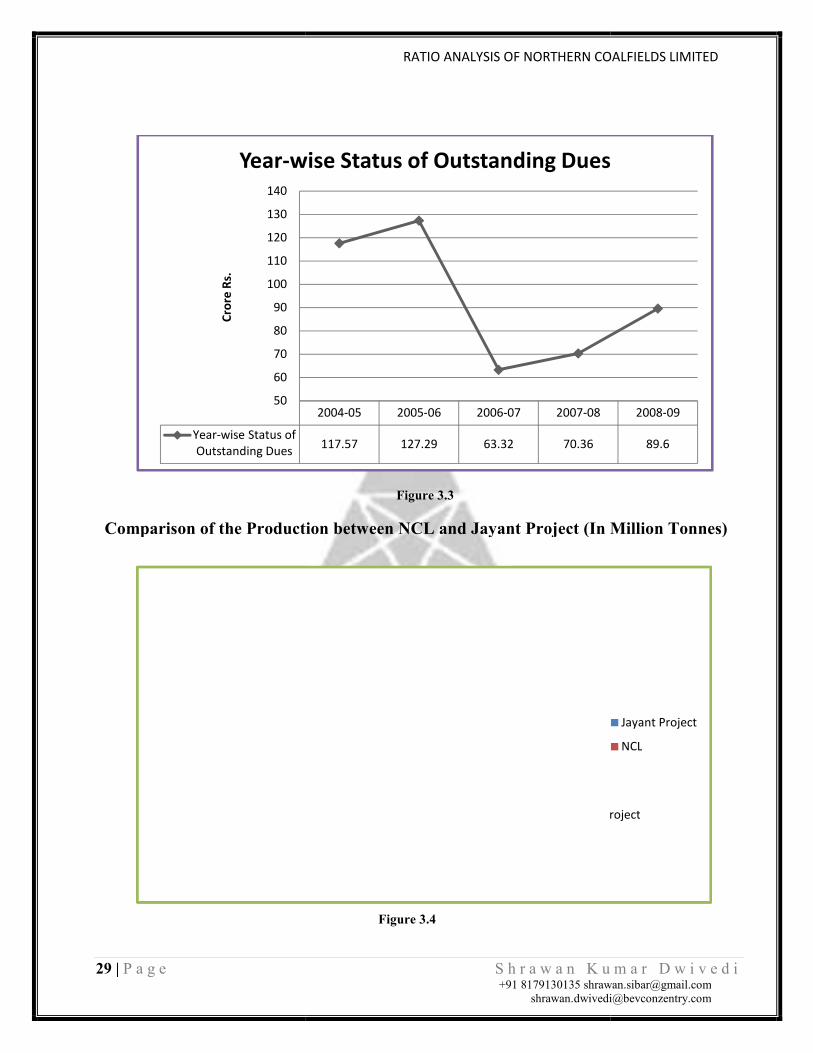

Comparison of the Production between NCL and Jayant Project (In Million Tonnes)

Year-wise Status of Outstanding Dues

50

60

70

80

90

100

110

120

130

140

Cror

e Rs

.

Year-wise Status of Outstanding Dues

0

10

20

30

40

50

60

70

2004-052005-06

10 9.9

49.95

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Figure 3.3

Comparison of the Production between NCL and Jayant Project (In Million Tonnes)

Figure 3.4

2004-05 2005-06 2006-07 2007-08

117.57 127.29 63.32 70.36

wise Status of Outstanding Dues

Jayant Project

NCL

062006-07

2007-082008-09

10.57 12.79 13.02

51.52 52.1659.62 63.65

ANALYSIS OF NORTHERN COALFIELDS LIMITED

S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected]

Comparison of the Production between NCL and Jayant Project (In Million Tonnes)

2008-09

89.6

wise Status of Outstanding Dues

Jayant Project

Jayant Project

NCL

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

30 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

International Standards

ISO 14000 Certification for Environmental Management System since 2001 and renewed

up to 2010.

ISO 9001:2000 Certification for Quality Management System since 11 May 2009 and

valid until 14 November 2010.

Efforts for certification of Integrated Management System complying ISO 14001:2004,

ISO 9001:2008, OHSAS 18001:2007 and SA 8000:2008 are being made and stage- 1

audit for the same is scheduled from 04.01.2010 by the Certification Body.

3.7 Future plans of the organization

After achieving profits and coal production more than the targeted value, NCL in collaboration

with UPRUVNL is planning to set up a 1000 megawatt coal-based power plant in Uttar Pradesh.

NCL is also planning to set up a power plant of 1000 megawatts in Madhya Pradesh with

Neyewali Lignite Corporation. NCL has already got the permission with the Directors of CIL.

Coal India Plans to raise Rs 4,500 cr by issue of fresh capital thru book-building route. Coal

India has equity base of Rs 6,316 crore is holding company of seven coal producers Aggregate

profit to top Rs 7,043 cr this year. Performance of the company is continuously improving

quantitatively and qualitatively. As a part of liberalization Process, the CIL is going for proposed

disinvestments through Initial Public Offer (IPO). In deregulated environment, market is the best

judge for performance and market discounts all past and future events, CIL is confident to get

high value quote in the secondary market.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

31 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

3.8 Awards and achievements Prestigious “ INDIRA GANDHI NATIONAL AWARD FOR EXCELLENCE” Given to

the BEST ENTERPRISES Amongst the Public Sector

NATIONAL SAFETY AWARDS ( By the Hon’ble President of India)

Four Awards of Excellence ( By the Hon’ble Prime Minister for Bina, Nigahi, Amlohri

And Jhingurda Projects.

National Award for promotion of Family Planning

Coal India Award of Excellence

For excellence in pollution Control – Indira Gandhi National Gold Award

Jawaharlal Nehru Memorial National Award

Dadabhai Naoroji International Millennium Award

Teri National Award for Environment

Rajbhasha Shri Award

Best Chief Executive Gold Award by WHAT HAILS PUBLIC SECTOR TODAY

Bharat Gaurav Award by India International Friendship Society

9th Gold Award in Metal & Mining Sector for outstanding achievement in Environment

Management by GREENTECH

SCOPE Meritorious award for environmental excellence & sustainable development –

Gold Plaque Certificate of Excellence in Corporate Performance awarded by CIL.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

32 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CHAPTER IV

DATA ANALYSIS

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

33 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

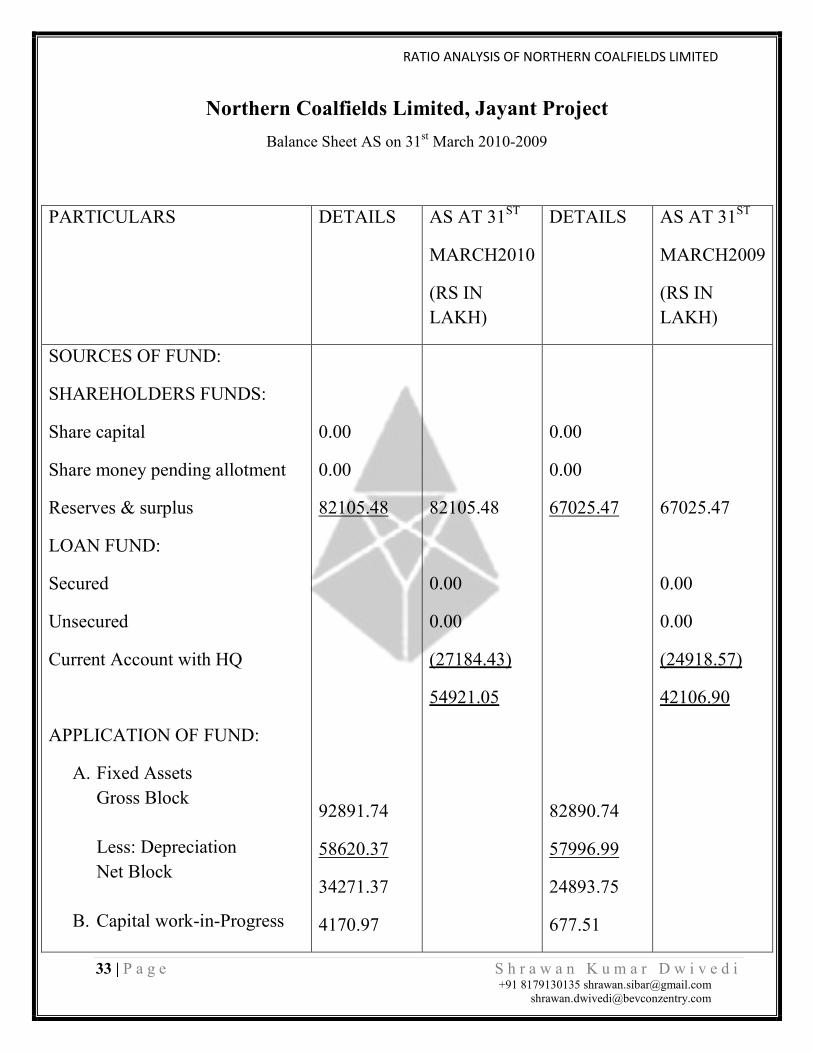

Northern Coalfields Limited, Jayant Project Balance Sheet AS on 31st March 2010-2009

PARTICULARS DETAILS AS AT 31ST

MARCH2010

(RS IN LAKH)

DETAILS AS AT 31ST

MARCH2009

(RS IN LAKH)

SOURCES OF FUND:

SHAREHOLDERS FUNDS:

Share capital

Share money pending allotment

Reserves & surplus

LOAN FUND:

Secured

Unsecured

Current Account with HQ

APPLICATION OF FUND:

A. Fixed Assets Gross Block Less: Depreciation Net Block

B. Capital work-in-Progress

0.00

0.00

82105.48

92891.74

58620.37

34271.37

4170.97

82105.48

0.00

0.00

(27184.43)

54921.05

0.00

0.00

67025.47

82890.74

57996.99

24893.75

677.51

67025.47

0.00

0.00

(24918.57)

42106.90

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

34 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

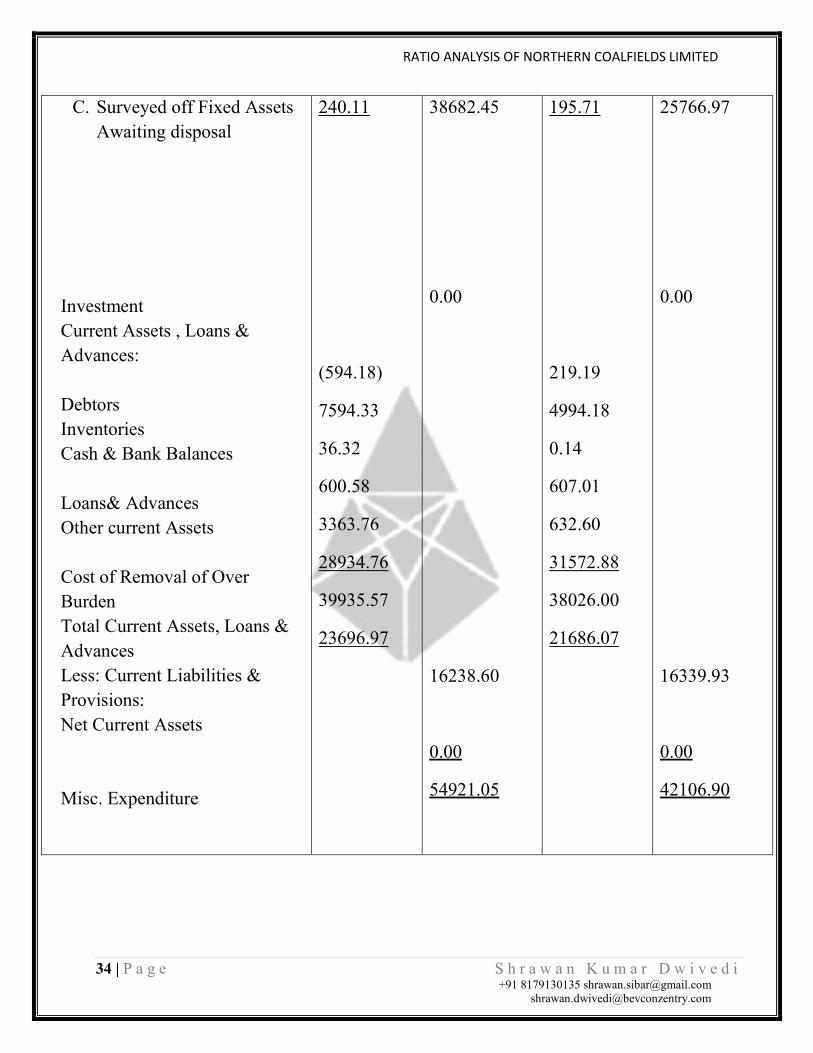

C. Surveyed off Fixed Assets Awaiting disposal

Investment Current Assets , Loans & Advances: Debtors Inventories Cash & Bank Balances Loans& Advances Other current Assets Cost of Removal of Over Burden Total Current Assets, Loans & Advances Less: Current Liabilities & Provisions: Net Current Assets Misc. Expenditure

240.11

(594.18)

7594.33

36.32

600.58

3363.76

28934.76

39935.57

23696.97

38682.45

0.00

16238.60

0.00

54921.05

195.71

219.19

4994.18

0.14

607.01

632.60

31572.88

38026.00

21686.07

25766.97

0.00

16339.93

0.00

42106.90

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

35 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

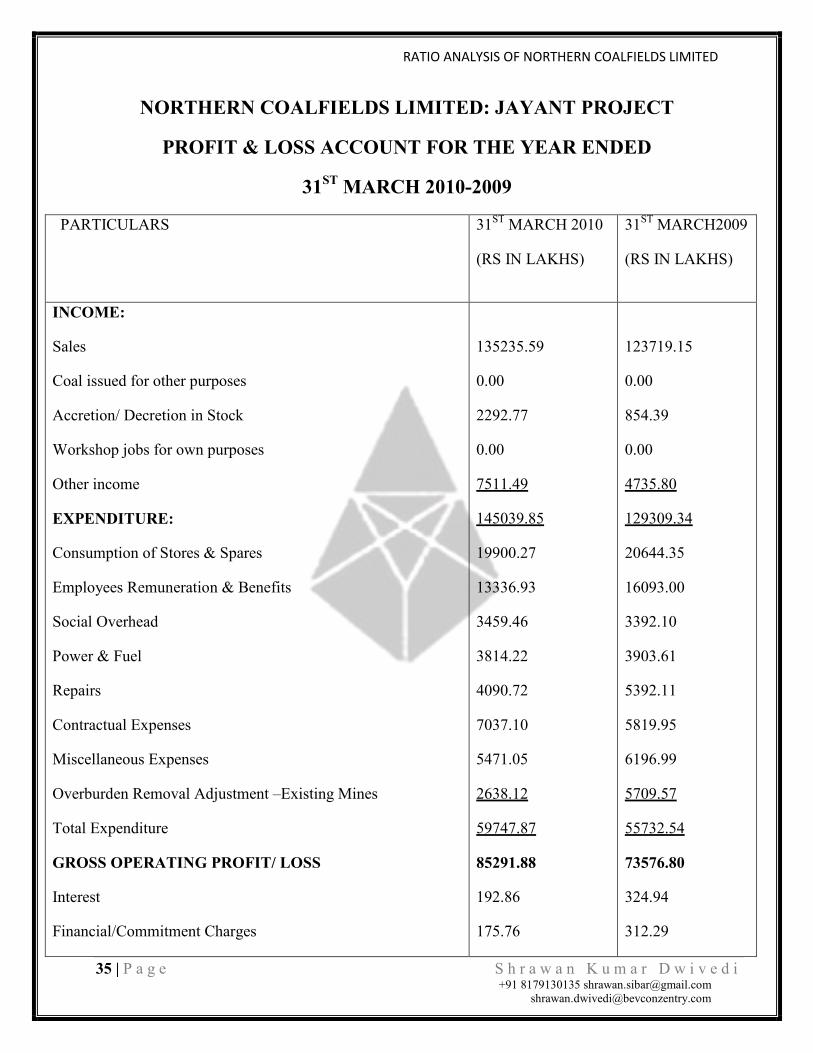

NORTHERN COALFIELDS LIMITED: JAYANT PROJECT

PROFIT & LOSS ACCOUNT FOR THE YEAR ENDED

31ST MARCH 2010-2009

PARTICULARS 31ST MARCH 2010

(RS IN LAKHS)

31ST MARCH2009

(RS IN LAKHS)

INCOME:

Sales

Coal issued for other purposes

Accretion/ Decretion in Stock

Workshop jobs for own purposes

Other income

EXPENDITURE:

Consumption of Stores & Spares

Employees Remuneration & Benefits

Social Overhead

Power & Fuel

Repairs

Contractual Expenses

Miscellaneous Expenses

Overburden Removal Adjustment –Existing Mines

Total Expenditure

GROSS OPERATING PROFIT/ LOSS

Interest

Financial/Commitment Charges

135235.59

0.00

2292.77

0.00

7511.49

145039.85

19900.27

13336.93

3459.46

3814.22

4090.72

7037.10

5471.05

2638.12

59747.87

85291.88

192.86

175.76

123719.15

0.00

854.39

0.00

4735.80

129309.34

20644.35

16093.00

3392.10

3903.61

5392.11

5819.95

6196.99

5709.57

55732.54

73576.80

324.94

312.29

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

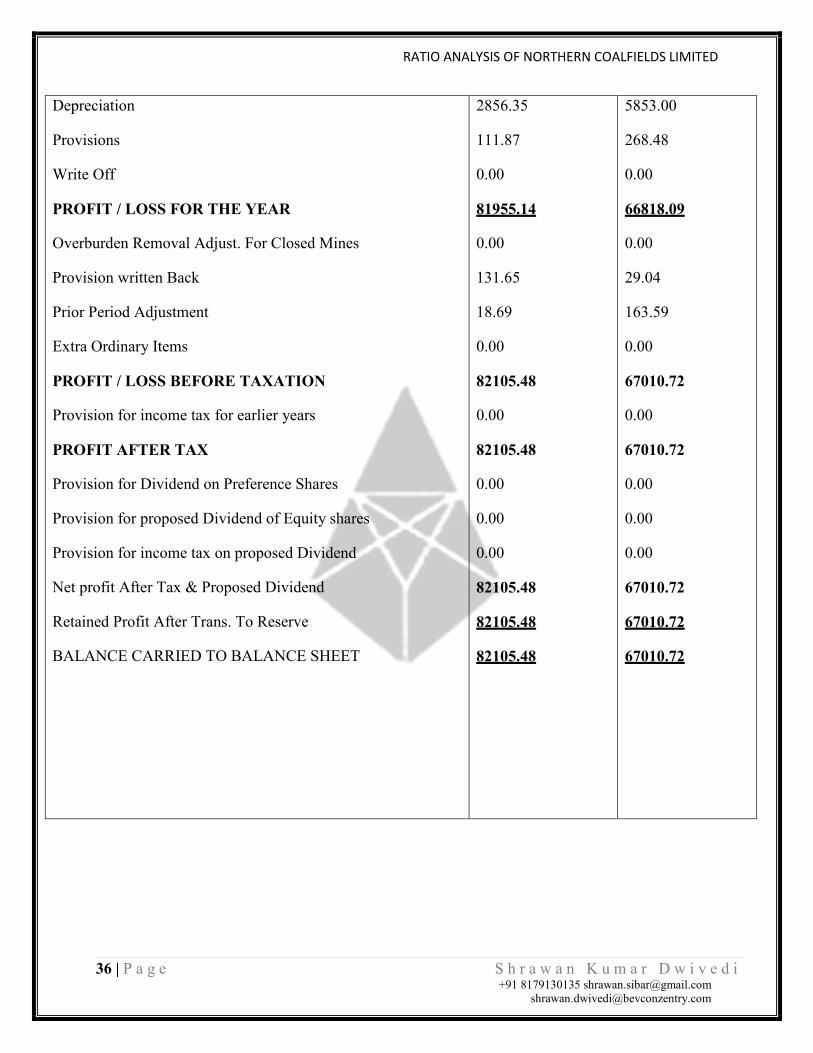

36 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Depreciation

Provisions

Write Off

PROFIT / LOSS FOR THE YEAR

Overburden Removal Adjust. For Closed Mines

Provision written Back

Prior Period Adjustment

Extra Ordinary Items

PROFIT / LOSS BEFORE TAXATION

Provision for income tax for earlier years

PROFIT AFTER TAX

Provision for Dividend on Preference Shares

Provision for proposed Dividend of Equity shares

Provision for income tax on proposed Dividend

Net profit After Tax & Proposed Dividend

Retained Profit After Trans. To Reserve

BALANCE CARRIED TO BALANCE SHEET

2856.35

111.87

0.00

81955.14

0.00

131.65

18.69

0.00

82105.48

0.00

82105.48

0.00

0.00

0.00

82105.48

82105.48

82105.48

5853.00

268.48

0.00

66818.09

0.00

29.04

163.59

0.00

67010.72

0.00

67010.72

0.00

0.00

0.00

67010.72

67010.72

67010.72

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

37 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CALCULATION & INTERPRETATION OF RATIOS

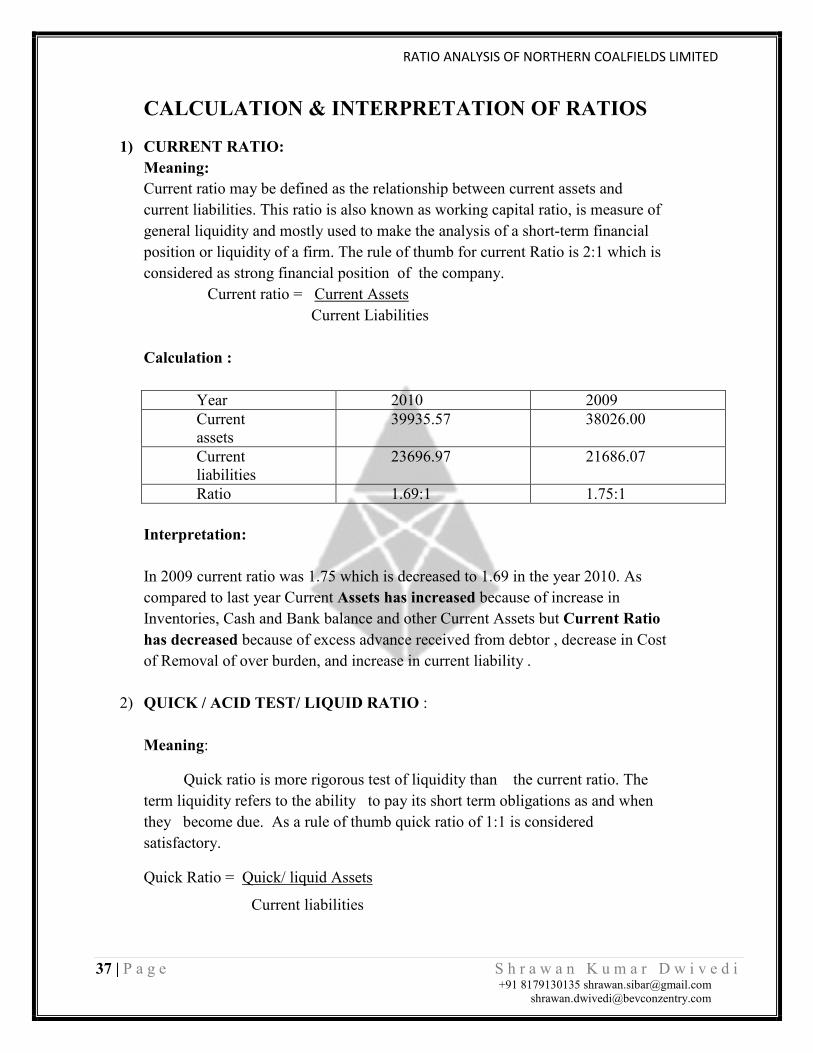

1) CURRENT RATIO: Meaning: Current ratio may be defined as the relationship between current assets and current liabilities. This ratio is also known as working capital ratio, is measure of general liquidity and mostly used to make the analysis of a short-term financial position or liquidity of a firm. The rule of thumb for current Ratio is 2:1 which is considered as strong financial position of the company. Current ratio = Current Assets Current Liabilities Calculation :

Year 2010 2009 Current assets

39935.57 38026.00

Current liabilities

23696.97 21686.07

Ratio 1.69:1 1.75:1 Interpretation: In 2009 current ratio was 1.75 which is decreased to 1.69 in the year 2010. As compared to last year Current Assets has increased because of increase in Inventories, Cash and Bank balance and other Current Assets but Current Ratio has decreased because of excess advance received from debtor , decrease in Cost of Removal of over burden, and increase in current liability .

2) QUICK / ACID TEST/ LIQUID RATIO : Meaning:

Quick ratio is more rigorous test of liquidity than the current ratio. The term liquidity refers to the ability to pay its short term obligations as and when they become due. As a rule of thumb quick ratio of 1:1 is considered satisfactory.

Quick Ratio = Quick/ liquid Assets

Current liabilities

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

38 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

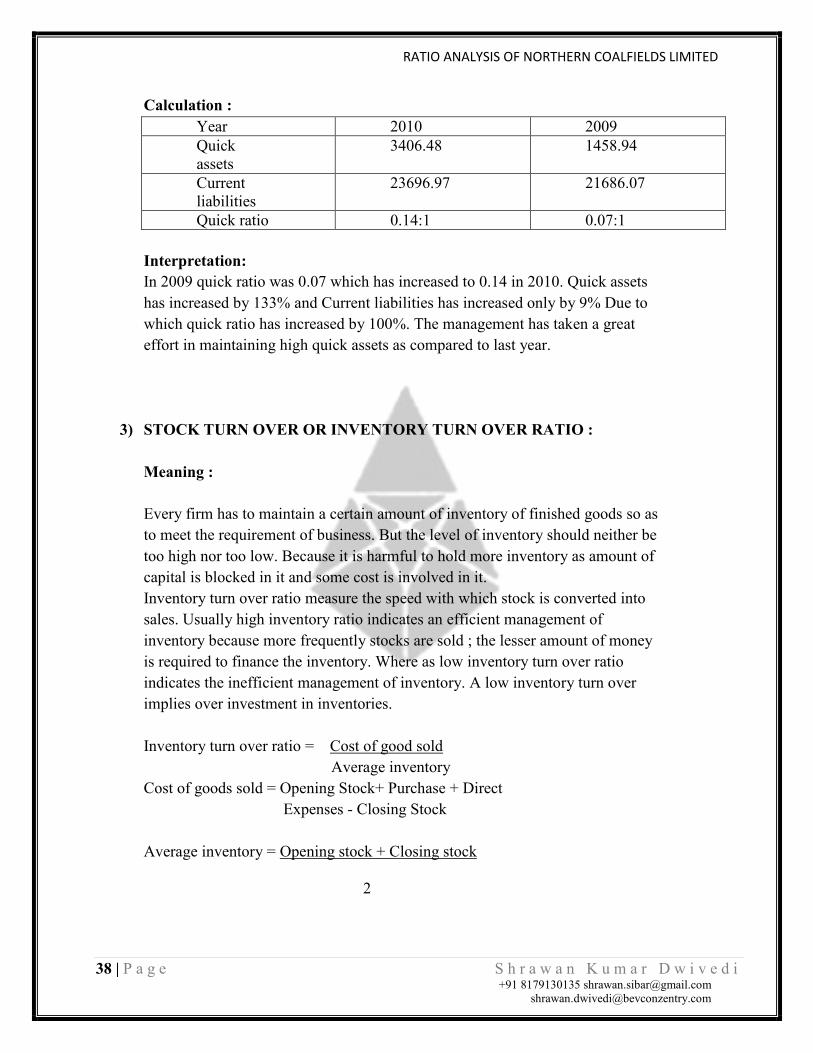

Calculation : Year 2010 2009 Quick assets

3406.48 1458.94

Current liabilities

23696.97 21686.07

Quick ratio 0.14:1 0.07:1 Interpretation: In 2009 quick ratio was 0.07 which has increased to 0.14 in 2010. Quick assets has increased by 133% and Current liabilities has increased only by 9% Due to which quick ratio has increased by 100%. The management has taken a great effort in maintaining high quick assets as compared to last year.

3) STOCK TURN OVER OR INVENTORY TURN OVER RATIO : Meaning : Every firm has to maintain a certain amount of inventory of finished goods so as to meet the requirement of business. But the level of inventory should neither be too high nor too low. Because it is harmful to hold more inventory as amount of capital is blocked in it and some cost is involved in it. Inventory turn over ratio measure the speed with which stock is converted into sales. Usually high inventory ratio indicates an efficient management of inventory because more frequently stocks are sold ; the lesser amount of money is required to finance the inventory. Where as low inventory turn over ratio indicates the inefficient management of inventory. A low inventory turn over implies over investment in inventories. Inventory turn over ratio = Cost of good sold Average inventory Cost of goods sold = Opening Stock+ Purchase + Direct Expenses - Closing Stock Average inventory = Opening stock + Closing stock

2

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

39 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

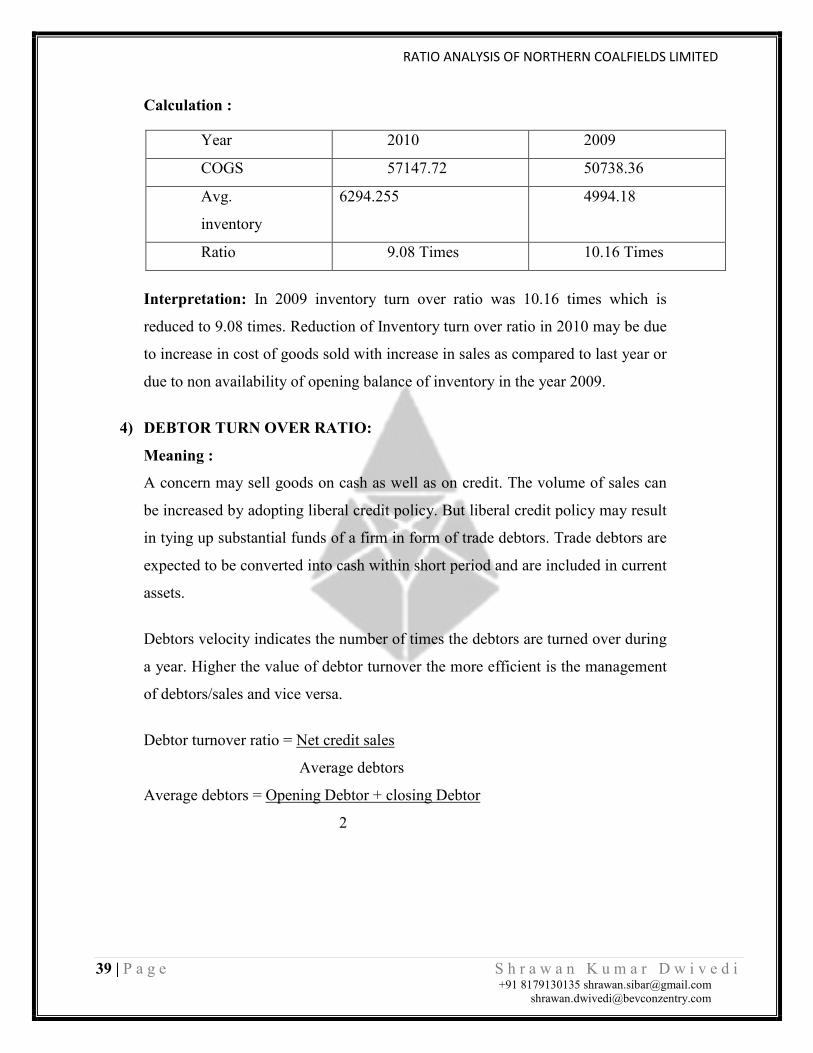

Calculation :

Year 2010 2009

COGS 57147.72 50738.36

Avg.

inventory

6294.255 4994.18

Ratio 9.08 Times 10.16 Times

Interpretation: In 2009 inventory turn over ratio was 10.16 times which is

reduced to 9.08 times. Reduction of Inventory turn over ratio in 2010 may be due

to increase in cost of goods sold with increase in sales as compared to last year or

due to non availability of opening balance of inventory in the year 2009.

4) DEBTOR TURN OVER RATIO:

Meaning :

A concern may sell goods on cash as well as on credit. The volume of sales can

be increased by adopting liberal credit policy. But liberal credit policy may result

in tying up substantial funds of a firm in form of trade debtors. Trade debtors are

expected to be converted into cash within short period and are included in current

assets.

Debtors velocity indicates the number of times the debtors are turned over during

a year. Higher the value of debtor turnover the more efficient is the management

of debtors/sales and vice versa.

Debtor turnover ratio = Net credit sales

Average debtors

Average debtors = Opening Debtor + closing Debtor

2

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

40 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

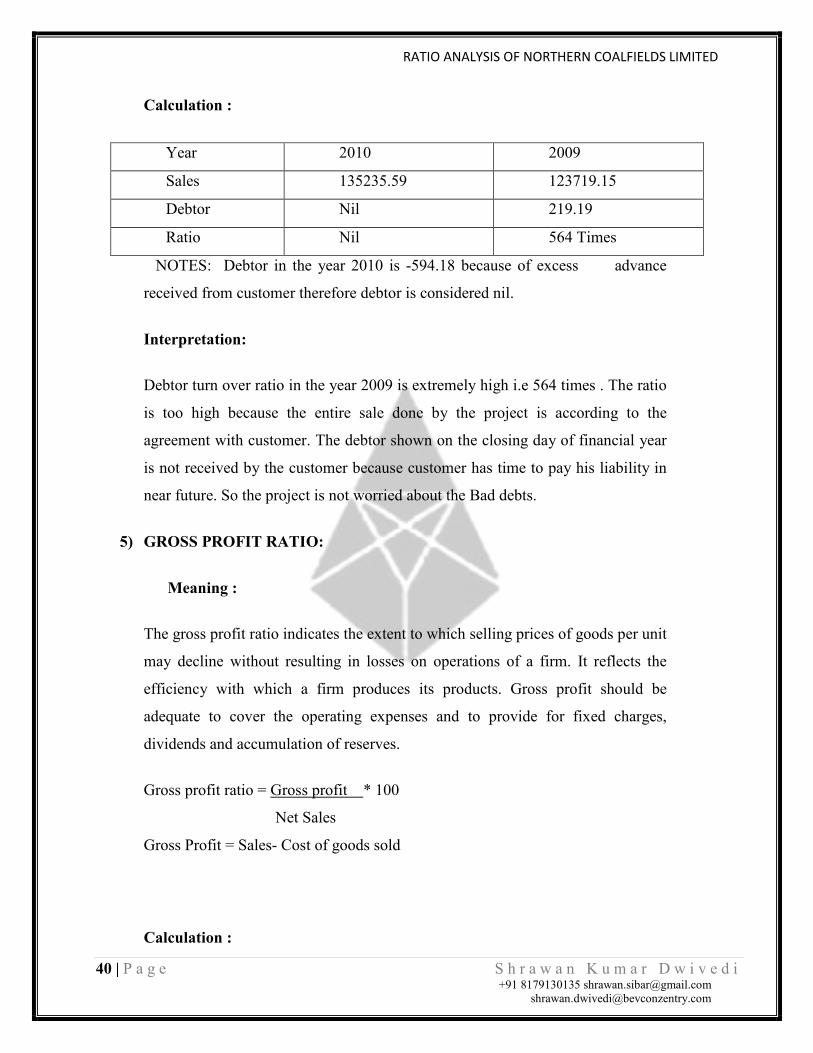

Calculation :

NOTES: Debtor in the year 2010 is -594.18 because of excess advance

received from customer therefore debtor is considered nil.

Interpretation:

Debtor turn over ratio in the year 2009 is extremely high i.e 564 times . The ratio

is too high because the entire sale done by the project is according to the

agreement with customer. The debtor shown on the closing day of financial year

is not received by the customer because customer has time to pay his liability in

near future. So the project is not worried about the Bad debts.

5) GROSS PROFIT RATIO:

Meaning :

The gross profit ratio indicates the extent to which selling prices of goods per unit

may decline without resulting in losses on operations of a firm. It reflects the

efficiency with which a firm produces its products. Gross profit should be

adequate to cover the operating expenses and to provide for fixed charges,

dividends and accumulation of reserves.

Gross profit ratio = Gross profit * 100

Net Sales

Gross Profit = Sales- Cost of goods sold

Calculation :

Year 2010 2009

Sales 135235.59 123719.15

Debtor Nil 219.19

Ratio Nil 564 Times

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

41 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

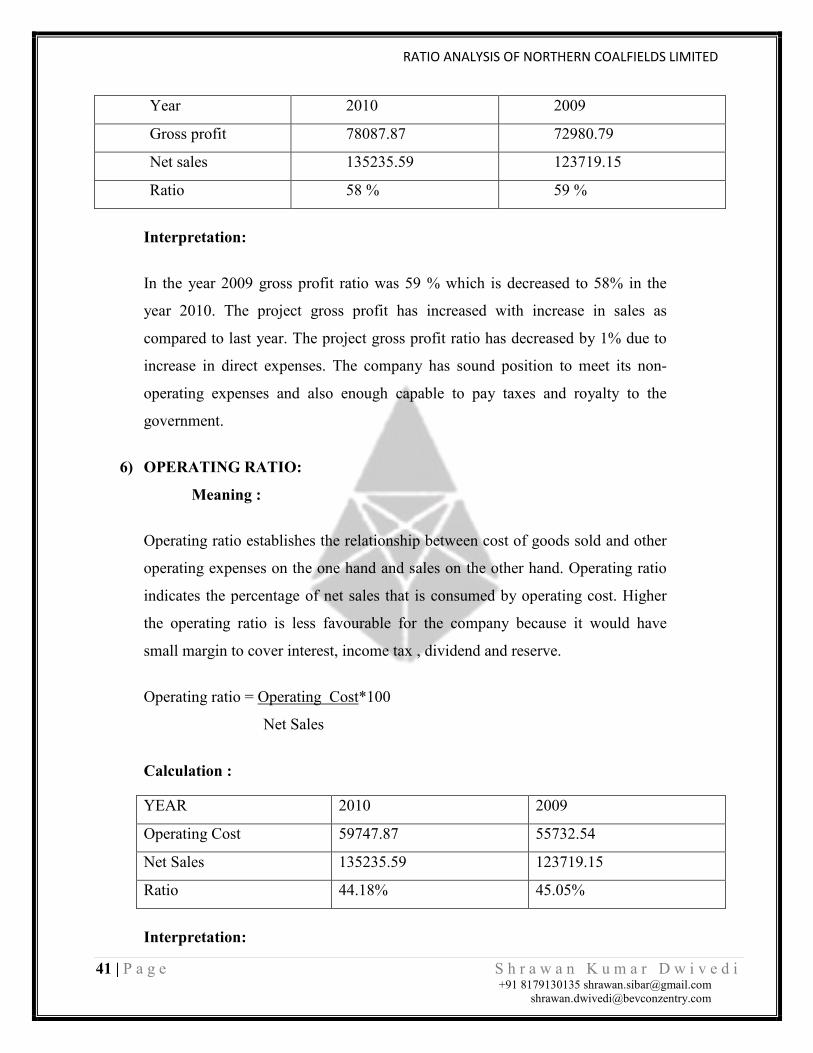

Year 2010 2009

Gross profit 78087.87 72980.79

Net sales 135235.59 123719.15

Ratio 58 % 59 %

Interpretation:

In the year 2009 gross profit ratio was 59 % which is decreased to 58% in the

year 2010. The project gross profit has increased with increase in sales as

compared to last year. The project gross profit ratio has decreased by 1% due to

increase in direct expenses. The company has sound position to meet its non-

operating expenses and also enough capable to pay taxes and royalty to the

government.

6) OPERATING RATIO:

Meaning :

Operating ratio establishes the relationship between cost of goods sold and other

operating expenses on the one hand and sales on the other hand. Operating ratio

indicates the percentage of net sales that is consumed by operating cost. Higher

the operating ratio is less favourable for the company because it would have

small margin to cover interest, income tax , dividend and reserve.

Operating ratio = Operating Cost*100

Net Sales

Calculation :

YEAR 2010 2009

Operating Cost 59747.87 55732.54

Net Sales 135235.59 123719.15

Ratio 44.18% 45.05%

Interpretation:

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

42 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

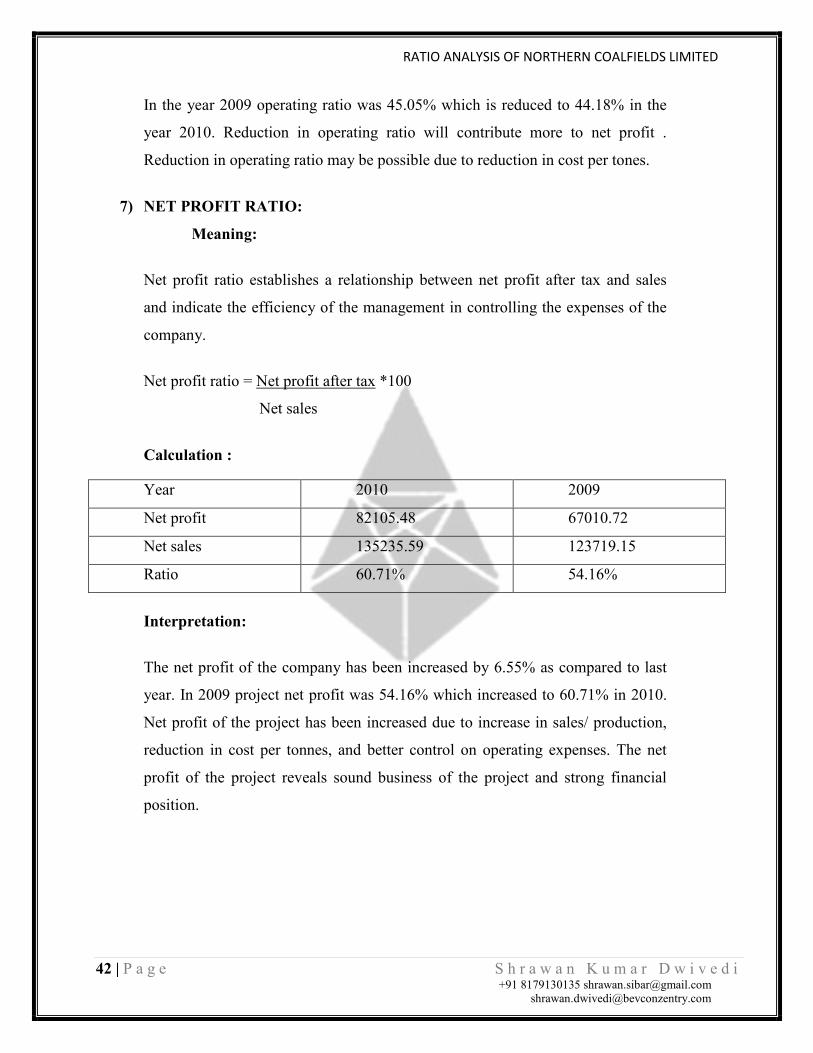

In the year 2009 operating ratio was 45.05% which is reduced to 44.18% in the

year 2010. Reduction in operating ratio will contribute more to net profit .

Reduction in operating ratio may be possible due to reduction in cost per tones.

7) NET PROFIT RATIO:

Meaning:

Net profit ratio establishes a relationship between net profit after tax and sales

and indicate the efficiency of the management in controlling the expenses of the

company.

Net profit ratio = Net profit after tax *100

Net sales

Calculation :

Year 2010 2009

Net profit 82105.48 67010.72

Net sales 135235.59 123719.15

Ratio 60.71% 54.16%

Interpretation:

The net profit of the company has been increased by 6.55% as compared to last

year. In 2009 project net profit was 54.16% which increased to 60.71% in 2010.

Net profit of the project has been increased due to increase in sales/ production,

reduction in cost per tonnes, and better control on operating expenses. The net

profit of the project reveals sound business of the project and strong financial

position.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

43 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

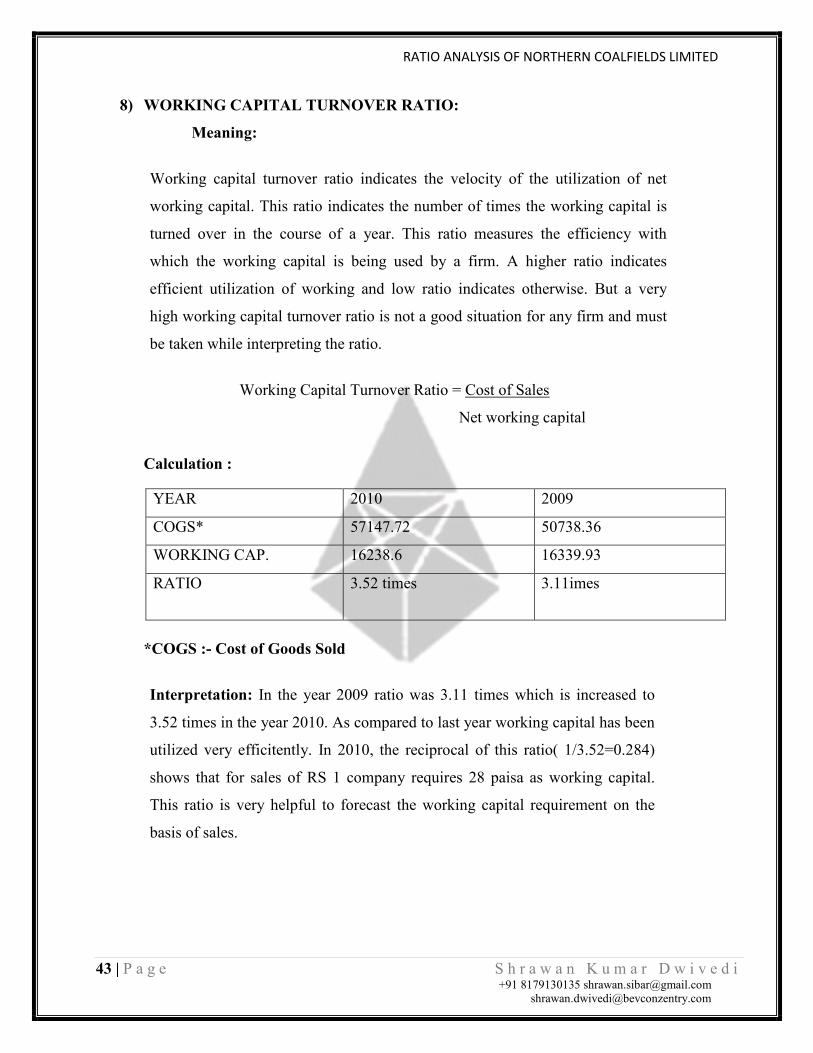

8) WORKING CAPITAL TURNOVER RATIO:

Meaning:

Working capital turnover ratio indicates the velocity of the utilization of net

working capital. This ratio indicates the number of times the working capital is

turned over in the course of a year. This ratio measures the efficiency with

which the working capital is being used by a firm. A higher ratio indicates

efficient utilization of working and low ratio indicates otherwise. But a very

high working capital turnover ratio is not a good situation for any firm and must

be taken while interpreting the ratio.

Working Capital Turnover Ratio = Cost of Sales

Net working capital

Calculation :

YEAR 2010 2009

COGS* 57147.72 50738.36

WORKING CAP. 16238.6 16339.93

RATIO 3.52 times 3.11imes

*COGS :- Cost of Goods Sold

Interpretation: In the year 2009 ratio was 3.11 times which is increased to

3.52 times in the year 2010. As compared to last year working capital has been

utilized very efficitently. In 2010, the reciprocal of this ratio( 1/3.52=0.284)

shows that for sales of RS 1 company requires 28 paisa as working capital.

This ratio is very helpful to forecast the working capital requirement on the

basis of sales.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

44 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

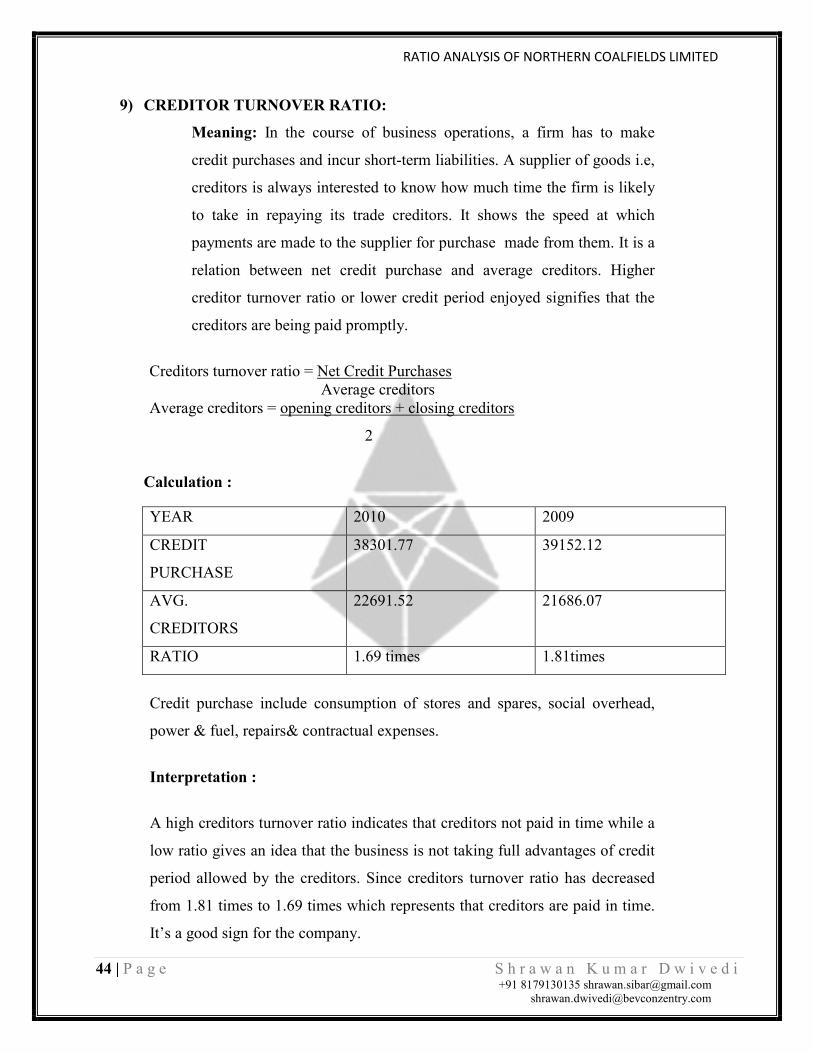

9) CREDITOR TURNOVER RATIO:

Meaning: In the course of business operations, a firm has to make

credit purchases and incur short-term liabilities. A supplier of goods i.e,

creditors is always interested to know how much time the firm is likely

to take in repaying its trade creditors. It shows the speed at which

payments are made to the supplier for purchase made from them. It is a

relation between net credit purchase and average creditors. Higher

creditor turnover ratio or lower credit period enjoyed signifies that the

creditors are being paid promptly.

Creditors turnover ratio = Net Credit Purchases Average creditors Average creditors = opening creditors + closing creditors

2

Calculation :

YEAR 2010 2009

CREDIT

PURCHASE

38301.77 39152.12

AVG.

CREDITORS

22691.52 21686.07

RATIO 1.69 times 1.81times

Credit purchase include consumption of stores and spares, social overhead,

power & fuel, repairs& contractual expenses.

Interpretation :

A high creditors turnover ratio indicates that creditors not paid in time while a

low ratio gives an idea that the business is not taking full advantages of credit

period allowed by the creditors. Since creditors turnover ratio has decreased

from 1.81 times to 1.69 times which represents that creditors are paid in time.

It’s a good sign for the company.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

45 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

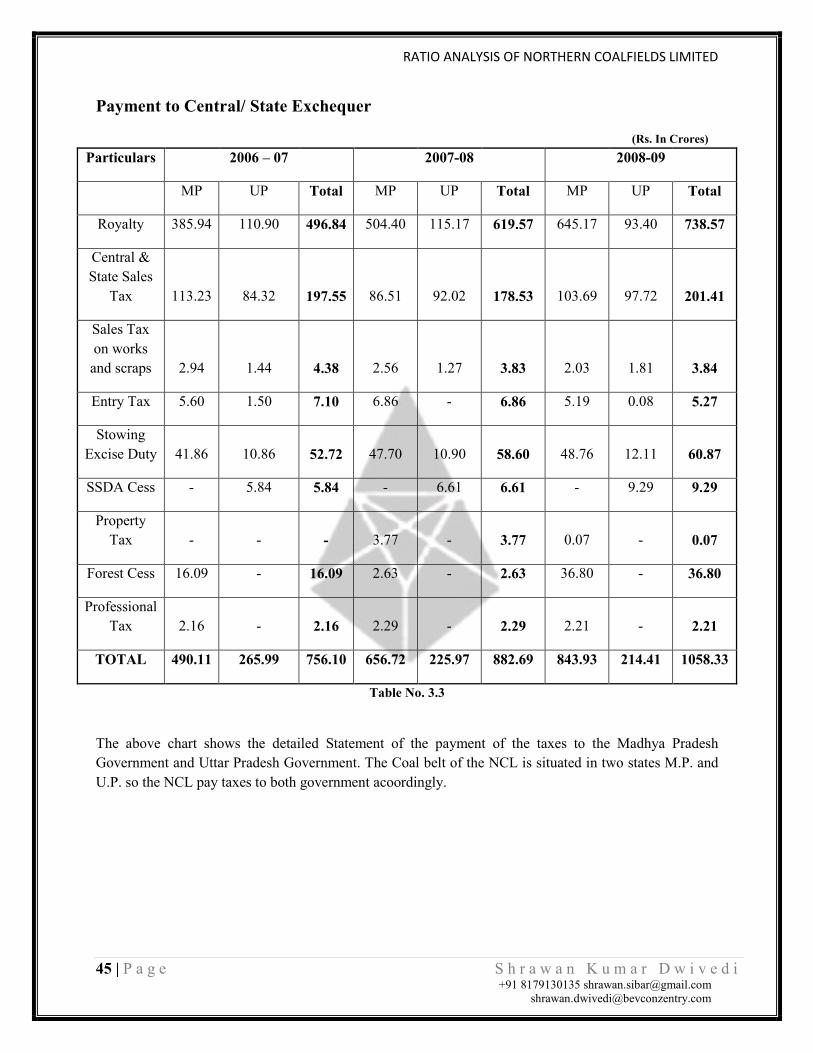

Payment to Central/ State Exchequer

(Rs. In Crores) Particulars 2006 – 07 2007-08 2008-09

MP UP Total MP UP Total MP UP Total

Royalty 385.94 110.90 496.84 504.40 115.17 619.57 645.17 93.40 738.57

Central & State Sales

Tax 113.23 84.32 197.55 86.51 92.02 178.53 103.69 97.72 201.41

Sales Tax on works and scraps 2.94 1.44 4.38 2.56 1.27 3.83 2.03 1.81 3.84

Entry Tax 5.60 1.50 7.10 6.86 - 6.86 5.19 0.08 5.27

Stowing Excise Duty 41.86 10.86 52.72 47.70 10.90 58.60 48.76 12.11 60.87

SSDA Cess - 5.84 5.84 - 6.61 6.61 - 9.29 9.29

Property Tax - - - 3.77 - 3.77 0.07 - 0.07

Forest Cess 16.09 - 16.09 2.63 - 2.63 36.80 - 36.80

Professional Tax 2.16 - 2.16 2.29 - 2.29 2.21 - 2.21

TOTAL 490.11 265.99 756.10 656.72 225.97 882.69 843.93 214.41 1058.33

Table No. 3.3

The above chart shows the detailed Statement of the payment of the taxes to the Madhya Pradesh Government and Uttar Pradesh Government. The Coal belt of the NCL is situated in two states M.P. and U.P. so the NCL pay taxes to both government acoordingly.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

46 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

CHAPTER V

SUMMARY AND CONCLUSION

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

47 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

5.1 Major Findings & Suggestions I came across following suggestions and findings during undergoing the project work on topic

“FINANCIAL ANALYSIS OF NORTHERN COALFIELDS LIMITED”.

1. In NCL the coordination among the various sections of the Finance & Accounts

department is very nice, as the Finance & Accounts department is a big department

consisting of near about 32 sections. It is the work force of the Finance & Accounts

department, which makes it possible.

2. In the NCL there not to create debtors they generally deal with first to receive the cash

or cheque, and then they supply the finished material.

3. In the NCL there working capital management is very good, they use the IBS (ERP

system) to manage the over all activity.

4. During the study I find that their is no huge variation in budget decided and the actual

one.

5. The taxation policy is to be made flexible because of which bulkiness of the work is to

be removed.

6. The tendering process time is to be minimized so that the current market price benefits

if any can be availed.

7. Monthly return filling is not on line process, hence sales and excise department face

problem.

8. Online inventory valuation can be implemented.

9. The departmental policies is to made flexible which leads to decrease in the work flow

process as well as it leads in better profits.

10. Some The staff members of the NCL are lack of the Computer knowledge. During my internship I observed that the employees don’t have the necessary training to do the job efficiently and properly. So I think the management should arrange special training for educating them. Proper distribution of work leads to success in every organization. Proper distribution of work prevents the employee from over and under work situation. So for a smooth running of an organization proper distribution of work is the hint to be followed. During my internship I observed that there was no proper distribution of work in the organization. So ln this case the organization would not be able to utilize their energy. So their should be proper distribution of work

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

48 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

5.2 Conclusion After analyzing the different Ratios of the Northern Coalfields Limited I found that the Company is really in Good financial condition because the management has taken a great effort in managing the funds like acquiring and allocation of the funds, optimum utilization of the available resources.The analysis shows that the profitability of the company is increases as compared to the last years due to high production and sells with lesser expenses. The organization is in sound position which is good for the company, stakeholders as well as the Country also.Good financial position not just beneficial for the company stake holders but it helps to improves the GDP as well as the per capita income of the entire country.

As compared to the last year Current ratio is decreased due to increase in Inventories, Cash and Bank

balance and other Current Assets. If we talk about the Quick Ratio then In 2009 it was 0.07 which has

increased to 0.14 in 2010. The management has taken a great effort in maintaining high quick assets as

compared to last year. The company has sound position to meet its non-operating expenses and also

enough capable to pay taxes and royalty to the government. The net profit of the company has been

increased by 6.55% as compared to last year. Net profit of the project has been increased due to increase

in sales/ production, reduction in cost per tonnes, and better control on operating expenses. The net profit

of the project reveals sound business of the project and strong financial position.

It is currently in good financial condition and it is continuously trying to implement new tools and

techniques to improve its productivity as well as profitability.

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

49 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

REFERENCE SECTION

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

50 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

BIBLIOGRAPHY:

1. Published books:

Ajoy K Ghose, Mining, Challenges of the 21st century, 2000

International Energy Agency Coal in the energy supply of India,2002

C.R. Kothari, Research methodology-methods and techniques, New Age

International Publishers, New Delhi 1985, second edition.

Text book of coal (indian context) first edition (2000) by D. Chandra, R.M.

Singh & M.P. Singh

Anubhuti Ranjan Prasad, Coal nIndustry of India, 1986

Ashish Publishing House

2. Journals/Periodical::

KHANIJ URJA, Volume No. 48, September 2009 KHANIJ URJA, Volume No. 52, January 2010 NCL DIARY, Published by the organization every year

Online Published material on the world wide web:

URL : http://www.coalindia.nic.in June 05, 2010

URL : http://www.ncl.nic.in June 05, 2010

URL : http://www.wikipedia.nic.in June 07, 2010

URL : http://www.geologydata.info July 15, 2010

URL : http://books.google.co.in July 15, 2010

RATIO ANALYSIS OF NORTHERN COALFIELDS LIMITED

51 | P a g e S h r a w a n K u m a r D w i v e d i +91 8179130135 [email protected] [email protected]

Thanks a lot for going through my project. Feel free to Contact me anytime for further queries and any help regarding this project or any other topic related to the Finance. All the best for your bright future. And one thing always keep in mind that smart work always pays, so work smartly. Thanks & Regards, Shrawan Kumar Dwivedi +91 81791 30135 [email protected] [email protected] You can also catch me on Facebook at http://www.facebook.com/#!/shrawan.dwivedi

Related Documents