COMPANY COMPANY PROFILE PROFILE 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COMPANYCOMPANYPROFILEPROFILE

1

INTRODUCTION

Shivalik Agro Poly Products Limited (SAPL) was established in 1976 as a pioneering venture in India for the manufacture of polyethylene wide width film for use in agriculture, agricultural/industrial storage covers & irrigation - water management. The plant is capable of making polyethylene film/ sheets up to 12 meters wide width and in thickness range from 100 Micron to 2000 Micron. The company’s works is located at Parwanoo (H.P) 30 Kms from Chandigarh city on the Chandigarh – Shimla national highway on 2.5 acres of land with well organized infrastructure and manufacturing facilities. The company has a good standing in the polyethylene film market and is well known for its enterprising work in the use of plastics in agriculture and water management. The company has been members of ASSOCHAM and PHD chamber of commerce and Industries since long. The company has an annual installed capacity to process 5100 M.T. of polyethylene granules and 400 M.T. of polyurethane systems. The company diversified and entered into a manufacturing agreement, in the year 2004 with Reckitt Benckiser (India) Ltd. to operate and manage their activities setup at the works of the company at plot no. 1, sector 3, industrial Area, Parwanoo to manufacture Dettol antiseptic and skin care range of bathing soaps under this unit.

SAPL Accreditions

SAPL is an ISO 9001-2008 accredited Company SAPL hold BIS Manufacturing License for manufacture of LDEP Films SAPL got its financial rating done from CRISIL

2

HISTORY

SHIVATHENE LINOPACK (SLP) - A UNIT OF SHIVALIK AGRO POLY PRODUCTS- PU DIVISION

Shivathene Linopack (A Unit of Shivalik Agro Poly Products Ltd.) manufactures polyols and PU systems for polyurethane industries at its works, located at Parwanoo (H.P) and has an installed capacity of 600 M.T. per annum.

Polyurethanes are very versatile and their nature varies depending upon the additives contained in the polyol part of polyurethane system. Shivathene Linopack, is engaged in manufacturing of polyols /polyurethanes systems for Rigid Polyurethane Foam, Cold Cure Foam, Integral Skin Foam, Coating, Cable Jointing Compounds, Potting & Encapsulation Compounds for Electrical and Electronic components, Elastomers and Polymer Concrete.

This unit with an aim to diversify entered into a manufacturing agreement in the year 2003 with M/s Reckitt Benckiser (India) Ltd. to operate and manage their activities setup at the works of the company at Plot No. 1-A, Sector 3, Industrial Area, Parwanoo to manufacture household liquid cleaners such as Harpic, Colin, Teepol, and Lizol.

3

CONCEPTALISATION

Product application division ( PAD )

SAPL through its product application division undertakes application of the products manufactured by SAPL and, SLP through a well experienced proficient technically qualified team of engineers and dedicated work force who have hands down experience in the given areas of application.

MISSION AND VISSION

Our Mission To provide the best value proposition to our vendors and resellers/Consumers through innovation, and responsiveness and be the partner of choice for them. Consistent innovation and an unyielding commitment of providing impeccable quality standards are the core objective of our business.

Our VisionTo effectively contribute to the cause of water management & conservation, prevent sub soil water contamination and promote the use of high quality plastics for agricultural growth, to facilitate storage and protection of harvested crop in the field and provide effective high quality portable warehousing for temporary open storage of the crop. To promote the concept of Plasticulture. To make Shivathene Group the most innovative supplier of quality products, focused on highest value creation for its customers.

4

QUALITY POLICY

Excellence in Quality, across all aspects from Raw Material to Final Product , including Packing is our basis to manufacture.

We are committed to QUALITY, ON-TIME DELIVERY and COST-EFFECTIVENESS, and will:

Provide products and services which meet or exceed customer needs and expectations: o Manufacture products which meet customer specifications.o Strive to meet customer’s target values.o Monitor customer satisfaction.

Deliver on-time. o Ship on the date required by the customer. o Monitor on-time delivery performance.

5

MANAGEMENT

Board of Directors

1. Mr. Pankaj K. Mahajan, Chairman & Managing Director 2. Mrs. Alka Mahajan, Vice Chairperson 3. Dr. G.D. Tyagi, Executive Director (Technical & operations)4. Mr. Sanjay Gupta 5. Mr.Tushar Dasgupta 6. Mr. M. S. Raghav 7. Ms. Priyanka Mahajan 8. Mr. Hoshiar Singh 9. Mr. Naresh Arora 10.Nominee - Punjab State Civil Supplies Corp. Ltd. (PUNSUP)11.Mr. Vikas Pratap, IAS 12.Finance Controller & Company Secretary13.Mr. B.L.Jain 14.Chief General Manager15.Mr. Ashok Mittal 16.Advisor Corporate17.Mr. R.C.Gupta

PE COVERS FOR FUMIGATION OF FOODGRAINS

Polyethylene covers, for fumigation of bulk food grains are manufactured by the company since 1978. These covers are extensively used for fumigation of food grains stored in the open or in godowns.

6

CAP COVERS FOR FUMIGATION OF FOODGRAINS

PE covers are fabricated from heavy duty PE film processed from PE granules, are chemically inert.

PE covers are having high degree of retention of fumigants. PE covers are UV stabilized which increases the shelf life of covers. PE cover is having single seam at the side and the seam is thermally

welded to provide added strength. PE films remain unaffected in temperatures ranging from -2°C to + 50°C. PE covers are having excellent barrier characteristics to provide total

protection from rain, dust, dew and storms.

Standard Specification of PE Cover

PE cover standard size is : 32’x21’x17’ for stack of food grains having capacity of 3200 bags of 50 kgs. each.

PE cover thickness is 300 micron or 1200 gauges or 0.30 mm. PE cover weight is approximate is 60-62 kg. PE covers can also be fabricated as per customers specifications.

COST SAVINGSUnserviceable covers can be sold as scrap for partial recovery of original investment.

DURABILITY

Even after two years usage and folding, due to strong welding, the joints will not break and leaks or cracks will not appear at the folding of the Cover.

7

POLY TARPAULINS

Black Tarpaulins are manufactured out of PE Granules of size 30’x40’ having thickness of 300 micron+/-20% and having weight of around 30-34 kgs. These are meant for outside storage of food grains, particularly for paddy.

U.V.STABILIZED POLYETHYLENE FILM FOR GREEN HOUSES & TUNNELS

PE film used for green houses and tunnels is having two to three years life.

PE is available up to 12 meters width and thickness range from 100 microns to 250 microns.

Colour-transparent or translucent-The colour of green house film is considered based on the percentage of required sun light.

PE green house film is having excellent tensile strength and elongation.

CONVERSION TABLE (Thickness V/s Area)(Density-0.93 g/cc)

Approx. Area Coverage Per Kg. of PE Film

Thickness in

Microns MM Gauge Sq. Mtrs. Sq. Ft.100 0.10 400 10.75 115.67150 0.15 600 7.17 77.15200 0.20 800 5.38 57.89

8

PE SHRINK WRAP FILM

The concept of shrink wrapping consumer products is prevalent in most of the technologically advanced countries. The process achieved remarkable success as a technique for functional applications such as bundling, tray packing and pallet-load utilization. Today it is one of the most accepted packaging system for a wide range of consumer and industrial products.

Shrink wrap film is available in thickness ranging from 25 Microns to 250 microns in different width as per individual customer requirements. It is available in the form of lay flat tubing and also single ply wide width film.

Areas of application

Cosmetics & pharmaceuticals Paper products & stationery Items Soaps and detergents Food products Engineering goods

CO – EXTRUDED MULTILAYER (THREE LAYER) PE FILMS

The film meets growing demand in the flexible packaging segment of the market. The multilayer film finds extensive application in industries such as dairy, sugar, processed food, edible oils, poly laminates, detergents, etc.

Areas of application

Dairy: Packing of liquid / powder Milk Sugar: Packing of sugar Processed Food: Packing of foodstuff Edible Oils: Packing of Ghee Detergents: Packing of detergents in pouches/ bags

9

PE FILM FOR OTHER APPLICATIONS LIKE LINNING OF RESERVOIRS/TANKS/PONDS/CANELS ETC

Poly lining has made it easier to develop captive ponds for storage of water for irrigation, industry and domestic uses both in hills and plains.

POLY FILM & GEOMEMBRANE LINING APPLICATION

PE GEOMEMBRANE

PE thick sheets are referred to as geomembranes. PE sheets upto 7.0 meters width and thickness ranging from 0.50 mm - 2.0 mm are manufactured at SAPL; these sheets are normally available in accordion fold/bundle of length 30 meters or as per individual customer requirement. The prime application of these geomembrane is linning of water storage tanks/ ponds, large reservoirs, effluent tanks, fish farming ponds landfills, ash dike, etc.

POLYOLS AND P.U. SYSTEMS

Polyols and P.U. systems manufactured and marketed by Shivathene Linopack (A Unit of SAPL) find extensive application in the following areas.

Rigid foam: Hot and cold Insulation Integral skin: Automobile and furniture Coating/Paints: Water proofing for buildings and anticorrosive for

metallic and non metallic surfaces Polymer concrete: Industrial floorings Potting and encapsulation compound: Electronic and electrical

components Grouting: grouting of machines Sealants: Civil application for expansion and contraction joints

10

PRODUCTS

Thermo Plastic SHIVAPRIME* C5 CRYSTALEX* (TDS) SHIVAPRIME* C5 (TDS)

ABOUT US

Shivalik Prismo India Private Ltd. (SPIPL) was incorporated in the year 1999 and established to manufacture and promote the use of hot applied Thermoplastic Road Marking materials of the highest quality for the Indian subcontinent.

SPIPL has in the past couple of years established itself as India’s leading manufacturer and supplier of Thermoplastic Road Marking material with supplies being made to the large number of prestigious projects and customers. The company has supplied Thermoplastic Road Marking Material to over 90 NHAI Projects.

The company is a 50:50 joint venture between Prismo Ltd., U.K and Shivalik Agro Poly Products Ltd. (SAPL), India.

SPIPL brought the combined expertise of both these companies while offering the world class quality products in the thermoplastic road markings sector. SPIPL is committed to quality, safety, environment protection and value for money.

The Company aim to offer complete solutions to the consumer’s need in thermoplastic products and allied services with 100% customer satisfaction.

11

SPIPL Accredition

The Company is an ISO 9001-2008 accredited Company.

Copyright © 2011 Shivalik Prismo India Pvt. Ltd. All Rights Reserved. | Disclaimer

Designed and Developed By Pugmarks

MISSION AND VISSION

Our VisionTo promote the application of hot applied retro reflective thermoplastic road marking materials of the highest quality for the Indian subcontinent. To be a part of highway road safety campaign in providing well demarcated visible lanes and road signage. To offer complete solution to the need of thermoplastic road marking products and allied services.

Our Mission To provide all weather day night road visibility for sane lane driving and clear demarcation and linage on roads and highways to minimize accidents. Aim at complete consumer satisfaction, Highways & Road safety, and highest quality standards thru consistent innovation.

QUALITY POLICY

“SPIPL is committed to produce quality Road Marketing Materials and Road products that meet and satisfy customer requirements and expectations at minimum cost by efficient utilization of its technological, human and material resources. Our means to continually improve are by enhancing product quality, minimizing material wastage and providing a framework from establishing and reviewing quality object.

12

BOARD OF DIRECTORS (INDIA BASED)

1. Mr. Pankaj K. Mahajan 2. Dr. G.D. Tyagi

THERMO PLASTIC ROAD MARKINGS

YELLOW TPR MARKING

GRADE: MORTH & BSo Reflective thermoplastic marking material is recommended for

use with the thermoplastic screed application prams, motorised marking machines etc. These products of reflective screed are ideal for high output marking on highways.

o SPECIFICATION AS PER BS: 3262 with White Reflective (Crystallex) and Yellow Reflective (Crystallex)

o SPECIFICATION AS PER MORTH: 803.4 with White Reflective (Crystallex) and Yellow Reflective (Crystallex)

SHIVAPRIME* C5

INTRODUCTIONSHIVAPRIME C5 is a specially formulated, single component air dying road marking clear primer used on RCC or cemented Roads. The road marking material can be easily applied on the primed surface.

OTHER AREAS OF APPLICATIONSHIVAPRIME can be also find a wide range of application on concrete, asbestos, bricks, tiles, parapets, RCC, drainage pipes, FRP surface, stone slabs, Pyrex slab. The product has good adhesion properties for various surface like Bituminous & Concrete roads.

13

CRYSTALEX* - TECHNICAL DATA SHEET

INTRODUTIONCRYSTALLEX is a specially formulated, hot applied fast drying thermoplastic road marking materials. It has thickness control, skid resistance and long life than conventional road marking materials.

AREAS OF APPLICATIONCRYSTALEX can be applied on all type of surfaces likes Bitumen, RCC/Cemented roads with Shiva prime.

COLOURS AVAILABLE White and Yellow

PROPERTIES (AS PER MORTH SPECIFICATIONS)

Colour White YellowBinder contents (% min) 18 18Glass Beads (% min) 30 30Titanium (% min) 10 -Yellow Pigment - As requiredDrying time (minutes) 5-10 5-10Luminance at 45deg. Angle (% min) 65 45Skid resistance (% mim) 45 45Coverage (Kg. /me, at 2.5mm thickness) 5 5

RECOMMENDED COVERAGE:5 Kg per sq. meter for 2.5 mm thickness on smooth surface.

METHOD OF APPLICATION

PROCESS CONDITIONS

Road Temperature: Ambient Safe Healing Temperature: 160 – 200°C Optimum Heating Temperature: 180°C (+ /- 10°C)

14

OBJECTIVES OBJECTIVES OF OF

STUDYSTUDY

15

OBJECTIVES OF STUDY

Working capital is necessary to run day to day business activities. There is

hardly any company which does not require working capital. It is also

helpful in knowing the capabilities of company and company is running well

or not. The objective of the study is as follow:

To know the daily operations of the company.

To find out the liquidity ratio, activity ratio, profitability ratio

and long term solvency ratio.

To assess the cash management of shivalik agro poly product

private limited.

To know that how the company fulfill its monetary requirement

on the time of shortage.

How to utilize Working Capital in the company in order to

maximize the performance of the company?

To know how resources can be efficiently utilized.

16

SCOPESCOPEANDAND

RATIONALERATIONALEOF OF THETHE

STUDYSTUDY

17

SCOPE AND RATIONALE OF THE STUDY

Working capital is the difference between current assets and current

liabilities. In the present study the working capital management has been

analyzed using ratios.

The working capital management is studied in respect of:

Cash management

Receivables management

Inventory management

Liquidity ratio

Activity ratio

Profitability ratio

Solvency ratio

These ratios help to analyze how well the working capital is being

managed over the period.

18

INTRODUCTIONINTRODUCTIONOF THEOF THE

“WORKING CAPITAL“WORKING CAPITALMANAGEMENT”MANAGEMENT”

19

WORKING CAPITAL MANAGEMENT

Working Capital management is the management of assets that are current in

nature. Current assets, by accounting definition are the assets normally

converted into cash in a period of one year. Hence working capital

management can be considered as the management of cash, market securities

receivables, inventories and current liabilities.

CONCEPTS OF WORKING CAPITAL

There are two concepts of working capital:

Gross Working Capital

Net Working Capital

1. GROSS WORKING CAPITAL

Gross working capital refers to the firm’s investment in current asset.

Thus, it is the capital invested in total current assets of the enterprise.

These two aspects will help in remaining away from the two danger

points of excessive or inadequate investment in current assets.

2. NET WORKING CAPITAL

Net working capital is the excess of current assets over current

liabilities.Net working capital may be positive or negative. Positive

working capital refers to the situation where current assets exceed

current liabilities and negative working capital refers to the situation

current liabilities exceed current assets.

NET WORKING CAPITAL = CURRENT ASSETS–CURRENT

LIABILITIES

20

CONSTITUENTS OF CURRENT ASSETS

1. Cash in hand and bank balances

2. Bills Receivables

3. Sundry Debtors(less provision for bad debts)

4. Short-term loans and advances

5. Inventories of stocks, as:

a) Raw materials

b) Work-in-process

c) Stores and spares

d) Finished goods

6. Temporary Investments of surplus funds

7. Prepaid Expenses

8. Accrued Incomes

CONSTITUENTS OF CURRENT LIABILITIES

1. Bills Payable

2. Sundry Creditors or Accounts Payable

3. Accrued or Outstanding Expenses

4. Short-term loans, advances and deposits

5. Dividends Payable

6. Bank Overdraft

7. Provision for Taxation, if it does not amount to appropriation of

profits

KINDS OF WORKING CAPITAL

21

Permanent or Fixed Working Capital

Temporary or Variable Working Capital

1. PERMANENT OR FIXED WORKING CAPITAL

Permanent or Fixed Working Capital is the minimum level of

current assets. It is permanent in the same way as the firm’s fixed

assets are. It can be further classified as:

o Regular working capital to ensure circulation of current

assets from cash to inventories, from inventories to

receivables and from receivables to cash and so on.

o Reserve working capital is the excess amount over the

requirement for regular working capital which may be

provided for contingencies that may arise at unstated periods

such as strikes, rise in prices etc.

2. TEMPORARY OR VARIABLE WORKING CAPITAL

Temporary or Variable Working Capital is the amount of working

capital which is required to meet the seasonal demands and some

special exigencies. It can be further classified as:

o Seasonal working capital is the capital required to meet

the seasonal needs of the enterprise.

o Special working capital is that part of working capital

which is required to meet special exigencies such as

launching of extensive marketing campaigns for conducting

research etc.

22

IMPORTANCE OF ADEQUATE WORKING CAPITAL

Management of working capital is very much important for the success of

the business. It has been emphasized that a business should maintain a

sound working capital position and also that there should not be an excessive

level of investment in the working capital components. The main advantages

of maintaining adequate amount of working capital are as follows:-

SOLVENCY OF THE BUSINESS

Adequate working capital helps in maintaining solvency of the

business by providing uninterrupted flow of production.

GOODWILL

Sufficient working capital enables a business concern to make prompt

payments and hence helps in creating and maintaining goodwill.

REGULAR SUPPLY OF RAW MATERIALS

Sufficient working capital ensures regular supply of raw materials and

continuous production.

REGULAR PAYMENT OF SALARIES,WAGES AND OTHER

DAY-TO-DAY COMMITMENTS

A company which has ample working capital can make regular

payment of salaries, wages and other day-to-day commitments which

raises the morale of its employees, increases their efficiency, reduces

wastages and costs and enhances production and profits.

23

EXCESS OR INADEQUATE WORKING CAPITAL

The firm should maintain a sound working capital position. It should

have adequate working capital to run its business operations. Both

excessive as well as inadequate working capital positions are

dangerous from firm’s point of view.

DISADVANTAGES OF EXCESSIVE WORKING CAPITAL

Excessive working capital means idle funds which earn no profits for

the business and hence the business cannot earn a proper rate of

return on its investment.

It may result into overall inefficiency in the organization.

DISADVANTAGES OF INADEQUATE WORKING CAPITAL

It cannot buy its requirements in bulk and cannot avail discounts.

The firm cannot pay day-to-day expenses of its operations and it

creates inefficiencies, increases costs and reduces the profits of the

business.

It becomes impossible to utilize efficiently the fixed assets due to non-

availability of liquid funds.

DETERMINANTS OF WORKING CAPITAL

24

There is no specific method to determine working capital requirement for a

business. There are a number of factors affecting the working capital

requirement. The following is the description of factors which generally

influence the working capital requirements of firms:

Nature of business

This is an important factor in determining the working capital

requirements. There are some businesses which require a very

nominal amount to be invested in fixed assets but a large chunk of the

total investment is in the form of working capital.

Size of business

The working capital requirements of a concern are directly influenced

by the size of its business which may be measured in terms of scale of

operations.

Manufacturing Process

Manufacturing cycle comprises of the purchase and use of raw

material and the production of finished goods. Longer the

manufacturing cycle, larger will be firm’s working capital

requirements.

Credit Policy

The credit policy of a firm affects the working capital by influencing

the level of debtors. A concern that purchases its requirements on

credit and sells its products or services on cash requires lesser amount

of working capital.

25

Availability of Credit

The terms on which a company is able to manage its credit also

affects the working capital requirement. If a company in a position to

get credit on liberal terms and in a short span of time then it will be in

a position to work with less amount of working capital.

Seasonal Variations

In certain industries raw material is not available throughout the year.

They have to buy raw materials in bulk during the season to ensure an

interrupted flow and process them during the entire year.

Price level changes

Changes in the price level affect the working capital requirements.

Generally, the rising prices will require the firm to maintain higher

amount of working capital. Same levels of current assets will need

increased investment when prices are increasing.

Operating Efficiency

The operating efficiency of the firm relates to the optimum utilization

of all its resources at minimum costs. The efficiency in controlling

operating costs and utilizing fixed and current assets leads to

operating efficiency.

TYPES OF WORKING CAPITAL

The working capital is of following types:-

26

CASH MANAGEMENT

RECEIVABLES MANAGEMENT

INVENTORY MANAGEMENT

CASH MANAGEMENT

Cash is the important current asset for the operations of the business. Cash is

the basic input needed to keep the business running on a continuous basis; it

is also the ultimate output expected to be realized by selling the service or

product manufactured by the firm. Thus, a major function of the financial

manager is to maintain a sound cash position.

Cash Planning

Cash inflows and cash outflows should be planned to project cash

surplus or deficit for each period of the planning period. Cash budget

should prepare for this purpose.

Managing the cash flows

The flow of cash should be properly managed. The cash inflows

should be accelerated while, as far as possible, the cash outflows

should be decelerated.

Investing surplus cash

The surplus cash balances should be properly invested to earn profits.

The firm should decide about the division of such cash balance

between bank deposits, marketable securities and inter corporate

lending.

MOTIVES FOR HOLDING CASH

27

There are four primary motives for maintaining cash balances:

Transaction motive

Speculative motive

Compensating motive

Transaction motive

The transaction motive requires a firm to hold cash to conduct its

business in the ordinary course. The need to hold cash would not arise

if there were perfect synchronization between cash receipts and cash

payments, i.e. enough cash is received when the payment has to be

made.

Speculative motive

The speculative motive relates to holding of cash for investing in

profitable opportunities as and when they arise. Such opportunities do

not come in a regular manner. Such opportunities can be availed of if

a firm has cash balance with it.

Compensation motive

Another motive to hold cash balances is to compensate banks for

providing certain services and loans. Banks provide a variety of

services to business firms, such as clearances of cheques, supply of

credit information, transfer of funds, etc. To be compensated for their

services indirectly in this form, they require the clients to always keep

a bank balance sufficient to earn a return equal to the cost of services.

28

MANAGING CASH FLOWS

The following methods of cash management will help in better cash

management:-

Prompt payment by customers

In order to accelerate cash inflows, the collections from customers

should be prompt. This will be possible by prompt billing. The

customers should be promptly informed about the amount payable and

the time by which it should be paid.

Quick conversion of payment into cash

Cash inflows can be accelerated by improving the cash collecting

process. Once the customer writes a cheque in favor of the concern

the collection can be quickened by its collection. There is a time gap

between the cheque sent by the customer and the amount collected

against it.

Decentralized collections

A big firm operating over wide geographical area can accelerate

collections by using the system of decentralized collections. A number

of collecting centers are opened in different areas instead of collecting

receipts at one place. This system saves mailing and processing time

and thus, reduces the financial requirements.

MANAGEMENT OF RECEIVABLES

29

Receivables represent amounts owed to the firm as a result of sale of goods

or services in the ordinary course of business. Receivables are also termed

as trade receivables, accounts receivables, customer receivables, book debts;

trade acceptance, debtors and bills receivables. The purpose of maintaining

or investing in receivables is to meet competition and to increase the sales

and profits.

COSTS OF MAINTAINING RECEIVABLES

The concern incurs the following costs on maintaining receivables:

Cost of Financing Receivables

When goods and services are provided on credit then concern’s capital

is allowed to be used by the customers. The receivables are financed

from the funds supplied by shareholders for long term financing and

through retained earnings. The concern incurs some cost for collecting

funds which finance receivables.

Cost of Collection

A proper collection of receivables is essential for receivables

management. The customers who do not pay the money during a

stipulated credit period are sent reminders for early paymentsAll these

costs are known as collection costs which a concern is generally

required to incur.

Bad Debts

Some customers may fail to pay the amounts due towards them. The

amounts which the customers fail to pay are known as bad debts.

Though a concern may be able to reduce bad debts through efficient

collection machinery but one cannot altogether rule out this cost.

30

FACTORS INFLUENCING THE SIZE OF RECEIVABLES

Size of Credit Sales

The volume of credit sales increases or decreases the size of

receivables. If a concern sells only on cash basis, then there will be no

receivables. The higher the part of credit sales out of total sales, then

receivables will be more and vice versa.

Credit Policies

A firm with conservative credit policy will have a low size of

receivables while a firm with liberal credit policy will have a high size

of receivables.

Relation with Profits

The credit policy is followed with a view to increase sales. When

sales increase beyond a certain level the additional costs incurred are

less than the increase in revenues. The increase in profits will be

followed by an increase in the size of receivables or vice versa.

Credit Collection Efforts

The customers should be sent periodical reminders if they fail to pay

in time. On the other hand, if adequate attention is not paid towards

credit collection then the concern can land itself in a serious financial

problem. Efficient credit collection machinery will reduce the size of

receivables.

31

MANAGEMENT OF INVENTORY

Inventories constitute the most significant part of current assets of a large

majority of companies in India. On an average, inventories are

approximately 60 per cent of current assets in public limited companies in

India. A firm neglecting the management of inventories will be jeopardizing

its long run profitability and may fail ultimately. It is possible for a company

to reduce its levels of inventories to a considerable degree. The reduction in

“excessive” inventories carries a favorable impact on a company’s

profitability.

NATURE OF INVENTORY

Inventories are stock of the product a company is manufacturing for sale and

components that make up the product. The various forms in which

inventories exist in a manufacturing company are:

Raw Material

Raw Materials are those basic inputs that are converts into finished

product through the manufacturing process. Raw Materials inventories

are those units, which have been purchased and stored for future

productions.

Work in progress

Work in progress inventories are semi-manufactured products. They

represent products that need more work before they become finished

products for sale.

32

Finished goods

These are completely manufactured products which are ready for sale.

Stocks of raw materials and work in progress facilitate production

while stock of finished goods is required for smooth marketing

operations.

Consumables

These are the materials which are needed to smooth the process of

production. These materials do not directly enter production but they

act as catalysts. These may be classified according to their

consumption and critically.

PURPOSE OF HOLDING INVENTORY

A firm also needs to maintain inventories to reduce ordering costs and avail

quantity discounts. There are three main purposes or motives of holding

inventories:

Transactions motive

It emphasizes the need to maintain inventories to facilitate smooth

production and sales operations.

Precautionary motive

It necessitates holding of inventories to guard against the risk of

unpredictable changes in demand and supply force and other factors.

Speculative motive

33

It influences the decision to increase or reduce inventory levels to take

advantage of price fluctuations.

OBJECTIVES OF INVENTORY MANAGEMENT

The main objectives of inventory management are operational and financial.

The operational objectives mean that the materials and spares should be

available in sufficient quantity so that work is not disrupted for want of

inventory. The financial objective means that investments in inventories

should not remain idle and minimum working capital should be locked in it.

The following are the objectives of inventory management:

To ensure continuous supply of raw materials, spares and finished

goods so that production should not suffer at any time and the

customers demand should also be met.

To minimize losses through deterioration, pilferage, wastages and

damages.

To keep material cost under control so that they contribute in reducing

cost of production and overall costs.

INVENTORY MANAGEMENT TECHNIQUES

34

Effective inventory management requires an effective control system for the

inventories. In managing inventories, the firm’s objective should be in

consonance with the shareholder wealth maximization principle. To achieve

this, the firm should determine the optimum level inventory. This increases

the level of investment and makes the firm unprofitable.

To manage inventories efficiency, answers should be sought to the following

two questions:

How much should be ordered?

When should it be ordered?

The first question, how much to order, relates to the problem of determining

economic order quantity (EOQ) and is answered with an analysis of costs of

maintaining certain level of inventories.

The second question, when to order, arises because of uncertainty and is a

problem of determining the re-order point.

ECONOMIC ORDER QUANTITY

One of the major inventory management problems to be resolved is

how much inventory should be added when inventory is replenished.

If the firm is buying raw materials, it has to decide lots in which it has

to be purchased on each replenish.

Determining an optimum inventory level involves two types of costs:

o Ordering costs

o Carrying costs

ORDERING COST

35

These are the costs which are associated with the purchasing or

ordering of materials. They include costs incurred in the following

activities: purchase ordering, transporting, receiving, inspecting and

storing.

CARRYING COST

Costs incurred for maintaining a given level of inventory are called

carrying costs. They include storage, insurance, taxes, deterioration

and obsolescence. This behavior is contrary to that of ordering costs

which decline with increase in inventory size

It is that order size at which annual total costs of ordering and holding

are the minimum.

EOQ = 2AS

I

Where, A = ANNUAL CONSUMPTION IN RUPEES

S = COST OF PLACING AN ORDER

I = INVENTORY CARRYING COSTS OF ONE UNIT

RE-ORDER POINT

The problem, how much to order, is solved by determining the

economic order quantity, yet the answer should be sought to the

second problem, when to order. To determine the re-order point under

certainty, we should know:

(a) Lead time

(b) Average usage

(c) Economic order quantity

36

That is:

Re-order point= Lead Time* Average usage

SAFETY STOCK

It is difficult to predict usage and lead time accurately. The demand

for material may fluctuate from day to day or from week to week.

Similarly, the actual delivery time may be different from the normal

lead time. If the actual usage increases or the delivery of inventory is

delayed, the firm can face a problem of stock-out which can prove to

be costly for the firm.

ABC ANALYSIS

Large numbers of firm have to maintain several types of inventories.

It is not desirable to keep the same degree of control on all of the

items. This analytical approach is called ABC analysis and tends to

measure the significance of each item of inventories in terms of its

value.

Combine items on the basis of their relative value to form three

categories A, B and C.

The data in the following table illustrate the ABC analysis.

CLASS NO. OF

ITEMS (%)

VALUE OF

ITEMS (%)

A 10 70

B 20 20

C 70 10

37

RESEARCHRESEARCH METHODOLOGYMETHODOLOGY

38

RESEARCH METHODOLGY

RESEARCH

Research comprises defining and redefining problems, formulating

hypothesis or suggested solutions, collecting, organizing and evaluating

data, making deductions and reaching conclusions and at last carefully

testing the conclusions to determine whether they fit the formulating

hypothesis.

RESEARCH METHODOLOGY

Research methodology is a way to systematically solve the problems. It is a

way of studying how research is done scientifically. It consists of various

steps that are generally adopted by the researcher in studying his research

problems along with the logic behind them.

RESEARCH DESIGN

Research design is a framework or the blue print for conducting the research

project. Research design is the arrangement of conditions for collection and

analysis of data in a manner that aims to combine relevance to the research

purpose with economy in procedure. It includes an outline of what the

researcher will do from writing the hypothesis and its operational

implications to the final analysis of data.

TYPES OF RESEARCH DESIGN

39

Exploratory research design

Descriptive research design

Experimental research design

EXPLORATORY RESEARCH DESIGN

It is also termed as formulate research design. The main purpose of the study

is to formulate a problem for more precise investigation.

DESCRIPTIVE RESEARCH DESIGN

In descriptive research design, those studies are taken which are concerned

with describing the characteristics of a particular individual or a group.

EXPERIMENTAL RESEARCH DESIGN

In this casual relationships between the variables are tested. It is also known

as hypothesis testing research design.

SAMPLE DESIGN

Sample design is a technique or the procedure which the researcher would

adopt in selecting items for the sample. So, he selects small portion of the

universe, which is its true representative. This group known is sample and

this process is called Sampling.

Sample designs are basically of two types:

40

Non – Probability Sampling

Probability Sampling

NON- PROBABILITY SAMPLING

In this items for the sample are selected deliberately by the researcher, by

using his own judgment. In this every item of universe does not have equal

chances of inclusion in the sample.

It can be of following type:

Convenience Sampling

Judgment Sampling

Quota Sampling

PROBABILITY SAMPLING

It is also known as Random Sampling or Chance Sampling. In this, each

population element has equal chance of selection.

It can be of following type:

Random Sampling

Stratified Sampling

Cluster Sampling

Multi stage Sampling

41

METHODS OF DATA COLLECTION

It is of two types:-

Primary Data

Secondary Data

PRIMARY DATA

Primary data are those data, which is originally collected. It is of following

type’s questionnaire, interview, observation etc.

SECONDARY DATA

Secondary data are those data which are collected and which has been

passed through statistical research.

In this project, secondary data has been collected from following sources:-

Annual Reports

Books

Internet

Other material and report published by company

42

STUDYSTUDYOFOF

“RATIO ANALYSIS”“RATIO ANALYSIS”

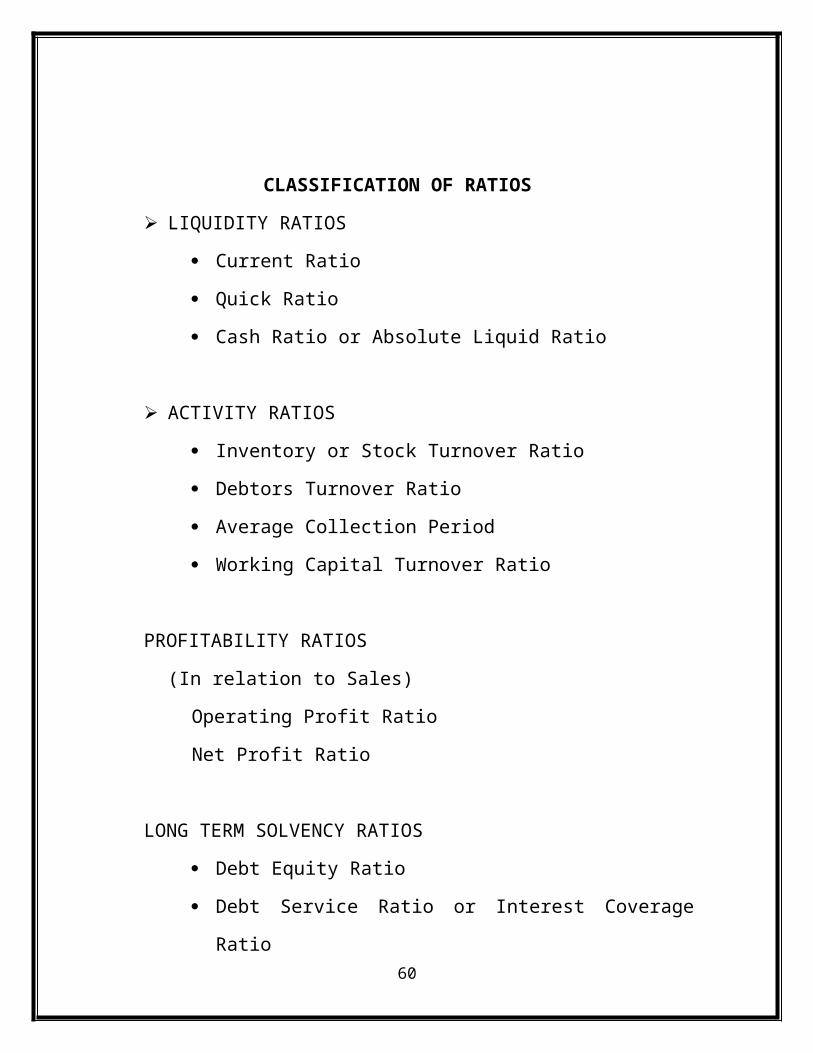

CLASSIFICATION OF RATIOS

LIQUIDITY RATIOS

43

Current Ratio

Quick Ratio

Cash Ratio or Absolute Liquid Ratio

ACTIVITY RATIOS

Inventory or Stock Turnover Ratio

Debtors Turnover Ratio

Average Collection Period

Working Capital Turnover Ratio

PROFITABILITY RATIOS

(In relation to Sales)

Operating Profit Ratio

Net Profit Ratio

LONG TERM SOLVENCY RATIOS

Debt Equity Ratio

Debt Service Ratio or Interest Coverage Ratio

LIQUIDITY RATIOS

Liquidity refers to the ability to meet its current obligation as and

when these become due. The short term obligations are met by

releasing amounts from current, floating or circulating assets.

CURRENT RATIO

Current ratio may be defined as the relationship between current

assets and current liabilities. This ratio, also known as working capital

44

ratio, is a measure of general liquidity and is most widely used to

make the analysis of a short-term financial position or liquidity firm.

IDEAL RATIO = 2:1

CURRENT RATIO = CURRENT ASSESTS / CURRENT

LIABILITIES

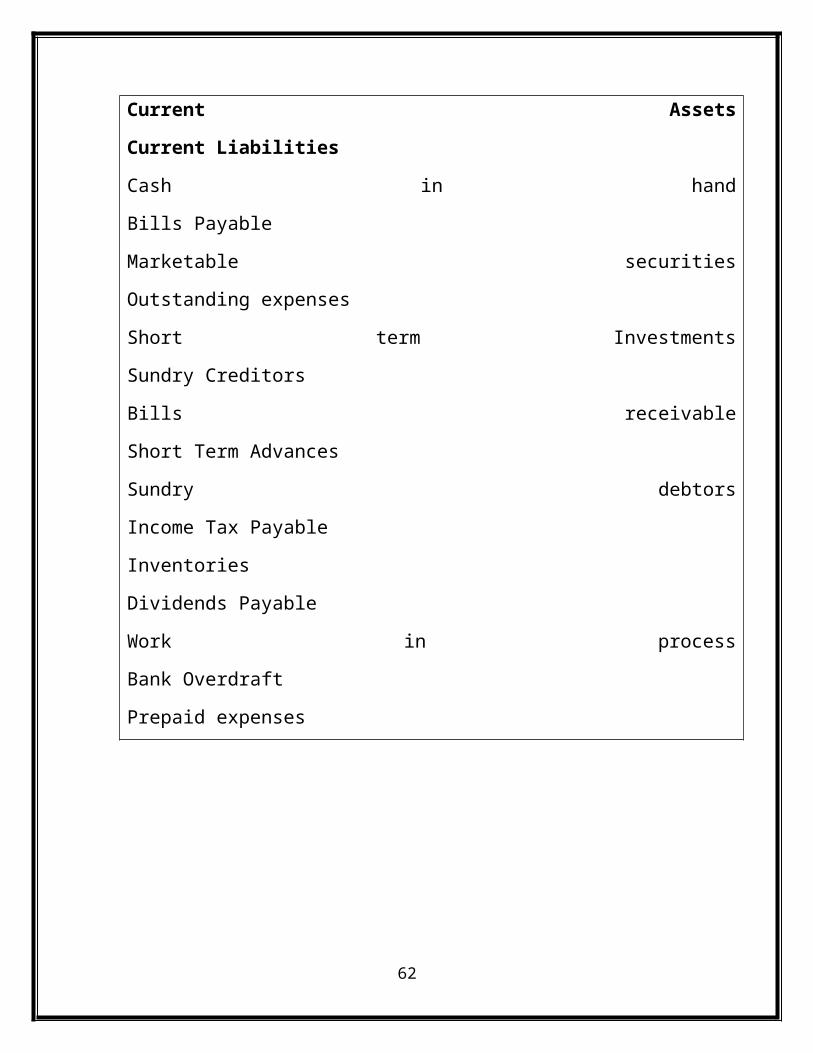

COMPONENTS OF CURRENT RATIO

Current Assets Current Liabilities

Cash in hand Bills Payable

Marketable securities Outstanding expenses

Short term Investments Sundry Creditors

Bills receivable Short Term Advances

Sundry debtors Income Tax Payable

Inventories Dividends Payable

Work in process Bank Overdraft

Prepaid expenses

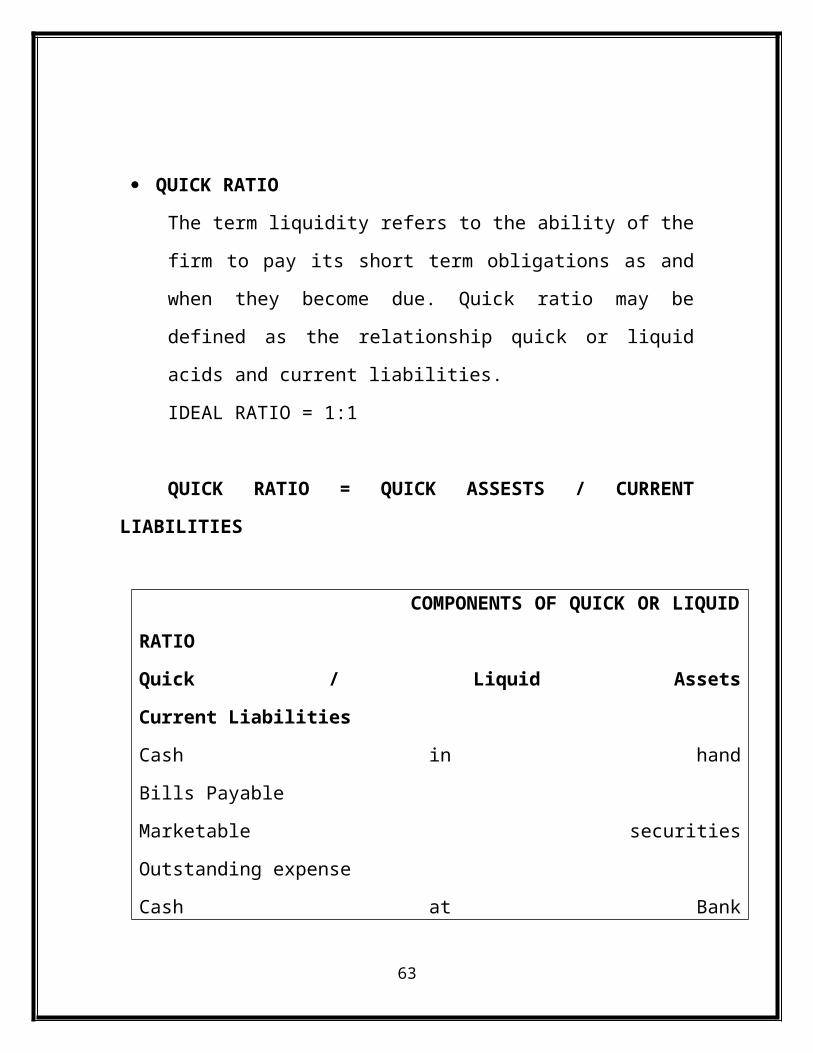

QUICK RATIO

45

The term liquidity refers to the ability of the firm to pay its short term

obligations as and when they become due. Quick ratio may be defined

as the relationship quick or liquid acids and current liabilities.

IDEAL RATIO = 1:1

QUICK RATIO = QUICK ASSESTS / CURRENT LIABILITIES

COMPONENTS OF QUICK OR LIQUID RATIO

Quick / Liquid Assets Current Liabilities

Cash in hand Bills Payable

Marketable securities Outstanding expense

Cash at Bank Sundry Creditors

Bills Receivables Short Term Advances

Sundry Debtors Income Tax Payable

Temporary Investments Dividends Payable

Bank Overdraft

ABSOLUTE LIQUID RATIO OR CASH RATIO

Absolute liquid assets include cash in hand and cash at bank and

marketable securities or temporary investments. The acceptable norm

for this ratio is 50% or 0.5: 1 or 1:2.

CASH RATIO = CASH AND BANK / CURRENT LIABILITIES

ACTIVITY RATIO

46

Activity ratios measure the efficiency or effectiveness with which a

firm manages it resources or assets. Theses ratios are also called

turnover ratios because they indicate the speed with which assets are

converted into sales.

For example: inventory turnover ratio indicates the rate at which the

funds invested in inventories are converted into sale. Depending upon

the purpose, a number of turnover ratios are calculated.

INVENTORY TURNOVER RATIO OR STOCK TURNOVER

RATIO

Inventory turnover ratio indicates whether inventory has been

efficiently used or not. Turnover ratio indicates the number of times

the stock has been turned over during the period and evaluates the

efficiency with which a firm is able to manage its inventory.

INVENTORY TURNOVER RATIO = NET SALES / INVENTORY

DEBTORS TURNOVER RATIO

Debtors turnover ratio indicates the velocity of debt collection of firm.

In simple words, it indicates the number of times average debtors

(receivables) are turned over during a year.

DEBTORS TURNOVER RATIO = TOTAL SALES / DEBTORS

47

AVERAGE COLLECTION PERIOD

The average collection period represents the average number of days

for which a firm has to wait before its receivables are converted into

cash.

AVERAGE COLLECTION PERIOD = NUMBER OF WORKING

DAYS/ DEBTORS TURNOVER RATIO

WORKING CAPITAL TURNOVER RATIO

Working capital of a concern is directly related to sales. The current

assets like debtors, bills receivables, cash, stock etc. change with the

increase or decrease in sales.

Working capital = Current Assets – Current Liabilities

It indicates the velocity of the utilization of net working capital. This

ratio indicates the number of times the working capital is turned over in

the course of a year. This ratio measures the efficiency with which the

working capital is being used by a firm.

WORKING CAPITAL TURNOVER RATIO = SALES/NET

WORKING CAPITAL

48

PROFITABILITY RATIO

Profits to the management are the test of the efficiency and a

measurement of a control; to owners, a measure of worth of their

investment; to the creditors, the margin of safety; to employees, and a

source of fringe benefits; to government a measure of tax paying

capacity and the basis of the legislative action etc.

OPERATING PROFIT RATIO

This ratio is calculated by dividing operating profit by sales.

OPERATING PROFIT RATIO = OPERATING PROFIT X 100

SALES

Operating profit = Net profit + Non operating expenses- Non operating

income

NET PROFIT RATIO

It establishes the relationship between net profits (after interest) and

sales, sand indicates the efficiency of the management in

manufacturing, selling, administrative and other activities of the firm.

This ratio is the overall measure of firm’s profitability.

NET PROFIT RATIO = NET PROFIT AFTER TEX X 100

NET SALES

LONG TERM SOLVENCY RATIOS

49

The term solvency refers to the ability of a concern to meet its long

term obligations. It indicates a firm’s ability to meet the fixed interest

and costs and repayment schedules associated with its long-term

borrowings.

DEBT EQUITY RATIO

Debt equity ratio also known as External – Internal Equity Ratio is

calculated to measure the relative claims of outsiders and the owners

(i.e. shareholders) against the firm’s assets.

DEBT EQUITY RATIO = OUTSIDER’S FUND/SHAREHOLDER’S FUND

INTEREST COVERAGE RATIO

Net income to debt service ratio or simply debt service ratio is used to

test the debt servicing capacity of a firm. The ratio is also known as

Interest Coverage Ratio or Fixed Charges Cover ratio or Time Interest

Earned.

INTEREST COVERAGE RATIO = NET PROFIT BEFORE INTEREST AND TEXES

FIXED INTEREST CHARGES FIXED INTEREST CHARGES

50

DATA ANALYSISDATA ANALYSISANDAND

INTERPRETATIONSINTERPRETATIONS

LIQUIDITY RATIOS

CURRENT RATIO = CURRENT ASSETS/CURRENT LIABILTIES

51

YEAR 2008-2009 2009-2010 2010-2011

Current Assets 5,06,58,00,000 6,15,47,80,000 6,25,89,40,000

Current

Liabilities

2,54,56,80,000 2,99,40,1,0,000 3,29,79,60,000

Current Ratio 1.99 2.06 1.89

2008-2009 2009-2010 2010-20110

0.5

1

1.5

2

2.5

Current Ratio

INTERPRETATION

IDEAL CURRENT RATIO IS 2:1.

The current ratio has increased from 1.99 to 2.06 between the year

2008-2009 and 2009-2010. But it decreased to 1.89 in the year 2010-

2011.

QUICK RATIO = QUICK ASSETS/CURRENT LIABILITIES

YEAR 2008-2009 2009-2010 2010-2011

52

Quick Assets 3,09,59,87,000 2,82,41,89,000 3,08,46,70,000

Current

Liabilities

2,54,56,80,000 2,99,40,10,000 3,29,79,60,000

Quick Ratio 1.22 0.94 0.93

2008-2009 2009-2010 2010-20110

0.2

0.4

0.6

0.8

1

1.2

1.4

Quick Ratio

INTERPRETATION

THE IDEAL QUICK RATIO IS 1:1.

The quick ratio has decreased from 1.22 to 0.94 between the year

2008-2009 and 2009-2010. But it decreased to 0.93 in the year 2010-

2011.

CASH RATIO = CASH AND BANK/CURRENT LIABILITIES

YEAR 2008-2009 2009-2010 2010-2011

53

Cash 59,08,80,000 82,19,10,00 83,93,87,000

Current

Liabilities

2,54,56,80,000 2,99,40,10,000 3,29,79,60,000

Cash Ratio 0.23 0.27 0.25

2008-2009 2009-2010 2010-20110

0.05

0.1

0.15

0.2

0.25

0.3

Cash Ratio

INTERPRETATION

The cash ratio has first increased from 0.23 to 0.27 between the

year b2008-2009 and 2009-2010. But it decreased to 0.25 in the

year 2010-2011.

ACTIVITY RATIOS

INVENTORY TURNOVER RATIO = NET SALES /

INVENTORY

54

YEAR 2008-2009 2009-2010 2010-2011

Net Sales 9,45,96,94,000 9,61,89,60,000 9,91,85,70,000

Inventory 2,09,63,80,000 3,37,73,80,000 3,60,11,80,000

Inventory

Turnover Ratio

4.51 2.85 2.75

2008-2009 2009-2010 2010-20110

0.51

1.52

2.53

3.54

4.55

Inventory Turnover Ratio

INTERPRETATION

The inventory turnover ratio has decreased from 4.51 to 2.85

between the year 2008-2009 and 2009-2010. But it decreased to

2.75 in the year 2010-2011.

DEBTORS TURNOVER RATIO = SALES/DEBTORS

YEAR2008-2009

2009-2010 2010-2011

55

Sales 9,45,96,94,000 9,61,89,60,000 9,91,85,70,000

Debtors 2,47,65,40,000 3,01,23,65,000 3,00,12,96,000

Debtors

Turnover Ratio

3.82 3.19 3.30

2008-2009 2009-2010 2010-20110

0.51

1.52

2.53

3.54

Debtors Turnover Ratio

INTERPRETATION

The debtor turnover ratio has decreased from 3.82 to 3.19 between

the year 2008-2009 and 2009-2010. But it increased to 3.30 in the

year 2010-2011.

WORKING CAPITAL TURNOVER RATIO = SALES /

NET WORKING CAPITAL

YEAR 2008-2009 2009-2010 2010-2011

Sales 9,45,96,94,000 9,61,89,60,000 9,91,85,70,000

Net Working 3,29,87,60,000 2,87,69,83,000 3,13,29,76,000

56

Capital

Working Capital

Turnover Ratio

2.87 3.34 3.17

2008-2009 2009-2010 2010-2011

0

0.5

1

1.5

2

2.5

3

3.5

Working Capital Turnover Ratio

INTERPRETATION

The working capital turnover ratio has increased from 2.87 to

3.34 between the year 2008-2009 and 2009-2010. But it

decreased to 3.17 in the year 2010-2011.

NET PROFIT RATIO = NET PROFIT AFTER TAX X 100

NET SALES

YEAR 2008-2009 2009-2010 2010-2011

57

Net Profit After

Tax

87,56,45,000 98,45,91,000 1,06,55,30,000

Net Sales 9,45,96,94,000 9,61,89,60,000 9,91,85,70,000

Net Profit Ratio 9.26 10.24 10.74

2008-2009 2009-2010 2010-20110

2

4

6

8

10

12

Net Profit Ratio

INTERPRETATION

The net profit ratio has increased from 9.26 to 10.24 in the year

2008-2009 and 2009-2010.Then it increased to 10.74 in the year

2010-2011.

LONG TERM SOLVENCY RATIOS

DEBT EQUITY RATIO = OUTSIDER’S

FUNDS/SHAREHOLDER’S FUNDS

58

YEAR 2008-2009 2009-2010 2010-2011

Outsider’s funds 1,15,87,75,000 1,95,34,21,000 2,35,39,40,000

Shareholder’s

funds

6,95,30,18,00

0

7,65,32,09,

000

9,58,27,60,0

00

Debt Equity Ratio 0.17 0.26 0.25

2008-2009 2009-2010 2010-20110

0.05

0.1

0.15

0.2

0.25

0.3

Debt Equity Ratio

INTERPRETATION

The debt equity ratio has increased from 0.17 to 0.26 in the year

2008-2009 and 2009-2010. But it decreased to 0.25 in the year

2010-2011.

59

CONCLUSION CONCLUSION

CONCLUSION

After studying the various ratios it is concluded that. The current ratio has

decreased over the period. This means the company will not be able to meet

60

its current liabilities. However, the cash position of the company is quiet

favorable as it has not decreased to much extent.

The inventory management system is not efficient as the amount of

inventory is not properly utilized to generate sales. The debtor management

system has been declining in the efficiency as revealed, by the decreasing

debtor turnover ratio and average collection period.

There is a high dependence on external debt which brings in inflexibility in

company’s operation. But still the company is in a stronger position because

profits have increased with sales.

61

LIMITATIONSLIMITATIONSOF THEOF THESTUDYSTUDY

LIMITATIONS

Although every effort has been made to collect the relevant information

through the sources available, still some relevant information could not be

gathered.

62

The time duration could not provide ample opportunity to study every

detail of management in the company.

There are restrictions not to visit some specific areas.

The concerned executives were having very busy schedule.

As some figures have not been disclosed by the company on account

of confidential report.

Estimates are based upon predictions.

63

SUGGESTIONSSUGGESTIONSANDAND

RECOMMENDATIONSRECOMMENDATIONS

SUGGESTIONS AND RECOMMENDATIONS

1. It is necessary to prepare the cash budget and try to achieve the actual

target and budgeted figures.

64

2. Companies should control, review and improve their discount policy

so as to improve company’s image.

3. More attention should be paid to customer’s complaints and efforts

should be made to remove them.

4. Some special planning on appointment of dealers should be there to

avoid the complications.

5. Funds should be available in smooth and steady flow so that

construction at the site is not affected and proper balance is

maintained if more than one site is going on in the same time.

6. Terms and conditions with the suppliers should be decided in advance

in order to get rid of the future problems.

7. Stock should be verified more frequently to avoid differences between

book figures and actual figures.

8. Every department should be made cost conscious to increase

profitability.

65

BIBLIOGRAPHYBIBLIOGRAPHY

BIBLIOGRAPHY

Books Pandey, I.M., “Financial Management”, Ed. 2007, Vikas Publishing

House Private Ltd., New Delhi.

66

Gupta, Shashi K., “Management Accounting”, Ed. 2007, Kalyani Publishers, New Delhi.

Kothari, C.R., “Research Methodology”, Ed. 2007, New Age International (P) Limited, Publishers, New Delhi.

Manual Annual reports

Websiteswww.shivathin .com.in

67

Related Documents