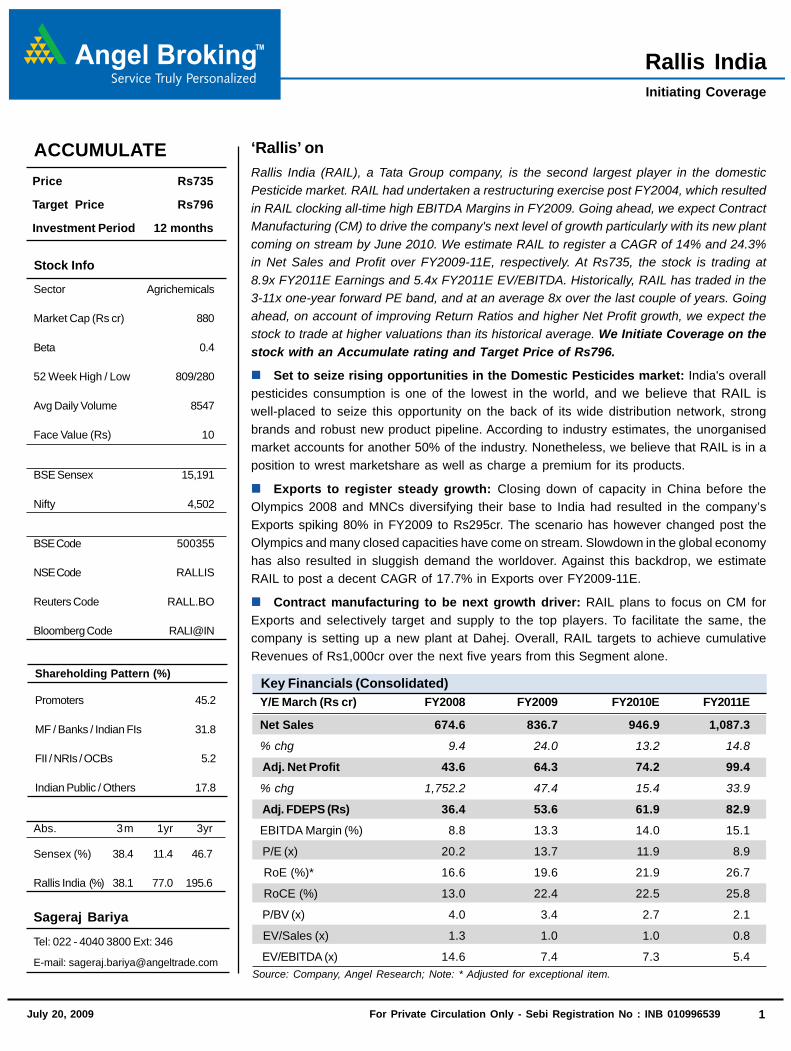

1 January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539 July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 1 Rallis India Initiating Coverage Sageraj Bariya Tel: 022 - 4040 3800 Ext: 346 E-mail: [email protected] Source: Company, Angel Research; Note: * Adjusted for exceptional item. Key Financials (Consolidated) Y/E March (Rs cr) FY2008 FY2009 FY2010E FY2011E Net Sales 674.6 836.7 946.9 1,087.3 % chg 9.4 24.0 13.2 14.8 Adj. Net Profit 43.6 64.3 74.2 99.4 % chg 1,752.2 47.4 15.4 33.9 Adj. FDEPS (Rs) 36.4 53.6 61.9 82.9 EBITDA Margin (%) 8.8 13.3 14.0 15.1 P/E (x) 20.2 13.7 11.9 8.9 RoE (%)* 16.6 19.6 21.9 26.7 RoCE (%) 13.0 22.4 22.5 25.8 P/BV (x) 4.0 3.4 2.7 2.1 EV/Sales (x) 1.3 1.0 1.0 0.8 EV/EBITDA (x) 14.6 7.4 7.3 5.4 Stock Info ACCUMULATE Price Rs735 Target Price Rs796 Investment Period 12 months ‘Rallis’ on Rallis India (RAIL), a Tata Group company, is the second largest player in the domestic Pesticide market. RAIL had undertaken a restructuring exercise post FY2004, which resulted in RAIL clocking all-time high EBITDA Margins in FY2009. Going ahead, we expect Contract Manufacturing (CM) to drive the company's next level of growth particularly with its new plant coming on stream by June 2010. We estimate RAIL to register a CAGR of 14% and 24.3% in Net Sales and Profit over FY2009-11E, respectively. At Rs735, the stock is trading at 8.9x FY2011E Earnings and 5.4x FY2011E EV/EBITDA. Historically, RAIL has traded in the 3-11x one-year forward PE band, and at an average 8x over the last couple of years. Going ahead, on account of improving Return Ratios and higher Net Profit growth, we expect the stock to trade at higher valuations than its historical average. We Initiate Coverage on the stock with an Accumulate rating and Target Price of Rs796. Set to seize rising opportunities in the Domestic Pesticides market: India's overall pesticides consumption is one of the lowest in the world, and we believe that RAIL is well-placed to seize this opportunity on the back of its wide distribution network, strong brands and robust new product pipeline. According to industry estimates, the unorganised market accounts for another 50% of the industry. Nonetheless, we believe that RAIL is in a position to wrest marketshare as well as charge a premium for its products. Exports to register steady growth: Closing down of capacity in China before the Olympics 2008 and MNCs diversifying their base to India had resulted in the company’s Exports spiking 80% in FY2009 to Rs295cr. The scenario has however changed post the Olympics and many closed capacities have come on stream. Slowdown in the global economy has also resulted in sluggish demand the worldover. Against this backdrop, we estimate RAIL to post a decent CAGR of 17.7% in Exports over FY2009-11E. Contract manufacturing to be next growth driver: RAIL plans to focus on CM for Exports and selectively target and supply to the top players. To facilitate the same, the company is setting up a new plant at Dahej. Overall, RAIL targets to achieve cumulative Revenues of Rs1,000cr over the next five years from this Segment alone. Sector Agrichemicals Market Cap (Rs cr) 880 Beta 0.4 52 Week High / Low 809/280 Avg Daily Volume 8547 Face Value (Rs) 10 BSE Sensex 15,191 Nifty 4,502 Shareholding Pattern (%) Promoters 45.2 MF / Banks / Indian FIs 31.8 FII / NRIs / OCBs 5.2 Indian Public / Others 17.8 Abs. 3 m 1yr 3yr Sensex (%) 38.4 11.4 46.7 Rallis India (%) 38.1 77.0 195.6 BSE Code 500355 NSE Code RALLIS Reuters Code RALL.BO Bloomberg Code RALI@IN

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 1

Rallis IndiaInitiating Coverage

Sageraj Bariya

Tel: 022 - 4040 3800 Ext: 346

E-mail: [email protected]: Company, Angel Research; Note: * Adjusted for exceptional item.

Key Financials (Consolidated)Y/E March (Rs cr) FY2008 FY2009 FY2010E FY2011E

Net Sales 674.6 836.7 946.9 1,087.3

% chg 9.4 24.0 13.2 14.8

Adj. Net Profit 43.6 64.3 74.2 99.4

% chg 1,752.2 47.4 15.4 33.9

Adj. FDEPS (Rs) 36.4 53.6 61.9 82.9

EBITDA Margin (%) 8.8 13.3 14.0 15.1

P/E (x) 20.2 13.7 11.9 8.9

RoE (%)* 16.6 19.6 21.9 26.7

RoCE (%) 13.0 22.4 22.5 25.8

P/BV (x) 4.0 3.4 2.7 2.1

EV/Sales (x) 1.3 1.0 1.0 0.8

EV/EBITDA (x) 14.6 7.4 7.3 5.4

Stock Info

ACCUMULATEPrice Rs735

Target Price Rs796

Investment Period 12 months

‘Rallis’ onRallis India (RAIL), a Tata Group company, is the second largest player in the domesticPesticide market. RAIL had undertaken a restructuring exercise post FY2004, which resultedin RAIL clocking all-time high EBITDA Margins in FY2009. Going ahead, we expect ContractManufacturing (CM) to drive the company's next level of growth particularly with its new plantcoming on stream by June 2010. We estimate RAIL to register a CAGR of 14% and 24.3%in Net Sales and Profit over FY2009-11E, respectively. At Rs735, the stock is trading at8.9x FY2011E Earnings and 5.4x FY2011E EV/EBITDA. Historically, RAIL has traded in the3-11x one-year forward PE band, and at an average 8x over the last couple of years. Goingahead, on account of improving Return Ratios and higher Net Profit growth, we expect thestock to trade at higher valuations than its historical average. We Initiate Coverage on thestock with an Accumulate rating and Target Price of Rs796.

Set to seize rising opportunities in the Domestic Pesticides market: India's overallpesticides consumption is one of the lowest in the world, and we believe that RAIL iswell-placed to seize this opportunity on the back of its wide distribution network, strongbrands and robust new product pipeline. According to industry estimates, the unorganisedmarket accounts for another 50% of the industry. Nonetheless, we believe that RAIL is in aposition to wrest marketshare as well as charge a premium for its products.

Exports to register steady growth: Closing down of capacity in China before theOlympics 2008 and MNCs diversifying their base to India had resulted in the company’sExports spiking 80% in FY2009 to Rs295cr. The scenario has however changed post theOlympics and many closed capacities have come on stream. Slowdown in the global economyhas also resulted in sluggish demand the worldover. Against this backdrop, we estimateRAIL to post a decent CAGR of 17.7% in Exports over FY2009-11E.

Contract manufacturing to be next growth driver: RAIL plans to focus on CM forExports and selectively target and supply to the top players. To facilitate the same, thecompany is setting up a new plant at Dahej. Overall, RAIL targets to achieve cumulativeRevenues of Rs1,000cr over the next five years from this Segment alone.

Sector Agrichemicals

Market Cap (Rs cr) 880

Beta 0.4

52 Week High / Low 809/280

Avg Daily Volume 8547

Face Value (Rs) 10

BSE Sensex 15,191

Nifty 4,502

Shareholding Pattern (%)

Promoters 45.2

MF / Banks / Indian FIs 31.8

FII / NRIs / OCBs 5.2

Indian Public / Others 17.8

Abs. 3 m 1yr 3yr

Sensex (%) 38.4 11.4 46.7

Rallis India (%) 38.1 77.0 195.6

BSE Code 500355

NSE Code RALLIS

Reuters Code RALL.BO

Bloomberg Code RALI@IN

2January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 2

Rallis India

Agrichemicals

Company Overview

Second largest Pesticide player

RAIL is one of the oldest and second largest pesticide agrichemical companies in the countrywith a marketshare of around 13% and belongs to the Tata Group. The company also has acredible presence in the international market. Pesticide accounts for 97% of the company'sTotal Revenues, while plant nutrients, seeds and leather chemicals constitute the balance.Historically contribution from the Domestic business has stood at 77% levels while Exportsaccounted for the balance.

Source: Company, Angel Research; Note - AI - Active Ingredients, CM - Contract Manufacturing

Exhibit 1: Sales Mix and Break-up

90

92

94

96

98

100

FY2007 FY2008 FY2009

Sales Mix (%)

Pesticides Nutrients Seeds Chemicals

Domestic -

Branded

55%

Export-CM

13%

Export-bulk

12%

Export-

Branded

10%

Domestic -

AI 10%

Sales Break up (%) for FY2009

Product break up

Paddy and Cotton are the two largest contributors to RAIL's Revenues, which is in line with theagrichemical consumption of the country wherein the two crops dominate the consumption. Interms of types of pesticides, Insecticides dominate the company's Revenue share with acontribution of almost 70%, followed by Fungicides and Herbicides, which contribute 20% and10% of the company's Total Revenues, respectively.

70%

20%

10%

Insecticides Fungicides Herbicides

Source: Company, Angel Research

Exhibit 2: Pesticides Sales break up (%)

Pesticide accounts for 97% ofthe company's Total Revenues

Insecticides dominate thecompany's Revenue sharewith a contribution of almost70%

3January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 3

Rallis India

Agrichemicals

Preferred distribution partner with MNCs

RAIL has one of the best distribution networks in the country with approximately 40,000retailers covering around 80% of India's districts. RAIL derives around 65% of its Revenues fromits domestic business through sale of own branded formulations (55%) and supply of bulk (10%)to other branded sellers.We believe that RAIL's distribution network is its key strength and thedifferentiating feature vis-a-vis competition. Hence, many MNC global players have inkedstrategic alliances with RAIL for distribution of their products (pesticides and seeds) in thedomestic market. strategic alliance contributes 1/3rd of domestic formulation.

Source: Company, Angel Research

Exhibit 3: Strategic AlliancesCompany Product CropE I Dupont Indoxacarb Cotton & GramSyngenta India Pretilachlor Rice

Thiomethozam Cotton & RiceEmmamaectine Benzoate Cotton

Makhteshim Chemical Works Atrazine SugarcaneCaptan General Fungicide

Bayer India Thirodicarb Cotton & VegetableNihon Nohayaku Fuji one RiceFMC India Carbofuran Rice

Carbosulfan Fruits & BrinjalBifenthrin Cotton & others

Gharda Chemicals Sulfosulfuron WheatChloro + Cyper Cotton & Rice

Yara International Calcium nitrate solution Water soluable fertilizersfor various crop

Borax International Boron 20% Cotton, Chillies & Tomato

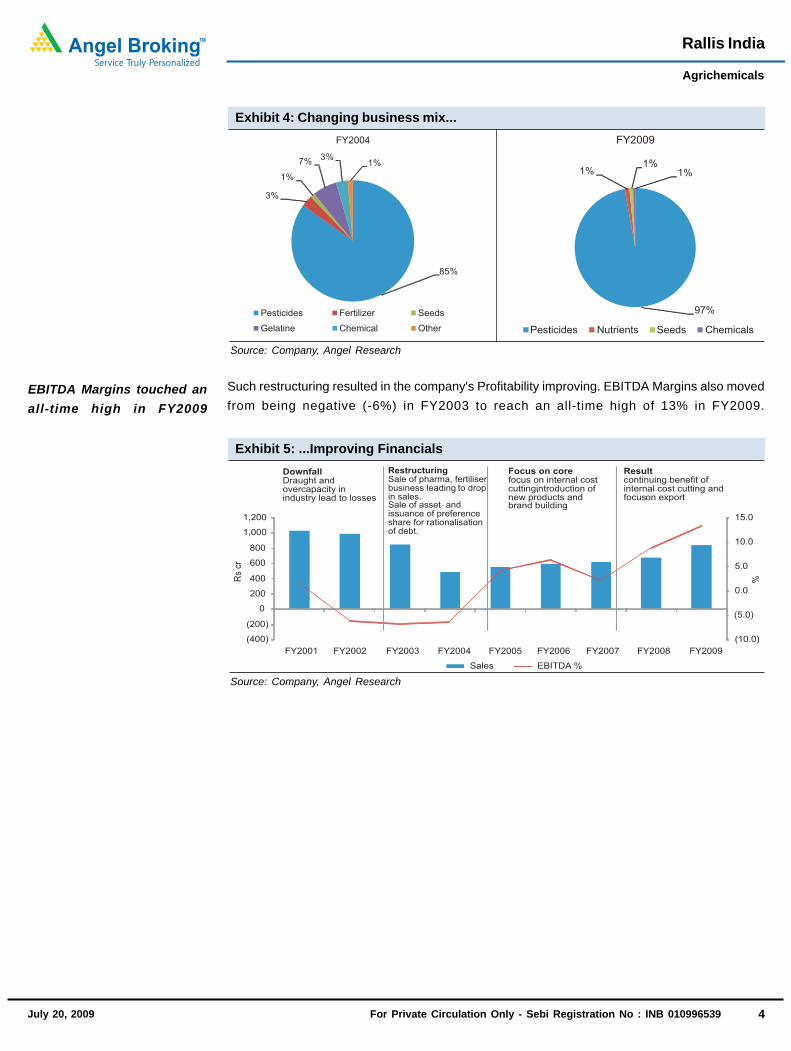

Business restructuring aids turnaround

During FY2001-04, the company was involved in too many businesses which dilutedmanagement's focus and was in the red. Since then, it has come a long way. RAIL initiatedseveral measures to restructure its business following which it managed to turn the corner.Some of the measures initiated by the company included the following:

Selling of non-core business like Pharma and Gelatin;

Merger of subsidiaries to reduce operating expenses;

Disposing land to generate cash; and

Issuance of Preference share worth Rs88cr to Tata group companies.

We believe that RAIL'sdistribution network is its keystrength and thedifferentiating feature vis-a-viscompetition

4January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 4

Rallis India

Agrichemicals

Source: Company, Angel Research

Exhibit 4: Changing business mix...

Pesticides Nutrients Seeds Chemicals

97%

1%1%

1%

FY2009

85%

3%

1%

7%3%

1%

FY2004

Pesticides Fertilizer Seeds

Gelatine Chemical Other

Such restructuring resulted in the company's Profitability improving. EBITDA Margins also movedfrom being negative (-6%) in FY2003 to reach an all-time high of 13% in FY2009.

Source: Company, Angel Research

Exhibit 5: ...Improving Financials

(10.0)

(5.0)

0.0

5.0

10.0

15.0

(400)

(200)

0

200

400

600

800

1,000

1,200

FY2001 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 FY2009

Sales EBITDA %

RestructuringSale of pharma, fertiliserbusiness leading to dropin sales.Sale of asset andissuance of preferenceshare for rationalisationof debt.

Focus on corefocus on internal costcutting,introduction ofnew products andbrand building

Resultcontinuing benefit ofinternal cost cutting andfocuson export

DownfallDraught andovercapacity inindustry lead to losses

Rs

cr

%

EBITDA Margins touched anall-time high in FY2009

5January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 5

Rallis India

Agrichemicals

Investment Argument

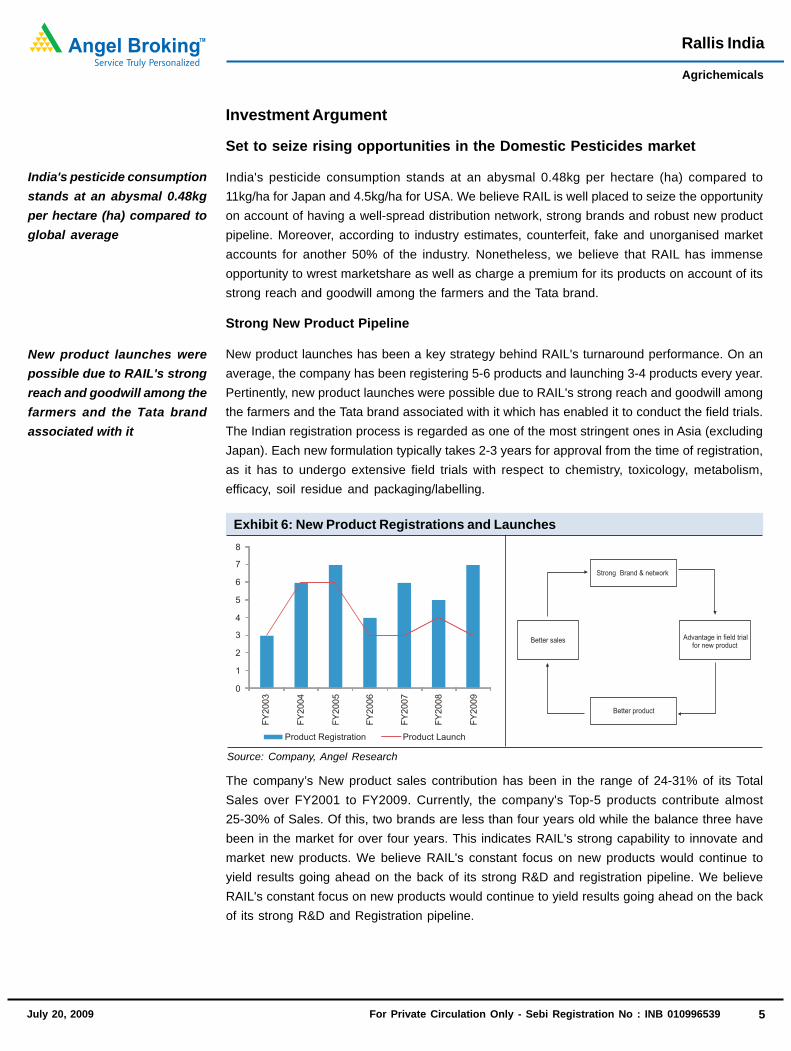

Set to seize rising opportunities in the Domestic Pesticides market

India's pesticide consumption stands at an abysmal 0.48kg per hectare (ha) compared to11kg/ha for Japan and 4.5kg/ha for USA. We believe RAIL is well placed to seize the opportunityon account of having a well-spread distribution network, strong brands and robust new productpipeline. Moreover, according to industry estimates, counterfeit, fake and unorganised marketaccounts for another 50% of the industry. Nonetheless, we believe that RAIL has immenseopportunity to wrest marketshare as well as charge a premium for its products on account of itsstrong reach and goodwill among the farmers and the Tata brand.

Strong New Product Pipeline

New product launches has been a key strategy behind RAIL's turnaround performance. On anaverage, the company has been registering 5-6 products and launching 3-4 products every year.Pertinently, new product launches were possible due to RAIL's strong reach and goodwill amongthe farmers and the Tata brand associated with it which has enabled it to conduct the field trials.The Indian registration process is regarded as one of the most stringent ones in Asia (excludingJapan). Each new formulation typically takes 2-3 years for approval from the time of registration,as it has to undergo extensive field trials with respect to chemistry, toxicology, metabolism,efficacy, soil residue and packaging/labelling.

The company’s New product sales contribution has been in the range of 24-31% of its TotalSales over FY2001 to FY2009. Currently, the company's Top-5 products contribute almost25-30% of Sales. Of this, two brands are less than four years old while the balance three havebeen in the market for over four years. This indicates RAIL's strong capability to innovate andmarket new products. We believe RAIL's constant focus on new products would continue toyield results going ahead on the back of its strong R&D and registration pipeline. We believeRAIL's constant focus on new products would continue to yield results going ahead on the backof its strong R&D and Registration pipeline.

India's pesticide consumptionstands at an abysmal 0.48kgper hectare (ha) compared toglobal average

New product launches werepossible due to RAIL's strongreach and goodwill among thefarmers and the Tata brandassociated with it

Source: Company, Angel Research

Strong Brand & network

Advantage in field trialfor new product

Better product

Better sales

0

1

2

3

4

5

6

7

8

FY

2003

FY

2004

FY

2005

FY

2006

FY

2007

FY

2008

FY

2009

Product Registration Product Launch

Exhibit 6: New Product Registrations and Launches

6January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 6

Rallis India

Agrichemicals

Source: Company, Angel Research

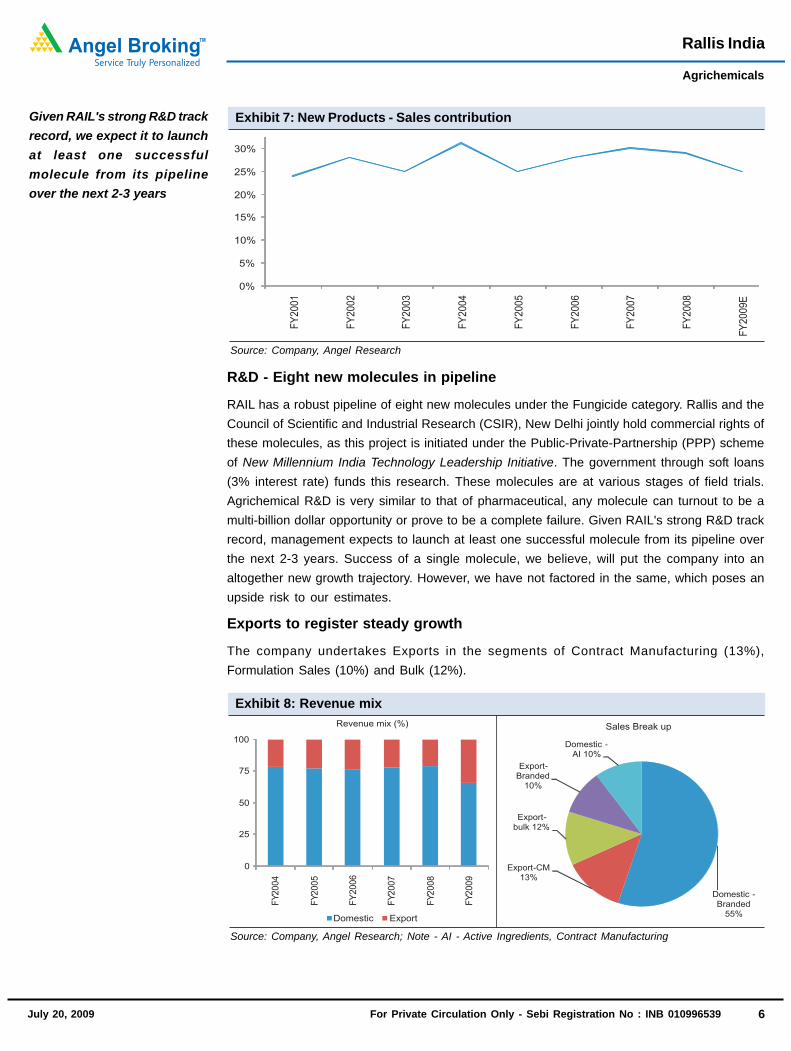

Exhibit 7: New Products - Sales contribution

R&D - Eight new molecules in pipeline

RAIL has a robust pipeline of eight new molecules under the Fungicide category. Rallis and theCouncil of Scientific and Industrial Research (CSIR), New Delhi jointly hold commercial rights ofthese molecules, as this project is initiated under the Public-Private-Partnership (PPP) schemeof New Millennium India Technology Leadership Initiative. The government through soft loans(3% interest rate) funds this research. These molecules are at various stages of field trials.Agrichemical R&D is very similar to that of pharmaceutical, any molecule can turnout to be amulti-billion dollar opportunity or prove to be a complete failure. Given RAIL's strong R&D trackrecord, management expects to launch at least one successful molecule from its pipeline overthe next 2-3 years. Success of a single molecule, we believe, will put the company into analtogether new growth trajectory. However, we have not factored in the same, which poses anupside risk to our estimates.

Exports to register steady growth

The company undertakes Exports in the segments of Contract Manufacturing (13%),Formulation Sales (10%) and Bulk (12%).

Given RAIL's strong R&D trackrecord, we expect it to launchat least one successfulmolecule from its pipelineover the next 2-3 years

Source: Company, Angel Research; Note - AI - Active Ingredients, Contract Manufacturing

Exhibit 8: Revenue mix

0

25

50

75

100

FY2004

FY2005

FY

2006

FY2007

FY2008

FY2009

Revenue mix (%)

Domestic Export

Domestic -

Branded

55%

Export-CM

13%

Export-

bulk 12%

Export-

Branded

10%

Domestic -

AI 10%

Sales Break up

7January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 7

Rallis India

Agrichemicals

Over FY2004-09, RAIL's Exports registered a decent CAGR of 27.7%. However, FY2009 was anexceptional year where the company's exports spiked a significant 80% to Rs295cr andcontribution to Total Revenue stood at around 35% compared to 21% and 22% in FY2007 andFY2008, respectively. Thus, excluding the phenomenal growth registered in FY2009, thecompany's Exports CAGR during FY2004-08 stood at 10.3%.

The company's exceptional FY2009 performance was driven by a combination of factorsincluding:

Closing down of capacity in China before the Olympics 2008Closing of many manufacturing units on ecological ground created overall shortage.

Diversification of manufacturing base globallyMany global MNCs were dependent on Chinese manufacturing base for supply of their

product. To mitigate risks arising from such dependence, they started sourcing from the Indianmanufacturers.

Post the Olympics, the scenario has changed with many closed capacities coming on stream.Besides, overall slowdown in the global economy has also resulted in sluggish demand theworldover. It is against this backdrop that we estimate RAIL to post a decent CAGR of 17.7% inExports over FY2009-11E.

Contract Manufacturing - Cumulative Revenue target of Rs1,000cr over nextfive years

Currently, RAIL is an exclusive contract manufacturer and supplier of two agrichemicals andone speciality polymer to a global player. RAIL has entered into long-term (5-7 years) supplyagreement with global MNCs. Revenue and Profit visibility is usually high in such dedicatedmanufacturing supply agreements. Hence, going ahead, we expect this Segment to be the keygrowth driver for the company.

Global supplier for AI

Global agrichemical companies have been reducing manufacturing capacity of low valueproducts to concentrate on higher-value products. Conversely, they are maintaining their stronghold on off-patent AI through outsourcing the same. For example, Germany's BASF has cut itsrange of AI from 300 in 2001 to 130 in 2006. Syngenta has also reduced its portfolio from 120 to80. Bayer CropScience reduced its portfolio by 29 actives between 2000 and 2006. Total globalsales of agrichemicals were estimated to be worth US $41bn in CY2008. Sales of patentedproduct constituted approximately 1/3rd of the total and another 1/3rd is proprietary off patent(Patent of molecule has expired but no credible generic brand has been able to garner significantmarketshare from patented brand). Opportunity of even 10% of the total market size wouldtranslate into US $4bn. Hence, RAIL plans to selectively target this opportunity by supplying AIto the industry top players. Overall, RAIL is targeting cumulative Revenues of Rs1,000cr overthe next five years from this Segment alone.

FY2009 was an exceptionalyear with the company'sexports spiking a significant80% to Rs295cr

Revenue and Profit visibility ishigh in the manufacturingsupply agreements with theMNCs

Rising trend of outsourcingby global MNCs

8January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 8

Rallis India

Agrichemicals

Targeting niche high-Margin Agrichemicals

Agrichemicals being crop specific have varying demand based on the specific type of pest thathampers growth of the crop. Hence, one crop might need different type of insecticides or fungicideor herbicide in different regions. In addition, there are many crops that are grown in very specificregions and may require less amount of agrichemicals which may not be economical to produceand profitable to sell to the big global players. Therefore, the smaller regional players very oftendominate these niche segments. RAIL plans to meet the requirements of such niche demand,as it commands higher Margin.

Setting up new plant for CM

RAIL is setting up a new plant at Dahej for manufacturing AI for the export market as well as tomeet its own formulation consumption. Total capex of the Dahej plant is estimated at Rs150cr.The company has already incurred Rs40cr in FY2009. The plant is likely to be up and ready byJune 2010. The plant will enjoy SEZ status and avail tax exemptions. We expect this plant tocontribute Rs450cr to the company's Total Sales at peak capacity utilisation.

Formulation Exports - Still at investment stage

The company sells formulations under its own brand name post registration in the respectivecountries. Currently, the company sells its formulations in almost 25 different countries acrossthe world in regions like Latin American, USA, Japan, South East Asia, Australia and Africa.Registration and distribution network are the key requirements for this business. In line withthis, the company has tied up with local distributors for the supply of its product. However, webelieve that this business is still at the investment stage as the company is building its productportfolio through registrations, branding and network tie-ups. Nonetheless, we believe that exportformulation will be the next growth driver for the company post CM. We expect sustainablecontribution from this business to start trickling over the next 2-3 years. We believe that RAILmight acquire a company with a strong distribution network to meet its targets in the Segment.However, this seems sometime away as it is still in the process of building its product portfolio.

Hidden Gems

Advinus Therapeutics

During 2005, the company transferred its Knowledge Services Business, a Research &Development Centre at Bangalore to Advinus Therapeutics Pvt Ltd for a consideration of Rs26cr.Advinus is India's finest Clinical Research Organisation (CRO) involved in business of New DrugDiscovery (Pharma & Agriculture) and clinical trials. The company is the first of its kind in Indiato offer end-to-end development services to the global Pharma, Agro and Biotech industries.Advinus was named as India's best emerging CRO in drug discovery services, according to asurvey conducted by Proximare, a management consulting firm based in New Jersey thatexclusively serves pharmaceutical and biotechnology companies with strategic issues. Webelieve Advinus has one of the best management teams in place to capitalise on the R&Doutsourcing opportunity.

The Dahej plant is expected tobe operational by June 2010

The company is building itsproduct portfolio forinternational markets

Advinus is India's finest CROin the business of New DrugDiscovery (Pharma &Agriculture) and clinical trials

9January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 9

Rallis India

Agrichemicals

Source: Company

Exhibit 9: Advinus - Illustrious ManagementExecutive CommitteeDr. Rashmi Barbhaiya - CEO and Managing Ex-President of R&D - Ranbaxy ResearchDirector Laboratories

Ex-Vice President in the PharmaceuticalResearch Institute, Bristol-Meyers Squibb (BMS).

Dr. Kasim Mookhtiar - CSO and Senior Vice Ex-Bristol-Meyers Squibb & Ranbaxy Lab.President, Drug DiscoveryDr. Nimish Vachharajani - Vice President and Ex-Bristol-Meyers SquibbHead - Pharmaceuticals and AgrochemicalDevelopmentScientific Advisory BoardChristopher M. Cimarusti, Ph.D Ex-Bristol-Meyers Squibb (BMS) - worked in drug

discovery and development.Perry B. Molinoff, MD Professor of Pharmacology at the University of

Pennsylvania. More than 30 years of experiencein academic and industrial sectors

David C. U'Prichard, Ph.D President of Druid Consulting LLC, consultantto the pharmaceutical and biotechnologyindustries

The Tata group is a major shareholder in Advinus while RAIL holds 15% stake in it while thecompany management holds minority stake. As per media reports, Advinus Revenues are in theregion of Rs80-100cr, while total investment are estimated at around Rs200cr. Advinus iscurrently loss making and under investment mode. RAIL does not plan to sell its stake as itconsiders it as a strategic investment. We have not taken any value of Advinus in our valuationof Rallis however any developments on this front would have ripple effects on Rallis.

Real Estate

RAIL has considerable amount of surplus real estate that it can divest if the need arises. Thecompany in the past had sold real estate to raise funds for its core business. As per mediareports, the company currently has excess land of 85 acres in Hyderabad and 22 acres inThane, Maharashtra. We have conservatively estimated value of the same in the region ofRs300-400cr translating into Rs250-334 per share. Our valuations are in line with the historicdeal done by RAIL wherein it had sold 31 acre property at Hyderabad for Rs90cr to Peninsula inFY2008. We have not factored any value of Real Estate in our valuation.

Miscellaneous

RAIL derives a small amount (3% of Total Revenues) of revenue through sale of seeds, plantnutrients and leather chemical. In case of its Seeds business, the company markets hybrid,high yielding and genetic modified seeds of different crops (Bt Cotton, Wheat, Paddy, etc). RAILalso has a small presence in the Leather Chemical business through its brand Vegtan for theTannery Industry. Vegtan holds 45% marketshare in the domestic market.

We have not taken any valueof Advinus in our valuation ofRallis; however, anydevelopments on this frontwould have ripple effects onRallis

We estimate value of thecompany’s surplus realestate at Rs300-400crtranslating into Rs250-334 pershare

10January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 10

Rallis India

Agrichemicals

Financial Performance

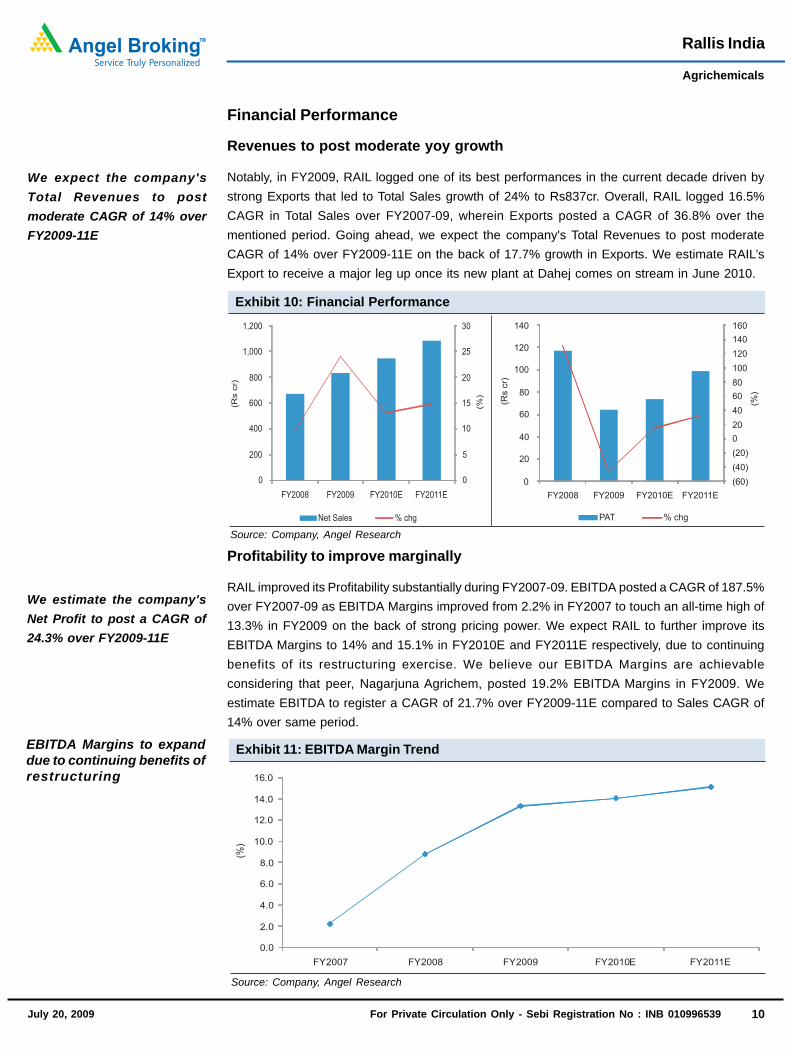

Revenues to post moderate yoy growth

Notably, in FY2009, RAIL logged one of its best performances in the current decade driven bystrong Exports that led to Total Sales growth of 24% to Rs837cr. Overall, RAIL logged 16.5%CAGR in Total Sales over FY2007-09, wherein Exports posted a CAGR of 36.8% over thementioned period. Going ahead, we expect the company's Total Revenues to post moderateCAGR of 14% over FY2009-11E on the back of 17.7% growth in Exports. We estimate RAIL’sExport to receive a major leg up once its new plant at Dahej comes on stream in June 2010.

Profitability to improve marginally

RAIL improved its Profitability substantially during FY2007-09. EBITDA posted a CAGR of 187.5%over FY2007-09 as EBITDA Margins improved from 2.2% in FY2007 to touch an all-time high of13.3% in FY2009 on the back of strong pricing power. We expect RAIL to further improve itsEBITDA Margins to 14% and 15.1% in FY2010E and FY2011E respectively, due to continuingbenefits of its restructuring exercise. We believe our EBITDA Margins are achievableconsidering that peer, Nagarjuna Agrichem, posted 19.2% EBITDA Margins in FY2009. Weestimate EBITDA to register a CAGR of 21.7% over FY2009-11E compared to Sales CAGR of14% over same period.

We expect the company'sTotal Revenues to postmoderate CAGR of 14% overFY2009-11E

We estimate the company'sNet Profit to post a CAGR of24.3% over FY2009-11E

Source: Company, Angel Research

Exhibit 11: EBITDA Margin Trend

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

FY2007 FY2008 FY2009 FY2010E FY2011E

(%)

EBITDA Margins to expanddue to continuing benefits ofrestructuring on strongpricing power

Source: Company, Angel Research

Exhibit 10: Financial Performance

0

5

10

15

20

25

30

0

200

400

600

800

1,000

1,200

FY2008 FY2009 FY2010E FY2011E

Net Sales % chg

(Rs

cr)

(%)

(60)

(40)

(20)

0

20

40

60

80

100

120

140

160

0

20

40

60

80

100

120

140

FY2008 FY2009 FY2010E FY2011E

PAT % chg

(Rs

cr)

(%)

11January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 11

Rallis India

Agrichemicals

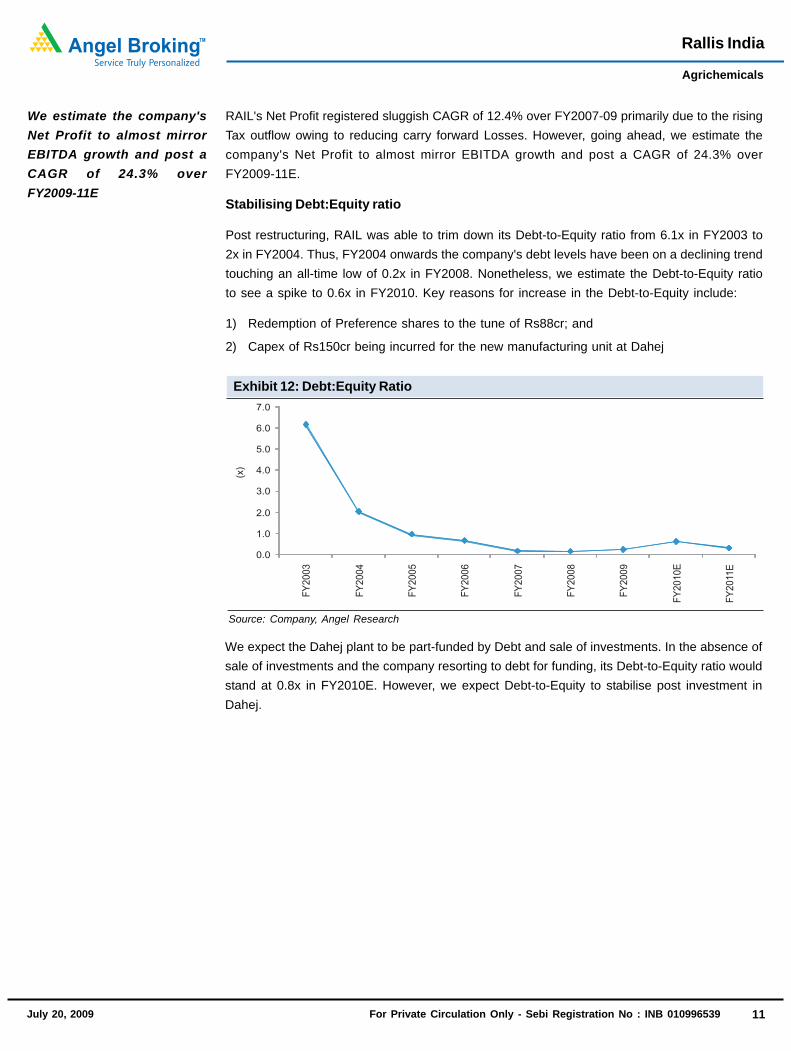

RAIL's Net Profit registered sluggish CAGR of 12.4% over FY2007-09 primarily due to the risingTax outflow owing to reducing carry forward Losses. However, going ahead, we estimate thecompany's Net Profit to almost mirror EBITDA growth and post a CAGR of 24.3% overFY2009-11E.

Stabilising Debt:Equity ratio

Post restructuring, RAIL was able to trim down its Debt-to-Equity ratio from 6.1x in FY2003 to2x in FY2004. Thus, FY2004 onwards the company's debt levels have been on a declining trendtouching an all-time low of 0.2x in FY2008. Nonetheless, we estimate the Debt-to-Equity ratioto see a spike to 0.6x in FY2010. Key reasons for increase in the Debt-to-Equity include:

1) Redemption of Preference shares to the tune of Rs88cr; and

2) Capex of Rs150cr being incurred for the new manufacturing unit at Dahej

Source: Company, Angel Research

Exhibit 12: Debt:Equity Ratio

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY

20

03

FY

20

04

FY

20

05

FY

20

06

FY

20

07

FY

20

08

FY

20

09

FY

20

10

E

FY

20

11E

(x)

We expect the Dahej plant to be part-funded by Debt and sale of investments. In the absence ofsale of investments and the company resorting to debt for funding, its Debt-to-Equity ratio wouldstand at 0.8x in FY2010E. However, we expect Debt-to-Equity to stabilise post investment inDahej.

We estimate the company'sNet Profit to almost mirrorEBITDA growth and post aCAGR of 24.3% overFY2009-11E

12January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 12

Rallis India

Agrichemicals

Return Ratios set to improve

The company’s RoE soared to 45.2% in FY2008 on the back of exceptionally high OtherIncome arising from sale of assets. In FY2009, the company recorded RoE of 19.6% on theback of expansion in EBITDA Margins. Going ahead, we estimate the company to furtherimprove its RoE to 21.9% and 26.7% in FY2010 and FY2011E respectively, following animprovement in EBITDA Margins due to continuing benefits of restructuring.

Downside risks to our call

Growth challenge in Exports: If the company is unable to meet our export target due to anyunforeseen external factors, the company may post dismal performance and pose a downsiderisk to our estimates.

Vagaries of Monsoon: Agrichemicals are the last input in any agricultural operation andprotect the final output ie. crop. In case of India, most of the agricultural production is rain fedand hence highly dependent on monsoon. Hence, vagaries in season could affect the demandfor agrichemicals and in turn impact our estimates.

Source: Company, Angel Research; Note: Adjusted for exceptional item.

Exhibit 14: DuPont AnalysisFY2008 FY2009 FY2010E FY2011E

EBITDA/Sales (%) 8.8 13.3 14.0 15.1

Sales/Total Assets (x) 1.9 1.9 1.8 2.0

PBT/EBITDA(x) 2.3 0.9 0.9 0.9

PAT/PBT (x) 0.8 0.6 0.7 0.7

Total Assets/Net Worth (x) 1.6 1.7 1.6 1.3

RoE (%) 16.6 19.6 21.9 26.7

0

5

10

15

20

25

30

FY2008 FY2009 FY2010E FY2011E

(%)

RoE (%) RoCE (%)

Exhibit 13: Improving Return Ratios

Source: Company, Angel Research; Note: Adjusted for exceptional item.

13January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 13

Rallis India

Agrichemicals

Source: Company, Angel Research

Exhibit 15: One-year Forward P/E Chart

0

100

200

300

400

500

600

700

Apr-

03

Jul-

03

Oct

-03

Jan

-04

Apr-

04

Jul-

04

Oct

-04

Jan

-05

Apr-

05

Jul-

05

Oct

-05

Jan

-06

Apr-

06

Jul-

06

Oct

-06

Jan

-07

Apr-

07

Jul-

07

Oct

-07

Jan

-08

Apr-

08

Jul-

08

Oct

-08

Jan

-09

Apr-

09

3x

5x

7x

9x

11x

(Rs)

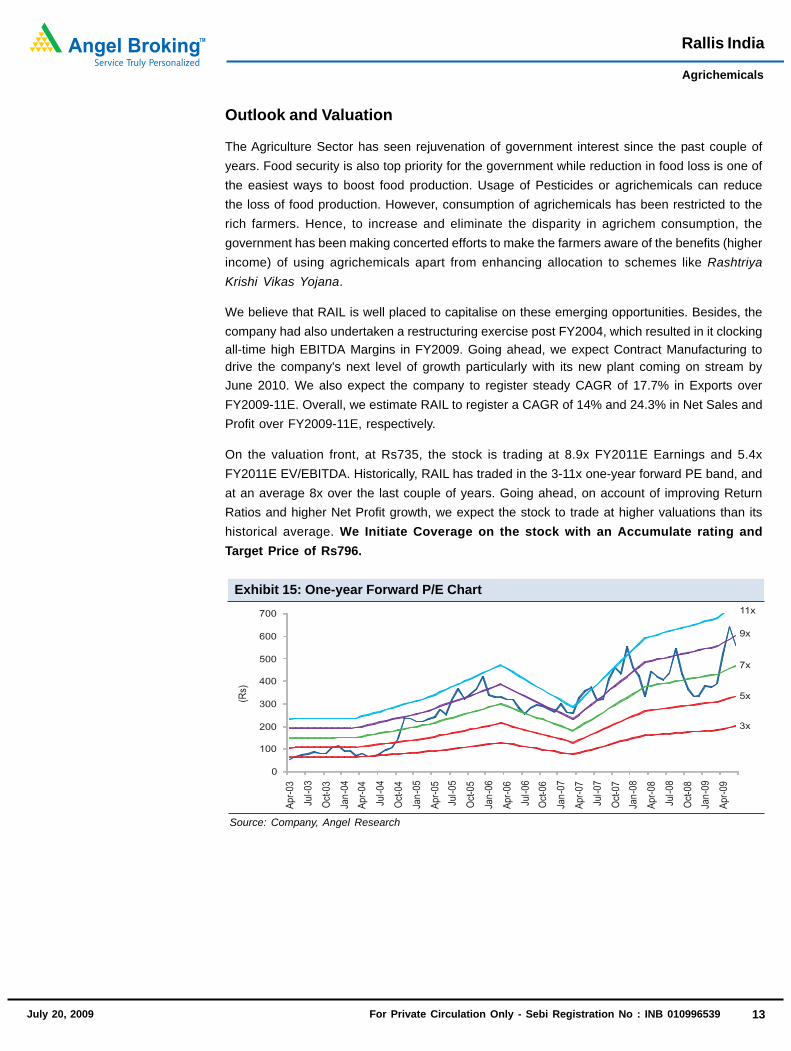

Outlook and Valuation

The Agriculture Sector has seen rejuvenation of government interest since the past couple ofyears. Food security is also top priority for the government while reduction in food loss is one ofthe easiest ways to boost food production. Usage of Pesticides or agrichemicals can reducethe loss of food production. However, consumption of agrichemicals has been restricted to therich farmers. Hence, to increase and eliminate the disparity in agrichem consumption, thegovernment has been making concerted efforts to make the farmers aware of the benefits (higherincome) of using agrichemicals apart from enhancing allocation to schemes like RashtriyaKrishi Vikas Yojana.

We believe that RAIL is well placed to capitalise on these emerging opportunities. Besides, thecompany had also undertaken a restructuring exercise post FY2004, which resulted in it clockingall-time high EBITDA Margins in FY2009. Going ahead, we expect Contract Manufacturing todrive the company's next level of growth particularly with its new plant coming on stream byJune 2010. We also expect the company to register steady CAGR of 17.7% in Exports overFY2009-11E. Overall, we estimate RAIL to register a CAGR of 14% and 24.3% in Net Sales andProfit over FY2009-11E, respectively.

On the valuation front, at Rs735, the stock is trading at 8.9x FY2011E Earnings and 5.4xFY2011E EV/EBITDA. Historically, RAIL has traded in the 3-11x one-year forward PE band, andat an average 8x over the last couple of years. Going ahead, on account of improving ReturnRatios and higher Net Profit growth, we expect the stock to trade at higher valuations than itshistorical average. We Initiate Coverage on the stock with an Accumulate rating andTarget Price of Rs796.

14January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 14

Rallis India

Agrichemicals

Annexure

Industry Overview

Agrichemicals also known as Pesticides are substance or mixture of substances that are usedto avert, destroy or control any kind of pests or unwanted type of plants or animals that causeharm to crops or hampers the normal growth process of a crop. As per a Government of Indiaestimate of 2002, value of crop losses caused due to non-usage of pesticides was aroundRs90,000cr. Thereon, assuming losses grew at an average 2%, total losses would have amountedto Rs101,355cr in FY2009, a staggering 2.2% of India's GDP. Pesticides are the last input inany agricultural operation, which protects all the other inputs as significant investment arealready committed by then.

Size

Global Agrichemical industry has grown at an average 7.1% over CY2001-08 to US $41.7bn.For CY2008, the industry registered outstanding growth of 25% yoy on the back of volumegrowth and increase in price. On the other hand, the Indian Agrichemical Industry wasestimated at around US $1bn (Rs5,000cr) at the end of FY2009. In FY2009, overall industrywitnessed marginal volume decline, but saw a price increase of 10-12%.

Land

Seed

Labour

Fertilisers

Agrichemicals

Exhibit 16: Investment chain of farmer

Source: Industry , Angel research

Pesticides are the last input inany agricultural operation,which protects all the otherinputs as significantinvestment are alreadycommitted by then

Year US $mn % yoy2001 25,7602002 25,150 (2.4)2003 26,710 6.22004 30,725 15.02005 31,190 1.52006 30,425 (2.5)2007 33,390 9.72008 41,735 25.0

Source: Company

Exhibit 17: Global Agrichemical market

15January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 15

Rallis India

Agrichemicals

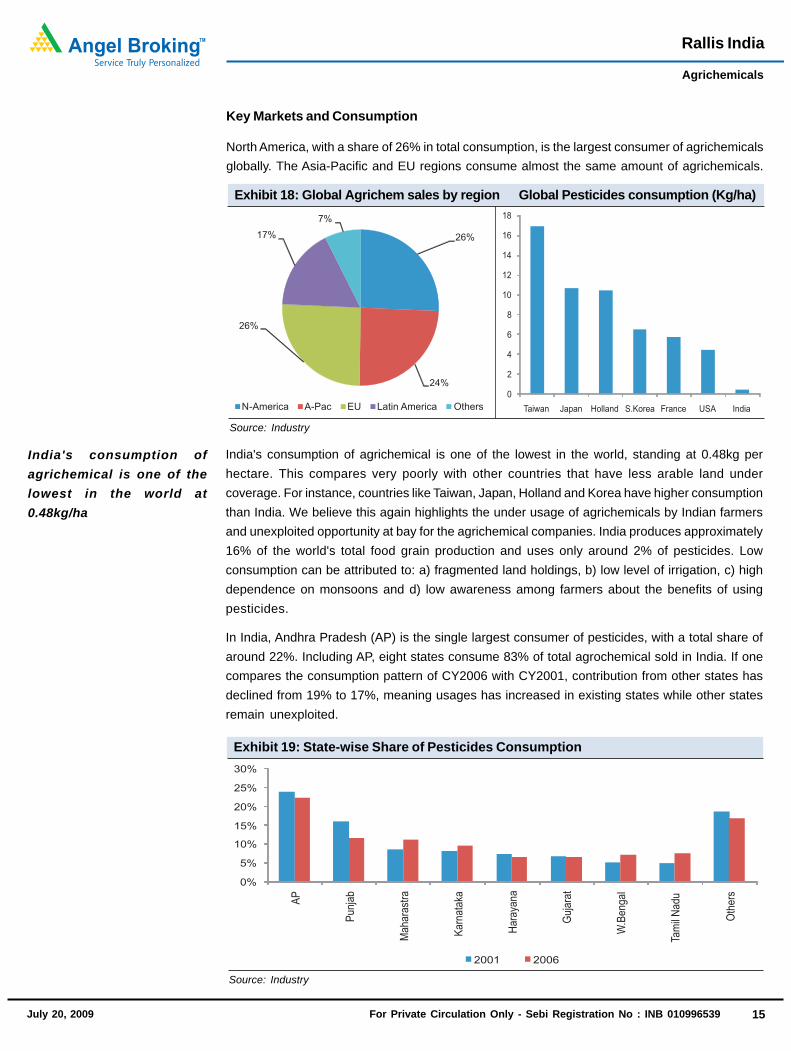

India's consumption of agrichemical is one of the lowest in the world, standing at 0.48kg perhectare. This compares very poorly with other countries that have less arable land undercoverage. For instance, countries like Taiwan, Japan, Holland and Korea have higher consumptionthan India. We believe this again highlights the under usage of agrichemicals by Indian farmersand unexploited opportunity at bay for the agrichemical companies. India produces approximately16% of the world's total food grain production and uses only around 2% of pesticides. Lowconsumption can be attributed to: a) fragmented land holdings, b) low level of irrigation, c) highdependence on monsoons and d) low awareness among farmers about the benefits of usingpesticides.

In India, Andhra Pradesh (AP) is the single largest consumer of pesticides, with a total share ofaround 22%. Including AP, eight states consume 83% of total agrochemical sold in India. If onecompares the consumption pattern of CY2006 with CY2001, contribution from other states hasdeclined from 19% to 17%, meaning usages has increased in existing states while other statesremain unexploited.

India's consumption ofagrichemical is one of thelowest in the world at0.48kg/ha

Key Markets and Consumption

North America, with a share of 26% in total consumption, is the largest consumer of agrichemicalsglobally. The Asia-Pacific and EU regions consume almost the same amount of agrichemicals.

Source: Industry

Exhibit 18: Global Agrichem sales by region Global Pesticides consumption (Kg/ha)

N-America A-Pac EU Latin America Others

26%

24%

26%

17%

7%

0

2

4

6

8

10

12

14

16

18

Taiwan Japan Holland S.Korea France USA India

Source: Industry

Exhibit 19: State-wise Share of Pesticides Consumption

0%

5%

10%

15%

20%

25%

30%

AP

Pu

nja

b

Ma

ha

rast

ra

Ka

rna

taka

Ha

raya

na

Gu

jara

t

W.B

en

ga

l

Tam

ilN

ad

u

Oth

ers

2001 2006

16January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 16

Rallis India

Agrichemicals

Source: Industry

Exhibit 21: India’s Changing Pesticides Consumption Pattern

Fungicides Herbicides Insecticides

15%

18%

67%

FY2007

Pesticides Classification and Marketshare

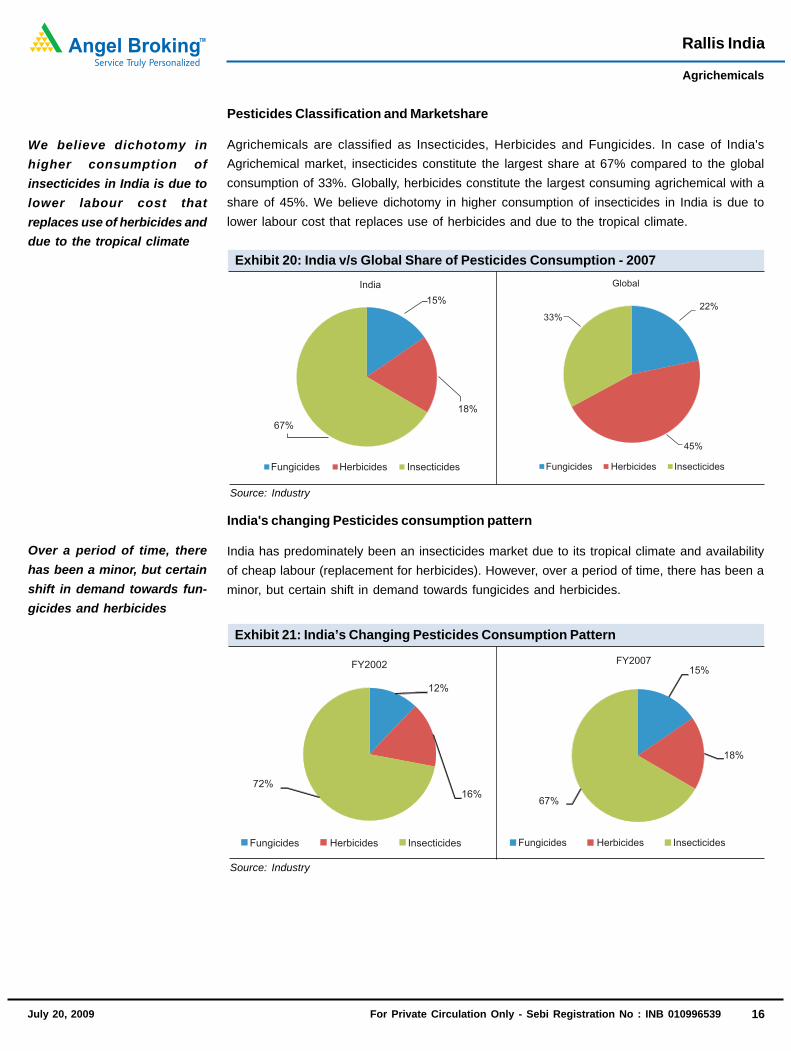

Agrichemicals are classified as Insecticides, Herbicides and Fungicides. In case of India'sAgrichemical market, insecticides constitute the largest share at 67% compared to the globalconsumption of 33%. Globally, herbicides constitute the largest consuming agrichemical with ashare of 45%. We believe dichotomy in higher consumption of insecticides in India is due tolower labour cost that replaces use of herbicides and due to the tropical climate.

Source: Industry

Exhibit 20: India v/s Global Share of Pesticides Consumption - 2007

India's changing Pesticides consumption pattern

India has predominately been an insecticides market due to its tropical climate and availabilityof cheap labour (replacement for herbicides). However, over a period of time, there has been aminor, but certain shift in demand towards fungicides and herbicides.

Fungicides Herbicides Insecticides

15%

18%

67%

India

Fungicides Herbicides Insecticides

22%

45%

33%

Global

We believe dichotomy inhigher consumption ofinsecticides in India is due tolower labour cost thatreplaces use of herbicides anddue to the tropical climate

Over a period of time, therehas been a minor, but certainshift in demand towards fun-gicides and herbicides

12%

16%72%

FY2002

Fungicides Herbicides Insecticides

17January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 17

Rallis India

Agrichemicals

Key consuming crops

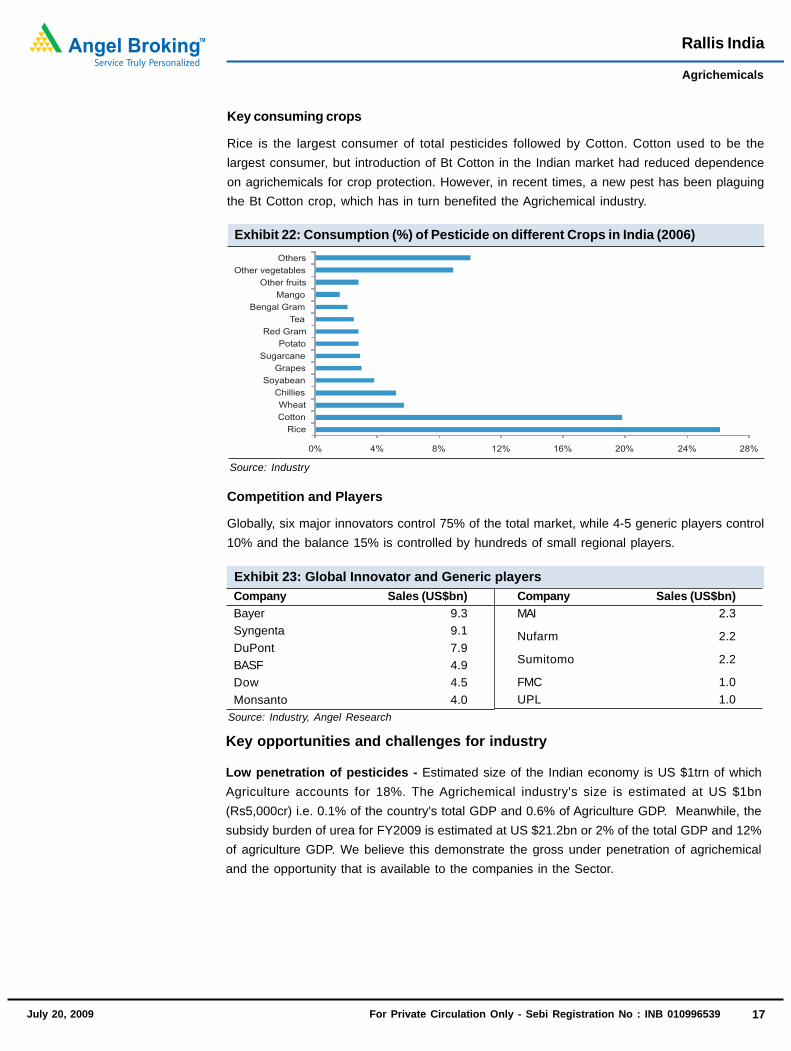

Rice is the largest consumer of total pesticides followed by Cotton. Cotton used to be thelargest consumer, but introduction of Bt Cotton in the Indian market had reduced dependenceon agrichemicals for crop protection. However, in recent times, a new pest has been plaguingthe Bt Cotton crop, which has in turn benefited the Agrichemical industry.

Competition and Players

Globally, six major innovators control 75% of the total market, while 4-5 generic players control10% and the balance 15% is controlled by hundreds of small regional players.

Company Sales (US$bn)MAI 2.3

Nufarm 2.2

Sumitomo 2.2

FMC 1.0UPL 1.0

Exhibit 23: Global Innovator and Generic playersCompany Sales (US$bn)Bayer 9.3Syngenta 9.1DuPont 7.9BASF 4.9Dow 4.5Monsanto 4.0

Source: Industry, Angel Research

Source: Industry

Exhibit 22: Consumption (%) of Pesticide on different Crops in India (2006)

0% 4% 8% 12% 16% 20% 24% 28%

Rice

Cotton

Wheat

Chillies

Soyabean

Grapes

Sugarcane

Potato

Red Gram

Tea

Bengal Gram

Mango

Other fruits

Other vegetables

Others

Key opportunities and challenges for industry

Low penetration of pesticides - Estimated size of the Indian economy is US $1trn of whichAgriculture accounts for 18%. The Agrichemical industry's size is estimated at US $1bn(Rs5,000cr) i.e. 0.1% of the country's total GDP and 0.6% of Agriculture GDP. Meanwhile, thesubsidy burden of urea for FY2009 is estimated at US $21.2bn or 2% of the total GDP and 12%of agriculture GDP. We believe this demonstrate the gross under penetration of agrichemicaland the opportunity that is available to the companies in the Sector.

18January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 18

Rallis India

Agrichemicals

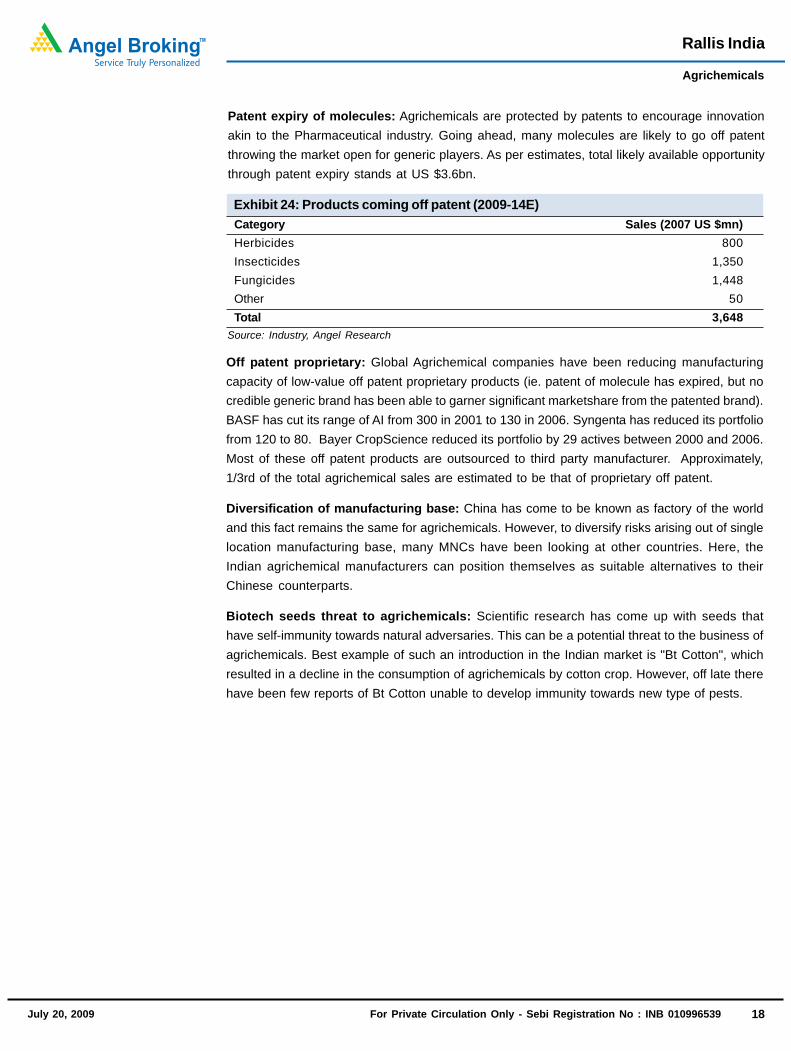

Exhibit 24: Products coming off patent (2009-14E)

Source: Industry, Angel Research

Category Sales (2007 US $mn)Herbicides 800Insecticides 1,350Fungicides 1,448Other 50Total 3,648

Off patent proprietary: Global Agrichemical companies have been reducing manufacturingcapacity of low-value off patent proprietary products (ie. patent of molecule has expired, but nocredible generic brand has been able to garner significant marketshare from the patented brand).BASF has cut its range of AI from 300 in 2001 to 130 in 2006. Syngenta has reduced its portfoliofrom 120 to 80. Bayer CropScience reduced its portfolio by 29 actives between 2000 and 2006.Most of these off patent products are outsourced to third party manufacturer. Approximately,1/3rd of the total agrichemical sales are estimated to be that of proprietary off patent.

Diversification of manufacturing base: China has come to be known as factory of the worldand this fact remains the same for agrichemicals. However, to diversify risks arising out of singlelocation manufacturing base, many MNCs have been looking at other countries. Here, theIndian agrichemical manufacturers can position themselves as suitable alternatives to theirChinese counterparts.

Biotech seeds threat to agrichemicals: Scientific research has come up with seeds thathave self-immunity towards natural adversaries. This can be a potential threat to the business ofagrichemicals. Best example of such an introduction in the Indian market is "Bt Cotton", whichresulted in a decline in the consumption of agrichemicals by cotton crop. However, off late therehave been few reports of Bt Cotton unable to develop immunity towards new type of pests.

Patent expiry of molecules: Agrichemicals are protected by patents to encourage innovationakin to the Pharmaceutical industry. Going ahead, many molecules are likely to go off patentthrowing the market open for generic players. As per estimates, total likely available opportunitythrough patent expiry stands at US $3.6bn.

19January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 19

Rallis India

Agrichemicals

Profit & Loss Statement (Consolidated) Rs croreY/E March FY2008 FY2009 FY2010E FY2011E

Net Sales 674.6 836.7 946.9 1,087.3

% chg 9.4 24.0 13.2 14.8

Total Expenditure 615.5 725.8 814.4 923.1

EBIDTA 59.1 110.9 132.6 164.2

(% of Net Sales) 8.8 13.3 14.0 15.1

Other Income 111.7 22.7 24.4 26.3

Depreciation& Amortisation 20.1 22.9 24.4 26.8

Interest 12.1 11.2 19.0 13.0

PBT 138.7 99.5 113.6 150.7

(% of Net Sales) 20.6 11.9 12.0 13.9

Tax 21.1 35.2 39.4 51.4

(% of PBT) 15.2 35.4 34.7 34.1

PAT 117.6 64.3 74.2 99.4

% chg 131.2 (45.3) 15.4 33.9

Exceptional item (Adj. for Tax) 74.0 0.0 0.0 0.0

Adj PAT( After Excp. item ) 43.6 64.3 74.2 99.4

Y/E March FY2008 FY2009 FY2010E FY2011E

SOURCES OF FUNDSEquity Share Capital 12.0 12.0 12.0 12.0Preference capital 88.0 88.0 0.0 0.0Reserves & Surplus 207.8 249.8 316.9 402.3Shareholders fund 307.8 349.7 328.9 414.3Total Loans 46.6 82.5 199.7 124.2Defered Tax Liability 0.0 0.0 0.0 0.0Minority Interest 0.0 0.0 0.0 0.0Total Liabilities 354.4 432.2 528.6 538.5APPLICATIONGross Block 296.0 337.7 339.3 484.3Less: Acc.Depreciation 161.4 179.1 203.4 230.2Net Block 134.6 158.6 135.8 254.1Capital Work-in-Progress 13.2 29.1 137.5 17.5Investments 55.5 136.2 98.5 98.5Current Assets 338.1 351.9 411.0 472.0Current liabilities 201.1 260.8 267.6 305.7Net Current Assets 137.1 91.1 143.4 166.3Misc exp 14.0 17.3 13.4 2.1Total Assets 354.4 432.2 528.6 538.5

Balance Sheet (Consolidated) Rs crore

Cash Flow Statement (Consolidated) Rs croreY/E March FY2008 FY2009 FY2010E FY2011E

Profit before tax 146.4 107.2 113.6 150.7

Depreciation & others (61.8) 32.9 43.4 39.7

Change in Working Capital (103.6) 40.3 (35.0) (23.0)

Direct taxes paid (25.9) (31.0) (34.6) (45.2)

Cashflow from operation (44.9) 139.1 87.3 122.2

(Inc)./ Dec. in Fixed Assets 63.3 (64.4) (110.0) (25.0)

Free Cash Flow 18.3 74.7 (22.7) 97.2

Inc./ (Dec.) in Investments (20.9) (77.9) (37.6) 0.0

Issue of Equity 0.0 0.0 (88.0) 0.0

Inc./(Dec.) in loans 10.7 36.6 117.2 (75.5)

Dividend Paid (Incl. Tax) (18.9) (30.2) (22.4) (7.0)

Others (4.3) (3.4) (19.0) (13.0)

Cash Flow from Financing(33.5) (74.8) (49.8) (95.5)

Inc./(Dec.) in Cash (15.1) (0.2) 2.7 1.7

Opening Cash balances 22.2 7.0 8.2 10.9

Closing Cash balances 8.4 8.2 10.9 12.6

Key Ratios

Y/E March FY2008 FY2009 FY2010E FY2011E

Per Share Data (Rs)EPS 36.4 53.6 61.9 82.9

Cash EPS 114.9 72.8 82.2 105.2

DPS 16.0 16.0 5.0 10.0

Book Value 183.4 218.4 274.5 345.7

Operating Ratio (%)Inventory (days) 79.9 65.1 70.0 70.0

Debtors (days) 55.1 50.6 51.0 51.0

Debt / Equity (x) 0.2 0.3 0.6 0.3

Returns (%)RoE* 16.6 19.6 21.9 26.7

RoCE 13.0 22.4 22.5 25.8

Dividend Payout 19.1 34.9 9.4 14.1

Valuation Ratio (x)P/E 20.2 13.7 11.9 8.9

P/E (Cash EPS) 6.4 10.1 8.9 7.0

P/BV 4.0 3.4 2.7 2.1

EV / Sales 1.3 1.0 1.0 0.8

EV / EBITDA 14.6 7.4 7.3 5.4

Note: * Adjusted for exceptional item.

20January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 20

Rallis India

Agrichemicals

DisclaimerThis document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons into whose possessionthis document may come are required to observe these restrictions.Opinion expressed is our current opinion as of the date appearing on this material only. While we endeavor to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change withoutnotice. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true and are for general guidance only. While everyeffort is made to ensure the accuracy and completeness of information contained, the company takes no guarantee and assumes no liability for any errors or omissions of the information. No one can usethe information as the basis for any claim, demand or cause of action.Recipients of this material should rely on their own investigations and take their own professional advice. Each recipient of this document should make such investigations as it deems necessary to arriveat an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determinethe merits and risks of such an investment. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide for future performance. Certain transactions- futures, options and other derivatives as well as non-investment grade securities - involve substantial risks and are not suitable for all investors. Reports based on technical analysis centers on studyingcharts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company's fundamentals.We do not undertake to advise you as to any change of our views expressed in this document. While we would endeavor to update the information herein on a reasonable basis, Angel Broking, its subsidiariesand associated companies, their directors and employees are under no obligation to update or keep the information current. Also there may be regulatory, compliance, or other reasons that may prevent AngelBroking and affiliates from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change without notice. Angel BrokingLimited and affiliates, including the analyst who has issued this report, may, on the date of this report, and from time to time, have long or short positions in, and buy or sell the securities of the companiesmentioned herein or engage in any other transaction involving such securities and earn brokerage or compensation or act as advisor or have other potential conflict of interest with respect to company/ies mentioned herein or inconsistent with any recommendation and related information and opinions.Angel Broking Limited and affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companiesreferred to in this report, as on the date of this report or in the past.

Buy (Upside > 15%) Accumulate (Upside upto 15%) Neutral (5 to -5%)Reduce (Downside upto 15%) Sell (Downside > 15%)

Ratings (Returns) :

Fund Management & Investment Advisory ( 022 - 3952 4568)P. Phani Sekhar Fund Manager - (PMS) [email protected] Bhamre Head - Derivatives and Investment Advisory [email protected] Mehta AVP - Investment Advisory [email protected] Team ( 022 - 3952 4568)Hitesh Agrawal Head - Research [email protected] Kour Nangra VP-Research, Pharmaceutical [email protected] Agrawal VP-Research, Banking [email protected] Jajoo Automobile [email protected] Shah IT, Telecom [email protected] Pareek Oil & Gas [email protected] Burde Metals & Mining, Cement [email protected] Solanki Power, Mid-cap [email protected] Kanani Infrastructure, Real Estate [email protected] Shah FMCG , Media [email protected] Bambha Capital Goods, Engineering [email protected] Dalmia Pharmaceutical [email protected] Desai Logistics [email protected] Bariya Fertiliser, Mid-cap [email protected] Nadkarni Retail [email protected] Vora Research Associate (Oil & Gas) [email protected] Waghmare Research Associate (Metals & Mining, Cement) [email protected] Mate Research Associate (Infra, Real Estate) [email protected] Srinivasan Research Associate (Power, Mid-cap) [email protected] Agrawal Jr. Derivative Analyst [email protected]

Amit Bagaria PMS [email protected] Wagle Chief Technical Analyst [email protected] Joshi AVP Technical Advisory Services [email protected] Ail Manager - Technical Advisory Services [email protected] Jagtap Sr. Technical Analyst [email protected] Sanghvi Sr. Technical Analyst [email protected] Vasudeo Technical Analyst [email protected] Dayma Derivative Analyst - (TAS) [email protected]

Sanket Padhye AVP Mutual Fund [email protected] Rathod Research Associate (MF) [email protected] Jangid Research Associate (MF) [email protected]

Commodities Research TeamAmar Singh Research Head (Commodities) [email protected] P Sr. Technical Analyst [email protected] Gupta Sr. Technical Analyst [email protected] Patki Sr. Technical Analyst [email protected] Chauhan Technical Analyst abhishek [email protected] Joshi Technical Analyst [email protected]

Commodities Research Team (Fundamentals)Badruddin Sr. Research Analyst (Agri) [email protected] Pote Research Analyst (Energy Complex) [email protected] Walia Research Analyst ( Base Metals) [email protected] Narvekar Research Analyst ( Agri) [email protected] Rao Research Analyst (Agri) [email protected]

Bharathi Shetty Research Editor [email protected] Adhyaru Assistant Research Editor [email protected] Patil Production [email protected]

Research & Investment Advisory: Acme Plaza, 3rd Floor ‘A’ wing, M.V. Road, Opp Sangam Cinema, Andheri (E), Mumbai - 400 059

21January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539July 20, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 21

Rallis India

Agrichemicals

Central Support & Registered Office:G-1, Akruti Trade Centre, Road No. 7, MIDC Marol, Andheri (E), Mumbai - 400 093 Tel : 2835 8800 / 3083 7700

Regional Offices:

Private Client Group Offices: Sub - Broker Marketing:

Branch Offices:

Andheri (W) - Tel: (022) 2635 2345 / 6668 0021

Bandra (W) - Tel: (022) 2655 5560 / 70

Andheri ( L o k h a n d w a l a ) - Te l : ( 0 2 2 ) 3 9 5 2 5 6 7 9

Bandra (W) - Tel: (022) 6643 2694 - 99

Borivali (W) - Tel: (022) 3952 4787

Borivali (Punjabi Lane) - Tel: (022) 3951 5700.

Chembur - (Basant) - Tel:(022) 022) 6156 1111 / 01

Kalbadevi - Tel: (022) 2243 5599 / 2242 5599

Kandivali (W) - Tel: (022) 2867 3800/2867 7032

Chembur - Tel: (022) 6703 0210 / 11 /12

Fort - Tel: (022) 3958 1887

Ghatkopar (E) - Tel: (022) 3955 8400/2510 1525

Malad (E) - Tel: (022) 2880 4440

Kandivali - Tel: (022) 4245 1300

Malad (Natraj Market) - Tel:(022) 28803453 / 24

Masjid Bander - Tel: (022) 2345 5130 /1 / 8 / 42 /28

Mulund (W) - Tel: (022) 2562 2282

Nerul - Tel: (022) 2771 9012 - 17

Sion - Tel: (022) 3952 7891

Powai (E) - Tel: (022) 3952 5887

Thane (W) - Tel: (022) 2539 0786 / 0650 / 1

Vashi - Tel: (022) 2765 4749 / 2251

Vile Parle (W) - Tel: (022) 2610 2894 / 95

Wadala - Tel: (022) 2414 0607 / 08

Agra - Tel: (0562) 4037200

Ahmedabad (Kalupur) - Tel: (079) 3041 4000 / 01

Ahmedabad (Maninagar) - Tel: (079) 3981 7430 / 1

Ajmer - Tel: (0145) 3941 394

Alwar - Tel: (0144) 3941 394 / 99833 60006

Ahmeda. (Bapu Nagar) - Tel : (079) 3091 6900 - 02

Ahmeda. (Gurukul) - Tel: (079) 3011 0800 / 01

Ahmedabad (C. G. Road) - Tel: (079) 4021 4023

Ahmedabad (Sabarmati) - Tel : (079) 3091 6100 / 01

Ahmedabad (Satellite) - Tel: (079) 4000 1000

Ahmedabad (Shahibaug) -Tel: (079)3091 6800 / 01

Amreli - Tel: (02792) 228 800/231039-42

Anand - Tel : (02692) 398 400 / 3

Amritsar - Tel: (0183) 3941 394

Indore - Tel: (0731) 4238 600

Jaipur - (Rajapark) Tel: (0141) 3057 900 / 99833 40004

Gandhinagar - Tel: (079) 4010 1010 - 31

Gajuwaka - Tel: (0891) 3987 100 - 30

Faridabad - Tel: (0129) 3984 000

Gandhidham - Tel: (02836) 237 135

Gondal - Tel: (02825) 398 200

Ghaziabad - Tel: (0120) 3980 800

Gurgaon - Tel: (0124) 3050 700

Himatnagar - Tel: (02772) 241 008 / 241 346

Hyderabad - A S Rao Nagar Tel: (040) 4222 2070-5

Hubli - Tel: (0836) 4267 500 - 22

Indore - Tel: (0731) 3049 400

Bhopal - Tel :(0755) 3941 394

Bikaner - Tel: (0151) 3941 394 / 98281 03988

Chandigarh - Tel: (0172) 3092 700

Deesa - Mobile: 97250 01160

Erode - Tel: (0424) 3982 600

Ankleshwar - Tel: (02646) 398 200

Baroda - Tel: (0265) 2226 103-04 / 6624 280

Baroda (Akota) - Tel: (0265) 2355 258 / 6499 286

Baroda (Manjalpur) - Tel: (0265) 6454280-3

Bhavnagar (Shastrinagar)- Mobile: 92275 32302

Bhavnagar - Tel: (0278) 3941 394

Bengaluru - Tel: (080) 4072 0800 - 29

Ahmeda. (Ramdevnagar) - Tel : (079) 4024 3842 / 43 Pune (Camp) - Tel: (020) 3092 1800

Pune - Tel: (020) 6640 8300 / 3052 3217

Rajamundhry - Tel: (0883) 3941 394

Rajkot (Ardella) Tel.: (0281) 2926 568

Rajkot (University Rd.) - Tel: (0281) 2331 418

Rajkot - (Bhakti Nagar) Tel: (0281) 2361 935

Rajkot - (Indira circle) Tel : 99258 84848

Rajkot (Orbit Plaza) - Tel: (0281) 3983 485

Rajkot (Pedak Rd) - Tel: (0281) 3985 100

Rajkot (Ring Road)- Mobile: 99245 99393

Surat (Ring Road) - Tel : (0261) 3071 600

Surendranagar - Tel : (02752) 223305

Udaipur - (0294) 3941 394

Valsad - Tel - (02632) 645 344 / 45

Vapi - Tel: (0260) 3941 394

Varachha - (0261) 3091 500

Secunderabad - Tel : (040) 3093 2600

Surat (Mahidharpura) - Tel: (0261) 3092 900

Surat - (Parle Point) - Tel : (0261) 3091 400

Vijayawada - Tel :(0866) 3984 600

Rajkot (Star Chambers) - Tel : (0281)3981 200

Rajkot - (Star Chambers) - Tel : (0281) 2225 401-3

Salem - Tel: (0427) 3941 394

Warangal - Tel: (0870) 3982 200

Varanasi - Tel: (0542) 2221 129, 3058 066

Nagaur - Tel: (01582) 244 648

Jamnagar (Cross Word) - Tel: (0288) 2751 118

Jamnagar(Indraprashta) - Tel: (0288) 3941 394

Jodhpur - Tel: (0291) 3941 394 / 99280 24321

Junagadh - Tel : (0285) 3941 3940

Keshod - Tel: (02871) 234 027 / 233 967

Kolkata (N. S. Rd) - Tel: (033) 3982 5050

Kolkata (P. A. Shah Rd) - Tel: (033) 3001 5100

Mehsana - Tel: (02762) 645 291 / 92

Kota - Tel : (0744) 3941 394

Mansarovar - Tel:(0141) 3057 700/99836 74600

Mysore - Tel: (0821) 4004 200 - 30

Nadiad - Tel : (0268) - 2527 230 / 34

New Delhi (Nehru Place) - Tel: (011) 3982 0900

New Delhi (Preet Vihar) - Tel: (011) 4310 6400

Palanpur - Tel: (02742) 308 060 - 63

Patel Nagar - Tel : (011) 45030 600

Patan - Tel: (02766) 222 306

Porbandar - Tel : (0286) 3941 394

Noida - Tel : (0120) 4639 900 / 1 / 9

Nashik - Tel: (0253) 3011 500 / 1 / 11

New Delhi (Bhikaji Cama) - Tel: (011) 41659711

New Delhi (Lawrence Rd.) - Tel: (011) 3262 8699 / 8799

New Delhi (Pitampura) - Tel: (011) 4751 8100

Porbandar (Kuber Life Style) - Mob.-98242 53737

Pune - Tel : (020) 3093 4400 / 3052 3217

Jamnagar (Moti Khawdi) - Tel: (0288) 2846 026

Jamnagar(Madhav Plaza) - Tel: (0288) 2665 708

Jalgaon - Tel: (0257) 2234 832

Pune (Aundh) - Tel: (020) 4104 1900

Mangalore - Tel: (0824) 3982 140

Kolhapur - Tel: (0231) 6632 000

Madurai Tel: (0452) 3941 394

Ahmedabad (C. G. Road) - Tel: (079) 3982 9934 Powai - Tel: (022) 3952 6500Rajkot (Race course) - Tel: (0281) 2490 847Surat - Tel: (0261) 3071 600

Ahmedabad - Tel: (079) 3941 3940

Bengaluru - Tel: (080) 3941 3940

Chennai - Tel: (044) 3941 3940

Hyderabad - Tel: (040) 3941 3940

Coimbatore - Tel: (0422) 3941 394

Cochin - Tel: (0484) 3941 394

Indore - Tel: (0731) 3941 394

Jaipur - Tel: (0141) 3941 394

Kanpur - Tel: (0512) 3941 394

Kolkata - Tel: (033) 3941 3940

Lucknow - Tel: (0522) 3941 394

Ludhiana - Tel: (0161) 3941 394

Mumbai (Powai) - Tel: (022)3952 6500

Pune - Tel: (020) 3941 3940

New Delhi - Tel: (011) 3941 3940

Nagpur - Tel: (0712) 3941 394

Nashik - Tel: (0253) 3941 394

Mumbai (Goregoan) Tel: (022) 2879 0411-15

Surat - Tel: (0261) 3941 394

Rajkot - Tel :(0281) 3941 394

Visakhapatnam - Tel :(0891) 3941 394

Corporate & Marketing Office : 612, Acme Plaza, M.V. Road, Opp Sangam Cinema, Andheri (E), Mumbai - 400 059 Tel : (022) 3952 7100 / 4000 3600NRI Helpdesk : e-mail : [email protected] Tel : (022) 4000 3622 / 4026 2700Investment Advisory Helpdesk : e-mail : [email protected] Tel : (022) 3958 4000Commodities : e-mail : [email protected] Tel : (022) 3081 7400PMS : e-mail : [email protected] Tel: (022) 3953 2800Feedback : e-mail : [email protected] Tel : (022) 2835 5000

Related Documents

![Comparing First, Second and Third Generation …...[2006], Gorton and Rouwenhorst [2006], Miffre and Rallis [2007], Fuertes, Miffre and Rallis [2010] amongst others). An easy way to](https://static.cupdf.com/doc/110x72/5e974b9ffaa92454ae3b4dab/comparing-first-second-and-third-generation-2006-gorton-and-rouwenhorst.jpg)