Rachel Coghlan, Misty Parkinson | Dec. 2014 U.S. Department of Education 2014 FSA Training Conference for Financial Aid Professionals Demonstrating Expected Family Contribution (EFC) Hand-Calculations Session 39

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Rachel Coghlan, Misty Parkinson | Dec. 2014

U.S. Department of Education

2014 FSA Training Conference for Financial Aid Professionals

Demonstrating Expected Family Contribution (EFC) Hand-Calculations

Session 39

Agenda

• Purpose of the Expected Family Contribution (EFC)• Formula calculation

• Six Types• Intermediate steps• Simplified Needs Test (SNT)• Auto Zero (AZ)

• Exercise – Formula 1• Review exercise• Overview of Formulas 2 - 6• Wrap Up

2

Purpose

• What is an EFC • An EFC is the calculated number determined based on information

reported on the FAFSA• The EFC along with other data is used by the school to determine a

student’s financial aid package

3

EFC Formulas

• There are six different formulas used to calculate an EFC. The following items will determine which formula is used:• Dependency• Meets Simplified Needs or Auto Zero• Number of Dependents

4

Simplified Needs/Auto Zero

• To qualify for simplified needs (SNT)• Dependent

• Any parent’s means benefit question is yes, OR• Parent is a dislocated worker, OR• Parents filed or were eligible to file a 1040A/1040EZ, filed a 1040 but

were not required to do so, or were not required to file any income tax return

AND• If tax filer, P. AGI is $49,999 or less• If non tax filer, Father’s plus Mother’s Income is $49,999 or less

5

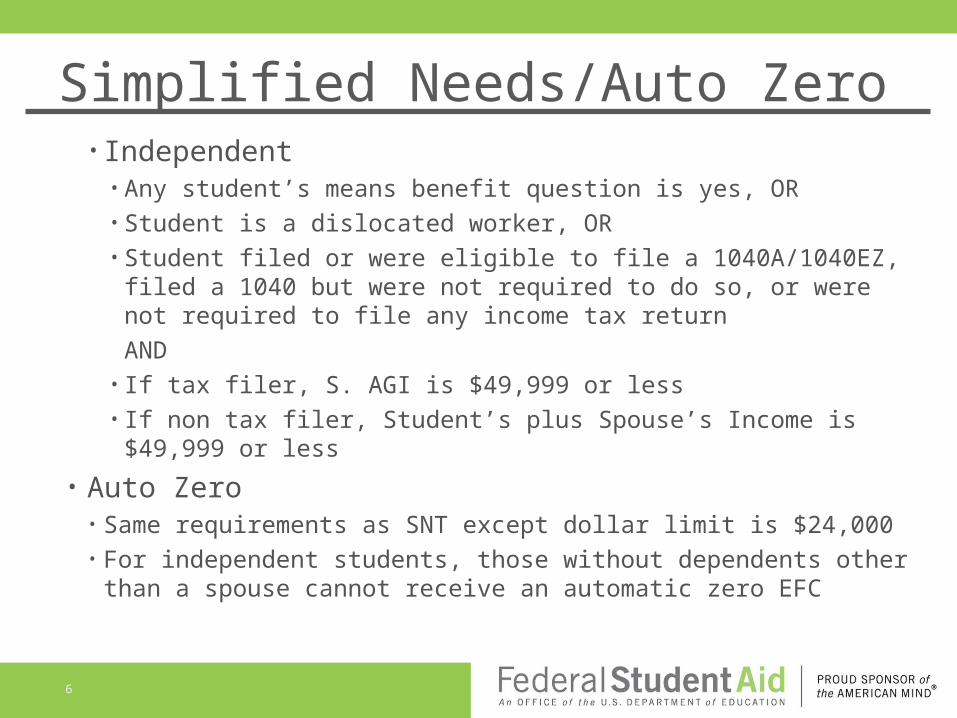

Simplified Needs/Auto Zero• Independent

• Any student’s means benefit question is yes, OR• Student is a dislocated worker, OR• Student filed or were eligible to file a 1040A/1040EZ, filed a 1040

but were not required to do so, or were not required to file any income tax return

AND• If tax filer, S. AGI is $49,999 or less• If non tax filer, Student’s plus Spouse’s Income is $49,999 or less

• Auto Zero• Same requirements as SNT except dollar limit is $24,000• For independent students, those without dependents other than a

spouse cannot receive an automatic zero EFC

6

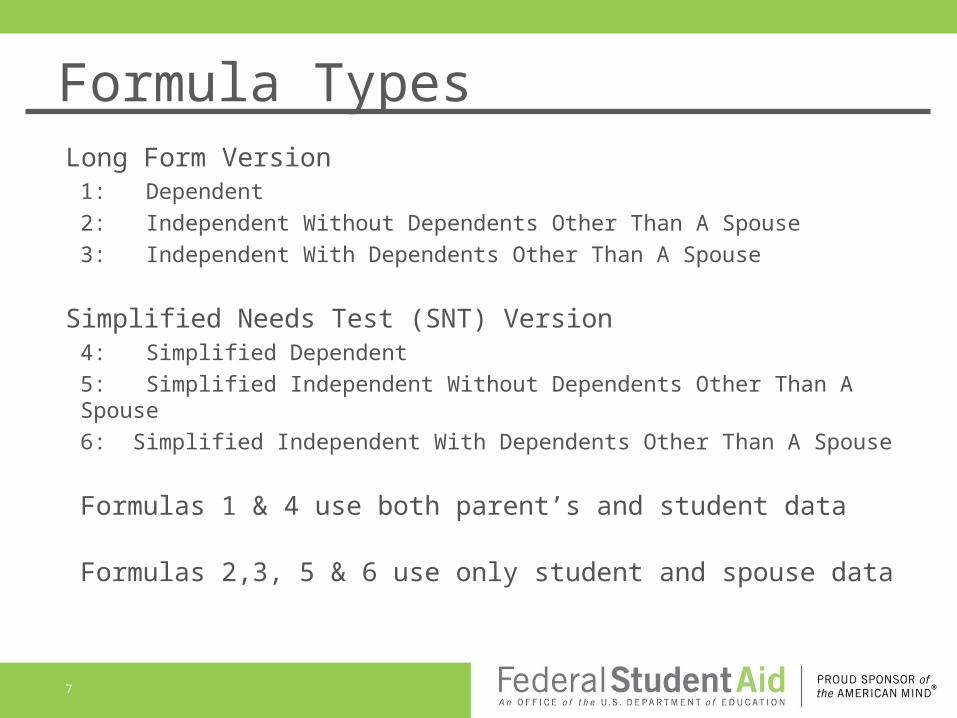

Formula TypesLong Form Version

1: Dependent

2: Independent Without Dependents Other Than A Spouse

3: Independent With Dependents Other Than A Spouse

Simplified Needs Test (SNT) Version4: Simplified Dependent

5: Simplified Independent Without Dependents Other Than A Spouse

6: Simplified Independent With Dependents Other Than A Spouse

Formulas 1 & 4 use both parent’s and student data

Formulas 2,3, 5 & 6 use only student and spouse data

7

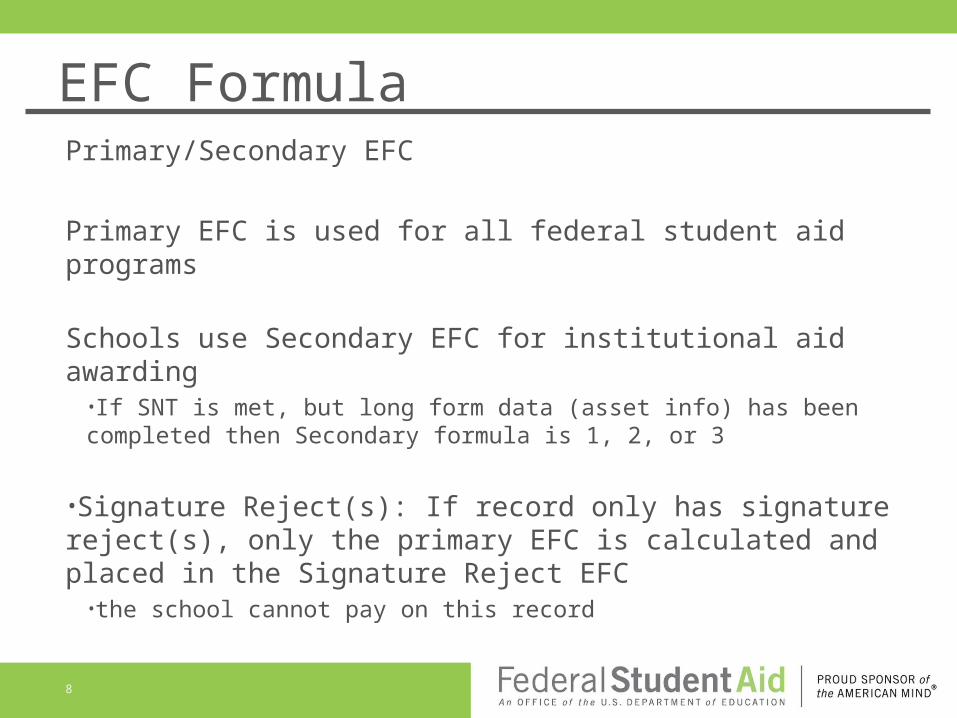

EFC FormulaPrimary/Secondary EFC

Primary EFC is used for all federal student aid programs

Schools use Secondary EFC for institutional aid awarding•If SNT is met, but long form data (asset info) has been completed then Secondary formula is 1, 2, or 3

•Signature Reject(s): If record only has signature reject(s), only the primary EFC is calculated and placed in the Signature Reject EFC

•the school cannot pay on this record

8

EFC Formula

• If record qualifies for Auto Zero EFC:• Primary EFC set to 0• If long form data is present no Secondary EFC is calculated

• Alternate EFCs• Eleven alternate EFCs are calculated for programs of shorter than

or longer than nine months• Displayed under EFC1, EFC2, EFC3…..

9

EFC Formula• Each formula uses FAFSA data such as: AGI, household

size, and number in college to calculate the EFC• Annually, information changes in the following tables:

• Income Protection Allowance• Adjusted Net Worth of a Business or Farm• Education Savings and Asset Protection Allowances• Assessment Schedule and Rates• Social Security Tax Tables

10

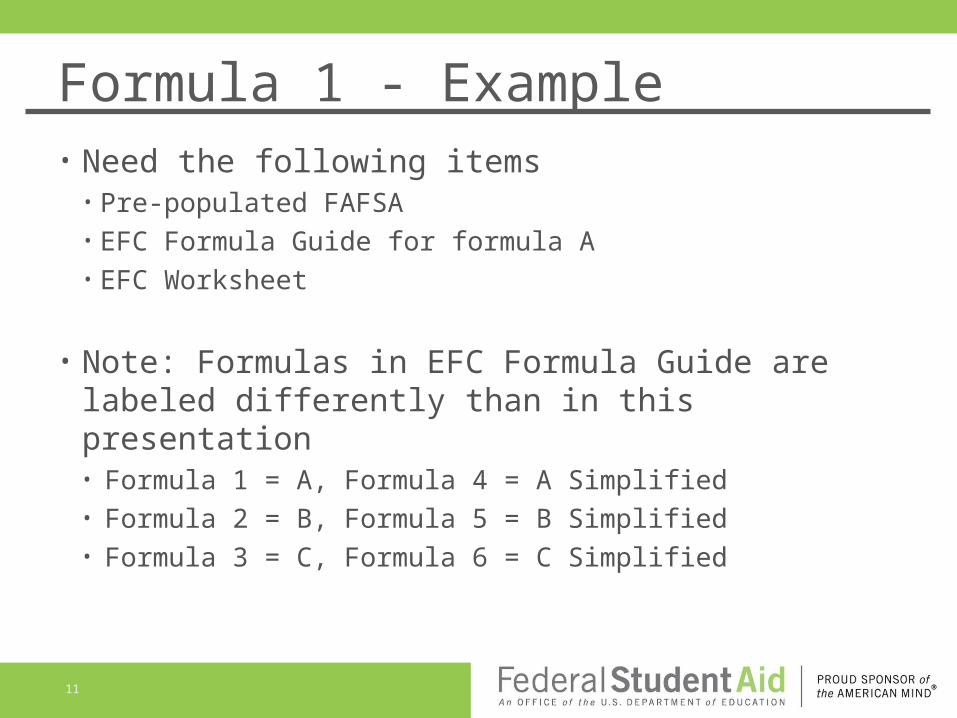

Formula 1 - Example• Need the following items

• Pre-populated FAFSA• EFC Formula Guide for formula A• EFC Worksheet

• Note: Formulas in EFC Formula Guide are labeled differently than in this presentation• Formula 1 = A, Formula 4 = A Simplified• Formula 2 = B, Formula 5 = B Simplified• Formula 3 = C, Formula 6 = C Simplified

11

Parent’s Income1 Par AGI (Field 85)

2a Parent 1 Income (Field 88)

2b Parent 2 Income (Field 89)

3 Par Taxable Income

4 Total Untaxed income (94a – 94i)

5 Taxable & Untaxable Income Lines 3 + 4

6 Total Add Fin Info (93a – 93f)

7 Total Income Line 5 – Line 6

49780

21780

20000

49780

3600

53380

0

53380

12

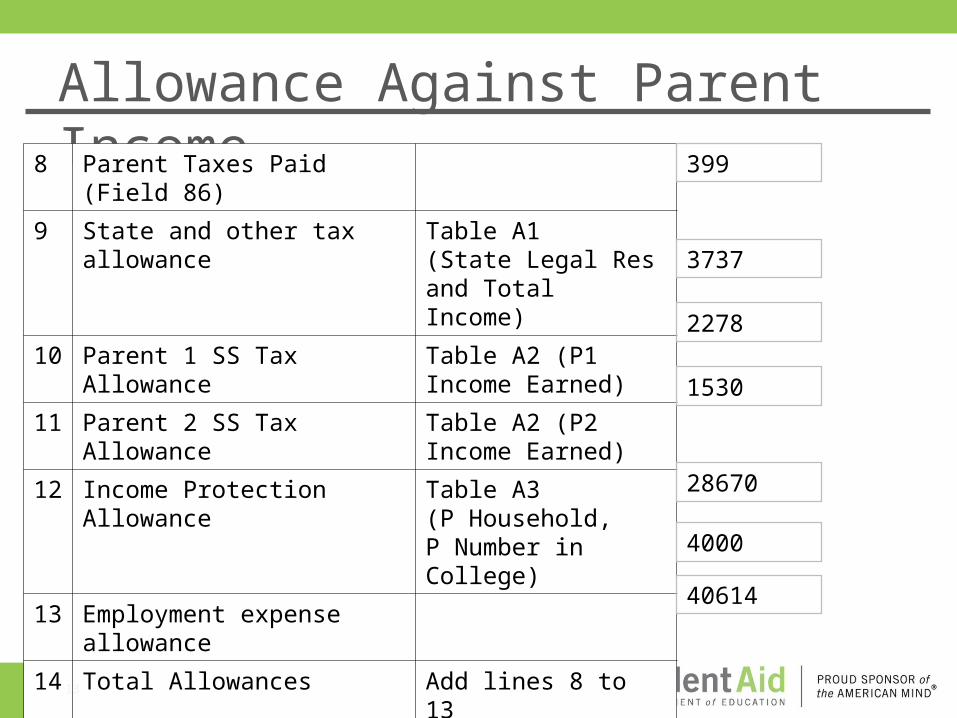

Allowance Against Parent Income8 Parent Taxes Paid (Field 86)

9 State and other tax allowance Table A1 (State Legal Res and Total Income)

10 Parent 1 SS Tax Allowance Table A2 (P1 Income Earned)

11 Parent 2 SS Tax Allowance Table A2 (P2 Income Earned)

12 Income Protection Allowance Table A3 (P Household, P Number in College)

13 Employment expense allowance

14 Total Allowances Add lines 8 to 13

3737

2278

1530

28670

4000

399

40614

13

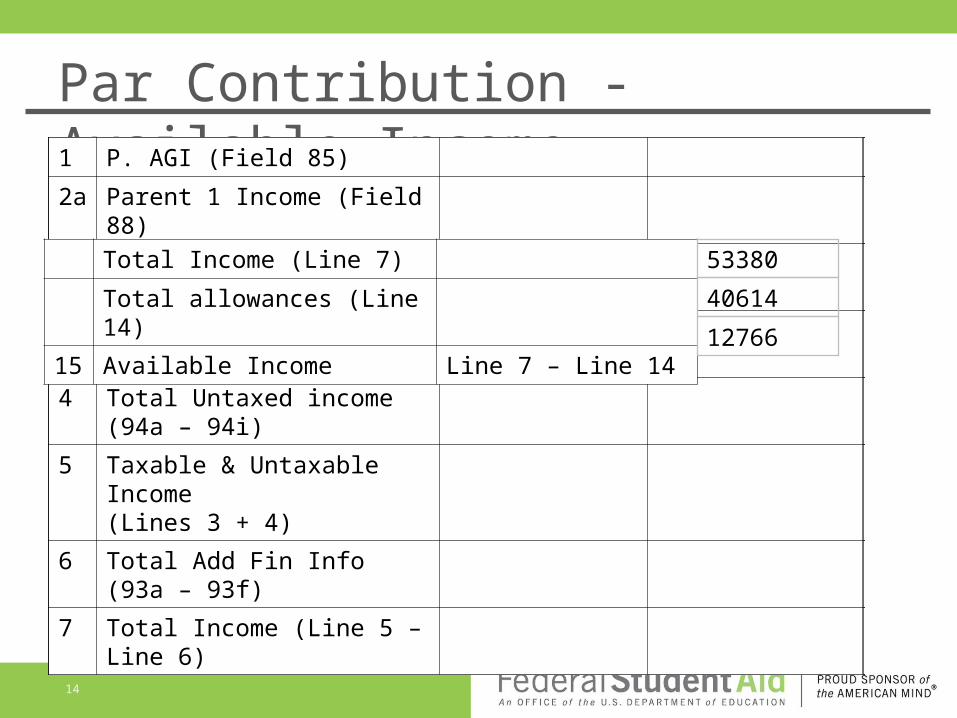

Par Contribution - Available Income1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88) 29780

2b Parent 2 Income (Field 89) 20000

3 Par Taxable Income

49780

4 Total Untaxed income (94a – 94i) 3600

5 Taxable & Untaxable Income (Lines 3 + 4)

53380

6 Total Add Fin Info (93a – 93f) 0

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88) 29780

2b Parent 2 Income (Field 89) 20000

3 Par Taxable Income

49780

4 Total Untaxed income (94a – 94i) 3600

5 Taxable & Untaxable Income (Lines 3 + 4)

53380

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88) 29780

2b Parent 2 Income (Field 89) 20000

3 Par Taxable Income

49780

4 Total Untaxed income (94a – 94i) 3600

5 Taxable & Untaxable Income (Lines 3 + 4)

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88) 29780

2b Parent 2 Income (Field 89) 20000

3 Par Taxable Income

4 Total Untaxed income (94a – 94i)

5 Taxable & Untaxable Income (Lines 3 + 4)

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88) 29780

2b Parent 2 Income (Field 89) 20000

3 Par Taxable Income

49780

4 Total Untaxed income (94a – 94i)

5 Taxable & Untaxable Income (Lines 3 + 4)

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85) 49780

2a Parent 1 Income (Field 88)

2b Parent 2 Income (Field 89)

3 Par Taxable Income

4 Total Untaxed income (94a – 94i)

5 Taxable & Untaxable Income (Lines 3 + 4)

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

1 P. AGI (Field 85)

2a Parent 1 Income (Field 88)

2b Parent 2 Income (Field 89)

3 Par Taxable Income

4 Total Untaxed income (94a – 94i)

5 Taxable & Untaxable Income (Lines 3 + 4)

6 Total Add Fin Info (93a – 93f)

7 Total Income (Line 5 – Line 6)

Total Income (Line 7)

Total allowances (Line 14)

15 Available Income Line 7 – Line 14

53380

40614

12766

14

Parent Contributions from Assets16 Parent Cash (Field 90)

17 Par Net Investment (Field 91)

18 Par Business/Farm (Field 92)

19 Adjusted Net Worth Bus/Farm Table A4 (P Bus/Farm)

20 Net Worth Add Lines 16, 17, 19

21 Asset Protection Allowance Table A5

22 Discretionary Net Worth Line 20 – Line 21

23 Asset conversion rate 12%

24 Contribution from assets

1790

1000

0

0

-4285 set to 0

-35710

38500

2790

15

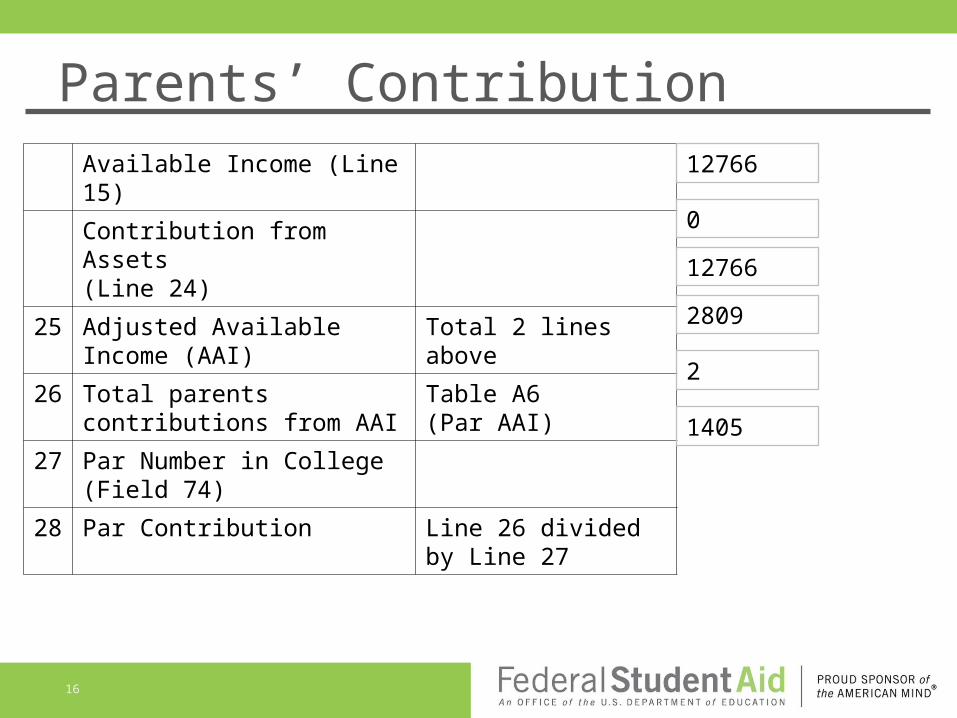

Parents’ ContributionAvailable Income (Line 15)

Contribution from Assets (Line 24)

25 Adjusted Available Income (AAI) Total 2 lines above

26 Total parents contributions from AAI

Table A6(Par AAI)

27 Par Number in College (Field 74)

28 Par Contribution Line 26 divided by Line 27

12766

1405

2

2809

12766

0

16

Student Income29 Student AGI (Field 36)

30 Student Income (Field 39)

31 Taxable Income Tax filer – Line 29Non filer – Line 30

32 Total Untaxed income (45a – 45j)

33 Taxable & Untaxable Income Lines 31 + 32

34 Total Add Fin Info (44a – 44f)

35 Total Income Line 33 – Line 34

1600

1550

1600

0

1600

0

1600

17

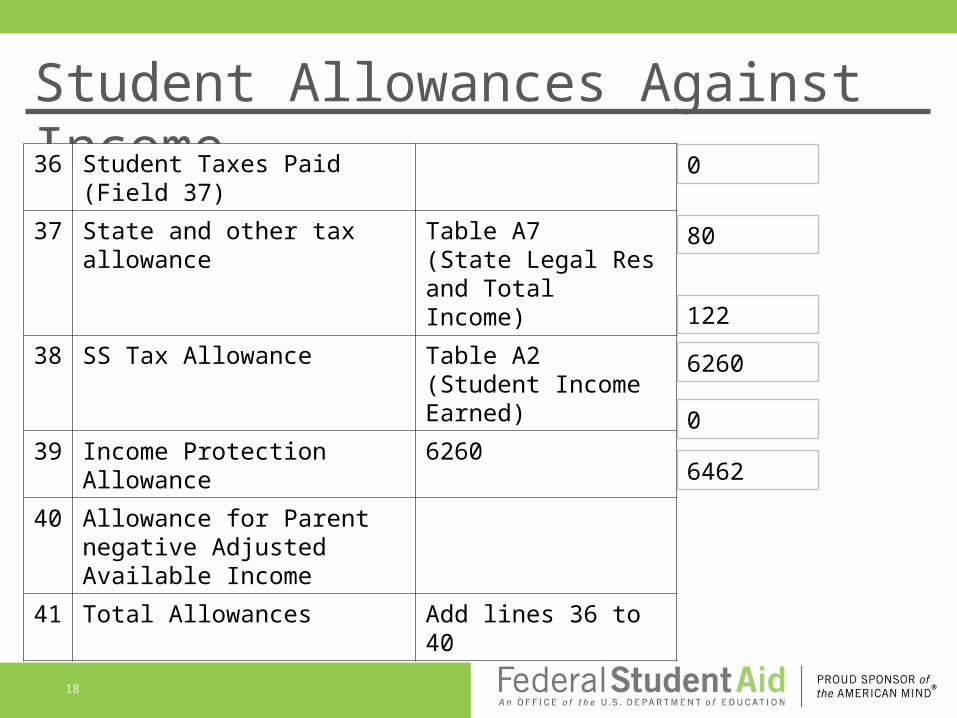

Student Allowances Against Income36 Student Taxes Paid (Field 37)

37 State and other tax allowance Table A7 (State Legal Res and Total Income)

38 SS Tax Allowance Table A2 (Student Income Earned)

39 Income Protection Allowance 6260

40 Allowance for Parent negative Adjusted Available Income

41 Total Allowances Add lines 36 to 40

0

80

122

6260

0

6462

18

Stu Contribution from Available Income

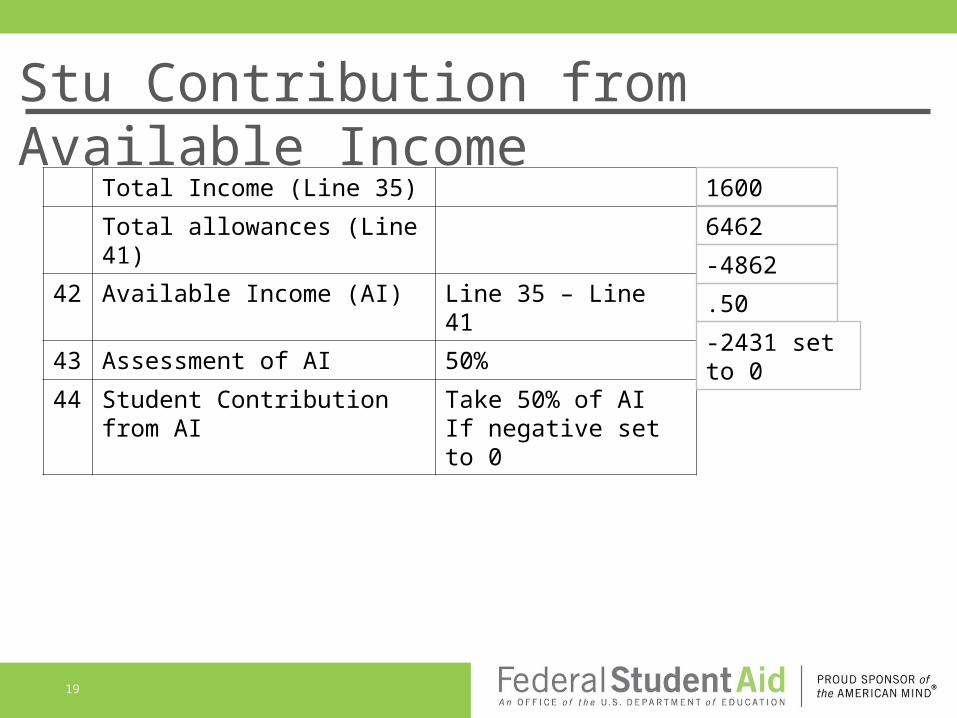

Total Income (Line 35)

Total allowances (Line 41)

42 Available Income (AI) Line 35 – Line 41

43 Assessment of AI 50%

44 Student Contribution from AI Take 50% of AIIf negative set to 0

1600

6462

-4862

.50

-2431 set to 0

19

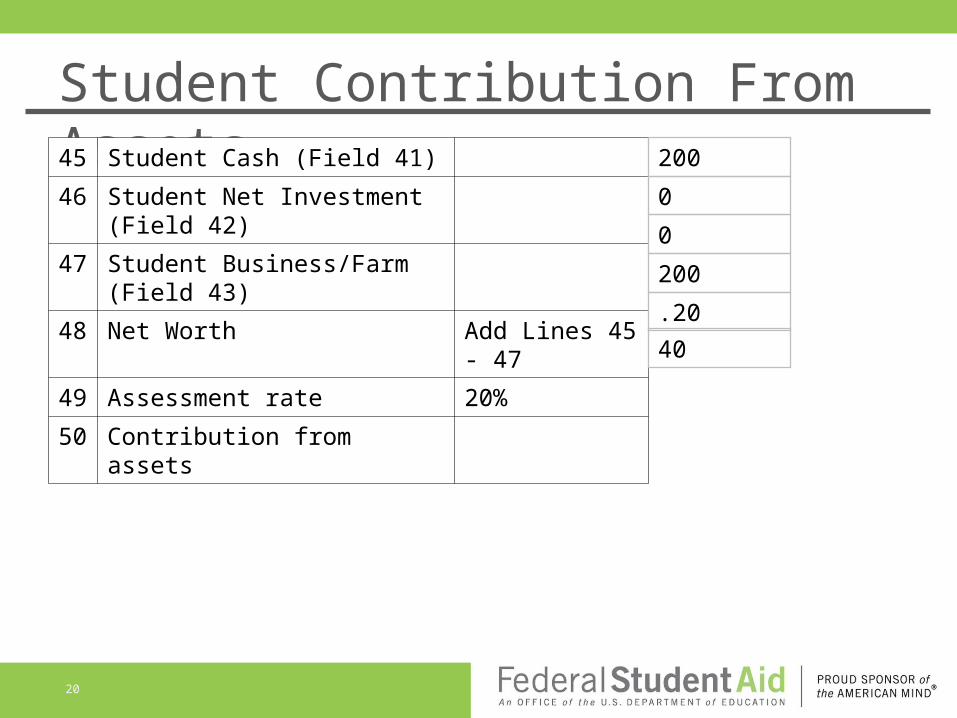

Student Contribution From Assets45 Student Cash (Field 41)

46 Student Net Investment (Field 42)

47 Student Business/Farm (Field 43)

48 Net Worth Add Lines 45 - 47

49 Assessment rate 20%

50 Contribution from assets

200

0

0

200

.20

40

20

Expected Family Contribution

Parents’ Contribution (Line 28)

Student Contribution from AI (Line 44)

Student Contribution from Assets (Line 50)

51 Expected Family Contribution Add Lines 28, 44 and 50

1405

0

40

1445

21

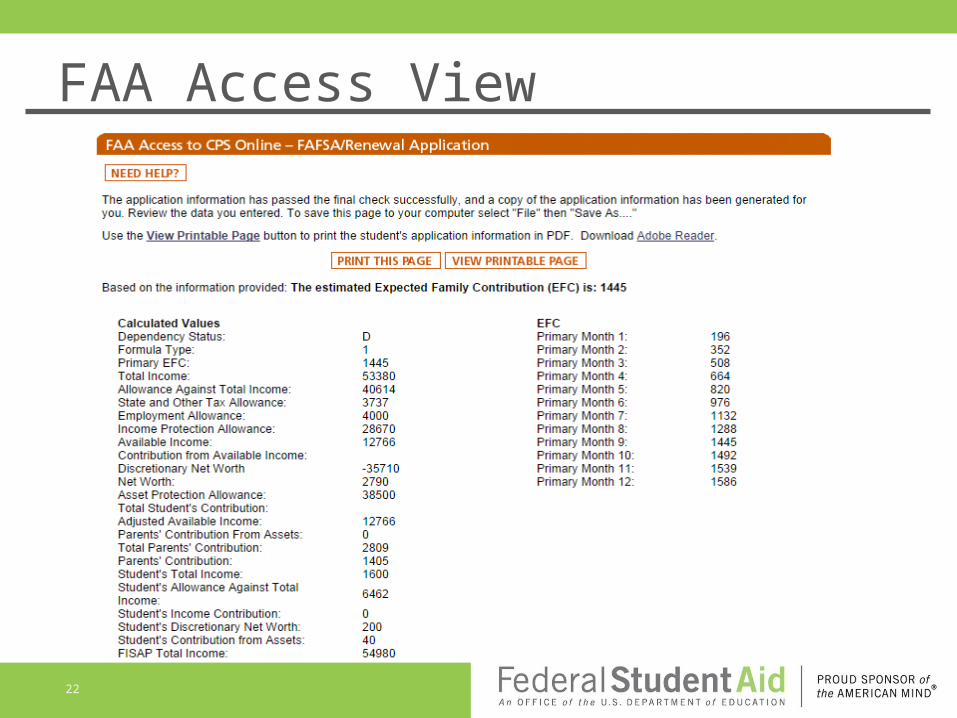

FAA Access View

22

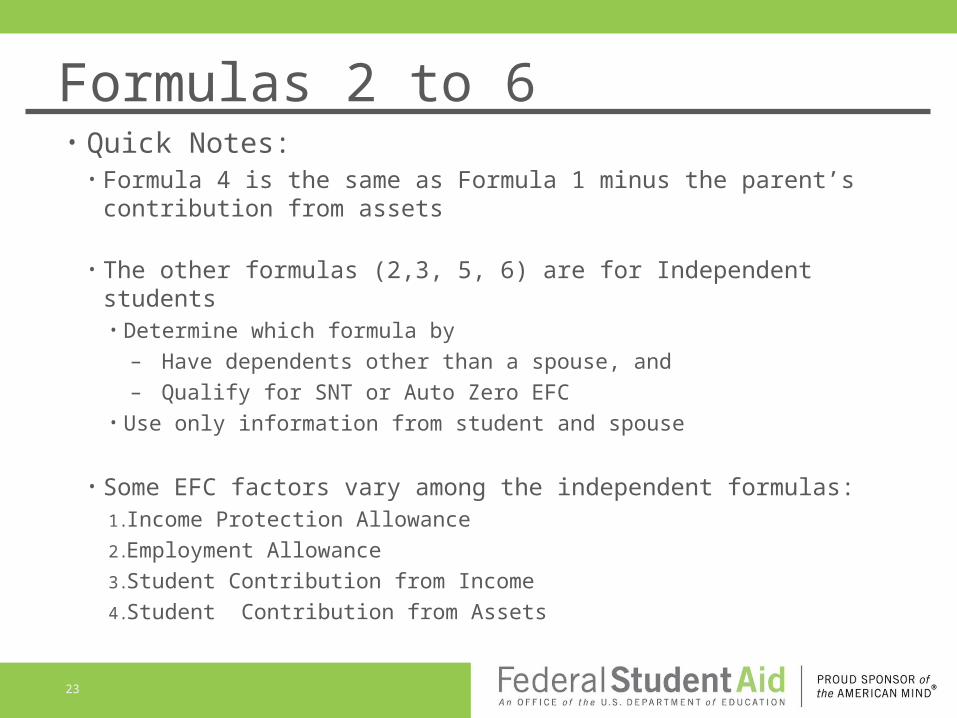

Formulas 2 to 6• Quick Notes:

• Formula 4 is the same as Formula 1 minus the parent’s contribution from assets

• The other formulas (2,3, 5, 6) are for Independent students• Determine which formula by

– Have dependents other than a spouse, and – Qualify for SNT or Auto Zero EFC

• Use only information from student and spouse

• Some EFC factors vary among the independent formulas:1.Income Protection Allowance

2.Employment Allowance

3.Student Contribution from Income

4.Student Contribution from Assets

23

References

• 14-15 EFC Guide:http://ifap.ed.gov/efcformulaguide/attachments/

091913EFCFormulaGuide1415.pdf

• 14-15 Financial Aid Handbook, Chapter 3:http://ifap.ed.gov/fsahandbook/attachments/1415AVGCh3.pdf

• 15-16 EFC Formula Table Federal Register Noticehttp://www.gpo.gov/fdsys/pkg/FR-2014-05-30/pdf/2014-12569.pdf

24

QUESTIONS?

25

Related Documents

![Clarinet in B Trio voor Klarinet , Altviool en piano files/Chamber/[Clarinet_Institute] Ostijn... · misty misty misty misty 3 3 Trio voor Klarinet , Altviool en piano Willy Ostyn](https://static.cupdf.com/doc/110x72/5ac4c16d7f8b9af91c8d36c3/clarinet-in-b-trio-voor-klarinet-altviool-en-clarinetinstitute-ostijnmisty.jpg)