QUARTERLY REPORT ON AGRI COMMODITIES APRIL TO JUNE 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

QUARTERLY REPORT ON

AGRI COMMODITIESAPRIL TO JUNE 2013

AGRI COMMODITIES APRIL TO JUNE 2013

2

India has many growing seasons due to prevalence of high/low temperature

through a long period.

Kharif crop refers to the planting, cultivation and harvesting of any domesticated

plant sown in the rainy (monsoon) season on the Asian subcontinent. Such crops

are planted for autumn harvest and may also be called the summer or monsoon

crop in India.

Kharif crops are usually sown with the beginning of the first rains in July, during the

south-west monsoon season. India the kharif season varies by crop and state, with

kharif starting at the earliest in May and ending at the latest in January, but is

popularly considered to start in June and to end in October. Crops which require

large quantities of water are cultivated during the Kharif season.

This season is also called as hot weather period / pre monsoon season. This period

is characterized by high temperature. The temperature is higher in north compared

south. March to May month is the summer season. The weather gets hotter steadily

from the beginning of March. April & May are the hottest months of the year. The

average temperature is 30-40C. The rainfall receives during this period are mainly

useful for preparatory cultivation. In this period hot wind blows & sometimes dust

storms also take place. Some time these dust storms create problems due to their

intensity for considerable period.

The main Kharif crops are :

1. Rice,

2. Sugar-cane,

3. Jute,

4. Cotton,

5. Tobacco,

6. Maize etc.

These crops cover 65% of total cultivated area.

Rabi crops or Rabi harvest refers to agricultural crops sown in winter and harvested

in the summer season. The term is derived from the Arabic word for "spring", which

is used in the Indian subcontinent. The Rabi crop is the spring harvest (also known

as the "winter crop") in Indian subcontinent.

The Rabi Season starts in the middle of October when the south-west monsoon

retreats and the north-east Monsoon begins. Seeds are sown in October and crops

are harvested in March and April. Generally, crops which require less water are

grown during the rabi season.

This season is called as cold weather period. January & February months are the

cold months in the most parts of the country. Temperature distribution over India

KHARIF CROP OR SUMMER CROP

RABI CROP OR WINTER CROP

OVERVIEW: CROPPING SEASONS IN INDIA

shows a marked decrease from south to north. In north India average temperature

during this season is about 10-15 degree and in south India is about 21-28 degree.

Weather during this period is cool, dry & pleasant with dew-fall during morning.

This period is practically rainless except occasional drizzles.

The main rabi crops are:

1. Wheat,

2. Barley,

3. Gram,

4. Mustard,

5. Linseed etc.

These crops require cooler conditions and less moisture Rabi crops account for

33% of cropped area.

There are certain crops which are grown throughout the year in all parts of the

country under artificial irrigation, they are called zaid crops.

The chief Zaid crops are :

1. Rice

2. Maize

3. Melons

4. Groundnut

5. Water melons

6. Cucumber

7. Leafy

8. Tuber vegetables etc.

For the large farming community of Punjab and Haryana, Baisakhi marks a New

Year's time as it is time to harvest rabi crop. On Baisakhi, farmers thank god for the

bountiful crop and pray for good times ahead. People buy new clothes and make

merry by singing, dancing and enjoying the best of festive food.

Everyday farming scenes of sowing, harvesting, winnowing and gathering of crops

are expressed through zestful movements of the body to the accompaniment of

ballads and dhol music.

In Assam in the northeastern part of India, a harvest festival called Bhogali Bihu is

celebrated to mark the end of the harvest season in mid-January. In southern parts

of India, particularly in Andhra Pradesh, Tamil Nadu and Mumbai, the Bhogi festival

is celebrated on the last day of 'Maarkali', which is also the first day of the farmer

festival Pongal.

ZAID CROP

SIGNIFICANCE OF CROP HARVESTING FOR FARMERS

AGRI COMMODITIES APRIL TO JUNE 2013

3

TYPES OF FARMING

Dry

Farming

Meaning Followed in States Crops growns

Humid

Farming

Irrigation

Farming

Shifting

Cultivation

Plantation

Farming

Single

Cropping

Double

Cropping

Multiple

Cropping

Arable

Farming

A system under which farming is carried on in the regions

where the rainfall is scanty i.e. less than 50 Cm annually

and where irrigation facilities are either absent or very

little.

A system of farming practised in regions where the rainfall

is adequate i.e. between 100 Cm to 200 Cm without the

help of irrigation.

A system of farming under which crops are grown with

the help of irrigation i.e. supply of water from rivers,

reservoirs, tanks, wells to land for cultivation in regions of

seasonal or low rainfall.

Its means the migratory subsistence farming. Under this

system, a plot of land is cultivated for a few years and

then, when the crop yield declines because of soil

exhaustion and the effects of pests and weeds, is

deserted for another area.

Plantation farming means the cultivation of a single cash

crop in plantations or estates on a large scale. The farming

is carried on with the help of technically advanced

methods of cultivation and tools.

Also known as mono-cropping or mono-culture is a

system of farming under which the cultivators grow one

crop from the lands during the year.

A system under which two crops are raised by the farmers

from the same plot of land during the year.

Multiple cropping is a system under which the farmer grown

more than two crops from the same plot of land during the

year. It is a highly intensive system of farming.

It is a system under which the farms are used only for the

cultivation of crops

The system of farming by which different crops are

alternately grown on the same land in a specific order.

Mixed cropping means the cultivation of more than one

crop simultaneously on the same piece of land. The two

crops are sown together but harvested at different times

because the growth period of the plants of the different

crop varies.

Crop

Rotation

Mixed

Cropping

Gujarat, Rajasthan, South Punjab,

Northern Maharashtra

West Coast, West Bengal, Parts of

Bihar, U.P and Assam.

Western U.P., Punjab, Haryana, Parts of

Bihar, Orissa, A.P., Tamil Nadu,

Karnataka etc.

Assam, Meghalaya, Nagaland, Manipur,

Tripura, Mizoram, Arunchal Pradesh,

Madhya Pradesh, Orissa and Andhra

Pradesh

Assam, West Bengal, Karnataka,

Kerala & Tamil Nadu

Assam, Darjeeling, Kerala

West Bengal, Kerala, Uttar Pradesh

Maharashtra, Uttar Pradesh, Madhya

Pradesh

Punjab, Rajasthan

Gujrat, Madhya Pradesh, Rajasthan

Gujrat, Maharashtra

Jowar and Bajra

Rice, Sugarcane, jute etc

Rice, sugarcane, cotton, wheat,

tobacco etc.

Rainfed rice, Maize, buck wheat, small

millets, root crops and vegetables

Coffee plantations, tea plantations,

rubber plantations

Tea, Coffee, etc.

Rice

Food crops and cash crops

Leguminous crops like pulses are

grown alternately with wheat, barley or

mustard

Early maturing crops are mixed with

groundnut, cotton or pulses which

mature late

Cotton, tobacco, vegetables

AGRI COMMODITIES APRIL TO JUNE 2013

4

CROPS HARVESTED IN APRIL – JUNE QUARTER

CHANA

INTRODUCTION

Chana (Gram) is one of the oldest pulses known and cultivated in Asia and Europe.

Chana is widely appreciated as health food. This light brown colored pulse is

considered to be a good source of protein and is also called by the name of

Garbanzo beans. Chana, also called Bengal gram or chick pea, is the premiere pulse

crop in the Indian subcontinent. India is the largest consumer and producer of

chana in the world. Chana is used as an edible seed and is also used for making

flour throughout the globe.

Having a capacity to stand in drought conditions, this crop doesn't have the

requirement of being fed with nitrogen fertilizers. There are basically two varieties of

chana (gram):

Desi Chana– These are spilt peas and are relatively smaller in size having a thicker

seed coat. They appear dark brown in color .

Kabuli Chana– Kabuli Chana has a whitish-cream color and are relatively bigger in

size having a thinner seed coat. They are generally used in soups /salads or as flour.

Chana is a Rabi crop sown during the winter months in India. Fertile sandy and loam

soil with good drainage is required for cultivation. Cooler climate and low rainfall

suits chana cultivation. Kabuli type is grown in temperate regions, while the desi

type chana is grown in the semi-arid tropics. India is the world largest pulses

producing country accounting for around 27-28% of world total pulses production.

Chana is the largest pulses produced around world accounting for 40% of pulses

production. India is the largest producer and consumer of chana in the world. Chana

is the most important of pulse crops grown in India, ranking fourth among the grain

crops in acreage and production.

Chana is planted in India during Rabi season i.e. in the months of October to

December and is harvested in February, March and April.

As it is sensitive to rainfall, an appropriate drainage system is required otherwise it

can hamper the yield levels of product. The peak arrival period begins from March-

April at the major trading centers of the country.

This crop is often cultivated as a sole crop but sometimes it is also grown

rotationally with other crops such as jowar, bajra, wheat and coriander.

CULTIVATION AND SEASONALITY

CROP CALENDAR

CHANA CROP CALENDAR

Country

India

Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

Harvesting Sowing

DOMESTIC SCENARIO

India is the largest producer of Chana in the world sharing 67% of the total world

production.

The major Chana growing States are Madhya Pradesh, Maharashtra, Rajasthan,

Uttar Pradesh and Andhra Pradesh. Madhya Pradesh is the largest producer of

Chana approx 47% of total production followed by Rajasthan, Uttar Pradesh and

Maharashtra.

47%

14%

12%

9%

6%4%

2%6%

CHANA PRODUCING STATES (2012-13e)

MP

Rajasthan

Uttar Pradesh

Maharashtra

Andhra Pradesh

Karnataka

Chatisghar

Others

MAJOR TRADING HUBS IN INDIA

MAJOR TRADING CENTRES - CHANA

AGRI COMMODITIES APRIL TO JUNE 2013

5

The major trading centres for chana in India are Indore, Mumbai, Delhi, Bikaner,

Hyderabad, Latur, Akola, Kanpur, Chennai and Jaipur. Indore is the major market for

chana, which along with Akola, Latur etc set prices for this commodity.

According to advance Estimates released Total pulses output for 2012-13 season

has been pegged at 17.58 mn tn, down 3.3% compared to previous year. There has

been a sharp increase in the chana output estimates on the back of higher acreage

and good yield.

Chana Production is expected to rise to 8.57 million tonnes for 2013-14 compare to

last year of 7.9million tonnes due to increased in area under cultivation and

favorable weather condition. India's production depends upon the monsoon rains

and the moisture availability in the soil since most of the area under this crop falls

under rain fed regions.

DEMAND SUPPLY FUNDAMENTALS

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-

14*

0

1

2

3

4

5

6

7

8

9

5.47 5.66.33

5.757.06 7.48 8.25

7.58 7.98.57

CHANA PRODUCTION IN INDIA

Source:Ministry of Agriculture

Fig

in M

illio

ns T

onn

es

CHANA AREA AND YIELD

Years Area ( in 000 ha ) Yield(in Kg /ha)

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13*

6710

6930

7490

7540

7893

8210

9668

8960

9320

815

808

845

762

895

915

895

912

-

YIELD & AREA OF CHANA

Indian chana yield is in the range of 800 to 900 kg per hectare from 2004-05 to

2011-12. Due to its dependence of monsoon rain, as most of the chana growing

area falls under rainfed conditions, its yield fluctuates.

MINIMUM SUPPORT PRICE (MSP)

Government timely revises Minimum Support Prices (MSP) on timely basis to

encourage farmer to grow more of the crop and also to keep in line with cost of

production. The Minimum Support Price (MSP) for Chana (Gram) is rising

continuously. The main reason behind this move of Government is to encourage the

farmers to enhance the output. The MSP of Chana is increased to Rs 3,000 per

quintal for the 2013-14 marketing year from Rs 2,800 per quintal in the marketing

year 2012-13. This should also encourage farmers mainly in Rajasthan to go for

Chana sowing.

As per the latest release of Department of Commerce (GOI), imports of chickpea for

the current year have risen over the previous year. As also, depreciation in Indian rupee

has resulted in costlier imports which in turn have made domestic pulses prices dearer.

IMPORT AND EXPORT OF CHANA FROM INDIA

2007-08 2008-09 2009-2010 2010-2011 2011-12

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.150.20

0.34

0.10

0.20

0.160.13

0.10

0.20

0.06

INDIA CHANA EXPORTS & IMPORTS

YEARS

IMPORT

EXPORT

FIG

IN

MIL

LIO

NS

TO

NN

ES

Being largest producer and consumer of chana, India also imports chana from

Australia, Canada, Turkey and Myanmar while it exports kabuli chana to US, UK,

Saudi Arabia and UAE. The exports of chana are declining gradually after imposition

of export ban in June 2006. However, kabuli chana is exported as it is exempted

from the ban.

The current chana crop is higher by about 15 per cent over last year. This may lead

to lower imports at around 3 mt in 2013-14,said by President, India Pulses and

Grains Association.

NAME TREND CMP SUPPORT KEY LEVELS RESISTANCE

S1 S2 S3 R1 R2 R3

CHANA BULLISH 3439 3330 3210 3050 3520 3710 3960 4175

AGRI COMMODITIES APRIL TO JUNE 2013

6

CHANA TRADING SPECIFICATIONS

Spot Market Trading Futures Market Trading

Bags/Pack Size Quotation/Base Value Delivery Center Unit of trading Quotation/Base Value Delivery Center

100,60,50 kg at Delhi,

Bikaner & 90,60,50 kg

at Indore

Rs/Quintal Indore,Delhi Bikaner 100 MT Rs/Quintal Indore,Delhi Bikaner

CHANA STOCK LIMIT

State

Maharashtra

Rajasthan

Delhi

Retailer

5

3

5

Wholesaler/

Stockist

50

100

200

Current Stock Limit (in Tons)

Government regularly takes measures to control the rising pulses prices by

imports, imposing stock limits and moral persuasion. Central government imposes

the stock limits with the help of state government and looking at the production and

stock availability of various states the stock limits are decided by the states.

Different limits are applicable for wholesaler and retailers.

GLOBAL SCENARIO

69%

8%

3%

3%

3%

2%

2%2%

2%6%

CHANA MAJOR PRODUCING COUNTRIES

2012-13e

India

Turkey

Iran

Mexico

Pakistan

Ethopia

Canada

Australia

Myanmar

Others

Chana is produced in various countries across the countries. India is the largest

producer (around 70%) in the world. India is also the largest consumer of chana

accounting for 88-90% of world's consumption. Canada and Australia though

produce just 2% of world's crop they are among the major exporter mainly on

account of limited consumption. Pakistan produces around 2% and consumes 90%

of its production.

Chana can withstand moisture stress to a certain extent. However, the

production highly fluctuates between years, depending on the rains received

and the moisture availability in the soil.

The sentiments of traders play a significant role currently, as a consequence of

the lack of free-flow of information.

Stocks present with stockists and the stocks-to-consumption ratio.

MARKET INFLUENCING FACTORS

•

•

•

TRADING SPECIFICATIONS OF CHANA

•

•

•

•

CURRENT FUNDAMENTALS DRIVING THE MARKETS

•

•

•

•

•

•

•

•

•

OUTLOOK

Imports and the crop situation in the countries from where imports originate,

viz., Canada, Australia, Myanmar.

Obstruction in the information movement

Prices of the other competitive pulses produced

Black-marketing and hoarding

Expectations of higher output this season against restricted buying further

influenced the prices.

The current chana crop is higher by about 15 per cent over last year. This may

lead to lower imports at around 3 mt in 2013-14.

The Government has been trying to encourage production of pulses, but the

efforts have not paid off significantly. The Commission for Agriculture Costs

and Prices (CACP) has suggested to the Government to levy 10 per cent import

duty on pulses and open up exports to encourage domestic production.

Presently, there is no import duty on pulses, while exports of many varieties are

banned. CACP believes that imposing 10 per cent duty on imports would

enhance domestic output by attracting more irrigated areas under pulses.

Indirectly, such a move would result in saving on fertiliser subsidy as pulses are

nitrogen fixing and help towards stabilising production.

Supplies from the new crop have started arriving in Andhra Pradesh,

Karnataka, Maharashtra and Madhya Pradesh, and are likely to rise further.

Meanwhile, chana sown area surged to 93.20 lakh ha. as compared from

89.60 lakh ha. in last year.

However, expectations of higher output and rising arrivals from the new season

crop in the physical market restricted the gains.

According to IBIS, imports of chana in the month of February declined to 0.46

lakh metric tonnes compared to 2.31 lakh metric tonnes during the previous

month.

Agriculture Canada forecasts exports of chickpeas will reach 60,000 MT this

season and 65,000 MT in the coming marketing year.

Chana is expected to continue to trade in the range to lower in coming 2-3 weeks

tracking increasing arrivals of the new crop coupled with higher imports. However,

sharp downside may be capped as demand will emerge at lower levels. Also, prices

may not sustain below Rs 3020 as farmers will not liquidate their produce below

these levels. Technically, on break and close below Rs. 3100 prices could come

down to 2800 to 2650.

AGRI COMMODITIES APRIL TO JUNE 2013

7

RICE

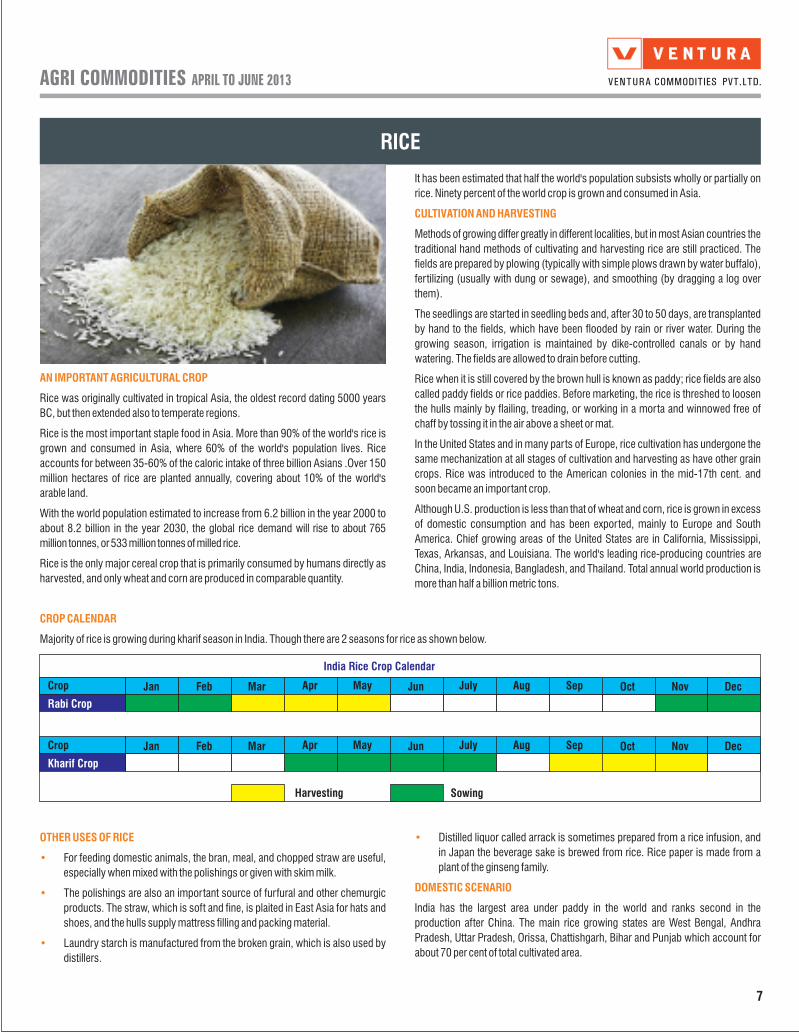

AN IMPORTANT AGRICULTURAL CROP

Rice was originally cultivated in tropical Asia, the oldest record dating 5000 years

BC, but then extended also to temperate regions.

Rice is the most important staple food in Asia. More than 90% of the world's rice is

grown and consumed in Asia, where 60% of the world's population lives. Rice

accounts for between 35-60% of the caloric intake of three billion Asians .Over 150

million hectares of rice are planted annually, covering about 10% of the world's

arable land.

With the world population estimated to increase from 6.2 billion in the year 2000 to

about 8.2 billion in the year 2030, the global rice demand will rise to about 765

million tonnes, or 533 million tonnes of milled rice.

Rice is the only major cereal crop that is primarily consumed by humans directly as

harvested, and only wheat and corn are produced in comparable quantity.

It has been estimated that half the world's population subsists wholly or partially on

rice. Ninety percent of the world crop is grown and consumed in Asia.

Methods of growing differ greatly in different localities, but in most Asian countries the

traditional hand methods of cultivating and harvesting rice are still practiced. The

fields are prepared by plowing (typically with simple plows drawn by water buffalo),

fertilizing (usually with dung or sewage), and smoothing (by dragging a log over

them).

The seedlings are started in seedling beds and, after 30 to 50 days, are transplanted

by hand to the fields, which have been flooded by rain or river water. During the

growing season, irrigation is maintained by dike-controlled canals or by hand

watering. The fields are allowed to drain before cutting.

Rice when it is still covered by the brown hull is known as paddy; rice fields are also

called paddy fields or rice paddies. Before marketing, the rice is threshed to loosen

the hulls mainly by flailing, treading, or working in a morta and winnowed free of

chaff by tossing it in the air above a sheet or mat.

In the United States and in many parts of Europe, rice cultivation has undergone the

same mechanization at all stages of cultivation and harvesting as have other grain

crops. Rice was introduced to the American colonies in the mid-17th cent. and

soon became an important crop.

Although U.S. production is less than that of wheat and corn, rice is grown in excess

of domestic consumption and has been exported, mainly to Europe and South

America. Chief growing areas of the United States are in California, Mississippi,

Texas, Arkansas, and Louisiana. The world's leading rice-producing countries are

China, India, Indonesia, Bangladesh, and Thailand. Total annual world production is

more than half a billion metric tons.

CULTIVATION AND HARVESTING

CROP CALENDAR

Majority of rice is growing during kharif season in India. Though there are 2 seasons for rice as shown below.

OTHER USES OF RICE

•

•

•

For feeding domestic animals, the bran, meal, and chopped straw are useful,

especially when mixed with the polishings or given with skim milk.

The polishings are also an important source of furfural and other chemurgic

products. The straw, which is soft and fine, is plaited in East Asia for hats and

shoes, and the hulls supply mattress filling and packing material.

Laundry starch is manufactured from the broken grain, which is also used by

distillers.

•

DOMESTIC SCENARIO

Distilled liquor called arrack is sometimes prepared from a rice infusion, and

in Japan the beverage sake is brewed from rice. Rice paper is made from a

plant of the ginseng family.

India has the largest area under paddy in the world and ranks second in the

production after China. The main rice growing states are West Bengal, Andhra

Pradesh, Uttar Pradesh, Orissa, Chattishgarh, Bihar and Punjab which account for

about 70 per cent of total cultivated area.

India Rice Crop Calendar

Crop Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

Harvesting Sowing

Rabi Crop

Crop Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

Kharif Crop

AGRI COMMODITIES APRIL TO JUNE 2013

8

West Bengal

Andhra Pradesh

Uttar Pradesh

Punjab

Orissa

Others

15.8

12.71

11.9110.86 7.31

41.41

Major Rice Producing States (2012-13e)

% Production to All India

India is one of the world's largest producer of rice, accounting for 20% of all world

rice production..

The India's rice production reached to a record high of 100 million tonnes in 2012-

13 crop-year.

RICE AREA AND YIELD

Years Area (in 000 ha) Yield(Rough MT/hec)

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13e

42300

43400

44000

43770

45400

41850

44000

44500

43000

2.95

3.17

3.18

3.31

3.28

3.19

3.25

3.27

3.52

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13e

0

20000

40000

60000

80000

100000

120000

83130 9179093350

9669099180

89090 95300 105310

101000

RICE PRODUCTION IN INDIA

YearsFig in 000 Tonnes

COMPARISON OF RICE BALANCE SHEET

Fundamentals

Beginning stocks

Production

Imports

Consumption

Exports

Total Supply

Ending Stocks

2012-2013e

25226

101000

-

95000

7600

126226

23626

2011-12

23500

105310

-

93334

10250

128810

25226

Rice Balance Sheet 2011-12 & 2012-2013e – India (in '000' tonnes)

MINIMUM SUPPORT PRICE (MSP)

The MSP for RICE has been increased to Rs 1,250 per quintal from Rs 1,080 in the

previous year. Higher MSP has been announced to give better returns to paddy

farmers, whose cost of cultivation has risen substantially due to rise in cost of labor,

power and fertilizer.

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

0

200

400

600

800

1000

1200

1400

630 640700

850

10001080 1100 1080

1250

RICE MSP

Years

Rs/

Qui

ntal

DEMAND SUPPLY FUNDAMENTALS

MONTHLY RICE ARRIVALS 2012 Vs 2013

SPOT MARKET TRADING SPECIFICATIONS

Commodity Bags/Pack SizeQuotation / Base Value

Types of Rice export by India

Rice Rs/Quintal

Parboiled rice Basmati RiceWhite Rice

Long Grain Yellow RiceIR-64 RiceRaw Rice

50Kg in Haryana, Punjab,

Sirsa,70 Kg in Wrangle & 35 Kg

in Khamanon

AGRI COMMODITIES APRIL TO JUNE 2013

9

GLOBAL SCENARIO

Rice is a food staple worldwide and China is the world's leading rice producing

country, producing just over one-third (33.9%) of the world's rice supply. India is

the world's second largest producer and exporter. Among the exporting countries,

Thailand, Vietnam, India and Pakistan are the major countries exporting rice in size

able quantity.

143000

101000 3690034000

27710

20500

104961

Major Rice Producing Countries (2012-13e)

Figures in 000' MT

China

India

Indonesia

Bangladesh

Vietnam

Thailand

Others

RICE EXPORTS FROM INDIA

Total rice exports in 2012-13 drop 29 per cent less than last year, as Indian

exporters are slowly raising prices.

Gulf region remains the major markets for Indian basmati rice and inside Gulf, Saudi

Arabia accounts for the major chunk of basmati imports from India.

Major destinations for India's non-basmati rice exports are Bangladesh, Australia,

Bahrain, Ethiopia, Djibouti, France, Germany, U.K., Hong Kong, Korea, Sri-Lanka,

Maldives, Mauritius, Malaysia, Nigeria etc.

However, with a bumper harvest in excess of 100 mt in 2011-12 and record stocks

of a little over 34 mt in state-run warehouses, India will continue to remain a major

player in the global market till at least June 2013, even if on a lower scale than 2011-

12.

2004-052005-06

2006-072007-08

2008-092009-10

2010-112011-12

2012-13e

0

2000

4000

6000

8000

10000

12000

45694688 5740

4654

21492228

4637

10250

7600

EXPORTS OF RICE FROM INDIA

YEARSSource:USDA

Fig

in 0

00 T

onnes

MARKET INFLUENCING FACTORS

Weather:

Minimum Support Price:

Role of weather in rice production is immense. Temperature, rainfall and

soil moisture are the important parameters that determine the crop condition.

Further, natural calamities can also affect crops. Markets keep watch of these

developments.

Changes in the minimum support prices (MSP) by the

government also have immense impact on the price of rice.

Government policies:

Substitute Product:

Consumption:

Seasonal cycles:

Demand:

CURRENT FUNDAMENTALS DRIVING THE MARKETS

•

•

•

•

OUTLOOK

Exchange rates, Fiscal policies, Export incentives and

export promotion also influence price.

Availability of substitute products at cheaper rate may lead to

weakness in demand. This situation happens especially when the main products

price tends to become higher.

Rice consumption depends on two factors - population and Income.

Let's take for example Asia. Rice is the staple food of Asia. Low-income groups

consume more rice according to the per capita income increase. But as the income

increases, there arrives a point when the consumption starts to dip. Income growth

and reduction in population result in a low consumption of rice.

Seasonal cycles are present in rice cultivation. Price tends to be

lower as harvesting progresses and produce starts coming into the market. At the

time of sowing and before harvesting price tends to rise in view of tight supply

situation.

Export demands as well as domestic demand.

Rice export of India 74.67 lakh tons during April-December 2012 against

71.75 lakh tons in the full fiscal year of 2011-12.

As the export price of Indian rice was more competitive than the Thai rice,

India has displaced Thailand from the position of top exporter of rice during

2011-12,” said Minister of State Commerce and Industry D Purandeswari.

The export performance of both the countries in coming years would depend

upon quantum of production of rice in India and Thailand as also the overall

global supply scenario and other nuances of internal trade in agricultural

commodities.

In the global market, the 2012/13 world production forecast was raised 2.3

million tons to a record 468.1 million tons, with productions forecasts raised

for Cambodia, India, and Peru.

Last year, India became the world's largest rice exporter for the first time in recorded

history, helped by consecutive bumper harvests and a huge surplus accumulated

due to three-year ban on rice exports. The country exported around 10.4 million

tons of rice (including 3.48 million tons basmati, and 6.9 million tons non-basmati)

in 2011-12. However, India's rice exports are likely to drop about 20-30% in 2013

due to higher domestic prices and bumper crop in the international market.

AGRI COMMODITIES APRIL TO JUNE 2013

10

RAPE / MUSTARD SEED

INTRODUCTION

Mustard seeds are yellowish colored, small seeds that are used as a spice in many

countries. These seeds are obtained from bush like mustard plant that belongs to

the genus Brassica that also include vegetables like cabbage and turnips.

CROP CALENDAR

The crop starts flowering in the months of December, January and February. The harvesting period is from March to May. It needs a right proportion of rainfall that is provided

by the monsoon during the sowing seasons of the crop. The rapeseed/mustard crop is actually acts as a very good cover of soil in winters.

Rapeseed belongs to the plant of the same genus and also known as canola in many

countries. In old English, rapum is a name of the present day turnip and the name

rapeseed is derived from rapum only.

Mustard seed and rapeseed have great importance in many countries as spices.

But, these seeds have important by-products too. Rapeseeds and mustard seeds

are sources of rapeseed/mustard seed oil and oilcake. Yellow colored oil is obtained

by extraction process of the crushed rape/mustard seeds. In the market, rape oil is

not distinguished from mustard oil as both of these come from the same species

and possess same properties.

During the production of oil, pressed cakes of the seeds are left over that have some

amount of oil content. These cakes are distilled to make oil cakes, which serves as

an animal feed. In the production process, around 37% oil is yielded and the rest is

oil cake.

Mustard/Rapeseed cultivation is done widely throughout the world. It is basically a

winter crop and it requires a temperate climate to prosper. The planting season or

the sowing period in India is during the Rabi season i.e. October to December.

CULTIVATION PATTERN

Mustard Seed Crop Calendar

Country

India

Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

Harvesting Sowing

DOMESTIC SCENARIO

In India, mustard seed is grown as a rabi crop, which is sowed during October-

December and the harvesting begins from March onwards. The largest mustard

seed producing states in India are Rajasthan (45%), Haryana (13%), Madhya

Pradesh (13%) and Uttar Pradesh (11%).

Rajasthan and Haryana produce the major share of rape/mustard contributing to

over 50% of the total Indian produce. It also has the maximum area under cultivation

for this crop.

Mustard seeds are yellowish colored, small seeds that are used as a spice in many

countries. These seeds are obtained from bush like mustard plant that belongs to

the genus Brassica that also include vegetables like cabbage and turnips.

MAJOR TRADING HUBS IN INDIA

Delhi, Kota and Hapur are the major market for mustard in India and the prices of

these markets serve as 'reference' for other subsidiary markets.

MAJOR TRADING CENTRES – MUSTARD SEED

AGRI COMMODITIES APRIL TO JUNE 2013

11

DEMAND SUPPLY FUNDAMENTALS

In India, mustard seed is the third largest produced oilseed after soybean and

groundnut. Mustard seed production is fluctuating over year, as this crop is growing

mainly on rain fed area.

The unfavorable weather conditions during November-December 2011 not only

hampered planting but also affected the mustard seed yield. The drop in area under

mustard seed cultivation by 3.5% to 7mn hectares and yield by 4% has resulted in a

drop in output by 12% to 6.2 mn tonne in 2011-12.

2004-052005-06

2006-072007-08

2008-092009-10

2010-112011-12

2012-13

0

1000

2000

3000

4000

5000

6000

7000

80006500 7000

58005450

67006400 7100

6200 6800

RAPE MUSTARD SEED PRODUCTION

YEARSSource :-USDA

Fig

in 0

00

to

nn

es

MUSTARD AREA &YIELD

Years Area (in 000 Ha) Yield (Kg/Hec)

2008-09

2009-10

2010-11

2011-12

2012-13

6600

6450

7250

7000

6750

900

920

980

940

1001

COMPARISON OF MUSTARD SEED BALANCE SHEET

Fundamentals

Production

Imports

Consumption

Exports

Total Supply

Ending Stocks

Beginning Stocks

2012-2013e

6800

-

6900

-

7104

204

304

2011-2012

6200

-

6825

-

7129

304

929

Mustard Seed Balance Sheet 2011-2012 & 2012-2013e - India

(in '000' tonnes)

MINIMUM SUPPORT PRICE (MSP)

In the past two years, the government has hiked the MSP of oilseeds, along with that

of mustard seed, to boost production and reduce the dependency on import. From

Rs 2,500 per quintal in 2011-12, the government raised the support price to Rs

3,000 per quintal in 2012-13.

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

0

500

1000

1500

2000

2500

3000

3500

1700 1715 1715 1800 1830 1830 1850

2500

3000

MSP OF MUSTARD SEED

YEARS

Rs/

Qui

ntal

SPOT PRICE OF MUSTARD SEED VS YOY ARRIVALS

The prices in the country are largely dependent on the domestic production of

mustard seed and its arrivals in the market. Peak arrival period is between February

and May in these markets. Thereafter, arrivals start declining and least in the month

of July.

IMPORT & EXPORT OF MUSTARD SEED

• India is self-sufficient in mustard seed and oil as import and export of the

commodity is almost non-existent.

MUSTARD TRADING SPECIFICATIONS

Spot Market Trading Futures Market Trading

Bags/Pack Size Quotation/Base Value Delivery Center Unit of trading Quotation/Base Value Delivery Center

85 kg Rs/Quintal Kota, Hapur ,Haryana 100 MT Rs/Quintal

Alwar,Kota,Sri Ganga nagar,Bikaner(Rajasthan),

Hapur & Agra (UP)

CONTRACT SPECIFICATION OF MUSTARD SEED

AGRI COMMODITIES APRIL TO JUNE 2013

12

NCDEX ACCREDITED WAREHOUSE OF MUSTARD SEED

GLOBAL SCENARIO

The global mustard seed production has grown at 4.08% CAGR in the past two decades

and is currently 60.55 million tonne (2011-12). Regarding the production of rape/

mustard oil, China holds the first place followed by Canada and India and France.

MARKET INFLUENCING FACTORS

•

•

•

•

•

•

•

•

•

CURRENT FUNDAMENTALS DRIVING THE MARKETS

•

•

•

•

•

•

OUTLOOK

Various supply-demand factors revolving around the global edible oil scenario

Influence of internationally traded substitutes (Palm, soya oil)

The nature of the existing supply

The presence of a large unorganized crushing sector

Government policies and intervention.

The ups and downs in production, arrivals in the mandis, international prices

of other oilseeds and oils

Stocks present with stockist and the stocks-to-consumption ratio.

Weather plays a profound influence in determining the trader's sentiments and

the production.

The price of other major oilseeds like castor, soybean, also influence the

prices of Rmseeds.

Surge in the main winter-sown rapeseed crop due to favourable weather has

helped in production rise.

Output of rapeseed rose about 22% to 6.8 million ton in the 2012-13 harvest,

said the Central Organisation for Oil Industry and Trade (COOIT).

In a bid to arrest spiraling prices of edible oil in the state, the Gujarat

government recently imposed stock limit on edible oil and oil seeds with

immediate effect.

The state government's move of limiting stock of oilseeds and edible oils has

come in the wake of groundnut oil prices touching Rs 2,100 per tin of 15 litres,

almost double than last year.

A conference on Oilseeds industry held at Agra to discuss the likely supply

scenario of Rabi oilseeds. The Industry estimated 71.5 Lakh tons of RMseed

production this year.

As per the latest USDA report, China rapeseed production is projected at 13.5

million tons, up 0.9million based on increased area and yield indicated in

recently released official government statistics.

RM Seed is expected to continue to trade in the range to lower in coming 2-3 weeks

as output of rapeseed rose about 22 percent to 6.8 million tonnes in the 2012/13

harvest, said the Central Organisation for Oil Industry and Trade (COOIT), which

was giving its estimate after the crop had been harvested. After the recent surge in

prices, we feel correction in mustard seed till Rs 3,250-3,200 will provide a fresh

buying opportunity. Buying should be avoided at current levels. The demand-

supply scenario for the domestic market projects higher supply of most rabi crops.

Weather developments in Argentina and US will determine meal exports from India.

This will be an important factor to watch out for.

Mustard Seed - Ncdex Accredited Warehouse

State City Warehouse

Rajasthan Alwar

LTC Commercial Company Private LimitedJICS Logistics

Star Agriwarehousing and Collateral Management Ltd.

NCMSL Commodity Multilink Point

Rajasthan BikanerJanhavi Promoters Pvt.Ltd

JICS Logistics

Uttar Pradesh

Hapur NCMSL Commodity Multilink Point

Haryana HisarThe Haryana State Co-op Supply &

Marketing Federation Limited

Rajasthan Kota

NCMSL Commodity Multilink PointStar Agriwarehousing and

Collateral Management Ltd. Total Logistics (India) Private Limited

Shree Shubham Logistics LimitedJICS Logistics

Rajasthan Jaipur

Star Agriwarehousing and Collateral Management Ltd.

Total Logistics (India) Private LimitedACE Audit Control and Expertise (India) Pvt. Ltd.

JICS LogisticsLTC Commercial Company Private Limited

NCMSL Commodity Multilink Point

S1 S2 S3 R1 R2 R3

MUSTARD SEED BULLISH 3470 3350 3230 3020 3700 3944 4250 4500

NAME TREND CMP SUPPORT KEY LEVELS RESISTANCE

AGRI COMMODITIES APRIL TO JUNE 2013

13

MAIZE

INTRODUCTION

Maize (Indian Corn) constitutes a primary poultry feed ingredient.

Corn is generally grown in two seasons. The first is Kharif, for which sowing starts

in June and harvested October onwards. Karnataka, Andhra Pradesh, Gujarat,

Maharashtra and Orissa have Kharif crops.

The second is Rabi, for which sowing starts from November and harvested by May.

Rabi crop is mainly grown in Bihar and coastal Andhra Pradesh. In Tamil Nadu corn

production starts from January and peaks by April. Corn may also be produced in

small quantities during other times of the year.

Corn has several uses. It is used in the poultry and animal feed industry, in starch

and food industry, in breweries and for human consumption. In the poultry feed

industry, corn constitutes about 60% of the feed and hence is extremely a

significant raw material.

Maize is the only crop which has got the highest weight of production even as

compared to rice and wheat. The planting of the maize crop is done in the spring

season so that it could get the benefit of the rains in this season. Rains for this crop,

are very important as maize is very sensitive to drought. This crop is generally

cultivated in a two or three crop rotation. The cultivation of maize involves the

following steps:

Planting – Planting of the crop is when the crop is planted. The planting of

maize is generally done in mid of April to mid of May.

Silking – Silking is the most crucial stage in the crop cultivation. It means

pollination of the crop.

Doughing – When the maize crop starts to show a thick substance, the crop is

said to be doughed.

Denting- During the process of doughing, the plant spends all its resources in

the formation of those dough like substance and this causes the plant to

reduce and a 'dent' starts to show, on the end of the substance. This is called

denting.

Maturing – When the green foliage is gone and maize appears from the

opening of the foliage, the crop is said to be matured.

Harvesting – The crop usually gets matured around the year end and then it

harvested.

CULTIVATION PATTERN

•

•

•

•

•

•

CROP CALENDAR

Maize Crop Calendar

Country

India

Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

Harvesting Sowing

DOMESTIC SCENARIO

India's produces around 10-14 million tons of maize annually. This contributes to

about 2% of the total world production. Most of the corn produced in India mainly

comes from the southern Corn Belt states of Karnataka and Andhra Pradesh. In

India, major maize producing states are Karnataka, Andhra Pradesh and Bihar.

Other states including Tamil Nadu, Uttar Pradesh, Madhya Pradesh, Maharashtra,

and Orissa are producers of a smaller scale.

MAJOR TRADING HUBS IN INDIA

MAJOR TRADING CENTRES – MAIZE

AGRI COMMODITIES APRIL TO JUNE 2013

14

DEMAND SUPPLY FUNDAMENTALS

Indian maize prices were at a record high in 2011-12 due to a substantial increase in

exports due to the weak Indian rupee. The performance of competing crops and

price of maize crop influences area, production and yield of maize. For the last five

years the area under maize has increased considerably

Maize is grown in all the three seasons in an area of 8.6 to 8.9 lakh ha with an annual

production of 2.1 to 2.5 million tonnes. Earlier in 50's and 60's, the maize

production was improved through crop management techniques and increasing the

area under cultivation. Now it is being improved through improvement in yield levels.

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

0

5000

10000

15000

20000

25000

1418014710

1510018960 19730

16720

2173021570

21000MAIZE PRODUCTION

YEARS

Fig

in 0

00 to

nnes

MAIZE AREA & YIELD

Years Area (in 000 Ha) Yield(Million/Ha)

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

7500

7600

7800

8260

8170

8330

8600

8670

8930

1.89

1.94

1.94

2.3

2.41

2.01

2.53

2.49

2.35

COMPARISON OF MAIZE BALANCE SHEET

Fundamentals

Beginning Stocks

Production

Imports

Consumption

Exports

Total Supply

Ending Stocks

2012-2013e

407

21000

-

18000

3000

7104

407

2011-2012

511

21570

-

17000

4674

22081

407

Maize Balance Sheet 2011-2012 & 2012-2013e - India (in '000' tonnes)

MINIMUM SUPPORT PRICE (MSP)

The Government of India has increased the Minimum Support Price (MSP) of maize

of Fair Average Quality (FAQ) from Rs. 980 per quintal to Rs. 1175 per quintal for the

crop year 2012-2013.Every year, the Government of India determines the Minimum

Support Price of maize based on the recommendations of the Commission for

Agricultural Cost and Prices (CACP).

MSP OF MAIZE

1400

1200

1000

800

600

400

200

02004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

YEARS

525 540 540620

840 840 880980

1175

Rs/

Qui

ntal

SPOT PRICES OF MAIZE - KARNATAKA Vs YOY ARRIVALS

Davangere is the major maize producing district in Karnataka accounting for 25 per

cent of the state production. The kharif maize crop has started arriving in major

mandies of Karnataka. The late arrival of monsoon has delayed maize arrivals in

Davanagere. The widespread drought and weak crop prospects worldwide has

raised the prices of maize in Karnataka.

MAIZE TRADING SPECIFICATIONS

MAIZE TRADING SPECIFICATIONS

Spot Market Trading Futures Market Trading

Bags/Pack Size Quotation/Base Value Delivery Center Unit of trading Quotation/Base Value Delivery Center

50,60,100 kg Rs/Quintal 100 MT Rs/Quintal

Banglore, Davangere Kanpur, Bahraich(UP), Patna,

Chapra(Bihar)

(Karnataka), Nizamabad, Davangere, Karimnagar, Delhi,Sangli

AGRI COMMODITIES APRIL TO JUNE 2013

15

MAIZE - NCDEX ACCREDITED WAREHOUSE

Maize - Ncdex Accredited Warehouse

State City Warehouse

Rajasthan NimbaheraLTC Commercial Company Private Limited

NCMSL Commodity Multilink Point

Andhra PradeshNizamabad

Andhra Pradesh State Warehousing CorporationJICS Logistics

NCMSL Commodity Multilink Point

Madhya Pradesh Ratlam NCMSL Commodity Multilink Point

Uttar Pradesh Bahraich NCMSL Commodity Multilink Point

Maharashtra Jalna NCMSL Commodity Multilink Point

Karnataka Davangere NCMSL Commodity Multilink Point

GLOBAL SCENARIO

The US is the leading producer of Maize with 40 per cent of the global production.

China and Brazil comes on the 2nd and 3rd place India is Asia's biggest maize

producer behind China. The US is the largest exporter of maize while, India

contributes about 2 percent of global trade. Indian maize prices were at a record

high in 2011-12 due to a substantial increase in exports due to the weak Indian

rupee. The performance of competing crops and price of maize crop influences

area, production and yield of maize.

MAIZE EXPORTS FROM INDIA

Indian maize prices were at a record high in 2011-12 due to a substantial increase in

exports due to the weak Indian rupee. According to reports, India exported around

S1 S2 S3 R1 R2 R3

NAME TREND CMP SUPPORT KEY LEVELS RESISTANCE

MAIZE BULLISH 1323 1220 1035 950 1485 1650 1800 1980

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

0

1000

2000

3000

4000

5000

448 521

1208

4473

2608

1939

3376

4674

3000

Maize Exports

Years

Fig

in 0

00 T

onne

s

4mt of the 2011-12 corn output mainly to Far-East nations such as Malaysia,

Singapore and Indonesia and Vietnam. Egypt and Iran are new buyers of Indian corn

this year.

Weather of the area in which it is produced and natural calamities like floods,

droughts etc

Temperature, rainfall and soil moisture in the cultivating areas.

Demand for the maize in poultry and industrial uses

Changes in the government policies relating to the minimum support prices

Cheaper prices of the substitute product

Seasonal cycles: Price tends to be lower as harvesting progresses and

produce starts coming into the market. At the time of sowing and before

harvesting price tends to rise in view of tight supply situation.

Carryover stocks, consumption and the import-export policy also affects the

prices

Technological changes and improvements

Maize exports in the current season are expected to be lower by about a third

over last year's record high of 4.7 million tonnes on a lower crop and rising

domestic demand.

Trader expects maize exports to be in the region of around 3-3.5 MT for the

crop marketing year-ending August 2013.

The lower output in the kharif season has already resulted in a decline in

exports during the first half,” an official with a multinational exporting firm

said.

Maize output in 2012-13 is pegged at around 21 MT on account of lower crop in

Karnataka, Andhra Pradesh, Maharashtra and Rajasthan due to erratic monsoons.

Further, the maize has an export window only for the next two to three months

till June-July after which the global supplies are expected to ease.

The rabi maize crop in Bihar, which has been slightly delayed, looks higher by

about 20 per cent. There is a potential to export till June-July.

With easing global supplies from August and prices coming under pressure, as

reflected in the Chicago futures, exports from India were likely to be unviable.

The Chicago corn prices have eased on better planting prospects in the US

and Brazil.

Reports said corn planting in the US for 2013 is forecast to touch 97.75

million hectares, the highest in 77 years.

The long-term price trend in the domestic market is likely to remain bullish due to a

robust export demand. According to reports, India exported around 4mt of the

2011-12 corn output mainly to Far-East nations such as Malaysia, Singapore and

Indonesia and Vietnam. Egypt and Iran are new buyers of Indian corn this year.

Domestic demand for India is pegged at 17-18 million tonnes annually.

MARKET INFLUENCING FACTORS

•

•

•

•

•

•

•

•

CURRENT FUNDAMENTALS DRIVING THE MARKETS

•

•

•

•

•

•

•

•

•

OUTLOOK

Bigha

0.598

1.477

1.000

Acre

1.000

2.471

1.674

Hectare

0.405

1.000

0.677

Square Feet

43560.0

107639.1

17424.0Bigha

Acre

Hectare

CONVERSION TABLE – AREA

Wheat (Kg)

27.24

Soybean (Kg)

27.24

Corn (Kg)

25.42US Bushel

CONVERSION TABLE – VOLUME

US Gallon

1.000

9.309

0.264

US Bushel

0.107

1.000

0.028

Litre

3.785

35.239

1.000

US Gallon

US Bushel

Litre

CONVERSION TABLE – WEIGHTMaund Pound (lb) Kilogram Quintal Metric Ton

Maund

Pound (lb)

Kilogram

Quintal

Bales

Metric Ton

1.000

0.012

0.027

2.679

4.550

26.792

82.287

1.000

2.205

220.462

480.000

2204.630

37.324

0.454

1.000

100.000

170.000

1000.000

0.373

0.005

0.010

1.000

1.700

10.000

0.037

0.000

0.001

0.100

0.217

1.000

501.1

1,277.4

1,585.3

2,417.0

42.7

15.0

14.4 14.3

14.1

13.8

13

14

15

16

0

500

1000

1500

2000

2500

3000

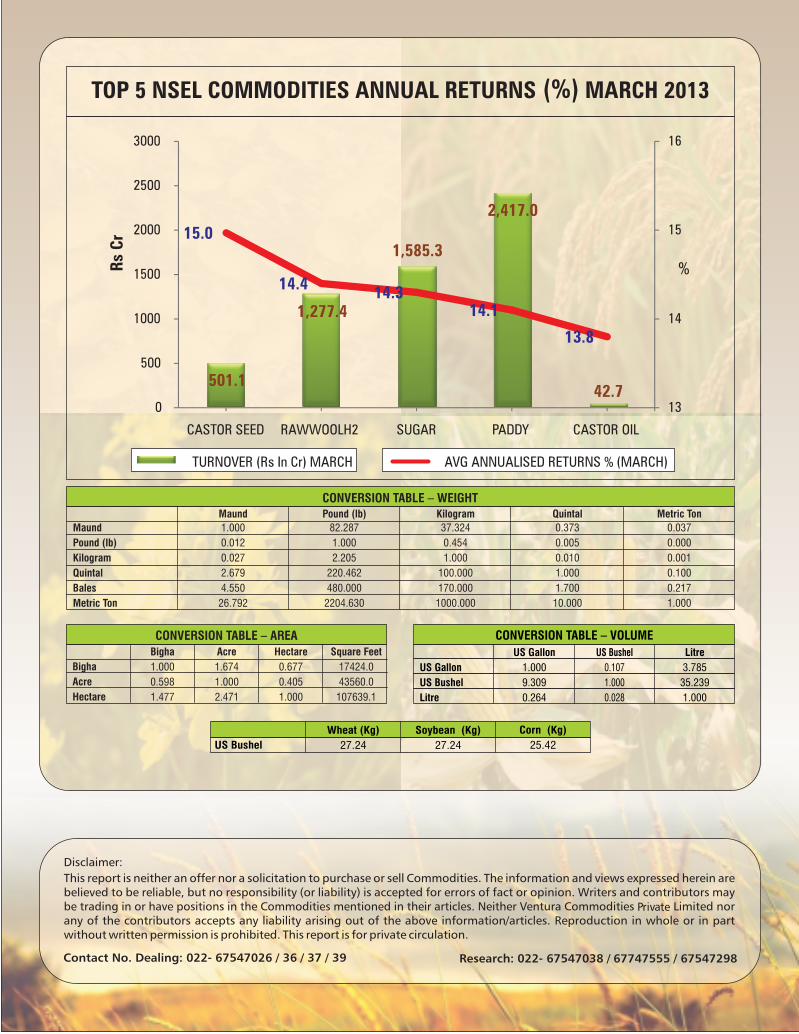

CASTOR SEED RAWWOOLH2 SUGAR PADDY CASTOR OIL

%Rs

Cr

TOP 5 NSEL COMMODITIES ANNUAL RETURNS (%) MARCH 2013

AVG ANNUALISED RETURNS % (MARCH)TURNOVER (Rs In Cr) MARCH

Related Documents