SERVICE QUALITY OF E-BANKING IN PAKISTAN: A COMPARISON OF ISLAMIC AND COMMERCIAL BANKS SUPERVISOR Mr. Asad Ejaz Sheikh MEMBERS Umer Iqbal Siddiqi MS09MBA055 Syed Fazal Abbas MS09MBA065 HAILEY COLLEGE OF BANKNG & FINANCE UNIVERSITY OF THE PUNJAB, LAHORE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 1/66

SERVICE QUALITY OF E-BANKING IN PAKISTAN:

A COMPARISON OF ISLAMIC AND COMMERCIAL BANKS

SUPERVISOR

Mr. Asad Ejaz Sheikh

MEMBERS

Umer Iqbal Siddiqi MS09MBA055

Syed Fazal Abbas MS09MBA065

HAILEY COLLEGE OF BANKNG & FINANCE

UNIVERSITY OF THE PUNJAB, LAHORE

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 2/66

Sanctity is attributable to Thee alone,

we cherish no knowledge save for what Thou have bestowed upon us

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 3/66

ii

ACKNOWLEDGEMENTS

We would like to offer our humble gratitude to Allah Almighty to make us able to

complete this study. Afterwards, we thank our College authorities to polish us so well

that we were able to comprehend such a difficult task. Importantly we are grateful to

Madam Fouzia Naheed Khawaja to teach us the subject of “Research Methodology”

with utmost proficiency and to our Research Advisor Mr. Asad Ejaz Sheikh whose

guidance paved the way of success for us.

Umer Iqbal Siddiqi

Syed Fazal Abbas

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 4/66

iii

ABSTRACT

Using an already developed model for measuring the quality of online services, the

authors of this thesis have developed and later on modified a theoretical model

(instrument) for measuring the quality of online banking services in particular. Using

quantitative research method including the design and distribution of a questionnaire,

empirical data was collected on which statistical analysis has been performed. For the

measuring of service quality eight basic dimensions were extracted from the 22 items

which were Assurance/Trust, Site Aesthetics, Contact, Privacy, System Availability,

Fulfillment, Responsiveness and Efficiency. A questionnaire consisting of 20

questions was conducted to the sample of target population, selected through

convenient sampling method. The results were then analyzed using SPSS and

Microsoft Excel and the findings were recorded along with the analytical discussion

and managerial recommendations.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 5/66

iv

TABLE OF CONTENTS

CHAPTER ONE INTRODUCTION ....................................................... ............................................. 1

1.1 PROBLEM STATEMENT ............................................................. ....................................................... 2

1.2 PURPOSE AND SIGNIFICANCE OF THE STUDY ............................................................ ....................... 2 1.3 LIMITATIONS ........................................................................................................... ....................... 2

1.4 DEFINITIONS ...................................................... ................................................................. ............ 2

1.4.1 E-banking Services ................................................................................................................ 2

1.4.2 E-service Quality ...................................................................... ............................................. 3

1.4.3 ServQual ......................................................................................................... ....................... 3

1.4.4 E-SQ Instrument .................................................................................................................... 3

DISPOSITION OF THESIS .............................................................................................................. .... 4

CHAPTER TWO LITERATURE REVIEW ................................................................ ....................... 5

2.1 IMPORTANCE OF SERVICE QUALITY IN BANKING ............................................................... ............ 9

2.2 WHAT IS SERVICE QUALITY? .............................................................. .......................................... 10 2.3 SERVICE QUALITY AND ITS DETERMINANTS ............................................................ ..................... 11

2.4 E-BANKING SERVICES ............................................................. ..................................................... 18

CHAPTER THREE RESEARCH METHODOLOGY ......................... ........................................... 20

3.1 R ESEARCH DESIGN ....................................................................................................................... 20

3.1.1 Population of the Study .............................................................. .......................................... 21

3.1.2 Element of the Study ............................................................................................................ 21

3.1.3 Sample of the Study ......................................................... ..................................................... 21

3.1.4 Sphere of the Study .............................................................................................................. 21

3.2 VARIABLES ........................................................ ................................................................. .......... 21

3.3 D

ATAC

OLLECTION....................................................................................................................... 22 3.4 DATA A NALYSIS ........................................................... ................................................................ 23

CHAPTER FOUR DATA ANALYSIS ............................................................... ................................ 24

4.1 EFFICIENCY .................................................................................................................................. 24

4.2 FULFILLMENT ............................................................... ................................................................ 26

4.3 SYSTEM AVAILABILITY ................................................................................................... ............. 28

4.4 PRIVACY ............................................................ ................................................................. .......... 29

4.5 ASSURANCE / TRUST .................................................................................................................... 31

4.6 SITE AESTHETICS .......................................................... ................................................................ 33

4.7 R ESPONSIVENESS .......................................................... ................................................................ 35

4.8 CONTACT ........................................................... ................................................................. .......... 37

CHAPTER FIVE CONCLUSION AND DISCUSSION ................................................................... 39

5.1 CONCLUSION ..................................................... ................................................................. .......... 39

5.2 DISCUSSIONS ..................................................... ................................................................. .......... 41

5.3 R ECOMMENDATIONS .................................................................................................................... 42

R EFERENCES ...................................................................................................................................... 44

APPENDICES ........................................................ ................................................................. .......... 46

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 6/66

v

LIST OF TABLESTABLE 1: ELEMENTS OF SERVQUAL .............................................................. ................................ 15

TABLE 2: DIMENSIONS OF PERCEIVED SERVICE QUALITY ................................ ..................... 16

TABLE 3: CROSS-TABULATION OF EFFICIENCY AND CATEGORY OF THE BANK ............... 24

TABLE 4: CROSS-TABULATION OF FULFILLMENT AND CATEGORY OF THE BANK ........... 26

TABLE 5: CROSS-TABULATION OF SYSTEM AVAILABILITY AND CATEGORY OF THE

BANK ..................................................... ................................................................. ..................... 28

TABLE 6: CROSS-TABULATION OF PRIVACY AND CATEGORY OF THE BANK .................... 29

TABLE 7: CROSS-TABULATION OF ASSURANCE AND CATEGORY OF THE BANK .............. 31

TABLE 8: CROSS-TABULATION OF SITE AESTHETICS AND CATEGORY OF THE BANK ..... 33

TABLE 9: CROSS-TABULATION OF RESPONSIVENESS AND CATEGORY OF THE BANK .... 35

TABLE 10: CROSS-TABULATION OF CONTACT AND CATEGORY OF THE BANK ................. 37

LIST OF FIGURESFIGURE 1: GAP MODEL OF SERVICE QUALITY .......................................................................... .. 11

FIGURE 2: COMPONENT OF TRANSACTION SPECIFIC EVALUATION .................................... 14

FIGURE 3: GRAPHICAL REPRESENTATION OF TABLE 3 ............................................................ 25

FIGURE 4: GRAPHICAL INTERPRETATION OF TABLE 4 ............................................................. 27

FIGURE 5: GRAPHICAL INTERPRETATION OF TABLE 5 ............................................................. 28

FIGURE 6: GRAPHICAL INTERPRETATION OF TABLE 6 ............................................................. 30

FIGURE 7: GRAPHICAL INTERPRETATION OF TABLE 7 ............................................................. 32

FIGURE 8: GRAPHICAL INTERPRETATION OF TABLE 8 ............................................................. 34

FIGURE 9: GRAPHICAL INTERPRETATION OF TABLE 9 ............................................................. 36

FIGURE 10: GRAPHICAL REPRESENTATION OF TABLE 10 ........................................................ 38

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 7/66

1

CHAPTER ONEINTRODUCTION

Globalization and deregulations have increased competition in the market

place, as now-a-days it has become much easier for companies to cross borders and

compete internationally. The increased competition, on its behalf, has made

organizations to constantly try to increase their productivity and decrease their costs.

One way for them to achieve that is by investing in information technology. The

recent development of IT has led to major changes in the way services are delivered

to the customers. Currently, customers are using more and more self-service options,

which are more convenient and fast. In addition, the advent and use of the Internet has

changed considerably the daily activities of most people, such as shopping and

banking. The popularity of banking services delivered over the Internet (online

banking services) is increasing in recent years.

E-services, including online banking services, are becoming an attractive

alternative to visiting service outlets or phoning call centers for increasing number of

customers. Some of the reasons for customers to prefer online services (as online

banking services) are: convenience, feeling more in control of the service process and

avoiding human contact and saving time. As far as online services are concerned, it is

quite easier for customers to evaluate and compare the benefits of competing services.

In addition, the switching costs are very low, that is why retaining the customer in the

Internet space is of vital importance. In order for service providers to retain their e-

customers, they should have better understanding of how customers’ perceive and

evaluate the quality of the electronically offered services. Customers have some

expectations and criteria when they judge whether the provided E-banking service is

satisfactory or not. This is what banks, which provide E-banking services should try

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 8/66

2

to find out, so that they can improve their online services and gain competitive

advantage in the banking industry.

1.1 Problem Statement

Is there any significant difference in the quality of E-banking services offered

by Commercial and Islamic Banks of Pakistan?

1.2 Purpose and significance of the StudyThe purpose of this study is to provide insight into how customers perceive the

quality of e-banking services and to help the banks (Islamic as well as conventional

banks) to improve their e-banking services to the ultimate customers to keep pace

with the latest IT.

1.3 LimitationsOwing to the time and cost of our study, it is confined to the area of Lahore

only. Its sample includes all the conventional and Islamic banks’ customers who are

using E-Banking service of the banks due to convenience and flexibility. Sample will

collect data on the basis of convenient sample method.

1.4 DefinitionsA short description of the terms which are mostly used throughout the thesis is

being given for the clear understanding of the readers.

1.4.1 E-banking Services

Banking services delivered over the Internet. These include opening/closing of

account, domestic/foreign money transfer, standing orders, direct debit, debit card

application, loan application, credit card application, insurance investment, mutual

funds investment, foreign/domestic equity investment, deposit account opening, life

insurance contract, traffic insurance contract and etc (Centeno, 2003)

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 9/66

3

1.4.2 E-service Quality

“Consumers’ overall evaluation and judgment of the excellence and quality of

e-service offerings in the virtual marketplace” (Santos, 2003 p.235)

1.4.3 ServQual

A 22-item instrument for measuring customers’ expectations and perceptions

from a service along five quality dimensions: tangibles, reliability, responsiveness,

assurance and empathy. (Parasuraman et al, 1991)

1.4.4 E-SQ Instrument

An instrument similar to the SERVQUAL scale, developed specifically for

measuring online services (e-services) quality. It includes two scales: the E-S-QUAL

scale consists of 4 dimensions with 22 attributes, including efficiency, fulfillment,

system availability and privacy and the E-RecS-QUAL scale which consists of 3

dimensions with 11 attributes, including responsiveness, compensation and contact

(Parasuraman et al, 2005)

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 10/66

4

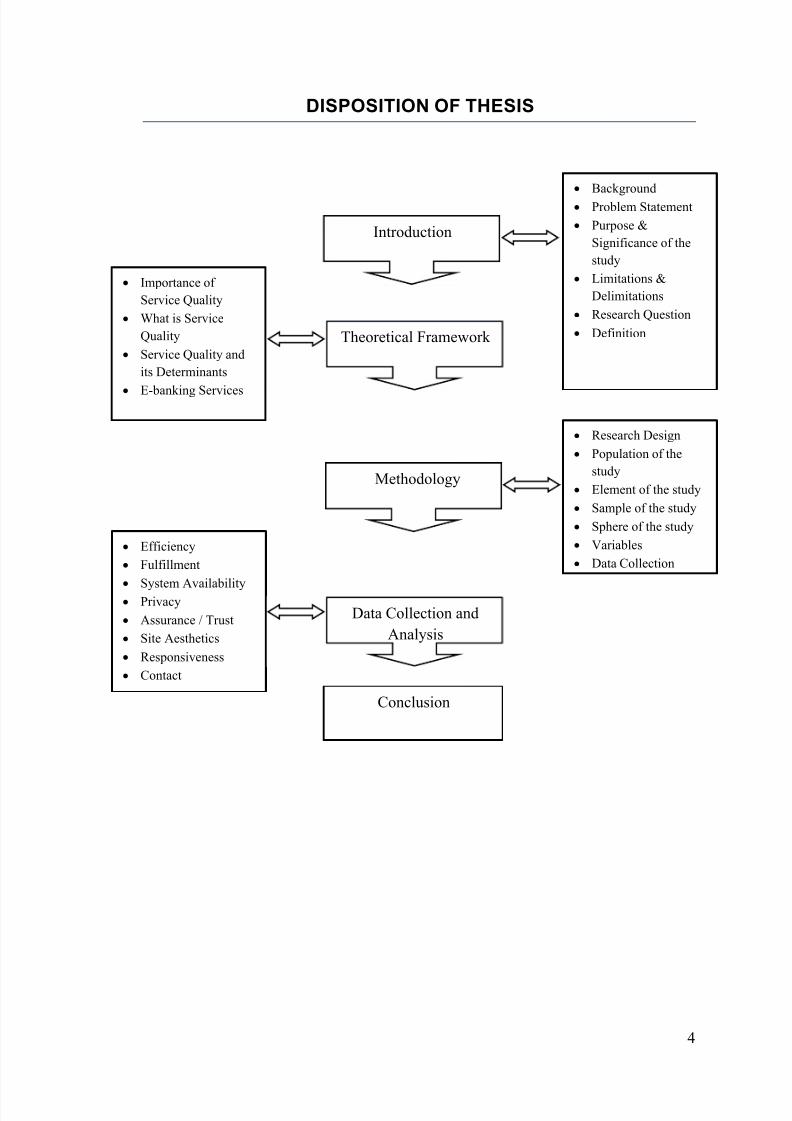

DISPOSITION OF THESIS

Introduction

Theoretical Framework

Methodology

Data Collection and

Analysis

Conclusion

Background

Problem Statement

Purpose &

Significance of the

study

Limitations &

Delimitations

Research Question

Definition

Importance of

Service Quality

What is Service

Quality

Service Quality and

its Determinants

E-banking Services

Research Design

Population of the

study

Element of the study

Sample of the study

Sphere of the study

Variables

Data Collection

Efficiency

Fulfillment

System Availability

Privacy

Assurance / Trust

Site Aesthetics

Responsiveness

Contact

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 11/66

5

CHAPTER TWOLITERATURE REVIEW

Islamic finance has gripped the world with a strong fervor and passion.

Interest in this discipline has proliferated to almost 60 countries, going beyond the

Islamic world to the leading global financial centers. For quite some time, United

Kingdom has adopted an open door policy and provided a level playing field to

Islamic finance and now Singapore is following its lead. Every day, Islamic finance is

breaking new boundaries and new frontiers. Leading Islamic banks have fast spread

their network from home base to develop a regional and global reach. Some of the

Middle East banks are now entering into African and Central Asian markets and are

sizing up Australian financial market (Akhtar, 2007). Islamic banking system has

emerged as a competitive and a viable substitute for the conventional banking system

during the last three decades. It is especially true for Muslim world where presently

Islamic banking strides at two separate fronts. At one side, efforts are also underway

to cover the entire financial systems in accordance to Islamic laws (Shariah). At the

other side, separate Islamic banks are allowed to operate in parallel to conventional

interest based banks (Khizer, 2010).

The process of Islamization of the financial system of Pakistan is coincided

with the globally resurgence of Islamic banking in the late seventies. Pakistan was

among the three countries in the world that has been trying to implement Islamic

banking at national level. This process started with presidential order to the local

Council of Islamic Ideology (CII) on September 29, 1977. The council was asked to

prepare the blueprint of interest free economic system. The council included panelists

of bankers and economists who submitted their report in February 1980, highlighting

various ways and sufficient details for eliminating the interest from the financial

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 12/66

6

system of Pakistan. This report was a landmark in the efforts for Islamizing the

banking system in Pakistan (Khizer, 2010).

The Constitution of 1956 requires an immediate elimination of Riba based

transactions according to Article 28. Similarly, the Council of Islamic Ideology was

established under the Constitution of 1962, to eliminate the interest from the economy

especially from banking sector. Interestingly the Constitution of Pakistan (1973) also

requires a prompt elimination of interest (Riba) from the economy as shown by the

article 2A, 31, 37, 38 (F) and 227 of the said constitution. The council consulted a

large number of bankers and economists to recommend some alternatives to replace

interest-based financial structure in the economy during 1980s. In 1991, Full Bench of

Supreme Court of Pakistan ordered the elimination of Riba from the economy until

June 30, 1992. (Ahmad, Malik, & Humayoun, Banking Developments in Pakistan: A

Journey from Conventional to Islamic Banking, 2010)

The Govt. of Pakistan has taken a number of initiatives during 1979-1992 to

introduce interest free products in the market especially in the banking sector. In

1979, National Investment Trust (NIT), Investment Corporation of Pakistan (ICP) and

House Building Finance Corporation (HBFC) started interest free transactions.

Similarly, during 1980 a number of actions were taken as Mudarbah companies were

established, Participatory Term Certificates (PTC) was launched and Zakat ordinance

was announced. In addition, nationalized banks were required to open interest-free

counters for their customers in 1981. However, Usher ordinance came into force in

1983 throughout the Pakistan. In the same year, financial services ordinance was

amended to introduce non-interest system. SBP was assigned the duty for transition of

interest based financial institutions into interest-free financial institution till 1985

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 13/66

7

(Ahmad, Malik, & Humayoun, Banking Developments in Pakistan: A Journey from

Conventional to Islamic Banking, 2010).

The deregulation and liberalization during 1990s encouraged the local as well

as foreign investors to initiate their operation in Pakistan. This phenomenon resulted

in the competition amongst banks. Ahmad et al. (2010) gives reference of La Porta

that government ownership of banks could be discouraged due to slower financial

development, low productivity and slow economic progress. Economic growth is the

main transmission channel for development. Islam does not contradict growth; it

promotes sustainable development and growth (Hussain, 2006). The measures taken

for Islamization in Pakistan are traced back decades ago. The Eighth Amendment of

the 1973 Constitution, adopted by the National Assembly in 1985, also made room for

creation of the Federal Shariat Court (FSC). Practically measures taken included the

introduction of Zakat (June, 1980), and Usher (tithe) (March, 1983) and elimination

of interest from the operations of Specialized Financial Institutions (July, 1979 to

July, 1985) and the commercial banks (January, 1981 to July, 1985).

The inception of 21st century heightened the competition among banks

regarding service quality to have satisfied customers for better profitability. SBP plays

an active role to establish a sound Islamic banking system in Pakistan according to

principles of Shariah as mentioned in its mission statement that read “To promote and

develop Islamic Banking industry in line with best international practices, ensuring

Shariah Compliance and transparency”. In 2002, Islamic banks have started their

operations in Pakistan and experienced stiff competition from its peers as well as from

conventional banks. Islamic bank offers a wide range of products based on profit and

loss according to principles of Shariah. It develops the sense of collective welfare by

sharing the risk among different stakeholder. While the interest is the central tenet of

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 14/66

8

the conventional banking and it maximizes the return even at the cost of other

stakeholders by transferring the burden of risk to other parties. Islamic banks are

primarily concerned to eliminate Riba from the economy by promotion of risk sharing

practices for economic prosperity.

Pakistani banking sector is continuously improving with diversified pattern of

ownership due to an active participation of foreign and local stakeholder. It resulted

into an increased competition among banks to attract a greater number of customers

by the provision of quality services for long-term benefits. Now there are six full-

fledged Islamic banks and 13 Conventional banks offering products and services

according to principles of Shariah in different parts of the country. They are

competing in a highly competitive environment for the provision of quality services

according to customers' expectations (Ahmad, Malik, & Humayoun, Banking

Developments in Pakistan: A Journey from Conventional to Islamic Banking, 2010).

It is reported that customers of Islamic bank have greater perception of service quality

as compared to customers of conventional bank in Pakistan (Ahmad, Kashif-ur-

Rehman, Saif, & Safwan, 2010).

Now bank customers are much concerned regarding the quality of services due

to increased awareness. They continue to deal with their current bank only if they feel

satisfied; otherwise they feel no hesitation to switch to other banks. Islamic banks

work within the limits prescribed by Shariah to stimulate business and trade activities.

It experienced an expansion in its network, size and structure due to beautiful

blending of commercial banks, micro finance institutions and Islamic banks in the

country

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 15/66

9

2.1 Importance of Service Quality in Banking

In service industries, globally, the subject of service quality remains a critical

one as businesses strive to maintain a comparative advantage in the marketplace.

Since financial services, particularly banks compete in the marketplace with generally

undifferentiated products; service quality becomes a primary competitive weapon

(Hossain & Leo, 2009). The existence of two bank streams i.e. conventional banks

and Islamic banks poses some questions about service quality and customers'

satisfaction in Pakistan. The banking profit as well as its existence and growth count

on the service imparted whilst dealing with the customers. Moreover, banks that excel

in quality service can have a distinct marketing edge since improved levels of service

quality are related to higher revenues, increased cross-sell ratios and higher customer

retention and expanded market share. Moreover, the banks understand that customers

will be loyal if they can produce greater value than competitors (Hossain & Leo,

2009). Islamic banks have opened new avenues for acceptance of deposits on interest

free-basis and extend credit facilities excluding interest e.g. Qarz-e-Hasana etc.

Ahmad et al (2010) in their research paper gives reference of a number of authors

who emphasized the importance of quality in the banking sector. It was found that

relationships with bank personnel are important criteria for selection of bank.

Similarly, it is documented that Islamic banks have shown an excellent performance

and they should diversify their products/services to meet customers’ expectations.

However, there is a significant relationship between service quality and financial

performance. Therefore, it is concluded that superior delivery of services results into

superior profitability. Pakistani banking sector witnessed a major change due to key

role of private sector having about 80% of banking assets. Finally, bankers should

concentrate on service quality to have satisfied customers as it is evident that service

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 16/66

10

quality has greater and strong positive impact on customer satisfaction in case of

Islamic banks as compared to conventional banks in Pakistan (Ahmad, Kashif-ur-

Rehman, Saif, & Safwan, 2010).

2.2 What is Service Quality?

Despite its popularity, the concept of service quality in the marketing literature

is still ambiguously and vaguely defined. Several measurement scales have been

proposed, but some of these take into account only the method of measurement and

ignore the idea that the same instrument may not be able to be automatically applied

in different industries or in different cultures (Korda & Snoj, 2010). When judging the

quality of the provided banking services, customers consider a lot of factors which

influence their judgment. For some customers the response and efficiency of the

service providers would be of greatest importance, for others the security and privacy

issues might be more important, and still for others what matters most may be the

website design and ease of use. In reality, customers have different expectations and

requirements. They deem different aspects of the service delivery process for essential

in order for them to be satisfied with the service (Kenova & Jonasson, 2006).

Service quality in simple words is the combination of tangible and intangible

things that satisfies the customers. Service expectations are the beliefs about service

delivery that function as standards or reference points against which performance is

judged. Customers compare their a priori expectations with actual service

performance to judge service quality. According to gap model of service quality,

service quality is regarded as high when service performance is perceived to be higher

than expectations of service. A fixed level of perceived performance, service quality

varies according to the level of service expectations that customers develop. In

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 17/66

11

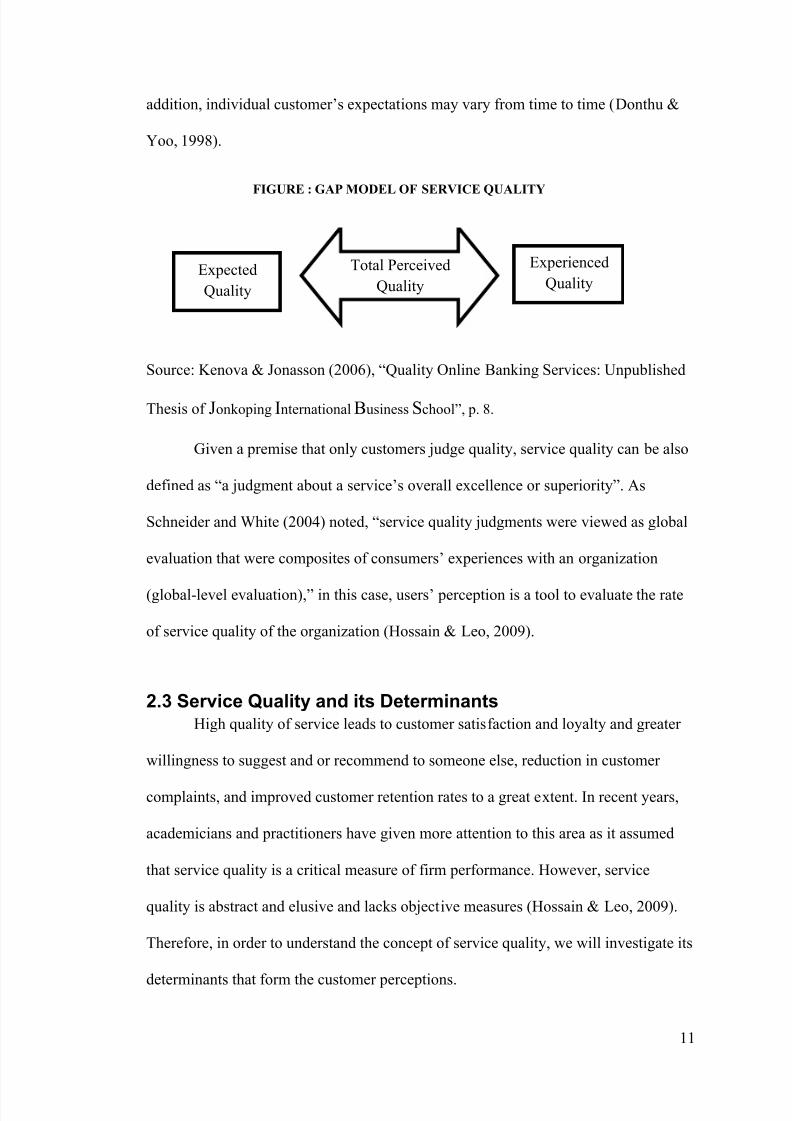

addition, individual customer’s expectations may vary from time to time (Donthu &

Yoo, 1998).

Source: Kenova & Jonasson (2006), “Quality Online Banking Services: Unpublished

Thesis of Jonkoping International Business School”, p. 8.

Given a premise that only customers judge quality, service quality can be also

defined as “a judgment about a service’s overall excellence or superiority”. As

Schneider and White (2004) noted, “service quality judgments were viewed as global

evaluation that were composites of consumers’ experiences with an organization

(global-level evaluation),” in this case, users’ perception is a tool to evaluate the rate

of service quality of the organization (Hossain & Leo, 2009).

2.3 Service Quality and its DeterminantsHigh quality of service leads to customer satisfaction and loyalty and greater

willingness to suggest and or recommend to someone else, reduction in customer

complaints, and improved customer retention rates to a great extent. In recent years,

academicians and practitioners have given more attention to this area as it assumed

that service quality is a critical measure of firm performance. However, service

quality is abstract and elusive and lacks objective measures (Hossain & Leo, 2009).

Therefore, in order to understand the concept of service quality, we will investigate its

determinants that form the customer perceptions.

Total Perceived

QualityExpected

Quality

Experienced

Quality

FIGURE : GAP MODEL OF SERVICE QUALITY

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 18/66

12

There is not a consensus over the determinants of the service quality. It

should be kept into mind that the service quality is a multidimensional concept and it

means different to different people but some instrument have been developed to gauge

it. In the past SERVQUAL model had been used to assess the service quality but

many a researcher raised their concerns over the dimensions used in this model. It is

necessary to understand and review those critiques to expunge the ambiguities.

Opponents of this approach argue that measuring only customers’ perceptions is more

reliable. Some of the opponents are Cronin and Taylor, who developed the

SERVPERF instrument in 1992. This instrument is similar to the SERVQUAL

instrument, but it measures service quality only on the basis of customers’ perceptions

of a given service. Other opponents to the disconfirmation method are Dabholkar,

Shepherd and Thorpe (2000) who have found that measuring only the perception of

customers can better evaluate their intention and evaluation (Kenova & Jonasson,

2006).

The major criticism of the instrument SERVQUAL was done by Cronic &

Taylor (1992) and Teas (1993). They objected the specification of service quality as a

gap between the customers’ expectation and perception. C & T surveyed the

customers in four sectors using the questionnaire based upon SERVQUAL instrument

and some other questions independent of former instrument. Concluding their study C

& T (1992) concluded that is not necessary to measure customer expectations in

service quality rather measuring perceptions is sufficed. They also concluded that

service quality failed to affect purchase intentions (Parasuraman, Zeithaml, & Berry,

Reassessment of Expectations as a Comparison Standard in Measuring Service

Quality:Implications for Further Research, 1994).

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 19/66

13

Parasuraman et al. (1994) focused on three issues, raised by C &T in their study,

to address their concerns.

Conceptual Issues

Methodology and analytical issues

Practical issues

The conceptual issue was germane to the perception-expectations gap

conceptualization of Service Quality. The critique contended that if any empirical

evidence espoused the relevance of the expectations-performance gap as the basis for

measuring service quality. Later on it was emphasized that SERVQUAL provides the

strong support for defining SQ as the discrepancy between customers’ expectations

and perceptions. Many studies support that expectations, performance, and

disconfirmation are key in the formulation of customer attitudes but the instrument of

SERVQUAL does take it into consideration. However, it is contended that this

instrument is designed merely to measure perceived SQ- an attitude level- at a given

point in time regardless of the process by which it is formed.

C&T’ conclusion that the 22 SERVQUAL items form a one-dimensional scale

is unwarranted. However, replications studies have shown significant correlations

among the five dimensions originally derived for SERVQUAL. Therefore, exploring

why and how the five device quality dimensions are interrelated is a fertile area for

additional research. Pursuing such a research avenue would be more appropriate for

advancing our understanding of SQ than hastily discarding the multidimensional

nature of the construct (Parasuraman, Zeithaml, & Berry, Reassessment of

Expectations as a Comparison Standard in Measuring Service Quality:Implications

for Further Research, 1994).

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 20/66

14

The relationship of causality between SQ and CS is an important unresolved

issue that C&T’s article addresses empirically and Teas’ article conceptually though

the former concludes that SQ leads to CS, and not vice versa. Specifically, the view

held by many service quality researchers that CS leads to SQ is at odds with the

causal direction implied in models specified by CS researchers. These differences

could be owing to the global or overall attitude focus in most SQ research in contrast

to the transaction specific focus in most CS research.

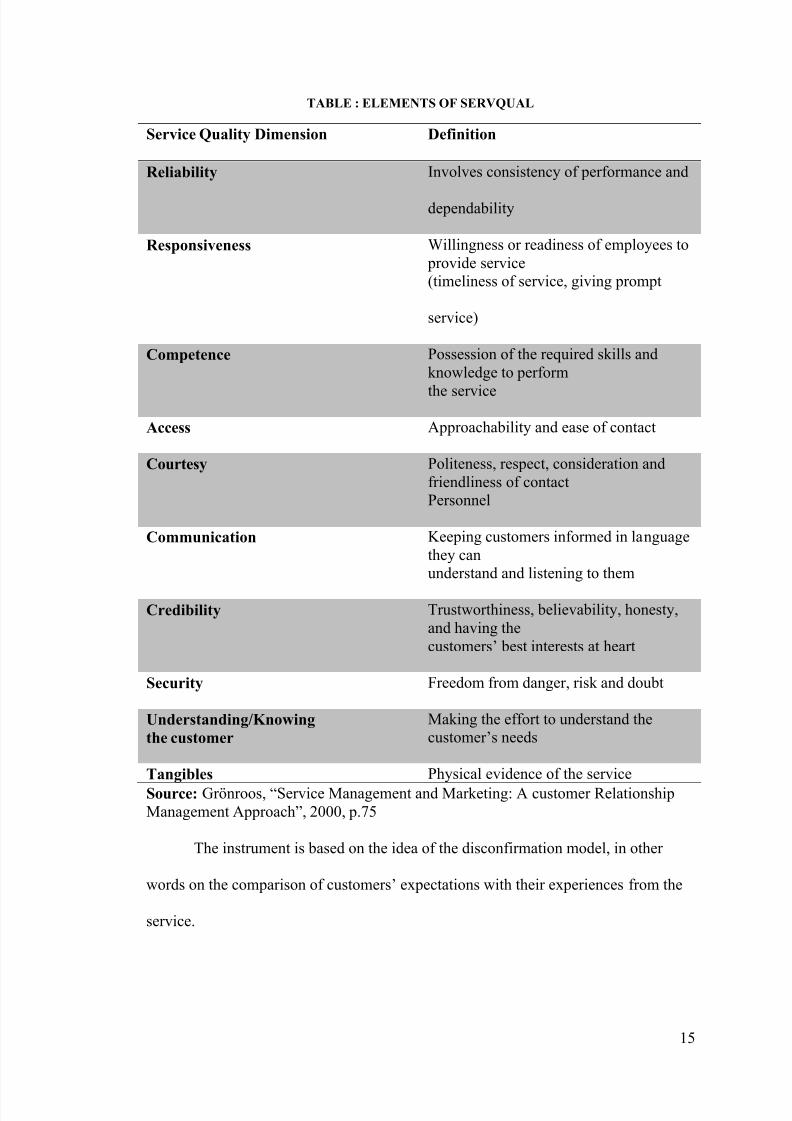

ServQual is an instrument of customer’s perception of the quality of service.

Developed by Parasuraman and his colleagues this model determines the dimensions

or attributes of service for measuring it. Initially this instrument included 10 service

quality dimensions, which were later reduced to the following five: tangibles,

reliability, responsiveness, assurance and empathy (Kenova & Jonasson, 2006).

The following table describes the initial 10 elements of the ServQual

instrument.

Transaction

Satisfaction

Evaluation of

Service Qualit

Evaluation of

roduct Qualit

Evaluation of Price

FIGURE : COMPONENT OF TRANSACTION SPECIFIC EVALUATION

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 21/66

15

TABLE : ELEMENTS OF SERVQUAL

Service Quality Dimension Definition

Reliability Involves consistency of performance and

dependability

Responsiveness Willingness or readiness of employees to

provide service

(timeliness of service, giving prompt

service)

Competence Possession of the required skills and

knowledge to perform

the service

Access Approachability and ease of contact

Courtesy Politeness, respect, consideration and

friendliness of contact

Personnel

Communication Keeping customers informed in language

they can

understand and listening to them

Credibility Trustworthiness, believability, honesty,

and having the

customers’ best interests at heart

Security Freedom from danger, risk and doubt

Understanding/Knowing

the customer

Making the effort to understand the

customer’s needs

Tangibles Physical evidence of the service

Source: Grönroos, “Service Management and Marketing: A customer Relationship

Management Approach”, 2000, p.75

The instrument is based on the idea of the disconfirmation model, in other

words on the comparison of customers’ expectations with their experiences from the

service.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 22/66

16

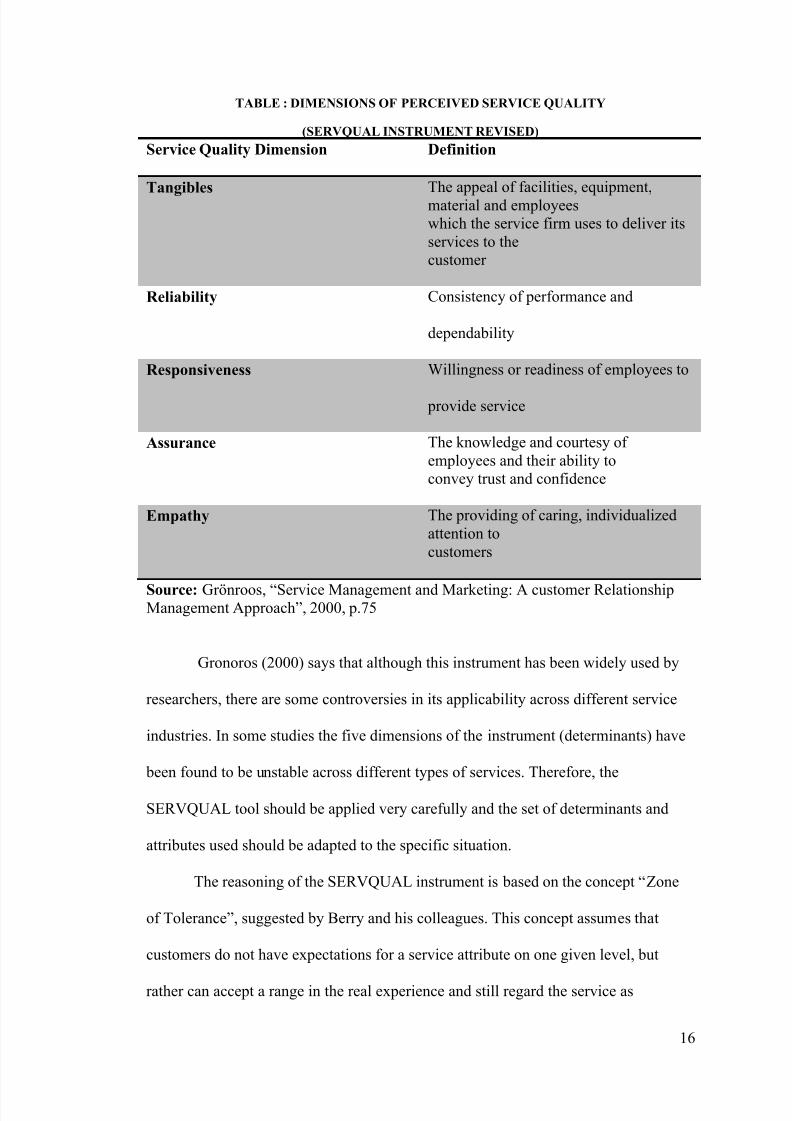

TABLE : DIMENSIONS OF PERCEIVED SERVICE QUALITY

(SERVQUAL INSTRUMENT REVISED)

Service Quality Dimension Definition

Tangibles The appeal of facilities, equipment,

material and employees

which the service firm uses to deliver its

services to the

customer

Reliability Consistency of performance and

dependability

Responsiveness Willingness or readiness of employees to

provide service

Assurance The knowledge and courtesy of

employees and their ability to

convey trust and confidence

Empathy The providing of caring, individualized

attention to

customers

Source: Grönroos, “Service Management and Marketing: A customer RelationshipManagement Approach”, 2000, p.75

Gronoros (2000) says that although this instrument has been widely used by

researchers, there are some controversies in its applicability across different service

industries. In some studies the five dimensions of the instrument (determinants) have

been found to be unstable across different types of services. Therefore, the

SERVQUAL tool should be applied very carefully and the set of determinants and

attributes used should be adapted to the specific situation.

The reasoning of the SERVQUAL instrument is based on the concept “Zone

of Tolerance”, suggested by Berry and his colleagues. This concept assumes that

customers do not have expectations for a service attribute on one given level, but

rather can accept a range in the real experience and still regard the service as

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 23/66

17

satisfactory. The borders of the customer’s “Zone of tolerance” are formed by a

Desired Level – the level on which the customers believe the service should be, and

an Adequate Level – the minimum level of service that customers are willing to

accept. Customers consider the service performance which falls within the borders of

this “Zone of Tolerance” to be good.

According to the study conducted by Cowling and Newman in 1995

concerning the SERVQUAL scale, one bank found out that the highest disparity

between the expectations and perceptions of customers was found to exist for

reliability, responsiveness, and empathy, and the lowest for tangibles. Also,

concerning the banking industry, by using the critical incident technique, Johnston

(1995) examined the service quality perceptions of the customers. He found out 18

service quality attributes: access, aesthetics, attentiveness/helpfulness, availability,

care, cleanliness/tidiness, comfort, commitment, communication, competence,

courtesy, flexibility, friendliness, functionality, integrity, reliability, responsiveness

and security. Furthermore, an alternative measure of service quality in retail banking

that comprises 31 items with six underlying key dimensions was proposed by Bahia

and Nantel (2000). These six dimensions are: effectiveness and assurance, access,

price, tangibles, service portfolio and reliability. In addition, by using conjoint

experiments to measure the service quality of retail banks, Oppewal and Vriens

(2000) proposed the use of 28 attributes including four service quality dimensions to

evaluate service quality. These four dimensions are: accessibility, competence,

accuracy and friendliness, and tangibles. Of those four dimensions, the most

important in determining banking preference turned out to be the accuracy and

friendliness, followed by competence, tangibles and accessibility.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 24/66

18

2.4 E-Banking Services

E-Banking services are banking services delivered over the Internet. The

services provided by banks over the Internet that once entailed only checking of

accounts, have recently risen to include a full range of banking services. It is not rare

the case nowadays, when approximately all services accessible at the branch or by

phone can be accessed on the Internet as well. The development of technology allows

banks to offer not only “branch- based” services over the Internet, but also new Value

Added Services which are available only online such as electronic commerce, real-

time brokerage, financial information menus, e-mail alerts and third party services

(tax payment, portals or management of electricity bills). The increased use of online

banking services has many advantages for both customers and banks. For customers,

E-banking services allow them to have better overview of their banking business and

help them to manage their banking transactions more conveniently and fast.

Additionally, customers who use Internet banking prove to be involved in more

banking transactions, which is beneficial for the banks themselves. Moreover, through

the Internet, the bank productivity increases as well, as the distribution and production

of their services become more efficient. Customers’ motivation to use E-banking

services rises from a number of factors which include freedom of time and space,

speed, convenience, 24 hours a day availability and price incentives.

Among all the advantages the Internet offers to both banks and their customers

in terms of increased productivity and reduced costs, it also hides a lot of

disadvantages and challenges for the service providers especially the Islamic banks

who have low acceptability and less branches as compare to the conventional banks.

On the Internet, the comparison between different service offerings is much easier and

switching costs are lower, which makes it easier for customers to change service

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 25/66

19

providers. This, on its behalf, posts a challenge for the banks to not only acquire new

customers, but retain their existing ones as well. To retain its customers, banks should

try to make them satisfied with their services and offerings and this can be achieved

through delivering high quality services. Delivering high quality online services

requires understanding of the online service quality dimensions considered crucial and

trying to improve the quality of the services provided over the Internet, so that a

competitive advantage is gained (Kenova & Jonasson, 2006)

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 26/66

20

CHAPTER THREERESEARCH METHODOLOGY

The “Methodology” describes the different research methods and gives explanation of

those chosen methods for a study and the reason for the choice. Furthermore, this

chapter will describe the chosen sampling technique, the way the data for the study

chosen, and the statistical technique used to analyze the data.

3.1 Research Design

The design of the research is a path that leads the whole research work from

starting point to the end. It is like the blueprint of research work, which defines the

whole research process. It describes the type of research, variables and their

relationships, sphere of the research and its limitations etc.

The area of “online banking” in the sphere of Islamic banking is not new to

the researcher. There is a considerable volume of research work in the area, though

the literature of Islamic banking is under the development process yet. We chose

descriptive study keeping in view the research work already done in the field of

Islamic banking. Descriptive research is carried out in those areas where a lot of

research work has been done and basic understanding of the variables and their effects

has been established. Our research design is based on a pre-developed tool for the

testing of quality of service, commonly known as SERVQUAL. In describing the

effects and relationships of the variables involved this tool will serve as a scale.

An understanding of the variables and the scale has already been established

using secondary data collection through literature review in the previous chapter. The

data for the research purpose will be collected using questionnaire developed on the

basis of the literature review.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 27/66

21

3.1.1 Population of the Study

Population of the study refers to the entire group of people, events or things of

interest i.e. the whole universe of the area of study. In our research all bank customers

of Islamic as well as conventional banks who use internet banking services are our

population of the study.

3.1.2 Element of the Study

Element of the study means each individual unit of the population. In our

study it refers to each online banking user is our element of the study.

3.1.3 Sample of the Study

Sampling means selecting a few elements out of whole population for the

purpose of study as studying the whole population is impossible. Sample is selected

using some pre-determined method. Keeping in view the limitations applied to this

study, we chose convenient sampling. We selected only those respondents for the

purpose of our research who were easily available and willing to provide information.

We chose a sample of 100 respondents from different areas of Lahore city, mostly

from the down-town area. Out of total 100 respondents 50 uses Islamic online

banking services, and remaining 50 uses conventional online banking services.

3.1.4 Sphere of the Study

Sphere of the study describe the applicability of the research work. In our case

the applicability of the research is very limited as we chose only the area of Lahore

city keeping in view the time and cost limitations.

3.2 Variables

In our study of the previous literature about the topic eight variables are

identified which effect the consumers’ perception about the e-services quality. These

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 28/66

22

variables are Efficiency, Fulfillment, System Availability, Privacy, Assurance/ Trust,

Site Aesthetics, Responsiveness and Contact.

Efficiency refers to the agility of online context and processing speed of the

transactions being carried out. Fulfillment refers to the accuracy of the transactions

and the information being disseminated to the customer. System Availability, as the

name suggest, refers the online availability of the system. Privacy refers to both the

security of online content as well as bank’s vigilance to ensure the security of

customers’ transaction. Assurance / Trust shows the level of confidence customers put

in the name of bank. This also indicates the brand image of the bank. Site aesthetics

refers to the attractiveness of the bank site to the customer and its logical designing.

Responsiveness delineates the bank’s response time to resolve the customer queries

and customers’ satisfaction with that. Contact refers to the ease of contact for the

customer to put any query or to seek for guidance while working online.

3.3 Data Collection

Data collection is paramount in the research work and quality of data ensures

the quality of research work. Data collection is carried out in two different stages.

Firstly data is collected for understanding of the topic of the research and building

research design. This data is mostly collected using already published research work

and other sources like Internet, library books, Govt. censures etc. Such data is called

Secondary Data. This constitute the second chapter of our study i.e. Literature

Review. We collected our secondary data mostly through online available journals

and articles through Internet.

Secondly, data is collected specifically for the topic of interest using tools like

questionnaires, surveys, interviews, group discussion etc. Such data collected

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 29/66

23

typically by the researcher himself is called Primary Data. We developed a

questionnaire using the variables identified from the secondary data or literature

review, for the purpose of primary data collection. The questionnaires were personally

administered by the researchers to the respondents and have filled thereof.

3.4 Data Analysis

Data analysis is an important step in the research process. It involves not only

analyzing data for interpretation but also for possible errors of omission or

perceptional biases etc. The type of analysis to be carried out depends on the type of

data collected. In the case of quantitative data, which is the data collected in this

study, statistical tools are applied to quantify the data collected and interpreting

thereafter. With the advent of computer technology this analysis and interpretation

can be performed by special developed software called SPSS. We used SPSS

version14.0 and Microsoft Excel for the purpose of our data analysis.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 30/66

24

CHAPTER FOURDATA ANALYSIS

The data gathered through questionnaire will be analyzed using SPSS and

Microsoft Excel software. In order to make our analysis comprehensive and easy to

understand, the data interpretation will be assisted with bar-chart diagrams. This data

analysis comprises of the comparison of data collected against eight variable of

interest and two categories of banks.

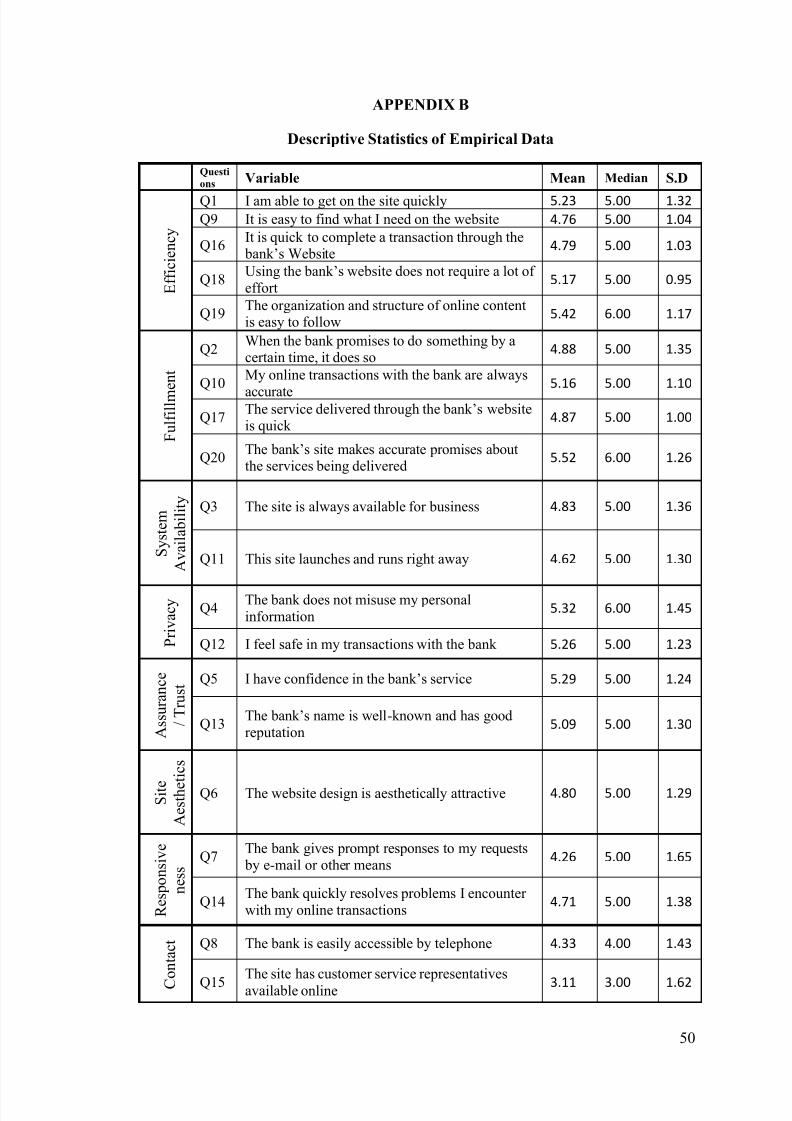

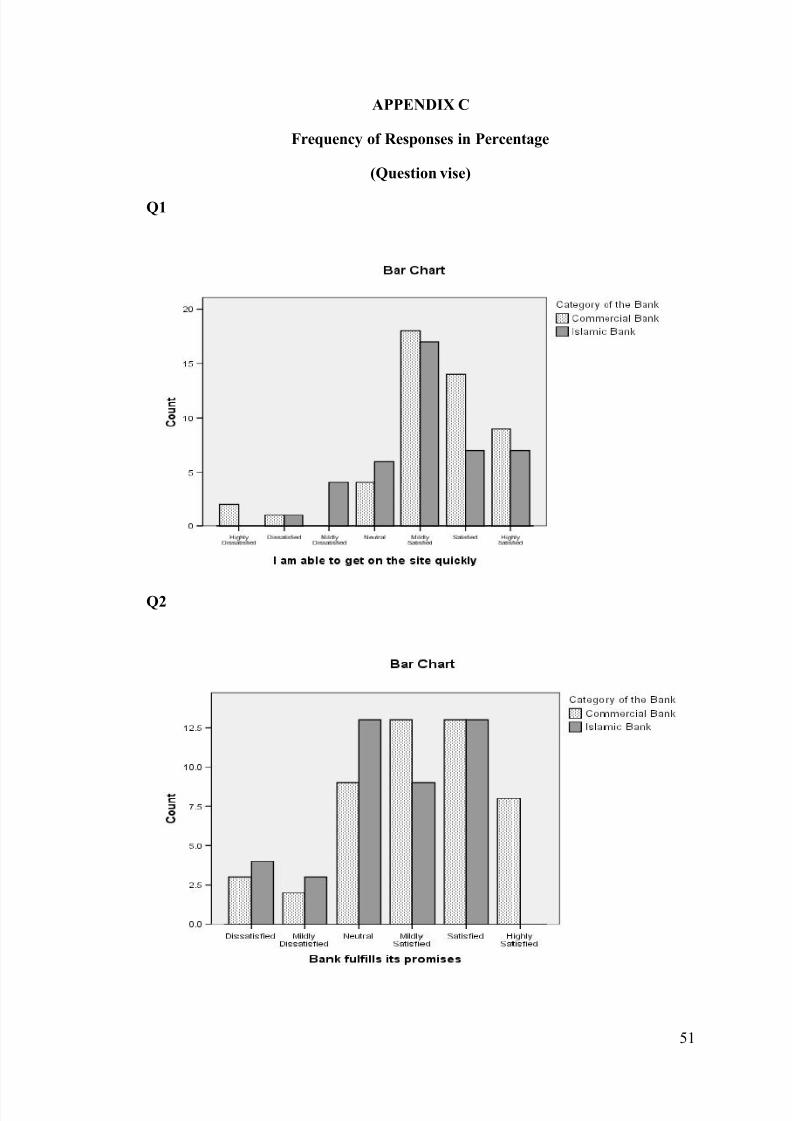

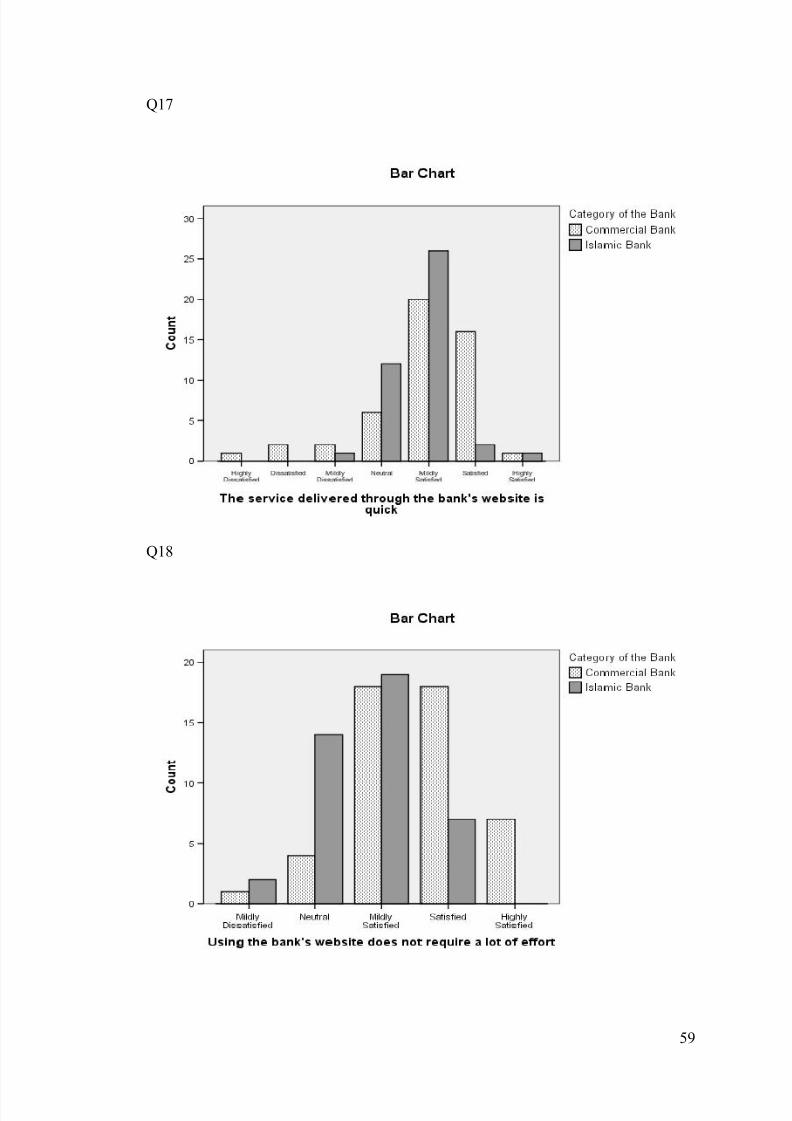

4.1 Efficiency

The first variable of interest “Efficiency” comprises of five questions in the

questionnaire i.e. Q1, Q9, Q16, Q18 and Q19. The analysis of the independent

questions has been shown in the Appendix C. The overall mean of 5.23 shows that

more than 60% of total respondent lies in satisfied region of the scale. In order to

arrive at the conclusion regarding the difference of service quality in Islamic and

Commercial banks, we used cross-tabulation of Efficiency and category of the bank.

The results are as follows:

TABLE : CROSS-TABULATION OF EFFICIENCY AND CATEGORY OF THE BANK

Category of the Bank

C.Bs I.Bs Total

Efficiency Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11 Neutral Count 2.00 7.00 9.00

% of Total 2.22 7.78 10.00

Mildly

Satisfied

Count 29.00 34.00 63.00

% of Total 32.22 37.78 70.00

Satisfied Count 16.00 1.00 17.00

% of Total 17.78 1.11 18.89

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 31/66

25

FIGURE : GRAPHICAL REPRESENTATION OF TABLE 3

As efficiency envelops the simplicity, proper structure, and minimum

information input while using e-banking services, the above bars speak in favor of the

Islamic banks surpassing the mildly satisfied bar in comparison to the commercial

banks. The bar diagram says that no customer is dissatisfied with the completion

content of the website of the Islamic banks, whilst 1.11% are dissatisfied with speed

of the commercial banks. This may aptly be attributed to larger size of the banks and

large number of transaction that hinder the process of completion and access to the

services. Though Islamic banks are in the emerging phase in Pakistan yet the data

show efficient services provided by them. These results can be considered rewarding

for the banks as this feature is fairly important, because it helps to determine the

efficiency of the provided online banking services.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 32/66

26

Conclusively, although the speed of completing transactions through the

banks’ websites seems rather satisfactory for most of the respondents, the time it takes

for the overall online services to be delivered should still be improved.

4.2 FulfillmentThe second variable of interest “Fulfillment” represents four questions in the

questionnaire i.e. Q2, Q10, Q17 and Q20. The analysis of independent questions has

been shown in Appendix C. This variable has a mean of 5.11 along with median of

5.25 and standard deviation of 1.18, suggesting that at least more than 50% of total

respondents show satisfaction with this variable. The results are as follows:

TABLE : CROSS-TABULATION OF FULFILLMENT AND CATEGORY OF THE BANK

Category of the Bank

C.Bs I.Bs Total

Fulfillment Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Mildly Dissatisfied Count 0.00 2.00 2.00

% of Total 0.00 2.22 2.22

Neutral Count 2.00 4.00 6.00

% of Total 2.22 4.44 6.67

Mildly Satisfied Count 21.00 25.00 46.00

% of Total 23.33 27.78 51.11

Satisfied Count 24.00 11.00 35.00

% of Total 26.67 12.22 38.89

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 33/66

27

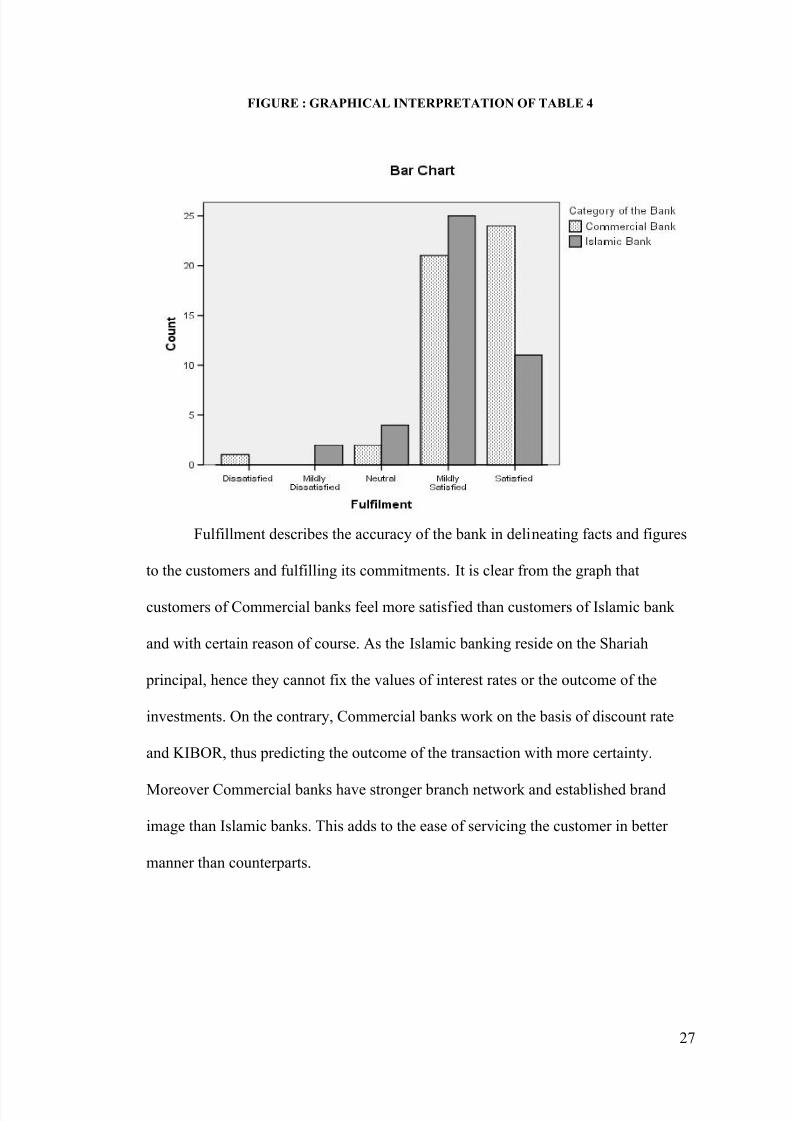

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 4

Fulfillment describes the accuracy of the bank in delineating facts and figures

to the customers and fulfilling its commitments. It is clear from the graph that

customers of Commercial banks feel more satisfied than customers of Islamic bank

and with certain reason of course. As the Islamic banking reside on the Shariah

principal, hence they cannot fix the values of interest rates or the outcome of the

investments. On the contrary, Commercial banks work on the basis of discount rate

and KIBOR, thus predicting the outcome of the transaction with more certainty.

Moreover Commercial banks have stronger branch network and established brand

image than Islamic banks. This adds to the ease of servicing the customer in better

manner than counterparts.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 34/66

28

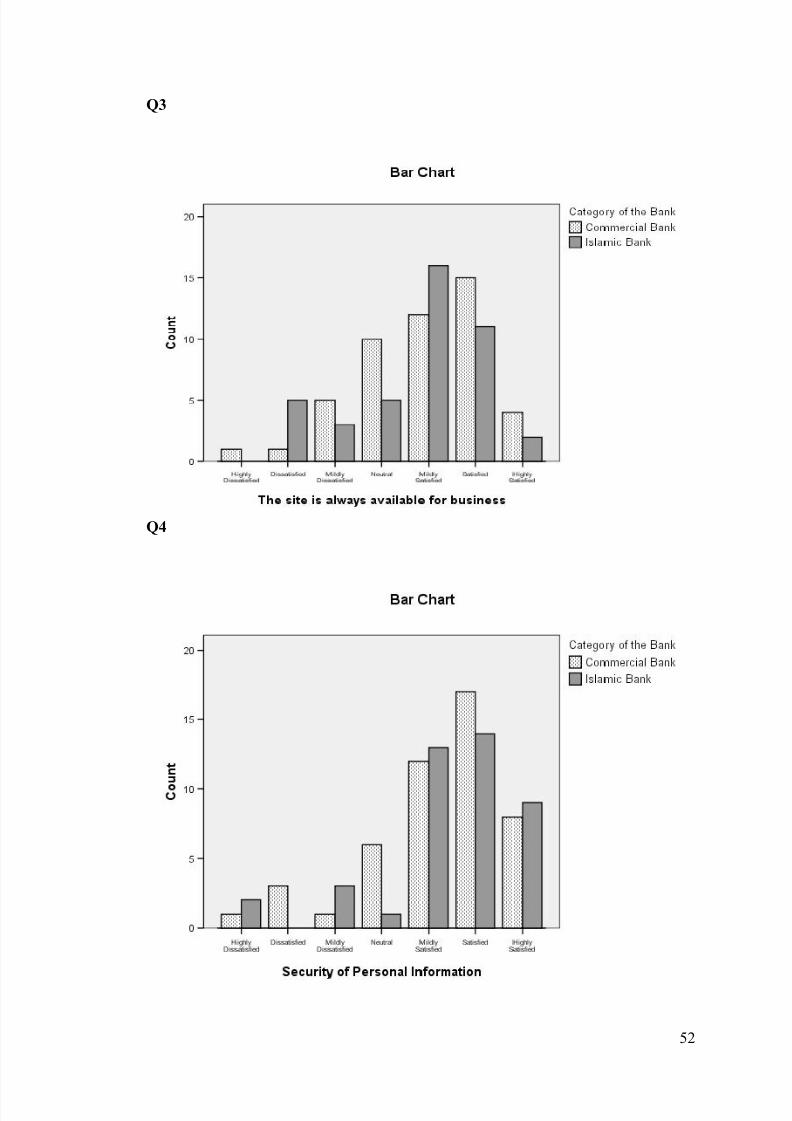

4.3 System AvailabilityThird variable of interest “System Availability” is derived from two questions

in the questionnaire i.e. Q3 and Q11. The results of the data shows an overall mean of

4.73 with median 5 and standard deviation of 1.33, suggesting that below 60% of the

total respondents show satisfaction with the variable. The results are as follows:

TABLE : CROSS-TABULATION OF SYSTEM AVAILABILITY AND CATEGORY OF THE

BANK

Category of the Bank

C.Bs I.Bs Total

System

Availability

Highly Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Mildly Dissatisfied Count 1.00 7.00 8.00

% of Total 1.11 7.78 8.89

Neutral Count 11.00 4.00 15.00

% of Total 12.22 4.44 16.67

Mildly Satisfied Count 15.00 15.00 30.00

% of Total 16.67 16.67 33.33

Satisfied Count 18.00 16.00 34.00

% of Total 20.00 17.78 37.78

Highly Satisfied Count 2.00 0.00 2.00

% of Total 2.22 0.00 2.22

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 5

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 35/66

29

The system availability encapsulates the readiness of the website whenever

and wherever is needed. The result catches the satisfaction level for both the category

of banking in the tolerance level. About 30% of the commercial banks’ customers are

satisfied with this faced of the system availability, whilst the zone of tolerance against

the Islamic banks is found to be 28%. It is encouraging for the Islamic banks that their

highly dissatisfaction part of the “dissatisfaction zone” is free of any bar. So they have

an active opportunity to maintain it while touching their high satisfaction zone though

seems negligible in the bar-chart mentioned.

The commercial banks owing to their larger size of transaction and period of

longevity have higher satisfaction level that comparatively not a big one. So they need

an expeditious and ad-hoc strategy to improve their satisfaction zone and to nip their

dissatisfaction zone also.

4.4 PrivacyFourth variable of interest “Privacy” comprises of two questions in

questionnaires i.e. Q4 and Q12. The result of independent questions has been shown

in appendix C. The overall result shows mean of 5.29, median of 5.50 and standard

deviation of 3.34, suggesting that more than 60% of the total respondents have shown

satisfaction with this variable. The results are as follows:

TABLE : CROSS-TABULATION OF PRIVACY AND CATEGORY OF THE BANK

Category of the Bank

C.Bs I.Bs Total

Privacy Highly Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Mildly Dissatisfied Count 2.00 2.00 4.00

% of Total 2.22 2.22 4.44

Neutral Count 4.00 4.00 8.00

% of Total 4.44 4.44 8.89Mildly Satisfied Count 16.00 10.00 26.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 36/66

30

% of Total 17.78 11.11 28.89

Satisfied Count 17.00 15.00 32.00

% of Total 18.89 16.67 35.56

Highly Satisfied Count 8.00 11.00 19.00

% of Total 8.89 12.22 21.11

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

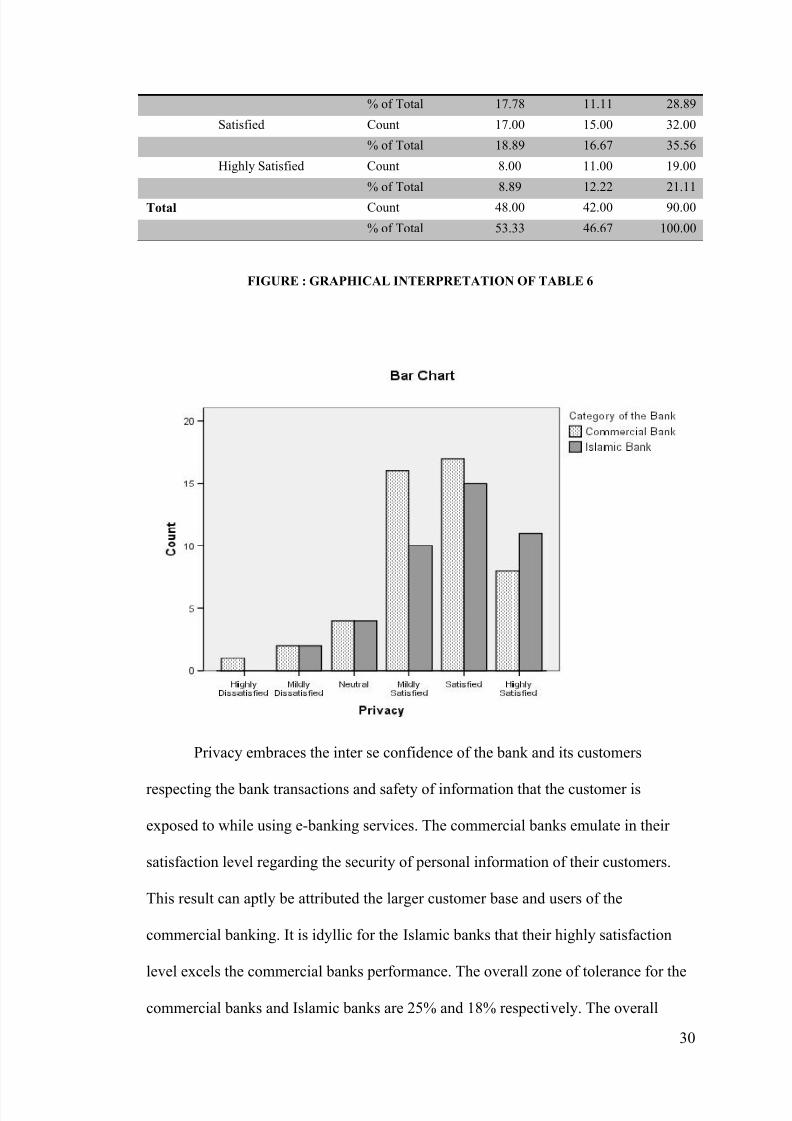

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 6

Privacy embraces the inter se confidence of the bank and its customers

respecting the bank transactions and safety of information that the customer is

exposed to while using e-banking services. The commercial banks emulate in their

satisfaction level regarding the security of personal information of their customers.

This result can aptly be attributed the larger customer base and users of the

commercial banking. It is idyllic for the Islamic banks that their highly satisfaction

level excels the commercial banks performance. The overall zone of tolerance for the

commercial banks and Islamic banks are 25% and 18% respectively. The overall

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 37/66

31

dissatisfaction level for the Islamic banks is waving nil while for the commercial

banks hoisting at 1.11%.

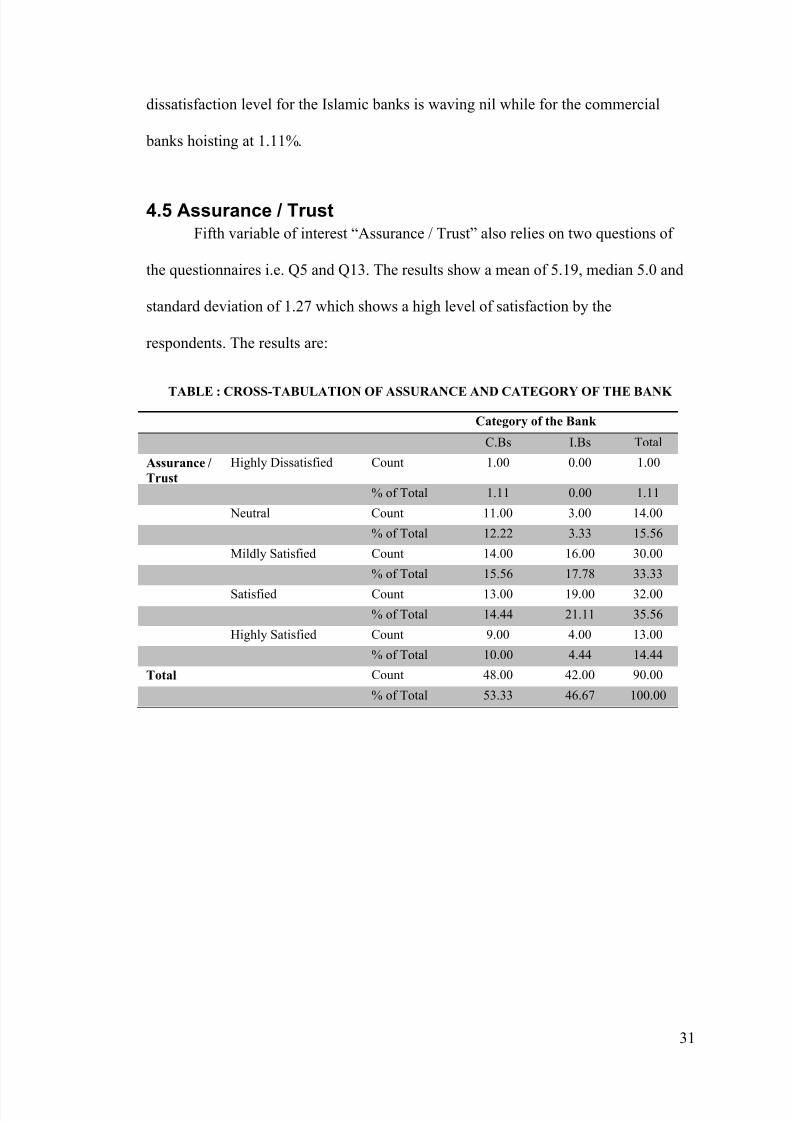

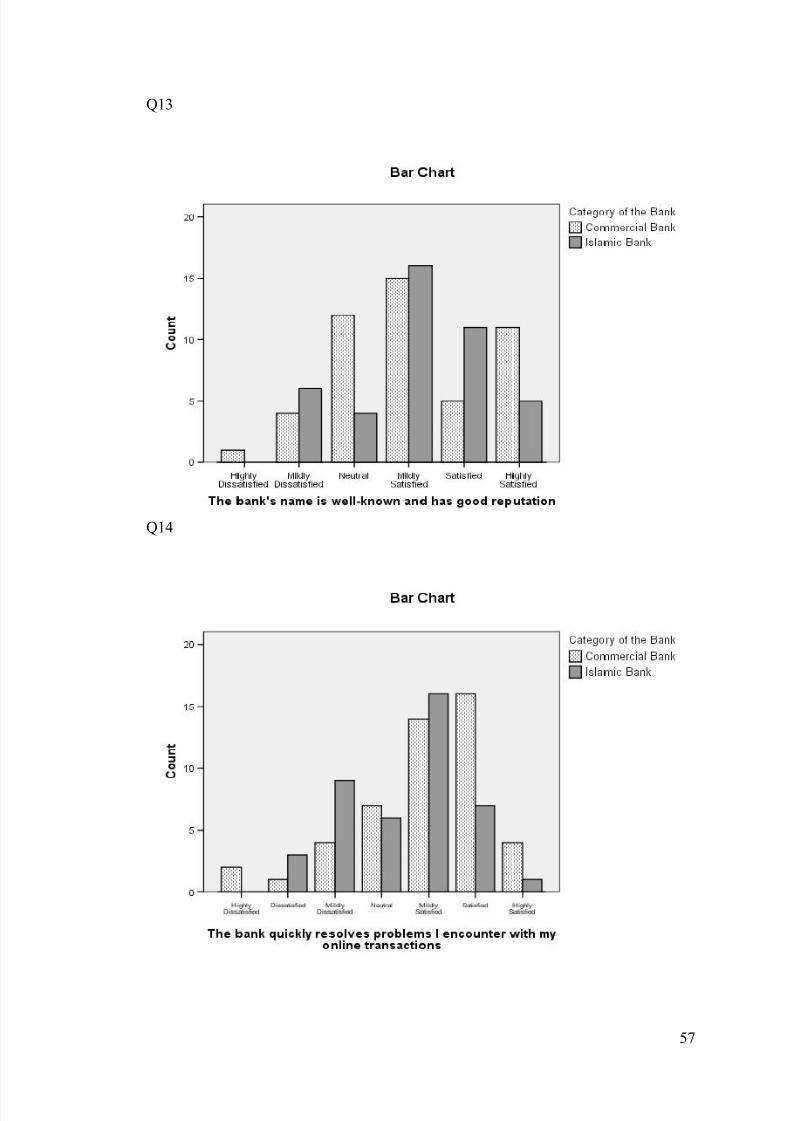

4.5 Assurance / TrustFifth variable of interest “Assurance / Trust” also relies on two questions of

the questionnaires i.e. Q5 and Q13. The results show a mean of 5.19, median 5.0 and

standard deviation of 1.27 which shows a high level of satisfaction by the

respondents. The results are:

TABLE : CROSS-TABULATION OF ASSURANCE AND CATEGORY OF THE BANK

Category of the Bank

C.Bs I.Bs Total

Assurance /

Trust

Highly Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Neutral Count 11.00 3.00 14.00

% of Total 12.22 3.33 15.56

Mildly Satisfied Count 14.00 16.00 30.00

% of Total 15.56 17.78 33.33

Satisfied Count 13.00 19.00 32.00

% of Total 14.44 21.11 35.56

Highly Satisfied Count 9.00 4.00 13.00

% of Total 10.00 4.44 14.44

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 38/66

32

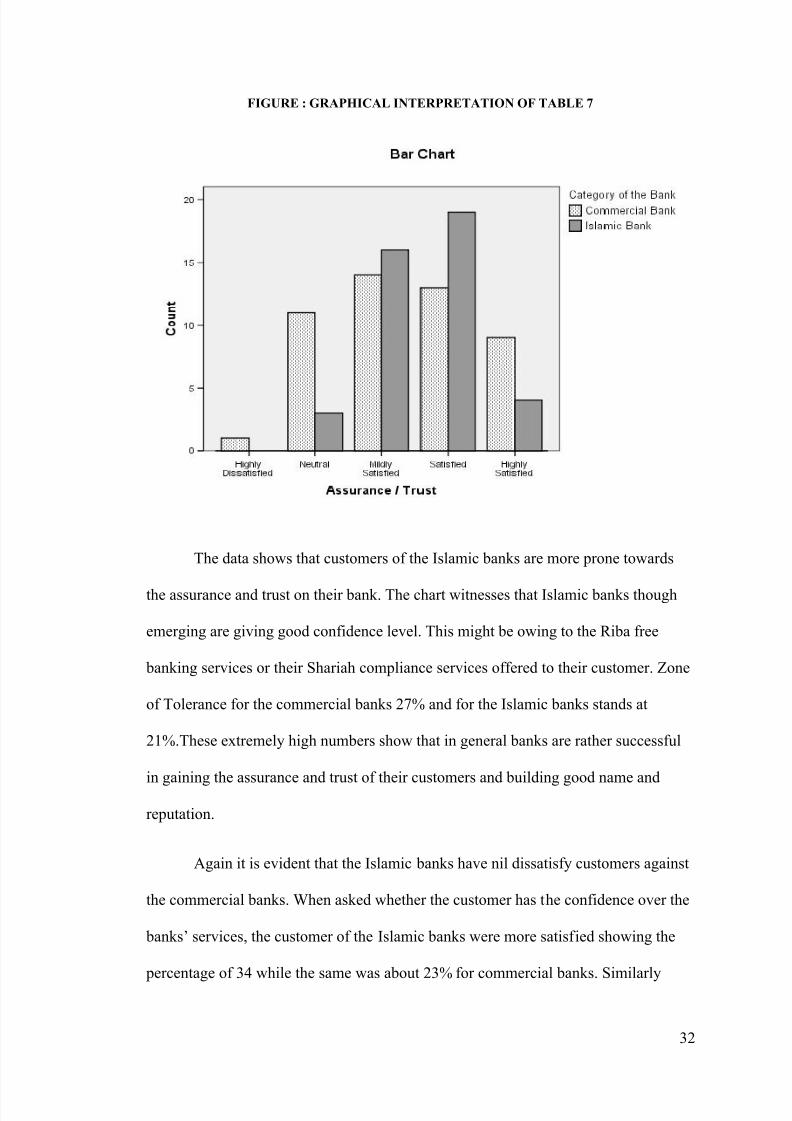

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 7

The data shows that customers of the Islamic banks are more prone towards

the assurance and trust on their bank. The chart witnesses that Islamic banks though

emerging are giving good confidence level. This might be owing to the Riba free

banking services or their Shariah compliance services offered to their customer. Zone

of Tolerance for the commercial banks 27% and for the Islamic banks stands at

21%.These extremely high numbers show that in general banks are rather successful

in gaining the assurance and trust of their customers and building good name and

reputation.

Again it is evident that the Islamic banks have nil dissatisfy customers against

the commercial banks. When asked whether the customer has the confidence over the

banks’ services, the customer of the Islamic banks were more satisfied showing the

percentage of 34 while the same was about 23% for commercial banks. Similarly

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 39/66

33

highly satisfied customer of the Islamic banks surpassed with 17% on the same

question against 16% of commercial banks. In comparison, customers of the Islamic

bank seemed to be most satisfied with aspects of the service such as: well-known

name and reputation of the bank.

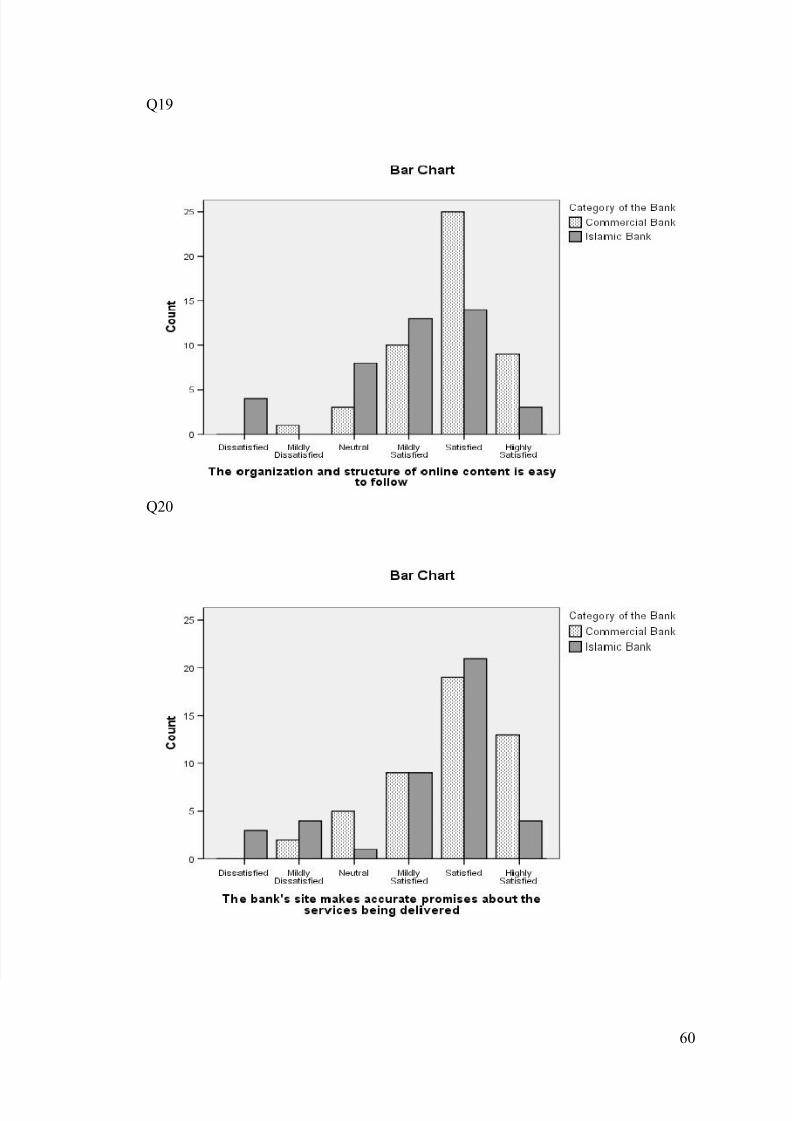

4.6 Site Aesthetics

Site aesthetics has only one question Q6 in the questionnaire. It has a mean of

4.8 median 5.0 and standard deviation of 1.29 which means there is considerable high

dissatisfaction for this variable though overall trend shows satisfaction among the

respondents. The results are:

TABLE : CROSS-TABULATION OF SITE AESTHETICS AND CATEGORY OF THE BANK

Category of the Bank Total

C.Bs I.Bs

Site

Aesthetics

Dissatisfied Count 0.00 4.00 4.00

% of Total 0.00 4.44 4.44

Mildly Dissatisfied Count 10.00 3.00 13.00

% of Total 11.11 3.33 14.44

Neutral Count 6.00 9.00 15.00

% of Total 6.67 10.00 16.67

Mildly Satisfied Count 18.00 12.00 30.00

% of Total 20.00 13.33 33.33

Satisfied Count 11.00 10.00 21.00

% of Total 12.22 11.11 23.33

Highly Satisfied Count 3.00 4.00 7.00

% of Total 3.33 4.44 7.78

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 40/66

34

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 8

“Site Aesthetics” signifies the web-characteristic of the banks. On the basis of

count, the site aesthetics of the commercial banks are more soothing and pleasant as

compared to the Islamic banks. The zone of tolerance for the commercial banks

calculated to be 37% against 26% of the Islamic banks. The satisfaction zone of both

the categories is same while the dissatisfaction zone of the 4.44% of Islamic banks

stands against 0.00% of the commercial banks. This signals that the Islamic banks

should make their site aesthetically attractive towards their customers to promote and

excel in the field of e-banking services thus enhancing their profitability through

virtual banking.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 41/66

35

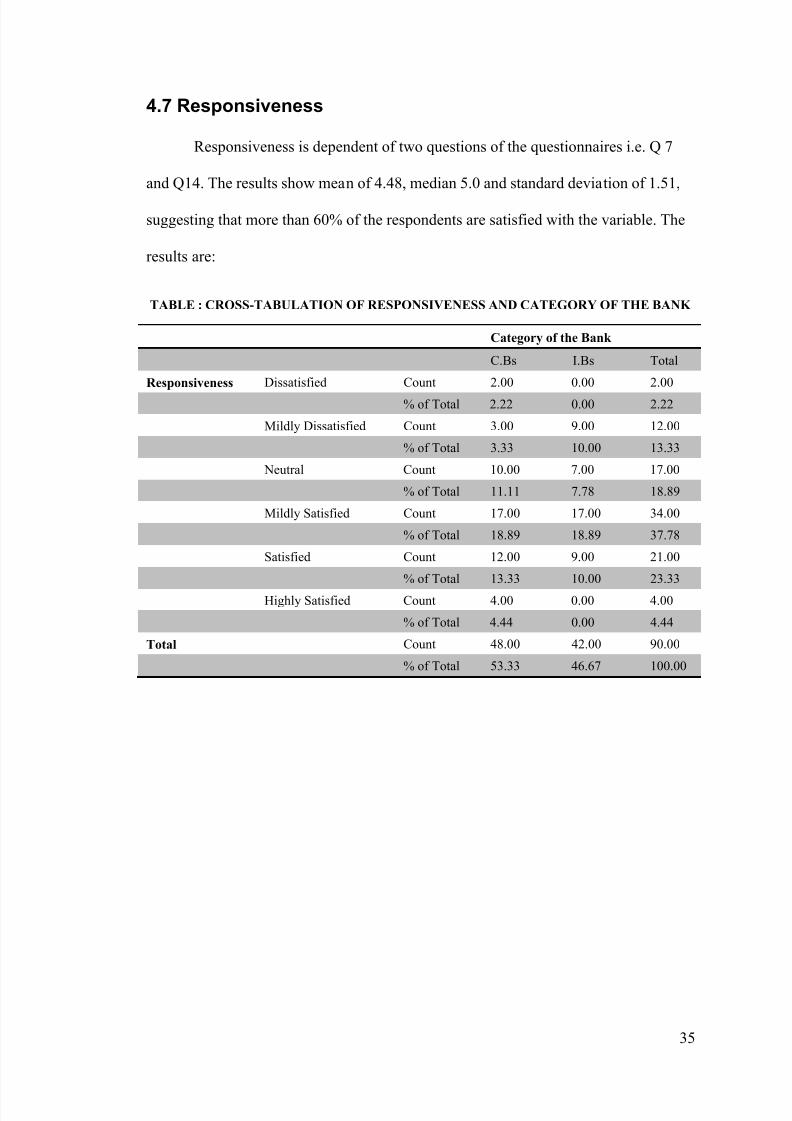

4.7 Responsiveness

Responsiveness is dependent of two questions of the questionnaires i.e. Q 7

and Q14. The results show mean of 4.48, median 5.0 and standard deviation of 1.51,

suggesting that more than 60% of the respondents are satisfied with the variable. The

results are:

TABLE : CROSS-TABULATION OF RESPONSIVENESS AND CATEGORY OF THE BANK

Category of the Bank

C.Bs I.Bs Total

Responsiveness Dissatisfied Count 2.00 0.00 2.00

% of Total 2.22 0.00 2.22

Mildly Dissatisfied Count 3.00 9.00 12.00

% of Total 3.33 10.00 13.33

Neutral Count 10.00 7.00 17.00

% of Total 11.11 7.78 18.89

Mildly Satisfied Count 17.00 17.00 34.00

% of Total 18.89 18.89 37.78

Satisfied Count 12.00 9.00 21.00

% of Total 13.33 10.00 23.33

Highly Satisfied Count 4.00 0.00 4.00

% of Total 4.44 0.00 4.44

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 42/66

36

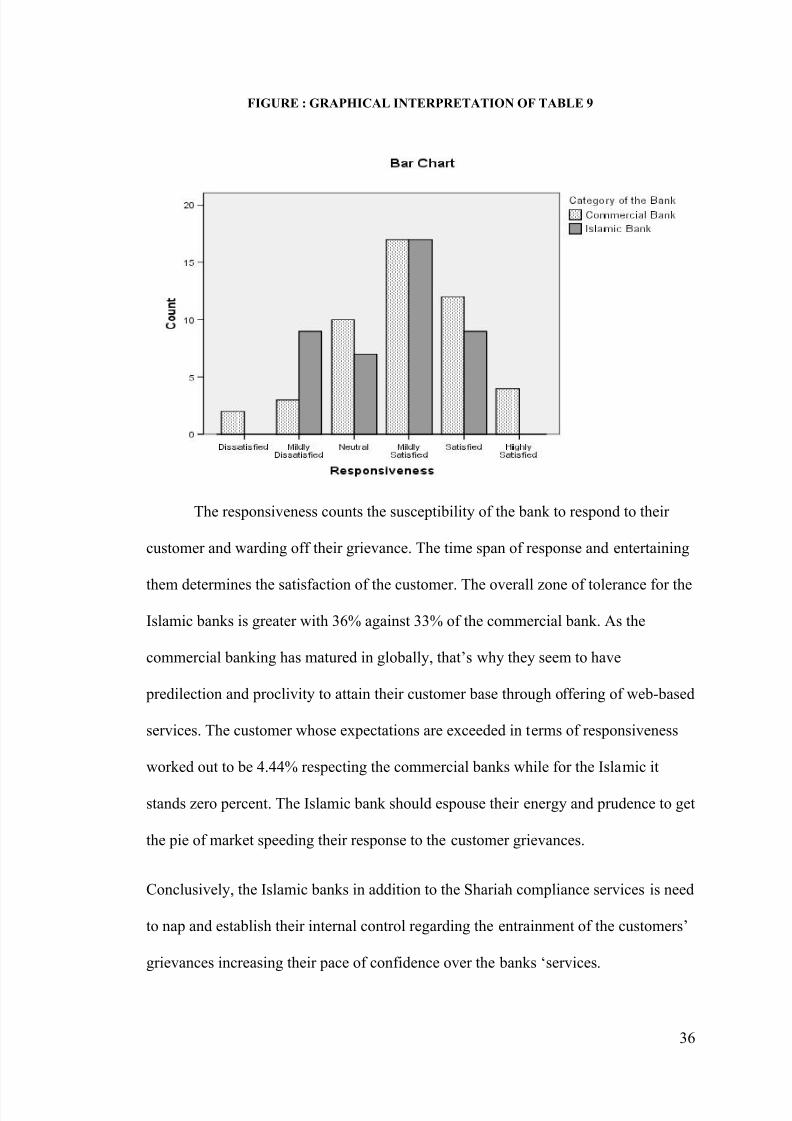

FIGURE : GRAPHICAL INTERPRETATION OF TABLE 9

The responsiveness counts the susceptibility of the bank to respond to their

customer and warding off their grievance. The time span of response and entertaining

them determines the satisfaction of the customer. The overall zone of tolerance for the

Islamic banks is greater with 36% against 33% of the commercial bank. As the

commercial banking has matured in globally, that’s why they seem to have

predilection and proclivity to attain their customer base through offering of web-based

services. The customer whose expectations are exceeded in terms of responsiveness

worked out to be 4.44% respecting the commercial banks while for the Islamic it

stands zero percent. The Islamic bank should espouse their energy and prudence to get

the pie of market speeding their response to the customer grievances.

Conclusively, the Islamic banks in addition to the Shariah compliance services is need

to nap and establish their internal control regarding the entrainment of the customers’

grievances increasing their pace of confidence over the banks ‘services.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 43/66

37

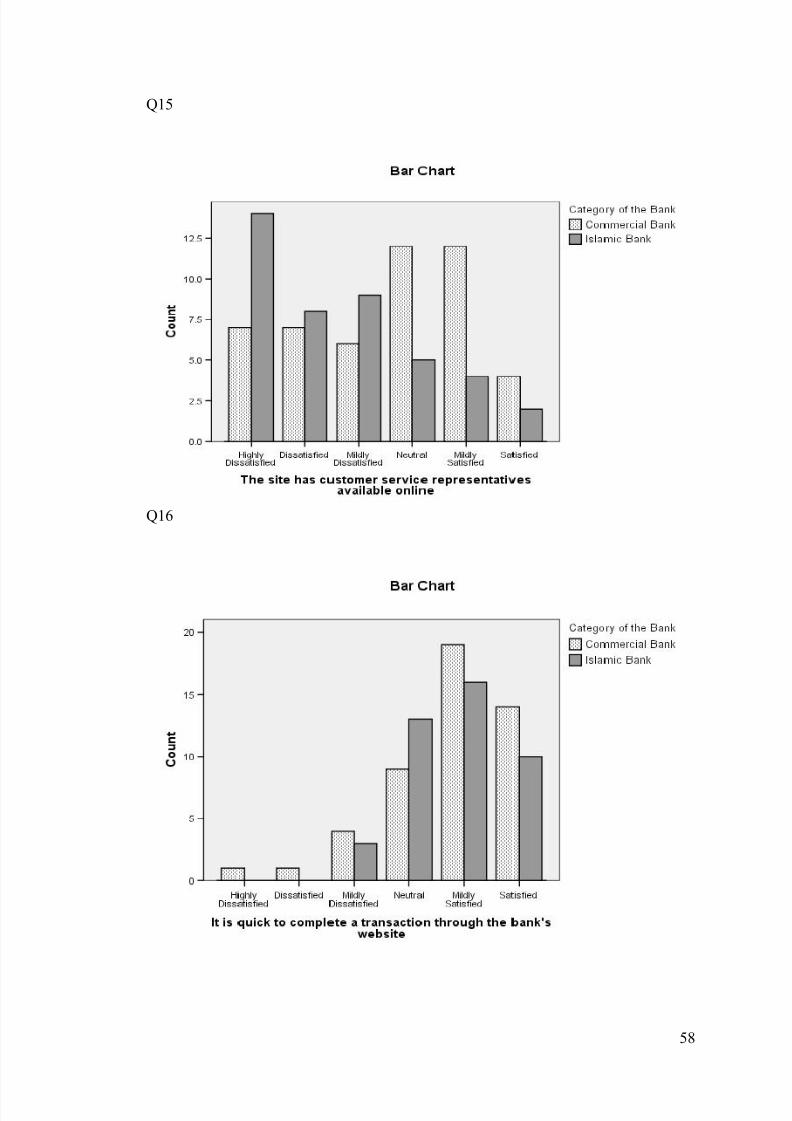

4.8 ContactThe last variable of interest is “Contact” which depends on two questions of

the questionnaires i.e. Q8 and Q15. The results indicate mean of 3.72, median 3.50

and standard deviation of 1.52, which suggest a high level of dissatisfaction of the

respondents with the variable. The results are:

TABLE : CROSS-TABULATION OF CONTACT AND CATEGORY OF THE BANK

Category of the Bank Total

C.Bs I.Bs

Contact Highly Dissatisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Dissatisfied Count 4.00 2.00 6.00

% of Total 4.44 2.22 6.67

Mildly Dissatisfied Count 11.00 18.00 29.00

% of Total 12.22 20.00 32.22

Neutral Count 10.00 12.00 22.00

% of Total 11.11 13.33 24.44

Mildly Satisfied Count 15.00 8.00 23.00

% of Total 16.67 8.89 25.56

Satisfied Count 6.00 2.00 8.00

% of Total 6.67 2.22 8.89

Highly Satisfied Count 1.00 0.00 1.00

% of Total 1.11 0.00 1.11

Total Count 48.00 42.00 90.00

% of Total 53.33 46.67 100.00

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 44/66

38

FIGURE : GRAPHICAL REPRESENTATION OF TABLE 10

The feature of contact is interlinked with the banks response to their

customers. The most of the commercial bank’ customers responded mild

dissatisfaction. But the overall Zone of Tolerance was satisfactory for both the

categories of the bank with 40% and 42% for the commercial and Islamic banks

respectively. When asked whether the bank is accessible by the customer through the

telephone, majority were neutral in this respect while the customers of the Islamic

banks are witnessed mildly satisfied with big number when compared with

commercial banks’ customers (Appendix D).

Regarding the online representative availability, the Islamic bank sketches a

long bar in the highly dissatisfaction section of the scale, presumably, owing to the

cost incurring and the small number of the e-banking transaction of the Islamic banks.

In comparison, the situation in the same aspect seems controlled amongst the

commercial bank as evident from the same Appendix.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 45/66

39

CHAPTER FIVECONCLUSION AND DISCUSSION

The final Chapter of the study Conclusion and Discussion entails a detailed overview

of the results and in the light of the independent commenting made in the previous

chapter a complete result of the study. This is also important as this chapter actually

depicts our learning and understanding of the topic. This conclusion and the

discussion might not be widely applicable pertaining to the limitations of the study

but it does add knowledge in the literature of Islamic Banking versus Commercial

Banking studies.

5.1 ConclusionTaking into consideration the huge investments banks make in Internet

infrastructure, customer satisfaction and retention are turning into the crucial factors

for success in online banking meaning that the generation of positive customer value

on the Internet requires the establishment of long-term customer relationships. Our

study instrument for measuring the quality of online banking services consists of one

scale with total of eight quality dimensions: Assurance/Trust, Site Aesthetics,

Contact, Privacy, System Availability, Fulfillment, Responsiveness and Efficiency.

According to the conducted study, these are the service quality dimensions that banks

should consider when evaluating the quality of their online banking services.

Furthermore, twenty items are used to describe these eight dimensions. Banks might

use the eighteen items described in this work to measure the quality of their online

services along the eight different dimensions of service quality assessed in the study.

Based on the performed evaluations mentioned above, the following

conclusions can be made. First of all, most customers of both the category of banks

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 46/66

40

(Islamic and Conventional) have shown dissatisfaction or indifference with the

following aspects of the online banking services: prompt responses of the bank to

customers’ requests; design of the bank’s website; quickly solution of customers’

problems; the easiness to reach the bank by telephone and the easiness to find what

the customer needs on the website. Secondly, both the category of banks seem to

perform very well on the System Availability and Efficiency dimensions of the

offered online services as those dimensions rank highest on satisfaction of customers.

Finally, the aspects consistently ranking highest on dissatisfaction is Website

Characteristics i.e., Site Aesthetics which should be considered from banks’ managers

for immediate amendment. Islamic banks seem less concentrated and focused on this

aspect of the e-banking service quality.

Furthermore, what is interesting to be observed is that the aspects of the online

services on which banks rank higher in satisfaction of customers like System

Availability and Efficiency are not specific for the Internet context, but are typical for

the traditional settings as well. In comparison, the aspect of the E-banking services on

which banks rank higher in dissatisfaction like the Website Characteristics dimension

are more Internet specific. A reason for that might be that banks do not consider this

feature important for the quality of their E-services and have concentrated their efforts

on the other aspects of the online services. Nevertheless, because of the lack of human

interaction in the online space, it should not be forgotten that the website is the

“moment of truth” between customers and their banks as far as E-banking services are

concerned, and as such the website should be consistent with the total quality efforts

of the service provider, meaning that a high quality website is an important aspect of

the offered online banking services.

8/13/2019 Quality of e-banking services Islamic vs. Commercial Banks

http://slidepdf.com/reader/full/quality-of-e-banking-services-islamic-vs-commercial-banks 47/66

41

5.2 Discussions

In our thesis we have arrived at many a finding bridging the questionnaire

developed to assess the quality of E-banking services. The research conducted shows

that banks especially the Islamic bank have huge potential to tape and broaden the

customer base and cementing its presence in the financial environment in the country.

Furthermore, it should be taken into consideration that this attempt has led to a lot of

findings which needs to be further tested and modified based on surveys conducted

with higher number of respondents from different age-groups and national contexts.

Interestingly Islamic banks competed with the quality of E-banking services of the

long established commercial banks, including some of which are predominately

Internet based like Standard Chartered Ltd. This suggests a huge potential for the

Islamic bank in the banking sector of Pakistan.

In addition, owing to the time and cost of our thesis, it has a poor