Quail West Foundation, Inc. Financial Report December 31, 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Quail West Foundation, Inc.

Financial Report December 31, 2020

Contents

Independent auditor’s report 1-2

Financial statements

Balance sheets 3

Statements of revenues, expenses and changes in members’ equity 4-5

Statements of cash flows 6-7

Notes to financial statements 8-17

Required supplementary information on future major repairs and replacements (unaudited) 18-19

Independent auditor’s report on the supplementary information 20

Supplementary information

Statements of revenues and expenses information:

Departmental schedules of certain revenues and expenses 21-22

Schedules of certain revenues and expenses – allocated operating activities 23

1

Independent Auditor’s Report

Board of Directors Quail West Foundation, Inc.

Report on the Financial Statements We have audited the accompanying financial statements of Quail West Foundation, Inc. (the Foundation), which comprise the balance sheets as of December 31, 2020 and 2019, the related statements of revenues, expenses and changes in members’ equity and cash flows for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Foundation’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Foundation’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

2

Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Quail West Foundation, Inc. as of December 31, 2020 and 2019, and its revenues, expenses and changes in its members’ equity and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matter Accounting principles generally accepted in the United States of America require that the supplementary information on future major repairs and replacements on pages 18 and 19 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Financial Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Naples, Florida March 2, 2021

3

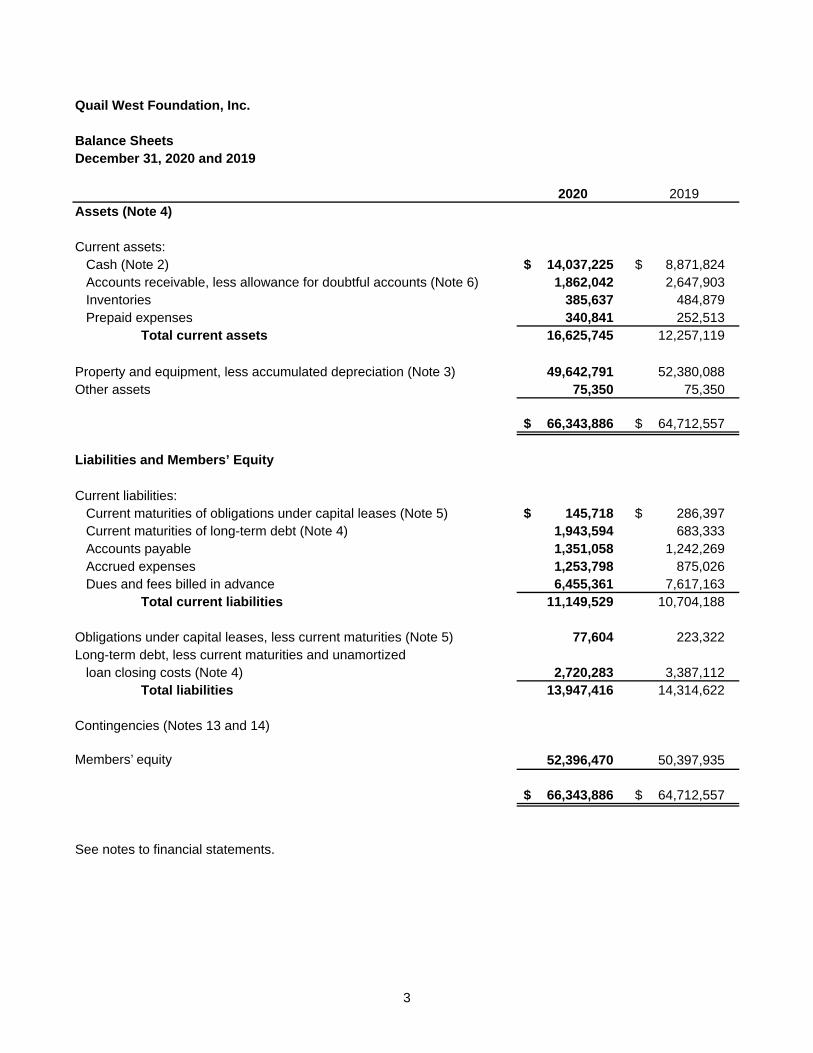

Quail West Foundation, Inc.

Balance SheetsDecember 31, 2020 and 2019

2020 2019Assets (Note 4)

Current assets:Cash (Note 2) 14,037,225 $ 8,871,824 $ Accounts receivable, less allowance for doubtful accounts (Note 6) 1,862,042 2,647,903 Inventories 385,637 484,879 Prepaid expenses 340,841 252,513

Total current assets 16,625,745 12,257,119

Property and equipment, less accumulated depreciation (Note 3) 49,642,791 52,380,088 Other assets 75,350 75,350

66,343,886 $ 64,712,557 $

Liabilities and Members’ Equity

Current liabilities:Current maturities of obligations under capital leases (Note 5) 145,718 $ 286,397 $ Current maturities of long-term debt (Note 4) 1,943,594 683,333 Accounts payable 1,351,058 1,242,269 Accrued expenses 1,253,798 875,026 Dues and fees billed in advance 6,455,361 7,617,163

Total current liabilities 11,149,529 10,704,188

Obligations under capital leases, less current maturities (Note 5) 77,604 223,322 Long-term debt, less current maturities and unamortized

loan closing costs (Note 4) 2,720,283 3,387,112 Total liabilities 13,947,416 14,314,622

Contingencies (Notes 13 and 14)

Members’ equity 52,396,470 50,397,935

66,343,886 $ 64,712,557 $

See notes to financial statements.

4

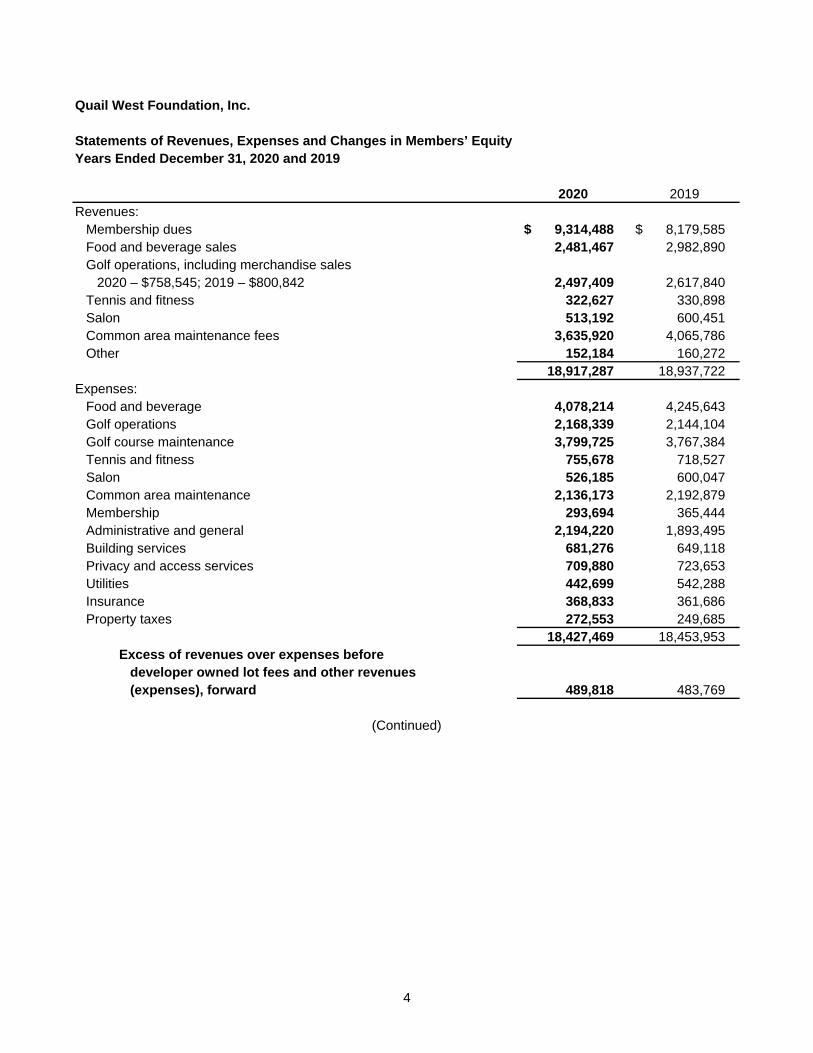

Quail West Foundation, Inc.

Statements of Revenues, Expenses and Changes in Members’ EquityYears Ended December 31, 2020 and 2019

2020 2019Revenues:

Membership dues 9,314,488 $ 8,179,585 $ Food and beverage sales 2,481,467 2,982,890 Golf operations, including merchandise sales

2020 – $758,545; 2019 – $800,842 2,497,409 2,617,840 Tennis and fitness 322,627 330,898 Salon 513,192 600,451 Common area maintenance fees 3,635,920 4,065,786 Other 152,184 160,272

18,917,287 18,937,722 Expenses:

Food and beverage 4,078,214 4,245,643 Golf operations 2,168,339 2,144,104 Golf course maintenance 3,799,725 3,767,384 Tennis and fitness 755,678 718,527 Salon 526,185 600,047 Common area maintenance 2,136,173 2,192,879 Membership 293,694 365,444 Administrative and general 2,194,220 1,893,495 Building services 681,276 649,118 Privacy and access services 709,880 723,653 Utilities 442,699 542,288 Insurance 368,833 361,686 Property taxes 272,553 249,685

18,427,469 18,453,953 Excess of revenues over expenses before

developer owned lot fees and other revenues(expenses), forward 489,818 483,769

(Continued)

5

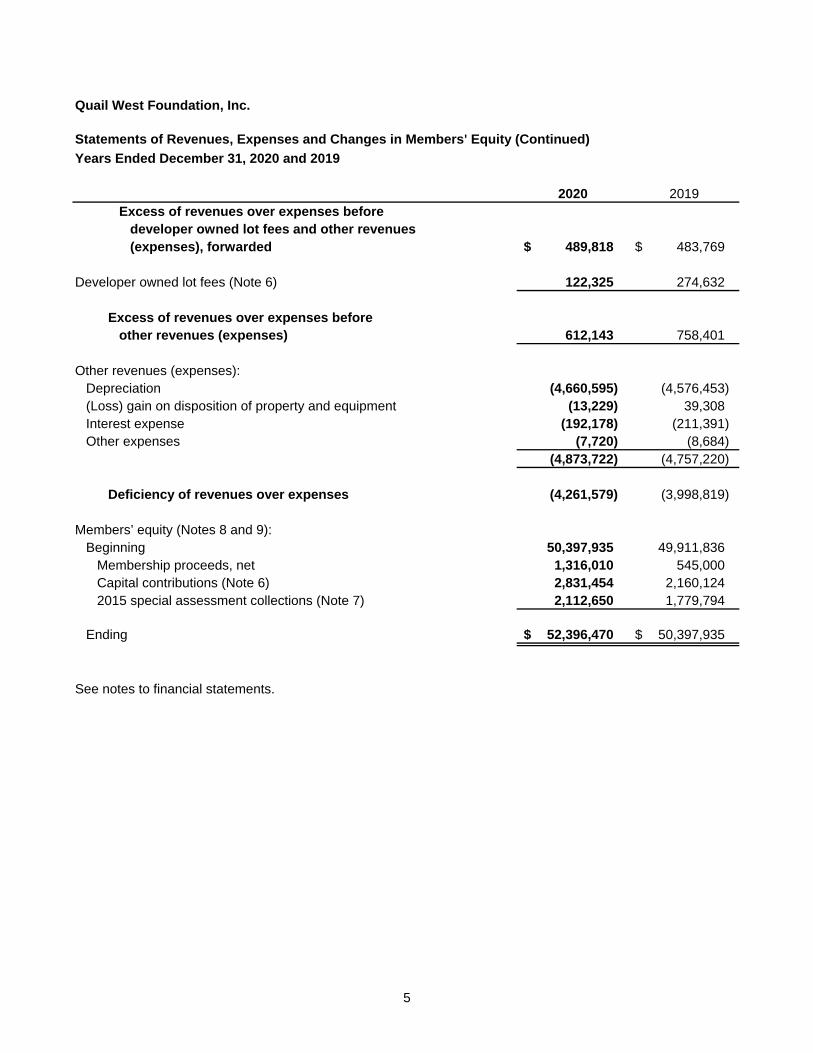

Quail West Foundation, Inc.

Statements of Revenues, Expenses and Changes in Members' Equity (Continued)

Years Ended December 31, 2020 and 2019

2020 2019Excess of revenues over expenses before

developer owned lot fees and other revenues(expenses), forwarded 489,818 $ 483,769 $

Developer owned lot fees (Note 6) 122,325 274,632

Excess of revenues over expenses before other revenues (expenses) 612,143 758,401

Other revenues (expenses):Depreciation (4,660,595) (4,576,453) (Loss) gain on disposition of property and equipment (13,229) 39,308 Interest expense (192,178) (211,391) Other expenses (7,720) (8,684)

(4,873,722) (4,757,220)

Deficiency of revenues over expenses (4,261,579) (3,998,819)

Members’ equity (Notes 8 and 9):Beginning 50,397,935 49,911,836

Membership proceeds, net 1,316,010 545,000 Capital contributions (Note 6) 2,831,454 2,160,124 2015 special assessment collections (Note 7) 2,112,650 1,779,794

Ending 52,396,470 $ 50,397,935 $

See notes to financial statements.

6

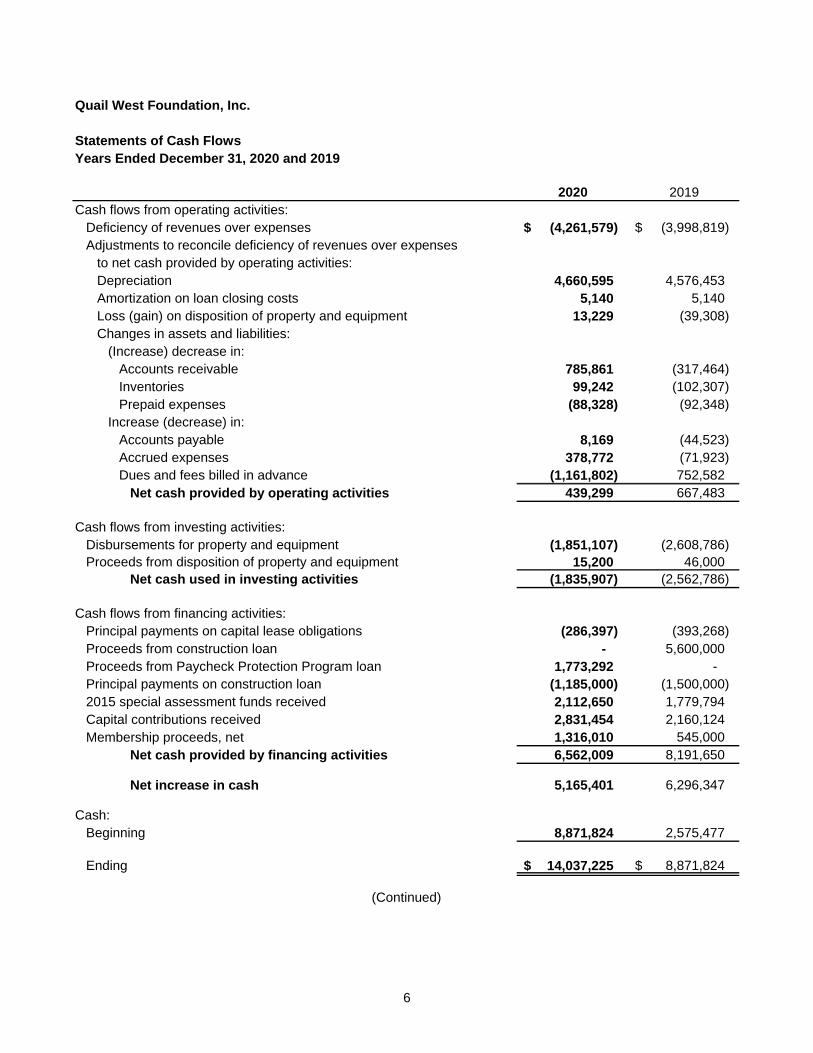

Quail West Foundation, Inc.

Statements of Cash FlowsYears Ended December 31, 2020 and 2019

2020 2019Cash flows from operating activities:

Deficiency of revenues over expenses (4,261,579) $ (3,998,819) $ Adjustments to reconcile deficiency of revenues over expenses

to net cash provided by operating activities:Depreciation 4,660,595 4,576,453 Amortization on loan closing costs 5,140 5,140 Loss (gain) on disposition of property and equipment 13,229 (39,308) Changes in assets and liabilities:

(Increase) decrease in:Accounts receivable 785,861 (317,464) Inventories 99,242 (102,307) Prepaid expenses (88,328) (92,348)

Increase (decrease) in:Accounts payable 8,169 (44,523) Accrued expenses 378,772 (71,923) Dues and fees billed in advance (1,161,802) 752,582

Net cash provided by operating activities 439,299 667,483

Cash flows from investing activities:Disbursements for property and equipment (1,851,107) (2,608,786) Proceeds from disposition of property and equipment 15,200 46,000

Net cash used in investing activities (1,835,907) (2,562,786)

Cash flows from financing activities:Principal payments on capital lease obligations (286,397) (393,268) Proceeds from construction loan - 5,600,000 Proceeds from Paycheck Protection Program loan 1,773,292 - Principal payments on construction loan (1,185,000) (1,500,000) 2015 special assessment funds received 2,112,650 1,779,794 Capital contributions received 2,831,454 2,160,124 Membership proceeds, net 1,316,010 545,000

Net cash provided by financing activities 6,562,009 8,191,650

Net increase in cash 5,165,401 6,296,347

Cash:Beginning 8,871,824 2,575,477

Ending 14,037,225 $ 8,871,824 $

(Continued)

7

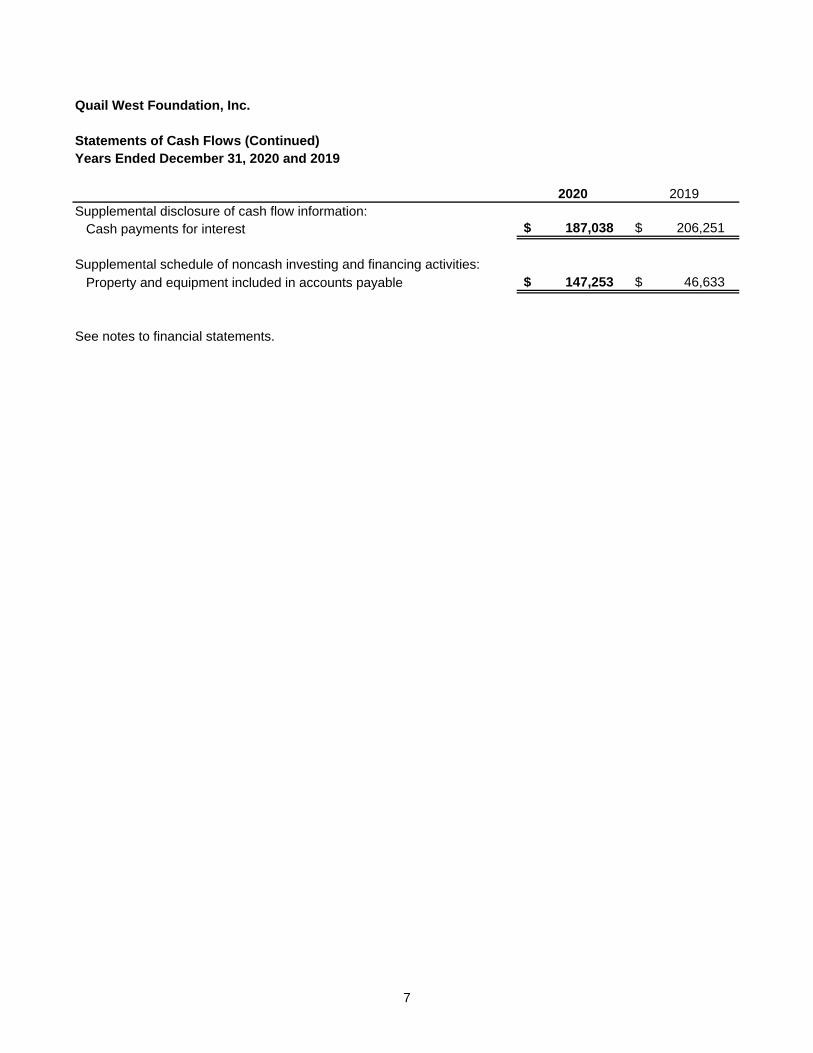

Quail West Foundation, Inc.

Statements of Cash Flows (Continued)Years Ended December 31, 2020 and 2019

2020 2019Supplemental disclosure of cash flow information:

Cash payments for interest 187,038 $ 206,251 $

Supplemental schedule of noncash investing and financing activities:Property and equipment included in accounts payable 147,253 $ 46,633 $

See notes to financial statements.

Quail West Foundation, Inc. Notes to Financial Statements

8

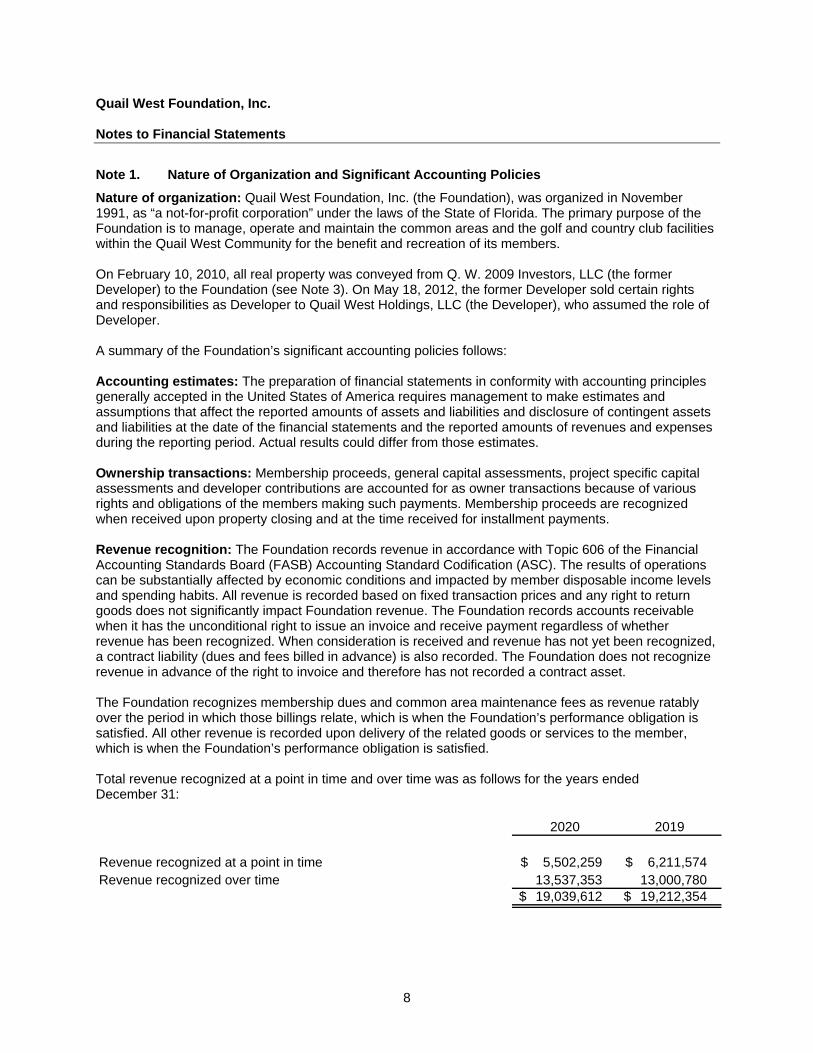

Note 1. Nature of Organization and Significant Accounting Policies

Nature of organization: Quail West Foundation, Inc. (the Foundation), was organized in November 1991, as “a not-for-profit corporation” under the laws of the State of Florida. The primary purpose of the Foundation is to manage, operate and maintain the common areas and the golf and country club facilities within the Quail West Community for the benefit and recreation of its members. On February 10, 2010, all real property was conveyed from Q. W. 2009 Investors, LLC (the former Developer) to the Foundation (see Note 3). On May 18, 2012, the former Developer sold certain rights and responsibilities as Developer to Quail West Holdings, LLC (the Developer), who assumed the role of Developer. A summary of the Foundation’s significant accounting policies follows: Accounting estimates: The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Ownership transactions: Membership proceeds, general capital assessments, project specific capital assessments and developer contributions are accounted for as owner transactions because of various rights and obligations of the members making such payments. Membership proceeds are recognized when received upon property closing and at the time received for installment payments. Revenue recognition: The Foundation records revenue in accordance with Topic 606 of the Financial Accounting Standards Board (FASB) Accounting Standard Codification (ASC). The results of operations can be substantially affected by economic conditions and impacted by member disposable income levels and spending habits. All revenue is recorded based on fixed transaction prices and any right to return goods does not significantly impact Foundation revenue. The Foundation records accounts receivable when it has the unconditional right to issue an invoice and receive payment regardless of whether revenue has been recognized. When consideration is received and revenue has not yet been recognized, a contract liability (dues and fees billed in advance) is also recorded. The Foundation does not recognize revenue in advance of the right to invoice and therefore has not recorded a contract asset. The Foundation recognizes membership dues and common area maintenance fees as revenue ratably over the period in which those billings relate, which is when the Foundation’s performance obligation is satisfied. All other revenue is recorded upon delivery of the related goods or services to the member, which is when the Foundation’s performance obligation is satisfied. Total revenue recognized at a point in time and over time was as follows for the years ended December 31:

2020 2019

Revenue recognized at a point in time 5,502,259 $ 6,211,574 $ Revenue recognized over time 13,537,353 13,000,780

19,039,612 $ 19,212,354 $

Quail West Foundation, Inc.

Notes to Financial Statements

9

Note 1. Nature of Organization and Significant Accounting Policies (Continued)

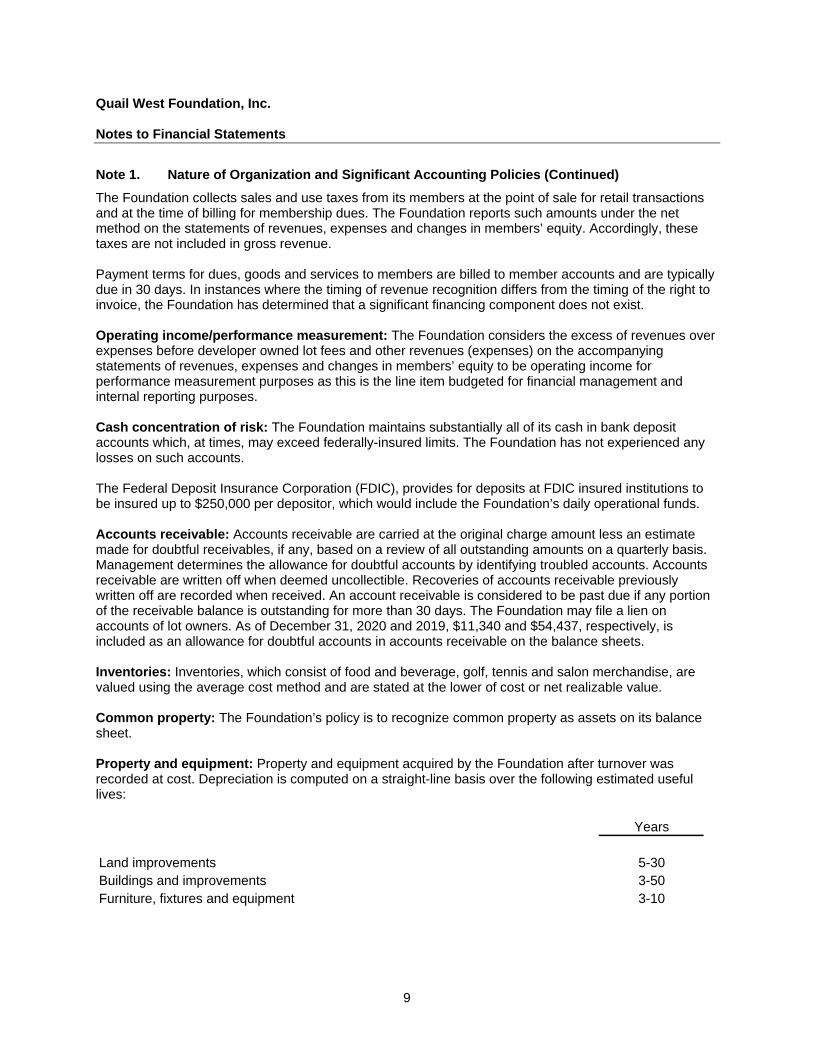

The Foundation collects sales and use taxes from its members at the point of sale for retail transactions and at the time of billing for membership dues. The Foundation reports such amounts under the net method on the statements of revenues, expenses and changes in members’ equity. Accordingly, these taxes are not included in gross revenue.

Payment terms for dues, goods and services to members are billed to member accounts and are typically due in 30 days. In instances where the timing of revenue recognition differs from the timing of the right to invoice, the Foundation has determined that a significant financing component does not exist.

Operating income/performance measurement: The Foundation considers the excess of revenues over expenses before developer owned lot fees and other revenues (expenses) on the accompanying statements of revenues, expenses and changes in members’ equity to be operating income for performance measurement purposes as this is the line item budgeted for financial management and internal reporting purposes.

Cash concentration of risk: The Foundation maintains substantially all of its cash in bank deposit accounts which, at times, may exceed federally-insured limits. The Foundation has not experienced any losses on such accounts.

The Federal Deposit Insurance Corporation (FDIC), provides for deposits at FDIC insured institutions to be insured up to $250,000 per depositor, which would include the Foundation’s daily operational funds.

Accounts receivable: Accounts receivable are carried at the original charge amount less an estimate made for doubtful receivables, if any, based on a review of all outstanding amounts on a quarterly basis. Management determines the allowance for doubtful accounts by identifying troubled accounts. Accounts receivable are written off when deemed uncollectible. Recoveries of accounts receivable previously written off are recorded when received. An account receivable is considered to be past due if any portion of the receivable balance is outstanding for more than 30 days. The Foundation may file a lien on accounts of lot owners. As of December 31, 2020 and 2019, $11,340 and $54,437, respectively, is included as an allowance for doubtful accounts in accounts receivable on the balance sheets.

Inventories: Inventories, which consist of food and beverage, golf, tennis and salon merchandise, are valued using the average cost method and are stated at the lower of cost or net realizable value.

Common property: The Foundation’s policy is to recognize common property as assets on its balance sheet.

Property and equipment: Property and equipment acquired by the Foundation after turnover was recorded at cost. Depreciation is computed on a straight-line basis over the following estimated useful lives:

Years

Land improvements 5-30Buildings and improvements 3-50Furniture, fixtures and equipment 3-10

Quail West Foundation, Inc. Notes to Financial Statements

10

Note 1. Nature of Organization and Significant Accounting Policies (Continued)

Depreciation expense on assets acquired under capital leases is included with depreciation expense on owned assets. Assets under capital leases are amortized over the shorter of their estimated useful lives or the terms of such leases. Unamortized loan closing costs: Loan closing costs are being amortized using the effective interest method over the term of the loan agreement and are present on the balance sheet as a direct reduction to the long-term debt balance. Amortization expenses is included in interest expense on the statement of revenues, expenses and changes in members’ equity. Income taxes: The Foundation is incorporated as a not-for-profit corporation under the laws of the State of Florida, as contained in chapter 617 of the Florida Statutes. However, the Foundation is not exempt from income taxes. For income tax purposes, the Foundation is required to segregate the results of its member activities from its nonmember activities and is separately taxed on each element. Nonmember activity losses may be used to offset member activity profits in current or future periods. Due to the nature of the Foundation’s operations, the Foundation believes it is remote that it would utilize any loss carryforwards. As a result, it is the Foundation’s policy not to record the deferred tax asset and related valuation allowances associated with the carryforwards. The Foundation has evaluated its tax positions and concluded that it has taken no uncertain tax positions that require adjustment to the financial statements to comply with the provisions of the Income Tax Topic of FASB ASC. Recent Accounting Pronouncement: In February 2016, FASB issued ASU 2016-02, Leases (Topic 842). Under the guidance, lessees will be required to recognize at the commencement date for all leases (with the exception of short-term leases): (a) a lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and (b) a right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. Lessees will no longer be provided with a source of off-balance sheet financing. This standard will be effective for fiscal years beginning after December 15, 2021, with early application permitted. Lessees (for capital and operating leases) must apply a modified retrospective transition approach for leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements. The modified retrospective approach would not require any transition accounting for leases that expired before the earliest comparative period presented. Lessees may not apply a full retrospective transition approach. The Foundation is currently evaluating the effect that the updated standard will have on the financial statements. Reclassifications: Certain reclassifications were made to the 2019 financial statements in order to conform to the 2020 presentation, with no net effect on increase in, or balance of, members’ equity. Subsequent events: Management has assessed subsequent events through March 2, 2021, the date the financial statements were available to be issued.

Quail West Foundation, Inc.

Notes to Financial Statements

11

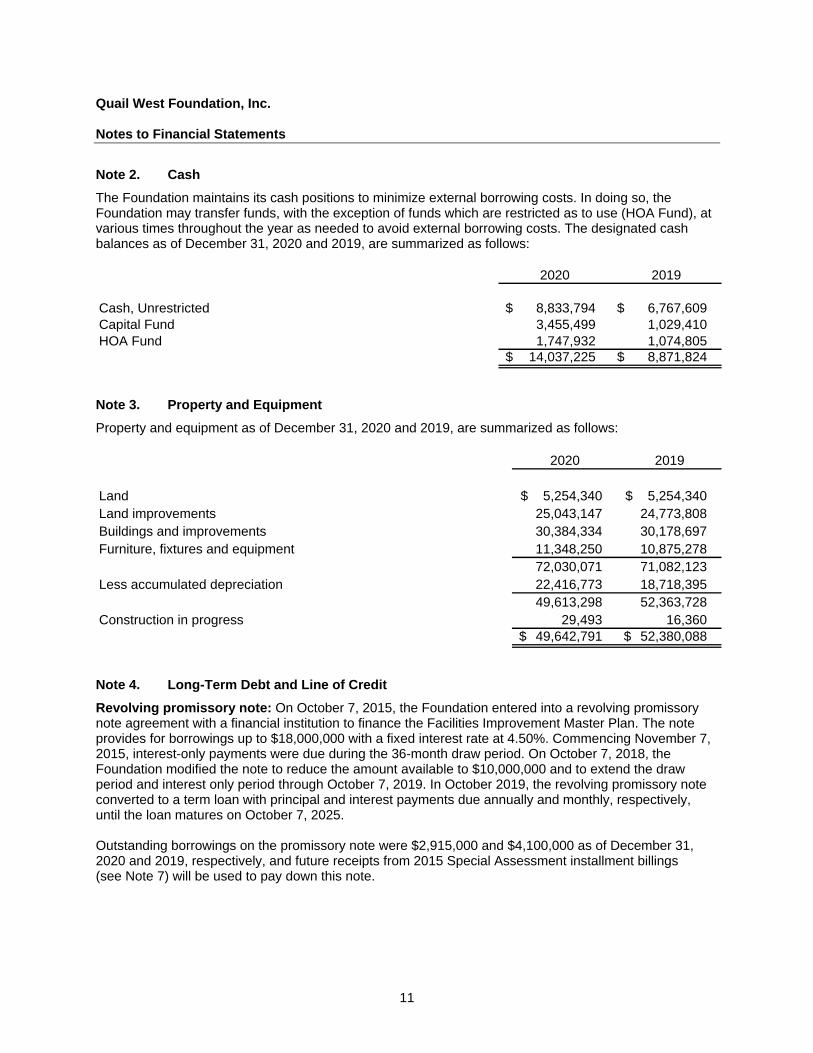

Note 2. Cash

The Foundation maintains its cash positions to minimize external borrowing costs. In doing so, the Foundation may transfer funds, with the exception of funds which are restricted as to use (HOA Fund), at various times throughout the year as needed to avoid external borrowing costs. The designated cash balances as of December 31, 2020 and 2019, are summarized as follows:

2020 2019

Cash, Unrestricted 8,833,794 $ 6,767,609 $ Capital Fund 3,455,499 1,029,410 HOA Fund 1,747,932 1,074,805

14,037,225 $ 8,871,824 $

Note 3. Property and Equipment

Property and equipment as of December 31, 2020 and 2019, are summarized as follows:

2020 2019

Land 5,254,340 $ 5,254,340 $ Land improvements 25,043,147 24,773,808 Buildings and improvements 30,384,334 30,178,697 Furniture, fixtures and equipment 11,348,250 10,875,278

72,030,071 71,082,123 Less accumulated depreciation 22,416,773 18,718,395

49,613,298 52,363,728 Construction in progress 29,493 16,360

49,642,791 $ 52,380,088 $

Note 4. Long-Term Debt and Line of Credit

Revolving promissory note: On October 7, 2015, the Foundation entered into a revolving promissory note agreement with a financial institution to finance the Facilities Improvement Master Plan. The note provides for borrowings up to $18,000,000 with a fixed interest rate at 4.50%. Commencing November 7, 2015, interest-only payments were due during the 36-month draw period. On October 7, 2018, the Foundation modified the note to reduce the amount available to $10,000,000 and to extend the draw period and interest only period through October 7, 2019. In October 2019, the revolving promissory note converted to a term loan with principal and interest payments due annually and monthly, respectively, until the loan matures on October 7, 2025.

Outstanding borrowings on the promissory note were $2,915,000 and $4,100,000 as of December 31, 2020 and 2019, respectively, and future receipts from 2015 Special Assessment installment billings (see Note 7) will be used to pay down this note.

Quail West Foundation, Inc. Notes to Financial Statements

12

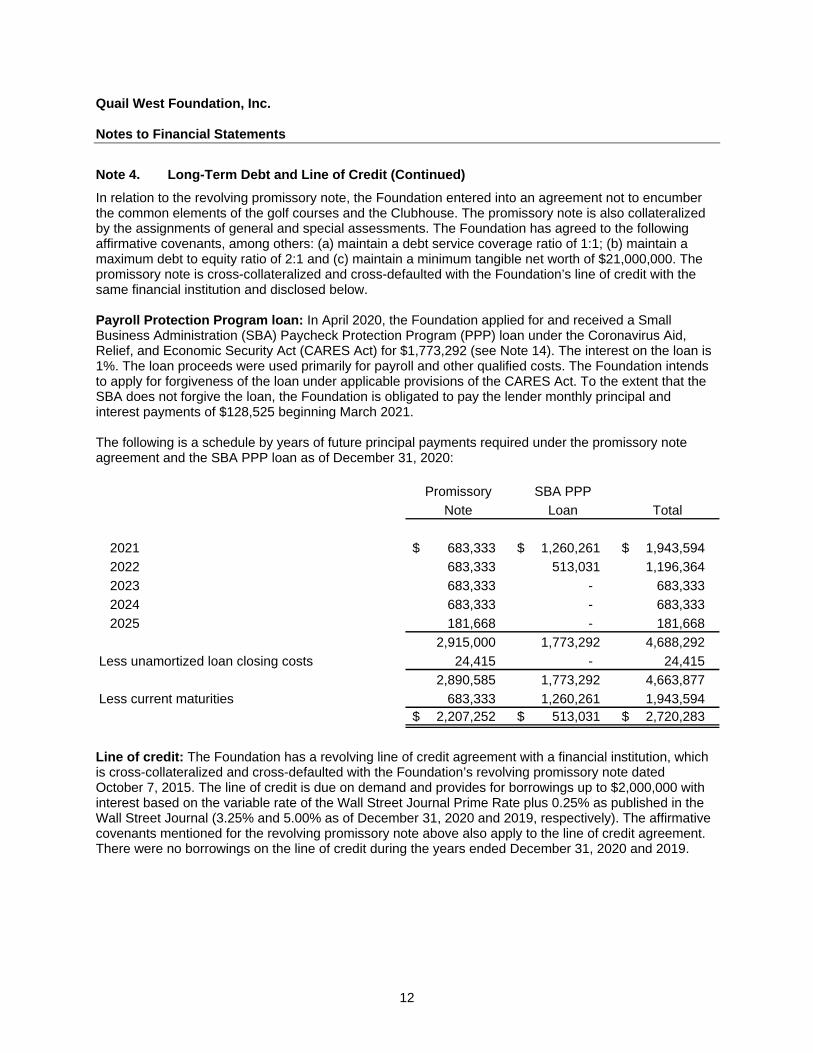

Note 4. Long-Term Debt and Line of Credit (Continued)

In relation to the revolving promissory note, the Foundation entered into an agreement not to encumber the common elements of the golf courses and the Clubhouse. The promissory note is also collateralized by the assignments of general and special assessments. The Foundation has agreed to the following affirmative covenants, among others: (a) maintain a debt service coverage ratio of 1:1; (b) maintain a maximum debt to equity ratio of 2:1 and (c) maintain a minimum tangible net worth of $21,000,000. The promissory note is cross-collateralized and cross-defaulted with the Foundation’s line of credit with the same financial institution and disclosed below. Payroll Protection Program loan: In April 2020, the Foundation applied for and received a Small Business Administration (SBA) Paycheck Protection Program (PPP) loan under the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) for $1,773,292 (see Note 14). The interest on the loan is 1%. The loan proceeds were used primarily for payroll and other qualified costs. The Foundation intends to apply for forgiveness of the loan under applicable provisions of the CARES Act. To the extent that the SBA does not forgive the loan, the Foundation is obligated to pay the lender monthly principal and interest payments of $128,525 beginning March 2021. The following is a schedule by years of future principal payments required under the promissory note agreement and the SBA PPP loan as of December 31, 2020:

Promissory SBA PPP

Note Loan Total

2021 683,333 $ 1,260,261 $ 1,943,594 $

2022 683,333 513,031 1,196,364

2023 683,333 - 683,333

2024 683,333 - 683,333

2025 181,668 - 181,668

2,915,000 1,773,292 4,688,292

Less unamortized loan closing costs 24,415 - 24,415

2,890,585 1,773,292 4,663,877

Less current maturities 683,333 1,260,261 1,943,594 2,207,252 $ 513,031 $ 2,720,283 $

Line of credit: The Foundation has a revolving line of credit agreement with a financial institution, which is cross-collateralized and cross-defaulted with the Foundation’s revolving promissory note dated October 7, 2015. The line of credit is due on demand and provides for borrowings up to $2,000,000 with interest based on the variable rate of the Wall Street Journal Prime Rate plus 0.25% as published in the Wall Street Journal (3.25% and 5.00% as of December 31, 2020 and 2019, respectively). The affirmative covenants mentioned for the revolving promissory note above also apply to the line of credit agreement. There were no borrowings on the line of credit during the years ended December 31, 2020 and 2019.

Quail West Foundation, Inc.

Notes to Financial Statements

13

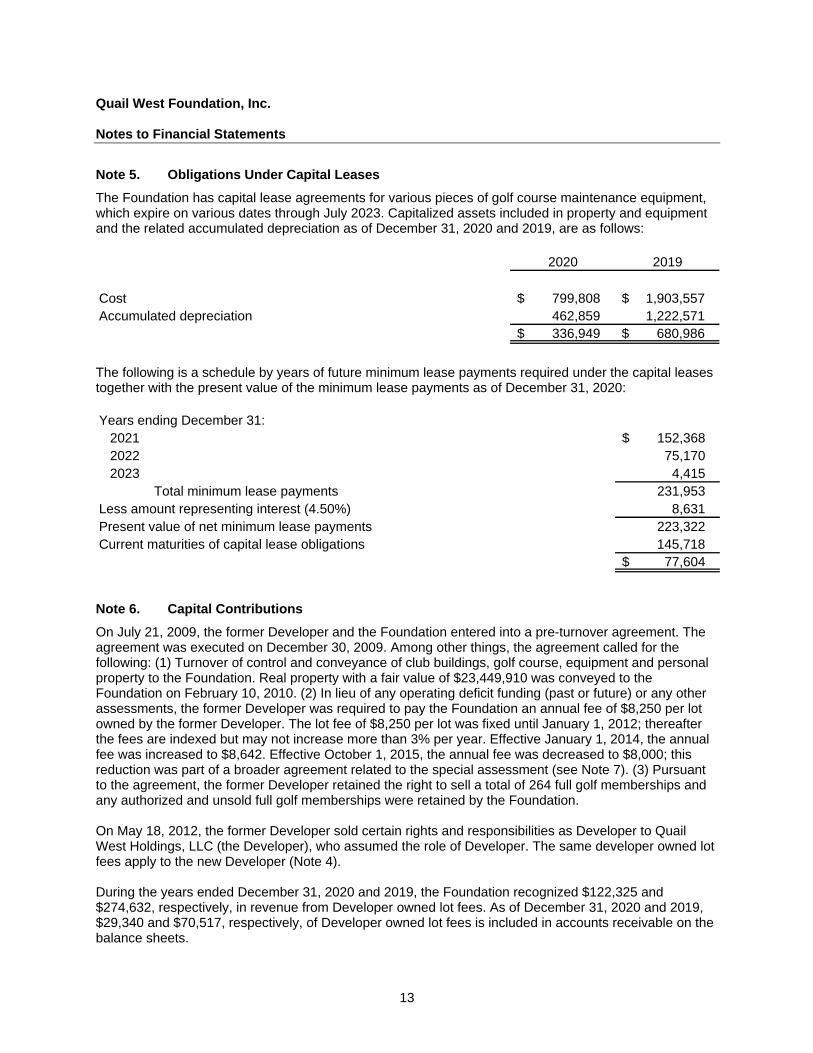

Note 5. Obligations Under Capital Leases

The Foundation has capital lease agreements for various pieces of golf course maintenance equipment, which expire on various dates through July 2023. Capitalized assets included in property and equipment and the related accumulated depreciation as of December 31, 2020 and 2019, are as follows:

2020 2019

Cost 799,808 $ 1,903,557 $ Accumulated depreciation 462,859 1,222,571

336,949 $ 680,986 $

The following is a schedule by years of future minimum lease payments required under the capital leases together with the present value of the minimum lease payments as of December 31, 2020:

Years ending December 31:2021 152,368 $ 2022 75,170 2023 4,415

Total minimum lease payments 231,953 Less amount representing interest (4.50%) 8,631 Present value of net minimum lease payments 223,322 Current maturities of capital lease obligations 145,718

77,604 $

Note 6. Capital Contributions

On July 21, 2009, the former Developer and the Foundation entered into a pre-turnover agreement. The agreement was executed on December 30, 2009. Among other things, the agreement called for the following: (1) Turnover of control and conveyance of club buildings, golf course, equipment and personal property to the Foundation. Real property with a fair value of $23,449,910 was conveyed to the Foundation on February 10, 2010. (2) In lieu of any operating deficit funding (past or future) or any other assessments, the former Developer was required to pay the Foundation an annual fee of $8,250 per lot owned by the former Developer. The lot fee of $8,250 per lot was fixed until January 1, 2012; thereafter the fees are indexed but may not increase more than 3% per year. Effective January 1, 2014, the annual fee was increased to $8,642. Effective October 1, 2015, the annual fee was decreased to $8,000; this reduction was part of a broader agreement related to the special assessment (see Note 7). (3) Pursuant to the agreement, the former Developer retained the right to sell a total of 264 full golf memberships and any authorized and unsold full golf memberships were retained by the Foundation.

On May 18, 2012, the former Developer sold certain rights and responsibilities as Developer to Quail West Holdings, LLC (the Developer), who assumed the role of Developer. The same developer owned lot fees apply to the new Developer (Note 4).

During the years ended December 31, 2020 and 2019, the Foundation recognized $122,325 and $274,632, respectively, in revenue from Developer owned lot fees. As of December 31, 2020 and 2019, $29,340 and $70,517, respectively, of Developer owned lot fees is included in accounts receivable on the balance sheets.

Quail West Foundation, Inc. Notes to Financial Statements

14

Note 6. Capital Contributions (Continued)

During the years ended December 31, 2020 and 2019, the Foundation collected transfer fees totaling $279,000 and $240,000, respectively. The Board has elected to restrict these funds for future capital use and thus they are included as part of the Capital Fund. In fiscal year 2018, the Board approved annual capital fees of $4,000 for each golf member and $3,000 for each house member (except as described in Note 8, for those members participating in the Membership Exchange Program). These funds are to be utilized for ongoing capital replacement/maintenance purchases. During the years ended December 31, 2020 and 2019, the Foundation collected $1,826,556 and $1,757,060, respectively, from members for the Capital Fund. In fiscal year 2020, the Foundation commenced annual capital fees for the HOA Fund of $1,000 for each owner with certain owners only subject to a third of the fee. During the year ended December 31, 2020, the Foundation collected $610,623 from members for the HOA Fund. On April 10, 2014, the Foundation entered into a capital funding agreement with the Developer in which the Developer agreed to pay the Foundation an amount equal to 5% of the membership initiation fee paid by the purchaser to the Developer as well as $1,200 for each lot owner or purchaser submitting plans for architectural review. For any lot or residence sold on or after March 15, 2014, the Developer will pay the Foundation $2,000 as a road repair fee, and additionally, the Developer has agreed to a $2,000 surcharge for each new property which is sold. The Board has elected to restrict these funds for future use and accordingly, they are included as part of the Capital Fund or, in the case of the road repair fee, part of the HOA Fund. During the years ended December 31, 2020 and 2019, the Foundation collected $115,275 and $163,064, respectively, from the Developer.

Note 7. 2015 Special Assessment

The Board of Directors approved a special assessment to fund the Facilities Improvement Master Plan in 2015. The approved assessment rates are $57,750 per resident golf member, $33,000 per non-resident golf member, $41,250 per resident house member and $24,750 per non-resident house member. Members were required to make their first payment under their chosen payment plan by October 31, 2015. Members were billed for the assessment based on their membership category and had the option of paying a one-time payment with a 7.3% discount, 3 or 10 annual installments. The Developer was assessed for each lot it owned at September 30, 2015. The amount of Developer assessment is $4,125 per year per lot owned for up to 10 years, which is the assessment rate for a Resident House member. Purchasers of a Developer lot will be required to assume the balance of the assessment for the membership status they choose, at the time of closing on the purchase of a Developer lot. Purchasers will be given the option of paying remaining payments due in one payment, or continue to pay the remaining payments due at $4,125 plus interest. If a purchaser of a Developer lot acquires a Golf membership during the assessment period, the assessment will be changed to the rate for Resident Golf member for the remainder of the assessment period.

Quail West Foundation, Inc.

Notes to Financial Statements

15

Note 7. 2015 Special Assessment (Continued)

The Foundation collected $2,112,650 and $1,779,794 from the members and Developer during the years ended December 31, 2020 and 2019, respectively, which was recognized as members’ equity when received on the statements of revenues, expenses and changes in members’ equity.

The following is a schedule by years of expected future collections as of December 31, 2020:

Years ending December 31:2021 848,860 $ 2022 810,788 2023 810,587 2024 809,752

3,279,987 Less amount representing interest 328,695

2,951,292 $

Note 8. Membership Exchange Program

On April 17, 2017, the Board of Directors approved a Membership Exchange Program (MEP) the purpose of which is to: a) increase the proceeds the Foundation retains from membership sales, b) reduce and eventually eliminate the Resignation List, and c) reduce the Foundation’s dependence on capital fees to pay for future capital projects. The MEP is a voluntary program – if a member does not participate in the MEP, there is no change in the member’s current rights, privileges, or terms and conditions of membership as determined by the Foundation’s Founding Documents, Rules, and Regulations.

The primary benefits of participating in the MEP include: a) a 50% discount off of the annual capital fee for the years 2018 through 2022, which period may be extended in the future, solely at the discretion of the Board of Directors, b) an equity refund equal to the greater of 33% or $30,000 for a golf membership and $10,000 for a house membership when the home/membership is sold, and c) elimination of the one year notice period for golf members choosing to downgrade to a house membership.

Note 9. Membership Refunds

The Foundation’s bylaws do not provide for the refund of a resigned equity member’s membership certificate until a replacement member is obtained, has paid all required fees, and purchases the certificate, at which time the funds are remitted to the resigned member. The only equity membership of the Foundation subject to a refund of their resigned equity is golf with the exception of exchanged house memberships (see Note 8). Golf memberships are not to exceed 600 members. The Foundation is not obligated to redeem a resigned member’s equity until these events occur and all available membership certificates have been issued. As of December 31, 2020 and 2019, there were 78 and 76 golf members, respectively, on the resignation list, of which 36 and 31, respectively, are active members. Members on the resignation list that have not elected to participate in the membership exchange program are obligated to pay one year of dues from the date of resignation.

Note 10. Retirement Plan

The Foundation sponsors a 401(k) retirement savings plan for the benefit of its employees. All employees over the age of 21 with at least 2 months of service are eligible to participate in the plan with contributions of up to 20% of their compensation up to the IRS limitation. Matching employer contributions are at the discretion of the Foundation. For the years ended December 31, 2020 and 2019, the matching employer contributions to the 401(k) plan totaled $71,628 and $70,654, respectively.

Quail West Foundation, Inc. Notes to Financial Statements

16

Note 11. Deferred Compensation Plan

The Foundation has deferred compensation agreements with certain key employees. The agreements provide for an annual contribution, which is based on a percentage of the employee’s base salary and approved annually at the sole discretion of the Foundation’s Board of Directors.

Note 12a. Major Repairs and Replacements – HOA Fund

The Foundation has set aside certain funds for a portion of future major repairs and replacements to common property referred to as the HOA Fund. Accumulated funds are held in separate bank accounts and generally are not permanently available for expenditures for normal operations (see Note 2). In 2018, the Board of Directors engaged a third party with expertise in such matters to conduct a study to estimate the current replacement costs and remaining useful lives of certain components of common property. The table included in the unaudited supplementary information on future major repairs and replacements on page 19 is based on these estimates. Accordingly, the Board has committed to fund approximately $660,000 for such major repairs and replacements for the fiscal year beginning January 1, 2021. Actual expenditures may vary from the estimated future expenditures and the variations may be material. Therefore, amounts accumulated in the HOA Fund may not be adequate to meet all future needs for major repairs and replacements. If additional funds are needed, the Foundation has the right to increase regular assessments, pass special assessments or delay major repairs and replacements until funds are available. Due to these circumstances, the statutes of the State of Florida require the following statements to be included in the financial statements:

The budget of the Foundation provides for limited voluntary deferred expenditure accounts, including capital expenditures and deferred maintenance, subject to limits on funding contained in our governing documents. Because the owners have not elected to provide for reserve accounts pursuant to Section 720.303(6), of the Florida Statutes, these funds are not subject to the restrictions on use of such funds set forth in that statute, nor are reserves calculated in accordance with that statute.

Considering the above referenced study of existing property and equipment funded by the HOA Fund, and other relevant considerations in the judgment of the Board, the Board has determined to fund ongoing capital expenditures for the replacement and/or extension of the useful lives of currently existing property and equipment on an annual basis through annual recurring capital fees, which may vary from year to year with a target minimum fund balance of approximately $1,000,000.

Note 12b. Major Repairs and Replacements – Capital Fund

The Foundation has set aside certain funds for a portion of future major repairs and replacements to the Foundation’s recreational facilities referred to as the Capital Fund. Accumulated funds are held in separate bank accounts and generally are not permanently available for expenditures for normal operations (see Note 2).

Quail West Foundation, Inc.

Notes to Financial Statements

17

Note 12b. Major Repairs and Replacements – Capital Fund (Continued)

In 2018, the Board of Directors engaged a third party with expertise in such matters to conduct a study to estimate the current replacement costs and remaining useful lives of certain components of common property. The table included in the unaudited supplementary information on future major repairs and replacements on page 18 is based on these estimates. Accordingly, the Board has committed to fund approximately $1,350,000 for such major repairs and replacements for the fiscal year beginning January 1, 2021.

Actual expenditures may vary from the estimated future expenditures and the variations may be material. Therefore, amounts accumulated in the Capital Fund may not be adequate to meet all future needs for major repairs and replacements. If additional funds are needed, the Foundation has the right to increase regular assessments, pass special assessments or delay major repairs and replacements until funds are available.

Considering the above referenced study of existing recreational facilities property and equipment, and other relevant considerations in the judgment of the Board, the Board has determined to fund ongoing capital expenditures for the replacement and/or extension of the useful lives of currently existing property and equipment on an annual basis through annual recurring capital fees, which may vary from year to year. While the Board has not currently established a minimum capital reserve target, the Capital Fund balance was $3,455,499 and $1,029,410 at December 31, 2020 and 2019, respectively.

Note 13. Insurance Matters

Where possible, the Foundation attempts to mitigate risk of hurricane damage through insurance. The Foundation’s insurance policies were renewed through February 28, 2022. The Foundation’s windstorm deductible on business personal property is $25,000 per occurrence. The windstorm deductible for named storms is 3% per building subject to a $25,000 minimum. Due to the Foundation’s coverage and deductibles, losses from future catastrophic weather events may require special membership assessments or funding from existing reserves.

Note 14. COVID-19 Pandemic

On January 30, 2020, the World Health Organization declared the coronavirus (COVID-19) outbreak a “Public Health Emergency of International Concern” and on March 11, 2020, declared it to be a global pandemic. Actions taken around the world to help mitigate the spread of COVID-19 include restrictions on travel, quarantines in certain areas and forced closures for certain types of public places and businesses. COVID-19 and actions taken to mitigate it have had and are expected to continue to have an adverse impact on the economies and financial markets of many countries, including the geographical area in which the Foundation operates. It is unknown how long these conditions will last and what the complete financial effect will be to the Foundation. As a result, the Foundation has been and will continue to be impacted and experience varying degrees of business interruption. The extent to which the COVID-19 outbreak will continue to impact the Foundation’s operations will continue to be dependent on past, current and future developments, which are uncertain as of March 2, 2021, the date the financial statements were available to be issued.

In April 2020, the Foundation applied for and received an SBA PPP loan under the CARES Act for $1,773,292 (see Note 4).

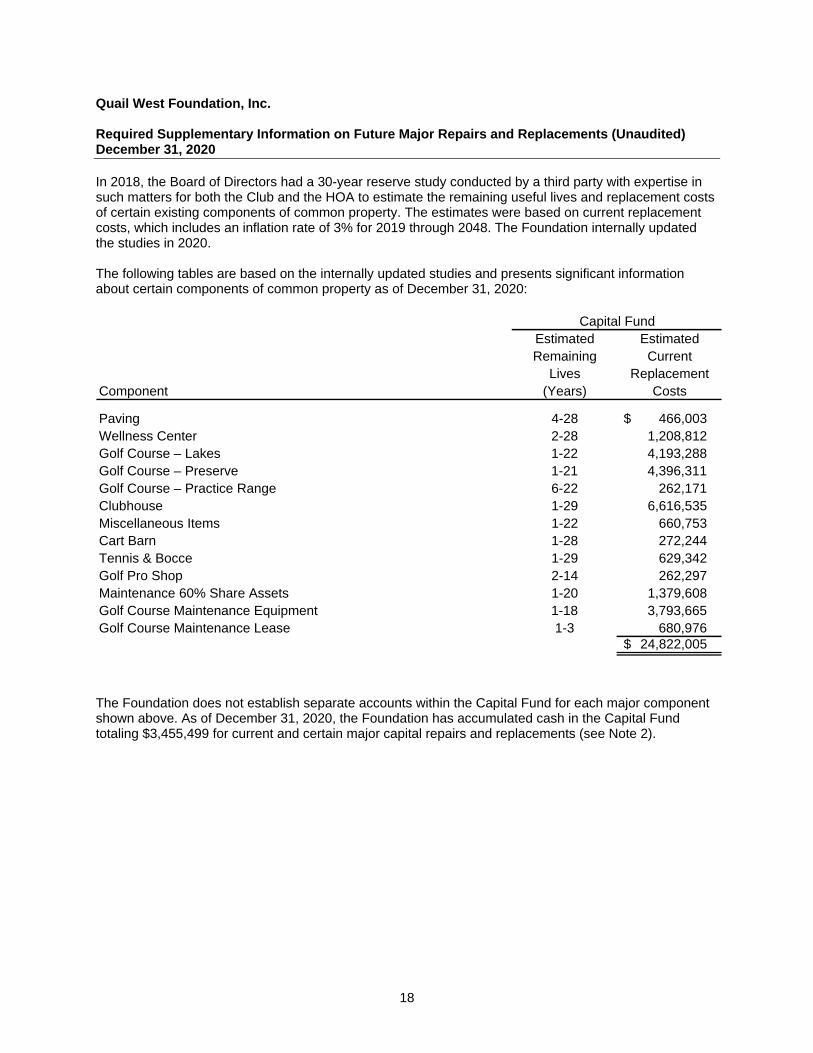

Quail West Foundation, Inc. Required Supplementary Information on Future Major Repairs and Replacements (Unaudited) December 31, 2020

18

In 2018, the Board of Directors had a 30-year reserve study conducted by a third party with expertise in such matters for both the Club and the HOA to estimate the remaining useful lives and replacement costs of certain existing components of common property. The estimates were based on current replacement costs, which includes an inflation rate of 3% for 2019 through 2048. The Foundation internally updated the studies in 2020. The following tables are based on the internally updated studies and presents significant information about certain components of common property as of December 31, 2020:

Estimated EstimatedRemaining Current

Lives ReplacementComponent (Years) Costs

Paving 4-28 466,003 $ Wellness Center 2-28 1,208,812 Golf Course – Lakes 1-22 4,193,288 Golf Course – Preserve 1-21 4,396,311 Golf Course – Practice Range 6-22 262,171 Clubhouse 1-29 6,616,535 Miscellaneous Items 1-22 660,753 Cart Barn 1-28 272,244 Tennis & Bocce 1-29 629,342 Golf Pro Shop 2-14 262,297 Maintenance 60% Share Assets 1-20 1,379,608 Golf Course Maintenance Equipment 1-18 3,793,665 Golf Course Maintenance Lease 1-3 680,976

24,822,005 $

Capital Fund

The Foundation does not establish separate accounts within the Capital Fund for each major component shown above. As of December 31, 2020, the Foundation has accumulated cash in the Capital Fund totaling $3,455,499 for current and certain major capital repairs and replacements (see Note 2).

Quail West Foundation, Inc.

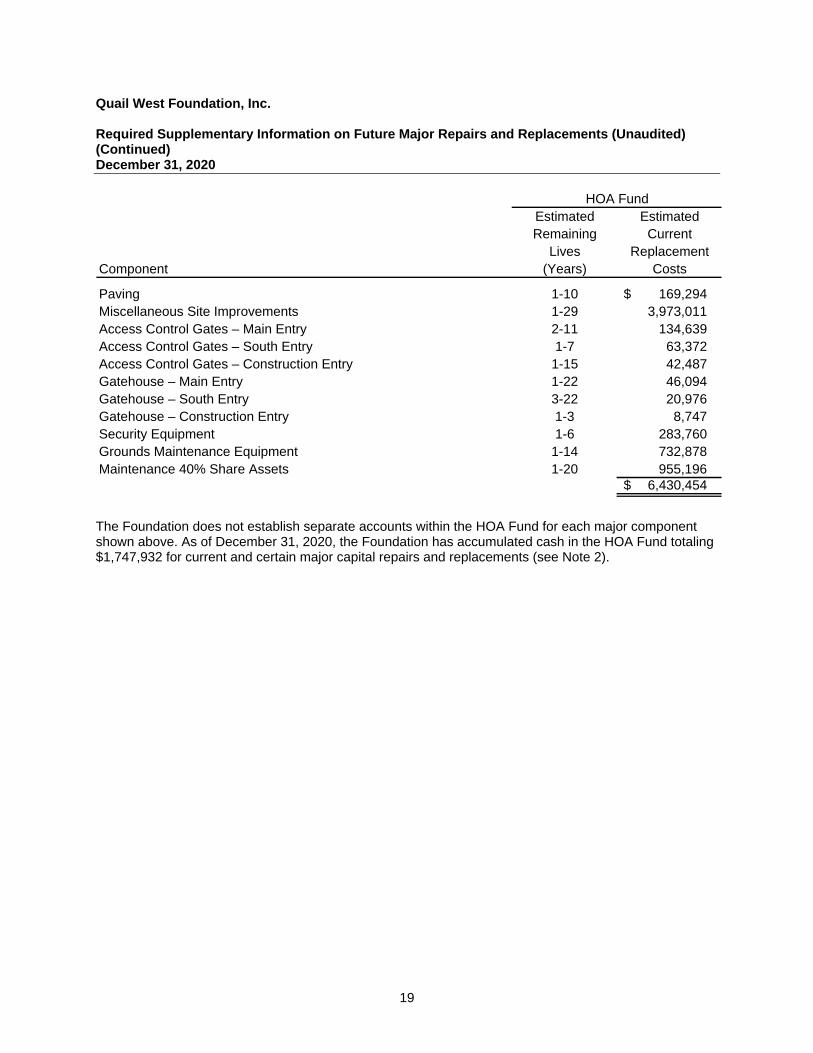

Required Supplementary Information on Future Major Repairs and Replacements (Unaudited) (Continued) December 31, 2020

19

Estimated EstimatedRemaining Current

Lives ReplacementComponent (Years) Costs

Paving 1-10 169,294 $ Miscellaneous Site Improvements 1-29 3,973,011 Access Control Gates – Main Entry 2-11 134,639 Access Control Gates – South Entry 1-7 63,372 Access Control Gates – Construction Entry 1-15 42,487 Gatehouse – Main Entry 1-22 46,094 Gatehouse – South Entry 3-22 20,976 Gatehouse – Construction Entry 1-3 8,747 Security Equipment 1-6 283,760 Grounds Maintenance Equipment 1-14 732,878 Maintenance 40% Share Assets 1-20 955,196

6,430,454 $

HOA Fund

The Foundation does not establish separate accounts within the HOA Fund for each major component shown above. As of December 31, 2020, the Foundation has accumulated cash in the HOA Fund totaling $1,747,932 for current and certain major capital repairs and replacements (see Note 2).

20

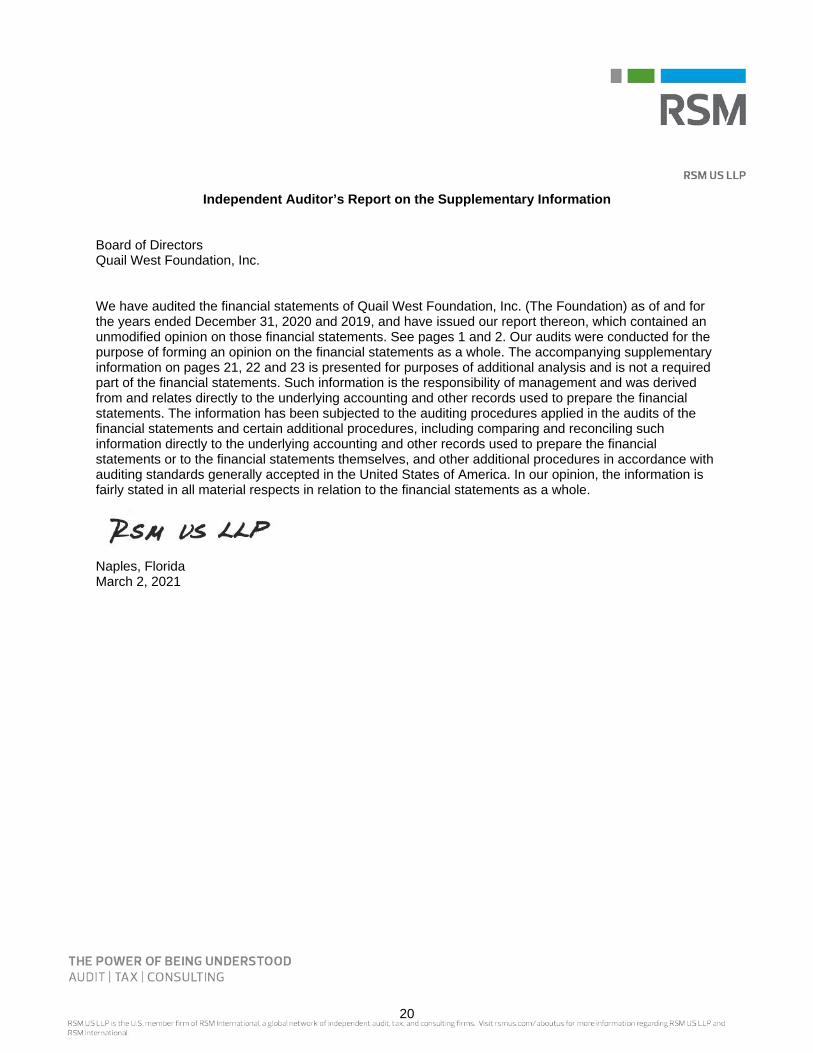

Independent Auditor’s Report on the Supplementary Information

Board of Directors Quail West Foundation, Inc.

We have audited the financial statements of Quail West Foundation, Inc. (The Foundation) as of and for the years ended December 31, 2020 and 2019, and have issued our report thereon, which contained an unmodified opinion on those financial statements. See pages 1 and 2. Our audits were conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying supplementary information on pages 21, 22 and 23 is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audits of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole.

Naples, Florida March 2, 2021

21

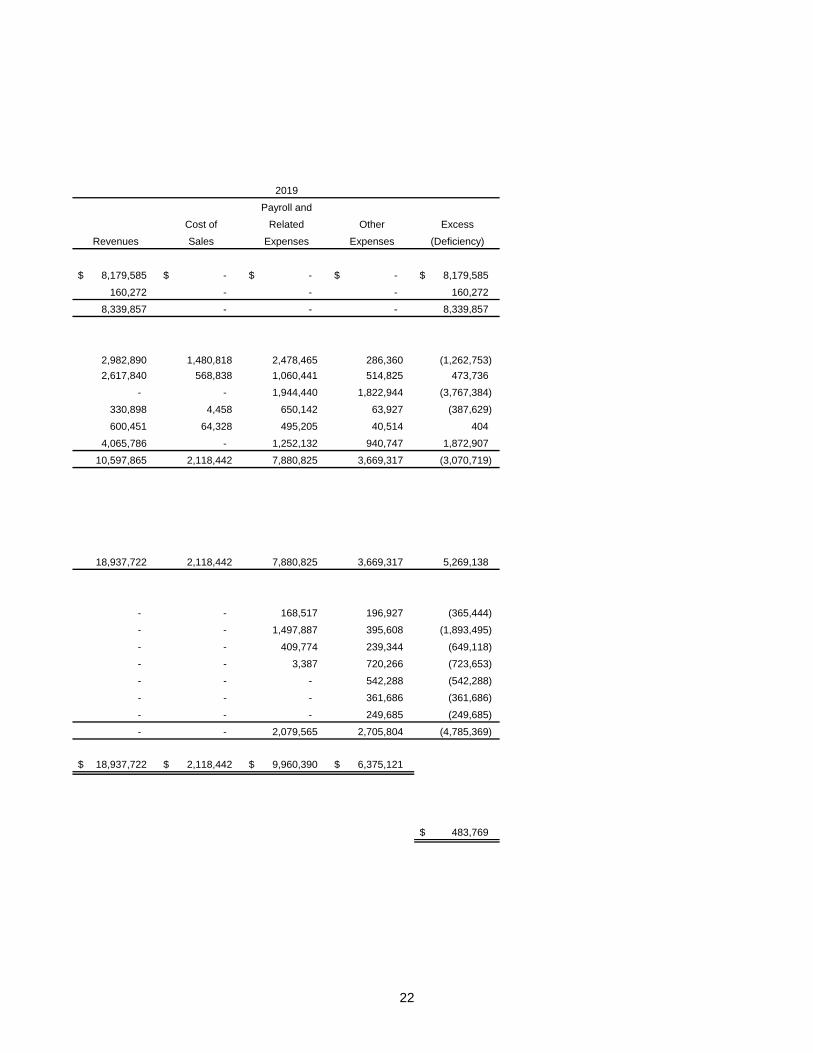

Quail West Foundation, Inc.

Statements of Revenues and Expenses InformationYears Ended December 31, 2020 and 2019

Payroll and

Departmental Schedules of Certain Cost of Related Other Excess

Revenues and Expenses Revenues Sales Expenses Expenses (Deficiency)

General revenues:

Membership dues 9,314,488 $ -$ -$ -$ 9,314,488$

Other 152,184 - - - 152,184

9,466,672 - - - 9,466,672

Departmental revenues and expenses:

Food and beverage 2,481,467 1,291,467 2,454,012 332,735 (1,596,747)

Golf operations 2,497,409 581,529 1,152,965 433,845 329,070

Golf course maintenance - - 2,036,924 1,762,801 (3,799,725)

Tennis and fitness 322,627 7,704 681,943 66,031 (433,051)

Salon 513,192 52,287 434,340 39,558 (12,993)

Common area maintenance 3,635,920 - 1,212,187 923,986 1,499,747

9,450,615 1,932,987 7,972,371 3,558,956 (4,013,699)

Excess of revenues over

expenses before undistributed

expenses, developer owned

lot fees and other

revenues (expenses) 18,917,287 1,932,987 7,972,371 3,558,956 5,452,973

Undistributed expenses:

Membership - - 205,184 88,510 (293,694)

Administrative and general - - 1,844,406 349,814 (2,194,220)

Building services - - 422,298 258,978 (681,276)

Privacy and access services - - 6 709,874 (709,880)

Utilities - - - 442,699 (442,699)

Insurance - - - 368,833 (368,833)

Property taxes - - - 272,553 (272,553)

- - 2,471,894 2,491,261 (4,963,155)

18,917,287 $ 1,932,987 $ 10,444,265 $ 6,050,217 $

Excess of revenues over

expenses before developer owned

lot fees and other revenues (expenses) 489,818 $

2020

22

Payroll and

Cost of Related Other Excess

Revenues Sales Expenses Expenses (Deficiency)

8,179,585 $ -$ -$ -$ 8,179,585$

160,272 - - - 160,272

8,339,857 - - - 8,339,857

2,982,890 1,480,818 2,478,465 286,360 (1,262,753)

2,617,840 568,838 1,060,441 514,825 473,736

- - 1,944,440 1,822,944 (3,767,384)

330,898 4,458 650,142 63,927 (387,629)

600,451 64,328 495,205 40,514 404

4,065,786 - 1,252,132 940,747 1,872,907

10,597,865 2,118,442 7,880,825 3,669,317 (3,070,719)

18,937,722 2,118,442 7,880,825 3,669,317 5,269,138

- - 168,517 196,927 (365,444)

- - 1,497,887 395,608 (1,893,495)

- - 409,774 239,344 (649,118)

- - 3,387 720,266 (723,653)

- - - 542,288 (542,288)

- - - 361,686 (361,686)

- - - 249,685 (249,685)

- - 2,079,565 2,705,804 (4,785,369)

18,937,722 $ 2,118,442 $ 9,960,390 $ 6,375,121 $

483,769 $

2019

23

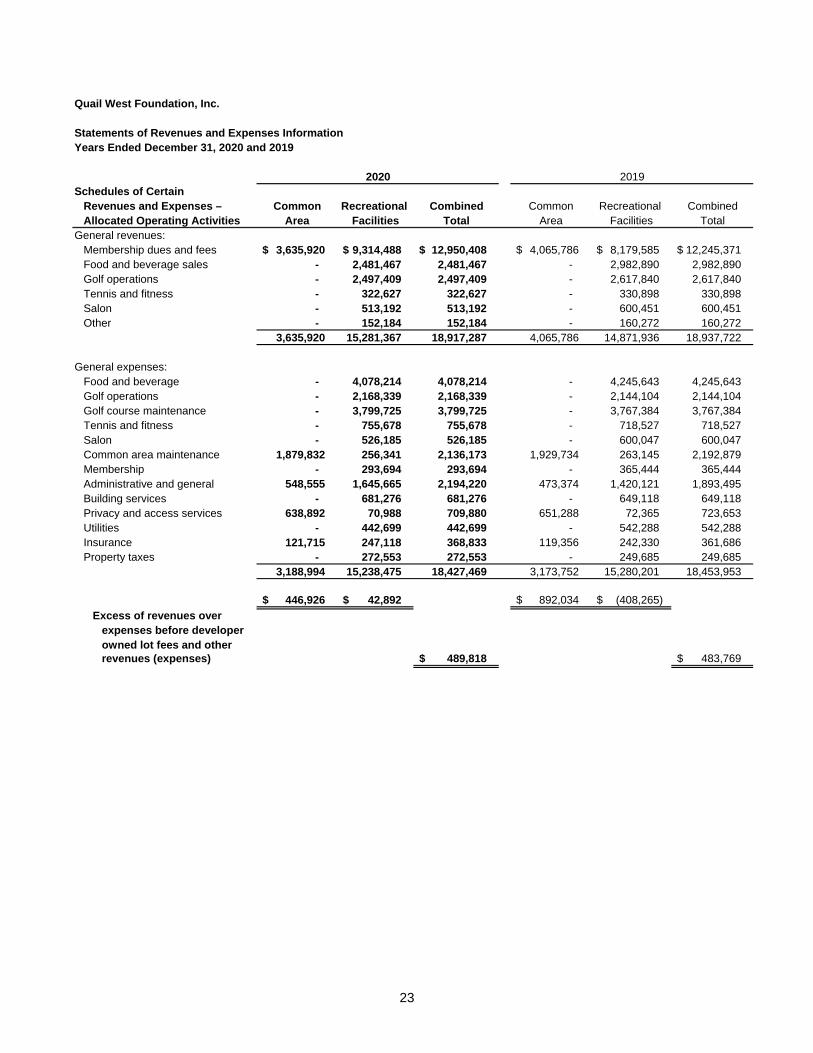

Quail West Foundation, Inc.

Statements of Revenues and Expenses InformationYears Ended December 31, 2020 and 2019

Schedules of CertainRevenues and Expenses – Common Recreational Combined Common Recreational CombinedAllocated Operating Activities Area Facilities Total Area Facilities Total

General revenues:Membership dues and fees 3,635,920 $ 9,314,488 $ 12,950,408 $ 4,065,786 $ 8,179,585 $ 12,245,371 $ Food and beverage sales - 2,481,467 2,481,467 - 2,982,890 2,982,890 Golf operations - 2,497,409 2,497,409 - 2,617,840 2,617,840 Tennis and fitness - 322,627 322,627 - 330,898 330,898 Salon - 513,192 513,192 - 600,451 600,451 Other - 152,184 152,184 - 160,272 160,272

3,635,920 15,281,367 18,917,287 4,065,786 14,871,936 18,937,722

General expenses:Food and beverage - 4,078,214 4,078,214 - 4,245,643 4,245,643 Golf operations - 2,168,339 2,168,339 - 2,144,104 2,144,104 Golf course maintenance - 3,799,725 3,799,725 - 3,767,384 3,767,384 Tennis and fitness - 755,678 755,678 - 718,527 718,527 Salon - 526,185 526,185 - 600,047 600,047 Common area maintenance 1,879,832 256,341 2,136,173 1,929,734 263,145 2,192,879 Membership - 293,694 293,694 - 365,444 365,444 Administrative and general 548,555 1,645,665 2,194,220 473,374 1,420,121 1,893,495 Building services - 681,276 681,276 - 649,118 649,118 Privacy and access services 638,892 70,988 709,880 651,288 72,365 723,653 Utilities - 442,699 442,699 - 542,288 542,288 Insurance 121,715 247,118 368,833 119,356 242,330 361,686 Property taxes - 272,553 272,553 - 249,685 249,685

3,188,994 15,238,475 18,427,469 3,173,752 15,280,201 18,453,953

446,926 $ 42,892 $ 892,034 $ (408,265) $

Excess of revenues overexpenses before developerowned lot fees and otherrevenues (expenses) 489,818 $ 483,769 $

2020 2019

Related Documents