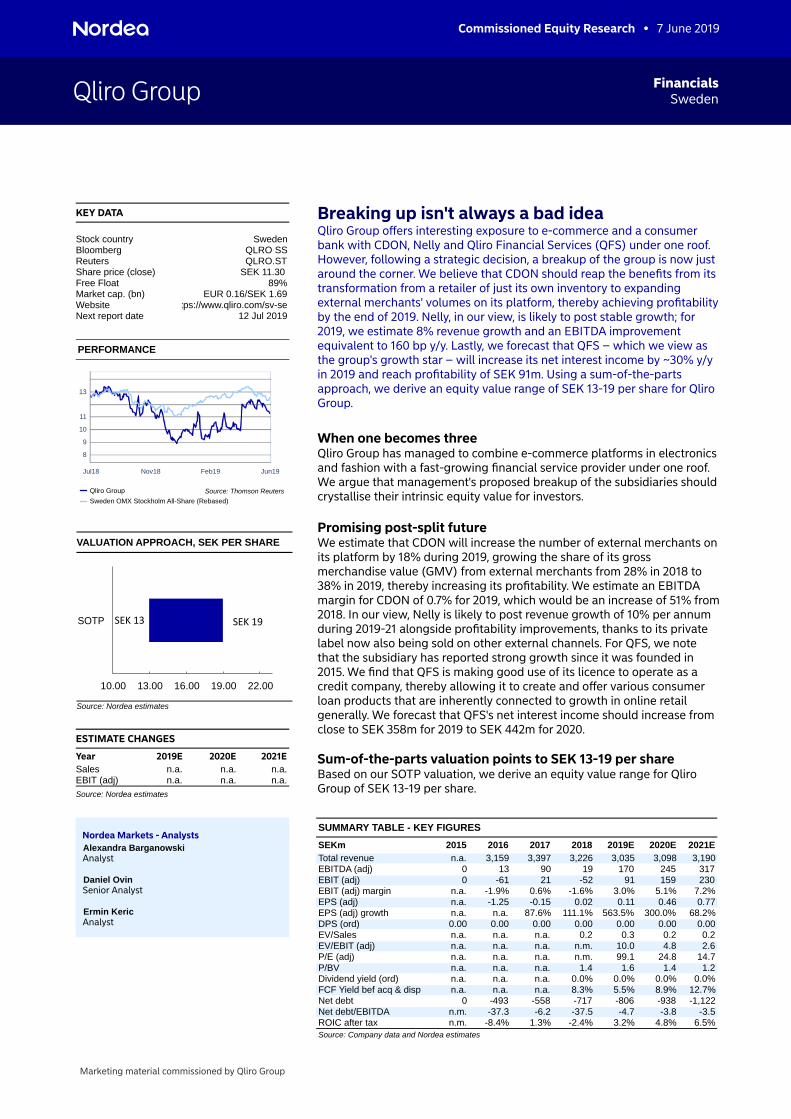

Qliro Group Sweden Financials Commissioned Equity Research • 7 June 2019 KEY DATA Sweden Stock country QLRO SS Bloomberg QLRO.ST Reuters SEK 11.30 Share price (close) 89% Free Float EUR 0.16/SEK 1.69 Market cap. (bn) tps://www.qliro.com/sv-se Website 12 Jul 2019 Next report date PERFORMANCE Jul18 Nov18 Feb19 Jun19 8 9 10 11 13 Qliro Group Sweden OMX Stockholm All-Share (Rebased) Source: Thomson Reuters VALUATION APPROACH, SEK PER SHARE 10.00 13.00 16.00 19.00 22.00 SOTP SEK 13 SEK 19 Source: Nordea estimates ESTIMATE CHANGES 2021E 2020E 2019E Year n.a. n.a. n.a. Sales n.a. n.a. n.a. EBIT (adj) Source: Nordea estimates Breaking up isn't always a bad idea Qliro Group offers interesting exposure to e-commerce and a consumer bank with CDON, Nelly and Qliro Financial Services (QFS) under one roof. However, following a strategic decision, a breakup of the group is now just around the corner. We believe that CDON should reap the benefits from its transformation from a retailer of just its own inventory to expanding external merchants' volumes on its platform, thereby achieving profitability by the end of 2019. Nelly, in our view, is likely to post stable growth; for 2019, we estimate 8% revenue growth and an EBITDA improvement equivalent to 160 bp y/y. Lastly, we forecast that QFS – which we view as the group's growth star – will increase its net interest income by ~30% y/y in 2019 and reach profitability of SEK 91m. Using a sum-of-the-parts approach, we derive an equity value range of SEK 13-19 per share for Qliro Group. When one becomes three Qliro Group has managed to combine e-commerce platforms in electronics and fashion with a fast-growing financial service provider under one roof. We argue that management's proposed breakup of the subsidiaries should crystallise their intrinsic equity value for investors. Promising post-split future We estimate that CDON will increase the number of external merchants on its platform by 18% during 2019, growing the share of its gross merchandise value (GMV) from external merchants from 28% in 2018 to 38% in 2019, thereby increasing its profitability. We estimate an EBITDA margin for CDON of 0.7% for 2019, which would be an increase of 51% from 2018. In our view, Nelly is likely to post revenue growth of 10% per annum during 2019-21 alongside profitability improvements, thanks to its private label now also being sold on other external channels. For QFS, we note that the subsidiary has reported strong growth since it was founded in 2015. We find that QFS is making good use of its licence to operate as a credit company, thereby allowing it to create and offer various consumer loan products that are inherently connected to growth in online retail generally. We forecast that QFS's net interest income should increase from close to SEK 358m for 2019 to SEK 442m for 2020. Sum-of-the-parts valuation points to SEK 13-19 per share Based on our SOTP valuation, we derive an equity value range for Qliro Group of SEK 13-19 per share. Nordea Markets - Analysts Alexandra Barganowski Analyst Daniel Ovin Senior Analyst Ermin Keric Analyst SUMMARY TABLE - KEY FIGURES 2021E 2020E 2019E 2018 2017 2016 2015 SEKm 3,190 3,098 3,035 3,226 3,397 3,159 n.a. Total revenue 317 245 170 19 90 13 0 EBITDA (adj) 230 159 91 -52 21 -61 0 EBIT (adj) 7.2% 5.1% 3.0% -1.6% 0.6% -1.9% n.a. EBIT (adj) margin 0.77 0.46 0.11 0.02 -0.15 -1.25 n.a. EPS (adj) 68.2% 300.0% 563.5% 111.1% 87.6% n.a. n.a. EPS (adj) growth 0.00 0.00 0.00 0.00 0.00 0.00 0.00 DPS (ord) 0.2 0.2 0.3 0.2 n.a. n.a. n.a. EV/Sales 2.6 4.8 10.0 n.m. n.a. n.a. n.a. EV/EBIT (adj) 14.7 24.8 99.1 n.m. n.a. n.a. n.a. P/E (adj) 1.2 1.4 1.6 1.4 n.a. n.a. n.a. P/BV 0.0% 0.0% 0.0% 0.0% n.a. n.a. n.a. Dividend yield (ord) 12.7% 8.9% 5.5% 8.3% n.a. n.a. n.a. FCF Yield bef acq & disp -1,122 -938 -806 -717 -558 -493 0 Net debt -3.5 -3.8 -4.7 -37.5 -6.2 -37.3 n.m. Net debt/EBITDA 6.5% 4.8% 3.2% -2.4% 1.3% -8.4% n.m. ROIC after tax Source: Company data and Nordea estimates Marketing material commissioned by Qliro Group

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Qliro Group SwedenFinancials

Commissioned Equity Research • 7 June 2019

KEY DATA

SwedenStock countryQLRO SSBloombergQLRO.STReuters

SEK 11.30 Share price (close)89%Free Float

EUR 0.16/SEK 1.69Market cap. (bn)tps://www.qliro.com/sv-seWebsite

12 Jul 2019Next report date

PERFORMANCE

Jul18 Nov18 Feb19 Jun19

8

9

10

11

13

Qliro Group

Sweden OMX Stockholm All-Share (Rebased)

Source: Thomson Reuters

VALUATION APPROACH, SEK PER SHARE

10.00 13.00 16.00 19.00 22.00

SOTP SEK 13 SEK 19

Source: Nordea estimates

ESTIMATE CHANGES

2021E2020E2019EYearn.a.n.a.n.a.Salesn.a.n.a.n.a.EBIT (adj)

Source: Nordea estimates

Breaking up isn't always a bad ideaQliro Group offers interesting exposure to e-commerce and a consumer bank with CDON, Nelly and Qliro Financial Services (QFS) under one roof. However, following a strategic decision, a breakup of the group is now just around the corner. We believe that CDON should reap the benefits from its transformation from a retailer of just its own inventory to expanding external merchants' volumes on its platform, thereby achieving profitability by the end of 2019. Nelly, in our view, is likely to post stable growth; for 2019, we estimate 8% revenue growth and an EBITDA improvement equivalent to 160 bp y/y. Lastly, we forecast that QFS – which we view as the group's growth star – will increase its net interest income by ~30% y/y in 2019 and reach profitability of SEK 91m. Using a sum-of-the-parts approach, we derive an equity value range of SEK 13-19 per share for Qliro Group.

When one becomes threeQliro Group has managed to combine e-commerce platforms in electronics and fashion with a fast-growing financial service provider under one roof. We argue that management's proposed breakup of the subsidiaries should crystallise their intrinsic equity value for investors.

Promising post-split futureWe estimate that CDON will increase the number of external merchants on its platform by 18% during 2019, growing the share of its gross merchandise value (GMV) from external merchants from 28% in 2018 to 38% in 2019, thereby increasing its profitability. We estimate an EBITDA margin for CDON of 0.7% for 2019, which would be an increase of 51% from 2018. In our view, Nelly is likely to post revenue growth of 10% per annum during 2019-21 alongside profitability improvements, thanks to its private label now also being sold on other external channels. For QFS, we note that the subsidiary has reported strong growth since it was founded in 2015. We find that QFS is making good use of its licence to operate as a credit company, thereby allowing it to create and offer various consumer loan products that are inherently connected to growth in online retail generally. We forecast that QFS's net interest income should increase from close to SEK 358m for 2019 to SEK 442m for 2020.

Sum-of-the-parts valuation points to SEK 13-19 per shareBased on our SOTP valuation, we derive an equity value range for Qliro Group of SEK 13-19 per share.

Nordea Markets - AnalystsAlexandra BarganowskiAnalyst

Daniel OvinSenior Analyst

Ermin KericAnalyst

SUMMARY TABLE - KEY FIGURES

2021E2020E2019E2018201720162015SEKm3,1903,0983,0353,2263,3973,159n.a.Total revenue

3172451701990130EBITDA (adj)23015991-5221-610EBIT (adj)

7.2%5.1%3.0%-1.6%0.6%-1.9%n.a.EBIT (adj) margin0.770.460.110.02-0.15-1.25n.a.EPS (adj)

68.2%300.0%563.5%111.1%87.6%n.a.n.a.EPS (adj) growth0.000.000.000.000.000.000.00DPS (ord)0.20.20.30.2n.a.n.a.n.a.EV/Sales2.64.810.0n.m.n.a.n.a.n.a.EV/EBIT (adj)

14.724.899.1n.m.n.a.n.a.n.a.P/E (adj)1.21.41.61.4n.a.n.a.n.a.P/BV

0.0%0.0%0.0%0.0%n.a.n.a.n.a.Dividend yield (ord)12.7%8.9%5.5%8.3%n.a.n.a.n.a.FCF Yield bef acq & disp-1,122-938-806-717-558-4930Net debt

-3.5-3.8-4.7-37.5-6.2-37.3n.m.Net debt/EBITDA6.5%4.8%3.2%-2.4%1.3%-8.4%n.m.ROIC after tax

Source: Company data and Nordea estimates

Marketing material commissioned by Qliro Group

Qliro Group7 June 2019

Contents

Factors to consider when investing in Qliro Group 3

Company overview 14

E-commerce 24

Consumer Financial Services 43

Peer overview 55

Historical financials 63

Estimates 69

Detailed estimates: Quarterly 73

Detailed estimates: Annual 76

Valuation 79

Risks factors 84

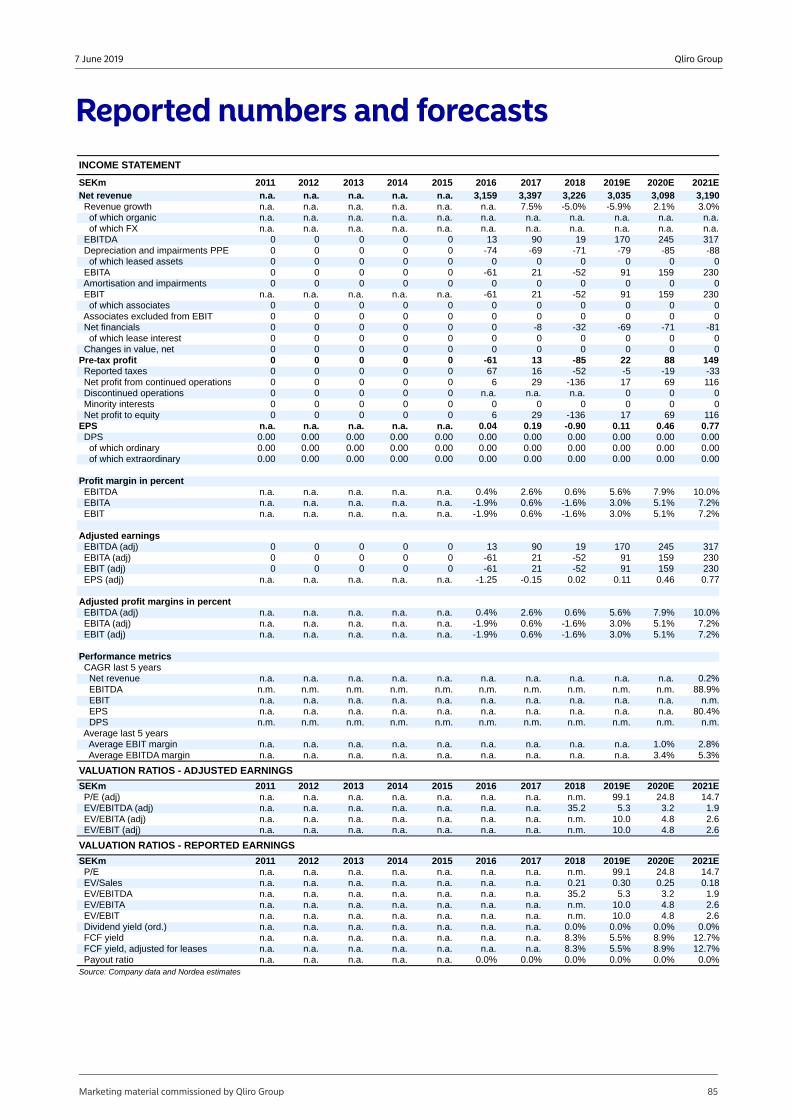

Reported numbers and forecasts 85

Disclaimer and legal disclosures 88

Marketing material commissioned by Qliro Group 2

Qliro Group7 June 2019

Factors to consider when investing in Qliro GroupQliro Group holds three different but promising companies – CDON, Nelly and Qliro Financial Services (QFS) – under one roof. However, we believe the company has struggled to realise the full potential of these companies, primarily because each has different requirements for its operations. Against that backdrop, the company introduced a new strategy in 2018 to prepare each subsidiary to operate on a standalone basis within 24 months. We believe that CDON, the centrepiece of the group's turnaround case, should reap the benefits from its transformation from an online retailer of just its own inventory to a marketplace expanding external merchants' volumes on its platform, thereby achieving profitability by the end of 2019. Nelly, in our view, will likely post stable growth; for 2019, we estimate 8% revenue growth and an EBITDA improvement equivalent to 160 bp y/y. Lastly, QFS – which we view as the company's growth star – should increase its net interest income by ~30% y/y in 2019E and reach profitability of SEK 91m. We value the three companies on a standalone basis, and then using a sum-of-the-parts valuation derive an equity value range of SEK 13-19 per share.

The road to independence – when one becomes threeIn October 2018, Qliro Group presented its new strategy for the company, highlighting that its three subsidiaries should be prepared to operate independently within 24 months. The company set targets for each of the subsidiaries and is now well on its way to separating them into three entities, through either separate listings or restructuring. We delve into each of CDON, Nelly and QFS to see what the future could hold for each as a standalone company. Given Qliro Group's strategy to split up the group, we believe there is a good likelihood of crystallising the value of each entity ahead.

Qliro Group – the Nordics' original e-commerce platformQliro Group is currently a holding company that offers exposure to Nordic e-commerce brands for popular consumer products (through CDON.com), fashion (through Nelly) and consumer finance (through Qliro Financial Services).

CDON.com, which launched in 1999 as a Nordic e-commerce site (spun off from MTG), and now is often referred to as the "Nordic Amazon", laid the foundations for Qliro Group as it stands today. The original strategy of Qliro Group was to build a portfolio of e-commerce companies, which it has done over the years by acquiring various online merchants. Some of them, such as Lekmer and HSNG (Gymgrossisten), have since been sold in order to streamline the portfolio.

The company changed its name to Qliro Group in 2015 and CDON.com became the largest subsidiary, with a clear aim to become the largest marketplace for media products in the Nordics. Beyond those products, the marketplace also sells everything from electronics to clothing, shoes, sports and leisure items, mobile phones, books, games, furnishings and toys.

Regarding the other two pieces of the Qliro Group puzzle, Nelly was launched in 2004 and acquired by the group in 2007. As a key milestone, NLY Man was introduced as a fashion e-tailer for men in 2014. During the same year, the company created Qliro Financial Services (QFS), initially as the group realised the need to offer a payment solution for customers who purchased items on CDON and Nelly. QFS now offers financial services to more than 30 external e-merchants, as well as consumer loans to customers in the Nordic region.

In 2018, around 48% of the group's revenue was derived from CDON, 43% from the fashion platform Nelly and the remaining 9% from QFS.

Marketing material commissioned by Qliro Group 3

Qliro Group7 June 2019

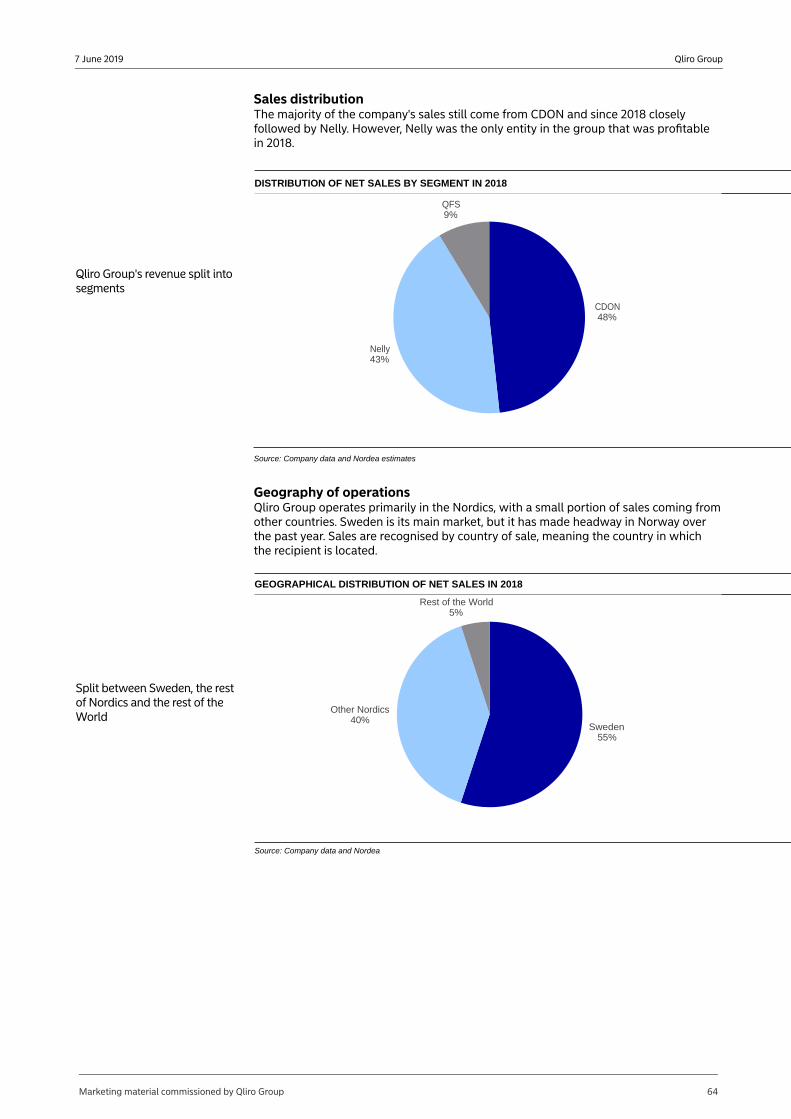

Qliro Group's revenue split into segments

DISTRIBUTION OF NET SALES BY SEGMENT IN 2018

CDON48%

Nelly43%

QFS9%

Source: Company data and Nordea estimates

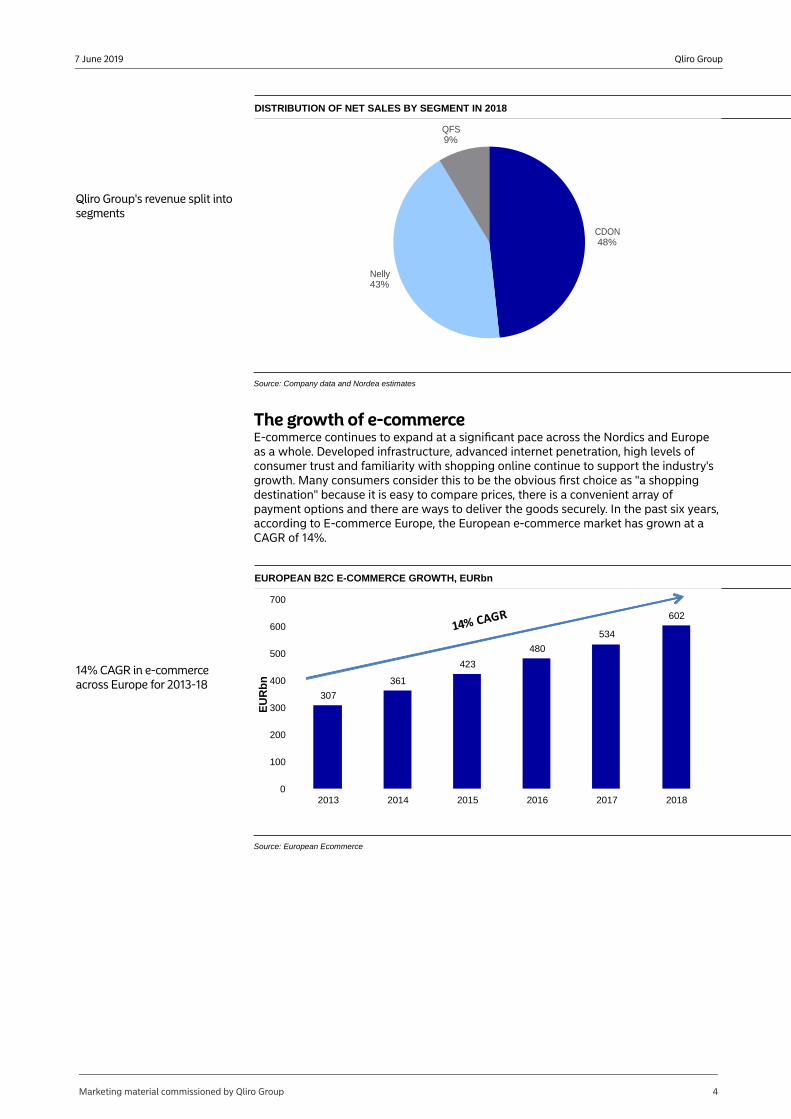

The growth of e-commerceE-commerce continues to expand at a significant pace across the Nordics and Europe as a whole. Developed infrastructure, advanced internet penetration, high levels of consumer trust and familiarity with shopping online continue to support the industry's growth. Many consumers consider this to be the obvious first choice as "a shopping destination" because it is easy to compare prices, there is a convenient array of payment options and there are ways to deliver the goods securely. In the past six years, according to E-commerce Europe, the European e-commerce market has grown at a CAGR of 14%.

14% CAGR in e-commerce across Europe for 2013-18

EUROPEAN B2C E-COMMERCE GROWTH, EURbn

307

361

423

480

534

602

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017 2018

EU

Rb

n

Source: European Ecommerce

Marketing material commissioned by Qliro Group 4

Qliro Group7 June 2019

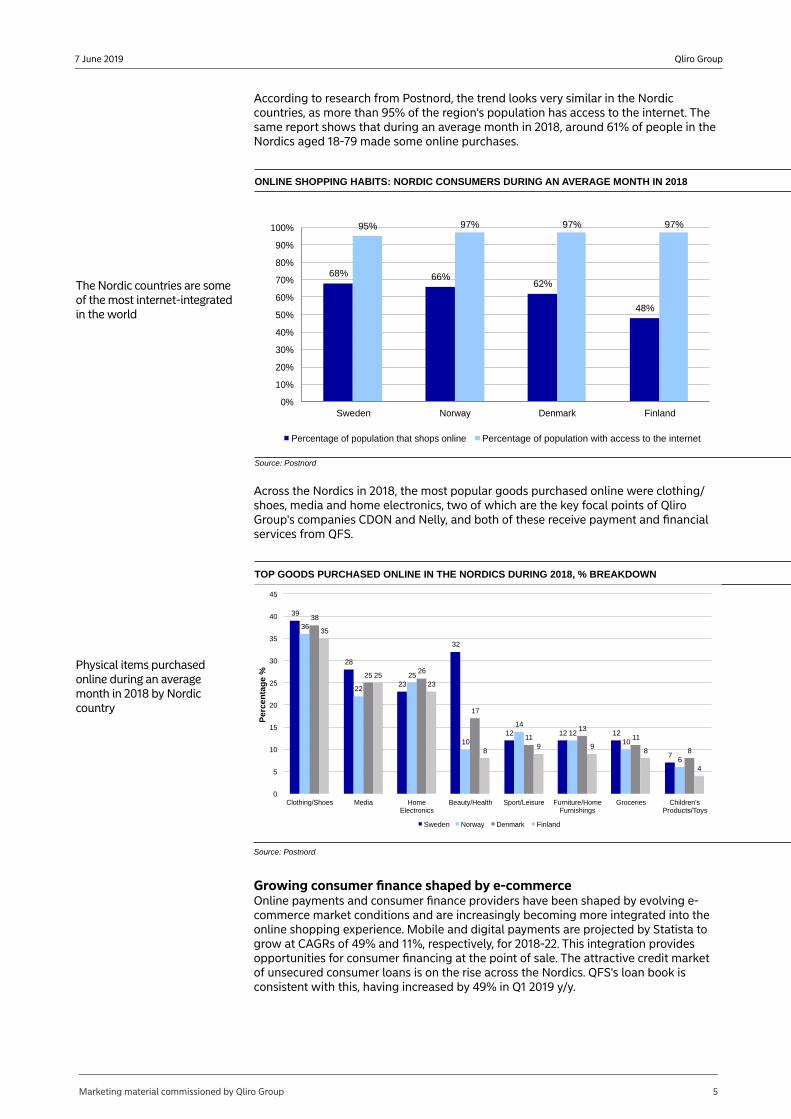

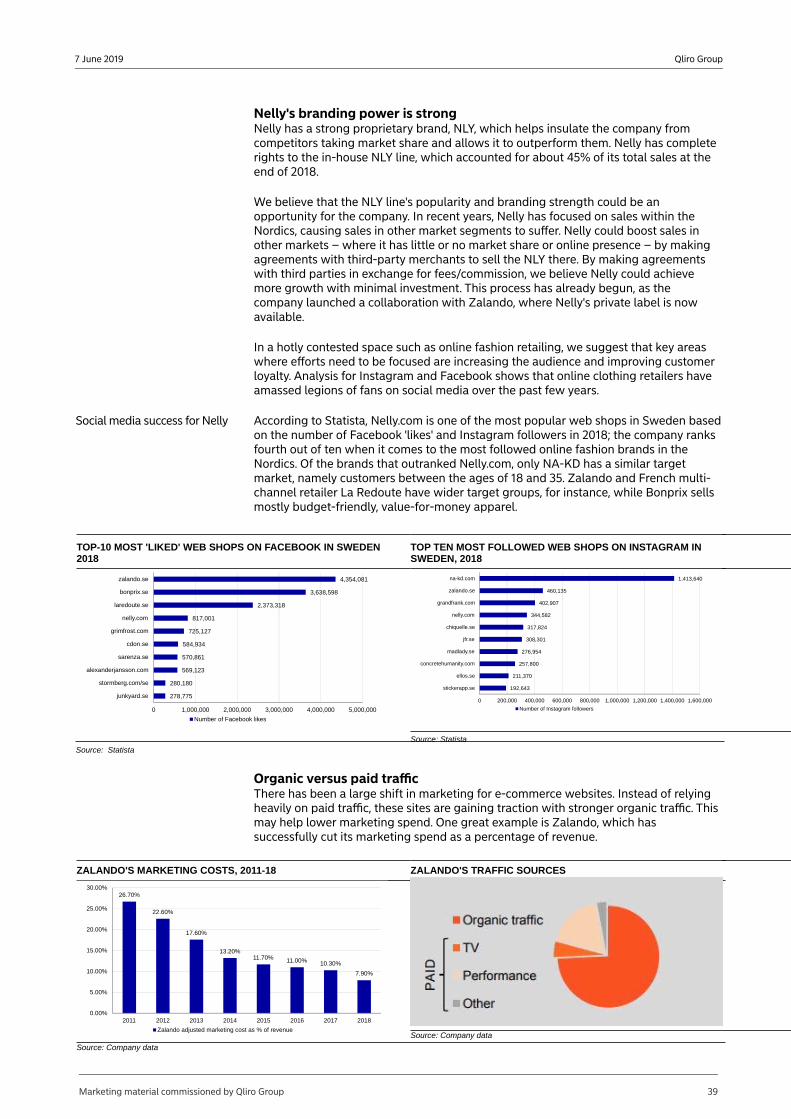

According to research from Postnord, the trend looks very similar in the Nordic countries, as more than 95% of the region's population has access to the internet. The same report shows that during an average month in 2018, around 61% of people in the Nordics aged 18-79 made some online purchases.

ONLINE SHOPPING HABITS: NORDIC CONSUMERS DURING AN AVERAGE MONTH IN 2018

The Nordic countries are some of the most internet-integrated in the world

68% 66%62%

48%

95% 97% 97% 97%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sweden Norway Denmark Finland

Percentage of population that shops online Percentage of population with access to the internet

Source: Postnord

Across the Nordics in 2018, the most popular goods purchased online were clothing/shoes, media and home electronics, two of which are the key focal points of Qliro Group's companies CDON and Nelly, and both of these receive payment and financial services from QFS.

Physical items purchased online during an average month in 2018 by Nordic country

TOP GOODS PURCHASED ONLINE IN THE NORDICS DURING 2018, % BREAKDOWN

39

28

23

32

12 12 12

7

36

22

25

10

1412

10

6

38

2526

17

1113

11

8

35

2523

89 9

8

4

0

5

10

15

20

25

30

35

40

45

Clothing/Shoes Media HomeElectronics

Beauty/Health Sport/Leisure Furniture/HomeFurnishings

Groceries Children'sProducts/Toys

Pe

rce

nta

ge

%

Sweden Norway Denmark Finland

Source: Postnord

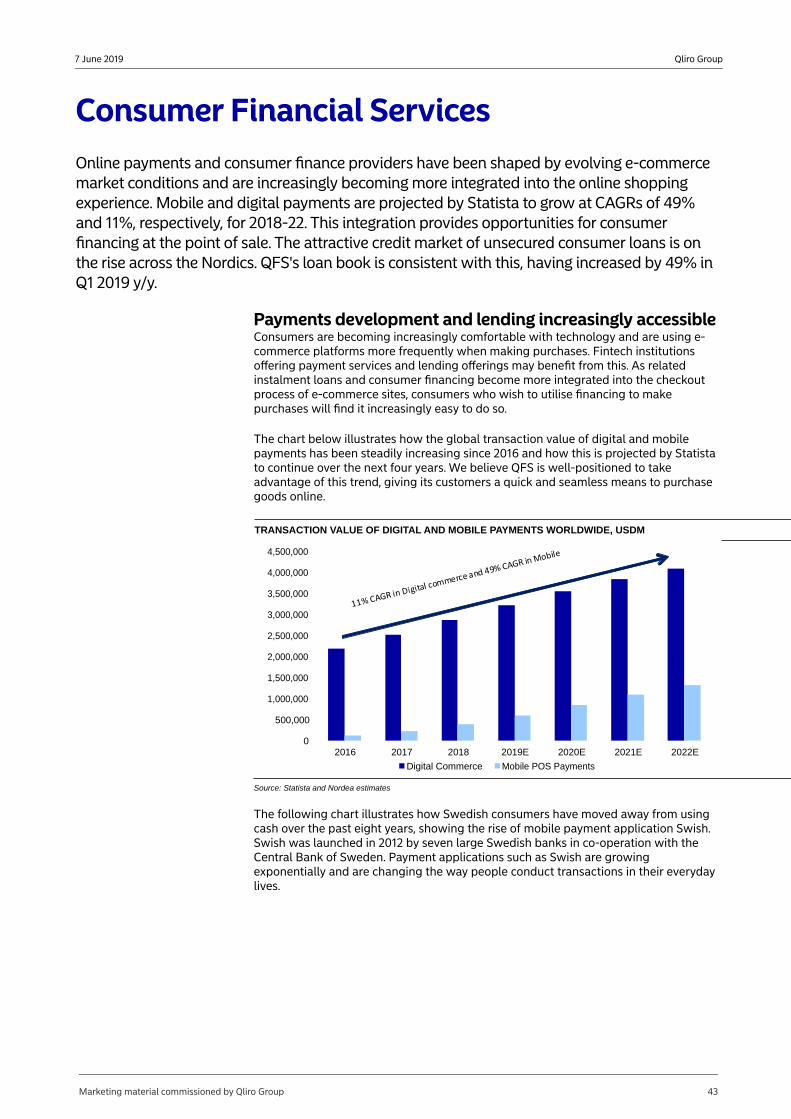

Growing consumer finance shaped by e-commerceOnline payments and consumer finance providers have been shaped by evolving e-commerce market conditions and are increasingly becoming more integrated into the online shopping experience. Mobile and digital payments are projected by Statista to grow at CAGRs of 49% and 11%, respectively, for 2018-22. This integration provides opportunities for consumer financing at the point of sale. The attractive credit market of unsecured consumer loans is on the rise across the Nordics. QFS's loan book is consistent with this, having increased by 49% in Q1 2019 y/y.

Marketing material commissioned by Qliro Group 5

Qliro Group7 June 2019

TRANSACTION VALUE OF DIGITAL AND MOBILE PAYMENTS WORLDWIDE, USDm

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2016 2017 2018 2019E 2020E 2021E 2022E

Digital Commerce Mobile POS Payments

Source: Statista

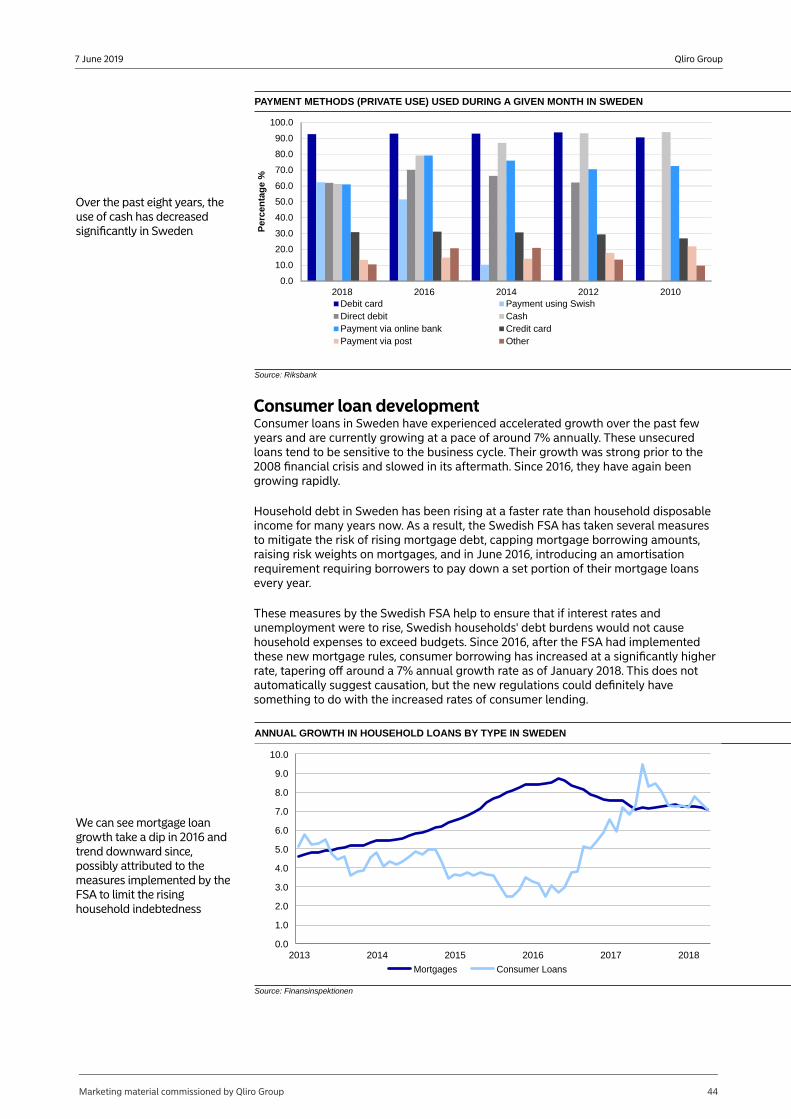

Swedish consumers have moved away from using cash over the past eight years, highlighted by the rise of the mobile payment application Swish. Swish was launched in 2012 by seven large Swedish banks in co-operation with the Central Bank of Sweden. Payment applications such as Swish are growing exponentially and are changing the way people conduct transactions in their everyday lives.

PAYMENT METHODS (PRIVATE USE) USED DURING A GIVEN MONTH IN SWEDEN

Over the past eight years, the use of cash has decreased significantly in Sweden

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2018 2016 2014 2012 2010

Per

cen

tag

e %

Debit card Payment using SwishDirect debit CashPayment via online bank Credit cardPayment via post Other

Source: Riksbank

Consumer loan developmentConsumer loans in Sweden have experienced accelerated growth over the past few years and are growing at a pace of around 7% annually, according to Finansinspektionen. These unsecured loans tend to be sensitive to the business cycle. Their growth was strong prior to the 2008 financial crisis and slowed in its aftermath. Since 2016, data from the Swedish FSA shows that they have again been growing rapidly.

Household debt in Sweden has been rising at a faster rate than household disposable income for many years. As a result, the Swedish FSA has taken several measures to mitigate the risk of rising mortgage debt, capping mortgage borrowing amounts, raising risk weights on mortgages, and in June 2016, introducing an amortisation requirement mandating that borrowers pay down a set portion of their mortgage loans every year.

Marketing material commissioned by Qliro Group 6

Qliro Group7 June 2019

These measures by the Swedish FSA help to ensure that if interest rates and unemployment were to rise, Swedish households' debt burdens would not cause household expenses to exceed budgets. Since 2016, after the FSA had implemented these new mortgage rules, consumer borrowing has increased at a significantly higher rate, tapering off at around a 7% annual growth rate as of January 2018. This does not automatically suggest causation, but the new regulations could definitely have something to do with the increased rates of consumer lending.

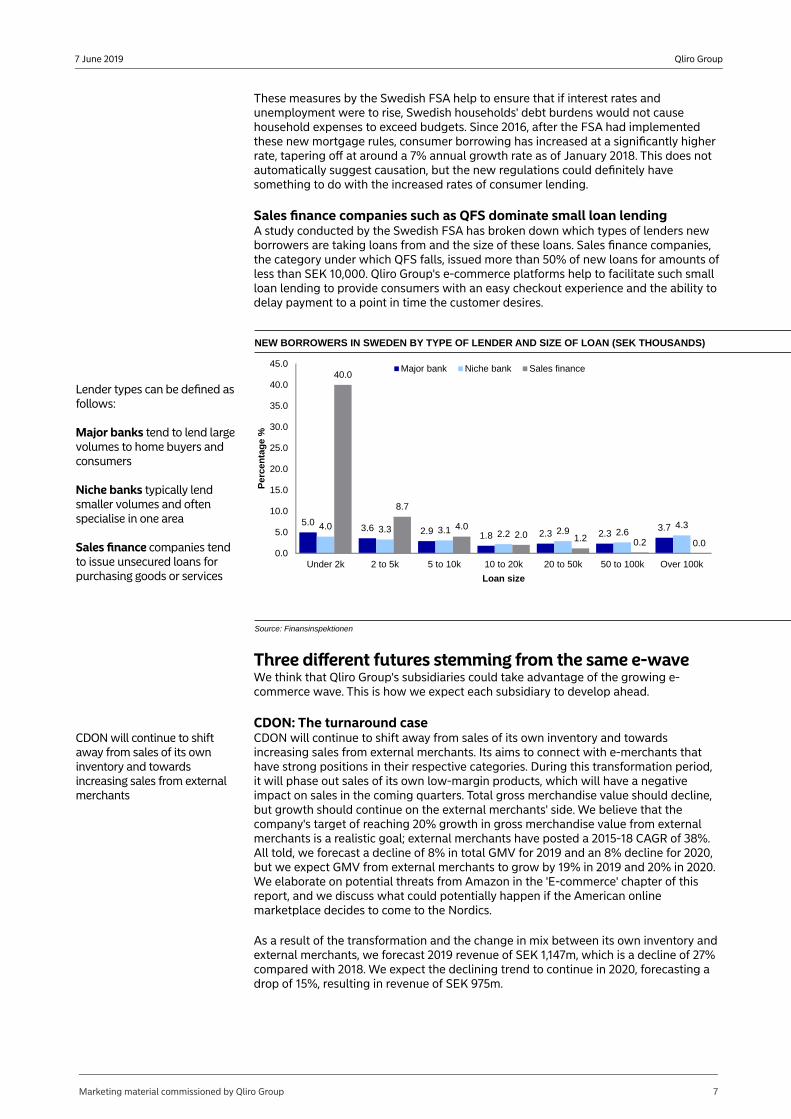

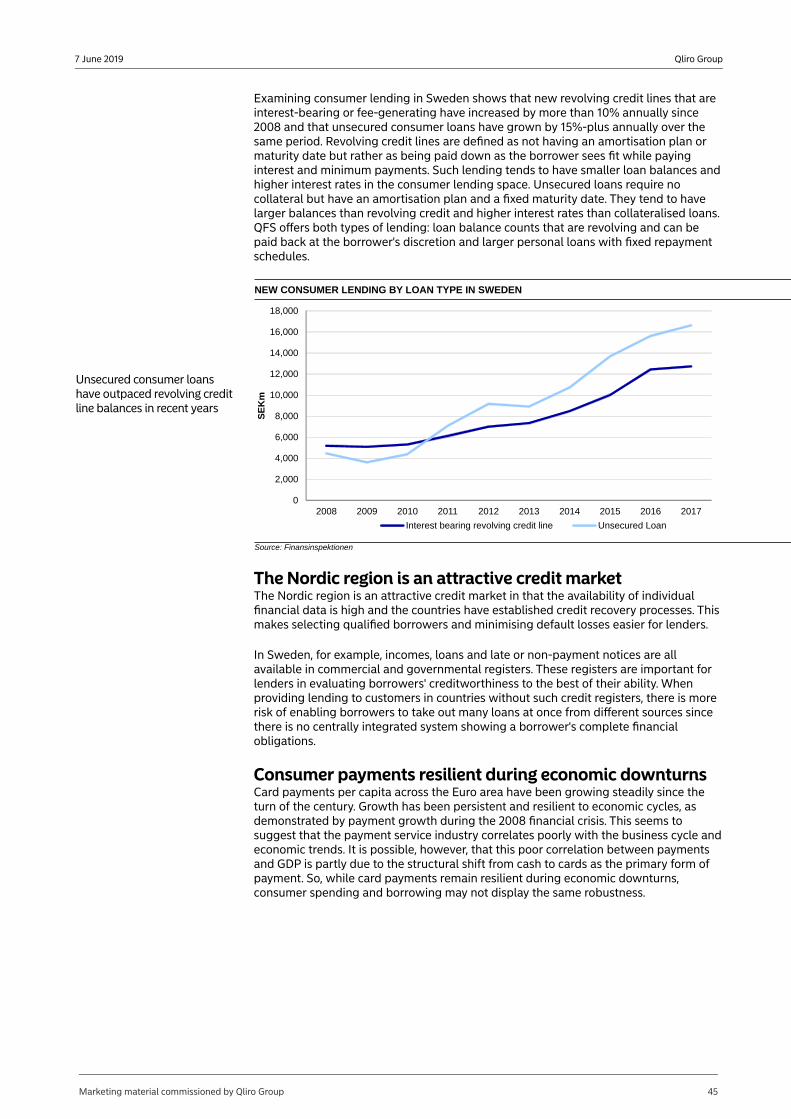

Sales finance companies such as QFS dominate small loan lendingA study conducted by the Swedish FSA has broken down which types of lenders new borrowers are taking loans from and the size of these loans. Sales finance companies, the category under which QFS falls, issued more than 50% of new loans for amounts of less than SEK 10,000. Qliro Group's e-commerce platforms help to facilitate such small loan lending to provide consumers with an easy checkout experience and the ability to delay payment to a point in time the customer desires.

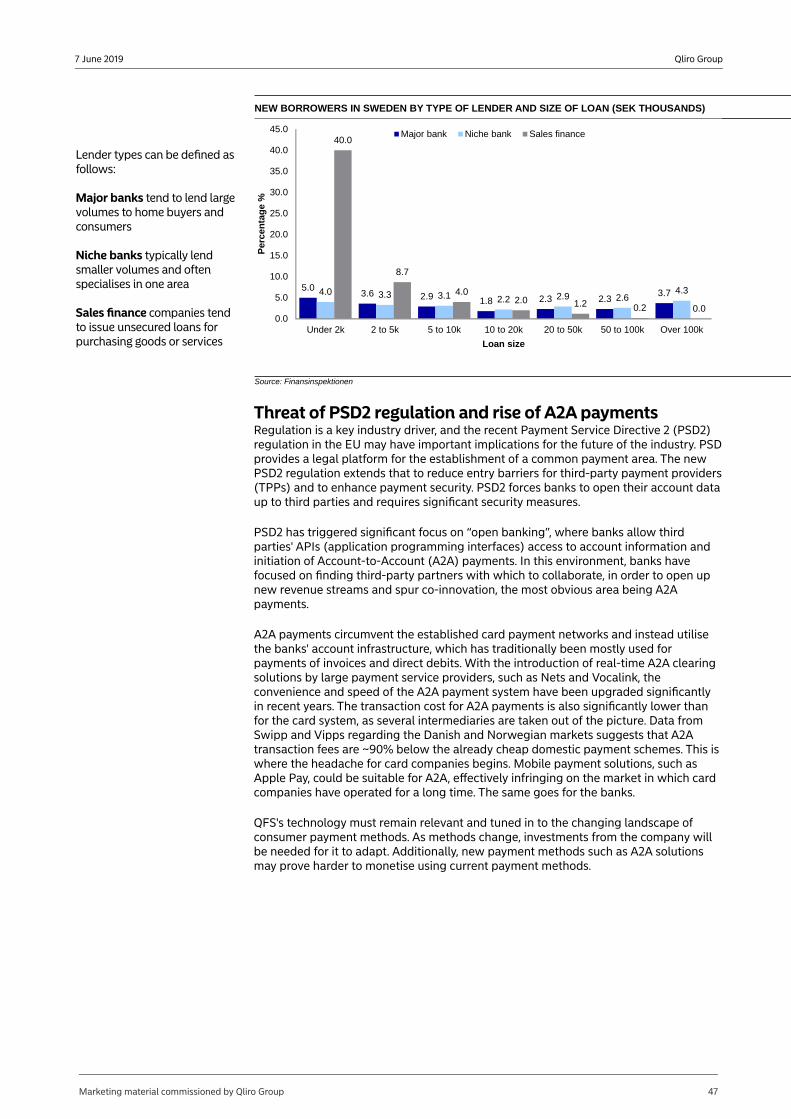

NEW BORROWERS IN SWEDEN BY TYPE OF LENDER AND SIZE OF LOAN (SEK THOUSANDS)

Lender types can be defined as follows:

Major banks tend to lend large volumes to home buyers and consumers

Niche banks typically lend smaller volumes and often specialise in one area

Sales finance companies tend to issue unsecured loans for purchasing goods or services

5.03.6 2.9 1.8 2.3 2.3

3.74.0 3.3 3.1 2.2 2.9 2.64.3

40.0

8.7

4.02.0 1.2 0.2 0.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Under 2k 2 to 5k 5 to 10k 10 to 20k 20 to 50k 50 to 100k Over 100k

Per

cen

tag

e %

Loan size

Major bank Niche bank Sales finance

Source: Finansinspektionen

Three different futures stemming from the same e-waveWe think that Qliro Group's subsidiaries could take advantage of the growing e-commerce wave. This is how we expect each subsidiary to develop ahead.

CDON: The turnaround caseCDON will continue to shift away from sales of its own inventory and towards increasing sales from external merchants

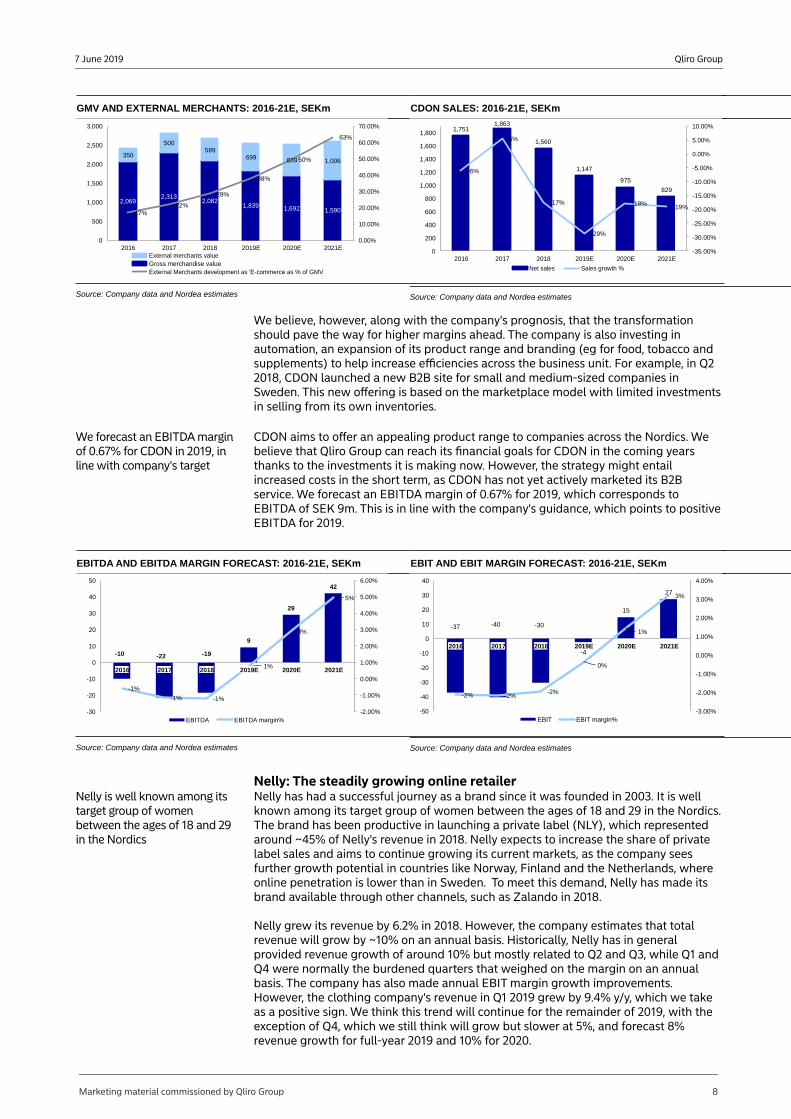

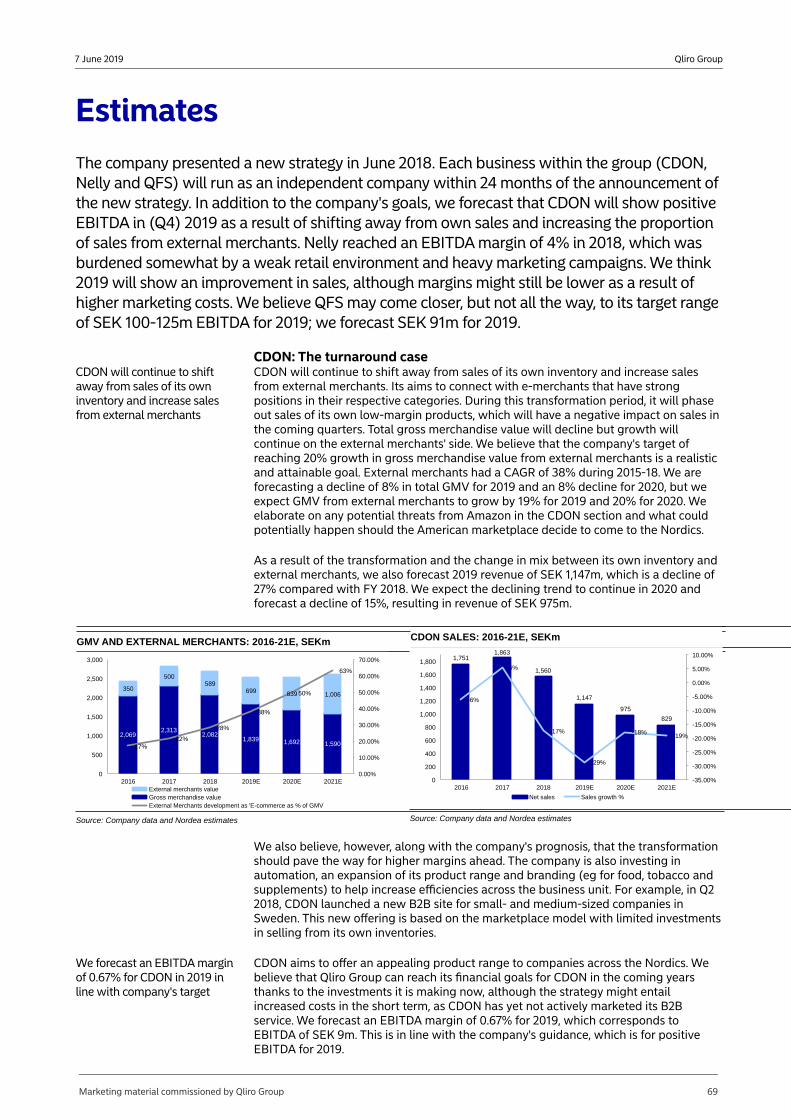

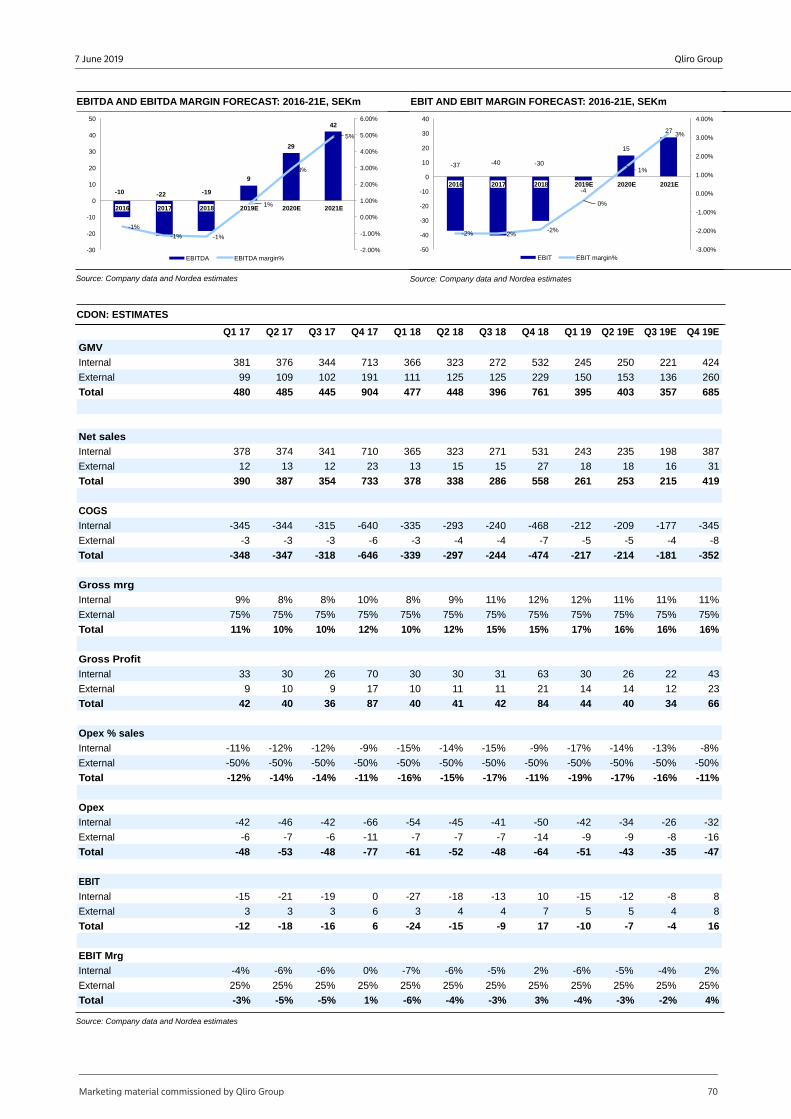

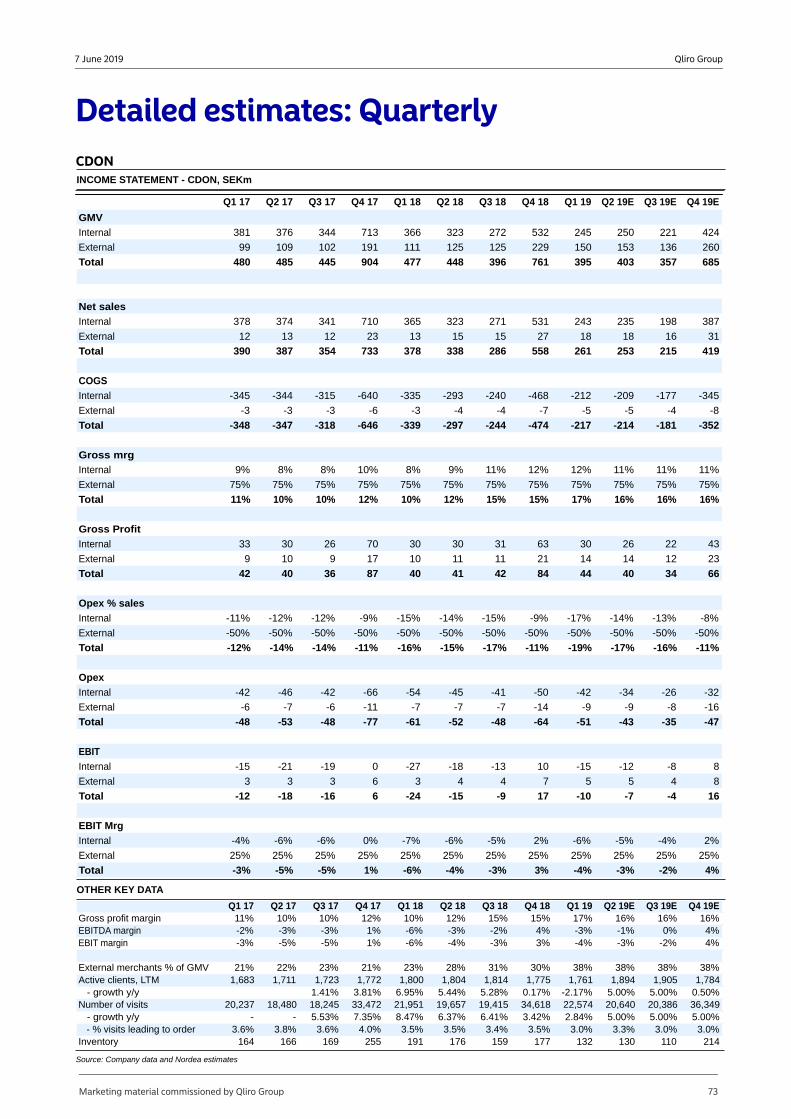

CDON will continue to shift away from sales of its own inventory and towards increasing sales from external merchants. Its aims to connect with e-merchants that have strong positions in their respective categories. During this transformation period, it will phase out sales of its own low-margin products, which will have a negative impact on sales in the coming quarters. Total gross merchandise value should decline, but growth should continue on the external merchants' side. We believe that the company's target of reaching 20% growth in gross merchandise value from external merchants is a realistic goal; external merchants have posted a 2015-18 CAGR of 38%. All told, we forecast a decline of 8% in total GMV for 2019 and an 8% decline for 2020, but we expect GMV from external merchants to grow by 19% in 2019 and 20% in 2020. We elaborate on potential threats from Amazon in the 'E-commerce' chapter of this report, and we discuss what could potentially happen if the American online marketplace decides to come to the Nordics.

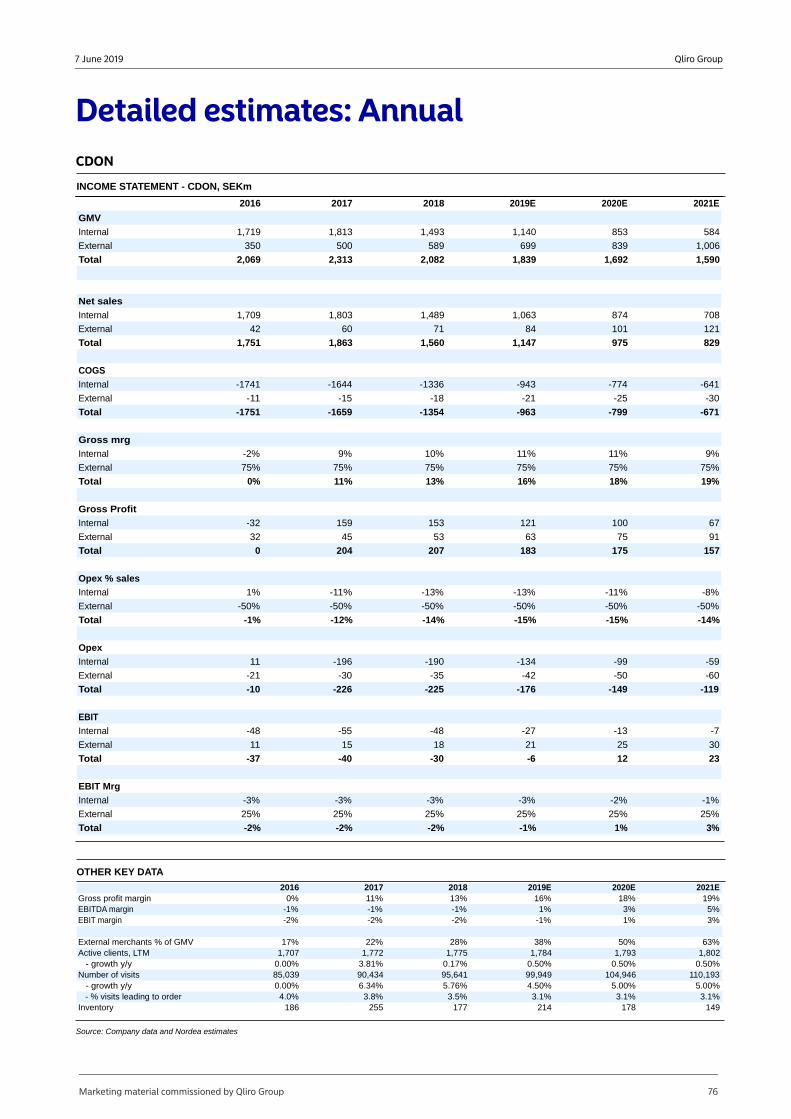

As a result of the transformation and the change in mix between its own inventory and external merchants, we forecast 2019 revenue of SEK 1,147m, which is a decline of 27% compared with 2018. We expect the declining trend to continue in 2020, forecasting a drop of 15%, resulting in revenue of SEK 975m.

Marketing material commissioned by Qliro Group 7

Qliro Group7 June 2019

GMV AND EXTERNAL MERCHANTS: 2016-21E, SEKm

2,0692,313

2,0821,839 1,692 1,590

350

500589

699 839 1,006

17%22%

28%

38%

50%

63%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

0

500

1,000

1,500

2,000

2,500

3,000

2016 2017 2018 2019E 2020E 2021EExternal merchants valueGross merchandise valueExternal Merchants development as 'E-commerce as % of GMV

Source: Company data and Nordea estimates

CDON SALES: 2016-21E, SEKm

1,7511,863

1,560

1,147

975

829

-6%

6%

-17%

-29%

-18% -19%

-35.00%

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2016 2017 2018 2019E 2020E 2021E

Net sales Sales growth %

Source: Company data and Nordea estimates

We believe, however, along with the company's prognosis, that the transformation should pave the way for higher margins ahead. The company is also investing in automation, an expansion of its product range and branding (eg for food, tobacco and supplements) to help increase efficiencies across the business unit. For example, in Q2 2018, CDON launched a new B2B site for small and medium-sized companies in Sweden. This new offering is based on the marketplace model with limited investments in selling from its own inventories.

We forecast an EBITDA margin of 0.67% for CDON in 2019, in line with company's target

CDON aims to offer an appealing product range to companies across the Nordics. We believe that Qliro Group can reach its financial goals for CDON in the coming years thanks to the investments it is making now. However, the strategy might entail increased costs in the short term, as CDON has not yet actively marketed its B2B service. We forecast an EBITDA margin of 0.67% for 2019, which corresponds to EBITDA of SEK 9m. This is in line with the company's guidance, which points to positive EBITDA for 2019.

EBITDA AND EBITDA MARGIN FORECAST: 2016-21E, SEKm

-10 -22 -19

9

29

42

-1%

-1% -1%

1%

3%

5%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

-30

-20

-10

0

10

20

30

40

50

2016 2017 2018 2019E 2020E 2021E

EBITDA EBITDA margin%

Source: Company data and Nordea estimates

EBIT AND EBIT MARGIN FORECAST: 2016-21E, SEKm

-37 -40 -30

-4

15

27

-2% -2%-2%

0%

1%

3%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

-50

-40

-30

-20

-10

0

10

20

30

40

2016 2017 2018 2019E 2020E 2021E

EBIT EBIT margin%

Source: Company data and Nordea estimates

Nelly: The steadily growing online retailerNelly is well known among its target group of women between the ages of 18 and 29 in the Nordics

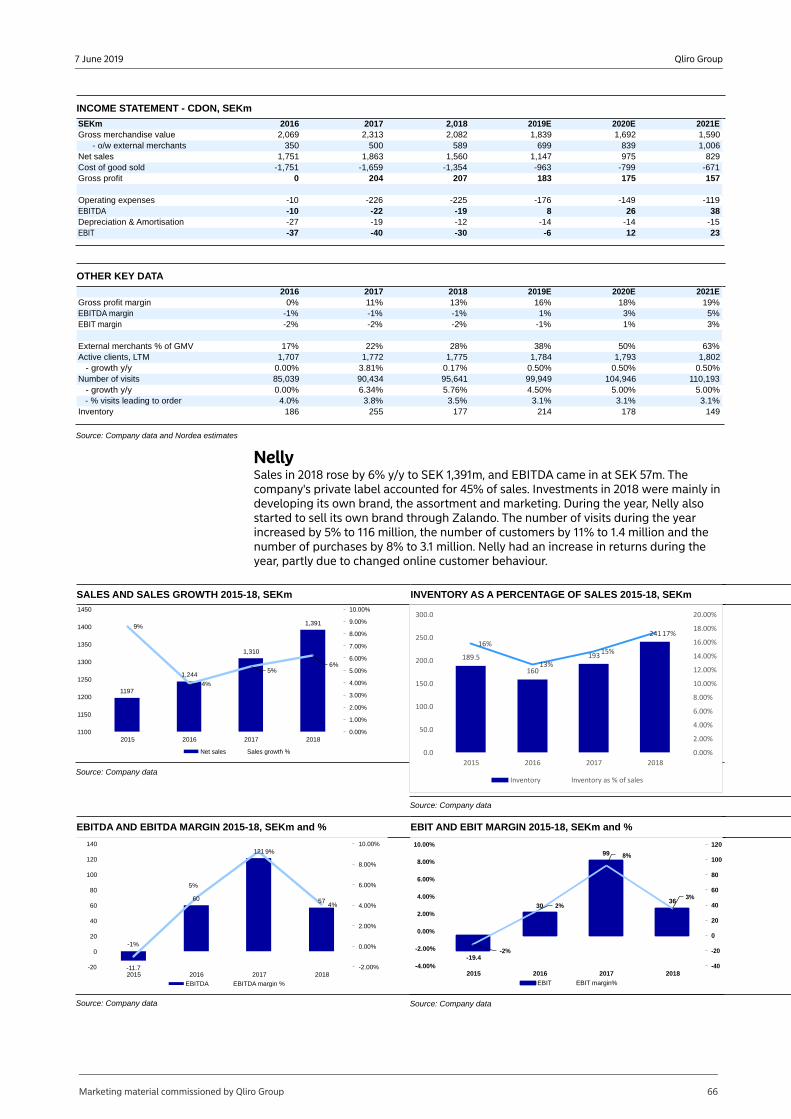

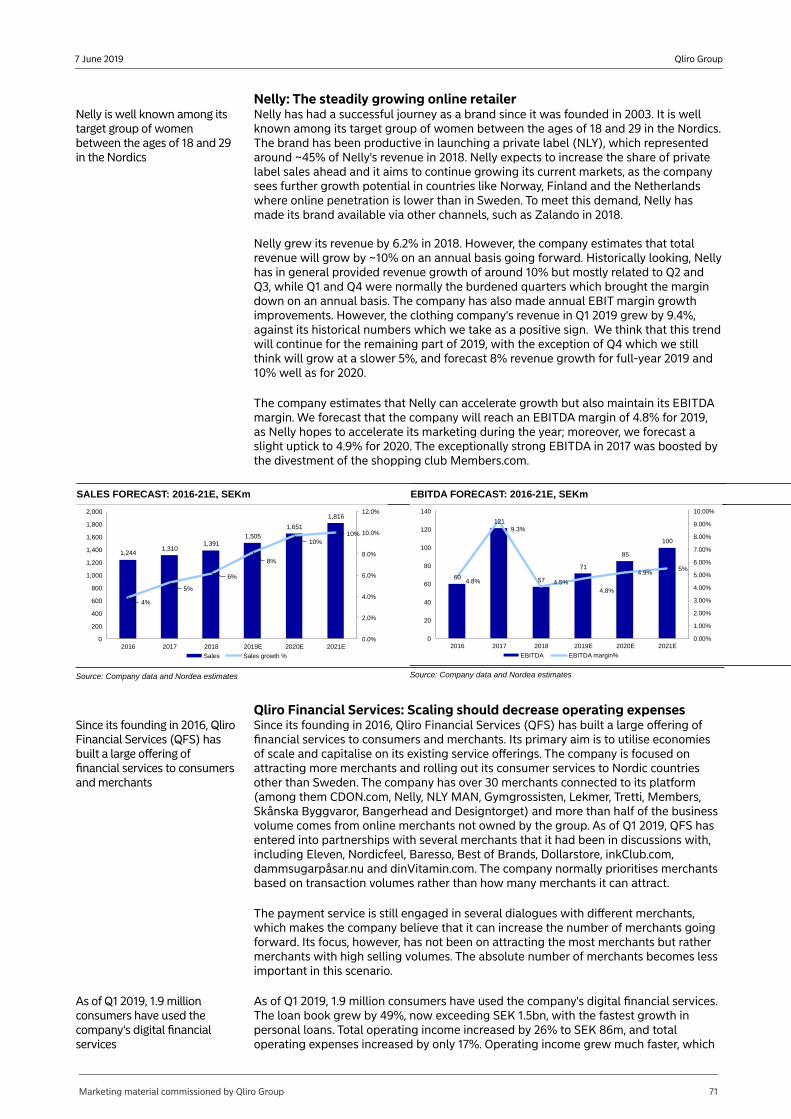

Nelly has had a successful journey as a brand since it was founded in 2003. It is well known among its target group of women between the ages of 18 and 29 in the Nordics. The brand has been productive in launching a private label (NLY), which represented around ~45% of Nelly's revenue in 2018. Nelly expects to increase the share of private label sales and aims to continue growing its current markets, as the company sees further growth potential in countries like Norway, Finland and the Netherlands, where online penetration is lower than in Sweden. To meet this demand, Nelly has made its brand available through other channels, such as Zalando in 2018.

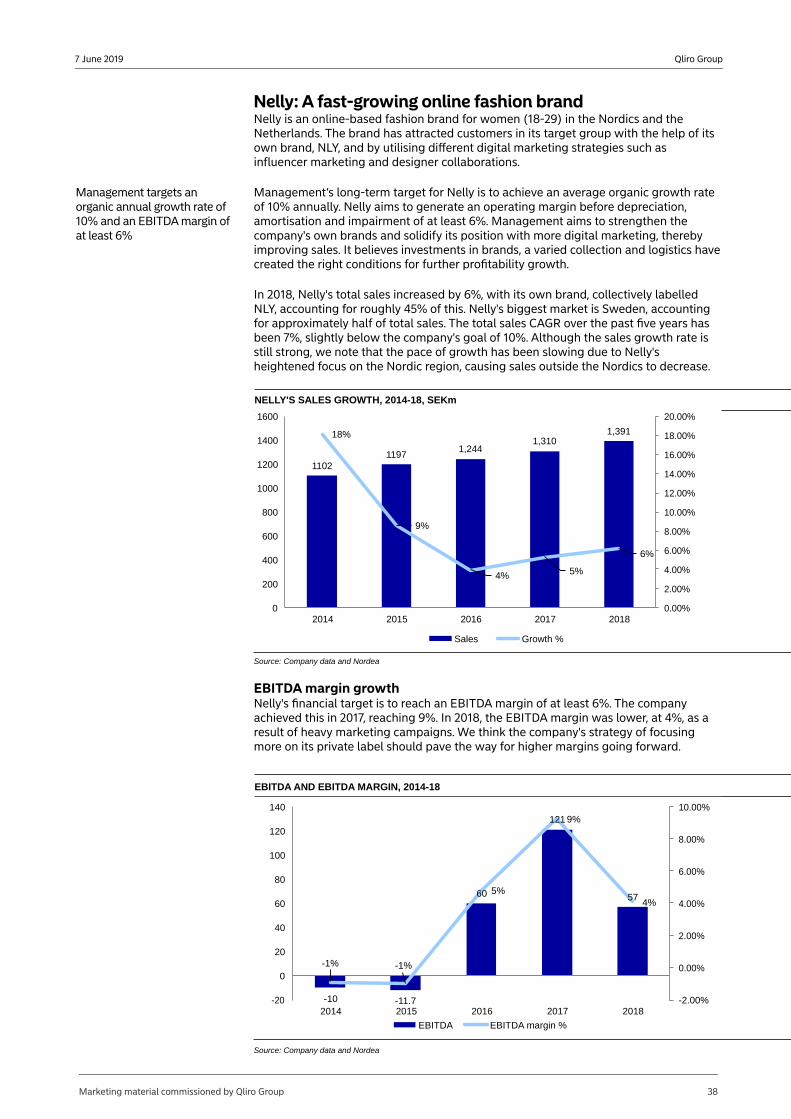

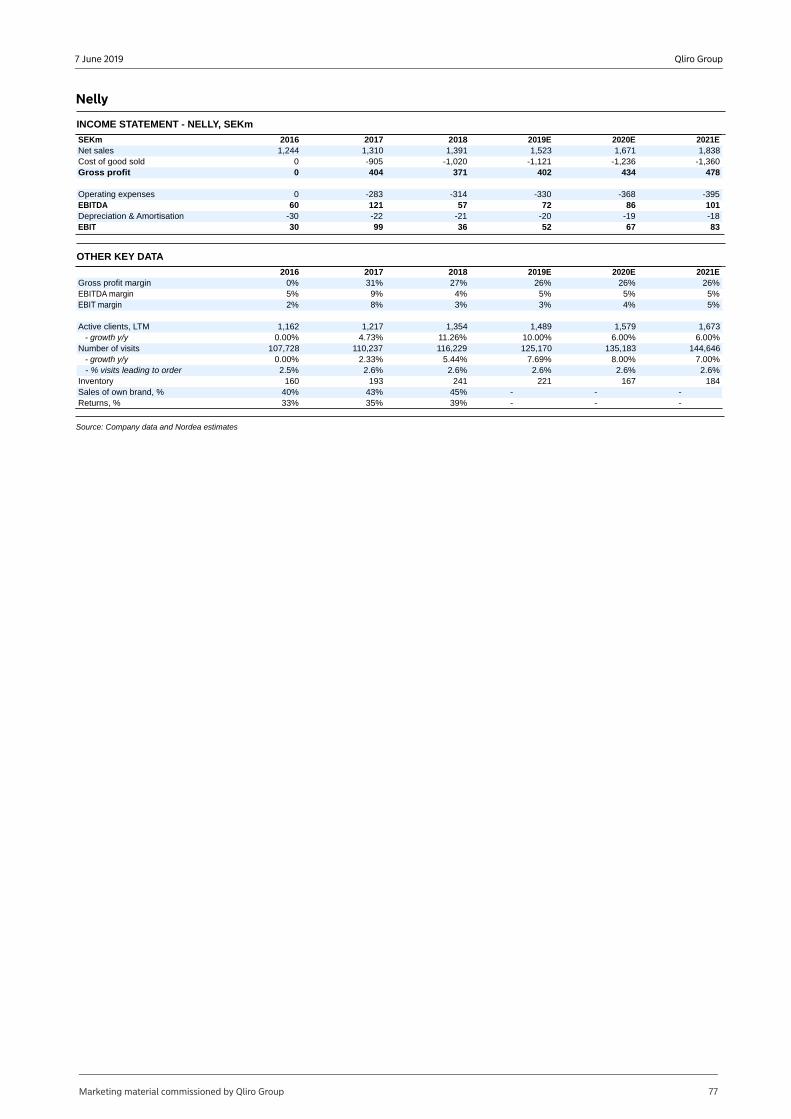

Nelly grew its revenue by 6.2% in 2018. However, the company estimates that total revenue will grow by ~10% on an annual basis. Historically, Nelly has in general provided revenue growth of around 10% but mostly related to Q2 and Q3, while Q1 and Q4 were normally the burdened quarters that weighed on the margin on an annual basis. The company has also made annual EBIT margin growth improvements. However, the clothing company's revenue in Q1 2019 grew by 9.4% y/y, which we take as a positive sign. We think this trend will continue for the remainder of 2019, with the exception of Q4, which we still think will grow but slower at 5%, and forecast 8% revenue growth for full-year 2019 and 10% for 2020.

Marketing material commissioned by Qliro Group 8

Qliro Group7 June 2019

The company estimates that Nelly can accelerate growth but also maintain its EBITDA margin. We forecast that the company will reach an EBITDA margin of 4.8% for 2019, as Nelly hopes to accelerate its marketing during the year; moreover, we forecast a slight uptick to 4.9% for 2020. The exceptionally strong EBITDA in 2017 was boosted by the divestment of the shopping club Members.com.

SALES FORECAST: 2016-21E, SEKm

1,2441,310

1,3911,505

1,651

1,816

4%

5%

6%

8%

10%10%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2016 2017 2018 2019E 2020E 2021E

Sales Sales growth %

Source: Company data and Nordea estimates

EBITDA FORECAST: 2016-21E, SEKm

60

121

57

71

85

100

4.8%

9.3%

4.5%4,8%

4.9%5%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

0

20

40

60

80

100

120

140

2016 2017 2018 2019E 2020E 2021E

EBITDA EBITDA margin%

Source: Company data and Nordea estimates

Qliro Financial Services: Scaling should decrease operating expensesSince its founding in 2016, Qliro Financial Services (QFS) has built a large offering of financial services to consumers and merchants

Since its founding in 2016, Qliro Financial Services (QFS) has built a large offering of financial services to consumers and merchants. Its primary aim is to use economies of scale and capitalise on its existing service offerings. The company is focused on attracting more merchants and rolling out its consumer services to Nordic countries other than Sweden. The company has over 30 merchants connected to its platform (among them CDON.com, Nelly, NLY MAN, Gymgrossisten, Lekmer, Tretti, Members, Skånska Byggvaror, Bangerhead and Designtorget) and more than half of the business volume comes from online merchants not owned by the group. As of Q1 2019, QFS has entered into partnerships with several merchants that it had been in discussions with, including Eleven, Nordicfeel, Baresso, Best of Brands, Dollarstore, inkClub.com, dammsugarpåsar.nu and dinVitamin.com. The company normally prioritises merchants based on transaction volumes rather than how many merchants it can attract.

The payment service is still engaged in several dialogues with different merchants, which makes the company believe that it can increase the number of merchants. Its focus, however, has not been on attracting the most merchants but rather those merchants with high selling volumes. The absolute number of merchants becomes less important in this scenario.

As of Q1 2019, 1.9m consumers have used the company's digital financial services

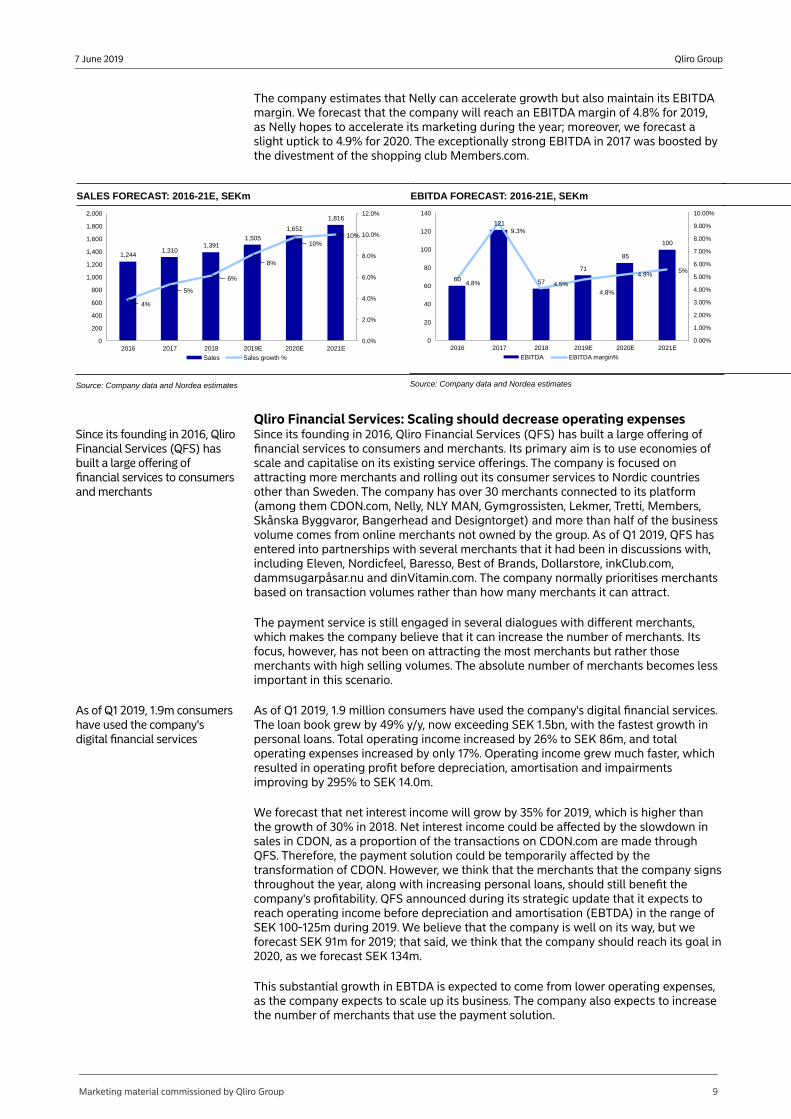

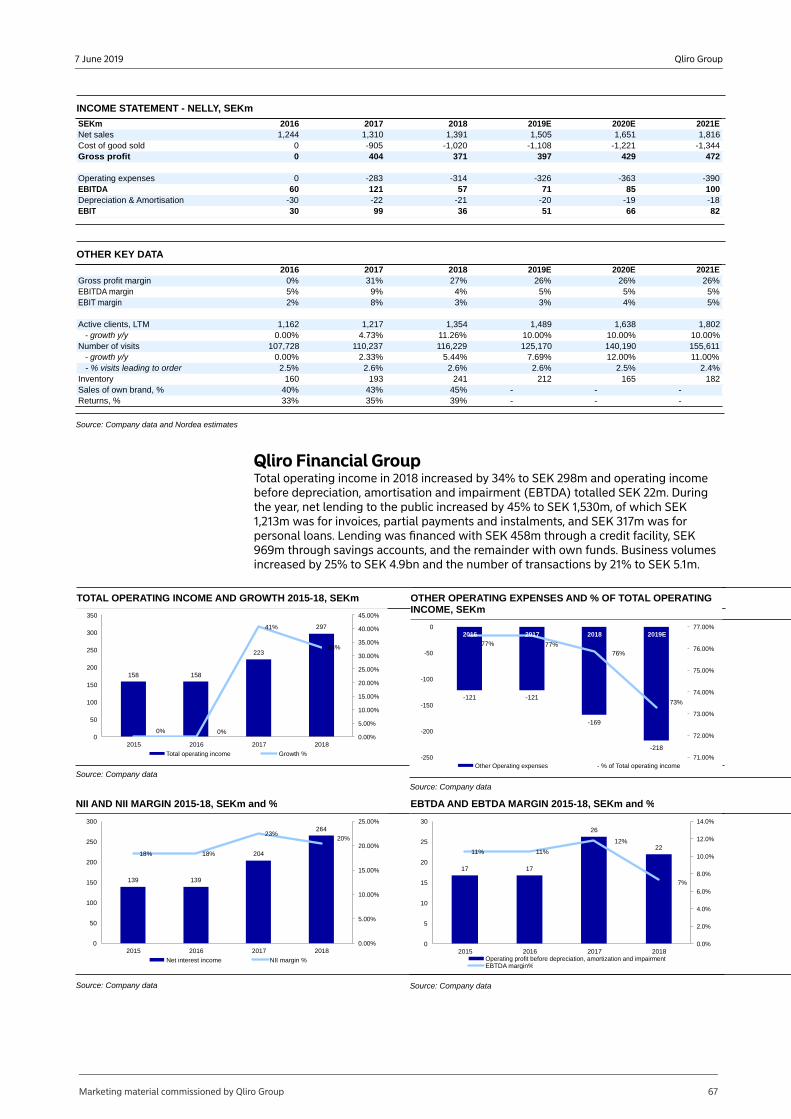

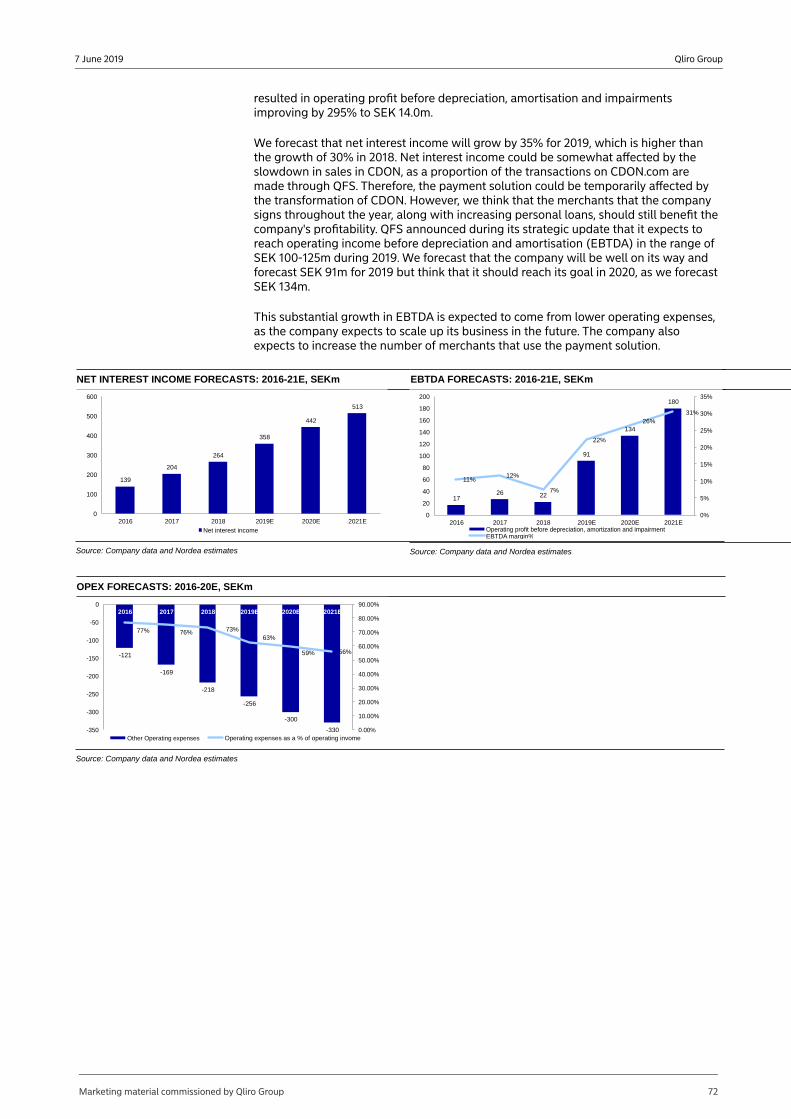

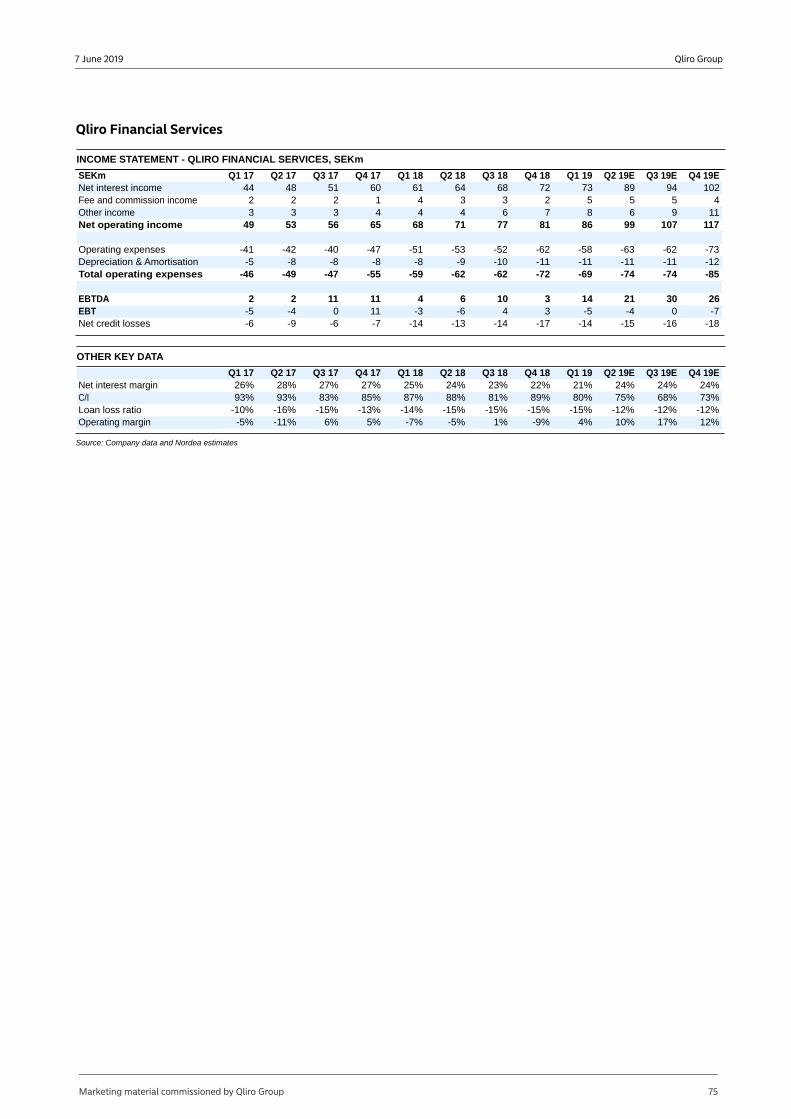

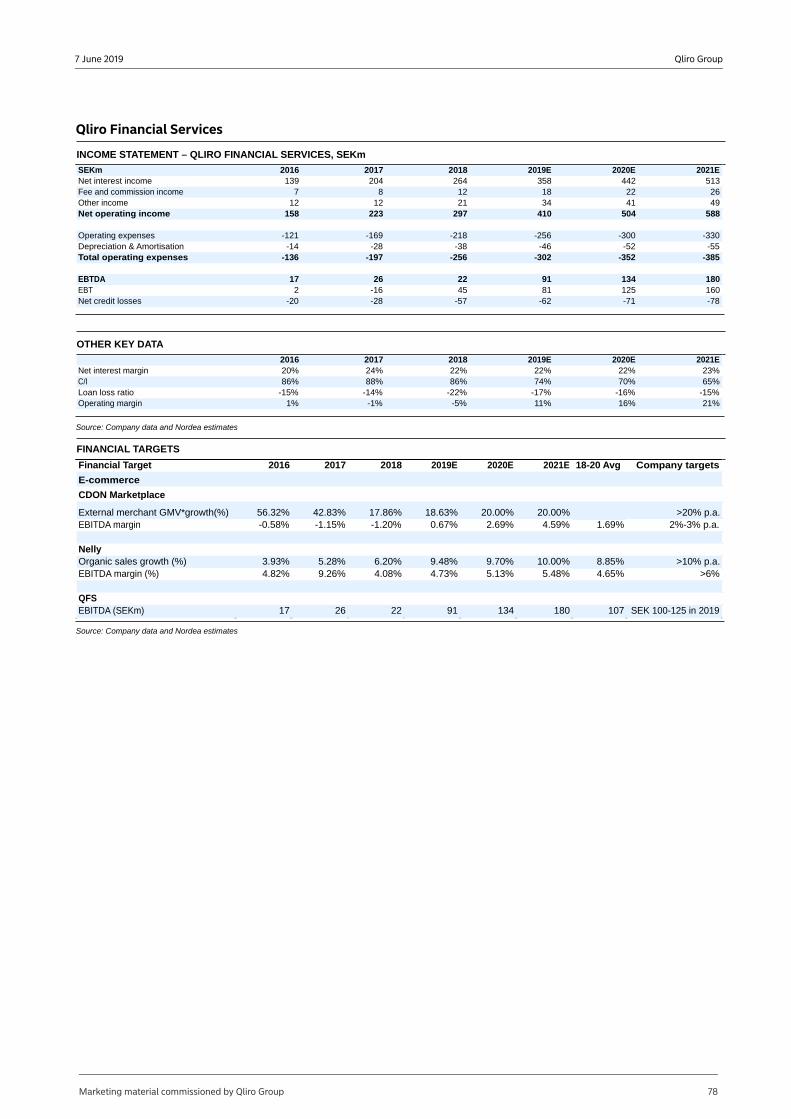

As of Q1 2019, 1.9 million consumers have used the company's digital financial services. The loan book grew by 49% y/y, now exceeding SEK 1.5bn, with the fastest growth in personal loans. Total operating income increased by 26% to SEK 86m, and total operating expenses increased by only 17%. Operating income grew much faster, which resulted in operating profit before depreciation, amortisation and impairments improving by 295% to SEK 14.0m.

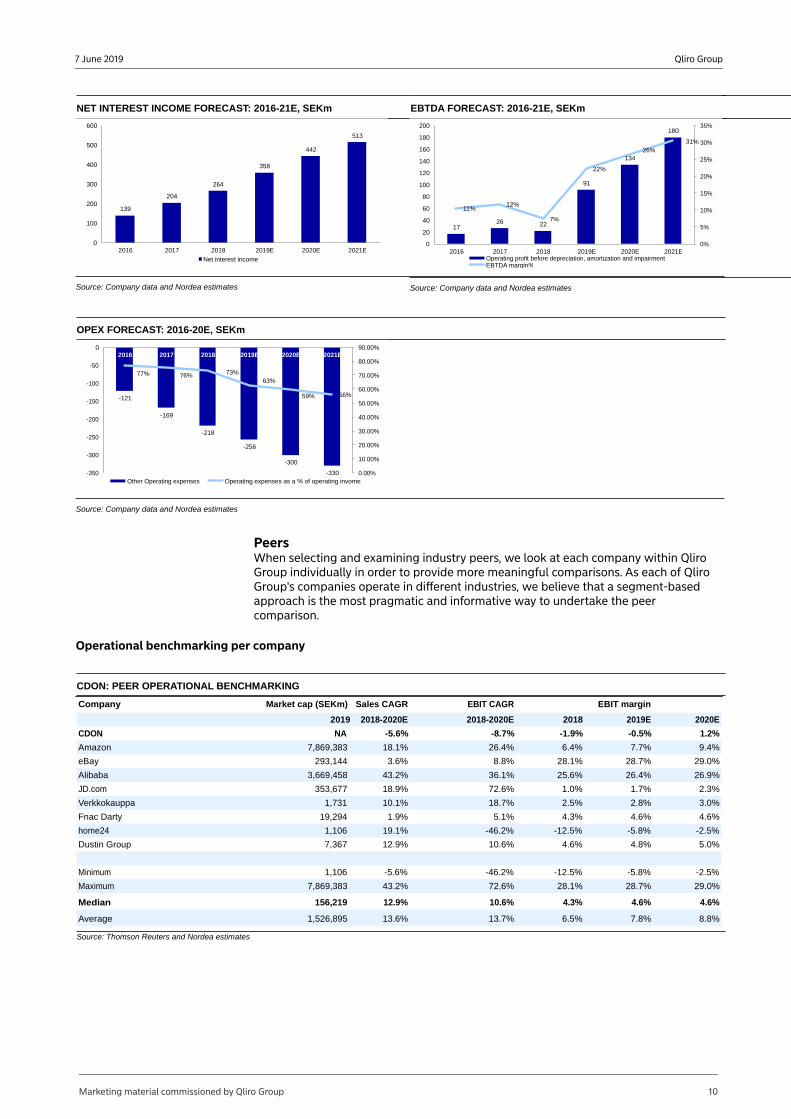

We forecast that net interest income will grow by 35% for 2019, which is higher than the growth of 30% in 2018. Net interest income could be affected by the slowdown in sales in CDON, as a proportion of the transactions on CDON.com are made through QFS. Therefore, the payment solution could be temporarily affected by the transformation of CDON. However, we think that the merchants that the company signs throughout the year, along with increasing personal loans, should still benefit the company's profitability. QFS announced during its strategic update that it expects to reach operating income before depreciation and amortisation (EBTDA) in the range of SEK 100-125m during 2019. We believe that the company is well on its way, but we forecast SEK 91m for 2019; that said, we think that the company should reach its goal in 2020, as we forecast SEK 134m.

This substantial growth in EBTDA is expected to come from lower operating expenses, as the company expects to scale up its business. The company also expects to increase the number of merchants that use the payment solution.

Marketing material commissioned by Qliro Group 9

Qliro Group7 June 2019

NET INTEREST INCOME FORECAST: 2016-21E, SEKm

139

204

264

358

442

513

0

100

200

300

400

500

600

2016 2017 2018 2019E 2020E 2021E

Net interest income

Source: Company data and Nordea estimates

EBTDA FORECAST: 2016-21E, SEKm

1726 22

91

134

180

11%12%

7%

22%

26%31%

0%

5%

10%

15%

20%

25%

30%

35%

0

20

40

60

80

100

120

140

160

180

200

2016 2017 2018 2019E 2020E 2021EOperating profit before depreciation, amortization and impairmentEBTDA margin%

Source: Company data and Nordea estimates

OPEX FORECAST: 2016-20E, SEKm

-121

-169

-218

-256

-300

-330

77% 76% 73%63%

59% 56%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

-350

-300

-250

-200

-150

-100

-50

02016 2017 2018 2019E 2020E 2021E

Other Operating expenses Operating expenses as a % of operating invome

Source: Company data and Nordea estimates

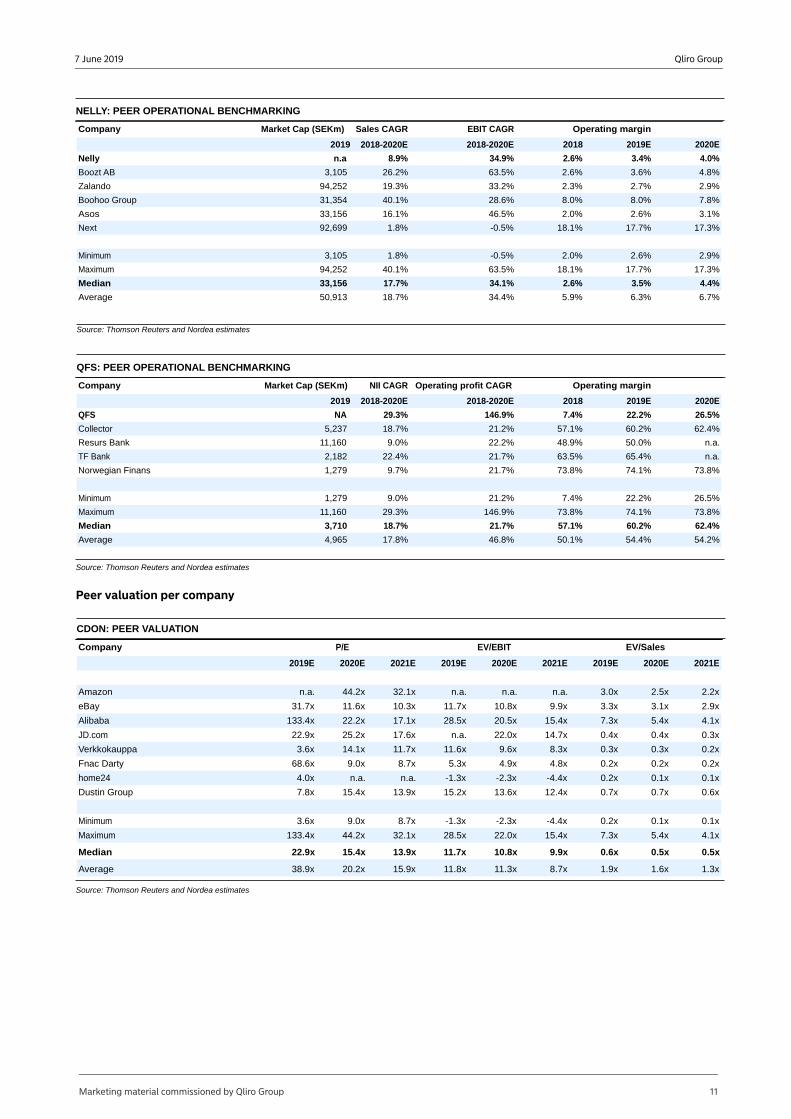

PeersWhen selecting and examining industry peers, we look at each company within Qliro Group individually in order to provide more meaningful comparisons. As each of Qliro Group's companies operate in different industries, we believe that a segment-based approach is the most pragmatic and informative way to undertake the peer comparison.

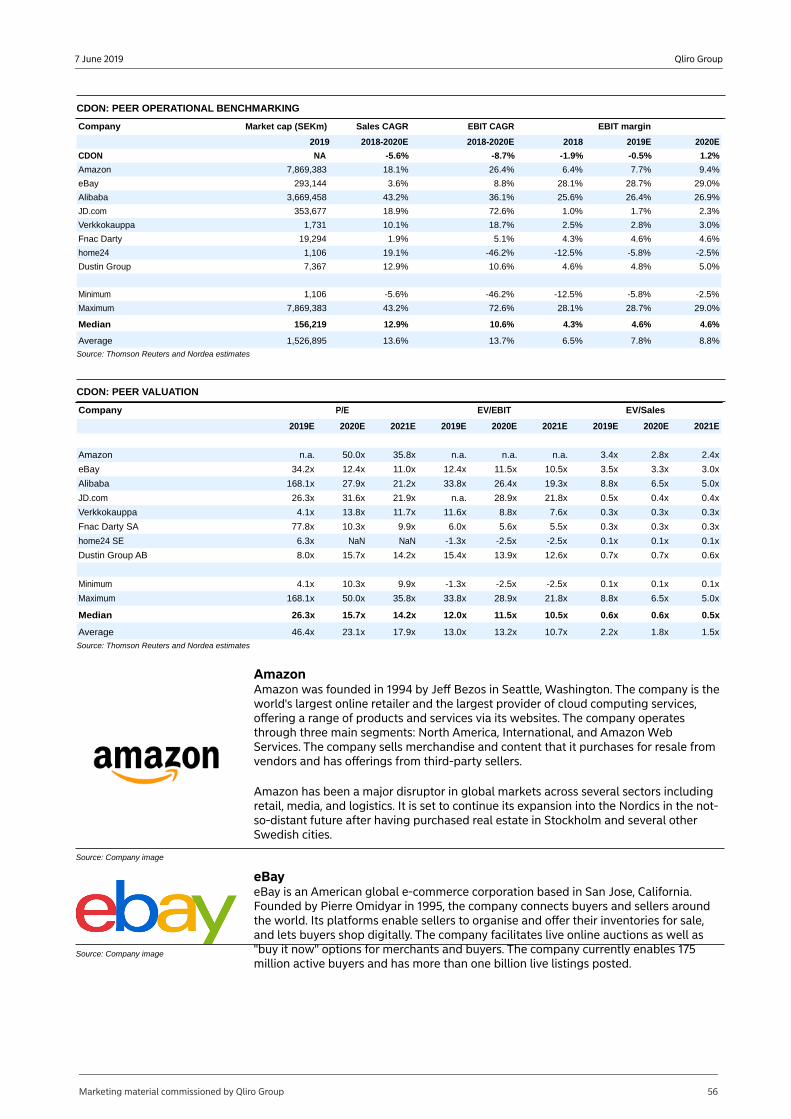

Operational benchmarking per company

CDON: PEER OPERATIONAL BENCHMARKING

Company Market cap (SEKm) Sales CAGR EBIT CAGR EBIT margin

2019 2018-2020E 2018-2020E 2018 2019E 2020E

CDON NA -5.6% -8.7% -1.9% -0.5% 1.2%

Amazon 7,869,383 18.1% 26.4% 6.4% 7.7% 9.4%

eBay 293,144 3.6% 8.8% 28.1% 28.7% 29.0%

Alibaba 3,669,458 43.2% 36.1% 25.6% 26.4% 26.9%

JD.com 353,677 18.9% 72.6% 1.0% 1.7% 2.3%

Verkkokauppa 1,731 10.1% 18.7% 2.5% 2.8% 3.0%

Fnac Darty 19,294 1.9% 5.1% 4.3% 4.6% 4.6%

home24 1,106 19.1% -46.2% -12.5% -5.8% -2.5%

Dustin Group 7,367 12.9% 10.6% 4.6% 4.8% 5.0%

Minimum 1,106 -5.6% -46.2% -12.5% -5.8% -2.5%

Maximum 7,869,383 43.2% 72.6% 28.1% 28.7% 29.0%

Median 156,219 12.9% 10.6% 4.3% 4.6% 4.6%

Average 1,526,895 13.6% 13.7% 6.5% 7.8% 8.8%

Source: Thomson Reuters and Nordea estimates

Marketing material commissioned by Qliro Group 10

Qliro Group7 June 2019

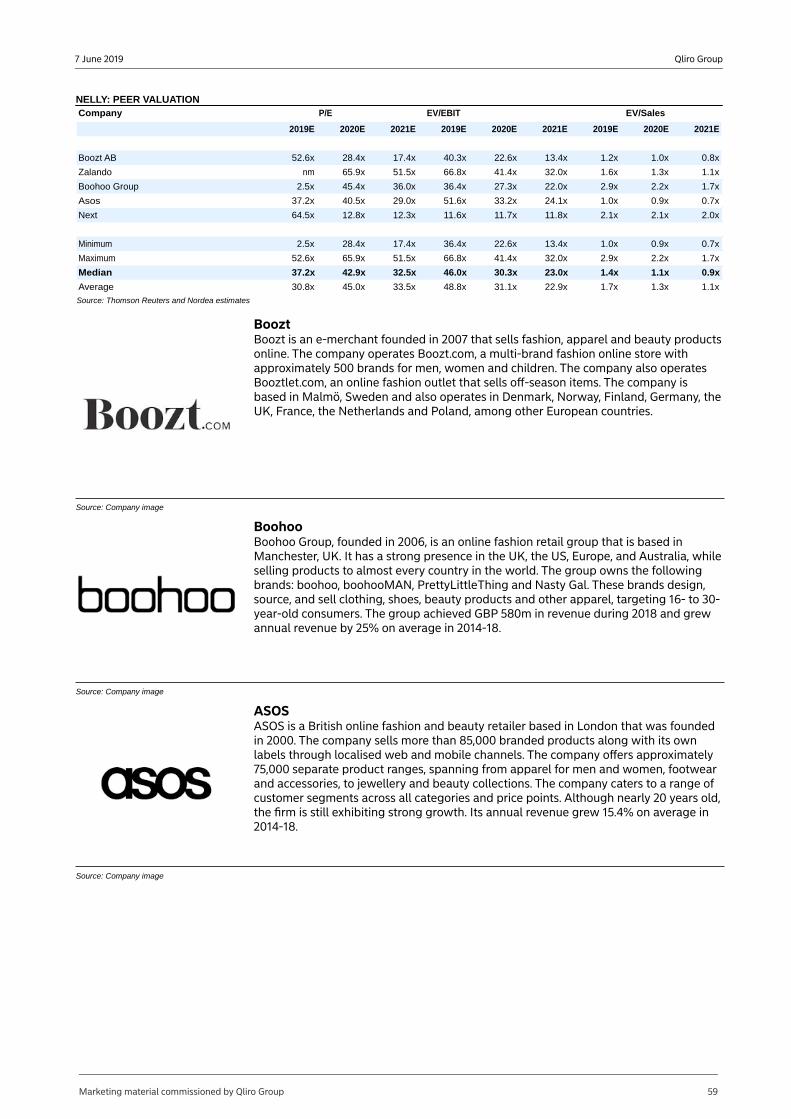

NELLY: PEER OPERATIONAL BENCHMARKING

Company Market Cap (SEKm) Sales CAGR EBIT CAGR Operating margin

2019 2018-2020E 2018-2020E 2018 2019E 2020E

Nelly n.a 8.9% 34.9% 2.6% 3.4% 4.0%

Boozt AB 3,105 26.2% 63.5% 2.6% 3.6% 4.8%

Zalando 94,252 19.3% 33.2% 2.3% 2.7% 2.9%

Boohoo Group 31,354 40.1% 28.6% 8.0% 8.0% 7.8%

Asos 33,156 16.1% 46.5% 2.0% 2.6% 3.1%

Next 92,699 1.8% -0.5% 18.1% 17.7% 17.3%

Minimum 3,105 1.8% -0.5% 2.0% 2.6% 2.9%

Maximum 94,252 40.1% 63.5% 18.1% 17.7% 17.3%

Median 33,156 17.7% 34.1% 2.6% 3.5% 4.4%

Average 50,913 18.7% 34.4% 5.9% 6.3% 6.7%

Source: Thomson Reuters and Nordea estimates

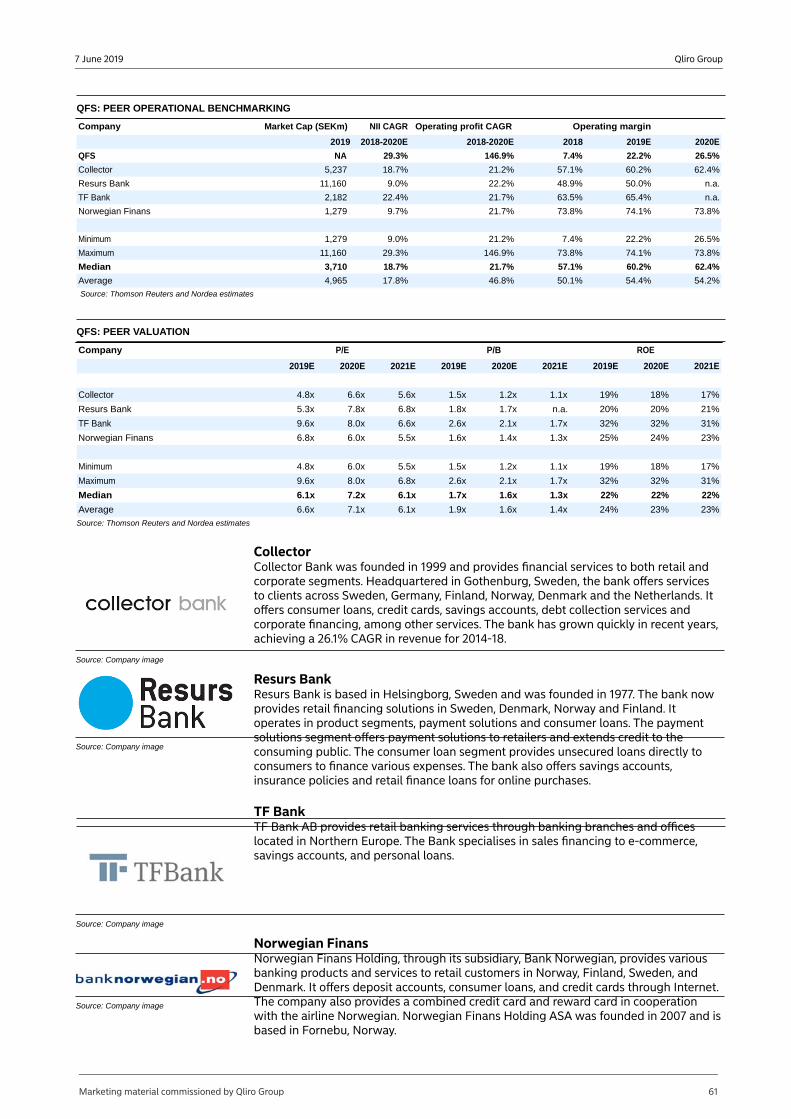

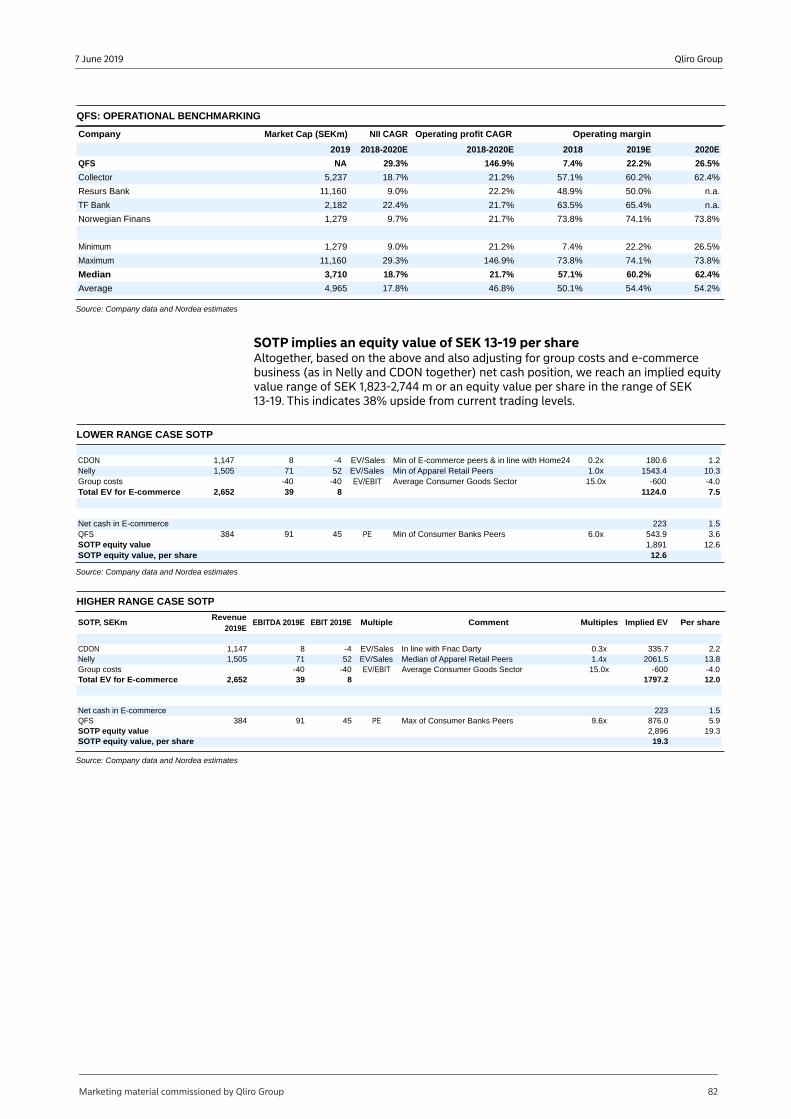

QFS: PEER OPERATIONAL BENCHMARKING

Company Market Cap (SEKm) NII CAGR Operating profit CAGR Operating margin

2019 2018-2020E 2018-2020E 2018 2019E 2020E

QFS NA 29.3% 146.9% 7.4% 22.2% 26.5%

Collector 5,237 18.7% 21.2% 57.1% 60.2% 62.4%

Resurs Bank 11,160 9.0% 22.2% 48.9% 50.0% n.a.

TF Bank 2,182 22.4% 21.7% 63.5% 65.4% n.a.

Norwegian Finans 1,279 9.7% 21.7% 73.8% 74.1% 73.8%

Minimum 1,279 9.0% 21.2% 7.4% 22.2% 26.5%

Maximum 11,160 29.3% 146.9% 73.8% 74.1% 73.8%

Median 3,710 18.7% 21.7% 57.1% 60.2% 62.4%

Average 4,965 17.8% 46.8% 50.1% 54.4% 54.2%

Source: Thomson Reuters and Nordea estimates

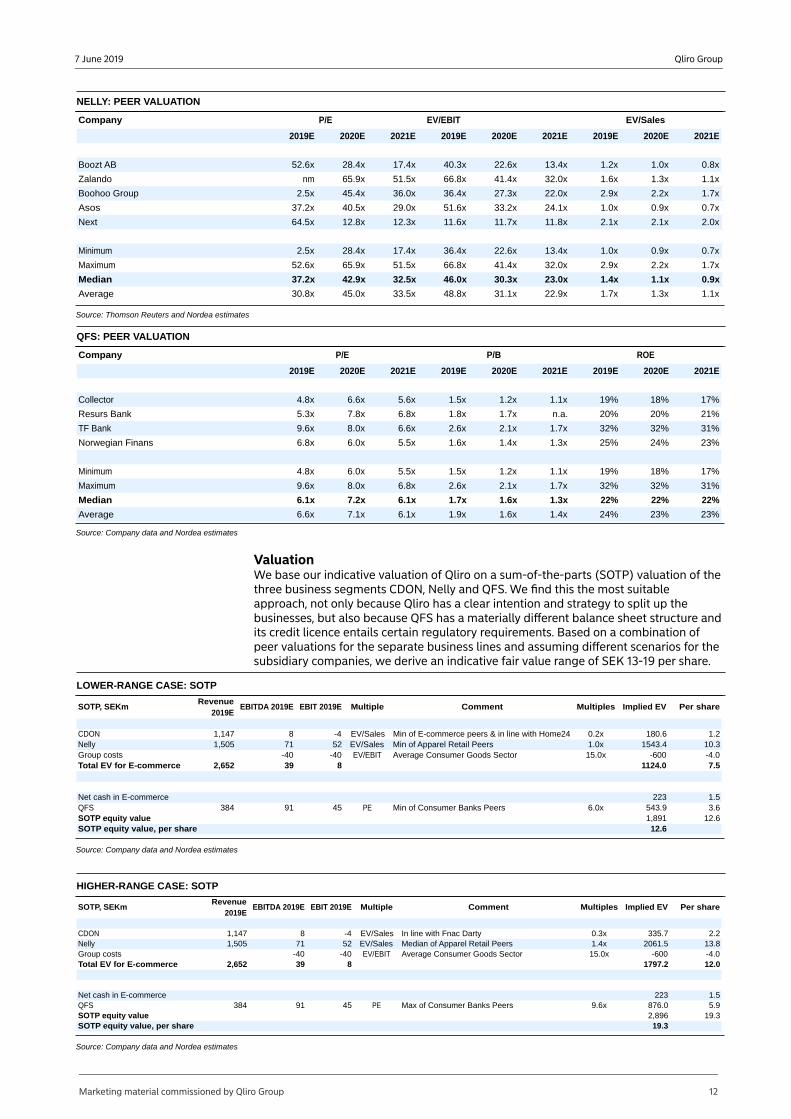

Peer valuation per company

CDON: PEER VALUATION

Company P/E

2019E 2020E 2021E 2019E 2020E 2021E 2019E 2020E 2021E

Amazon n.a. 44.2x 32.1x n.a. n.a. n.a. 3.0x 2.5x 2.2x

eBay 31.7x 11.6x 10.3x 11.7x 10.8x 9.9x 3.3x 3.1x 2.9x

Alibaba 133.4x 22.2x 17.1x 28.5x 20.5x 15.4x 7.3x 5.4x 4.1x

JD.com 22.9x 25.2x 17.6x n.a. 22.0x 14.7x 0.4x 0.4x 0.3x

Verkkokauppa 3.6x 14.1x 11.7x 11.6x 9.6x 8.3x 0.3x 0.3x 0.2x

Fnac Darty 68.6x 9.0x 8.7x 5.3x 4.9x 4.8x 0.2x 0.2x 0.2x

home24 4.0x n.a. n.a. -1.3x -2.3x -4.4x 0.2x 0.1x 0.1x

Dustin Group 7.8x 15.4x 13.9x 15.2x 13.6x 12.4x 0.7x 0.7x 0.6x

Minimum 3.6x 9.0x 8.7x -1.3x -2.3x -4.4x 0.2x 0.1x 0.1x

Maximum 133.4x 44.2x 32.1x 28.5x 22.0x 15.4x 7.3x 5.4x 4.1x

Median 22.9x 15.4x 13.9x 11.7x 10.8x 9.9x 0.6x 0.5x 0.5x

Average 38.9x 20.2x 15.9x 11.8x 11.3x 8.7x 1.9x 1.6x 1.3x

EV/EBIT EV/Sales

Source: Thomson Reuters and Nordea estimates

Marketing material commissioned by Qliro Group 11

Qliro Group7 June 2019

NELLY: PEER VALUATION

Company P/E EV/EBIT EV/Sales

2019E 2020E 2021E 2019E 2020E 2021E 2019E 2020E 2021E

Boozt AB 52.6x 28.4x 17.4x 40.3x 22.6x 13.4x 1.2x 1.0x 0.8x

Zalando nm 65.9x 51.5x 66.8x 41.4x 32.0x 1.6x 1.3x 1.1x

Boohoo Group 2.5x 45.4x 36.0x 36.4x 27.3x 22.0x 2.9x 2.2x 1.7x

Asos 37.2x 40.5x 29.0x 51.6x 33.2x 24.1x 1.0x 0.9x 0.7x

Next 64.5x 12.8x 12.3x 11.6x 11.7x 11.8x 2.1x 2.1x 2.0x

Minimum 2.5x 28.4x 17.4x 36.4x 22.6x 13.4x 1.0x 0.9x 0.7x

Maximum 52.6x 65.9x 51.5x 66.8x 41.4x 32.0x 2.9x 2.2x 1.7x

Median 37.2x 42.9x 32.5x 46.0x 30.3x 23.0x 1.4x 1.1x 0.9x

Average 30.8x 45.0x 33.5x 48.8x 31.1x 22.9x 1.7x 1.3x 1.1x

Source: Thomson Reuters and Nordea estimates

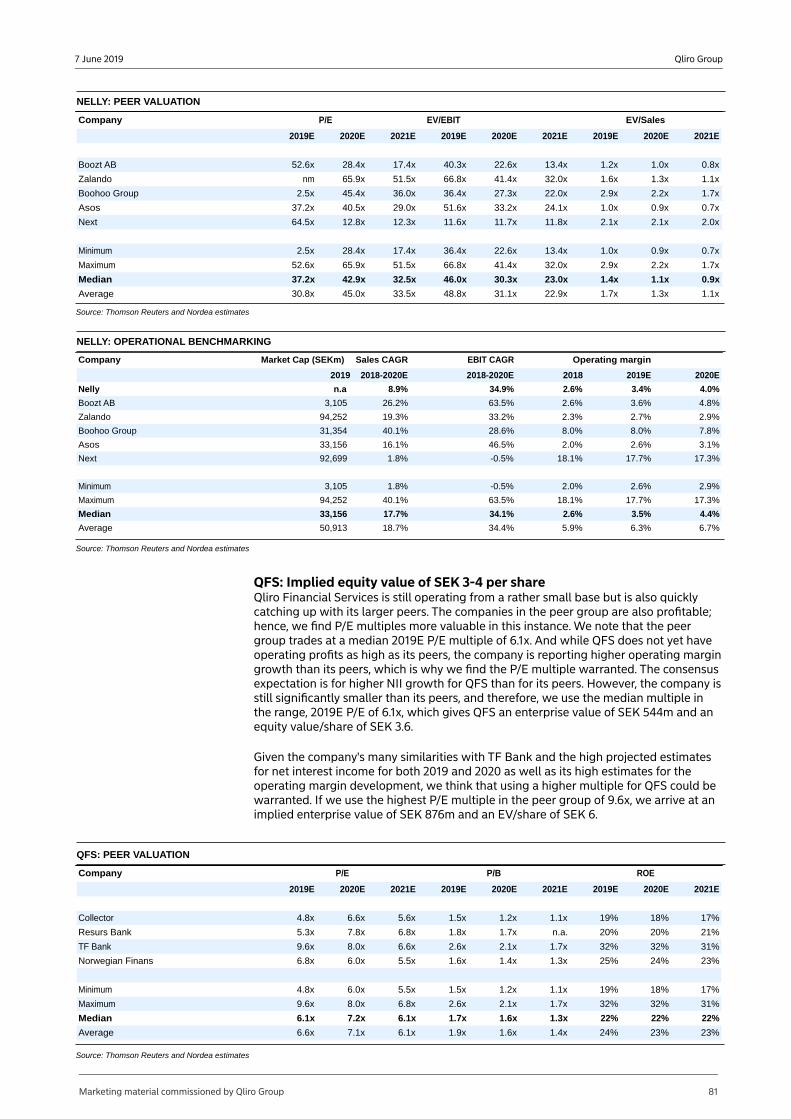

QFS: PEER VALUATION

Company P/E P/B ROE

2019E 2020E 2021E 2019E 2020E 2021E 2019E 2020E 2021E

Collector 4.8x 6.6x 5.6x 1.5x 1.2x 1.1x 19% 18% 17%

Resurs Bank 5.3x 7.8x 6.8x 1.8x 1.7x n.a. 20% 20% 21%

TF Bank 9.6x 8.0x 6.6x 2.6x 2.1x 1.7x 32% 32% 31%

Norwegian Finans 6.8x 6.0x 5.5x 1.6x 1.4x 1.3x 25% 24% 23%

Minimum 4.8x 6.0x 5.5x 1.5x 1.2x 1.1x 19% 18% 17%

Maximum 9.6x 8.0x 6.8x 2.6x 2.1x 1.7x 32% 32% 31%

Median 6.1x 7.2x 6.1x 1.7x 1.6x 1.3x 22% 22% 22%

Average 6.6x 7.1x 6.1x 1.9x 1.6x 1.4x 24% 23% 23%

Source: Company data and Nordea estimates

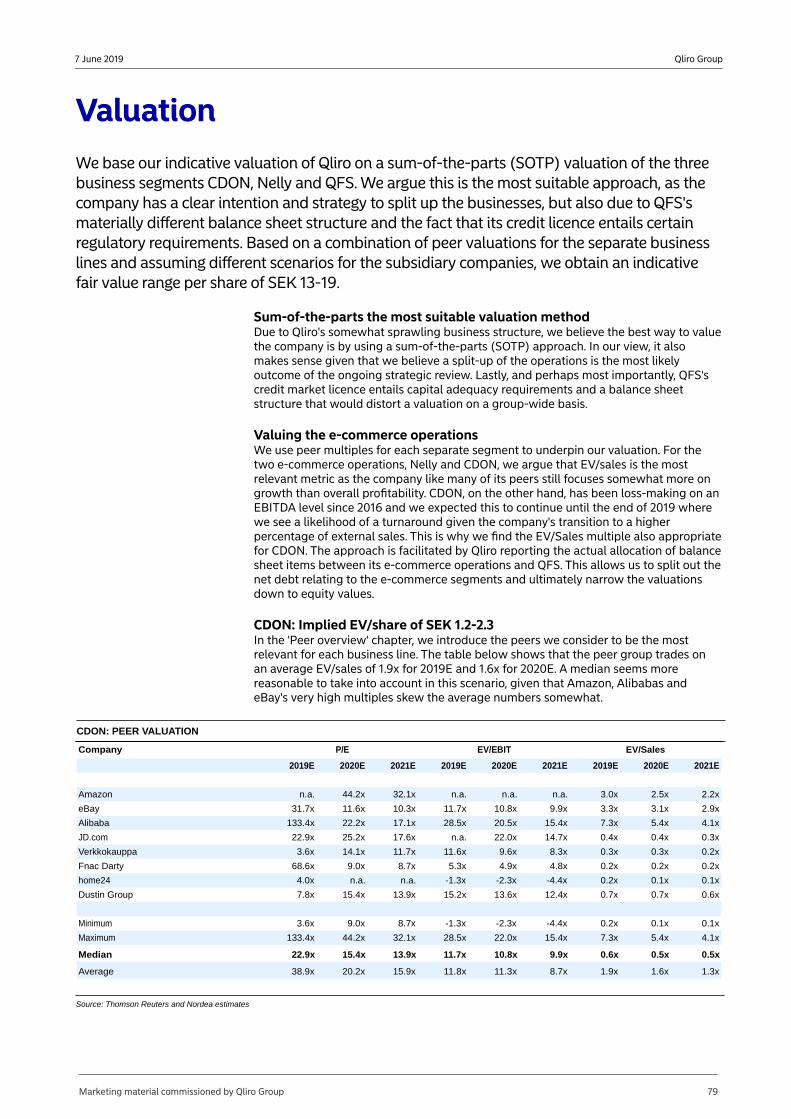

ValuationWe base our indicative valuation of Qliro on a sum-of-the-parts (SOTP) valuation of the three business segments CDON, Nelly and QFS. We find this the most suitable approach, not only because Qliro has a clear intention and strategy to split up the businesses, but also because QFS has a materially different balance sheet structure and its credit licence entails certain regulatory requirements. Based on a combination of peer valuations for the separate business lines and assuming different scenarios for the subsidiary companies, we derive an indicative fair value range of SEK 13-19 per share.

LOWER-RANGE CASE: SOTP

SOTP, SEKmRevenue

2019EEBITDA 2019E EBIT 2019E Multiple Comment Multiples Implied EV Per share

CDON 1,147 8 -4 EV/Sales Min of E-commerce peers & in line with Home24 0.2x 180.6 1.2Nelly 1,505 71 52 EV/Sales Min of Apparel Retail Peers 1.0x 1543.4 10.3Group costs -40 -40 EV/EBIT Average Consumer Goods Sector 15.0x -600 -4.0Total EV for E-commerce 2,652 39 8 1124.0 7.5

Net cash in E-commerce 223 1.5QFS 384 91 45 PE Min of Consumer Banks Peers 6.0x 543.9 3.6SOTP equity value 1,891 12.6SOTP equity value, per share 12.6

Source: Company data and Nordea estimates

HIGHER-RANGE CASE: SOTP

SOTP, SEKmRevenue

2019EEBITDA 2019E EBIT 2019E Multiple Comment Multiples Implied EV Per share

CDON 1,147 8 -4 EV/Sales In line with Fnac Darty 0.3x 335.7 2.2Nelly 1,505 71 52 EV/Sales Median of Apparel Retail Peers 1.4x 2061.5 13.8Group costs -40 -40 EV/EBIT Average Consumer Goods Sector 15.0x -600 -4.0Total EV for E-commerce 2,652 39 8 1797.2 12.0

Net cash in E-commerce 223 1.5QFS 384 91 45 PE Max of Consumer Banks Peers 9.6x 876.0 5.9SOTP equity value 2,896 19.3SOTP equity value, per share 19.3

Source: Company data and Nordea estimates

Marketing material commissioned by Qliro Group 12

Qliro Group7 June 2019

RisksWe outline various risks that Qliro Group may face that could impact its future financial performance. We look at each company in the group individually, as Qliro Group's companies operate in different industries, each with their own specific risks.

CDON

The competitive landscape could become fiercer with the entry of new participants such as Amazon.The structural growth in e-commerce could prove more temporary than currently expected by the market. Inventory levels might become elevated if consumer preferences and demand shift, making the products less attractive.Investments in improving logistics might be required to keep up with consumer demand and preferences.

Nelly

New collections could be poorly received by consumers, leading to markdowns and inflated inventory levels.Salary inflation could put pressure on COGS and gross margins as products are sourced from low-wage countries.Increased competition could lead to pressured gross margins.Failure to attract and detect upcoming influencers in social media could hurt Nelly's ability to reach new generations of its target group.

QFS

The majority of volumes processed by QFS are still generated from group internal merchants. On a standalone basis, QFS could face challenges growing.Pricing power is low in the checkout process, as competition is high, while the product is quite standardised.New regulation on consumer finance could limit QFS's growth if it constrains access to credit.Capital adequacy requirements could rise as a result of regulatory decisions.

Marketing material commissioned by Qliro Group 13

Qliro Group7 June 2019

Company overviewFounded in 1999 as CDON Group, the company changed its name to Qliro Group in 2015. Qliro Group now operates an e-commerce platform primarily within Sweden, Denmark, Norway and Finland through three business segments: CDON Marketplace, Nelly and Qliro Financial Services. The company has recently narrowed its strategic focus and sold off its less fruitful business units. Qliro aims to make all three companies independent: CDON.COM aims to become the leading Nordic online marketplace, Nelly plans to strengthen its online fashion niche and Qliro Financial Services will further develop its financial services offering.

Qliro GroupQliro Group's renewed strategy focuses on its three pillar companies: Qliro Financial Services, Nelly and CDON.com

Qliro Group, the group that holds the marketplace CDON.COM, the online clothing company Nelly and the payment solution company Qliro Financial Services, is headquartered in Stockholm, Sweden and also holds offices in Malmö and Borås. The company employs a total of 691 people across all of its business areas and around the country. In 2018, the group posted SEK 3.2bn in net sales, received SEK 6.3m in orders, generated 212 million site visits, and served approximately three million customers across the Nordic region.

Company historyCDON.com, which was launched in 1999 as a Nordic e-commerce site, laid the foundations for the Qliro Group as it is today. A portfolio of companies was built by acquiring various online merchants. In 2004, Nelly was launched and then subsequently acquired by the group in 2007. NLY Man was introduced as a fashion e-tailer for men in 2014. During the same year, the company also created Qliro Financial Services (QFS), which now offers financial services to e-merchants and consumers throughout the Nordic region. In 2015, the firm changed its name from CDON Group to the Qliro Group. In January 2017, a new strategy focusing on Qliro Financial Services, Nelly and CDON Marketplace was introduced. Following this strategic change, Lekmer, Members.com, and Health and Sports Nutrition Group were all sold. In 2018 the company decided that the three remaining companies (QFS, Nelly and CDON) should be led separately and the plan is for them to be operationally independent by the second half of 2019.

QLIRO GROUP: KEY HISTORICAL EVENTS

Year Event

1999 CDON.COM was launched

2004 Nelly was launched

2007 Nelly was acquired by group

2010 CDON Group demerged from MTG and distributed via stock dividend to shareholders

2010 CDON Group listed on the Stockholm Stock Exchange

2013 New share issue

2013 External merchants are able to sell goods on CDON.COM

2014 New share issue

2014 Qliro Financial Services was established

2014 NLY Man was introduced

2015 Firm changes name from CDON Group to Qliro Group

2017 Three year senior unsecured bond issue takes place

2017 Qliro Financial Services became a credit market company under the supervision of the Swedish FSA

2017 Savings accounts and personal loans were launched in Sweden

2017 Full payment service launched in Norway

2018 New group strategy which focuses on separating QFS, Nelly and CDON into independent companies

Source: Company data and Nordea estimates

Marketing material commissioned by Qliro Group 14

Qliro Group7 June 2019

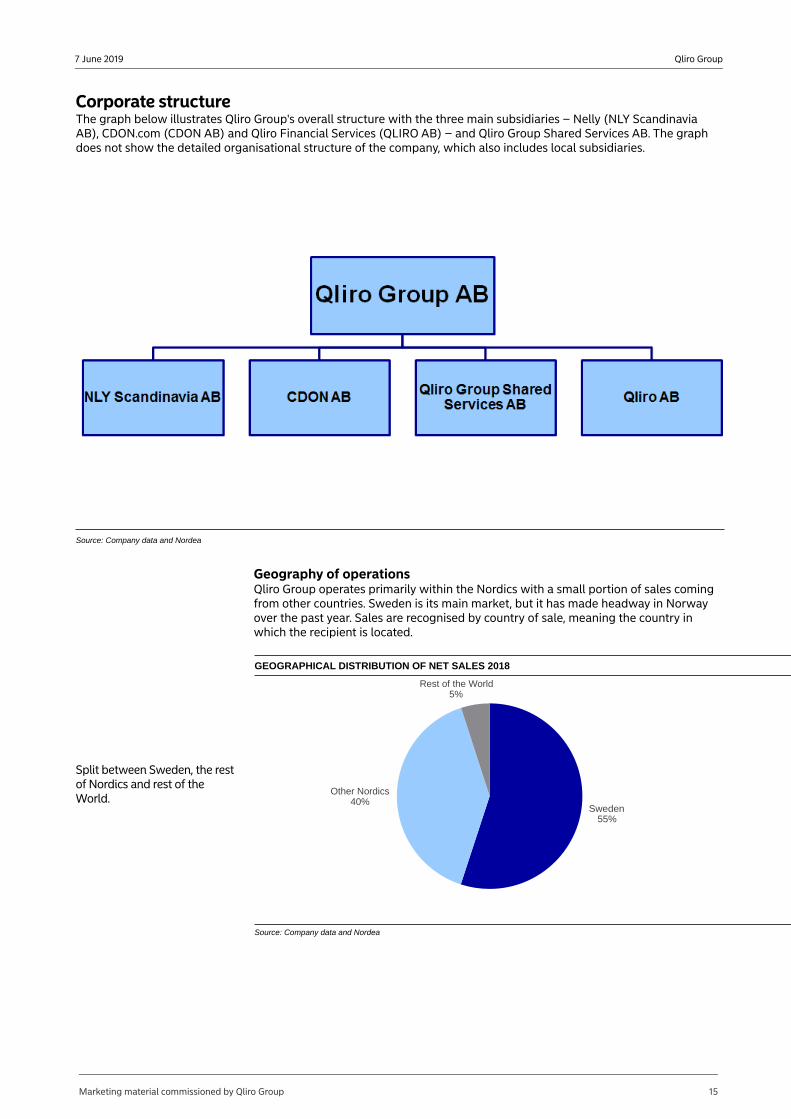

Corporate structureThe graph below illustrates Qliro Group's overall structure with the three main subsidiaries – Nelly (NLY Scandinavia AB), CDON.com (CDON AB) and Qliro Financial Services (QLIRO AB) – and Qliro Group Shared Services AB. The graph does not show the detailed organisational structure of the company, which also includes local subsidiaries.

Source: Company data and Nordea

Geography of operationsQliro Group operates primarily within the Nordics with a small portion of sales coming from other countries. Sweden is its main market, but it has made headway in Norway over the past year. Sales are recognised by country of sale, meaning the country in which the recipient is located.

GEOGRAPHICAL DISTRIBUTION OF NET SALES 2018

Split between Sweden, the rest of Nordics and rest of the World.

Sweden55%

Other Nordics40%

Rest of the World5%

Source: Company data and Nordea

Marketing material commissioned by Qliro Group 15

Qliro Group7 June 2019

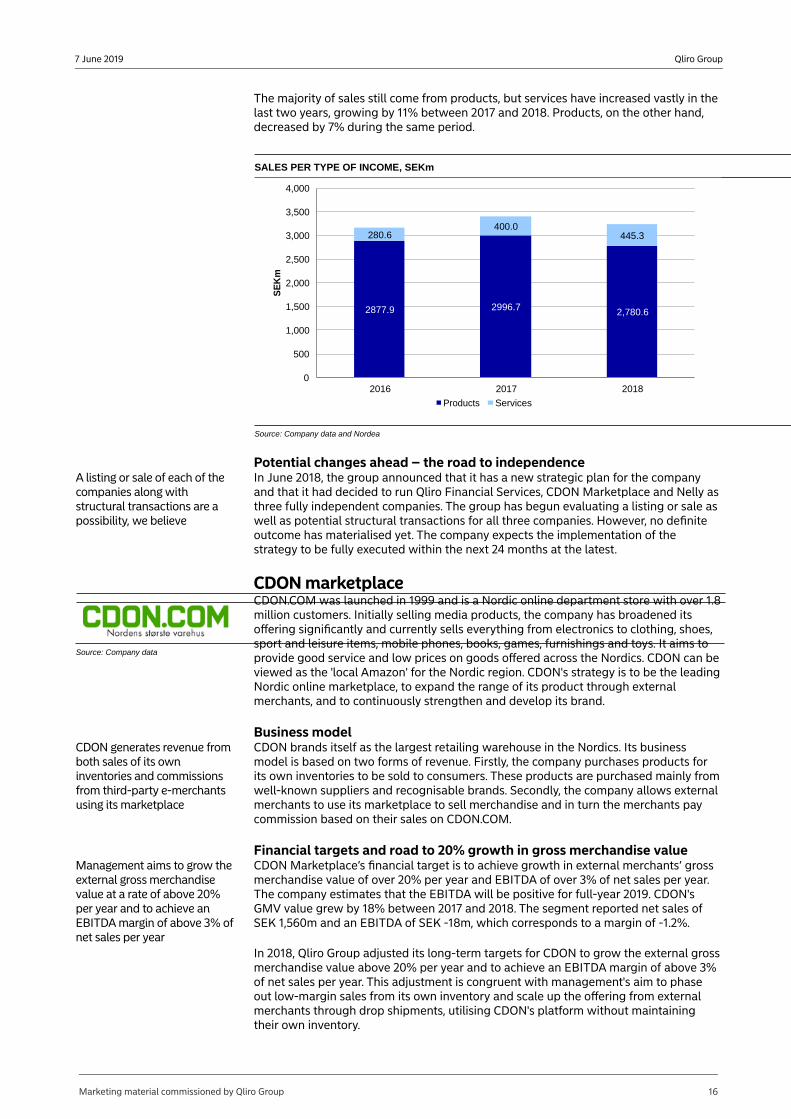

The majority of sales still come from products, but services have increased vastly in the last two years, growing by 11% between 2017 and 2018. Products, on the other hand, decreased by 7% during the same period.

SALES PER TYPE OF INCOME, SEKm

2877.9 2996.7 2,780.6

280.6400.0

445.3

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2016 2017 2018

SE

Km

Products Services

Source: Company data and Nordea

Potential changes ahead – the road to independenceA listing or sale of each of the companies along with structural transactions are a possibility, we believe

In June 2018, the group announced that it has a new strategic plan for the company and that it had decided to run Qliro Financial Services, CDON Marketplace and Nelly as three fully independent companies. The group has begun evaluating a listing or sale as well as potential structural transactions for all three companies. However, no definite outcome has materialised yet. The company expects the implementation of the strategy to be fully executed within the next 24 months at the latest.

CDON marketplace

Source: Company data

CDON.COM was launched in 1999 and is a Nordic online department store with over 1.8 million customers. Initially selling media products, the company has broadened its offering significantly and currently sells everything from electronics to clothing, shoes, sport and leisure items, mobile phones, books, games, furnishings and toys. It aims to provide good service and low prices on goods offered across the Nordics. CDON can be viewed as the 'local Amazon' for the Nordic region. CDON's strategy is to be the leading Nordic online marketplace, to expand the range of its product through external merchants, and to continuously strengthen and develop its brand.

Business modelCDON generates revenue from both sales of its own inventories and commissions from third-party e-merchants using its marketplace

CDON brands itself as the largest retailing warehouse in the Nordics. Its business model is based on two forms of revenue. Firstly, the company purchases products for its own inventories to be sold to consumers. These products are purchased mainly from well-known suppliers and recognisable brands. Secondly, the company allows external merchants to use its marketplace to sell merchandise and in turn the merchants pay commission based on their sales on CDON.COM.

Financial targets and road to 20% growth in gross merchandise valueManagement aims to grow the external gross merchandise value at a rate of above 20% per year and to achieve an EBITDA margin of above 3% of net sales per year

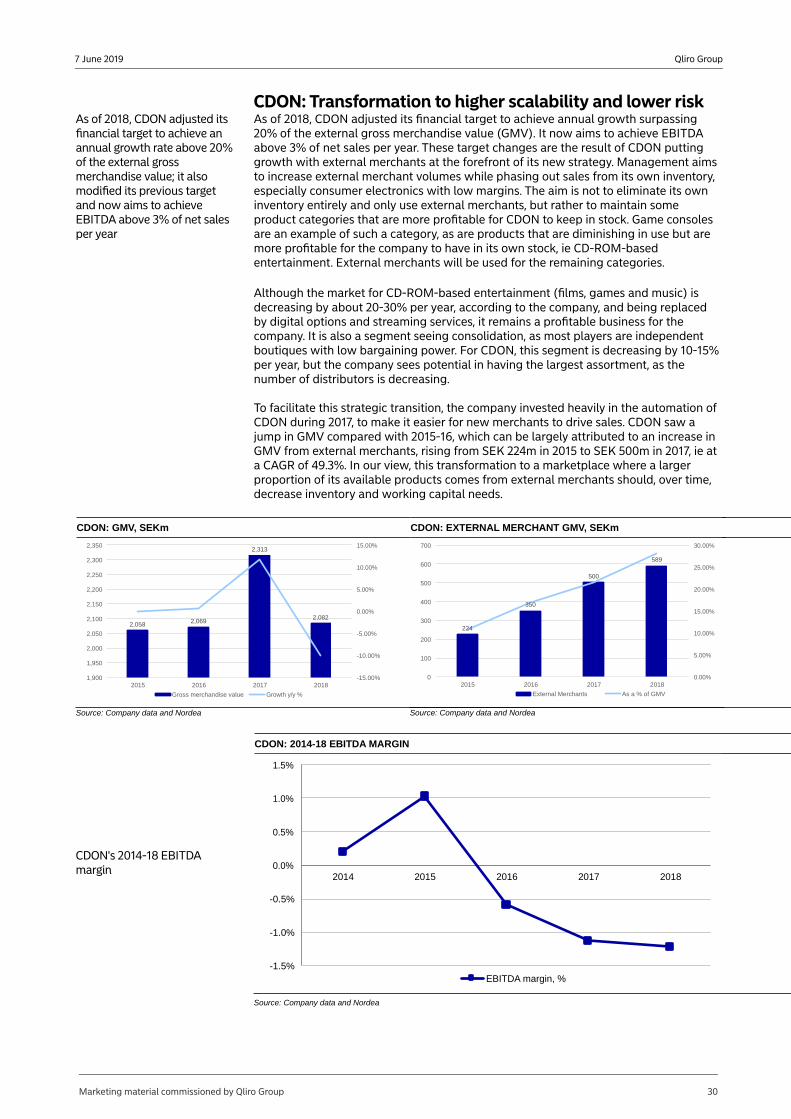

CDON Marketplace’s financial target is to achieve growth in external merchants’ gross merchandise value of over 20% per year and EBITDA of over 3% of net sales per year. The company estimates that the EBITDA will be positive for full-year 2019. CDON's GMV value grew by 18% between 2017 and 2018. The segment reported net sales of SEK 1,560m and an EBITDA of SEK -18m, which corresponds to a margin of -1.2%.

In 2018, Qliro Group adjusted its long-term targets for CDON to grow the external gross merchandise value above 20% per year and to achieve an EBITDA margin of above 3% of net sales per year. This adjustment is congruent with management's aim to phase out low-margin sales from its own inventory and scale up the offering from external merchants through drop shipments, utilising CDON's platform without maintaining their own inventory.

Marketing material commissioned by Qliro Group 16

Qliro Group7 June 2019

The company does not intend to eliminate its own inventory entirely, however, as some product categories are more profitable for the company to keep in stock, eg CD-ROM based entertainment or game consoles. While the CD-ROM based entertainment (films, games and music) market is decreasing at about 20-30% a year – largely being replaced by digital/streaming options – it is still a profitable business for the company. It is also a segment that is in consolidation mode, as most players are independent boutiques with low bargaining power. For CDON, this segment is decreasing by 10-15% per year but the company sees potential from having the largest assortment, as the number of distributors in the market is decreasing.

NellyNelly and NLY Man offer proprietary clothing lines along with selected external brands to supplement their offerings

Nelly offers fashion and beauty products for young women through Nelly.com and for men through NLY Man. The company offers its own brand, NLY, along with more than 200 other brands in its online store. It has strong brand recognition in the Nordics and leverages social media to target its main customer segment, 16-26 year old women.

Business model

Source: Company data

Nelly's business model relies on a core base of its own labels and designs, supplemented by a range of ~200 external brands. The clothing and accessories are purchased from manufacturers in China, the UK, Turkey and other countries, then sold primarily in the Nordics. Nelly's largest markets are Sweden and Norway, but outside the Nordics it is currently experiencing the fastest growth in the Netherlands. In 2018, Nelly's own brands accounted for 45% of sales, which was up from 43% in 2017. The inventory of products is transported and stored at the company's logistics centre in Falkenberg, Sweden, where the items are digitally marketed and subsequently sold at Nelly.com and NLYman.com

Management's financial targets and future focusManagement targets an organic annual growth rate of 10% and an EBITDA margin of at least 6%

Management's long-term target for Nelly is to achieve an organic growth rate of 10% per year for net sales. This target was increased from 8% as Nelly has a strong market position and so far successful growth strategy. Management aims to further strengthen the company's own brands and solidify its position through digital marketing and sales. It believes investments in brands, variety and logistics have created the right conditions for profitable growth. During 2018 the company reached sales growth of 6%, which amounted to sales of SEK 1,391m and EBITDA of SEK 56,8m, corresponding to a margin of 3%.

Qliro Financial Services (QFS)Loan book of SEK 1.5bn and ~5.1 million orders processed in 2018

Source: Company data

QFS provides financial services to merchants and consumers. The company leverages its e-commerce marketplace to offer credit and financing to its consumers but with time the company has also started to offer its services to external merchants. Consumers are offered several services, primarily safe payment options along with savings and borrowing opportunities. Merchants are offered a checkout solution with the most common forms of payment such as credit card, direct debit from Nordic banks, partial payment and invoices. QFS consists of the subsidiary Qliro AB, which became a credit market company under the supervision of the Swedish Financial Supervisory Authority in March 2017. QFS posted SEK 298m in operating income for 2018, increased its loan book by 45% to SEK 1.5bn, and processed ~5.1 million orders.

Business modelQFS's business model is based on offering a payment solution to e-merchants and benefiting from their transactions. Some of these transactions lead to partial and instalment payments, which add to a loan book that generates interest income for the company. Since the company's inception, more than 11.4 million transactions have been executed and SEK 10bn has been lent. The loan book is the main driver of revenue and profit. Credit from the partial and instalment payments can generate revenue for up to three years. This interest income earned is shared with the e-merchants.

Marketing material commissioned by Qliro Group 17

Qliro Group7 June 2019

QFS earns interest income on its loan book made up of primarily credit from partial and instalment payments

The company benefits from e-merchant volumes and has low customer acquisition costs due to the integrated nature of the online purchases and the offering of financing to the consumer. External merchants account for more than 40% of e-commerce volumes, with the remaining portion of 60% coming from CDON and Nelly in equal parts. In addition to payment credit, the company offers longer-term personal loans and savings accounts to consumers in the Swedish market. The company conducts data-driven credit testing when evaluating customers' creditworthiness and their potential to repay.

The company has largely launched its personal loan offering by targeting existing customers through its own channels, primarily via its mobile app, website and targeted email campaigns towards customers with which it already has a relationship. Over 95% of personal loan borrowers have had a previous relationship with QFS. The company conducts the credit scoring in an automated way, building on both internal and external data that is analysed in real time.

Management's financial targets and future focusManagement aims to achieve EBITDA of SEK 100-125m in 2019

In 2018, management set a new target for QFS – to achieve operating income before depreciation, amortisation and impairments of SEK 100-125m in 2019 (from previously higher target of SEK 150m). This target reduction is largely based on the management's belief that volumes will be negatively affected by the CDON Marketplace's transition, where it is phasing out sales from its own inventories and boosting sales from external merchants. QFS's operating income before depreciation, amortisation and impairments in 2018 amounted to SEK -15.4m.

QFS seeks to further develop products to broaden and strengthen its offering to consumers and e-merchants. For example, savings accounts and personal loans are currently only offered in Sweden, but management is entertaining rolling out this offering to all Nordic countries. Given the current product offering, the company believes it is large enough to handle considerable growth in the loan book without having to significantly increase its number of employees, which could create some economies of scale.

Marketing material commissioned by Qliro Group 18

Qliro Group7 June 2019

Executive managementThe structure of Qliro Group’s management was changed in 2018 following the company's new strategy to separate the three companies. For this to be achieved Qliro Group has appointed a CEO for each respective company. During 2018, Anna Ullman Sersé was appointed head of Nelly, and Carolina Brandtman was appointed head of Qliro Financial Services. Most recently, Kristoffer Väliharju was appointed CEO of CDON. The current team in place has significant experience in the e-commerce and financial services space.

Source: Company data

CEO and President: Marcus Lindqvist

Qliro Group experience: Took over as president and CEO in August 2016Born: 1970Background: Most recently, head of B2B Sweden & Products at Dustin. Formerly held senior management positions at Hewlett Packard and Dell in the Nordics.Education: Associate degree from FEI in StockholmEquity stake: 466,979 shares

Source: Company data

CFO: Mathias Pedersen

Qliro Group experience: Appointed CFO of Qliro Group in August 2016Born: 1971Background: Most recently, investment director at Kinnevik AB. Formerly held CFO positions at East Capital Group, East Capital Explorer and ETAC.Education: Holds a Master’s degree from the Stockholm School of Economics and completed the Program for Management Development at Harvard Business School.Equity stake: 240,000 shares

Source: Company data

CEO of CDON: Kristoffer Väliharju

Qliro Group experience: Appointed head of CDON in September 2018. Formerly COO and member of the CDON executive team.Born: 1975Background: Has previous leadership experience at Dustin as a sales manager and at Dell as a sales distribution manager in the Nordic region.Equity stake: 12,240 shares

Source: Company data

CEO of Qliro Financial Services: Carolina Brandtman

Qliro Group experience: Joined as CEO of Qliro Financial Services in December 2018.Born: 1975Background: Most recently, managing director at Santander Consumer Bank after it acquired GE Money, where she held various positions, the last one as chief risk officer.Education: Degree from University of Örebro and Central Queensland UniversityEquity stake: 11,415 shares

Source: Company data

CEO of Nelly: Anna Ullman Sersé

Qliro Group experience: Joined the group as head of business development in December 2016 and was appointed interim head of Nelly in April 2018Born: 1973Background: Most recently, Nordic lead for retail and marketing & content at Accenture InteractiveEducation: MSc in Law and Business Administration from Stockholm UniversityEquity stake: 34,944 shares

Marketing material commissioned by Qliro Group 19

Qliro Group7 June 2019

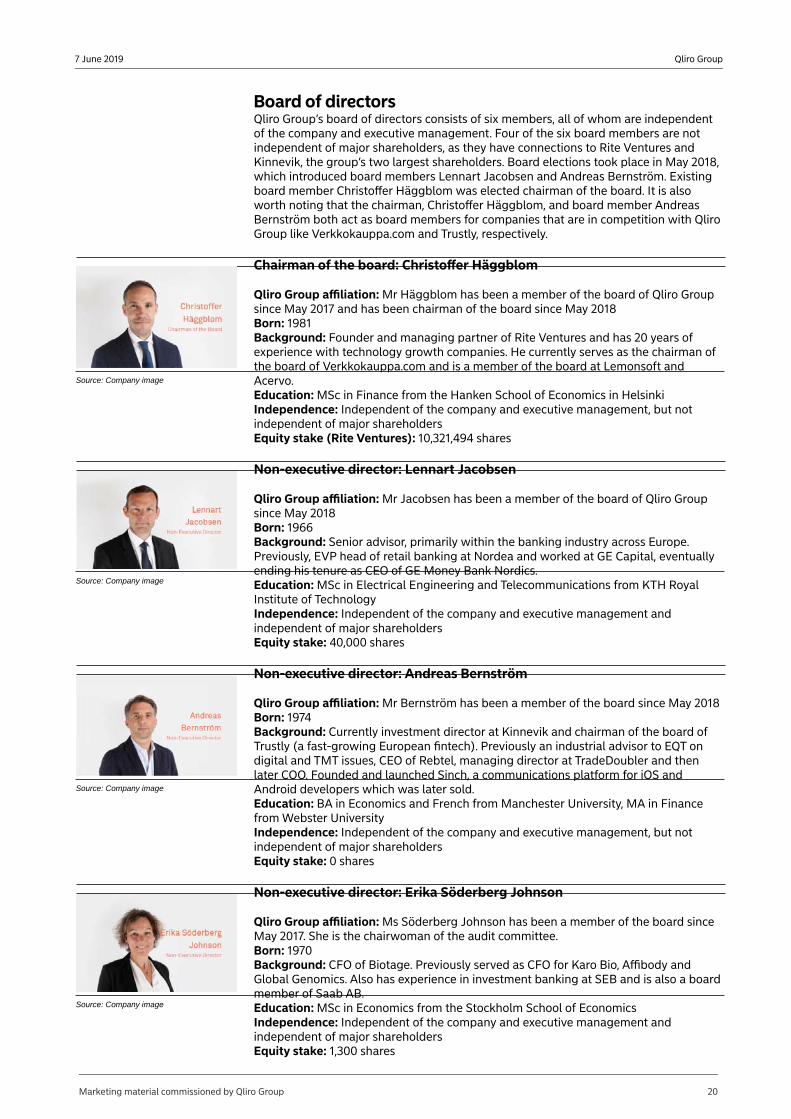

Board of directorsQliro Group’s board of directors consists of six members, all of whom are independent of the company and executive management. Four of the six board members are not independent of major shareholders, as they have connections to Rite Ventures and Kinnevik, the group’s two largest shareholders. Board elections took place in May 2018, which introduced board members Lennart Jacobsen and Andreas Bernström. Existing board member Christoffer Häggblom was elected chairman of the board. It is also worth noting that the chairman, Christoffer Häggblom, and board member Andreas Bernström both act as board members for companies that are in competition with Qliro Group like Verkkokauppa.com and Trustly, respectively.

Source: Company image

Chairman of the board: Christoffer Häggblom

Qliro Group affiliation: Mr Häggblom has been a member of the board of Qliro Group since May 2017 and has been chairman of the board since May 2018Born: 1981Background: Founder and managing partner of Rite Ventures and has 20 years of experience with technology growth companies. He currently serves as the chairman of the board of Verkkokauppa.com and is a member of the board at Lemonsoft and Acervo.Education: MSc in Finance from the Hanken School of Economics in HelsinkiIndependence: Independent of the company and executive management, but not independent of major shareholdersEquity stake (Rite Ventures): 10,321,494 shares

Source: Company image

Non-executive director: Lennart Jacobsen

Qliro Group affiliation: Mr Jacobsen has been a member of the board of Qliro Group since May 2018Born: 1966Background: Senior advisor, primarily within the banking industry across Europe. Previously, EVP head of retail banking at Nordea and worked at GE Capital, eventually ending his tenure as CEO of GE Money Bank Nordics. Education: MSc in Electrical Engineering and Telecommunications from KTH Royal Institute of TechnologyIndependence: Independent of the company and executive management and independent of major shareholdersEquity stake: 40,000 shares

Source: Company image

Non-executive director: Andreas Bernström

Qliro Group affiliation: Mr Bernström has been a member of the board since May 2018 Born: 1974Background: Currently investment director at Kinnevik and chairman of the board of Trustly (a fast-growing European fintech). Previously an industrial advisor to EQT on digital and TMT issues, CEO of Rebtel, managing director at TradeDoubler and then later COO. Founded and launched Sinch, a communications platform for iOS and Android developers which was later sold.Education: BA in Economics and French from Manchester University, MA in Finance from Webster UniversityIndependence: Independent of the company and executive management, but not independent of major shareholdersEquity stake: 0 shares

Source: Company image

Non-executive director: Erika Söderberg Johnson

Qliro Group affiliation: Ms Söderberg Johnson has been a member of the board since May 2017. She is the chairwoman of the audit committee.Born: 1970Background: CFO of Biotage. Previously served as CFO for Karo Bio, Affibody and Global Genomics. Also has experience in investment banking at SEB and is also a board member of Saab AB.Education: MSc in Economics from the Stockholm School of EconomicsIndependence: Independent of the company and executive management and independent of major shareholdersEquity stake: 1,300 shares

Marketing material commissioned by Qliro Group 20

Qliro Group7 June 2019

Source: Company image

Non-executive director: Jessica Pedroni Thorell

Qliro Group affiliation: Ms Pedroni Thorell has been a member of the board since May 2017. She is a member of the remuneration committee and the audit committee.Born: 1983Background: Investment Manager at Kinnevik. Previously served as a senior associate at an equity investment firm, General Atlantic, and worked on Goldman Sachs’ Nordic investment banking desk.Education: MSc in Economics and Business Administration from the Stockholm School of Economics, CEMS Master in International Management from University of St GallenIndependence: Independent of the company and executive management, not independent of major shareholdersEquity stake: 0 shares

Source: Company image

Non-executive director: Daniel Mytnik

Qliro Group affiliation: Mr Mytnik has been a member of the board since May 2014. He is a member of the audit committee and chairman of the remuneration committee.Born: 1971Background: Co-founder and managing partner of private equity firm Ventiga Capital Partners. Previously served as partner at Palamon Capital Partners, as managing director at investment bank Altium Capital, and worked in Morgan Stanley’s Private Equity and Investment Banking department.Education: BA in Philosophy, Politics and Economics and an MPhil in Economics from Oxford UniversityIndependence: Independent of the company and executive management, not independent of major shareholdersEquity stake: 131,513 shares

Subsidiary boards:

Governance was strengthened in Qliro Group with subsidiary boards

As a part of Qliro Group’s revised strategic direction to run Qliro Financial Services, CDON Marketplace and Nelly as three completely independent companies, corporate governance was strengthened in Qliro Group’s subsidiaries. From the second half of 2018, Nelly and CDON Marketplace have held regular board meetings. The board of Qliro Financial Services has held regular board meetings since 2014. All subsidiaries have separate boards with representatives from the parent company’s board and management as well as external board members for Qliro Financial Services and Nelly. This means that the subsidiaries are run independently of each other and that group management focuses on making the companies independent and ready for listing, as well as evaluating potential strategic transactions. As of 31 December 2018, the subsidiary boards had the following composition:

Qliro Financial Services:

Lennart Jacobsen (chairman, also board member of Qliro Group) Andreas Bernström (also a board member of Qliro Group)Marcus Lindqvist (also CEO of Qliro Group)Robert Burén (external member)Lennart Francke (external member)Helena Nelson (external member)Johan Wigh (external member)

Marketing material commissioned by Qliro Group 21

Qliro Group7 June 2019

Nelly:

Marcus Lindqvist (chairman, also CEO of Qliro Group)Christoffer Häggblom (also board chairman of Qliro Group)Jessica Pedroni Thorell (also board member of Qliro Group)Mathias Pedersen (also CFO of Qliro Group)Louise Nylén (external member)Maj-La Pizzelli (externalmember)

CDON Marketplace:

Marcus Lindqvist (chairman, also CEO of Qliro Group)Christoffer Häggblom (alsoboard chairman of Qliro Group)Andreas Bernström (alsoboard member of Qliro Group)Mathias Pedersen (also CFO of Qliro Group).

Marketing material commissioned by Qliro Group 22

Qliro Group7 June 2019

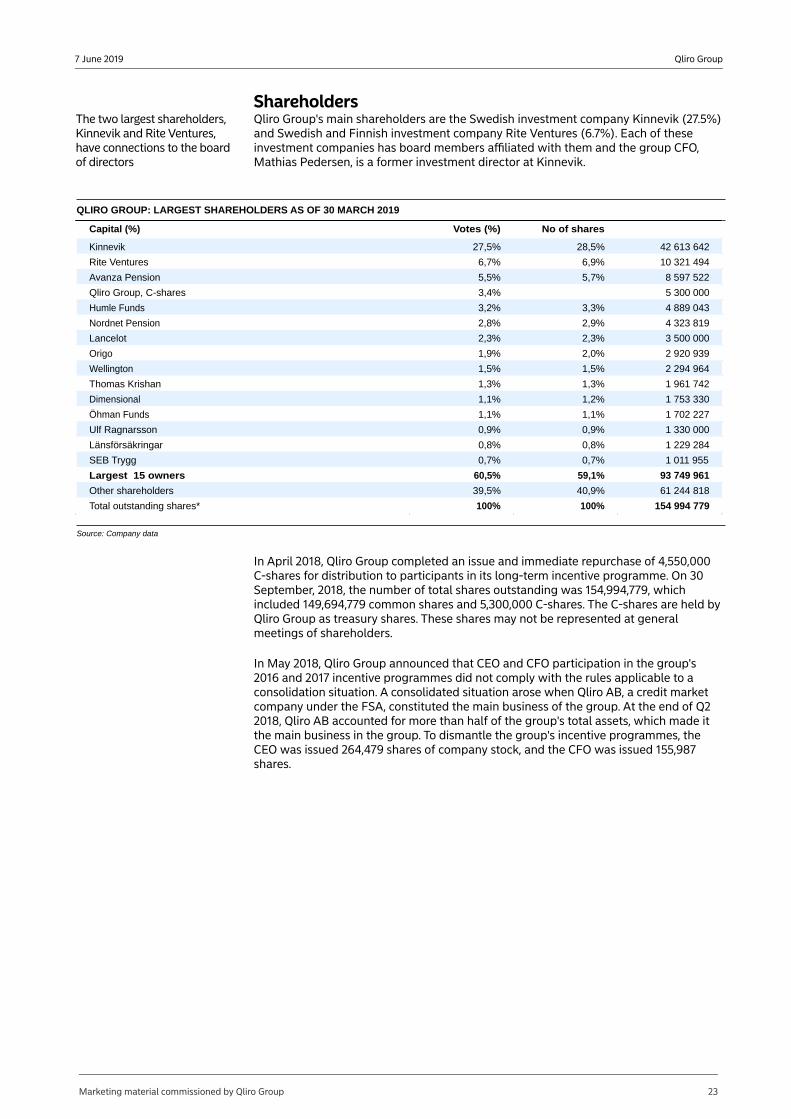

ShareholdersThe two largest shareholders, Kinnevik and Rite Ventures, have connections to the board of directors

Qliro Group's main shareholders are the Swedish investment company Kinnevik (27.5%) and Swedish and Finnish investment company Rite Ventures (6.7%). Each of these investment companies has board members affiliated with them and the group CFO, Mathias Pedersen, is a former investment director at Kinnevik.

QLIRO GROUP: LARGEST SHAREHOLDERS AS OF 30 MARCH 2019

Capital (%) Votes (%) No of shares

Kinnevik 27,5% 28,5% 42 613 642

Rite Ventures 6,7% 6,9% 10 321 494

Avanza Pension 5,5% 5,7% 8 597 522

Qliro Group, C-shares 3,4% 5 300 000

Humle Funds 3,2% 3,3% 4 889 043

Nordnet Pension 2,8% 2,9% 4 323 819

Lancelot 2,3% 2,3% 3 500 000

Origo 1,9% 2,0% 2 920 939

Wellington 1,5% 1,5% 2 294 964

Thomas Krishan 1,3% 1,3% 1 961 742

Dimensional 1,1% 1,2% 1 753 330

Öhman Funds 1,1% 1,1% 1 702 227

Ulf Ragnarsson 0,9% 0,9% 1 330 000

Länsförsäkringar 0,8% 0,8% 1 229 284

SEB Trygg 0,7% 0,7% 1 011 955

Largest 15 owners 60,5% 59,1% 93 749 961

Other shareholders 39,5% 40,9% 61 244 818

Total outstanding shares* 100% 100% 154 994 779

Source: Company data

In April 2018, Qliro Group completed an issue and immediate repurchase of 4,550,000 C-shares for distribution to participants in its long-term incentive programme. On 30 September, 2018, the number of total shares outstanding was 154,994,779, which included 149,694,779 common shares and 5,300,000 C-shares. The C-shares are held by Qliro Group as treasury shares. These shares may not be represented at general meetings of shareholders.

In May 2018, Qliro Group announced that CEO and CFO participation in the group's 2016 and 2017 incentive programmes did not comply with the rules applicable to a consolidation situation. A consolidated situation arose when Qliro AB, a credit market company under the FSA, constituted the main business of the group. At the end of Q2 2018, Qliro AB accounted for more than half of the group's total assets, which made it the main business in the group. To dismantle the group's incentive programmes, the CEO was issued 264,479 shares of company stock, and the CFO was issued 155,987 shares.

Marketing material commissioned by Qliro Group 23

Qliro Group7 June 2019

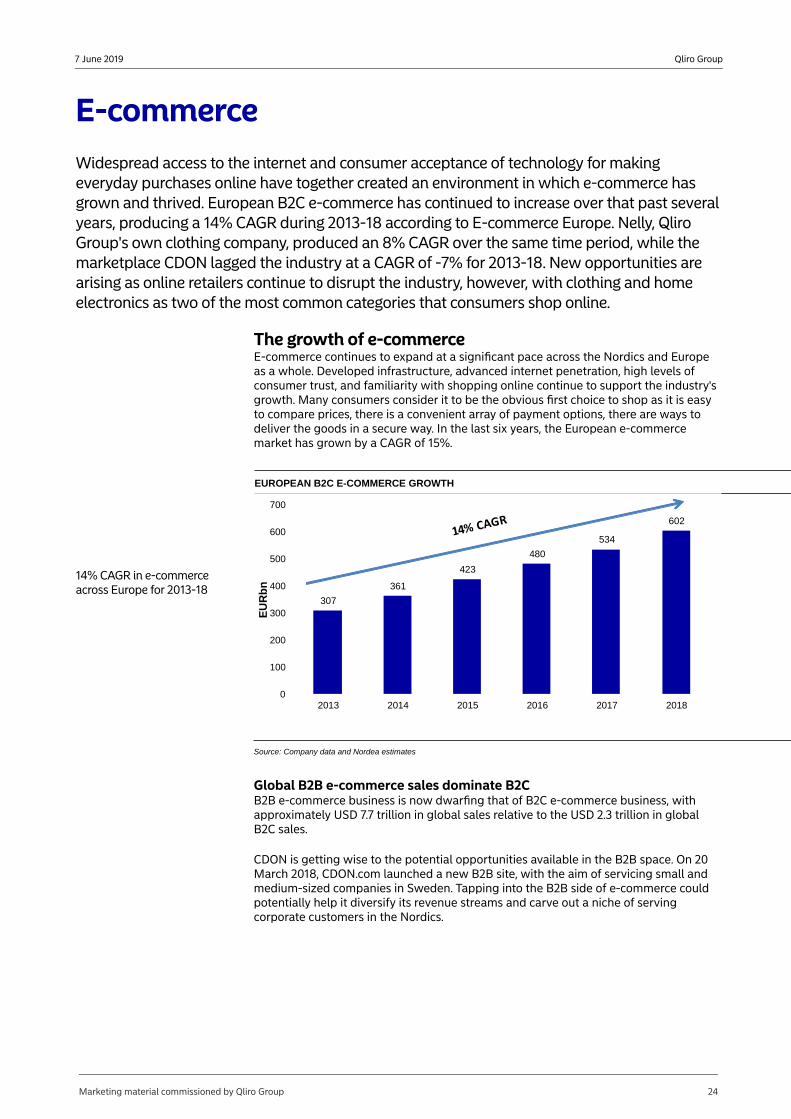

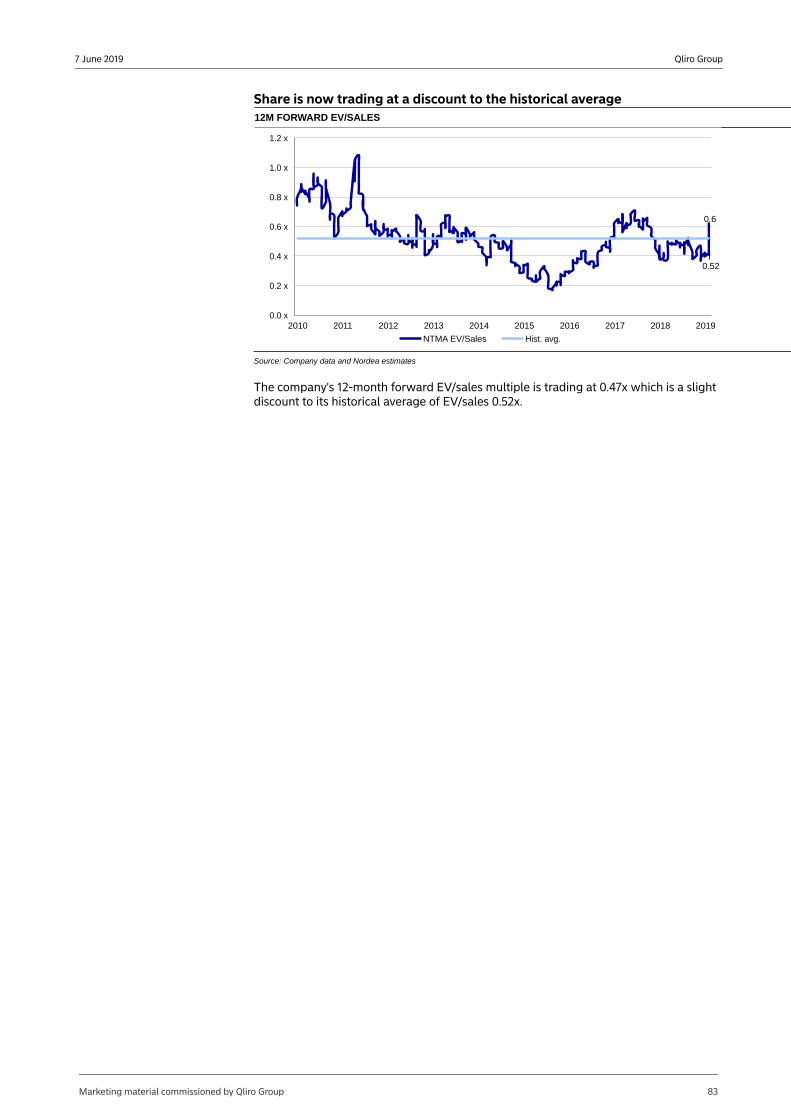

E-commerceWidespread access to the internet and consumer acceptance of technology for making everyday purchases online have together created an environment in which e-commerce has grown and thrived. European B2C e-commerce has continued to increase over that past several years, producing a 14% CAGR during 2013-18 according to E-commerce Europe. Nelly, Qliro Group's own clothing company, produced an 8% CAGR over the same time period, while the marketplace CDON lagged the industry at a CAGR of -7% for 2013-18. New opportunities are arising as online retailers continue to disrupt the industry, however, with clothing and home electronics as two of the most common categories that consumers shop online.

The growth of e-commerceE-commerce continues to expand at a significant pace across the Nordics and Europe as a whole. Developed infrastructure, advanced internet penetration, high levels of consumer trust, and familiarity with shopping online continue to support the industry's growth. Many consumers consider it to be the obvious first choice to shop as it is easy to compare prices, there is a convenient array of payment options, there are ways to deliver the goods in a secure way. In the last six years, the European e-commerce market has grown by a CAGR of 15%.

14% CAGR in e-commerce across Europe for 2013-18

EUROPEAN B2C E-COMMERCE GROWTH

307

361

423

480

534

602

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017 2018

EU

Rb

n

Source: Company data and Nordea estimates

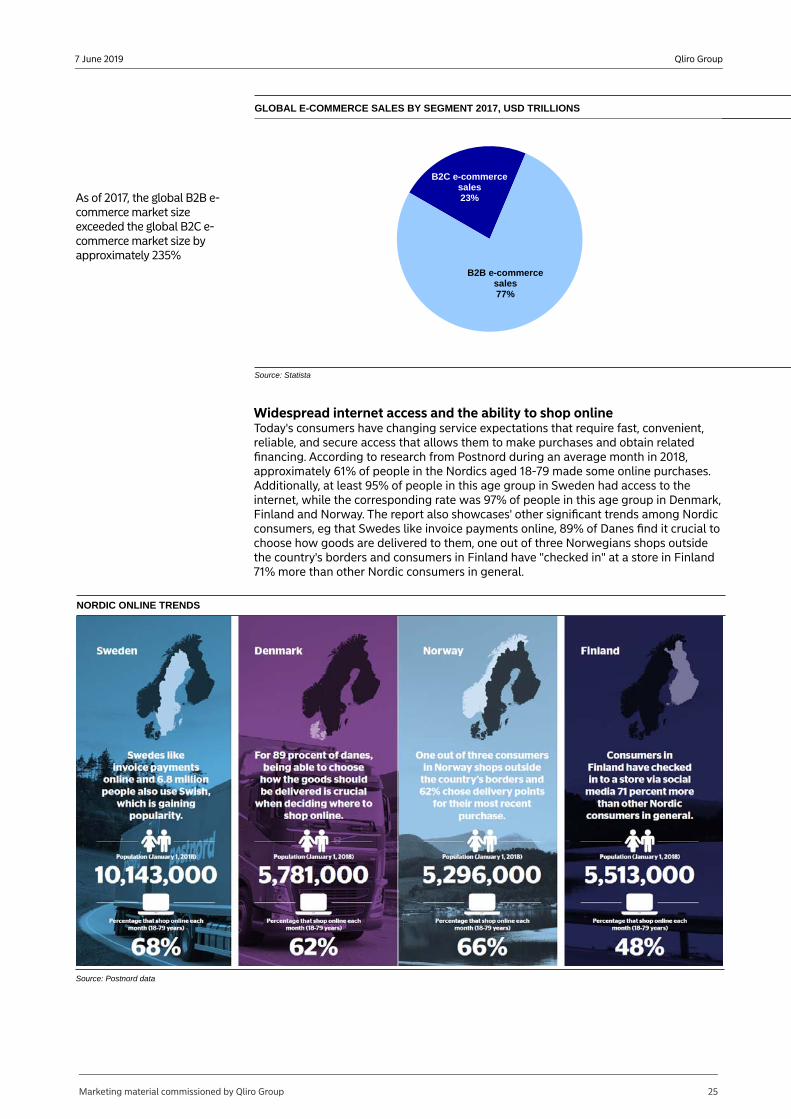

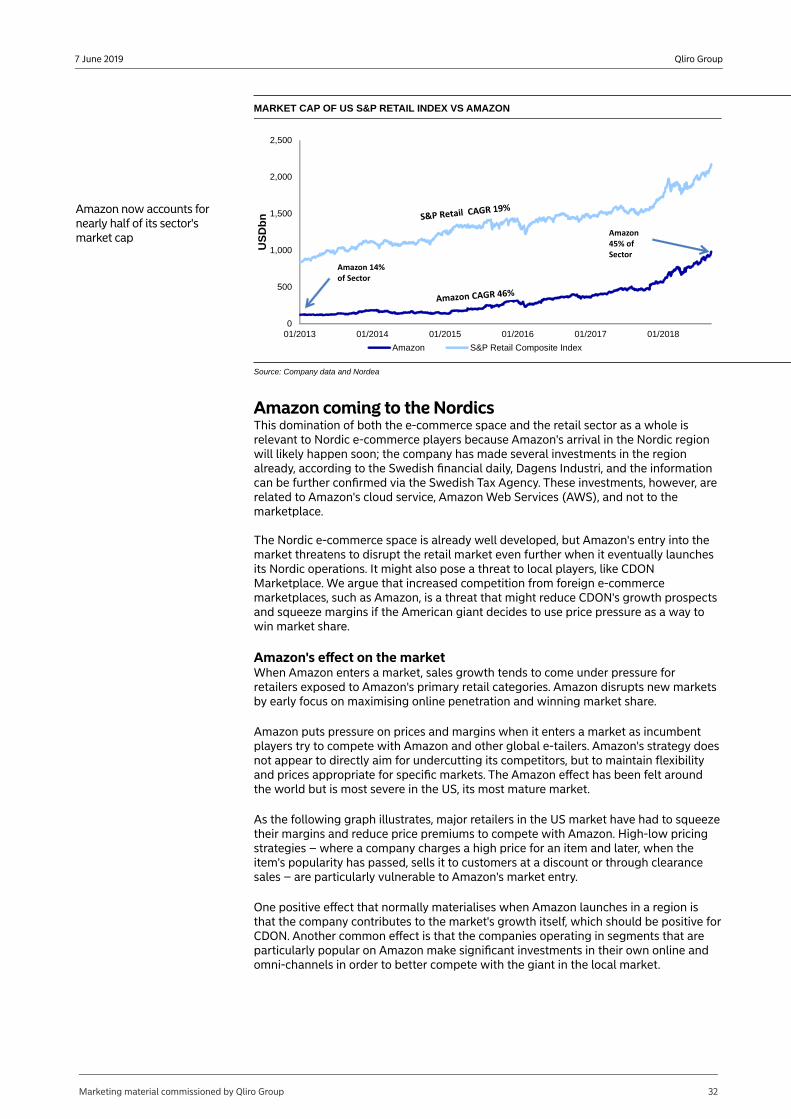

Global B2B e-commerce sales dominate B2CB2B e-commerce business is now dwarfing that of B2C e-commerce business, with approximately USD 7.7 trillion in global sales relative to the USD 2.3 trillion in global B2C sales.

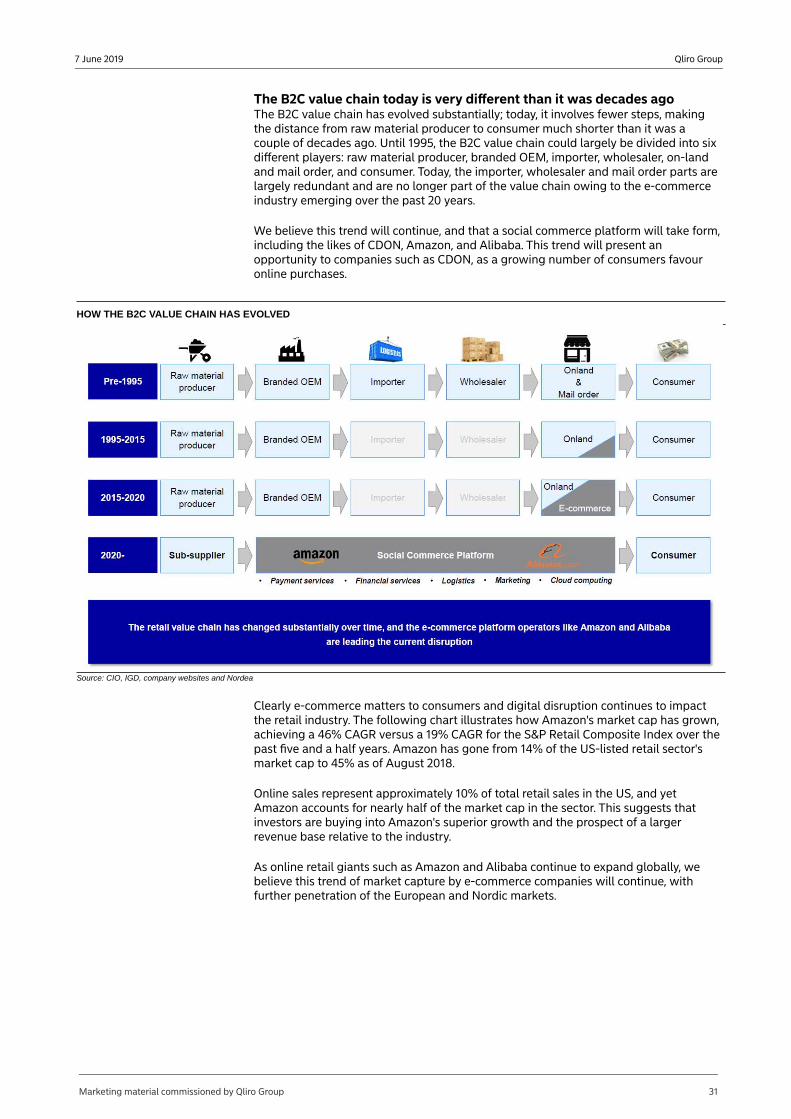

CDON is getting wise to the potential opportunities available in the B2B space. On 20 March 2018, CDON.com launched a new B2B site, with the aim of servicing small and medium-sized companies in Sweden. Tapping into the B2B side of e-commerce could potentially help it diversify its revenue streams and carve out a niche of serving corporate customers in the Nordics.

Marketing material commissioned by Qliro Group 24

Qliro Group7 June 2019

GLOBAL E-COMMERCE SALES BY SEGMENT 2017, USD TRILLIONS

As of 2017, the global B2B e-commerce market size exceeded the global B2C e-commerce market size by approximately 235%

B2C e-commerce sales23%

B2B e-commerce sales77%

Source: Statista

Widespread internet access and the ability to shop onlineToday's consumers have changing service expectations that require fast, convenient, reliable, and secure access that allows them to make purchases and obtain related financing. According to research from Postnord during an average month in 2018, approximately 61% of people in the Nordics aged 18-79 made some online purchases. Additionally, at least 95% of people in this age group in Sweden had access to the internet, while the corresponding rate was 97% of people in this age group in Denmark, Finland and Norway. The report also showcases' other significant trends among Nordic consumers, eg that Swedes like invoice payments online, 89% of Danes find it crucial to choose how goods are delivered to them, one out of three Norwegians shops outside the country's borders and consumers in Finland have "checked in" at a store in Finland 71% more than other Nordic consumers in general.

NORDIC ONLINE TRENDS

Source: Postnord data

Marketing material commissioned by Qliro Group 25

Qliro Group7 June 2019

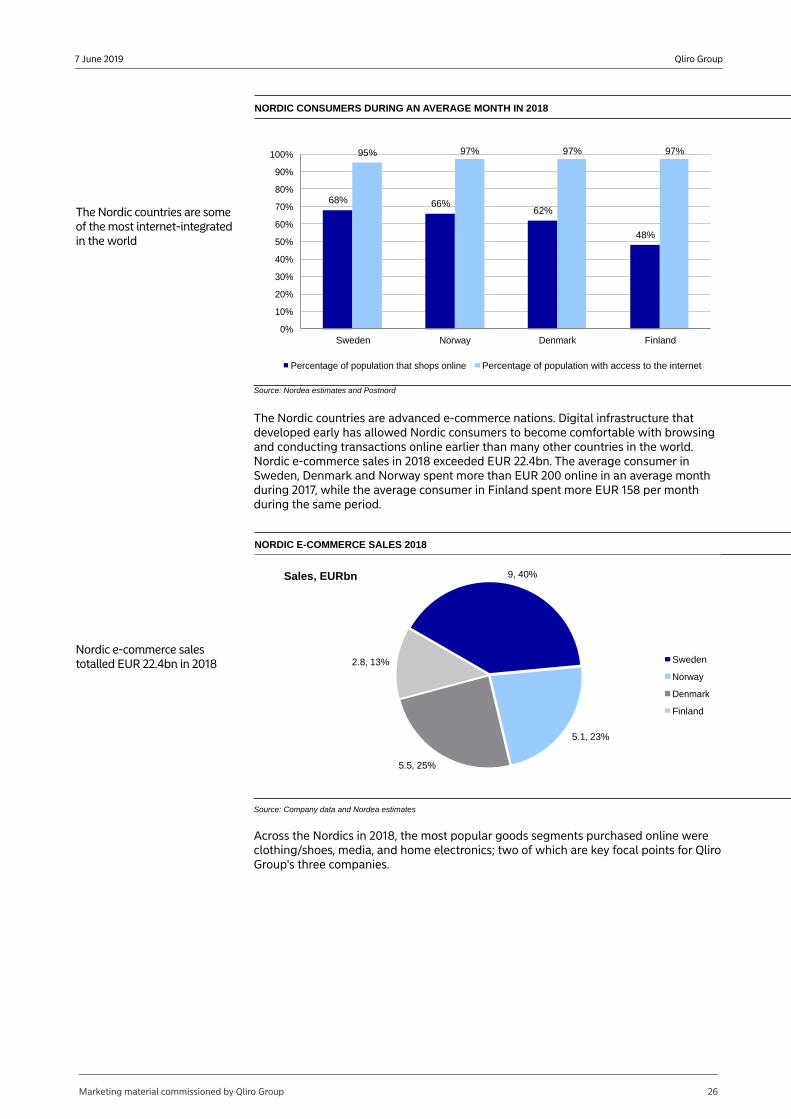

NORDIC CONSUMERS DURING AN AVERAGE MONTH IN 2018

The Nordic countries are some of the most internet-integrated in the world

68% 66%62%

48%

95% 97% 97% 97%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sweden Norway Denmark Finland

Percentage of population that shops online Percentage of population with access to the internet

Source: Nordea estimates and Postnord

The Nordic countries are advanced e-commerce nations. Digital infrastructure that developed early has allowed Nordic consumers to become comfortable with browsing and conducting transactions online earlier than many other countries in the world. Nordic e-commerce sales in 2018 exceeded EUR 22.4bn. The average consumer in Sweden, Denmark and Norway spent more than EUR 200 online in an average month during 2017, while the average consumer in Finland spent more EUR 158 per month during the same period.

Nordic e-commerce sales totalled EUR 22.4bn in 2018

NORDIC E-COMMERCE SALES 2018

9, 40%

5.1, 23%

5.5, 25%

2.8, 13%

Sales, EURbn

Sweden

Norway

Denmark

Finland

Source: Company data and Nordea estimates

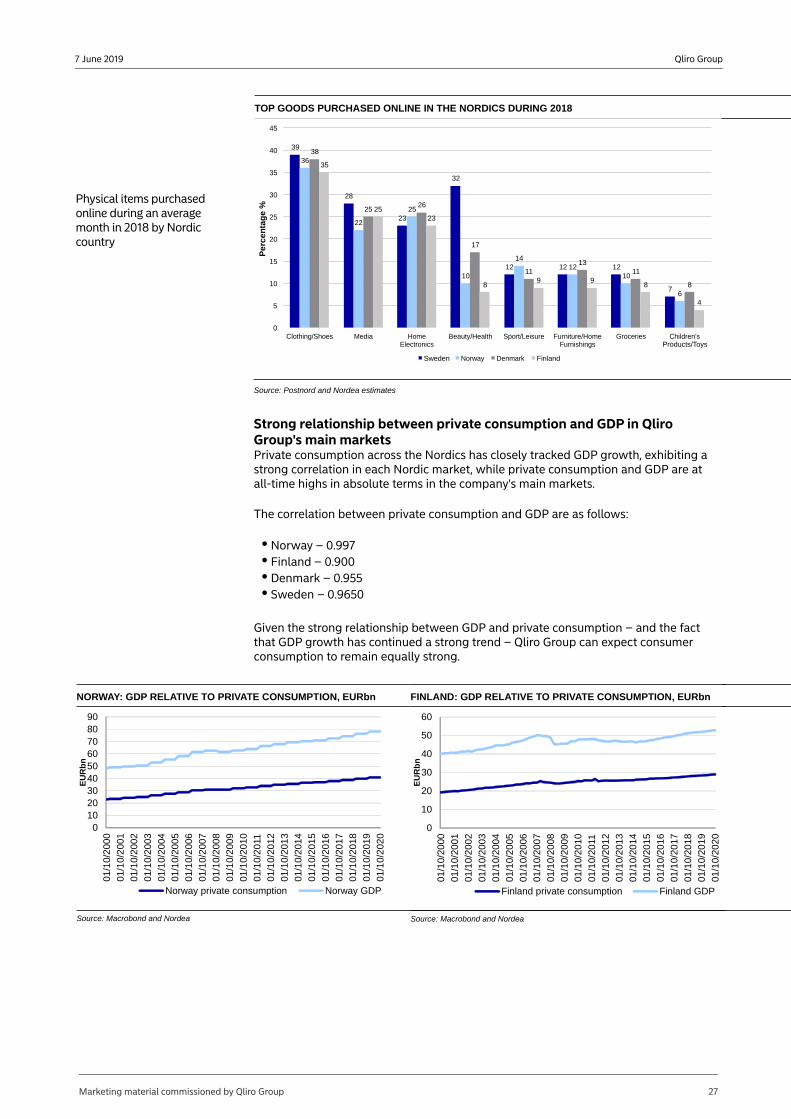

Across the Nordics in 2018, the most popular goods segments purchased online were clothing/shoes, media, and home electronics; two of which are key focal points for Qliro Group's three companies.

Marketing material commissioned by Qliro Group 26

Qliro Group7 June 2019

Physical items purchased online during an average month in 2018 by Nordic country

TOP GOODS PURCHASED ONLINE IN THE NORDICS DURING 2018

39

28

23

32

12 12 12

7

36

22

25

10

1412

10

6

38

2526

17

1113

11

8

35

2523

89 9

8

4

0

5

10

15

20

25

30

35

40

45

Clothing/Shoes Media HomeElectronics

Beauty/Health Sport/Leisure Furniture/HomeFurnishings

Groceries Children'sProducts/Toys

Pe

rce

nta

ge

%

Sweden Norway Denmark Finland

Source: Postnord and Nordea estimates

Strong relationship between private consumption and GDP in Qliro Group's main marketsPrivate consumption across the Nordics has closely tracked GDP growth, exhibiting a strong correlation in each Nordic market, while private consumption and GDP are at all-time highs in absolute terms in the company's main markets.

The correlation between private consumption and GDP are as follows:

Norway – 0.997Finland – 0.900Denmark – 0.955Sweden – 0.9650

Given the strong relationship between GDP and private consumption – and the fact that GDP growth has continued a strong trend – Qliro Group can expect consumer consumption to remain equally strong.

NORWAY: GDP RELATIVE TO PRIVATE CONSUMPTION, EURbn

0102030405060708090

01/1

0/2

000

01/1

0/2

001

01/1

0/2

002

01/1

0/2

003

01/1

0/2

004

01/1

0/2

005

01/1

0/2

006

01/1

0/2

007

01/1

0/2

008

01/1

0/2

009

01/1

0/2

010

01/1

0/2

011

01/1

0/2

012

01/1

0/2

013

01/1

0/2

014

01/1

0/2

015

01/1

0/2

016

01/1

0/2

017

01/1

0/2

018

01/1

0/2

019

01/1

0/2

020

EU

Rb

n

Norway private consumption Norway GDP

Source: Macrobond and Nordea

FINLAND: GDP RELATIVE TO PRIVATE CONSUMPTION, EURbn

0

10

20

30

40

50

60

01/1

0/20

00

01/1

0/20

01

01/1

0/20

02

01/1

0/20

03

01/1

0/20

04

01/1

0/20

05

01/1

0/20

06

01/1

0/20

07

01/1

0/20

08

01/1

0/20

09

01/1

0/20

10

01/1

0/20

11

01/1

0/20

12

01/1

0/20

13

01/1

0/20

14

01/1

0/20

15

01/1

0/20

16

01/1

0/20

17

01/1

0/20

18

01/1

0/20

19

01/1

0/20

20

EU

Rb

n

Finland private consumption Finland GDP

Source: Macrobond and Nordea

Marketing material commissioned by Qliro Group 27

Qliro Group7 June 2019

DENMARK: GDP RELATIVE TO PRIVATE CONSUMPTION, EURbn SWEDEN: GDP RELATIVE TO PRIVATE CONSUMPTION, EURbn

0

10

20

30

40

50

60

70

80

01/1

0/20

00

01/1

0/20

01

01/1

0/20

02

01/1

0/20

03

01/1

0/20

04

01/1

0/20

05

01/1

0/20

06

01/1

0/20

07

01/1

0/20

08

01/1

0/20

09

01/1

0/20

10

01/1

0/20

11

01/1

0/20

12

01/1

0/20

13

01/1

0/20

14

01/1

0/20

15

01/1

0/20

16

01/1

0/20

17

01/1

0/20

18

01/1

0/20

19

01/1

0/20

20

EU

Rb

n

Denmark private consumption Denmark GDP

Source: Macrobond and Nordea

0

20

40

60

80

100

120

140

01/1

0/20

00

01/1

1/20

01

01/1

2/20

02

01/0

1/20

04

01/0

2/20

05

01/0

3/20

06

01/0

4/20

07

01/0

5/20

08

01/0

6/20

09

01/0

7/20

10

01/0

8/20

11

01/0

9/20

12

01/1

0/20

13

01/1

1/20

14

01/1

2/20

15

01/0

1/20

17

01/0

2/20

18

01/0

3/20

19

01/0

4/20

20

EU

Rb

n

Sweden private consumption Sweden GDP

Source: Macrobond and Nordea

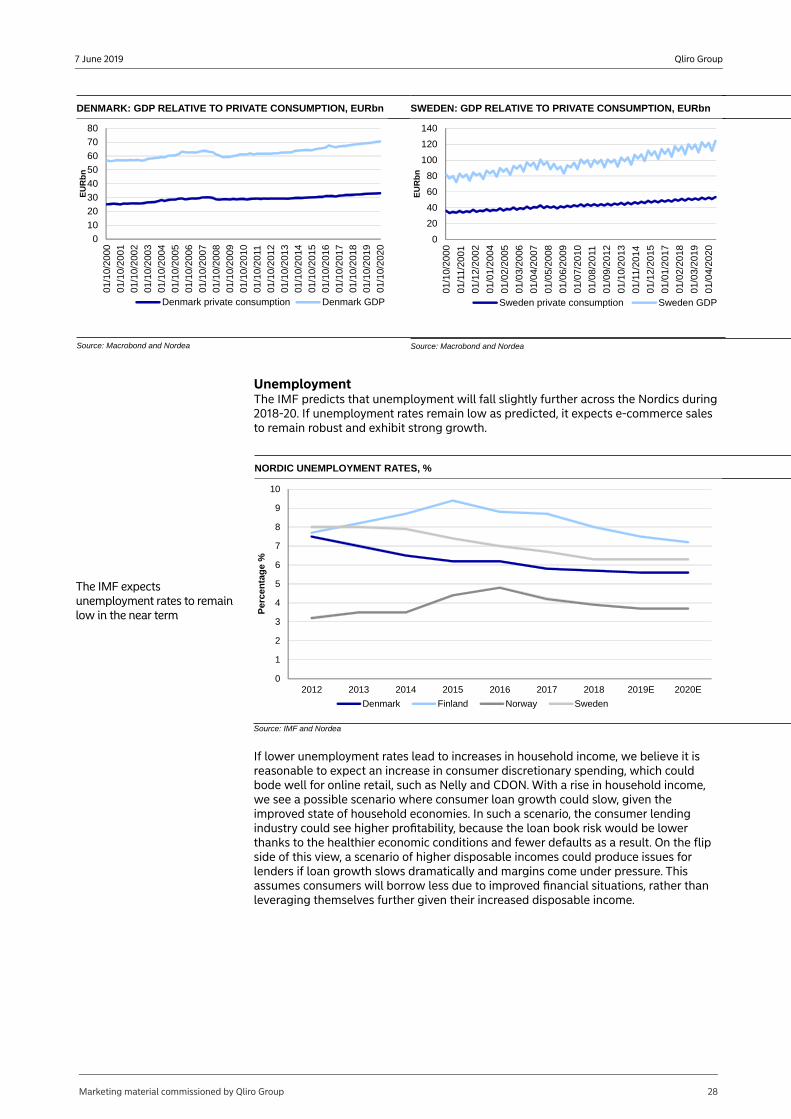

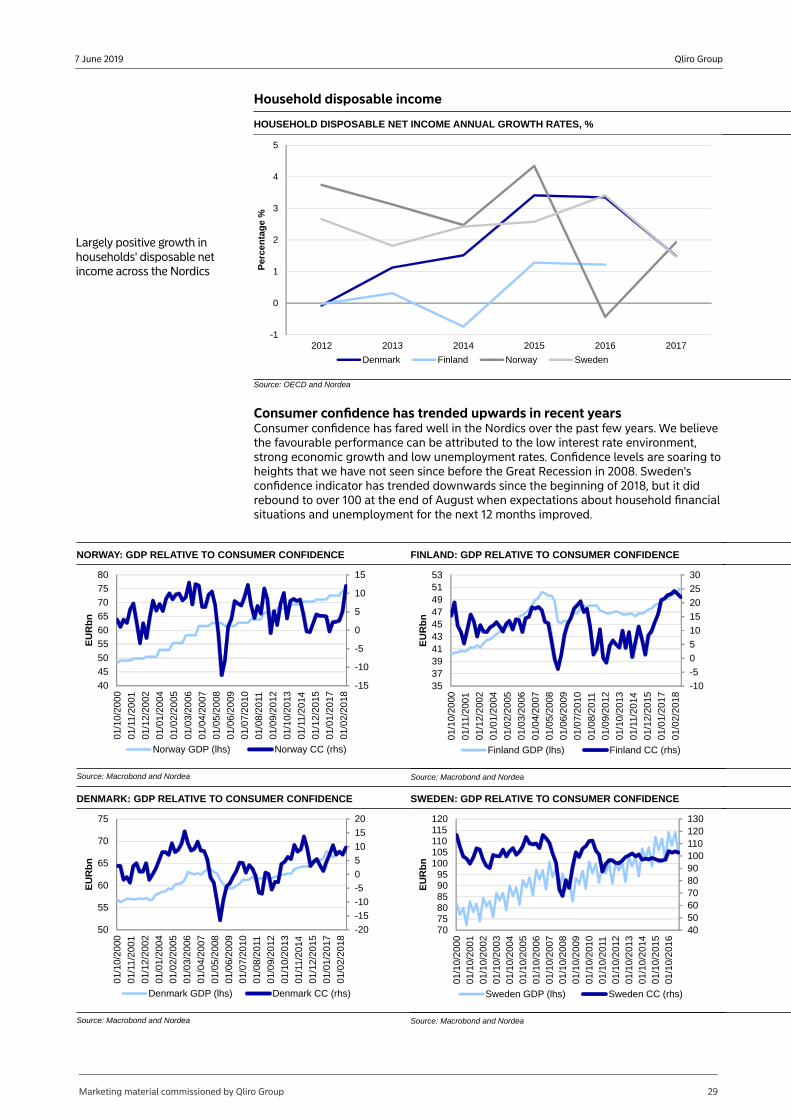

UnemploymentThe IMF predicts that unemployment will fall slightly further across the Nordics during 2018-20. If unemployment rates remain low as predicted, it expects e-commerce sales to remain robust and exhibit strong growth.

NORDIC UNEMPLOYMENT RATES, %

The IMF expects unemployment rates to remain low in the near term

0

1

2

3

4

5

6

7

8

9

10

2012 2013 2014 2015 2016 2017 2018 2019E 2020E

Per

cen

tag

e %

Denmark Finland Norway Sweden

Source: IMF and Nordea