PRE-AWARD PRE-AWARD CLOSE OUT / EXTENSION CLOSE OUT / EXTENSION PROCESS PROCESS CRYSTAL MILLER CRYSTAL MILLER AMY CARSON AMY CARSON OCTOBER 27 - 2:00-3:30 PM OCTOBER 27 - 2:00-3:30 PM OCTOBER 29 – 9:00-10:30AM OCTOBER 29 – 9:00-10:30AM CON 1010 CON 1010

Purpose To clarify award close out policy, procedures, roles and responsibilities related to Sponsored Projects from the Pre-Award perspective.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PRE-AWARD PRE-AWARD CLOSE OUT / CLOSE OUT /

EXTENSION PROCESSEXTENSION PROCESS

CRYSTAL MILLERCRYSTAL MILLERAMY CARSONAMY CARSON

OCTOBER 27 - 2:00-3:30 PMOCTOBER 27 - 2:00-3:30 PMOCTOBER 29 – 9:00-10:30AMOCTOBER 29 – 9:00-10:30AM

CON 1010CON 1010

Purpose

To clarify award close out policy, procedures, roles and responsibilities

related to Sponsored Projects from the Pre-Award perspective

BackgroundBackground

Everyone Has a Role

SPAdmin SPAcct Principal Investigators Departmental/Unit Administrator

What is the Role of SPAdmin? Understanding and assisting in

interpretation ofSponsor’s requirementsEffects of these requirements on

department/unitRestrictions/flexibility of SPAcct to meet

spoonsor’s termsUniversity policies and procedures related to

close outs

What is the Role of SPAdmin? Negotiating subagreements

Out○ Flowdown sponsor agreements○ Ensure reports and deliverables are received

on timeIn

○ Ensure project is not continuing without a contract in place

○ Ensure prime monitoring expectations are being met

What is the Role of SPAdmin? Monitoring End dates

Notify PIs and departmental/unit administrators of upcoming award expirations

Clarify departmental needs and sponsor expecations○ Extension○ Advance Accounts○ Close Outs

What is the Role of SPAdmin? Reporting to Board of Regents

Reconciling Revenue reported (Plans) to Revenue Received

Myths Pre-award does not need to know when a

grant/contract is closed out If it’s not federal – begin and end dates don’t matter No cost extensions are not required in industry

sponsored agreements We do not have to treat clinical trial contracts the

same as grants Advance accounts are not allowable on contracts Residuals are allowable on non-federal projects Receiving partial indirects is a justification for

keeping greater than 25% residuals

Myth 1

Pre-award does not need to know when a grant/contract is closed outBOR reportingSponsor reportingTerms/ConditionsAdvance accounts

Myth 2

If it’s not federal – begin and end dates don’t matterConsistencyLiabilityIndemnification

Myth 3

No cost extensions are not required in industry sponsored agreementsConsistencyContract specific

Myth 4

We do not have to treat clinical trial contracts the same as grantsMaybe – maybe not

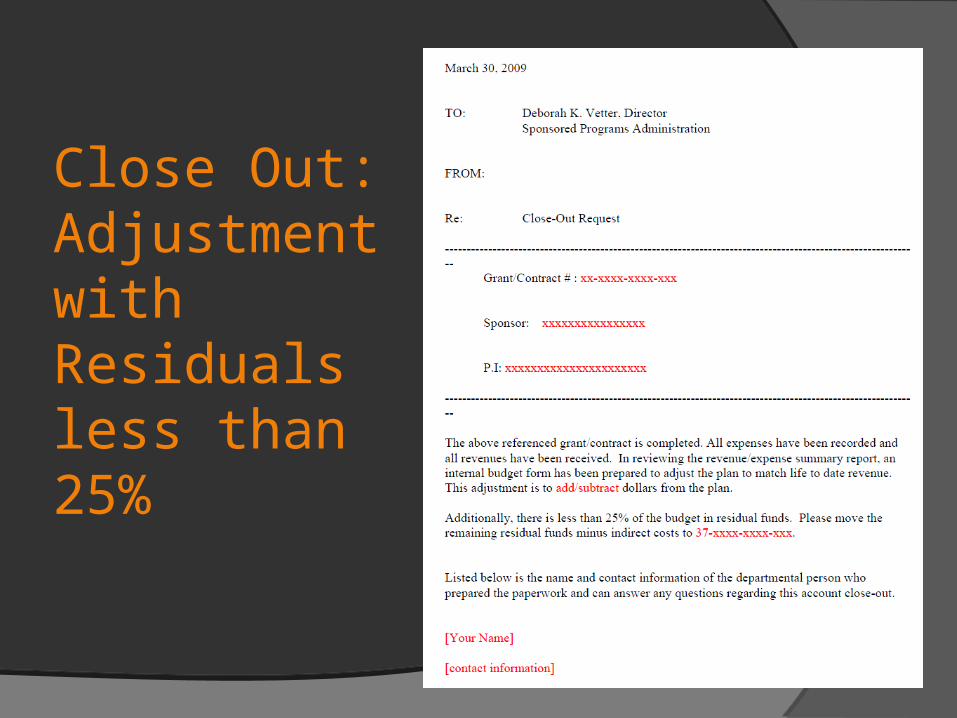

Extension Memos

Use one of the following

PI must sign

Provide information in red

Extension:No Sponsor ApprovalRequired

Extension:Sponsor ApprovalRequired

Advance AccountsAdvance Accounts

Myth 5

Advance accounts are not allowable on contractsIRB feesNo IRB/IACUC/IBC approvals requiredWork separate from approvals being

conducted

Advance Accounts

Background Assigned to a sponsored project before the award

or extension process is completed Most common with subcontracts

Approval includes authorization to incur costs outside of the official project start and end dates

Are zero balance accounts Incur expenses No budget or revenue

35 & 36 WBS advance accounts will become account number

34 accounts will be assign as 37 WBS advance accounts

Advance Accounts

Advance accounts might be appropriate if:

The project start date occurs before the award process has been completed

A contract extension is in negotiation and has yet to b signed by all parties

Extension of awards or subcontracts are delayed pending finalization by the sponsor or the federal government

Sponsor grants pre-spend authority

Advance Account Form

Close OutsClose Outs

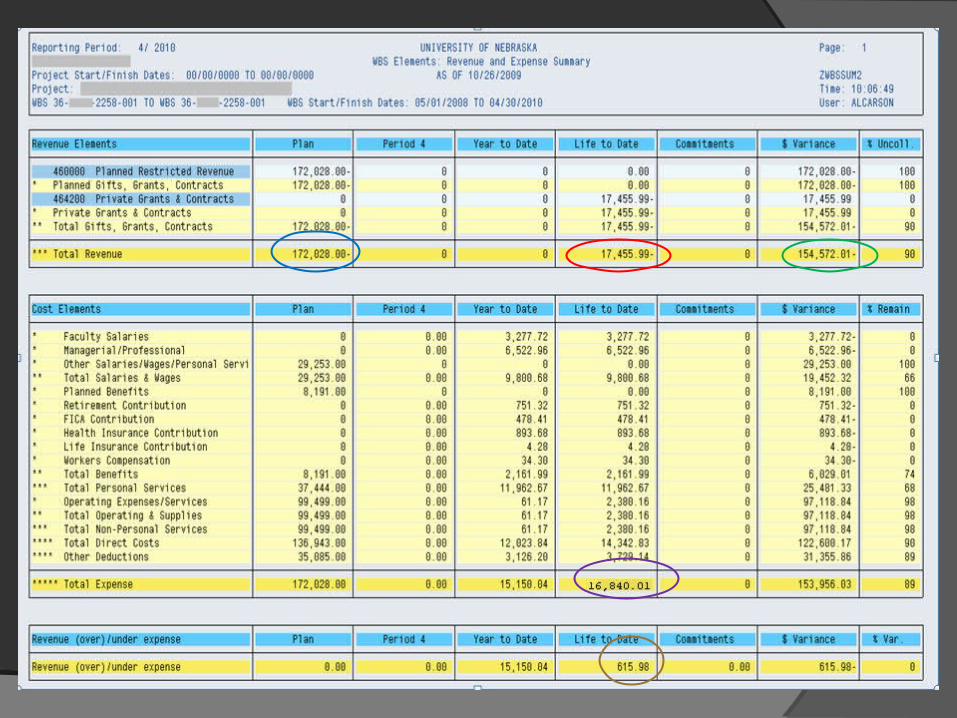

Revenue and Expense Revenue and Expense Summary Report from Summary Report from SAP – example…SAP – example…

Myth 6

Residuals are allowable on non-federal projectsDepends

○ Terms/ConditionsCost reimbursement vs. Fixed PriceGuidelinesContracts

Myth 7

Receiving partial indirects is a justification for keeping greater than 25% residualsConsistencyAnti-KickbackPre-award consideration – not at close-out

Important Aspects of Revenue and Expense Summary for SPAdmin

Revenue (over)/under

expense

Revenue

Plan

Life to Date

Variance

Total Expense

Expenses

Revenue Plan is information that is reported to Board of Regents (BOR)

$100 million = Revenue not Plan Big disconnects:

Clinical Trial agreements○ number of patients recruited

Adjustments need to be made, when Plan does not match Life to Date – to reflect actual funds received

Plan= Amount of Award Checklists set up in SPAdmin Database

Life to Date = Actual Funds Received

*Note: Close outs should not be requested until all revenue is received from the Sponsor

Variance= +/- the difference between Plan and Life to Date= the dollar figure that must be on the internal budget sentto SPAdmin for close out

= Revenue Reported to BOR

Revenue Formulas

Example:77,433/1.26 = 61,454.76 (Direct Costs)77,433 – 61,454.76 = 15,978.24 (F&A Costs)

* F&A rate

Variance / 1.26* = Direct Costs

Variance Direct Costs = F&A Costs

Close Out Budget Fields

Completed Close Out Budget Using the Example Provided in this Process Illustration

Close Out Memos

Use one of the following

PI must sign

Provide information in red

No Adjustments

= 0 (No budget Needed)

= (No Residual Funds)

= 0 (No Residual Funds)Revenue (over)/under

expense

Variance

Total Expense

Life to Date

Close Out: No Adjustments

Adjustment/No Residuals

> 0 (Budget Needed - ± for amount)

= (No Residual Funds)

= 0 (No Residual Funds)Revenue (over)/under

expense

Variance

Total Expense

Life to Date

Close Out: Adjustment with no Residuals

Adjustment/Residuals <25%

• > 0 (Budget Needed - ± for amount)

• ≠ (Residual Funds)

• ≠ 0 (Residual Funds)• × 25% = 25% threshold• < 25% threshold

Revenue (over)/under

expense

Variance

Total Expense Life to Date

Revenue (over)/under

expense

Life to Date

Close Out: Adjustment with Residuals less than 25%

Adjustment/Residuals >25%

• > 0 (Budget Needed - ± for amount)

• ≠ (Residual Funds)

• ≠ 0 (Residual Funds)• × 25% = 25% threshold• > 25% threshold• Provide justification

Revenue (over)/under

expense

Variance

Total Expense

Life to Date

Revenue (over)/under

expense

Life to Date

Close Out: Adjustment with Residuals Greater than 25%

Residual Justification?• Anti-Kickback Act of 1986 - Compliance

• If there is significant residual fund balance, i.e., an amount greater than or equal to 25 percent of the contract/grant price, at the completion of work for the contract/grant, the Principal Investigator must provide a written explanation for the substantial discrepancy between the cost to perform the contract/grant and the contract/grant price. • This explanation should be supplied by the Principal Investigator to Sponsored Programs Administration, which will use it along with the information that the Principal Investigator is required to provide upon closeout of the agreement as the basis for an audit of the project.

University Residual Policy Comparisons

University of Idaho 10%

San Francisco State University $1,000

Georgia Southern University 25%

Texas A & M 25%

University of Pennsylvania Health System

50%

Return Residuals to Sponsor

• > 0 (Budget Needed - ± for amount)

• ≠ (Residual Funds)

• ≠ 0 (Residual Funds)

Variance

Total Expense

Life to Date

Revenue (over)/under

expense

Close Out: Return Residuals To the Sponsor

Conclusion

Timely project close out/extension action is critical to:•Accurate revenue reporting to BOR •Comply with internal and external policy• Ensure receipt of final payment• Save time, money and reputation of the institution• Protect against withholding of new awards campus-wide by the awarding agency• Prevent suspension of payments for costs incurred on other projects funded by the same agency

Policy References

A-21 A-133 A-110 Anti-Kickback Act of 1986

42 U.S.C. 1320a-7b(b)

Questions?

Related Documents

![Welcome [d2h44nai6dnz3i.cloudfront.net] · 2020-08-04 · • Clarify roles and responsibilities. • Review adaptation/resilience measures that you are already working on • Integrate](https://static.cupdf.com/doc/110x72/5faa61ca04a26829a02b29b6/welcome-2020-08-04-a-clarify-roles-and-responsibilities-a-review-adaptationresilience.jpg)