1 A PROJECT REPORT ON ³CUSTOMER SATISFACTION TOWARDS INSURANCE INDUSTRY ´ . Submitted to CENTRAL UNIVERSITY OF HIMACHAL PRADESH (In partial fulfilment of requirement of the prescribed course) Masters of Business Administration (2010-2012) Supervised By: Submitted by: Mr. Shabab Ahmed PUNEET SHARMA Roll No. CUHP10MBA18

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 1/40

1

A

PROJECT REPORT

ON

³CUSTOMER SATISFACTION TOWARDS INSURANCE INDUSTRY .́

Submitted to

CENTRAL UNIVERSITY OF HIMACHAL PRADESH

(In partial fulfilment of requirement of the prescribed course)

Masters of Business Administration

(2010-2012)

Supervised By: Submitted by:

Mr. Shabab Ahmed PUNEET SHARMA

Roll No. CUHP10MBA18

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 2/40

2

PREFACE

The liberalization of the Indian insurance sector has been the subject of much heated debate for some years.

The policy makers where in the catch 22 situation wherein for one they wanted competition, development

and growth of this insurance sector which is extremely essential for channelling the investments in to the

infrastructure sector. At the other end the policy makers had the fears that the insurance preemie, which are

substantial, would seep out of the country; and wanted to have a cautious approach of opening for foreign

participation in the sector.

As one of the rare occurrences the entire debate was put on the back burner and the IRDA saw the day of the

light thanks to the maturing polity emerging consensus among factions of different political parties. Though

some changes and some restrictive clauses as regards to the foreign participation were included the IRDA

has opened the doors for the private entry into insurance.

Whether the insurer is old or new, private or public, expanding the market will present multitude of

challenges and opportunities. But the key issues, possible trends, opportunities and challenges that insurance

sector will have still remains under the realms of the possibilities and speculation. What is the likely impact

of opening up India¶s insurance sector?

The large scale of operations, public sector bureaucracies and cumbersome procedures hampers nationalized

insurers. Therefore, potential private entrants expect to score in the areas of customer service, speed and

flexibility. They point out that their entry will mean better products and choice for the consumer. The critics

counter that the benefit will be slim, because new players will concentrate on affluent, urban customers as

foreign banks did until recently. This seems to be a logical strategy. Start-up costs-such as those of settingup a conventional distribution network-are large and high-end niches offer better returns. However, the

middle-market segment too has great potential. Since insurance is a volumes game. Therefore, private

insurers would be best served by a middle-market approach, targeting customer segments that are currently

untapped.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 3/40

3

ACKNOWLEDGEMENT

The project period has been a great platform for me since it makes me experience certain things which could

not be experienced during the studies in the university.

The project was a great help in learning since it made me to observe and understand practical things which

were far away from our course books.

My foremost thanks to our Vice Chancellor Mr. FURQAN QAMAR who provided us an opportunity and

gave me the permission for this survey. I would like to thank Mr. SHABAB AHMAD (In charge) who

guided me at all stages in the preparation of this dissertation. This project would not have been possible

without his valuable suggestion and encouragement.

This whole effort is the result of guidance, assistance and inspiration of several people who helped me

during my preparation of this report.

I found no words to express my gratitude & thanks to all of them.

Last but not the least all that I am capable of doing I owe to THE ALMIGHTY. I request the readers to

excuse for the short comings.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 4/40

4

EXECUTIVE SUMMARY

In today¶s corporate and competitive world, I find that insurance sector has the maximum growth and

potential as compared to the other sectors. Insurance has the maximum growth rate of 70- 80% while as

FMCG sector has maximum 12-15% of growth rate. This growth potential attracts me to enter in this sector

and get experience in highly competitive and enhancing sector.

The success story of good market share of different market organizations depends upon the availability of

the product and services near to the customer, which can be distributed through a distribution channel. In

Insurance sector, distribution channel includes only agents or agency holders of the company. If a particular

insurance company has adequate agents in the market it can capture big market as compared to the other

companies. For long run stay in insurance sector company must be loyal for its customers and provide them

best services to compete with its competitors, otherwise it will lose its recognition from this corporate world.

Agents are the only way for a company of Insurance sector through which policies and benefits of thecompany can be explained to the customer. Thus every company wants that it have best agents with them

which serve its customer in best way than any other company can serve. It¶s directly related to feel the

customer satisfy.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 5/40

5

TABLE OF CONTENT

1. INTRODUCTION

1.1 TOPIC INTRODUCTION......................................................................... ..................................................6

1.2 THE NEED TO MEASURE CUSTOMER SATISFACTION.................. ..................................................7

1.3 SERVICE QUALITY AND CUSTOMER SATISFACTION................................................... .................8

1.4 EXPECTATIONS AND CUSTOMER SATISFACTION..........................................................................8

1.5 MARKETING OF INSURANCE IN INDIA............................................................. ...........................9

1.10 MAJOR COMPAINES IN INSURANCE INDUSTRY.......................................................... ................11

1.11 SWOT ANALYSIS OF INSURANCE INDUSTRY....................................................... .....................13

1.12 MAJOR STEPS TAKEN BY INSURANCE INDUSTRY FOR CUSTOMER SATISFACTION........15

2. LITERATURE REVIEW....................................................................................................... ......................17

3.1 NEED OF THE STUDY........................................................................................................ ....................20

3.2 TITLE JUSTIFICATION.......................................................................................................... .................20

3.3 OBJECTIVES OF THE STUDY......................................................................................... ......................21

3.4 SCOPE OF THE STUDY............................................................................................................. .............22

3.5 SIGNIFICANCE OF THE STUDY........................................................................................ ...................22

3.6 RESEARCH METHODOLOGY..................................................................................................... ..........23

4. DATA ANALYSIS.............................................................................................. ............................... .........24

5.1 FACTS/FINDINGS................................................................................................................... .................34

5.2 SUGGESTION.............................................. ..................................................................................... ........35

5.3 LIMITATION OF RESEARCH........................................................................................................ ........36

5.4CONCLUSION............................................................................................................................. ..............37

6. BIBLIOGRAPHY................................................................................................... .............................. .......38

7. ANNEXURE

7.1 QUESTIONNAIRE................................................................................................................................ ....39

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 6/40

6

1. INTRODUCTION

1.1 TOPIC INTRODUCTION

The meaning of satisfaction: "Satisfied" has a range of meanings to individuals, but it generally seems to be

a positive assessment of the service. The word "satisfied" itself had a number of different meanings for

respondents, which can be split into the broad themes of contentment/happiness, relief, and achieving aims

and happy with outcome.

It's a well known fact that no business can exist without customers. It¶s important to work closely with your

customers to make sure the service you create or provide for them is as close to their requirements as you

can manage. Because it's critical that you form a close working relationship with your client, customer

service is of vital importance. What follows are a selection of tips that will make your clients feel valued,

wanted and loved.

Thus the ³customer satisfaction´ refers to how satisfied customers are with the products or services they

receive from a particular agency. The level of satisfaction is determined not only by the quality and type of

customer experience but also by the customer¶s expectations.

A customer may be defined as someone who has a direct relationship with, or is directly affected by your

agency and receives or relies on one or more of your agency¶s services or products. Customer in human

service is commonly referred to as service users, consumers or clients.

Attributes of customer satisfaction can be summarized as:

1) Product Quality

2) Product Packaging

3) Keeping delivery commitments

4) Price

5) Responsiveness and ability to resolve complaints and reject reports

6) Overall communication, accessibility and attitude

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 7/40

7

1.2 THE NEED TO MEASURE CUSTOMER SATISFACTION

Satisfied customers are central to optimal performance and financial returns. In many places in the world,

business organizations have been elevating the role of the customer to that of a key stakeholder over the past

twenty years. Customers are viewed as a group whose satisfaction with the enterprise must be incorporated

in strategic planning efforts. Forward-looking companies are finding value in directly measuring and

tracking customer satisfaction (CS) as an important strategic success indicator. Evidence is mounting that

placing a high priority on CS is critical to improved organizational performance in a global marketplace.

With better understanding of customers' perceptions, companies can determine the actions required to meet

the customers' needs. They can identify their own strengths and weaknesses, where they stand in comparison

to their competitors, chart out path future progress and improvement. Customer satisfaction measurement

helps to promote an increased focus on customer outcomes and stimulate improvements in the work

practices and processes used within the company.

When buyers are powerful, the health and strength of the company's relationship with its customers ± its

most critical economic asset ± is its best predictor of the future. Assets on the balance sheet ± basically

assets of production ± are good predictors only when buyers are weak. So it is no wonder that the

relationship between those assets and future income is becoming more and more tenuous. As buyers

become empowered, sellers have no choice but to adapt. Focusing on competition has its place, but with

buyer power on the rise, it is more important to pay attention to the customer.

Customer satisfaction is quite a complex issue and there is a lot of debate and confusion about what exactly

is required and how to go about it. This point is an attempt to review the necessary requirements, and discuss

the steps that need to be taken in order to measure and track customer satisfaction.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 8/40

8

1.3 SERVICE QUALITY AND CUSTOMER SATISFACTION

There is a great deal of discussion and disagreement in the literature about the distinction between service

quality and satisfaction. The service quality school view satisfaction as an antecedent of service quality -

satisfaction with a number of individual transactions "decay" into an overall attitude towards service quality.

The satisfaction school holds the opposite view that assessments of service quality lead to an overall attitude

towards the service that they call satisfaction. There is obviously a strong link between customer satisfaction

and customer retention. Customer's perception of Service and Quality of product will determine the success

of the product or service in the market.

If experience of the service greatly exceeds the expectations clients had of the service then satisfaction will

be high, and vice versa. In the service quality literature, perceptions of service delivery are measured

separately from customer expectations, and the gap between the two provides a measure of service quality.

1.4 EXPECTATIONS AND CUSTOMER SATISFACTION

Expectations have a central role in influencing satisfaction with services, and these in turn are determined by

a very wide range of factors lower expectations will result in higher satisfaction ratings for any given level

of service quality. This would seem sensible; for example, poor previous experience with the service or

other similar services is likely to result in it being easier to pleasantly surprise customers. However, there are

clearly circumstances where negative preconceptions of a service provider will lead to lower expectations,

but will also make it harder to achieve high satisfaction ratings - and where positive preconceptions and highexpectations make positive ratings more likely and seem to be an oversimplification.

Major overall satisfaction measure, consisting of four subscales: general satisfaction (e.g. You feel happy

recommending the bank to a friend); Trust (e.g. You trust the staff at your branch to do what is best for you);

Reliability (e.g. Requests are carried out right first time); and professionalism (e.g. Staff have the knowledge

to deal with any queries you have).

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 9/40

9

1.5 MARKETING OF INSURANCE IN INDIA

Insurance is in a manner of speaking the last frontier in the financial sector to open. It is also a sector, which

leads to benefits across the full spectrum, from the individual who now have wider choices, to the economy,

which see increased savings, to the infrastructure sector, which can look forward to long term funding being

available. In an under-insured economy, newer channels of distribution have to be utilized to intensify thereach of insurance both in urban and rural markets. This will create huge employment opportunities not only

within insurance companies but also as agents and consultants of insurance companies.

Marketing Mix Policies

Different companies can choose to position themselves differently and hence the Marketing Mix is different.

However, there are certain common characteristics that one can cull out from the possible strategies that

companies adopt.

Product:

The development of flexible products to suit individual requirements is what will differentiate the winners

from the also-rans. The key to success is in providing insurance solutions, not standardized insurance

products. The concept of riders/optional benefits has already been a huge innovation brought about by the

new players, which has led to customization of products for individual needs. However, companies may

differentiate themselves on the basis of product segments that they choose to focus on and excel in.

Place:

Different companies may however choose different channels and different geographies to focus on. The

channel options are - tied agency force, corporate agents and brokers and this is an area where different

companies will make different choices. Many companies like HDFC Standard Life are focusing on all

channels whereas companies like Max New York Life are focusing on the tied agency force only. Customer

interface will be a key challenge for life insurance companies and includes every that interaction that the

customer has with the company, such as sales, new business underwriting, policy servicing, premium

payments, claim processing and so on. Technology can play a crucial role in delivering the highest standards

of service set by the company and it will be imperative for any serious player to excel in all of these.

Price:

Price is a relevant differentiator only in two segments - pure term insurance and in pure annuities. Here too,

service delivery and financial strength will need to be present at a minimum acceptable level for price to be

a relevant differentiator. In case of savings oriented products, long-term returns generated are more relevant

than just the price of the product. A focus on generating good investment performance and keeping a tight

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 10/40

10

Control on costs help in generating good long-term maturity value for customers. Norms have been laid

down on all of these by IRDA and adhering to these while delivering good returns will be a challenge.

Promotion and Advertising:

The level of demand is latent and will have to be activated considerably. The market needs to be developed.

Greater awareness of insurance and the need to have it as a protection tool rather than as a tax planning

measure needs to be appreciated by the Indian people. Various communication tools including advertising,

direct marketing and road shows contribute to all this and different companies take different approaches on

these.

Process:

Cashless settlement: One of the most defining and customer-friendly changes that we¶ve seen indecent years

relates to the way claims settlements are made. The advent of the third-party administrator (TPA) regime has

facilitated the transition to the hugely convenient era of cashless settlement of health and auto insurance

claims. TPAs are entities who process claims on behalf of insurers: the IRDA licenses them after it is

satisfied that they have the financial strength, the trained manpower, the infrastructure and the skills to

undertake this activity.

Likewise, with auto insurance, the TPA ties up with garages and authorized service centres for cashless

settlement of auto insurance claims.

People:

The most important factor that materializes sales and maintains customer relationships on a long- term basis

is this factor. No matter what distribution strategy a company adopts, customer relationship has to be taken

care of in order to maintain the customer base on a long-term basis.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 11/40

11

1.6 MAJOR INSURANCE COMPANIES ARE AS UNDER :

1.Life Insurance Corporation of India (LIC)

Life Insurance Corporation of India (LIC) was established on 1 September 1956 to spread the message of

life insurance in the country and mobilise people¶s savings for nation-building activities. LIC with its central

office in Mumbai and seven zonal offices at Mumbai, Calcutta, Delhi, Chennai, Hyderabad, Kanpur and

Bhopal, operates through 100 divisional offices in important cities and 2,048 branch offices. LIC has 5.59

lakh active agents spread over the country.

The Corporation also transacts business abroad and has offices in Fiji, Mauritius and United Kingdom. LIC

is associated with joint ventures abroad in the field of insurance, namely, Ken-India Assurance Company

Limited, Nairobi; United Oriental Assurance Company Limited, Kuala Lumpur; and Life Insurance

Corporation (International), E.C. Bahrain. It has also entered into an agreement with the Sun Life (UK) for

marketing unit linked life insurance and pension policies in U.K.

In 1995-96, LIC had a total income from premium and investments of $ 5 Billion while GIC recorded a net

premium of $ 1.3 Billion. During the last 15 years, LIC's income grew at a healthy average of 10 per cent as

against the industry's 6.7 per cent growth in the rest of Asia (3.4 per cent in Europe, 1.4 per cent in the US).

LIC has even provided insurance cover to five million people living below the poverty line, with 50 per cent

subsidy in the premium rates. LIC's claims settlement ratio at 95 per cent and GIC's at 74 per cent are higher

than that of global average of 40 per cent. Compounded annual growth rate for Life insurance business has

been 19.22 per cent per annum.

2. Max New York Life Insurance Co. Ltd.

Max New York Life Insurance Company Limited is a joint venture that brings together two large forces -

Max India Limited, a multi-business corporate, together with New York Life International, a global expert in

life insurance. With their various Products and Riders, there are more than 400 product combinations to

choose from. They have a national presence with a network of 57 offices in 37 cities across India.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 12/40

12

3. ICICI Prudential Life Insurance Company Ltd.

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank, a premier financial

powerhouse and prudential plc, a leading international financial services group headquartered in the United

Kingdom. ICICI Prudential was amongst the first private sector insurance companies to begin operations in

December 2000 after receiving approval from Insurance Regulatory Development Authority (IRDA). Thecompany has a network of about 56,000 advisors; as well as 7 banc assurance and 150 corporate agent tie-

ups.

4. Om Kotak Mahindra Life Insurance Co. Ltd.

Kotak Mahindra Old Mutual Life Insurance Ltd. is a joint venture between Kotak Mahindra Bank Ltd.

(KMBL), and Old Mutual plc.

5. Birla Sun Life Insurance Company Ltd.

Birla Sun Life Insurance Company is a joint venture between Aditya Birla Group and Sun Life financial

Services of Canada.

Others are:

Tata AIG Life Insurance Company Ltd.

SBI Life Insurance Company Limited

ING Vysya Life Insurance Company Private Limited

Allianz Bajaj Life Insurance Company Ltd.

Metlife India Insurance Company Pvt. Ltd.

AMP SANMAR Assurance Company Ltd.

Dabur CGU Life Insurance Company Pvt. Ltd.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 13/40

13

1.7 SWOT ANALYSIS OF INSURANCE INDUSTRY

STRENGTH

1. Domestic image of companies supported by Prudential¶s international image is strength of the company.

2. Strong and well spread network of qualified intermediaries and sales person.

3. Strong capital and reserve base.

4. The companies provide customer service of the highest order.

5. Huge basket of product range which are suitable to all age and income groups.

6. Large pool of technically skilled manpower with in depth knowledge and understanding of the market.

7. The companies also provide innovative products to cater to different needs of different customers.

WEAKNESS

1.Heavy management expenses and administrative costs.

2. Low customer confidence on the private players.

3. Vertical hierarchical reporting structure with many designations and cadres leading to power politics at all

levels without any exception.

4. Poor retention percentage of tied up agents.

OPPORTUNITIES

1. There will be inflow of managerial and financial expertise from the world¶s leading insurance markets.

Further the burden of educating consumers will also be shared among many players.

2. International companies will help in building world class expertise in local market by introducing the best

global practices.

3. Insurance liberalization in India is expected to result in a wider choice of major commercial insurance

covers, such as fire, export credit etc.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 14/40

14

THEARTS

1. Large numbers of competitor¶s especially major threat from the India¶s biggest insurance company i.e.

LIC.

2. Entrance of many more companies in insurance sector with better plans and schemes which attracts most

of customer.

3. Switching of customers from one to other insurance company because of better schemes provided by

other companies.

4. Because of fraud done by fake companies many of customers does not trust easily on private companies.

INSURANCE INDUSTRY: KEYS STRENGHS

FINANCIAL EXPERTISE

As a joint venture of leading financial services groups , companies have the financial expert iserequired to manage your long-term investments safely and efficiently.

RANGE OF SOLUTIONS

We have a range of individual and group solutions , which can be easily, customised to specific needs

o u r group solutions have been designed to offer you complete flexibility combined with a low

charging structure.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 15/40

15

1.8 MAJOR STEPS TAKEN BY INSURANCE SECTOR FOR CUSTOMER

SATISFACTION

1. ENCOURAGE FACE-TO-FACE DEALINGS

This is the most daunting and downright scary part of interacting with a customer. If you're not used to this

sort of thing it can be a pretty nerve-wracking experience. Rest assured, though, it does get easier over time.

It's important to meet your customers face to face at least once or even twice during the course of a project.

2. RESPOND TO MESSAGES PROMPTLY & KEEP CLIENTS INFORMED

This goes without saying really. We all know how annoying it is to wait days for a response to an email or

phone call. It might not always be practical to deal with all customers' queries within the space of a few

hours, but at least email or call them back and let them know you've received their message and you'll

contact them about it as soon as possible. Even if you're not able to solve a problem right away, let the

customer know you're working on it.

3. BE FRIENDLY AND APPROACHABLE

A fellow Site Pointer once told me that you can hear a smile through the phone. This is very true. It's very

important to be friendly, courteous and to make your clients feel like you're their friend and you're there to

help them out. There will be times when you want to beat your clients over the head repeatedly with a blunt

object - it happens to all of us. It's vital that you keep a clear head, respond to your clients' wishes as best

you can, and at all times remain polite and courteous.

4. HAVE A CLEARLY-DEFINED CUSTOMER SERVICE POLICY

This may not be too important when you're just starting out, but a clearly defined customer service policy is

going to save you a lot of time and effort in the long run. If a customer has a problem, what should they do?

If the first option doesn't work, then what? Should they contact different people for billing and technical

enquiries? If they're not satisfied with any aspect of your customer service, who should they tell?

There's nothing more annoying for a client than being passed from person to person, or not knowing who to

turn to. Making sure they know exactly what to do at each stage of their enquiry should be of utmost

importance. So make sure your customer service policy was presented and anywhere else it may be useful.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 16/40

16

5. ATTENTION TO DETAIL

Have you ever received a Happy Birthday email or card from a company you were a client of? Have you

ever had a personalised sign-up confirmation email for a service that you could tell was typed from scratch?

These little niceties can be time consuming and aren't always cost effective, but remember to do them.

Even if it's as small as sending a Happy Holidays email to all your customers, it's something. It shows you

care; it shows there are real people on the other end of that screen or telephone; and most importantly, it

makes the customer feel welcomed, wanted and valued.

6. ANTICIPATE CLIENT'S NEEDS & GO OUT OF YOUR WAY TO HELP THEM OUT

Sometimes this is easier said than done! However, achieving this supreme level of understanding with your

clients will do wonders for your working relationship.

7. HONOUR PROMISES

The simple message, when you promise something, delivers. The most common example here is project

delivery dates.

Clients don't like to be disappointed. Sometimes, something may not get done, or you might miss a deadline

through no fault of your own. Projects can be late, technology can fail and sub-contractors don't always

deliver on time. In this case a quick apology and assurance it'll be ready ASAP wouldn't go amiss.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 17/40

17

2. LITERATURE REVIEW

AshishBhave, March 2006

The customer's requirements must be translated and quantified into measurable targets. This provides an

easy way to monitor improvements, and deciding upon the attributes that need to be concentrated on in order to improve customer satisfaction. We can recognize where we need to make changes to create improvements

and determine if these changes, after implemented, have led to increased customer satisfaction.

Adam Faulkner, 2006

Increasingly the companies that are winning - the smarter organisations - are the ones that understand how

contact centre business processes and their supporting technologies can be combined to allow for a more

holistic customer experience. Currently many of the different technology and process components - WFM,

IVR, quality monitoring, eLearning, CRM integration and analytical tools - that can support the goal of a

more integrated customer experience are only available as standalone systems, with just basic links between

the different components. To enable effective customer lifecycle management - like that being achieved by

companies such as Churchill and BA - requires deep expertise in the integration and interoperability of all

these different solutions - it's difficult, but it's not impossible - and it's worth getting right.

Jeanne Bliss October 23rd

, 2007

At some point, your business will suffer a failure that disappoints customers. The measure of a company is

taken at such moments. Customers see your true colours at these times more than at any other. How you

explain, react, remove the pain, and take accountability for your actions, clearly signal your sentiment

toward customers and reveals the collective "heart" of your organization.

Elaine Fogel, 2007

Glitches happen and setbacks occur when we deal with customers -- they're as inevitable as death and taxes.

The key to retaining these customers when an error occurs is handling them right from the start. Whether

your company or organization delivers products, services, or promises... its credibility and reputation is on

the line when you don't deliver what you say you will, and when. There's no magic pill to averting these

situations, but you can be proactive in redeeming yourself and retaining customers when things go wrong.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 18/40

18

Wikis Mandle 2002

Customer satisfaction, business term, is a measure of how products and services supplied by a company

meet or surpass customer expectation. It is seen as a key performance indicator within business and is part of

the four of a Balanced Scorecard.

In a competitive marketplace where businesses compete for customers, customer satisfaction is seen as a key

differentiator and increasingly has become a key element of business strategy. However, the importance of

customer satisfaction diminishes when a firm has increased bargaining power .

Paul & Nick Hague

Developing a customer satisfaction programme is not just about carrying out a survey. Surveys provide the

reading that shows where attention is required but in many respects, this is the easy part. Very often, major

long lasting improvements need a fundamental transformation in the company, probably involving training

of the staff, possibly involving cultural change. The result should be financially beneficial with less

customer churn, higher market shares, premium prices, stronger brands and reputation, and happier staff.

However, there is a price to pay for these improvements. Costs will be incurred in the market research

survey. Time will be spent working out an action plan. Training may well be required to improve the

customer service. The implications of customer satisfaction surveys go far beyond the survey itself and will

only be successful if fully supported by the echelons of senior management.

Marcus Fidel, 2007

Customer satisfaction differs depending on the situation and the product or service. A customer may be

satisfied with a product or service, an experience, a purchase decision, a salesperson, store, service provider,

or an attribute or any of these. Some researchers completely avoid ³satisfaction´ as a measurement objective

because it is ³too fuzzy an idea to serve as a meaningful benchmark.´4 Instead, they focus on the customer¶s

entire experience with an organization or service contact and the detailed assessment of that experience.

A group of researchers of the Centre for the Study of Social Policy (2007) conceptualize that satisfaction is

based on the customer¶s experience of both contact with the organization (the moment of truth) and personaloutcomes. According to these researchers, satisfaction can be experienced in a variety of situations and

connected to both goods and services. To another extent, these researchers defined satisfactions as a ³highly

personal assessment´ that is greatly influenced by ³individual expectations´. This definition views

³individual´ element as powerful force to create satisfaction. Likewise, many researchers (Oliver, 1981;

Brady and Robertson, 2001) conceptualize customer satisfaction as an individual¶s feeling of pleasure or

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 19/40

19

Disappointment resulting from comparing a product¶s perceived performance (or outcome) in relation to his

or her expectations.

Jones and Suh (2000)stated that customer satisfaction is highly variable assessment individuals do based on

their experiences with specific features of products and services they receive, it makes sense for servicing

organizations to involve customer satisfaction measurement as their meaningful benchmark for

development.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 20/40

20

3.1NEED OF THE STUDY

The project was an attempt to explore the ³Customer satisfaction towards INSURANCE INDUSTRY´ in

JALANDHAR.

The study basically focuses on measurement of customer satisfaction related to Services offered and

rendered by the insurance industry. This study gives a bird¶s eye view of the hard and soft services provided

by insurance companies to their clients.

The project started in JALANDHAR region covering all the local market. In this process I meet 100

persons to get response from them to know about the satisfaction level. During my work I found the

different response from the people about insurance and what they desire from it. Also, the need of my

research was that, what the industry should do to serve its customer in more efficient and effective manner

so the satisfaction level reaches to maximum level.

3.2TITLE

To determine customer satisfaction level towards Insurance industry.

TITLE JUSTIFICATION

The above title is self explanatory. The study deals mainly with studying the satisfaction level of customer in

the insurance industry with a special focus on consumer behaviour towards the most emerging sector now a

days in INDIA. The various segments of the markets divided in terms of Insurance Needs, Age groups,

Area.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 21/40

21

3.3 OBJECTIVE OF THE STUDY

y To determine reasons behind opting for an insurance and reasons for opting for that particular

policies.

y To study the types of benefits provided by insurance services.

y To determine the feedback on services provided by insurance agent.

y To know the satisfaction level of the customers.

y To know how insurance companies can reach to a maximum level of satisfaction.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 22/40

22

3.4 SCOPE OF THE STUDY

A big boom has been witnessed in Insurance Industry in recent times. A large number of new players have

entered the market and are trying to gain market share in this rapidly improving market. The study then goes

on to evaluate and analyse the findings so as to present a clear picture of trends in the Insurance sector

related to satisfaction of customer. This project will help to understand the current market scenario andmarketing in stiff competition. Being a student of management I can draw the relevant conclusion from the

market survey and give the appropriate suggestion to the companies.

3.5 SIGNIFICANCE OF THE STUDY

SIGNIFICANCE TO THE INDUSTRY

This is a limited study which takes into consideration the responses of 100 people. This data can be

explorated to take in the trends across the industry. The significance for the industry lies in studying these

trends that emerge from the study. It is a rapidly changing and evolving sector. People are only beginning to

wake up to its vast possibilities. A study like this can attempt to guide the future of the industry based on

current trends.

SIGNIFICANE FOR THE RESEARCHER

To facilitate and provide all the useful information to the companies.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 23/40

23

3.6 RESEARCH METHODOLOGY

RESEARCH DESIGN

The research is primarily descriptive in nature. The sources of information are both primary & secondary.

A well-structured questionnaire was prepared and personal interaction was done.

SAMPLING METHODOLOGY

POPULATION: All the customers of different insurance companies having different policies.

SAMPLING TECHNIQUE: Initially, a rough draft was prepared keeping in mind the objective of the research.

A pilot study was done in order to know the accuracy of the Questionnaire. The final Questionnaire was

arrived only after certain important changes were done. Thus my sampling came out to be judgemental and

convenient

SAMPLING UNIT: The respondents who were asked to fill out questionnaires are the sampling units. These

comprise of employees of Private companies, Govt. Employees, and Self-employed etc.

SAMPLE SIZE: The sample size was restricted to only 100, which comprised of mainly peoples from

JALANDHAR due to time constraints.

SAMPLING AREA: The area of the research was JALANDHAR, PUNJAB, INDIA.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 24/40

24

4. DATA ANAL AND INTE ETATION

1. How long you have been the customer of insurance companies?

a) 1-3 yrs___ c) 5-10 yrs___

b) 3-5 yrs___ d) any ot r (Speci y) _____

INTER R ETATION

As per survey t e pie char t shows that the invest ent rate of customers has been increased two timesmore

in last three years as comparative to last f ive years. This shows that Insurance industry increased its market.

¡ %27%

14%0%

1-3yrs

3-5yrs

5-10yrs

any other

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 25/40

25

2. In which plan have you invested?

a) Market link___ b) Traditional ___

INTER R ETATION

Most of the customers have invested in market link planinstead of traditional. Market link plan are relatedto mutual fund investment. This shows that most of them are ready to bear little bit market r isk with assur ing

their life through insurance policies.

69%

31%

PLAN IN WHICH INVE TED

Marked linked

Traditional

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 26/40

26

3. What is the reason to invest in Insurance Industry?

a) Returns and savings___ b) Tax benefits___

c) By known agent ___ d) Security___

INTERPRETATION

Through survey I find out that the main reason for investing in insurance sector by the customers is

³security´. 63% of respondents were agreed that they have invested for securing their life from uncertain

future risk whereas 19% of people have invested for the purpose of return and savings. Rest of them goes for

tax benefits and through agents.

19 ¢

11%

7%

63%

REASONS OR INVESTMENT

Re£

u¤ ¥

s and savings

¦

ax benef its

By known agent

Secu § ity

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 27/40

27

4. Have you invested in bank ing sector?

a) Yes___ b) No___

If yes, then specify where_________

INTER R ETATION

The pie char t clear ly shows that 83% of customers of INSUR ANCE INDUSTR Y have also invested in the

bank ing sector and most of them specif ied that they have invested in Fi ed Deposits.

83%

17%

INVE TED IN BANKING SECTOR

Yes

No

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 28/40

28

5. Are you satisf ied with current policy which you have taken?

a) Satisf ied saving tool ____ b) Non satisf ied___

c) Non responding___

INTER R ETATION

Pie char t shows that maximum [74%] of the customers are satisf ied with the current policy which they have

taken. Where the 21% of customer are not satisf ied with the current policy due to some reason and rest of

them did not give any response. So it s not so good results for the company that 21% of its customers are not

satisf ied with the policy provided to them, so the 21% of customer¶s possi bility of re-investing in insurance

industry also decreases with this result.

74%

21%

5%

SATISFIED WITH POLICY

Satis ̈ ied saving tool

Non satis© ied

Non responding

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 29/40

29

6. Is communication channels followed by the companies easily approachable?

a) Always___ b) Sometimes____

c) Never___

INTER PR ETATION

27% of customers said that the communication channels is not easily approachable to them due to some

barr ier like, semantic barr ier, miscommunication which leaves a bad impact of company on its customers,

and 4% directly says that there is no communication source to communicate and 69% of themare fully

satisf ied. So the industry is suffer ing from the problem of communication barr ier which is not good for the

image of companies.

69%

27%

4%

APPROACH OF COMMUNICATION CHANNEL

Always

Sometimes

Never

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 30/40

30

7. Does the company provides the needed information at right time?

a) Yes___ b) No___

INTER PR ETATION

The effect of bad communication is shown here. 19% of respondents do not get any impor tant

information on time which is the greatest barr ier in front of customers. They don¶t come to know the

premium date, matur ity date, any newly introduced schemes by the company andany other things which

give direct benef its to the customers.

81%

19%

TIMLY INFORMATION

Yes

No

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 31/40

31

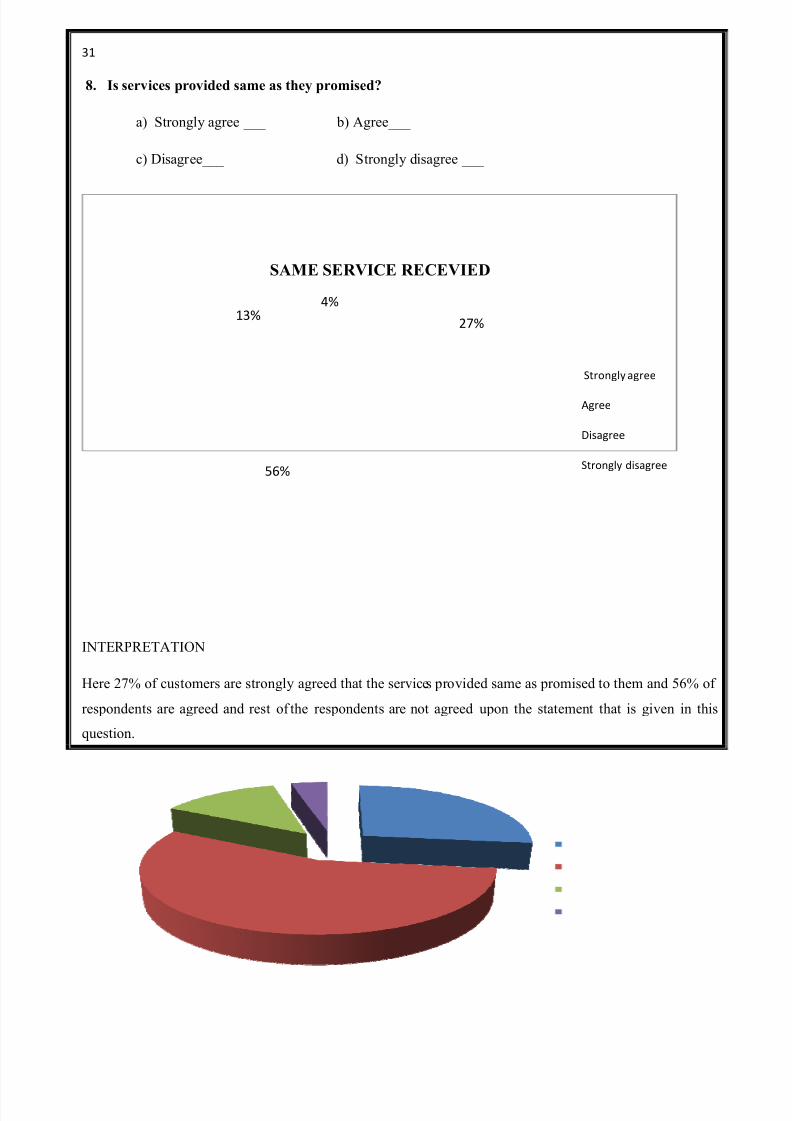

8. Is services provided same as they promised?

a) Strongly agree ___ b) Agree___

c) Disagree___ d) Strongly disagree ___

INTER PR ETATION

Here 27% of customers are strongly agreed that the services provided same as promised to them and 56% of

respondents are agreed and rest of the respondents are not agreed upon the statement that is given in this

question.

Near ly most of respondent are agreed with the statementwhich is good for the industry.

27%

56%

13%4%

SAME SERVICE R ECEVIED

Strongly agree

Agree

Disagree

Strongly disagree

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 32/40

32

9. Are you satisf ied with the service of agent?

a) Every time___ b) Sometimes___

c) R arely___ d) Never___

INTER PR ETATION

Data gives that 44% of total respondentsare satisf ied every time with the service of agent. 35% says

sometimes and 14% says rarely. This result shows that the agentsare not much concerned with their existing

customers as they should. This behaviour can lose its existing customers in future.

44%

35%

14%

7%

AGENT SERVICES

Every time

Sometimes

Rerely

Never

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 33/40

33

10. How would you rate the services provided by insurance industry in comparison to other sectors in

which you have invested?

a) Excellent ___ b) Very good___

c) Good___ d) Average___

e) Poor___ f) Very poor__

INTER PR ETATION

Here the mixed response was given by the customers40% says that the service is very good as compare to

other sector and 25% says its good where 11% says the service is excellent as ,5% customer response was

poor and 2% was very poor.

From the above data I would like to conclude that services provided by insurance industry are quite

satisfactory. But in compar ison of other sectors it is bit unsatisfactory reason being its poor communication

channel and unawareness of agents towards its customers.

11%

40%

5%

17%

5%

%

Excellent

Ver g d

G

d

Average

P r

Ver p r

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 34/40

34

5.1 FACTS/FINDINGS

1. As the people think that insurance is a tool to protect their family & a tax saving device. They are aware

of the fact & realizing its, importance. The company should try to expand & build up its infrastructure

because there is a large potential for insurance in India.

2. Companies should come up with more branches in INDIA with the objective and goals to meet the

demands & expectations of the public. Because the entrance of private players will increase the competition

and it would be a tough task to secure a good position in market.

3. Since Insurance industry is leading with several other sectors, it should be easy for them to penetrate into

the market and secure a good position if they pay greater attention to the service part provided to their

customer and thereby forming a long and trusted relationship.

4. Two major factors that can be determine from the survey data are:

A. Performance Matrix (Performance relative to customer¶s priorities)

B. Satisfaction Index (Customers Satisfaction over a period of time)

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 35/40

35

5.2 SUGGESTION

E-mails can be used effectively for disseminating information among customers. Since application of this is

most cost effective, the organization can mail the required information to their customer which is most need

and useful to each and every customer and agents should be concerned with their existing and get proper

feedback from them which helps to know the weak points where the company lacks in comparison to others.

The collected data was analyzed to calculate the customer satisfaction for the different sets of respondent.

Is a satisfied customer asset for a company? Definitely not. Until or unless he becomes a loyal customer.

This is the area where the organization can improve in the near future.

Thus the company have to convert the entire satisfied customer into a loyal customer.

This study is an earnest effort to enhance the practical knowledge by measuring the customer satisfaction as

well as contributing to the organizational efficiency by suggesting ways to manage and improve the same

profitably in the highly competitive time to come.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 36/40

36

5.3 LIMITATIONS OF THE RESEARCH

1. The research is confined to a certain parts of Jalandhar and does not necessarily shows a pattern

applicable to all of Country.

2. Some respondents were reluctant to divulge personal information which can affect the validity of all

responses.

3. In a rapidly changing industry, analysis on one day or in one segment can change very quickly. The

environmental changes are vital to be considered in order to assimilate the findings.

4. There is no surety that respondents truly give their response.

5. The research is cost constraint as well as time constraint also.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 37/40

37

5.4 CONCLUSION

Customer service, like any aspect of business, is a practiced art that takes time and effort to master. All you

need to do to achieve this is to stop and switch roles with the customer. An organisation with a strong

customer satisfaction power places the customer at the centre of service design, planning and best service

delivery.

What would you want from your business if you were the client? How would you want to be treated? Treat

your customers like your friends and they'll always come back. This is the main step towards satisfying your

customer. Meeting the needs of the customer is the underlying rationale for the existence of community

service organizations. Customers have a right to quality services that deliver outcomes. Where the services

are delivered best customer surely go for there and in the business customer is a king and he`s always right.

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 38/40

38

6. BIBLIOGRAPHY

BOOKS

y Marketing Management ± Philip Kotler

y Marketing.Com ± Vijay Mukhi

WEBSITES

www.marketingterms.com

www.atsinfotech.com

http://ezinearticles.com/?Sales-Promotion---A-Cutting-Edge-Marketing-Tool&id=2035509

http://ezinearticles.com/?Sales-Promotion---A-Sure-Way-of-Increasing-Consumers-Brand-

Loyalty&id=4013089

y http://www.highbeam.com/doc/1G1-166778609.html

y http://www.highbeam.com/doc/1G1-198547971.html

y http://ezinearticles.com/?Marketing-Mix---Top-4-Promotion-Mix-Tactics&id=1398510

y http://kalyan-city.blogspot.com/2010/05/marketing-marketing-mix-4-ps-of.html

y http://www.marcommwise.com/article.phtml?id=7

y http://www.informaworld.com/smpp/content~db=all~content=a779581691s

y http://www.msi.org/publications/publication.cfm?pub=203

JOURNALS

y Goldsmith, Ronald, & Lafferty, Barbara. (2002). Consumer response to websites and their influence

on advertising effectiveness. Internet research, 12, 318-328.

REFERENCES

y Marketing Communications Management: Concepts and Theories, Cases and Practices; Paul Copley; 2004

y Sales Promotion: How To Create, Implement and Integrate Campaigns; Julian Cummings; 2003

y Promotional Spending Trends 2008

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 39/40

39

7. ANNEXURE

7.1 QUESTIONNAIRE ON CUSTOMER SATISFACTION TOWARDS INSURANCE INDUSTRY:

NAME:

AGE:

GENDER:

OCCUPATION:

1. How long you have been the customer of INSURANCE COMPANIES?

a) 1-3 yrs___ c) 5-10yrs___

b) 3-5 yrs___ d) Any other (Specify) ____

2. In which plan have you invested?

a) Market link___ b) Traditional___

3. What is the reason to invest in INSURANCE INDUSTRY?

a) Returns and savings___ b) Tax benefits___

c) By known agent ___ d) Security___

4. Have you invested in BANKING SECTOR?

a) Yes___ b) No___

If yes then specify ________________________________

5. Are you satisfied with current policy which you have taken?

a) Satisfied saving tool____ b) Non satisfied___

c) Non responding___

6. Is communication channels followed by companies are easily approachable?

a) Always___ b) Sometimes____

c) Never___

8/4/2019 Puneet Project

http://slidepdf.com/reader/full/puneet-project 40/40

40

7. Does the companies provide needed information at right time?

a) Yes___ b) No___

8. Is services provided same as they promised?

a) Strongly agree ___ b) Agree___

c) Disagree___ d) Strongly disagree

9. Are you satisfied with the service of agent?

a) Every time___ b) Sometimes___

c) Rarely___ d) Never___

10. How would you rate the services provided by insurance industry in comparison to other sector in

which you have invested?

a) Excellent___ b) Very good___

c) Good___ d) Average___

e) Poor___ f) Very poor__

11. How would the sector improve or provide better services to you, please suggest_____________

Related Documents