Reviewing compliance obligations A good practice approach

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Reviewing compliance obligations

A good practice approach

Enquiries:

Public Sector Renewal Division, Public Sector Commission

Dumas House, 2 Havelock Street, West Perth 6005

Locked Bag 3002, West Perth WA 6872

Telephone: (08) 6552 8500 Fax: (08) 6552 8710

Email: [email protected]

Website: www.publicsector.wa.gov.au

© State of Western Australia 2015

There is no objection to this publication being copied in whole or part, provided there is due acknowledgement of any

material quoted or reproduced from the publication.

Published by the Public Sector Commission (Western Australia), June 2015.

Copies of this report are available on the Public Sector Commission website at www.publicsector.wa.gov.au

Disclaimer

The Western Australian Government is committed to quality service to its customers and makes every attempt to ensure

accuracy, currency and reliability of the data contained in these documents. However, changes in circumstances after

time of publication may impact the quality of this information.

Confirmation of the information may be sought from originating bodies or departments providing the information.

Accessibility

Copies of this document are available in alternative formats upon request.

Reviewing compliance obligations Contents 3

Contents

Commissioner’s foreword ................................................................................... 5

Executive summary ............................................................................................. 6

Background .......................................................................................................... 9

‘Red tape’ reduction .............................................................................................. 10

Purpose of this report ............................................................................................ 10

Compliance obligations ..................................................................................... 12

What is the purpose of compliance obligations? ................................................. 12

What form do they take? ......................................................................................... 12

Application of an obligation ................................................................................... 13

Assessing compliance ............................................................................................ 13

Non-compliance ....................................................................................................... 13

Review of compliance obligations ................................................................... 14

Methodology ............................................................................................................ 14

Working group and consultation ............................................................................ 15

Review against good practice principles ............................................................... 15

Key findings ............................................................................................................. 16

Recommendations................................................................................................... 17

A good practice approach ................................................................................. 18

Cost and utility ......................................................................................................... 18

Good practice principles ......................................................................................... 19

Purpose ................................................................................................................. 19

Implementation ...................................................................................................... 20

A good practice approach- responsible agencies ................................................ 20

1. Identify public interest outcome ..................................................................... 21

2. Develop compliance approach ...................................................................... 21

3. Implement a compliance obligation ............................................................... 22

4. Monitor compliance ....................................................................................... 22

5. Regularly review compliance obligations....................................................... 23

Reviewing compliance obligations Contents 4

A good practice approach- complying agencies .................................................. 24

1. Prepare systems and staff ............................................................................ 24

2. Implement programs, collect data and information ........................................ 25

3. Report ........................................................................................................... 25

4. Utilise information ......................................................................................... 25

5. Review system and process ......................................................................... 25

Glossary .............................................................................................................. 26

Appendix A ......................................................................................................... 29

Review of compliance obligations ......................................................................... 29

Appendix B ......................................................................................................... 41

Good practice principles – evaluation questions ................................................. 41

Purpose ................................................................................................................. 41

Implementation ...................................................................................................... 43

Appendix C ......................................................................................................... 45

Resources and further reading ............................................................................... 45

Reviewing compliance obligations Commissioner’s foreword 5

Commissioner’s foreword

The resources required to meet internal administrative compliance obligations within the

public sector are significant. While acknowledging the importance of effective oversight

from an accountability and governance perspective, this review has been undertaken in

response to chief executive officer (CEO) perceptions of ever increasing public sector

wide compliance burdens. CEOs have expressed concern about the impact on agency

operations, in particular the compliance burden placed on smaller agencies with limited

resources.

My firm view is that the most effective and efficient compliance programs are a joint

responsibility of the agencies administering the program (responsible agencies) and

those agencies which must comply (complying agencies). The design and delivery of

regulatory programs require regular scrutiny and adjustment to ensure that they meet

identifiable public interest objectives and that their costs do not outweigh these benefits.

They should appropriately address, rather than seek to eliminate risk, and should not

unnecessarily add to the overall compliance burden for agencies.

The review has highlighted good practice in responsible and complying agencies.

Examples are the regular review of obligations by responsible agencies as part of a

process of continuous improvement, and complying agencies which proactively use

information generated through compliance activities to inform their own planning and

operations. The review shows that there is scope for these good practices to be more

comprehensively adopted across the WA public sector. Organisational and employee

capability and commitment to good governance are key elements which can be better

harnessed to add value to compliance activities, resulting in reduced costs of compliance.

Thank you to all agencies who contributed to this review, including the cross sector

reference group and other responsible and complying agencies who were consulted.

I hope that the initiatives described in this report will serve as a catalyst for further reform

and ongoing attention to efficiency and effectiveness in administrative compliance

programs.

MC Wauchope

PUBLIC SECTOR COMMISSIONER

Reviewing compliance obligations Executive summary 6

Executive summary

Effective compliance and regulatory programs, systems and processes are essential to

good governance and contribute to the achievement of broad public sector and individual

agency goals and outcomes. Compliance requirements have increased over the last

decade, as a response to greater expectations around accountability and transparency in

the use of public resources and measurement of outcomes.

It is increasingly important that the public sector reconsiders its approach to internal

regulation to ensure that compliance burden appropriately addresses risk while

contributing to accountability, productivity and performance goals.

With this in mind, and prompted by concerns from some CEOs of smaller agencies at the

perceived undue compliance burden, the Public Sector Commission in 2014 undertook a

review of administrative compliance obligations within the WA public sector. The review

was conducted in partnership with a range of agencies that institute and manage

compliance obligations (called ‘responsible agencies’ in the report) and those that are

required to comply with the obligations (called ‘complying agencies’ in the report).

The review sought to:

achieve better awareness of the issues regarding costs and burden of internal

compliance and reporting

identify whether responsible agencies were already taking action to ensure

efficiency in compliance obligations

stimulate further action and progress in this area through providing good practice

principles and information

achieve better scrutiny of proposals to introduce any additional compliance

obligations.

The review resulted in the development of good practice principles for reviewing

compliance obligations. They may also be applied to assessing proposed compliance

obligations. The principles consider the purpose and implementation for the compliance

obligation.

Reviewing compliance obligations Executive summary 7

Purpose

Need - is there a public interest need for the obligation and the information

derived from it?

Cost - what are the costs (time, systems, employees, opportunity costs) to

complying agencies and the responsible agency?

Benefit - what ultimate benefit is derived and does this outweigh the cost?

Implementation

Technology - is the best use made of technology in complying, analysing and

reporting?

Approach - are there alternative approaches to instituting a compliance obligation,

based on consideration of risk, that may be more beneficial?

Use of the information - how widely is the information used; can it be used without

significant re-working?

The report includes examples of initiatives and programs being run by responsible

agencies, current and proposed initiatives to review obligations and good practice

observed in complying agencies.

The review found that:

Responsible agencies are aware of the burden which administrative compliance

places on agencies, especially small agencies.

Many responsible agencies provide ongoing assistance to complying agencies by

way of standardised templates, enquiry and assistance hotlines, facilitating

networks for information sharing.

Some responsible agencies are proactive in reviewing systems and processes for

compliance and considering alternative approaches to compliance and have

recently reviewed and streamlined some obligations.

There is further scope for responsible agencies to review some compliance

obligations, with a view to streamlining or minimising them.

The review highlighted a number of opportunities, such as better definition of

obligations and assistance material from responsible agencies; improvements in

the timeliness of reporting by responsible agencies; improved data collection

systems and analysis; broader analysis and use of compliance information for

sector-wide and organisational performance and planning purposes; and greater

‘return on investment’ for complying agencies by information being made

available and suitable for their own management activities.

Reviewing compliance obligations Executive summary 8

To improve efficiency, effectiveness and accountability in relation to administrative

compliance, the Public Sector Commissioner recommends that:

responsible agencies regularly review, and make improvements where possible

to, the compliance obligations they administer, using the good practice principles

contained in the report

before instituting new compliance obligations, responsible agencies fully consider

any alternative approaches. If a compliance obligation is proposed, it should be

assessed against the good practice principles outlined in the report.

to better harness opportunities for improving efficiency and adding value to

compliance activities, the good practice approaches outlined in this report should

be considered by responsible agencies and complying agencies.

Reviewing compliance obligations Background 9

Background

Effective compliance and regulatory programs, systems and processes are essential

components of good governance and contribute to the achievement of broad public

sector and individual agency goals and outcomes. Agencies which institute compliance

and reporting requirements (referred to in this report as ‘responsible agencies’) or comply

with them (referred to in this report as ‘complying agencies’) expend significant public

funds in doing so. All agencies have specific roles in the shared responsibility for

compliance.

Public sector compliance requirements have been increasing over the last decade, as a

response to greater expectations of the public sector and government for accountability

and transparency in the use of public resources and measurement of outcomes.

Sometimes an obligation is introduced as a response to a specific risk event. Simply

increasing compliance obligations, however, without considering the resource burden or

whether it appropriately addresses risks may not necessarily contribute to accountability

and can have a negative impact on productivity.

It is increasingly important that the public sector reconsiders its approach to internal

regulation and where possible reduces the level of compliance burden on agencies

without impeding essential measures to ensure accountability for performance. This

requires:

reviewing compliance obligations, eliminating and streamlining any requirements

or elements that over time have become non-productive or have a low return

continuing to develop more efficient reporting methods for agencies to be able to

meet the requirements that are necessary

ensuring that any proposals for introducing new requirements are carefully

considered in terms of costs, benefits and risks

considering alternative methods to reporting or compliance approaches, such as

audits or reviews; or approaches which build organisational capability, such as

education and awareness raising programs.

This will ensure the best use of available resources, while still maintaining confidence

that compliance obligations provide transparency and accountability and support good

management and administration.

Reviewing compliance obligations Background 10

‘Red tape’ reduction

The growth of ‘red tape’ has been considered as reflective of a general attitude of risk

aversion in regulatory and administrative decision-making, both in Australia and

overseas.1 As a response to increasing levels of regulation, ‘red tape’ reduction and

regulatory reform programs have been in place for some time in governments nationally

and internationally to reduce the administrative burden on business, thereby improving

productivity and profitability.

Recent Western Australian government initiatives to reduce ‘red tape’ for business

commenced with the 2009 ‘Reducing the Burden Report.2’ The Minister for Finance

recently launched the ‘Plan to Reinvigorate Regulatory Reform’, of which a key element

is the reduction of ‘red tape’. Compliance requirements within government (‘government

to government red tape’), whether administrative processes or reporting obligations to

central agencies, have also received attention as part of efforts to reduce unnecessary

overheads, improve efficiency and increase innovation. A recent example of this is the

Western Australian Auditor General’s recommendation in the Audit Results Report:

Annual 2013-14 Financial Audits Auditor General’s Report 18 of November 2014 that

‘(S)trong consideration should be given to reducing the financial reporting requirements

of small agencies.’3

Purpose of this report

This report provides information about a Public Sector Commission (Commission) review

conducted in partnership with a number of agencies to review and enhance practice in

relation to compliance obligations in public sector administration and management. The

report is intended to stimulate debate and encourage good practice among both

responsible and complying agencies. The issues raised here also challenge responsible

agencies to consider how much compliance is required and what those requirements

should entail.

The review was conducted in accordance with the Public Sector Commissioner’s general

functions under s.21A of the Public Sector Management Act 1994 (PSM Act) to promote

the overall efficiency and effectiveness of the public sector, having regard to the public

sector principles for public administration and management.

1 Australian Public Sector Commission, 2007 ‘Reducing red tape in the APS’

https://resources.apsc.gov.au/2007/redtape.pdf 2 Government of Western Australia, 2009: Reducing the Burden: report of the Red Tape reduction

group http://www.treasury.wa.gov.au/cms/uploadedFiles/Home/Publications/Independent_Reports/reducing_the_burden.pdf?n=1005 3 Western Australian Auditor General, 2014 ‘Auditor General’s Report 18, Audit Results Report:

Annual 2013-14 Financial Audits’ https://audit.wa.gov.au/wp-content/uploads/2014/12/report2014_18-AuditResults.pdf

Reviewing compliance obligations Background 11

The review sought to:

achieve better awareness of the issues regarding costs and burden of internal

compliance and reporting

identify whether responsible agencies were already taking action to ensure

efficiency in compliance obligations

stimulate further action and progress in this area through providing good practice

principles and information

achieve better scrutiny of proposals to introduce any additional compliance

obligations.

Reviewing compliance obligations Compliance obligations 12

Compliance obligations

What is the purpose of compliance obligations?

The purposes of public sector compliance obligations are manifold:

to ensure transparency and accountability

to provide information for planning and management purposes

to ensure public policy outcomes are met

to emphasise a strong commitment to an issue by highlighting its importance.

What form do they take?

They can take a number of forms, including:

Acts of Parliament and subsidiary legislation

Premier’s Circulars

Public Sector Wages Policy

Commissioner’s Instructions

Public Sector Commissioner’s Circulars

Treasurer’s Instructions

other sector wide policies

other sector wide guidelines

These are described in the ‘Glossary’.

Some compliance obligations are mandatory while others are recommended (although it

is generally expected that these will also be complied with).

Many compliance obligations include a reporting component to a responsible agency or

to Parliament. The nature of this reporting obligation varies: from annual reporting of

information (e.g. employment or financial outcomes) readily available within the agency,

to complex or detailed reporting requiring input and monitoring of large numbers of

transactions and monthly reporting of information, or reporting on the progress of

ongoing activity within the context of a whole of agency operational plan.

Reviewing compliance obligations Compliance obligations 13

Application of an obligation

Some obligations apply generally across the public sector, while others only apply to an

agency because of their business context.

When compliance obligations are set, it is important to determine the scope of the

application of the obligation, i.e. to which agencies it applies. This can either be

determined by virtue of using a specific instrument which automatically applies to a

particular group of agencies or employees, or be specifically defined in the legislation or

instrument which establishes the obligation.

Assessing compliance

Because of the diverse nature of compliance obligations, an assessment of whether or

not an agency has complied can be simple, such as whether an agency has provided the

required information or statistics, for example the cost of a discrete activity; or the

number of public interest disclosures an agency has received.

In many other cases a compliance obligation can involve meeting a broad public interest

outcome, involving the collation and reporting on activities and data. Evaluation of

compliance will involve an assessment of whether sufficient and appropriate activities

have been undertaken by the complying agency. This can sometimes be complex, will

require judgment and may result in a ‘maturity’ rating, rather than a yes/no evaluation.

For example a low (but not the lowest) maturity rating would signify that the activities

undertaken by the complying agency, while meeting a minimum threshold, are at the

lower end of engagement that would be expected to achieve good practice outcomes.

In all circumstances, the criteria set by the responsible agency for assessing compliance

should be clear and unambiguous, in order that they can be clearly understood by

complying agencies.

Non-compliance

Unlike many regulatory functions attached to the business sector, there is generally no

specific penalty provision attached to non-compliance with administrative obligations.

This is because the public sector works within a broad legislative and accountability

framework and is structured towards meeting comprehensive good administration and

management standards where failure can have performance and disciplinary outcomes.

Nevertheless, a failure to comply can have a range of consequences and resultant

actions. The responsible agency will consider what action to take. In some cases the

most appropriate response may be to build the capacity of the complying agency to more

fully comply in the future, for example through awareness raising, training and building

systems within the agency. Cases of non-compliance may be published in compliance-

related reports. Where there is continued non-compliance, this may be the subject of

attention in a report to Parliament. Reports of non-compliance may identify agencies by

name or simply refer to numbers or proportions of agencies.

Reviewing compliance obligations Review of compliance obligations 14

Review of compliance obligations

In 2014 in response to concerns from some CEOs about the level of compliance burden,

the Commission undertook a review to document and consider the compliance

obligations with which all Western Australian public sector authorities must comply. The

additional obligations with which individual authorities must also comply, because of their

business context or obligations to the Commonwealth government, and those obligations

which relate only to Schedule 1 PSM Act entities4, were not a specific focus of the review.

It is, however, acknowledged that these also constitute part of the total compliance

obligations for other state government bodies.

Methodology

The review involved the following steps:

preparation of a consolidated list of all compliance obligations

research into national and international public sector administrative compliance

approaches

research into and development of good practice models:

o for efficiency and effectiveness in the approach to compliance

o for systems and processes within responsible and complying agencies

establishment of a cross sector working group

research and analysis of the background and scope of the perceived ‘most

onerous’ and ‘limited value’ obligations

broader consultation with other complying agencies about these obligations

consultation with responsible agencies with regard to:

4 Schedule 1 PSM Act entities are not regarded as part of the Western Australian public sector under

the PSM Act. Examples of these entities include universities and local government authorities.

Reviewing compliance obligations Review of compliance obligations 15

o good practice within responsible agencies to ensure efficiency in setting

and maintaining compliance systems and processes, especially the

perceived most onerous and limited value obligations

o any recent or proposed initiatives to reduce the compliance burden on

complying agencies

o good practice observed within complying agencies

finalisation of conclusions regarding good practice for responsible and complying

agencies.

Working group and consultation

A cross sector working group comprising representatives from a range of WA public

sector organisations, including local government and the university sector, provided input

to the review. The working group:

reviewed the consolidated list of all compliance obligations

considered the good practice models developed by the Commission

identified compliance obligations considered ‘most onerous’ (resource

implications, such as time, systems and opportunity costs)

identified those perceived to be of ‘limited value’ to complying agencies for the

time and effort taken to comply.

Feedback was also obtained from a number of other public sector agencies about the

‘most onerous’ and ‘limited value’ obligations. Perhaps not surprisingly, those relating to

financial and budget management and reporting were considered the most resource

intensive.

Review against good practice principles

Good practice principles were developed in conjunction with the working group to provide

a framework for reviewing compliance obligations. The framework focused on the

elements relevant to establishing a strong purpose for the obligation, as well as the

elements to consider when implementing an obligation. The good practice principles are

outlined in the next section and evaluation questions for assessing against them are

provided in Appendix B.

In partnership with a number of responsible agencies, the good practice principles were

used to analyse those compliance obligations perceived to be the most onerous or of

limited value. These were seen as a priority for action due to resources expended or

perceived limited return.

The outcomes of this analysis and consultation with responsible agencies are described

in Appendix A, which provides examples of specific initiatives and progress.

Reviewing compliance obligations Review of compliance obligations 16

Key findings

The review has highlighted the following:

Responsible agencies are aware of the burden which compliance places on

agencies, especially small agencies.

Some responsible agencies are proactive in reviewing systems and processes for

compliance and considering alternative approaches to compliance.

During the period of the review some responsible agencies reviewed and

streamlined compliance requirements, while a number of others are in the

process of or have plans to review specific obligations. Some responsible

agencies also have plans to improve communication to complying agencies, for

example about the outcomes of reporting. (See Appendix A).

There is further scope for responsible agencies to review some compliance

obligations, with a view to streamlining or minimising them. This is consistent with

government expectations that CEOs take action to reduce unnecessary ‘red tape’

in government compliance obligations. Any such review should involve

consultation with complying agencies.

Many responsible agencies provide ongoing assistance to complying agencies,

for example by way of standardised templates, enquiry and assistance hotlines,

facilitating networks for information sharing.

This review has highlighted a number of opportunities:

o In some cases there could be better definition of obligations and assistance

material from responsible agencies, including providing more information

about the objectives and outcomes of the compliance activity.

o Where appropriate, responsible agencies could improve timeliness of

reporting, to enhance transparency and accountability.

o Improved data collection systems and analysis may improve efficiency and

effectiveness for both responsible and complying agencies.

o There is scope for both responsible and complying agencies to analyse and

use compliance information more broadly for sector-wide and organisational

performance and planning purposes.

o In particular, there would be greater ‘return on investment’ for complying

agencies by information being made available and suitable for their own

management activities, such as cross sector benchmarking and comparison.

Reviewing compliance obligations Review of compliance obligations 17

Recommendations

1. It is recommended that responsible agencies regularly review, and make

improvements where possible to, the compliance obligations they administer,

using the good practice principles contained in this report (pages 19-20). Such a

review should include consultation with complying agencies.

2. Before instituting new compliance obligations, responsible agencies should fully

consider any alternative approaches. If a compliance obligation is proposed, it

should be assessed against the good practice principles.

3. To better harness opportunities for improving efficiency and adding value to

compliance activities, the good practice approaches outlined in this report should

be considered by responsible agencies (pages 20-23) and complying agencies

(pages 24-25).

Reviewing compliance obligations A good practice approach 18

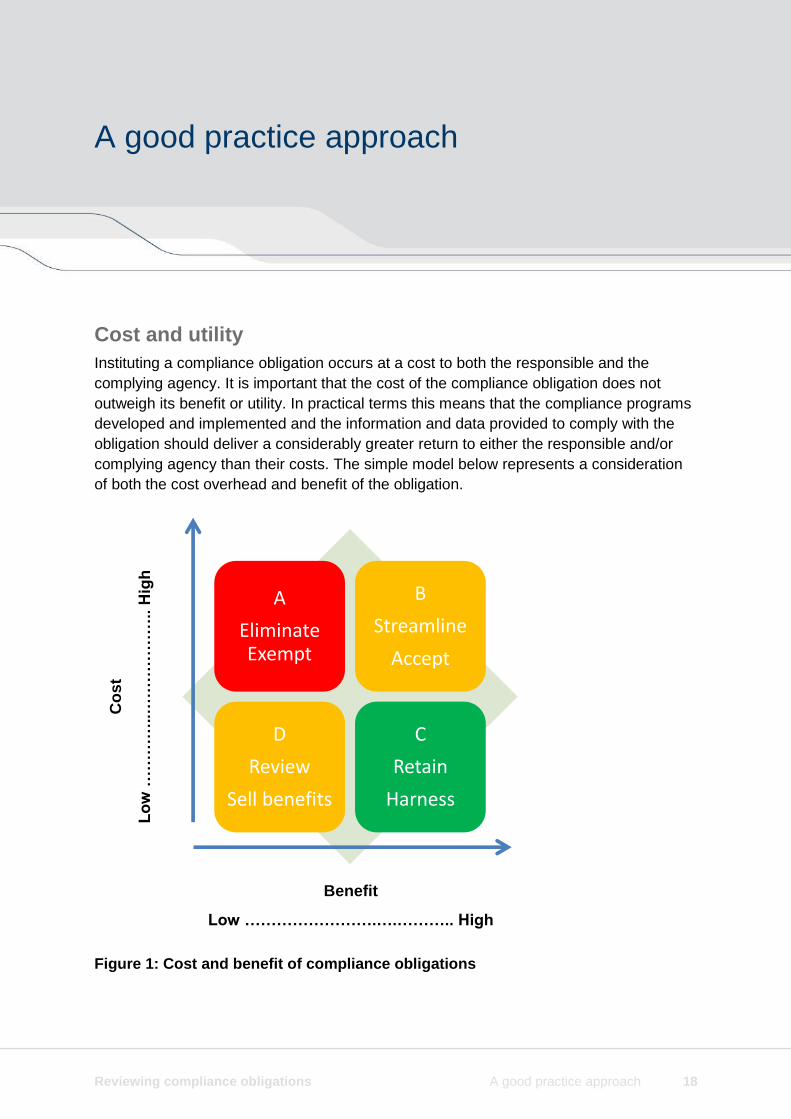

A

Eliminate Exempt

B

Streamline

Accept

D

Review

Sell benefits

C

Retain

Harness

A good practice approach

Cost and utility

Instituting a compliance obligation occurs at a cost to both the responsible and the

complying agency. It is important that the cost of the compliance obligation does not

outweigh its benefit or utility. In practical terms this means that the compliance programs

developed and implemented and the information and data provided to comply with the

obligation should deliver a considerably greater return to either the responsible and/or

complying agency than their costs. The simple model below represents a consideration

of both the cost overhead and benefit of the obligation.

Figure 1: Cost and benefit of compliance obligations

Co

st

Lo

w …

……

…..…

……

……

…..

Hig

h

Benefit

Low …………………….….……….. High

Reviewing compliance obligations A good practice approach 19

In this model, obligations which have a high benefit or utility and occur at a low cost

(quadrant C) are the most efficient. These should be retained and harnessed for

maximum value. Some occur at a high cost but the benefits outweigh this cost (quadrant

B). In this case there may be opportunities to streamline and simplify, resulting in

reduced costs. In other cases, however, it may be a case of simply accepting the cost

due to the significant benefit gained, perhaps providing a more fulsome explanation (and

quantification) of the purposes served and the benefits sought to be gained.

Some obligations have a low utility and low cost (quadrant D). In these cases, there is an

opportunity for review to ascertain if further benefit can be gained, such as value adding

for stakeholders, refining and streamlining the requirement, or better promoting the

benefits where these are not well known. When low benefit obligations occur at a high

cost (quadrant A), efforts should be made to rescind them or exempt agencies from

compliance as appropriate.

Of course, the requirements and the external environment are not static and these

assessments can change over time. Regular review assists in determining the cost of

compliance and the utility to be gained from the obligation.

Evaluating compliance obligations against the ‘Principles for efficient and effective

reporting obligations’ below enables conclusions to be drawn against the cost/benefit

model. These principles underpinned the Commission review.

Good practice principles

The Commission has identified the following good practice principles as a framework for

reviewing the effectiveness of compliance obligations. These principles provide a

structured way to assess cost and benefit shown in Figure 1. They form a two stage

process whereby the purpose must be clearly re-affirmed and the most efficient

approach to implementation considered. While the cost benefit analysis is informed and

will be affected by the method of implementation, if the benefit does not outweigh the

cost, consideration should be given to rescinding or limiting the obligation.

The purpose and the implementation should be reviewed on a regular basis to ensure

compliance with the obligation still adds value and that implementation is undertaken in

the most efficient and effective manner possible.

These principles can also be applied to any new compliance obligations which are

contemplated.

Purpose

In establishing the purpose for retaining the compliance obligation, it is important to

consider:

need - is there a public interest need for the obligation and the information derived

from it?

Reviewing compliance obligations A good practice approach 20

cost - what are the costs (time, systems, employees, opportunity costs) to

complying agencies and the responsible agency?

benefit - what ultimate benefit is derived and does this outweigh the cost?

Implementation

In the implementation of the compliance obligation, it is important to consider:

technology - is the best use made of technology in complying, analysing and

reporting?

approach - are there alternative approaches to instituting a compliance obligation,

based on consideration of risk, that may be more beneficial?

use of the information - how widely is the information used; can it be used without

significant re-working?

Evaluation questions at Appendix B provide practical assistance in making an evaluation

against these six principles.

A good practice approach- responsible agencies

There is only a small group of responsible agencies. These are in the main within the

group of agencies known as ‘central agencies’, such as the Department of Treasury,

Department of the Premier and Cabinet, or ‘oversight agencies’, such as the Public

Sector Commission or the Information Commissioner.

Commission research into compliance monitoring literature and consultation across the

public sector has shown that CEOs of responsible agencies can facilitate high levels of

compliance and achieve good practice through considering the good practice principles

described above in relation to five key areas of activity.

1. Identify public interest

outcome

2. Develop compliance approach

3. Implement 4. Monitor compliance

5. Review

Reviewing compliance obligations A good practice approach 21

1. Identify public interest outcome

Compliance obligations respond to a particular public interest need. These are not static,

as circumstances change over time. Technological and other changes impacting on

transparency of information also mean that the identification of public interest outcomes

should be re-considered from time to time.

Consider whether imposing a compliance obligation and associated reporting is

really necessary to achieve the public interest outcome and why. In doing so,

consider whether other forms of monitoring or regulation would be more beneficial.

Consider overall sector capability to deliver on the public interest outcome.

Using a risk based approach, assess the risk of not having the obligation in place,

avoiding reactive cross sector measures as a response to high profile problems.

Consider any unintended consequences of imposing a new obligation.

Consult

Consult with other policy makers as appropriate, to ensure compliance obligations

are not duplicated and do not conflict with current or proposed obligations.

When considering new obligations, consult with agencies which may be affected

by the imposition of compliance obligations, to ensure the effect of this

compliance is understood.

2. Develop compliance approach

Develop compliance mechanism

Consider how the obligation will be imposed, to best suit the purpose of the

compliance activities e.g. legislation, Commissioner’s Instruction, Commissioner’s

circular, Treasurer’s Instructions (TI) and why.

Consider whether there are similar compliance instruments already in place and if

so, whether they should be rescinded, reviewed or modified.

Consider whether the obligation needs to apply to all agencies, regardless of size.

Ensure that the obligation is very clearly defined and the scope of any reporting

process is very clear.

Ensure that any desired flexibility in the application of the obligation is clearly

described.

Consider the timing of compliance obligations already in place when setting

timeframes/deadlines for complying agencies to meet, to try to even out the

overall compliance load.

Consider evaluation and review mechanisms and plan their implementation.

Publish review dates in compliance instruments.

Reviewing compliance obligations A good practice approach 22

Consider whether the compliance obligation should have a defined life, i.e.

whether a sunset clause is appropriate.

Especially for high impact and high cost obligations, consider trialing the

obligation in a small number of agencies or circumstances, to ensure the

methodology is appropriate before rolling out more broadly.

Consult

Consult with complying agencies, to understand the impact of the compliance

obligation on them. This creates a greater level of understanding of the

requirement and greater likelihood of accuracy in the information provided.

Seek feedback on current and proposed information collection methodologies

and systems, to see if they are manageable and to enable efficient and effective

methods to be designed, such as cross sector IT platforms or templates. Where

possible seek a methodology for provision of the compliance information which is

a ‘by-product’ of normal business transactions, rather than an additional

workload.

Be prepared to adjust the proposed approach and methodology if consultation

identifies significant barriers to efficiency and effectiveness.

3. Implement a compliance obligation

Define and create awareness

Ensure that complying agencies are aware of the obligation, for example through

communicating with CEOs and compliance officers.

Clearly explain the purpose and scope of the obligation, and clarify the activities

and the level of detail required to comply and to report.

Build capacity

Take responsibility, together with complying agencies, for improving

organisational and sector capability in the activities necessary to achieve

compliance.

Create systems which facilitate reporting, including automated templates for data

input and quality checking.

As appropriate, support agencies to comply by providing relevant information and

guidelines on your website, as well as advice on an ongoing basis.

4. Monitor compliance

Ensure compliance obligations are met

Maintain effective systems and processes for receiving the information provided

by complying agencies.

Reviewing compliance obligations A good practice approach 23

Monitor compliance rates and the quality of information provided, through review

and audit as appropriate.

Provide individual feedback and support to agencies which are having difficulty in

complying, to enable them to improve compliance.

Analyse and utilise the information for the purpose it was collected.

Publish information and analysis in a timely manner, in accordance with legislative

requirements and the objectives of the compliance obligation.

Act on non-compliance

Based on a risk management approach, follow up as appropriate with agencies

which don’t comply.

Enact consequences, if any, for non-compliance.

Consider the reasons for non-compliance and where appropriate make

improvements to systems and build capacity to enhance future compliance.

5. Regularly review compliance obligations

Undertake regular review of the obligation to ensure it fulfils the public interest

objectives originally intended and to ascertain its relevance, considering the

principles relating to purpose (need, cost, benefit) and implementation

(technology, approach, use).

When reviewing current obligations, consult with complying agencies, to

understand its effect and consider alternative approaches.

Collaborate with other agencies as appropriate about compliance obligations and

processes, in order to consolidate and streamline obligations where there are

synergies or overlapping responsibilities.

Reviewing compliance obligations A good practice approach 24

A good practice approach- complying agencies

Accountability and transparency in the management and operation of organisations are

fundamental aspects of public sector governance. The responsibilities of CEOs as

outlined in s.29 of the PSM Act and other legislation and instruments (e.g. employment

contracts, job descriptions, performance agreements), reflect this need for accountability

and transparency.

While it is accepted that compliance reporting can create an administrative burden for

agencies, compliance systems play a strong role in facilitating good governance within

the agency.

In meeting compliance obligations in an efficient and effective manner, CEOs consider

issues in relation to five key areas of activity:

1. Prepare systems and staff

Consider the nature of the compliance obligation and clarify any uncertainty

around definition or scope which may arise for the agency.

Consider the nature and scope of any agency programs required to fulfil the

compliance obligation, including systems for collecting data and information.

Develop programs and data collection systems appropriate to the compliance task

and assign responsibility for these.

Train and build capability within the agency in relation to these programs, systems

and processes.

Raise awareness of the importance of compliance activities and how they

contribute to good governance.

Build skills and knowledge in governance systems and processes which

contribute to meeting compliance and reporting obligations.

1. Prepare

2. Implement

3. Report 4. Utilise

information

5. Review

Reviewing compliance obligations A good practice approach 25

2. Implement programs, collect data and information

Adopt a systematic approach to planning for and meeting compliance obligations,

and assign responsibility for meeting each relevant obligation.

At appropriate times undertake activities and collect information consistent with

the intent and stated outcomes of the obligation, utilising efficient and effective

methods for data collection.

Monitor data systems and quality of information collection on an ongoing basis.

Clarify any issues as necessary with the responsible agency.

3. Report

Ensure compliance obligations are met within specified timeframes and in the

manner required, to facilitate aggregation and understanding of information

collected.

Utilise the most efficient methods for providing information.

4. Utilise information

Where possible and efficient, ensure information collected through compliance

activities is comprehensively utilised, for example by corporate and senior

executive to enable continuous improvement for management, evaluation,

planning and reporting purposes.

More broadly, promote a culture of continuous improvement and opportunities for

performance excellence which flow from evaluation and compliance activities.

If not routinely provided, proactively seek from the responsible agency cross

sector information and data to use for agency planning and management.

5. Review system and process

As appropriate, monitor compliance quality and timeliness through audit and

quality assurance programs.

Review methods for data collection from time to time to ensure they are efficient

and effective.

Seek information from the responsible agency, such as cross sector comparisons

and benchmarking data, to supplement agency data and information.

Work with the responsible agency to improve systems and processes.

Ensure that compliance systems don’t expand beyond what is required to

effectively comply, i.e. avoid layering compliance obligations with inefficient

additional self-imposed compliance processes.

Reviewing compliance obligations Glossary 26

Glossary

Further information is provided below on the following terms used within this report.

Term Explanation

Commissioner’s

Circulars

Commissioner’s Circulars are issued by the Public Sector

Commissioner in carrying out his/her functions under s. 21A

of the Public Sector Management Act 1994 (PSM Act). They

communicate public sector management policy or

arrangements to promote and improve the overall

effectiveness and efficiency of the public sector or

mandatory compliance obligations that do not originate from

the Commissioner’s functions or the PSM Act.

Commissioner’s Circulars are found on the website of the

Public Sector Commission.

Commissioner’s

Instructions

Commissioner’s Instructions (CIs) are issued by the Public

Sector Commissioner under s. 22A of the PSM Act to

provide directions to public sector bodies and/or employees

on matters relating to the Commissioner’s functions or the

application of the PSM Act. The Commissioner may grant

an exemption or variation from a CI in exceptional

circumstances, such as where an agency can demonstrate

that compliance would significantly impact on service

delivery and the situation is unable to be addressed by the

agency through planning or appropriate management. CIs

are found on the website of the Public Sector Commission.

Complying

agency

A term used within this report to refer to those agencies

which are required to comply with compliance and reporting

requirements established and managed by ‘responsible

agencies.’

Reviewing compliance obligations Glossary 27

Term Explanation

Guidelines A statement which offers advice on the implementation of a

policy (Macquarie Dictionary). Guidelines usually provide

information and guidance about processes which support

and assist with policy implementation. Unless specifically

stated, guidelines have lesser force (consequences for non-

compliance) than an instruction or policy.

Legislated

compliance

obligations

Compliance obligations can be enshrined in legislation and

subsidiary legislation, such as regulations and some

codes. An example of these is the requirement under s. 19

of the State Records Act 2000 (the SR Act) for agencies to

prepare a recordkeeping plan and submit it to the State

Records Commission (the SR Commission) for approval.

In accordance with s. 61 of the SR Act, the SR

Commission’s gazetted Standards have the same force of

law as regulations.

Under s. 21(7) and (9) of the PSM Act the public sector

standards in human resource management and the Public

Sector Code of Ethics are considered to be regulations and

also have the force of law.

Opportunity cost (From economics) The value of a benefit forgone in the

process of adopting an alternative policy, course of action,

etc., which can be taken to be a cost of the alternative

adopted. (Macquarie Dictionary).

Policy A course or line of action adopted and pursued by a

government… (Macquarie Dictionary). Policies can apply

at whole of government and whole of sector level, or to

specific agencies or parts of the sector.

Premier’s

Circulars

Premier’s Circulars are issued by the Premier in his

capacity as the head of the Executive Government of

Western Australia, and are used to communicate matters

of whole of government policy and issues of strategic

importance to the State. There are situations where a

specific public sector entity may be exempt from a

particular Premier’s Circular, such as where the Premier’s

Circular details a specific process by which public sector

entities can seek an exemption from compliance. Premier’s

Circulars are found on the website of the Department of

the Premier and Cabinet.

Reviewing compliance obligations Glossary 28

Term Explanation

Responsible

agency

A term used within this report to refer to those agencies

which institute compliance and reporting requirements,

with which ‘complying agencies’ must comply. There are

only a few ‘responsible agencies.’ In the main they are

within the group of agencies known as ‘central agencies’,

such as the Department of Treasury, Department of the

Premier and Cabinet, or ‘oversight agencies’, such as the

Public Sector Commission or the Information

Commissioner.

Treasurer’s

Instructions

TIs are issued by the Treasurer in accordance with s. 78 of

the Financial Management Act 2006 (FM Act) in relation to

matters of financial administration. The TIs prescribe

requirements at a minimum level on such matters as

accounting for revenue, expenditure and property, the

standards of reporting and such other matters necessary to

achieve the objects and purposes of the FM Act. They

contain sufficient flexibility to be applied to agencies of all

sizes and scope, from centrally funded departments to

those statutory authorities that operate in a commercial

environment. To enhance organisational flexibility without

prejudicing the level of accountability, the requirements of

the TIs are expressed in terms of control objectives rather

than prescribing the techniques or procedures to be

employed. They have the force of law and therefore must

be observed by all agencies to which they apply. In

accordance with TI 104 (Exemptions), the Treasurer may

grant exemptions from the requirements of TIs where

he/she considers it warranted. TIs are found on the

website of the Department of Treasury.

Reviewing compliance obligations Appendix A 29

Appendix A

Review of compliance obligations

During consultation with responsible agencies about the good practice principles and the role of responsible agencies, the following

selected compliance obligations were considered. It is noted that these range in scope from simple reporting of information to large

agency - wide programs and so responsible agency systems are proportionate to the scope of the obligation.

The table includes a brief overview of the obligation; initiatives and programs within the responsible agency to facilitate efficient and

effective compliance; current and proposed initiatives to review and streamline compliance obligations; and good practice observed

in complying agencies. Responsible agencies are listed in alphabetical order.

Reviewing compliance obligations Appendix A 30

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Department of Finance (Finance) –

Regulatory Gatekeeping Unit (RGU)

The regulatory development process in

Western Australia requires compliance

with the Regulatory Impact Assessment

(RIA) program. RIA drives better

regulatory outcomes for the benefit of

business, consumers and government by

ensuring complying agencies meet best

practice principles for policy

development.

The RGU administers the RIA program

and helps agencies achieve better

outcomes by guiding them through the

RIA requirements and providing

regulatory design advice.

The compliance obligations apply in

particular circumstances and, where

relevant, require agencies to complete a

Preliminary Impact Assessment and a

Regulatory Impact Statement.

The RGU offers training and support to

agencies in complying with the RIA

program.

The support and service provided to

agencies include:

- Web based forms and

assistance through Factsheets

and Guidelines.

- Tailored and customised

training sessions provided on

an as-needs basis to guide

agencies through their RIA

obligations.

- Efficient service with a

commitment to respond to any

queries or submissions from

agencies within ten business

days.

- A biannual Regulatory Impact

Assessment Working Group

(RIAWG) forum with guest

speakers and opportunities to

workshop improvement

proposals.

The RGU also undertake training and

staff development opportunities to

ensure staff knowledge is kept up to

date.

The RGU is currently reviewing its RIA

program to improve the process,

provide better service, enhance

accountability and transparency, and

build capabilities across complying

agencies.

One aspect of this improvement

initiative is streamlining the Preliminary

Impact Assessment (PIA) stage of

analysis. This involves introducing

agency self-assessment of exception

categories, removing the PIA

requirement for proposals that satisfy

an exception category, and reworking

the PIA template to make it more

succinct and effective at eliciting

meaningful, relevant information.

Other improvement initiatives include

updated Guidelines, new Guidance

Notes and Fact Sheets, and a formal

roll-out of RIA training workshops to

assist agencies with their compliance

obligations.

Finance is also consulting with agencies

across government on a plan to

reinvigorate regulatory reform.

The RIA program helps agencies

achieve best practice in policy

development. It does not impose any

additional burden on those agencies

already compliant with best practice.

Good processes practiced by complying

agencies include:

Ensuring there is a regulatory

champion within the agency.

The regulatory champion

attends RIAWG forums and

engages in regular contact

with the RGU to maintain an

ongoing partnership.

Early engagement with the

RGU to ensure RIA can guide

the policy development

process.

A careful consideration of at

least three alternative options,

other than regulation, when

developing policy.

An attempt by the agencies to

compare the costs of

implementation and

compliance to the regulations

to the benefits of the regulatory

outcomes.

Effective consultation with

relevant stakeholders.

Reviewing compliance obligations Appendix A 31

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Department of Finance (Finance) -

Economic Reform

The economic reform process requires

compliance with the Regulatory Impact

Assessment (RIA) process, designed to

steer agencies through best regulatory

practice.

Training opportunities and regular

economics lectures ensure staff

knowledge is kept up to date.

Finance offers training and support to

agencies engaging in the RIA process,

including a quarterly forum with guest

speakers and opportunities to workshop

improvement proposals.

Finance is currently revising its process

of preliminary impact assessment, to

increase early detection of legislative

changes suitable for exemption.

Finance is also completing a mini cost

benefit analysis on the savings

available from this process

improvement.

Finance is currently consulting with

agencies across government on a plan

to reinvigorate regulatory reform.

Agencies which are already pursuing a

reform agenda would perceive there to

be little compliance burden.

Where agencies consider options and

apply cost benefit analysis to their

regulation, they gather the information

required for a regulatory impact

statement and thus compliance

reporting represents a limited burden.

Department of Finance

- Building Management and Works

The Who Buys What & How (WBW&H)

report provides a snapshot of WA

Government expenditure.

The report and associated data is used

to provide Government agencies with

information for contracting analysis,

reporting purposes and ministerial

enquiries. It also provides suppliers,

industry commentators or consultants

with information about government

expenditure.

On request from Finance, agencies must

provide information for the compilation of

the WBW&H and Buy Local reports.

Finance has made improvements to

data systems, allowing ease of analysis

and reporting across various criteria.

Tenders WA has been modified to

capture additional information, providing

Finance with an opportunity to use this

system as a primary source of

information and reducing the onus on

agencies to provide data.

The current WBW&H report replaced

several previous large and detailed

reports.

Recent improvements to Buy Local

reporting include reducing data

collection activities within agencies and

making reporting less onerous

(summary form only).

Agency Expenditure reporting has been

streamlined through the provision of a

tool kit, guides and templates.

Finance has now upgraded its

procurement systems for expenditure

mapping.

Other modifications to Tenders WA are

under consideration to capture data in

relation to major government initiatives.

Agency Expenditure – some agencies

have created their own mapping tables

within their chart of accounts or

reporting systems, allowing for ease of

reporting expenditure.

Agency Expenditure - A number of

agencies ensure that miscellaneous

general ledger accounts are rarely used

internally, as this may require a

considerable amount of time analysing

expenditure and mapping.

Buy Local information is now sourced

from Tenders WA by Finance, which

provides a draft report to agencies for

verification. A number of agencies

ensure that contract information is up to

date to avoid delays caused by having

to enter missing contract data into

Tenders WA.

Reviewing compliance obligations Appendix A 32

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Department of Finance- Government

Procurement: General government

agencies are required to submit a 10

Year Strategic Office Accommodation

Plan (SOAP) to Finance by 31 October

each year. This contains information

about agencies’ current and future office

accommodation requirements which is

then used to conduct analysis and

planning at a portfolio level and identify

across government opportunities to

deliver better office accommodation

solutions (service delivery needs, cost

savings and value-for-money for

government).

Finance provides each agency with a

pre-populated template for completion.

A final report is then generated and

returned to the agency for review and

sign-off.

The provision of the pre-populated

template is a significant assistance to

agencies.

Since the system improvements the

responses from agencies in 2014 have

been more timely and the collection of

information from agencies is being

completed in a much shorter period

than in previous years. In turn this

means that the value of the information

provided is retained.

Finance has improved the system and

database supporting the generation of

the template and the final reports to

improve timeliness and accuracy.

Finance meets with agencies with large

or complex portfolios to assist in the

completion of the template and provides

assistance to others on request.

Each year Finance considers feedback

from agencies about the process and

ways it could be improved.

Future initiatives planned include

regular update/refresh of the SOAP

information into the regular meetings

already held with the larger agencies;

further streamlining of information and

creation of the templates and reports;

and consideration of reduced reporting

for smaller agencies with less volatile

property portfolios.

Some agencies use the SOAP template

to manage their property portfolio, and

others use it to inform their internal

management processes or to inform

their budget submissions.

Those agencies with larger, more

complex portfolios tend to have internal

expertise and capacity. Finance

consults with these agencies about how

this process could add value to their

business operations.

Reviewing compliance obligations Appendix A 33

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Department of the Premier and

Cabinet (DPC)

Reporting of travel

Under Premier’s Circular 2014/02 the

Government requires the public sector to

exercise the strictest economy and

accountability in relation to publicly

funded air travel.

Ministers, Parliamentary Secretaries,

DG/CEO must adhere to Guidelines.

Premier’s Circulars are reviewed every

two years for relevance and are

rescinded as required.

Travel Proposal and Quarterly Return

for Overseas Travel Forms are provided

for departments and agencies to

complete the required information.

A recent removal of the requirement for

interstate travel to be reported has

significantly reduced the reporting effort.

As this requirement has been in place

for some time and involves reporting of

straightforward information, the

requirement is well understood by

agencies.

Department of the Premier and

Cabinet (DPC)

Government Advertising and

Communications Policy (GACP)

Under Premier’s Circular 2014/03, all

public sector agencies other than

Schedule 1 PSM Act agencies must

comply with the GACP and Guidelines.

All campaign advertising must be

approved by DPC.

Premier’s Circulars are reviewed every

two years for relevance and are

rescinded as required.

DPC provides an application form for

departments and agencies to complete.

DPC recently reviewed the policy and

reduced sic separate policies down to

one. Approvals by DPC for non-

campaign advertising are no longer

required.

Only submissions with a value greater

than $40 000 are required to be referred

to the Independent Communications

and Review Committee for approval.

The revised policy and guidelines

clearly define agency responsibilities

and initial feedback from agencies is

that the revised policy, guidelines and

processes will assist agencies to more

easily meet their obligations under this

Circular.

Reviewing compliance obligations Appendix A 34

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Department of the Premier and

Cabinet (DPC)

Reporting on use of consultants

Under Premier’s Circular 2005/08

departments and agencies are to

prepare and submit details of all

consultants engaged on contracts for

services on a six monthly basis.

Ministerial Offices are required to collate

returns from government departments

and agencies and submit these to DPC

within eight weeks of the end of each six

month period.

Premier’s Circulars are reviewed every

two years for relevance and are

rescinded as required.

DPC provides a form to assist

departments and agencies to provide

the required information.

The circular is under review. As this requirement has been in place

for some time and involves reporting of

straightforward information, the

requirement is well understood by

agencies.

Reviewing compliance obligations Appendix A 35

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Disability Services Commission (DSC)

Public sector and local government

agencies have a number of obligations

under the Disability Services Act 1993.

These include the requirement to

develop and implement a Disability

Access and Inclusion Plan (DAIP), to

report annually to the Disability Services

Commission (DSC) on the agency’s

progress in implementing the DAIP, as

well as in their own annual report and to

review the DAIP at least every five years.

Each year DSC aggregates the

information provided by public sector

agencies into an annual report for the

Minister.

This report provides an overview of

public sector progress in implementing

strategies to ensure equal access to

services for people with a disability.

DSC utilises a number of methods to

improve understanding of and build

capability within agencies about the

DAIP program, such as ‘google groups’

(networking forums) for both local

government authorities and public

sector agencies, which are run in

person or through teleconferencing and

provide an opportunity for information

sharing and presentations by good

practice agencies. DSC also provides

regular emails to DAIP officers to

provide information and share examples

of best practice. Templates are

provided as far as possible to facilitate

reporting.

DSC commenced a project in mid-2014

to review the reporting obligations for

agencies.

Current initiatives being progressed by

DSC include encouraging links between

procurement and DAIP officers to

ensure that information about DAIP

requirements is made known to

contractors through the contract

process

While this compliance obligation is

generally well understood, DSC plans to

further streamline reporting on the DAIP

through the following:

considering enhancements to ICT

applications to enable agencies to

report on the strategies within their

DAIP throughout the year, rather

than at a fixed time

providing a longer window for

specific annual reporting

exploring ways to streamline

reporting back to agencies

enhancing the information

contained in the Annual Reporting

Framework.

Some good practice agencies provide

information on their systems and

process more broadly across the public

sector.

Reviewing compliance obligations Appendix A 36

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Public Sector Commission

(Commission) - Human Resource

Minimum Obligatory Information

Requirement (HRMOIR)

The HRMOIR process was developed to

ensure that government has access to

information required for the strategic

management of the Western Australian

public sector workforce and for reporting

to Parliament. It was previously

implemented by a Premier’s Circular and

is now implemented by Commissioner’s

Instruction No.6.

Every quarter, all public sector employing

authorities extract data from their human

resource management information

system (HRMIS) and submit it to the

Commission via an online collection tool.

Agencies are required to follow the data

definitions issued by the Commission.

The Commission then checks, analyses,

and prepares the data which will then be

used to inform workforce reports, answer

Parliamentary Questions, media

enquiries, and other regular or ad hoc

queries from agencies and the public.

The Commission assists agencies to

ensure accuracy of data through

undertaking extensive quality assurance

processes in conjunction with agencies;

providing templates for small agencies

which do not have HR information

systems; and responding to queries

from agencies. Over a number of years

there has been a focus on improving

and ensuring data quality through

developing validation steps and tools.

These are recognised as good practice

by other jurisdictions in Australia.

The ANZSCO coding guide was written

to help agencies better understand how

the Australia and New Zealand

Standard Classification of Occupations

(ANZSCO) codes are determined,

especially codes which can cause data

quality issues.

The Quarterly Entity Profile report was

developed to provide agencies with a

snapshot profile of their agency against

the public sector as a whole. This

allows agencies to make continuous

assessment of their own data and use

the information for workforce planning

and diversity reporting.

The Commission plans to maintain

focus on continuous improvement,

including a focus on methods to

improve data quality, for example,

working with HRMIS providers and

agencies; and ways in which duplication

of data collection in the HRMIS of some

agencies and HRMOIR can be

minimised.

The Commission is also considering

how it might better promote use of the

HRMOIR data by agencies, for

example, for strategic workforce

planning purposes, as the information

enables comparability between the

agency and the public sector, and some

cross jurisdictional comparison with

other states or like organisations in

other states.

A number of agencies have taken the

initiative in ensuring accuracy of data by

utilising the Commission’s data quality

assessment mechanism prior to

submitting their quarterly report, thus

minimising the need for follow up.

A small number of agencies actively

request and utilise data for workforce

planning purposes.

Some agencies proactively seek

systems solutions by making changes

to their HRMIS to ensure a faster and

more efficient data collection process.

In addition, cross collaboration occurs

among agencies to identify and address

issues to minimise duplication and

maximise knowledge base.

Reviewing compliance obligations Appendix A 37

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Public Sector Commission- Reporting

costs of producing the annual report

There has been a requirement for some

years for agencies to report the cost of

producing their annual report (AR). Prior

to 2011 reporting was to the relevant

Minister and since 2011 to the Public

Sector Commissioner by way of

Commissioner’s Circular 2013/01.

The intent of the requirement is to

discourage excessive costs in the

production of ARs. Information to be

reported includes details of the number

of hard copies printed; printing costs;

cost of staff time; and costs of

consultants/external resources.

The information provided by agencies is

reviewed by the Commission. Any issues

identified are discussed with the agency

concerned.

The Commission supports this

obligation by providing in the Annual

Reporting Framework (ARF) guidance

on the need for constraining costs in AR

production. The ARF is produced

annually by the Commission and

outlines and references the information

to be included in an AR.

In recent years the Commission has

analysed the data provided by agencies

and reviewed the process for providing

it. This has resulted in clarification of the

reporting requirement and provision of a

template in the ARF to facilitate and

simplify reporting.

Over time ARs have moved from being

largely hard copy, printed documents to

being online. This may have had the

effect of reducing total costs. Feedback

to the Commission indicates this

requirement is seen to have limited

value to the complying agencies.

For the above reasons, consideration

will be given to whether annual costs

should continue to be reported to the

Commission in the current format or

whether there may be other means by

which some or all of this information can

be collected and reported.

This requirement involves the provision

of information once a year, so there is

limited need for systems and processes

to manage this requirement.

Reviewing compliance obligations Appendix A 38

Overview of obligation Good practice in responsible agency Current improvement initiatives Good practice in complying agencies

Public Sector Commission: Public

Sector Entity Survey (PSES)

Under s.22D of the PSM Act the Public

Sector Commissioner must report to

Parliament each year on the state of

administration and management of the

public sector and the compliance and