P2Binvestor Small Business Webinar Series Presented by R.P. Burrasca ColoradoCrowdfunding.org Facilitated by Krista Morgan CEO, P2Binvestor P2Bi.com February 13, 2015 Public and Private Offerings Under the JOBS Act

Public and Private Offerings Under the JOBS Act

Jul 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

P2Binvestor Small BusinessWebinar Series

Presented by R.P. BurrascaColoradoCrowdfunding.org

Facilitated by Krista MorganCEO, P2Binvestor

P2Bi.com

February 13, 2015

Public and Private Offerings Under the

JOBS Act

2

Presenter Info: R.P. BurrascaManaging Director, Windom Peaks Capital, LLC; Founder & Organizer of Colorado Crowdfunding Ray Burrasca is a seasoned company finance professional and experienced corporate lawyer with over 40+ years experience in corporate finance, securities compliance and transactional law. He has practiced finance and corporate law both in privately-held and publicly-traded corporations, and has practiced on Wall Street and in Silicon Valley.

He previously served as the chief financial officer of $500 million dollar pulp & paper company located in Maine as well as CFO of a startup game-development company previously located in Colorado.

His experience includes all facets of corporate finance and private equity, including, among others:

Registered and private securities offerings (including IPOs) Private and public mergers & acquisitions Leveraged buyouts (including management-led, hostile and “vulture”

fund driven) Mezzanine lending, venture capital, and startups Hedging & corporate debt swaps and hedge funds Derivative securities

3

Jumpstart Our Business Startups ActPrimarily designed to increase American job

creation and economic growth by improving access to the public capital markets for emerging growth companies

Seven Titles, including “IPO On Ramp” for emerging growth companiesAllowing public solicitation in certain private

offeringsCrowdfundingIncreasing dollar limits for Regulation AIncreasing thresholds for ‘34 Act registration

4

JOBS Act & TimingSigned into law April 5, 2012Many provisions are self-executing

Facilitating IPOs for emerging growth companies (EGCs)

Relaxing reporting requirements for EGCsPublic Company Registration Thresholds

Many require SEC rulemaking:Private offerings legalized September 23, 2013Study on Blue Sky Laws impact on Regulation A –

Accomplished - Proposed regulations issuedCrowdfunding originally due by December 31,

2012Regulation A+ - Proposed Regulations issued

5

What is an Emerging Growth Company?An EGC is a company with gross annual revenues

of less than $1 billionA company remains an EGC until the earliest of:

Gross revenues of $1 billion or moreFifth anniversary of its IPOIssuance of $1 billion in non-convertible debt

during the previous three yearsPublic float is $700 million or more

A company does not qualify as an EGC if it conducted its IPO on or before December 8, 2011

6

Reporting and Other Requirements Reduced for EGCs Two years (not three years) of audited financial

statements in IPO registration statementExempt from certain proxy rules

"say-on-pay" shareholder vote shareholder vote on golden parachute

compensationCertain executive comp. disclosures

Exempt from the auditor attestation requirements with respect to internal controls

Permitted to delay application of new public company financial accounting standards until they become mandatory for private companies

7

Communications Prior to and During a Securities OfferingEGCs can “test the waters”

Can communicate with qualified institutional buyers (QIBs) and institutional accredited investors (“IAIs”) before and after the filing of registration statement

Includes communications by underwritersOral and written communications to QIBs and

IAIs remain subject to potential liability under Section 12 of the Securities Act for any material misstatement or omission

8

Confidential Submission of IPO Registration Statements Permitted to submit any IPO registration statement

and subsequent amendments confidentially IPO registration statement and amendments

required to be publicly filed with the SEC no later than 21 days before a road show If an EGC submits its IPO registration statement

to the SEC confidentially, management of the EGC may be limited in its ability to communicate with QIBs and IAIs to gauge their interest in the potential offering for 21day quiet period

9

Analyst Research Reports

Publication of research on EGCs by Investment Banks is not considered an offer or a prospectus, even if the bank is participating or will participate in the offeringApplies to equity offerings including IPOsReports no longer subject to liability under

Section 12 of the Securities Act for material misstatements or omissions

Still subject to other securities law liability Neither the SEC nor FINRA may adopt or maintain

quiet periods for equity research reports for EGCs

10

Research Analysts’ Communications and MeetingsProhibits the SEC and FINRA from adopting or

maintaining rules or regulations in connection with an IPO of an EGC that restrict:who at a broker-dealer may arrange for

communication between a securities analyst and a potential investor

participation of a securities analyst in meetings with management, even if investment bankers are present

11

Private Offering ExemptionsElimination of prohibition against general solicitation

and general advertising in Rule 506 OfferingsSEC amended Rule 506 in July of 2013 – General

solicitation and advertising now legal for accredited investor offerings

Requires that all purchasers be accredited investorsIssuer using public solicitation must take reasonable

steps to verify that the purchasers are accredited using methods determined by the SEC

SEC revised Rule 144A to allow general solicitation and general advertisingSeller and any person acting on behalf of the seller

must reasonably believe the buyer is a QIB

12

Private Offering ExemptionsOnly available to U.S. organized issuersMay be available to private funds

New Section 4(b) of 33 Act now provides that general advertising or general solicitation Not deemed public offering under Federal securities

laws Funds set up under 3(c)(1) and 3(c)(7) of Investment

Company Act may now use general solicitation and advertising (Caveat: May not be available to commodity pools)

Not available to:Registered investment companies;Issuers already subject to reporting requirements; andIssuers with “bad actors”

13

Rule 506 IntermediariesRule 506 Intermediary is not subject to broker-dealer

registration solely because that person:Maintains a platform or mechanism that permits

the offer, sale, purchase, negotiation, general solicitation, advertisements, or similar activities in connection with the offering;

Co-invests in the securities being offered; orProvides ancillary services in connection with the

offeringState law is not pre-empted for 506 Intermediaries

14

Rule 506 IntermediariesRule 506 Intermediary not registered as a broker

dealer must:Receive no compensation in connection with

the purchase or sale of securities in the offering (transaction based compensation);

Not be in possession of customer funds or securities in connection with the offering; and

Not be subject to a statutory disqualification under section 3(a)(39) of the Securities Act (No “Bad Actor”)

Equity Crowdfunding… the backstory Using “general solicitation” and “advertising” to promote the funding of

businesses online wasn’t legal in the U.S. for accredited-investor or non-accredited investor investing until September 23, 2013

On September 23, 2013, “accredited investor crowdfunding” became legal

“Non-accredited crowdfunding” at the federal level is still not legal unless a registration statement for the crowdfunding has become effective (with the SEC) or there is an available exemption under both federal and state (Colorado) law.

While there are some available exemptions or mini-registration processes available under Colorado law, discussion of them is for another meeting … it is not a topic for this today’s presentation.

When accredited investor crowdfunding became legal last year, why didn’t we jump on the bandwagon at that time?

Okay, so if proposed changes in existing form and filing requirements were the reason for waiting, has that situation changed? Have the proposed changes been either finalized or withdrawn?

If not, then why have we decided to move forward with equity crowdfunding at this time? 15

Definition of “Accredited Investor”“Accredited investor” is defined by various

countries' securities laws and delineates investors who can invest in certain types of higher-risk investments including seed money, limited partnerships, hedge funds, private placements, and angel investor networks

In the U.S., an accredited investor is currently defined as Any natural person who had an individual income in excess of

$200,000 in each of the two most recent years or joint income with that person's spouse in excess of $300,000 in each of those years and has a reasonable expectation of reaching the same income level in the current year; or

Any natural person whose individual net worth, or joint net worth with that person's spouse, exceeds $1,000,000, excluding his or her primary residence

16

Definition of Accredited Investor is Required to be Updated under Dodd-Frank’s MandateTremendous controversy right now about the

proposed changes to the definitionAngel and VC communities are up in arms about

proposal – They claim that the revised definition (more than $450,000 on net income and more than $2.5 million on net worth) would drive 60% of the accredited investors out of the market.

Not clear if and when SEC will move on this issue, given the tremendous amount of kickback.

17

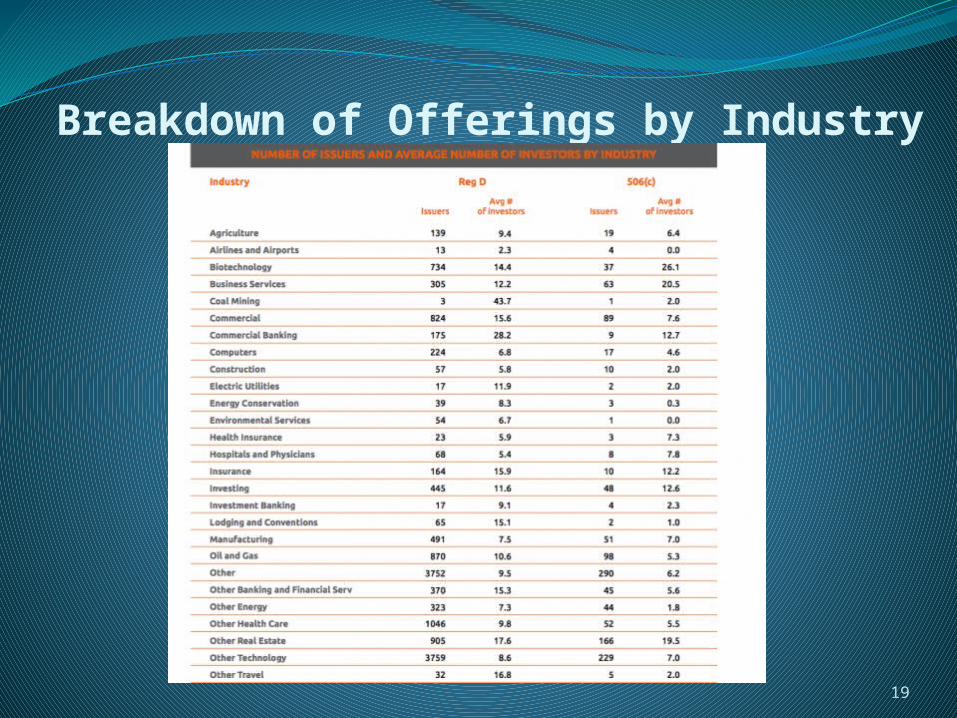

Definition Since Accredited Investor Crowdfunding Became LegalBetween September 23rd of 2013 and September

22nd of 2014, Form D’s, representing over $118 billion worth of offerings, were filed with the SEC under the new "accredited investor crowdfunding provisions" (Title II) of the JOBS Act, SEC Rule 506(c).

It now appears a substantial portion of these offerings involved offers to invest in companies.

18

Breakdown of Offerings by Industry

19

20

CrowdfundingCapital Raising Online While Deterring Fraud and

Unethical Non-Disclosure ActSmall offerings seeking small investments from

many investorsNew Section 4(6) of the Securities Act$1 million annual limit (debt or equity)Not effective until SEC rulemaking - Proposed

regs, 585 pages worth issued in October, 2013 --- Regs. Not yet final and no definitive date for when they will be.

21

SEC proposed rules honor statutory mandate:Investor with net worth or annual income of

$100,000 or greater may invest up to 10% of net worth or income, with a ceiling of $100,000

Investor with net worth or annual income of less than $100,000 are limited to greater of $2,000 or 5% of net worth or income

In all crowdfunding offerings, issuer must verify whether Investor has money in other crowdfunding investments

Crowdfunding

22

“Covered Securities” under Section of the Securities ActNot subject to state blue sky registration

requirementsStill subject to state anti-fraud enforcement

Securities remain restrictedMandatory one year holding period with certain

exceptions

Crowdfunding

23

Certain disclosures required depending on offeringLess than $100K - financials certified by CEO$100K-$500K - financials reviewed by CPAOver $500K - audited financials

Issuer not required to register under ‘34 ActStill must make annual SEC filings and

disclosures to investors as the SEC determines to be appropriate

Crowdfunding

24

Crowdfunding offerings must be conducted through a broker-dealer or through a “funding portal” that does not:Offer investment advice or recommendationsSolicit purchases, sales, or offers to buy the

securities offered or displayed on its website or portal

Compensate employees, agents, or other persons for such solicitation or based on the sale of securities displayed on its website or portal

Hold manage or possess, or otherwise handle investor funds or securities

Engage in such other activities as the SEC, by rule determines appropriate

Crowdfunding

25

Funding portal is required to:Register as a funding portal with the SECObtain membership in a national securities

association (FINRA)Obtain a background and securities regulatory

enforcement check for the directors, officers, and holders of more than 20% of the outstanding equity of the issuer

Meet any other requirements that the SEC, or FINRA as the regulator of Funding Portals, prescribes as appropriate

Crowdfunding

26

To prevent fraud by the issuer, the Broker-Dealer/Funding Portal must “ensure” that no offering proceeds are distributed to the issuer until the target offering amount is established

The offering may not be advertised except by directing the investors to the Broker-Dealer or Funding Portal

Broker-Dealer/Funding Portal must also make available to investors and the SEC, at least 21 days before any sale, any disclosures provided by the issuer

Crowdfunding

Federal – Title III – Non-Accredited Crowdfunding : What’s Up and Why Is It Taking So Long?

The Bad News About Non-Accredited Investor Crowdfunding: Title III of the JOBS Act

27

Two years after the deadline, final Title III Non-Accredited Investor Crowdfunding regulations have still not issued. Why?The SEC’s statutory mandate and the problem

caused by many “voices”SEC’s statutory mandate:

to protect investors; to maintain fair, orderly and efficient markets; to facilitate capital formation.

The many voices: Crowdfunding portals Venture capital, accredited investor groups, and

entrenched industry FINRA Investor Advisory Committee Recommendations under

Section 911 of the Dodd-Frank Act Investor protection groups – CFA, AARP, AFL-CIO, NASAA 28

Still no firm commitment as to when final regulations will issueMissed initial required issuance dateMissed promised (July, 2014) October 2014

month-end dateNow, indication that final regs won’t issue until

October 2015 month-end.

TRUTH: No one knows, and if the do know, they’re not telling

29

But, There’s Good News, Too ….

30

There is currently a bill in the house which would amend the JOBS Act to Solve some of the many problems raised by the original Title III of the JOBS Act and by the proposed regs under it …. JOBS Act, Version 2 – Startup Capital Modernization Act of 2014

Raises crowdfunding limits from $1 million to up to $5 million.

Allows self–certified financials for raises under $500,000 – and independently

reviewed financials statements for raises between $500,000 and $3 million –

leaving the more onerous audited financials for raises above $3 million.

Eliminates the requirement that the SEC promulgate rules requiring detailed,

registration statement-like non-financial disclosure resembling a public

company report.

Eliminates the need for ongoing annual reporting in perpetuity.

Allows non-broker-dealer intermediaries (funding portals) to register only with

the SEC, avoiding registration with FINRA and compliance with its rules.

Allows intermediaries which are not licensed broker-dealers to “curate”

crowdfunded transactions, screening out those not deemed suitable for their

portal.

Removes the more onerous liability provisions for intermediaries and issuers.

31

… Also, there’s legislation pending right now, here, in Colorado ….New bill has just been introduced by Representative

Pete Lee to allow non-accredited crowdfunding to occur in the state …

There are a lot of conditions …. But it is a true crowdfunding bill and, despite the many flaws in the concept behind it (my opinion), it could become a reality by mid-year and could allow for true non-accredited crowdfunding by early next year.

I posted a link to the proposed bill on the Colorado Crowdfunding meetup site if you’d like to take a look at it.

32

33

Regulation A+‘33Act registration exemption to be increased

from $5 million to $50 million raised in 12 monthsRequires SEC rulemaking – Proposed

regulations have been issuedOnly equity, debt and convertible debt

Securities may be publicly offered and will not be restricted

State law generally pre-empted SEC Rules will require certain annual filings and

investor disclosures

34

Increased Registration Threshold for Public Company ReportingNo requirement to register until company reaches

2000 shareholders (or 500 shareholders who are not accredited investors) “of record”Excludes record holders who receive the

securities pursuant to an employee compensation plan exempt from registration under Section 5 of the Securities Act

SEC must exempt securities held by crowdfunding investors

35

Thank you! Time for Q&AAny questions?

Contact Ray at [email protected]

Learn more about Colorado Crowdfundingat ColoradoCrowdfunding.org Still have questions? Contact us at [email protected] after the webinar.

Interested in P2Bi’s business financing, investor platform, or client referral program? Learn more at P2Bi.com or contact us at [email protected] or at (720) 361-1500.

Related Documents