Ptak prizeindia2014 SCNext_limesoda_NMIMS

Jul 12, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Team: Lime Soda

Team Members:Shamika Kulkarni

Gaurav KumarNirmal Chandrahas

College : NMIMS, Mumbai

There are some growth requirements that have to be fulfilled for e-commerce to truly take off they are as follows: The basic infrastructure must be in place, including logistics. Customers and businesses must have access to the Internet. Sites must have multiple language functions. The cost of Internet access must decrease. E-commerce must be safe in terms of privacy and monetary transactions. The speed of the technology must be satisfactory. International standards must develop.

At present e-commerce is pursued to a fairly high degree between companies, but is still not very developedbetween companies and private persons. The business-to-consumer (B2C) relation is expected to grow rapidlythough, and when this happens it will result in several changes for actors in the logistics area. When delivering toprivate persons instead of companies, the demand for fast and accurate deliveries will increase. This is becauseone or more of the physical nodes will disappear when the Customer Order point (COP) will be moved upwardsthe supply chain. Direct home deliveries will request shorter lead times, and more complex distribution systemswill be necessary to make this possible.

E-commerce will impact all elements in the supply chain, which rely on data flow to improve efficiency. Still,physical transportation is needed for most products, implying the usefulness of deriving e-commerce demands onlogistics by analysing the logistics customers. Demands on a smooth integration of these flows will increase inthe future, from being a competitive advantage to a necessity.

In the distribution chain we will see a number of new possibilities. There wont be one way to distribute ecommercegoods. In fact, even for one company, there will a number of ways. The distribution alternatives willbe different for different customers as well as for different categories of products. Which alternative thecompany (or actually the customer) will choose will be regarding to time limits and how much the customerwants to pay for the service. This means that a company will use more than one sales channel for, a customer, ifthe customer buys different products with different demands regarding e.g. time as well as for different articles.

Executive Summary

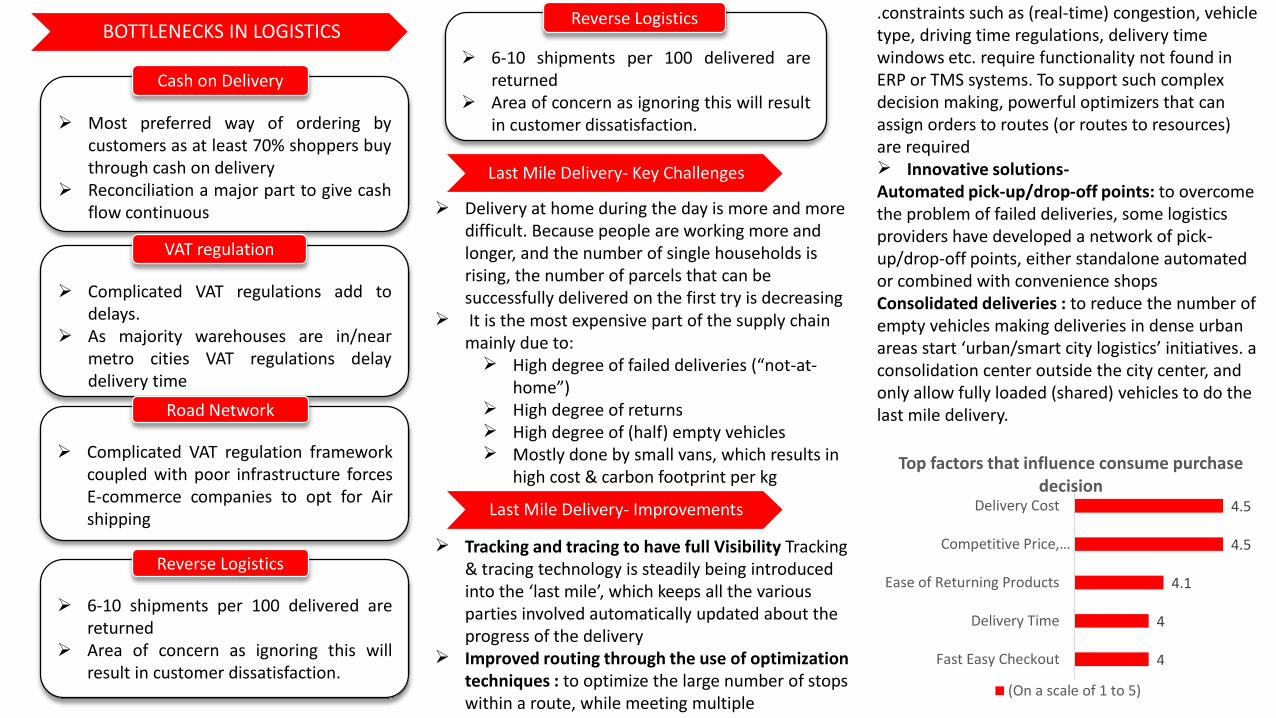

Most preferred way of ordering bycustomers as at least 70% shoppers buythrough cash on delivery

Reconciliation a major part to give cashflow continuous

Cash on Delivery

Complicated VAT regulations add todelays.

As majority warehouses are in/nearmetro cities VAT regulations delaydelivery time

VAT regulation

Complicated VAT regulation frameworkcoupled with poor infrastructure forcesE-commerce companies to opt for Airshipping

Road Network

6-10 shipments per 100 delivered arereturned

Area of concern as ignoring this willresult in customer dissatisfaction.

Reverse Logistics

6-10 shipments per 100 delivered arereturned

Area of concern as ignoring this will resultin customer dissatisfaction.

Reverse LogisticsBOTTLENECKS IN LOGISTICS

4

4

4.1

4.5

4.5

Fast Easy Checkout

Delivery Time

Ease of Returning Products

Competitive Price,…

Delivery Cost

Top factors that influence consume purchase decision

(On a scale of 1 to 5)

Last Mile Delivery- Key Challenges

Delivery at home during the day is more and more difficult. Because people are working more and longer, and the number of single households is rising, the number of parcels that can be successfully delivered on the first try is decreasing

It is the most expensive part of the supply chain mainly due to: High degree of failed deliveries (“not-at-

home”) High degree of returns High degree of (half) empty vehicles Mostly done by small vans, which results in

high cost & carbon footprint per kg

.constraints such as (real-time) congestion, vehicle type, driving time regulations, delivery time windows etc. require functionality not found in ERP or TMS systems. To support such complex decision making, powerful optimizers that can assign orders to routes (or routes to resources) are required Innovative solutions-Automated pick-up/drop-off points: to overcome the problem of failed deliveries, some logistics providers have developed a network of pick-up/drop-off points, either standalone automated or combined with convenience shops Consolidated deliveries : to reduce the number of empty vehicles making deliveries in dense urban areas start ‘urban/smart city logistics’ initiatives. a consolidation center outside the city center, and only allow fully loaded (shared) vehicles to do the last mile delivery.

Last Mile Delivery- Improvements

Tracking and tracing to have full Visibility Tracking & tracing technology is steadily being introduced into the ‘last mile’, which keeps all the various parties involved automatically updated about the progress of the delivery

Improved routing through the use of optimization techniques : to optimize the large number of stops within a route, while meeting multiple

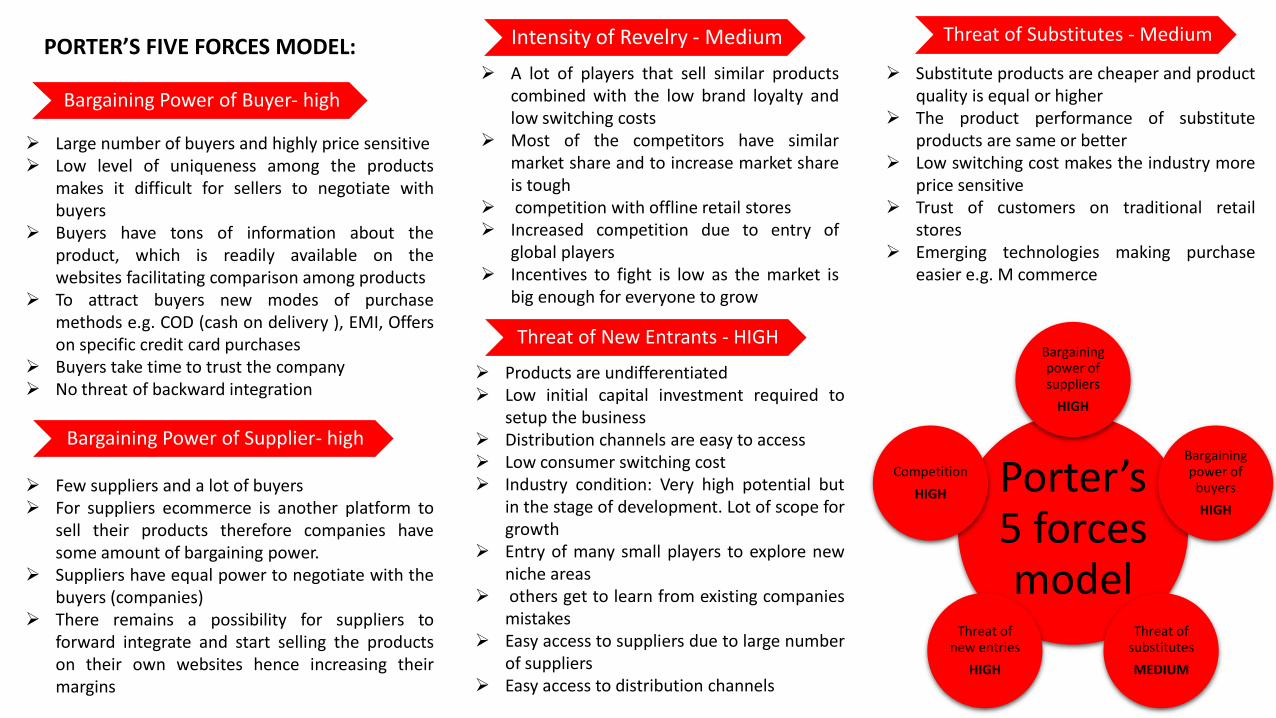

Intensity of Revelry - Medium

Bargaining Power of Buyer- high

Bargaining Power of Supplier- high

Large number of buyers and highly price sensitive Low level of uniqueness among the products

makes it difficult for sellers to negotiate withbuyers

Buyers have tons of information about theproduct, which is readily available on thewebsites facilitating comparison among products

To attract buyers new modes of purchasemethods e.g. COD (cash on delivery ), EMI, Offerson specific credit card purchases

Buyers take time to trust the company No threat of backward integration

Few suppliers and a lot of buyers For suppliers ecommerce is another platform to

sell their products therefore companies havesome amount of bargaining power.

Suppliers have equal power to negotiate with thebuyers (companies)

There remains a possibility for suppliers toforward integrate and start selling the productson their own websites hence increasing theirmargins

A lot of players that sell similar productscombined with the low brand loyalty andlow switching costs

Most of the competitors have similarmarket share and to increase market shareis tough

competition with offline retail stores Increased competition due to entry of

global players Incentives to fight is low as the market is

big enough for everyone to grow

Threat of New Entrants - HIGH

Products are undifferentiated Low initial capital investment required to

setup the business Distribution channels are easy to access Low consumer switching cost Industry condition: Very high potential but

in the stage of development. Lot of scope forgrowth

Entry of many small players to explore newniche areas

others get to learn from existing companiesmistakes

Easy access to suppliers due to large numberof suppliers

Easy access to distribution channels

Threat of Substitutes - Medium

Substitute products are cheaper and productquality is equal or higher

The product performance of substituteproducts are same or better

Low switching cost makes the industry moreprice sensitive

Trust of customers on traditional retailstores

Emerging technologies making purchaseeasier e.g. M commerce

Porter’s 5 forces model

Bargaining power of suppliers

HIGH

Bargaining power of

buyers

HIGH

Threat of substitutes

MEDIUM

Threat of new entries

HIGH

Competition

HIGH

PORTER’S FIVE FORCES MODEL:

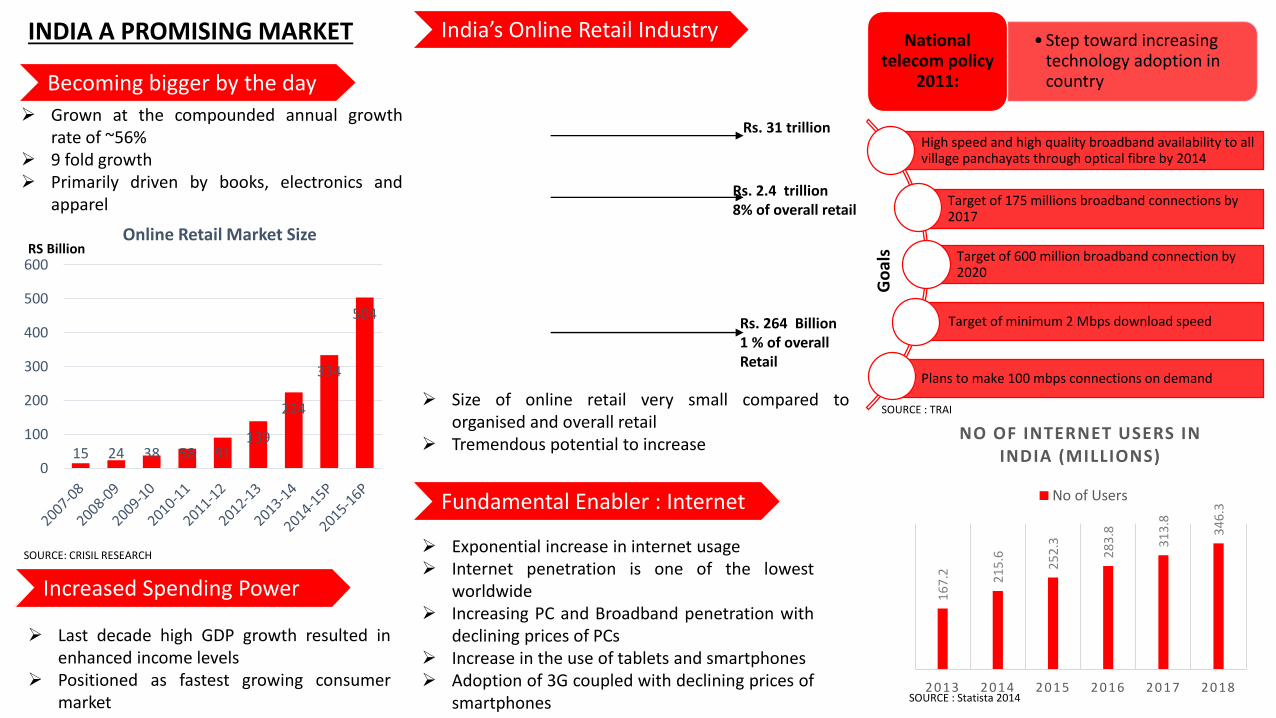

INDIA A PROMISING MARKET

Becoming bigger by the day

15 24 38 58 91139

224

334

504

0

100

200

300

400

500

600

Online Retail Market Size

SOURCE: CRISIL RESEARCH

RS Billion

Grown at the compounded annual growthrate of ~56%

9 fold growth Primarily driven by books, electronics and

apparel

India’s Online Retail Industry

Rs. 31 trillion

Rs. 2.4 trillion8% of overall retail

Rs. 264 Billion1 % of overall Retail

Size of online retail very small compared toorganised and overall retail

Tremendous potential to increase

Increased Spending Power

Last decade high GDP growth resulted inenhanced income levels

Positioned as fastest growing consumermarket

Fundamental Enabler : Internet

Exponential increase in internet usage Internet penetration is one of the lowest

worldwide Increasing PC and Broadband penetration with

declining prices of PCs Increase in the use of tablets and smartphones Adoption of 3G coupled with declining prices of

smartphones

16

7.2 21

5.6

25

2.3

28

3.8

31

3.8

34

6.3

2013 2014 2 0 1 5 2016 2017 2018

NO OF INTERNET USERS IN INDIA (MILLIONS)

No of Users

SOURCE : Statista 2014

• Step toward increasing technology adoption in country

National telecom policy

2011:

High speed and high quality broadband availability to all village panchayats through optical fibre by 2014

Target of 175 millions broadband connections by 2017

Target of 600 million broadband connection by 2020

Target of minimum 2 Mbps download speed

Plans to make 100 mbps connections on demand

Go

als

SOURCE : TRAI

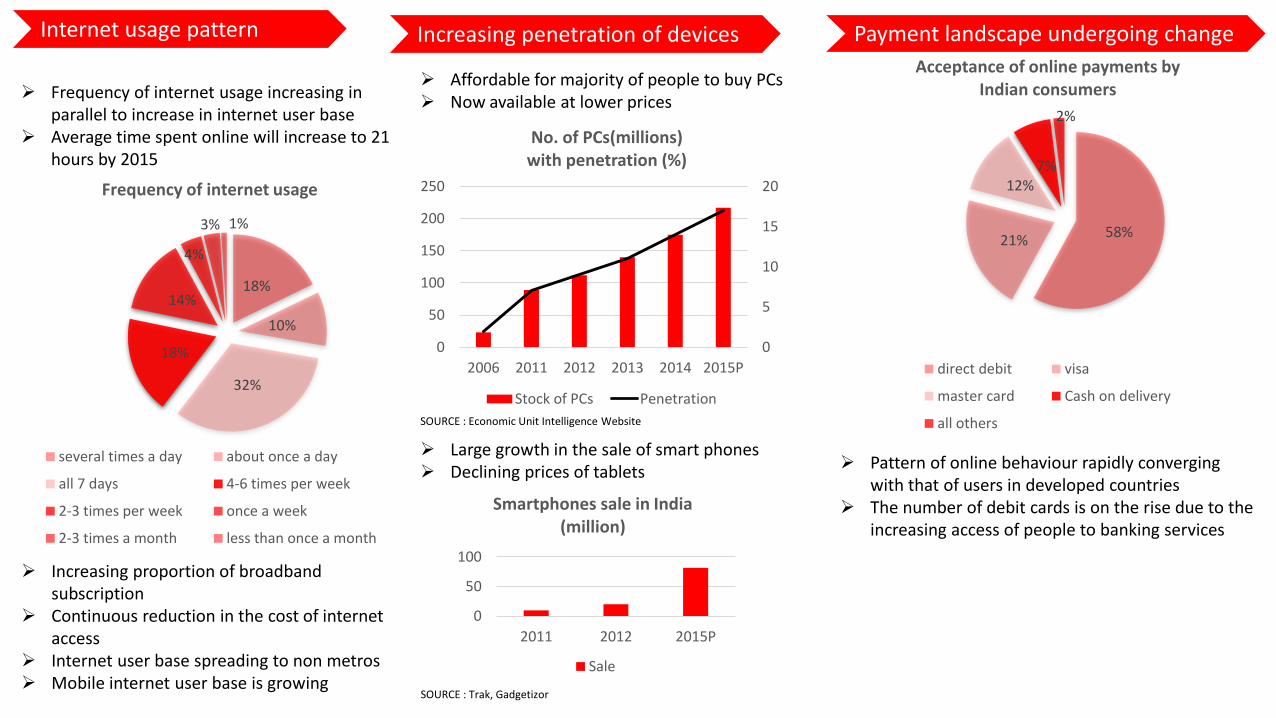

Increasing penetration of devices

Affordable for majority of people to buy PCs Now available at lower prices

0

5

10

15

20

0

50

100

150

200

250

2006 2011 2012 2013 2014 2015P

No. of PCs(millions) with penetration (%)

Stock of PCs Penetration

SOURCE : Economic Unit Intelligence Website

Large growth in the sale of smart phones Declining prices of tablets

0

50

100

2011 2012 2015P

Smartphones sale in India (million)

Sale

SOURCE : Trak, Gadgetizor

Frequency of internet usage increasing in parallel to increase in internet user base

Average time spent online will increase to 21 hours by 2015

18%

10%

32%

18%

14%

4%

3% 1%

Frequency of internet usage

several times a day about once a day

all 7 days 4-6 times per week

2-3 times per week once a week

2-3 times a month less than once a month

Increasing proportion of broadband subscription

Continuous reduction in the cost of internet access

Internet user base spreading to non metros Mobile internet user base is growing

Internet usage pattern Payment landscape undergoing change

58%21%

12%7%

2%

Acceptance of online payments by Indian consumers

direct debit visa

master card Cash on delivery

all others

Pattern of online behaviour rapidly converging with that of users in developed countries

The number of debit cards is on the rise due to the increasing access of people to banking services

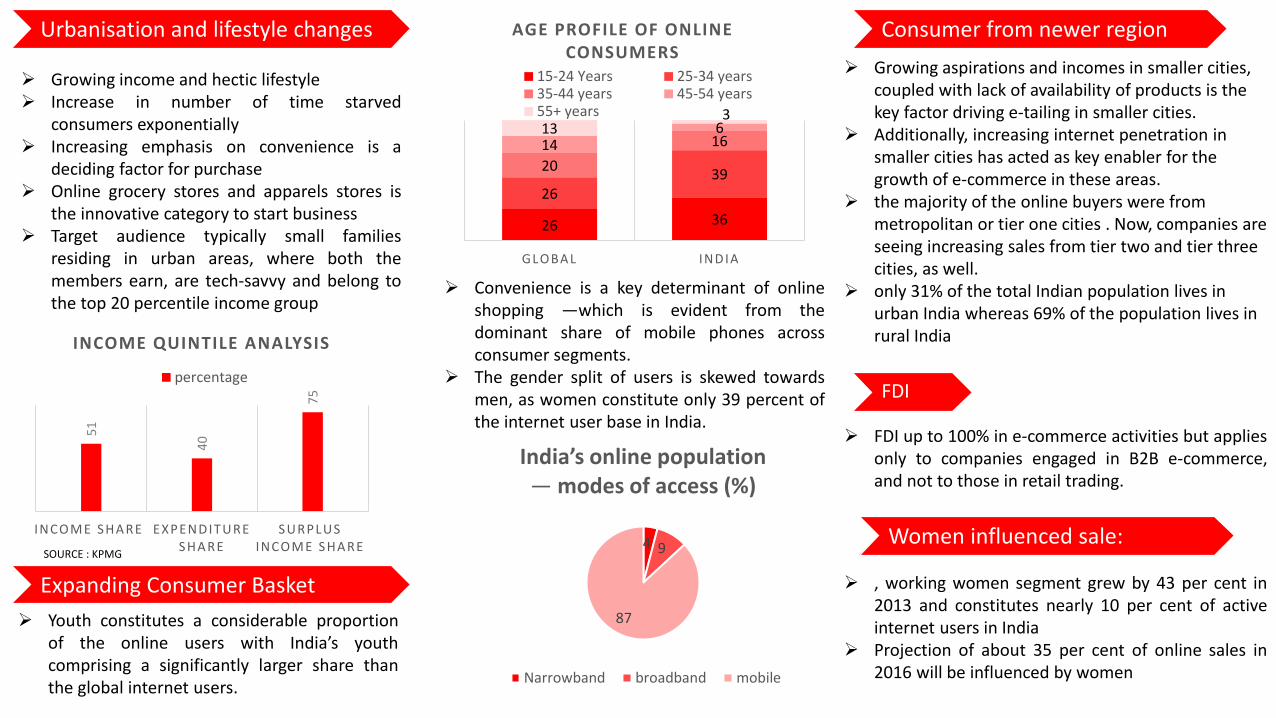

Urbanisation and lifestyle changes

Growing income and hectic lifestyle Increase in number of time starved

consumers exponentially Increasing emphasis on convenience is a

deciding factor for purchase Online grocery stores and apparels stores is

the innovative category to start business Target audience typically small families

residing in urban areas, where both themembers earn, are tech-savvy and belong tothe top 20 percentile income group

51

40

75

INCOME SHA RE EXPENDITURE S HA RE

SURPLUS INCOME SHA RE

INCOME QUINTILE ANALYSIS

percentage

SOURCE : KPMG

Expanding Consumer Basket

Youth constitutes a considerable proportionof the online users with India’s youthcomprising a significantly larger share thanthe global internet users.

26 36

2639

20

16146133

GLOBA L IND IA

AGE PROFILE OF ONLINE CONSUMERS

15-24 Years 25-34 years35-44 years 45-54 years55+ years

Convenience is a key determinant of onlineshopping —which is evident from thedominant share of mobile phones acrossconsumer segments.

The gender split of users is skewed towardsmen, as women constitute only 39 percent ofthe internet user base in India.

4 9

87

India’s online population— modes of access (%)

Narrowband broadband mobile

Consumer from newer region

Growing aspirations and incomes in smaller cities, coupled with lack of availability of products is the key factor driving e-tailing in smaller cities.

Additionally, increasing internet penetration in smaller cities has acted as key enabler for the growth of e-commerce in these areas.

the majority of the online buyers were from metropolitan or tier one cities . Now, companies are seeing increasing sales from tier two and tier three cities, as well.

only 31% of the total Indian population lives in urban India whereas 69% of the population lives in rural India

FDI

FDI up to 100% in e-commerce activities but appliesonly to companies engaged in B2B e-commerce,and not to those in retail trading.

Women influenced sale:

, working women segment grew by 43 per cent in2013 and constitutes nearly 10 per cent of activeinternet users in India

Projection of about 35 per cent of online sales in2016 will be influenced by women

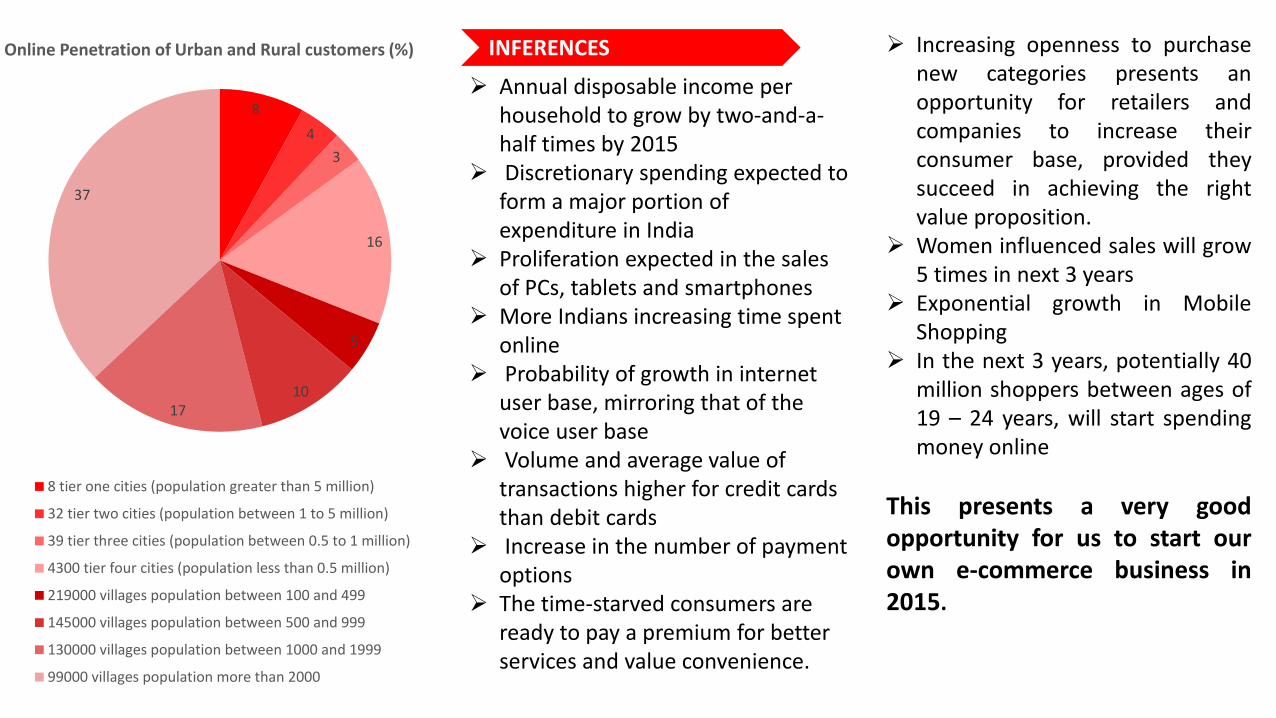

8

4

3

16

5

1017

37

Online Penetration of Urban and Rural customers (%)

8 tier one cities (population greater than 5 million)

32 tier two cities (population between 1 to 5 million)

39 tier three cities (population between 0.5 to 1 million)

4300 tier four cities (population less than 0.5 million)

219000 villages population between 100 and 499

145000 villages population between 500 and 999

130000 villages population between 1000 and 1999

99000 villages population more than 2000

Annual disposable income per household to grow by two-and-a-half times by 2015

Discretionary spending expected to form a major portion of expenditure in India

Proliferation expected in the sales of PCs, tablets and smartphones

More Indians increasing time spent online

Probability of growth in internet user base, mirroring that of the voice user base

Volume and average value of transactions higher for credit cards than debit cards

Increase in the number of payment options

The time-starved consumers are ready to pay a premium for better services and value convenience.

Increasing openness to purchasenew categories presents anopportunity for retailers andcompanies to increase theirconsumer base, provided theysucceed in achieving the rightvalue proposition.

Women influenced sales will grow5 times in next 3 years

Exponential growth in MobileShopping

In the next 3 years, potentially 40million shoppers between ages of19 – 24 years, will start spendingmoney online

This presents a very goodopportunity for us to start ourown e-commerce business in2015.

INFERENCES

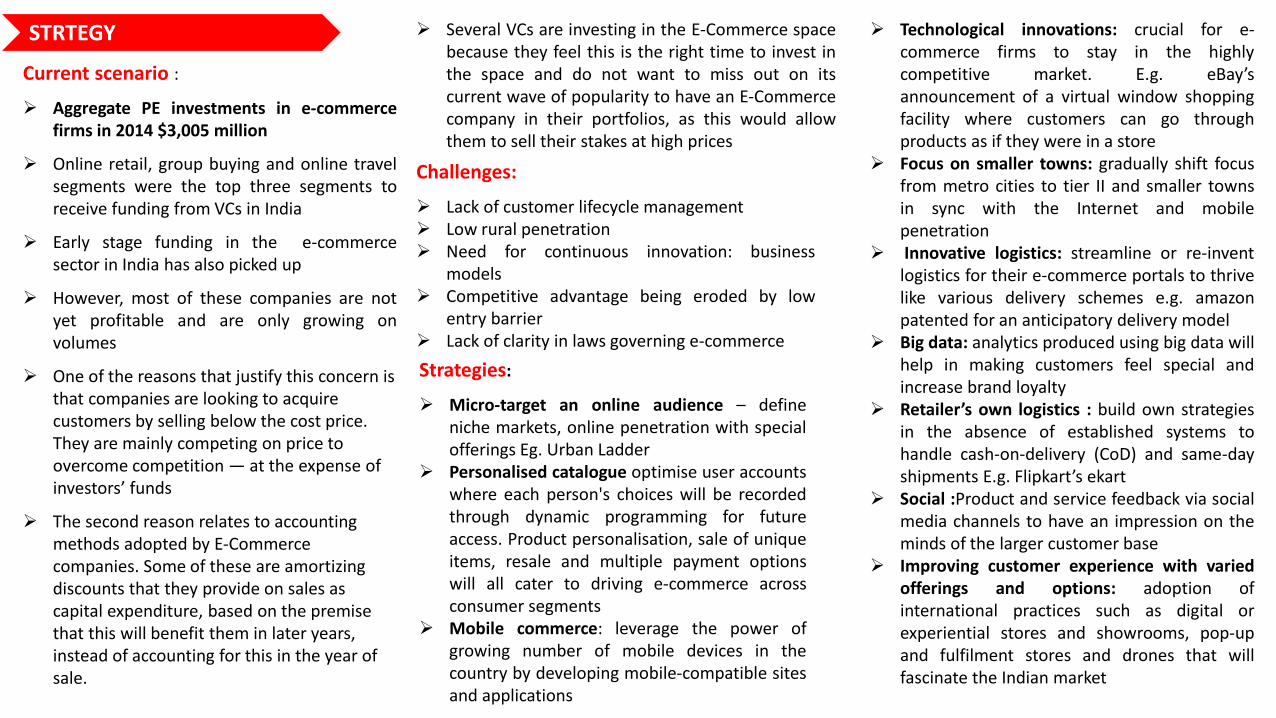

Current scenario :

Aggregate PE investments in e-commercefirms in 2014 $3,005 million

Online retail, group buying and online travelsegments were the top three segments toreceive funding from VCs in India

Early stage funding in the e‐commercesector in India has also picked up

However, most of these companies are notyet profitable and are only growing onvolumes

One of the reasons that justify this concern is that companies are looking to acquire customers by selling below the cost price. They are mainly competing on price to overcome competition — at the expense of investors’ funds

The second reason relates to accounting methods adopted by E‐Commerce companies. Some of these are amortizing discounts that they provide on sales as capital expenditure, based on the premise that this will benefit them in later years, instead of accounting for this in the year of sale.

Several VCs are investing in the E‐Commerce spacebecause they feel this is the right time to invest inthe space and do not want to miss out on itscurrent wave of popularity to have an E‐Commercecompany in their portfolios, as this would allowthem to sell their stakes at high prices

Challenges:

Lack of customer lifecycle management Low rural penetration Need for continuous innovation: business

models Competitive advantage being eroded by low

entry barrier Lack of clarity in laws governing e‐commerce

Strategies:

Micro-target an online audience – defineniche markets, online penetration with specialofferings Eg. Urban Ladder

Personalised catalogue optimise user accountswhere each person's choices will be recordedthrough dynamic programming for futureaccess. Product personalisation, sale of uniqueitems, resale and multiple payment optionswill all cater to driving e-commerce acrossconsumer segments

Mobile commerce: leverage the power ofgrowing number of mobile devices in thecountry by developing mobile-compatible sitesand applications

Technological innovations: crucial for e-commerce firms to stay in the highlycompetitive market. E.g. eBay’sannouncement of a virtual window shoppingfacility where customers can go throughproducts as if they were in a store

Focus on smaller towns: gradually shift focusfrom metro cities to tier II and smaller townsin sync with the Internet and mobilepenetration

Innovative logistics: streamline or re-inventlogistics for their e-commerce portals to thrivelike various delivery schemes e.g. amazonpatented for an anticipatory delivery model

Big data: analytics produced using big data willhelp in making customers feel special andincrease brand loyalty

Retailer’s own logistics : build own strategiesin the absence of established systems tohandle cash-on-delivery (CoD) and same-dayshipments E.g. Flipkart’s ekart

Social :Product and service feedback via socialmedia channels to have an impression on theminds of the larger customer base

Improving customer experience with variedofferings and options: adoption ofinternational practices such as digital orexperiential stores and showrooms, pop-upand fulfilment stores and drones that willfascinate the Indian market

STRTEGY

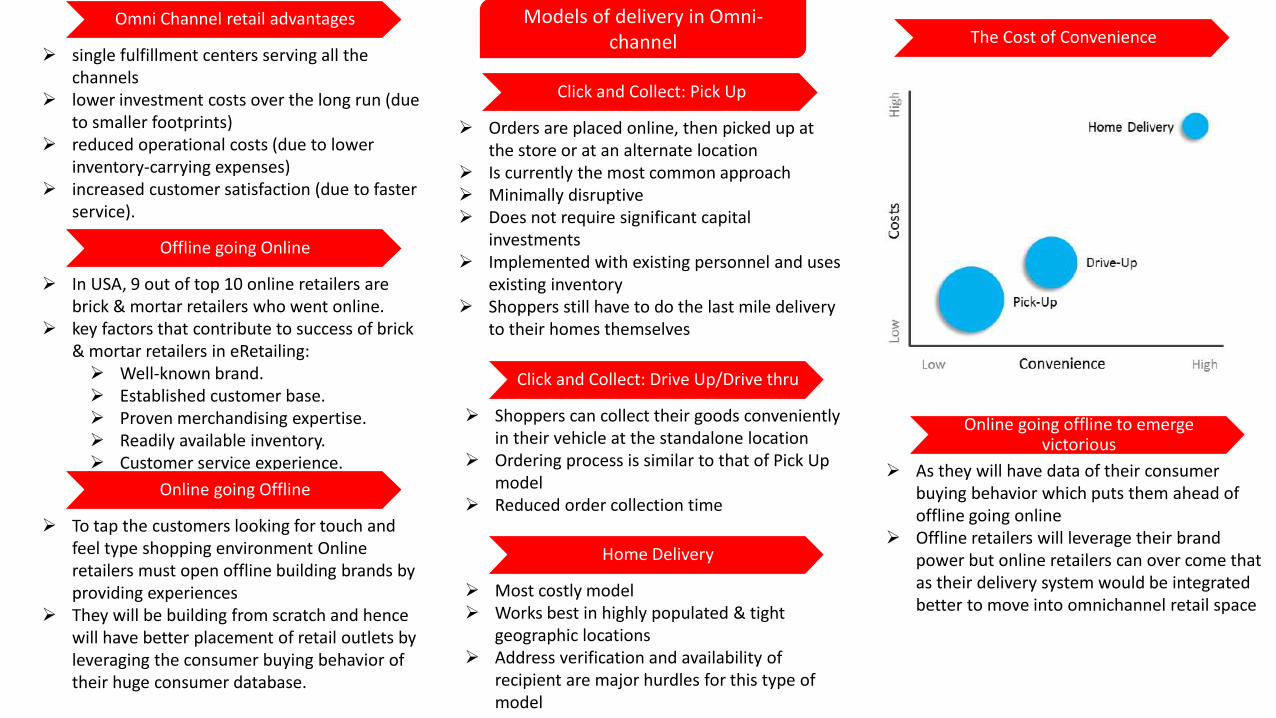

Omni Channel retail advantages

single fulfillment centers serving all the channels

lower investment costs over the long run (due to smaller footprints)

reduced operational costs (due to lower inventory-carrying expenses)

increased customer satisfaction (due to faster service).

Click and Collect: Pick Up

Orders are placed online, then picked up at the store or at an alternate location

Is currently the most common approach Minimally disruptive Does not require significant capital

investments Implemented with existing personnel and uses

existing inventory Shoppers still have to do the last mile delivery

to their homes themselves

Click and Collect: Drive Up/Drive thru

Shoppers can collect their goods conveniently in their vehicle at the standalone location

Ordering process is similar to that of Pick Up model

Reduced order collection time

Home Delivery

Most costly model Works best in highly populated & tight

geographic locations Address verification and availability of

recipient are major hurdles for this type of model

Models of delivery in Omni-channel

Offline going Online

In USA, 9 out of top 10 online retailers are brick & mortar retailers who went online.

key factors that contribute to success of brick & mortar retailers in eRetailing: Well-known brand. Established customer base. Proven merchandising expertise. Readily available inventory. Customer service experience.

Online going Offline

To tap the customers looking for touch and feel type shopping environment Online retailers must open offline building brands by providing experiences

They will be building from scratch and hence will have better placement of retail outlets by leveraging the consumer buying behavior of their huge consumer database.

Online going offline to emerge victorious

As they will have data of their consumer buying behavior which puts them ahead of offline going online

Offline retailers will leverage their brand power but online retailers can over come that as their delivery system would be integrated better to move into omnichannel retail space

The Cost of Convenience

Thank You

Related Documents