SLIDE 1 PRUDENTIAL STANDARD FRAMEWORK RULE CHANGE REQUEST 14 December 2011 PRESENTED BY RUTH GUEST

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SLIDE 1

PRUDENTIAL STANDARD FRAMEWORK

RULE CHANGE REQUEST

14 December 2011

PRESENTED BY RUTH GUEST

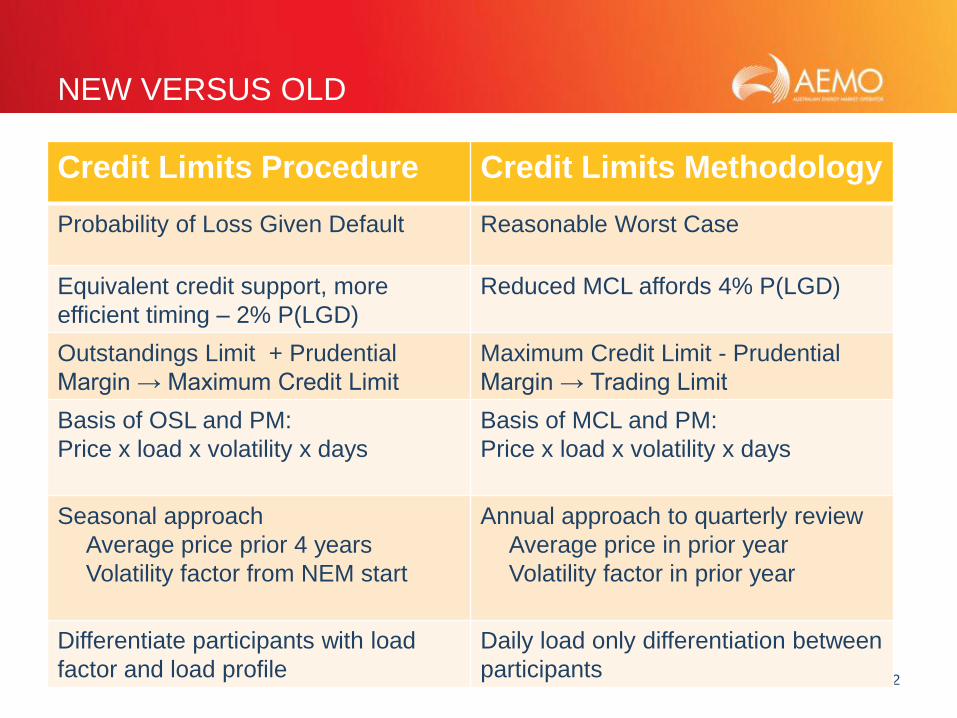

SLIDE 2

NEW VERSUS OLD

Credit Limits Procedure Credit Limits Methodology

Probability of Loss Given Default Reasonable Worst Case

Equivalent credit support, more

efficient timing – 2% P(LGD)

Reduced MCL affords 4% P(LGD)

Outstandings Limit + Prudential

Margin → Maximum Credit Limit

Maximum Credit Limit - Prudential

Margin → Trading Limit

Basis of OSL and PM:

Price x load x volatility x days

Basis of MCL and PM:

Price x load x volatility x days

Seasonal approach

Average price prior 4 years

Volatility factor from NEM start

Annual approach to quarterly review

Average price in prior year

Volatility factor in prior year

Differentiate participants with load

factor and load profile

Daily load only differentiation between

participants

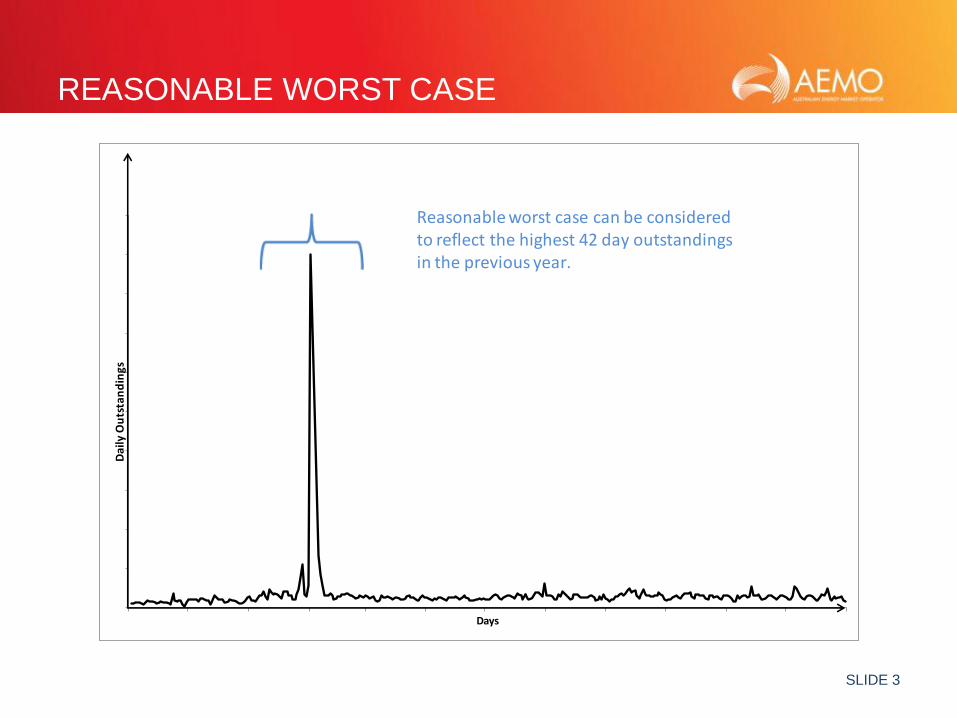

SLIDE 3

REASONABLE WORST CASE D

aily

Ou

tsta

nd

ings

Days

Reasonable worst case can be considered to reflect the highest 42 day outstandings in the previous year.

SLIDE 4

LOSS GIVEN DEFAULT

• P(LGD) is to be met for each region over life of NEM

• 2% is equivalent to approximately 7 days a year

Ou

tsta

nd

ings

Days

Trading Limit Breach - Loss Given Default

Reaction PeriodOutstandingsLimit

Outstandings

Prudential Margin Trading Limit Breach

Suspension

Loss

SLIDE 5

MAXIMUM CREDIT LIMIT (NEW)

• MCL = outstandings limit plus prudential margin

o OSL and PM calculated simultaneously to meet P(LGD)

o Daily load x price x volatility factor x (21, 7) days

o Model calibrated for VFs to meet the P(LGD)

o Price and volatility factors are a region parameter

• Outstandings limit is a new term which is distinguishable

from trading limit when credit support > MCL

o Trading limit = credit support – prudential margin

o Outstandings limit ≡ MCL – prudential margin

SLIDE 6

AVERAGE PRICE AND LOAD

Credit Limit Methodology

• Previous year’s average

price - region parameter

• Trending of daily load –

participant specific

Credit Limit Procedure

• Average price of previous

four equivalent seasons-

region parameter

• Trending of daily load –

participant specific

SLIDE 7

VOLATILITY FACTOR

Credit Limits Methodology

• Ratio in last year

Maximum 42 day outstandings :

Average 42 day outstandings

Credit Limits Procedure

• VF each day over life of

NEM for OSL and PM

• Seasonal approach to ratio

35 or 7 day outstandings:

35 or 7 day average in

previous 4 seasons

• Set VF percentiles for OSL

and PM equivalent

• Calibrate the model to meet

P(LGD)

SLIDE 8

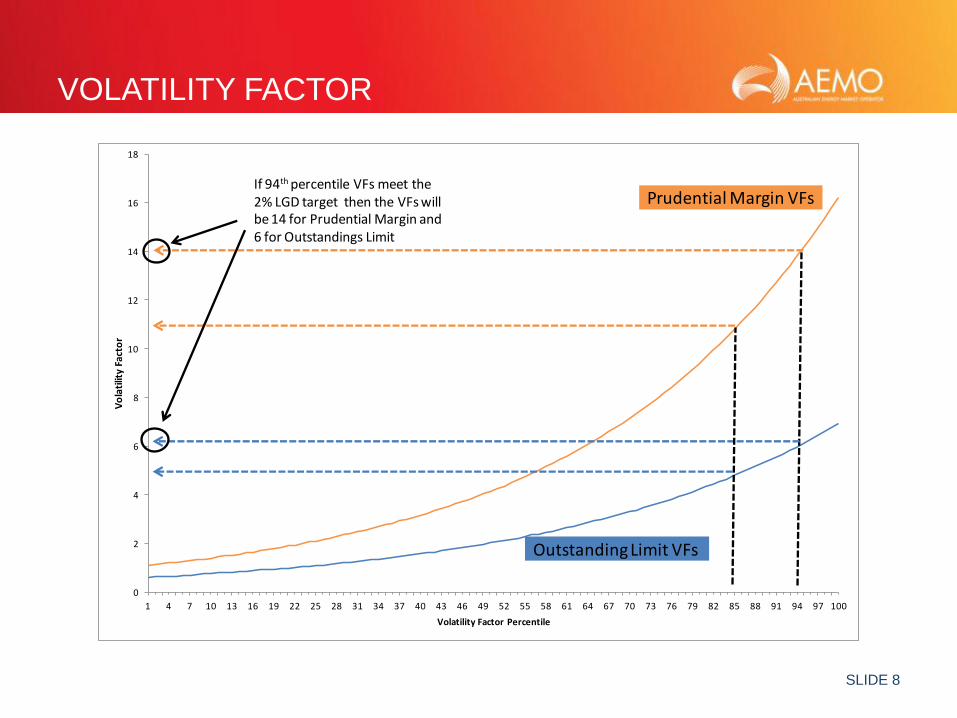

VOLATILITY FACTOR

0

2

4

6

8

10

12

14

16

18

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 100

Vo

lati

lity

Fact

or

Volatility Factor Percentile

Prudential Margin VFs

OutstandingLimit VFs

If 94th percentile VFs meet the 2% LGD target then the VFs willbe 14 for Prudential Margin and 6 for Outstandings Limit

SLIDE 9

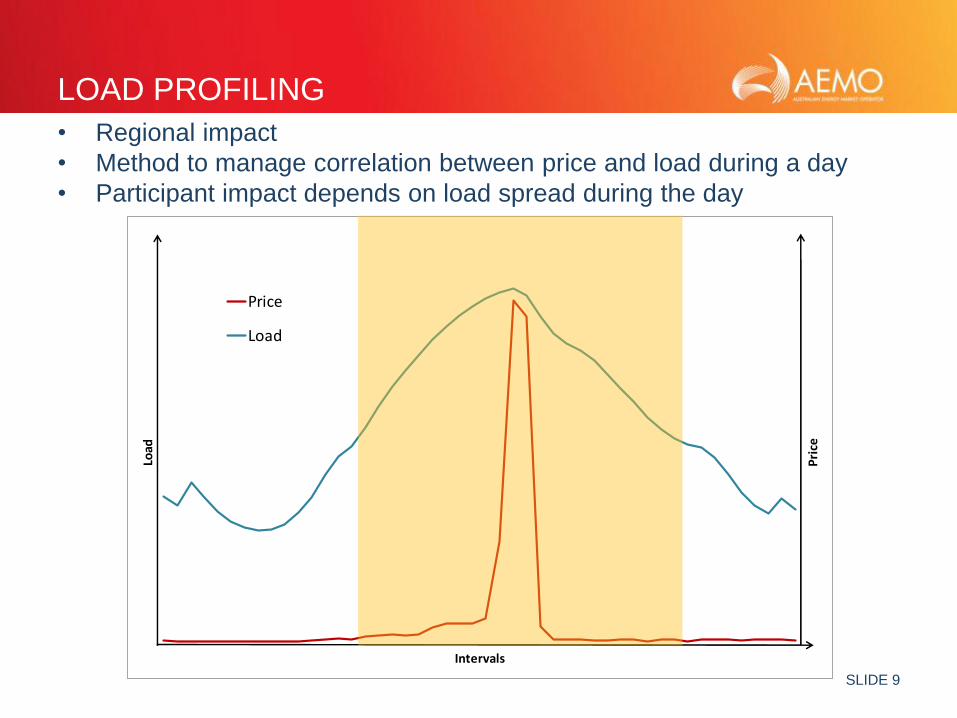

LOAD PROFILING

• Regional impact

• Method to manage correlation between price and load during a day

• Participant impact depends on load spread during the day

Pri

ce

Load

Intervals

Price

Load

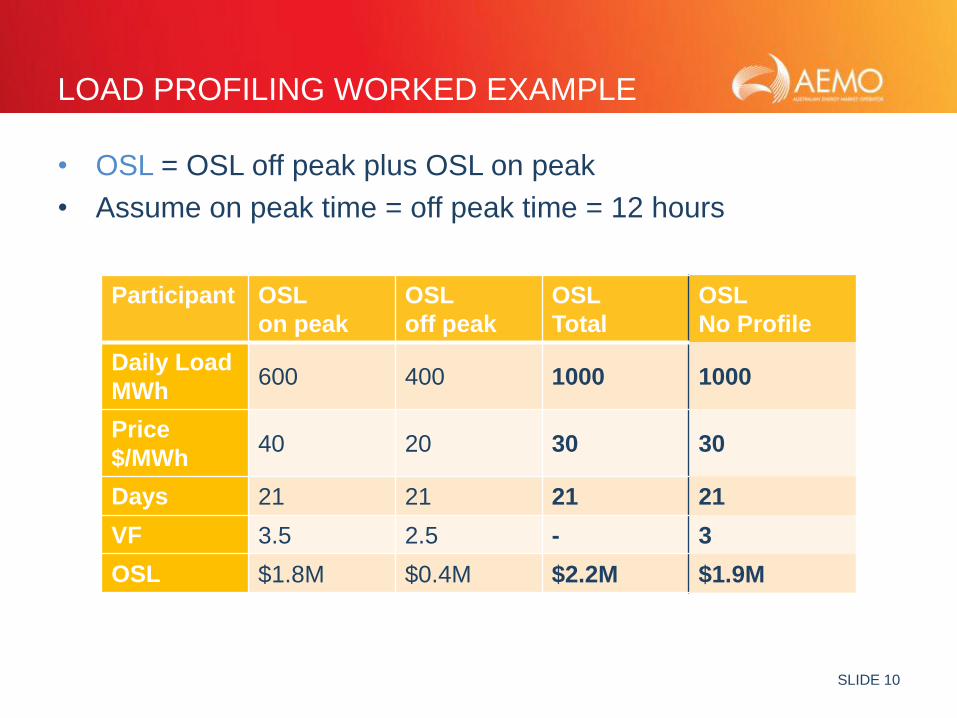

SLIDE 10

LOAD PROFILING WORKED EXAMPLE

• OSL = OSL off peak plus OSL on peak

• Assume on peak time = off peak time = 12 hours

Participant OSL

on peak

OSL

off peak

OSL

Total

OSL

No Profile

Daily Load

MWh 600 400 1000 1000

Price

$/MWh 40 20 30 30

Days 21 21 21 21

VF 3.5 2.5 - 3

OSL $1.8M $0.4M $2.2M $1.9M

SLIDE 11

LOAD FACTOR

• Participant parameter

• Method to manage participant volatility greater or lower than region

• In general the peakier the load the greater the credit support requirement

• Envisaged to encourage management of load patterns.

Load

Days

Region Peakier Flatter

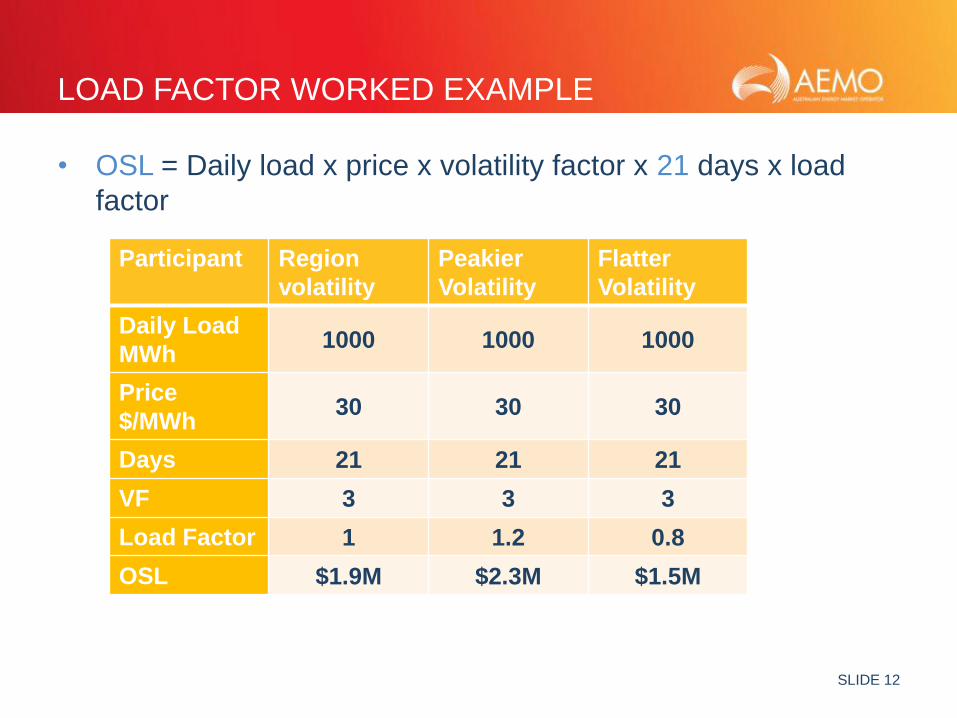

SLIDE 12

LOAD FACTOR WORKED EXAMPLE

• OSL = Daily load x price x volatility factor x 21 days x load

factor

Participant Region

volatility

Peakier

Volatility

Flatter

Volatility

Daily Load

MWh 1000 1000 1000

Price

$/MWh 30 30 30

Days 21 21 21

VF 3 3 3

Load Factor 1 1.2 0.8

OSL $1.9M $2.3M $1.5M

SLIDE 13

IMPACT OF RULE AND NEW PROCEDURE

• A clear (and previously accepted) target for prudential

surety

• Dramatic changes in credit support lagging a high

outstandings event are avoided.

• Differentiation of more risky profiles

• Provide a driver for managing NEM risk

o Matching load profiles with generation and reallocation

profiles

o Reduce volatility of load

SLIDE 14

Related Documents