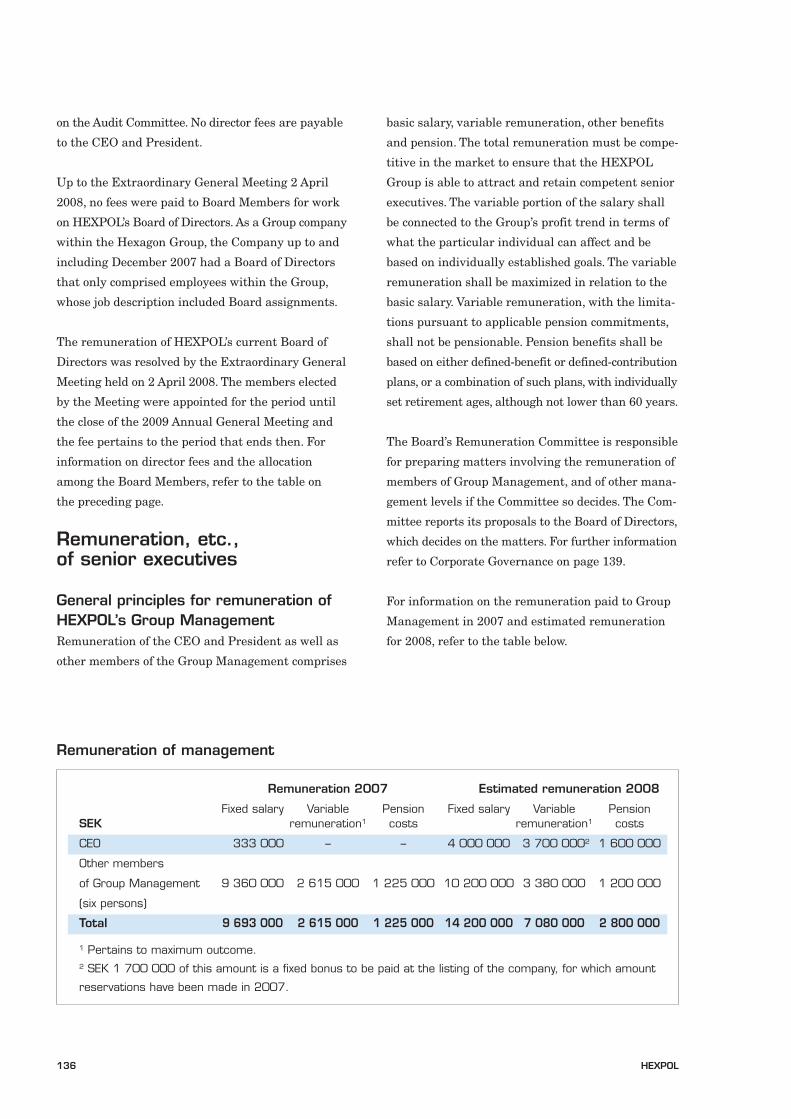

Prospectus concerning the listing of shares in HEXPOL AB (publ)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Prospectus concerning the listing of shares inHEXPOL AB (publ)

This prospectus has been prepared in connection with the application by

the Board of Directors of HEXPOL AB (publ) to have the Company’s Class B

shares listed on the OMX Nordic Exchange.

Unless otherwise specified, the terms “HEXPOL,” “the HEXPOL Group,”

“the Group,” or “the Company” refer to HEXPOL AB (publ), Corp. Reg. No.

556108-9631, and its wholly owned subsidiaries, or a particular subsidiary,

depending on context. HEXPOL AB refers to the Parent Company. Unless

otherwise specified, the term “Hexagon” refers to Hexagon AB (publ), Corp.

Reg. No. 556190-4771, and its wholly owned subsidiaries, or a particular

subsidiary, depending on context. Hexagon AB refers to the Parent Company.

The terms “OMX Nordic Exchange” or “the Nordic Exchange” refer to OMX

Nordic Exchange in Stockholm.

In this prospectus, statements regarding future prospects are made by the

Board of Directors of HEXPOL AB and are based on current market condi-

tions. Although such statements have been well processed, readers should

be aware that they, and all other estimates of the future, are associated with

uncertainty. For an overview of risk factors, refer to pages 11-16.

Apart from what is specified in the auditors’ statement on pages 128-129,

or what is expressly stated, no information in this prospectus has been

examined or audited by the Company’s auditors.

This prospectus is subject to Swedish law. Disputes relating to the prospectus,

or associated legal conditions, shall be determined exclusively by a Swedish

court.

The prospectus has been approved and registered by the Swedish Financial

Supervisory Authority pursuant to the provisions of Chapter 2, Sections 25

and 26 of the Financial Instruments Trading Act (1991:980).

This prospectus is available on HEXPOL’s website www.hexpol.com,

Hexagon’s website www.hexagon.se and on Swedbank’s website

www.swedbank.se/prospekt.

The information in this prospectus is a translation of the text in the Swedish-language

prospectus and, accordingly, corresponds in all material respects with the original Swedish

document. In the event of any contradictions between the texts contained in this document

and the text in the Swedish-language prospectus, the latter shall prevail.

HEXPOL 3

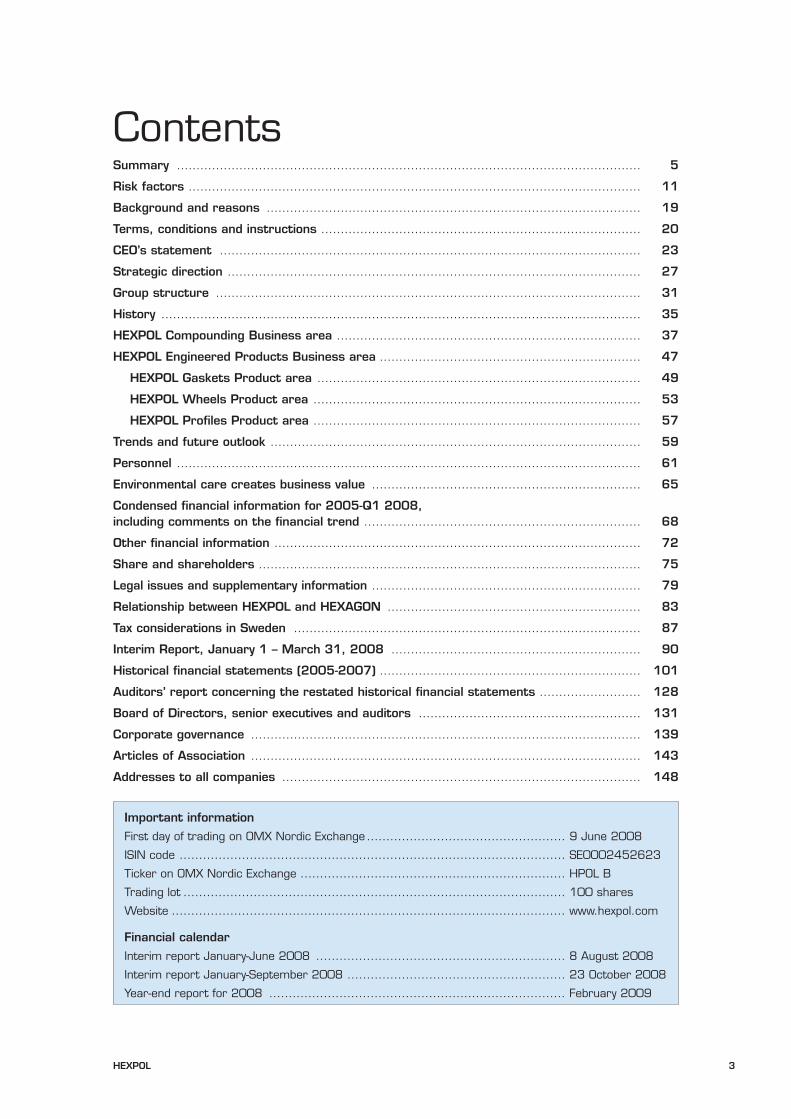

Important information

First day of trading on OMX Nordic Exchange ................................................... 9 June 2008

ISIN code ................................................................................................... SE0002452623

Ticker on OMX Nordic Exchange .................................................................... HPOL B

Trading lot .................................................................................................. 100 shares

Website ..................................................................................................... www.hexpol.com

Financial calendar

Interim report January-June 2008 ................................................................ 8 August 2008

Interim report January-September 2008 ........................................................ 23 October 2008

Year-end report for 2008 ............................................................................ February 2009

ContentsSummary ....................................................................................................................... 5

Risk factors .................................................................................................................... 11

Background and reasons ................................................................................................ 19

Terms, conditions and instructions .................................................................................. 20

CEO’s statement ............................................................................................................ 23

Strategic direction .......................................................................................................... 27

Group structure ............................................................................................................. 31

History ........................................................................................................................... 35

HEXPOL Compounding Business area .............................................................................. 37

HEXPOL Engineered Products Business area ................................................................... 47

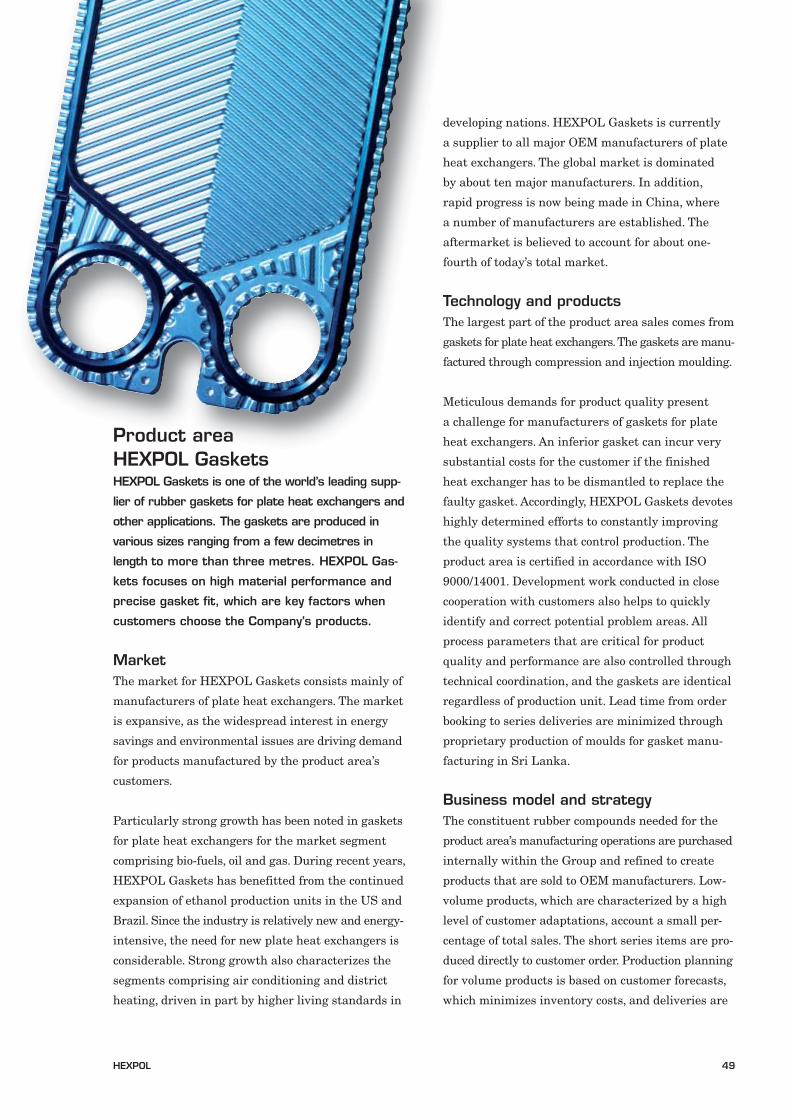

HEXPOL Gaskets Product area ................................................................................... 49

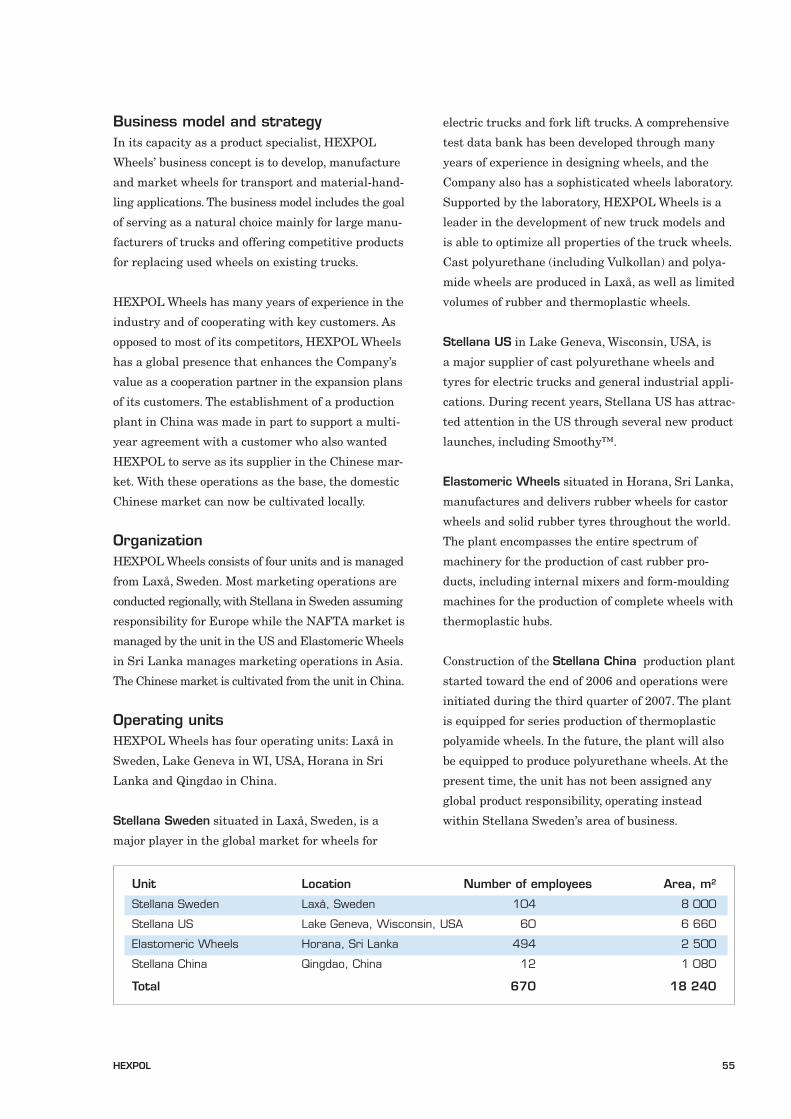

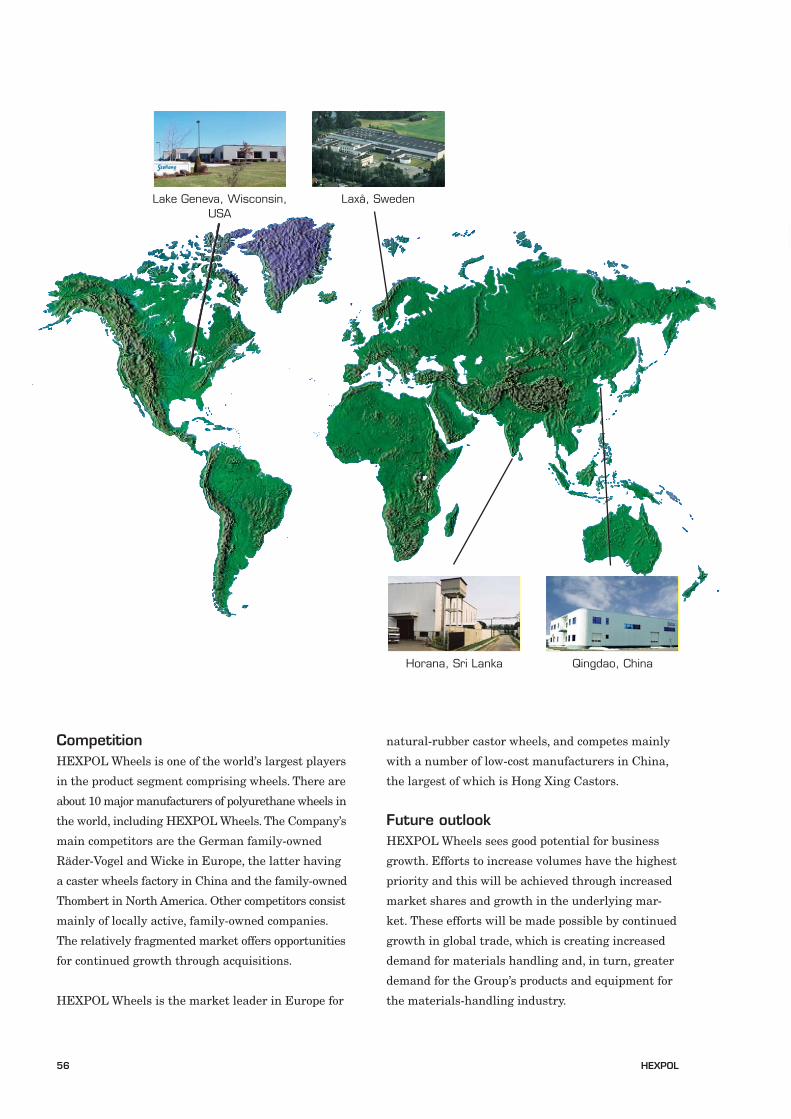

HEXPOL Wheels Product area .................................................................................... 53

HEXPOL Profiles Product area .................................................................................... 57

Trends and future outlook ............................................................................................... 59

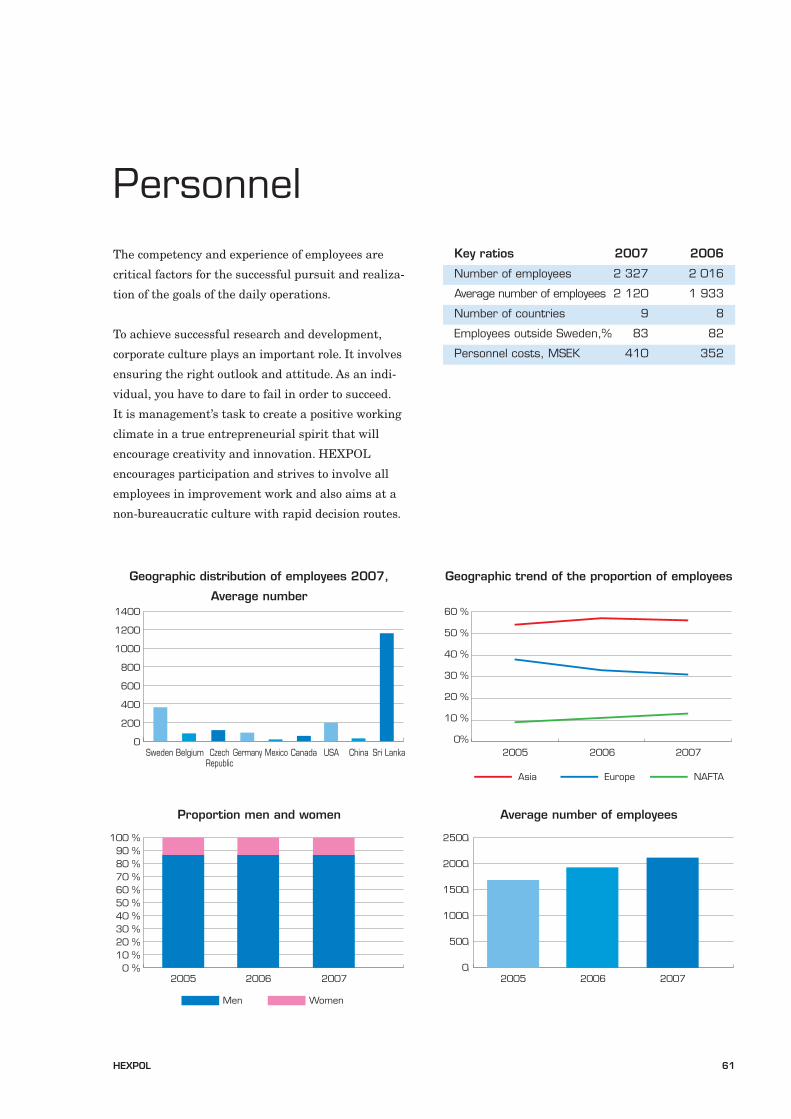

Personnel ....................................................................................................................... 61

Environmental care creates business value ..................................................................... 65

Condensed financial information for 2005-Q1 2008, including comments on the financial trend ....................................................................... 68

Other financial information .............................................................................................. 72

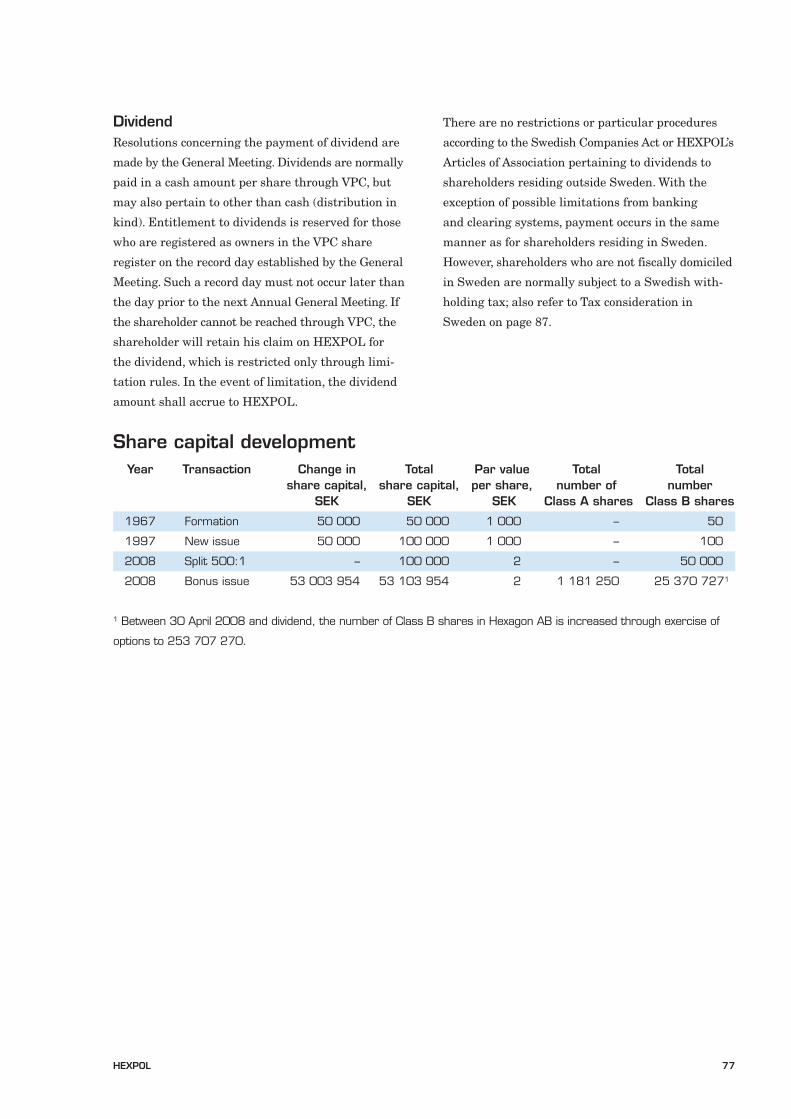

Share and shareholders .................................................................................................. 75

Legal issues and supplementary information ..................................................................... 79

Relationship between HEXPOL and HEXAGON ................................................................. 83

Tax considerations in Sweden ......................................................................................... 87

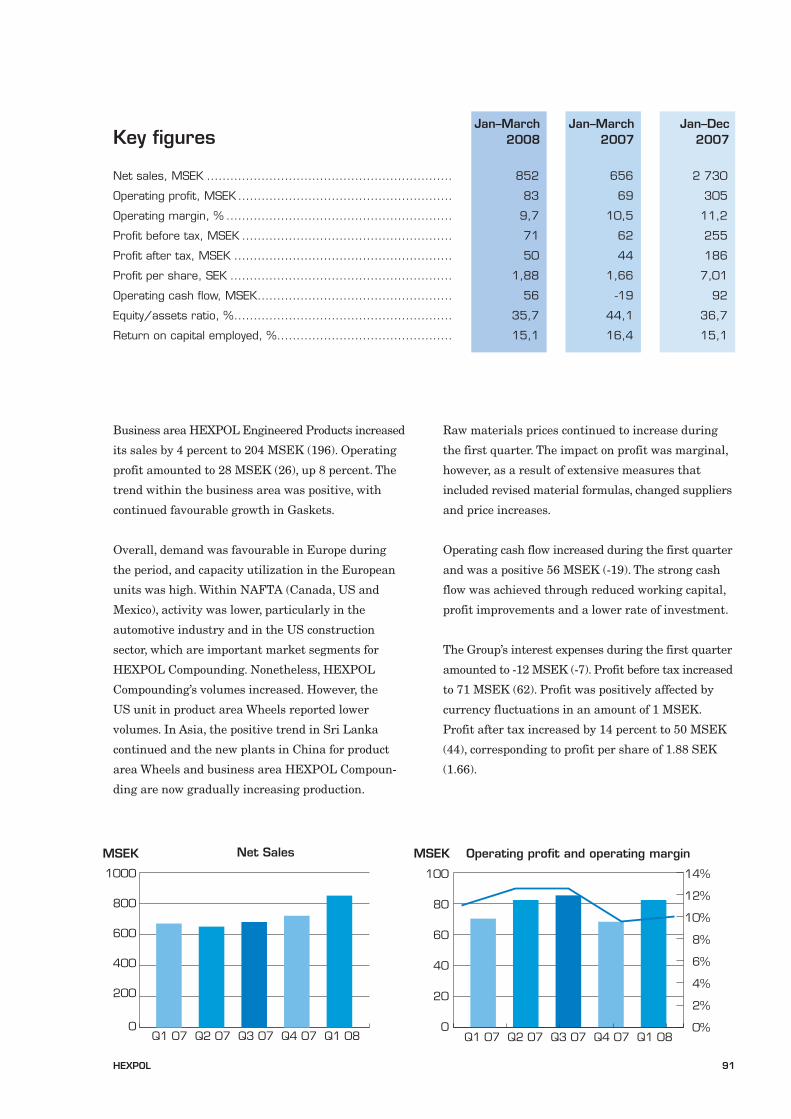

Interim Report, January 1 – March 31, 2008 ................................................................ 90

Historical financial statements (2005-2007) ................................................................... 101

Auditors’ report concerning the restated historical financial statements .......................... 128

Board of Directors, senior executives and auditors ......................................................... 131

Corporate governance .................................................................................................... 139

Articles of Association .................................................................................................... 143

Addresses to all companies ............................................................................................ 148

4 HEXPOL

HEXPOL 5

This summary should be regarded only as an intro-

duction to and a summary of the other parts of this

prospectus. The prospectus has been prepared in

connection with the listing of HEXPOL AB’s Class B

shares on the OMX Nordic Exchange Stockholm.

Each decision to invest in HEXPOL should be based

on an evaluation of the prospectus in its entirety,

and not just on this summary.

A person may be held responsible for information

that is included or lacking in the summary, or a trans-

lation of it, only if the summary or the translation is

misleading, erroneous or irreconcilable in relation to

other parts of the prospectus. Note that a person

who files claims in a court with reference to informa-

tion in this prospectus may be forced to bear the

costs for translation of the prospectus.

Summary

Background and reasonsHexagon AB’s shareholders resolved at Hexagon’s

Annual General Meeting on 5 May 2008 that all of

the shares in HEXPOL would be transferred to the

shareholders of Hexagon in the form of a dividend.

The intention is that Class B HEXPOL shares will

be listed on the OMX Nordic Exchange Stockholm,

with 9 June 2008 as the first day of trading.

The reason for the separate market listing is that

HEXPOL has reached a size and profitability that

makes its operations attractive as an independently

listed company. HEXPOL has the necessary resources

in terms of management, administration, operational

control and business development, and is thus ready

to continue to develop as an independent company.

By so doing, HEXPOL will be able to capitalize on

opportunities for continued robust growth via the

establishment of new and acquisitions of existing

operations in accordance with an adapted growth

strategy, with an organization and capital structure

that supports this growth.

The Board of Directors of Hexagon is of the opinion

that, over the long term, the value for Hexagon’s

shareholders will increase through a spin-off of

these operations and a distribution of HEXPOL

shares. In addition, a separate market listing of

HEXPOL will make it possible for both current and

new shareholders to choose to invest directly in

HEXPOL.

The Group in brief HEXPOL is one of the world’s leading polymer

groups with strong global market positions that

enable it to offer innovative solutions and products

based on advanced rubber compounds (Compoun-

ding), gaskets for plate heat exchangers (PHE

Gaskets) and wheels made of polyurethane, plastic

and rubber materials for forklifts and castor wheel

applications (Wheels).

The Group is organized in two business areas:

HEXPOL Compounding and HEXPOL Engineered

Products, and has production units in nine countries.

The business areas operate in separate market

segments. Despite this, HEXPOL utilizes distinct

synergies in the areas of technology, purchasing and

production. Customers outside Sweden account for

about 90 percent of invoiced sales, and seven of the

Group’s 15 production units are situated in expan-

sive regions of Asia, Mexico and Eastern Europe.

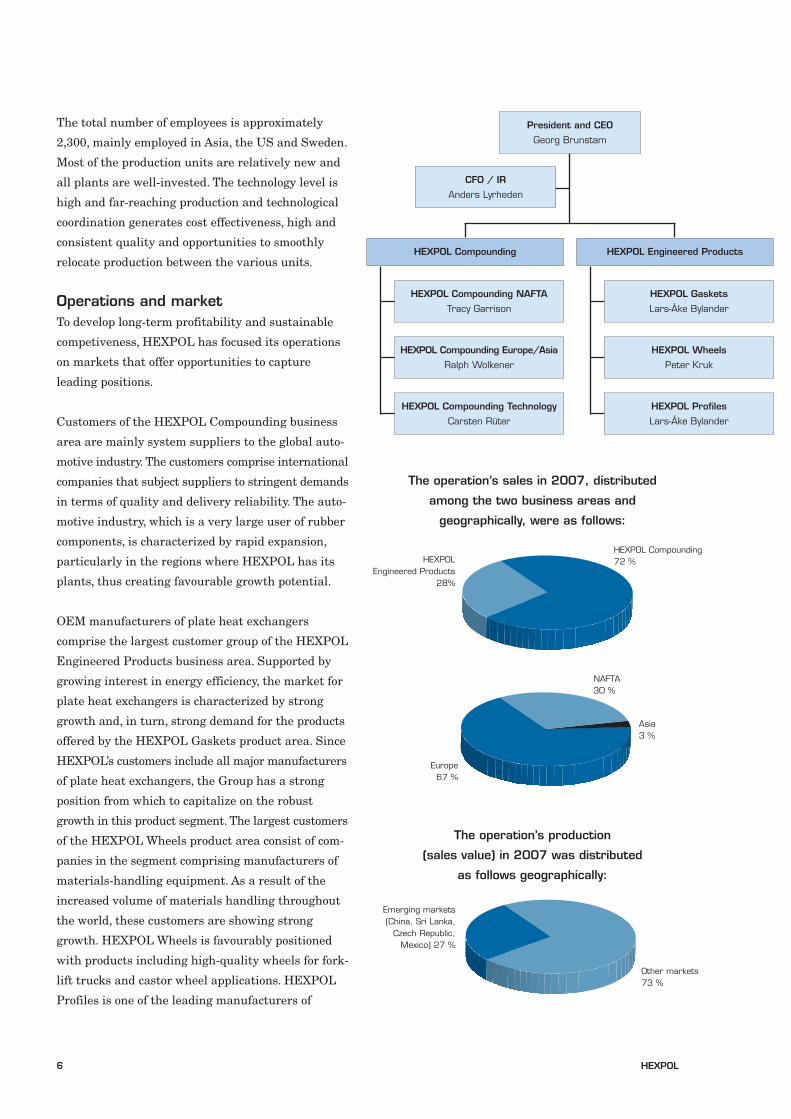

6 HEXPOL

HEXPOL Compounding

HEXPOL Compounding NAFTA

Tracy Garrison

HEXPOL Engineered Products

HEXPOL Gaskets

Lars-Åke Bylander

HEXPOL Compounding Europe/Asia

Ralph Wolkener

HEXPOL Wheels

Peter Kruk

HEXPOL Compounding Technology

Carsten Rüter

HEXPOL Profiles

Lars-Åke Bylander

President and CEO

Georg Brunstam

CFO / IR

Anders Lyrheden

The total number of employees is approximately

2,300, mainly employed in Asia, the US and Sweden.

Most of the production units are relatively new and

all plants are well-invested. The technology level is

high and far-reaching production and technological

coordination generates cost effectiveness, high and

consistent quality and opportunities to smoothly

relocate production between the various units.

Operations and marketTo develop long-term profitability and sustainable

competiveness, HEXPOL has focused its operations

on markets that offer opportunities to capture

leading positions.

Customers of the HEXPOL Compounding business

area are mainly system suppliers to the global auto-

motive industry. The customers comprise international

companies that subject suppliers to stringent demands

in terms of quality and delivery reliability. The auto-

motive industry, which is a very large user of rubber

components, is characterized by rapid expansion,

particularly in the regions where HEXPOL has its

plants, thus creating favourable growth potential.

OEM manufacturers of plate heat exchangers

comprise the largest customer group of the HEXPOL

Engineered Products business area. Supported by

growing interest in energy efficiency, the market for

plate heat exchangers is characterized by strong

growth and, in turn, strong demand for the products

offered by the HEXPOL Gaskets product area. Since

HEXPOL’s customers include all major manufacturers

of plate heat exchangers, the Group has a strong

position from which to capitalize on the robust

growth in this product segment. The largest customers

of the HEXPOL Wheels product area consist of com-

panies in the segment comprising manufacturers of

materials-handling equipment. As a result of the

increased volume of materials handling throughout

the world, these customers are showing strong

growth. HEXPOL Wheels is favourably positioned

with products including high-quality wheels for fork-

lift trucks and castor wheel applications. HEXPOL

Profiles is one of the leading manufacturers of

The operation’s sales in 2007, distributed

among the two business areas and

geographically, were as follows:

HEXPOL Engineered Products

28%

HEXPOL Compounding72 %

Other markets 73 %

Asia3 %

NAFTA30 %

Europe67 %

Emerging markets (China, Sri Lanka,

Czech Republic, Mexico) 27 %

The operation’s production

(sales value) in 2007 was distributed

as follows geographically:

HEXPOL 7

extruded profiles in the Scandinavian market.

What all of the areas of business have in common is

the importance of cutting-edge expertise related to

polymer materials, applications know-how in the

groups business areas and cost-efficient production

operation.

CompetitorsHEXPOL’s principal competitors are Excel Polymers

and AirBoss in North America and the German com-

pany Kraiburg in Europe (Compounding), the British

TRP Group with business in Great Britain, Dubai and

Romania (Gaskets), the German family-owned com-

panies Räder-Vogel and Wicke in Europe, and the

also family-owned Thombert in North America plus

the Chinese caster wheels manufacturer Hong Xing

Castors (Wheels) and the Swedish company Trelle-

borg (Profiles).

HistoryHEXPOL has its origins in Svenska Gummifabriks

AB, a Swedish industrial company established near

the end of the 19th century in Gislaved, Sweden.

This segment of the once highly diversified Gislaved

Group with operations focused on rubber compounding

and technical products was acquired by Hexagon in

1994. The operations have since been developed

through investments in product development and

acquisitions of complementary companies, most

recently GoldKey in the US, which was acquired

in the autumn of 2007. In addition, proprietary

production units have been constructed in China

and Mexico and production capacity in Sri Lanka

has been increased sharply.

VisionThe vision is to be market leader, ranking number

one or two in selected technological or geographical

segments, to be able to generate growth and share-

holder value.

Business conceptThe business concept is to operate as a product and

application specialist in a limited number of selected

niche areas for the development and production of

polymer products. HEXPOL shall be the most pre-

ferred partner for customers in key industries, such

as the automotive and construction industries, the

energy sector and the materials-handling industry,

based on its offering of innovative and specialized

polymer products and solutions.

StrategyTo achieve sustainable profitability and competitive-

ness, five operating strategies are applied:

• Product development through in-depth and

broad polymer and applications expertise

• The most cost-effective company in the industry

• Efficient supply management that generates

volume and technological benefits

• Management skills through competent and

experienced teams

• Speed management through short and fast

decision-making procedures

In addition to the operating strategies outlined

above, the Group also pursues a strategy to achieve

continued growth, both organically and through

acquisitions.

Financial objectivesThe Board of Directors has established the following

financial objectives over a business cycle: The aim is

that the organic sales growth will be at least 7-10

percent annually and that the operating margin will

be at least 8-10 percent.

Dividend policyHEXPOL’s profit trend and equity/assets ratio deter-

mine the size of the dividend. HEXPOL’s dividend

policy is that 25–50 percent of after-tax net profit for

the year will be distributed as a dividend to HEXPOL’s

shareholders, on condition that the Company’s

equity/assets ratio is regarded as satisfactory.

Success factorsSince 2000, Group operations have expanded from

annual sales of 482 MSEK to slightly more than

3,100 MSEK on an annual basis, with operating

margins that – in most cases – are much better than

those of comparable companies. The operating margin

8 HEXPOL

in 2007 exceeded 11 percent. Cash flow has been strong

despite the rapid growth and, when combined with

approved credit lines, provides the Group with a

strong financial base for continued growth and

expansion.

This favourable trend is the result of deep and

comprehensive product development skills, cost-

effective production plants and successful company

acquisitions. The Group is also positioned strongly

in segments characterized by healthy growth. The

corporate culture is strong, with skilled and experi-

enced employees led by experienced management

teams with short and speedy decision-making routes.

Trends and future outlookHEXPOL operates in markets where short and long-

term growth, both geographically and in terms of

applications, is considered favourable for both the

HEXPOL Group and its customers. Three markets

that offer particularly promising growth potential

are the energy sector, the automotive industry and

the materials-handling industry, areas where

HEXPOL’s customers are key suppliers in various

sub-segments. The Group has also recently established

units in such interesting growth markets as China

and Mexico, which provides competitive advantages

in the form of lower production costs and continued

growth opportunities. These factors, combined with

a continued acquisition-oriented focus, provide the

Group with a strong platform for sustaining its

favourable development.

RisksHEXPOL is an international Group and is thus

exposed to a number of different risks when conduc-

ting its daily operations. The greatest risks include

the general market trend, the competitive situation,

the future price trend, customer relations, the ability

to retain and recruit key personnel, financial risks

and the additional risks that are presented under

the “Risk factors” heading. There are also risks that

are not known to the Company or that the Company

currently regards as insignificant and that could

have an adverse impact on the Company’s operations.

For an overview of risk factors, reference is made to

pages 11–16.

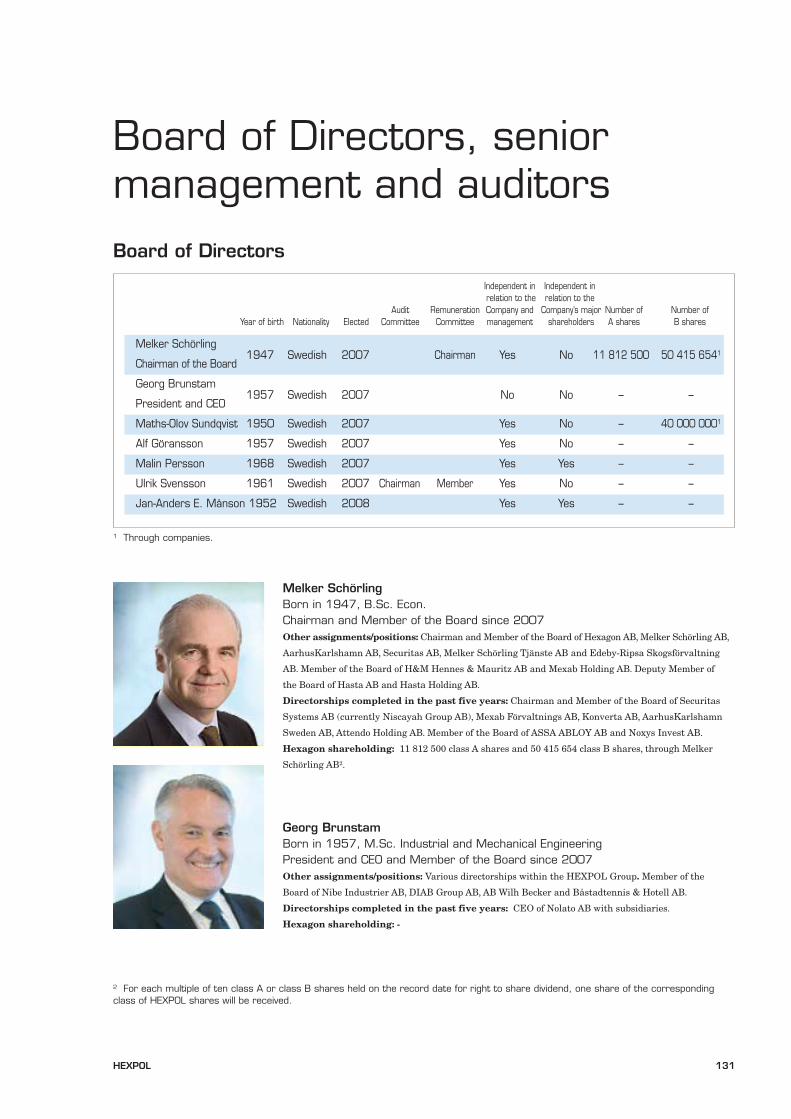

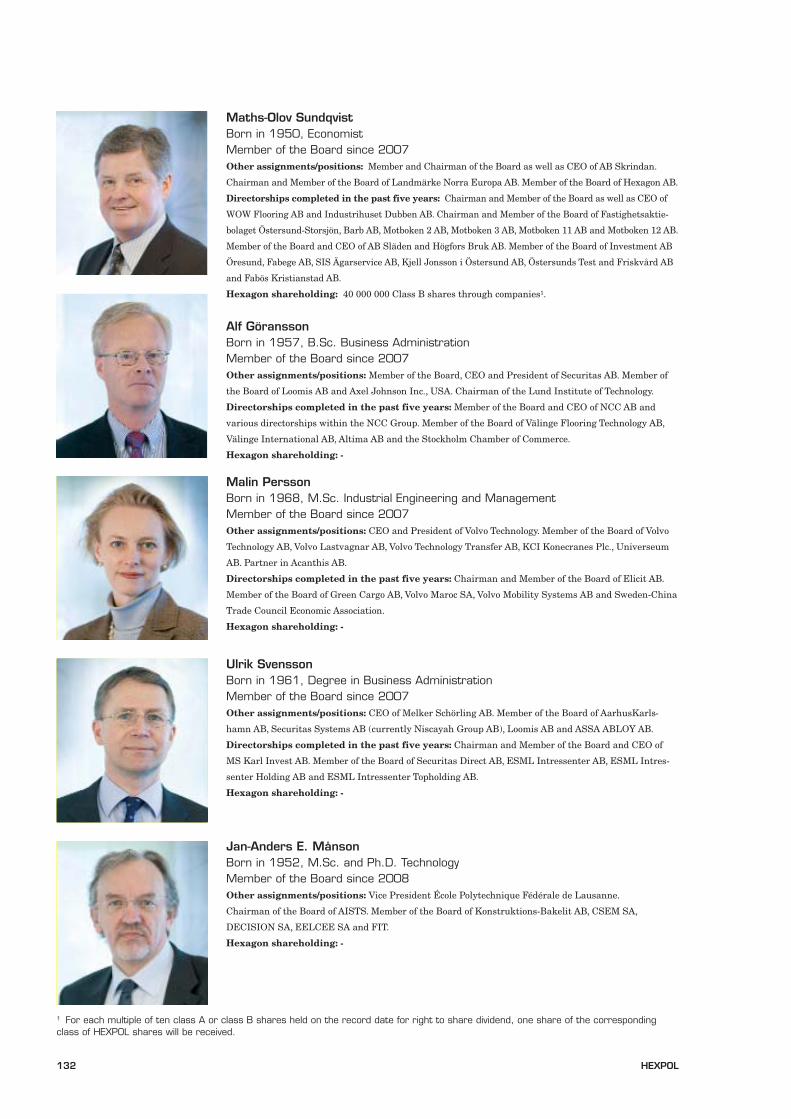

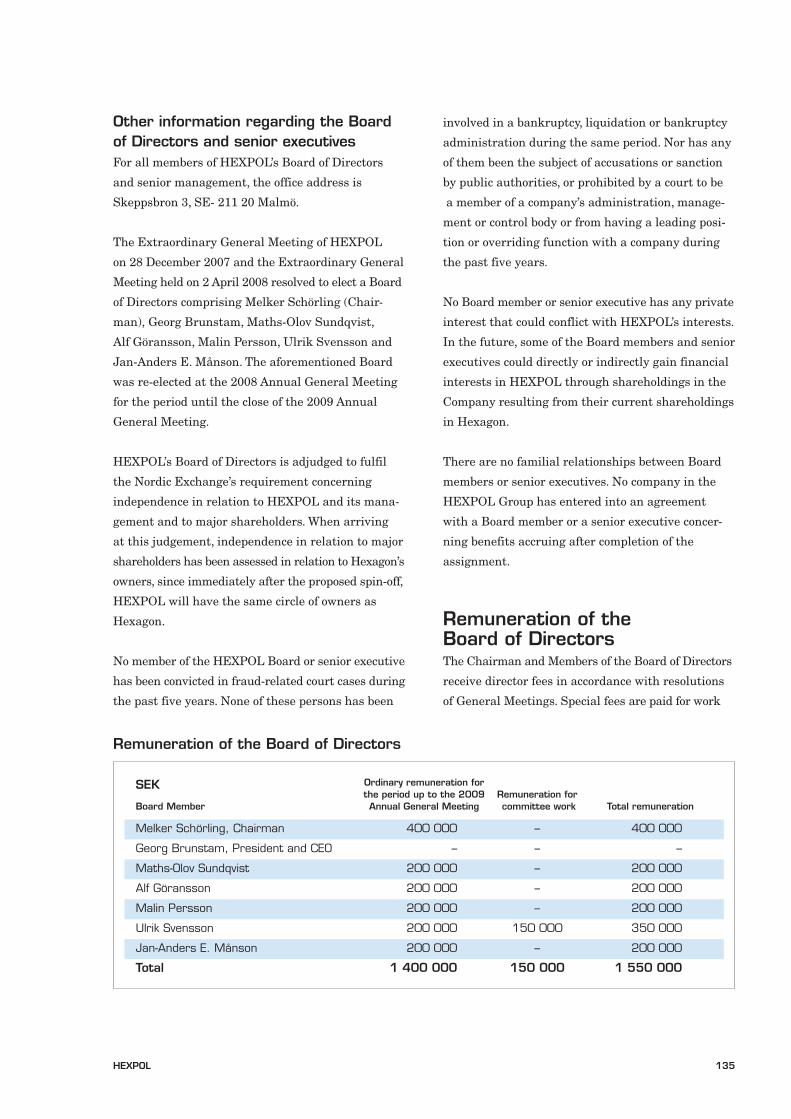

The Board of Directors’ composition,Group Management and auditorsThe Board of Directors of HEXPOL AB consists of

Melker Schörling (Chairman of the Board), Maths O.

Sundqvist, Alf Göransson, Malin Persson, Ulrik

Svensson, Jan-Anders E. Månson and Georg Brun-

stam. Group Management consists of Georg Brunstam

(CEO), Anders Lyrheden, Lars-Åke Bylander, Tracy

Garrison, Peter Kruk, Carsten Rüter and Ralph

Wolkener. All members of Group Management and

the Board of Directors have well-documented indust-

rial experience.

The Company’s auditor is Ernst & Young AB, with

Ingvar Ganestam as auditor-in-charge, and Stefan

Engdahl, Ernst & Young AB.

For additional information concerning the members

of the Board, Group Management and the Company’s

auditors, reference is made to pages 131–137.

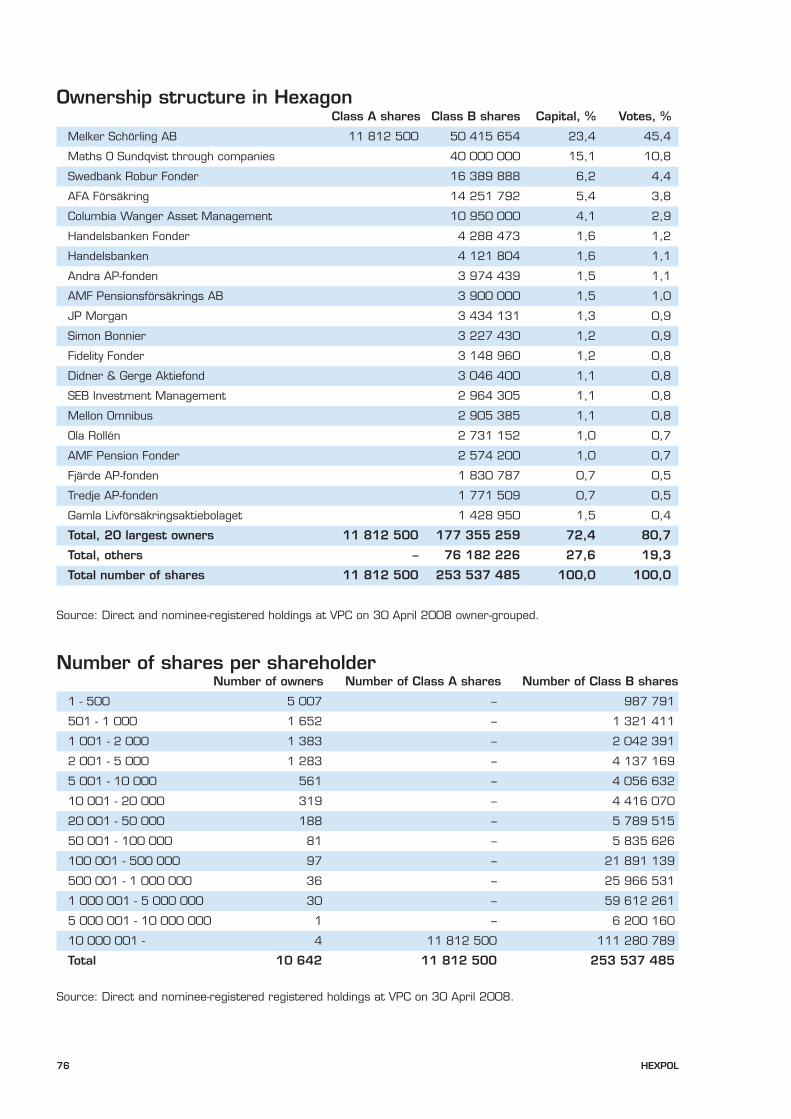

Major shareholdersImmediately after the distribution of the shares in

HEXPOL, the ownership structure of the Company

will be identical to that of Hexagon (apart from

share fractions). The number of shareholders in

Hexagon on 30 April 2008 was approximately

10,000, of whom the largest were Melker Schörling

AB, Maths O. Sundqvist, through companies, and

Swedbank Robur Fonder, which jointly accounted for

nearly 45 percent of the capital and approximately

60 percent of the voting rights.

For additional information concerning the ownership

structure, reference is made to pages 75–76.

HEXPOL 9

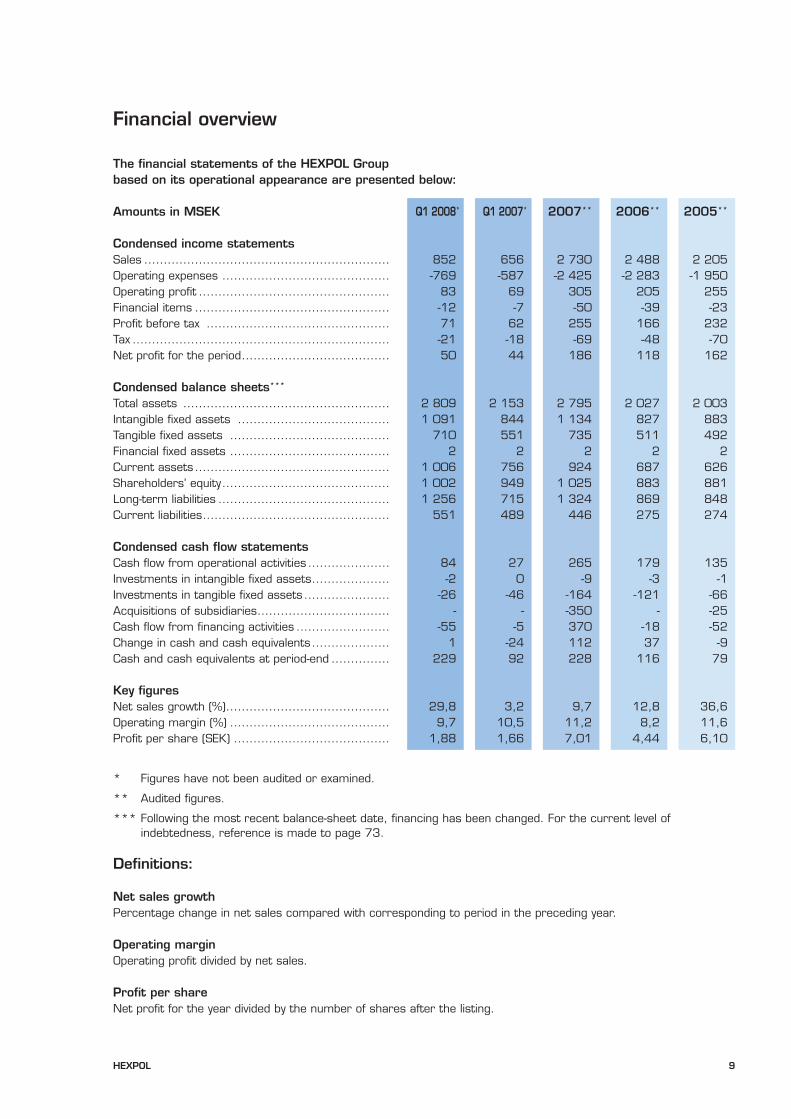

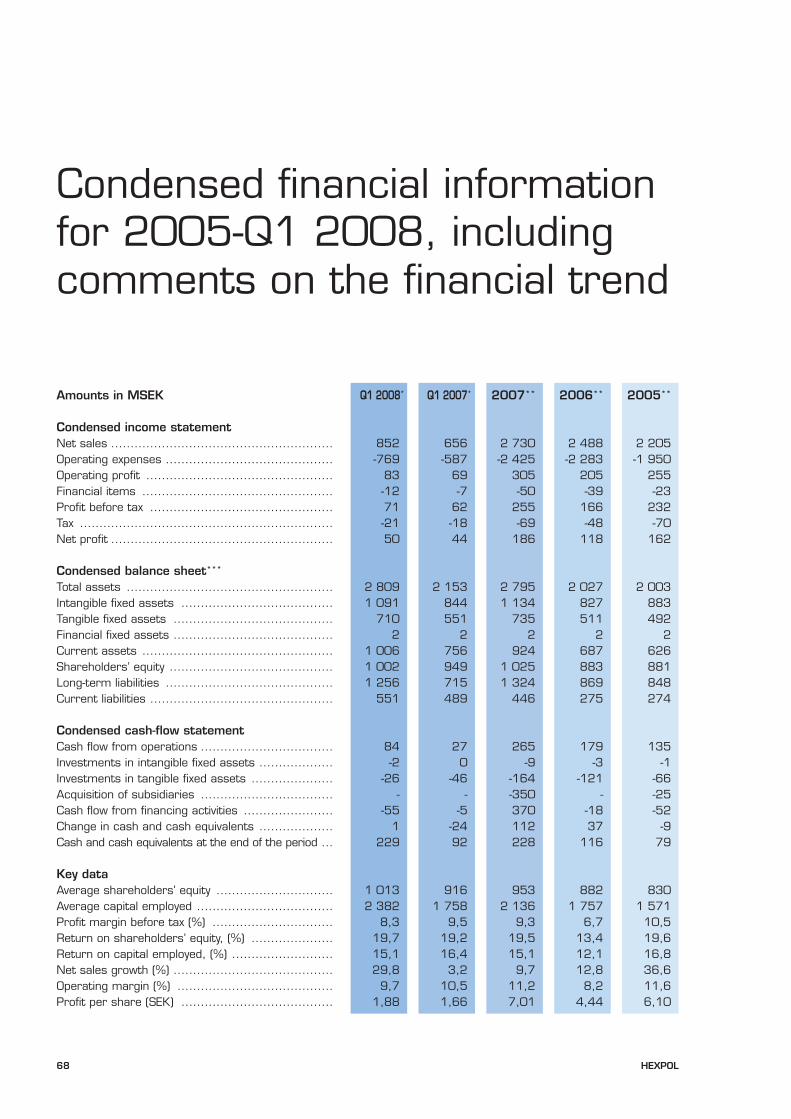

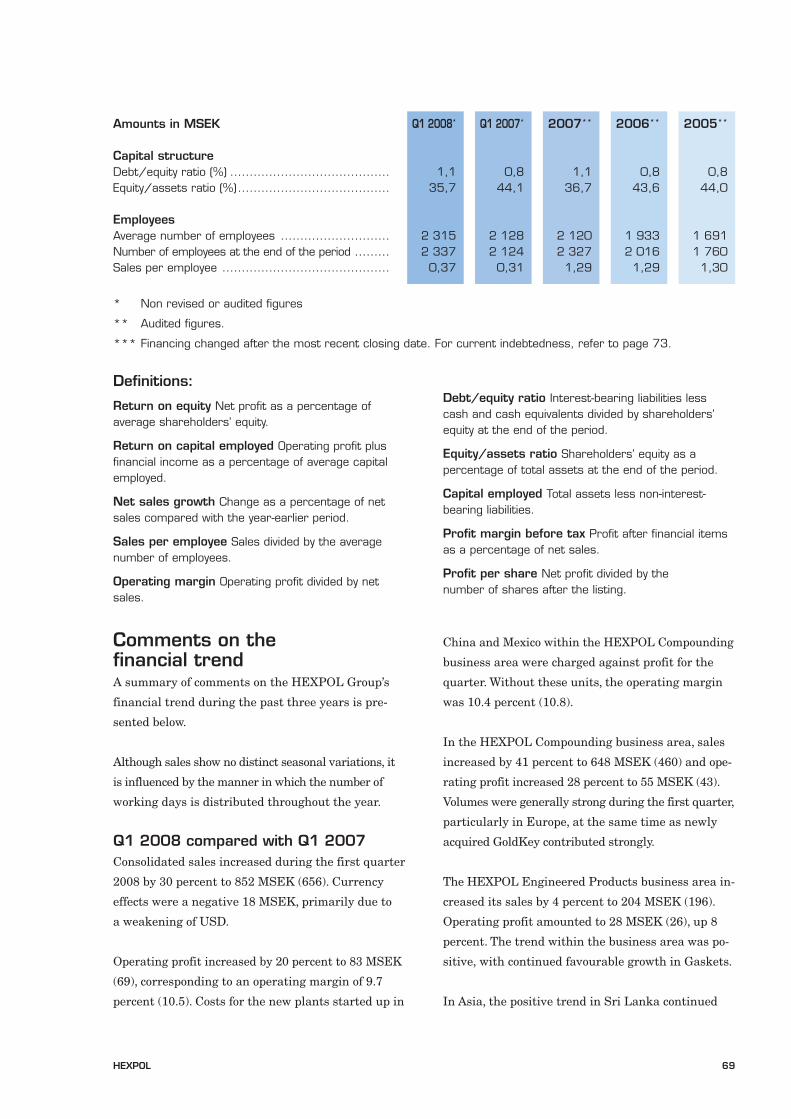

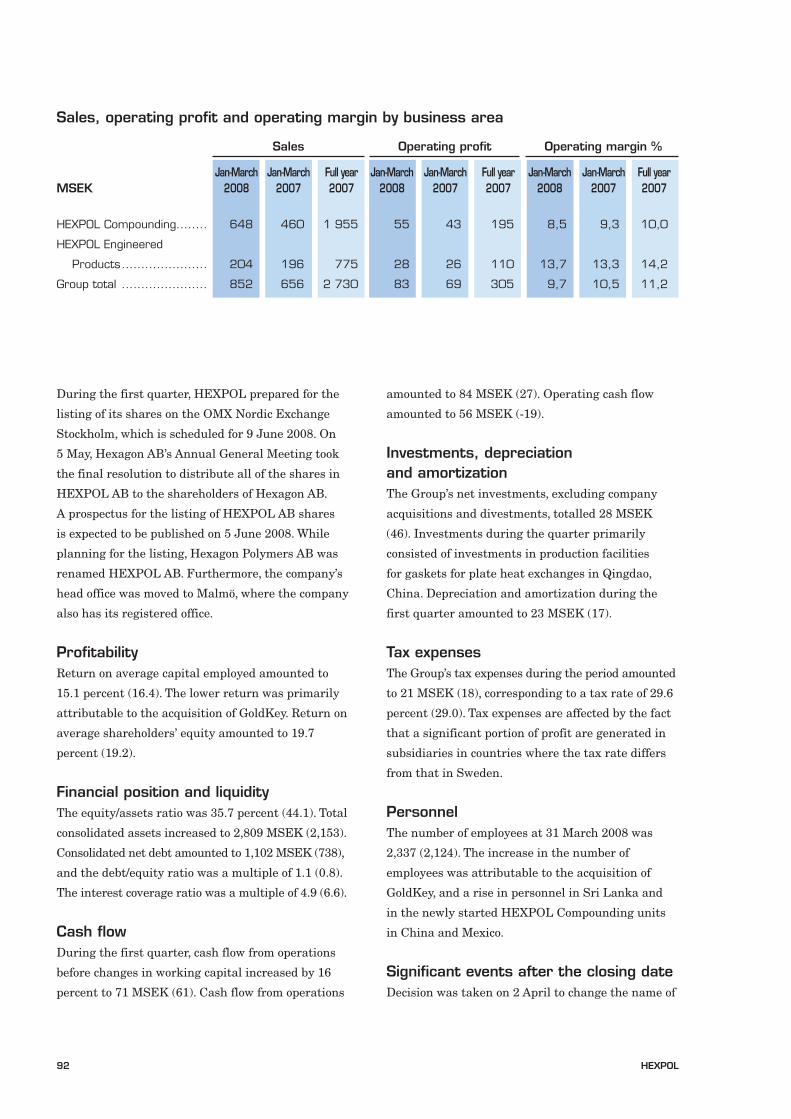

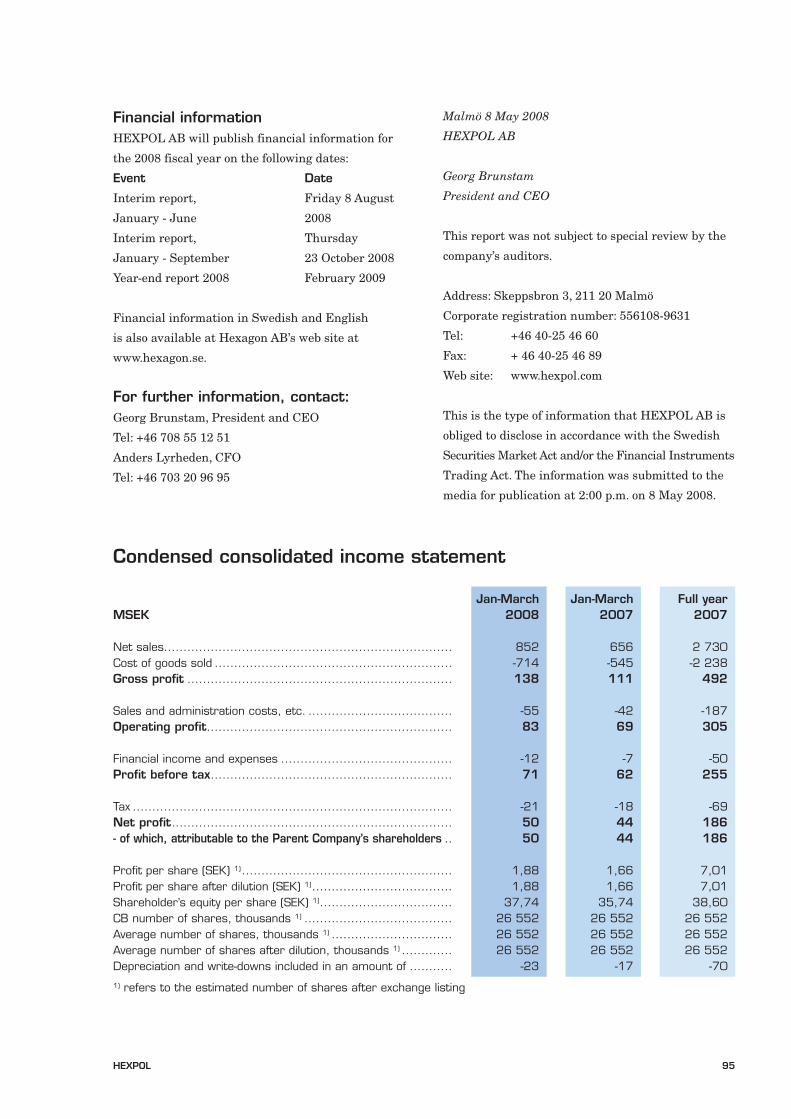

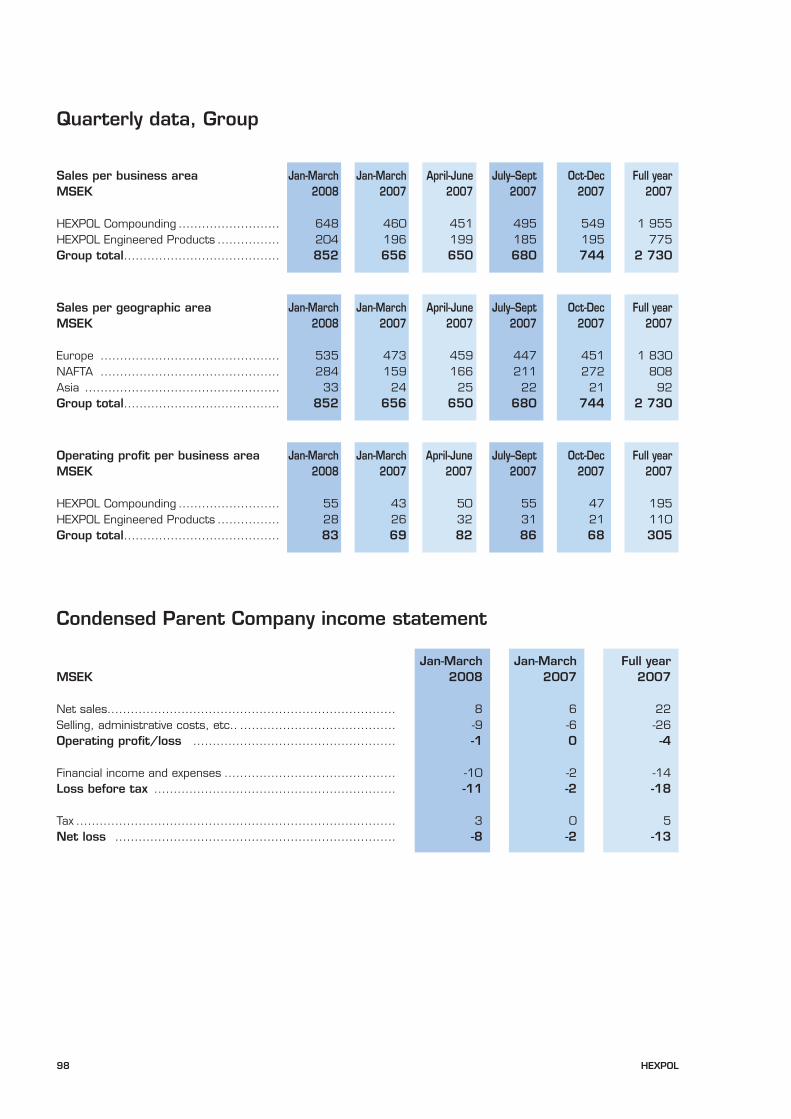

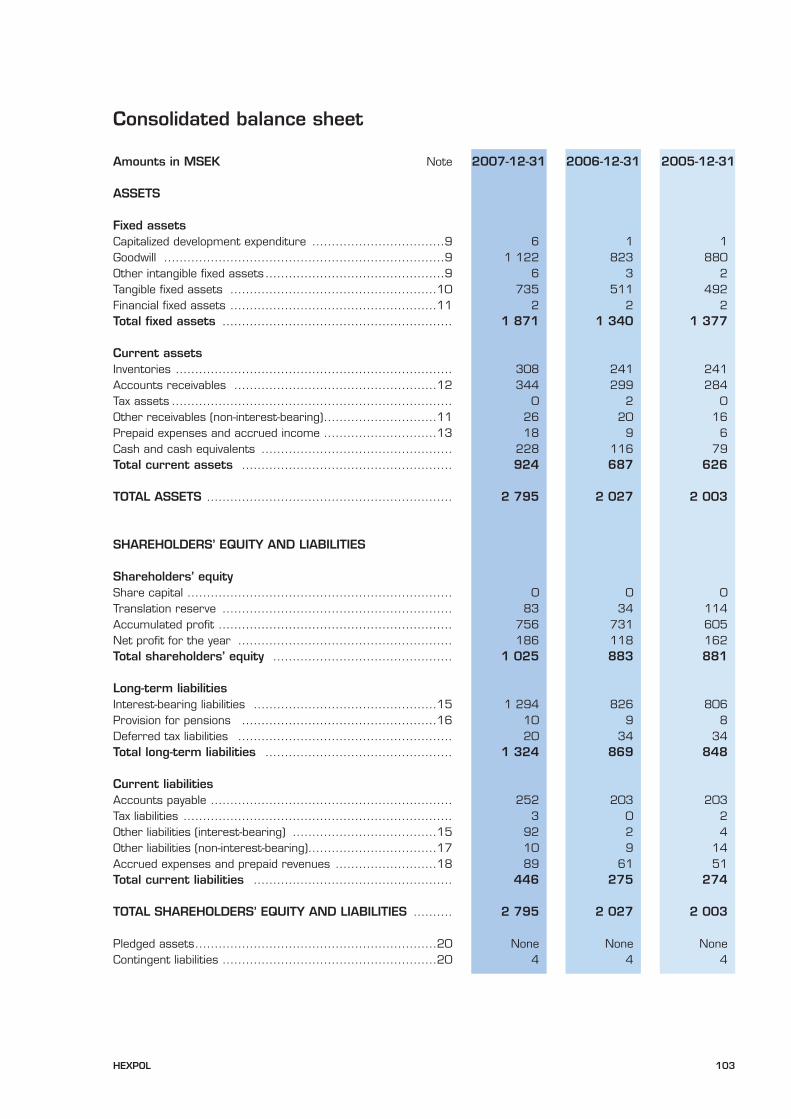

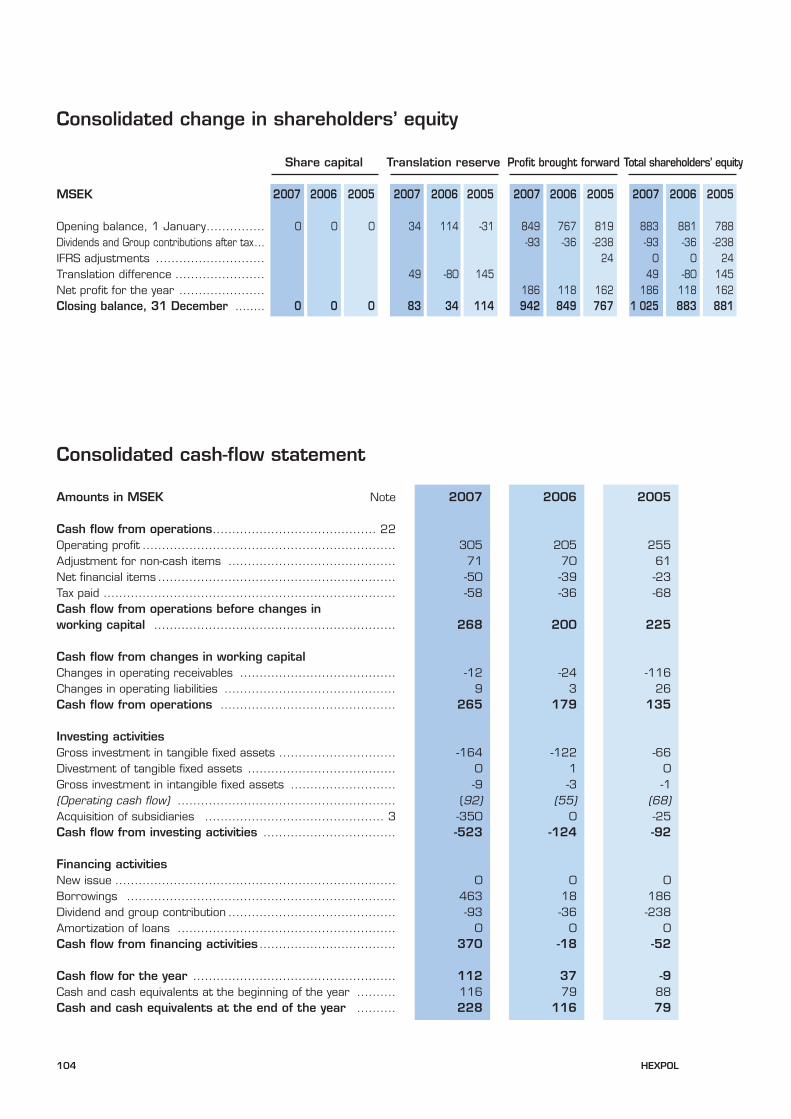

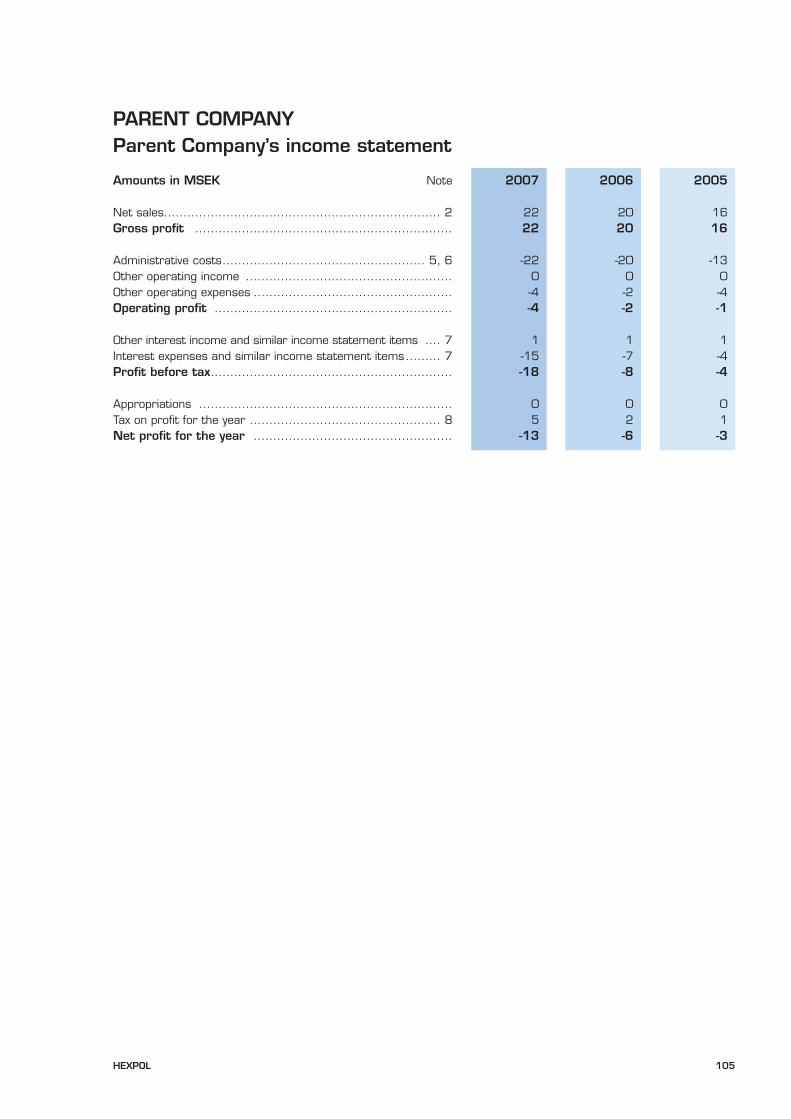

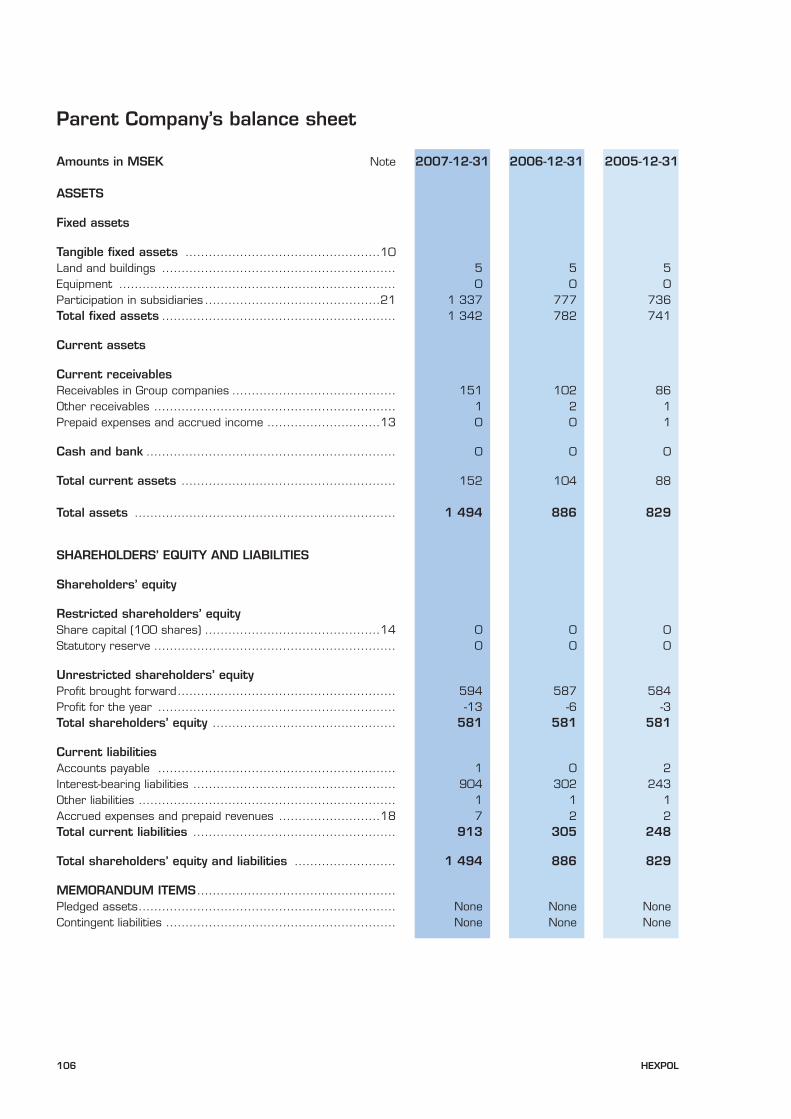

The financial statements of the HEXPOL Group based on its operational appearance are presented below:

Amounts in MSEK Q1 2008* Q1 2007* 2007** 2006** 2005**

Condensed income statementsSales ............................................................... 852 656 2 730 2 488 2 205Operating expenses ........................................... -769 -587 -2 425 -2 283 -1 950Operating profit ................................................. 83 69 305 205 255Financial items .................................................. -12 -7 -50 -39 -23Profit before tax ............................................... 71 62 255 166 232Tax .................................................................. -21 -18 -69 -48 -70Net profit for the period...................................... 50 44 186 118 162

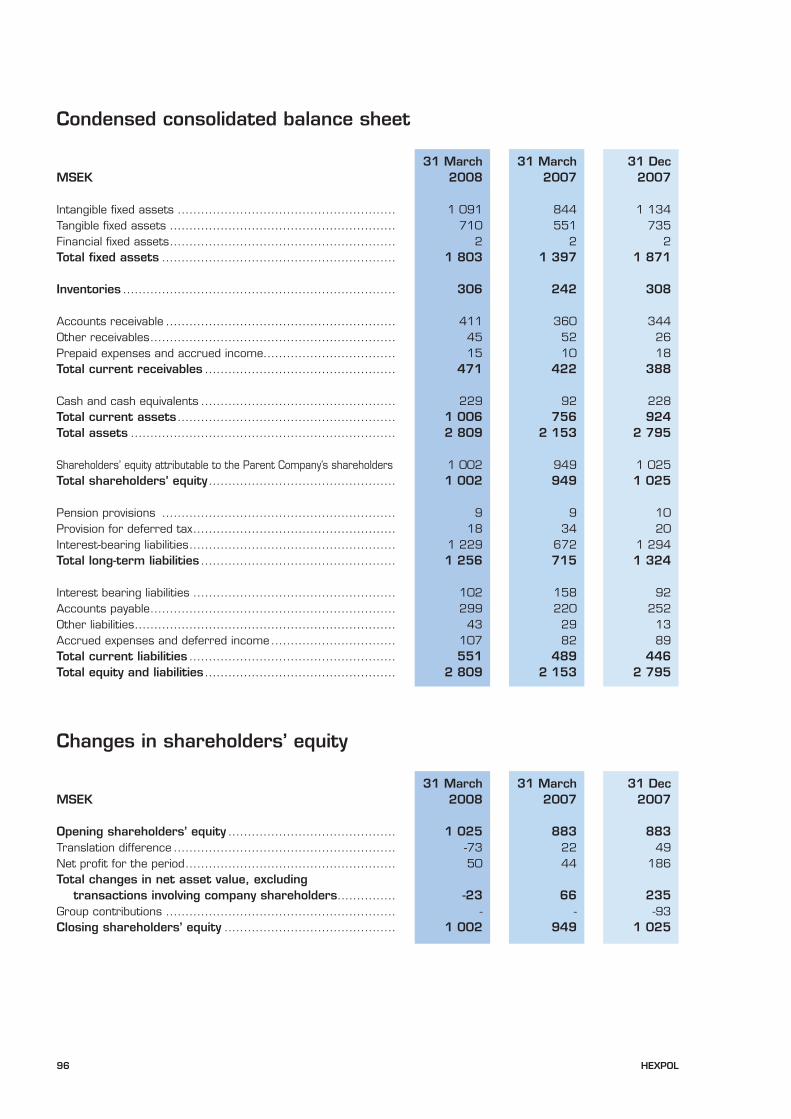

Condensed balance sheets***

Total assets ..................................................... 2 809 2 153 2 795 2 027 2 003Intangible fixed assets ....................................... 1 091 844 1 134 827 883Tangible fixed assets ......................................... 710 551 735 511 492Financial fixed assets ......................................... 2 2 2 2 2Current assets .................................................. 1 006 756 924 687 626Shareholders’ equity........................................... 1 002 949 1 025 883 881Long-term liabilities ............................................ 1 256 715 1 324 869 848Current liabilities................................................ 551 489 446 275 274

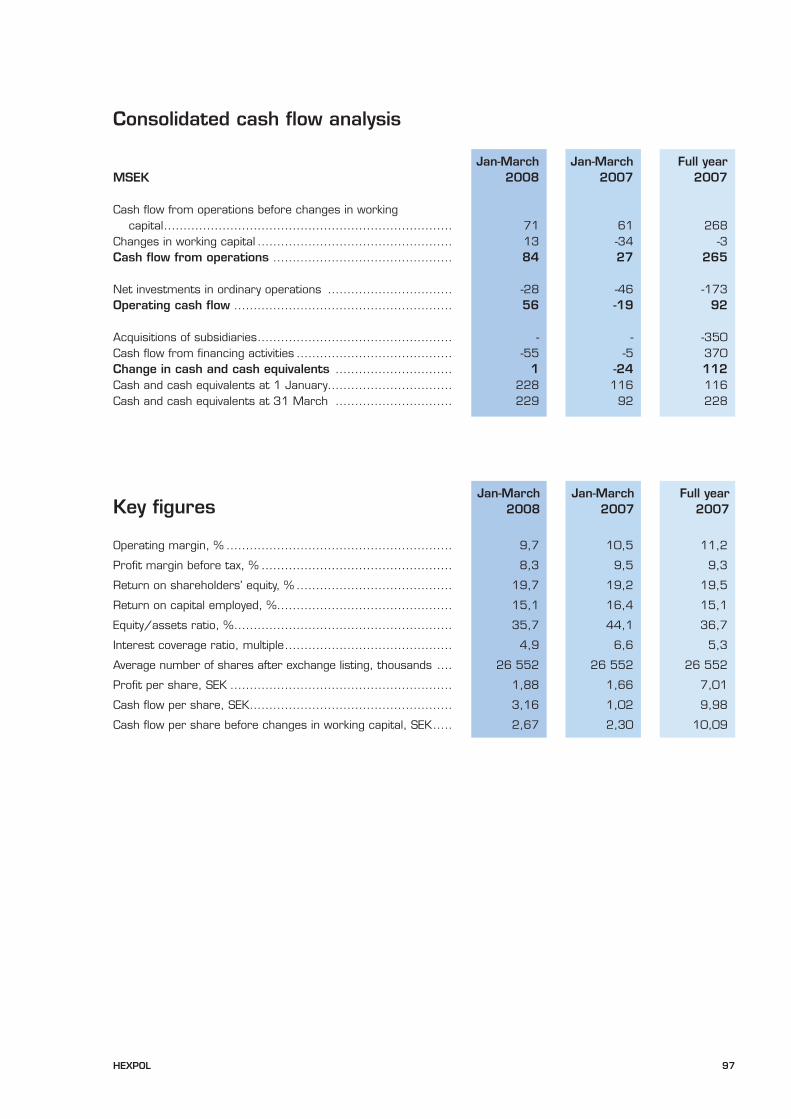

Condensed cash flow statementsCash flow from operational activities ..................... 84 27 265 179 135Investments in intangible fixed assets.................... -2 0 -9 -3 -1Investments in tangible fixed assets ...................... -26 -46 -164 -121 -66Acquisitions of subsidiaries.................................. - - -350 - -25Cash flow from financing activities ........................ -55 -5 370 -18 -52Change in cash and cash equivalents .................... 1 -24 112 37 -9Cash and cash equivalents at period-end ............... 229 92 228 116 79

Key figuresNet sales growth (%).......................................... 29,8 3,2 9,7 12,8 36,6Operating margin (%) ......................................... 9,7 10,5 11,2 8,2 11,6Profit per share (SEK) ........................................ 1,88 1,66 7,01 4,44 6,10

* Figures have not been audited or examined.

** Audited figures.

*** Following the most recent balance-sheet date, financing has been changed. For the current level of indebtedness, reference is made to page 73.

Financial overview

Definitions:

Net sales growthPercentage change in net sales compared with corresponding to period in the preceding year.

Operating marginOperating profit divided by net sales.

Profit per share Net profit for the year divided by the number of shares after the listing.

10 HEXPOL

HEXPOL 11

Ownership of shares is subject to risk. A number of

factors currently affect and could affect the opera-

tions conducted by the HEXPOL Group in either a

positive or negative direction. The risks that exist

concern conditions that are directly connected to

HEXPOL and ones that lack a specific connection to

HEXPOL but which still affect the industry in which

HEXPOL is active.

Here follows a brief and general overview of certain

risk factors that, according to HEXPOL’s Board of

Directors, could be of importance to the Company’s

future development or an investment in the HEXPOL

share.

The greatest risks include the general market trend,

the competitive situation, the future price trend,

customer relations, the ability to retain and recruit

key personnel and financial risks. The risk factors

are described without any internal ranking and the

account does not claim to be exhaustive. This

means that there could be additional risks that

could be of greater of lesser importance to

HEXPOL’s operations.

In addition to the risk factors specified below and

other risks that pertain, the reader should also

carefully consider other information in this prospectus.

Risk factors

Industry and market risksThe HEXPOL Group engages in worldwide opera-

tions that are dependent on both the general economic

and political situation in the world and conditions

that are unique for a certain country or region.

Risk management within the Group is determined

by established policies and procedures that are revised

continuously by the Board of Directors. The Parent

Company’s Board has overall responsibility for

identifying, following up and managing risks.

Impact of the economyAs is the case for almost all business operations,

the general economic climate affects the investment

inclination and investment ability of HEXPOL’s

existing and potential customers. Accordingly, a

weak economic trend in all or parts of the world

could result in lower-than-expected market growth.

Developments in HEXPOL’s customer segments

constitute one of the principal risks related to the

business environment. This results in stringent

demands in terms of understanding of the current

and future requirements, demands and wishes of

both direct and end customers. To reduce the risk

of economic impact, HEXPOL engages in close

cooperation with customers, conducts comprehensive

business intelligence work and continuously reviews

its selected strategies. Although HEXPOL’s operations

have a wide geographic spread, and otherwise an

extensive customer base, HEXPOL’s sales and

operations are exposed to a potential risk of being

adversely affected by a weak economic trend.

Competition and price pressureHEXPOL’s operations are conducted in sectors subject

to competition and are thus affected by, for example,

severe price pressures, which in turn drive demand

for cost-effective solutions. Competing companies

with operations in Asia and other low-cost regions

may, through improvements of their technology and

12 HEXPOL

production expertise, come to produce at low cost

and compete with HEXPOL’s products. HEXPOL’s

future competitive capacity is dependent on its ability

to utilize the Company’s leading-edge knowledge

with respect to rubber compounds and rubber and

plastic products and to transform this knowledge

into attractive products and customized solutions at

competitive prices. To ensure the Company’s compe-

titiveness, investments will be required to maintain

the Group’s prominent position in the area of product

development. While constantly striving to adapt to

changes in the competitive situation, HEXPOL may

also be forced to implement costly restructuring

measures to be able to retain the Company’s market

position and profitability.

Strategic and operational risksHEXPOL’s business is dependent on a number of

factors, each of which may significantly affect the

Group’s profits both positively and negatively.

Technical and market developmentPortions of HEXPOL’s operations are conducted in

industries subject to price pressure and rapid tech-

nical and material developments. To reduce these

risks, HEXPOL’s ability to compete in this market

environment by developing new products that offer

improved functionality while reducing costs for new

and existing products is of great importance. Being

able to attract the right competence for research,

product development, marketing and sales is critical

for success.

Costs of raw materials and energyIn recent years, trends in many raw materials markets

have resulted in higher purchasing prices for raw

materials that are important for HEXPOL. To coun-

ter continued increases in raw materials prices and

increased energy costs, HEXPOL devotes considerable

effort to increasing production efficiency, developing

more cost-effective processes and passing on price

increases to customers. Given the competitive market

situation, however, there is a risk that HEXPOL

cannot increase prices enough to fully offset the

increased costs, thus resulting in reduced margins.

SuppliersHEXPOL’s products consist of raw materials and

goods from several different suppliers. To be able to

manufacture, sell and deliver products, HEXPOL

is dependent on external supplies meeting agreed

requirements with respect to quantity, quality and

delivery time, for example. Incorrect, delayed or

missing deliveries from a company supplier may in

turn mean that HEXPOL’s deliveries are delayed,

deficient or incorrect, which could result in reduced

sales and a negative impact on the Group’s profits.

In HEXPOL’s assessment, the Company is not

dependent on any single supplier, meaning that

interruption of deliveries would not result in any

long-term consequences for HEXPOL’s operations.

No single supplier accounts for more than 12 per-

cent of the Group’s purchases, and all major

suppliers are further replaceable.

CustomersHEXPOL’s operations are conducted in a large

number of geographic markets with many customer

categories. No single customer accounts for more

than 10 percent of the Group’s total sales. HEXPOL

is thus not dependent on any single customer and

therefore has a favourable risk spread in this respect.

The largest single group of customers are system supp-

liers to the automotive industry. For HEXPOL this

customer group may imply certain risks. A decline or

a weak trend in the automotive industry may have a

negative effect on HEXPOL’s business. In the Com-

pany’s assessment, however, the division of the auto-

motive industry in different segments in combination

with the industry’s geographic diversity entails a

more limited overall risk exposure than what the

volume collective sales to the automotive industry

might give the impression of.

Political risksHEXPOL’s operations in Sri Lanka may be affected

by the ongoing armed conflict. HEXPOL follows

developments in Sri Lanka continuously and has

developed an action plan to be able to counter the

risks that an unstable political development in

HEXPOL 13

Sri Lanka may entail for HEXPOL’s operations in

the country.

Key personnelHEXPOL’s future success is in large part dependent

on its ability to recruit, retain and develop qualified

leaders and other key persons. Being an attractive

employer is thus an important success factor. If key

persons leave the Company and appropriate succes-

sors cannot be recruited, this may have a negative

effect on the Company’s operations.

Legal risksThrough its global operations, HEXPOL is affected

by a number of laws, directives, regulations, agreements

and guidelines, including many that relate to the

environment, health, safety, trade restrictions, compe-

tition legislation and currency regulation.

Legislation and regulationTo counter the legal risks, HEXPOL closely monitors

the rules and regulations applying in each market

and works to quickly adapt its operations to identified

future changes in this area. However, changes in

legislation, customs regulations and other obstacles

to trade, price and currency controls and other

government guidelines in the countries in which

HEXPOL operates may limit the Group’s operations.

Health, safety and the environmentIn HEXPOL’s assessment, operations are conducted

in all significant respects in compliance with appli-

cable laws and regulations regarding health, safety

and the environment. A number of companies within

the Group conduct operations that are subject to

permits or reporting obligations according to local

environmental legislation. These operations are thus

under the supervision of due authorities. HEXPOL

strives to continuously ensure that all material

permits are obtained and that all material appli-

cable reporting obligations are fulfilled. Changes in

legislation and regulation by the authorities entailing

tougher requirements and changes in terms relating

to health, safety and the environment or a trend

toward more stringent application of laws and regu-

lations by the authorities may require further invest-

ments and result in increased costs and other obliga-

tions for the companies within the Group that are

subject to such regulation. Changes in legislation and

official regulations may also prevent or limit HEXPOL’s

operations.

Tax risksHEXPOL conducts its operations through companies

in a number of countries. Its business, including

transactions between Group companies, is conducted

in accordance with the Company’s interpretation of

prevailing tax legislation, tax agreements and regu-

lations in the various countries and tax authorities

in question. The Company has obtained advice in

these matters from independent tax advisors.

However, it cannot be generally ruled out that the

Company’s interpretation of applicable laws, tax

agreements and regulations or their interpretation

or administrative application by the authorities is

deemed incorrect or that such rules may change,

possibly with retroactive effect. HEXPOL’s tax

situation may change through decisions by the

relevant authorities.

DisputesHEXPOL is occasionally involved in disputes in the

course of its normal business operations. Major and

complicated disputes may be costly and demanding

in terms of time and resources and could interfere

with the normal business operations. Neither can it

be ruled out that the result of such disputes could

have a negative impact on HEXPOL’s profits and

financial position.

Intellectual property rightsHEXPOL has entered into an agreement with Hexagon

regarding continued use of the name “Hexagon” in

combination with the word “Polymers” in the names

of certain subsidiaries within the HEXPOL Group.

If certain events specified in the agreement occur,

including changes in control over HEXPOL or changes

in HEXPOL’s area of operations, HEXPOL is obligated

to ensure that the use of the Hexagon name is dis-

continued prematurely. This could result in a tempo-

14 HEXPOL

rary negative effect for HEXPOL until new company

names for the subsidiaries in question are established

in the market.

Under a licensing agreement with Bayer AG, HEXPOL

is entitled to use the Vulkollan brand and logotype

in connection with wheel manufacturing and marketing

within HEXPOL Wheels. The licensing agreement is

valid for periods of one year at a time and can be ter-

minated following three-month notice. Termination

of the licensing agreement by Bayer would have an

adverse impact, since Vulkollan wheels currently

account for a large portion of the subsidiary Stellana

AB’s sales.

HEXPOL sells products under several well-known

brands. It is of great commercial importance for the

Group that these brands can be protected against

unauthorized use by competitors and that the good-

will associated with the brands can be maintained.

To meet market requirements, HEXPOL must

continuously develop new technical solutions and

applications. To guarantee a return on the resources

that HEXPOL invests in research and development,

it is of the utmost importance that such new techno-

logy can be protected against unauthorized use by

competitors.

It is not certain that applications for protection of

patents, brands and other intellectual property

rights will be granted or, if they are granted, that

they will provide satisfactory protection that cannot

be circumvented by competitors. Neither is there

any guarantee that HEXPOL will not be considered

to infringe on other companies’ intellectual property

rights or that HEXPOL’s rights will not be questioned

or contested by others. In addition, HEXPOL’s com-

petitors may develop or acquire intellectual property

rights that may prove to be essential for portions

of HEXPOL’s operations. Furthermore, HEXPOL

depends on know-how that falls outside the realm

of protectable intellectual property rights. It cannot

be ruled out that competitors may develop the corre-

sponding know-how or that HEXPOL will not succeed

in protecting its expertise effectively.

If it should prove to be the case that HEXPOL’s

operations are considered to infringe on another

party’s valid intellectual property rights or entail

impermissible use of another party’s business secrets,

it cannot be ruled out that the resulting claims may

have a negative effect on HEXPOL’s profits and

financial position.

Financial risksIn its capacity as a net borrower and through its

extensive operations outside Sweden, HEXPOL is

exposed to various financial risks. The Group’s

financial policy provides guidelines for financial

exposure and how these risks are to be managed

within the Group. The financial policy is established

each year by the Board of Directors.

HEXPOL’s financial operations are centralized in

the Group’s internal bank, which is responsible for

coordinating currency and interest exposure. The

internal bank is also responsible for the Group’s

external and internal financing. Centralization

results in significant economies of scale, lower

financing costs and better control and management

of the Group’s financial risks. The internal bank

does not have any mandate to conduct commercial

trading with currency or interest instruments.

Credit risk at the customer level is managed by the

relevant subsidiary.

Currency riskIn its operations, HEXPOL is exposed to various

financial risks, of which the currency risk is the domi-

nant one. Currency fluctuations affect HEXPOL’s

profits in part when sales and purchases take place

in different currencies (transaction exposure) and in

part when the income statements and balance sheets

of foreign subsidiaries are translated to Swedish

kronor, SEK (translation exposure).

HEXPOL’s net flows in foreign currency amounted

to about 362 MSEK in 2007. Contracted currency

flows are hedged in their entirety. Expected flows

in excess of contracted flows are hedged by between

40 and 75 percent with a horizon of twelve months.

The Group’s translation exposure is managed

HEXPOL 15

through currency hedging via loans or forward

contracts in the currency of the net asset.

Interest riskHEXPOL is also affected by interest rate fluctuation.

Changes in interest rates affect the Group’s net inte-

rest income and/or cash flow. Based on the average

interest-rate period in the Group’s total loan port-

folio at 31 December 2007, a simultaneous change

of one percent in all of HEXPOL’s loan currencies

would have an effect on full-year profit of about

10 MSEK before tax. This is also deemed to reflect

the situation for the current year.

Credit riskThe financial risks to which HEXPOL is exposed

also include credit risks, meaning the risk that a

customer or other business party will not be able

to settle his obligations to HEXPOL. There is no

significant concentration of credit risks, either

geographically or to any given customer segment.

Acquisitions and financing of acquisitionsHEXPOL has long worked with an active acquisition

strategy, resulting in a number of successful acquisi-

tions. Strategic acquisitions will also be a part of the

growth strategy in the future. It cannot be guaranteed,

however, that HEXPOL will be able to find suitable

acquisition targets nor can it be guaranteed that the

necessary financing for future acquisition targets

can be obtained on terms that are acceptable for the

Company. This may result in reduced or declining

growth for HEXPOL.

The completion of acquisitions also entails risks. In

addition to the Company-specific risks, the acquired

company’s relations with customers, suppliers and

key persons may be affected negatively. There is also

a risk that integration processes may prove more

costly or take more time than estimated and that

anticipated synergies in whole or in part fail to

materialize.

Future capital requirementsIn the assessment of HEXPOL’s Board of Directors,

the Group’s future financial position is favourable,

and its operations generate strong cash flow under

normal market conditions. If the Group’s develop-

ment deviates from what is anticipated, it cannot,

however, be ruled out that a situation may arise in

the future in which new capital must be raised.

There is no guarantee that HEXPOL will be able

to raise the necessary capital on terms that are

favourable for the Company. In this respect, also the

general market conditions for raising capital are of

considerable importance.

Equity market risks

Share price performancePrior to the distribution of HEXPOL, no trading has

occurred in the HEXPOL share. Although an appli-

cation has been submitted for a listing of HEXPOL’s

B share on the OMX Nordic Exchange Stockholm, no

guarantees can be made regarding the share’s liquidity.

Neither are there any guarantees that the share

price will perform positively. Factors affecting the

share price include variations in the Company’s

profits and financial position, changes in the stockmar-

ket’s expectations regarding future profits, supply

and demand for the shares, developments in the

Company’s market segments and general economic

trends. This means that the price at which the share

trades will vary and that, even if HEXPOL’s business

develops positively, investors may risk incurring a

loss of capital when the shares are sold.

Cost base as an independent listed companyPrior to the distribution of the shares in HEXPOL,

the Company is a wholly owned subsidiary of the lis-

ted company Hexagon AB. HEXPOL thus has a

limited history on which the Group can be assessed

and has not previously had any direct responsibility

for corporate governance, financial reporting and the

publication requirements to which listed companies

are subject. As a listed company, HEXPOL may be

affected by increased costs for which the Company

has not previously been directly responsible. This

increase is estimated at between 3 and 5 MSEK.

16 HEXPOL

Future dividendsFuture dividends will be proposed by HEXPOL’s

Board of Directors. In its assessment, the Board of

Directors will take into consideration several factors,

including business development, profits, cash flow,

financial position and expansion plans. See also the

section Dividend policy on page 28. There are risks

that may affect the Company’s profits negatively,

and there are no guarantees that HEXPOL will be

able to generate profits that permit a dividend

to the shareholders during each fiscal year in

the future.

HEXPOL 17

18 HEXPOL

HEXPOL 19

The Board of Directors of HEXPOL, headquartered in Malmö, is responsible for the information in this prospectus.

Assurance is hereby given that all reasonable precautions have been taken to ensure that the information in

this prospectus, to the best of the knowledge of the Board of Directors of HEXPOL, complies with actual

conditions and that nothing has been omitted that could impact its meaning.

Malmö, 22 May 2008

HEXPOL AB (publ)

Board of Directors

Background and reasonsThe shareholders of Hexagon resolved at the

Annual General Meeting of Hexagon on 5 May 2008

to distribute all of the shares of HEXPOL to the

shareholders of Hexagon in the form of a dividend.

The intention is that the Class B HEXPOL shares

will be listed on the OMX Nordic Exchange Stock-

holm, with 9 June 2008 as the first day of trading.

A separate listing of HEXPOL is a natural step in

the development of the operations of Hexagon and

HEXPOL. During recent years, HEXPOL has evolved

from a local Nordic player to a rapidly growing group

of companies with global manufacturing and global

customers. The Company is currently a world leader

in advanced rubber compounds and gaskets for plate

heat exchangers, and is also one of the leading players

in the global market for the manufacture of poly-

urethane, plastic and rubber wheels.

The reason for a separate listing of the polymer

operations is that HEXPOL has reached a size

and level of profitability that makes the business

attractive as an independently listed company.

The spin-off will enable the management and Board

of Directors of both Hexagon and HEXPOL to capi-

talize on the operational and strategic opportunities

that arise in each company, including increased

potential to continue to grow via the establishment

of new operations and the acquisition of companies.

HEXPOL has sufficient resources in terms of manage-

ment, administration, operational control and busi-

ness development, and is thus ready to continue to

develop as an independent company.

As an independent company, HEXPOL can apply a

focused and well-adapted growth strategy, with an

organization and capital structure that supports this

growth.

In the opinion of the Board of Directors of Hexagon,

the long-term value for the shareholders will increase

through a spin-off of the operation and the distribu-

tion of the shares in HEXPOL. A separate market

listing of HEXPOL will further enable both current

and new shareholders to choose to invest directly in

HEXPOL.

20 HEXPOL

SVER

IGES RIKSBANK

SVER

IGES RIKSBANK

RIKSBANK

SVER

IGES RIKSBANK

SVER

IGES RIKSBANK

RIKSBANK

SVER

IGES RIKSBANK

RIKSBANK

100 Hexagon shares

5,000 Hexagon shares

343 Hexagon shares

8 Hexagon shares

10 HEXPOL shares

500 HEXPOL shares

34 HEXPOL shares

A cash amount corresponding to the sales proceeds for

0.3 HEXPOL shares

A cash amount corresponding to the sales proceeds for 0.8 HEXPOL shares

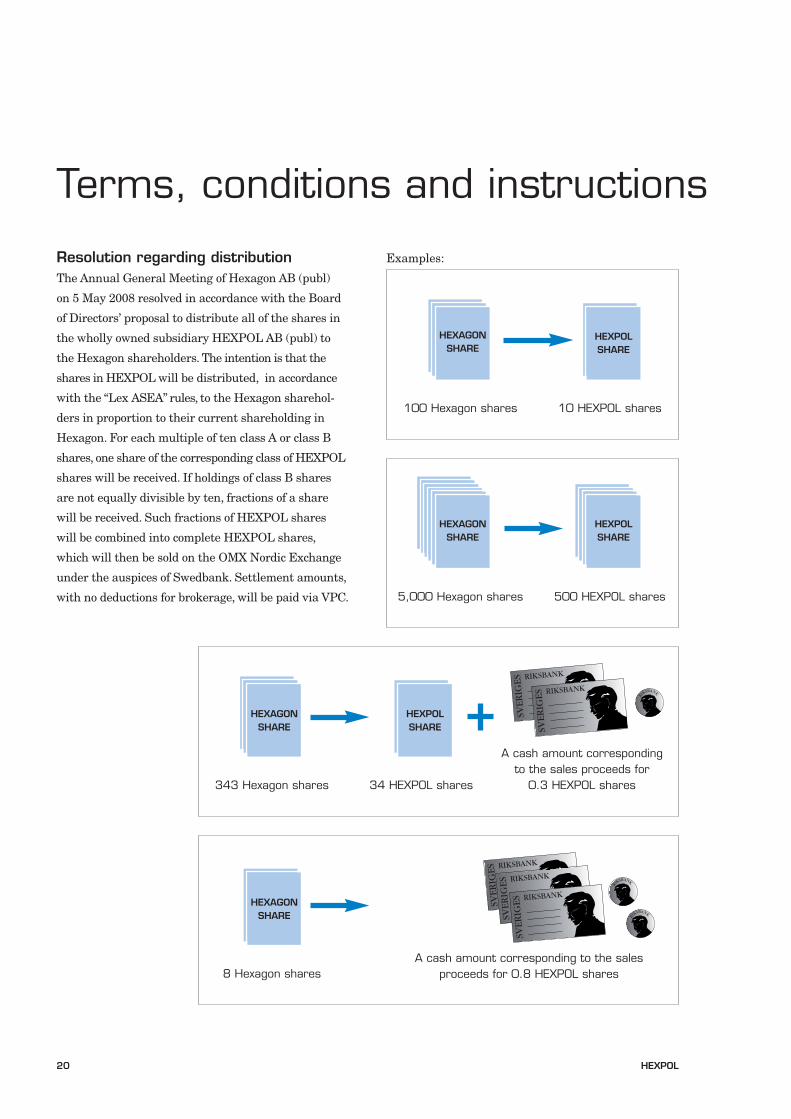

Resolution regarding distributionThe Annual General Meeting of Hexagon AB (publ)

on 5 May 2008 resolved in accordance with the Board

of Directors’ proposal to distribute all of the shares in

the wholly owned subsidiary HEXPOL AB (publ) to

the Hexagon shareholders. The intention is that the

shares in HEXPOL will be distributed, in accordance

with the “Lex ASEA” rules, to the Hexagon sharehol-

ders in proportion to their current shareholding in

Hexagon. For each multiple of ten class A or class B

shares, one share of the corresponding class of HEXPOL

shares will be received. If holdings of class B shares

are not equally divisible by ten, fractions of a share

will be received. Such fractions of HEXPOL shares

will be combined into complete HEXPOL shares,

which will then be sold on the OMX Nordic Exchange

under the auspices of Swedbank. Settlement amounts,

with no deductions for brokerage, will be paid via VPC.

Examples:

HEXAGONSHARE

HEXPOLSHARE

Terms, conditions and instructions

HEXAGONSHARE

HEXPOLSHARE

HEXAGONSHARE

HEXPOLSHARE

HEXAGONSHARE

HEXPOL 21

Record dateThe record date at VPC for determining the share-

holders that will be entitled to receive HEXPOL

shares is 5 June 2008. The final day of trading in

Hexagon shares including rights to the distribution

of HEXPOL shares is 2 June 2008. The shares in

Hexagon will be traded ex-rights to HEXPOL shares

as of 3 June 2008.

Receipt of sharesThose persons who on the record date are registered

in the share register of shareholders in Hexagon

maintained by VPC will receive HEXPOL shares

without having to take any action. On the day after

the record date, the HEXPOL shares will be available

in the shareholders’ VP accounts (or in the VP accounts

belonging to those that in some other manner are

entitled to distribution). Subsequently, VPC will

send a VP notice stating the number of shares that

are registered in the recipient’s VP account.

Nominee-registered shareholdingsShareholders whose holdings in Hexagon are nominee-

registered by a bank or other nominee will receive

no issue report. Instead, notification will be sent in

accordance with the directions of the respective

nominee.

ListingThe Board of Directors of HEXPOL has applied for

a listing of the Company’s class B share on the OMX

Nordic Exchange Stockholm. The first day of

trading is expected to be 9 June 2008. The ISIN code

for Class B HEXPOL shares is SE0002452623. The

Company’s ticker on the OMX Nordic Exchange

Stockholm will be HPOL B. HEXPOL does not intend

to apply for a listing of the HEXPOL share on any

other exchange or marketplace. Nor does the Com-

pany intend to register the shares under the United

States Securities Act of 1933 or any other foreign

equivalent, or take any actions that would subject

HEXPOL to the reporting requirements of the SEC

(United States Securities and Exchange Commission).

Right to dividendsThe HEXPOL shares carry entitlement to dividends

as of the 2008 financial year. Payment of any dividend

will be executed by VPC or, if the shares are nominee-

registered, in accordance with the procedures of the

particular nominee.

AdvisorIn connection with the distribution and listing of

HEXPOL shares, Swedbank Markets is serving as

the issuer agent and financial advisor to

Hexagon and HEXPOL.

Important dates

2 June 2008 Final day of trading in Hexagon shares including rights to the distribution

of HEXPOL shares

3 June 2008 Hexagon shares traded ex-rights to HEXPOL shares

5 June 2008 Record date for receipt of HEXPOL shares

5 June 2008 Publication of listing prospectus

9 June 2008 Estimated date for the listing of class B HEXPOL shares on OMX Nordic

Exchange Stockholm

22 H

HEXPOL 23

CEO’s statement

Very strong growth with good profitabilityHEXPOL is one of the world’s leading polymer Groups

with strong global market positions in advanced

rubber compounds (Compounding), gaskets for plate

heat exchangers (PHE Gaskets) and wheels made of

polyurethane, plastic and rubber materials for fork-

lifts and castor wheel applications (Wheels). The opera-

tions are organized in two business areas – HEXPOL

Compounding and HEXPOL Engineered Products.

With our global presence, we have strong positions

in these areas. Our customers are mainly system

suppliers to the global automotive industry and

OEM manufacturers of plate heat exchangers and

forklift trucks.

HEXPOL is the new name of Hexagon’s former

Hexagon Polymers business area. The operations

originated as the Technical Products Division of

Svenska Gummifabriks AB in Gislaved, which created

the core of a niche-based growth strategy in polymer

products. Growth has been very strong under

Hexagon’s ownership, which started in 1994. Sales

in 1997 amounted to 350 MSEK; 10 years later, sales

had risen to 2,730 MSEK and, based on the annualized

effect of the GoldKey acquisition, sales totalled

about 3,100 MSEK. Growth has been achieved with

a sustained strong cash flow. The Group’s plants are

well-invested with high technological standards.

New expansion-oriented investments in China and

Mexico have been completed and will generate

growth with a lower level of investments in the

years ahead.

Business expansion has been achieved through

organic growth and successful acquisitions. From

our start as a Swedish business, we have developed

into a global polymer group with 90 percent of sales

invoiced outside Sweden. We have production opera-

tions today in nine countries, including emerging

markets such as China, Sri Lanka, Mexico and the

Czech Republic. Seven of our 15 production companies,

or nearly 50 percent, are situated in these countries.

Our presence for global OEM manufacturers is strong.

Expansion and profitabilityThe operations have expanded sharply during recent

years, with operating margins that – in most cases –

are higher than many of our competitors. Our opera-

ting margin in 2007 exceeded 11 percent.

Our largest acquisitions in Compounding have

been GFD (Germany) in 2002, Thona Group (the US,

Belgium, Czech Republic and Canada) in 2004 and

GoldKey (USA) in 2007.

To create a global platform for wheel operations

(Wheels), the wheels activities of Trostel (USA)

were acquired in 2005.

Background to the listingHEXPOL has now reached a size, position and level

of profitability that make the business attractive on

its own merits. Accordingly, the Annual General

Meeting of Hexagon AB has resolved to distribute

the shares in HEXPOL and has applied for a listing

of the Company’s Class B shares on the OMX Nordic

Exchange, effective June 9, 2008. The listing will

support HEXPOL’s continued growth, both organi-

cally and through acquisitions.

StrategyOur goal is to achieve continued rapid growth with

healthy profitability, based on a strategy of strong

organic growth and continued acquisitions in the

polymer segment.

24 HEXPOL

We have large global customers in growth markets

such as the automotive industry, plate heat exchangers

and materials handling products.

We will continue to expand our Compounding opera-

tions in emerging markets such as China, Mexico,

eastern and central Europe. Our customers in the

automotive industry are growing strongly in these

markets, and we are well equipped to meet their

demand. We also have a strong position and business

growth based on Japanese and Korean systems and

OEM manufacturers in NAFTA1 , Asia and Eastern

Europe.

Our strategy is based on comprehensive and broad

polymer and applications expertise. For example,

unique proprietary formulas that we offer our

customers through technical cooperation agreements

account for 80 percent of Compounding’s sales

in Europe.

During recent years, we have invested strongly in

PHE Gaskets to meet the segment’s strong demand.

The next stage in our expansion is the new production

plant in China, which will be placed in operation

gradually during the latter part of 2008.

The strategy within Wheels is also based on the

offering of global deliveries to major OEM customers.

In addition to operations in Europe and the US, we

also started production in China during 2007.

Our strong brands provide a solid base for our

future positioning in the marketplace.

ResultsWe had a successful year in 2007. We strengthened

our global positions through the acquisition of

GoldKey and production start-ups at new plants in

China (Compounding and Wheels) and Mexico

(Compounding). We increased our sales by 10 percent

and operating profit improved by nearly 49 percent.

We are also off to a good start in 2008. The first

quarter of 2008 showed continued strong sales

growth, +30 percent, and a continued increase

in profits.

FutureOur strategy for achieving favourable profitable

growth through strong global positions in growth

industries is based on highly skilled personnel and

a powerful corporate culture. Our affiliation with

Hexagon has provided us with healthy growth and

a profitability-oriented culture based on competence

and a flexible and rapid organization.

I am convinced that this base and this heritage are a

solid foundation for continued success and an exciting

journey on “our own two feet”.

Welcome as shareholders in HEXPOL AB!

Georg Brunstam

President and CEO

1 North American Free Trade Agreement – Canada, Mexico, USA.

HEXPOL 25

26 HEXPOL

Vision

The Company’s vision is to be a market leader,

ranking number one or two in each selected

technological or geographical segments, to be

able to generate growth and shareholder value.

Business concept

The business concept is to operate as a product

and application specialist in a limited number of

selected niche areas for the development and

production of polymer products. HEXPOL shall be

the most preferred partner for customers in key

industries, such as the automotive and construction

industries, the energy sector and the materials-

handling industry, based on its offering of innovative

and specialized polymer products and solutions.

HEXPOL 27

HEXPOL is one of the world’s leading polymer

groups with strong positions in markets for rubber

compounds (Compounding), gaskets for plate heat

exchangers (PHE Gaskets) and wheels made of

polyurethane, plastic and rubber materials for fork-

lifts and castor wheel applications (Wheels). Customers

are mainly system suppliers to the global automotive

industry and OEM manufacturers of plate heat

exchangers and forklifts.

The Group is organized in two business areas,

HEXPOL Compounding and HEXPOL Engineered

Products, and has production operations in nine

countries. Markets outside Sweden account for a

full 90 percent of total invoiced sales and seven of

the manufacturing units are located in expansive

regions of Asia, Mexico and Eastern Europe. The

number of employees is approximately 2,300, most

of whom are active in Asia, the US and Sweden.

Most of the plants are relatively new and all of them

are well invested. The level of technology is high and

far-reaching production and technological coordination

results in cost-effectiveness, high and uniform quality

and the ability to smoothly relocate production

among the units.

Operational strategyTo be able to sustain its long-term profitability and

sustainable competitiveness, HEXPOL attaches

great importance to the competitiveness of each in-

dividual business line. In order to attain the vision,

the following five operational strategies are applied:

1. Product development

The Group possess in-depth and broad polymer

and applications expertise. Within the HEXPOL

Compounding business area, for example, 80 percent

of the products marketed in Europe are based on

unique proprietarily developed formulas and the

Group offers its customers technological cooperation

for the products’ continued development. Product

development is conducted at each production unit

and the HEXPOL Compounding business area has

a corporate technology department in Belgium.

In total, approximately 5 percent of HEXPOL

Compounding’s employees work in the field of

development work and many of them are highly

qualified chemists and technicians.

2. Most cost-effective company in the industry

Well-invested plants characterized by a high level

of technology and broad-based expertise in a flat and

cost-effective organization facilitate success and

progress.

3. Efficient supply management

The Group continuously focuses on finding cost-

effective supply solutions that enable the exploitation

of benefits resulting from high volume and advanced

technologies. Close cooperation with customers

through local presence also provides opportunities

for effective solutions.

4. Superior management expertise

Skilled and experienced management teams based

on global coordination and continuous exchanges of

experiences enables all the units to be adapted to

best practice in the Group and the industry.

5. Speed Management

Short and fast decision-making processes and time-

effective implementation enhance competitiveness

and boost the organization’s capacity.

Strategic direction

28 HEXPOL

Growth strategyOver the years, HEXPOL has expanded robustly on

the basis of healthy organic growth and strategic

acquisitions. The same orientation will be pursued

in the future.

Organic growthThe Group’s principal markets and customers are

showing favourable growth. One example is the

market for plate heat exchangers, which is under-

going very strong growth driven by the quest for

energy savings and in which HEXPOL supplies

key components to all major OEM manufacturers.

Another example is the automotive industry, which

is growing robustly in Asia, Mexico and Eastern

Europe. In these areas, HEXPOL has established

state-of-the-art facilities for satisfying the techno-

logical and demand requirements of customers.

The strategy continues to be to capitalize on the

opportunities that arise when manufacturers of

rubber compounds have to decide whether to switch

to outsourcing or continue with their in-house com-

pounding operations, with the resulting investment

and renovation requirements. The materials-handling

industry is also growing globally, as a result of sharply

increasing volumes of cargo, which entails increased

demand for forklifts and thus increased demand for

HEXPOL’s products in the form of wheels.

HEXPOL’s acquisition strategyThe Group’s strategy is to continue to acquire

companies in the polymer field, primarily within

current business areas but including a broadening

of application areas and geography.

Potential acquisition targets are monitored continu-

ously in accordance with a distinct acquisition

model, whereby interesting targets are analyzed

on the basis of a series of strategic parameters.

The Group has a strong cash flow and a healthy

financial position which, together with committed

lines of credit, generate the financial preparedness

required for acquisitions.

BrandsHEXPOL markets its products via a number of

well-established brands. For example, the Gislaved

Gummi brand is well-known and highly reputed far

beyond the borders of Sweden. In addition, GoldKey,

Stellana and Elastomeric are recognized brands in

their respective product areas and geographical

markets.

Financial objectivesThe Board of Directors has established the following

financial objectives over a business cycle: The aim

is that the organic sales growth will be at least

7-10 percent annually and that the operating margin

will be at least 8-10 percent.

Dividend policyHEXPOL’s profit trend and equity/assets ratio deter-

mine the size of the dividend. HEXPOL’s dividend

policy is that 25–50 percent of after-tax net profit for

the year will be distributed as a dividend to HEXPOL’s

shareholders, on condition that the Company’s

equity/assets ratio is regarded as satisfactory.

HEXPOL 29

30 HEXPOL

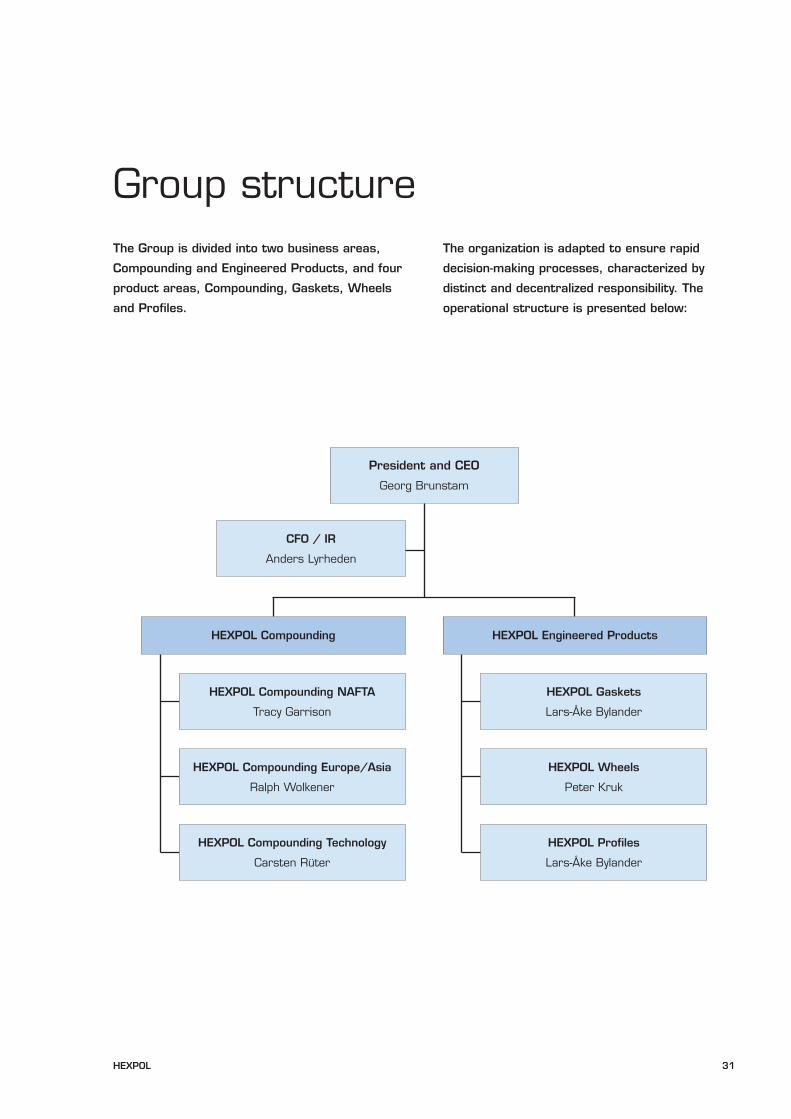

HEXPOL 31

The Group is divided into two business areas,

Compounding and Engineered Products, and four

product areas, Compounding, Gaskets, Wheels

and Profiles.

The organization is adapted to ensure rapid

decision-making processes, characterized by

distinct and decentralized responsibility. The

operational structure is presented below:

Group structure

President and CEO

Georg Brunstam

CFO / IR

Anders Lyrheden

HEXPOL Compounding

HEXPOL Compounding NAFTA

Tracy Garrison

HEXPOL Engineered Products

HEXPOL Gaskets

Lars-Åke Bylander

HEXPOL Compounding Europe/Asia

Ralph Wolkener

HEXPOL Wheels

Peter Kruk

HEXPOL Compounding Technology

Carsten Rüter

HEXPOL Profiles

Lars-Åke Bylander

32 HEXPOL

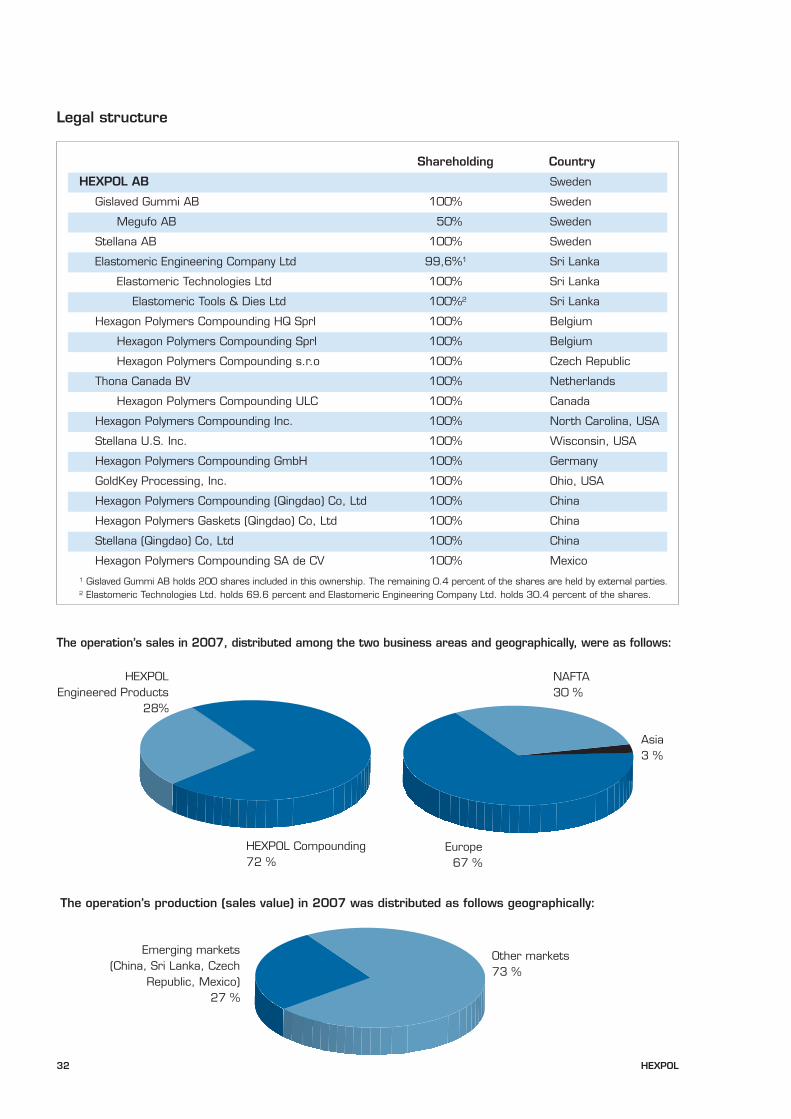

Shareholding Country

HEXPOL AB Sweden

Gislaved Gummi AB 100% Sweden

Megufo AB 50% Sweden

Stellana AB 100% Sweden

Elastomeric Engineering Company Ltd 99,6%1 Sri Lanka

Elastomeric Technologies Ltd 100% Sri Lanka

Elastomeric Tools & Dies Ltd 100%2 Sri Lanka

Hexagon Polymers Compounding HQ Sprl 100% Belgium

Hexagon Polymers Compounding Sprl 100% Belgium

Hexagon Polymers Compounding s.r.o 100% Czech Republic

Thona Canada BV 100% Netherlands

Hexagon Polymers Compounding ULC 100% Canada

Hexagon Polymers Compounding Inc. 100% North Carolina, USA

Stellana U.S. Inc. 100% Wisconsin, USA

Hexagon Polymers Compounding GmbH 100% Germany

GoldKey Processing, Inc. 100% Ohio, USA

Hexagon Polymers Compounding (Qingdao) Co, Ltd 100% China

Hexagon Polymers Gaskets (Qingdao) Co, Ltd 100% China

Stellana (Qingdao) Co, Ltd 100% China

Hexagon Polymers Compounding SA de CV 100% Mexico1 Gislaved Gummi AB holds 200 shares included in this ownership. The remaining 0.4 percent of the shares are held by external parties.2 Elastomeric Technologies Ltd. holds 69.6 percent and Elastomeric Engineering Company Ltd. holds 30.4 percent of the shares.

The operation’s sales in 2007, distributed among the two business areas and geographically, were as follows:

HEXPOL Engineered Products

28%

HEXPOL Compounding72 %

Asia3 %

NAFTA30 %

Europe67 %

Legal structure

Emerging markets(China, Sri Lanka, Czech

Republic, Mexico) 27 %

Other markets 73 %

The operation’s production (sales value) in 2007 was distributed as follows geographically:

HEXPOL 33

34 HEXPOL

The brothers Carl and Wilhelm Gislow formed

Svenska Gummifabriks AB in 1895.

The principal phases in the development into the current HEXPOL have been:

• 1893 The Gislow brothers form a rubber factory in Gislaved

• 1966 A new factory for Technical Rubber is built

• 1990 The Technical Rubber division becomes Gislaved Gummi AB

• 1991 Production of gaskets for plate heat exchangers is acquired

• 1994 Hexagon AB acquires the Company

• 1995 Stellana AB in Laxå is acquired

• 1998 Elastomeric Engineering Co. Ltd. in Sri Lanka is acquired

• 2002 GFD Technology GmbH in Germany is acquired

• 2004 Thona Group of Belgium, with operations in Belgium, Czech Republic, Canada and the US, is acquired

• 2005 Trostel SEG of the US is acquired

• 2007 Establishment of three new plants for rubber compounds, wheels and gaskets in China and a new plant

for rubber compounds in Mexico

• 2007 GoldKey Processing Ltd of the US is acquired

HEXPOL 35

0

500

000

500

2000

2500

3000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

3000

2500

2000

1500

1000

500

0

GoldKey (September 2007)

Trostel (September 2005)

Thona Group (May 2004)

GFD (July 2002)

Elastomeric (July 1998)

HEXPOL

History

Acquired units are shown in a different colour, representing consolidated

sales during the year of acquisition and following year.

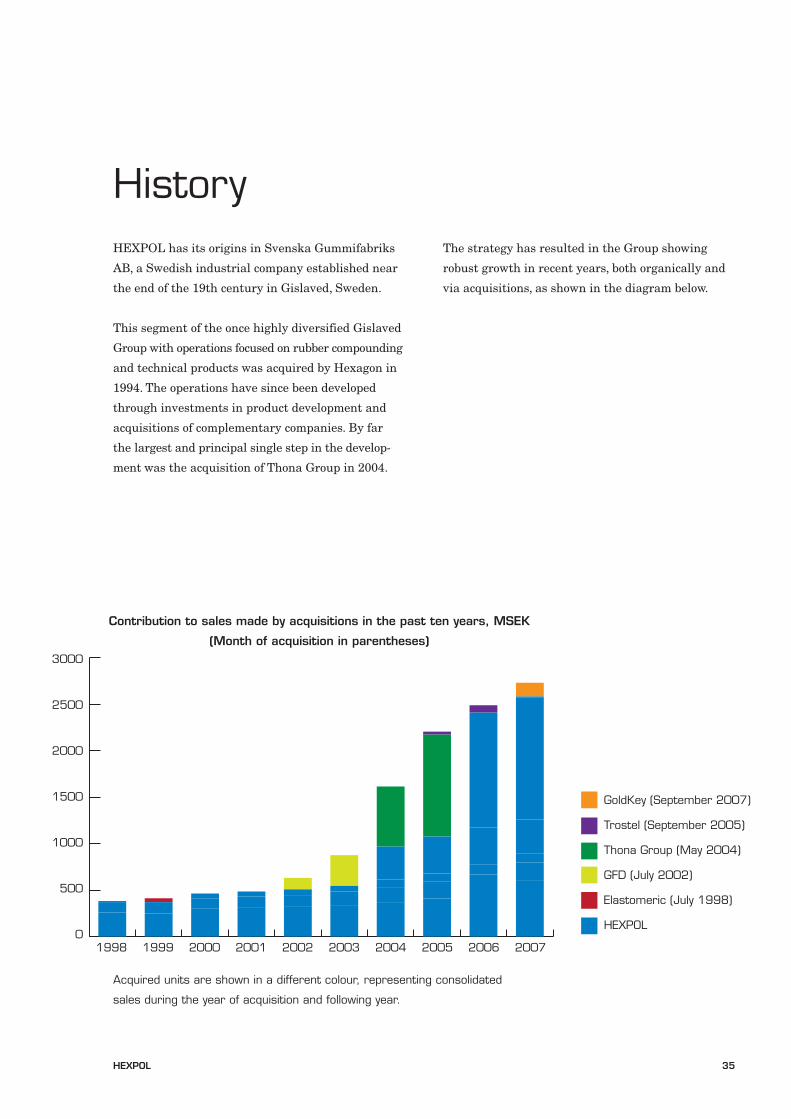

Contribution to sales made by acquisitions in the past ten years, MSEK

(Month of acquisition in parentheses)

HEXPOL has its origins in Svenska Gummifabriks

AB, a Swedish industrial company established near

the end of the 19th century in Gislaved, Sweden.

This segment of the once highly diversified Gislaved

Group with operations focused on rubber compounding

and technical products was acquired by Hexagon in

1994. The operations have since been developed

through investments in product development and

acquisitions of complementary companies. By far

the largest and principal single step in the develop-

ment was the acquisition of Thona Group in 2004.

The strategy has resulted in the Group showing

robust growth in recent years, both organically and

via acquisitions, as shown in the diagram below.

36 HEXPOL

HEXPOL 37

0

500

000

500

000

500

0

50

100

150

200

250

0

2

4

6

8

10

12

14

20072006200520042003

14 %

12 %

10 %

8 %

6 %

4 %

2 %

0 %

2500

2000

1500

1000

500

02003 2004 2005 2006 2007

72 %

63 %

31 %

250

200

150

100

50

0

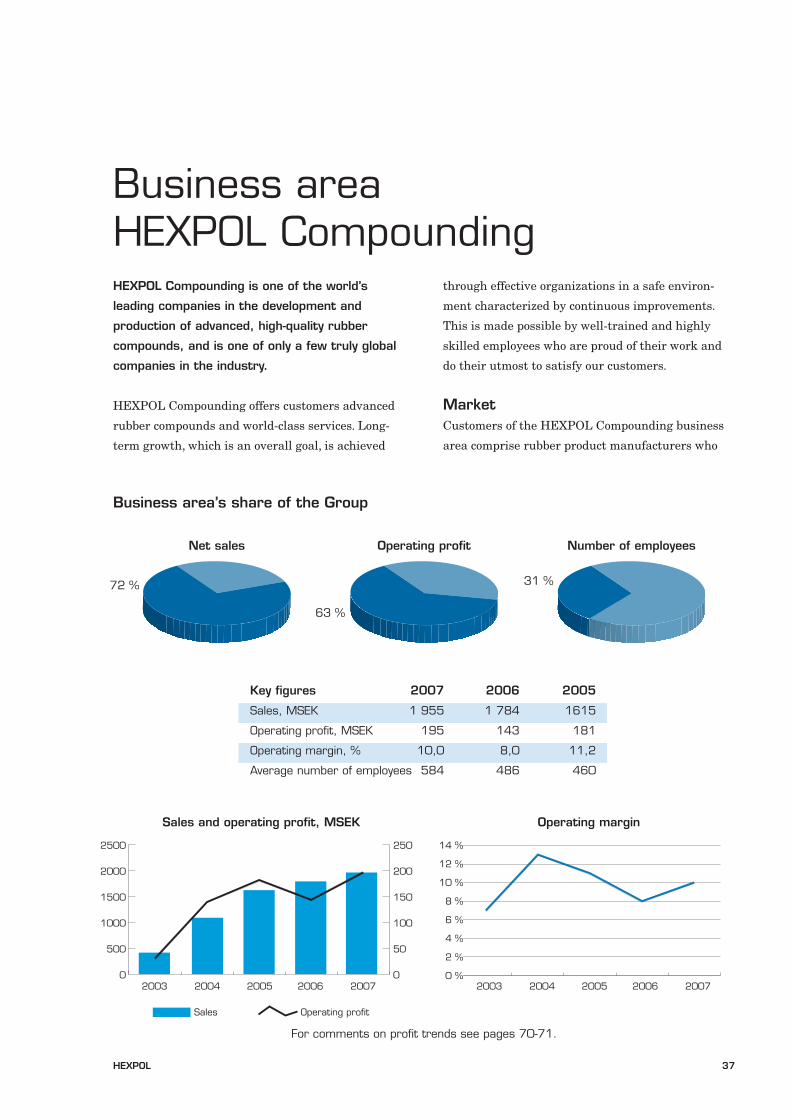

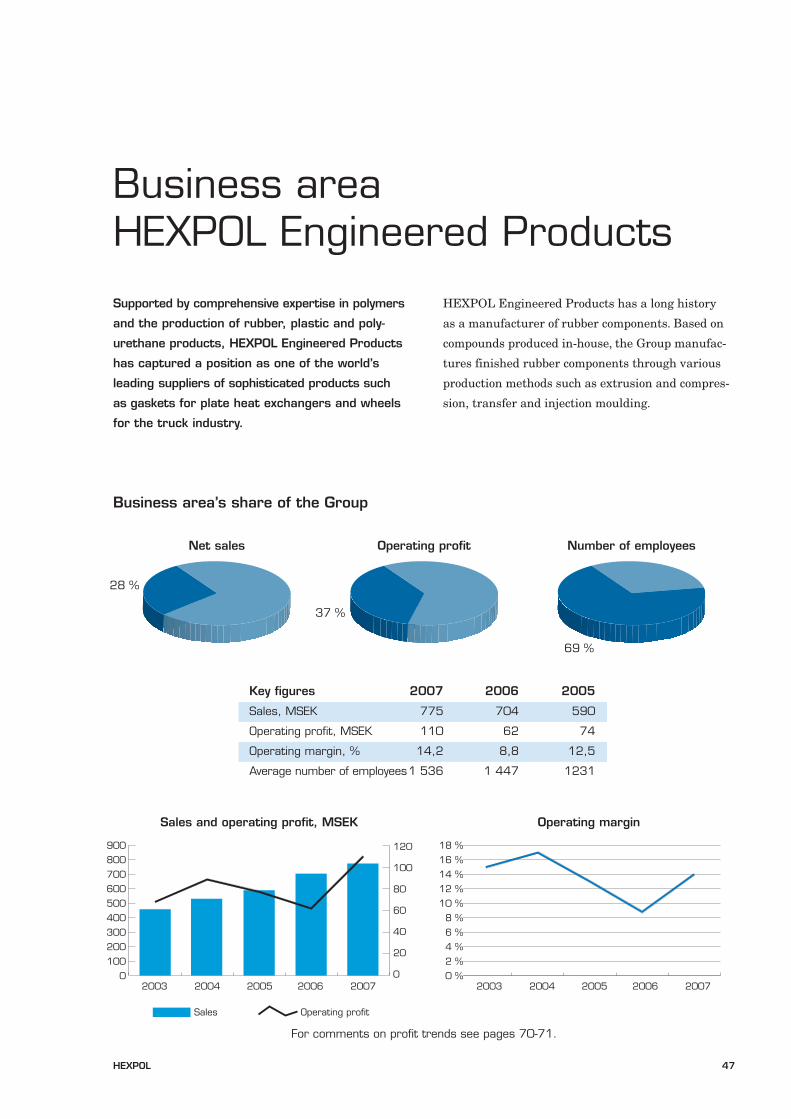

Key figures 2007 2006 2005

Sales, MSEK 1 955 1 784 1615

Operating profit, MSEK 195 143 181

Operating margin, % 10,0 8,0 11,2

Average number of employees 584 486 460

Operating profitSales

Sales and operating profit, MSEK Operating margin

Net sales Operating profit Number of employees

HEXPOL Compounding is one of the world’s

leading companies in the development and

production of advanced, high-quality rubber

compounds, and is one of only a few truly global

companies in the industry.

HEXPOL Compounding offers customers advanced

rubber compounds and world-class services. Long-

term growth, which is an overall goal, is achieved

through effective organizations in a safe environ-

ment characterized by continuous improvements.

This is made possible by well-trained and highly

skilled employees who are proud of their work and

do their utmost to satisfy our customers.

MarketCustomers of the HEXPOL Compounding business

area comprise rubber product manufacturers who

Business area HEXPOL Compounding

Business area’s share of the Group

For comments on profit trends see pages 70-71.

38 HEXPOL

1 CSM Worldwide – CSM Global Production Summary, 1Q 2008.

place high demands on performance and global delivery

capabilities. The largest market segment is the auto-

motive industry, followed by building and construction.

Other key segments include cable, water management,

pharmaceutical, energy and oil industries.

The automotive industry currently accounts for 68

percent of sales invoiced by HEXPOL Compounding.

A modern passenger car contains hundreds of rubber

components and a luxury car, for example, contains

more than 50 metres of sealing profile. For many car

manufacturers, particularly in the premium segment,

high-quality sealing systems represent a key compo-

nent. The sealing system often influences the end-

customer’s quality impressions in the form of quiet

performance. HEXPOL Compounding is one of the

leading suppliers of synthetic rubber compounds in

this area.

All major manufacturers in the automotive industry

and their system suppliers are global companies.

These factors favour HEXPOL Compounding, which

focuses on global delivery capabilities for the market’s

best products, with identical quality regardless of

the production unit.

The global automotive market is growing rapidly.

The number of light vehicles manufactured in the

next few years is expected to increase sharply, mainly

due to greater demand from emerging markets such

as China and India. According to statistics from

CSM1, approximately 68 million new light vehicles

were manufactured during 2007. Weak production

growth is expected in North America in the next few

years, following a decline in light vehicle production

this year. This will be offset primarily by markets in

Southern Asia, China and South America, where

strong growth is expected in the next few years.

According to forecasts by CSM, global production

of light vehicles in 2012 is projected at about 84

million new units, corresponding to an average

annual increase of slightly more than 4 percent.

At the same time, the industry is undergoing exten-

sive changes. Many manufacturers are gradually

transferring parts of their production to low-cost

countries and new, more expansive markets such as

Eastern Europe, China, India and Mexico. For supp-

liers, this trend is creating demands from customers

to follow their example and offer production in these

new markets. As a result of these trends, HEXPOL

Compounding has established units in Mexico and

China. Operations were already established in the

Czech Republic, where the business area has one

of its largest production plants, which supplies the

markets in Central and Eastern Europe.

In addition to the business expansion outlined above,

Japanese and Korean automotive manufacturers are

also increasing their global and regional production

operations. HEXPOL Compounding has positioned

itself favourably to meet these market changes.

Technology and productsGeneral definition of rubber compounds

Rubber compounds are semi-finished products and

can be seen as homogenous mixtures of different

ingredients that have been defined in a specific for-

mulation or “recipe”. These ingredients, or raw ma-

terials, can be subdivided into the following

categories: polymers, fillers, plasticizers, accelerators,

cross-linking agents and many other special products.

Only the right composition and a perfect mixing

process result into optimum properties of the final

product.

Rubber compounds leaving the HEXPOL Compoun-

ding production facilities will be further processed

by their customers via processes such as extrusion,

injection molding or compression molding in order

to reach the part’s final shape. Finally, continuous

or discontinuous vulcanization will provide to the

rubber part its typical elastic behavior.

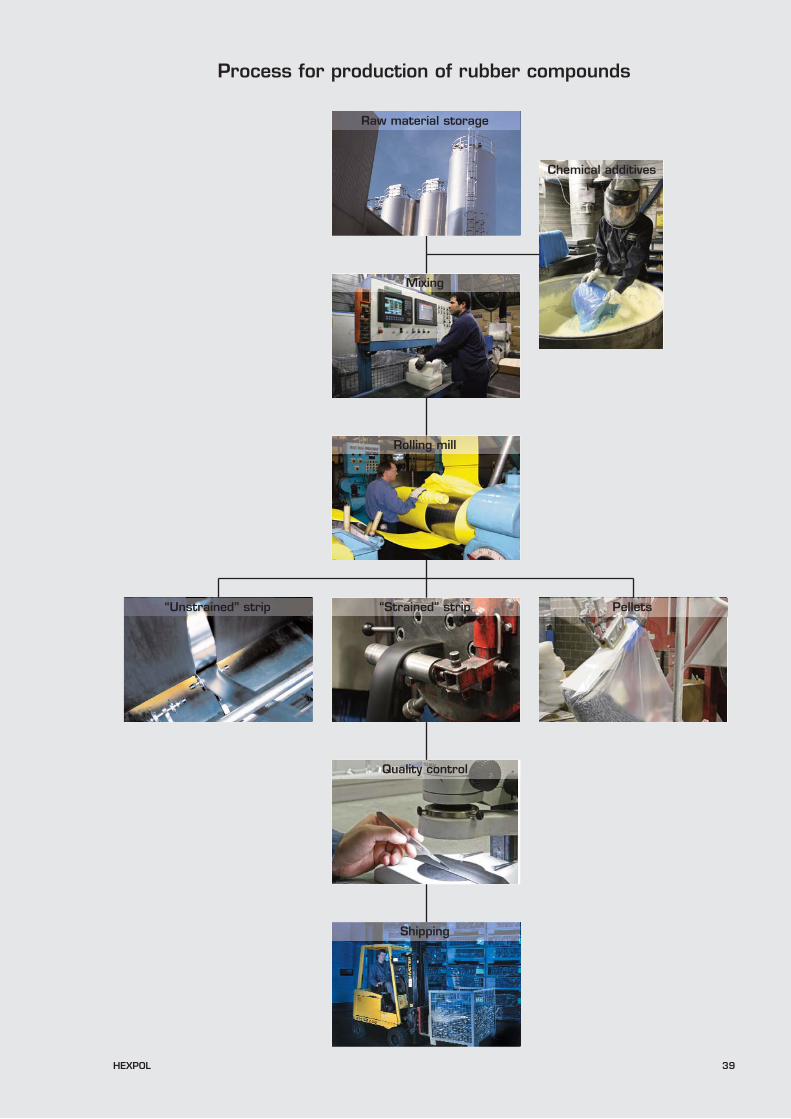

Production process

The production sites of HEXPOL Compounding

feature some of the most advanced processing lines

HEXPOL 39

“Strained” strip

Rolling mill

Mixing

Raw material storage

Chemical additives

Quality control

Shipping

“Unstrained” strip Pellets

Process for production of rubber compounds

40 HEXPOL

found in an industry that, otherwise, has not tradi-

tionally been considered particularly sophisticated

in terms of technology. The plants are equipped with

an impressing quality assurance concept, covering

data gathering of raw materials, mixing parameters

and final control. The entire production process is

fully computerized in order to assure efficiency and

quality.

Raw material and preparation

After a quality assurance inspection, the various

raw materials are stored in large silos, tanks or a

warehouse. Mixing in an internal mixer is a so-called

batch process and, as a result, all ingredients must