Prospects for shale development outside the USA: evaluating nations’ regulatory and fiscal regimes for unconventional hydrocarbons Grant Mark Nu ¨lle* Pursuant to a generous Association of International Petroleum Negotiator (AIPN) 2014 Summer Research Award, this article identifies, evaluates and compares the legal and fiscal rules, regulations and incentives necessary for countries with significant shale petroleum and natural gas formations to attempt to replicate the boom that is ongoing in the USA. As others have pointed out, 1 several legal, tax, and operational barriers can impair duplication of the US shale revolution in similarly endowed nations. This article identifies key factors responsible for the surge in US shale pro- duction, distill the fundamental forces from the US experience that are applicable to any jurisdiction, and evaluate and compare how several countries fare in this vein. The report also identifies avenues for reform and innovative policies that could be applied in other jurisdictions. 1. Upheaval in the global energy balance The commercial and geopolitical implications of the US shale revolution continue to emerge with major ramifications for the entire world. Already the premier natural gas producer, the USA is poised to surpass Saudi Arabia and Russia as the largest oil producer and will likely become a net exporter of both oil and gas within a decade or more thanks to unconventional resource extraction. 2 Regardless of whether the sharp decline in pet- roleum prices that began in the fourth quarter of 2014 delays this eventuality, the re- naissance in US oil and gas production effectuated by shale gas and tight oil production is one of the most transformative events in energy markets and the global economy in the last decade. According to the US Energy Information Administration (EIA), extraction of shale gas helped push US natural gas production from 24.2 trillion cubic feet (tcf) in 2000 to just * MS, MBA, PhD (ABD), Colorado School of Mines, PO Box 5681, Denver, CO 80217, USA. This research was generously funded by the Association of International Petroleum Negotiators (AIPN) Education Committee. The author wishes to thank Steve Otillar, AIPN Executive Committee—Vice President of Education; Linda Battalora, Colorado School of Mines, who served as the academic advisor on this project; Graham Cooper of EnQuest plc and Gabor Zelei of Mol Plc, co-chairs of the 2014 AIPN International Conference, for allowing me to present the findings of this research at the conference. Email: [email protected]. 1 Jose Martinez de Hoz, Tomas Lanardonne, and Alex Maculus, ‘Shale We Dance an Unconventional Tango?’ (2013) 6(3) JWELB 179–209. 2 International Energy Agency (IEA), ‘World Energy Outlook’ (2013). 232 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3 ß The Author 2015. Published by Oxford University Press on behalf of the AIPN. All rights reserved. doi:10.1093/jwelb/jwv014 Advance Access publication 10 April 2015 at AIPN on May 30, 2016 http://jwelb.oxfordjournals.org/ Downloaded from

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Prospects for shale development outside the USA:evaluating nations’ regulatory and fiscal regimes forunconventional hydrocarbonsGrant Mark Nulle*

Pursuant to a generous Association of International Petroleum Negotiator (AIPN)

2014 Summer Research Award, this article identifies, evaluates and compares thelegal and fiscal rules, regulations and incentives necessary for countries with significant

shale petroleum and natural gas formations to attempt to replicate the boom that isongoing in the USA. As others have pointed out,1 several legal, tax, and operationalbarriers can impair duplication of the US shale revolution in similarly endowed

nations. This article identifies key factors responsible for the surge in US shale pro-duction, distill the fundamental forces from the US experience that are applicable to

any jurisdiction, and evaluate and compare how several countries fare in this vein. Thereport also identifies avenues for reform and innovative policies that could be applied

in other jurisdictions.

1. Upheaval in the global energy balance

The commercial and geopolitical implications of the US shale revolution continue to

emerge with major ramifications for the entire world. Already the premier natural gas

producer, the USA is poised to surpass Saudi Arabia and Russia as the largest oil producer

and will likely become a net exporter of both oil and gas within a decade or more thanks

to unconventional resource extraction.2 Regardless of whether the sharp decline in pet-

roleum prices that began in the fourth quarter of 2014 delays this eventuality, the re-

naissance in US oil and gas production effectuated by shale gas and tight oil production is

one of the most transformative events in energy markets and the global economy in the

last decade.

According to the US Energy Information Administration (EIA), extraction of shale gas

helped push US natural gas production from 24.2 trillion cubic feet (tcf) in 2000 to just

* MS, MBA, PhD (ABD), Colorado School of Mines, PO Box 5681, Denver, CO 80217, USA. This research was generously

funded by the Association of International Petroleum Negotiators (AIPN) Education Committee. The author wishes to thank

Steve Otillar, AIPN Executive Committee—Vice President of Education; Linda Battalora, Colorado School of Mines, who

served as the academic advisor on this project; Graham Cooper of EnQuest plc and Gabor Zelei of Mol Plc, co-chairs of the

2014 AIPN International Conference, for allowing me to present the findings of this research at the conference. Email:

[email protected] Jose Martinez de Hoz, Tomas Lanardonne, and Alex Maculus, ‘Shale We Dance an Unconventional Tango?’ (2013) 6(3)

JWELB 179–209.2 International Energy Agency (IEA), ‘World Energy Outlook’ (2013).

232 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

� The Author 2015. Published by Oxford University Press on behalf of the AIPN. All rights reserved.

doi:10.1093/jwelb/jwv014 Advance Access publication 10 April 2015

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

shy of 29 tcf in 2011. During that same period, the proportion of natural gas produced

from shale grew from 2% of total US natural gas production to 34%. Shale gas produc-

tion is expected to grow by more than 113% over the next 30 years and is expected to

comprise 79% of US natural gas production. In addition to natural gas, shale oil pro-

duction has helped increase US liquids production by nearly 45% since 2008.3

The USA is not alone in possessing major shale resources. The US Department of

Energy4 estimates the USA is ranked second in technically recoverable shale oil resources

behind Russia and fourth in technically recoverable shale gas resources, trailing China,

Argentina and Algeria. Several other countries including Australia, Brazil and Mexico

have shale oil and gas resources that rival those of the USA. Tables 1 and 2 display the 15

largest countries in terms of unproven, technically recoverable, shale gas and petroleum,

respectively. These figures speak to the broader point that the overwhelming majority of

shale resources are found outside North America. Figures 1 and 2 display the distribution

of shale gas and oil resources by major regions. For both shale gas and oil resources, less

than a quarter of the resources are found in North America.

Consequently, the major technological transformations in hydrocarbon extraction

techniques in the USA and geopolitical implications thereof compel policy-makers in

Table 1 Largest shale gas resources by country

Country Unproved wet shale gas

technically recoverable

resources

Natural Gas

Production (2011)

Proved Natural Gas

Reserves (2013)

China 1115 4 124

Argentina 802 2 12

Algeria 707 3 159

Canada 573 6 68

USA 567 24 318

Mexico 545 2 17

Australia 437 2 43

South Africa 390 0 –

Russia 287 24 1688

Brazil 245 1 14

Venezuela 167 1 195

Poland 148 51 3

France 137 51 51

Ukraine 128 1 39

Libya 122 51 55

Source: DOE (2013). Units in Trillion Cubic Feet.

3 EIA–US Energy Information Administration, ‘Annual Energy Outlook 2013’ (15 July 2014).4 DOE–US Department of Energy, ‘Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale

Formations in 41 Countries outside the United States’ (2013)5http://www.eia.gov/analysis/studies/worldshalegas/4 accessed

14 June 2014.

Grant Mark Nulle � Prospects for shale development outside the United States 233

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Table 2 Largest shale oil resources by country

Country Unproved shale oil

technically recoverable

resources

Petroleum

Production (2011)

Proved Petroleum

Reserves (2013)

Russia 75,800 3737 80,000

USA 58,100 3699 25,181

China 32,200 1587 25,585

Argentina 27,000 279 2805

Libya 26,100 183 48,010

Australia 17,500 192 1433

Venezuela 13,400 909 297,570

Mexico 13,100 1080 10,264

Pakistan 9100 23 248

Canada 8800 1313 173,105

Indonesia 7900 371 4030

Colombia 6800 343 2200

Algeria 5700 680 12,200

Brazil 5300 980 13,154

Turkey 4700 21 270

Source: DOE (2013). Units in Million Barrels.

Figure 1 Shale gas resources by major regions. Source: DOE (2013). Units in Trillion Cubic Feet.

234 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

jurisdictions endowed with unconventional resources to decide whether or not to allow

energy companies to engage in shale oil and gas development. As pointed out by Hoz

et al. (2013),5 shale or unconventional resources development poses several unique chal-

lenges to regulators, policy-makers and the citizens they serve and represent. The specia-

lized knowledge, equipment and capital intensive processes involved in extracting liquids

and gas from shale elevate the importance of project economics. In order for nations to

replicate elements of the shale revolution in the USA, changes to accommodate the

unique project economics of shale are necessary.

To detail the challenges, opportunities and areas of potential hydrocarbon sector regu-

latory and fiscal reform needed to facilitate unconventional hydrocarbons development,

the remainder of this report is organized as follows. Section 2 describes the key charac-

teristics of shale operations and how these attributes affect hydrocarbons policy. Section 3

examines the US shale experience in detail and distills key considerations with which

similarly endowed nations must grapple. The penultimate section reviews and evaluates

aspects of hydrocarbon fiscal and regulatory regimes of nine shale-endowed countries to

determine how well these nations have re-configured policies and laws to accommodate

unconventional resource development. The closing section draws conclusions, recom-

mendations and avenues for further research.

Figure 2 Shale oil resources by major regions. Source: DOE (2013). Units in Million Barrels.

5 See Hoz, Lanardonne and Maculus (n 1) 180–81.

Grant Mark Nulle � Prospects for shale development outside the United States 235

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

2. Key considerations for shale oil and gas extraction

The importance of having a hydrocarbons fiscal and regulatory regime appropriately

balancing the requirements and interests of International Oil Companies (IOCs) and

host governments is amplified by the extraction of unconventional resources,6 as it

poses several unique geologic, economic and environmental challenges.

Principally, shale oil and gas resources are more complex to produce than conventional

counterparts. Unconventional hydrocarbons are generally found deeper than conven-

tional deposits, and—to complicate matters—both may be found on the same tract of

land.7 Shale formations tend to extend across much larger geographic areas and possess a

great deal of heterogeneity in composition, placing a premium on utilizing geological

information, advanced technology and extensive testing to find the location of areas of

high productivity or ‘sweet spots’.8 Because shale is much easier to find and is generally a

harbinger of the presence of conventional resources, the pivotal question becomes

whether the gas or liquids trapped in the shale can be released at flow rates that are

economical. While each well drilled for appraisal purposes in a conventional reservoir

tends to increase knowledge about the overall reservoir structure, it is much more dif-

ficult in unconventional operations to extrapolate the results of each pilot well to the

acreage as a whole.9 As such, it is critical, according to the AIPN Unconventional

Resources Operating Agreement10 for operators to be able to (i) establish the extent of

the shale resources; (ii) undertake a pilot programme to determine whether the produc-

tion technology and methodology with respect to the shale characteristics is effective and

commercially viable before committing to a broader long-term development plan. These

points recognize that efforts at finding commercially viable shale flow may fail even in the

late stages.11

Additionally, shale oil and gas outputs decline more rapidly and with lower recovery

factors than conventional resources.12 This necessitates a higher number of wells

(increased well density) to cover operational and capital costs and a longer production

period—up to 50 years or more. Due to the geological challenges, extensive testing,

appraisal and drilling required, high density of wells and costs of water acquisition and

treatment, the cost per shale well can range from of $3 to $9 million in the USA and three

to four times more elsewhere.13

6 The terms ‘unconventional resources’ and ‘shale oil and gas’ are synonymous and are used interchangeably throughout this

article.7 Susan L Sakmar, ‘The Global Shale Gas Initiative: Will the United States be the Role Model for the Development of Shale Gas

around the World?’ (2011) 33(2) Houston J Int L 402.8 ibid. Hoz, Lanardonne and Maculus (n 1) 180.9 IEA—International Energy Agency. ‘Golden Rules for a Golden Age of Gas – Special Report on Unconventional Gas’ (2012)

5http://www.worldenergyoutlook.org/goldenageofgas/4 accessed 17 June 2014.10 AIPN, ‘2014 Model Unconventional Resource Operating Agreement (UROA)’ (2014).11 English, James—Anadarko Petroleum, Private Correspondence. 17 July 2014.12 ibid (n 9).13 Dallas Parker and John D Furlow—Mayer Brown LLP Houston, ‘The U.S. Shale Revolution: will it happen around the World?’

(2014) Unpublished Manuscript. Received from Jose Valera Mayer Brown LLP Houston via email 25 June 2014; Paul Stevens,

‘The Shale Gas Revolution: Developments and Changes’ (2012) Chatham House. 5http://www.chathamhouse.org/sites/files/

chathamhouse/public/Research/Energy,%20Environment%20and%20Development/bp0812_stevens.pdf4 accessed 17 June

2014.

236 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Expenses of this magnitude significantly raise the capital requirements needed for shale

projects and heighten the sensitivity of the project economics to changes in market

assumptions, regulations and taxes. In this sense, unconventional resources are not alto-

gether different than conventional resource projects—the former are simply a more

capital intensive, risky and expensive class of onshore Exploration and Production

(E&P) undertaking.

Given the complexity of shale oil and gas extraction faced by operators, governments

contemplating opening up land for shale oil and gas extraction must have regulations,

laws and policies in place to address the following questions:

Rights, access, permitting

. Are rights to explore and produce unconventional resources ‘deep rights’ treated as

separate and distinct from conventional resources ‘shallow rights?’14

. If rights to conventional and unconventional resources are different and overlap the

same tracts of land, what are terms of access to property and use of above-ground

facilities and infrastructure?15

. How are landowners, nearby communities and indigenous people affected given the

large amount of machinery and equipment, volume of truck traffic and high-density

well counts?16

. Is the contract area large enough to cover the geographical scope of the unconven-

tional resource, sufficiently so that it is potentially commercial?

. Are concessions or PSCs/PSAs flexible enough to expand access to ‘sweet spots’ by

extending the material acreage covered under an agreement to adjacent open acre-

age—acreage that does not yet have an operator?

. Does a streamlined licensing and permitting regime exist?17

Exploration, appraisal and relinquishment18

. Do agreements covering unconventional oil and gas development allow for an

extended ‘appraisal period’ for shale resource exploration that recognizes shale re-

quires little exploration, but instead entails extensive drilling and testing to ascertain

the amount of shale gas and oil—appraisal—that can technically and economically

be recovered?19

. How aggressive are the requirements for relinquishment? A balance must be struck

between safeguarding against contractors holding land area as inventory (no relin-

quishment) versus an aggressive timeline that prevents the contractor from deter-

mining whether any sweet spots exist over the entire span of the contract area.

14 See Hoz, Lanardonne and Maculus (n 1) 186.15 See UROA (n 10).16 This is a particularly acute problem in countries where there is high population density in the proximity of shale plays (eg India,

Pakistan).17 Delays in licensing can kill project economics, as the idle time created on rigs increases cost and opportunities to find

economical flows or shale oil and gas (English 2014).18 See UROA 2014 for a fuller treatment of these issues.19 See Hoz, Lanardonne and Maculus (n 1) 188–89.

Grant Mark Nulle � Prospects for shale development outside the United States 237

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

. Even if the underlying resource is relinquished, can above-ground facilities and

infrastructure still be used?

. Is a pilot programme deemed part of appraisal or part of the production phase?

. Once a pilot well is completed, are sales of pilot production allowed to occur and

which parties financially benefit?

. How is declaration of commerciality handled? Does it allow for pilot production

before declaration or after declaration, which will affect whether a contractor can

commit to a full or phased development plan?

Production, pricing and operational constraints

. What is the lifespan of production? Does the timeline take into account the longer

duration needed to extract unconventional resources?

. Are market-based price regimes in place, and if not, are price-control regimes that

provide guaranteed sales prices at or above break-even prices provided?

. Does the oil and gas output have defined and ranked end-use priorities (domestic

consumption versus export sales via Pipeline/Liquefied Natural Gas terminals)? Is

delivery of shale oil and gas output free of contract interference or re-routing of oil

and gas to different consumers (Hoz et al. 2013)?

. Transport—are there guarantees of pipeline access at the same tariff rates National

Oil Companies (NOCs) or domestic firms are paying?

. Marketing—does the IOC or NOC control marketing?

Fiscal, macroeconomic and sectoral considerations

. Are tax incentives (R&D tax credits, immediate expensing of tangible and/or intan-

gible drilling costs, reduced royalty rates) available to attract shale gas and oil

investment?

. Does ring fencing, in terms of both cost recovery and taxation purposes, apply?

. Given the technical complexity of shale oil and gas exploration, appraisal, develop-

ment and production, is there free or automatic importation of capital goods and

special equipment and parts necessary for undertaking unconventional operations?

. Are foreign exchange provisions unduly restrictive, that is do the measures signifi-

cantly impede flows of capital, profits and dividends effectuated by shale gas and oil

operations back to investors?

. Are local content requirements for use of domestic labour and machinery suffi-

ciently flexible to recognize that unconventional E&P projects, particularly in the

early stages, are incompatible with the high level of specialized and scarce expertise

necessary to find commercially viable shale oil and gas?

Before evaluating how several nations possessing significant shale oil and gas resources

have addressed these issues through regulatory, statutory and even constitutional

changes, it is both necessary and proper to first evaluate the treatment of shale resources

by the USA, the birthplace of the shale revolution.

238 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

3. The USA as benchmark

The growth of shale US oil and gas production over the last decade has been nothing

short of phenomenal. Despite having only 9.1% of the world’s technically recoverable

shale gas resources and only 16.8% of total world-wide technically recoverable ‘tight oil’

resources, the USA is one of only two major producers of shale oil and gas in the world.20

In 2012 shale gas comprised 39% of US natural gas output and by 2040 nearly 80% of

total gas production is anticipated to come from unconventional resources.21 For these

reasons, the USA represents the ‘benchmark’ by which countries similarly endowed with

shale resources can be evaluated.22

As a prelude to identifying those factors that ignited the shale revolution, a cautionary

note is in order. In commerce as well as in policy-making, benchmarking is an attractive

tool as it aims to identify particular indicators useful for measurement and comparison

between business competitors or countries.23 However, without careful consideration of

context, it is easy for policy-makers to fall prey to ‘naıve benchmarking’ whereby a best

practice from the benchmark fails to translate into success in the entity that attempts to

replicate it. Such disappointments stem from the absence of other intervening factors that

made the particular practice viable in the benchmark. Without properly accounting for

the many structural and institutional factors that cannot be easily changed—eg cultural

and historical experiences, socio-economic conditions and composition of natural

endowments—benchmarking can lead to erroneous conclusions and poor policy out-

comes.24 Consequently, it is critically important to understand the underlying processes

that made success in the benchmark possible by distilling them from the benchmark’s

particular policies, institutions and structural contexts. Once those underlying processes

have been identified, decision makers can then determine how those forces can be infused

into their own countries via means best suited to their own country’s unique institutional

and structural opportunities and constraints.

Bearing those caveats in mind, the factors contributing to shale development in the

USA are classified as follows:

Technical expertise and experience

The USA has been engaged in oil and gas extraction dating back to the mid-19th century

and has been regularly at the forefront of generating technical innovations to econom-

ically extract oil and gas from difficult-to-reach places. US expertise, in terms of human

capital and specialized machinery, is so vast in the sphere of oil and gas E&P that it has

attained the moniker of an oligopoly. In particular, the combination of hydraulic

20 EIA, ‘North America Leads the World in Production of Shale Gas’ (2013) 5http://www.eia.gov/todayinenergy/detail.

cfm?id¼13494 accessed 17 August 2014. The other major producer is Canada.21 ibid (n 3).22 Juan Roberto Lozano Maya, ‘The United States Experience as a Reference of Success for Shale Gas Development: The Case of

Mexico’ (2014) Energy Policy 62, 70–78.23 Kathleen C. Dominique, Ammar Anees Malik, and Valerie Remoquillo-Jenni, ‘International Benchmarking: Politics and Policy’

(2013) 40(4) Sci Public Policy 504–13.24 Marianne Paasi, ‘Collective Benchmarking of Policies: An Instrument for Policy Learning in Adaptive Research and Innovation

Policy’ (2005) 32(1) Sci Public Policy 17–27.

Grant Mark Nulle � Prospects for shale development outside the United States 239

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

fracturing and horizontal drilling, pioneered by the USA is sine qua non to economical

extraction of unconventional resources.25 Furthermore, the development, application and

deployment of advanced technologies such as directional drilling in shale, 3D micro-

seismic modelling and mapping of subsurface seismic activity, and other tools has trans-

formed extraction of shale gas from a wild-catting venture to a quasi-manufacturing

process.26

Production and distribution infrastructure

The scale of available pipeline infrastructure across the USA has facilitated delivery

of upstream shale oil and gas output from wells to mid-stream processing facilities and

end-consumers. This infrastructure includes:27

. 305,000 miles of interstate and intrastate transmission pipelines.

. More than 1400 compressor stations that maintain pressure on the natural gas

pipeline network and assure continuous forward movement of supplies.

. More than 11,000 delivery points, 5000 receipt points and 1400 interconnection

points that provide for the transfer of natural gas throughout the USA.

. The 24 hubs or market centres that provide additional interconnections.

. The 400 underground natural gas storage facilities.

. The 49 locations where natural gas can be imported/exported via pipelines.

. The 8 LNG import facilities and 100 LNG peaking facilities.

Equally important is that transportation capacity rights in the USA are distinct from

pipeline ownership, making it possible for a producer to reach customers by bidding for

pipeline capacity.28 The pre-existence of available capacity of installed pipelines accessible

on a non-discriminatory basis presented an opportunity for operators to undertake shale

exploration, development and production without incurring the cost of installing a com-

plete infrastructure.29

Market structure and financing

The US features a nimble and highly competitive oil and gas industry, an ecosystem

predominantly composed of numerous small and medium independent companies.30

These firms have been the essential innovators of the technologies, processes and know-

ledge necessary in shale extraction bearing the financial and operational risks. The de-

regulation of natural gas prices in the USA has made operators highly price-sensitive,

providing the impetus to constantly innovate to remain in business.

25 ibid (n 7).26 Robert A Hefner, ‘The United States of Gas: Why the Shale Revolution Could Have Happened Only in America’ (2014) 93(3)

Foreign Affairs 9–14.27 EIA, ‘About U.S. Natural Gas Pipelines - Transporting Natural Gas’ (2014) 5http://www.eia.gov/pub/oil_gas/natural_gas/

analysis_publications/ngpipeline/index.html4 accessed 14 August 2014.28 ibid (n 1).29 Tathiany R Camargo and others, ‘Major Challenges for Developing Unconventional Gas in Brazil – Will Water Resources

Impede the Development of the Country’s Industry?’ (2014) 41 Resources Policy 60–71.30 ibid (n 23).

240 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

From a financial perspective, the depth and breadth of financial instruments (trades,

swaps, futures, hedging) provides an additional means of operational flexibility and risk

management for producers.31 Shale operators have also been able to grow due a wide

variety of options to obtain capital financing including, equity stakes, debt instruments,

convertible securities and conventional or mezzanine bank financing. Firms can also

utilize a number of legal structures such as joint ventures and royalty trusts to facilitate

expansion.

Private ownership of minerals

Cujust est solum usque ad coelem et ad infernos (to whomever the soil belongs, he

owns also to the sky and the depths)

The USA is a legal anomaly in that it is one of the only countries in the world that

recognizes the right of individuals to own the rights to subsurface hydrocarbons and

minerals. Any oil and gas company can lease the rights, in return for a royalty, to the

hydrocarbons beneath a landowner’s property and commence drilling and production.

These arrangements allow for flexible operating conditions and rapid access to uncon-

ventional resources.32 Due to the royalty payments, US landowners are among the main

champions of shale development. To the extent states and local government in the US

federal system can share in the proceeds of shale gas activity via property taxes and other

levies, these entities are also positively inclined to shale development.

Regulatory predictability and stability

A well-established and stable regulatory framework arising from several decades of oil and

gas development in the USA has attenuated uncertainty around the extraction of con-

ventional and unconventional resources, including shale gas. In the US federal system of

governance, regulations for oil and gas are generally devised and enforced by the states,

with the national government exercising responsibility over federal lands and inter-state

pipeline transportation. Both the states and the national government have developed a

high degree of sophistication, experience and expertise over their areas of responsibility.33

The USA has an even longer history of strict adherence to the rule of law, sanctity of

contracts and an aversion to nationalization of natural resources.

Government incentives and support

In addition to fostering micro and macroeconomic conditions conducive for private

sector firms to devise economical methods of extracting unconventional resources, the

US government has provided direct support via public R&D expenditures and tax in-

centives. The Eastern Shale Gas Project, which ran from 1975 to 1992, sought to generate

technologies to make shale gas production viable and transfer the breakthroughs to the

31 ibid (n 13).32 ibid (n 13, n 27).33 ibid (n 23).

Grant Mark Nulle � Prospects for shale development outside the United States 241

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

industry for further refinement and direct application.34 Federal R&D monies also con-

tributed to the cost share of industry demonstration projects such as the first successful

multi-fracture horizontal drilling project in 1986, and assisted Mitchell Energy, which is

credited with combining horizontal drilling with hydraulic fracturing, fund its first hori-

zontal well in the Texas Barnett shale in 1991.35 Likewise, the Crude Oil Windfall Profit

Act of 1980 provided the Alternative Fuel Production Credit that subsidized unconven-

tional energy production in the USA. Until its expiration in 2002, the credit provided

$0.50/MBtu subsidy for shale gas produced. The landmark 1980 legislation also author-

ized the Intangible Drilling Cost Expensing rule which generally covers 70% or more of

the well development costs, a critical tax reform for the small and medium size oil and gas

companies that pioneered shale development.36

Beyond direct R&D expenditure and tax breaks, indirect support for unconventional

oil and gas development has been provided by public and private non-profit research

bodies such as the US Geological Survey, US Department of Energy, and the Potential Gas

Committee at the Colorado School of Mines have accumulated and shared extensive

geological and technical knowledge crucial to mineral and energy development.

Combined with the insights gained from decades of learning-by-doing in the US oil

and gas industry, the geological risk of developing shale resources have been drastically

reduced. From 2006 to 2010, the estimated resource base for shale gas grew by nearly a

factor of five.37

Home truths abroad

Based on the factors identified above, what aspects of the US shale experience can be

replicated elsewhere? Just as no single hydrocarbon regulatory and fiscal system is right

for all countries at all times, using the USA as a benchmark by which all other nations

should model legal, regulatory, fiscal and macroeconomic policy regimes for shale is not

altogether advisable or even practicable. It is unlikely that sovereign nations are going to

break with ancient traditions of state ownership of minerals and hydrocarbons to transfer

or sell hydrocarbon rights to the landowners where those resources reside. Nor is it

plausible these nations can introduce the unique microeconomic and macroeconomic

reforms necessary to foster a large, highly dynamic, and innovative oil and gas sector

composed of scores of small- and medium-sized private sector firms.

Given the unique legal, social, economic and environmental features of the USA, at

best other governments can ‘import and modify’ those aspects of the US model that suit

each country’s particular circumstances. More importantly, the focus should be based not

necessarily on specific measures or features themselves, but the fundamental forces

underlying the specific features.

34 ibid (n 30).35 Michael Shellenberger and others, ‘Where the Shale Gas Revolution Came From’ (2012) Breakthrough Institute.36 ibid (n 14).37 EIA, ‘Annual Energy Outlook 2012’ (11 July 2014).

242 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Based on the US experience and the key considerations posed by shale oil and gas

extraction, countries contemplating exploiting unconventional resources must focus on

these most salient issues:

. Access to and the treatment of unconventional resource rights as distinct from

conventional resources.

. Extended period for exploration and appraisal.

. Flexible relinquishment terms for land and flexible requirements for declaration of

commerciality.

. Early and reliable access to pipeline and other transportation infrastructure.

. Liberalized or guaranteed prices sufficient to cover operational and capital costs.

. Ability to automatically and cheaply import specialized labour and machinery.

. Provide a tax system that encourages rather than inhibits high-risk, high-cost shale

development.

. Provide R&D support and expand availability of geological knowledge to reduce

geologic and technical risks.

. Provide means to efficiently repatriate profits from highly capitalized shale projects

back to investors.

. Ensure stability and predictability of hydrocarbon regulation, permitting, taxation

and policy objectives.

Overall the project economics are pivotal. Successful projects are highly dependent on

specialized equipment and human capital performing extensive and difficult work on

complex geological formations. Because most nations lack the technology and human

capital to perform this work, governments must contract via concessions or production

sharing contracts/agreements (PSCs/PSAs) for shale development to occur. To the extent

governments modify those aspects of its hydrocarbon fiscal and regulatory regimes that

heighten the financial risk of shale projects, the more likely the project economics will

succeed and governments will reap the rewards of shale oil and gas extraction. The key

issues enumerated above are the criterion by which nations with aspirations of successful

shale development should be evaluated. This is the subject of the next section.

4. Comparison of shale fiscal and regulatory regimes

In order to ascertain how countries endowed with shale resources similar in size to the

USA have modified existing hydrocarbon legislation, policies and regulations to make

shale development potentially viable, this report relies on two principal sources. First, the

author developed and distributed a questionnaire38 designed to garner baseline informa-

tion from AIPN country-specific practitioners regarding the fiscal and regulatory envir-

onment in countries possessing significant shale oil and gas resources. The questions were

designed to determine to what extent governments of these nations have configured fiscal

policies and regulatory regimes to anticipate and accommodate the unique

38 See the Appendix.

Grant Mark Nulle � Prospects for shale development outside the United States 243

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

characteristics, opportunities and challenges posed by shale oil and gas. Second, the

author researched national laws and secondary sources of legal and economic research

to supplement AIPN members’ responses to the questionnaire and analysed countries

from which AIPN members’ assistance could not be obtained or in cases where responses

were still pending completion.

For the questionnaire specifically, candidate countries included the following: the

Russian Federation, China, Australia, South Africa, Argentina, Mexico, South Africa,

Colombia, Brazil, Algeria, Indonesia, Poland, Tunisia, France and the UK. The question-

naire was distributed beginning 23 June 2014 and responses were received through 4

September 2014.

Full or partial questionnaire responses were obtained from AIPN practitioners in the

Russian Federation, Australia, Poland, Indonesia, Argentina, France, the UK and Mexico,

with responses being completed, but not yet returned to the author from Algeria and

Tunisia.39 Table 3 presents the names of the firms and individual AIPN members that

generously answered the baseline questionnaire or answered the author’s questions via

private correspondence.40

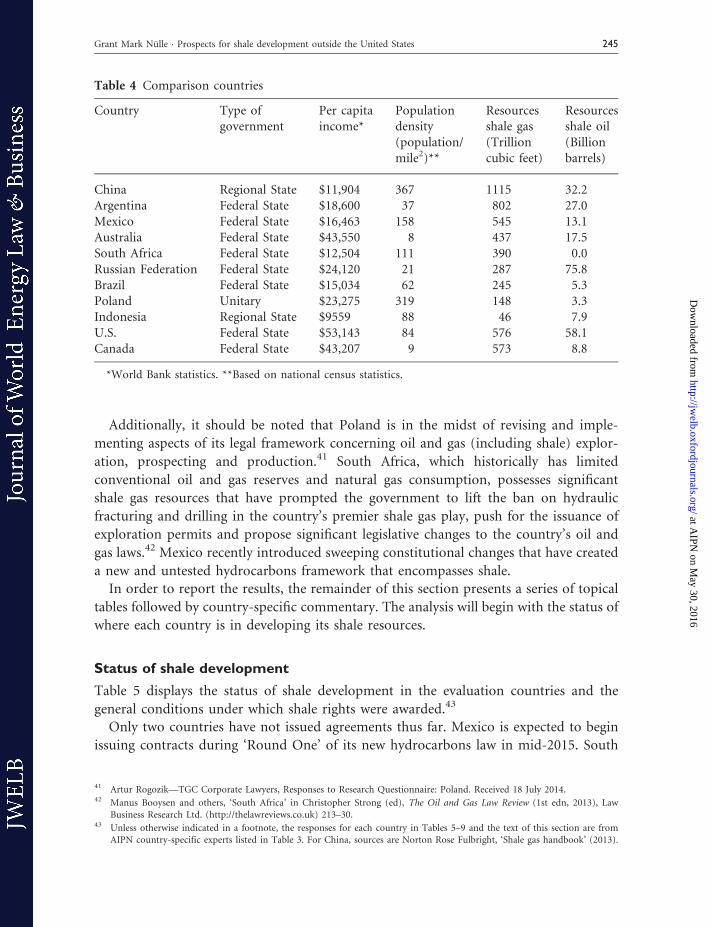

Table 4 lists the countries included in this initial comparison. The nations vary con-

siderably in geographic location, economic and demographic indicators, type of govern-

ment, and volume of technically recoverable shale resources. For further comparison the

USA and Canada are included as well.

Table 3 Questionnaire respondents

Country Firm(s) Lead Respondent(s)

South Africa Webber Wentzel Kenny Paton

Russian

Federation

King & Spalding—Moscow Alexandra Rotar Jennifer Josefson

Poland TGC Corporate Lawyers BNK

Polska

Artur Rogozik Jacek Wroblewski

Mexico Lopez Velarde, Heftye y Soria

Mayer Brown LLP—Houston

Jorge Jimenez Jose L. Valera

Indonesia PT Chevron Pacific Indonesia Peter Dumanauw Rachmat

Abdoellah

Brazil State University of Rio de Janeiro Illana Zeitoune Marilda Rosado

Australia Cowell Clark Paul Bradley Leah Cowell

Argentina Shell Oil Exploration &

Production Company

Rick Goenner

39 AIPN members were reached in Tunisia and Algeria. Since initial contact, agreement to answer the questionnaire and follow-up

emails, questionnaire responses have not been returned. No AIPN practitioners could be reached for China or Colombia.40 It should be noted that the responses received from AIPN members are subject to change as country conditions, politics and

policies respond to the unique challenges posed by shale resources and other exogenous transformations occur. As such, the

need for ongoing research and revisions to this article becomes paramount.

244 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Additionally, it should be noted that Poland is in the midst of revising and imple-

menting aspects of its legal framework concerning oil and gas (including shale) explor-

ation, prospecting and production.41 South Africa, which historically has limited

conventional oil and gas reserves and natural gas consumption, possesses significant

shale gas resources that have prompted the government to lift the ban on hydraulic

fracturing and drilling in the country’s premier shale gas play, push for the issuance of

exploration permits and propose significant legislative changes to the country’s oil and

gas laws.42 Mexico recently introduced sweeping constitutional changes that have created

a new and untested hydrocarbons framework that encompasses shale.

In order to report the results, the remainder of this section presents a series of topical

tables followed by country-specific commentary. The analysis will begin with the status of

where each country is in developing its shale resources.

Status of shale development

Table 5 displays the status of shale development in the evaluation countries and the

general conditions under which shale rights were awarded.43

Only two countries have not issued agreements thus far. Mexico is expected to begin

issuing contracts during ‘Round One’ of its new hydrocarbons law in mid-2015. South

Table 4 Comparison countries

Country Type of

government

Per capita

income*

Population

density

(population/

mile2)**

Resources

shale gas

(Trillion

cubic feet)

Resources

shale oil

(Billion

barrels)

China Regional State $11,904 367 1115 32.2

Argentina Federal State $18,600 37 802 27.0

Mexico Federal State $16,463 158 545 13.1

Australia Federal State $43,550 8 437 17.5

South Africa Federal State $12,504 111 390 0.0

Russian Federation Federal State $24,120 21 287 75.8

Brazil Federal State $15,034 62 245 5.3

Poland Unitary $23,275 319 148 3.3

Indonesia Regional State $9559 88 46 7.9

U.S. Federal State $53,143 84 576 58.1

Canada Federal State $43,207 9 573 8.8

*World Bank statistics. **Based on national census statistics.

41 Artur Rogozik—TGC Corporate Lawyers, Responses to Research Questionnaire: Poland. Received 18 July 2014.42 Manus Booysen and others, ‘South Africa’ in Christopher Strong (ed), The Oil and Gas Law Review (1st edn, 2013), Law

Business Research Ltd. (http://thelawreviews.co.uk) 213–30.43 Unless otherwise indicated in a footnote, the responses for each country in Tables 5–9 and the text of this section are from

AIPN country-specific experts listed in Table 3. For China, sources are Norton Rose Fulbright, ‘Shale gas handbook’ (2013).

Grant Mark Nulle � Prospects for shale development outside the United States 245

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Africa has received applications for exploration rights from Shell Oil Exploration &

Production, Bundu Gas and Falcon Oil & Gas.

In China, commercial production has already commenced. While the volumes con-

tribute less than 1% of total natural gas production, compared to 39% in the USA and

15% in Canada, the rapid emergence of shale production speaks to the importance the

Chinese national government attaches to it.44 In its 12th Five-Year Plan developed in

2012, China set the target of annual shale gas production of 6.5 billion cubic metre (bcm)

Table 5 Questionnaire responses concerning shale development

Country Have concessions or

PSCs involving

shale oil and gas

been issued?

What stage of the project

lifecycle have the most

advanced projects

reached?

Are shale rights treated

separately or included in

a conventional

Concession / PSC?

China Yes Commercial production Shale leased separately

Argentina Yes Appraisal Rights issued by national

or provincial operating

company

Mexico Not under the new

legislation

PEMEX has drilled

exploratory wells in

several basins

E&P Contract will be

based on a certain

surface and depth

attributes, allowing for

different rights on the

same land

Australia Yes, in five of six

states

Production stage in two

states

Shale and conventional

resources included in

petroleum titles

South Africa None issued, but

exploration

applications

under review

Technical cooperation

stage; no exploration at

this juncture

To be included in con-

ventional concession

Russian

Federation

Yes, albeit under

concessions

covering

conventional

production

Exploration or Appraisal Shale can be included in

conventional concession

agreement

Brazil Yes Exploration or Appraisal Included in same

concession

Poland Yes Exploration or Appraisal Shale covered under trad-

itional concession &

mining usufruct

Indonesia Yes Exploration Separate but based on

conventional PSC

44 ibid (n 21).

246 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

of shale gas annually by 2015 and 60–100 bcm by 2020. Other objectives include com-

pleting surveys and evaluations of the country’s shale gas resources by 2015, selecting

30–50 shale gas prospects and 50–80 favourable target areas, and developing shale gas

exploration technology and equipment. Australia has reached the production stage in the

Copper Basin in the State of South Australia as well as in the State of New South Wales.

In contrast, Brazil remains in the formative stages of shale development. The country

has 29 sedimentary basins with the potential for conventional and unconventional hydro-

carbons, covering 4.7 million square miles, a third of which is located offshore.45

However, 78% of the land has little or no geologic knowledge and only 5% of the

entire area has petroleum wells in operation.46 Because so little of the country’s conven-

tional resources have been explored, the commercial attractiveness of the pre-salt areas

dominates national attention, and the prioritization of offshore production by Petrobras

demands scarce machinery, labour and capital, the country remains in the very early

stages of shale E&P.47

Regarding the treatment of unconventional resources in concessions or PSCs, the

countries vary considerably. China recognizes shale as a separate mineral distinct from

conventional hydrocarbons and has categorized shale as the 172nd mineral asset.

Furthermore, China has successfully launched two rounds of public bidding for shale

rights in 2010 and 2012.

In Poland, rights to unconventional resources can be obtained separately from con-

ventional resources, but must undergo the same process to obtain such rights. Polish law

requires two legal titles to be able to prospect for, explore or produce shale gas and oil or

conventional gas or oil—a concession and a mining usufruct. The concession is an ad-

ministrative decision issued by the Minister of Environment allowing the entity to carry

out prospecting, exploration or production activity in a defined area, after having met the

conditions prescribed by law, setting out in particular the scope and method of work.

A mining usufruct is a civil law title allowing the entity to enter and take benefits of the

subsurface owned by the Polish State. The Polish Minister of Environment has issued

concessions to and signed mining usufruct agreements with IOCs for the express purpose

of shale gas and oil exploration and recognition discovery, but not production. As of May

2014, there are 82 concessions held by 21 domestic and foreign operators in Poland.

Indonesia follows a similar tack, with rights to unconventional resources leased sep-

arately, albeit structured under the nation’s traditional PSC for conventional oil and gas.

Likewise, Argentina has not developed concessions expressly for shale gas and oil, but is

instead trying to adapt current conventional concessions for shale operations. Australia’s

onshore petroleum regimes treat shale resources in the same manner as conventional

petroleum resources. South Africa’s geo- and mineral-centric licensing regime is config-

ured such that all hydrocarbons contained within an area may be explored and extracted

regardless of depth.

45 ibid (n 23).46 ANP—Agencia Nacional do Petroleo, ‘Anuario Estatıstico Brasileiro do Petroleo, Gas Natural e Biocombustı- veis 2013’

5http://www.anp.gov.br/?pg¼668334 accessed 18 July 2014.47 ibid (n 23).

Grant Mark Nulle � Prospects for shale development outside the United States 247

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

In Russia, shale rights are subsumed in the broader concession agreement. Russian

regulations for the exploration and production of unconventional hydrocarbon resources

remain in the formative stages of development; as such, there are no specific procedures

in place for the award of subsoil use rights with respect to shale gas and oil. Nonetheless,

subsoil use rights for unconventional resources can be awarded on the same basis as

conventional oil or gas (eg via auction or tender), but the subsoil licence would not

explicitly state that issuance is predicated on the existence of unconventional resources—

even if the licence does contain such resources. Indeed, entities holding subsoil licences

may already have rights to unconventional resources located within the licensed acreage,

depending on the terms of the particular licence.

However, two practical problems remain. First, it is currently not possible under the

Russian Federation’s regulatory regime for a holder of a subsoil licence to amend it to

obtain ‘deep rights’ if they have not been initially included in the licence (eg the depth

stipulated in the licence is shallower than the unconventional resources); nor is it possible

for another subsoil user to obtain ‘shallow rights’ with respect to the deep resources

underlying the licence area of another licence holder. Secondly, most of the unconven-

tional reserves have not been recognized as recoverable reserves and, therefore, are not

included in the Russian Federation’s official calculation of national reserves. In that case

the unconventional resources are not included as ‘discovered’ reserves in the individual

subsoil licences for blocks in which the unconventional reserves are located. This means

that holders of subsoil licences do not possess the right to develop unconventional re-

serves until process of exploration and discovery are complete.

In order to develop unconventional reserves that are not included in the Russian

Federation’s calculation of reserves, the subsoil user must provide detailed evidence of

the reserves’ existence to federal authorities and apply for their registration in the State

balance of reserves. An expert opinion of a special commission within the Federal Agency

for Subsoil Use and a formal decision of the Federal Agency for Subsoil Use on inclusion

of reserves in the State balance of reserves are required to obtain registration of the

reserves in the State balance.

Under Mexico’s newly promulgated hydrocarbons law (Ley de Hidrocarburos) licensing

rounds awarding blocks to private operators will commence in 2015 to include separate

blocks for shale plays, deep-water offshore and onshore conventional projects. The

Ministry of Energy will determine the type of contract to be used for each project,

whether a licence, PSA or profit-sharing agreement. Shale development projects are

likely to be issued as licences, while PSAs are more likely to be used offshore.

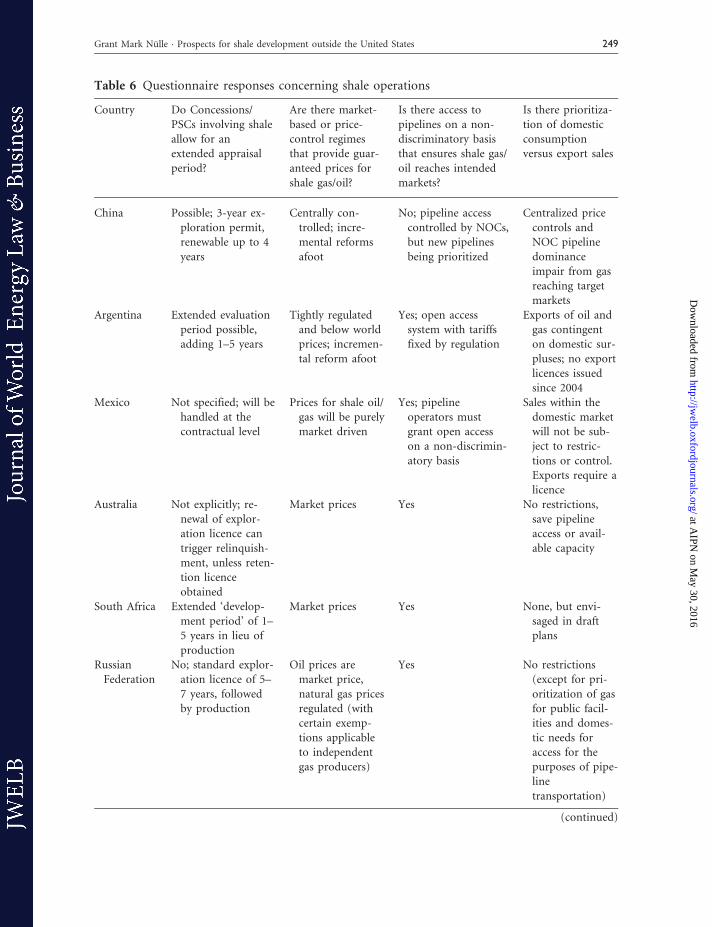

Operational considerations

Table 6 displays how the comparison countries approach key operational considerations,

such as an extended appraisal period, price regime, pipeline access and restrictions on

distribution of shale oil and gas production.

In terms of extensions to appraisal terms, a number of the comparison countries have

allowed for special considerations—with each approaching the matter differently.

248 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Table 6 Questionnaire responses concerning shale operations

Country Do Concessions/

PSCs involving shale

allow for an

extended appraisal

period?

Are there market-

based or price-

control regimes

that provide guar-

anteed prices for

shale gas/oil?

Is there access to

pipelines on a non-

discriminatory basis

that ensures shale gas/

oil reaches intended

markets?

Is there prioritiza-

tion of domestic

consumption

versus export sales

China Possible; 3-year ex-

ploration permit,

renewable up to 4

years

Centrally con-

trolled; incre-

mental reforms

afoot

No; pipeline access

controlled by NOCs,

but new pipelines

being prioritized

Centralized price

controls and

NOC pipeline

dominance

impair from gas

reaching target

markets

Argentina Extended evaluation

period possible,

adding 1–5 years

Tightly regulated

and below world

prices; incremen-

tal reform afoot

Yes; open access

system with tariffs

fixed by regulation

Exports of oil and

gas contingent

on domestic sur-

pluses; no export

licences issued

since 2004

Mexico Not specified; will be

handled at the

contractual level

Prices for shale oil/

gas will be purely

market driven

Yes; pipeline

operators must

grant open access

on a non-discrimin-

atory basis

Sales within the

domestic market

will not be sub-

ject to restric-

tions or control.

Exports require a

licence

Australia Not explicitly; re-

newal of explor-

ation licence can

trigger relinquish-

ment, unless reten-

tion licence

obtained

Market prices Yes No restrictions,

save pipeline

access or avail-

able capacity

South Africa Extended ‘develop-

ment period’ of 1–

5 years in lieu of

production

Market prices Yes None, but envi-

saged in draft

plans

Russian

Federation

No; standard explor-

ation licence of 5–

7 years, followed

by production

Oil prices are

market price,

natural gas prices

regulated (with

certain exemp-

tions applicable

to independent

gas producers)

Yes No restrictions

(except for pri-

oritization of gas

for public facil-

ities and domes-

tic needs for

access for the

purposes of pipe-

line

transportation)

(continued)

Grant Mark Nulle � Prospects for shale development outside the United States 249

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Indonesia, Poland and China have appraisal terms best-suited for conventional resources,

while the new hydrocarbons law in Mexico has yet to spell out specifics for shale.

Argentina, Australia, Brazil, South Africa and Russia have measures that at least par-

tially address the extended appraisal period needed for shale. The Argentine Province of

Neuquen allows exploration licence-holders that discover conventional or unconven-

tional resources that are not commercially exploitable at the time of discovery to request

an ‘evaluation period’ to gauge the commercial potential of discovery.48 The extension of

the evaluation period can vary between one to 5 years based on field characteristics and

the time remaining on the exploration permit. The extended evaluation period does come

at a cost however. For conventional resources, surface fees increase four-fold while un-

conventional resources increase seven-fold.

In Australia, the general exploration licence provisions that apply to conventional gas

exploration also apply to shale gas, posing significant issues for the latter. For example, in

the State of South Australia if the 5-year exploration term is renewed once that renewal

triggers 50% relinquishment. If renewal occurs a second time, the licensed area must be

relinquished further such that the tenement holder only holds 33% of the original

licensed area. To properly explore for shale resources licence-holders need both to

extend the exploration period while retaining the entirety of the licensed area. In order

to accomplish this, a licencse holder can obtain a Retention Licence from the State of

South Australia49 that does not mandate any relinquishment of the licensed area. The

retention license has a term of 5 years that may be renewed for a further 5 years if state

Table 6 Continued

Country Do Concessions/

PSCs involving shale

allow for an

extended appraisal

period?

Are there market-

based or price-

control regimes

that provide guar-

anteed prices for

shale gas/oil?

Is there access to

pipelines on a non-

discriminatory basis

that ensures shale gas/

oil reaches intended

markets?

Is there prioritiza-

tion of domestic

consumption

versus export sales

Brazil Yes, extended explor-

ation phase avail-

able for 2–6 years

Market prices Yes No restrictions

Poland Not under current

Geological and

Mining Law

Work underway to

achieve liberal-

ized natural gas

market

NA NA

Indonesia Not in current un-

conventional PSC

A quasi market-

based price

regime depend-

ing on export

access

No guarantee of

third-party access

Domestic Market

Obligation of up

to 25% or higher

48 ibid (n 1).49 The State of Western Australia has a similar provision. Petroleum and Geothermal Energy Resources Act 1967.

250 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

authorities are satisfied the contract area will be commercially feasible within 15 years of

the first issuance of a retention license. However, if the licence-holder wishes to move

from an exploration licence to a retention licence, the South Australia Act requires a

‘discovery’ of petroleum. What constitutes a discovery of unconventional gas and oil is

not defined in the Act and may well vary from the traditional conventional gas concept of

a discovery. As such, legislative clarification is needed to make this a viable legal vehicle to

extend the exploration and appraisal period for.

The general licensing regime in the Russian Federation provides for a standard 5-year

exploration licence that allows for (i) an additional 2 years if the exploration licence is

performed on subsoil plots located within the regions of Kamchatka, Khabarovsk,

Sakhalin and Yakutia and other regions specified in the Subsoil Law, and (ii) an add-

itional 5 years for geological works carried out within the internal sea waters, the terri-

torial sea and the continental shelf of Russia.50 Upon discovery of oil, a production

licence is issued without a tender or auction to the holder of the exploration licence.

However, for deposits that have already proven reserves but require substantial additional

exploration a Combined Licence may be issued. The term of a combined licence is split

between the period required for the exploration and the period required for the produc-

tion. Combined licences are awarded by tender or auction.

Among the comparison countries, Brazil and South Africa are unique in that their

concession agreements and production licences, respectively, provide for an extended

appraisal period. In Brazil, if a concessionaire makes a discovery of unconventional re-

sources during the exploration phase, the concessionaire, may at its sole discretion work

within an Extended Exploration Phase, lasting up to 6 years (up to three 2-year terms).51

Granting of the extended exploratory period is predicated on certification by Brazilian

authorities of the discovery of unconventional resources and government approval of an

unconventional resources exploration and evaluation plan.

In South Africa, there are at least two avenues to obtain a de facto extension of the

appraisal period. First, in the case where a holder of an exploration right52 discovers

petroleum, but the economical production of the resource is contingent on whether the

attendant natural gas resources can be economically sold as well, then the rights holder

has the option to suspend a production right for up to 5 years. In lieu of production

commencing, a ‘development period’ begins from the effective date of the production

right during which the holder of the right must conduct studies to determine whether the

gas can be commercially produced. Second, the Mineral and Petroleum Resources

Development Act (MPRDA),53 provides ministerial discretion in amending any aspect

of a right, including the duration thereof.

50 Jennifer Josefson, Alexandra Rotar, and Brandon Rice, King & Spalding—Moscow, ‘Oil and Gas Regulation in the Russian

Federation: Overview’ (2014) Practical Law Multi-Jurisdictional Guide 2014: Energy and Natural Resources.51 ANP, Brazil, ‘Concession Contract for Exploration and Production of Oil and Natural Gas for the 12th Bidding Round’

Received via private correspondence from Illana Zeitoune 25 August 2014.52 In South Africa a ‘right’ (eg prospecting, exploration, production) is equivalent to a licence in other countries.53 Chapter 6, Section 102 5http://www.dmr.gov.za/publications/summary/109-mineral-and-petroleum-resources-development-

act-2002/225-mineraland-petroleum-resources-development-actmprda.html4

Grant Mark Nulle � Prospects for shale development outside the United States 251

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Turning to the pricing regimes, the comparison countries feature a full spectrum from

market-based prices to centrally controlled, and everything in between. As a developed

country steeped in the Anglo-Saxon traditions of law and market economics, Australia

operates a market-based price system. On the other hand, China and Argentina tightly

regulate the price of oil and gas, with domestic prices de-linked and significantly lower

than world prices.

Nevertheless, the pendulum is swinging towards further price liberalization in the

following countries:

. Mexico’s new hydrocarbons legislation envisions market-driven prices for shale

resources.

. China announced plans in 2011 to liberalize the wellhead price of unconventional

gas and pilot reform schemes have been underway since 2012 in Guangdong and

Guangxi provinces with liberalized prices at the point of extraction and linked to

import prices in Shanghai.54

. Natural gas liberalization efforts are underway in Poland.55

. Argentina has recently offered ‘Guaranteed Price Agreements’ for sales of incremen-

tal natural gas output above an adjusted base supply quantity to the domestic

market. The law provides a minimum price of $7.5/MBtu that is nearly three

times the average domestic price.56

Regarding pipeline access, six of the countries require pipeline operators to provide

open access on a non-discriminatory basis, subject to available capacity. Conversely,

pipeline transportation is a major issue in China. The USA has more than 305,000

miles of interstate and intrastate transmission pipelines, more than 100 times the mileage

of China.57 Just as important, China’s natural gas pipelines are virtually monopolized by

the NOCs Sinopec and CNPC,58 which are not obligated by law to accept privately

produced shale gas on their pipelines.59 This discriminatory access to pipelines puts

the NOCs at a distinct competitive advantage vis-a-vis private operators in terms of

economically developing shale. To address these issues, the Chinese government plans

to construct 27,400 additional miles of natural gas pipelines by 2015, effectively doubling

its present level.60 In June 2013, the first dedicated shale gas pipeline in Sichuan province

began construction. Furthermore, China’s National Energy Administration has encour-

aged the use of private capital to facilitate the construction of pipeline infrastructure, and

54 Reuters News, ‘China Reforms Shale Gas Price, Pilots New Scheme’ (2011)5http://www.reuters.com/article/2011/12/27/china-

gas-pricing-idUSL3E7NR3UR201112274 accessed 3 August 2014.55 Oil and Gas Institute—Krakow, ‘The Polish Petroleum and Natural Gas Market’ (2013)5http://www.inig.pl/inst/RPNIG/files/

Rynek2013EN.pdf4 accessed 17 August 2014.56 ibid (n 1).57 EIA, ‘China – Analysis’5http://www.eia.gov/countries/cab.cfm?fips¼CH4 accessed 27 August 2014.58 Susan Forbes, ‘The United States and China: Moving toward Responsible Shale Gas Development’ (2013) Draft Paper,

Brookings Institution, Washington DC.59 Ella Chou, ‘Shale Gas in China: Development and Challenges’ (2013) Draft Manuscript, Harvard University Law School.

5http://blogs.law.harvard.edu/ellachou/files/2013/07/Shale-Gas-in-China-Draft.pdf4 accessed 15 July 2014.60 ibid.

252 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

for the first time in October 2013 the Chinese government announced that shale gas

producers and distributors should be able to access the existing pipeline network and

infrastructure on a non-discriminatory basis61—a major policy shift.

Lack of pipeline capacity impairs broad marketing and consumption of natural gas in

Brazil as well. Brazil’s gas network currently comprises 5100 miles of pipeline.

Additionally, Brazil’s new regulatory framework for building pipelines, which features

competitive bidding for the concessions to build new gas pipelines as well as requires

documented demand for transportation, has scarcely been tested, elevating uncertainty

regarding the ability of shale operators to get unconventional resources to market.

Finally, prioritization of shale oil and gas output between domestic consumption and

export sales is decidedly mixed among the comparison countries. The most explicit

example of domestic market obligations (DMO) is found in Indonesia, which requires

a DMO of 25% or greater depending on demand requirements. Combine Indonesia’s

DMO with heavily-subsidized domestic oil and gas prices de-linked from world prices, a

relatively limited pipeline infrastructure, and no guarantee of operator access to pipeline

infrastructure, it is clear the country faces significant challenges to making shale oil and

gas economics viable.

At present, South Africa has no DMO measures in place, but that could change in the

near future. The ‘Gas Utilisation Master Plan’ being developed by the country is expected

to include some DMO measures. It remains to be seen whether such preferences will

manifest as statutory changes, contractual obligations or be rooted in government policy

pronouncements.

Fiscal considerations

Table 7 displays how the comparison countries approach key fiscal issues that can acutely

affect the economic viability of shale projects, including incentives and R&D spending,

ring-fencing provisions and export taxes.

More than half of the comparison countries offer incentives or are contemplating

making tax reductions available, with each taking a slightly different tack. Indonesia

provides for a lower government ‘take’ to incentivize IOC interest in shale projects.

Mexico’s new Hydrocarbons Income Law (Ley de Ingesos sobre Hidrocarburos) provides

both specific and general tax incentives to facilitate private sector shale development

investments. The former entails a royalty exemption on gas prices below $5/MBtu

while the latter measures concern the following:

Income tax deductions:

. 100% of the original investment amount made for exploration, secondary and im-

proved recovery, and non-capitalized maintenance, in the fiscal year when they were

made;

61 Sidley Austin LLP, ‘China’s First Shale Gas Policy’ (2013) 5http://www.sidley.com/Chinas-First-Shale-Gas-Policy-11-12-

2013/4 accessed 22 August 2014.

Grant Mark Nulle � Prospects for shale development outside the United States 253

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

Table 7 Questionnaire responses concerning fiscal policy

Country Do concessions or

PSCs provide tax

incentives and/or

R&D support?

Does project ring-

fencing for tax and

cost recovery purposes

apply?

Is shale production

exempt from

export taxes?

Are there

Guarantees of tax

stability over the

life of the shale

gas/oil project?

China Yes; multiple in-

centives available

If the contractor has

more than one con-

tract, it can offset

the tax losses against

profits from other

contracts

Export taxes

imposed on all

hydrocarbons

No

Argentina None specifically,

but promotion

of major hydro-

carbon invest-

ments on offer

Strict ring-fencing Export taxes

imposed on all

hydrocarbons

No

Mexico Yes; royalty ex-

emption for

shale gas sold

below $5/MBtu

threshold

New law relaxes strict

ring-fencing, but

falls short of conso-

lidated tax return

Unclear at this

point

Not anticipated

Australia None Project ring-fencing

not imposed as part

of corporate tax

liability

Exemptions con-

sistent with other

Australian

exports

No

South Africa Income tax laws

contain favour-

able provisions

for hydrocarbons

generally

Ring-fencing applies No export taxes

currently, but

expected as

sector develops

Yes

Russian

Federation

Yes; beneficial rate

of mineral ex-

traction tax for

‘difficult reserves’

Project ring-fencing

not imposed as part

of corporate tax

liability

Beneficial rate

provided for

calculation of

export customs

rates

No, except for

legacy PSAs

Brazil Yes, 1% of gross

revenues from

projects reserved

for R&D

Project ring-fencing

not imposed as part

of corporate tax

liability

No export tax on

shale gas exists

in Brazil

No

Poland Not currently; tax

changes antici-

pated in 2015

Project ring-fencing

not imposed as part

of corporate tax

liability

No export tax on

shale gas exists

in Poland

No

Indonesia Yes, via lower gov-

ernment take

Strict ring-fencing No exemption.

Need to secure

export permit

No

254 Journal of World Energy Law and Business, 2015, Vol. 8, No. 3

at AIPN

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from

. 25% of the original investment amount made for the development and production

of oil or natural gas field, in every fiscal year;

. 10% of the original investment amount made for storage and transportation infra-

structure essential to carry out the activities under the E&P Contract, such as oil

pipelines, gas pipelines, storage terminals or tanks, required to take the production

to delivery, metering or audit points determined under each E&P Contract, in each

fiscal year.

South Africa provides similar tax considerations to Mexico. The Tenth Schedule of the

Income Tax Act, 1962, contains provisions for oil and gas companies. Regarding capital

allowances, not only can companies deduct all expenditures and losses actually incurred,

but a supplemental deduction is permitted over and above the expenditure actually

incurred. These supplemental deductions include 100% of all capital expenditures incurred

for exploration activities and 50% of all capital expenditures incurred for post-exploration

activities. Effectively, an oil and gas company may recognize a deduction equal to 200% of

its capital expenditures related to exploration and 150% post-exploration.62 Additionally, a

dividends tax of up to 5% is generally levied on oil and gas companies. However, if the

income to be taxed is singularly derived from and oil and gas production right and no other

related or unrelated activity, than the income is exempted from dividends tax. Sundry

withholding taxes assessed on interest, services and hydrocarbon royalties may also be

offset in part or altogether depending on double taxation treaties.63

Amendments to the Russian Federation’s Mineral Extraction Tax that became effective

in January 2014 provide an advantageous tax rate for extraction of tight oil64 or ‘difficult

reserves’. Pursuant to these changes the standard tax rate for extracted oil is multiplied by

a number of coefficients that are determined by the permeability of hydrocarbon re-

source, size of the oil-filled formation, and depletion of reserves of ‘difficult oil’.

Effectively a 0% rate for the mineral extraction tax is specifically established for the

following shale-rich formations: Bazhenov, Abalak, Khadym and Domanic.65 In all

such cases, the preferential tax treatment only applies to shale oil, not gas.

In addition to the $0.064 per cubic meter subsidy for shale gas produced from 2012 to

2015, China’s Shale Gas Industry Policy released in October 2013 strengthens the coun-

try’s financial support for shale production. The policy announcement includes (i) des-

ignating shale gas as one of the nation’s strategic emerging industries; (ii) providing

national subsidies and encouraging provincial subsidies to shale producers; (iii) tax re-

ductions and exemptions for producers; (iv) customs tariff exemptions for imported

equipment.66 With government approval, shale gas projects could be exempt from the

Mineral Resources Compensation Fee and from the country’s royalty regime.67

62 E&Y—Ernst & Young, ‘Global Oil and Gas Tax Guide 2014’ (2014).63 PwC—PricewaterhouseCoopers, ‘Oil and Gas Tax Guide for Africa 2013’ (2013).64 ibid (n 51).65 ibid (n 63).66 ibid (n 63).67 ibid (n 44).

Grant Mark Nulle � Prospects for shale development outside the United States 255

at AIPN

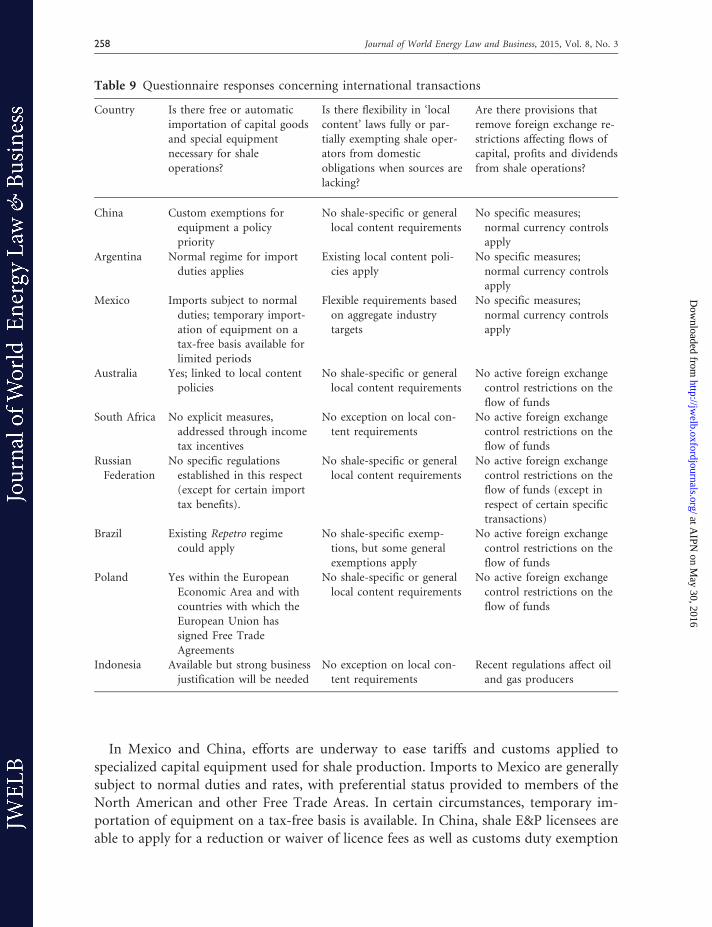

on May 30, 2016

http://jwelb.oxfordjournals.org/

Dow

nloaded from