Proposed Accounting Standards Update to Lease Accounting February 22, 2011

Proposed Accounting Standards Update to Lease Accounting February 22, 2011.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Proposed Accounting Standards Update to Lease AccountingFebruary 22, 2011

2 February 10, 2011

Presenters

Paul Anderson, CPADirector of AssuranceGBQ Partners LLC

Jeff Alton, CPAAssurance ManagerGBQ Partners LLC

Today’s presenters:

3

Overview

• The core principle is that lease contracts give rise to assets and liabilities that should be reflected in the balance sheets of lessees and lessors.

• All lessees would use a single method of accounting for all leases.

• The accounting by a lessor would reflect its exposure to the risks or benefits of the underlying leased asset.

• Users of financial statements would have more timely information about variable features such as renewal options and contingent rentals.

• A simplified approach would apply to short-term leases.

• The proposal does not change the current definition of a lease contract.

February 10, 2011

Proposed Accounting Standards Update: Leases (Topic 840)

• Released August 2010/Joint project with IASB

• Significant change to existing lease accounting model

• Would impact both lessees and lessors

• Eliminates off-balance sheet (i.e., operating) leases

• Retrospective application on adoption, thus no grandfathering of existing leases is expected

• Comment period ended: December 15, 2010

• Final standard issuance: June 2011 (expected)

• Effective date: ?

February 10, 20114

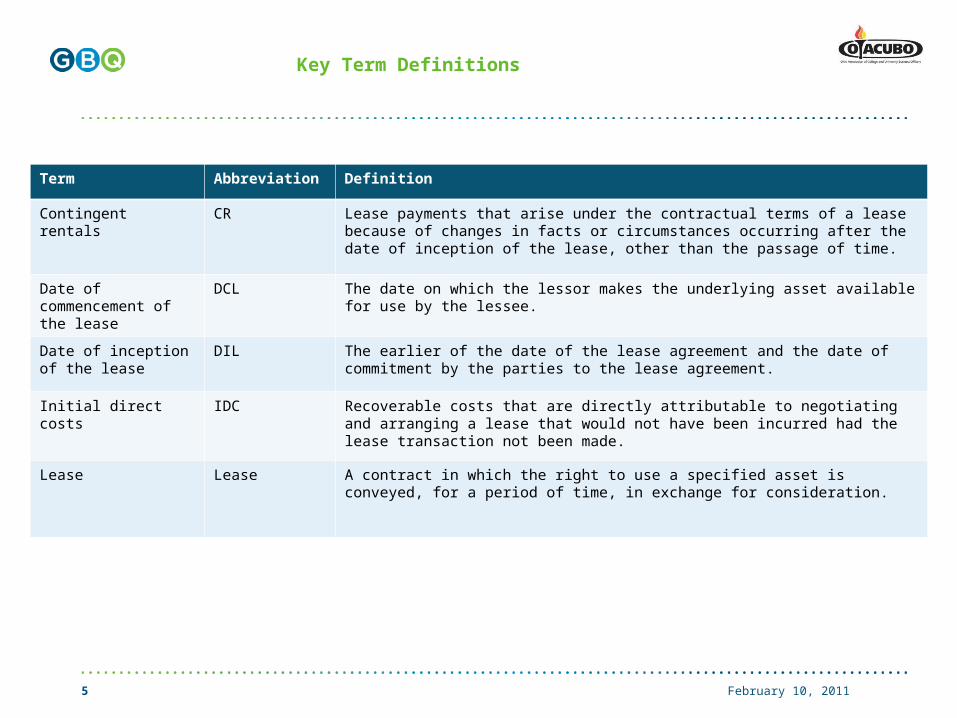

Key Term Definitions

Term Abbreviation Definition

Contingent rentals

CR Lease payments that arise under the contractual terms of a lease because of changes in facts or circumstances occurring after the date of inception of the lease, other than the passage of time.

Date of commencement of the lease

DCL The date on which the lessor makes the underlying asset available for use by the lessee.

Date of inception of the lease

DIL The earlier of the date of the lease agreement and the date of commitment by the parties to the lease agreement.

Initial direct costs

IDC Recoverable costs that are directly attributable to negotiating and arranging a lease that would not have been incurred had the lease transaction not been made.

Lease Lease A contract in which the right to use a specified asset is conveyed, for a period of time, in exchange for consideration.

February 10, 20115

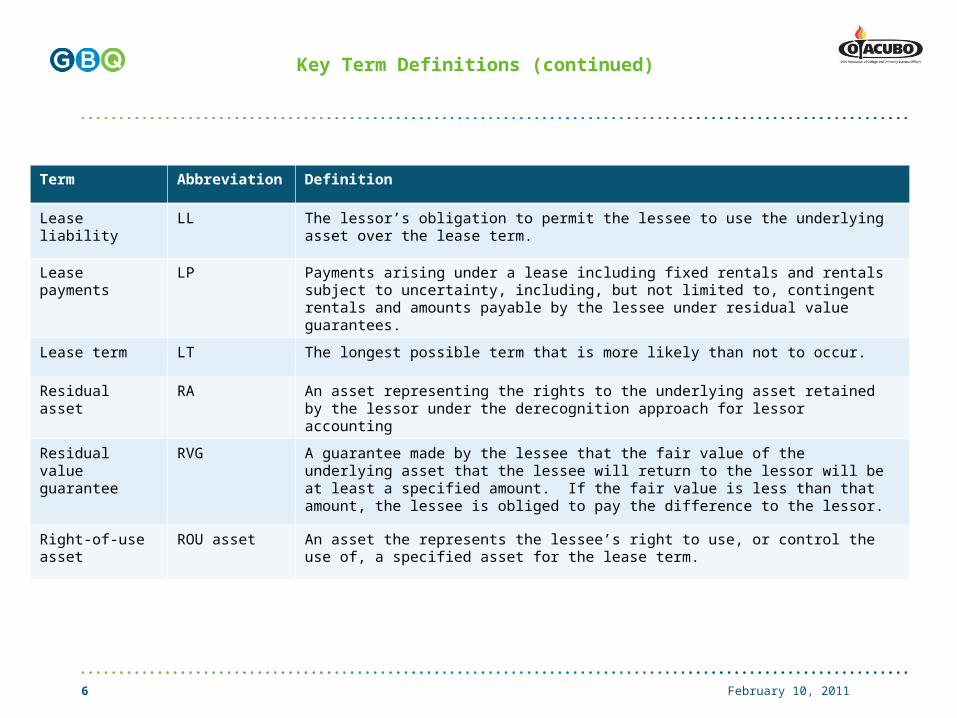

Key Term Definitions (continued)

Term Abbreviation Definition

Lease liability

LL The lessor’s obligation to permit the lessee to use the underlying asset over the lease term.

Lease payments

LP Payments arising under a lease including fixed rentals and rentals subject to uncertainty, including, but not limited to, contingent rentals and amounts payable by the lessee under residual value guarantees.

Lease term LT The longest possible term that is more likely than not to occur.

Residual asset

RA An asset representing the rights to the underlying asset retained by the lessor under the derecognition approach for lessor accounting

Residual value guarantee

RVG A guarantee made by the lessee that the fair value of the underlying asset that the lessee will return to the lessor will be at least a specified amount. If the fair value is less than that amount, the lessee is obliged to pay the difference to the lessor.

Right-of-use asset

ROU asset An asset the represents the lessee’s right to use, or control the use of, a specified asset for the lease term.

February 10, 20116

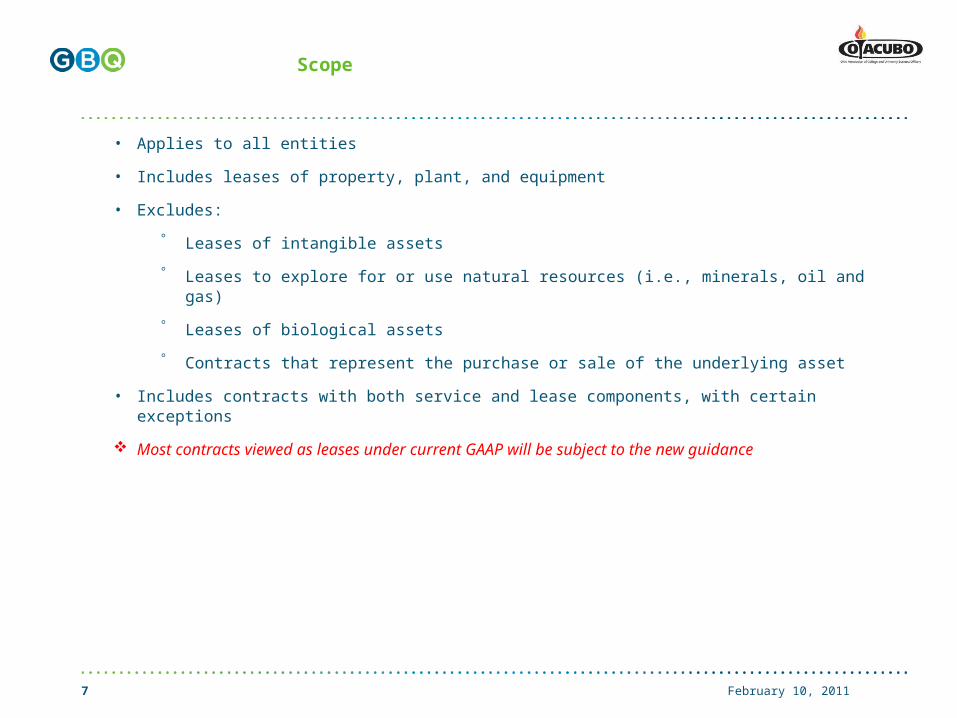

Scope

• Applies to all entities

• Includes leases of property, plant, and equipment

• Excludes:

Leases of intangible assets

Leases to explore for or use natural resources (i.e., minerals, oil and gas)

Leases of biological assets

Contracts that represent the purchase or sale of the underlying asset

• Includes contracts with both service and lease components, with certain exceptions

Most contracts viewed as leases under current GAAP will be subject to the new guidance

February 10, 20117

Lessee Accounting Model - Recognition

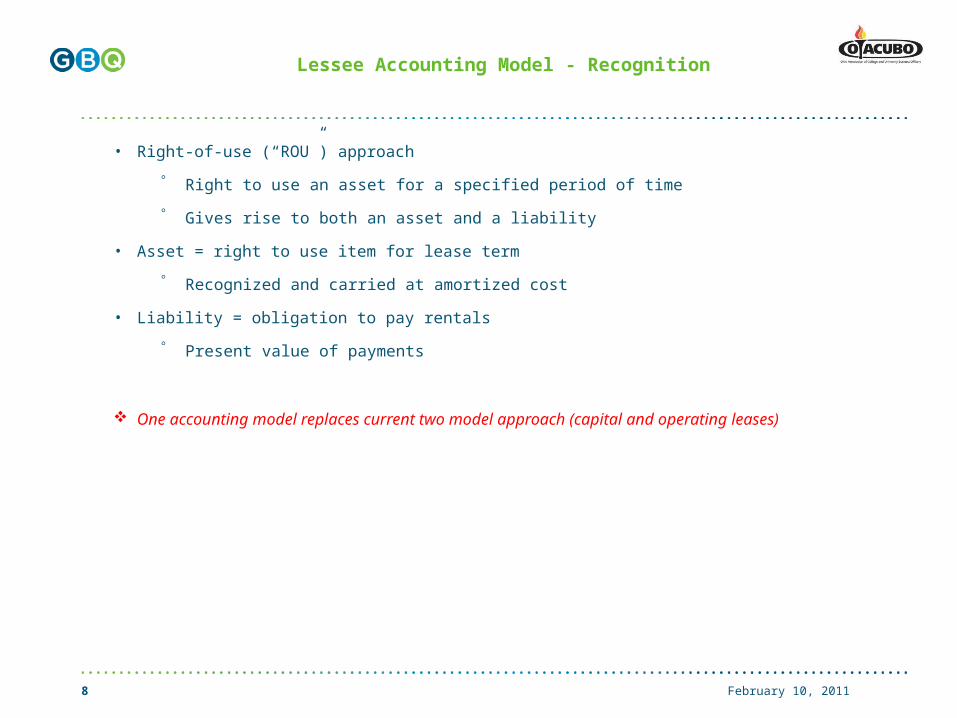

• Right-of-use (“ROU”) approach

Right to use an asset for a specified period of time

Gives rise to both an asset and a liability

• Asset = right to use item for lease term

Recognized and carried at amortized cost

• Liability = obligation to pay rentals

Present value of payments

One accounting model replaces current two model approach (capital and operating leases)

February 10, 20118

Lessee Accounting Model - Recognition

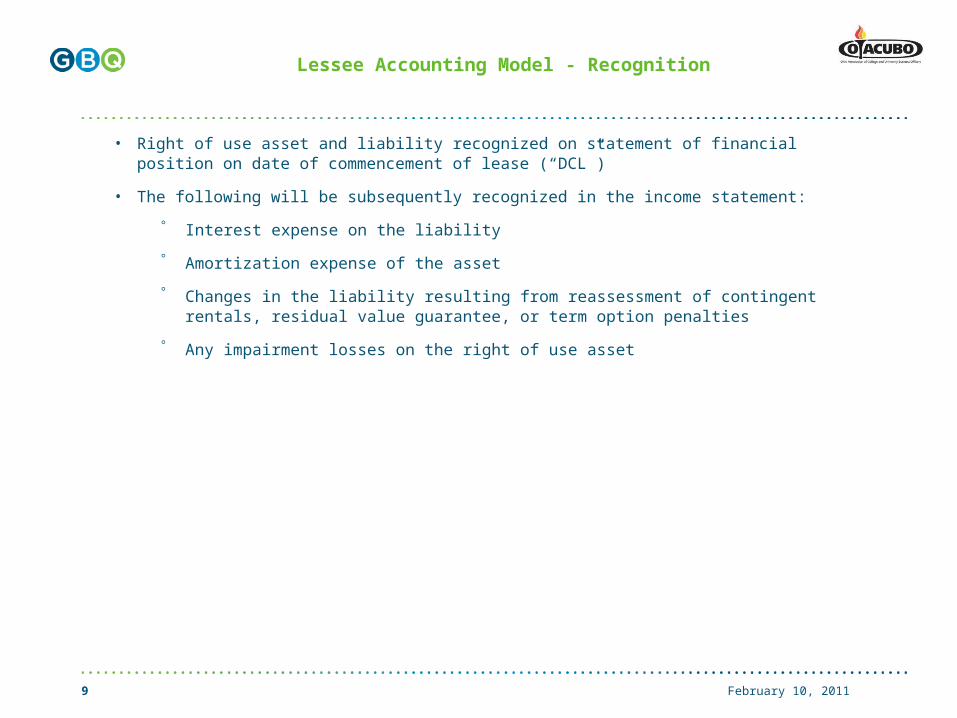

• Right of use asset and liability recognized on statement of financial position on date of commencement of lease (“DCL”)

• The following will be subsequently recognized in the income statement:

Interest expense on the liability

Amortization expense of the asset

Changes in the liability resulting from reassessment of contingent rentals, residual value guarantee, or term option penalties

Any impairment losses on the right of use asset

February 10, 20119

Measurement of Asset and Liability

• Initially done as of date of inception of lease

• Present value of lease payments

Discounted at either:

Lessee’s incremental borrowing rate, or

Rate charged by lessor, if known

• At inception, asset will be the same as the liability plus any initial direct costs, such as:

Commissions

Legal fees

Costs incurred in evaluating lessee, guarantees, and collateral

Closing costs

Note: the following costs are not considered initial direct costs: general overhead expense, advertising or soliciting expense, costs associated with servicing an existing lease.

February 10, 201110

Measurement - Lease Term

• “Longest possible term that is more likely than not to occur”

• Include optional renewal periods that are more likely than not to be exercised

Different than “old’ accounting where optional renewal periods were ignored

• Continually reassessed based on significant changes

Renewal periods and early termination options

Estimates adjusted in period that facts and circumstances change

• Assessment should consider both contractual and non-contractual factors

February 10, 201111

Example - Lease Term

• Non-cancellable 10-year term

• Option to renew for 5 years at the end of 10 years and an option to renew for an additional 5 years at the end of 15 years

• The lessee estimates the probability for each term as follows: 40% for 10-year term, 30% for 15-year term and 30% for 20-year term

• Under these scenarios, the term would be at least 10 years, with a 60% chance that the term would be 15 years or longer, but only a 30% chance that the term would be 20 years. Therefore, there is a 60% chance that the term would be 15 years, which is the longest possible term more likely than not to occur. As such, the lease term would be 15 years.

This example is adapted from Paragraph B17 of the Exposure Draft.

February 10, 201112

Measurement - Lease Payments

• Initially used to measure asset and liability

• “Expected outcome approach”

Present value of the probability-weighted average of the cash flows for a reasonable number of outcomes

Estimating expected outcome involves:

a. Identifying each reasonably possible outcome. An entity need not assess every possible outcome to identify the reasonably possible outcomes included in the expected PV of the cash flows.

b. Estimating the amount and timing of the cash flows for each reasonably possible outcome

c. Determining the present value of those cash flows

d. Estimating the probability of each outcome

• Include contingent amounts

• Continually reassess

February 10, 201113

Expected Outcome Approach – Contingent Rents Example

The Facts: A retailer enters into a 5 year lease which, in addition to fixed monthly payments, calls for contingent rents to be paid at a rate of 1% of annual sales in excess of $1M. Contingent rents are to be paid at the end of each year of the lease. Based on past performance and future projections, management prepares the following analysis related to estimated forecasted sales. The retailer’s incremental borrowing rate is 10%. As a result of the foregoing analysis, the retailer would include contingent rent of $39,221 in its estimate of lease payments. The present value of estimated yearly payments is $7,844 ($39,221/5).

Estimated Present ProbabilityEstimated Annual Sales Probability Contingent Rent Value Weighted

< $1.0 million 0% -

-

-

$1.0 M to $1.5 M 25% 25,000 19,611

4,903

$1.5 M to $2.0 M 50% 50,000 39,221

19,611

$2.0 M to $2.5 M 25% 75,000 58,832

14,708

$2.5 M > 0% -

-

-

150,000 117,664

Probability weighted outcome 39,222

February 10, 201114

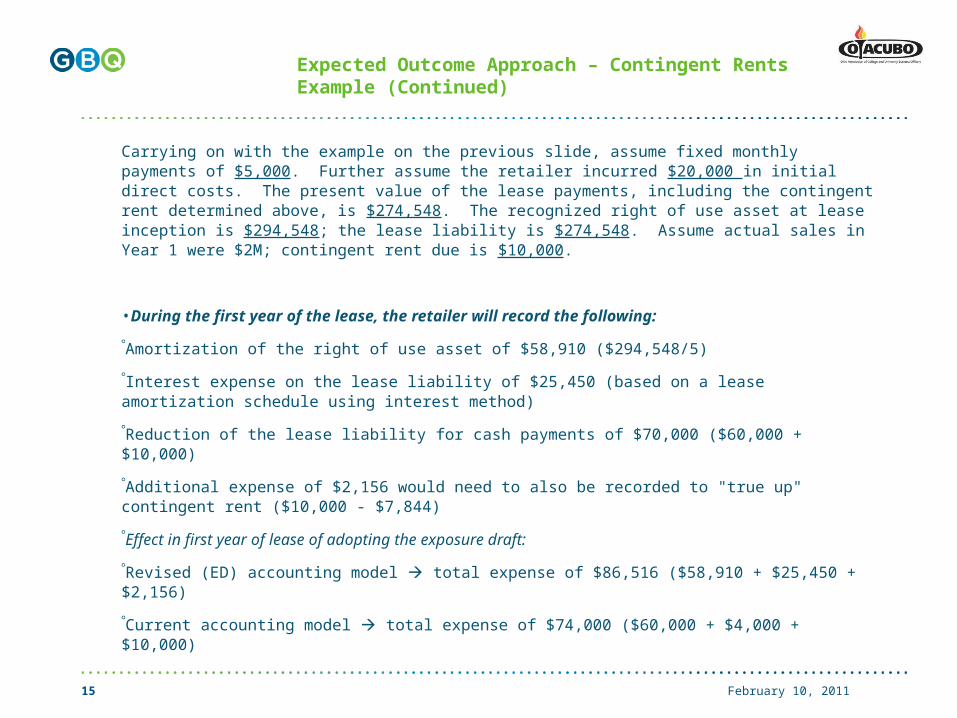

Expected Outcome Approach – Contingent Rents Example (Continued)

Carrying on with the example on the previous slide, assume fixed monthly payments of $5,000. Further assume the retailer incurred $20,000 in initial direct costs. The present value of the lease payments, including the contingent rent determined above, is $274,548. The recognized right of use asset at lease inception is $294,548; the lease liability is $274,548. Assume actual sales in Year 1 were $2M; contingent rent due is $10,000.

•During the first year of the lease, the retailer will record the following:

Amortization of the right of use asset of $58,910 ($294,548/5)

Interest expense on the lease liability of $25,450 (based on a lease amortization schedule using interest method)

Reduction of the lease liability for cash payments of $70,000 ($60,000 + $10,000)

Additional expense of $2,156 would need to also be recorded to "true up" contingent rent ($10,000 - $7,844)

Effect in first year of lease of adopting the exposure draft:

Revised (ED) accounting model total expense of $86,516 ($58,910 + $25,450 + $2,156)

Current accounting model total expense of $74,000 ($60,000 + $4,000 + $10,000)

February 10, 201115

Subsequent Measurement

• Right of Use Asset:

Amortized on a systematic basis over the shorter of the lease term or useful life of the underlying asset

Subject to impairment analysis under ASC 350

• Liability:

Amortized cost using the using the interest method

Subject to periodic reassessments “…if facts or circumstances indicate that there would be a significant change”

Discount rate is not reassessed unless specifically based on an index

February 10, 201116

Presentation

• Right of use asset:

Presented as a tangible asset within PP&E

Segregated from non-leased assets

• Liability:

Separately from other financial liabilities

• Interest and amortization expense presented separately from other interest/amortization expense (either on P&L or in the footnotes)

• Principal and interest cash payments will be a financing activity in the Statement of Cash Flows

February 10, 201117

Recognition/Presentation – Financial Statement Impact

• Income Statement

Current GAAP

Rent expense classification

Included in Operating Income/Loss

Proposed GAAP

Interest and amortization expense classification; no rent expense

Amortization expense included in Operating Income/Loss; Interest excluded

• Statement of Financial Position

The addition of lease liability on the balance sheet may impact debt ratios and possibly covenant calculations

Note: Change in classification may impact EBITDA

February 10, 201118

Lessor Accounting Model - Recognition

• Dual model approach

Performance obligation or

Derecognition

• Centers on whether significant risks or benefits of the leased asset are retained

Exposure to risk/benefits can occur during and after the lease term

If retained = performance obligation model

If transferred = derecognition

• Model determined at Date of Inception and not reassessed

• Both models require estimates of lease term and contingent rentals

February 10, 201119

Recognition – Performance Obligation Approach

• Underlying asset stays on the lessor’s books

• As of date of commencement of the lease, lessor will recognize:

Asset for the right to receive lease payments

Liability at the present value of the lease payments

• Subsequently, lessor will recognize:

Interest income on right to receive lease payments

Lease income as lease liability is satisfied

Changes in lease liability resulting from reassessment of contingent rentals, residual value guarantee or term option penalties

Potential for impairment losses on right to receive lease payments

February 10, 201120

Measurement – Performance Obligation Approach

• Lease liability measured as the sum of the PV of lease payments, discounted using the rate lessor charges the lessee

• Right to receive asset measured as the sum of lease liability and any initial direct costs

Initial measurement based on longest possible lease term that is more likely than not to occur

Measured at date of inception of the lease

Expected outcome approach

PV of the probability-weighted average of the cash flows for a reasonable number of outcomes

Asymmetrical amounts for lessor/lessee are probable

February 10, 201121

Subsequent Measurement – Performance Obligation Approach

• Right to receive asset is carried at amortized cost using the interest method

Subject to impairment testing under ASC 310-10 (loan impairment)

• Remaining lease liability measured based on pattern of use of the underlying asset by the lessee, if pattern can be reliably determined using either inputs or outputs

If not reliably determinable, use straight-line method

• Underlying asset is depreciated over its expected useful life

Systematic and rational approach

If none based on pattern of use, straight-line method should be used

Asset subject to ASC 360 impairment testing (long lived assets impairment)

22

Recognition - Derecognition Approach

• Apply if performance obligation criteria not met

• As of date of commencement of lease, lessor will:

Recognize a receivable for the right to receive rental payments with the offset to lease income

Remove portion of the carrying amount of underlying leased asset from books which represents the lessee’s right to use the asset during the lease term

Residual asset for the portion of the carrying amount of the leased asset that represents the lessor’s non-transferred rights in that asset

Portion of the carrying value of leased asset removed from balance sheet and recorded as cost of sale

February 10, 201123

Recognition - Derecognition Approach

Recognized in the income statement:

• Lease income = PV of lease payments

• Lease expense = cost of underlying asset derecognized

• Interest income on right to return asset

• Lease impact of any reassessments in right to return asset due to change in estimates of contingent amounts

• Impairment losses on right to return asset

If lessor’s ongoing, major, or central activities involve leasing activities, lease income is reported as revenue and lease expense as cost of revenue

February 10, 201124

Measurement - Derecognition Approach

Allocation:

• Amount to be derecognized computed as:

(FV of right to receive lease payments/FV of the underlying leased asset) X Carrying amount of the underlying leased asset

Residual asset is computed as the remaining amount of the carrying amount of the underlying leased asset

• Reassess when facts and circumstances indicate that there could be a significant change

February 10, 201125

Subsequent Measurement - Derecognition Approach

• Right to receive asset at amortized using interest method

• No remeasurement of residual asset unless:

Terms change

Asset is impaired

• ASC 310 used to assess impairment of right to receive asset

• ASC 350 or 360 used to assess impairment of residual asset

February 10, 201126

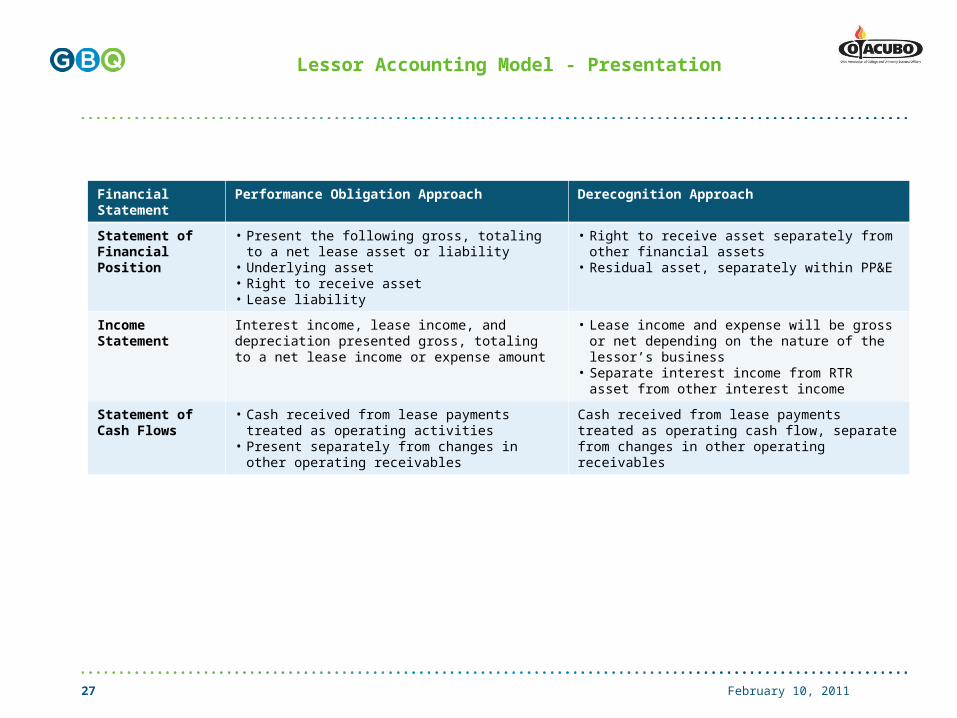

Lessor Accounting Model - Presentation

Financial Statement

Performance Obligation Approach Derecognition Approach

Statement of Financial Position

• Present the following gross, totaling to a net lease asset or liability

• Underlying asset• Right to receive asset• Lease liability

• Right to receive asset separately from other financial assets

• Residual asset, separately within PP&E

Income Statement

Interest income, lease income, and depreciation presented gross, totaling to a net lease income or expense amount

• Lease income and expense will be gross or net depending on the nature of the lessor’s business

• Separate interest income from RTR asset from other interest income

Statement of Cash Flows

• Cash received from lease payments treated as operating activities

• Present separately from changes in other operating receivables

Cash received from lease payments treated as operating cash flow, separate from changes in other operating receivables

February 10, 201127

Disclosure – Lessors and Lessees

• Quantitative and qualitative information relative to lease arrangements

• User should be able to understand amount and timing of expected cash flows; disaggregation of information to the appropriate level

• Significant NEW disclosure requirements:

Reconciliation of opening and closing balances of right-of-use assets and liabilities to make lease payments, disaggregated by class of underlying asset

Narrative disclosure about the options that were recognized as part of the right-of-use asset and those that were not

Assumptions and judgments relating to amortization methods and changes to those assumptions and judgments

Initial direct costs incurred during the reporting period and included in the measurement of the right-of-use asset or right to receive lease payments

Basis and terms on which contingent rentals are determined

February 10, 201128

Income Tax Considerations

• New model will create temporary differences

Assets/liabilities created for book purposes not reflected for tax purposes

ASC 740 requires gross basis recognition – no offsetting of deferred tax asset and deferred tax liability arising from lease items

• State and local taxes may be impacted

February 10, 201129

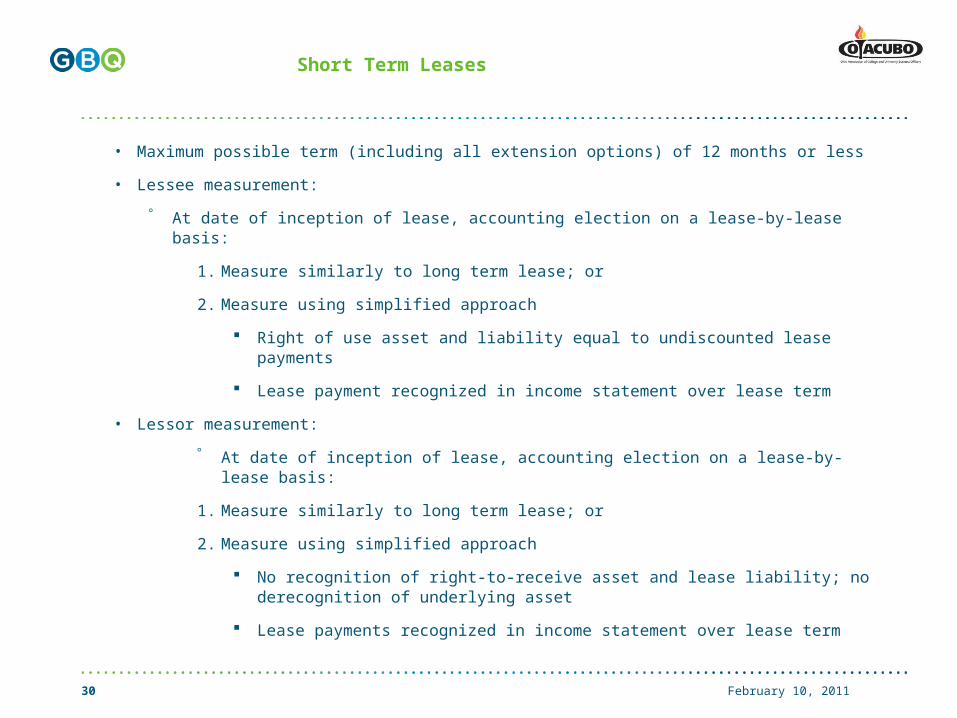

Short Term Leases

• Maximum possible term (including all extension options) of 12 months or less

• Lessee measurement:

At date of inception of lease, accounting election on a lease-by-lease basis:

1. Measure similarly to long term lease; or

2. Measure using simplified approach

Right of use asset and liability equal to undiscounted lease payments

Lease payment recognized in income statement over lease term

• Lessor measurement:

At date of inception of lease, accounting election on a lease-by-lease basis:

1. Measure similarly to long term lease; or

2. Measure using simplified approach

No recognition of right-to-receive asset and lease liability; no derecognition of underlying asset

Lease payments recognized in income statement over lease term

February 10, 201130

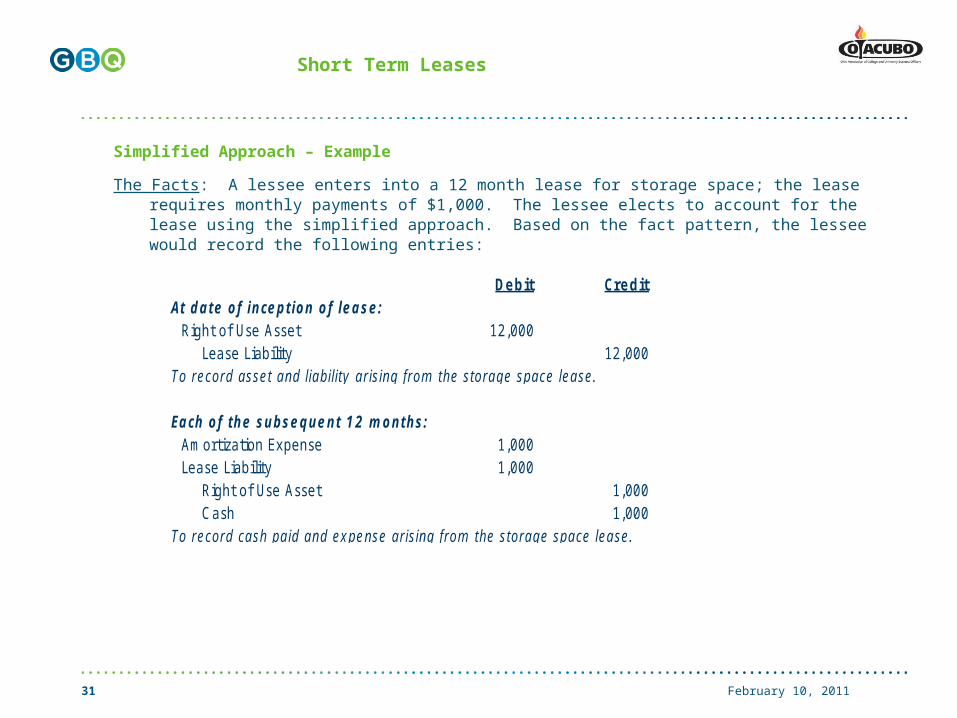

Short Term Leases

Simplified Approach – Example

The Facts: A lessee enters into a 12 month lease for storage space; the lease requires monthly payments of $1,000. The lessee elects to account for the lease using the simplified approach. Based on the fact pattern, the lessee would record the following entries:

Debit CreditAt date of inception of lease:

Right of Use Asset 12,000Lease Liability 12,000

Each of the subsequent 12 months:Amortization Expense 1,000Lease Liability 1,000

Right of Use Asset 1,000Cash 1,000

To record asset and liability arising from the storage space lease.

To record cash paid and expense arising from the storage space lease.

February 10, 201131

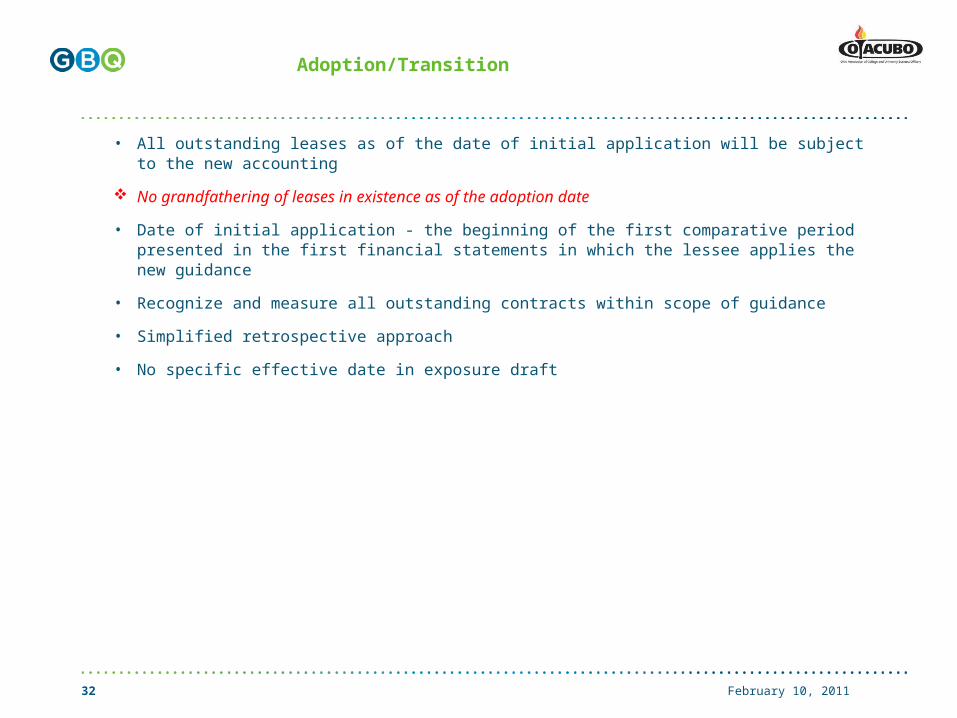

Adoption/Transition

• All outstanding leases as of the date of initial application will be subject to the new accounting

No grandfathering of leases in existence as of the adoption date

• Date of initial application - the beginning of the first comparative period presented in the first financial statements in which the lessee applies the new guidance

• Recognize and measure all outstanding contracts within scope of guidance

• Simplified retrospective approach

• No specific effective date in exposure draft

February 10, 201132

Sale and Leaseback Transactions

Scope

If an asset is transferred and leased back, transaction to be accounted for under the proposed ASU if the contracts are:

• Entered into at or near the same time

• Negotiated as a package with a single commercial objective

• Performed either concurrently or consecutively

Sale Criteria - at end of contract, seller-lessee transfers control and all but a trivial amount of risks/benefits

February 10, 201133

Sale and Leaseback Transactions

Seller-Lessee

• If sale criteria are met:

Record sale pursuant to other GAAP

Record lease asset and obligation pursuant to lease standard

Buyer-Lessor

• If purchase criteria are met:

Account for purchase pursuant to other GAAP

Account for lease using the performance obligation approach

February 10, 201134

Questions?

February 10, 201135

Thank you!

Related Documents