Property under IFRS A guide to the effects of the new International Financial Reporting Standards

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Property under IFRSA guide to the effects of the new International Financial Reporting Standards

Contents

Introduction Property called to account – under new rules 01

Section 1 Main features of the new accounting regime 02

The fair value revolution 02

Owner-occupied properties and investment properties 03

Dealing with the results of revaluations 03

Vital distinctions in accounting for leases 04

Quick guide to the key points of IFRS 05

Accounting for profits on disposal 06

Extensive disclosures – and more transparency 06

Section 2 Valuations and the property professional’s role under IFRS 07

Valuation basis for owner-occupied properties 07

Who can undertake valuations? 07

Operating or finance lease – the vital distinction 08

How frequently must companies revalue? 10

The role of the property professional 10

Leasehold investment properties – the new treatment 12

Section 3 How IFRS affects published figures and financial ratios 14

Repercussions of choosing cost or fair value 14

The effect of switching from cost to fair value 15

Takeover accounting 16

Tax and revaluation surpluses 16

Investment companies – volatile earnings 16

Lease lengths 18

Leasehold accounting 18

Author: Michael Brett

© Copyright 2004 The Royal Institution of Chartered Surveyors (RICS). All rights reserved. No

part of this publication may be reproduced, stored electronically or transmitted in any form,

electrical, mechanical, photocopied, recorded or otherwise without prior permission from RICS.

£20 (RICS members £10)

ISBN: 1842192051

Section 4 How different countries are affected by IFRS 19

Australia: revaluations already accepted 19

Czech Republic: big changes required in accounting for leases 19

France: no previous requirement to update valuations 19

Germany: domestic standards do not allow revaluation 19

Poland: less strict than IFRS on finance leases 20

Spain: fair values come as a culture shock 20

United Kingdom: use of fair values already allowed or required 21

United States: some convergence with IFRS but a fair way to go 21

Appendix A Disclosures required under IFRS 22

Appendix B Accounting treatment by class of property 24

Owner-occupied properties 24

If fair value model is used 25

Properties occupied by a business under a lease 25

Operating leases in the accounts of the lessee 25

Finance leases in the accounts of the lessee 25

Investment properties in the investor’s accounts 26

Cost model 26

Fair value model 26

Leasehold properties accounted for as investment properties 26

Properties in the accounts of the lessor 27

Lessor who grants operating lease 27

Lessor who grants finance lease 27

Sale and leaseback transactions 27

IFRS… could significantly affectthe way that companies that ownor occupy property are perceived‘

’

All who have dealings with property – companydirectors, lawyers, accountants and investorsamong them – will need to appreciate therepercussions of the new rules. In many casesthese international standards – InternationalFinancial Reporting Standards or IFRS (see below)– could radically change the figures thatcompanies publish for net assets, earnings andreturn on capital. The changes are therefore farmore than an accounting technicality. They couldsignificantly affect the way that companies thatown or occupy property are perceived.

Properly qualified property professionals, such as RICS members, have an important part to playin helping to advise landlords, tenants and owner-occupiers on the impact of IFRS. They will beneeded for valuations of commercial property.They will also be needed to help landlords, tenantsand owner-occupiers to resolve the numerousproperty related issues that the new rules throwup. And their knowledge of the property scene willbe essential in advising on the changes toproperty strategies that IFRS may require.

This publication provides a simple guide to the new accounting regime and its likelyrepercussions.

Under International Financial Reporting Standards,as they apply to long term property assets:

• Properties may be carried in the accounts atrevalued amounts or at depreciated cost

• There is a rigid distinction between owner-occupied properties and investment properties,and different accounting standards apply

• Leasehold properties that qualify as investmentproperties must be accounted for as financeleases

• Revaluation surpluses and shortfalls oninvestment properties will go through theincome statement

• Properties acquired via a takeover of anothercompany must normally be taken in initially atcurrent values

• Deferred tax must be provided on revaluation surpluses.

In many cases the new rules will differsignificantly from the domestic accountingstandards that they supplant. In particular, theoption of carrying both owner-occupied andinvestment properties at ‘fair values’ (currentvaluations) represents a radical departure fromtraditional historical cost accounting.

The most important aspects of the internationalaccounting regime, as they apply to property, areexamined in the following pages and on page 5we provide a checklist of the key points.

For those who need greater detail, a summary ofthe new rules is provided in Appendix ‘B’, brokendown according to the impact on owner-occupiers,tenants and investors while Appendix ‘A’ focuseson the extensive IFRS disclosure requirements.

In pages 7-13 we examine the implications forvaluations and the property professional’s services.The repercussions on companies’ published figuresand on different countries’ accounting practice areaddressed on pages 19-21.

Examples are provided to illustrate the keyimpacts of the new rules on companies’ publishedfigures and financial ratios.

1

Property called to account – under new rules

With the adoption of international accounting standards,compulsory from 2005 for companies listed on a EuropeanUnion stock exchange, come important changes in the waythat properties are presented in company accounts.

Introduction

But the effect of International Financial Reporting Standards will be much wider than this. Many countries outside the European Unionare voluntarily adopting the internationalstandards in place of their earlier domestic rules.Other countries are adapting their domesticstandards to bring them closer in line with theinternational pattern.

The effect will be that comparison of companies across national boundaries becomes a great deal easier.

International accounting standards lay down theground rules under which financial statementsmust be prepared. They are published by theInternational Accounting Standards Board (IASB),with its headquarters in London but a globalmembership. The individual standards are knowneither as International Accounting Standards(IASs) or International Financial ReportingStandards (IFRSs). The difference is only in name,with IFRS being used for the latest offerings. Inthis publication we use the term ‘InternationalFinancial Reporting Standards’ or ‘IFRS’ to describethe new accounting regime as a whole.

While many different standards impinge on thepresentation of property in company accounts,three are particularly important. These are:

• IAS 16 – Property, plant and equipment

• IAS 40 – Investment property

• IAS 17 – Leases.

All three were published in revised form at the end of 2003. Together they set out how companiesshould account for their long term propertyassets, whether as owner-occupiers, landlords ortenants. In many cases this will require significantchanges from the way that companies previouslydealt with their properties in published accounts.They also require information disclosures that areconsiderably more extensive than manycompanies are accustomed to.

The fair value revolutionThe most important single innovation ofInternational Financial Reporting Standards is to move a step away from the historical costprinciple under which accounts have traditionallybeen prepared. Companies are now given anoption. They may carry their long-term propertyand other assets at figures based on original cost.Or they may carry them at ‘fair values’: what theyare currently worth. In the second case the figuresfor properties in the accounts will be based on a valuation.

The choice applies both to owner-occupiedproperties and to investment properties, thoughthe detail varies a little between the two classes.But there are two cases where the use of fair valuewill be mandatory. Where one company acquiresanother, the properties of the acquired company –except in the very rare cases where mergeraccounting rules are applied – will need to bebrought into the accounts initially at fair values,not at historical cost figures. And where leaseholdproperties are to be treated as investmentproperties, they must be carried at valuation. In this specific case the historical cost option is not available.

The impact of the change will depend on thecountry concerned and on the individual choicesthat companies make. Under German accountingrules, for example, revaluations have notpreviously been permitted. But in the UKcompanies have long been obliged to carryinvestment properties at valuation rather thancost, while they could choose between the twosystems for owner-occupied properties. We look inmore detail at the impact on different countries inthe section ‘How different countries are affectedby IFRS’.

Where a company decides under the new rules to switch from carrying its properties at cost toshowing them in its accounts at valuation, theimpact on its financial ratios is likely to besignificant. In most cases current values will be farhigher than the out-dated cost-based figures. Weexamine some of the repercussions in the section

Main features of the new accounting regimeThe adoption of International Financial Reporting Standards is intended to harmonise the accountingpractices of listed companies across the European Union. For companies listed on a European Union stockexchange, the new rules will replace the various domestic accounting standards under which companieshave previously prepared their accounts.

2

‘How IFRS affects published figures and financialratios’. But the IFRS ‘fair value option’ also hasimplications for other aspects of companyaccounts, including the income statement and the information disclosures required under theIFRS system.

There can be little doubt that the IASB sees thefuture lying with the use of fair values rather than historical cost. Current values convey farmore useful information about a company thanoutdated cost figures. But because so manydomestic accounting standards are wedded to the historical cost principle and do not allowrevaluations, the IASB has had to move a littlecautiously and offer the ‘cost or fair value’ optionat the outset.

Owner-occupied properties and investmentpropertiesThe rigid distinction required under IFRS between the accounting treatment of owner-occupied properties and of investment propertieswill come as a jolt to countries which had notpreviously differentiated their properties in thisway. As noted, in both cases companies may carrythe properties at cost-based or valuation-basedfigures. Owner-occupied properties will need to be depreciated, whether carried at cost orvaluation. In the case of investment properties,depreciation must be provided when they arecarried at cost, but investment properties carriedat valuation are not depreciated.

As we saw, leaseholds that are to be treated asinvestment properties must be carried at valuation.They must also be accounted for as finance leasesunder IAS 17 via a complex procedure that wedescribe in more detail in the box ‘LeaseholdInvestment Properties – the new treatment’. Thiswill come as an innovation in most countries andmay cause some initial confusion among preparersand users of accounts. However, owner-occupiedleasehold properties will be accounted for in asimpler way under the rules of IAS 17. In other

words they will be accounted for by the lessee asoperating leases or finance leases, depending onthe classification into which they fall.

The distinction between owner-occupiedproperties and investment properties is veryimportant when it comes to the accountingtreatment of valuation surpluses and shortfalls.

Dealing with the results of revaluationsRevaluation surpluses and shortfalls receivedifferent treatment, depending on whether theproperties concerned qualify as owner-occupied or as investments. Shortfalls on owner-occupiedproperty will be charged to income except to theextent that they reverse a previous surplus on thatproperty. In most cases revaluation surpluses onowner-occupied properties that are carried atvaluation will go to reserves without impinging on the income statement. There are certainexceptions to this rule where a new valuationreverses the effect of a previous shortfall that hadbeen charged to income statement.

The position with investment properties is verydifferent. In this case all revaluation surpluses and shortfalls are taken through the incomestatement. Thus, they impinge directly on thepublished earnings figures, which could becomevery volatile as a result. This will come as a shockto companies that are used to taking thesesurpluses and shortfalls to reserves, withoutaffecting the income statement.

The IFRS regime also requires, under standard IAS 12, that companies should provide fordeferred tax on all revaluation surpluses, whetheron owner-occupied or investment properties. This will be revolutionary in countries such as theUnited Kingdom where deferred tax was notnormally provided if there was no intention ofselling the properties concerned. The change willclearly have a significant effect on published netasset figures for some companies that carry theirproperties at valuation.

3

…with investment properties…all revaluation surpluses andshortfalls are taken through theincome statement…‘

’

Vital distinctions in accounting for leasesThe IFRS regime is strict in differentiating between operating leases and finance leases.Broadly, a finance lease is one that transferssubstantially all of the risks and rewards ofownership of an asset to the lessee, even thoughhe is not the legal owner. An operating lease is onethat does not meet this criterion. Traditionally,most leases of land and property have beentreated as operating leases.

An operating lease does not appear on thebalance sheet of the lessee. All he shows in hisaccounts is the annual rental that he is due to pay. However, there are additional disclosuresthat he must make (see below).

On the other hand, under IFRS a finance leaseis capitalised on the balance sheet of the lessee. Inother words, the lessee has to show the leasedasset on his balance sheet much as if he were the legal owner and provide depreciation as hedoes for his own assets. On the other side of thebalance sheet he shows as a correspondingliability the present value of the lease paymentsthat he is committed to make over the term of the lease.

The accounting for leases, both by lessors and by lessees, therefore depends on the leaseclassification. This is an area of some debateamong accountants and surveyors. To assist withclassification, under IFRS a lessee may examine a lease according to its two constituent elements:a lease of land and a lease of the buildings thatstand on it (though this is not necessary in thecase of a leasehold treated as an investmentproperty, which will be accounted for as a financelease anyway).

A lease of land will normally classify as anoperating lease since the risks and rewards ofland ownership normally remain with the lessor

and the land reverts to him at the end of the lease. The lease of the buildings may sometimes bemore problematical. Though the buildings mayultimately revert to the lessor, what is thesituation if the lease covers the remaining usefullife of the buildings? Would the lease of thebuildings therefore qualify as a finance lease?

Surveyors as well as accountants may findthemselves called in to advise on such situationsunder the IFRS regime. The robust view is thatmost property leases will be immediatelyrecognisable as operating leases. In cases wherethere is doubt, it should be possible to arrive at ananswer by applying qualitative tests rather thanby attempting an arithmetic solution based onanalysis of the two separate elements of the lease.In the UK a working party of the British PropertyFederation has suggested a series ofcommonsense tests aimed at distinguishingbetween operating leases and finance leases.

Classification of leases and of properties underIFRS is important not only for the figures thatwill appear in the main financial statements. Italso has important implications for the additionalinformation that companies must disclose.

Many countries outside theEuropean Union are voluntarilyadopting the internationalstandards…‘

’

4

5

Quick guide to the key points of IFRS

• Distinction between owner-occupied and investment property and differentaccounting treatment for the two

• Option of carrying properties at cost or at fair value (valuation)

• Fair value for investment property is normally market value

• Fair value for owner-occupied property is not closely defined

• If investment properties are carried at cost, fair values must be disclosed

• If owner-occupied properties are carried at cost, disclosure of fair values is encouraged

• Where properties are carried at fair value, valuations must be kept up to date

• Companies must disclose whether valuations were carried out by an independent, professionally qualified valuer

• For owner-occupied properties carried at cost or at valuation and for investmentproperties carried at cost, depreciation must be provided

• Different classes of assets must be depreciated separately

• Owner-occupied property charged as security must be disclosed

• Revaluation gains and losses on investment property go through the income statement, resulting in volatile earnings

• Revaluation gains and losses on owner-occupied properties may sometimes impact onthe income statement

• Deferred tax must be provided on revaluation surpluses

• Properties acquired via a takeover must be recognised initially at fair values

• Strict distinction between operating and finance leases

• Some leases need to be viewed in two parts – a lease of land and a lease of the buildingon it – to assist in lease classification

• Granting of a finance lease constitutes a disposal by the lessor

• Finance leases must be capitalised in lessee’s accounts

• Leaseholds classified as investment properties must be accounted for as finance leasesin the investor’s accounts, involving considerable accounting contortions.

• Both lessors and lessees must provide a description of their material leasing arrangements

• Lessees with operating leases or finance leases must disclose and break down the total lease payments to which they are committed for the term of the lease

• Special rules apply to accounting for profits or losses on sale and leaseback transactions.

Accounting for profits on disposalProfits and losses on disposal of properties arecalculated under IFRS as the difference betweenthe carrying amount and the sale price. Recordedsale profits are therefore likely to be larger ifproperties are carried at outdated cost figuresrather than current values. If the proceeds aredeferred or received in instalments, under IFRS theselling price is taken as the cash price equivalent.Profits and losses on disposal will go through theincome statement. Note also that granting of afinance lease counts as a disposal under IFRS.

Where a property is disposed of via a sale andleaseback transaction, special conditions mayapply. If the transaction is at full market value andthe leaseback element results in an operatinglease, profit is calculated in the normal way. Butthere are complex rules for calculating and dealingwith any profit or loss where a sale at a figureother than market value is balanced by specialconditions on the leaseback side of thetransaction or where the leaseback results in afinance lease (see ‘Sale and leasebacktransactions’ in Appendix B for more detail).

Extensive disclosures – and more transparencyUnder IFRS companies will be required to giveconsiderably more detail on their propertyarrangements than many are accustomed to. Themost important single point is that companieswith investment properties cannot avoid the needfor valuations. Even if they decide to carry theproperties in their accounts at depreciated cost,they will be required to provide fair values asadditional information. Companies with owner-occupied properties carried in the books atdepreciated cost are ‘encouraged’ though notrequired to provide fair values as well.

There are also disclosure requirements relating toleases which will give a clearer picture of acompany’s property commitments. Tenants whooccupy properties under finance leases will, ofcourse, need to show as a liability on the balancesheet the present value of the lease payments towhich they are committed. Though the tenantthat occupies properties under an operating leasedoes not show an asset or liability on the balancesheet, he will still be required to disclose asadditional information the lease payments towhich he is committed over the non-cancellableterm of the lease.

Companies are also required to provide a general description of their leasing arrangementsas well as a considerable amount of other detail.See Appendix A for further information.

We have talked so far of ‘fair values’ and‘valuations’ without examining the specifics. These can be important and we look at therequirements for valuations and valuers in thenext section.

Current values convey far moreuseful information about a companythan outdated cost figures‘

’

6

Though accountants talk of carrying properties at ‘fair values’, it is not a term that valuers oftenuse. They will tend to talk of carrying properties ‘at valuation’ or at ‘market value’ or some otherspecific basis of valuation. Do these terms alwaysmean the same thing?

Not quite, under IFRS. With investment propertiesthere is normally no problem. ‘Fair value’ in this case would mean ‘market value’ – theinternationally-accepted valuation basis. Marketvalue is defined by the International ValuationStandards Committee (IVSC) and adopted into thedomestic valuation standards of many countries. In Britain RICS adopts the IVSC definition of marketvalue in the latest edition of its Appraisal andValuation Standards: its ‘Red Book’.

Market value will normally be based on marketevidence of transactions in similar properties.Where no active market exists, this may requireextrapolation from such market evidence as isavailable, or use of discounted cash flowprojections. In cases where market value cannotbe established by any of these methods, theinvestment property would be carried at cost.

Valuation basis for owner-occupied propertiesThe valuation basis for owner-occupied propertiesis less clear cut. Standard IAS 16 states that ‘thefair value of land and buildings is usuallydetermined from market based evidence byappraisal that is normally undertaken byprofessionally qualified valuers’. This leaves openthe question of whether the valuation basisshould be market value or a market-derived basissuch as ‘existing use value’ (EUV) which takesaccount of the value of the property only for itsexisting use. Whereas market value will allow forthe possibility of an alternative use for theproperty, valuation bases such as EUV exclude thisfactor. They assume that the property owner is anongoing business and needs the property for itsoperations. Possible alternative uses are nottherefore relevant for accounting purposes.

In many cases market value and EUV or some close equivalent would throw up the sameresult. Where they do not, the difference could be significant.

Some countries such as the United Kingdom have traditionally used EUV for owner-occupiedproperties. Others have used simple market value.

Who can undertake valuations?Neither the standard for investment propertiesnor that for owner-occupied properties specificallyinsists on the use of independent professionallyqualified valuers where properties are carried atvaluation. But use of a qualified professional isclearly preferred practice.

In the case of investment properties, companiesare encouraged to use a valuation ‘by anindependent valuer who holds a recognised andrelevant professional qualification and has recentexperience in the location and category of theinvestment property being valued’.

The standard for owner-occupied propertiesstates that ‘the fair value of land and buildings isusually determined from market-based evidenceby appraisal that is normally undertaken byprofessionally qualified valuers’.

In the case of both classes of property a companymust disclose whether it has used an independentprofessionally qualified valuer. And a considerableamount of detail is required on valuationmethodology – in particular, the extent to whichthe valuations were based on recent marketevidence and the main assumptions made.

7

Valuations and the property professional’s role under IFRSThe option of carrying properties at ‘fair values’ is the biggest single innovation of IFRS, but it also carriesconditions. Where a company decides to carry its properties at ‘fair values’, it must carry all properties ofthe same class at fair values. Thus, if some owner-occupied properties are carried at fair values, all owner-occupied properties must be carried at fair values. And valuations must be kept up to date.

Section 2

Operating or finance lease – the vital distinction

A finance lease is one where the lessee accepts substantially all the risks and rewards thatgo with the leased asset, though he is not the legal owner. He may have the right to acquirethe leased asset for a relatively modest sum at the end of the lease term. He thus treats theleased asset in his own accounts much as if he were the legal owner. He shows it as anasset, along with his owned assets, and depreciates it through his income statement in thesame way. Likewise, he has to show in his balance sheet a corresponding liability, much as ifhe had borrowed money to buy the leased asset. This liability is the present value of therental payments the lessee is committed to make over the life of the lease.

Standard IAS 17 considers that a property lease consists of two elements: a lease of landand a lease of the buildings that stand on it. Except in the case of a leasehold investmentproperty accounted for as a finance lease, the two elements may need to be consideredseparately to determine whether a lease is an operating lease or a finance lease.

IAS 17 also lists a number of examples that might indicate a finance lease. For instance, ifthe leased property is of such a specialised nature that only the lessee could use it withoutmajor modification. One other example that might cause problems for surveyors is wherethe lease term is for ‘the major part of the economic life of the asset’. While land normallyhas an indefinite life, the building that stands on it might be obsolete by the end of thelease term.

An operating lease is, basically, one which does not fit the definition of a finance lease.Most of the risks and rewards remain with the lessor, to whom the asset reverts at the end of the lease. The lessor may also remain responsible for servicing and maintaining theasset as with, for example, a typical lease of a photocopying machine. With an operatinglease the lessee does not show the asset – or any corresponding liability – in his balancesheet. He simply accounts, through his income statement each year, for the rent that he has to pay.

Most property leases have traditionally been accounted for as operating leases – they will not appear on the lessee’s balance sheet. The lessee does not normally take on the full risks and rewards of ownership, which remain with the lessor. And the property willnormally revert to the lessor at the end of the lease term. The main exception in the pasthas been certain types of lease which are more of a financing arrangement than a typicalproperty lease and have therefore been accounted for as finance leases. Under IFRS theclassification may require rather more thought.

As the example opposite shows, it makes a big difference whether a business is deemed to occupy its premises under an operating lease or a finance lease.

8

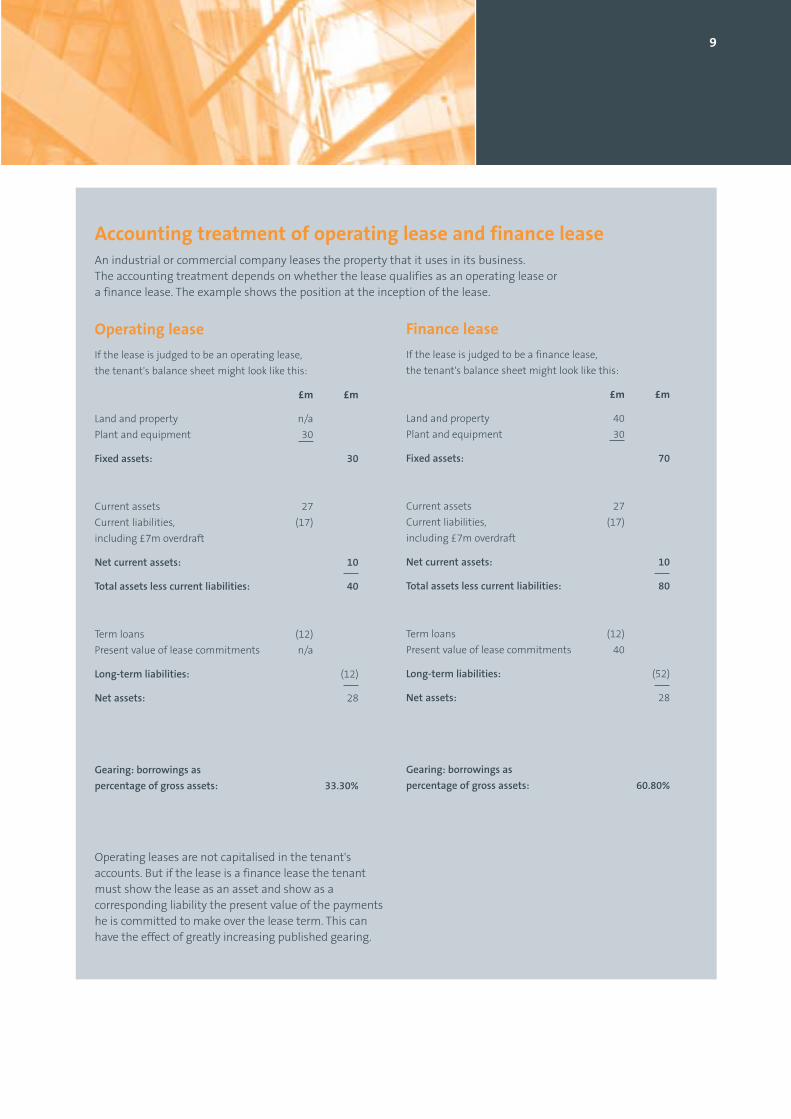

9

Accounting treatment of operating lease and finance leaseAn industrial or commercial company leases the property that it uses in its business. The accounting treatment depends on whether the lease qualifies as an operating lease or a finance lease. The example shows the position at the inception of the lease.

Finance lease

If the lease is judged to be a finance lease,

the tenant's balance sheet might look like this:

£m £m

Land and property 40

Plant and equipment 30

Fixed assets: 70

Current assets 27

Current liabilities, (17)

including £7m overdraft

Net current assets: 10

Total assets less current liabilities: 80

Term loans (12)

Present value of lease commitments 40

Long-term liabilities: (52)

Net assets: 28

Gearing: borrowings as

percentage of gross assets: 60.80%

Operating lease

If the lease is judged to be an operating lease,

the tenant's balance sheet might look like this:

£m £m

Land and property n/a

Plant and equipment 30

Fixed assets: 30

Current assets 27

Current liabilities, (17)

including £7m overdraft

Net current assets: 10

Total assets less current liabilities: 40

Term loans (12)

Present value of lease commitments n/a

Long-term liabilities: (12)

Net assets: 28

Gearing: borrowings as

percentage of gross assets: 33.30%

Operating leases are not capitalised in the tenant'saccounts. But if the lease is a finance lease the tenantmust show the lease as an asset and show as acorresponding liability the present value of the paymentshe is committed to make over the lease term. This canhave the effect of greatly increasing published gearing.

How frequently must companies revalue?If a company decides to carry its properties at fairvalues rather than cost, under IFRS valuations mustbe kept up-to-date. And normally all properties ofthe same class must be valued at the same time,though some element of rolling revaluation isallowed for owner-occupied properties.

The standard IAS 40 for investment propertiesdoes not specifically stipulate the frequency ofvaluation. But since it states that ‘the fair valueof investment property shall reflect marketconditions at the balance sheet date’ thepresumption is that investment properties willneed to be valued annually.

In the case of owner-occupied properties,valuations must be updated sufficiently regularlyto ensure that the figures used in the accounts donot differ materially from values applying at thebalance sheet date. But IAS 16 does not impose a required frequency of valuation. With volatileassets, annual revaluations may be required. Inslower moving markets less frequent valuationsmight be adequate.

The role of the property professionalQualified surveyors, such as RICS members, willfind their expertise in demand in a number ofdifferent areas under the IFRS regime. In additionto valuations, their experience will also be neededto help with other problems that IFRS throws up.

As valuers they will be needed to provide:

• Regular valuation of investment and owner-occupied properties for incorporation incompany accounts where companies carry theirproperties at fair values

• Valuations required for disclosure of fair values, even where properties are carried in the accounts at cost

• Valuation of leaseholds to be accounted for asinvestment properties

• Valuation of properties acquired via takeover,which must be taken in at fair values.

Their expertise will also be needed in some cases in helping to analyse leases between a leaseof land and a lease of buildings. As noted earlier,this analysis may be required under IFRS (except inthe case of leaseholds treated as investmentproperties) to arrive at the vital distinctionbetween operating leases and finance leases. And owner-occupiers will also need to separatethe land and building elements of their propertyholdings in order to calculate depreciationprovisions. Depreciation is normally provided onbuildings but not on the land element.

Accounting for operating leases as well as forfinance leases may require input from the valuerto back up the work of the accountant. In the caseof operating leases, lessees are required to disclosethe total of minimum rental payments to whichthey are committed under the terms of the lease.In the case of finance leases they need to showthe present value of these lease commitments asa liability on balance sheet.

The accounting standards describe thesecommitments (in the case of operating leases) as‘the total of future minimum lease paymentsunder non-cancellable operating leases…’. Butwhat is the term of, say, a 15 year lease with anextension option but also a break clause atyear 10? Standard IAS 17 provides some help bydefining a lease term as ‘the non-cancellableperiod for which the lessee has contracted to leasethe asset’ together with further terms on whichthe lessee has an option that, at the inception ofthe lease, he seems reasonably certain to exercise.

10

But it may require a surveyor’s knowledge ofmarket conditions to predict a tenant’s likelyactions and therefore the likely term of the leaseand the corresponding commitment to pay rent.

The enhanced disclosure required from propertyowners and tenants under IFRS are also likely toimpose additional requirements on propertyprofessionals. They will not always be used toproviding the level of detail that will be required invaluation reports on the methods and significantassumption used in arriving at values. They willneed to show to what extent their valuations werebased on market evidence and to describe anyother methods used. And where a companycannot establish fair value for an individualinvestment property, it is also likely to call on itsvaluer’s expertise. This is because it will have toexplain why the property cannot be valued reliablyand provide, if possible, a range within which fairvalue is likely to lie.

Finally, the property professional may have astrategic role to perform under the newaccounting regime. The option of carryingproperties at valuation is likely to force property-owners to think constructively about the marketvalues of their properties and the capital tied upin them. The enhanced disclosure requirementsfor companies that occupy their properties undera lease may cause them to re-evaluate the relativemerits of owning and leasing. The propertyprofessional has an vital input into any review ofproperty strategies.

11

Qualified surveyors, such as RICSmembers, will find their expertise indemand in a number of differentareas under the IFRS regime‘

’

Leasehold investment properties – the new treatmentAccounting for leasehold investment properties poses challenges under the internationalaccounting regime. This is because they must be accounted for as finance leases in theinvestor’s accounts, according to standard IAS 17 on leases. And this standard was drawn up largely with leases of plant and equipment in mind. Applying it to the rather differentcharacteristics of property leases has required considerable accounting contortions.

In countries with a leasehold tradition, such as the United Kingdom, leasehold investmentproperties have not in the past been treated very differently from freeholds. The valuermakes allowance for the rent that the ‘owner’ of the leasehold must pay to the superiorlandlord and for the fact that the property will ultimately revert to this superior landlord at the end of the lease.

The international accounting standards change all that. The latest versions of IAS 40 oninvestment properties and IAS 17 on leases allow leasehold investment properties toappear in the balance sheet as investment properties. But a very strict and not whollylogical accounting treatment is imposed which means that the treatment of leaseholds and freeholds is very different.

The IFRS rule is that the holder of the leasehold interest in a property (in other words the‘owner’ of the leasehold interest – we refer to him as the ‘investor’ ) may treat it as aninvestment property provided it satisfies other requirements for an investment property.But he may only do so provided he treats the leasehold as if he held it under a finance lease from the superior landlord and provided he carries it at fair value (i.e. at valuation)in his accounts. This is despite the fact that the lease from the superior landlord would infact normally be an operating lease and this landlord would account for it as such in hisown accounts.

What this means in practice is as follows. The leasehold will be valued by a valuer in thenormal way. And on the liabilities side of the investor’s balance sheet will be shown thetotal present value of the rental payments that the investor is committed to make to thesuperior landlord over the term of the lease. But this poses an immediate problem. Thisliability to pay rent to the superior landlord has already been allowed for in the value thatthe valuer put on the leasehold interest in the property. So, to square the circle and avoiddouble-counting of this liability. The present value of rents due under the lease is also added to the valuation figure for the leasehold that appears on the assets side, in order toarrive at the carrying amount.

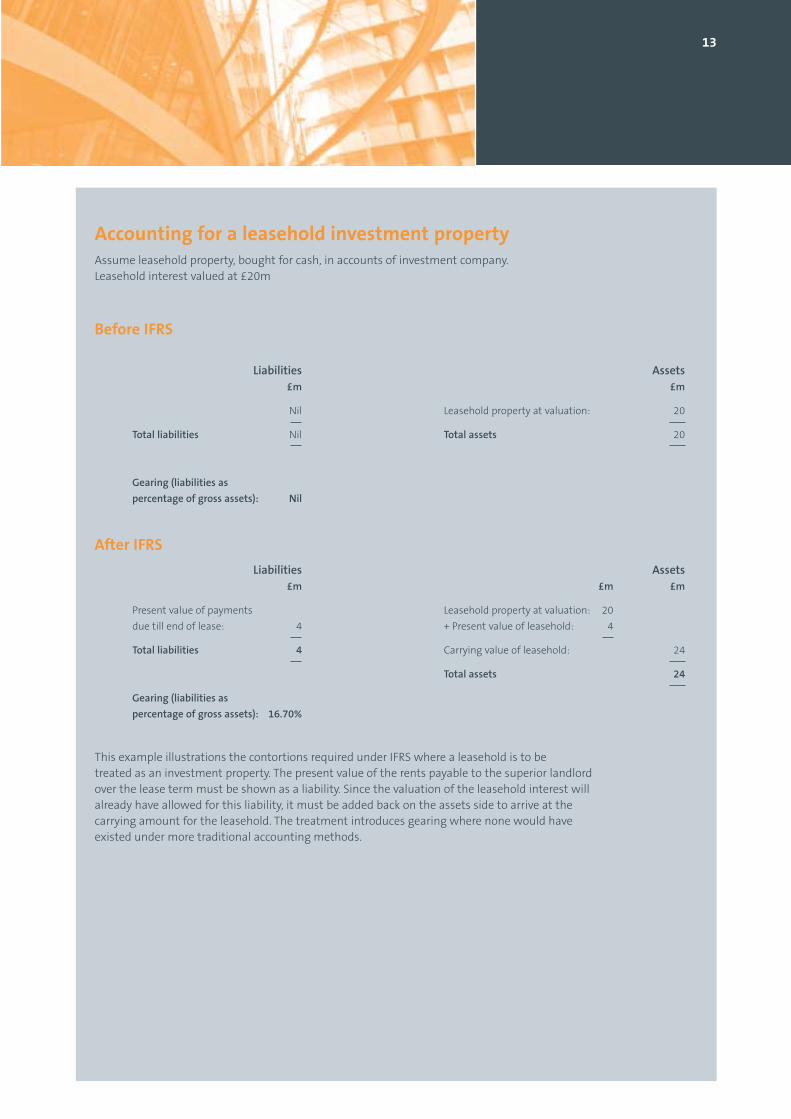

An example may help (see below). A property investment company owns a leaseholdproperty with 52 years to run on the lease, at a fixed ground rent of £250,000. Theleasehold interest is valued at £20m and the present value of the ground rent payable over the life of the lease is £4m at a discount rate of 6%. The company therefore shows aliability of £4m. On the assets side it shows the leasehold property at its valuation of £20m plus the £4m present value of the ground rents, for a total of £24m.

So the carrying value of £24m at which the property appears in the accounts is not thevalue of the leasehold interest but a sort of accounting confection that might correspondmore closely to what the property would be worth if it were a freehold. In the process abalance sheet liability is created where none would have been shown under moretraditional accounting methods, thus introducing financial gearing where none would have existed before.

In contrast to these convolutions, a leasehold property ‘owned’ and occupied by anindustrial or commercial company for its own business is classified as an operating lease or a finance lease in the normal way and accounted for accordingly under IAS 17.

12

13

Accounting for a leasehold investment propertyAssume leasehold property, bought for cash, in accounts of investment company. Leasehold interest valued at £20m

Assets£m

Leasehold property at valuation: 20

Total assets 20

Assets£m £m

Leasehold property at valuation: 20

+ Present value of leasehold: 4

Carrying value of leasehold: 24

Total assets 24

Before IFRS

Liabilities£m

Nil

Total liabilities Nil

Gearing (liabilities as

percentage of gross assets): Nil

After IFRS

Liabilities£m

Present value of payments

due till end of lease: 4

Total liabilities 4

Gearing (liabilities as

percentage of gross assets): 16.70%

This example illustrations the contortions required under IFRS where a leasehold is to be treated as an investment property. The present value of the rents payable to the superior landlordover the lease term must be shown as a liability. Since the valuation of the leasehold interest willalready have allowed for this liability, it must be added back on the assets side to arrive at thecarrying amount for the leasehold. The treatment introduces gearing where none would haveexisted under more traditional accounting methods.

In particular, properties acquired via takeoverwill need to be stated at fair values and deferredtax will have to be provided on revaluationsurpluses. Revaluation surpluses and shortfalls on investment properties will need to go through the income account. Disclosure requirements orrecommendations will deliver information oncurrent values even when properties are carried at cost, and there will be more information oncompanies’ leasing arrangements and leasecommitments. And the IFRS system of accountingfor leasehold investment properties will causesome initial head-scratching.

Repercussions of choosing cost or fair valueThe case for fair values is not difficult to make for investment properties, though propertyinvestment companies will need to educate theirinvestors to expect more volatile earnings figuresin future as valuation surpluses and shortfalls arechanneled through the income statement. TheEuropean Public Real Estate Association (EPRA)– a body representing the public real estate sectorin Europe – strongly recommends the use of fairvalues for investment properties by its members.EPRA has also published best practice guidance inthis area.

Industrial and commercial companies owningproperties that they use in their business may find the choice less clear-cut.

In favour of fair values:• The carrying figures for property assets are

likely to be higher than they would have beenwhen based on cost figures from years ordecades back. This would generally have theeffect of increasing gross assets and wouldtherefore emphasise financial strength

• It would increase the figure for shareholders’ funds and therefore for netassets per share (NAV)

• By decreasing the published financial gearingof the company it would provide a strongerbase for future capital raising.

But there might be negative implications as well:

• Increasing the carrying value of assets wouldincrease the published figure for capitalemployed in the business. This would have the effect of reducing the return on capitalemployed (ROCE) as normally calculated

A company that had appeared to earn adequatereturns with its properties shown at cost mightbe revealed as under-performing once assets wereshown at their true values. This might triggershareholder concern or even a takeover.

• The increase in shareholders’ equity wouldresult in a lower figure for return on equity

• Though a company would not normally providedepreciation on the land element of itsproperties, if a revaluation disclosed that thebuildings themselves had risen in value thecompany might have to increase thedepreciation provided on its owner-occupiedproperties. This could have an adverse effect onpublished profits

• If a future slump in the property market causedthe value of owner-occupied properties to fall,the company’s balance-sheet strength might beperceived to have fallen even though its tradingperformance had not been affected

• Valuation surpluses or shortfalls on owner-occupied properties could in somecircumstances have implications for the incomestatement. A valuation shortfall will normallybe recognised in the income statement, exceptto the extent that it reverses any credit balancein revaluation surplus relating to that particularproperty. While a valuation surplus willnormally go straight to reserves, it will berecognised in the income statement to theextent that it reverses an earlier revaluationshortfall in respect of that property that hadgone through the income statement.Depending on the circumstances, revaluationscan therefore affect published earnings

• Profits or losses on property disposals arecalculated as the difference between thecarrying amount and the sale price and, sincethey go through the income statement, they will affect published earnings. Disposalprofits are likely to be higher if the carryingamount is an outdated cost figure rather thana recent valuation.

How IFRS affects published figures and financial ratiosThe most obvious impact of IFRS on companies’ published accounts and financial ratios will come in thecases where they decide to move from carrying properties at cost to incorporating them at fair values. Buteven without this major switch, IFRS will impose changes on many companies.

14

Section 3

15

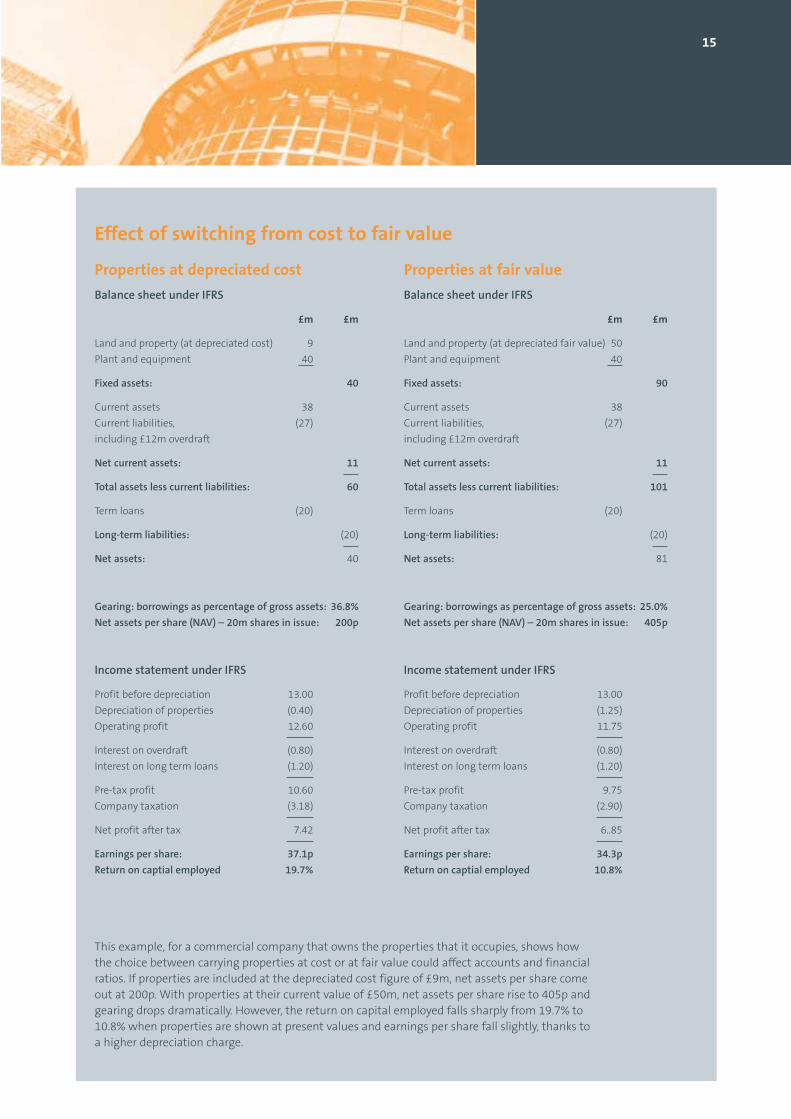

Effect of switching from cost to fair value

Properties at fair value

Balance sheet under IFRS

£m £m

Land and property (at depreciated fair value) 50

Plant and equipment 40

Fixed assets: 90

Current assets 38

Current liabilities, (27)

including £12m overdraft

Net current assets: 11

Total assets less current liabilities: 101

Term loans (20)

Long-term liabilities: (20)

Net assets: 81

Gearing: borrowings as percentage of gross assets: 25.0%

Net assets per share (NAV) – 20m shares in issue: 405p

Income statement under IFRS

Profit before depreciation 13.00

Depreciation of properties (1.25)

Operating profit 11.75

Interest on overdraft (0.80)

Interest on long term loans (1.20)

Pre-tax profit 9.75

Company taxation (2.90)

Net profit after tax 6..85

Earnings per share: 34.3p

Return on captial employed 10.8%

Properties at depreciated cost

Balance sheet under IFRS

£m £m

Land and property (at depreciated cost) 9

Plant and equipment 40

Fixed assets: 40

Current assets 38

Current liabilities, (27)

including £12m overdraft

Net current assets: 11

Total assets less current liabilities: 60

Term loans (20)

Long-term liabilities: (20)

Net assets: 40

Gearing: borrowings as percentage of gross assets: 36.8%

Net assets per share (NAV) – 20m shares in issue: 200p

Income statement under IFRS

Profit before depreciation 13.00

Depreciation of properties (0.40)

Operating profit 12.60

Interest on overdraft (0.80)

Interest on long term loans (1.20)

Pre-tax profit 10.60

Company taxation (3.18)

Net profit after tax 7.42

Earnings per share: 37.1p

Return on captial employed 19.7%

This example, for a commercial company that owns the properties that it occupies, shows how the choice between carrying properties at cost or at fair value could affect accounts and financialratios. If properties are included at the depreciated cost figure of £9m, net assets per share comeout at 200p. With properties at their current value of £50m, net assets per share rise to 405p andgearing drops dramatically. However, the return on capital employed falls sharply from 19.7% to10.8% when properties are shown at present values and earnings per share fall slightly, thanks toa higher depreciation charge.

Prepare for a tougher takeover accounting regimeInternational accounting standards areconsiderably tougher than many domesticstandards on accounting for takeovers. Mosttakeovers will need to be accounted for asacquisitions. Accounting for a businesscombination as a merger of interests is onlypermitted in very limited circumstances.

This has implications for the performance of acompany after a takeover. Under acquisitionaccounting the properties acquired will need tobe taken in at fair values. Returns on assets maytherefore be lower than if properties acquired bytakeover had been included at outdated cost oroutdated valuations.

Tax may dent those revaluation surplusesTreatment of deferred tax has varied a lotbetween different accounting regimes. In somecountries, such as the United Kingdom, companiesdid not normally provide for the tax that would bepayable if they were to sell their properties atrevalued amounts. This was justified by theargument that there was no intention to sell the properties.

International accounting standards requireprovision for deferred tax, even on unrealisedrevaluation surpluses. This provision woulddramatically reduce published asset values insome cases where deferred tax on revaluationshad not previously been provided. The directors ofsuch companies will need to explain the situationvery carefully to their shareholders.

Investment companies must prepare for volatile earningsShareholders in a property investment companyare usually interested quite as much in themovement in the value of the company’s propertyassets over the year as they are in the revenueoutcome for the year. Under IFRS, revaluationsurpluses or shortfalls will go through the incomestatement and published profits are thereforelikely to be a lot more volatile than in the past. On the other hand, by combining revenue andmovements in the value of assets, the incomestatement will give a more comprehensive view of changes in the value of the enterprise over theyear. But shareholders may take some time tofamiliarise themselves with an income statementthat incorporates both realised profits andunrealised revaluation gains.

…investment companies willneed to educate their investorsto expect more volatile earningsfigures in future‘

’

16

17

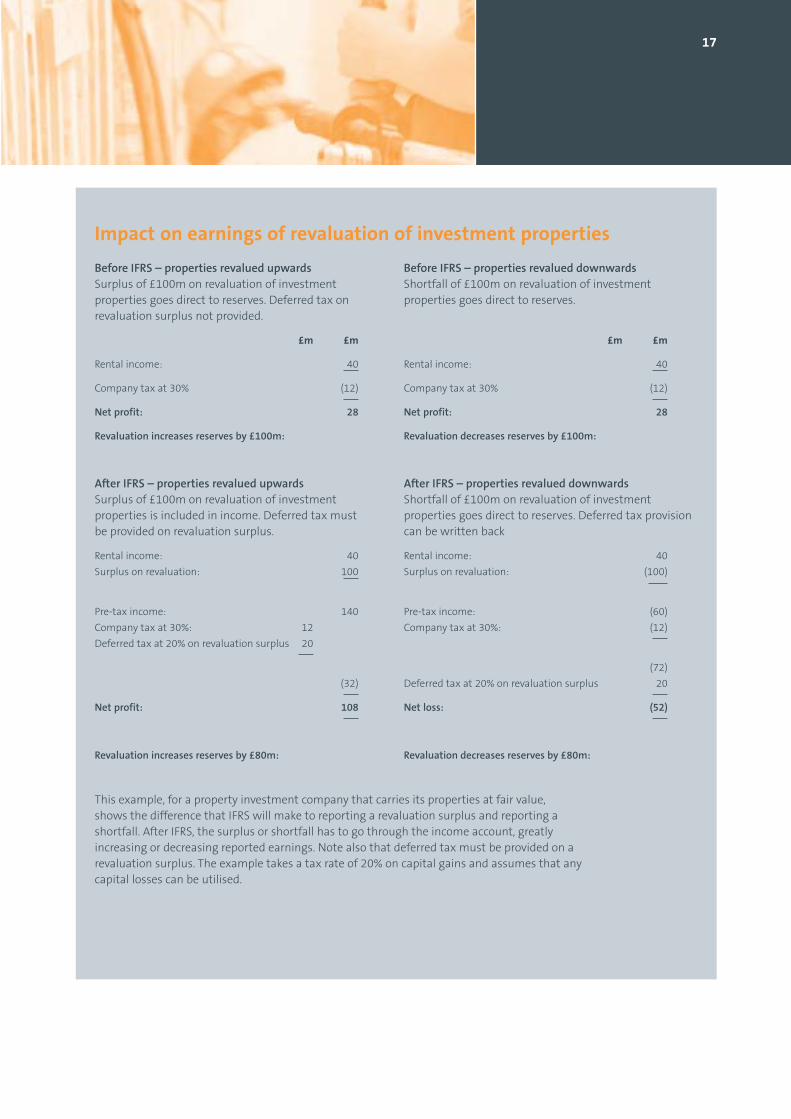

Impact on earnings of revaluation of investment properties

Before IFRS – properties revalued downwardsShortfall of £100m on revaluation of investmentproperties goes direct to reserves.

£m £m

Rental income: 40

Company tax at 30% (12)

Net profit: 28

Revaluation decreases reserves by £100m:

After IFRS – properties revalued downwardsShortfall of £100m on revaluation of investmentproperties goes direct to reserves. Deferred tax provisioncan be written back

Rental income: 40

Surplus on revaluation: (100)

Pre-tax income: (60)

Company tax at 30%: (12)

(72)

Deferred tax at 20% on revaluation surplus 20

Net loss: (52)

Revaluation decreases reserves by £80m:

Before IFRS – properties revalued upwardsSurplus of £100m on revaluation of investmentproperties goes direct to reserves. Deferred tax onrevaluation surplus not provided.

£m £m

Rental income: 40

Company tax at 30% (12)

Net profit: 28

Revaluation increases reserves by £100m:

After IFRS – properties revalued upwardsSurplus of £100m on revaluation of investmentproperties is included in income. Deferred tax mustbe provided on revaluation surplus.

Rental income: 40

Surplus on revaluation: 100

Pre-tax income: 140

Company tax at 30%: 12

Deferred tax at 20% on revaluation surplus 20

(32)

Net profit: 108

Revaluation increases reserves by £80m:

This example, for a property investment company that carries its properties at fair value, shows the difference that IFRS will make to reporting a revaluation surplus and reporting ashortfall. After IFRS, the surplus or shortfall has to go through the income account, greatlyincreasing or decreasing reported earnings. Note also that deferred tax must be provided on arevaluation surplus. The example takes a tax rate of 20% on capital gains and assumes that anycapital losses can be utilised.

Lease lengths may shortenThe accounting rules for leases under IAS 17 could have an impact on the length of lease thatoccupational tenants are prepared to sign up to infuture. If the lease is categorised as a financelease, the tenant will have to show as a liability inhis accounts the present value of the payments heis committed to make under the lease. In the morecommon situation where the lease counts as anoperating lease the tenant will still have todisclose the lease payments to which he iscommitted, even though this liability will notappear on balance sheet.

These rules are welcome in that they give a clearer picture of a company’s financialcommitments, either on the balance sheet or viadisclosure. It has been a weakness of accountingin the past that borrowed money had to be shownas a liability but payments due under operatingleases – which are an equally inescapable financialcommitment – did not have to be disclosed.

The rules will probably be less welcome totenants, however. They are unlikely to welcomeanything that underlines their financialcommitments, and will want to keep thesecommitments as low as possible. Take a tenantwith a non-cancellable lease of 15 years at a rentof £500 000 a year and another tenant with alease of only five years at the same rent. Using,say, a 6% discount rate and assuming for simplicityrents payable annual in advance, the present valueof £500,000 a year for 15 years is around £5.1m.

The present value of £500 000 a year for five years is £2.2m. Which commitment would atenant prefer to disclose? No prizes for guessingthat – in countries with a tradition of longishleases, such as the United Kingdom – the pressurewill grow on landlords to agree shorter terms.

Leasehold accounting may cause confusionExpect some confusion among investors and other accounts users as property investmentcompanies start accounting under theinternational accounting rules for the leaseholdproperties that they hold. We describe thetortuous process in the box ‘Accounting for aleasehold investment property’.

The important point to remember is that thecarrying value of the leasehold will be an artificialconstruct made up of the valuation of the propertyplus the present value of the minimum leasepayments to the superior landlord, with the presentvalue of these lease payments also appearing onthe liabilities side. Accounts users will need to getused to the apparent increase in gearing that willresult from this process where rents to the superiorlandlord are a significant item.

International accountingstandards are considerablytougher than manydomestic standards onaccounting for takeovers

‘’

18

In the long run the changes will probably begreatest in countries such as Germany (which has previously outlawed revaluation of properties in company accounts) or France (whererevaluation was sometimes allowed but did nothave to be kept up to date). But, in the short termat least, German and French companies maycontinue to carry their properties at cost if theywish. The impact will be smaller in countries suchas Britain, which has long allowed or (in the caseof investment properties) required revaluation,and Australia, which also already allows propertiesto be carried at fair values .

IFRS draws a clear distinction between owner-occupied properties and investment propertiesand between finance leases and operating leases.It is strict in requiring most takeovers to beaccounted for as acquisitions rather than mergers.It requires those preparing accounts to look atthe substance of transactions and not merely thelegal form. And while it deals with the content ofaccounts, it does not stipulate the format, asmany existing domestic accounting standards do.In these respects in particular the internationalregime will bring change in many instances.Below we look at some of the main differencesin accounting for property between IFRS anddomestic standards in a selection of countries.

Australia: revaluations already acceptedInsofar as they apply to property, Australianaccounting rules are similar to IFRS requirementsin many respects and the differences are oftenthose of detail. In particular, the principle of usingcurrent values is already accepted. Both propertyoccupied by a business and investment property(the two are not accounted for differently) may bestated either at cost or at valuation. However,there is no equivalent of the IFRS requirement todisclose the fair value of investment propertywhen this is carried at cost.

Under Australian accounting rules, all businesscombinations are treated as acquisitions ratherthan a pooling of interests (IFRS does not rule outthe pooling of interests completely) and assetsacquired are recognised at fair values, as under IFRS.

Classification of leases is similar to that requiredunder IFRS though the Australian rules providemore quantitative tests for a finance lease. Both inthe accounts of lessors and of lessees, operatingand finance leases are accounted for in a mannersimilar to that required by IFRS.

Czech Republic: big changes required inaccounting for leases Lease accounting in the Czech Republic willundergo substantial changes with the adoption of International Financial Reporting Standards.Under domestic accounting standards there areno specific rules on accounting for leases, whichare normally all treated as operating leases.Therefore leases which might count as financeleases under IFRS are not capitalised in the lessee’saccounts, and no corresponding liability isrecognised. Generally, the form of an arrangementtakes precedence over the substance.

Nor do Czech domestic accounting rules addressthe distinction between property used in thebusiness and investment property, which is centralunder IFRS. Revaluation of assets (includingproperty), which is required initially when assetsare acquired by takeover, is not otherwisepermitted. Most properties are therefore carried athistorical cost. There are no specific rules onaccounting for sale and leaseback transactions.

19

How different countries are affected by IFRSThe amount of change required by the switch to International Financial Reporting Standards will varyfrom country to country. And a number of countries have in any case been bringing their domesticaccounting standards into line with the international ones ahead of the European adoption deadline.

Section 4

France: no previous requirement to update valuationsFrench accounts generally follow a standardformat whereas IFRS specifies the content ratherthan the format. A statement of recognised gainsand losses is not required under French GAAP. Thelegal form of a contract rather than the substancemay be more important than it will be under IFRS.

French GAAP does not define a finance lease asIFRS does and not all finance leases are capitalised.

Takeovers are less strictly treated than under IFRS and merger accounting (‘uniting of interests’)is more widely used. There is not an accountingdistinction between owner-occupied property and investment property, and investmentproperty is accounted for as property, plant andequipment. Revaluations of property are allowedonly as part of a general revaluation of long-termfinancial instruments and of property plant andequipment and revaluation surpluses go direct toreserves. Unrealised gains are not generallyrecognised in the income statement. Where acompany has revalued, there is no requirementto keep valuations up to date.

Treatment of profits on sale and leasebacktransactions may need to change under IFRS.

Germany: domestic standards do notallow revaluationGerman accounts follow standard formats and the legal form of transactions carries greaterweight than under IFRS. A statement ofrecognised gains and losses is not required.

Accounts are firmly based on historical cost andrevaluations are not permitted. There is not anaccounting distinction between owner-occupiedand investment properties. The income accountgenerally recognises only realised gains.

Classification of leases is less rigid than underIFRS. Leases previously classified as operatingleases would often need to be accounted for asfinance leases under the international rules.

Depreciation does not always relate to theexpected useful life of the asset, as required under IFRS, but may be driven more by taxconsiderations.

It is easier to treat a business combination as auniting of interests (‘merger’) than under IFRS,which generally requires acquisition accounting.

Treatment of profits on sale and leasebacktransactions may need to change under IFRS.

Poland: less strict than IFRS on finance leasesPolish accounting does recognise the differencebetween properties used in the business andinvestment properties, but there is no obligationto disclose fair values of investment property. The owner may choose to carry it at revaluedamounts but there are no rules on frequency ofvaluations. Property used by the business isnormally carried at historical cost except when the Ministry of Finance infrequently promotes a revaluation for tax purposes. But suchrevaluations are not subsequently kept up to dateon a regular basis.

Properties acquired via a takeover accounted for as an acquisition will be recognised initially at fair values.

The classification of leases between operatingleases and finance leases is less strict than underIFRS and most leases are treated as operatingleases. However, where a finance lease isrecognised it is capitalised on the balance sheetof the lessee and the treatment is similar to thatrequired under IFRS. Domestic accounting ruleshave no specific provisions on accounting for saleand leaseback transactions.

Spain: fair values come as a culture shockSpanish domestic accounting rules are firmlyrooted in the historical cost tradition apart fromoccasional revaluations of fixed assets requiredunder government rules, which are not kept up todate. The fair value option of IFRS therefore comesas an innovation and meets some resistance.There is no requirement to disclose the fair valuesof investment properties, as under IFRS.Accounting for business combinations may alsodiffer markedly from that required by theinternational regime.

There are significant differences between SpanishGAAP and IFRS in the area of accounting for leases.This applies both to lessor and lessee accounting,and the treatment of finance leases in theaccounts of the lessee differs significantly fromthe IFRS model.

20

United Kingdom: use of fair values alreadyallowed or requiredThe United Kingdom is in the process of updating many of its domestic standards toachieve convergence with IFRS.

Along with Australia and South Africa the UK isone of the countries that allows revaluation ofproperties under its domestic standards. In fact, it requires investment properties to be shown at valuation and offers the option of cost or fairvalue for owner-occupied properties. Valuationsmust be regularly updated. IFRS will offer the costoption for investment properties as well as owner-occupied ones, but it seems unlikely that manycompanies will switch back from valuation to cost.

IFRS will bring an important change in thetreatment of revaluation gains and losses oninvestment properties. These have generallygone to reserves via the statement of totalrecognised gains and losses but under IFRS will go through the income statement. Previously,unrealised gains have not been recognised in the income statement.

Deferred tax on revaluation surpluses is notnormally provided, but will need to be providedunder IFRS.

The UK has a long leasehold tradition and many property investment companies haveleaseholds among their assets. In the past thesehave been valued and accounted for in much thesame way as freeholds. The treatment will changeradically under IFRS, which requires leaseholds inthe accounts of the investor to be treated asfinance leases.

Accounting for some sale and leasebacktransactions may need to change under IFRS.

United States: some convergence with IFRS buta fair way to goA convergence project aimed at eliminatingdifferences between IFRS and United Statesaccounting rules (US GAAP) has been in progresssince 2002. The two systems are similar in manyrespects, though US accounting is more rule-basedthan IFRS; requirements are generally specified inmore detail and pay greater attention to the legalform of a transaction than IFRS, which is moreconcerned with the substance.

But there is a fundamental difference in that USGAAP does not generally recognise the principle of carrying property, plant and equipment at fairvalues. Thus property (and there is not anaccounting distinction between the treatmentof owner-occupied property and investmentproperty) is carried in the books at depreciated cost.

However, the principle of fair values has beenaccepted to a limited extent. It applies in the case of business combinations, where acquiredliabilities and assets are taken at fair value at thedate of acquisition.

21

IFRS draws a clear distinctionbetween owner-occupiedproperties and investmentproperties and between financeleases and operating leases

‘’

• All companies must, of course, disclosewhether they are using the cost model or thefair value model in their accounts: are theycarrying properties at cost or at valuation?

• Companies are required to give considerabledetails of changes in their property portfoliosover the year: additions, acquisitions, disposals,depreciation provisions (where applicable),impairment provisions (where applicable),surpluses or deficits arising on revaluation, etc. They must also give details of movementsof properties between categories: inventories,owner-occupied properties and investmentproperties

• In the case of owner-occupied properties andinvestment properties that are carried atdepreciated cost, companies must giveconsiderable detail on the depreciationmethods and rates adopted

• For properties accounted for under IAS 16(which covers mainly owner-occupiedproperties) the company must disclose anyrestrictions on title, any property charged assecurity for loans and any contractualcommitments to acquire property. Expenditurerecognised in the carrying amount of propertiesin the course of construction must also bedisclosed. Note that even properties destinedon completion to be investment properties willbe accounted for at cost under IAS 16 ratherthan under IAS 40 during the constructionperiod, except where an existing investmentproperty is being redeveloped as an investmentproperty. In the case of investment properties,detail must be given of any restrictions onrealisation or on remittance of income ordisposal proceeds

• When owner-occupied properties orinvestment properties are carried at valuation,the company must disclose whether anindependent valuer was involved and the‘methods and significant assumptions’ used inthe valuation. Information is also required onwhether the valuation was based on marketevidence or relied on other techniques. Therequirements differ slightly between owner-occupied and investment properties, but thegeneral thrust is similar

• Where leaseholds are to be accounted for asinvestment properties, companies must makethe normal disclosures for investmentproperties as well as the specific disclosuresrelating to leases. Since a company withleasehold investment property is both a lesseeand a lessor, it must observe the disclosurerules applying to each

• Companies owning investment property mustdisclose the rental income derived from it, andalso disclose direct operating expenses relatingto it, divided between income generatingproperties and those that did not generateincome during the year

• Where a valuation of an investment propertyneeds to be adjusted to arrive at the carryingfigure in the accounts, the adjustments mustbe disclosed and explained. This would apply inthe case of a leasehold carried at fair value asan investment property, where the presentvalue of payments under the lease from thesuperior landlord would need to be added tothe valuation figure (see box ‘Leaseholdinvestment properties – the new treatment’) toarrive at the carrying amount.

• Changes in the classification of property mustbe disclosed. This means that any movementsbetween investment properties, owner-occupied properties and inventories wouldneed to be noted

Disclosures required under IFRSFor countries whose domestic accounting standards have not required very detailed disclosures in thepast, the international standards will come as a shock. The detail required on property holdings and onleases – from owners, lessors or lessees – is extensive. Note in particular that companies that choose tocarry their properties at cost do not necessarily avoid the need for a valuation. In the case of investmentproperties carried in the books at cost, fair value must also be disclosed. With owner-occupied propertiescarried at cost, companies are encouraged to disclose fair values where materially different from thecarrying amounts. The following paragraphs highlight some of the additional main disclosures requiredbut are not intended to be comprehensive.

22

Appendix A

• A feature of IFRS is the very extensiveinformation that both lessors and lessees are required to provide on their leasingarrangements. So, while it is only a lessee who occupies his property under afinance lease who has to capitalise the lease onhis balance sheet, very similar information onlease commitments has to be disclosed bycompanies occupying their properties underoperating leases. Both lessors and lessees arerequired to describe their material leasingarrangements and rents receivable andpayable, and are required to separate out anycontingent rents (such as those related toturnover) and the basis on which they arecalculated. Companies that occupy theirproperties under operating leases are required to disclose and break down the totalof the lease payments to which they arecommitted. They must also disclose anyrenewal or purchase options, or escalationclauses and any restrictions imposed by lease arrangements

• Lessors are generally required to provide similar information to lessees on their materialleasing arrangements, including a breakdownof future rents receivable, contingent rentsreceived, etc. Disclosures required of lessorswho grant a finance lease include a time break-down of the present value of lease paymentsreceivable in the future and a reconciliation ofthe present value at balance sheet date and the gross investment in the lease. The lessormust also disclose unearned finance income;information on residual values accruing to hisbenefit; the accumulated allowance foruncollectible lease payments; contingent rentsincluded in income; and a general descriptionof leasing arrangements.

23

International Financial Reporting Standards draw a rigid distinction between properties thata company occupies for its own business andthose that are classified as investment properties.The definition of an investment property is‘property (land or a building – or part of a building– or both held (by the owner or by the lesseeunder a finance lease) to earn rentals or for capitalappreciation or both…’. Properties held for sale inthe normal course of business do not qualify asinvestment properties.

The accounting treatment of properties occupiedby the business is governed mainly by IAS 16Property, plant and equipment in the case ofowner-occupied property and IAS 17 Leases forleased property. Investment property comes underIAS 40 Investment property. Both IAS 16 and IAS 40give the option of carrying properties at cost or atfair value, but there are significant differences inaccounting treatment between the two. Leaseholdinvestment properties require special treatment,covered by IAS 17 as well as by IAS 40.

Other international accounting standards that areparticularly relevant to property include IAS 2Inventories, IAS 12 Income taxes, IAS 22 Businesscombinations, IAS 32 Financial instruments:disclosure and presentation, IAS 36 Impairment ofassets and IAS 39 Financial instruments:recognition and measurement. In addition, IFRS 1First-time adoption of international financialreporting standards governs the initial switchfrom domestic to international standards.

As well as the distinction between investment andowner-occupied properties, there is a further rigiddistinction between the accounting treatment ofoperating leases and finance leases. This isexamined in more detail in the box ‘Operating orfinance lease – the vital distinction’. Broadly, afinance lease is one that transfers substantially allthe risks and rewards of ownership to the lesseeand a lease that does not meet this definition isan operating lease. In the case of a finance leasethe lessee carries the lease as an asset on hisbalance sheet and shows as a correspondingliability the present value of the payments he iscommitted to make over the term of the lease. Anoperating lease does not appear on the balancesheet of the lessee.

Below we summarise the main features of theaccounting treatment of different categories oflong-term property assets and of leases underIFRS. This is not intended as a substitute forreading the accounting standards themselves,which include much greater detail and, in somecases, significant qualifications to the generalrules.

Owner-occupied properties The accounting treatment is governed largely by IAS 16: Property, plant and equipment. Freehold properties that a company uses for itsbusiness and that are held as long term assets are recognised initially at cost, which includesdirect costs of bringing the property intooperation. Subsequently they are carried in theaccounts either at cost (‘cost model’) or atvaluation (‘revaluation model’), in both cases lessdepreciation and any impairment provisions. The building element of the property isdepreciated through the income statement overthe expected useful life of the asset, but the landelement is not normally depreciated.

Leasehold properties that are held under anoperating lease and occupied by the business areaccounted for according to the normal rules forleases under IAS 17. The special provisions relatingto leasehold investment properties do not apply.

Profits or losses on disposal are calculated on thedifference between the carrying amount and thesale price. The result will therefore differ,depending on whether the property is carried atcost or valuation. In the case of deferred payment,sale price will be the cash price equivalent. Specialrules may apply when a property is disposed of ina sale and leaseback transaction (see section ‘Saleand leaseback transactions’ below). Note thatgranting of a finance lease will count as a disposalby the lessor.

Disclosure requirements are extensive (see alsoAppendix A: ‘Disclosures required under IFRS’) and include details of any restrictions on title andof any property pledged as security for loans. Note that, where the cost model is used, thecompany is encouraged (though not required) todisclose fair values as well where these differmaterially from the carrying amount. Where thefair value model is used, the company mustdisclose what the carrying amount would havebeen under the cost model.

Accounting treatment by class of property

24

Appendix B

If fair value model is usedOnce the decision is made to carry properties atvaluation, the valuation must be kept up to date.Frequency of valuation will depend on conditionsand how fast values are moving – it must befrequent enough to keep book figures in line withmarket values. It might need to be annual, itmight be every three or five years. Normally, allassets of a class must be revalued at the sametime, though a rolling basis may be permissiblesubject to strict conditions.

The standard does not specify the valuation basis but simply says that fair value ‘is usuallydetermined from market-based evidence byappraisal that is normally undertaken byprofessionally qualified valuers’. This leaves openthe question of whether ‘market value’ or someversion of ‘existing use value’ should be used – seesection ‘Valuations and the property professional’srole under IFRS’ for the detail. The company mustdisclose whether an independent valuer wasinvolved and must provide information on thevaluation methods and assumptions.

Treatment of revaluation surpluses and shortfallscan be a little complex. If the book figure isincreased as a result of a revaluation, the surplusnormally goes direct to reserves. It will, however,go through the income statement to the extentthat it reverses a previous revaluation deficit onthat property that had gone through the incomestatement. If the book figure is decreased by arevaluation, the shortfall will go through theincome statement except to the extent that itreverses a previous revaluation surplus on theproperty in question, in which case it will bededucted from reserves. Both surpluses andshortfalls may therefore, in some circumstances,affect published profits.

Properties occupied by a business under a leaseThe accounting treatment is governed by standardIAS 17: Leases. For differences between operatingleases and finance leases see box ‘Operating orfinance lease – the vital distinction’. Note thatminimum lease payments (including any up-frontsum paid for the lease) may need to be allocatedbetween the land and buildings elements of theproperty, in proportion to the relative capitalvalues of the two elements. This is to enableclassification of the lease between operating andfinancial, where this is in doubt. If this allocation is impracticable, special rules apply.

Special provisions apply to leasehold properties thatare to be accounted for as investment properties(see below) and in this case the allocation betweenland and buildings is not required.

Operating leases in the accounts of the lesseeThe lessee (tenant) does not capitalise anoperating lease. In other words, no asset or liability is disclosed on his balance sheet. Leasepayments are simply charged as an expense to the income statement, usually on a straight-linebasis over the lease term. However, if an up-frontcapital sum is paid to acquire a lease, this istreated as pre-paid lease payments and isamortised over the lease term.

Finance leases in the accounts of the lesseeA finance lease is capitalised in the accounts ofthe lessee. In other words, the lease is recognisedin the lessee’s balance sheet as an asset. Thepresent value of payments to which the lessee iscommitted under the lease appears as acorresponding liability. At the start of the leaseterm the lease is included as an asset at fair valueor at the present value of minimum leasepayments if this is lower. For this purpose thepresent value would include any up-front capitalsum paid for the lease.