PROJECT REPORT ON “STUDY OF INVENTORY CONTROL AT TECHNOCRAT ENGINEERS” For TECHNOCRATS ENGINEERS By PRACHI TALEKAR Under the Guidance of PROF. VIJAY DESHMUKH Submitted to “University of Pune” In partial fulfillment of the requirement for the award of the degree of Master of Business Administration (MBA) Through Dr. Vikhe Patil Foundation’s 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PROJECT REPORT

ON

“STUDY OF INVENTORY CONTROL

AT TECHNOCRAT ENGINEERS”

For

TECHNOCRATS ENGINEERS

By

PRACHI TALEKAR

Under the Guidance of

PROF. VIJAY DESHMUKH

Submitted to

“University of Pune”

In partial fulfillment of the requirement for the award of the

degree of Master of Business Administration (MBA)

Through

Dr. Vikhe Patil Foundation’s

Centre for Management Research &Development

Pune-16

1

ACKNOWLEDGEMENT

Planning & Motivation are the two key factors in making any activity a success. Goal

achievement is a result of effort rather than individual effort. I have been the same of this

project the co-operation &support of many individuals has made this project a success.

I have the honor to express my heartfelt gratitude to Mr.S.V.Patki for giving me the

opportunity to undergo the summer training in their esteemed organization and for his valuable

guidance and support.

I take this opportunity to extend my sincere gratitude to all the staff members for their whole

hearted cooperation and valuable help throughout the training.

I sincerely express my gratitude to Prof. Vijay Deshmukh for his support in the completion of

the project.

Sr. No. PARTICULARS PAGE NO.2

1 EXECUTIVE SUMMARY 4

2 COMPANY PROFILE 5

3 OBJECTIVE OF THE STUDY 7

4 RESEARCH METHODOLOGY 8

5 INTRODUCTION

INVENTORY

MATERIAL

10

6 CONCEPTS OF INVENTORY 12

7 PURCHASE

DETAILS

PROCEDURE

FORMATS

23

8 STORES ORGANISATION 34

9 CLASSIFICATION OF MATERIALS 39

10 IDENTIFICATION OF MATERIALS 43

11 CODIFICATION 44

12 TECHNIQUES OF INVENTORY MANAGEMENT

FIXATION OF LEVELS

SELECTIVE CONTROL OF INVENTORIES

JIT

ANALYSIS OF INVESTMENT IN INVENTORY

45

13 DATA ANALYSIS 55

14 RECOMMENDATIONS &SUGGESTIONS 95

15 CONCLUSION 96

16 BIBLIOGRAPHY 97

CONTENTS:

EXECUTIVE SUMMARY

3

Inventory is the most significant part of the company, which accounts for over 30-40% of the

company’s expenditure. This project reflects the inventory management system of

TECNOCRAT ENGINEERS. Inventory means all the materials, parts, supplies, expensive

tools and semi finished or finished products recorded on the book by an organization and kept

in its stocks, warehouse or plant for some period of time.

DEFINITION OF INVENTORY

“Inventory is a list of names, quantities and monetary values of all or any group of items”

“Inventory is a detailed list of those movable items which are necessary to manufacture a

product and to maintain the equipment and machinery in good working order.” The quantity

and value of every item is also mentioned in the list

The area of focus of this project is to reduce the overall cost associated with inventory by the

undertaking activities:-

Obtaining the list of surplus stock and finding out reasons for growing surplus.

Attempt to reduce the existing surplus.

An attempt to prevent further accumulation of surplus

Making recommendations to the currently followed purchase procedure

Suggesting more effective method for the control of inventory.

Reduction of the accumulated/surplus stock period itself reduces unnecessary amount of

money blocked in the form of inventory and hence resulting in blocking the working capital of

the company.

COMPANY PROFILE

4

TECHNOCRAT ENGINEERS was started in1991. Today it provides complete solution to suit

the clients welding automation requirements. The design engineers of TECHNOCRATS work

out the right level of automation for the client & make a full proof welding system, to give the

client what he dreams for these years. The company is a proven name in the welding industry

for quality ARC welding equipments & accessories reliable & quick after sales service. In any

engineering goods manufacturing activity, welding plays a very important role. "Technocrat

engineers" work in the field of welding engineering with a view to supply good quality

welding equipments, accessories and special purpose automated welding systems. Technocrat

engineers is in the field for more than 10 years today. It is known for its excellent quality

products and customer oriented service back up.

Mr. S. V. Patki and Mr. D. M. Talekar the real "technocrats" are constantly in touch

with the customers, understanding their needs developing suitable welding systems to satisfy

the customer needs. The policy of continuous improvements in the products & services keep

the customers happy and satisfied. Both the partners’ viz. Mr. Patki and Mr. Talekar are

engineers working in this field for more than last 20 years and have hands on experience in

designing, production, quality control and marketing.

PRODUCT RANGE:

Industrial Duty range.

Industrial Duty Welding Rectifiers.

CO2/MIG Welding Outfits.

Tig Welding Outfits and Control Units.

Submerged ARC Welding Machines (Carriage and Boom Mounting Type)

Self Shielded Hard Facing Welding Systems.

Automating Modules Such as Turn Tables, Welding Lathes.

Automatic/Special Purpose Welding Systems to Suit Customer’s Specific

Requirements of Productivity and quality

OTHER ACTIVITIES:

5

Calibration of welding equipments as per ISO 9001 requirements.

Welding improvements and automation possibilities: Advice to customers after

studying the specific needs of productivity.

OBJECTIVES OF THE STUDY

6

The primary objective of this project is to reduce overall expenditure or costing for the

company by lowering the cost associated with inventory.

Various other objectives pursued to fulfill the primary objective are as follows-

Reduction of existing surplus stock.

To avoid any further accumulation of surplus

To device an appropriate cost reduction technique of inventory control, which can be

used along with the existing technique to improve performance.

RESEARCH METHEDOLOGY

7

MEANING OF RESEARCH

Research is an active, diligent and systematic process of inquiry aimed at discovering,

interpreting and revising facts. This intellectual investigation produces a greater knowledge of

events, behaviors, theories and laws and makes practical application possible. The term

research is also used to describe an entire collection of information about a particular subject,

and is usually associated with the output of science and the specific method. The word research

derives from the French recherché, from researcher, to search closely where “chercher” means

“to search”, its literal meaning is “to investigate thoroughly’. Research is funded by the public

authorities, by the charitable organization and by private groups, including many companies. It

is defined as the “systematic and objective analysis and recording of controlled observations

that may lead to the development of generalization principles or theories, resulting in

prediction and possibly ultimate control of events.”

Research can be classified into various classes. These classes are not watertight compartments.

There is a certain amount of overlap between the various classifications. Every classification

emphasizes certain aspect of research.

RESEARCH DESIGN

A research design specifies the method and procedures for conducting a particular study. In

this case exploratory and applied type of research is used. An exploratory is generally based on

the primary data that are readily available. It does not have rigid design as researcher may have

to change his focus or direction depending on the availability of variables i.e. statistics graphs

and charting. The second type- applied research is nothing but application of sciences and

knowledge to observe variables i.e. applied theory.

DATA SOURCES

8

SECONDARY DATA-

As the project is based on Aligning the Inventory, hence data involved in the analysis is

basically a secondary data.

The facts and figures along with the records were taken from the executives of the company.

Records related to inventory were taken from purchase department and stores department.

METHOD OF DATA COLLECTION:

Since this scope & topic is based on theory it was imperative to use secondary data method for

data collection.

A real attempt was done to simplify the project research. The report is written in organized

appearance. Observations and recommendations are presented in this report in simple and

systematic manner.

INTRODUCTION

9

INVENTORY

The raw materials, work-in-progress and completely finished goods that are considered to be

the portion of a business’s assets those are ready or will be ready for selling. Inventory

represents one of the most important assets that most business possesses, because the turnover

of inventory represents one of the primary sources of revenue generation and subsequent

earnings for the companies’ shareholders/owners.

Possessing a high amount of inventory for long periods of time is not usually good for a

business, because there are inventory shortage, obsolescence and spoilage costs. However,

possessing not enough inventory isn’t good either, because the business runs the risk of losing

out potential sales and potential market share as well.

Inventory management forecasts and strategies, such as a just-in-time inventory system, can

help minimize inventory costs because goods are created or received as inventory only when

needed.

MATERIALS

Materials are the key resource in an industrial enterprise since no production is possible

without materials. Materials also form a major constituent of the cost of the product and

therefore proper control over their procurement, storage, issue, movement and consumption is

necessary.

The storage of the material is of great interest to the company, because normally substantial

amount of the company’s working capital is invested in stores. There should be a system of

proper accounting of material and supplies and it should be given same attention as is given to

accounting for money. Raw material and supplies are the equivalent of cash. They form an

important part of cost of manufacturing ad it is essential that they should be safeguarded and

accounted properly.

Material control is important managerial function, which is directed to ensure that required

quantity and quality of material is provided at the proper time with minimum amount of

capital.

10

Material management, according to bethel and others, is a term used to connote “controlling

the kind, location, movement and timing of the various commodities used in and produced by

the industrial enterprise.” It involves all activities concerning materials right from the time the

need for the material is established until they are to production.

Thus, the functions of material management includes:-

Material Planning

Purchasing

Inventory control

Store –keeping

Store accounting

Transportation-Internal (i.e. material handling)&

External (i.e. traffic, shipping, etc.)

Disposal of scrap, surplus and obsolete materials

Material economics

Waste Management

CONCEPTS OF INVENTORY

MEANING

11

The literary meaning of the word inventory is stock of goods. To the finance manager,

inventory connotes the value of raw materials, consumables, spares, work-in-progress, finished

goods and scrap in which a company’s funds have been invested. Good inventory management

is good finance management. An efficient management of inventory should ultimately result in

the maximization of the owner’s wealth. Therefore inventory is considered as locked up

capital. Inventories mean tangible property held:

a. For sale in the ordinary course of business; or

b. In the process of production for such sale or

c. For consumption in the production of goods or services for sale, including

maintenance supplies and consumables other than machinery spares.

DEFINITION

Inventory management may be defined as the sum total of those activities which are necessary

for the acquisition, storage, sale and disposal or use of material. It is a subject which merits the

attention of the top level management and influences the decisions of the planning and

executive personnel.

Decisions relating to inventories are taken primarily by executives in production, purchasing

and marketing departments. Usually, raw material policies are shaped by purchasing and

production executives, work-in-progress inventory is influenced by the decisions of production

executives and finished goods inventory policy is involved by production and marketing

executives. The financial manager has the responsibility to ensure that inventories are properly

monitored and controlled. He has to emphasize the financial point of view and initiate

programmes with the participation and involvement of others for effective management of

inventories.

The inventories which include inventories of raw materials, finished goods and work-in-

progress constitute quite a significant part of the total current assets. It has been observed that

in many cases inventories are more than 60-65% of the total current assets of the firm. This

naturally means that a very large amount is blocked in inventories & therefore management of

inventories has assumed a greater importance. If properly managed, the profitability of a firm

in the long run can be definitely improved while if neglected, the profitability is definitely

affected adversely.

12

DIFFERENT PERCEPTIONS OF THE “INVENTORY”

It is interesting to note different departments of the same organization hold different points of

view, which often tends to conflict with one another. It can be said as follows:-

The financial manager justifies limited inventory stocks, because for him, inventory is

money which does not earn interest and ties up capital.

The production manager, on the other hand, encourages to keeping liberal inventory

stocks to guard against stock- outs in the face of fluctuating demands and uncertain

deliveries.

The marketing executive prefers to have reserves of the finished goods inventory.

Product designers are interested in getting an inventory which makes up the products

with all possible accuracy.

Engineers, on the other hand, are often inclined to have a critical mind towards value-

analysis, value engineering and other allied problems of inventory.

Thus although the different approaches to the problems of inventory are not misleading, they

are likely to be biased by their own considerations. The top level management should,

therefore, bear such diverse expressions in mind instead of getting lost in them and take a

bird’s eye-view of the overall objective of “neither too much nor too little” inventory by

attempting a cost benefit analysis. A well-reconciled scientific approach would enable the

management to plan and control inventory effectively.

TYPES OF INVENTORY

The inventories can be classified as follows:

1) Raw Materials:

13

A manufacturing concern converts the raw material into the finished products. The raw

materials are the basic inputs which are required for the conservation into finished goods.

2) Work-In-Progress:

Between the raw materials and there is an intermediate stage which is known as work-in-

progress. These units are therefore neither totally raw nor totally finished and is generally a

planned activity.

3) Finished Goods:

These are completed units awaiting the sale in the market. As the production in the modern

days is in anticipation of the demand, some amount of finished goods inventory is

inevitable. The inventory should be in sufficient quantity so that marketing operations of

the firm are smooth. Thus, the stock of finished goods provides a buffer between customer

and demand and manufacturer’s supplies.

4) Flabby Inventory

It comprises finished goods, raw material and stores held because of poor working capital

management and inefficient.

5) Profit-making Inventory:

It represents the stock of raw materials and finished goods held for realizing stock profit.

6) Safety Inventory:

It provides for the failure in supplies unexpected spurt in demand, etc., although there may

be an insurance cover.

7) Normal Inventory:

It is based on a production plan, lead time of supplies and economic ordering levels.

Normal inventories fluctuate primarily with change in the production plan. Normal

inventory also includes a reasonable factor of safety.

8) Excessive Inventory:

Even an effective management may be compelled to build up excessive inventory for

reasons beyond its control, as in the case of strategic import or as a measure of government

price support of a commodity.

ASPECTS OF INVENTORY MANAGEMENT

Inventories are quite crucial for any business firm. The raw materials inventory, if kept excess

of the requirement may lead to unnecessary blocking of the funds in such inventory, while if it

14

is in shortage, it will lead to disrupting the flow of production. Similar things can be said about

the work in progress and finished goods inventory. The option before the management is either

to keep a very low level of inventory which is also known as hand to mouth policy or to keep a

large quantity of inventory ensuring absolute safety.

As said, above, if inventory levels are kept very low. It will lead to frequent stoppages of

production. If finished goods inventories are kept very low it will result in distributing the

delivery schedule to the customers. It may further lead to the cancellations of some of the

orders. No firm can afford to take such risks.

Alternatively, if inventory levels are kept on a very high level, carrying cost like storage,

handling, insurance, recording and inspection also increase in proportion to the inventory

volumes. At the same time, as large amount of funds are blocked in those inventories, the

liquidity of the firm is severely affected. The high levels of inventory may ensure safety but the

cost of holding such a high level of inventory may nullify their advantage.

It will also not be out of place to mention here that form holds inventories basically for three

reasons:-

a) TRANSACTION MOTIVE:

This motive implies that inventories are maintained for the facilitation of smooth

production and sales.

b) PRECAUTIONARY MOTIVE:

It suggests that the inventories are maintained to take care against the risk of unforeseen

changes in demand and supply factors.

c) SPECULATIVE MOTIVE:

It says that the inventory maintenance (high or low) decision is affected by the motive

to take advantage of price fluctuations.

The aspects of inventory management can be described as follows:-

1. To ensure hat a very high level of inventory is avoided.

15

2. At the same time to ensure that inventories are not so adequate that it will affect

adversely the smooth flow of production and sales.

3. Minimize the carrying cost and

4. Maintain an optimum level of inventories.

OBJECTIVES OF INVENTORY MANAGEMENT

To have stocks available as when they are required.

To minimize available storage space, but prevent stocks level from exceeding space

availability.

To meet a high percentage of demand without creating excess stock levels. In other

words, “neither to over-stock nor to run out” is the bet policy.

To maintain adequate accountability of inventory assets.

To keep all the expenditure within the budget authorization.

To decide which items to stock and which items to procure on demand.

To ensure adequate supply of materials, stores, spares, etc. minimize stock-outs and

shortages and avoid costly interruption in operations.

To keep down investment in inventories, inventory carrying cost and obsolescence

losses to minimum.

To permit a better utilization of visible stocks by facilitating inter-departmental

transfers within a company.

To provide a check against losses of material through careless of pilferage

To serve as a means for the location and disposition of inactive and obsolete items of

stores.

To provide a perpetual inventory value and a consistent and reliable basis for the

preparation of financial statements.

To contribute to the nation’s economic well-being.

To contribute to profitability and

To bring down the inventory carrying cost inventory management is considerable.

BENEFITS OF INVENTORY MANAGEMENT

16

Inventory control ensures an adequate supply of material and store. Minimize stock out

and shortage and avoid costly interruption in operation.

It keeps down investment in inventories.

It facilities purchasing economics through the measurement of requirement on the basis

of recorded experience.

It provides a check against the losses of material through careless or pilferage.

It serves as a means for the location and deposition of inactive and obsolete item of

store.

FACTORS INFLUENCING INVENTORY

17

LEAD TIME:

Lead-time is defined as the period, which elapses between the recognition of a need and its

fulfillment. There is a direct relationship between lead-time and inventory, during lead time,

there is no delivery of materials and the consuming departments are served from the existing

inventories. Both lead-time and consumption rate can be increased without notice; and

inventories are generally geared up for this contingency. As lead time increases, inventories

increase correspondingly. Lead- time is the time taken for identifying the need and placing the

order, for procuring from suppliers, for shipping, transport, receipt and inspection of items to

the delivery of finished products.

COST OF HOLDING INVENTORY:

Inventory tie up funds. They also expose a firm to a number of risks and costs. The inventory

problem is one of balancing the various costs so that the total cost is minimized. The different

costs are material cost, cost of ordering, holding or carrying the inventory, under stocking cost

and over-stocking cost.

Material Cost:

This is the cost of purchasing goods plus the transportation and handling charges.

Order Cost:

This is a cost of placing an order for goods. Every time a firm places an order; a

particular procedure has to be followed. Forms must be typed, approved and

dispatched. When goods arrive, they must be accepted, inspected and counted. The

invoice must be checked against the goods and sent to the Account department.

Arrangements for the payment to suppliers must be made. All these expenses

accumulate into a variable cost which varies with individual orders. The smaller the

number of orders, the lower is the order cos. A firm, therefore, tries to reduce the

number of orders by placing a big order each time.

Cost of Carrying Inventory:

18

The components of those costs are;

a. The cost of capital.

b. The cost of storage.

c. The cost of deterioration.

d. Salaries and statutory payments of stores personnel.

Cost of typing-up of funds:

An inventory may be financed by trade credit, debt financing or even by the sale of

stock. Whatever the source of funds used for the financing of the inventory, the fact

remains that cost is involved in it.

Cost of Understocking:

Excess inventories represent additional and unnecessary costs. Storages of inventory

delay the fulfillment of contractual orders, which would involve a loss of profit or some

kind of indirect cost. Understocking or out-of-stock cost is due to the non-stocking of

an inventory. This is usually measured in terms of the opportunity cost arising out of

the loss in production by the idle cost of a line. It may result in expediting orders or

giving rush orders and extra charges will have to be incurred on these orders.

Cost of Overstocking:

It is basically opportunity cost arising out of the investment in inventory for a longer

period than necessary.

RE- ORDER POINT:

The re-order point indicates when an order should be placed and depends upon the

consumption rate and the duration of lead time. The simplest method is to place an order when

the inventory is depleted to the lead time consumption level. However, an organization will

have to take care of the long time with sufficient initial stock and then follow it up regularly

with EOQ cycles.

STOCK:

19

In inventory control, different terms are used, such as safety stock, reserve stock, buffer stock

and so on. The buffer stock provides for normal consumption during an average lead time. The

reserve stock provides for an increased consumption rate, while safety stock for an increasing

lead time. The buffer, in fact is the multiplication of normal consumption and average lead

time. The safety stock level is the multiplication of the average demand during a period of the

maximum delay and the probability of its occurrence.

VARIETY REDUCTION:

In organization which has to stock innumerable items, it is imperative to reduce the number of

items carried in an inventory, particularly the different small items which are sparingly used. In

the case of work in progress, the increase in varieties may be due to technical bottlenecks. With

an increase in the items of raw materials, work-in-progress, output, etc. inventory control

becomes more and more cumbersome. An organization will, therefore, have to take proper

steps to ensure that variety reduction is effected as far as possible.

MATERIAL PLANNING:

Production plans have to be converted into material plans so that the quality and time schedule

of requirements may be defined. A material planning is a mechanism which perceives the

environment for inventory control. To have a successful materials planning, adoption of a

definite methodology which would take care of internal as well as external factors is a must.

SERVICE LEVEL:

The degree of service indicates a percentage of the number of replenishment orders which

arrives without difficulty and makes it possible for a firm to render an adequate service to the

customer. The service levels refer to the “probability of not running out of stock” and the

“proposition of annual demand met ex-stock.”

OBSOLETE INVENTOY AND SCRAP:

An inventory becomes obsolete because of change in the product design or because of

technological changes. Obsolescence cannot be controlled without a proper identification of

inventories which might become obsolete from time to time.

20

QUANTITY DISCOUNTS:

Quantity discounts are offered by the purchasers. In order to induce purchasers, suppliers often

offer a reduced price for bulk orders.

TECHNIQUES OF INVENTORY MANAGAMENT

A. FIXATION OF THE LEVELS.

B. SELSCTIVE CONTROL OF INVENTORIES.

C. JIT

D. ANALYSIS OF INVESTMENT IN INVENTORY.

McDonalds’s vs. Wendy’s: An Example

It’s easy to see how higher inventory turn than competitors translates into superior business

performance. McDonalds is unquestionably the largest and most successful fast food restaurant

in the world. Let’s compare it to one of its main competitors, Wendy’s.

McDonalds’s

2000 1999

Inventories $99,300,000 $82,700,000

Cost of revenue $8,750,100,000

Wendy’s

2000 1999

Inventories $40,086,000 $40,271,000

Cost of revenue $1,610,075,000

Use the inventory turn formula [cost of sales or cost of revenue divided by the average

inventory values] to come up with the number of inventory turns for each business. Between

1999 and 2000, McDonalds had an inventory turn of rate of 96.1549[incredible for even a

high-turn industry such as fast food]. This means that every 3.79 days, McDonald’s goes

through its inventory. Wendy’s, on the other hand, has a turn rate of 40.073 and clears its

inventory every 9.10 days.

21

This inventory in efficiency can make a tremendous impact on the bottom line. By tying up as

little capital as possible in inventory, McDonalds can us the cash on hand to open more stores,

increase its advertising budget, or buy back shares. It eases the strain on cash flow

considerably, allowing management much more flexibility in planning for the long term.

PURCHASE

22

One of the most important aspects of inventory control is to have the items in stock at the

moment they are needed. This includes going into the market to buy the goods early enough to

ensure delivery at the proper time. Thus, buying requires advance planning to determine

inventory needs for each time period and then making the commitments without

procrastination. For retailers, planning ahead is very crucial. Since they offer new items for

sale months before the actual calendar date for the beginning of the new season, it is

imperative that buying plans be formulated early enough to allow for intelligent buying

without any last minute panic purchases.

The main reason for this early offering for sale of new items is that the retailer regards

the calendar date for the beginning of the new season as the merchandise date for the end of

the old season. For example, many retailers view March 21 as the end of the spring season,

June 21 as the end of summer and December 21 as the end of winter. Part of your purchasing

plan must include accounting for the depletion of the inventory. Before a decision can be made

as to the level of inventory to order, you must determine how-long the inventory you have in

stock will last. For instance, a retail firm must formulate a plan to ensure the sale of the

greatest number of units. Likewise, a manufacturing business must formulate a plan to ensure

enough inventories are on hand for production of a finished product.

In summary, the purchasing plan details, When commitments should be placed; When

the first delivery should be received; When the inventory should be peaked; When reorders

should no longer be placed; and When the item should no longer be in stock. Well-planned

purchases affect the price, delivery and availability of products for sale.

GROWING IMPORTANCE OF PURCHASE

23

Traditionally, purchasing was regarded as one of the activities of the production

management. Few important reasons for the change in emphasis are:

1. Higher cost of goods and services -

Raw materials, components and services account for a significant proportion of the

company's total expenditure. Effective purchasing, therefore, can result in a

substantial saving to the company.

2. Escalating cost of stock outs -

Lack of continuity in the availability of materials seriously affects all major companies.

It can damage profitability of the company and lower employee morale. Financial loss

due to stock outs of materials, process industries and in capital-intensive units can be

enormous.

3. Higher present day cost of capital-

The capital distribution between fixed and working capital in a firm is normally

around 60:40. Further, around 80% of the working capital is locked up in inventory.

No organization can afford to invest such a big part of its capital. The bulk of these

stocks can reduce un-necessary capital lockup can be avoided if purchasing is made

efficient.

4. Purchase is not mere act of buying -

Purchasing in today's context includes a wide range of material related activities such as

market research, vendor rating, standardization and variety reduction, codification,

indent control pre-purchase value analysis, price negotiation, inventory control, surplus

disposal., purchase budget, import substitution, purchase system design etc.

5. Changing nature of purchases -

Purchasing today is no longer just commercial activity, but it is techno-

commercial activity. The activity includes technical persons from production,

design and other departments.

24

6. Professionalization of material function -

Like other branches of industries, purchase too has experience development of many

management concepts such as: ABC analysis, economic lot size, learning curve, critical

analysis, line of balance, variety reduction, codification, value analysis, vendor rating

etc.

7. Changing concepts of buyer- seller - relationship-

Efficient buying - continuity and availability of material with the lowest inventory -

demands a buyer to be good at business relation. Retention of good supplier, with

increasing competition, is becoming difficult and hence the buying function is

becoming challenging day by day.

OBJECTIVES OF SCIENTIFIC PURCHASING

1. To procure at competitive price the needed material, supplies, tools and services of

the right quality in the right quantity and at the right time.

2. To maintain continuity of supply to ensure production schedule at minimum

inventory investment.

3. To ensure the production of goods of better quality and the competitive price by

procuring materials, which best suits, the product and the purposes for which they are

intend.

4. To suggest better substitutes to material which are currently being used with a view to

lower cost and maintain the quality of the product.

5. To render assistance in standardization, variety reduction, value analysis and cost

reduction programmes.

6. To advice on probable prices, delivery and performance items under consideration by

design, development and estimation department.

7. To create goodwill and enhance company reputation for fairness and integrity through

dealings with the suppliers.

8. To enable company to maintain competitive position and earn a fair return on its

investment.

FUNCTIONS OF PURCHASE DEPARTMENT

25

1. Locating, selecting and developing qualified sources of supply.

2. Scrutinizing purchase indents and deciding suitable method of buying.

3. Floating enquires, processing quotation, conducting negotiation and releasing purchase

orders.

4. Pre- delivery follow up and shortage chasing.

5. Co-ordination with inward inspection including timely return of defective materials back

to supplier.

6. Endorsing suppliers' invoices for payment.

7. Processing suppliers request for price increase including price renegotiation.

8. Attending to supplier's representative and traveling salesman.

9. Arranging discussion meetings between supplier's representative and company's officials.

10.Disposal of surplus, obsolete and scrap material.

11.Advising management as regards to new materials, new products, forward buying etc.

12.Acting as a link between company's finance department and suppliers for timely

payments / settlement of suppliers' bill.

13.Attending to periodical activities like applying for import license, quota etc.

14.Maintaining company's image among suppliers.

PRINCIPLES OF PURCHASING (5 P’S)

Elements of scientific purchasing:

Purchasing is the most important function of material management. Scientific purchasing

however, is not mere procurement of needed materials at the lowest price but their procurement

in a way that minimizes the overall cost of the product. To ensure this, scientific purchasing is

governed by five well-known parameters called basic elements of scientific purchasing or also

called "5 R's of buying"

These 5 R's are:

~ Right Quality ~ Right Quantity

~ Right Price

~ Right Time

~ Right Source

26

PURCHASING CYCLE

Purchasing activity plays a vital role in all the firms in general and in the manufacturing firms in

particular. Purchasing is not merely "Buying to satisfy the indenter’s requirements" but buying

goods of right quality in the right quantities, at the right time and-at the right price"

Purchase cycle consists of following eight major activities:

1. Establishing and communicating the need for procurement.

2. Scrutiny of the purchase indents.

3. market study and selection of sources of supply

4. order preparation

5. follow up

6. receiving and inspection

7. storage and record keeping

8. Invoicing and payment.

•

27

PURCHASE PROCEDURE OF TECHNOCRAT ENGINEERS

OBJECTIVE

To ensure that adequate technical & conventional data is provided to the vendors/sub-

contractor so as to enable them to supply product/material/service to the specified

requirements & on-time.

SCOPE

This procedure covers direct materials, tools, consumables capital items which go into the

product, packaging materials & service sub-contractors.

Products & services which do not affect the finished product quality are extended.

PROCEDURE

1) PURCHASE INDENT ACCEPTANCE:

a.. Purchase action shall be taken on the basis of purchase indents received from the

concerned department or on the basis of reorder levels fixed for the stock items, as

received from PPC. Indents received from various departments are filed serially.

b. If the items are being procured for the first time, purchase department shall get the

approved drawing or the specification sheet of the items from the indenting department.

2) PROCUREMENT ACTION:

a. Details of all purchase orders released by materials department shall be entered in the

purchase order register & the purchase order number as per the register serially. Control

shall be allotted to the purchase order released.

b. Imported Material: Purchase orders for imported material shall be placed on vendors

selected based on the recommendations of Technocrats Engineers principals, or based on

the past reorder as recommended by engineering department

c. Indigenous raw material: For raw materials & bought out components procured

indigenously purchase order shall be placed on the vendor selected from the list of

approved vendors/sub- contractors. All the purchase order numbers are entered in the 28

purchase order register.

d. Capital items: Machine tools & other capital equipment having value more than 1 lakh

shall be procured against 'capital equipment indenting proposals' accompanied by

approved purchase indents. Machine tools & other capital equipments having value les

than 1 lakh shall be procured against approved purchase indent. The indents shall be duly

signed & approved by the Director (Operations).

e. Whenever an order is placed on a new vendor/sub-contractor that is not yet approved, the

P.O shall be typed on trial purchase order.

f. The P.O shall include applicable items from the following:

i. The type, class, grade or other precise identification.

ii. The title or other positive identification & applicable issues of specifications,

drawings, process requirements for approval or qualification of product procedures,

process equipment & personnel.

iii. The title number & issue of the quality system standard to be applied.

g. For regular procured items, an open purchase order shall be placed on the vendors.

Delivery schedule from time to time shall be sent to the vendors. If additional

quantity is required for some orders, amended schedule shall be sent.

h. For regular orders related to brackets & adaptors, the purchase order shall be released

once in a month.

i. Material movement slip shall be used whenever our material is sent outside for

machining/testing.

PURCHASE ORDER & AMENDMENT:

P.O's shall be raised on the vendor/subcontractor selected as above to

authorize the supply of direct material/items/services as per the terms of the

contract & delivery mentioned therein. Purchase orders shall be amended

whenever required & informed to vendor through P.O amendments.

REVIEW OF PURCHASE ORDER:

The P.O shall be reviewed for adequacy of the specified requirements prior

to release. All the three copies of the purchase orders shall be approved of by

the appropriate authorities before release of the P.O to the vendors/sub

29

contractors to the concerned department in Technocrat Engineers. The

authorize signatures are indicated.

VERIFICATION OF THE PURCHASED PRODUCT:

Whenever specified in the contract, the customer or his representative shall be allowed for

the verification of the products either at Technocrat Engineers works or at vendor's place of

work. The co-ordination for such verification activity shall be done by marketing co-

coordinator.

DISPOSAL OF NON-CONFORMING MATERIAL:

Non - conforming material shall be disposed off as per the procedure. Nonconformities

observed shall be reported in the non - conformity analysis register for initiating the

required corrective actions. Vendor/sub-contractor shall be intimated demanding corrective

action for repetitive non-conformities through supplier corrective action request.

RESPONSIBILITY AND APPROVAL:

The authorities of the respective department shall be responsible for review,

implementation, control & verification of this procedure. He shall be responsible for

providing all means & facilities for smooth working of this procedure.

30

FORMATS OF PURCHASE

PURCHASE ORDER

Our Older No.

M/s..

Date

YOllIRef. No.

Date

Please supply the under-mentioned goods to our works S'Ilbject to corditioim overleaf:

Sr. No. Description Quantity Per Rate Value

-

- --

Excise: MST/CST.

Octroi: Freight

Delivery:

Payment Terms:

Remarks

31

PRUCHASE INDENT

Purchase Indent I~o,: Date:

Please Puchase the following materials for

Sr. No. Description Code

Qty. Reqd. WhenR.eqd

.

Stock on Avg. COllSU- Previo1lS rate

hand mption & OMel'llo.

-

•

Route

.

Inducted By Stores Purchase

32

QUOTATION

BILL OF MATERIAL

STORES ORGANIZATION

Normally substantial amount of company's working capital is invested in stores. Due attention

should be given to stores routine. There should be system of proper accounting of materials and

supplies and it should be given same attention as is given to accounting for money. Raw

materials and supplies are equivalent of cash. They form an important part of manufacturing

Material Code No. A.B.C.&Co. Date

Specimen of quotations File No.

Name of Minimum qty Rate per unit Time of delivery Terms of delivery Otberterms

supplier offered

Desc.

El-O-Matic (India) Pvt. Ltd. Bill OF MATERlAL Main Assly. Pune No.

Sheet No.

Sr. Drawing Description QtyfSet Source Material Reqd. Qty. Stock Stock

No No. Code For Regd. on Short- * (Sets) * Hand * age *

ICHD.BY IDATE I APPR.BY I DATE

33

M/s. G RR NO. &. Date

D. C. NO. &. Date

P. O. NO. &.Date

The following material(s) have been received and inspected as per details below:

Sr. Part Description &. Part No. Receipts Inspection Results

No.

As Per Actually Acce- Rew- Reed Under challan received pted ork with-

out op devia- op. tion

0

- -, -

Vendor/Customer I Accounts Stores I Planning I Sub Cont.

Receipt Purchas

e ,

and it is essential that they should be safeguarded and accounted for properly.

TYPES OF RAW MATERIAL

a. Raw Material Stores: -

It is the store where in incoming raw material, which directly contributes to the final

product, is received, stored and issued to the production department at various stages.

b.Engineering Stores:

In this store, materials required of running of plant, which do not directly contribute as a part

of finished product, are stored. Machinery spares, consumables, stationery etc. are stored in

this and issued as per requisitions raised by various users.

c. Finished Goods Stores:

It is the place where the finished products are stored after production and are ready to

dispatch to the respective locations or warehouses.

34

FUNCIONS OF STORES DEPARTMENT

In the company, the duties or functions broadly cover three types - physical task of storing and

preserving material, technical job of providing storing facilities and administrative procedure

for documentation and accounting of material movements. Referring to a full - fledged

storehouse of Technocrat Engineers the following duties and function can be enlisted.

1. Classification and codification of numerous materials by using suitable method of

codification is done in the stores. Then the manual of material - codes is circulated

among store staff and other concerned department managers.

2. The stores department takes physical charge of the material forwarded by goods

receiving and inspection section and places them in the respective bin.

3. The stores department provides necessary facilities for preserving the quality of

materials as long as they are in its custody.

4. It examines that issue procedure is properly followed by confirming the materials

supplied to production department only against written formal request/demand by

authorize through document material requisition note.

5. It keeps watch on actual stock level and compares the same with pre-set stock

limits (Maximum, Minimum, Reordering etc.) so that stock moves within limits.

6. Department prepares purchase requisition note for getting replenishment of stock

when actual quantity reaches reordering level.

7. The department carryout a regular review of stock for slow and fast moving

materials, damaged and substandard materials and reports such facts to top

management.

8. It ensures that correct accounting entries are entered in stock register and records for

each transaction like receipt, issue, return to supplier return from shop floor.

9. It arranges for all type of information and data required by top management and

other concerned officers, specially keeping ready the details of stock position /

balances.

10.The stores department undertakes physical verification (stock taking) for reconciling

actual balance with the book balance and identifying discrepancies, if any, with

possible causes for the same.

STORES DOCUMENTS AND RECORDS

Importance of stores documents & records:-

The stores department is all the time expected to give latest information about stock

balance, movement of the materials, and condition of the material. Such reporting has to be

based on some authentic source and hence, the stores and other concerned departments -

purchase, production, costing have to record their instructions, actions, decisions by using

well designed documents and registers. The store keeper is primarily held answerable for

each and every internal movement of materials, particularly for the stock under his custody.

Proper safeguarding and identification of materials should be done by the storekeeper.

STORES ACCOUNTING RECORDS

There are two basic records of inventory control viz. Bin Cards maintained by store keeper and

store ledger accounts kept by costing department. It is the parallel accounting exercise based

on same facts, recording same transaction i.e. movements of materials. Simultaneously posting

of same entries in two independent sets of accounts offers facility of reconciliation, which in

turn acts as an effective tool of inventory control.

BIN CARDS:-A bin card is used by storekeeper to keep quantitative records for all the

items of materials and goods in his stores. This is a document maintained by store

keeper in his stores to assist him to control stock.

The format of the bin card is given below: A bin card is used for each material. Each

receipt, issue or return is recorded on the bin card in a chronological order and the latest

balance is shown after each receipt and issue. Bin card is hung up in a convenient place

outside the bin, rack or shelf. Bin cards are hung near the bins, so that they are readily

available for making entries as and when the goods are placed into the bin or taken out. All

bins racks or shelves, etc. should be numbered consequently in order to indicate their

location to the store keeper and his assistance. This numbering also serves to connect the

bin card with the bin, to which it belongs.

STORES LEDGER SYSTEM

It is kept in the costing department. The store ledger is generally maintained in the form of

loose leaf cards, because they can be removed and inserted easily. Each account in store

ledger represents an item of material. The format of store ledger is shown below: -

The store ledger provides a continuous record of material and stores, received, issued,

returned or transferred. It discloses the balance in hand both in quantity and value at any

point of time. It serves the management with the perpetual inventory record for necessary for

decision making. Material Receipt Report, Material Requisition, Material Return Note form

the basis for making entries in store ledger accounts. Entries made in the store ledger are

identical to those on bin cards except that money values are shown only in store ledger. It is

very important that store staff should have nothing to do with writing up of stores ledger

account, which should be written only by the staff of costing department.

Since both bin card and store ledger account are written up from the same basic document,

the quantity balance are shown by these records should agree. The reasons for discrepancies

bin balances fewer than two sets are due to such reasons as:

a. Failure to post a particular transaction

b.Wrong posting in store ledger account

c. Wrong casting

d.Theft and

e. Items placed in wrong bin.

To avoid the problem of disagreement, the two sets should be reconciled either continuously

over a period. For automatic reconciliation, store department sends the original documents to

the revised balance of bin card after its inclusion. Costing department watch that the balance of

bin card intimated with the original document is correct.

FORMAT OF STORE LEDGER

Store Ledger Account X.Y z. & Co

Material Maximum Stock

CadeNo: Minimum Stock

Bin No: Re-older Level

Unit: Ordering Qty

On:lered Reserved Received

Date Ref. Qty. Date Ref. Qty. Date ORNote Qty. Rate Value

Issued Stock Stock verified

SrNo. Qty. Rate Value Qty. Rate Value Date Initials Remks.

CLASSIFICATION OF MATERIALS

MEANING

A manufacturing or a servicing organization generally requires large number of items.

Handling of such items - planning, procurement, storage, and accounting - becomes difficult if

each one of them is handled separately. Some sort of classification, therefore, is a must since

concentration of effort according to class system is more efficient and effective compared to

diluted effort corresponding to individuals.

DEFINITION

Classification of the materials is the process of grouping of items into few categories,

according to some criteria. Since an item can be placed into more than one class depending

upon the criteria used, some sort of formal classification, therefore, is a must.

OBJECTIVE OF CLASSIFICATION

Classification of materials is required to-

Evolve procedures of planning and control of materials in a class.

Decide systems of storage and issue of materials in a class.

Devise accounting and evaluation procedures common to all materials in a class.

BASIS OF CLASSIFICATION

Materials can be classified either on the basis of-

1. Stage of conversion process

2. Nature of materials

3. Usability of materials

1. CLASSIFICATION ON THE BASIS OF CONVERSION PROCES:

In a manufacturing organization, store materials can be classified broadly into direct materials

and indirect materials.

2. CLASSIFICATION ON THE BASIS OF NATURE OF MATERIALS:

It can be classified into following categories:-

Raw materials-

Raw materials are the basic materials which have not undergone any conversion since their

receipt from suppliers. They are the basic materials from which company’s parts/products are

manufactured.

Raw materials are further classified into;

a. Direct materials

b. Indirect materials

Consumables -

Consumables are the materials which both cease to exist or change their shape during

the manufacturing process and as such cannot be used for the second time. Examples of

consumable items are coal, coke, lubricants, cotton waste and stationery items.

Chemicals -

Chemicals are the substances in the form of powder, liquid, tablets etc. that undergo

certain process according to a devised formula. They require be storing, preserving and

issued very cautiously after a careful scrutiny since they involve risks. Examples are

chemicals like acids.

Inflammable items -

Inflammable items are the materials which are highly susceptible to fire. Being

hazardous, they require being stored farther from the main store with complete fire-

fighting equipment as standby.

Furniture-

Furniture is the movable items of a house or a place. It requires large storage space,

careful handling and maintenance of proper records of their repairs, renewals and

replacements.

Perishable materials -

Perishable materials are the materials which are short lived and decay easily. Such

materials require being stored in temperature controlled rooms to prolong their life.

Packaging -

Packaging materials are the materials including wrapping materials, protective coating

and containers.

Empties-

Empties are the used packages, which have been scrapped after use. Examples are

wooden cases, metal containers and glass wares.

Supplies-

Supplies include materials used up in running of the plant or in the making of

company's products but do not themselves to into the product.

3. CLASSIFICATION ON THE BASIS OF USABILITY OF MATERIALS:

Serviceable and Unserviceable Material-

Serviceable materials are the items, which have gone temporarily out-of-order and can

be put back into use after repairs.

Unserviceable materials are the items, which have outlived their life or gone out-of-

order permanently or damaged so badly that they cannot be repaired or their repair is

economically inadvisable.

• Semi- Finished and Finished Materials -

Semi- Finished materials are items in the partially completed condition of manufacture

and need some further processing before they are ready for sale/shipment to the

customer. Finished materials on the contrary are the items which have been

manufactured in complete form by the production department and are ready for sale.

• Dead Stock Items -

Dead stock items also called capital equipment are the furniture, office equipment,

material handling equipment, machinery, tools and other items which have definite life

and cannot be written off before the expiry date of their life.

Obsolete Items

Obsolete items are the items, which have gone out of date because of new invention in

design, use, etc. and therefore cannot profitably be used.

IDENTIFICATION OF MATERIALS

MEANING

Identification is the tracing of the part description, or part number including size, material of

construction, source of supply, batch number etc.

Proper identification is necessary to

Ensure issue of correct items

Sort out mix up of materials of same size of different specifications

Track identity of the batch number through different stages of operations.

Identify source of supply for the material accepted initially but found defective

during processing.

Differentiate items manufactured/procured to current and obsolete drawings.

METHODS OF INDENTIFYING MATERIALS

• Tagging or Labeling - Identification tags, made of paper board or tin plate can be either kept

along with items or affixed on the item itself .

• Writing or Plating - Identification details can be written on the cartons or drums or items in

ink, glass making crayons, paints etc.

Engraving- Vibrating marking tools can be used to engrave identification details.

• Etching - Stamping operation may not desirable on certain components. Chemicals may etch

code number in such items.

• Colour Coding - Raw materials/rubber parts in different specifications may be identified by

colour codes.

CODIFICATION

MEANING

An important factor concerning indenting, purchasing and issuing activities is an accurate and

logical identification of materials. Wrong identification results in wrong purchases and/or

issuance of a different item than what is intended. Codification systems too are not perfect but

codes are shorter and as such minimize errors.

Example: LIC has a wide clientele and to identify a client by his/her name, if it is not entirely

impossible it is certainly very difficult, since there can be several persons with the same names

and perhaps with the same surnames or initials. LIC, therefore, identifies its policyholders by

policy numbers consisting of numerals.

DEFINITION

Codification in an industry is the systematic concise representation of equipment, raw

materials, tools, spares, supplies etc. in an abbreviated form employing alphabets, numerals,

colors, symbols etc.

BENEFITS OF CODEFICATION

• Accurate and logical identification -

Correct quality descriptions are necessary to ensure that items are indented, purchased, stocked

and issued correctly. Codification makes it possible since each item is assigned a unique code

after due considerations to its group, kind, size, specifications and dimensional characteristics.

• A voidance of long and unwieldy descriptions

• Prevention of duplication

• Product simplification (variety reduction)

• Efficient storekeeping

• Accurate and reliable recording and accounting

• Easier computerization

TECHNIQUES OF INVENTORY MANAGEMENT

[A] FIXATION OF LEVELS

[B] SELETIVE €ONTROL OF INVENTORIES

A-B-C ANALYSIS

X-Y-Z ANALYSIS, etc.

[C] JUST - IN- TIME (JIT)

.[D] ANALYSIS OF INVESTMENT IN INVENTORY

[A] FIXATION OF THE LEVELS

The basic objective behind fixation of these levels is to avoid overstocking and

understocking. In addition to this one more level of inventory takes care that orders are to

be placed only when a particular level is reached. These levels are explained below:

1. RE-ORDER LEVEL:

This level is that level of material, at which when the inventory is reached, fresh

orders are placed. While fixing the re-order level

a. Maximum consumption

b. Maximum delivery time or lead-time should be taken into consideration.

Mathematically the re-order level can be worked out as under:

2. MAXIMUM LEVEL:

This is the highest level of inventory to be maintained above which the inventory

should not rise. While fixing the maximum level, factors like minimum

consumption, minimum re-order period as well as the re-order quantity is to be

taken into consideration. Other factors like storage space, interest on capital blocked

in inventories is also taken into consideration. The formula for calculating

maximum level is as follows:

Maximum level = Re-order level- [Minimum usage * Minimum delivery time] +

Reorder-quantity

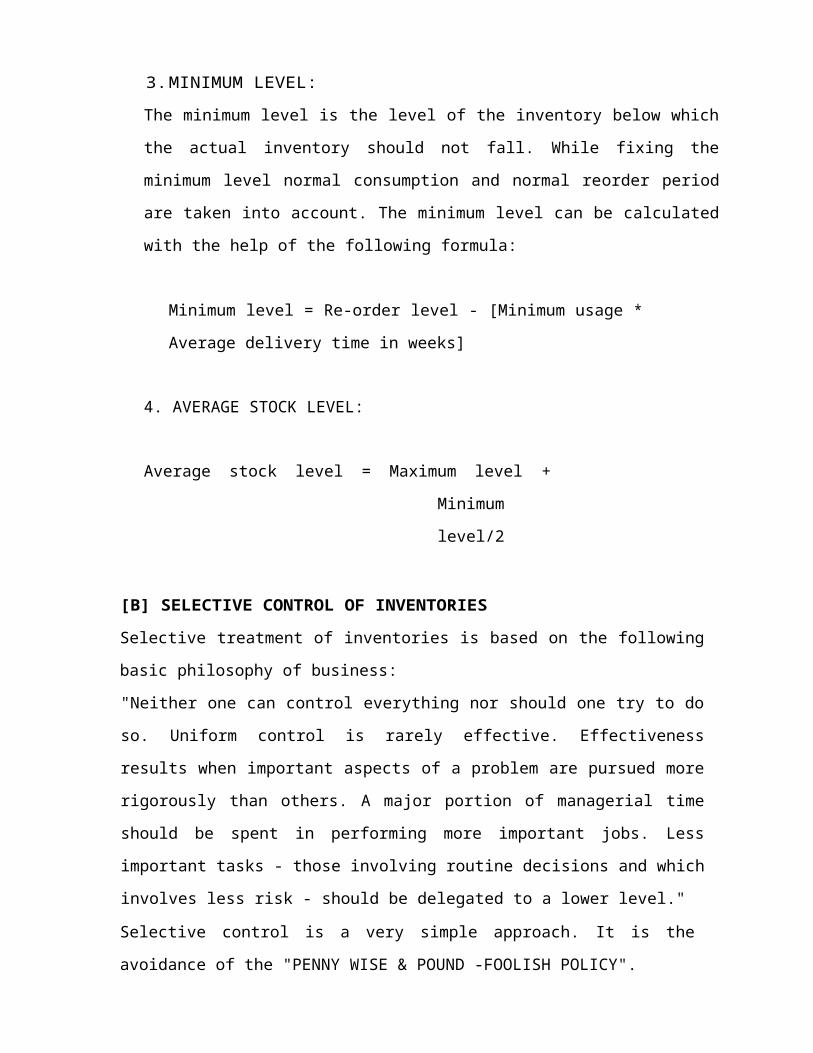

3. MINIMUM LEVEL:

The minimum level is the level of the inventory below which the actual inventory should

not fall. While fixing the minimum level normal consumption and normal reorder period

are taken into account. The minimum level can be calculated with the help of the

following formula:

Minimum level = Re-order level - [Minimum usage * Average delivery

time in weeks]

4. AVERAGE STOCK LEVEL:

Average stock level = Maximum level + Minimum level/2

[B] SELECTIVE CONTROL OF INVENTORIES

Selective treatment of inventories is based on the following basic philosophy of business:

"Neither one can control everything nor should one try to do so. Uniform control is rarely

effective. Effectiveness results when important aspects of a problem are pursued more

rigorously than others. A major portion of managerial time should be spent in performing

more important jobs. Less important tasks - those involving routine decisions and which

involves less risk - should be delegated to a lower level."

Selective control is a very simple approach. It is the avoidance of the "PENNY WISE &

POUND -FOOLISH POLICY".

THE ABC CLASSIFICATION:-

ABC analysis is a selective control technique which is required to be applied when we want to

control value of consumption of the item in rupees obviously when we want to control value of the

consumption of the material we must select those materials where consumption is very high. The

ABC classification system is to grouping items according to annual sales volume, in an attempt to

identify the small number of items that will account for most of the sales volume and that are the

most important ones to control for effective inventory management. ABC analysis is a system in

inventory management to minimize the cost of inventories incorporated in which are stored for long

time, these are classified into ABC groups whereas A stand for the most expensive inventories which

are purchased on customers demands so that it can be processed & then given to them on priority

basis, these items are carefully selected. B is classified for those goods which are less expensive than

A items in which can be stored for some time before it is processed and goes for those items which

are cheap in also can be abundantly used. These are items where its loss won’t cost much to the

company. ABC is class of inventory item.

A is the most important and the most expensive- under a ABC regime for minimum stock value A

should be managed by JFT since-its value makes this close management cost-effective

B are intermediate and medium expensive- .under a ABC regime for minimum stock value B

should be managed by Kanban pulling- the micromanagement by JIT is not cost effective for this

project but it should still be tracked methodically.

C are low value items- under an ABC regime for minimum stock value C should be managed by 2

bin- whereby two huge bins of (e.g. screws) item are kept and one is used at a time- when one runs

out another is ordered and the next bin is used. The low value does not justify management- and any

downtime because of running out would cost much more than the product itself.

In an analysis it is decided which products are A, B or C and exactly how they will be managed. In

any company manufacturing, there are number of items which are consumed or traded it may run

into thousands. It is found after number of studies of different companies that –

On the basis of above analysis these items are termed as ABC items as detailed below:

A-items- these are those items which are found hardly 5%--10% but their consumption may

amount 70%--75% of the total money spend on materials.

B-items-these are those items which are generally 100/0--15% of he total items and their

consumption amounts to 10%--15% of the money spend on the materials.

C-items-these are large number of items which are cheap and inexpensive and hence

insignificant. They are large in number s running into hardly 5%--10% of the total money

spends on materials.

Based on the above analysis decision can then be taken as to-

How to control the consumption value (rupees) and bring it down.

Value of consumption of No. of items Grade

items (value in Rs).

70% of consp. 10% of no. of items A

20% of consp. 15% of no. of items B .

10% of consp. 75% of no. of items C

CONTROL PEOCEDURE ARE GIVEN BELOW:-

A-items-someone at senior level must be made responsible to regularly review the consumption of

overseas items up to date and accurate records should be maintain for this items. The inventory of

these items must be minimum and the orders for these items should be staggered. So that timely

arrival of these items is insured attempt must be made to reduce internal and external lead-time of

these items. Safety stocks of these items should be minimum because frequency of ordering this

items are kept high, price discount for this items should not be avail because physical ordering is

very frequent.

B-item-this items should be kept under normal control and goods report keeping must be maintain.

Safety stock of these items can be moderate. Price discount can be avail and physical stocktaking

can also be moderate.

C-items-little control is required for c-items and the job of controlling should be left lower level

people such as those in charge of store. Large quantity or inventories can be maintain these stock

because they are cheap, so as to avoid stock out situation these items should not kept under lock and

key and must be kept at convenient places open to all for uses safety. Stock of these items can be

sufficient to avoid probability. Price discount can be avail to purchase in bulk quantity because they

are cheap. Physical checking of the stock can be done rarely once in six months.

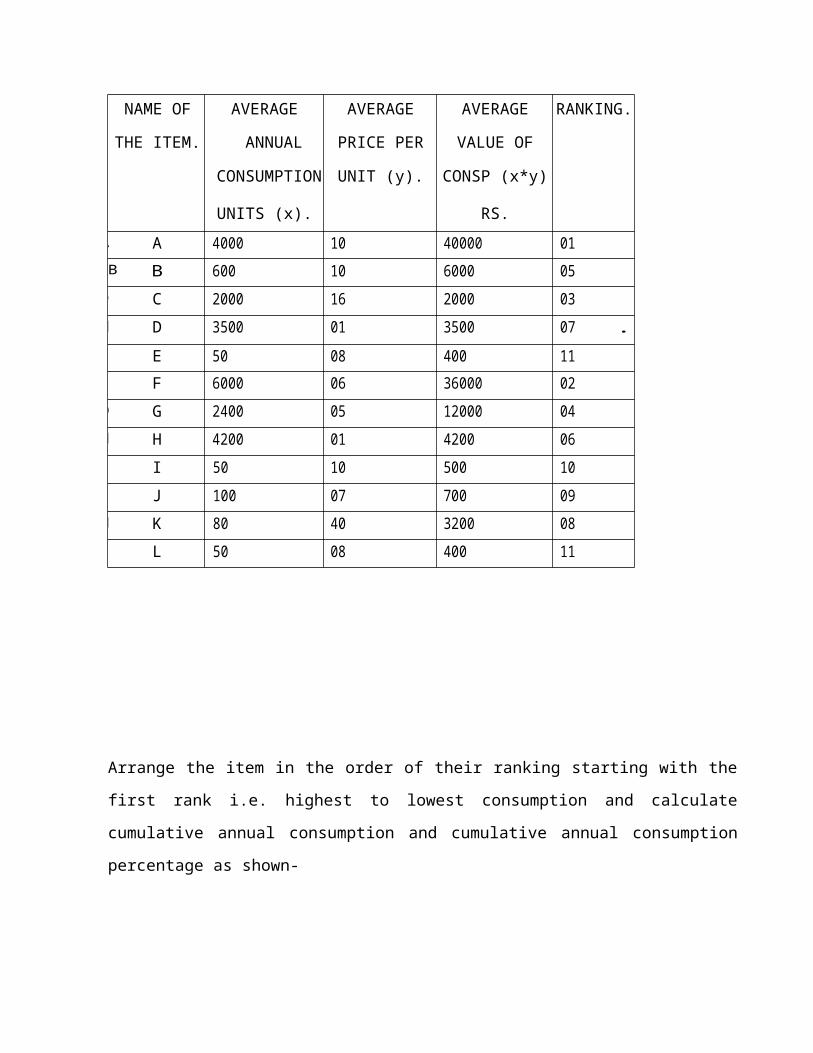

HOW TO CARRY OUT ABC ANALYSIS:

It is better to go through records of the stores for number of years and find out names of all items

consumed during the year, their average yearly consumption in units and average price per unit is

also found out as shown-

NAME OF AVERAGE AVERAGE AVERAGE RANKING.

THE ITEM. ANNUAL PRICE PER VALUE OF

CONSUMPTIONUNIT (y). CONSP (x*y)

UNITS (x). RS.

A A 4000 10 40000 01

B B 600 10 6000 05

C C 2000 16 2000 03

D D 3500 01 3500 07 .

E E 50 08 400 11

F F 6000 06 36000 02

G G 2400 05 12000 04

H H 4200 01 4200 06

I 50 10 500 10

J 100 07 700 09

K K 80 40 3200 08

L L 50 08 400 11

Arrange the item in the order of their ranking starting with the first rank i.e. highest to lowest

consumption and calculate cumulative annual consumption and cumulative annual consumption

percentage as shown-

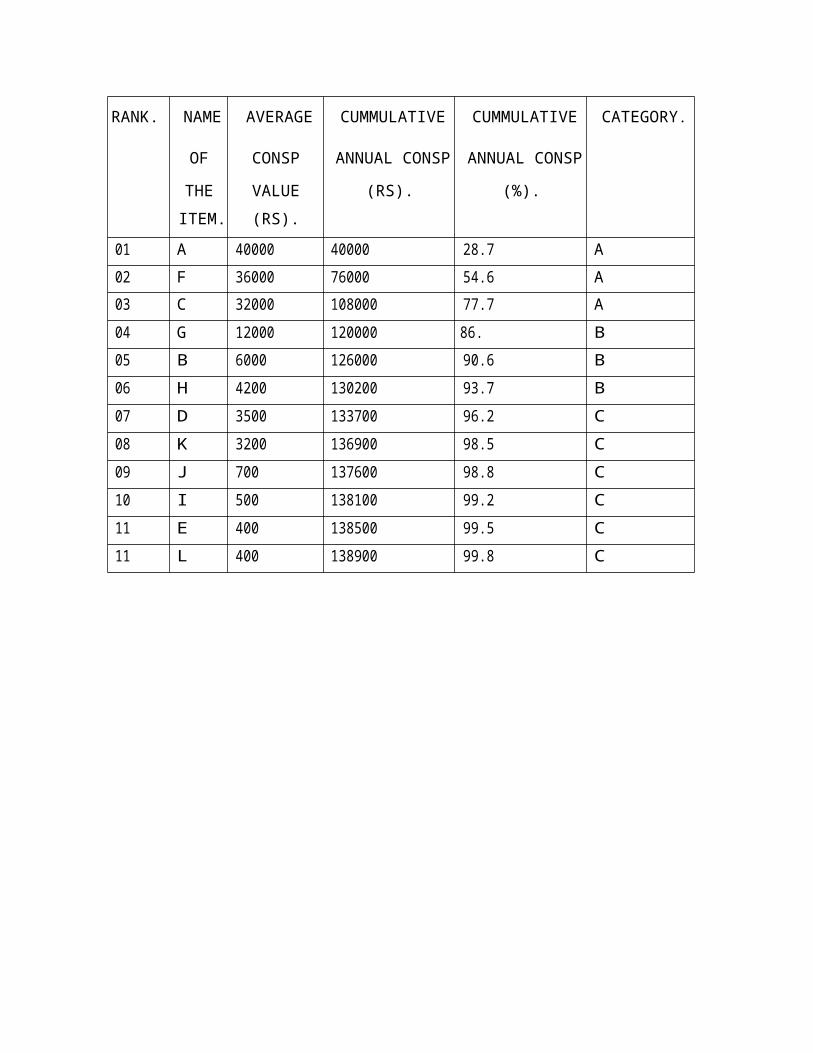

RANK. NAME AVERAGE CUMMULATIVE CUMMULATIVE CATEGORY.

OF CONSP ANNUAL CONSP ANNUAL CONSP

THE VALUE (RS). (%).

ITEM. (RS).

01 A 40000 40000 28.7 A

02 F 36000 76000 54.6 A

03 C 32000 108000 77.7 A

04 G 12000 120000 86.3 B

05 B 6000 126000 90.6 B

06 H 4200 130200 93.7 B

07 D 3500 133700 96.2 C

08 K 3200 136900 98.5 C

09 J 700 137600 98.8 C

10 I 500 138100 99.2 C

11 E 400 138500 99.5 C

11 L 400 138900 99.8 C

XYZ Analysis

X- Y -Z analysis is based on value of the stocks on hand. Items whose inventory values are high

are called X items while those whose inventory values are low are called Z items. And Y items are

those which have moderate inventory stocks. This type of analysis is carried out from the point of

view of value of balance stocks lying in the stores from time to time and classifies all the items as

given below.

‘X’ items are those items whose value of balance stock lying in the stock is very high.

'Y' items are those items whose value of balance stock is moderate.

'Z' items are those items whose value of balance stock lying in the stocks is very low.

After- knowing this type of classifications and their items can be taken to control the situation as

shown below:

1] From security point of view high value items must be stored and kept under lock and key or if

not possible they should be kept in such a way that they are always under supervision. Similarly

arrangement can be made for y and z items accordingly.

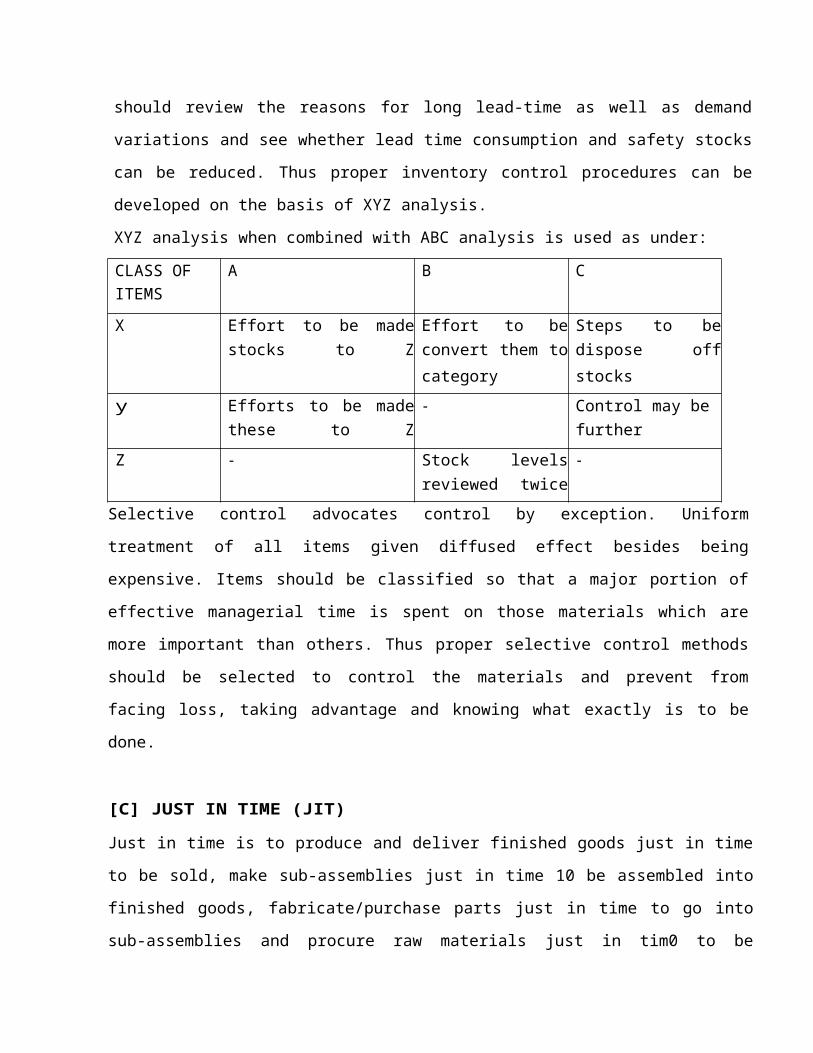

2] From inventory control point of view we must know why there is high inventory for 'X' items.

We should review inventory control procedure for each and every high item because stock should

be maintained to take care of lead-time consumption and also to provide safety stocks. For high

value items lying in stores we should review the reasons for long lead-time as well as demand

variations and see whether lead time consumption and safety stocks can be reduced. Thus proper

inventory control procedures can be developed on the basis of XYZ analysis.

XYZ analysis when combined with ABC analysis is used as under:

CLASS OF A B C

ITEMS

X Effort to be made reduce Effort to be made to Steps to be taken to

stocks to Z category convert them to Y dispose off surplus

category stocks

y Efforts to be made convert - Control may be

these to Z category. further tightened

Z - Stock levels may be -

reviewed twice a year

Selective control advocates control by exception. Uniform treatment of all items given diffused

effect besides being expensive. Items should be classified so that a major portion of effective

managerial time is spent on those materials which are more important than others. Thus proper

selective control methods should be selected to control the materials and prevent from facing loss,

taking advantage and knowing what exactly is to be done.

[C] JUST IN TIME (JIT)

Just in time is to produce and deliver finished goods just in time to be sold, make sub-assemblies just

in time 10 be assembled into finished goods, fabricate/purchase parts just in time to go into sub-

assemblies and procure raw materials just in tim0 to be transformed in to fabricated parts. JIT is a

complete business philosophy and the process of thinking, working and managing to eliminate

waste. TOYAT A, the originator of the JIT concept, defines waste as "anything other than minimum

amount of equipment, materials parts and working time absolutely essential to production."

OBJECTIVES:

1. Elimination of wastage in its many forms

2. Belief that ordering/holding cost can be reduced

3. Reduction in equipment lead time

4. Adjustment in the fluctuations in supply of material

5. Enhancement of quality

IMPLEMENTATION OF JIT CAN LEAD TO THE FOLLOWING BENEFITS TO THE

USER

Reduction in manufacturing lead time

Defects free production

Lower inventory investment

Greater conformance to delivery commitment

Lesser cost of production

Faster response to market needs

Improved morale of the work force.

TECHNIQUES OF JIT

Set up time reduction

JIT machining cells

JIT layout

The pull system (The Kanban system of production control)

Just in time purchasing

Quality at source

Employee involvement.

[D] ANALYSIS OF INVESTMENT IN INVENTORY

One of the major areas of decision - making for a finance manager is the investment decisions in

inventory. In the inventory, a large portion of the funds of a firm are invested. Therefore, whenever

a change in the inventory level is to be made, the profitability of such change should be found out.

In other words, the inventory policy of a firm will maximize the value of the firm at such point

where the incremental return from investments in inventory is either equal to or more than the

incremental cost of funds used for financing inventory.

DATA ANALYSIS

LIST OF PHYSICALLY CHECKED INVENTORY:

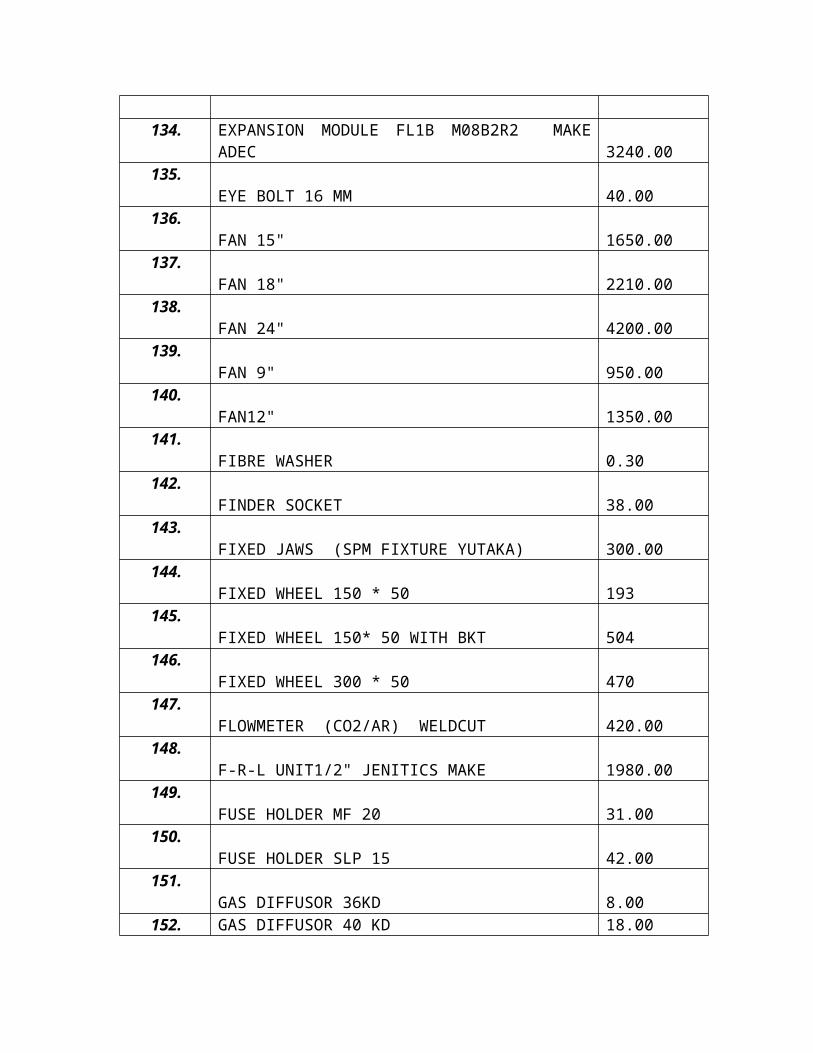

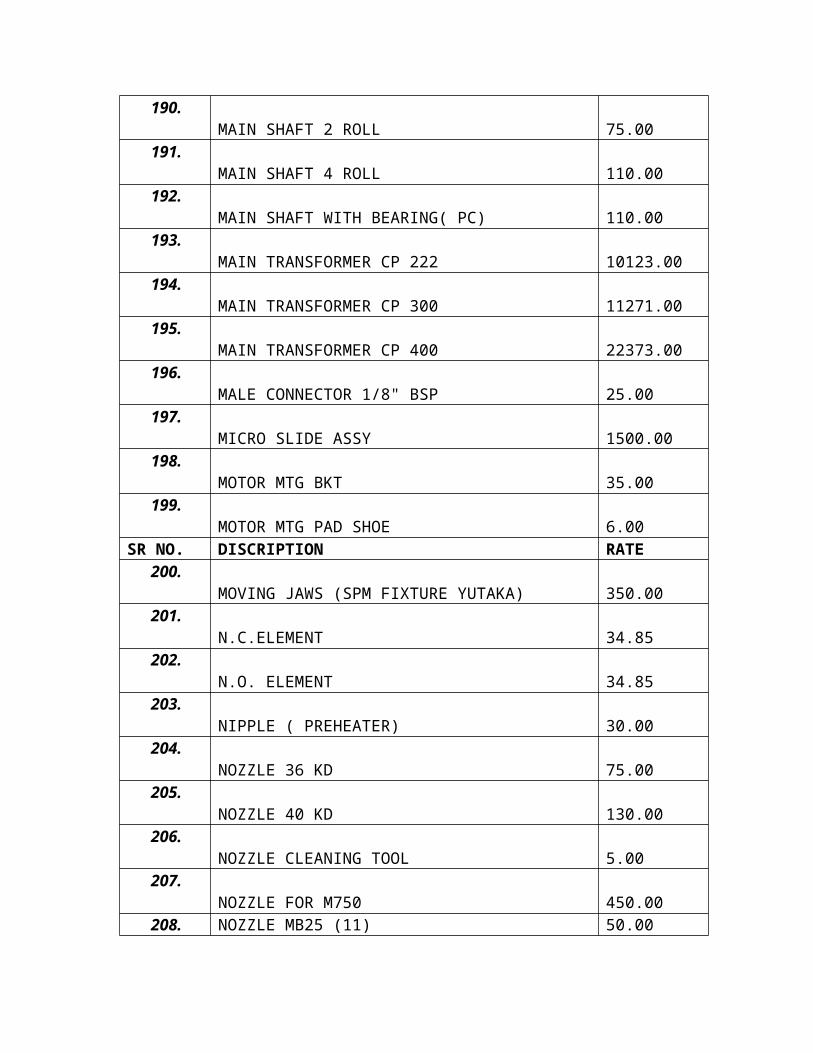

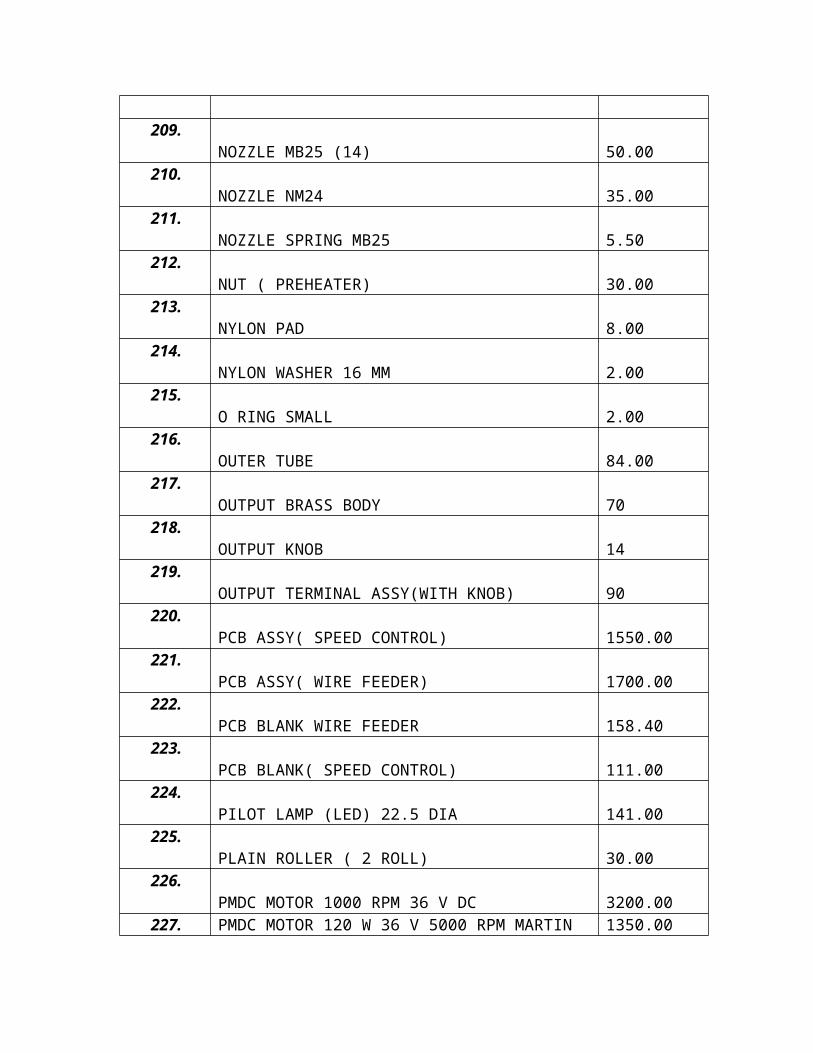

The lists of inventories in accordance with above mentioned categorization were procured from the management information system/electronic data processing department. The format is shown as below:

REVIEW OF ALL THE ITEMS AT THE STORE:

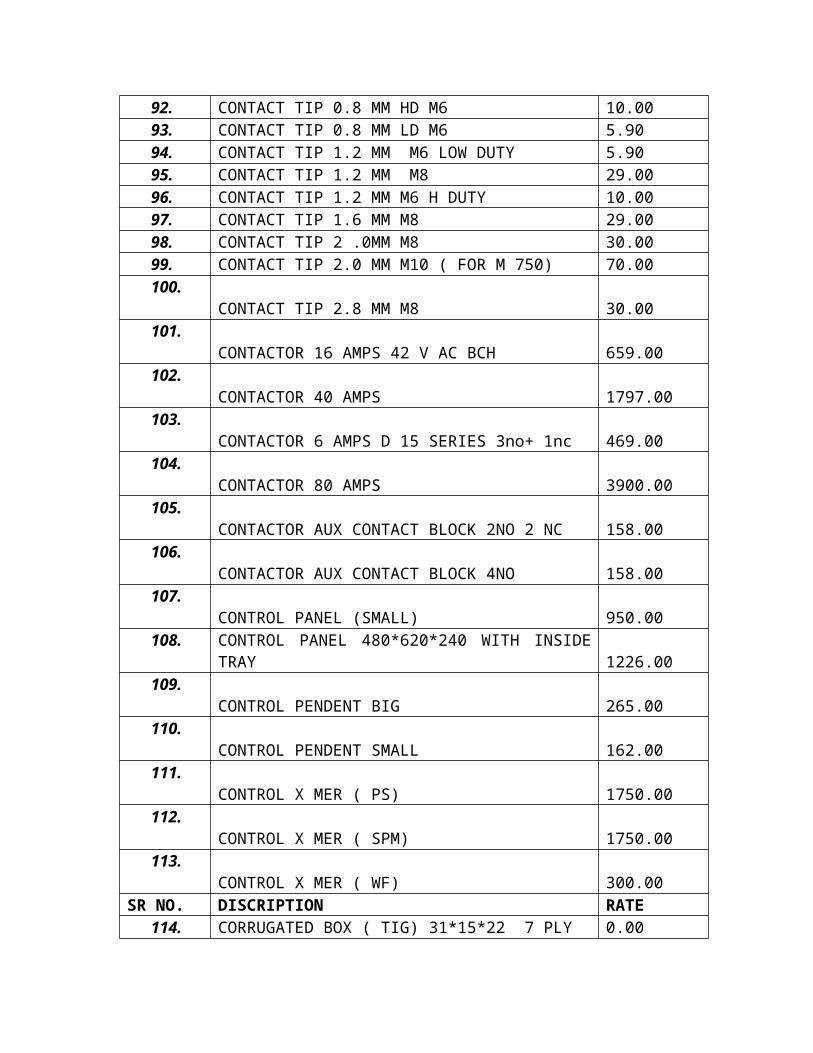

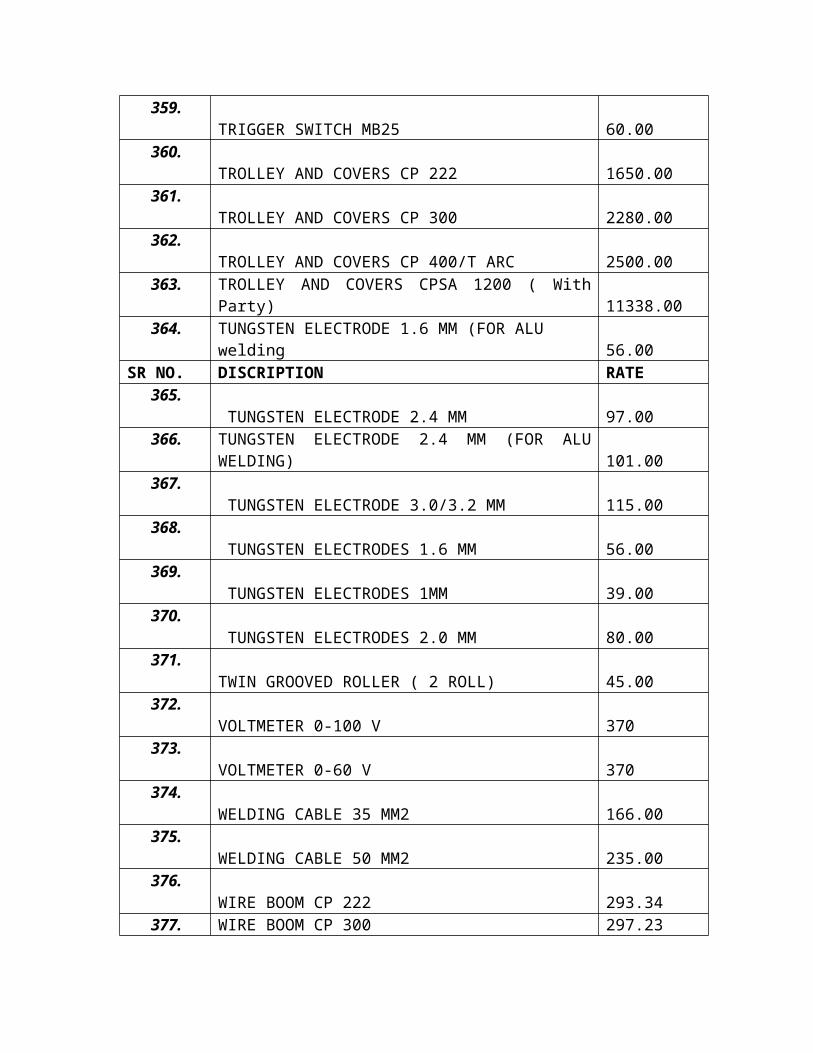

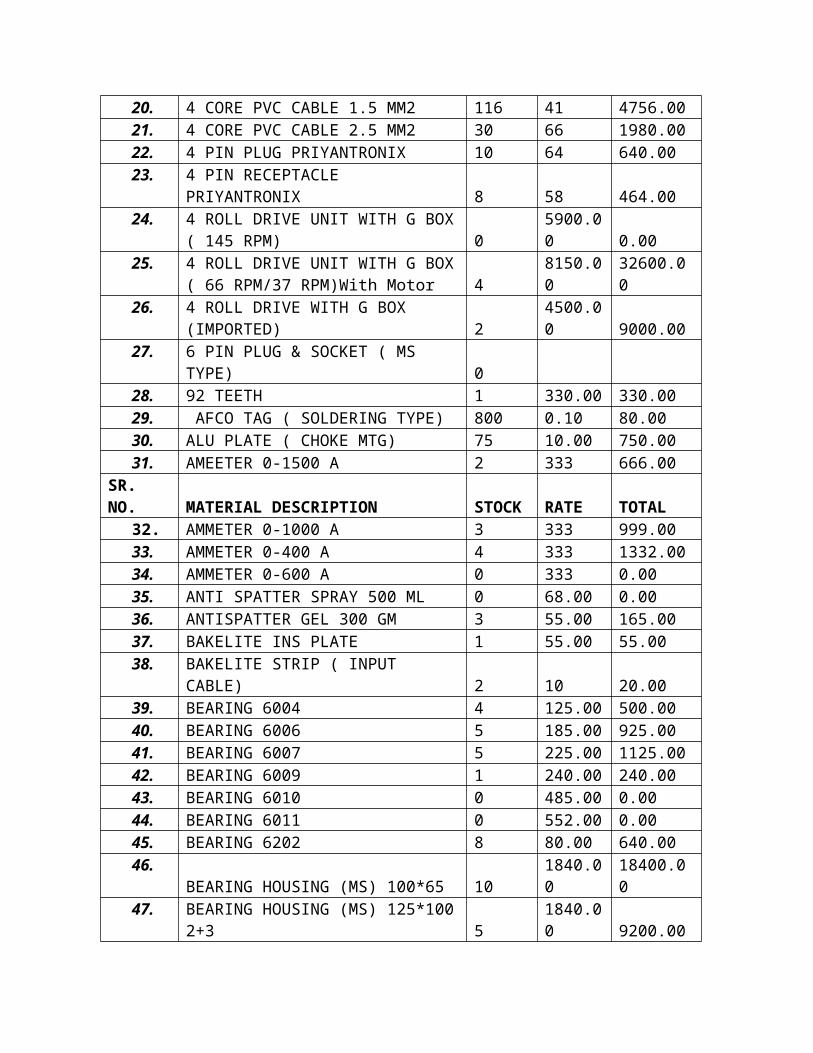

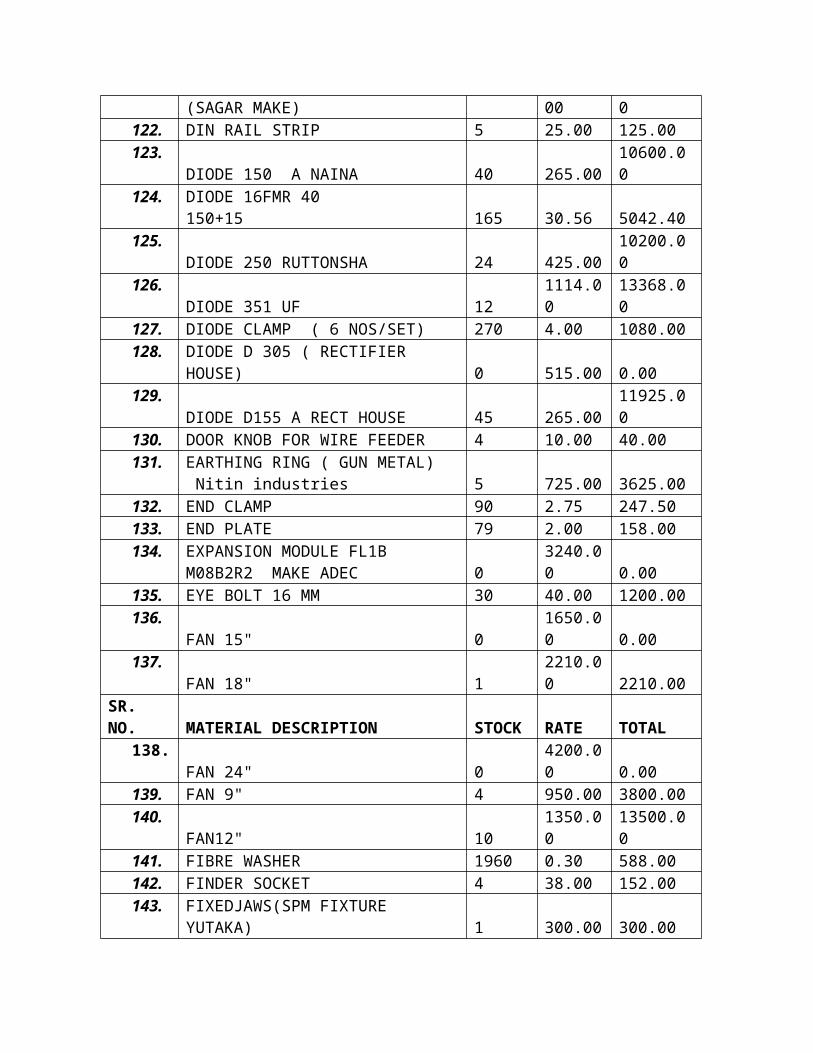

SR NO. DISCRIPTION RATE1. 1 CORE PVC CABLE 16 MM2 89.002. 1 CORE 1 MM2 BLACK 5.893. 1 CORE 1 MM2 BLUE 5.894. 1 CORE 1 MM2 GREEN 5.895. 1 CORE 1 MM2 GREY 5.896. 1 CORE 1 MM2 ORANGE 5.897. 1 CORE 1 MM2 RED 5.898. 1 CORE 1 MM2 WHITE 5.899. 1 CORE 1 MM2 YELLOW 5.8910. 10 PIN PLUG PRIYANTRONIX 30311. 10 PIN RECEPTACLE PRIYANTRONIX 29312. 2 CORE PVC CABLE 1.5 MM2 2413. 2 ROLL DRIVE WITH G BOX ( 250 RPM) 1850.0014. 2 ROLL DRIVE WITH G BOX ( IMPORTED) Geared

roller 3100.0015. 2 ROLL DRIVE WITH G BOX ( IMPORTED) Plain

roller 3100.0016. 3 CORE PVC CABLE 1.5 MM2 3117. 3 PIN PLUG & SOCKER MS TYPE 10818. 3 PIN PLUG PRIYANTRONIX ( TORCH) 5919. 3 PIN RECEPTACLE PRIYANTRONIX (WF/PS) 5520. 4 CORE PVC CABLE 1.5 MM2 4121. 4 CORE PVC CABLE 2.5 MM2 6622. 4 PIN PLUG PRIYANTRONIX 6423. 4 PIN RECEPTACLE PRIYANTRONIX 5824. 4 ROLL DRIVE UNIT WITH G BOX ( 145 RPM) 5900.0025. 4 ROLL DRIVE UNIT WITH G BOX ( 66 RPM/37

RPM)With Motor 8150.0026. 4 ROLL DRIVE WITH G BOX (IMPORTED) 4500.0027. 6 PIN PLUG & SOCKET ( MS TYPE)28. 92 TEETH 330.0029. AFCO TAG ( SOLDERING TYPE) 0.1030. ALU PLATE ( CHOKE MTG) 10.00

SR NO. DISCRIPTION RATE31. AMEETER 0-1500 A 33332. AMMETER 0-1000 A 33333. AMMETER 0-400 A 33334. AMMETER 0-600 A 33335. ANTI SPATTER SPRAY 500 ML 68.0036. ANTISPATTER GEL 300 GM 55.0037. BAKELITE INS PLATE 55.0038. BAKELITE STRIP ( INPUT CABLE) 1039. BEARING 6004 125.0040. BEARING 6006 185.0041. BEARING 6007 225.0042. BEARING 6009 240.0043. BEARING 6010 485.0044. BEARING 6011 552.0045. BEARING 6202 80.0046. BEARING HOUSING (MS) 100*65 1840.0047. BEARING HOUSING (MS) 125*100 2+3 1840.0048. BEARING HOUSING 100MM DIA*125 MM LONG 960.0049. BK WASHER AND BUSH ( FOR O/P TERMINAL) 1350. BK WEDGES ( FOR CHOKE) 5.0051. BOBBIN NO 13( 2 NOS/SET) 4.0052. BOBBIN NO 7 ( 12 NOS/SET) 7.0053. BRASS NIPPLE ( GAS HOSE) 12.5054. BRASS NIPPLE 3/8" * 1/8" 20.0055. BRASS NUT (GAS HOSE) 12.5056. BRUSH HOLDER ASSY WITH OUT BRUSH 20* 40 600.0057. BRUSH HOLDER ASSY Without BRUSH(8*10) V

TYPE Small 180.0058. C TYPE STRIP 18.0059. C.S.T 2.5 TERMINAL 7.0660. CAPACITOR 0.1 MFD 630V ( 6 NOS/SET) 7.0061. CARBON BRUSH 20*40 225.0062. CARBON BRUSH FOR MARTIN MOTOR 25.0063. CARBON BRUSH V 8*10 (SMALL) 75.0064. CARTRIDGE (WITH SEALING RING) 159.0065. CEBORA TIG 1565 IMPORTED 90000.0066. CERAMIC NOZZLE 2410640/WG2411 22.1067. CERAMIC NOZZLE 2411040 /WG2413 22.1068. CERAMIC NOZZLE 2461036/WG2463 22.1069. CERAMIC NOZZLE SAP 10 N 47 32.0070. CERAMIC NOZZLE SAP 10 N 48 32.0071. CHOKE BLOCK 63* 63* 180 MM (Duly drilled &

tapped) 300.0072. CHOKE CP 300 1872.00

SR NO. DISCRIPTION RATE73. CHOKE CP 400 3710.0074. CHOKE MTG ANGLE 10.0075. CHUCK PLATE 300* 16 MM 650.0076. CO2 WELDIN G TORCH RB 61 GD RGZ-2 3 MTR 12000.0077. CO2 WELDING TORCH 36KD 3250.0078. CO2 WELDING TORCH 40 KD (WITH 65 MM2 C/S

CABLE) 4800.0079. CO2 WELDING TORCH M/C MOUNTING NM24,0.75

mtr 1250.0080. CO2 WELDING TORCH NM24 2000.0081. CO2 WELDING WIRE 0.8 MM 15 KG SPOOLS TATA

MAKE 1020.0082. COLLET 1.6 MM SA26 10N23 27.0083. COLLET 2.0 MM SA 26 27.0084. COLLET 2.4 MM SA 26 27.0085. COLLET 3.2 MM SA26 27.0086. COLLET BODY 2.4 SA26 10N32 58.0087. COLLET BODY1.6 SA26 10N31 58.0088. COLLET GC 20 1.6 MM 26.0089. COLLET GC 20 2.0 MM 26.0090. COLLET GC 20 2.4 MM 26.0091. COLLET GC 20 3.0/3.2 MM 26.0092. CONTACT TIP 0.8 MM HD M6 10.0093. CONTACT TIP 0.8 MM LD M6 5.9094. CONTACT TIP 1.2 MM M6 LOW DUTY 5.9095. CONTACT TIP 1.2 MM M8 29.0096. CONTACT TIP 1.2 MM M6 H DUTY 10.0097. CONTACT TIP 1.6 MM M8 29.0098. CONTACT TIP 2 .0MM M8 30.0099. CONTACT TIP 2.0 MM M10 ( FOR M 750) 70.00100.

CONTACT TIP 2.8 MM M8 30.00101.

CONTACTOR 16 AMPS 42 V AC BCH 659.00102.

CONTACTOR 40 AMPS 1797.00103.

CONTACTOR 6 AMPS D 15 SERIES 3no+ 1nc 469.00104.

CONTACTOR 80 AMPS 3900.00105.

CONTACTOR AUX CONTACT BLOCK 2NO 2 NC 158.00106.

CONTACTOR AUX CONTACT BLOCK 4NO 158.00

107.CONTROL PANEL (SMALL) 950.00