CHAPTER ONE 1.0 INTRODUCTION 1.1 Background of the study We are in an era of considerable demands on public finances at all levels worldwide. As never before, public authorities are required to ensure that common resources are used in the most effective and efficient manner and that, essentials are targeted in the usage of resources, organizational planning and management (E.U Commission 2012). Besides, the growth in size and complexity of many companies in recent years, coupled with today’s numerous risk situations and public expectation of healthy risk assessment and evaluation have led to a corresponding increase in the need to establish effective internal control procedures. Additionally, new legal directives assert themselves in the domain of corporate governance of companies to control management decisions, define the role of independent committees, improve principles of corporate governance and set up and control internal control systems that are really effective in order to limit failures (Woolf, 1990). 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the study

We are in an era of considerable demands on public finances at

all levels worldwide. As never before, public authorities are

required to ensure that common resources are used in the most

effective and efficient manner and that, essentials are targeted

in the usage of resources, organizational planning and management

(E.U Commission 2012).

Besides, the growth in size and complexity of many companies in

recent years, coupled with today’s numerous risk situations and

public expectation of healthy risk assessment and evaluation

have led to a corresponding increase in the need to establish

effective internal control procedures. Additionally, new legal

directives assert themselves in the domain of corporate

governance of companies to control management decisions, define

the role of independent committees, improve principles of

corporate governance and set up and control internal control

systems that are really effective in order to limit failures

(Woolf, 1990).

1

The myriads of needs of the citizenry have led to the undertaking

and funding of several projects and programmes by government

through the Ministries, Departments, Agencies and Metropolitan

and district assemblies. This has led to much expenditures being

incurred in the Public Sector which warrants the need to ensure

economy, efficiency, effective and judicious use of public funds.

Treadway Commission (1994) defined internal control as a process,

effected by an entity’s board of directors, management and other

personnel, designed to provide reasonable assurance regarding the

achievement of objectives in effectiveness and efficiency of

operations, reliability of financial reporting and compliance

with applicable laws and regulations. The International

Organisation of Supreme Audit Institutions (2004) on the other

hand defined internal controls as an integral process that is

affected by an entity’s management and personnel and is designed

to address risks and to provide reasonable assurance that in

pursuit of the entity’s mission, the following general objectives

are being achieved: (1) executing orderly, ethical, economical,

efficient and effective operations; (2) fulfilling accountability

2

obligations; (3) complying with applicable laws and regulations;

and (4) safeguarding resources against loss, misuse and damage.

Effective Internal controls are series of actions that permeate

an entity’s activities. These actions are pervasive, and inherent

in the way management runs the business of an entity. It can

directly affect an entity’s ability to reach its goals and also

supports businesses’ quality initiatives. (Sarens De Visscher and

Van Gils, 2010)

1.2 Statement of the problem

In an era in which management and control of public finances

attracts national and international attention and scrutiny, it is

imperative that adequate and effective internal control and audit

systems are designed in such a way that they could contribute to

good governance and transparency (European commission PIC 2012).

Lots of funds from Donors and Government of Ghana (GOG) sources

as well as those generated internally by public institutions are

expended yearly by Public Institutions to finance Government

activities and projects. To ensure accountability, economy,

effectiveness, efficiency and also to evaluate organizational and

3

managerial performance, managers of state institutions account

for their stewardships to the citizens of Ghana, through Members

of Parliament who represent the citizenry through the Public

Accounts Committee (PAC) of parliament (The 1992 constitution of

Ghana).

Startling revelations of misapplication and misappropriation from

the sittings of the PAC of Parliament on the Auditor-General’s

report on Public Accounts are clear indication of existence of

weaknesses in controls and monitoring. The absence of, or weak

internal controls had been recognized as the primary cause of

various incidence of fraudulent entity financial reporting

(Treadway Commission Report 1987).

In order to address these weaknesses and ensure judicious and

economic use of funds for the intended purposes, it is imperative

that we examine and discuss whether existing internal controls

systems in the public sector are effective and are contributing

to good governance and transparency. It is in this light that

this study is being undertaken using Ashanti Regional Health

Directorate (ARHD) as a case study.

4

1.3 Objectives of the study

The general objective of this study is to ascertain the adequacy

and effectiveness of internal control systems in the Public

Sector taking the Ashanti Regional Health Directorate as a case

study. The specific objectives for the study are as follows:

1. To identify the types of internal controls in operations at

Ashanti Regional Health Directorate;

2. To examine the effectiveness of the internal controls at the

Regional Health Directorate

3. To examine the challenges in the internal control systems at

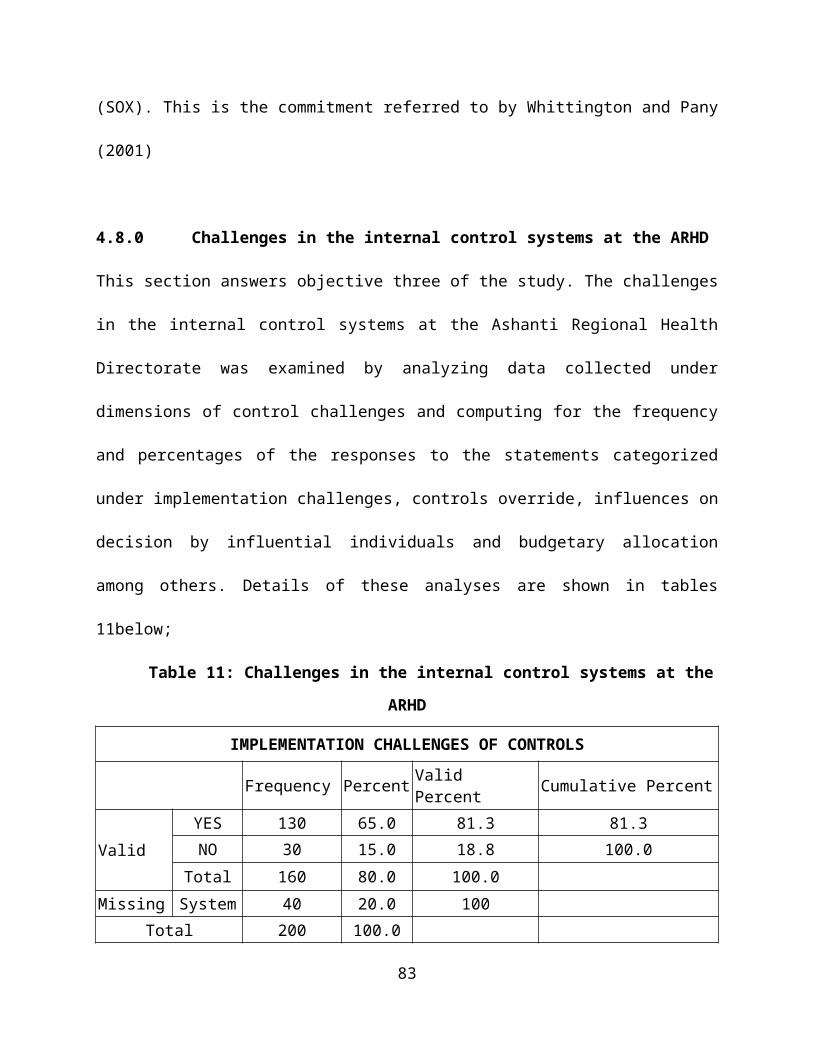

Ashanti Regional Health Directorate (ARHD).

1.4 Research Questions

In order to attain the above objectives drawn from the problem

statement, the research seeks to address the following main

questions:

5

1. What are the types of internal control in operations currently at

ARHD?

2. How effective are these types of internal controls in operations in

addressing Risk the organization is exposed to?

3. What are the challenges associated with the internal controls

at the ARHD?

1.5 Significance of the study

Although this study is limited to Ashanti Regional Health

Directorate, it is hoped that the study will be of immense

benefit to many similar public organizations. In addition, the

study will enable management to understand and appreciate the

need to put the necessary structures in place to ensure adequate

and effective internal controls.

Further, the study will contribute to the understanding of the

relationship existing among Internal control theoretical frame

work, adequate and effective working internal controls on the

ground and Management’s role and how the components of an

internal control systems can be integrated to ensure value for

money in the public sector. Finally, the research will add more

6

knowledge to the existing literature on the topic and serve as a

source of reference to researchers on the topic.

1.6 Brief Methodology

In this section, an over view of the research methodology is

presented. The study employed observations, interviews and

questionnaires as research tools for data collection. The

methodological framework for this study is based on

triangulation; thus both qualitative and quantitative analysis.

The population of this study comprises managerial positions and

lower staff ranks at Ashanti Regional Health Directorate. The

research on its outlook reflects the entire public sector in

Ghana but the survey will be limited to Ashanti Regional Health

Directorate.

Primary data will be collected in order to solicit responses

directly from the field. The data collected, will constitute the

basic information from which discussions and conclusions will be

drawn for decision making.

Data is hereafter entered into Statistical Package for Social

Sciences (SPSS) and a code book generated to help in the data

7

entry. Plausible checks are conducted and inconsistent data are

cleared as appropriate. Descriptive statistical tools such as

tables, frequencies, percentages are used. Linked questions are

matched out through crosstabs to see if they are internally

consistent and statistical test are also conducted. A linear

regression model is developed to establish the link between

effective internal control and effective use of public resources.

1.7 Scope of the Study

This study will cover and explore the adequacy and effectiveness

of internal control system at Ashanti Regional Health

Directorate. Critical look would be given to Managerial behaviour

towards effective integration of components of internal controls

to ensure adequate and effective internal control system to

address inherent risks both operational and financial within the

organizational risk appetite. However, all those issues which

are reasonably incidental to or consequential upon the attainment

of this objective shall be dealt with and discussed.

1.8 Limitation of the Study

8

The study is carried out in the Ashanti Regional Health

Directorate. The target institutions shall be Ashanti Regional

Health Directorate. Secondary data will be obtained from these

places for further studies and analysis.

In an environment such as ours where information is unduly

restricted and at times unavailable due to poor storage and

record keeping, the ability of the researcher under this

circumstance would be greatly limited since analysis can be made

into the extent of information derived.

This limitation is compounded by the time limit within which to

cover this important aspect of the accounting discipline.

However, the above mentioned limitations would not affect the

quality of information that would be gathered to any marked

degree.

1.9 Organization of the Study

To enhance the orderly and systematic presentation of the ideas,

this research is grouped into five chapters. Chapter one will be

the introduction which explains the background, statement of the

problem, objectives of the study, research questions,

9

justification of the study, scope and limitations of the study.

Chapter two deals with the literature review where theoretical or

conceptual framework and empirical basis of the study is looked

at and it was devoted to a detailed literature review on the

subject area.

Chapter three outlines the methodology which describes the

procedures that will be adopted in conducting the research.

Chapter four presents results of the data gathered about the

subject matter. It comprises the organization, description,

analysis and interpretation of the results obtained, and Chapter

five summarizes the findings of study; and presents the

recommendations and conclusion with suggestions for further

study.

CHAPTER TWO

LITERATURE REVIEW

10

2.0 Introduction

This chapter provides the theoretical and conceptual framework of

the study upon which a firm understanding of effective internal

controls system is established and how the common elements of

internal controls are employed at the Regional Health Directorate

and similar public sector organizations to ensure efficiency and

effectiveness of operations. Relevant literature on internal

controls, common components of internal controls, risk

managements and objective of systems of internal controls are

reviewed.

The corporate objective and environment in which firms operate in

this contemporary business world are continuously changing.

Consequently, the risks that firms are encountering are

constantly evolving too. In order to ensure faster adaptation to

these changes, an effective internal control must necessarily be

reactive to changes. Successful risk management and internal

control therefore depends on regular appraisal of the nature and

extent of risk. (KPMG, 1999).

11

2.1 Internal Control System

Drawing from Statements of Standard Auditing Practices No. 6 (SAP

6) Gupta (2001) defines

Internal control as “the plan of organization and all the methods

and procedures adopted by the management of an entity to assist

in achieving management objectives of ensuring as far as

practicable, the orderly and efficient conduct of its business,

including adherence to management policies, the safeguarding of

assets, prevention and detection of fraud and error, the accuracy

and completeness of accounting records and the timely preparation

of reliable financial information”.

Control is made up of those elements of an organization that in

sum assist people to achieve the objectives of the organization.

Controls are said to be effective as far as they provide

reasonable assurance that the business objectives of the company

would be reliably achieved (KPMG, 1999).

2.1.1 Internal Controls Systems

An internal control system is made up of the policies, processes,

behaviors, tasks and/or activities of a company that collectively

12

help its effective and efficient function by enabling it to react

correctly to material business, operational, financial,

compliance and other risks to achieving the company’s objectives.

It involves the safeguarding of assets from unauthorized usage or

from loss and fraud, and making sure that liabilities are

recognized and managed. In addition it helps in ensuring the

quality of internal and external reporting. (ACCA- Audit and

Assurance Services)

2.1.2 COSO control Framework

The Committee of Sponsoring Organization of the Treadway

Commission (COSO) created the 1992 COSO-control framework with

the aim of providing broadly accepted criteria for establishing,

monitoring, evaluating and reporting on internal control (COSO,

1992). It defines internal control as:”a process, effected by an

entity’s board of directors, management and other personnel,

designed to provide reasonable assurance regarding the

achievement of objectives in the following categories: l)

Effectiveness and efficiency of operations, 2) Reliability of

financial reporting and 3) Compliance with applicable laws and

13

regulations. The COSO definition is seen as the most widely

accepted in practice. This assertion can be seen almost in all

similar conceptual definitions by other relevant groups around

the world (Kinney 2000).

2.1.3 CoCo definition of Internal Control

The Canadian Guidance on Control Board (CoCo) explains internal

control as “all the resources, processes, culture, structure, and

tasks that, taken together, support people in achieving those

objectives”. From a broader perspective, the CoCo definition

overtly mentions internal elements such as “internal reporting”,

“information within the organization”, and “internal policies” as

part of internal control. Whilst definition by The Institute of

Chartered Accountants in England and Wales (ICAEW) lay emphasizes

on the significance of responding to risk by stating that

internal control deals with “behaviors” (Pfister, 2009).

2.1.4 The European Federation of Accountants (FEE)

The European Federation of Accountants (FEE) on the other hand

looks at internal control in relation to governance and sees

14

internal control as going “beyond procedures” to includes

“elements such as corporate culture, systems, structure, policies

and tasks” Notwithstanding these differences in emphasis all the

concepts support that of COSO ( Pfister 2009).

In addition, recognition for the need to update the 1992

guidelines for Internal Control Standards for the Public Sector,

the 17th INCOSAI (Seoul, 2001) accepted that the COSO integrated

framework for internal control should be relied upon. Though the

guidelines also addresses ethical values and provide more

information on the general principles of control activities

related to information processing.

2.1.5 Functions of internal control Systems

According to Flick (2010), internal control system ensures correct

functioning of organizational processes, reliability of financial

information and compliance with relevant regulation. Through

internal controls organizations check fraud and abuse. Generally,

internal controls are used to describe the manner in which

management assures that financial and other objectives of an

Organization are met.

15

2.1.5.1 The INTOSAI framework

The need to emphasis the importance of safeguarding resources in

the public sector needs to be stressed. The resources in the

public sector are mainly made up of public funds and how these

funds are utilized in the interest of the public calls for

special attention (INTOSAI, 2004).

In the public sector the budgetary accounting are mainly on cash

basis and it does not provide enough assurance in respect

acquisition, use and disposition of resources. Consequently,

records on assets are not up to date and therefore susceptible to

misuse. For these reason, safeguarding resources is an important

internal control. The focus and/or objectives of public entities

determine their characteristics; therefore the internal controls

of differing entities should be understood in this context (EIU

Compendium 2012).

The definition that is more relevant to the study is that of

INTOSAI (2004). Internal control is defined as an integral

process that is effected by an entity’s management and personnel

and is designed to address risks and to provide reasonable

16

assurance that in pursuit of the entity’s mission, the following

general objectives are being achieved: (1) executing orderly,

ethical, economical, efficient and effective operations, (2)

fulfilling accountability obligations;

(3) Complying with applicable laws and regulations, and (4)

Safeguarding resources against loss, misuse and damage. From the

perspective of the INTOSAI definition, internal controls are

embedded in the operations of an entity. It is built into the

infrastructure of an entity and form part of its culture.

Control is affected by individuals working across the company,

including the Board of directors, management and personnel. Those

responsible, as individuals or teams, for achieving objectives

are also responsible for the effectiveness of controls that

supports the achievement of set objectives (Pfaff and Ruud 2007).

2.2 Role of Board of Directors in Internal Control

The Board of Directors and/or the governing council of an entity

are responsible for internal controls. As the organ responsible

for internal controls, the Board should formulate and implement

suitable policies on internal controls and ensure that

17

appropriate processes are working effectively to monitor the

risks to which the company is exposed (Verschoor, 1999).

In addition, the board should ensure that the system of internal

controls is effective in mitigating risks within the entity’s

risk appetite. It is therefore necessary that the appropriate

tone is set at the top most level and the seriousness attached to

control responsibilities must be effectively communicated. The

task of establishing and operating and monitoring the internal

control systems will however be delegated to management (KPMG,

1999).

2.3 Categories of internal control

Internal controls related with the management of large firms have

been categorized into two major types (1) strategic controls and

(2) financial controls. Strategic controls involve evaluation of

business-level managers' actions and performance by using

criteria that are strategically relevant in the long term (Hitt

et al, 1996).

The operation and monitoring of the strategic system of internal

control should be undertaken by individuals who collectively

18

possess the necessary skills, technical knowledge, objectivity,

and understanding of the entity and the industries and markets in

which it operates. It also requires a rich information exchange

between corporate and Divisional managers (Hoskisson et al.,

1994).

2.4 Elements of internal control

According to Hayes et al., (2005) the common elements of internal

controls are: (1) Control environment, (2) the entity’s risk

assessment process, (3) the information and communication

systems, (4) control activities and (5) the monitoring of

controls.

2.4.1 Control environment

The control environment is the basic element in an organization

that influences the control awareness of its people. As the basic

element, the control environment is the fundamental component

upon which all other components of internal control system are

built by providing discipline and structure (Whittington and

Pany, 2001).

19

The control environment comprises of factors such as integrity,

ethical values and competence of the entity’s people;

organizational philosophy and operating style; the manner in

which authority and responsibility are assigned by management,

how its people are organized and developed; and the attention and

direction provided by the Board of directors (KPMG, 2009).

2.4.2 The entity’s risk assessment process

This involves identification and evaluation of risks and control

objectives. All entities encounter all sorts of risk from both

their external and internal environment that needs to be properly

assessed. Established objectives that must be linked at various

levels and internally consistent are the prerequisites for

effective risk assessment. Risk assessment involves

identification of significant risks to achievement of established

objectives. It forms the basis for determination of an entity’s

risk management process. Risk assessment is of more importance in

contemporary business environment as a result of constant changes

in economic, industry, regulatory and operating conditions (KPMG,

2009).

20

2.4.3 Control activities

These are the policies and procedures adopted by management to

ensure that directives are carried out as required. Control

activities are enablers that ensure that the required actions are

taken to deal with risks that may hinder the achievement of the

entity’s objectives. Control activities take place at all levels

and functions throughout the organization. It is made up of a

number of activities as diverse as approval, authorizations,

verifications, reconciliations, and reviews of operating

performance, security of assets and segregation of duties (KPMG

October 1999)

2.4.4 Information and communication processes

To ensure that people play their assigned roles effectively and

efficiently the relevant information must be identified recorded

and/or captured and communicated within an appropriate time

frame. The products of information systems are business reports.

These reports often contain operational, financial and

compliance-related information, which aids management to run and

21

control the business. An information system deals with both

internal data and information about external events, activities

and conditions that are essential to business decision making and

external reporting.

Channels of communications are usually depicted in organization

structures. In a broader sense, communication flows down, across

and up the organization. There is also the need to also

communicate effectively with external parties such as customers,

suppliers, regulators and shareholders ((KPMG, 1999).

The information and communication process provide a source of

strategic flexibility. It enhances a firm’s ability to meet

customer’s expectation. Moreover effective information and

communication enhances understanding and flow of work among

employees in the organization as well as among those employees

and their counterparts such as suppliers and other stake holders

(Hitt et al, 2005).

2.4.5 Processes for monitoring the effectiveness of the

system of internal control

22

Internal control systems need to be monitored - a process that

assesses the quality of the system’s performance over time. This

is accomplished through ongoing monitoring activities, separate

evaluations or a combination of the two. Ongoing monitoring

occurs in the course of operations. It includes regular

management and supervisory activities, and other actions

personnel take in performing their duties. The scope and

frequency of separate evaluations will depend primarily on an

assessment of risks and the effectiveness of ongoing monitoring

procedures. Internal control deficiencies should be reported

upstream, with serious matters reported to top management and the

Board (KPMG, 1999).

2.5 Evolution of internal control systems (The Agency Theory)

Agency Theory describes the relationship both economic and

otherwise, within an entity and between the entity and other

parties that have vested interest in the entity. Organizations

are seen as an indispensable structure to maintain a healthy

contract in a relationship between an agent and principal.

23

Moreover, entities make it possible to exercise control which

minimizes opportunistic behavior of agents.

Accordingly, Barlie and Means (1932) put forward that in order to

synchronize the interests of the agent and the Principal, a

detailed contract is written to deal with their interest. In

addition they also stated that the relationship between the

principal and the agent is enhanced if the principal employ an

expert to keep an eye on the agent.

The stand of Barlie and Means (1932) is supported by Coarse

(1937). He argues that the existence of contract gives the

platform for conflict resolution between the agent and principal.

He also suggested that the principal suffers shirking which

denies him or her gains from the work of the agent.

2.5.1 Relevance of agency theory in public organization

From the perspective of the agency theory, managers of public

funds and public servants in general could be seen as agents

whilst the general public is seen as the principal. The public

servants are therefore expected to serve the public interest with

fairness and manage public resources properly. In addition the

24

citizenry should be treated impartially on the basis of legality

and justice. Ensuring public interest is therefore a prerequisite

to, and underpins public trust and is a keystone of good

governance (INTOSAI, 2004).

Moreover, new legal directives assert themselves in the domain of

corporate governance of companies to control management

decisions, define the role of independent committees, improve

principles of corporate governance and set up and control

internal control systems that are really effective in order to

limit failures (Woolf, 1990).

2.5.2 Historical Perspective of Internal Controls

The last 15-20 years, have seen a significant attention on

governance and business perspectives of controls than accounting

and finance orientation of internal control. Origin of the term

internal controls may be traced to the accounting and auditing

discipline (Pfister, 2009).

Traditionally, it was perceived as “accounting control” that are

restricted to the systems that are tested by auditors as part of

gaining assurance as to the reliability of the financial

25

reporting. Consequently, internal control discussions were made

in the context of auditing (Pfister, 2009).

The distinction between recognition and lack of it was found in a

publication entitled Auditing by Lawrence Dicksee in 1905 (Brown,

1962).

Internal controls emerged as a result of reactive evolution.

According to Heir et al. (2005), the emergence of talks,

deliberations, interpretations, definitions and applications of

internal controls was as a result of responses to changes in the

economic conditions of a country as a whole and actions and

responses of firms within the economy.

The series of company failures linked to the Enron and WorldCom

scandals in early 2000 that led to major legislative reactions

such as Sarbanes-Oxley Act of 2002 (SOX), are examples of such

events and reactions (Maijoor, 2000). The restoration of public

confidence in the capital markets by ensuring the reliability of

financial reporting and effectiveness of corporate governance

were reasons for SOX (Ge and McVay, 2005).

The response to these scandals and failures was introduction of

more regulation and mandatory disclosure of internal control

26

aspects and/or to a widening of the interpretation of internal

control in public policy documents (Pfister, 2009).

2.5.3 Viewpoints on Internal Controls

Two viewpoints can be identified from the above historical

perspective; the focused view and the comprehensive view on

internal control. The focused view equates internal controls to

check and balances in systems of accounting whilst the

comprehensive view stresses on holistic approach by looking at

efficiency and effectiveness of operations and adherence to laws,

regulations and internal policies. Dealers in enterprise resource

planning (ERP) systems software have capitalized on this focus on

internal controls by stressing that an outstanding feature of ERP

systems is the integrated controls that reflect a firm’s

infrastructure. These features are often given prominence in

their marketing literature, asserting that these systems will

assist organizations improve the effectiveness of their internal

controls as required by SOX (John J. Morris, 2011).

One of the significant means of dealing with agency theory is

internal controls coupled with financial reporting, budgeting,

27

audit committees, and external audits (Jensen and Payne, 2003).

Studies have established that effective internal control leads to

reduction in agency costs (Barefield et al., 1993). Other writers

have also observed that firms have an economic incentive to

report on internal control, irrespective of SOX requirements

(Deumes and Knechel, 2008).

It is argue that, giving out this additional information about

the agent (management) to the principal (shareholder) leads to

reduction in information asymmetry and lowers investor risk and,

consequently, the cost of equity capital. Many studies have

concluded that there exist a correlation between weaknesses in

internal controls and increased in levels of earnings management

(Chan et al, 2008).

2.6.0 Importance of Internal control

For many years, internal controls had played a significant role

in addressing the agency problem in corporations. A number of

internal control procedures employed by the Baltimore and Ohio

Railroad as early as 1831 had been documented (Samson et al.,

2006).

28

The creation of the Committee of Sponsoring Organizations of the

Treadway Commission (COSO) was as a result of a number of audit

failures in the 1980s. The main objective was to reshape the

orientation of internal controls and standards for determining

the effectiveness of an internal control system (Simmons 1997).

The factors that lead to fraudulent financial reporting were

studied and the appropriate recommendations were developed for

public companies, independent auditors, educational institutions,

the Securities Exchange Commission (SEC), and other regulatory

bodies (COSO, 1985). The outcome of their study is known as the

COSO Internal Control Integrated Framework (Simmons, 1997).

The framework sees controls that are integral part of an entity’s

infrastructure as the most effective. It also acknowledged that

built in controls support quality and empowerment initiatives, it

helps in avoiding unnecessary costs and enables quick response to

changing conditions (COSO, 1992). Consequently, the need for

mechanisms to identify and deal with risks associated with change

coupled with public expectation of healthy risk assessment and

evaluation have led to a corresponding increase in the importance

of internal control procedures.

29

Section 404 of the ACT demands a separate management report on

the entity’s internal control over financial reporting and as

well as a report from a registered public accounting firm

attesting to the existence and effectiveness of the internal

controls.

Internal controls have been categorized into general entity wide

and specific (account level) controls. The expectations are that

internal control weakness associated with general controls will

exist, even if specific controls remain effective as far as

management do away with control features in order to manage

earnings. (John J. Morris, 2011). During audit, it is expected

that audit process would revealed this kind of occurrence. This

concern is specifically raised in auditing standard no. 5,

paragraph 24. This states that “entity-level controls include

controls over management override.” This goes to emphasis the

importance place on general controls.

In the Executive Summary of “Enterprise Risk Management-

Integrated Framework” 2004 by the Committee of Sponsoring

Organizations (COSO, 2004), of the Treadway Commission, Internal

controls have been incorporated into policies, rules and

30

regulations to help organizations achieve their established

objectives.

This is in line with Pany, Gupta and Hayes’ assertion that

internal controls are meant to help an organization achieve its

objectives. The COSO commission was partly instituted in response

to a series of high profile scandals and business failures where

stakeholders (particularly Investors) suffered tremendous losses.

This study however differs in that it is done for an institution

that is not ailing though there are reported incidences of

scandals and financial misfeasance. The end results should

therefore aid the preventive mechanism rather than being

reactionary. Entities exist to provide value to its stakeholders

but are normally face with uncertainty. Uncertainty presents

risks and opportunities.

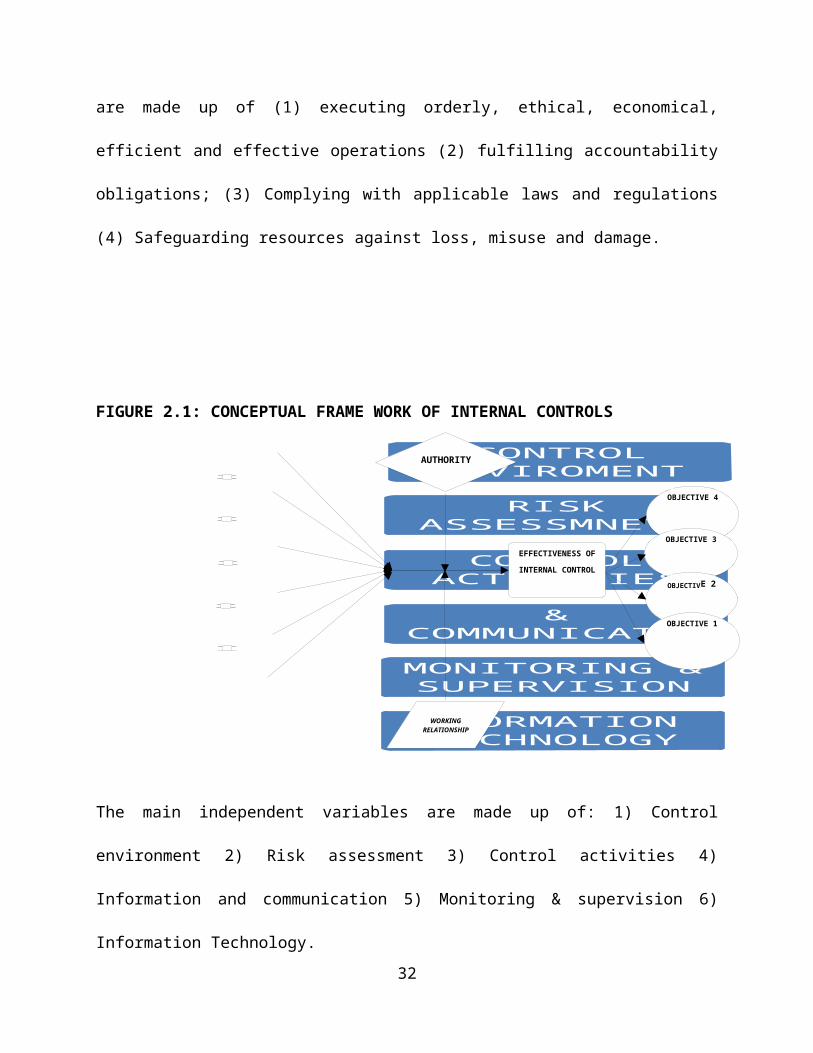

2.7.0 Conceptual frame work

The objective of the study is based on four key concepts; the

components of internal control (IC), Authority and working

relationship (AWR) and effectiveness of internal controls (EIC)

and Objectives. The interrelated objectives depicted in figure1

31

are made up of (1) executing orderly, ethical, economical,

efficient and effective operations (2) fulfilling accountability

obligations; (3) Complying with applicable laws and regulations

(4) Safeguarding resources against loss, misuse and damage.

FIGURE 2.1: CONCEPTUAL FRAME WORK OF INTERNAL CONTROLS

The main independent variables are made up of: 1) Control

environment 2) Risk assessment 3) Control activities 4)

Information and communication 5) Monitoring & supervision 6)

Information Technology.32

CONTROL ENVIROMENT

RISK ASSESSMNET

CONTROL ACTIVITIESINFORMATION

& COMMUNICATIO

NMONITORING & SUPERVISION

INFORMATION TECHNOLOGY

AUTHORITY

WORKINGRELATIONSHIP

EFFECTIVENESS OF

INTERNAL CONTROL

OBJECTIVE 4

OBJECTIVE 3

OBJECTIVE 2

OBJECTIVE 1

The effectiveness of internal control system is determined by the

existence and proper integration of the independent variables

into the organization’s infrastructure.

The moderating variables; thus authority and working relationship

feeds into the frame work to identify lapses and/or weaknesses in

the manner in which the major independent variables are employed.

There is a direct relationship between the results of the

dependent and the independent variables. The independent factors

are significant to each of the objectives. The minor independent

factors (internal control process) affect the effectiveness of

internal control systems. Notwithstanding the interdependency

among the independent variables, each has an impact on the

effectiveness of internal control systems.

Although there are other means of evaluating effectiveness of

internal controls, the model in Figure 2.1 is used. In this

respect, internal control evaluation is a step toward achieving

the objectives of the study.

33

CHAPTER THREE

METHODOLOGY AND ORGAINSATIONAL PROFILE

3.0.0 Introduction

This Chapter focuses on the methods that were used to collect

data and analyze it. It deals mainly with the research design,

the population that was studied, the sample selection procedures

and sampling techniques used, methods of verifying reliability

and validity of data and methods, as well as issues bothering on

ethics and the limitations of the methodology used and the

conclusions drawn from the methodologies used.

The rationale of this study is to analyze and appraise the

effectiveness of internal control systems in the Public Sector

34

and more specifically, in the Ashanti Regional Health

Directorate. In order to demonstrate the theoretical

understanding to the topic in the study, literature review was

conducted prior to the design of the research. The analyses in

this thesis were from senior management, staff in finance

department, program managers, administrators’ and other

perspective.

3.1.0 Data Sources

In an attempt to achieve the research objectives, data sources

both primary and secondary were gathered through administration

of questionnaires, interviews and documentary analysis.

3.1.1 Primary Data

The primary data provided first-hand information from the

finance, human resource, the clinical and the public health units

on their views and opinions on adequacy and effectiveness of

internal controls operation at the Ashanti Regional Health

Directorate and how they can affect 1) the orderly execution of

operations in an ethical, economical, and efficient manner, 2)

the fulfillment of accountability obligations, 3) complying with

35

applicable laws and regulations and lastly but not the least 4)

safeguarding resources against loss, misuse and damage. It also

provided information on how authority and working relationships

work to ensure the continuous effectiveness of internal control

operations.

3.1.2 Secondary Sources

The secondary sources on the other hand included desktop study of

policy manuals on human resources, accounting systems, internal

audit, procurement and the plan preventive maintenance (PPM) in

addition to financial reports of the institution, internal and

external audit reports, annual review reports, health programs

reports from program focal persons and the strategic plans of the

Ashanti Regional Health Directorate (ARHD).

3.2.0 Research design

A cross sectional survey designs and case study were used for

purposes of examining information, evaluating the internal

control system and analyzing the relationship between the

components of internal control system(IC), Authority and working

36

relationship (AWR), internal control effectiveness (EIC), and

objectives. Survey is an oriented methodology used in

investigating a population by analyzing a selected sample to

discover occurrences. Additionally, correlation and regression

were described as the determination of existence of relationship

or otherwise between two or more variables and extent of the

relationship. A case study is an Intensive descriptive and

holistic analysis of a single entity or a bounded case (Oso and

Onen, 2008).

In order to ensure economy, rapid collection of data and also

enhance ability to understand a population from part.(Oso and

Onen, 2008), a case study was used since RHD was chosen as a

representative of public sector organization where results of the

study can be replicated and applied to other public institutions.

Case study was also chosen because the study focused on the RHD

as representative of other Health Directorates in Ashanti Region.

3.3.0 Population of the Study, Sample and Sampling Techniques

Top and middle level management members were essentially targeted

for this study since they are the Custodians of Internal control.

37

Consequently all unit heads were targeted as respondent, but,

more prominence was giving to members in Finance and Finance

related offices. The aim was to interview at least 90% of the

departmental heads and all staff in finance and accounts related

offices. Both purposive and stratified random samplings were used

for the study. The purposive was used because it allows the use

of judgment to select cases that will best enable you to answer

your question(s) and to meet your objectives (Saunders et al.,

2009). This form of sampling is often used when working with very

small samples such as in case study research and when you wish to

select cases that are particularly informative (Neumann, 2000).

It was used simply because the study was targeting basically

custodians of the internal control systems.

The sample size was arrived at as per the formula in

(Saunders et al., 2009)

n = p% * q% *[Z/e %] ² and n' = n/1+ (n/p)

Where:

n= the minimum sample required

38

P% = the proportion of people belonging to the

specified category

q% = the proportion not belonging to the specified

category

Z = the z value corresponding to the level of

confidence required

℮% = the margin of error required

n' = adjusted sample size

p = the population

The Regional Health Directorate is made up of a population of

2900 Out these every 25 staff belongs to a specified category and

75 do not belong to the specified category. A confidence or risk

level of 90% is selected to ensure certainty and accuracy of the

estimate. The corresponding ‘z’ score is 1.65 and the acceptable

level of precision needed to guarantee the accuracy of the

estimate is±5% (the margin of error that can be tolerated) of the

true value of the population. Substituting all the parameters

where; p=25, q=75, z=1.65, ℮%=±5% in the formula gives;

n = 25 * 75 * [1.65/5]²

n = 1,875 * 0.1089

39

n = 204.1875

The minimum sample size required is 204. However the population

of the Directorate was 2900 as at 2013 therefore n' the adjusted

minimum was giving by:

n' = 204./1+(204/2900)

n' = 204.25 or rounded of to 200.

Stratified sampling and simple random sampling techniques were

applied. The population was first stratified into functional unit

and further into managerial levels within a functional unit

whereas among the junior staff, simple random sampling was used

right away.

3.4.0 Method of Data Collection

Data was gathered using both primary and secondary data

collection techniques. Primary data was gathered basically by

employing structured questionnaires and interviews with “Key

management members and units heads.” Secondary sources on the

other hand was collected through review of available financial

records like Audited Financial Statements, Auditor’s Management

letters, internal auditor’s reports, committee reports and

40

Publications. Besides desktop study of policy manuals on human

resources, accounting systems, internal audit, procurement and

the plan preventive Maintenance (PPM), annual review reports,

health programs reports from program focal persons and the

strategic plans of the Ashanti Regional Health Directorate

(ARHD).

Questionnaires are a data gathering technique in which a number

of issues are responded by respondents in writing (Oso and Onen,

(2008). The reasons for adopting Questionnaires were mainly

because of the time limitation and partly because the research

was dealing with an elite community (respondents). Interview was

the other data collection technique used by the Researcher to

gather additional data and also as a means to probe further into

the responses given in the questionnaires.

3.5.0 Method of Data Analysis

In order to assess the effectiveness of internal controls and its

impact on organizational objectives, primary data in the form of

responses to administered questionnaires and by means of

interviews were subjected to detailed analysis. Data gathered in

41

the questionnaires were both qualitative and quantitative in

nature. The collected data was statistically analyzed with the

aid of an Expert and using Statistical Package for Social

Sciences (SPSS) version 17.5 for easy analysis and interpretation

of results. The data was analyzed using both statistical and

narrative methods. Correlation was used as a way of assessing the

relationship between effective internal controls and objectives.

Narrative analysis was used to explain the qualitative results of

the survey.

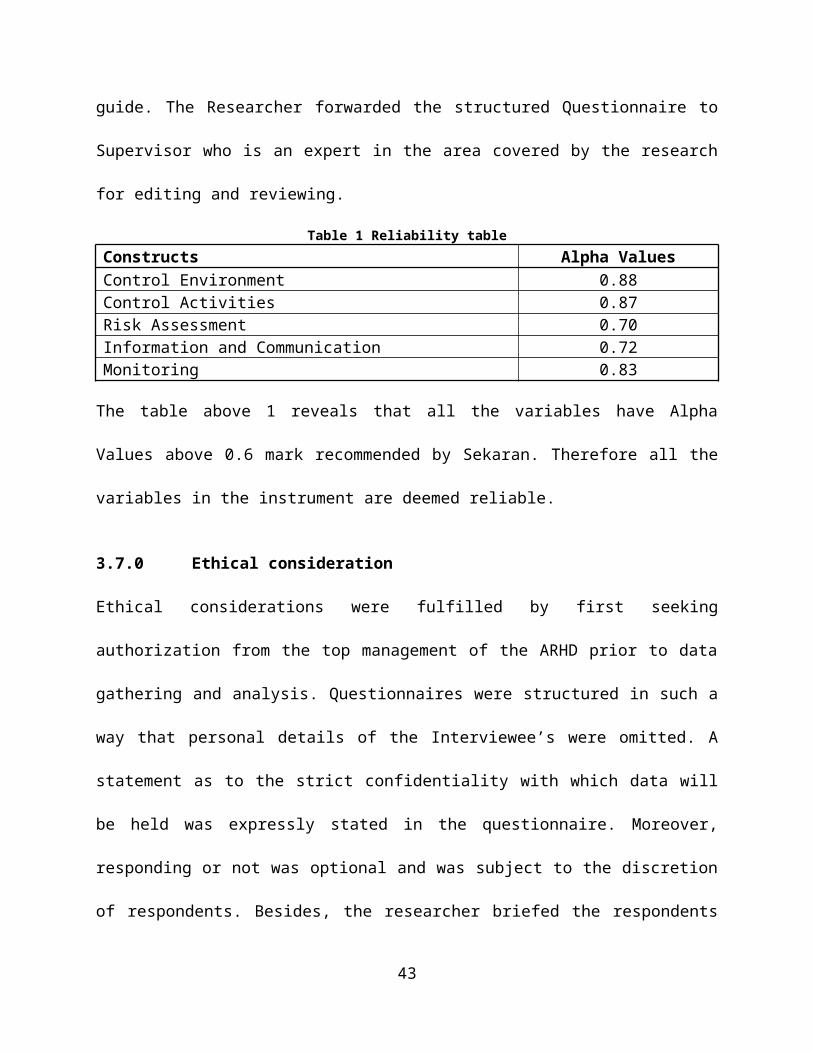

3.6.0 Reliability and Validity

The instruments were tested to ensure reliability of values

(Alpha values) in accordance with Cronbatch, (1946)

recommendations for analysis for Alpha values for each variable

under study. Alpha values for each variable under study were

expected to be more than 0.6 for the statements in the

Instruments to be considered reliable (Sekaran 2001).

Accordingly, all the statements under each variable were

subjected to this test and were proven to be not less than 0.6.

The validity of the data collection instruments was done with the

help of an Expert to edit the questionnaire and the Interview

42

guide. The Researcher forwarded the structured Questionnaire to

Supervisor who is an expert in the area covered by the research

for editing and reviewing.

Table 1 Reliability tableConstructs Alpha ValuesControl Environment 0.88Control Activities 0.87Risk Assessment 0.70Information and Communication 0.72Monitoring 0.83

The table above 1 reveals that all the variables have Alpha

Values above 0.6 mark recommended by Sekaran. Therefore all the

variables in the instrument are deemed reliable.

3.7.0 Ethical consideration

Ethical considerations were fulfilled by first seeking

authorization from the top management of the ARHD prior to data

gathering and analysis. Questionnaires were structured in such a

way that personal details of the Interviewee’s were omitted. A

statement as to the strict confidentiality with which data will

be held was expressly stated in the questionnaire. Moreover,

responding or not was optional and was subject to the discretion

of respondents. Besides, the researcher briefed the respondents

43

as to the purpose of the research, their relevance in the

research process, and expectations from them.

3.8.0 Limitations

The Research was limited by the following factors:

Study area: The Regional Health Directorate was use as a case

study; with an assumption that the results can be replicated

and applied to any other public organization. However, the

focus and/or objectives of public entities determine their

characteristics; therefore the internal controls of differing

entities should be understood in this context (EIU Compendium

2012). Some are wholly Government owned, quasi government

organization, some are formed with a profit motive yet others

are not. However, it was not economically feasible or

operationally possible to study all public organizations thus

culminating into the selection of the RHD so as to have an in-

depth understanding of effects of an effective internal

controls system on the objectives of public organizations.

This however does not vitiate the results of the study since

44

almost all public organizations have similar or related

objectives and have the same clientele.

Sample size used: The Researcher used Senior Managers, Heads

of departments and staff in

Finance and Finance related offices yet the Directorate has

other staff, implying that valuable information could have

been left out among the un-sampled staff members. The time

allocated to the study could not permit inclusion of other

staffs who are not directly involved with internal control

systems of the Directorate, even though some of them could

have had very valuable information in the area under study. It

is however presumed that a greater proportion of the un

sampled staff’s ideas were captured through their

representation by the Departmental heads, Management Committee

members and Finance and Accounts staff members, especially

given that the mentioned staff are the custodians of internal

controls or are the ones greatly involved with the Internal

control systems of the Directorate.

3.8.1 Organizational Profile

45

The Ashanti Regional Health Directorate (ARHD) is one the ten

(10) regional health Directorates in Ghana and as a division of

Ghana Health Service (GHS) which is a Public Service body

established under Act 525 of 1996 as required by the 1992

constitution. It is an autonomous Executive Agency responsible

for implementation of regional policies under the control of the

Director General of Ghana Health Services. The ARHD continue to

receive public funds and thus remain within the public sector.

However, its employees will no longer be part of the civil

service, and like all GHS agencies and divisions managers will no

longer be required to follow all civil service rules and

procedures. The independence is designed primarily to ensure

that staffs have a greater degree of managerial flexibility to

carry out their responsibilities, than would have been possible

if they remained wholly within the civil service. The RHD does

not include Komfo Anokye Teaching Hospital, Private and Mission

Hospitals. However, a close collaboration is required to ensure

effective and holistic approach to Health delivery in the Ashanti

Region.

46

3.8.2 Mission and Vision

As one of the critical sectors in the growth and development of

the Ghanaian economy, the mission of the ARHD is to improve the

health status of all people living in Ghana through the

development and promotion of proactive policies for good health

and longevity; the provision of universal access to basic health

services which are affordable and accessible. These services will

be delivered in a humane, efficient, and effective manner by

well-trained, friendly, highly motivated and client oriented

personnel. Whilst the vision of the ARHD is to provide quality

driven, results oriented, client focused and affordable health

service.

3.8.3 Composition of the ARHD

It is made up of the Office of the Regional Director (ORD), the

Regional Health Committees (RHC), Public Health Unit (PHU),

Clinical Care Unit (ICU), Regional Hospital (RH), Regional Health

Services Support Unit (RHSSU), Training Institutions (TI),

District Health Management (DHMT) Teams and Sub Districts Health

Teams (SDHT).

47

The ORD is made up of the health information Unit, the Accounts

and Finance Units, The Internal audit unit and the Training Unit.

PHU is made up of Public Health Nurses, Diseases Control unit,

Health Learning Materials Unit and the Family Planning Units. The

ICU is made up of the Laboratory technician, the pharmacist Unit,

the office of the director of Nursing, specialist and medical

Doctors. The HSSU also comprises of the procurement unit, human

resources Unit, estate and works unit, and the Transport unit.

The PHU is headed by a Deputy Director of Public Health, ICU is

headed by Deputy Director Clinical Care and Deputy Director

Pharmaceuticals, and the HSSU is headed by the Deputy Director

Administration.

3.8.4 Staff strength

The whole staff strength of the RHD as at 2013 was two thousand,

nine hundred (2900)

This is made up of health professionals and other auxiliary

staff.

3.8.5 Source of funding

48

Funding are mainly from internally generated fund (IGF),

Government of Ghana (GOG), and Donor Pool fund.

CHAPTER FOUR

PRESENTATION OF FINDINGS AND ANALYSIS

4.0 Introduction

This chapter presents the findings and the discussion of the

study. The discussion is tailored along finding solutions to the

research questions. It begins with the profile of the respondents

which is made up of staff of the ARHD. The subject of the

discussions was centered mainly on the types of controls in

operations at the ARHD, effectiveness of these internal controls

in operations as well as the challenges associated with the

internal controls in operation at the ARHD.

4.1 Background of Respondents

The background information of respondents was deemed necessary

because the study essentially targeted those who are the

Custodians of Internal control. Besides, the ability of the

respondents to give satisfactory information on the study

49

variables depends largely on their background. The data on

background information of respondents solicited for has been

categorized into gender, education levels, position held, age and

length of service in the organization.

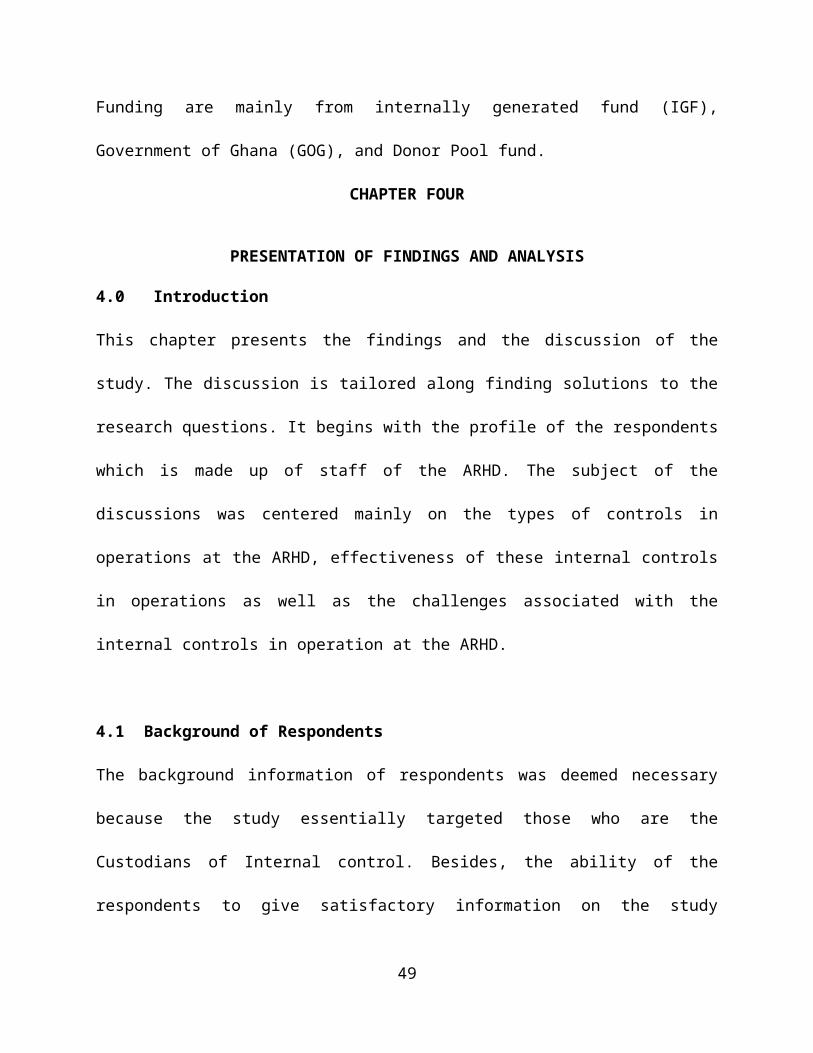

4.1.1 Gender characteristics of respondents

A total of Two Hundred (200) respondents of diverse background

were interviewed. Females constituted fifty (50) representing 25%

of the total respondents whilst male formed one hundred and fifty

(150) representing 75% as depicted in table 1.The findings

represent the views of the two sex groups about the effectiveness

of internal controls in the public sector.

Table 2: Gender characteristics of respondentsGENDER OF RESPONDENT

Frequency Percent Valid Percent Cumulative Percent

ValidMALE 150 75.0 75.0 75.0FEMALE 50 25.0 25.0 100.0Total 200 100.0 100.0

Source: Primary data

4.1.2 Educational background of respondents

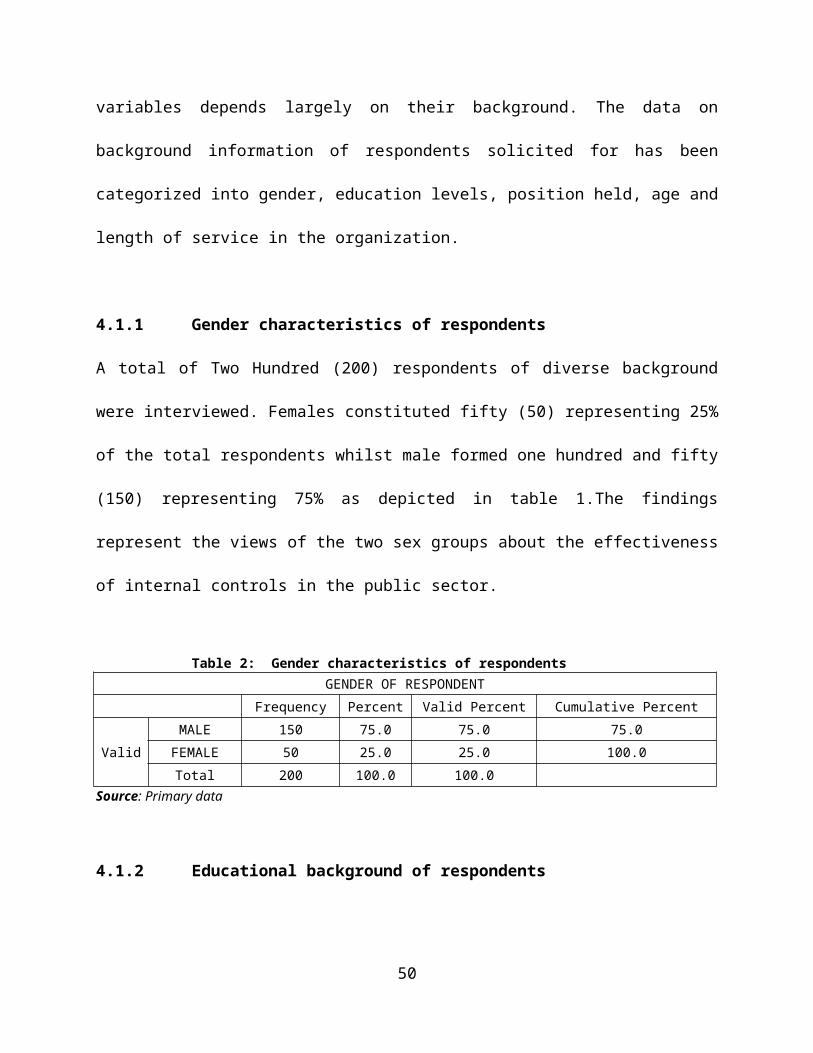

50

Details about the education levels of respondents were obtained

and the results are revealed in table 3 below. The statistics

provided in the table and figure below shows that majority of

respondents hold bachelor’s degree, followed by masters,

certificate/diploma, others, and PHD, in the orders of 49.5%,

27%, 20.5%, 2.5% and .5% respectively. This means that the

respondents are adequately qualified persons academically. It was

also gathered from respondents interviewed that 90% of

respondents had their masters whilst they were in active

employment through study leave with pay.

Table 3: Educational Levels of RespondentsEDUCATIONAL LEVELFrequency

Percent(%)

ValidPercent

(%)

CumulativePercent(%)

Valid

PHD 1 0.5 0.5 0.5CERTIFICATE/DIPLOMA 41 20.5 20.5 21.0BACHELOR 99 49.5 49.5 70.5MASTERS 54 27.0 27.0 97.5OTHERS 5 2.5 2.5 100.0Total 200 100.0 100.0

51

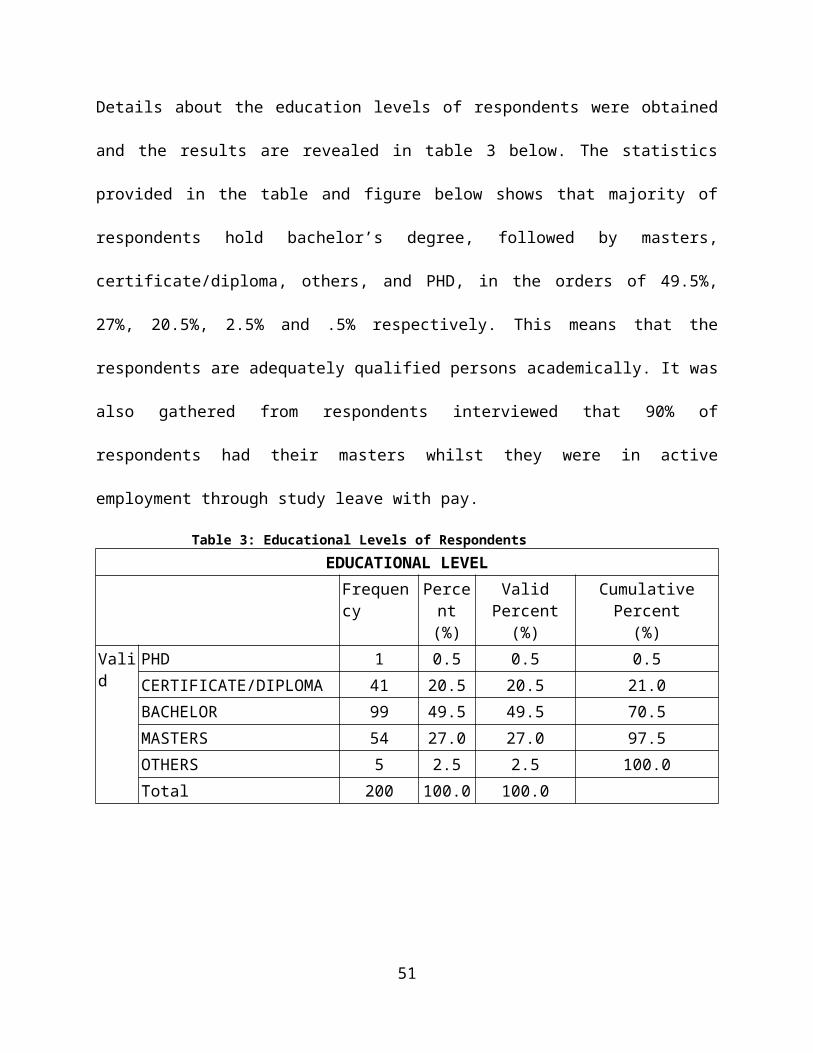

Source: Primary datafigure1: Pie chart of educational levels of

respondents

4.1.3 Description of the Positions of respondents

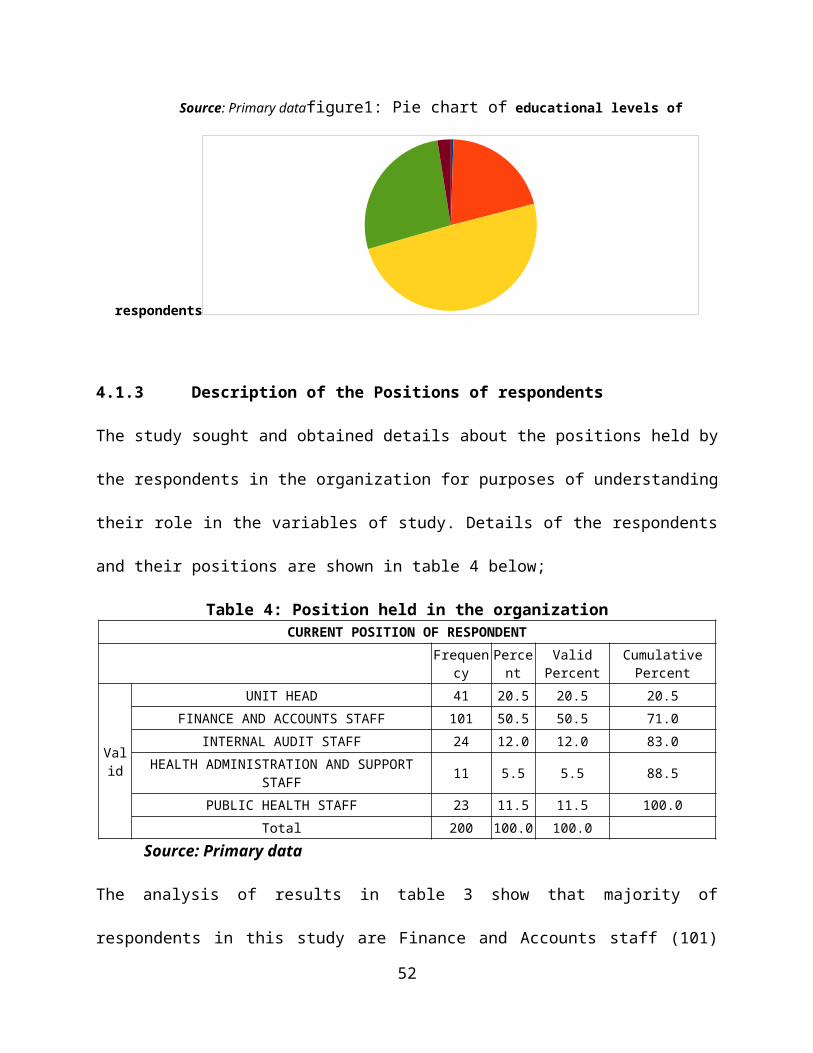

The study sought and obtained details about the positions held by

the respondents in the organization for purposes of understanding

their role in the variables of study. Details of the respondents

and their positions are shown in table 4 below;

Table 4: Position held in the organizationCURRENT POSITION OF RESPONDENT

Frequency

Percent

ValidPercent

CumulativePercent

Valid

UNIT HEAD 41 20.5 20.5 20.5FINANCE AND ACCOUNTS STAFF 101 50.5 50.5 71.0

INTERNAL AUDIT STAFF 24 12.0 12.0 83.0HEALTH ADMINISTRATION AND SUPPORT

STAFF 11 5.5 5.5 88.5

PUBLIC HEALTH STAFF 23 11.5 11.5 100.0Total 200 100.0 100.0

Source: Primary data

The analysis of results in table 3 show that majority of

respondents in this study are Finance and Accounts staff (101)

52

followed by Unit Heads (41), Internal Audit Staff (24), then

Public Health Staff (23), and Health Administration and Support

Staff (11). These represent 50.5%, 20.5%, 12.0%, 11.5%, and 5.5%

respectively. Besides, it was also ascertained that by virtue of

being a unit Head one automatically becomes a member of the

Regional Health Management Team (RHMT) or a member of the

District Health Management Team (DHMT).

However, there is also another group of managers who made up the

core management Team. This includes the Regional Director, all

deputy Directors and key unit’s heads of the organization.

The above description denotes that majority of the respondents in

this study are those directly responsible for or directly

involved in the implementation of the Internal Control Systems.

Consequently, their responses are deemed to be the true

reflection of what actually takes place at the ARHD.

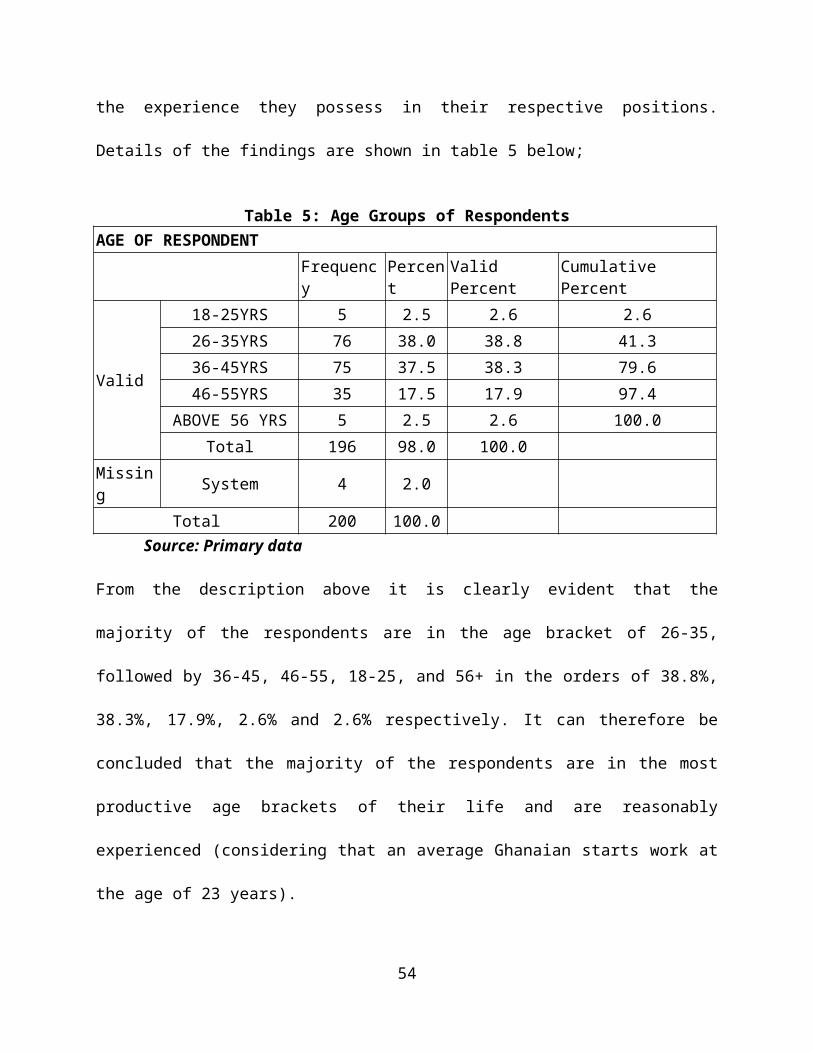

4.1.4 Description of age groups of respondents

The age groupings of the respondents were obtained for purposes

of understanding their level of maturity (age wise) and possibly

53

the experience they possess in their respective positions.

Details of the findings are shown in table 5 below;

Table 5: Age Groups of RespondentsAGE OF RESPONDENT

Frequency

Percent

ValidPercent

CumulativePercent

Valid

18-25YRS 5 2.5 2.6 2.626-35YRS 76 38.0 38.8 41.336-45YRS 75 37.5 38.3 79.646-55YRS 35 17.5 17.9 97.4

ABOVE 56 YRS 5 2.5 2.6 100.0Total 196 98.0 100.0

Missing System 4 2.0

Total 200 100.0Source: Primary data

From the description above it is clearly evident that the

majority of the respondents are in the age bracket of 26-35,

followed by 36-45, 46-55, 18-25, and 56+ in the orders of 38.8%,

38.3%, 17.9%, 2.6% and 2.6% respectively. It can therefore be

concluded that the majority of the respondents are in the most

productive age brackets of their life and are reasonably

experienced (considering that an average Ghanaian starts work at

the age of 23 years).

54

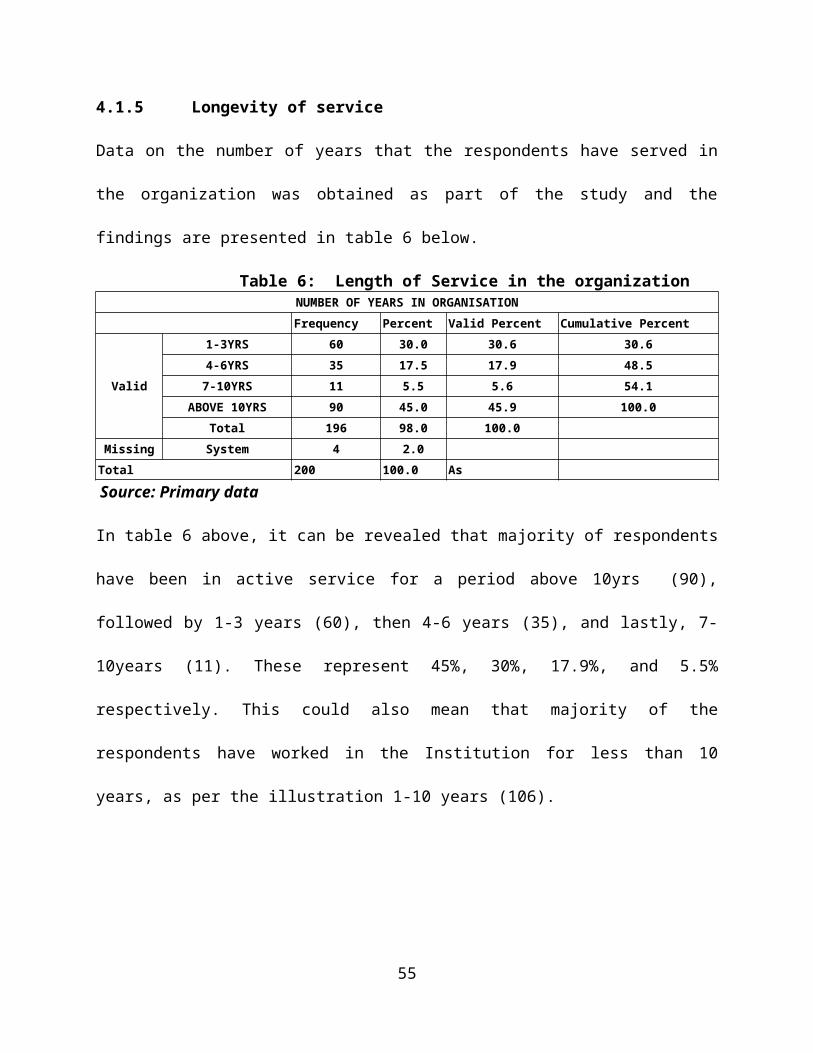

4.1.5 Longevity of service

Data on the number of years that the respondents have served in

the organization was obtained as part of the study and the

findings are presented in table 6 below.

Table 6: Length of Service in the organizationNUMBER OF YEARS IN ORGANISATIONFrequency Percent Valid Percent Cumulative Percent

Valid

1-3YRS 60 30.0 30.6 30.64-6YRS 35 17.5 17.9 48.57-10YRS 11 5.5 5.6 54.1

ABOVE 10YRS 90 45.0 45.9 100.0Total 196 98.0 100.0

Missing System 4 2.0Total 200 100.0 As Source: Primary data

In table 6 above, it can be revealed that majority of respondents

have been in active service for a period above 10yrs (90),

followed by 1-3 years (60), then 4-6 years (35), and lastly, 7-

10years (11). These represent 45%, 30%, 17.9%, and 5.5%

respectively. This could also mean that majority of the

respondents have worked in the Institution for less than 10

years, as per the illustration 1-10 years (106).

55

4.2.0 The types of internal controls in operations at ARHD

The study seeks to identify the types of controls in operations

at the ARHD as part of its objectives. In pursuant of this

objective the research examined and interviewed a number of key

personnel as to whether the organization operates systems of

internal control and as to whether the controls in operations can

be described as comprehensive internal controls which stresses on

holistic approach by looking at efficiency and effectiveness of

operations and adherence to laws, regulations and internal

policies or focused controls which equates controls to check and

balances in systems of accounting.

The respondents seem to agree that ARHD operates a system of

internal control; implementing strategic plans and measuring

actual performance against budgets, stating priorities and

implementing them on an annual basis through the budgeting

process, ensuring policies and procedures are followed in all

financial and operations of the organization, safeguarding assets

through the maintenance of a fixed assets register and updating

it regularly.

56

Additionally, it ensures (1) executing orderly, ethical,

economical, efficient and effective operations, (2) fulfilling

accountability obligations; (3) Complying with applicable laws

and regulations, and (4) Safeguarding resources against loss,

misuse and damage. The respondents also accepted that the type of

internal controls in operation can be described as comprehensive

internal controls.

4.2.1 organizational structure

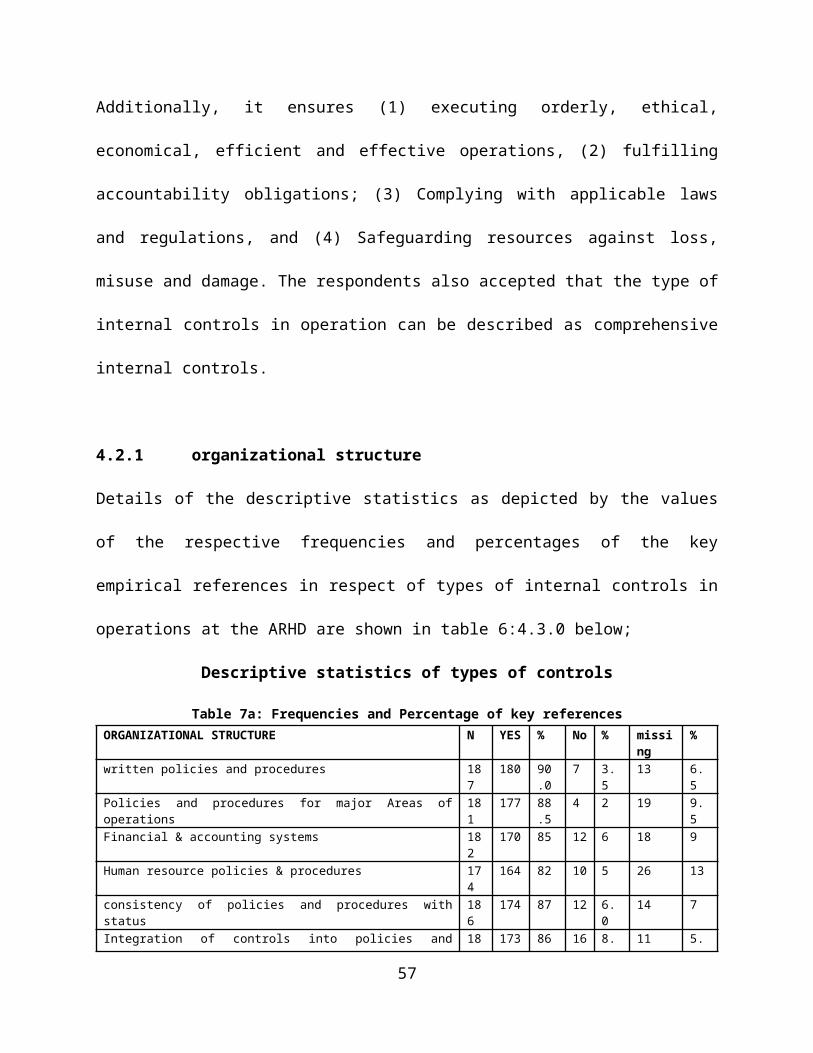

Details of the descriptive statistics as depicted by the values

of the respective frequencies and percentages of the key

empirical references in respect of types of internal controls in

operations at the ARHD are shown in table 6:4.3.0 below;

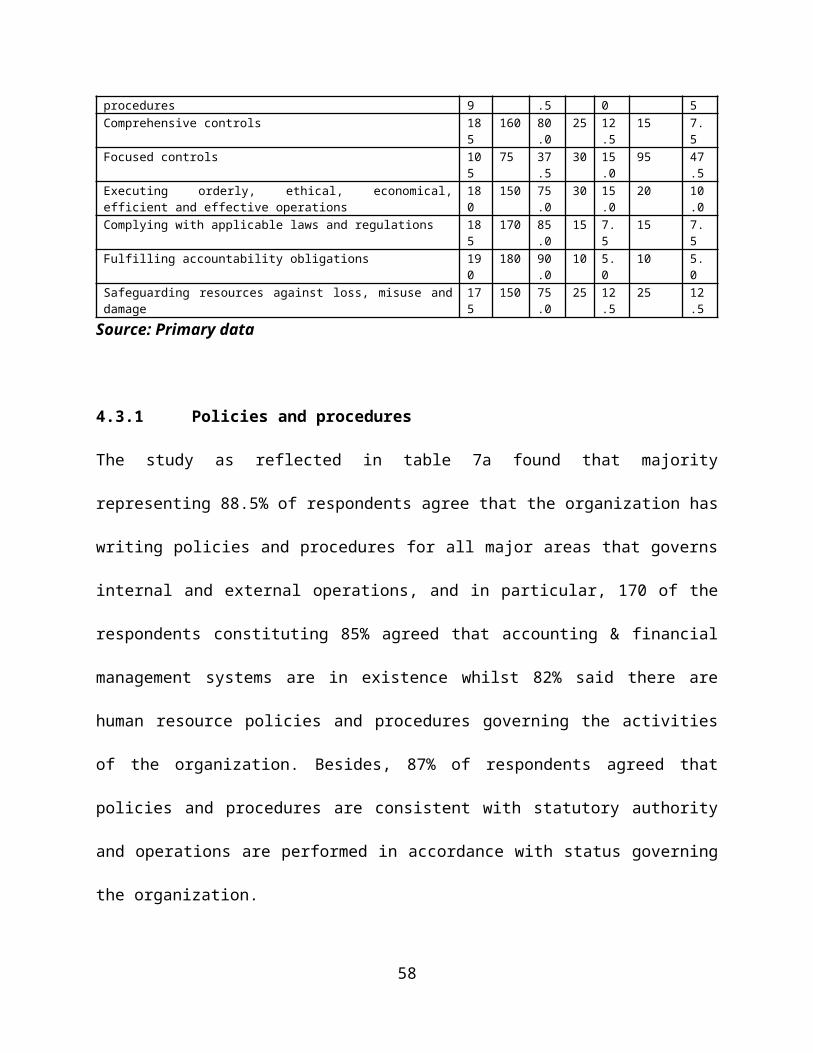

Descriptive statistics of types of controls

Table 7a: Frequencies and Percentage of key referencesORGANIZATIONAL STRUCTURE N YES % No % missi

ng%

written policies and procedures 187

180 90.0

7 3.5

13 6.5

Policies and procedures for major Areas ofoperations

181

177 88.5

4 2 19 9.5

Financial & accounting systems 182

170 85 12 6 18 9

Human resource policies & procedures 174

164 82 10 5 26 13

consistency of policies and procedures withstatus

186

174 87 12 6.0

14 7

Integration of controls into policies and 18 173 86 16 8. 11 5.

57

procedures 9 .5 0 5Comprehensive controls 18

5160 80

.025 12

.515 7.

5Focused controls 10

575 37

.530 15

.095 47

.5Executing orderly, ethical, economical,efficient and effective operations

180

150 75.0

30 15.0

20 10.0

Complying with applicable laws and regulations 185

170 85.0

15 7.5

15 7.5

Fulfilling accountability obligations 190

180 90.0

10 5.0

10 5.0

Safeguarding resources against loss, misuse anddamage

175

150 75.0

25 12.5

25 12.5

Source: Primary data

4.3.1 Policies and procedures

The study as reflected in table 7a found that majority

representing 88.5% of respondents agree that the organization has

writing policies and procedures for all major areas that governs

internal and external operations, and in particular, 170 of the

respondents constituting 85% agreed that accounting & financial

management systems are in existence whilst 82% said there are

human resource policies and procedures governing the activities

of the organization. Besides, 87% of respondents agreed that

policies and procedures are consistent with statutory authority

and operations are performed in accordance with status governing

the organization.

58

4.3.2 Integration of controls

As shown in table 6, 173 constituting 86.5% of the respondents

are of the view that controls and control objectives are built

into policies and procedures of the entity. Integrating controls

and control objectives into policies and procedures ensures that

controls permeate all aspects of the entity’s activities.

However, 16 constituting 8% of the respondents thought otherwise.

They were of the view that controls and control objectives are

not built into policies and procedures. However, 11 respondents

making up of 5.5% of the total respondents did not provide any

answer at all. If Controls are embedded in the operations of an

entity it becomes part of its infrastructure and culture. This

assertion is in line with KPMG 2009 argument that internal

controls are most effective when embedded in the operations of an

entity. By building controls into the infrastructure (policies

and procedures) of the entity as agreed to by respondents means

individuals and/or groups responsible for achievement of

objectives are also accountable for control operations and this

increases the likelihood that controls are operated properly.

59

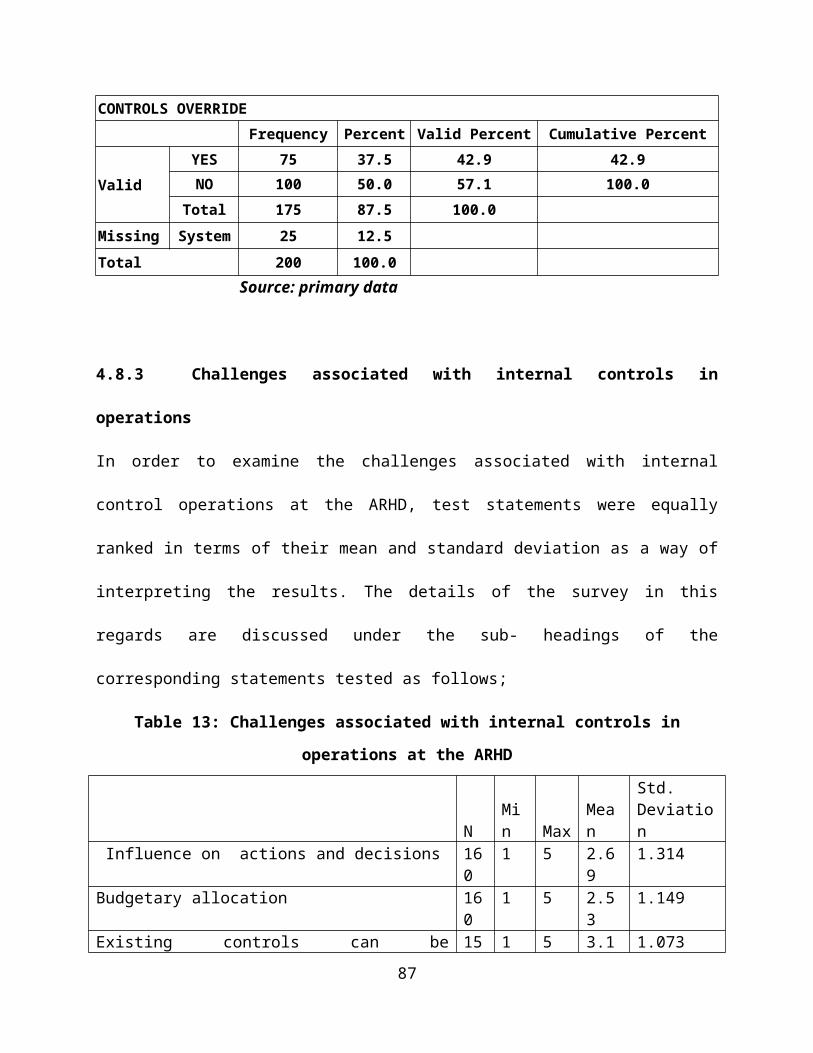

4.3.3 Comprehensive and focused internal controls

185 Out of the population of 200 provided responses as to whether

the controls in operations at the ARHD could be describe as

comprehensive or focused internal controls. Out of the 185

respondents 160 admitted that the controls in operations can be

described as comprehensive internal controls. The remaining 25

respondents representing 12.5% of the 185 respondents said the

internal controls in operations cannot be described as

comprehensive controls. 15 of the respondents however refrained

from giving any answer. Clearly majority of respondents

representing 80% of respondents assented that the controls in

operations at the ARHD is a comprehensive controls. As to whether

the controls in operations could be described as a focused

internal controls, 75 of the respondents said yes, whilst 30 said

no. the remaining 95 refrained from giving any answers. These

represents 37.5%, 15% and 47.5% respectively. The large number of

respondents who refrained from saying yes or no may be attributed

to the fact that majority of them had already assented that

comprehensive internal controls are in operations at the ARHD.

Whilst the 75 that said the control operations are focused were

60

influenced by the fact that focused control is an integral part

of comprehensive controls.

J. Pfister2009 asserts that a comprehensive control is seen as an

all-inclusive approach to internal control which duels much on

effectiveness and efficiency of operation, compliance with laws,

regulations and internal policies. The adoption and operation of

a comprehensive internal control system rhymes well with (Pfaff

and Ruud, 2007 assertion that “Internal control is pervasive

throughout any organization’s primary and secondary activities

and is inherently affected by the way management runs the

business”

4.3.4 Internal control objectives

4.3.5 Executing orderly, ethical, economical, efficient and

effective operations

150 of the respondents constituting 75% said policies and

procedures ensures executing orderly, ethical, economical,

efficient and effective operations whilst 30 of them representing

15% said the policies and procedures do not ensure executing

orderly, ethical, economical, efficient and effective operations

61

and 20 of them abstained from giving any answers. Clearly those

who said No added to those who abstained made up of 25% of the

sampled population for the study. Implying that majority of the

staffs agreed that policies and procedures ensure executing

orderly, ethical, economical, efficient and effective operations.

4.3.6 Complying with applicable laws and regulations

170 of the respondents assented that the policies and procedures

ensures compliance with applicable laws and regulations, 15 of

them dissented and the remaining 15 were not sure. These

represents 85%, 7.5% and 7.5% respectively.

4.3.7 Fulfilling accountability obligations

180 of the respondents said policies and procedures ensures

fulfillment of accountability obligations, 10 of them disagreed

and 10 did not say either Yes or No to the question. These

constitute 90%, 5% and 5% respectively. Clearly those who said No

62

and those who abstained, put together forms the minority. They

constitute 20% of the sampled population for the study.

4.3.8 Safeguarding resources against loss, misuse and damage

Lastly in respect of safeguarding resources against loss, misuse

and damage 150 of the respondent said yes and 25 of them said no,

whilst 25 of them refrained from saying yes or no. clearly those

who affirmed that the policies and procedures ensures

Safeguarding resources against loss, misuse and damage were in

the majority. They constituted 75% of the 200 respondents.

Majority of respondents did consent that the policies and

procedures among others ensures the 1) Executing orderly,

ethical, economical, efficient and effective operations, 2)

Complying with applicable laws and regulations, 3) Fulfilling

accountability obligations and 4) Safeguarding resources against

loss, misuse and damage. This is in consonance with the

perspective of the INTOSAI (2004) on internal controls.

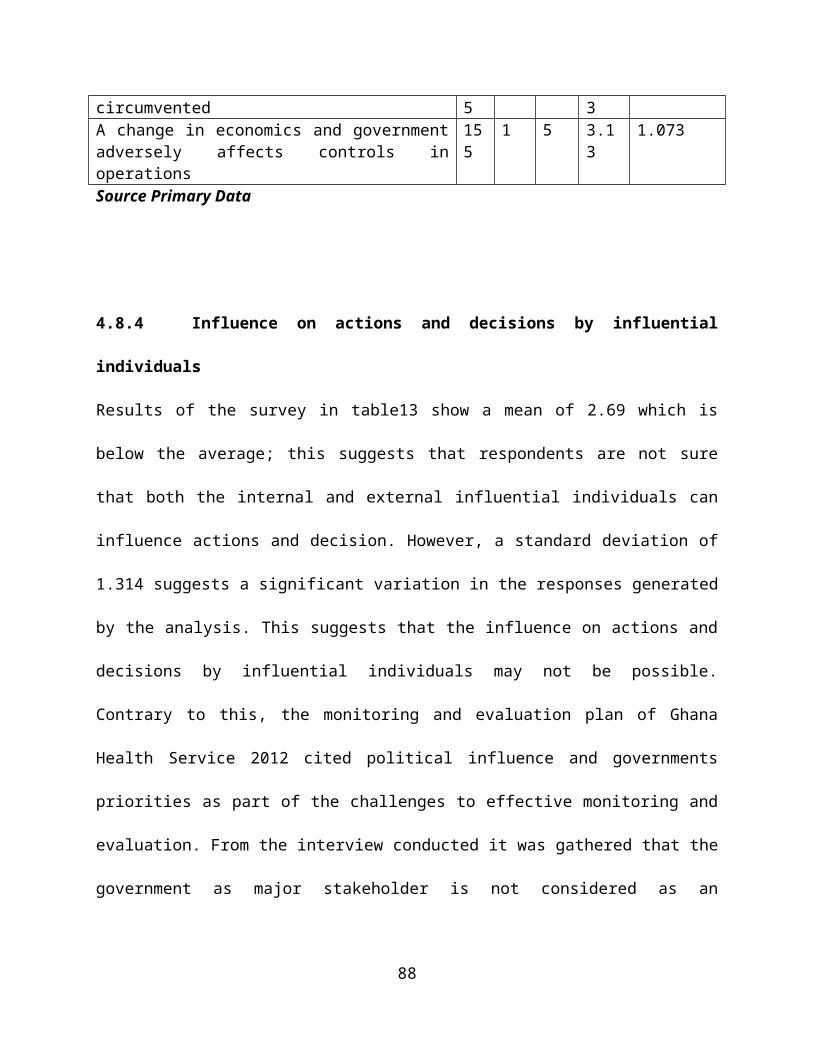

4.4.0 Effectiveness of controls in operations

63

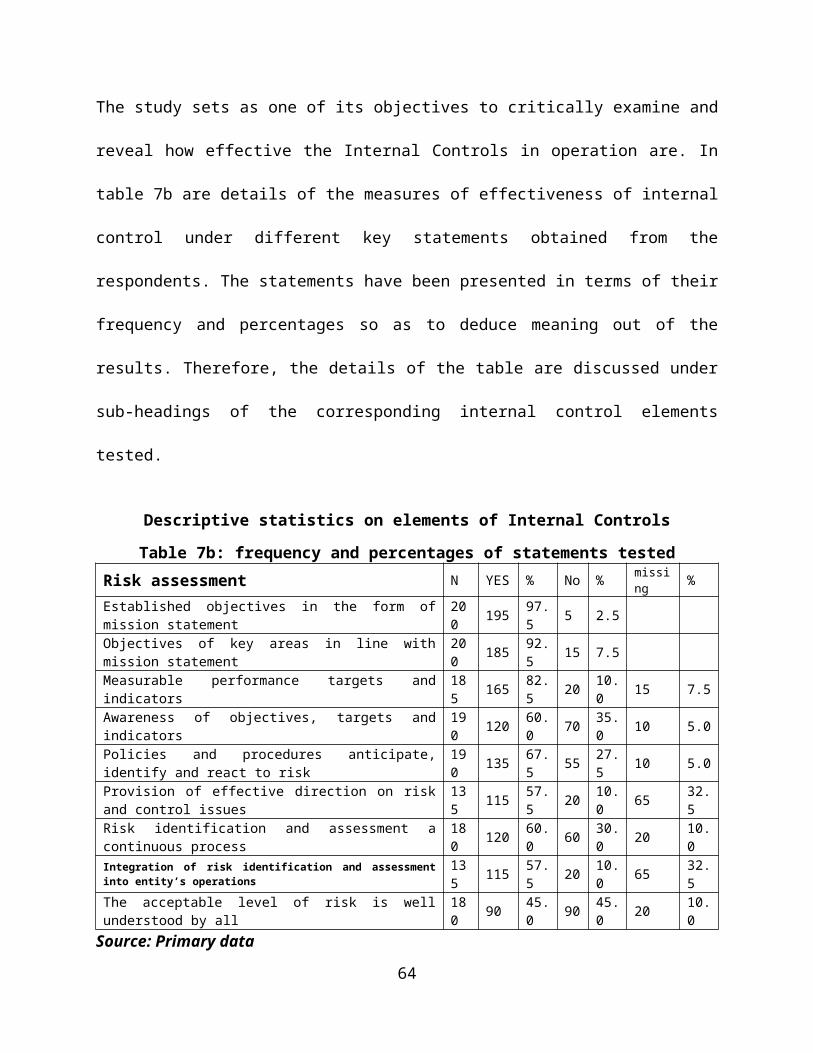

The study sets as one of its objectives to critically examine and

reveal how effective the Internal Controls in operation are. In

table 7b are details of the measures of effectiveness of internal

control under different key statements obtained from the

respondents. The statements have been presented in terms of their

frequency and percentages so as to deduce meaning out of the

results. Therefore, the details of the table are discussed under

sub-headings of the corresponding internal control elements

tested.

Descriptive statistics on elements of Internal Controls

Table 7b: frequency and percentages of statements testedRisk assessment N YES % No % missi

ng %Established objectives in the form ofmission statement

200 195 97.

5 5 2.5

Objectives of key areas in line withmission statement

200 185 92.

5 15 7.5

Measurable performance targets andindicators

185 165 82.

5 20 10.0 15 7.5

Awareness of objectives, targets andindicators

190 120 60.

0 70 35.0 10 5.0

Policies and procedures anticipate,identify and react to risk

190 135 67.

5 55 27.5 10 5.0

Provision of effective direction on riskand control issues

135 115 57.

5 20 10.0 65 32.

5Risk identification and assessment acontinuous process

180 120 60.

0 60 30.0 20 10.

0Integration of risk identification and assessmentinto entity’s operations

135 115 57.

5 20 10.0 65 32.

5The acceptable level of risk is wellunderstood by all

180 90 45.

0 90 45.0 20 10.

0Source: Primary data

64

4.4.1 Risk assessment

4.4.2 Established objectives, related plans and key

performance indicators

Given 195 yes responses in table 7b above, which represents 97.5%

of the respondent’s clearly indicates that respondents agreed

that there exist a mission statement that reflects the general

objectives of the organization. Besides, with a percentage value

of 92.5% respondents affirm that the objectives of key units and

department are in alignment with the organization’s mission

statements. There is also a general acceptance that objectives

and related plans include measurable performance targets and

indicators as expressed in a yes value of 165 constituting 82.5%

of responses in table 7b above. This is consistent with KPMG 2009

processes for review of effectiveness of internal controls which

makes establishment of objectives, linked at different levels and

internally consistent as prerequisite to risk assessment. It

advocates for identification of all the strategic business

objectives which are vital to the success of the organization.

65

4.4.3 Awareness of objectives, targets and indicators

Considering the yes value of 120 which constitute 60% of

respondent shows that objectives have been well communicated and

employees in all areas are fully aware of objectives, targets and

key performance indicators so as to provide effective directions

to employees on risk and control issues. By making the objectives

clear and creating awareness, the likelihood of overlooking key

business risks which threaten the survival of the organization or

could lead to a significant impact on its performance or

reputation will be reduced. However, giving the values of 70 and

10 for No and missing respectively means that a considerable

number of staffs of the ARHD are not aware of stated objectives,

targets and performance indicators. From the interview conducted

it was clear that only the senior managers and head of units

have a clear understanding of set objectives and are aware of

targets and indicators. This was however attributed to inadequate

guidance and processes for setting targets and weak process

indicators.

4.4.4 Risk identification and assessment process

66

The Respondents by the yes value of 135 which constitute 67.5%

said the Directorates policies and procedures are designed to

anticipate, identify and react to risk. It also provides

effective direction on risk and control issues as indicated in

table 7b by the yes frequency value of 115 and percentage value

of 57.5%. Additionally, majority of the respondents as

represented by a percentage value 60% affirmed that risk

identification and assessment is a continuous process in the

organization. This is also in line with KPMG review on internal

control practical guide, 1999. This is of the view that corporate

objective and environment in which firms operate in this

contemporary business world are continuously changing.

Consequently, the risks that firms are encountering are

constantly evolving too and In order to ensure faster adaptation

to these changes, an effective internal control must necessarily

be responsive to changes. Successful risk management and internal

control therefore depends on regular appraisal of the nature and

extent of risk.

67

4.4.5 Integration of risk identification and assessment into

entity’s operations

115 of the respondents representing 57.5% agree that risk

identification and assessment are integrated into the entity’s

operations. Respondents were evenly divided as to whether the

organization risk appetite is well defined and understood by

management and others within the Directorate. As depicted in

table 7b above, 90 of the respondents agree that the acceptable

level of risk is well understood by all whilst 90 disagree.

However, giving a frequency value of 20 of miss outs coupled with

the 90 respondents who dissented clearly indicates that the

acceptable level of risk is not well understood by significant

number of staffs. This implies that the likely hood of

overlooking a significant risk by a significant number of staff

is higher and might compromise the effectiveness of internal