Professional ethics and the Tax Professional- Module 1 Jan Dijkman BA LLB LLM H Dip Tax Adv Dip Labour Law Certified Ethics Officer

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Professional ethics and the Tax Professional-Module 1

Jan Dijkman

BA LLB LLM H Dip Tax Adv Dip Labour Law Certified Ethics Officer

Agenda

What is ethics?

Why is ethics important for Tax Professionals?

Professions and ethics

The Code of Professional Conduct in Relation to Taxation

Fundamental principles

Disciplinary trends

Solving ethical dilemmas – some guidelines

Final thoughts

Agenda for Module 1

What is ethics?

Why is ethics important for Tax Professionals?

Professions and ethics

The Code of Professional Conduct in Relation to Taxation

Fundamental principles

Disciplinary trends

Solving ethical dilemmas – some guidelines

Final thoughts

What is ethics?

Oxford Dictionary: “Set of principles of morals, rules of conduct”

Cambridge Dictionary: “A system of accepted beliefs which control behaviour; the study of what is morally right and what is not”

Wikipedia: “Ethics is a branch of philosophy that involves concepts of right and wrong conduct. Ethics seeks to resolve questions of dealing with human morality –concepts such as good and evil, right and wrong, virtue and vice, justice and crime”

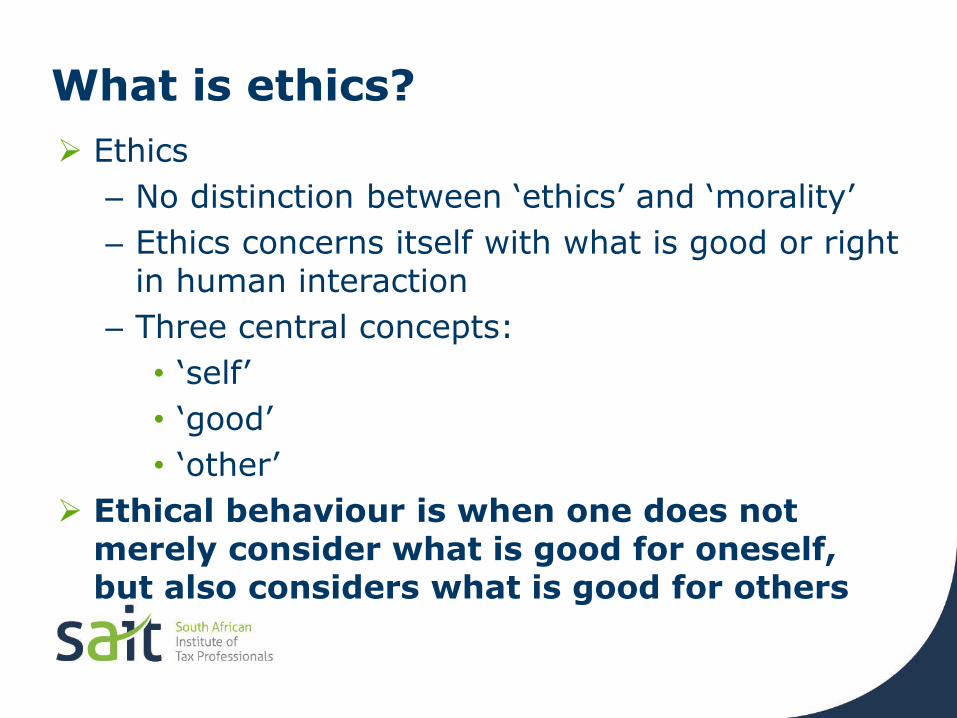

What is ethics?

Ethics

– No distinction between ‘ethics’ and ‘morality’

– Ethics concerns itself with what is good or right in human interaction

– Three central concepts:

• ‘self’

• ‘good’

• ‘other’

Ethical behaviour is when one does not merely consider what is good for oneself, but also considers what is good for others

What is ethics?

Ethics deals with well-based standards of how people ought to act and is prescriptive

Values and ethics

Law and ethics

Grey areas

Ethical relativism

Situation ethics

Conundrum

Understanding ethics is easy, being ethical isn’t

Why the emphasis on ethics?

King III Code of Corporate Governance

First governance principle – ethical leadership and corporate citizenship

Provide effective leadership based on an ethical foundation

Ethical leaders should –

Do business ethically

Set the values to which the company will adhere

Ensure that conduct is aligned to values and is adhered to in all aspects of the business

Social and ethics committee – Companies Act

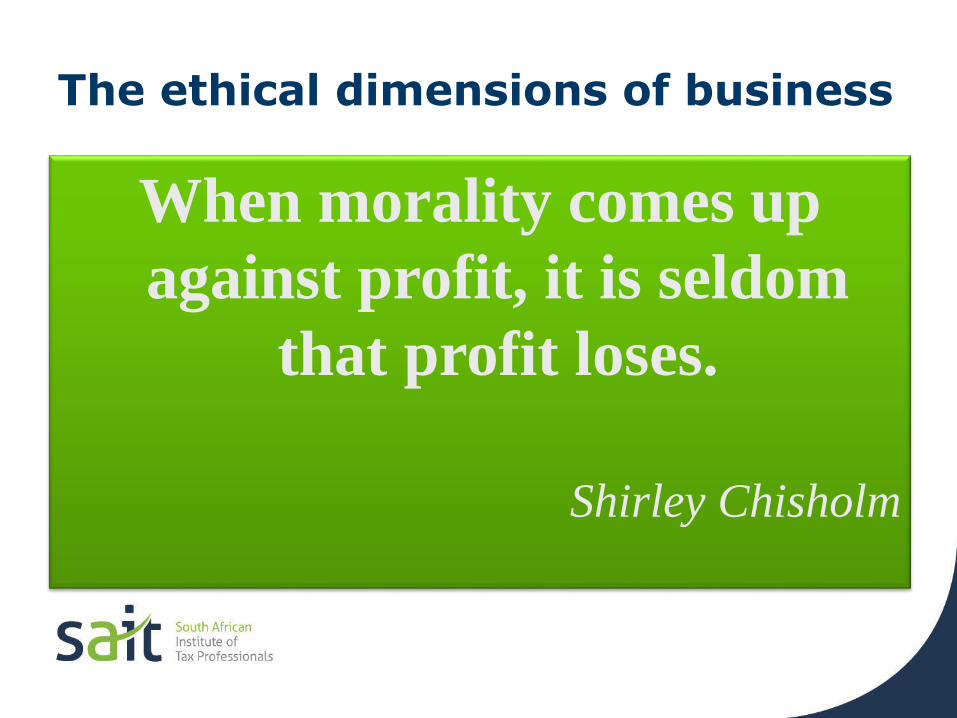

The ethical dimensions of business

When morality comes up

against profit, it is seldom

that profit loses.

Shirley Chisholm

Why is ethics important for Tax Professionals?

Integrity is the basis of a sound tax system

Integrity means that a person acts on principle

The ‘Golden Rule’ of ethics

Why is ethics important for Tax Professionals?

What is a profession?

A profession is distinguished by certain characteristics:

– Mastery of a particular intellectual skill, acquired by training and education;

– Acceptance of duties to society as a whole in addition to duties to the client or employer;

– An outlook which is essentially objective;

– Rendering personal services that adhere to a high standard of conduct and performance

Professional ethics

The norms and guidelines for moral and ethical behaviour for professionals. Guidelines for professional ethics are usually codified in codes of ethics or codes of professional conduct

What is the purpose of a Code?

Distinguishing characteristic of a profession is the adherence to ethical standards embodied in a professional Code

Code establishes ethical requirements for members of the profession

Code facilitates accountability, responsibility and trust

Why do we need an ethics code?

Because of diverse make-up of profession, need exists for common understanding of ethics

Hence the Code of Professional Conduct

Characteristic of a profession that there is a commitment to ethical behaviour

Good people do not need laws to tell them to act responsibly, while bad people will find a way around the laws.

PLATO

The Code of Professional Conduct in Relation to Taxation

What is the purpose of the SAIT Code?

Provides guidance on proper conduct for Tax Professionals

Adherence to the Code assists in protecting the public interest

Assists Tax Professionals to resist pressure to violate the Code

Provides a mechanism by which action can be taken against unethical conduct by Tax Professionals

Helps to achieve the objectives of the Tax Profession

Structure of the SAIT Code

Combination of principles-based / rules-based Code. What’s the difference?

Fundamental principles

Integrity

Objectivity

Professional competence and due care

Confidentiality

Professional behaviour

Threats

Self-interest threat

Self-review threat

Advocacy threat

Familiarity threat

Intimidation threat

Self - interest threats

The threat that a financial or other interest will inappropriately influence the Tax Professional’s judgment or behaviour

Examples:

Undue dependence on total fees from a client

Concern about losing a client

Self - review threats

The threat that a Tax Professional will not appropriately evaluate the results of a previous judgment made or service performed by the Tax Professional, or by another individual within the Tax Professional’s firm, on which the Tax Professional will rely when forming a judgment as part of providing a current service

Examples:

Discovery of significant error during re-evaluation of work

Having prepared the original data

Advocacy threats

The threat that a Tax Professional will promote a client’s position to the point that the Tax Professional’s objectivity is compromised

Examples:

Acting as advocate on behalf of assurance client in tax litigation or tax disputes

Familiarity threats

The threat that due to a long or close relationship with a client, a Tax Professional will be too sympathetic to their interests or too accepting of their work

Examples:

Long association of senior staff with client

Intimidation threats

The threat that a Tax Professional will be deterred from acting objectively because of actual or perceived pressures, including attempts to exercise undue influence over the Tax Professional

Examples:

Threatened with dismissal or replacement

Threatened with litigation or being reported to professional body

Safeguards

Safeguards are actions or other measures that may eliminate threats or reduce them to an acceptable level. They fall into two broad categories:

(a) Safeguards created by the profession, legislation or regulation; and

(b) Safeguards in the work environment.

Safeguards

Safeguards include:– Educational, training and experience requirements

– Continuing professional development requirements

– Compliance with tax standards

– Professional monitoring and disciplinary procedures

– Involving another Tax Professional to review the work undertaken

– Consulting an independent third party

Work environment safeguards include:– Leadership

– Published policies and procedures

Fundamental principles

Integrity

Objectivity

Professional competence and due care

Confidentiality

Professional behaviour

General compliance with the fundamental principles (1)

Most important duty is to ensure that actions comply with the law

Secondary duty to carry out the agreed tasks with the requisite care and skill

Need to advise client of obligations and the consequences of non-compliance

Must act in best interests of client (within the law!) Concept of ‘one client at a time’

Must act within the law

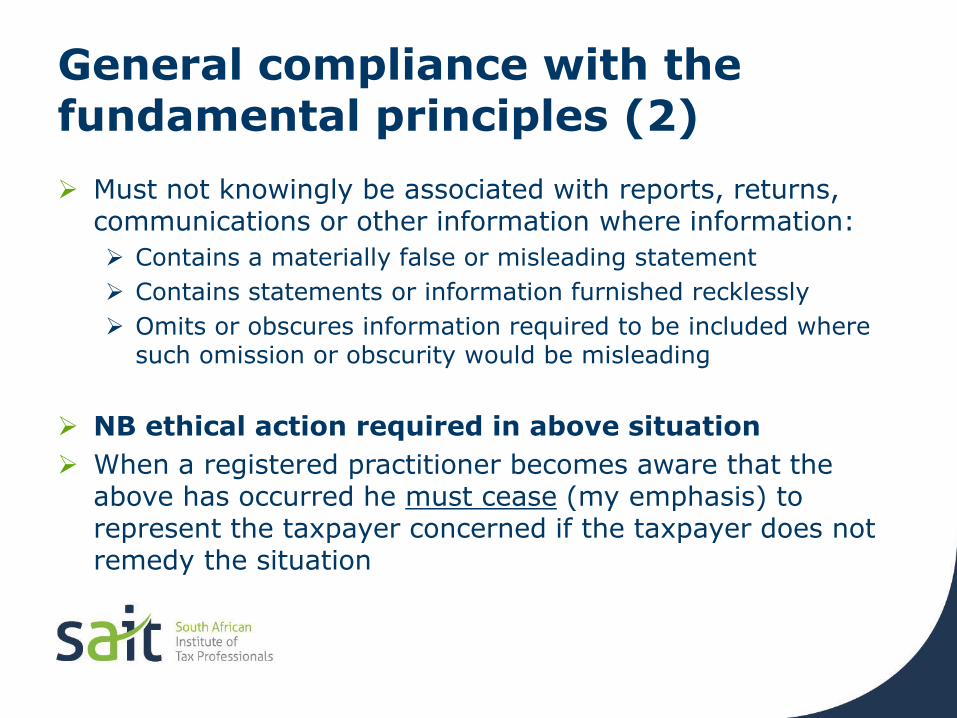

General compliance with the fundamental principles (2)

Must not knowingly be associated with reports, returns, communications or other information where information:

Contains a materially false or misleading statement

Contains statements or information furnished recklessly

Omits or obscures information required to be included where such omission or obscurity would be misleading

NB ethical action required in above situation

When a registered practitioner becomes aware that the above has occurred he must cease (my emphasis) to represent the taxpayer concerned if the taxpayer does not remedy the situation

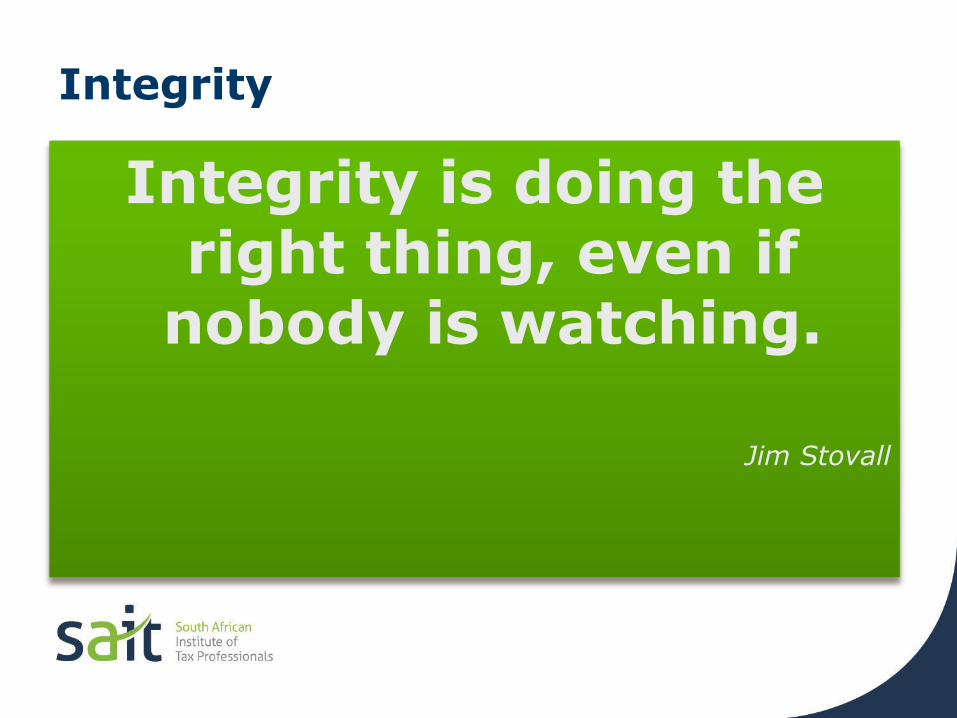

Integrity

Integrity is doing the right thing, even if

nobody is watching.

Jim Stovall

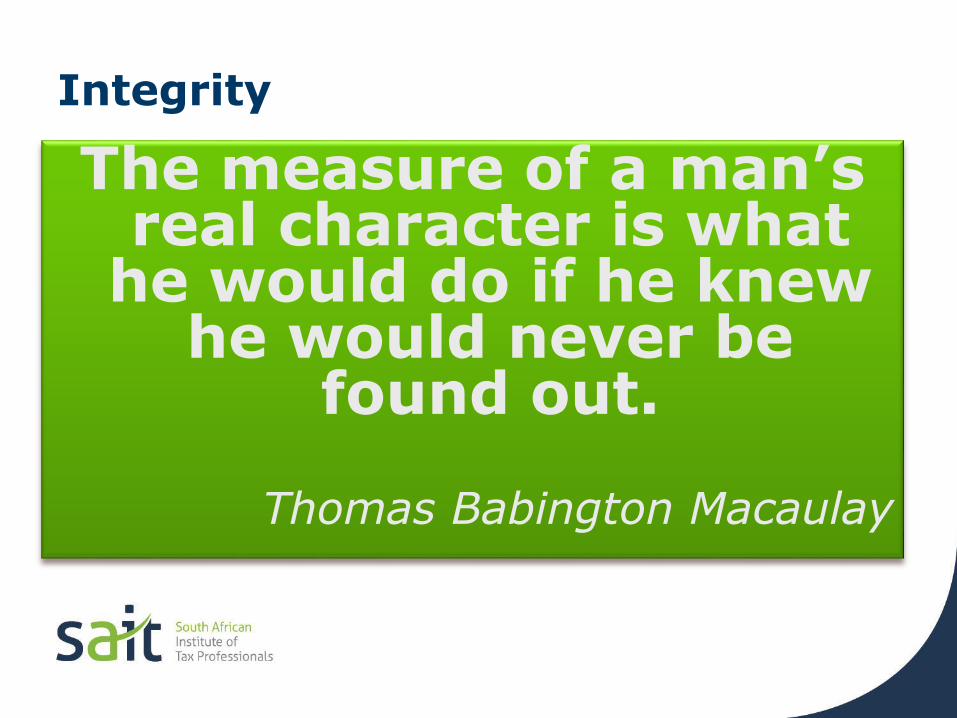

Integrity

The measure of a man’s real character is what

he would do if he knew he would never be

found out.

Thomas Babington Macaulay

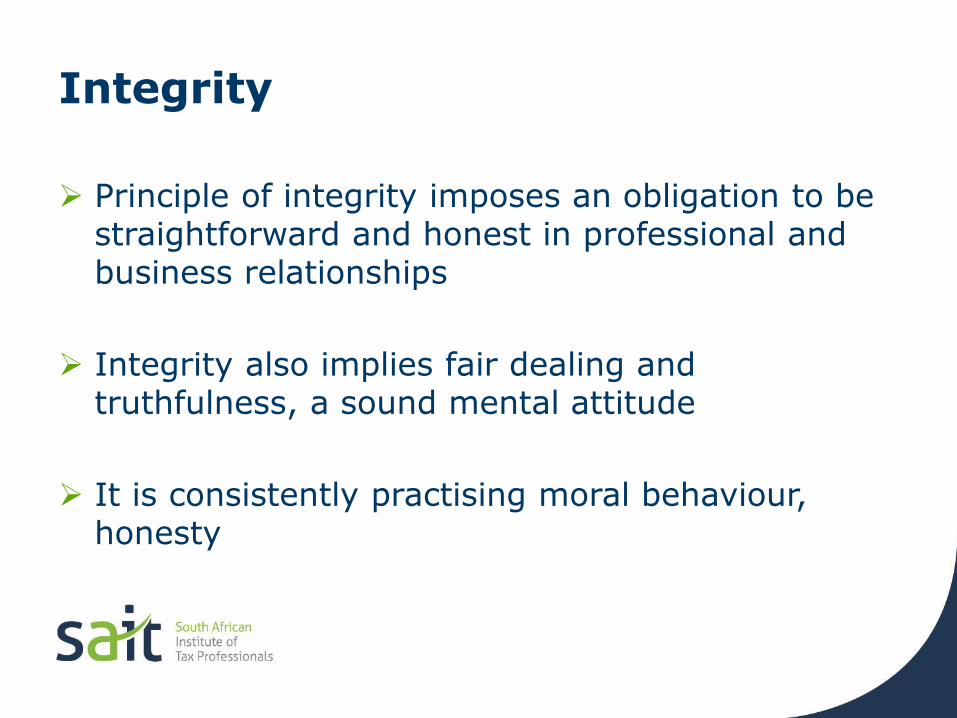

Integrity

Principle of integrity imposes an obligation to be straightforward and honest in professional and business relationships

Integrity also implies fair dealing and truthfulness, a sound mental attitude

It is consistently practising moral behaviour, honesty

Objectivity

Principle of objectivity imposes an obligation not to compromise professional or business judgment because of bias, conflict of interest or the undue influence of others

Objectivity is having an impartial mental attitude, fairness, taking a balanced approach

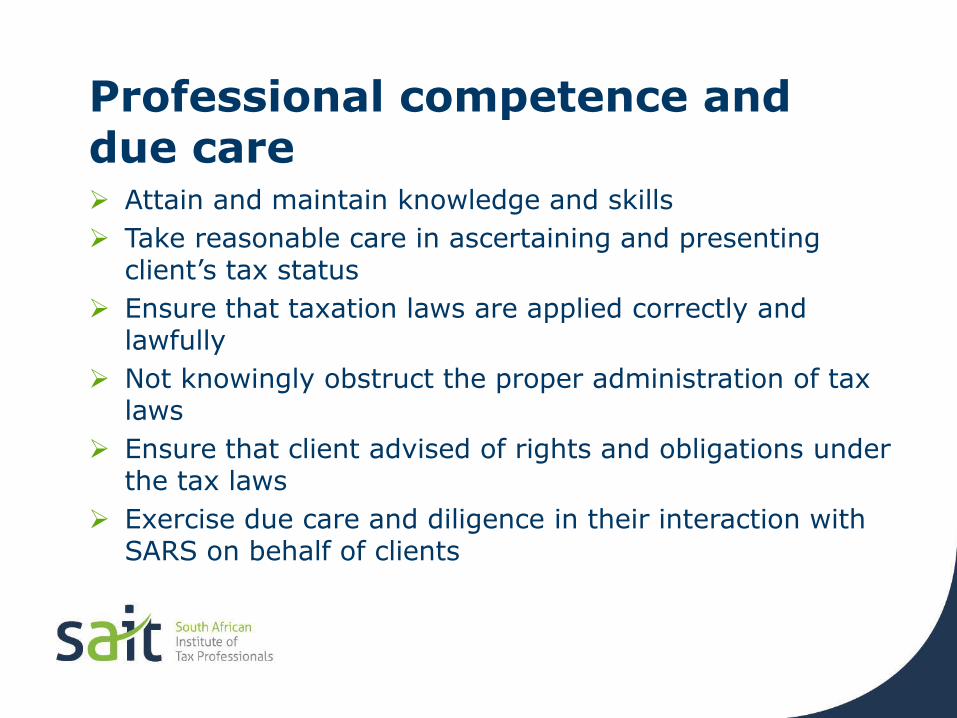

Professional competence and due care

Principle imposes obligation to:

Maintain professional knowledge and skill at the level to ensure competent professional service

Act diligently in accordance with applicable technical and professional standards

South African Taxation Standards

Preface to SA Tax Standards

SATS 1000: Knowledge of the client

SATS 2000: Filing tax returns

SATS 3000: Procedural aspects of preparing tax returns

SATS 4000: Use of estimates

SATS 5000: Departure from a position previously determined in an administrative proceeding or court decision

SATS 6000: Knowledge of error: Tax return preparation

SATS 7000: Knowledge of error: Administrative proceedings

SATS 8000: Form and content of advice to taxpayers

South African Taxation StandardsSATS 1000: Knowledge of the client

Tax professional must:

Confirm who is his client

Confirm that the client is who he says he is

Consider obtaining references

Identify any potential conflicts of interest

Satisfy initial obligations under AML regulations

Tax professional must become familiar with circumstances of client:

Understand scope of services

Understand client’s business and attitude to risk

Confirm terms of appointment in letter of engagement

South African Taxation StandardsSATS 2000: Filing tax returns

When involved with filing tax returns, the tax professional:

Should not recommend an unrealistic position

Should not prepare a return that is contrary to the Standards, the Code and tax law

Can take contrary view provided that appropriate disclosure is made and client advised of risks

Taxpayer has the final responsibility for positions taken on the return

In adopting a filing position, the tax professional must perform adequate and appropriate research to support the position

South African Taxation StandardsSATS 3000: Procedural aspects of preparing tax returns

Tax professional may rely in good faith on information provided by the taxpayer, but should make reasonable enquiries in certain circumstances

Confirmation from the client should be obtained if certain conditions need to be met before a certain outcome is achieved

Tax professional must consider all information known to him, even from other sources, but keeping confidentiality in mind

As taxpayer has ultimate responsibility for the contents of a return, tax professional must encourage full disclosure, and make taxpayer aware of consequences of non-disclosure

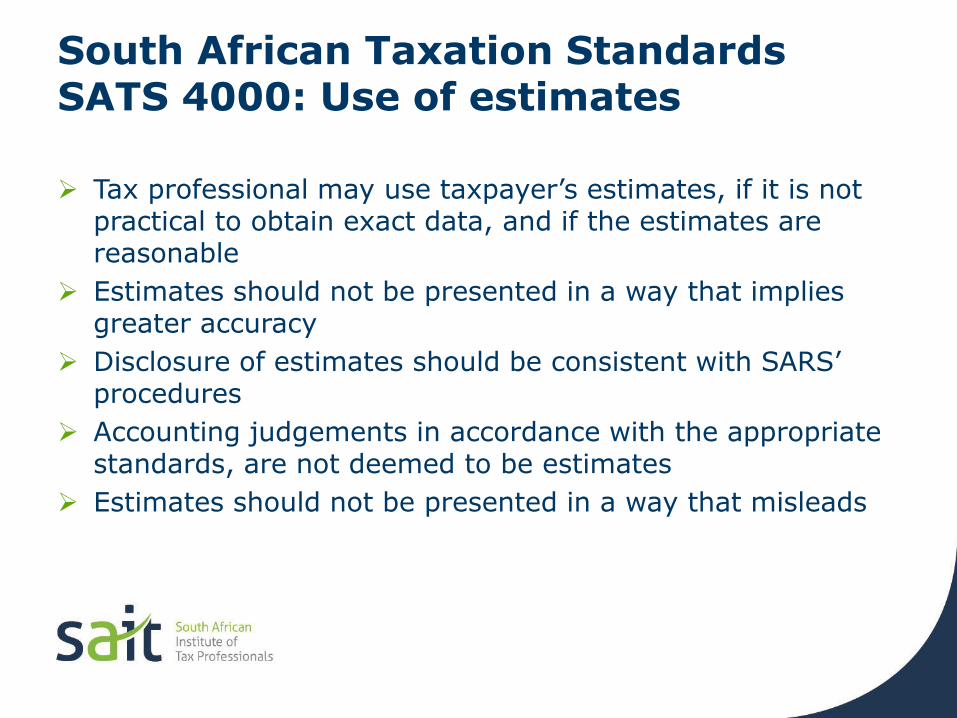

South African Taxation StandardsSATS 4000: Use of estimates

Tax professional may use taxpayer’s estimates, if it is not practical to obtain exact data, and if the estimates are reasonable

Estimates should not be presented in a way that implies greater accuracy

Disclosure of estimates should be consistent with SARS’ procedures

Accounting judgements in accordance with the appropriate standards, are not deemed to be estimates

Estimates should not be presented in a way that misleads

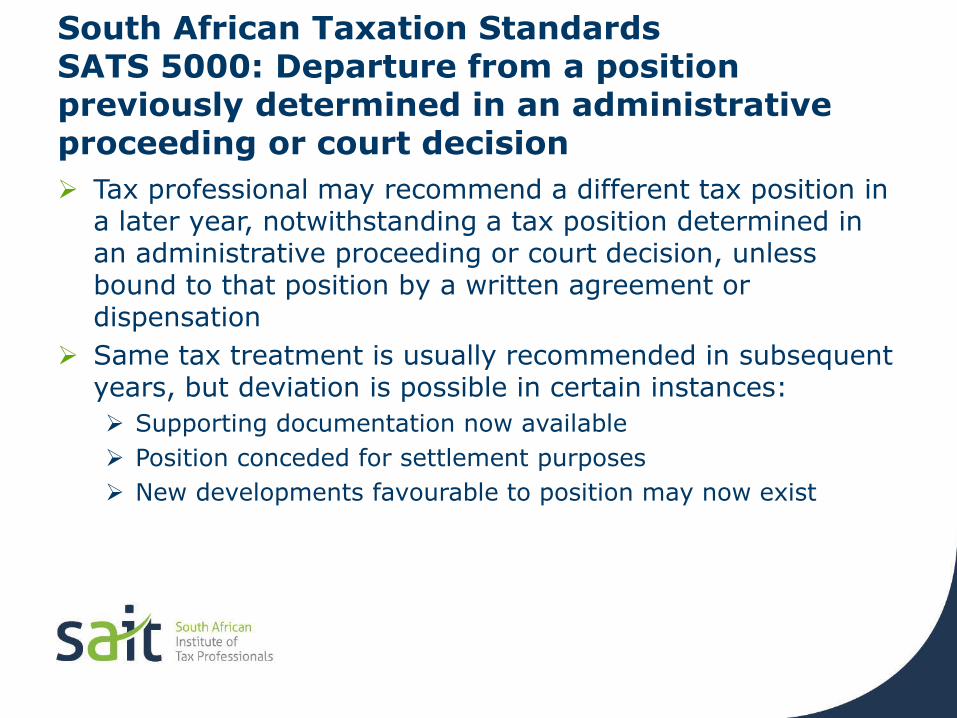

South African Taxation StandardsSATS 5000: Departure from a position previously determined in an administrative proceeding or court decision

Tax professional may recommend a different tax position in a later year, notwithstanding a tax position determined in an administrative proceeding or court decision, unless bound to that position by a written agreement or dispensation

Same tax treatment is usually recommended in subsequent years, but deviation is possible in certain instances:

Supporting documentation now available

Position conceded for settlement purposes

New developments favourable to position may now exist

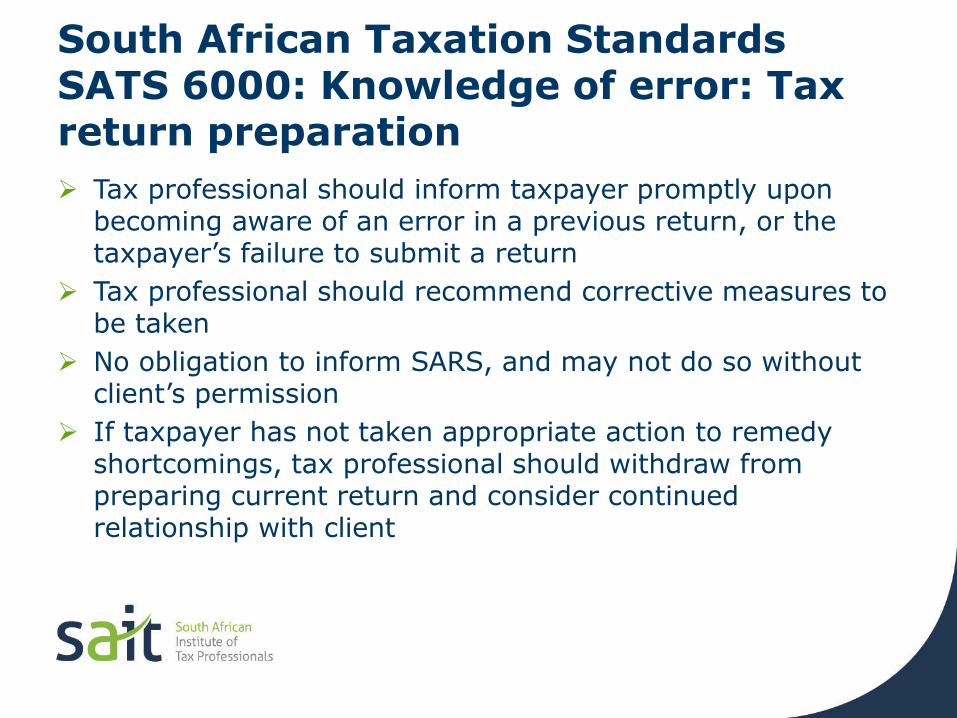

South African Taxation StandardsSATS 6000: Knowledge of error: Tax return preparation

Tax professional should inform taxpayer promptly upon becoming aware of an error in a previous return, or the taxpayer’s failure to submit a return

Tax professional should recommend corrective measures to be taken

No obligation to inform SARS, and may not do so without client’s permission

If taxpayer has not taken appropriate action to remedy shortcomings, tax professional should withdraw from preparing current return and consider continued relationship with client

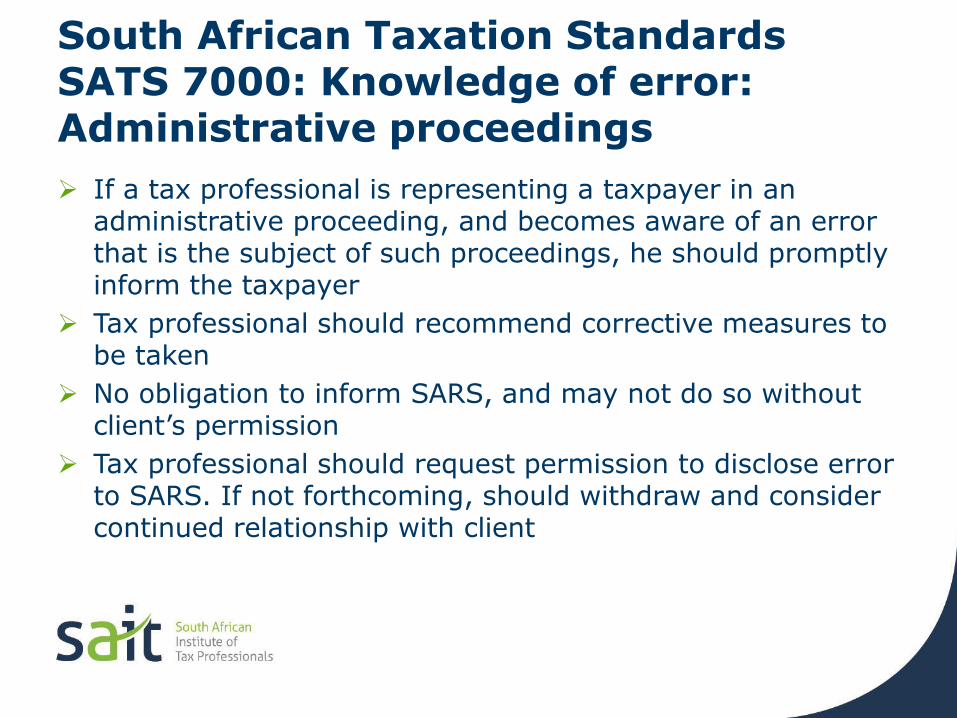

South African Taxation StandardsSATS 7000: Knowledge of error: Administrative proceedings

If a tax professional is representing a taxpayer in an administrative proceeding, and becomes aware of an error that is the subject of such proceedings, he should promptly inform the taxpayer

Tax professional should recommend corrective measures to be taken

No obligation to inform SARS, and may not do so without client’s permission

Tax professional should request permission to disclose error to SARS. If not forthcoming, should withdraw and consider continued relationship with client

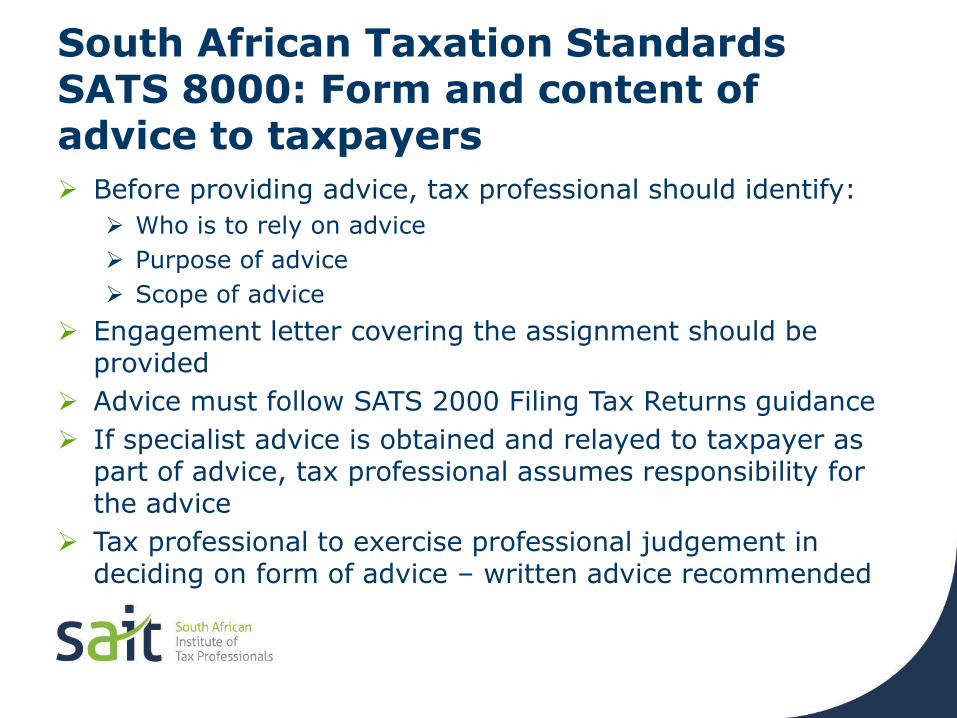

South African Taxation StandardsSATS 8000: Form and content of advice to taxpayers

Before providing advice, tax professional should identify:

Who is to rely on advice

Purpose of advice

Scope of advice

Engagement letter covering the assignment should be provided

Advice must follow SATS 2000 Filing Tax Returns guidance

If specialist advice is obtained and relayed to taxpayer as part of advice, tax professional assumes responsibility for the advice

Tax professional to exercise professional judgement in deciding on form of advice – written advice recommended

Professional competence and due care Attain and maintain knowledge and skills

Take reasonable care in ascertaining and presenting client’s tax status

Ensure that taxation laws are applied correctly and lawfully

Not knowingly obstruct the proper administration of tax laws

Ensure that client advised of rights and obligations under the tax laws

Exercise due care and diligence in their interaction with SARS on behalf of clients

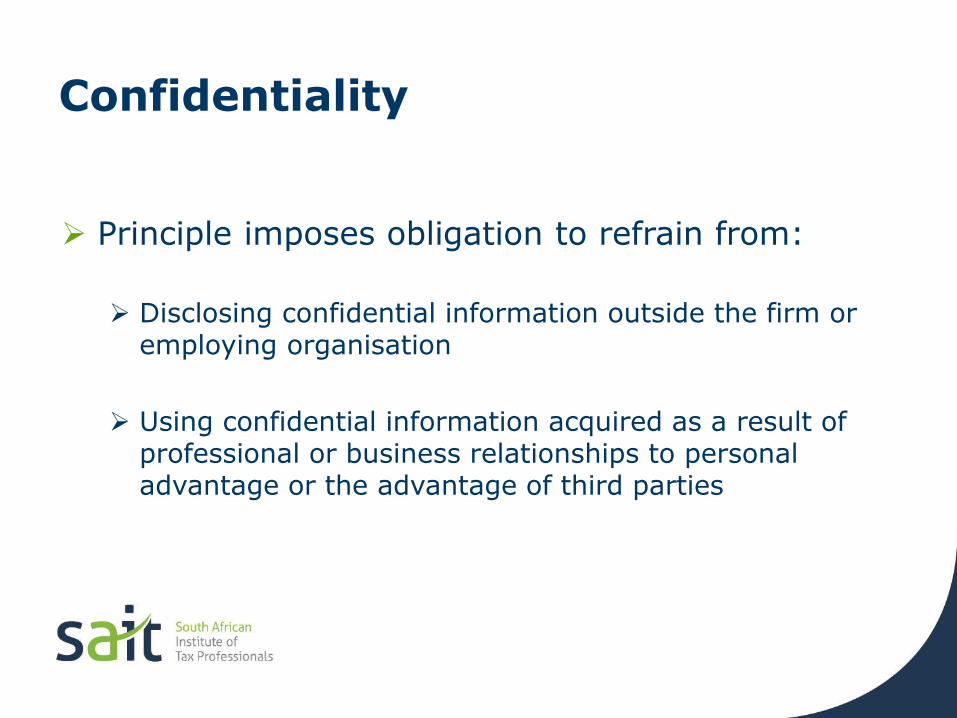

Confidentiality

Principle imposes obligation to refrain from:

Disclosing confidential information outside the firm or employing organisation

Using confidential information acquired as a result of professional or business relationships to personal advantage or the advantage of third parties

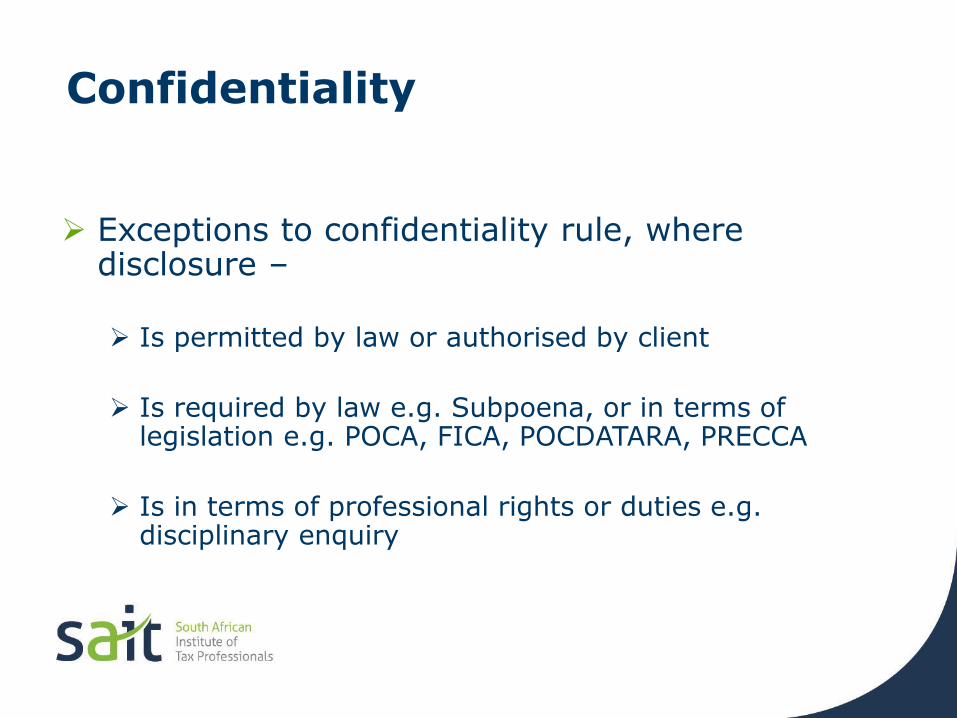

Confidentiality

Exceptions to confidentiality rule, where disclosure –

Is permitted by law or authorised by client

Is required by law e.g. Subpoena, or in terms of legislation e.g. POCA, FICA, POCDATARA, PRECCA

Is in terms of professional rights or duties e.g. disciplinary enquiry

Confidentiality and legal professional privilege

What is ‘legal professional privilege’?

Requirements for legal professional privilege to be claimed:

Communications made to a legal advisor acting in a professional capacity

Information must have been supplied in confidence

Information must have been supplied for purpose of pending litigation or obtaining professional advice

Client must claim the privilege

Responding to requests for information by SARS and third parties

If in doubt about disclosure, obtain client’s consent (preferably in writing)

Professional behaviour

Principle imposes an obligation to comply with relevant laws and regulations and avoid any action that he/she knows or should know may bring discredit to the profession

Professional behaviour

Act in a way that is consistent with the reputation of the profession

Refrain from misconduct

Act with courtesy and consideration to all third parties

Professional behaviour –Relationship with client (1)

Relationship should be governed by an appropriate letter of engagement

Set out in sufficient detail the ‘who, what, by when, by whom, and how much’

Ethical assistance

Tax professionals are urged to include the following statement: “We will observe the professional rules and guidelines of our professional Institute and accept instructions to act for you on the basis that we will act in accordance with those guidelines”

Comply with tax standard SATS 1000 – engagement letter must be obtained

Professional behaviour –Relationship with client (2)

Every contractual relationship should be covered in separate engagement letters

Basis of agreement is that client is prepared to disclose all necessary information to Tax Professional

Failure to do so should lead to Tax Professional considering their continued association with the client

If relationship is terminated, Tax Professional must update client wrt their tax position in writing

Keep detailed notes, get written confirmation of oral advice given

Obtain specialist knowledge when necessary

Remember ‘Confidentiality’ fundamental principle

Questions?

58

The Code of Professional Conduct in Relation to Taxation

... To be continued in Module 2

Related Documents