PROCAMS 2005 Chris Chinnock Insight Media

PROCAMS 2005 Chris Chinnock Insight Media. It’s a Jungle Out There A 10,000 foot view of the competitive landscape in consumer display markets.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PROCAMS 2005

Chris Chinnock

Insight Media

It’s a Jungle Out There

A 10,000 foot view of the competitive landscape in consumer display markets

Focus– Only market research firm with an exclusive

focus on microdisplay-based products

Products & Services– Newsletters– Reports– Conferences– Consulting Services

Insight Media Overview

The TV Revolution is Underway

CRT to Multiple Technologies– Thin CRTs– Projection

Front and Rear CRT, LCD, DLP, LCOS technologies

– LCD– Plasma

4:3 to 16:9 Analog to Digital Standard Definition to High Definition

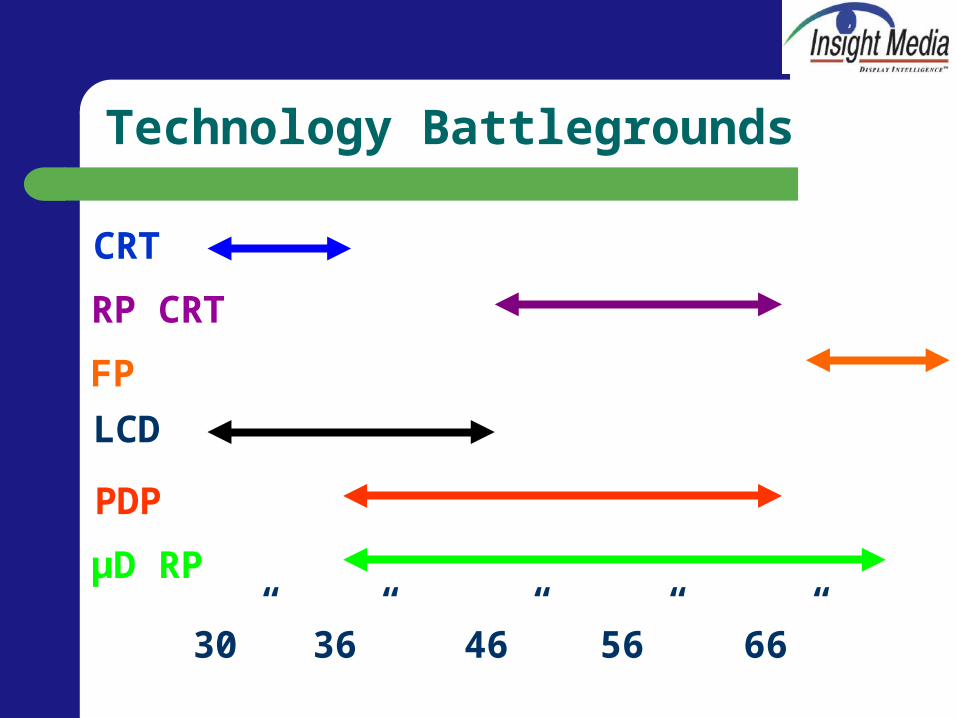

Technology Battlegrounds

30” 36” 46” 56” 66”

CRT

RP CRT

FP

LCD

PDP

µD RP

The Weapons

Screen Size Resolution Brightness Contrast Price Form Factor Cosmetics Features

Training Promotion Brand Channel Supply

Chain

Big Screen Displays Increasing

Over 30" Unit Share of Total TV Market

0%

5%

10%

15%

20%

25%

30%

35%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008

ASPs rising too – How many industries can claim that?

The Buying Process

Promotion, friends motivate into stores PDP-TVs attract most attention Price may push to

– Different Technology– EDTV

Consumer gets educated– Resolution, DVR, TiVo, home theater, etc.

Leaves frustrated to learn more or give up

Retail Environment

New brands popping up rapidly– Retailers, Chinese, Taiwanese, Korean, others

New ways to buy TVs– E-tailers, PC/IT channel, warehouse clubs

Consumers buy on:– Price– Image quality– Form factor, features & style

Consumers don’t really care about technology

The After Purchase Reality

Too complicated to set up Too complicated to operate/too many remotes DVDs/HDTV looks great NTSC looks bad Far more peculiarities to deal with than an

ordinary TV

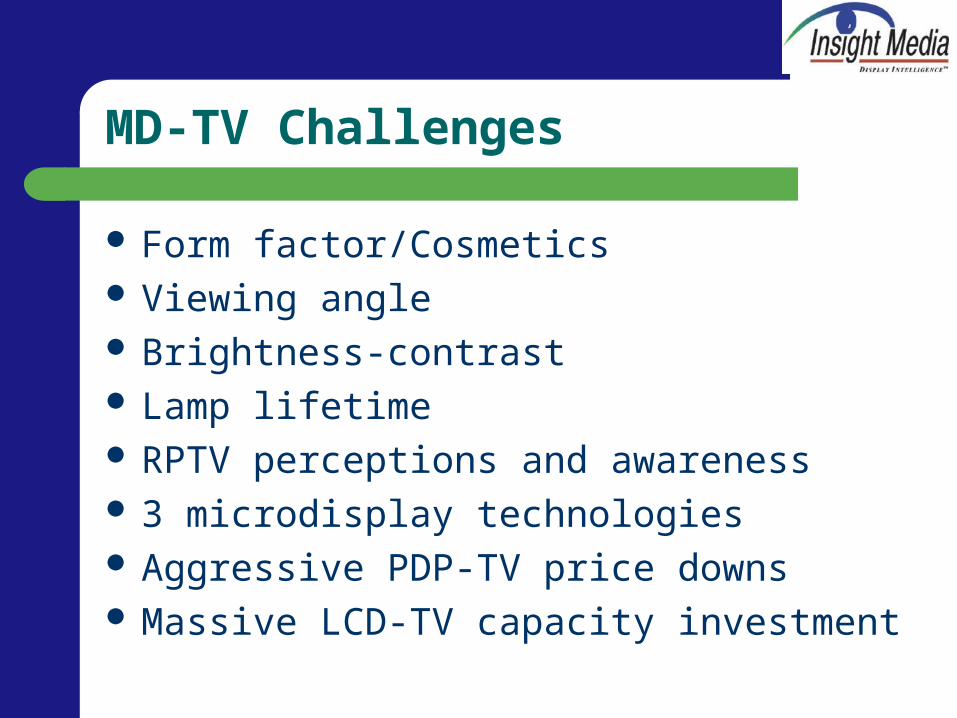

MD-TV Challenges

Form factor/Cosmetics Viewing angle Brightness-contrast Lamp lifetime RPTV perceptions and awareness 3 microdisplay technologies Aggressive PDP-TV price downs Massive LCD-TV capacity investment

Home Front Projection Challenges

Wide range in prices and quality of projectors– $1,300 to $13K– Potentially best $/screen size value

Complicated system– Projector, screen, accessories

Needs installation– Who will do this?

Consumers need education– Who will do it?

Requires significant floor space to sell it– Only acceptable for big margins

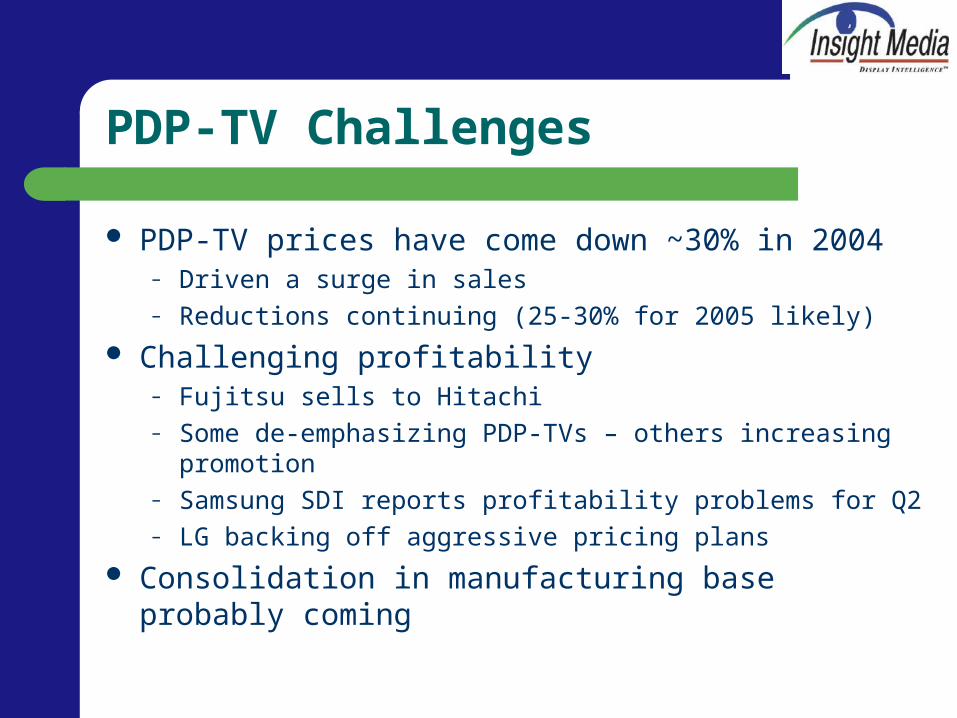

PDP-TV Challenges

PDP-TV prices have come down ~30% in 2004– Driven a surge in sales– Reductions continuing (25-30% for 2005 likely)

Challenging profitability– Fujitsu sells to Hitachi– Some de-emphasizing PDP-TVs – others increasing

promotion– Samsung SDI reports profitability problems for Q2– LG backing off aggressive pricing plans

Consolidation in manufacturing base probably coming

LCD-TV Challenges

Gen 6 and Gen 7 fabs will bring enormous capacity online in 2005

– $2B investments– Need to push panels into market– History of cycles of over supply and rapid price declines

If demand is not strong, cash flow problems develop, more price reductions to stimulate demand

– Could see prolonged periods of losses

Push to 40” and 50” LCD-TVs coming sooner than expected

The 42” Battle

$1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000

40-44” DLP RPTV

40-44” 3LCD RPTV

42” EDTV PDP

42-43” HDTV PDP

40-42” HDTV LCD

1Q2005

4Q2004

Source: PMA March 2005 FPD & RPTV Tracking Services

Crushing Price Reductions

RPTV price to drop by 18% from 2004 LCD price to drop by 40% PDP price to drop and 25% Margins will be squeezed at retail New business models will develop Some will loose money

MCG Optimistic Forecast

0

10

20

30

40

50

60

70

2000 2002 2004 2006 2008

Unit Sales of TVs over 30" by Technology

FP MD

RP MD

RP CRT

PDP

LCD

CRT

Forecast vs. Actuals (2004/2005)

Forecast Comparison for MD RPTV Sales (M units)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2004 2005

MCG Optimistic

Actual/forecast

MCG Conservative

Other analysts 2004

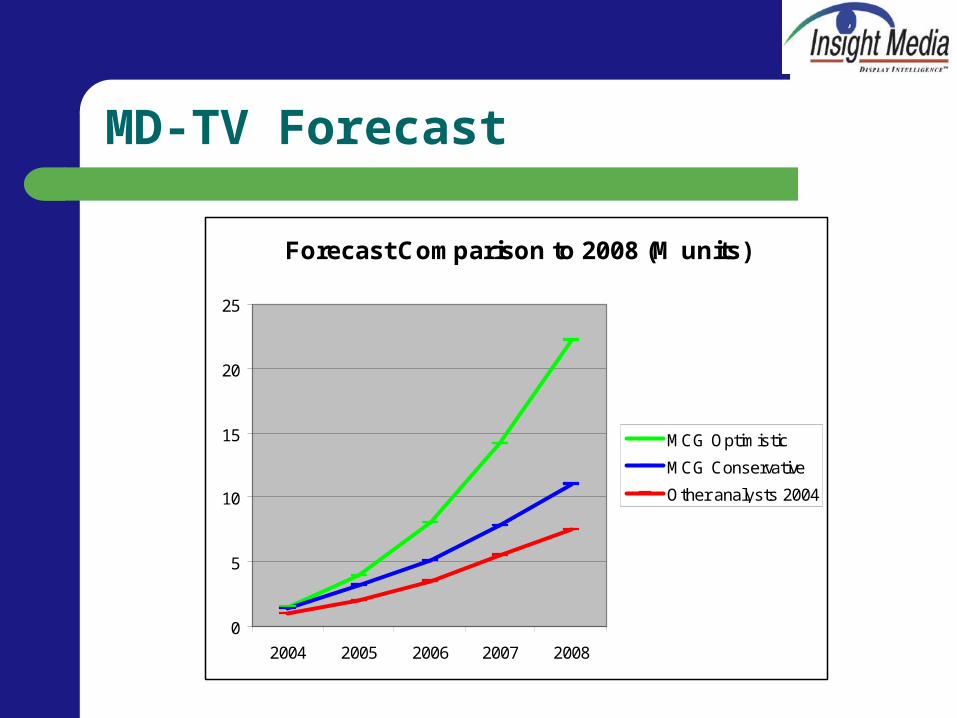

MD-TV Forecast

Forecast Comparison to 2008 (M units)

0

5

10

15

20

25

2004 2005 2006 2007 2008

MCG Optimistic

MCG Conservative

Other analysts 2004

MD-TV Realities

Many are giving up on the 40-49” size range abandoning to PDP

Many are lowering forecasts for MD-TV in 2005 CRT-RPTV is hanging on longer than expected

MD-TV Options

Vertically integrate to reduce margin stacks from many components and assemblies

Offer more aggressive pricing in 42” segment to stop PDP– $1,000 DLP-RPTV planned for 2006, but need to

survive 2005– Buy market share buy lowering prices with loss

leader product

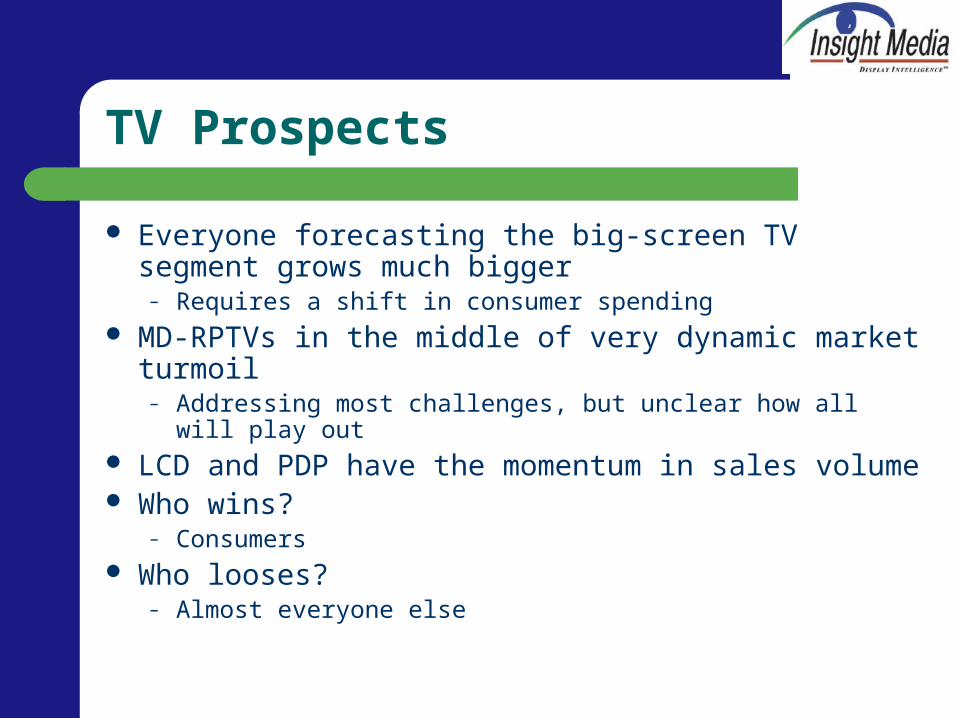

TV Prospects

Everyone forecasting the big-screen TV segment grows much bigger

– Requires a shift in consumer spending MD-RPTVs in the middle of very dynamic market

turmoil– Addressing most challenges, but unclear how all will play out

LCD and PDP have the momentum in sales volume Who wins?

– Consumers Who looses?

– Almost everyone else

Insight Media

3 Morgan Avenue

Norwalk, CT 06851 USA

203-831-8464

203-838-8432 fax

www.insightmedia.info

DTC Forecast

165,412,496

24,709,614

7,111,125

2,993,593

4,949,169

143,327,101

48,723,552

11,821,985

1,339,023

8,191,487

112,860,386

78,227,190

14,361,477

356,011

9,347,129

020,000,0

0040,000,0

0060,000,0

0080,000,0

00100,000,

000120,000,

000140,000,

000160,000,

000180,000,

000200,000,

000

CRT TV

LCD TV

Plasma TV

RPTV - CRT

RPTV - MD

2005

2006

2007

2008

2009

2010

US TV Size Trends (3MPO)

2%

16%

46%

3%6%

2% 3%0%1%

10%

40%

31%

4%7%

3% 2% 1%1%

43%

5%7%

3% 2% 1%2%

12%

36%

6%8%

3%5%

2%

23%

11%

28%27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Under 14" 14"-20" 21"-27" 28"-39" 40"-49" 50"-59" 60" OrMore

Don'tKnow Size

Don't Own A TV

2002 2003 2004 2005

TV Market Size

Total number of TVs WW in 2005 = 170M to 200M– Could grow to 215M by 2009

Related Documents