EFFECTS OF FINANCIAL STRATEGIES ON FINANCIAL SUSTAINABILITY OF NON-GOVERNMENTAL ORGANIZATIONS IN KENYA BY PRIYANKA LALLUBHAI DIVECHA UNITED STATES INTERNATIONAL UNIVERSITY FALL 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EFFECTS OF FINANCIAL STRATEGIES ON FINANCIAL

SUSTAINABILITY OF NON-GOVERNMENTAL ORGANIZATIONS IN

KENYA

BY

PRIYANKA LALLUBHAI DIVECHA

UNITED STATES INTERNATIONAL UNIVERSITY

FALL 2014

EFFECTS OF FINANCIAL STRATEGIES ON FINANCIAL

SUSTAINABILITY OF NON-GOVERNMENTAL ORGANIZATIONS IN

KENYA

BY

PRIYANKA LALLUBHAI DIVECHA

A Project Report Submitted to the Chandaria School of Business in Partial

Fulfillment of the Requirement for the Degree of Masters in Business

Administration

UNITED STATES INTERNATIONAL UNIVERSITY,

NAIROBI-KENYA

FALL 2014

i

STUDENT’S DECLARATION

I, the undersigned, declare that this is my original work and has not been submitted to

any other college, institution or university other than the United States International

University in Nairobi-Kenya for academic credit.

Signed: ________________________ Date: _____________________

Priyanka L. Divecha (ID: 638817)

This project has been presented for examination with my approval as the appointed

supervisor.

Signed: ________________________ Date: _____________________

Dr. George Achoki

Signed: ________________________ Date: _____________________

Dean, Chandaria School of Business

ii

DEDICATION

To my beloved dad (Late Mr. Lallubhai Divecha), whose dream was to see all his kids

grow greater and wiser, to his never ending faith and belief in his children; To my mother,

Mrs. Renuka Lallubhai and her sleepless nights of struggle towards her kids; To my

greatest wings, my brothers, Mr. Jiten Divecha and Mr. Ritesh Divecha for their hands

that always held mine and showing me the correct path, and their wives, Mrs. Sheetal

Jiten and Mrs. Suman Ritesh, for their continuous belief and push.

Special extended dedication goes to my Fiancé, Mr. Harsheet Chudasama, for his never

ending support and encouragement, and his continuous patience and love.

iii

ACKNOWLEDGEMENT

I am obligated to thank all of those who have helped me in the completion of my project.

My very first appreciation goes to my supervisor, Mr. George Achoki for his continuous

guidance, patience and support. It is his dedicated interest and sincerity in the accounting

and finance field that have given me the moral of pushing myself further ahead and

building my career.

My appreciation is also extended to my friends, colleagues and other professors of the

United States International University all of those who have been a part of my journey all

through.

Special appreciation is expressed to my Mum and Dad, Mrs. Renuka Lallubhai and Late

Mr. Lallubhai Divecha for their unbelievable support and struggle towards me, and to the

dream they held towards me.

My indebted appreciation goes to my brothers Mr. Jiten Divecha and Ritesh Divecha, I

would have never been able to stand where I stand today if it wasn’t for their guidance

and support. My appreciation to my sister in laws, Mrs. Sheetal Jiten and Mrs. Suman

Ritesh, their patience towards me and their sisterly support that kept me strong all

through.

My very special appreciation is expressed to my fiancé, Mr. Harsheet Chudasama, and his

continuous patience, love and care that held on to me all through. His strong support

helped me in completing my fieldwork on time, and his prayers and faith that secured my

belief in being able to complete this

Most of all, I give glory to the Almighty for keeping me strong all through.

iv

ABSTRACT

The purpose of this study was to investigate the effects of financial strategies on the

financial sustainability of Nongovernmental Organizations (NGOs) in Kenya. The study

sought to answer the following research questions, “How does income diversification

strategy affect the financial sustainability of NGOs?”, “How does a strategic partnership

affect the financial sustainability of NGOs?”, “How does strategic financial management

affect the financial sustainability of NGOs?” and “How does participation of NGOs in

income generating activities affect the financial sustainability of NGOs?”. Through this

study, an attempt was made to know whether the identified financial strategies help in

enhancing the financial status of NGOs in Kenya and how these financial strategies affect

the overall financial sustainability of NGOs in Kenya.

The study was an inferential study that was aimed to present the degree of variance in the

financial sustainability of NGOs caused or predicted by the four different financial

strategies adopted. Seventy five NGOs were sampled from Twenty Six different sectors

of NGOs operating in Nairobi, Kenya. Quantitative data was analyzed using the SPSS

version 22.0. The sample was selected using stratified proportionate random sampling

technique and reduced to twenty six strata of NGOs for quality and accuracy purposes.

The findings of the study are that all the four independent variables are positively

correlated to the financial sustainability of NGOs; Income diversification strategies that

enhance the financial sustainability of NGO’s identified from the study findings were

tapping international funding streams, fundraising and development plan and corporate

donor sourcing. The NGOs were studied to be developing their fund-raising activities and

tapping into new corporate donor streams for better monetary support as well as holding

one-time events in aspect of improving their income streams. Funding based strategic

partnerships between NGOs and other business entities was also found becoming a

central part of their financial development process. Strategic financial management was to

be affecting the financial sustainability of NGOs to a great extent. The drivers for

strategic financial management that mainly affected the financial sustainability of the

NGO to a great extent included strategic planning, financial analysis and plan

implementation. Participation of NGOs in their own income generating activities was also

found to be affecting the NGO’s financial sustainability to a great extent. The study found

v

that participating in business activities, receiving trust or endowment funds and receiving

public contribution were to be affecting financial sustainability of NGOs to a great extent.

The study concluded that poor financial management in specific categories such as

strategic planning, plan implementation and financial analysis led to poor management of

financial stability of NGOs. Income generation was also concluded to be a central

strategy used to respond to financial challenges and find alternatives to stabilize financial

status of NGO. The study further concluded that funding based partnerships benefited the

NGOs to a great extent in comparison to other strategic partnerships. Furthermore, the

study deduced that NGOs majorly depended on public contribution for stabilizing their

financial status and therefore NGOs participating in their own income generating

activities contributed majorly to most of the financial sustainability of the organization.

The study further recommends NGO’s in order to remain financially sustainable; they

should employ staffs that are capable of planning strategically, implementing the plan and

doing appropriate financial analysis to manage and maintain good financial status in

terms of cost recovery, cash flows and capital structure. The study also recommends all

the NGOs management to improve and maintain their income sources from their usual

source that is donors. Employees capable of identifying risk factors and those who are

able to manage risk should be employed so as to be able to manage their cash flow

appropriately. The study also suggests NGOs to reduce their dependency on major

donors, withdrawal of which would force the organization to close down.

vi

LIST OF ABBREVIATIONS

FS - Financial Sustainability

ID - Income Diversification

IG - Income Generation

IGPs - Income Generating Programs

SP - Strategic Partnerships

SFM - Strategic Financial Management

RBV - Resource-Based View

NGO - Non-governmental Organizations

SPSS - Statistical Package for Social Science

USAID - United States Agency for International Development

DFID - Department for International Development

vii

TABLE OF CONTENTS

STUDENT’S DECLARATION ................................................................................................................. i

DEDICATION ................................................................................................................................. ii

ACKNOWLEDGEMENT ............................................................................................................... iii

ABSTRACT .................................................................................................................................... iv

LIST OF ABBREVIATIONS ......................................................................................................... vi

CHAPTER 1 ..................................................................................................................................... 1

1.0 INTRODUCTION ................................................................................................................ 1

1.1 Background of the Study .................................................................................................. 1

1.2 Statement of the Problem ................................................................................................. 4

1.3 Purpose of the Study ......................................................................................................... 7

1.4 Research Questions .......................................................................................................... 7

1.5 Significance of the Study .................................................................................................. 7

1.6 Scope of the Study ............................................................................................................ 8

1.7 Definition of Terms .......................................................................................................... 8

1.8 Chapter Summary ........................................................................................................... 10

CHAPTER 2 ................................................................................................................................... 11

2.0 LITERATURE REVIEW ................................................................................................... 11

2.1 Introduction .................................................................................................................... 11

2.2 Income Diversification ................................................................................................... 11

2.3 Strategic Partnerships ..................................................................................................... 15

2.4 Strategic Financial Management .................................................................................... 19

2.5 Participation of NGOs in Income Generating Activities ................................................ 24

2.6 Chapter Summary ........................................................................................................... 26

CHAPTER 3 ................................................................................................................................... 27

3.0 RESEARCH METHODOLOGY ............................................................................................. 27

3.1 Introduction .......................................................................................................................... 27

3.2 Research Design ................................................................................................................... 27

3.3 Population and Sampling Design ................................................................................... 28

3.3.1 Population ............................................................................................................... 28

3.3.2 Sampling Design and Sample Size ......................................................................... 28

3.4 Data Collection Method ................................................................................................. 29

3.5 Research Procedure ........................................................................................................ 29

viii

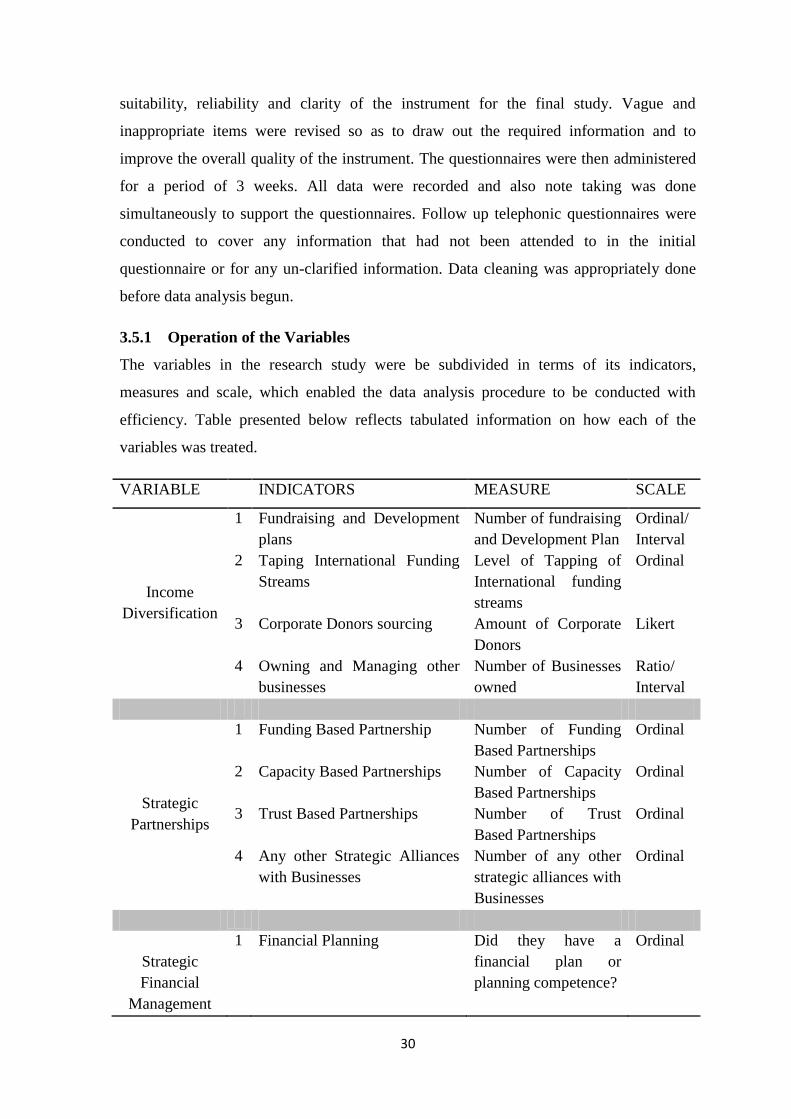

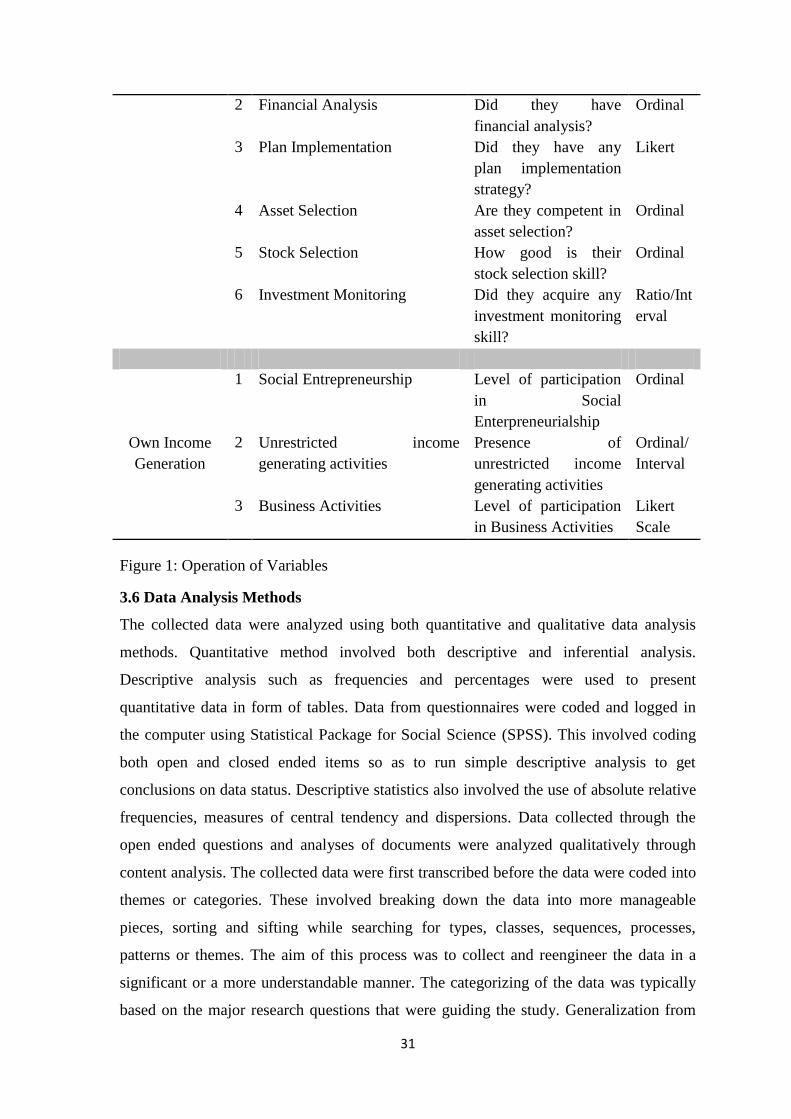

3.5.1 Operation of the Variables ...................................................................................... 30

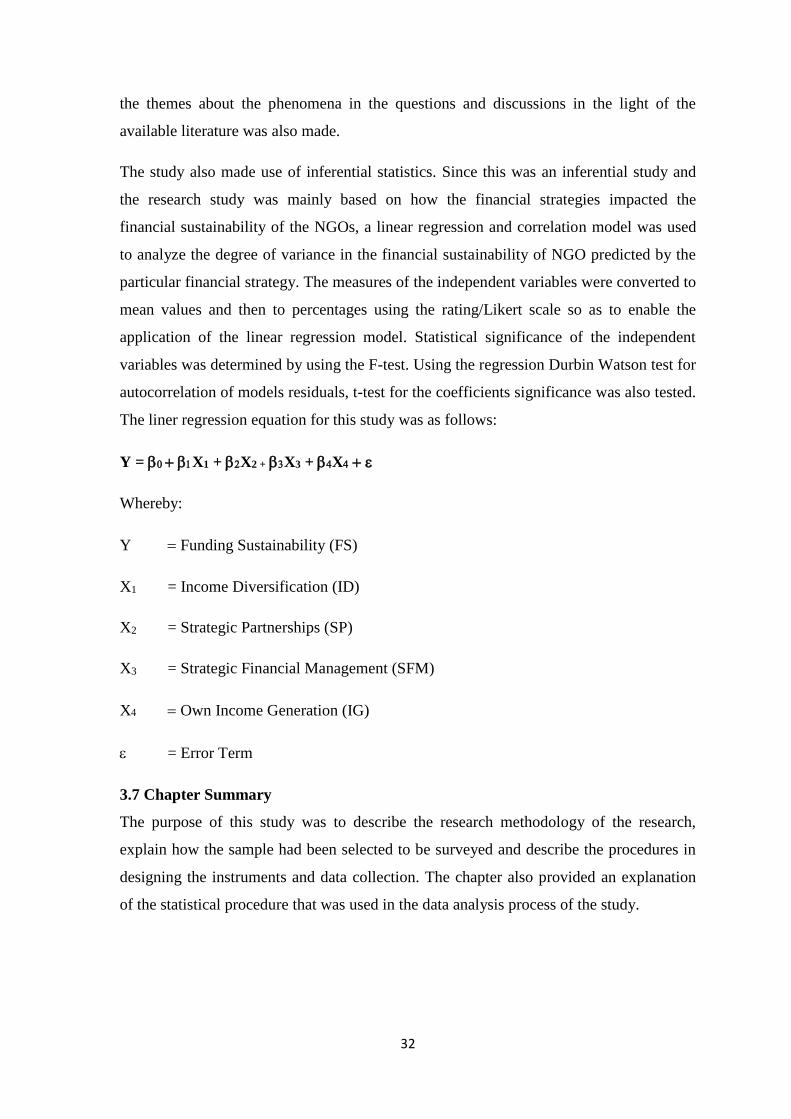

3.6 Data Analysis Methods................................................................................................... 31

3.7 Chapter Summary ........................................................................................................... 32

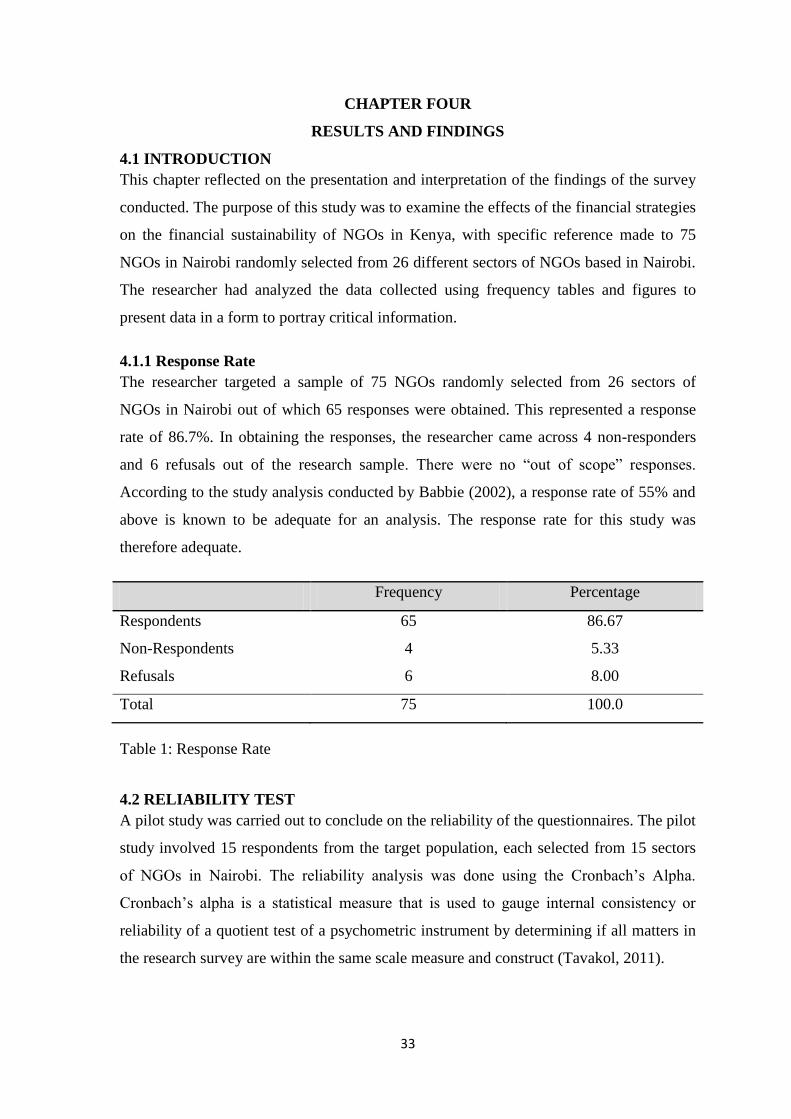

CHAPTER FOUR .......................................................................................................................... 33

RESULTS AND FINDINGS ......................................................................................................... 33

4.1 INTRODUCTION .................................................................................................................... 33

4.1.1 Response Rate ................................................................................................................... 33

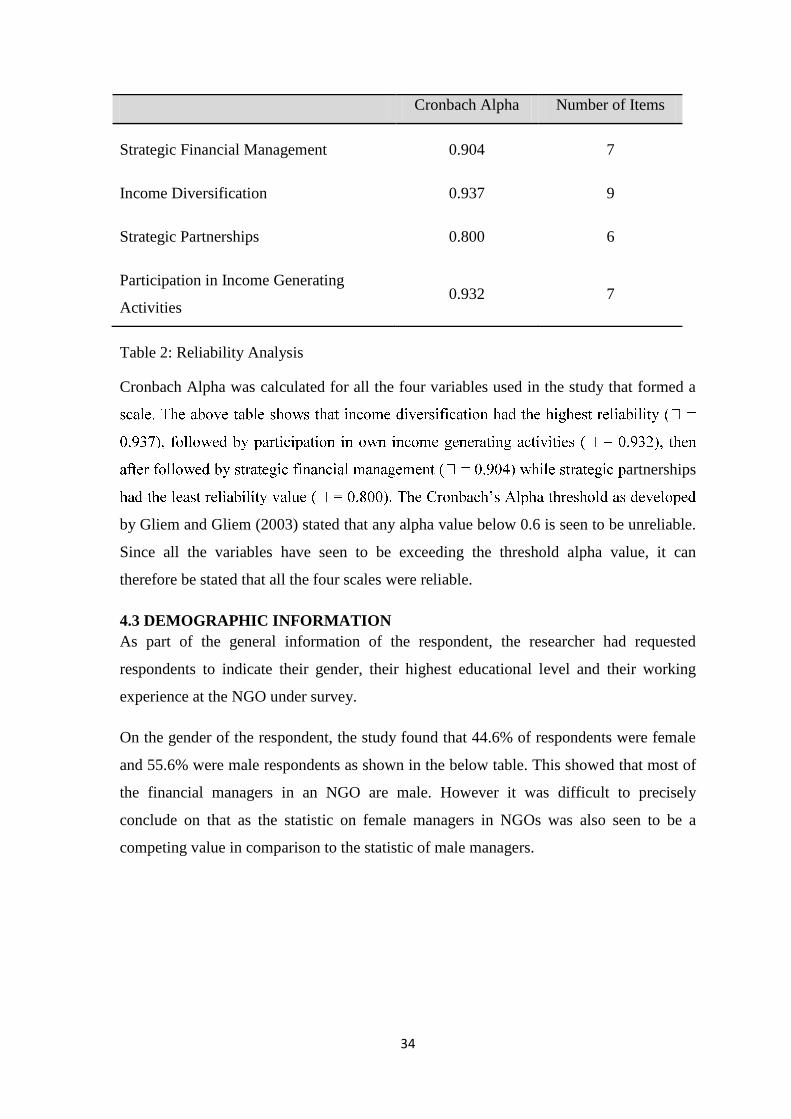

4.2 RELIABILITY TEST ............................................................................................................... 33

4.3 DEMOGRAPHIC INFORMATION ........................................................................................ 34

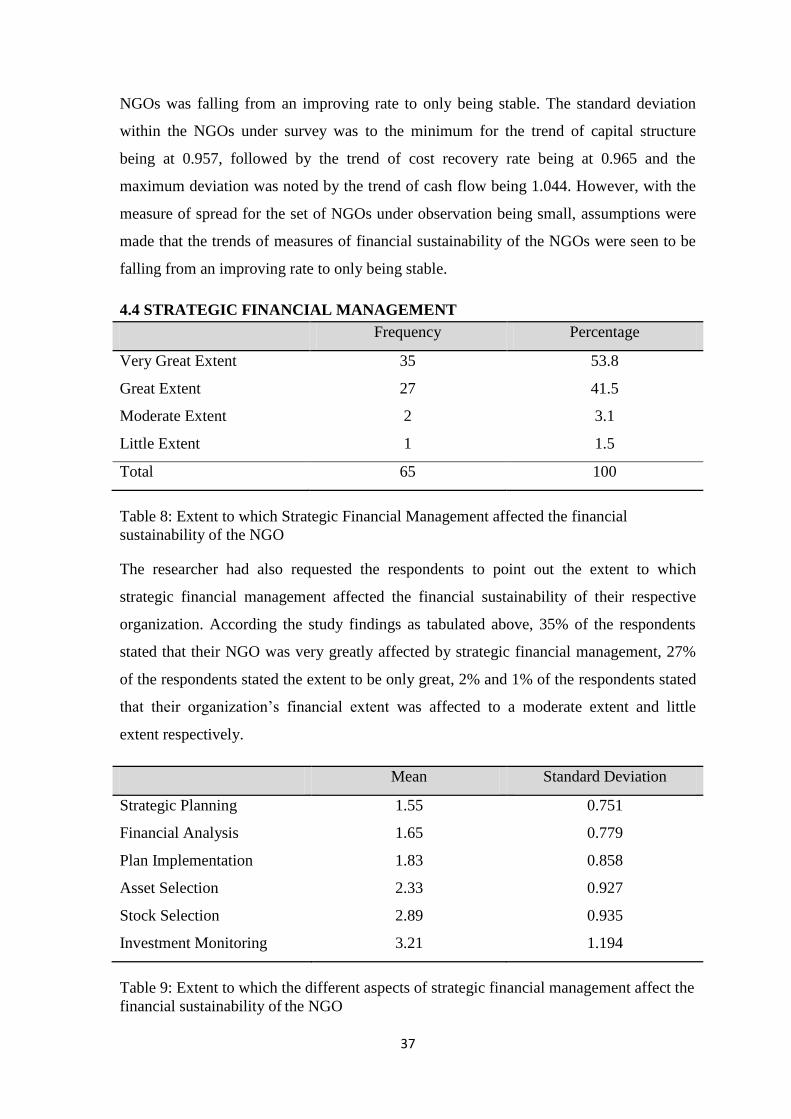

4.4 STRATEGIC FINANCIAL MANAGEMENT ........................................................................ 37

4.5 INCOME DIVERSIFICATION ............................................................................................... 38

4.6 STRATEGIC PARTNERSHIPS .............................................................................................. 40

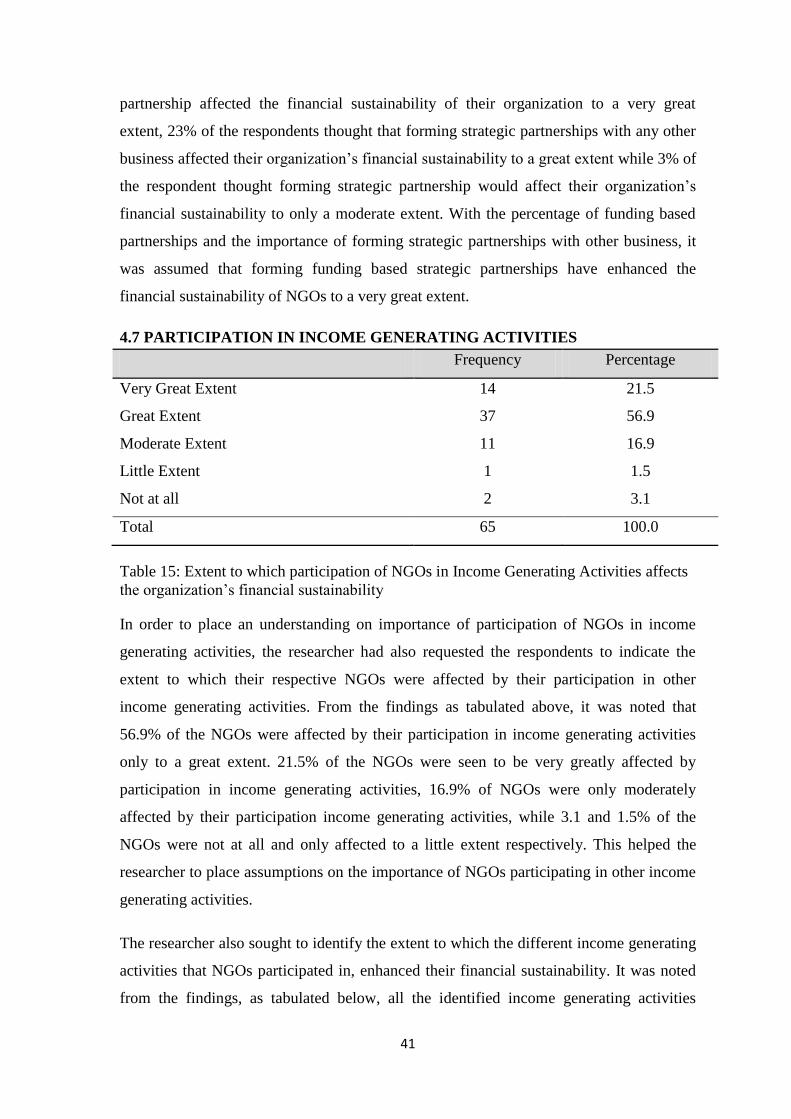

4.7 PARTICIPATION IN INCOME GENERATING ACTIVITIES ............................................ 41

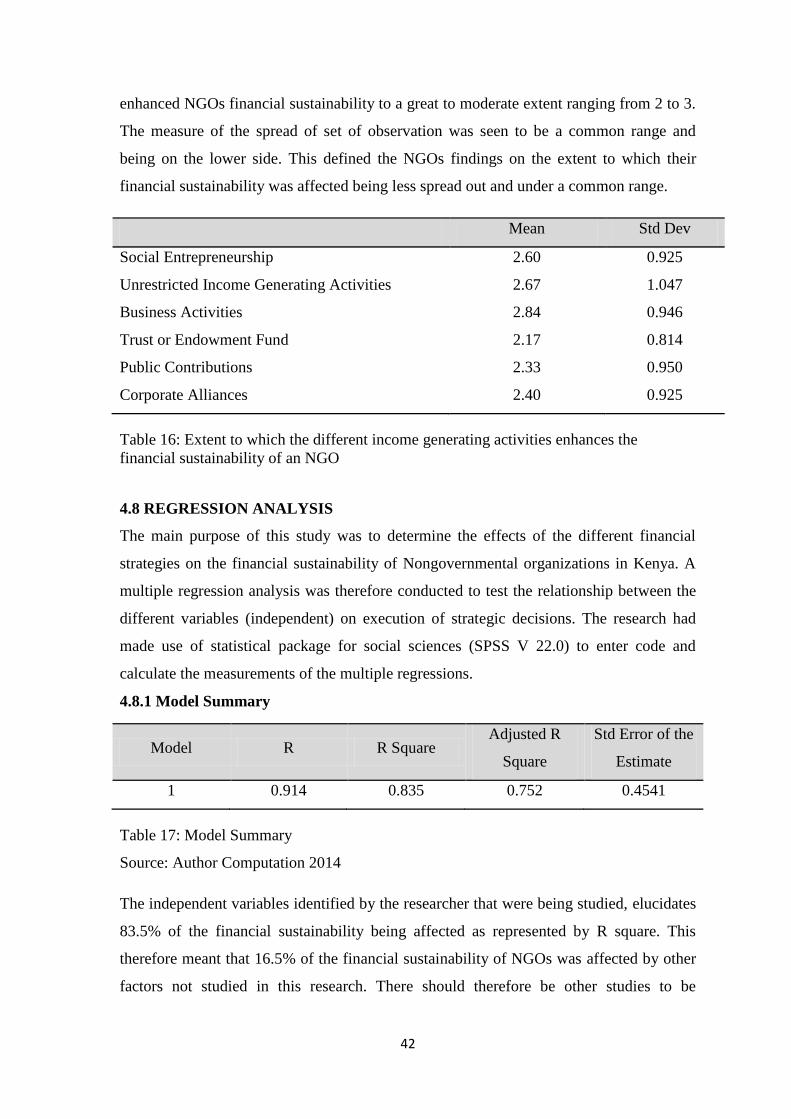

4.8 REGRESSION ANALYSIS ..................................................................................................... 42

CHAPTER FIVE ............................................................................................................................ 46

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS .................................................. 46

5.1 INTRODUCTION .................................................................................................................... 46

5.2 SUMMARY ............................................................................................................................. 46

5.2.1 Income Diversification ...................................................................................................... 46

5.2.2 Strategic Partnerships ........................................................................................................ 47

5.2.3 Strategic Financial Management ....................................................................................... 47

5.2.4 Participation in Income Generating Activities .................................................................. 48

5.3 CONCLUSION ........................................................................................................................ 49

5.4 RECOMMENDATION ............................................................................................................ 50

5.5 AREAS OF FURTHER RESEARCH ...................................................................................... 51

REFERENCES ............................................................................................................................... 52

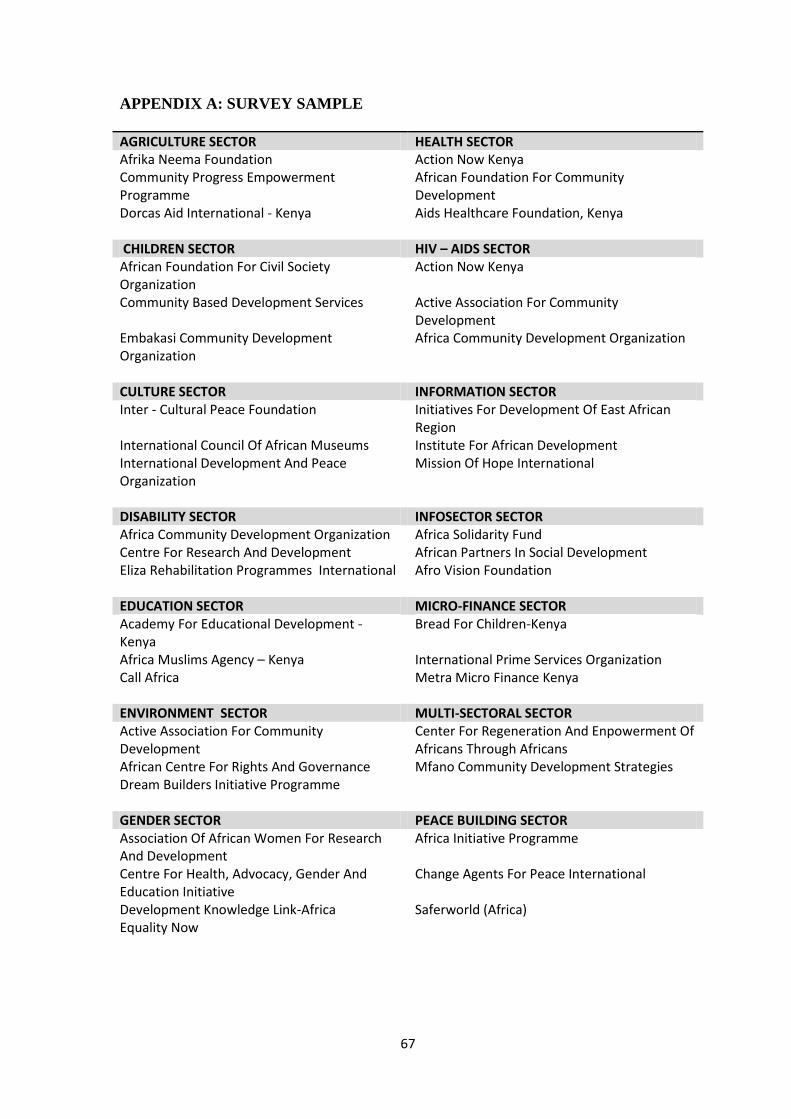

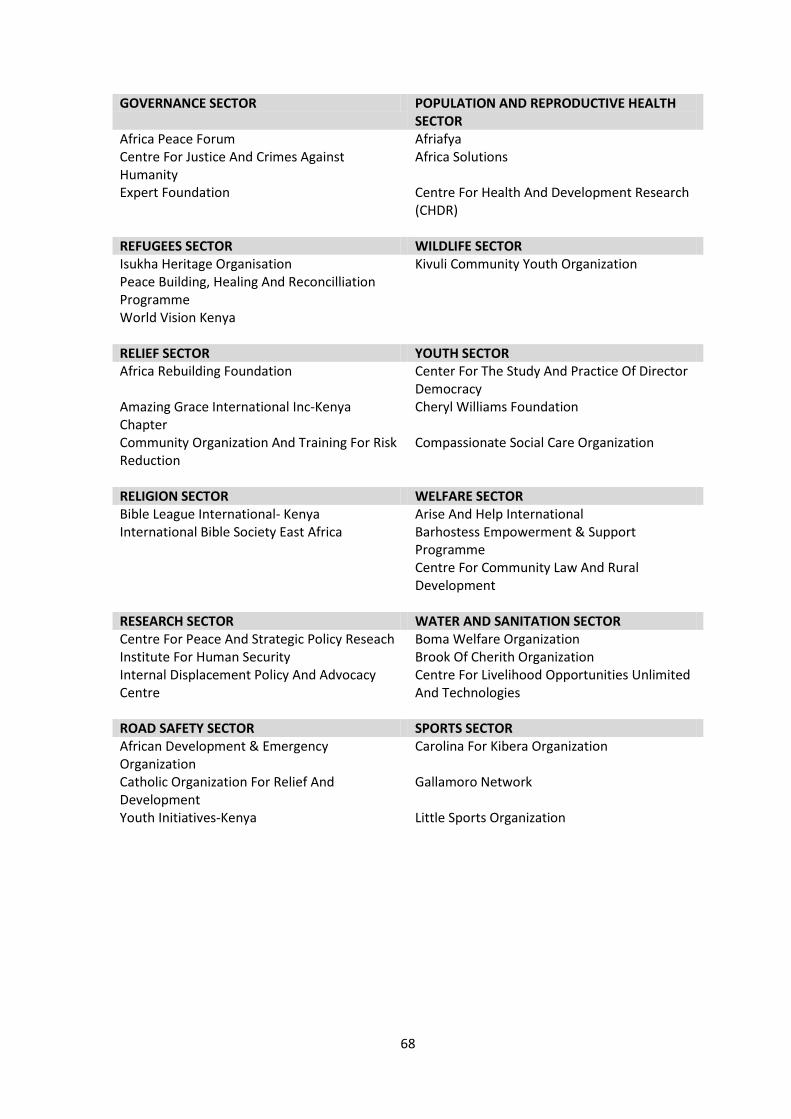

APPENDIX A: SURVEY SAMPLE .............................................................................................. 67

APPENDIX B: COVER LETTER ................................................................................................ 69

APPENDIX C: RESEARCH QUESTIONNAIRE......................................................................... 70

ix

LIST OF TABLES

Table 1: Response Rate ...................................................................................................... 33

Table 2: Reliability Analysis ............................................................................................. 34

Table 3: Gender of the respondent ..................................................................................... 35

Table 4: Age bracket of respondent ................................................................................... 35

Table 5: Highest level of education of the respondent ...................................................... 36

Table 6: Working experience of the respondent ................................................................ 36

Table 7: Trend of measures of financial sustainability for NGO in the last five years ..... 36

Table 8: Extent to which Strategic Financial Management affected the financial

sustainability of the NGO .................................................................................................. 37

Table 9: Extent to which the different aspects of strategic financial management affect the

financial sustainability of the NGO ................................................................................... 37

Table 10: Importance of Income Diversification drivers to an NGO ................................ 38

Table 11: Effectiveness of various income diversification strategies in enhancing financial

sustainability at an NGO .................................................................................................... 39

Table 12: Organizations in strategic partnerships .............................................................. 40

Table 13: Kind of Strategic partnership ............................................................................. 40

Table 14: Extent to which forming strategic partnerships affect the financial sustainability

of NGO............................................................................................................................... 40

Table 15: Extent to which participation of NGOs in Income Generating Activities affect

the organization’s financial sustainability ......................................................................... 41

Table 16: Extent to which the different income generating activities enhances the

financial sustainability of an NGO .................................................................................... 42

Table 17: Model Summary ................................................................................................ 42

Table 18: ANOVA ............................................................................................................. 43

Table 19: Regression Coefficient....................................................................................... 43

1

CHAPTER 1

1.0 INTRODUCTION

1.1 Background of the Study

Effects of financial strategies on financial sustainability of a Nongovernmental

organization are usually seen in terms of its establishing and managing operating costs,

setting financial goals, making financial projections as well as organizing for appropriate

funding needed for projects. In general a financial strategy is one of the crucial aspects of

any business. Financial strategies should be discussed and shared with the company

executives as well as employees, so that everyone is on a common understanding of the

financial state of the organization (Newton, 2012). Surviving under financial constraints

usually requires efficient resource allocation, but most nongovernmental organizations are

usually dominated by circumstances of resource scarcity. Such firms have lack of

opportunities for making additional income, but are more often faced with different

schedules of activities which require monetary funding (Giantris, 2012). These are

scenarios where the need of a financial strategy arises.

An organization is known to be financially stable when its immediate work is not affected

if its external funding is altered (Ahmed, 2012). Financial stability of an organization is

referred to as one of the sustainability factors that leads to the organizations having a

longer life span in the market as well as assisting it to translate its impacts into processes

that are advantageous to the society as stated by its mission statement (Drucker, 2000).

Financial sustainability as noted from a general scenario is one of the key challenges

faced by any Nongovernmental organizations. Only those organizations that have a stable

cash inflow and an established financial constitution are known to survive the financial

challenges faced, in terms of the more gradually, multifaceted global environment.

Nevertheless, financial stability is not only known for its survival but that it also

facilitates and guarantees the organization for its ability to invest in its future (Kiev,

2003).

Financial strategy is defined as a set of plan or policies that concludes on the sourcing of

funds, capitalization and resource attainability. It usually has a major impact on a

Nongovernmental organization’s capability to invest in for its value creation as well as its

sustainability in the sector. However, despite of its ongoing importance, most such

organizations give limited critical review to financial strategies (Mallette, 2013). Whilst

2

the main components of the organization’s operations are to be inspected and updated

regularly, Mallette (2012) also states that despite of the impacts of financial strategies on

the NGO’s sustainability, many NGOs do not have an ambient framework for

methodically reviewing their financial strategy to make sure it is associated with its

organizations operations and is internally consistent. Therefore due to such congregating

factors, there has been a rise in demand for the reassessment of financial strategies by the

management of most organizations (Rouse, 2010).

Kortan (1987) reviews Nongovernmental organizational cost management as an

important element of finance strategy, a key to improving efficiency in scheduled

transactional development that permits a shift to the center of building the organization’s

value in terms of its finance functions. This includes construing and counseling on

important business information; managing capital allocation as well as value creation, and

building a balanced view of the NGO’s cash flow and return on assets or equity. The

financial officers for many NGOs therefore face finance transformation in an

environment of globalization, increased cost stress as well as increasing governmental

regulations. Financial strategies employed would therefore offer an integrated plan to

bring into line the financial priorities of the organization with its overall mission (Sesic,

2011).

“The main problem is that organizations don't always know when the money is coming in

-- so it's hard to plan and shortfalls are common” stated by Giantris (2012). Organizations

need to understand the wise usage of their funds, according to their intended purpose.

More often when audits are taken place, it is witnessed that organization’s managers use

the company’s funds outside the extent of the organizations work plan. Effective

management practices in terms of strategic financial management require organizational

principles of sustainability, accountability and transparency for administrative efficiency

(Nicklous, 2012).

Nevertheless, strategic partnerships between NGOs and other businesses hold the

potential to tackle the different financial challenges as well as opportunities that could not

have been addressed in the same way outside a partnership. This therefore makes strategic

partnership as one of the financial strategies that NGOs adopt in order to counter their

financial challenges (Boue & Kjaer, 2010). Lowering transactional cost through strategic

partnerships also reduces interdependence and risks and thus improves efficiency.

3

Maintaining these partnerships can assist in lowering such external costs through

predicting some of the externalities that consequence from transactional costing (Barney,

2013). This lowers the chances of extra cost of monitoring and governance and would

thus lower the overall cash out flow hence stabilizing the financial position of the NGO.

Diversification of revenue on the other hand, is also important to the organization so as to

improve the financial stability of NGOs. According to a survey done by Suri (2009),

economic crisis has always had a strong impact on the NGOs revenue trends with having

decreased sources of funds. In order to respond to the economic crisis, NGOs have tapped

on international markets for better funding streams. As investigated by Boas (2012),

financial support from international governments and their respective agencies have

assisted in providing the NGOs with great opportunities. With the financial challenges

that most NGOs face, responses to these challenges with the same entrepreneurial

attitude, efficient planning and hard work have at least built a successful financial strategy

for most of these NGOs (Bezuneh, 2000).

Considering some of the financial strategies, most financially struggling NGOs are said to

have lack of clear mission and a strategic direction; these tools that are known to be the

necessary skills towards effective management of resources for sustainability (Ahmed,

2012). Financial sustainability is attained when an organization is capable of offering

products and services to the market at a price that wraps up their entire expenses and

generates a profit. Effective operations management is a critical tool as it helps to ensure

organizations meet its objectives and needs of the society over a sustainable period of

time (Kiev, 2003). Operations management would include effective planning of activities,

decision making and effective and responsible management of the purchase, production

and distribution of products and services.

The NGO’s in Kenya are under the control of The National Council of NGOs, more often

known as the NGO council of Kenya. The Non-Governmental Organizations Co-

ordination board more commonly known as the NGO Co-ordination Board was

recognized by an Act of Parliament in 1990 and began its business on June 15, 1992

(NGOBUREAU, 2011). The main reason for the formation of the board was to rationalize

and make more efficient the registration and co-ordination of NGOs.

Sustainability and financial stability of NGOs have been a challenge in Kenya. Financial

stability has become a catchphrase for NGOs within the development circles. It explains

4

the ability of the NGOs to work for its objective and being able to provide the society

with the objectives aimed even after external support is terminated. Not all are able to

accomplish this objective. The study notes this observable fact of the financial challenges

faced by the NGOs and therefore seeks to find the correlation of the financial strategies to

the financial sustainability of NGOs in Nairobi and how it affects the overall

sustainability of the NGO in the sector.

1.2 Statement of the Problem

There have been several observations and literature reviews on the financial challenges

faced by NGOs from various researchers and scholars. According to Rothlauf (2011),

financial management processes have generally been weak and have always been a

challenge to the NGOs. These are usually due to conditions of resource insufficiency; that

is considerations of events and social development activities which require most of the

organizational funds but in return no income generating activities take place. When

NGOs face such challenges, they require tactical planning of financial strategies resulting

to a positive impact on the overall sustainability of the organization (Chenhall, Hall &

Smith, 2012). Appropriate financial strategies have seen to be benefiting the NGOs in

terms of their financial sustainability but difficult economic times such as increased

inflations or global recessions have always affected the overall financial sustainability of

the NGOs in one way or the other (Waiganjo, 2012). There are many NGOs that continue

ceasing maneuver by the passing days usually due to lack of financial management and

sustainability. New NGOs also fall into snare of instability as they would operate for a

specific period of time and then grow fainter. NGOs are mostly known only with the

concern of elevating their resources and developing them depending on their available

planned budgets (Ng’ethe & Mugambi, 2012). This is a condition of concern that has

locked NGOs in a reliance syndrome which questions their financial stability and hence

their survival in the community. Despite the increased efforts by various strong donors

like USAID, DFID, OXFAM, World Bank, etc, on capacity building procedures of the

NGOs with refresher courses on the best applicable practices in the NGO sector, NGOs

need to adopt appropriate financial strategies to have a more reliable financial position

and gain sustainability (Nicklous, 2012).

The study analysis centered its base on the several financial strategies adopted by NGOs

and how it affects their financial sustainability in the sector. According to the study

conducted by Ahmed (2012), on the factors affecting the financial sustainability of NGOs

5

in Kenya, different sources of funding have been identified. Nevertheless, according to

the researcher’s knowledge, at the time of the study, no local studies had focused on the

impact of financial strategies on the financial sustainability of NGOs in Kenya. The

research recommendation was stated in the research conducted by Ahmed (2012) on the

factors affecting the financial sustainability of NGOs in Kenya. It is this consideration

that the researcher had in mind the aim to fill the obtainable gap by carrying out a study

on the how the financial strategies affect the financial sustainability of NGOs in Kenya.

The study reference was made to the NGOs in Nairobi only. As noted from the NGOs co-

ordination board online, the NGO Bureau, there are 26 sectors of NGOs in Nairobi. The

researcher had aimed to target 2-3 randomly selected NGOs from each sector summing to

75 NGOs to survey on the effect of financial strategies on the financial sustainability of

these NGOs.

Understanding the impacts that income diversification had on the financial sustainability

of NGO’s in Kenya is what the study focused on as one of the financial strategy. Study

investigation by Heinzberg (2012), identified income diversification as one of the factors

affecting the financial sustainability of NGOs (Heinzberg, 2012). Income Diversification

in general describes the level of activities that the NGOs take part in that aims at

minimizing dependency on some other type of income (donations), grants, some ruling

consumers, one particular country that is known to be the main source of funding or also

minimizing dependency on favorable currency exchange rates (Boas, 2012). It had been

studied that income diversification affects the financial sustainability of NGOs but

reference have only been made to one particular NGO, which in the researchers

knowledge is not enough to understand the level of impact it has on the organizations

financial sustainability. This study therefore focuses on income diversification being one

of the financial strategies that may affect the financial sustainability of the NGOs.

Secondly, the rising interests in strategic partnerships can be credited to “the realization

that strategic partnering can promote effective results for all concerned: Businesses,

NGOs and especially the society/community” (Boue & Kjaer, 2010). Therefore, strategic

partnership had also been identified as one of the financial strategies for NGOs. In the

literature, there is no particular agreement on whether strategic partnerships are similar to

firm-firm collaborations. There are only few scholars (Beckham, 2007), who have

reviewed the applicability of theories elaborating firm to firm collaborations to firm to

NGO collaborations and these have therefore given way to antithetical results. Few

6

studies (Graf, 2011) also argue on the opinion that the mainstream solitary sector

partnership theories of firm-to-firm collaboration can also be applied to collaborations

between firms and NGOs. This discloses the importance of further research regarding the

effects of strategic partnerships of NGOs and firm on the NGOs financial sustainability.

The researcher hence aimed to target strategic partnerships as another variable of

financial strategies to survey on the effect it has on the financial sustainability of NGOs.

The several studies that focused on the strategic planning as a financial factor for NGOs,

according to the researcher’s knowledge, had missed out on the elaboration of the

correlation it held on the overall financial sustainability of the organization. As

demonstrated by Grunewald (2011), strategic partnership between NGOs and other

business organizations were seen to strengthen the quality of humanitarian aid, but the

limit to which it contributed to its financial sustainability was not quite elaborated in

brief. A study by Damlamian (2006) focused on corporate and NGO partnerships as a

sustainability factor for the development of both the organization, once again, the

elaboration on how the strategic partnership affected the financial sustainability of the

NGO was not quiet focused on. This study therefore aimed to fill that gap and investigate

on the effect it might have had on the financial sustainability of the NGO under survey.

Thirdly, strategic financial management was usually an aspect that was given a very low

priority. This was more often exemplified by poor financial planning and monitoring

systems (Waiganjo, 2012). Since NGOs function in a speedy changing and a competitive

world, if they are to endure in a challenging environment, managers need to expand the

important understanding and self-assurance to make efficient use of the appropriate

financial management tools and resources (Lewis, 2009). The study thereby focused on

how strong is the correlation is between strategic financial management and the financial

sustainability of NGOs in Kenya. A study investigation by Ng’ethe & Mugambi (2012),

had nevertheless focused on this strategic financial management as one of the financial

strategies adopted by NGOs in Kenya, but there was a gap in presenting the impacts it

held on the overall financial sustainability of the organization. The level to which

strategic financial management affected the financial sustainability of the NGO had not

been addressed. The study aimed to bridge this gap and expand the knowledge on the

effects of different financial strategies on the financial sustainability of NGOs.

Lastly, but not at the least, the researcher centered this study on investigating whether

participating in income generating activities improved the financial sustainability of

7

NGOs to any better stage. The study aimed to focus on income generating activities in

NGOs as one of the financial strategies and study its impact on the financial sustainability

of the organizations under survey. Income generating activities have been studied to be

one of the financial strategies that enhance NGOs financial sustainability to a great extent.

However activities such as social entrepreneurship, unrestricted income generating

activities, business activities, endowment funds, public contributions and corporate

alliances have been studied to improve the financial status of NGOs in Uganda (Mallete,

2013), but according to the researchers knowledge, there are no such studies conducted in

Kenya to substantiate that these income generating activities may also be used to improve

the financial status of NGOs in Kenya. This study therefore aimed to fill the knowledge

gap and investigate on the effect of these income generating activities on the financial

sustainability of NGOs in Kenya.

1.3 Purpose of the Study

The purpose of the study was to investigate the effects of financial strategies on the

financial sustainability of the NGOs in Nairobi, Kenya.

1.4 Research Questions

The study aimed to respond to the following questions:

1. How does income diversification affect NGO’s financial sustainability?

2. How does strategic financial management affect NGO’s financial sustainability?

3. How does participating in income generating activities affect NGO’s financial

sustainability?

4. How does strategic partnership of NGOs with other firms affect the NGO’s

financial sustainability?

1.5 Significance of the Study

This study provides significance to the different stakeholders of the NGOs, such would

include as follows:

1.5.1 Managers of the NGO’s

This study carried out would not only be of importance to the researcher and the NGO’s

involved in the study but also to other managers in the NGO sector. It would assist them

in choosing better their strategic plans and practices and understand how such practices

8

would assist them in providing their NGO’s with better and stronger financial

sustainability.

1.5.2 Owners of the NGO’s

The owners of the NGOs will be able to identify their level of contribution in the

direction of the success of the NGO in terms of its financial sustainability. This would

enhance their understanding better in the ongoing operations and would stimulate them to

work on their individual roles more efficiently.

1.5.3 Society

The study would also assist in understanding and stabilizing the financial status of the

NGOs hence prompting its longer survival in the society. This would allow them to carry

out more society serving activities with better usage of resources hence benefiting the

society.

1.5.4 Other Researchers and Scholars

The study can also be valuable to other researchers and scholars as it would act as a base

for further research. The academicians and scholars will be able to use this study to

understand how NGOs can survive through financial instability and provide insights of

different strategic processes that can be used. The study acts as a reference provision for

further researchers on other topics of related importance.

1.6 Scope of the Study

The scope of the study aimed to target the financial managers within the NGOS in

Nairobi, Kenya. The study mainly focused on investigating on the effects of financial

strategies on the financial sustainability of NGOs in Kenya. The study was therefore

limited to the survey of 75 NGOs selected from the different sectors of NGOs in Nairobi,

as listed by the NGO co-ordination board of Kenya.

1.7 Definition of Terms

The researcher has explained in brief some of the subsequent concepts used so as to make

its understanding and interpretation in this study clear.

1.7.1 Financial Stability

This is referred to as a state in which the financial system of an organization is capable to

survive economic shocks and is able to reach its basic objectives, that is the

intermediation of financial funds, management of risks and the arrangement of payments

(Stain, 2011). The financial stability in this study is measured in terms of liquidity

9

position of the NGO (the ability of the NGO to pay its short and long term debts), the

capital structure of the NGO (relationship between the equity and debt of the NGOs), and

net and gross profit margins (the contribution margin of the revenues over the total

expenses).

1.7.2 Financial Management

Financial management refers to all efforts and measures undertaken so as to ensure

enough funding is available at the right time to meet the needs of the organization (Riley,

2012).

1.7.3 Funds

Funds are defined as a sum of resources saved, usually in terms of monetary values, for a

particular purpose (Ross, Westerfield & Jaffe, 2002).

1.7.4 Fund raising costs

Fund raising costs are referred to as the amounts of monetary value used up to persuade

others to make charitable aid to the NGOs. It includes spending on advertising and direct

merit materials, agent’s charges for acting as fund raiser on behalf of the NGO (Ahmed,

2012).

1.7.4 Risk Management

Risk Management is defined as the planning, organizing, leading and controlling

processes of the activities of an organization so to diminish the effects of risk on the

organization’s earnings and capital to the minimum. Risk management not only develops

the processes including risk with accidental loses, but also financial, operational, strategic

and other related risks (Rouse, 2010).

1.7.5 Strategy

Several explanation of strategy found in the literature of business management mainly

focuses on any one of the four main categories, that is, strategy being a plan, prototype,

position and viewpoint or perspective. With the different review of literature on strategy

Nicklous (2012) states that, “strategy is a plan or a means of getting from here to there, a

pattern in actions over time, a position, which in essence reflects decisions to offer

particular products or services in particular markets and a perspective, that is, a vision and

direction, a view of what the company or organization is to become”.

10

1.7.6 Strategic Financial Management

Strategic financial management is defined as the distribution of the scarce resources to

recognized probable strategies amongst competing opportunities and undertaking needed

crucial deeds so as to monitor the progress of the organization in the aim of attaining the

organizational objective (Alexander, 2012).

1.7.7 Sustainability

As stated by Heinzberg (2010), “The essence of the term sustainable is that which can be

maintained over time”. By insinuation, this states that any organization that is

unsustainable will not be maintained for long and will eventually cease to function at

some point. The term sustainability in this study has been used to state the ability of an

NGO to safeguard and run enough human, physical and financial resources in order to

fulfill its assignment efficiently in the long term.

1.7.8 Strategic Partnerships

Strategic partnerships as defined by Vonotas (2009), refers to a web of agreements where

two or more partners share a commitment to reach a common goal by bringing their

resources together and coordinate their activities.

1.8 Chapter Summary

This chapter aimed to address the crucial significance and consequences of financial

strategies as an influential means of gaining financial sustainability in NGOs. Also

covered was the purpose of the study and the objectives that guided the study within the

specified scope, in terms of geographical means. The chapter looked at the aim of this

study and outlined the research questions that were addressed by the study. The statement

of the problem to which this study was addressed to was also specified together with its

significance as well as the scope of the study, which in our study term was Nairobi,

Kenya.

11

CHAPTER 2

2.0 LITERATURE REVIEW

2.1 Introduction

This chapters presented literature and academic review on financial strategies with

reference NGOs. Books, journals as well as web articles had been used as the major

sources of literature in this chapter. The chapter had been prearranged with orientation of

the main areas that the study had focused on. The first section presents a literature review

on the theories related to income diversification as one of the financial strategies,

followed by second section presenting a literature review on the strategic partnerships.

The third section presents a literature review on strategic financial management and the

forth section elaborates on the literature related to NGO participation in income

generating activities. The last section of the chapter presents the chapter summary in

brief.

2.2 Income Diversification

Diversification of revenue is important to the organization so as to improve the financial

stability of NGOs. According to a survey done by Suri (2009), economic crisis has always

had a strong impact on the NGOs revenue trends with having decreased sources of funds.

In order to respond to the economic crisis, NGOs have tapped on international markets

for better funding streams.

As investigated by Boas (2012), financial support from international governments and

their respective agencies have assisted in providing the NGOs with great opportunities.

With the financial challenges that most NGOs have faced, responses to these challenges

with the same entrepreneurial attitude, efficient planning and hard work have at least built

a successful financial strategy for most of the NGOs in their main activities in terms of

financial sustainability (Bezuneh, 2000). NGOs have come up with numerous measures

by which fund raising activities have been represented and directed at the general public

by holding fund raising events. They have also managed to tap onto new corporate donors

for monetary and social support (Herlitschka, 2009). Cost-recovery components have also

been included in new program implementation strategies where the program pays all or

part of the program costs (Henin, 2002). To date, NGOs are seen to own and manage side

businesses such as restaurants, being part of tourist industry, medical clinics or other

businesses. As one of the definition stated by Henin, (2012), “The terms income

12

diversification describes a number of activities that strive to reduce the dependence on a

specific type of income (e.g. donations, earned income from a specific product or

service), specific donor or grant maker, dominating customer, country that is the only or

main source of funding and currency in which most or all funds are paid out”.

2.2.1 Resource-Based Theory

The resource based theory squabbles over the fact that organizations gain a competitive

advantage by building up and utilizing resources that are exceptional and tricky to copy

and substitute (Graff, 2011). Its existing importance is explained not only by its

supremacy in academic literature and journals, but also by its importance placed in the

strategic studies taught to students and undergraduate, masters’ and executive

practitioners (McWilliams & Seigel, 2001).

Conventional strategy models, such as Michael Porter’s five forces model, all center their

focus on an organization’s external competitive environment. Many such models neglect

the importance to focus on the organizations internal strengths and weaknesses. Converse

to that, the resource-based view strategy places a considerable importance on the need for

a link between the organizations internal capabilities and external environment (Graff,

2011). RBV strategy views the organizations as a compilation of different skills and

capabilities that pressures strategic financial growth and organizational development. This

tends to push most NGOs into more strategic financial management.

The RBV was a concept first recognized by Wernerfelt in 1984, and has even since

developed into a strategic thought of growth (Cleland, 2009). Depending on this view,

organizations develop their competitive advantage from their ability to gather and

develop an appropriate blend of resources. Since gaining sustainable competitive benefits

is attained by continuously working on exploiting or creating new resources, some

management specialists advice that organizations’ internal processes should work on

creating resource bundles that would assist them in building a sustainable competitive

advantage, whereby competitors would not be able to imitate the unique resource

combination (Meding, 2009). Meding (2009) also places a consideration on a fact which

is usually agreed upon most strategic managers and specialists; “Business strategy is

concerned with the match between the internal capabilities of the company and its

external environment”. Many NGOs that operate under financial distress and instability

witness an extreme unstable environment. These environmental distresses include local

economic conditions to regional politics, in which all areas of society face chaos in and

13

after political instability. In order for NGOs to match such an environment, the internal

capabilities of the organization must be supple, adaptive and varied (Meding, 2009).

Sharma (2000); classifies organizational resources into three main groups; physical

resources, human capital resources and organizational capital resources. These resources

are the ones that allow an organization to visualize and apply strategies that tend to

progress organizations efficiency and effectiveness. Nevertheless, under certain

conditions, such resources turn out to be a base for financial stability for the entire

organization.

An organization with more than one source of income and diversified RBV is likely to be

more broadened in their financial horizons than an organization that depends only on one

source of income. And also that an organization that has its income equally distributed

among its different sources of income would be more diversified than an organization that

has its income unequally distributed like 90% of income incorporated by one source and

10% by another (Yan, 2008). The resource-based view of an organization gives an

opportunity to diversify its income through identifying is applicable resources and with

appropriate utilization of each. For many NGOs, the degree of income diversification

depends on the amount of resources available in the organization, how are the resources

to be utilized, the percentage of funding available from donors, the proportion of funding

from international donors in comparison to funding from local donors, percentage of total

income being earned from self-financing and percentage of self-financing depending on

the largest customer or on largest selling product or service (Alymkulova, 2005).

Nevertheless, organizations that consider income diversification as one of their strategy

for financial sustainability must put into considerations some of the factors such as

organizational goals, organizational capacities in key areas and available strategies aimed

for income diversification.

For most NGOs, social projects work as a strategy to broaden their horizons on their

funding base, limit their dependence on donors and pull through and try to financially

support their entire program costs (Reardon, 2000). In these cases, social endeavors

would mainly offer ways to decrease program arrears and utilize the organizational

resources more efficiently. Social enterprise is recognized to be one of the main financial-

sustainability strategy constituent. It refers to any socially accountable income building

activity whose income is utilized to sustain and maintain the organization’s overall

mission (Grant, 2001). Increasing frustrations of the NGOs on their financial status quo

14

and their longing to minimize dependency on donors have pushed these organizations to

make use of the private sector entrepreneurial rules (Seipulnik, 2005). Counterparts have

initiated the social enterprise concept to NGOs in a belief to build a new strain of

entrepreneurs and to rouse the configuration of a larger and a more sustainable pool of

resources for NGO financial stability scheme (Mint, 2003).

Financial objectives are set by NGOs that seek to diversify their income knowing that

every organization is different and unique with its own capabilities (Barney, 2013).

However, there are different basis of practical support, defined information and thoughts

for NGOs that want to diversify their income base and survey on financial stability not

only as one particular source of income but rather as a whole process including various

related parts (Sharma, 2000).

Income diversification should start with strategic planning and analysis of both the

internal strengths and weaknesses of the organization as well as a scan of the external

environment in terms of competitor analysis, opportunities and other threats. Apart from

an analysis of the internal and external environment of the organization, and its cost

effectiveness and risk management, organizations also need to take in charge the

suitability of these activities in terms of the organizations’ mission, vision, values and

culture (Grant, 2001). NGO’s managers and leaders play a crucial role in determining the

necessary change required in the processes associated with revenue diversification, be it

an overall organizational change or a cultural change. There are many other ways to

increase funds both internationally and locally in different countries of the world. Some

of such sources of revenue give in direct financial assistance to NGOs for their social and

environment activities and programs. However others work through organizations that

prefer providing assistance on financing their projects on their behalf (Kaus, 2012).

The accomplishment of income diversification strategies and tactics are mainly dependent

on the organizations leadership capability to communicate effectively with the external

stakeholders of the NGOs. NGOs are required to reinforce consciousness and alertness

around the range of programs and activities that they commence and also have an added

value that they generate for the society; by assisting potential partners so as to assess their

different funding options (Minot, 2003). Large and widely based NGOs are more often

enhanced to broaden their horizons on their funding sources than most small NGOs. They

are usually opportune to take advantage of their recognizable name and logo. They are

15

also likely to have better technical skills which are used to support their social and

commercial activities (Lubatkin & Chatterjee, 2007). They are also known to have better

connections and links with outside groups to form collaborations with as one of the other

strategies of income diversification. Internally larger NGOs are also equipped with better

experience with working on new programs and adapting with organizational change.

Nevertheless, such large organizations together with the benefits that they opportune, they

often even have a greater need to look for more reliable funding from outside due to their

increased costs for support services and overhead (Shapiro, 2003). Smaller NGOs

however, are advantaged with a relatively small amount of self-earned revenue that is

more likely to make a large difference in ensuring their financial stability.

The potential proposition for resource dependence theory is diverse. At first, peripheral

control of NGOs through its exposure to the market forces or the external environment as

well as the use of the short-term contracts may lead to NGOs being business oriented.

This will help NGOs compete more effectively with other for-profit organizations and

increase their financial security. Secondly, external control of the NGOs may also

increase its ability to build innovative programs that would result in their goal

accomplishment. Bounded by the external environment, NGOs are encouraged to

influence their programs to match with the preference requirement of their donors,

regardless of the organizations’ beneficiary need.

2.3 Strategic Partnerships

The rising interests in strategic partnerships can be credited to “the realization that

strategic partnering can promote effective results for all concerned: Businesses, NGOs

and especially the society/community” (Boue & Kjaer, 2010). Therefore, strategic

partnership had also been identified as one of the financial strategies for NGOs. The

several studies that have focused on the strategic planning as a financial factor for NGOs,

according to the researcher’s knowledge have missed out on the elaboration of the

correlation it held on the overall financial sustainability of the organization. As

demonstrated by Grunewald (2011), strategic partnership between NGOs and other

business organizations is seen to strengthen the quality of humanitarian aid, but the limit

to which it contributes to its financial sustainability had not quite been elaborated in brief.

A study by Damlamian (2006) have focused on corporate and NGO partnerships as a

sustainability factor for the development of both the organization, once again, the

elaboration on how the strategic partnership effects the financial sustainability of the

16

NGO had not quiet been focused on. Nevertheless, there has been no particular theory

that dealt with all the different aspects of the strategic partnerships of NGOs with other

businesses. The study literature therefore reviewed the well-entrenched theories, such as

the stakeholders theory, transaction cost theory and social-network theory as they are

important to the strategic partnership of NGOs with other businesses.

2.3.1 Stakeholders Theory

Most financial and strategic management of NGOs view their organization’s primary

function being the maximization of their financial returns (Neegargard, 2010), however,

the stakeholder theory takes a step ahead in the organization’s objectives in terms of its

functions and dependencies. Stakeholder theory is one of the firm management theories

that have been developed by R.E. Freeman. The theory was to address the question of

why businesses should consider prioritizing the interests of the organization’s

stakeholders and build value for their shareholders (Boue & Kjaer, 2010). Freeman

widely describes a stakeholder as any individual or group who affects or is affected by the

organizations objectives, either achieved or lost (Freeman & Reed, 1983). A more narrow

definition to it can however be stated as stakeholders being groups or individuals, on

which the organization is entirely dependent on for its sustainability (Fontaine, Haarman

& Schmid, 2006). Freeman also argues that a success of an organization is dependent on

the management of the different and more often conflicting interests of the organizations

stakeholders and simultaneously on the never ending management of the organizations

over all relationships with its stakeholders (Freeman, 1984).

Gradually, stakeholders have started questioning the organizations on how do they serve

the society and what can they do to these societies and the other way round of questioning

the society on what it can do for the organization (Warhurst, 2005). Many of the

stakeholders have been pressurizing the organizations to change according to their

expectations. Moreover, a study by Boer & Kjaer (2010) also states that stakeholders

have started requiring their organizations “to be a positive force, to contribute to broader

societal development goals and to work in partnership with others to solve

humanitarian crises and endemic problems facing the world such as disease and poverty,

climate change and environmental stewardship”.

Due to the accelerating pressures and risk of losing reputation of the poor management of

stakeholders, organizations and other companies have begun to pay more attention and

prioritize the needs of the stakeholders (Googins and Rochlin, 2000). Organizations have

17

started to react with the attempt to appeal to and connect with their stakeholders, hence

leading them to look through the stakeholder management (Huijstee & Glasbergen,

2008). Given that the stakeholders’ expectations keep changing over time, dialogue is

important to sense their constantly changing interests and demands. Dialogue is also

useful in giving the organization’s own viewpoint to the stakeholders (Waddock, 2002).

However such dialogue could appear in many ways. Morsing & Schults (2006)

differentiates between the different communication strategies starting from the lowest

levels of intensity where the flow of information is just in one direction, to high

interactive involvement where stakeholders are directly engaged (Morsing & Schults,

2006).

NGOs are normally supposed to be substitutes for societal and environmental needs as

their organizational objectives are usually based on social representation (Valor & Diego,

2009). For business organizations, working with the NGOs can be more suitable than

trying to please and managing every stakeholder individually (Warhurst, 2005).

According to the stakeholder’s theory, forming strategic partnerships with NGOs has

been seen as the most potential stakeholder management approach as it would allow a

higher degree of information and knowledge flow. Hence, stakeholder theory holds much

potential to elaborate the growing interests in the strategic partnerships between the

NGOs and businesses, but however it fails to explain the impact it has on the

sustainability of the NGOs.

2.3.2 Transaction Cost Theory

The transaction cost theory states that “in imperfect markets, organizations face positive

transaction costs which have influence on the price of market transactions” (Graf &

Rothlauf, 2011). Graf & Rothlauf (2011) also describes transactional costs as “costs for

running an economic system”. Costs as such include contracting and negotiating costs as

well as costs incurred in monitoring and governance. Contracts don’t usually include all

possibilities that the organization may encounter and they therefore need to be

renegotiated. This usually accounts for extra costs to be incurred for the organization to

encounter.

Forming strategic partnerships with other businesses can assist in lowering such

transactional costs through adopting some of the externalities that consequence from

bargaining and contracting (Barney, 2013). Strategic partnerships usually entail contracts

that put both the partnered organization into a mutual hostage position. This lowers the

18

chances for the partners to get involved in other opportunistic behaviors, hence lowering

the overall transaction costs and therefore stabilizing the financial position of the

organization (Arya & Salk, 2006).

Lowering transactional cost through formation of strategic partnerships also reduces

interdependence and risks and thus improves efficiency (Yaziji & Doh, 2009). Risk

reduction can also be achieved by sharing the risks with the partner. This is why projects

that involve higher level of risk or large resource involvement may run through strategic

partnerships and not just by one organization on its own (Pfeffer & Salancick, 1978).

Transactional cost minimization hence plays a role in strategic partnerships since firms

can reduce risk and reach financial sustainability (Iyer, 2003).

According to Schoonhoven (1996) firm-NGO strategic partnerships permits businesses to

achieve a level of financial sustainability which would allow them to take ahead their

organizational activities without trouble. These objectives can be attained with minimized

costs when organizations form strategic partnerships rather than launching activities on its

own (Penrose, 2009). The focal firm can make use of the NGOs reputation within the

society, which otherwise would be needed to be built up from the beginning. For a firm to

build reputation on its own Das & Teng (2009) states examples of monetary costs for

advertising and managing offices for corporate matters and communication including

costs for developing product quality to be addressed by the firm. However giving too

much importance to reputation, brand and quality development may push the organization

to bankruptcy (Arya & Salk, 2006).

2.3.3 Social Network theory

Social Network theory is another theory that gives importance to strategic partnerships of

NGOs with other business organizations. It gives a sociological view point of how

relationships are recognized and maintained. This theory is measured to be the focal to

strategic partnerships of NGOs with business organizations. It places its main focus on

social interface and network relations between and within organizations (Yaziji & Doh,

2009). Understanding such relationships is critical because as Boue & Kjaer (2010) the

social background from previous partnerships and considering importance to strategic

independence can pressure partnership decisions. Social network theory is likely to

provide significant data about the partnered organizations’ capability and reliability.

19

There are two important considerations to be placed in the social network theory (Kilduff

& Tsai, 2003), the structural pattern of the network itself, and the capability and objective

of individual actors. The theory studies the relationship between the organizations in

society that are symbolized by a separate system (individuals, groups, organizations).

Social capital is one of the important elements of consideration in the social network

theory and is known to be a prerequisite for the social development of transferring and

exploiting knowledge required for the partnership to succeed. This explains and pressures

on the knowledge of how possible synergies come into consequence (Selsky & Parker,

2005). Social network theory also highlights the importance of trust in relationships. As

Selsky and Parker (2005) explains in their study, that trust guides partners to incorporate

the partnership into their own framework.

2.4 Strategic Financial Management

With the rising expansion of the number of Not-for-profit organizations around the world,

running these important organization have been seen to be a challenge. NGOs, like any

other business organization have ongoing processes in order to look for different models

and tools that will assist them in managing and expanding themselves in a way related to

their mission, vision, values and culture (Samour, 2012). Hard efforts as surveyed have

been witnessed in some areas such as marketing, finance, human resource and

information technology. Nevertheless, there also has been a constant increase in needs to

look for appropriate methods to assist NGOs in addressing some of the main queries

about their purposes, such as, “What are they trying to achieve?”, “How are they going to

determine and achieve their missions and goals?”. These are the basic questions that

mainly fall into the concept of strategic financial management (Analoui, 2012).

Financial Management in NGOs is mainly related to making sure that required funds are

obtainable during the time of need and that they are accessible and most efficiently

utilized in ways that benefit the NGO (Bromideh, 2011). From an organization’s practical

point of view, financial management is mainly linked with appropriate financial planning

and control of the organization’s resources. Financial planning aims to enumerate

different financial resources that are available and maps the amount of expenditure

required. Nevertheless, financial management practices requirement can inflict a

significant burden on NGOs (Sharma, 2000). It is crucial to manage the movement of

cash flows in relation to the allocated budget for the project. Mainly, at a more corporate

20

level, the organizations aim lies in the progress of managing the financial status quo and

to achieve various goals that the organization sets at a given point of time (Ahmed, 2012).

Financial managers therefore strive to boost the resources at their point of disposal.

2.4.1 Agency Theory

A strong rule for financial planning, control and budgeting is to take it as a strategic

process. Firstly it is crucial to understand that the capabilities and future opportunities of

the NGO lie on the organizational ability to secure their funding so as to develop and

progress their projects. Also to be kept in mind that all the members of the organization

are to be equally taking part in the planning organizing and monitoring process of the

financial stability of the organization and not only those members who are directly in

charge of the functions of the organization (fundsforngos, 2013).

The Agency theory gives a structure of how the relationships between the different

interest groups within an organization exist and are managed. It views the organization as

a compound unit that holds various interest groups (Lewis, 2009). Each of these interest

groups tend to hold their own interests and makes sure that their interest do also serve as

an advantageous factor to the organization. Each entity group nevertheless recognizes the

fact that their success is a result of their organizational sustainability. This theory brings

out an absolute illustration of some of the actions of managers who serve to their own

interests that contradicts with the objective of the organization (Rojas, 2007).

Agency relationship is usually seen in organizations where one person called the Principal

appoints another person called the Agent, to execute some of the duties of the principal

and provides the agent with the suitable decision making authorities. In relation to

strategic financial management, such relationship is usually seen between the

shareholders and managers or the creditors and shareholders (Serpa, 2008). To be crystal

clear on the strategies to be adopted enhances the organizations credibility in the

community and from the donor’s point of view. Effectiveness of the financial plan is also

equally crucial depending on a strong organizational plan. It is important for the

organization to see not only the effectiveness of a long-term strategy but also to develop

skills that are able to manage the budgetary controls and short-term operations

(fundsforngos, 2013). A financial instrument therefore as described by Ahmed (2012) is

“A contract that gives rise to both a financial asset of one enterprise and a financial

liability of another enterprise”. When placing a consideration on financial assets, these

21

can be described as investments in equity and government securities (Hill, 2012). With

such critical management of financial assets it is quite natural with the existence of the

agency relationships, conflicts of interests are ought to happen. These conflicts are

defined as the agency problem which is known as the underlying reason behind the

unstable financial status of most NGOs around. Owolabi (2010) elaborates in his study

that choices of the various appraisal technique is one of the reasons behind most of the

agency theory problems where managers in pursuit of their own interest, would prefer

taking over projects with short lives than those financial opportunistic projects but with

longer lives. Asset selection and capital budgeting in NGOs therefore need to be

addressed with better understanding techniques (Cleland, 2009).

With reference to the study by Oyedele (2013), most NGOs are vulnerable to agency

problem due to the appraisal of risky projects where financial managers undertake risky

projects due to their own personal financial benefits. With most NGOs being highly risk

adverse due to their sensitive financial status, their strategic financial management is

usually poor because of these agency problems. Strategic financial management therefore

defines the importance of its effectiveness with the financial stability that it provides if

these agency relationships are managed accordingly.

2.4.2 Corporate Governance

When strategic financial management is kept into consideration, there are several other

terminologies that come into picture as other financial instruments. Such would include

originated loans and receivable; these are liabilities formed by the organization as a result

of lending money to debtors. The organization would also have other financial liabilities

which would mainly comprise of unrealized and unexpected grants as well as trade

creditors. Noting these financial instruments, if used efficiently the organization can

manage to find a balance between the debt and equity levels of the organization which

would then assist them in achieving its missionary objectives and also ensuring the most

efficient use of resources (Khun, 2011). However, consequences of poor financial

management are nevertheless very serious resulting to lack of financial stability of the

organization. Good financial management processes require effective organizational

planning and implementation of workable schemes and processes that can react positively

with the financial challenges faced by the NGOs. In general, money is the base of

survival for all organization. It is the one thing that takes up majority of management’s

time.

22

With the current global economy, the growth of the national economy is usually depended

on the important role of an organization’s supremacy, transparency and the competitive

structure within which it operates. This is due to the fact that it is these organizations that

build the national economic value (Rojas, 2007).

According to Rauh (2010), the NGO sector has always been seriously challenged by the

difficulties of choosing and utilizing the appropriate tools of management, such as

strategic management tool that would allow the organizations to improve efficiency in

their overall organizational performance. Within an organizational culture that is doubtful

of both the private and public sectored organizations owning various techniques and

motivations, it is crucial for an organization to work on the appropriate management tool.

It is accounted that many of the NGOs now put into practice quarterly-annual processes

more often aiming to place the organization in its targeted position in regards to its

mission and long term goals (Suarez, 2003).

Corporate Governance as defined by Dayton (1984) stated it as processes, associations,

and arrangements through which the board of directors supervises the work done by the

executives and ensures that work is appropriately done so as to achieve the objective of

the organization. While investigation by Rauh (2010) declared that NGOs also have a

mission, strategy and goals but different from profit making organizations, other scholars

argued that NGOs are also concerned with using their management practices as fluent as

those utilized by other private companies (Hill, 2012). Suarez’s (2003) study also argued

that attaining goals and surviving through financial challenges need appropriate

responding and adjusting to social, economic, political and legal environment and the

changes that they unfold. He also added to this argument that strategic planning is as

important for NGOs as it is for every other type of organization.