Private complementary coverage in Private complementary coverage in France France Role, regulation, market, and Role, regulation, market, and challenges challenges Valérie PARIS – December 7th, 2006 Valérie PARIS – December 7th, 2006 Joint OECD / Korea Centre of Health and Social Joint OECD / Korea Centre of Health and Social Policy Policy

Private complementary coverage in France Role, regulation, market, and challenges Valérie PARIS – December 7th, 2006 Joint OECD / Korea Centre of Health.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Private complementary coverage in Private complementary coverage in FranceFrance

Role, regulation, market, and Role, regulation, market, and challengeschallenges

Valérie PARIS – December 7th, 2006Valérie PARIS – December 7th, 2006Joint OECD / Korea Centre of Health and Social Joint OECD / Korea Centre of Health and Social

PolicyPolicy

Outline of the presentationOutline of the presentation

• Role of the private complementary Role of the private complementary insurance in Franceinsurance in France

• Stakeholders on the market of Stakeholders on the market of complementary insurance: status complementary insurance: status and regulationand regulation

• Challenges for the French health Challenges for the French health systemsystem

The role of Voluntary Health Insurance The role of Voluntary Health Insurance (VHI) in France (1)(VHI) in France (1)

• Mandatory basic coverage by social Mandatory basic coverage by social health insurancehealth insurance

• Cost-sharing for most goods and servicesCost-sharing for most goods and services• Scope for voluntary complementary Scope for voluntary complementary

coveragecoverage• VHI finances 13% of health expendituresVHI finances 13% of health expenditures• Share of VHI in total expenditures varies Share of VHI in total expenditures varies

for different types of carefor different types of care

The role of Voluntary Health Insurance The role of Voluntary Health Insurance (VHI) in France (2)(VHI) in France (2)

• Voluntary coverage provided by private institutions, which Voluntary coverage provided by private institutions, which actually provide two types of insurance:actually provide two types of insurance:– Complementary coverage for goods and services Complementary coverage for goods and services

incompletely covered by the statutory health insurance:incompletely covered by the statutory health insurance:•Co-insurance rateCo-insurance rate•Extra-billings (on average + 17% / official tariff for Extra-billings (on average + 17% / official tariff for

specialists, 40% for surgeons, 30% for ophthalmologists)specialists, 40% for surgeons, 30% for ophthalmologists)•Prices of medical goods exceeding reimbursement pricesPrices of medical goods exceeding reimbursement prices

– Supplementary coverage for goods and services which are Supplementary coverage for goods and services which are not reimbursed at all by the statutory health insurancenot reimbursed at all by the statutory health insurance•e.g. individual room in private hospitals, alternative e.g. individual room in private hospitals, alternative

medicine non covered by statutory health insurancemedicine non covered by statutory health insurance

VHI role in financing of health VHI role in financing of health expenditures, by type of care - 2005expenditures, by type of care - 2005

29%

18%

21%

3%

22%

35%

11%

18%

20%

9%

2%

4%

13%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Other med. Goods

Pharmaceuticals

Medical goods

Transport

Laboratory

Dentists

Auxiliaries

Physicians

Ambulatory care

Private hosp

Public hosp

Hospital care

Total

Source: National Health Accounts (DREES)

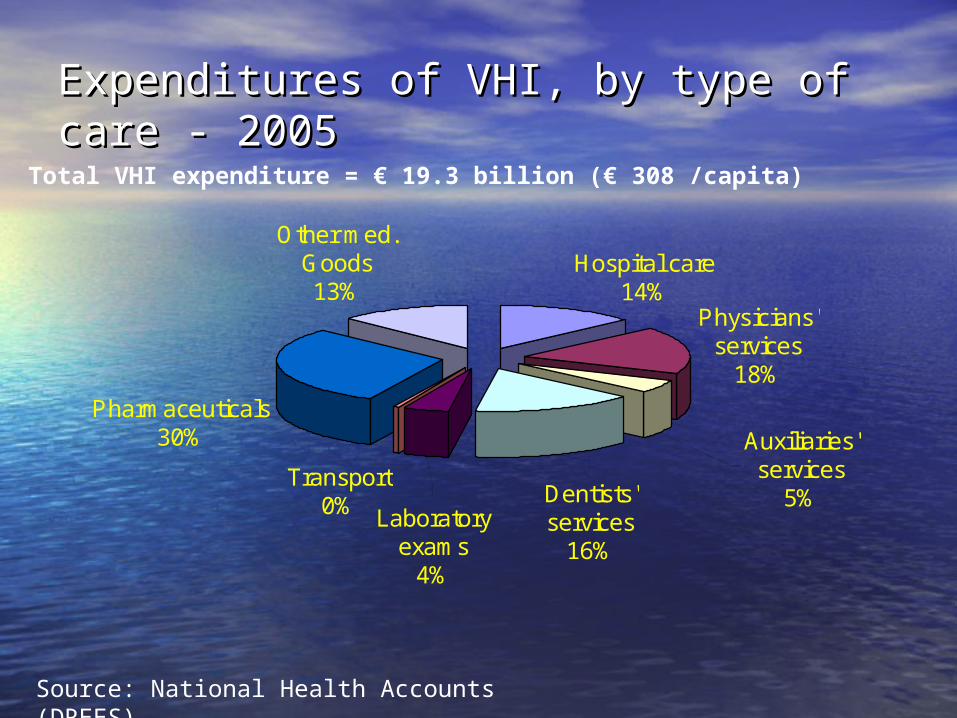

Expenditures of VHI, by type of care - Expenditures of VHI, by type of care - 20052005

Hospital care14%

Physicians' services

18%

Transport0%

Pharmaceuticals30%

Other med. Goods13%

Dentists' services

16%

Auxiliaries' services

5%Laboratory

exams4%

Source: National Health Accounts (DREES)

Total VHI expenditure = € 19.3 billion (€ 308 /capita)

The market of VHI: stakeholdersThe market of VHI: stakeholders

• Three types of institutions:Three types of institutions:– Mutual fundsMutual funds– Provident institutionsProvident institutions– Insurance companiesInsurance companies

• With different characteristics and With different characteristics and regulationregulation

The market of VHI: The market of VHI: Mutual funds Mutual funds (1)(1)

• Have been existing before 1945 Social Have been existing before 1945 Social Security ActSecurity Act

• Not-for-profit institutions, mainly financed Not-for-profit institutions, mainly financed through members’ contributions, in order to through members’ contributions, in order to provide providence, solidarity and mutual provide providence, solidarity and mutual aid to their members and their families.aid to their members and their families.

• Governed by decisions of members’ Governed by decisions of members’ representativesrepresentatives

• Limited use of risk-rating or risk-selection Limited use of risk-rating or risk-selection strategiesstrategies

The market of VHI: The market of VHI: Mutual funds Mutual funds (2)(2)

• Several types:Several types:– National funds for civil servantsNational funds for civil servants– Company-based, professional, inter-Company-based, professional, inter-

professionalprofessional– General recruitmentGeneral recruitment

• Some of them provide goods and services Some of them provide goods and services (hospitals, dental and optical care, (hospitals, dental and optical care, pharmacies)pharmacies)

• Some of them manage claims process on Some of them manage claims process on behalf of basic health insurancebehalf of basic health insurance

The market of VHI: The market of VHI: Mutual funds Mutual funds (3)(3)

• In 2001: In 2001: – 549 health funds (covering more than 549 health funds (covering more than

3,500 members each)3,500 members each)– 29.9 million people covered29.9 million people covered– For 20.5 million people contributingFor 20.5 million people contributing– Health = 95% of outlays (health, Health = 95% of outlays (health,

providence, social aid)providence, social aid)

• Consolidation within the past 10 years, Consolidation within the past 10 years, due to European legislationdue to European legislation

Source: Roussel, 2003

The market of VHI: The market of VHI: provident provident institutions institutions

• Private, not-for-profitPrivate, not-for-profit• Initiated by employers and employees, Initiated by employers and employees,

and administered by boards with equal and administered by boards with equal representation representation

• Mainly oriented towards collective Mainly oriented towards collective coverage and social protection coverage and social protection

• In 2001In 2001– 78 PI provide health coverage, for 5 million 78 PI provide health coverage, for 5 million

people (through mandatory membership for people (through mandatory membership for 80% of them)80% of them)

The market of VHI: The market of VHI: Insurance Insurance companiescompanies

• Two types, both privateTwo types, both private– Insurances: for-profit insurance companiesInsurances: for-profit insurance companies– Mutual insurances: insured members Mutual insurances: insured members

grouped on socio-professional basis and grouped on socio-professional basis and proprietors of the society – not-for-profitproprietors of the society – not-for-profit

• About 118 companies operate on the About 118 companies operate on the French market for health insuranceFrench market for health insurance

• Health represents 5% of their revenueHealth represents 5% of their revenue

VHI market (% of VHI expenditures, VHI market (% of VHI expenditures, 2005)2005)

Mutual funds56,9%Provident

institutions19,2%

Private Insurance

23,9%

Source: National Health Accounts (DREES)

VHI market: types of contractsVHI market: types of contracts

• Individual (40%)Individual (40%)

• Collective contracts (56%)Collective contracts (56%)– Generally co-sponsored by employersGenerally co-sponsored by employers– Mandatory in 50% of casesMandatory in 50% of cases

• Inequities in coverage and quality of Inequities in coverage and quality of coverage, according to activity, coverage, according to activity, sector of activity, professional status, sector of activity, professional status, ageage

Source: French Health, Health Care and Insurance Survey (ESPS), IRDES

Note: 3.5% of people do not know

Employer-sponsored Individual

% of population covered 56,4 40,1

By type of VHI

Mutual fund 56,6 62,7

Provident institution 19,2 6,4

Insurance company 19,9 28,2

n.a. 4,3 2,6

Type of affiliation and type of VHI (2004)Type of affiliation and type of VHI (2004)

Regulation: regulatory bodies and Regulation: regulatory bodies and legislationlegislation

Regulatory body and Regulatory body and legislationlegislation

Mutual funds /Mutual funds /

Provident Provident InstitutionsInstitutions

Ministry of social security Ministry of social security

Code de la Mutualité / Code de la Code de la Mutualité / Code de la protection socialeprotection sociale

Insurance Insurance companiescompanies

Ministry of Eco and FinanceMinistry of Eco and Finance

Code des assurancesCode des assurances

• The Commission for the control of mutual The Commission for the control of mutual funds, insurance companies and provident funds, insurance companies and provident institutions is responsible for consumer institutions is responsible for consumer protectionprotection

Regulation (1)Regulation (1)

• Exclusion of medical condition Exclusion of medical condition – Not allowed for collective contractsNot allowed for collective contracts– Allowed in individual contracts, with two Allowed in individual contracts, with two

conditionsconditions• Consumer must be informed of medical conditions Consumer must be informed of medical conditions

excluded prior to enrolmentexcluded prior to enrolment• In case of litigation, the insurer has to prove that the In case of litigation, the insurer has to prove that the

condition existed before enrolmentcondition existed before enrolment– After two-years, the insurer can not unilaterally After two-years, the insurer can not unilaterally

terminate the contractterminate the contract• Continuity of protectionContinuity of protection

– Collective contracts obtained through Collective contracts obtained through employment: the insurer is required to offer a employment: the insurer is required to offer a contract at retirement, with a premium capped contract at retirement, with a premium capped at 150% of the previous premiumat 150% of the previous premium

Regulation (2)Regulation (2)

• SpecialisationSpecialisation– Institutions providing insurance Institutions providing insurance

coverage can not provide other coverage can not provide other commercial servicescommercial services

– Issue for mutual funds formerly Issue for mutual funds formerly providing medical servicesproviding medical services

• Solvency requirementsSolvency requirements

Regulation (3)Regulation (3)

• Premiums requirementsPremiums requirements– Solidarity principle: premiums can be Solidarity principle: premiums can be

adjusted to take into account: income, adjusted to take into account: income, enrolment duration, mutual fund, enrolment duration, mutual fund, geographic location, number of geographic location, number of beneficiaries, age.beneficiaries, age.Typically mutual funds, PITypically mutual funds, PI

– If not, no requirement If not, no requirement Insurance companies often use health Insurance companies often use health

questionnaires to adjust premiumsquestionnaires to adjust premiums

Regulation (4)Regulation (4)

• Tax incentiveTax incentive– 7% of tax reduction on complementary 7% of tax reduction on complementary

health coverage for contracts compliant health coverage for contracts compliant with with the solidarity principlethe solidarity principle (i.e. not (i.e. not requesting health information before requesting health information before enrolment and not linking premiums to enrolment and not linking premiums to health status) health status)

– Since 2004, contracts must also be Since 2004, contracts must also be “responsible” to benefit from tax reduction“responsible” to benefit from tax reduction

Regulation: benefits requirementsRegulation: benefits requirements

• Creation of responsible contracts by the Health insurance reform, August 13, 2004, with specific requirements– No coverage of the deductible of €1 per physician visit– No coverage of penalties (increased cost-sharing and

possible extra-billing) for non-coordinated care– Coverage of cost-sharing for physician visits up to

100%– Coverage of cost-sharing for prescribed (important)

pharmaceuticals and laboratory exams up to 95%– Coverage up to 100% of at least 2 procedures in a list

of preventive procedures established by the Ministry of Health

Regulation: specific rules for Regulation: specific rules for complementary health universal complementary health universal coverage (CMU-C)coverage (CMU-C)• Inequities in complementary coverage and access Inequities in complementary coverage and access

to care to care • Creation of CMU-C in 2000Creation of CMU-C in 2000

– Means-tested access to free complementary health Means-tested access to free complementary health insurance (CMU-C) for the poorest part of the population. insurance (CMU-C) for the poorest part of the population.

– CMU-C provided by VHI institutions OR by sickness funds, CMU-C provided by VHI institutions OR by sickness funds, in exchange for a flat premium paid by a specific national in exchange for a flat premium paid by a specific national fundfund

– Benefit basket defined by the StateBenefit basket defined by the State– Providers not allowed to charge extra-billingProviders not allowed to charge extra-billing– Direct payment by third-party payersDirect payment by third-party payers

– In 2005, 4.7 million beneficiaries (7.5% of the population) In 2005, 4.7 million beneficiaries (7.5% of the population)

Regulation: specific rules for Regulation: specific rules for complementary health universal complementary health universal coverage (CMU-C)coverage (CMU-C)• Remaining issues:Remaining issues:

– Non take-up of CMU-C by eligible peopleNon take-up of CMU-C by eligible people– Refusal of care by health professionalsRefusal of care by health professionals– Lack of complementary insurance for people with Lack of complementary insurance for people with

income above the threshold for CMU-C eligibilityincome above the threshold for CMU-C eligibility

• Completed by vouchers for the purchase of Completed by vouchers for the purchase of complementary insurance for people with revenues complementary insurance for people with revenues exceeding CMU-C income threshold by less than exceeding CMU-C income threshold by less than 15%15%– Non take-up by eligible peopleNon take-up by eligible people

A new role for VHI institutions?A new role for VHI institutions?

• Until now, VHI institutions have been passive Until now, VHI institutions have been passive payers of co-paymentspayers of co-payments

• In 2004, creation of the Board of VHI In 2004, creation of the Board of VHI institutionsinstitutions– Gives advices to the Board of basic health insurance Gives advices to the Board of basic health insurance

about inclusion of procedures in the benefit basketabout inclusion of procedures in the benefit basket– Participates in the committee which negotiates drug Participates in the committee which negotiates drug

prices with the pharmaceutical industryprices with the pharmaceutical industry

• Some VHI announced that they will not cover Some VHI announced that they will not cover drugs whose reimbursement rate has been drugs whose reimbursement rate has been lowered to 15%lowered to 15%

A new role for VHI institutions?A new role for VHI institutions?

• Recent (and rare) new forms of Recent (and rare) new forms of contracts: contracts: – Bonus contracts: reduced premium Bonus contracts: reduced premium

associated with a deposit, which can be associated with a deposit, which can be partly (totally) refunded to the insured if the partly (totally) refunded to the insured if the level of benefits received is lower than the level of benefits received is lower than the deposit (or null)deposit (or null)

– Contracts with incitation to “preventive” care Contracts with incitation to “preventive” care (expenditures for supposed “healthy food” (expenditures for supposed “healthy food” partially reimbursed to the insured)partially reimbursed to the insured)

Impact of VHI on French health systemImpact of VHI on French health system

• Suspected of thwarting cost-containment plans Suspected of thwarting cost-containment plans based on increases in cost-sharingbased on increases in cost-sharing

• Has become indispensable for access to care Has become indispensable for access to care because of increases in cost-sharing on necessary because of increases in cost-sharing on necessary carecare

• Creation of CMU-C for poor people not covered by Creation of CMU-C for poor people not covered by complementary protection and of vouchers for the complementary protection and of vouchers for the purchase of complementary insurancepurchase of complementary insurance

• In terms of equity, VHI is regressive while basic In terms of equity, VHI is regressive while basic coverage is slightly progressivecoverage is slightly progressive

• Expansion of VHI coverage allows cost-shifting and Expansion of VHI coverage allows cost-shifting and therefore prevents from more rationale definition therefore prevents from more rationale definition of benefit basket insured by basic health insuranceof benefit basket insured by basic health insurance

Useful referencesUseful references

Private insurance in France,

T.C. Buchmueller & A. Couffinhal,

OECD Health working paper No. 12

Thank you for your Thank you for your attentionattention

Related Documents