Accounting for the Intel Pentium Chip Flaw Assignment Questions Question 1 Consider the following dates in the evolution of the Pentium chip during 1994: June 30: Intel has discovered the flaw. October 31: Dr. Nicely has posted information about the flaw on the internet and started an active discussion group. November 25: Article in Electrical Engineering Times has appeared, a story has been broadcast on CNN and articles have appeared in the New York Times and Boston Globe. December 12: IBM announces that it has stopped shipments of its computers with the flawed Pentium chip. At any of these dates, did Intel have a contingent liability as defined by FAS No.5? Accounting for the Intel Pentium Chip Flaw Situation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting for the Intel Pentium Chip Flaw

Assignment Questions

Question 1

Consider the following dates in the evolution of the Pentium chip during 1994:

June 30: Intel has discovered the flaw.

October 31: Dr. Nicely has posted information about the flaw on the internet and started an active discussion group.

November 25: Article in Electrical Engineering Times has appeared, a story has been broadcast on CNN and articles have appeared in the New York Times and Boston Globe.

December 12: IBM announces that it has stopped shipments of its computers with the flawed Pentium chip.

At any of these dates, did Intel have a contingent liability as defined by FAS No.5?

Accounting for the Intel Pentium Chip Flaw

Situation

On December 20, 1994 XYZ Corp, had a chemical spill in a field adjacent to their factory. They completed and paid cash for the immediate clean up prior to their December 31 year-end. However, they have consulted with an environmental engineering firm that indicated that there is a 90% chance that XYZ will have to perform a further clean up in six months. The cost of such a cleanup would most likely be $100,000. If the weather is perfect during the cleanup, it could cost as little as $95,000. On the other hand, there is a small chance that soil contamination could spread, increasing the costs to $150,000. Should XYZ recognize a liability in their 1994 financial statements? Assuming they do, what amount should be recognized? How would XYZ record such a liability on their books? What impact would the subsequent cash payment have if the liability were settled for the amount accrued? What if the actual clean-up costs are more or less than was accrued in 1994?

Example of Depreciation

Example 1

Elite Leisure is a private limited company that operates a single cruise ship. The ship was acquired on 1 January 2003. Details of the cost of the ship’s components and their estimated useful lives are:

Component Original cost($ million)

Depreciation Basis

Ship’s fabric (hull, decks, etc) 300 25 years straight-lineCabin and entertainment area fittings 150 12 years straight linePropulsion system 100 Useful life of 40,000 hours

Up to 31December 2010, no further capital expenditure has been incurred on the ship.

In the year ended 31 December 2010 the ship has experienced a high level of engine trouble which had cost the company considerable lost revenue and compensation costs. The measured expired life of the propulsion system at 31 December 2010 was 30,000 hours. Due to the unreliability of the engines, a decision was taken in early January 2011 to replace the whole of the propulsion system at a cost of $140 million. The expected life of the new propulsion system was 50,000 hours and in the year ended 31 December 2011 the ship had used its engines for 5000 hours.

At the same time as the propulsion system replacement, the company took the opportunity to do a limited upgrade to the cabin and entertainment facilities at a cost of $60 million and repaint the ship’s fabric at a cost of $20 million. After upgrade of the cabin and entertainment area fittings it was estimated that their remaining life was five years (from the date of the upgrade). For the purpose of calculating depreciation, all the work on the ship can be assumed to have been completed on 1 January 2011. All residual values can be taken as nil.

Required:

Calculate the carrying amount of Elite Leisure’s cruise ship at 31 December 2011 and its related expenditure in the income statement for the year ended 31 December 2011. You answer should explain the treatment of each item.

Analysis

Although there is only one ship, the ship is a complex asset made up from a number of smaller assets with different costs and useful lives. Each of the component assets of the

ship will be accounted for separately with its own cost, depreciation and profit or loss on disposal.

At 31 December 2010, the ship is eight years old.

Propulsion system

Carrying value on 31 December 2010: $m

Cost 100Accumulated depreciation to 31 December 2010(100m x 30,000 hrs/40,000 hrs) 75Carrying value on 31 December 2010 25

The old engine will be scrapped giving rise to a $25m loss on disposal.The new engine will be capitalised and depreciated over their 50,000 hour working life. The depreciation charge for current year to 31 December 2011 will be $140m x 5,000 hrs/50,000hrs = $14m.

Cabin and Entertainment area fittings

Carrying value on 31 December 2010: $m

Cost 150Accumulated depreciation to 31 December 2010(150m x 8 yrs/12 yrs) 100Carrying value on 31 December 2010 50

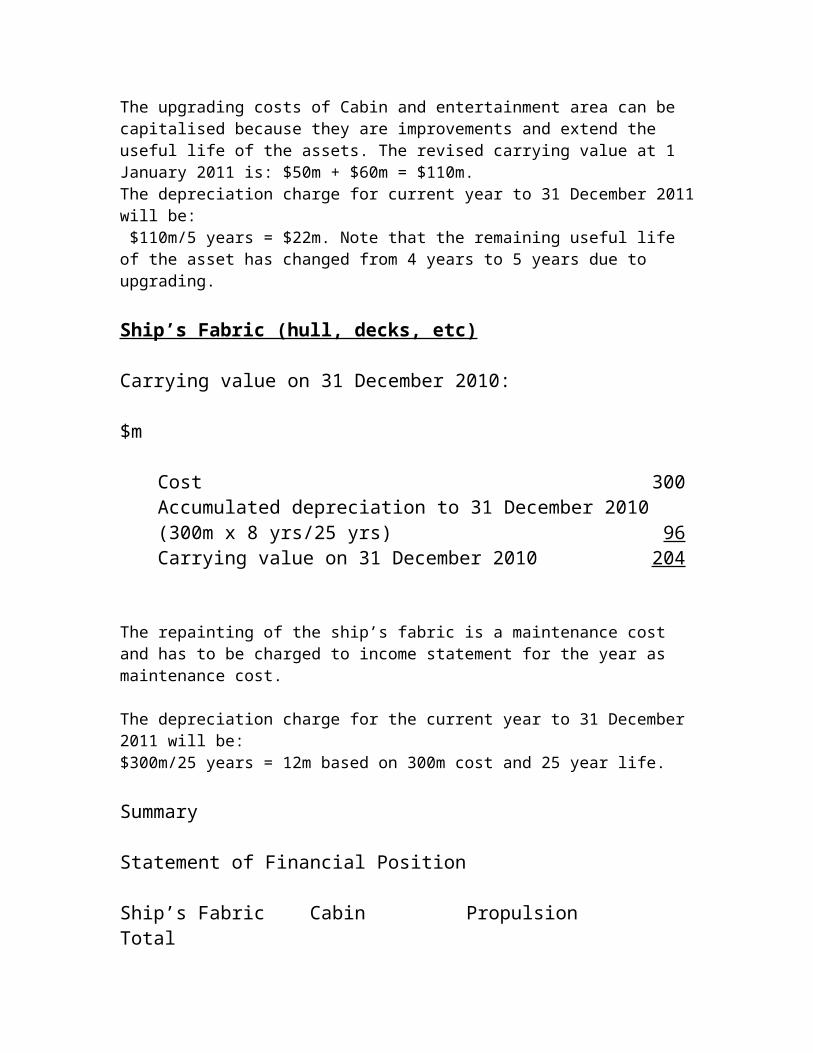

The upgrading costs of Cabin and entertainment area can be capitalised because they are improvements and extend the useful life of the assets. The revised carrying value at 1 January 2011 is: $50m + $60m = $110m.The depreciation charge for current year to 31 December 2011 will be: $110m/5 years = $22m. Note that the remaining useful life of the asset has changed from 4 years to 5 years due to upgrading.

Ship’s Fabric (hull, decks, etc)

Carrying value on 31 December 2010: $m

Cost 300Accumulated depreciation to 31 December 2010(300m x 8 yrs/25 yrs) 96Carrying value on 31 December 2010 204

The repainting of the ship’s fabric is a maintenance cost and has to be charged to income statement for the year as maintenance cost.

The depreciation charge for the current year to 31 December 2011 will be:$300m/25 years = 12m based on 300m cost and 25 year life.

Summary

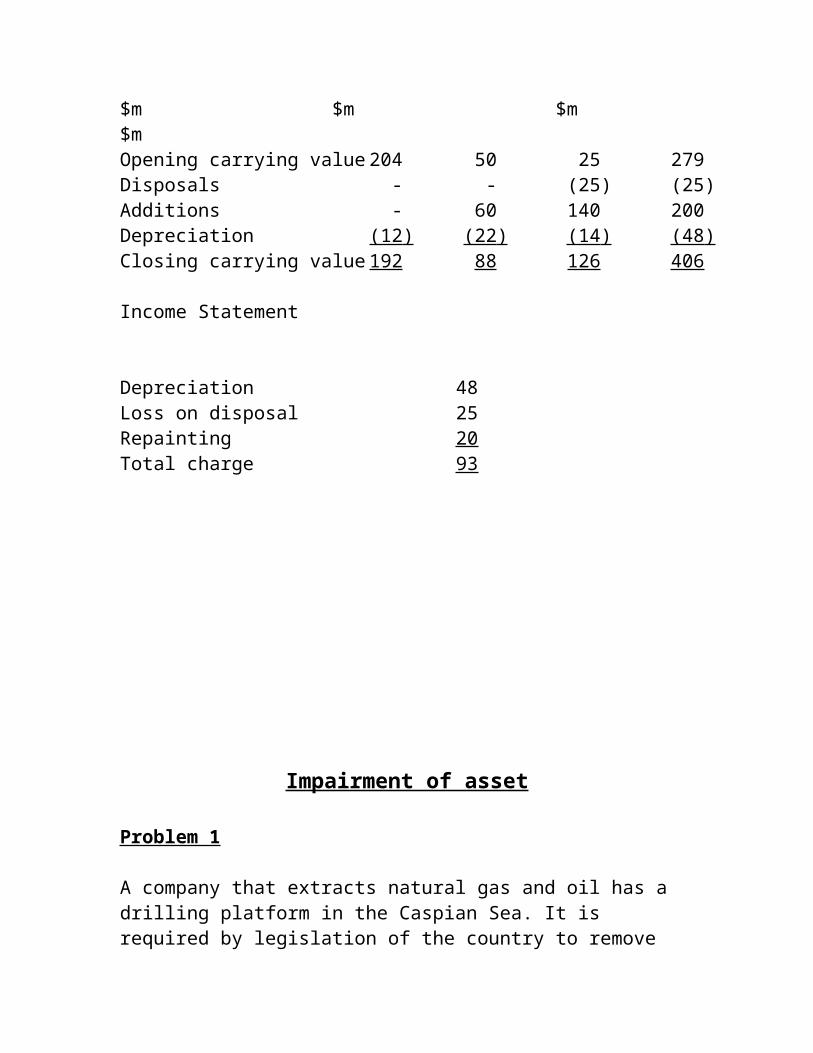

Statement of Financial Position Ship’s Fabric Cabin Propulsion Total $m $m $m $mOpening carrying value 204 50 25 279Disposals - - (25) (25)Additions - 60 140 200Depreciation (12 ) (22 ) (14 ) (48 ) Closing carrying value 192 88 126 406

Income Statement

Depreciation 48Loss on disposal 25Repainting 20Total charge 93

Impairment of asset

Problem 1

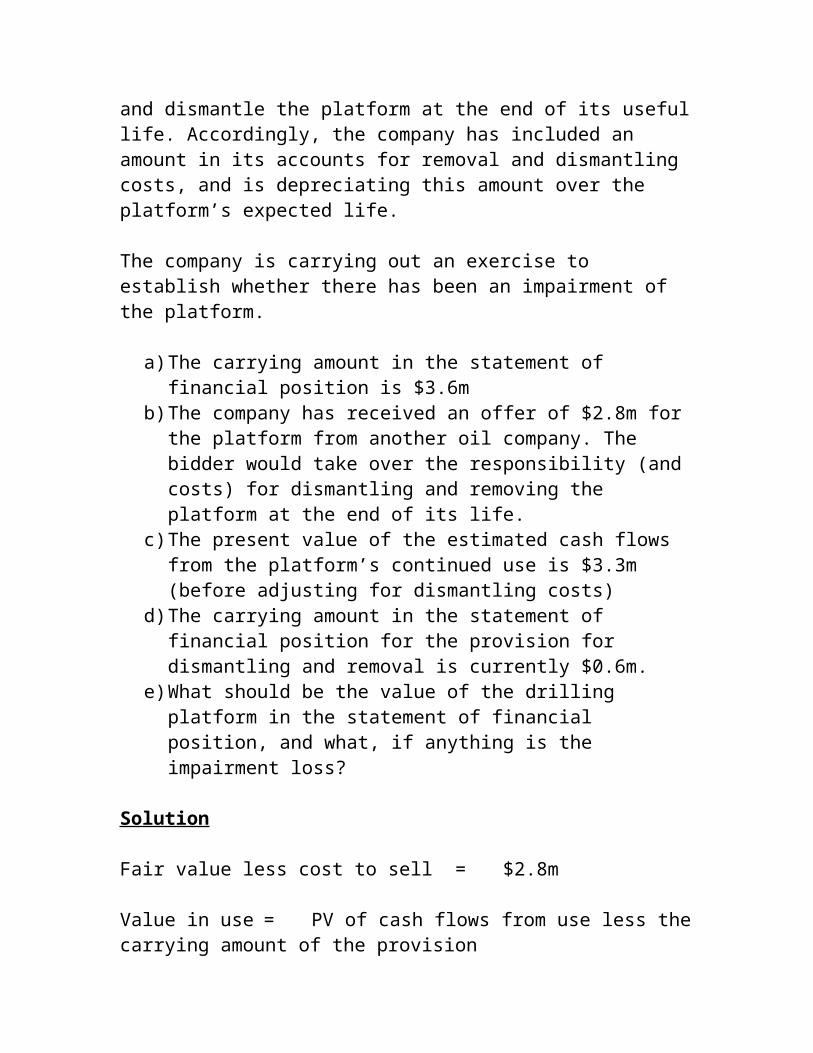

A company that extracts natural gas and oil has a drilling platform in the Caspian Sea. It is required by legislation of the country to remove and dismantle the platform at the end of its useful life. Accordingly, the company has included an amount in its accounts for removal and dismantling costs, and is depreciating this amount over the platform’s expected life.

The company is carrying out an exercise to establish whether there has been an impairment of the platform.

a) The carrying amount in the statement of financial position is $3.6mb) The company has received an offer of $2.8m for the platform from

another oil company. The bidder would take over the responsibility (and costs) for dismantling and removing the platform at the end of its life.

c) The present value of the estimated cash flows from the platform’s continued use is $3.3m (before adjusting for dismantling costs)

d) The carrying amount in the statement of financial position for the provision for dismantling and removal is currently $0.6m.

e) What should be the value of the drilling platform in the statement of financial position, and what, if anything is the impairment loss?

Solution

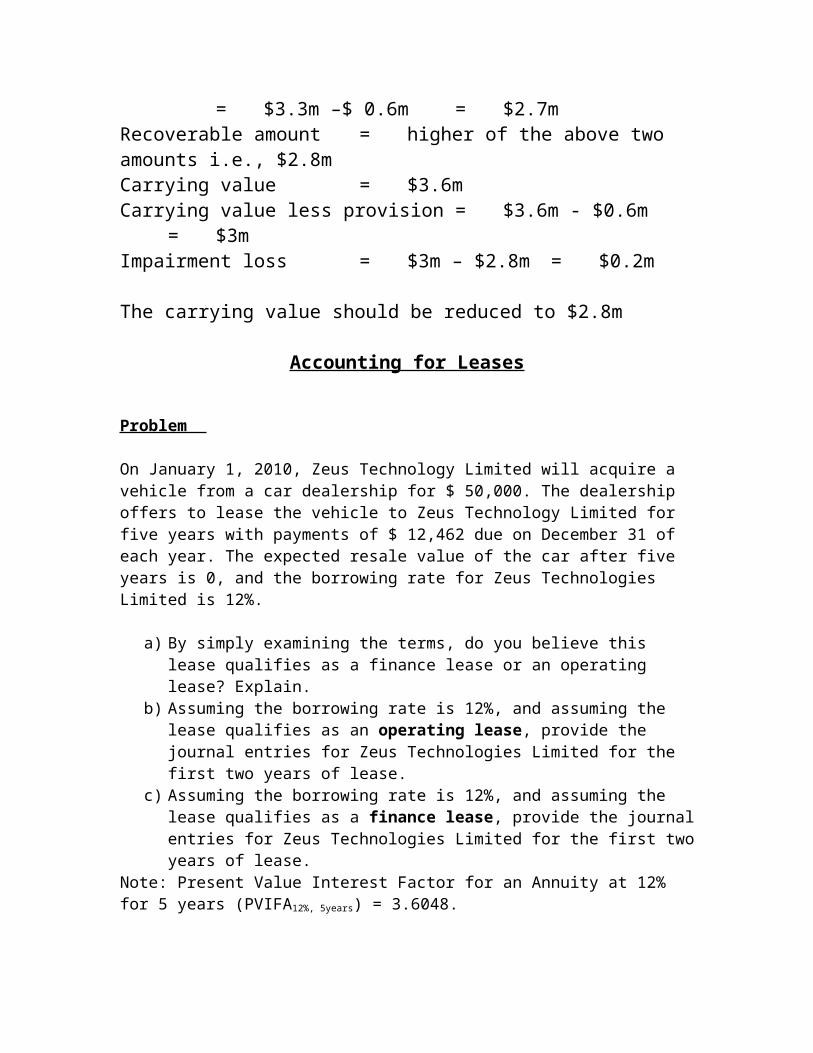

Fair value less cost to sell = $2.8m

Value in use = PV of cash flows from use less the carrying amount of the provision

= $3.3m –$ 0.6m = $2.7mRecoverable amount = higher of the above two amounts i.e., $2.8mCarrying value = $3.6mCarrying value less provision = $3.6m - $0.6m = $3mImpairment loss = $3m – $2.8m = $0.2m

The carrying value should be reduced to $2.8m

Accounting for Leases

Problem

On January 1, 2010, Zeus Technology Limited will acquire a vehicle from a car dealership for $ 50,000. The dealership offers to lease the vehicle to Zeus Technology Limited for five years with payments of $ 12,462 due on December 31 of each year. The expected resale value of the car after five years is 0, and the borrowing rate for Zeus Technologies Limited is 12%.

a) By simply examining the terms, do you believe this lease qualifies as a finance lease or an operating lease? Explain.

b) Assuming the borrowing rate is 12%, and assuming the lease qualifies as an operating lease, provide the journal entries for Zeus Technologies Limited for the first two years of lease.

c) Assuming the borrowing rate is 12%, and assuming the lease qualifies as a finance lease, provide the journal entries for Zeus Technologies Limited for the first two years of lease.

Note: Present Value Interest Factor for an Annuity at 12% for 5 years (PVIFA12%, 5years) = 3.6048.

Solution

(a) Finance lease because” the expected resale value of the car after five years is $0”, which means that the useful life of the car is five years. The company leases the car for the whole of the useful life of the car.

(b) If the lease qualifies as an operating lease, Zeus Technologies will show the lease rent as an expense in the income statement. The entries would be:

1st Year:

Lease rental expenses Dr 12462 To cash 12462

2nd t Year:

Lease rental expenses Dr 12462 To cash 12462

(c) Assuming the lease qualifies as a finance lease, the lessee (Zeus Technologies) should show the lease as an asset and a liability in the balance sheet. The initial value at which the lease is recognised in the balance is the Present value of the future lease payments. The journal entries are shown below:

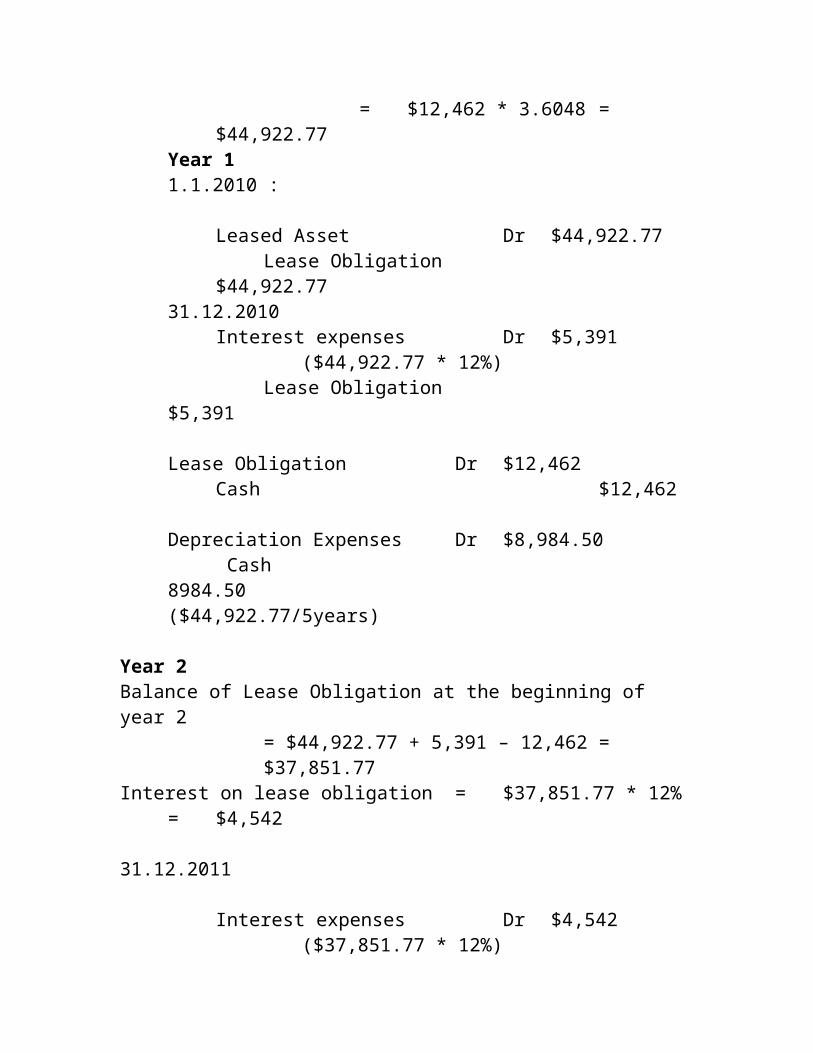

PV of lease payments = $12,462 * PVIFA ( 12%, 5 years)

= $12,462 * 3.6048 = $44,922.77Year 11.1.2010 :

Leased Asset Dr $44,922.77Lease Obligation $44,922.77

31.12.2010Interest expenses Dr $5,391

($44,922.77 * 12%)Lease Obligation $5,391

Lease Obligation Dr $12,462Cash $12,462

Depreciation Expenses Dr $8,984.50 Cash 8984.50

($44,922.77/5years)

Year 2Balance of Lease Obligation at the beginning of year 2

= $44,922.77 + 5,391 – 12,462 = $37,851.77Interest on lease obligation = $37,851.77 * 12% = $4,542

31.12.2011

Interest expenses Dr $4,542 ($37,851.77 * 12%)

Lease Obligation $4,542

Lease Obligation Dr $12,462Cash $12,462

Depreciation Expenses Dr $8,984.50 Cash 8984.50

($44,922.77/5years)

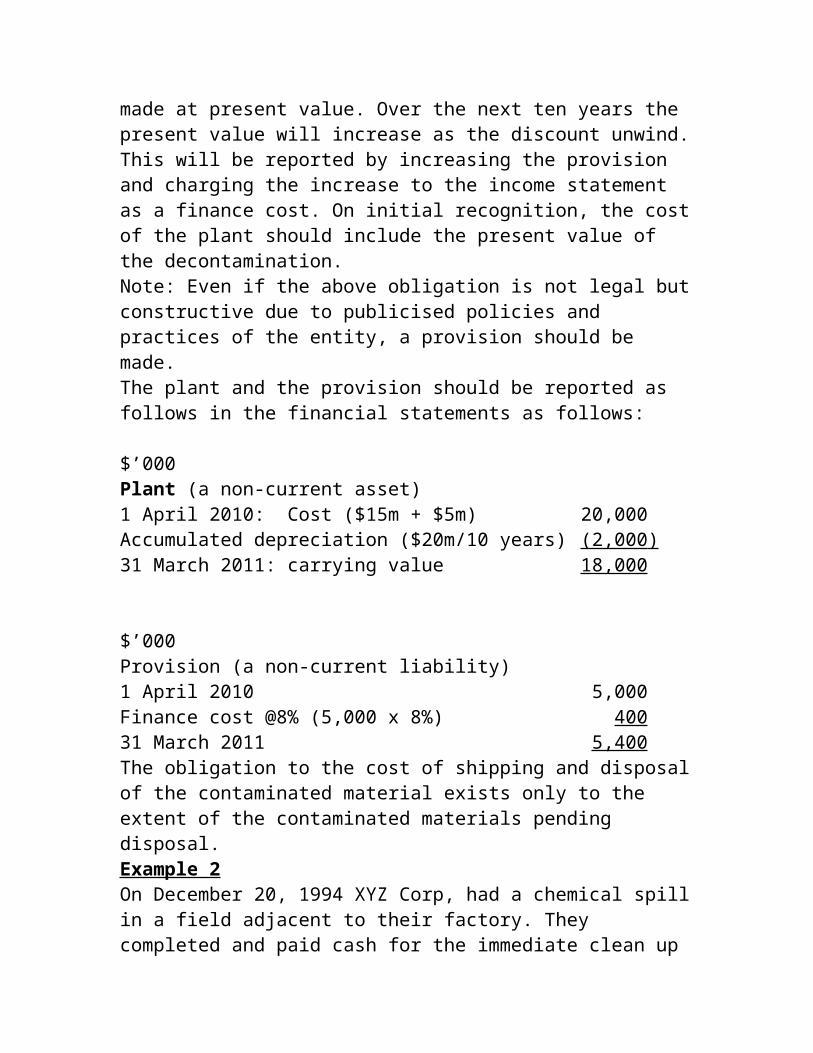

Examples of Recognition of ProvisionExample 1On 1st April 2010 a company brought into use a new processing plant that had cost $15 million to construct and had an estimated life of 10 years. The plant uses hazardous chemicals which are put in containers and shipped abroad for safe disposal after processing. The chemicals have also contaminated the plant itself which occurred as soon as the plant was used. It is a legal requirement that the plant is decontaminated at the end of its life. The estimated present value of this contamination, using a discount rate of 8% per annum, is $5million. Explain how the above item should be treated in the financial statements of the company for the year ended 31 March 2011. AnalysisThe legal obligation to clean up the contamination is a present obligation and existed from the day that the plant was brought into use. This is an obligating event. Therefore provision should be recognized on the balance sheet date. Since time value of money is material, the provision should be made at present value. Over the next ten years the present value will increase as the discount unwind. This will be reported by increasing the provision and charging the increase to the income statement as a finance cost. On initial recognition, the cost of the plant should include the present value of the decontamination. Note: Even if the above obligation is not legal but constructive due to publicised policies and practices of the entity, a provision should be made. The plant and the provision should be reported as follows in the financial statements as follows: $’000Plant (a non-current asset)1 April 2010: Cost ($15m + $5m) 20,000Accumulated depreciation ($20m/10 years) (2,000 ) 31 March 2011: carrying value 18,000

$’000Provision (a non-current liability)1 April 2010 5,000Finance cost @8% (5,000 x 8%) 400

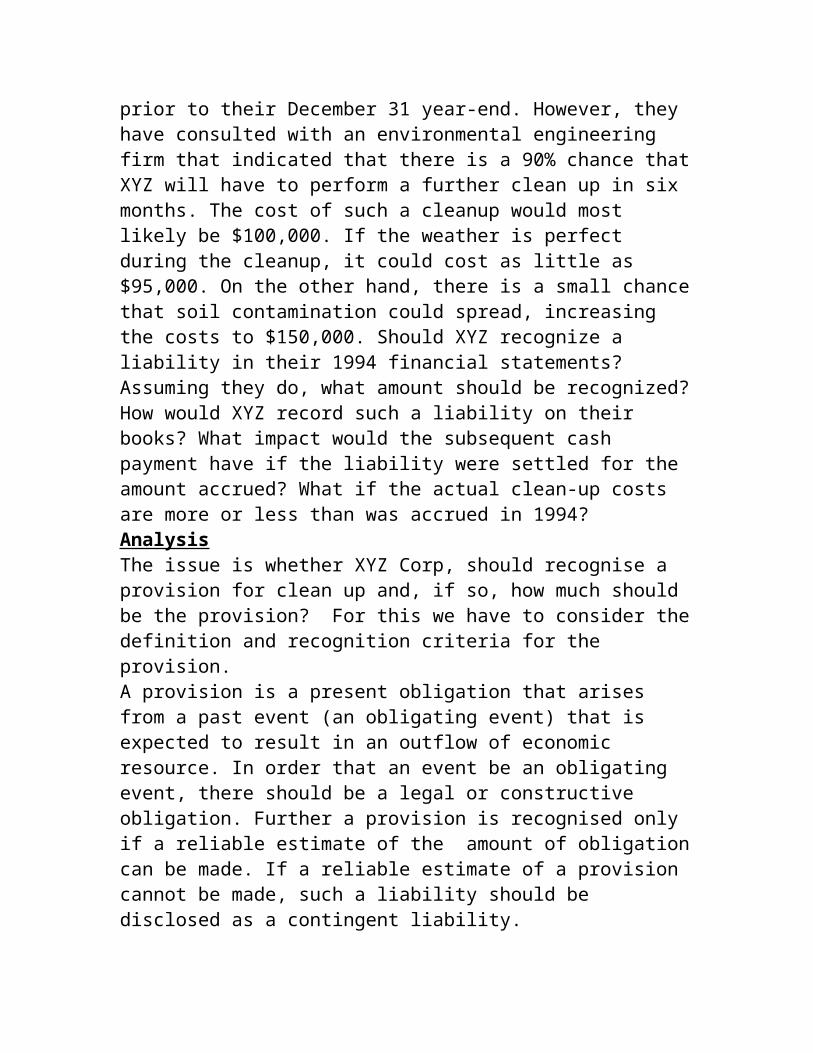

31 March 2011 5,400The obligation to the cost of shipping and disposal of the contaminated material exists only to the extent of the contaminated materials pending disposal. Example 2On December 20, 1994 XYZ Corp, had a chemical spill in a field adjacent to their factory. They completed and paid cash for the immediate clean up prior to their December 31 year-end. However, they have consulted with an environmental engineering firm that indicated that there is a 90% chance that XYZ will have to perform a further clean up in six months. The cost of such a cleanup would most likely be $100,000. If the weather is perfect during the cleanup, it could cost as little as $95,000. On the other hand, there is a small chance that soil contamination could spread, increasing the costs to $150,000. Should XYZ recognize a liability in their 1994 financial statements? Assuming they do, what amount should be recognized? How would XYZ record such a liability on their books? What impact would the subsequent cash payment have if the liability were settled for the amount accrued? What if the actual clean-up costs are more or less than was accrued in 1994?AnalysisThe issue is whether XYZ Corp, should recognise a provision for clean up and, if so, how much should be the provision? For this we have to consider the definition and recognition criteria for the provision.A provision is a present obligation that arises from a past event (an obligating event) that is expected to result in an outflow of economic resource. In order that an event be an obligating event, there should be a legal or constructive obligation. Further a provision is recognised only if a reliable estimate of the amount of obligation can be made. If a reliable estimate of a provision cannot be made, such a liability should be disclosed as a contingent liability. So, the first question to ask would be whether there is a present obligation (legal or constructive) as a result of an obligating event. An obligating event is a past event that leads to a present obligation. Although there is a past event (chemical spill), it seems that it has not yet resulted in a present obligation but there is only a possible obligation (the case states that “there is a 90% chance that XYZ will have to perform a further clean up in six months.”). Since the obligation arising from the chemical spill is only a possible obligation, XYZ Corp, should not recognise the obligation as a provision in its balance sheet but should disclose it as a contingent liability as a note on balance sheet.

Example 3On 1 January 2011, Caltex Corporation acquired a newly constructed oil platform at a cost of $30 million together with the right to extract oil from an offshore oilfield under a government licence. The terms of the licence are that Caltex Corporation will have to remove the platform (which will then have no value) and restore the sea bed to an environmentally satisfactory condition in 10 years’ time when the oil reserves have been exhausted. The estimated cost of this on 31 December 2020 will be $15 million. Ninety per cent of this cost relates to the removal of the oil platform and ten percent relates to the damage caused through extraction of oil. The appropriate discount rate for Caltex Corporation is 10%. [Note: PVIF(10%, 10 years)

= 0.3855]Required:

a) Explain and quantify how the oil platform should be treated in the financial statements of Caltex Corporation for the year ended 31 December 2011

b) Describe how your answer to (a) would change if the government licence did not require an environmental clean up.

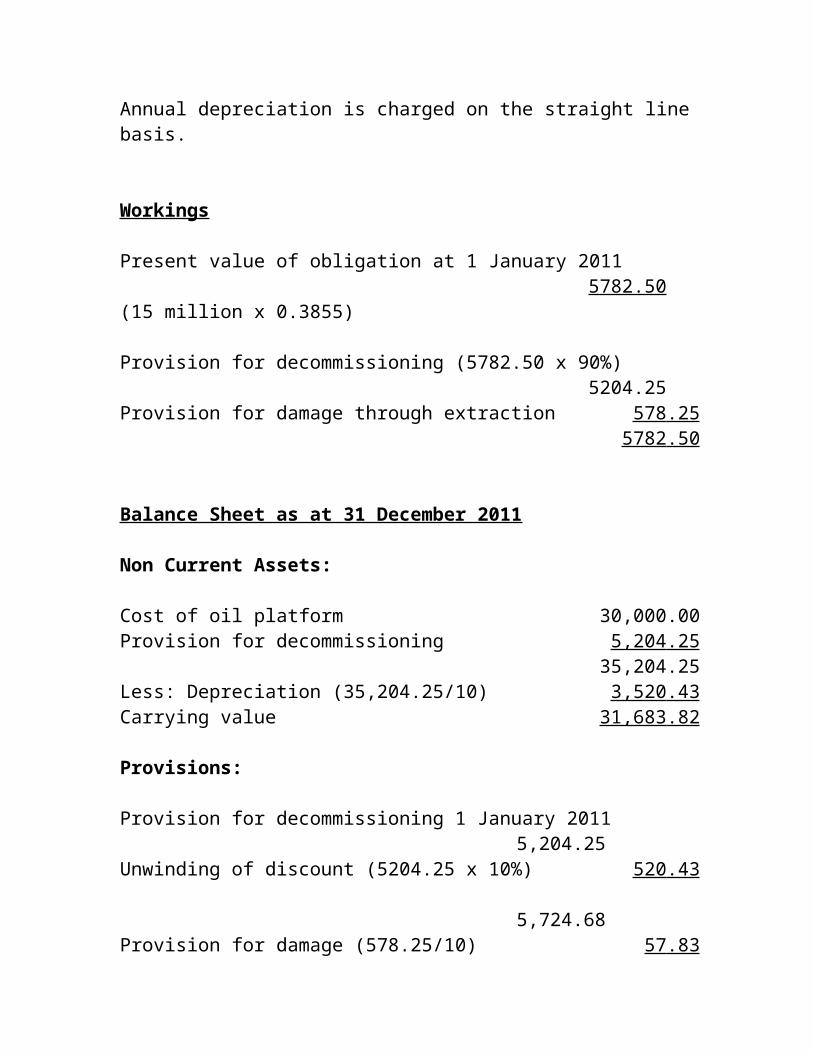

AnalysisPart (a)

Future costs associated with the acquisition/construction and use of non-current assets, such as the environmental costs in this case, should be treated as a liability as soon as they become unavoidable. For Caltex Corporation this would be at the same time as the platform is acquired and brought into use. The provision is for the present value of the expected costs. Ninety percent of this provision relates to cost of removal of the platform, which would be incurred only at the end of tenth year. This part of the provision should be treated as part of the cost of the asset. This part of the provision is also ‘unwound’ by charging a finance cost to the income statement each year and increasing the provision by that finance cost. The remaining ten per cent of the provision relates to the damage caused to the extraction of oil. This part of the provision should not be included in the cost of the asset but is charged to income statement equally as it relates to production and so accrued every year. Annual depreciation is charged on the straight line basis.

Workings

Present value of obligation at 1 January 2011 5782 .50 (15 million x 0.3855)

Provision for decommissioning (5782.50 x 90%) 5204.25Provision for damage through extraction 578 .25

5782 .50

Balance Sheet as at 31 December 2011

Non Current Assets:

Cost of oil platform 30,000.00Provision for decommissioning 5,204 .25

35,204.25Less: Depreciation (35,204.25/10) 3,520 .43 Carrying value 31,683 .82

Provisions:

Provision for decommissioning 1 January 2011 5,204.25Unwinding of discount (5204.25 x 10%) 520 .43

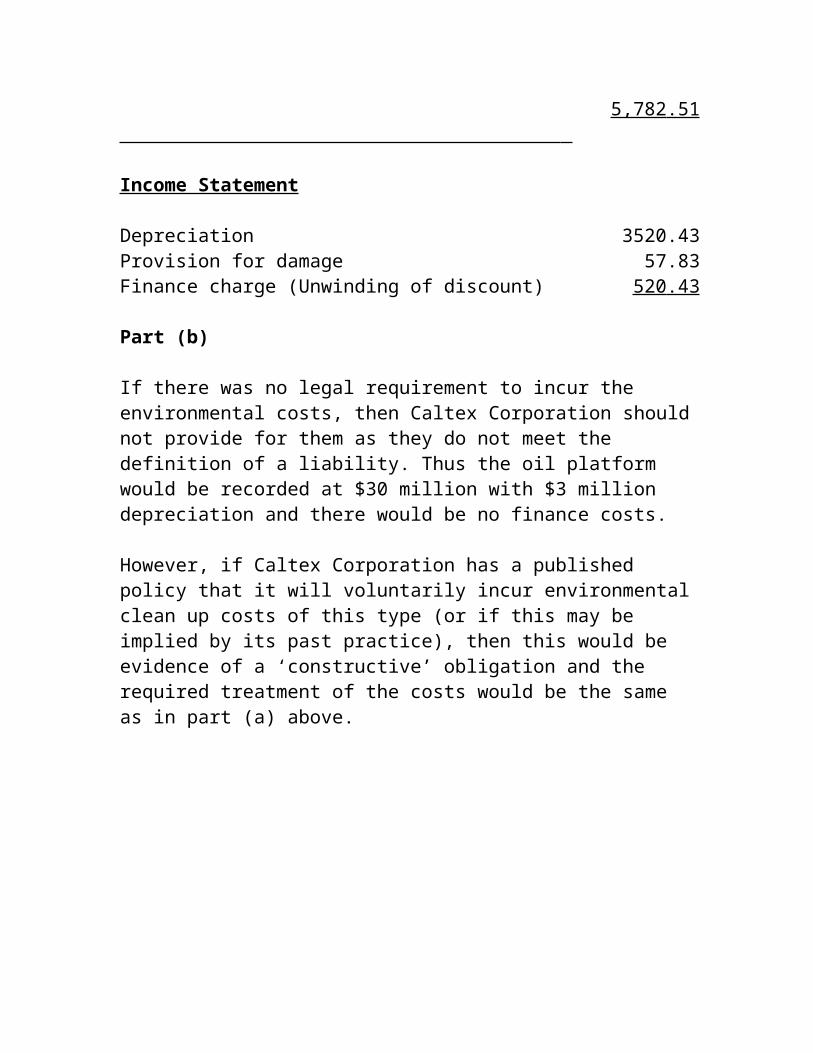

5,724.68Provision for damage (578.25/10) 57 .83

5,782 .51

Income Statement

Depreciation 3520.43Provision for damage 57.83Finance charge (Unwinding of discount) 520 .43

Part (b)

If there was no legal requirement to incur the environmental costs, then Caltex Corporation should not provide for them as they do not meet the definition of a liability. Thus the oil platform would be recorded at $30 million with $3 million depreciation and there would be no finance costs.

However, if Caltex Corporation has a published policy that it will voluntarily incur environmental clean up costs of this type (or if this may be implied by its past practice), then this would be evidence of a ‘constructive’ obligation and the required treatment of the costs would be the same as in part (a) above.

Provision to be made on 31 st December, 1994

A. Cost of only Replacing Chip (no labour):

Three factors to consider:

1. Number Returned2. Cost per unit returned3. Other costs (law suits, defective inventory)

1. Expected Number Returned

Sales – 6 million chips sold (Page 4)

Low end Mid High

6 million 6 million 6 million(Page 4 case) x 5% (Page 5) x ¼ x 1

300,000 1,500,000 6,000,000 Chips Chips Chips

2. Cost Per Unit Returned

$50 - $100 per chip (Page 4 case)

Combine 1 and 2 – Cost of Recall

Low end Mid High

Quantity 300,000 1,500,000 6,000,000Low Price x $50 x $50 x $50

$15,000,000 $75,000,000 $300,000,000High Price x $100 x $100 x $100

$30,000,000 $150,000,000 $600,000,000

3. Other Costs

Defective inventory

Lower of cost and market price rule to be applied

Cost per chip: $50 - $100

Low End:

Nothing, rename and sell at high enough price to cover costs.

High End:

(Page 4 case) 2,000,000X $100

$200,000,000

Lawsuits

Anyone’s guess. Do you really want to disclose a number?

Brand Value

Impact unclear, estimated value $6.4 billion. (Page 5)

Future Sales

Can the current production meet the demand?

No contingency, but need to disclose management discussion and analysis.

B. Cost of Replacing Chip and Direct Labour

1. Number Returned

As determined under assumption A ‘Cost of only Replacing Chip (no labour)’

2. Cost per Unit

$31 - $750, Average $400 per chip (page 4 of case)

Low end Mid High

Quantity 300,000 1,500,000 6,000,000Average x $400 x $400 x $400

$12,000,000 $75,000,000 $300,000,000High x $750 x $750 x $750

$225,000,000 $1,125,000,000 4,500,000,000

Related Documents