Principles of Economics An Intuitive Overview

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Principles of EconomicsAn Intuitive Overview

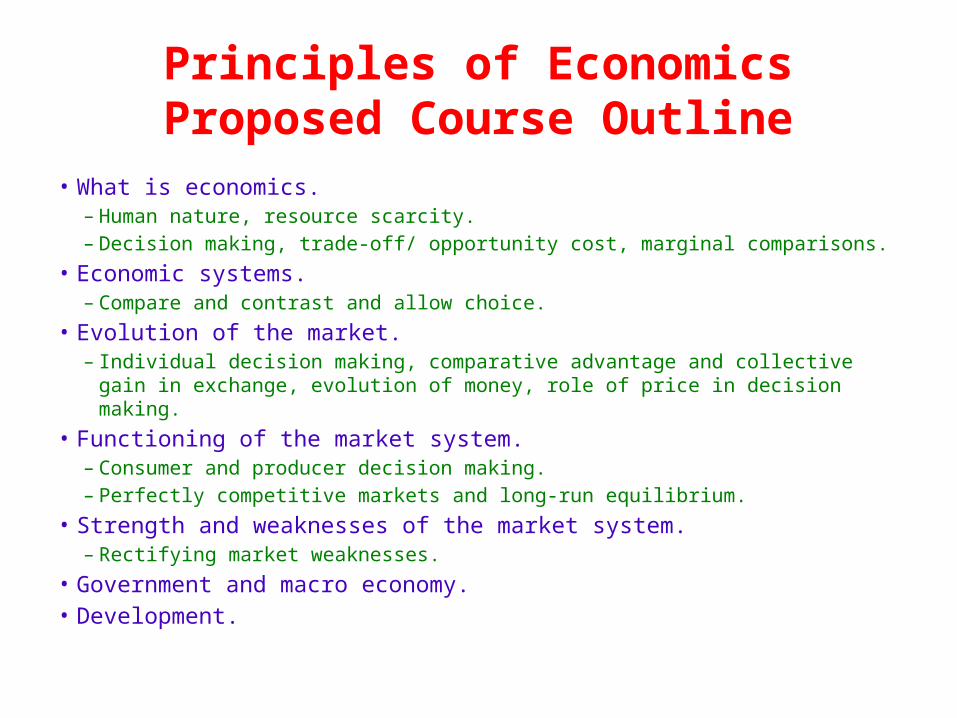

Principles of EconomicsProposed Course Outline

• What is economics.– Human nature, resource scarcity.– Decision making, trade-off/ opportunity cost, marginal comparisons.

• Economic systems.– Compare and contrast and allow choice.

• Evolution of the market.– Individual decision making, comparative advantage and collective gain

in exchange, evolution of money, role of price in decision making.

• Functioning of the market system.– Consumer and producer decision making.– Perfectly competitive markets and long-run equilibrium.

• Strength and weaknesses of the market system.– Rectifying market weaknesses.

• Government and macro economy.• Development.

What is Economics?

What do Economist do?

What do human beings aspire in life?

• Happiness.

What makes us happy?

• Fulfilling our desires.• What are our desires?

– Desires are pleasurable stimulants.– Desires are Physical and Meta-physical.– Physical desires are received by 5 senses:

• Sight, sounds, smell, taste and touch.

– Meta-physical desires are received by6th sense:• Love, respect, intellectual curiosity, spirituality.

• All desires originate in the mind.• Sources of desires are outside of mind.

What is an eternal and universal fact/truth of human aspiration towards happiness?• Happiness can not be absolutely

fulfilled. – Satisfaction is insatiable.

Why can not happiness be absolutely fulfilled?

• Because the physical sources of happiness are limited relative to human nature of in-satiation of desires.

• Limitedness/ scarcity leads to opportunity cost/ trade offs.

If sources of happiness are limited how could we make ourselves happy?

• Making decisions/ choices on what best makes us happy.

What is decision making?

• A cognitive process (could be supported by technology now).– Deciding on an objective/s.– Collecting and processing information in

relation to the objective.– Comparing alternatives.– Selecting the best alternative to achieve

the objective.

Module 2:Causes of Undernutrition: The World Food Problem

What is Economics? Economics is:• a scientific study, • of human/social behavior, • on how decisions are taken, • on the allocation of scarce resources,• for production and consumption, • to satiate insatiable human desires.

Module 2:Causes of Undernutrition: The World Food Problem

Economics is a Science

Economics is a science as it has the following characteristics of science. – Search for truth– Follows the scientific method– Based on evidence of observables– Findings are replicable– Findings could be falsified or strengthened– Findings enables prediction

Module 2:Causes of Undernutrition: The World Food Problem

Economics is a Social Science

• Economics is a social science as the main focus of analysis is human behavior.

• The degree of scientific character of a social science is less than that of a pure science, such as physics or chemistry.

KnowledgeScientific

Non-scientificPhysics, Chemistry,

Zoology, BotanyEconomics, Sociology, Psychology

History, Literature, Myths

Module 2:Causes of Undernutrition: The World Food Problem

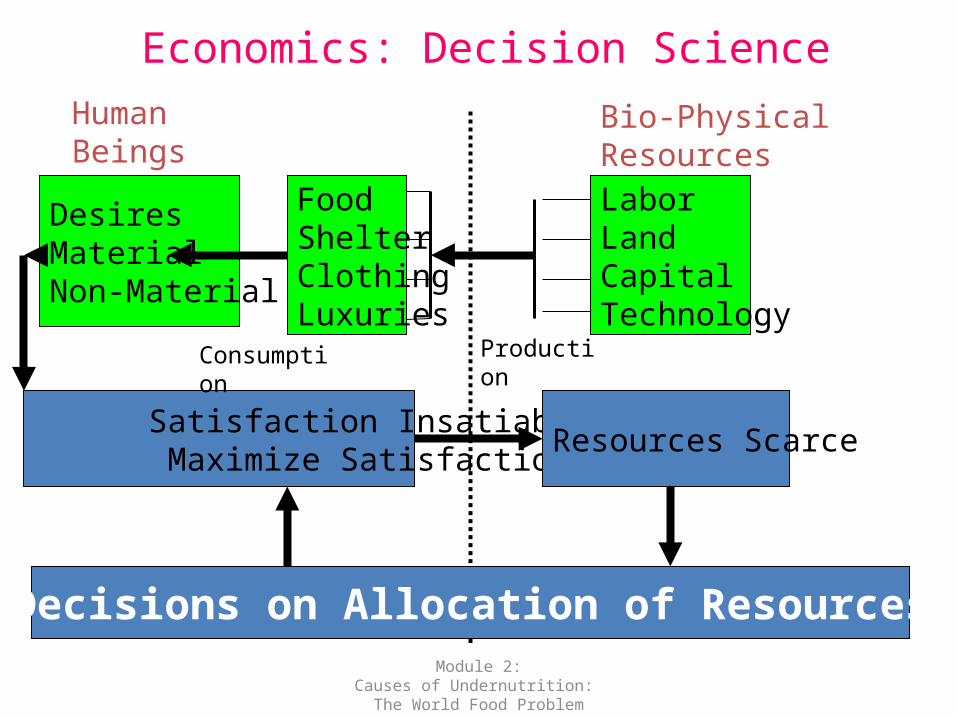

Human Beings Bio-Physical Resources

DesiresMaterialNon-Material

FoodShelterClothingLuxuries

LaborLandCapitalTechnology

Satisfaction Insatiable Maximize Satisfaction

Resources Scarce

Decisions on Allocation of Resources

ProductionConsumption

Economics: Decision Science

What do Economist do?

Facilitate decision Making on resource allocation to best satisfy human beings.

Module 2:Causes of Undernutrition: The World Food Problem

Different Economic Systems

• All economic systems aspire to solve the basic economic problem.

• Market : Property/ resources are owned by individuals and individuals take economic decisions.

• Centrally Planned: Property owned by the state and state takes economic decisions.

• Mixed economies: Mix of market and centrally planned characteristics.

Module 2:Causes of Undernutrition: The World Food Problem

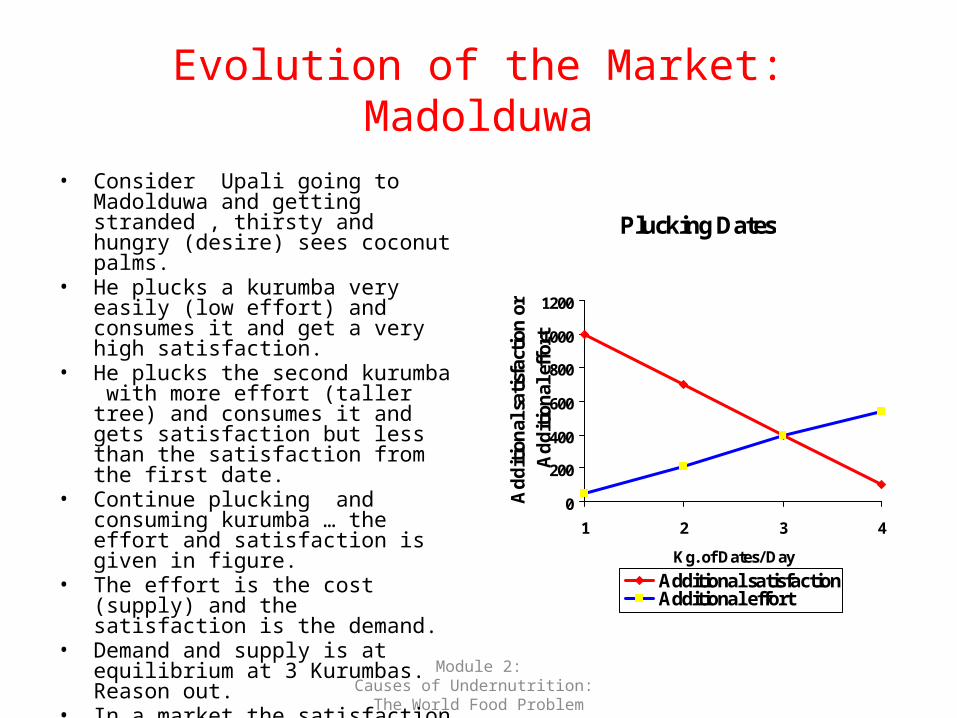

Evolution of the Market: Madolduwa

• Consider Upali going to Madolduwa and getting stranded , thirsty and hungry (desire) sees coconut palms.

• He plucks a kurumba very easily (low effort) and consumes it and get a very high satisfaction.

• He plucks the second kurumba with more effort (taller tree) and consumes it and gets satisfaction but less than the satisfaction from the first date.

• Continue plucking and consuming kurumba … the effort and satisfaction is given in figure.

• The effort is the cost (supply) and the satisfaction is the demand.

• Demand and supply is at equilibrium at 3 Kurumbas. Reason out.

• In a market the satisfaction and cost are quantified monetarily (price).

Plucking Dates

0

200

400

600

800

1000

1200

1 2 3 4

Kg. of Dates/ Day

Ad

dit

ion

al s

atis

fact

ion

or

Ad

dit

ion

al e

ffor

t

Additional satisfactionAdditional effort

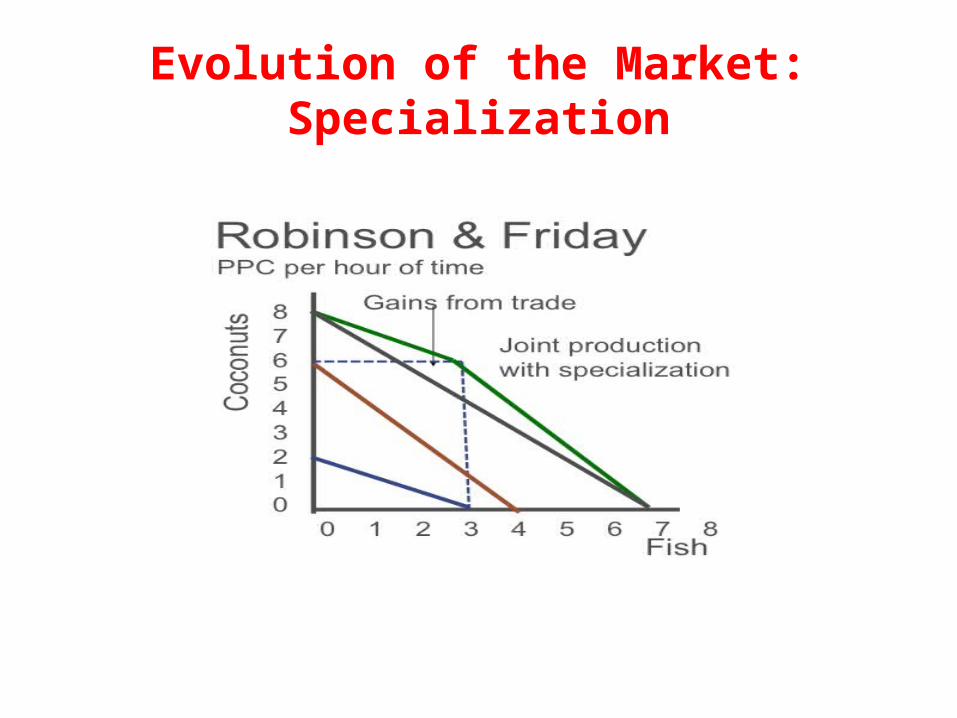

Evolution of the Market: Specialization

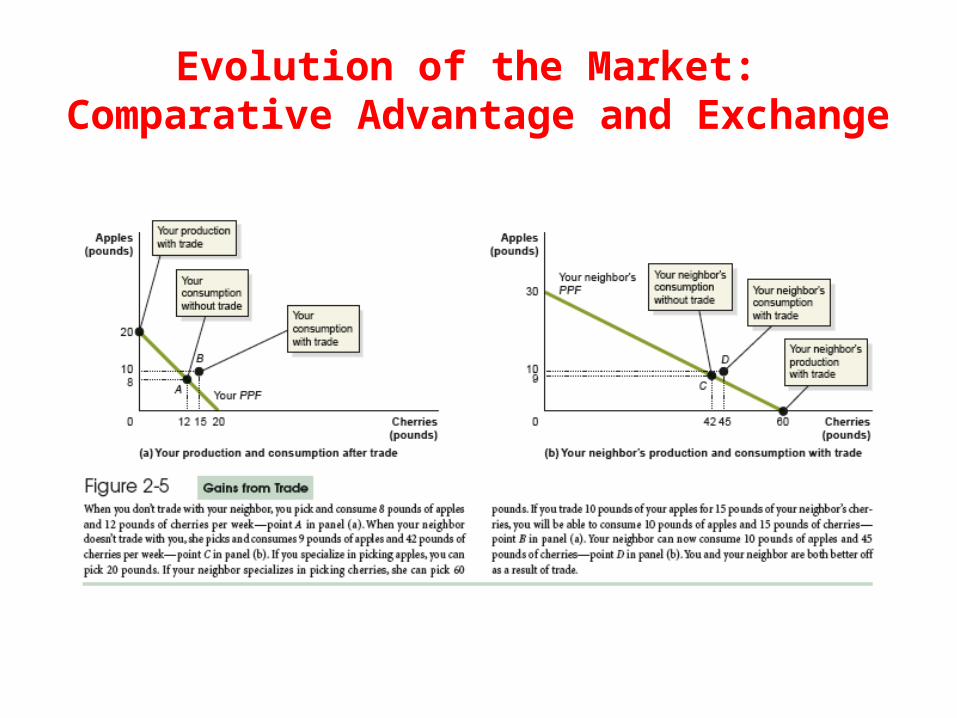

Evolution of the Market: Comparative Advantage and Exchange

Agricultural Finance: Module 2 Money Market

20

Evolution of the Market: Money

• Our ancestors did not use money!• Barter system of exchange.

• Barter system is an inefficient form of exchange due to difficulties in:– Double coincidence wants– Fixing a rate of exchange (every

commodity must have a value in relation to all other commodities).

– Etc,…• Money a socially acceptable medium

of exchange improved efficiency of exchange.

Market Evolution

• Market is an exchange system of wants of producers and consumers.

• Market evolution has been influenced by:– Product specialization– Comparative advantage– Invention of money– Information technology

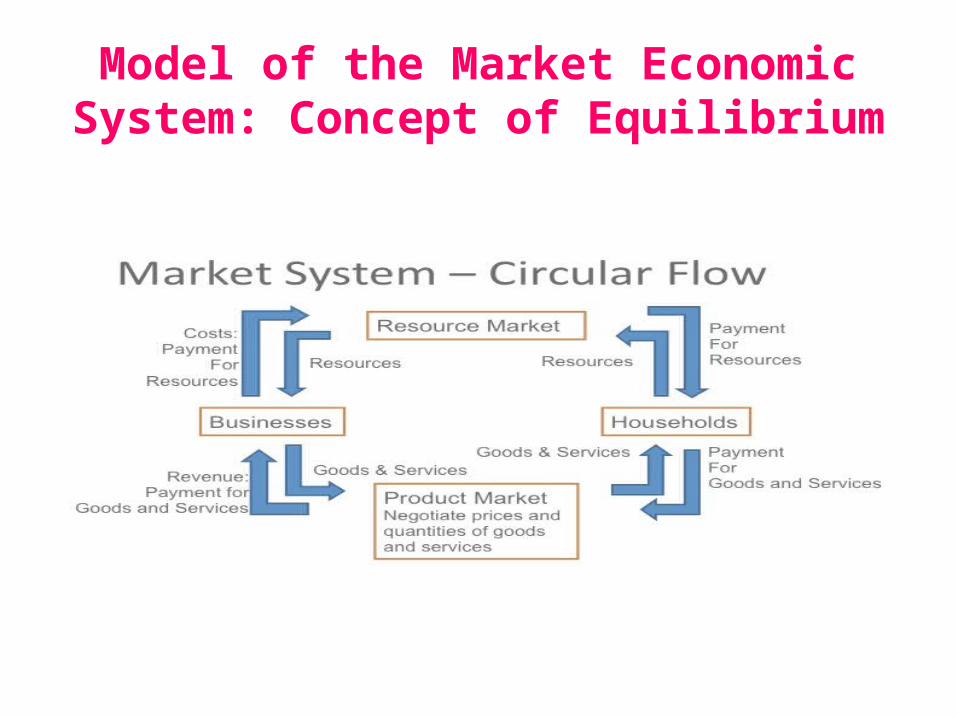

Model of the Market Economic System: Concept of Equilibrium

Module 2:Causes of Undernutrition: The World Food Problem

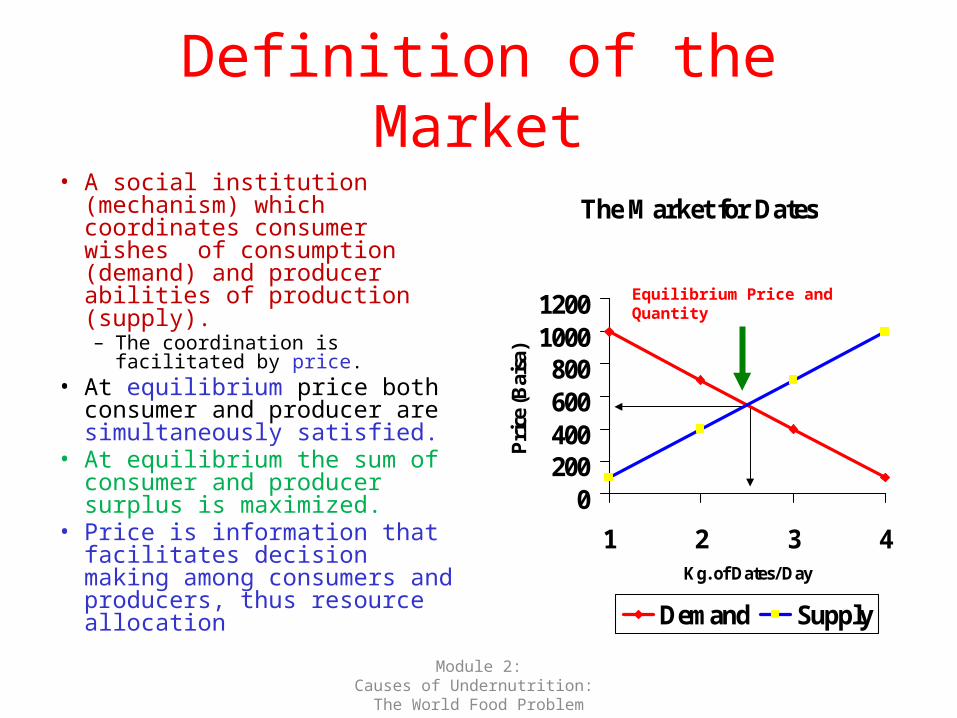

Definition of the Market• A social institution (mechanism)

which coordinates consumer wishes of consumption (demand) and producer abilities of production (supply).– The coordination is facilitated by

price.• At equilibrium price both

consumer and producer are simultaneously satisfied.

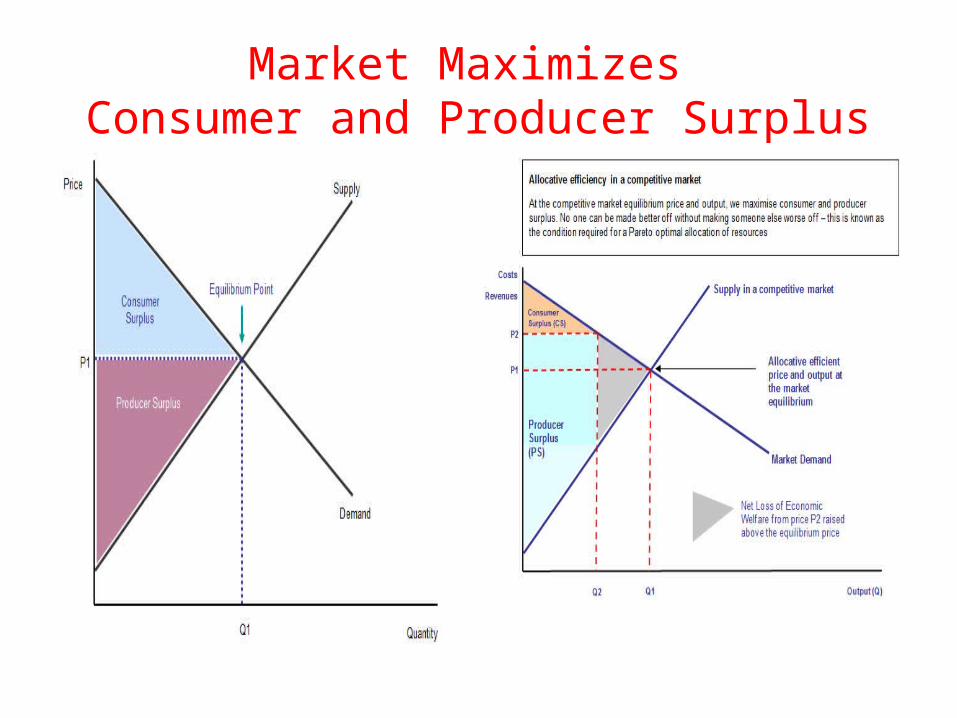

• At equilibrium the sum of consumer and producer surplus is maximized.

• Price is information that facilitates decision making among consumers and producers, thus resource allocation

The Market for Dates

0200400600800

10001200

1 2 3 4Kg. of Dates/ Day

Pri

ce (

Bai

sa)

Demand Supply

Equilibrium Price and Quantity

Market Maximizes Consumer and Producer Surplus

AGEC 2003 1 Module: Introduction 25

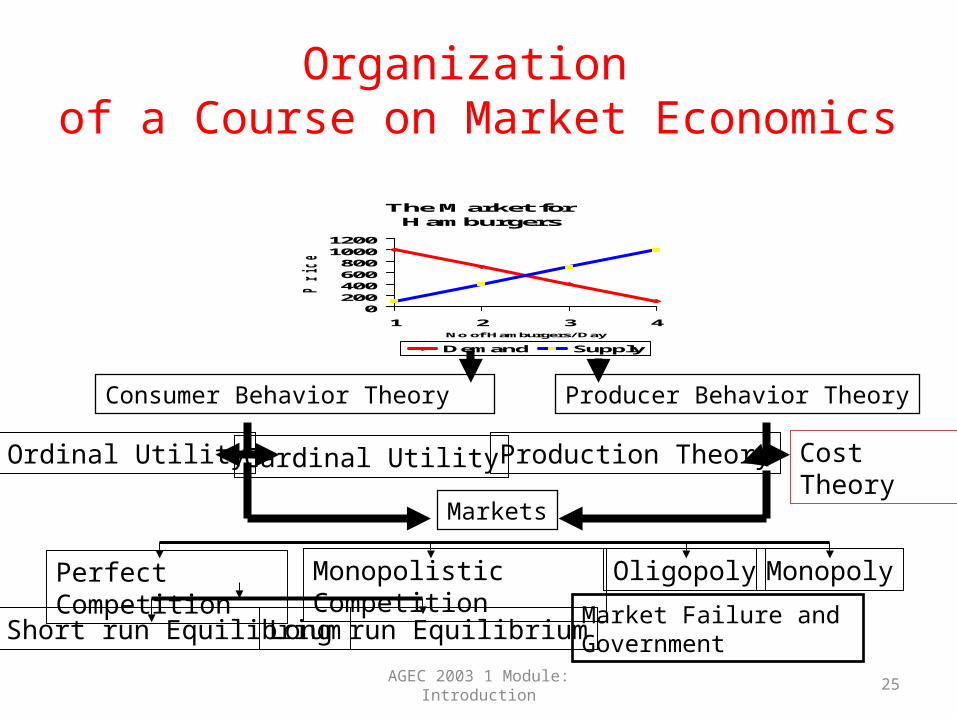

Organization of a Course on Market Economics

The Market for Hamburgers

0200400600800

10001200

1 2 3 4No of Hamburgers/ Day

Price (B

aisa

)

Demand Supply

Consumer Behavior Theory Producer Behavior Theory

Ordinal Utility Cardinal Utility Production Theory Cost Theory

Markets

Perfect Competition Monopolistic Competition Oligopoly Monopoly

Short run Equilibrium Long run Equilibrium Market Failure and Government

AGEC 2003 2 Module Consumer Theory Part 1

26

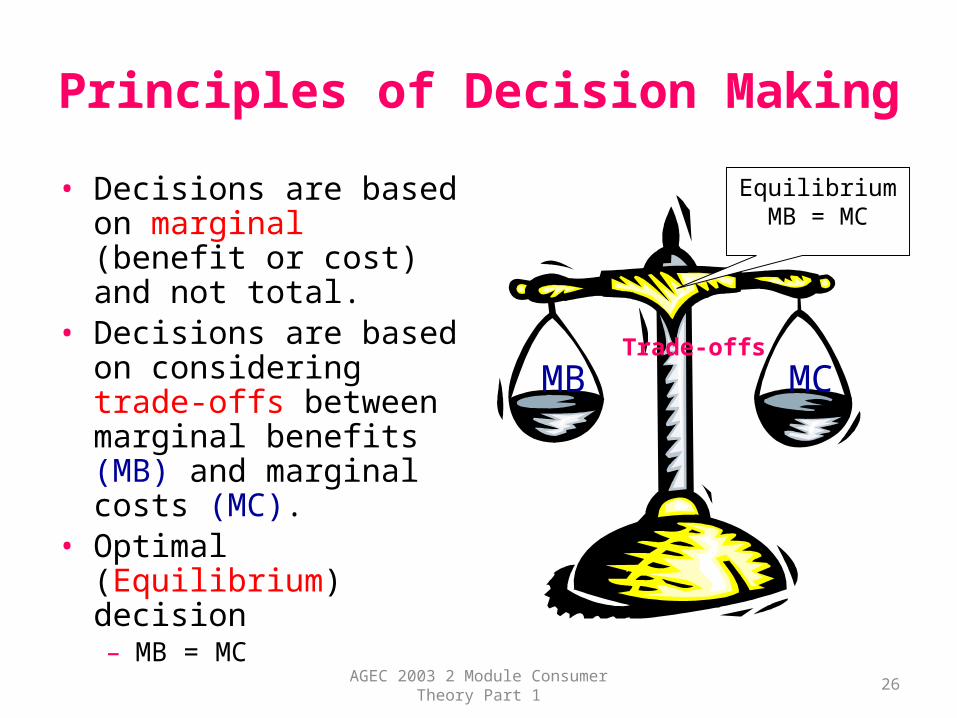

Principles of Decision Making

• Decisions are based on marginal (benefit or cost) and not total.

• Decisions are based on considering trade-offs between marginal benefits (MB) and marginal costs (MC).

• Optimal (Equilibrium) decision – MB = MC

MB MCTrade-offs

EquilibriumMB = MC

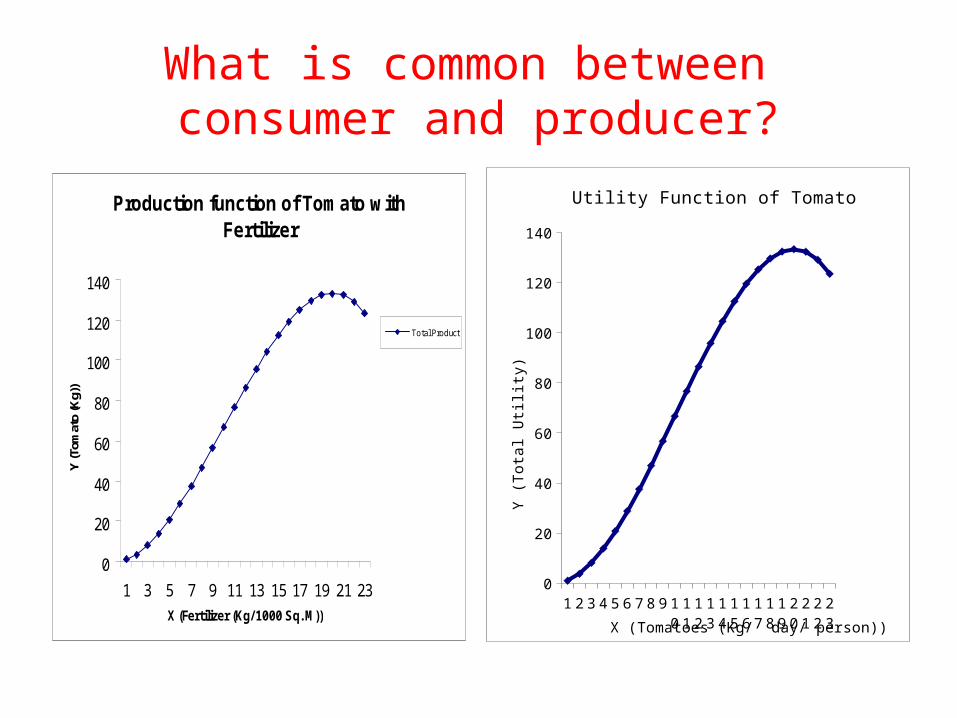

What is common between consumer and producer?

Production function of Tomato with Fertilizer

0

20

40

60

80

100

120

140

1 3 5 7 9 11 13 15 17 19 21 23

X (Fertilizer (Kg/ 1000 Sq. M))

Y (T

omat

o (K

g))

Total Product

1 2 3 4 5 6 7 8 9 10

11

12

13

14

15

16

17

18

19

20

21

22

23

0

20

40

60

80

100

120

140

Utility Function of Tomato

X (Tomatoes (Kg/ day/ person))

Y (

Tot

al U

tility

)

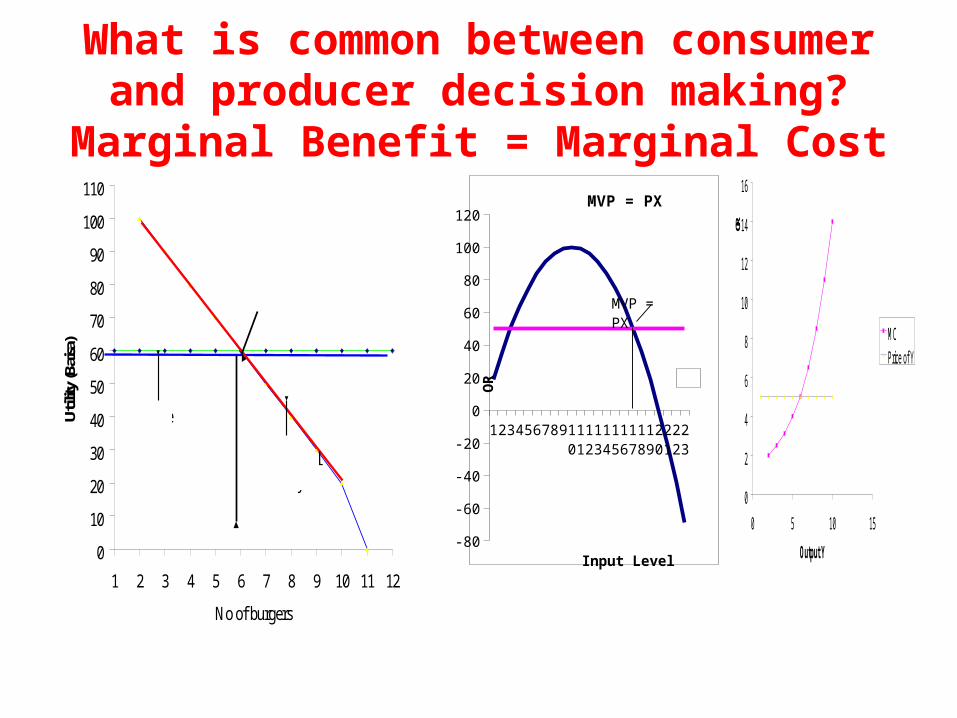

What is common between consumer and producer decision

making?Marginal Benefit = Marginal Cost

0

10

20

30

40

50

60

70

80

90

100

110

1 2 3 4 5 6 7 8 9 10 11 12

No of burgers

Utili

ty (B

aisa

)

Price

MarginalUtility

P = MU

0

2

4

6

8

10

12

14

16

0 5 10 15

Output Y

OR

MCPrice of Y

12345678910

11

12

13

14

15

16

17

18

19

20

21

22

23

-80

-60

-40

-20

0

20

40

60

80

100

120MVP = PX

Input Level

OR

MVP = PX

Mathematics of Economics

• Why mathematics?– Language: ABC

• Solving for Equilibrium– Marginal Benefit = Marginal Cost

EIA Workshop CESAR SQU 13-16 June 2010

30

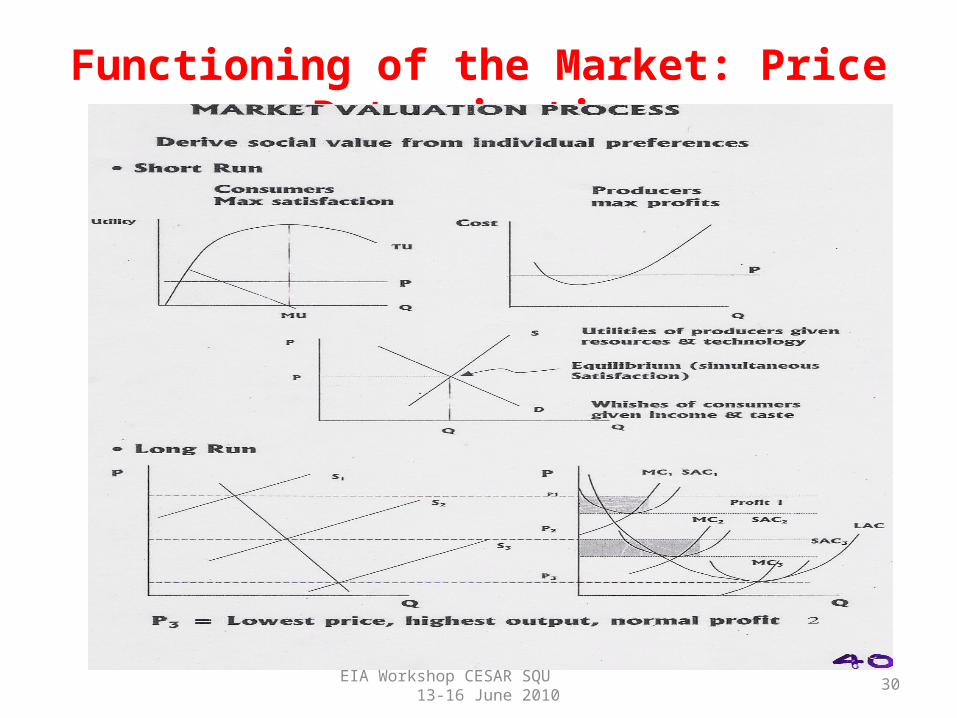

Functioning of the Market: Price Determination

EIA Workshop CESAR SQU 13-16 June 2010

31

MARKET: DECISION MAKING ON RESOURCE USE

• The market would – allocate resources to maximize social welfare (sum of

consumer and producer surpluses),– given individual freedom of choice on production and

consumption and – if property rights are defined and enforced,– And market is perfectly competitive.

• Market assures Pareto efficiency in resource allocation.– Pareto efficient situations are those in which it is impossible

to make one person better off without making someone else worse off.

EIA Workshop CESAR SQU 13-16 June 2010

32

Market Failure In Resource Allocation

• Imperfect markets– Natural monopoly due to economies of scale, etc.

• Lack of property rights– Technological inadequacy of measurement– High transaction costs of monitoring and enforcement.

• Externalities• Public goods• Missing preference

– Intra-generational– Inter-generational

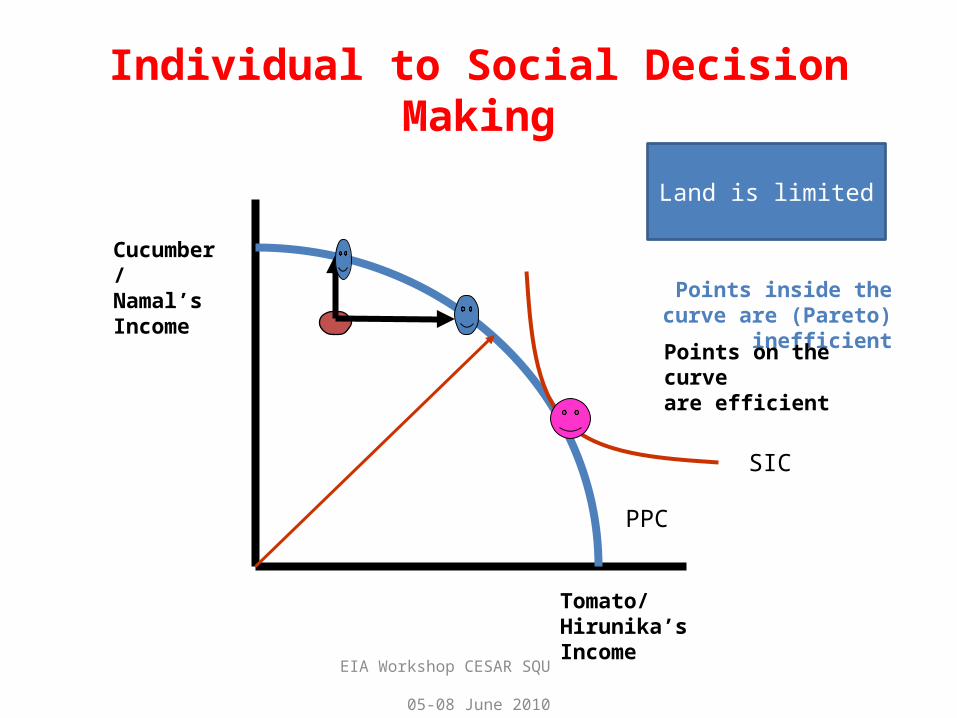

Individual to Social Decision Making

EIA Workshop CESAR SQU 05-08 June 2010

33

Tomato/ Hirunika’s Income

Cucumber/ Namal’s Income Points inside the curve

are (Pareto) inefficient

Points on the curve are efficient

PPC

SIC

Land is limited

EIA Workshop CESAR SQU 13-16 June 2010

34

Social Decision Making

• Decisions on the trade-off efficiency vs. equity.• Economic institutions: Efficiency

– Socialism (Command and Control) and Capitalism (Markets/ Incentives)

• Political institutions: Equity– Dictatorship and Democracy

EIA Workshop CESAR SQU 13-16 June 2010

35

Meaning Of Development

• Maximize social welfare/ satisfaction• 1950: Material development• 1960: Equitable development• 1970: Qualitative development• 1980: Righteous development• 1990: Sustainable development• 2000: Participatory development• 2010: ………………….?

Value of love is when it is shared

Value of knowledge is when it is shared

Related Documents