Principles for the execution of transactions in financial instruments (Best-execution policy) Issue January 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Principles for the execution of transactions in financial instruments (Best-execution policy)Issue January 2018

2

Principles for the execution of transactions in financial instruments (Best-execution policy)

The following principles apply in respect of the execution of orders given to us by clients for the purpose of acquiring or disposing of securities or other financial instruments (e.g. options). In this context, execution means that, on the basis of the client order, we conclude an appropriate transaction with another party via a market suited for that purpose for the account of the client (commission business). Where we and the client directly conclude a purchase contract with regard to financial instruments at a fixed or determinable price (fixed-price business), these principles apply only to a limited extent (cf. Clause 5). They do not apply with regard to the issue of non-stock-exchange-traded shares in invest-ment companies at the issue price, or to the return of such shares at redemption price, via the custody bank concerned.

The following principles also apply where we acquire or dispose of financial instruments for the account of the client in fulfilment of our obligations under an asset management agreement with the client.

Unless you object to these principles within 30 days of re-ceiving them, they will be deemed to have been approved by you.

Should the client require further information regarding our execution strategies, rules and verification proce-dures, we will be happy to provide such information with-in reasonable time.

1. Execution of orders / execution criteria

Client orders can regularly be executed via a variety of chan-nels and a variety of execution centres, for example on a stock exchange, over the counter, via third parties, in the do-mestic market or abroad. We execute client orders via those channels and centres where we can consistently expect the best possible execution in the client’s interest to be effect-ed. In doing so, we take the following execution criteria into account: cost, price, speed, likelihood of execution, size and nature of the order, together with all other aspects relevant to the execution of the order, taking duly into account the type of client, order and financial instrument concerned.

In determining which specific execution centres to use, we as-sume that the private client is primarily interested in achieving the best possible overall price (price of the financial instrument and all costs associated with execution), having due regard to all of the costs directly associated with the transaction. In view of the fact that securities are generally subject to price fluctuations and that price movements to the detriment of the client in the period following the placement of the order cannot therefore be excluded, attention is primarily paid to those execution centres at which complete execution is probable and can be achieved in a timely manner. In the context of the above-mentioned standards, we shall also factor in other relevant criteria (e.g. market situation, reliability of settlement).

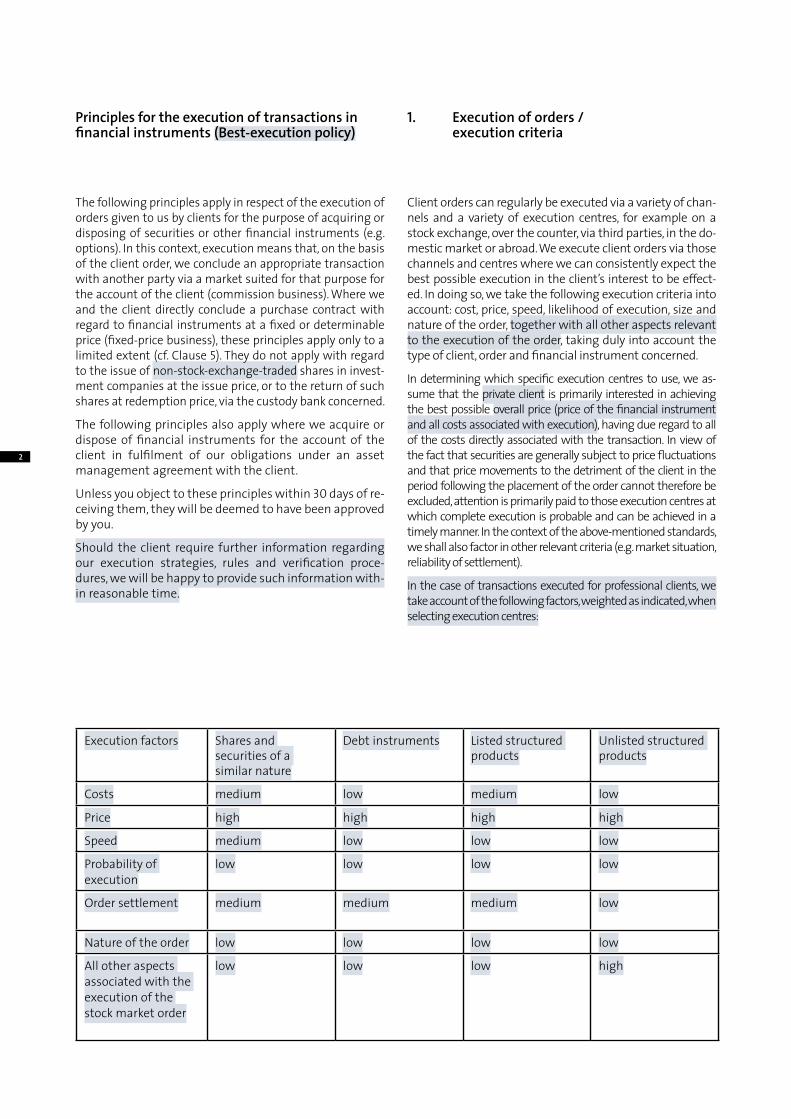

In the case of transactions executed for professional clients, we take account of the following factors, weighted as indicated, when selecting execution centres:

Execution factors Shares and securities of a similar nature

Debt instruments Listed structured products

Unlisted structured products

Costs medium low medium low

Price high high high high

Speed medium low low low

Probability of execution

low low low low

Order settlement medium medium medium low

Nature of the order low low low low

All other aspects associated with the execution of the stock market order

low low low high

3

2. Execution centres

2.1. Selection of execution centres

When it comes to selecting an execution centre, we take into account a) the clearing systems and disaster recov-ery systems in place at such trading centres and b) infor-mation published by the trading centres on a quarterly basis regarding order execution quality relating to the financial instruments traded in the centres concerned. Information provided by the trading centres includes the following:

- Nature, number and average duration of failures during normal trading periods

- Nature, number and average duration of terminated auctions during normal trading periods

- Number of failed transactions

- Value of failed transactions as a percentage of the ag- gregate value of transactions carried out

- Average price and aggregate value of all transactions in individual financial instruments that were carried out within the first two minutes after reference times were determined

- Price of the first transaction carried out where no trans- actions were carried out within two minutes, together with the execution time, transaction size, trading sys- tem, trading mode, trading platform and the best bid and offer prices for the appropriate reference price at the time at which each of these transactions was exe- cuted

- Daily information: simple, average and volume-weighted transaction price together with the highest and lowest prices executed

- Nature and level of cost components, discounts and rebates, non-monetary services, taxes and duties in the execution centre, as well as the nature and level of dif- ferences depending on user, financial instrument and amount

- Number of orders received, number and value of orders carried out, together with cancelled and amended orders, average effective range, average volumes, average range, number of cancellations, number of amendments and average speed of each of the bests bids and offers

- No bid or offer placements longer than 15 minutes

2.2. Execution

Based on the factors listed in Clause 1 regarding the se-lection of execution centres for private clients and pro-fessional clients respectively, and having due regard to the information provided by trading centres relating to the quality of their execution services (Clause 2.1), we ar-rive at the conclusion that client orders should generally be placed and executed in the domestic market. Orders may, alternatively, be executed in other markets, provid-ing equivalent market conditions prevail in the client’s interests – especially with regard to the amount of liquid-ity available and the price that can be attained. An up- to-date list of the execution centres regularly used for executing client orders can be found on our website www.bankalpinum.com.

Modifications to this list are not advised to clients on an individual basis. Up-to-date lists are available from us or from our website.

2.3. Systematic internalisers

We reserve the right to execute client orders via system-atic internalisers , providing, in general terms, this is not disadvantageous to the client in comparison to other ex-ecution channels.

2.4. Limit orders

In order to achieve the speediest possible stock exchange execution, limit orders are forwarded to a multilateral trading system (MTF) or an organised trading system (OTF) or are traded as shown in Clause 2.2, providing no-tification is published with a view to offering limit orders to other market participants.

2.5. Execution of orders outside a trading centre

We regularly carry out client orders at regulated markets, via MTFs, via OTFs and over the counter (OTC). Transac-tions that are carried out over the counter always contain a counterparty risk. This risk can result in a loss for the client – in a worst-case scenario, even a total loss – should the counterparty not be in a position to fulfil its contrac-tual obligations.

1) Systematic internaliser = a separate financial services company which, on an organised, regular and systematic basis, deals on its own ac-count by executing client orders outside a regulated market or MTF.2) Multilateral trading system = a multilateral system which brings together the interests of multiple third parties in the purchase and disposal of financial instruments within the system in accordance with non-discretionary rules in a manner that results in a contract.3) Multilateral system which is not a regulated market or MTF and which brings together the interests of multiple third parties in the pur-chase and disposal of bonds, structured financial products, emission certificates or derivatives within the system in a manner that results in a contract.

4

3. Orders exceptionally executed in a manner that does not conform to these principles

3.1. Client’s execution instructions

The client may instruct us on how their order is to be ex-ecuted. Where such instruction is provided, it shall take precedence over the execution principles listed here. We shall, therefore, execute the order in line with the client’s specific instructions, thereby ignoring these principles regarding best possible execution in the light of such instructions. A client instruction releases the Bank from having to take such measures as it has determined and implemented within the framework of its execution prin-ciples, in order that it may achieve the best possible result when executing the orders in line with the elements stip-ulated within the instruction concerned.

3.2. Special market situation

Exceptional market conditions or market disruptions can make it necessary for us to depart from the principles list-ed here; in such an event we shall act in the interests of the client to the best of our knowledge and belief.

3.3. Departure from principles in order to achieve better execution for the client in individual cases

We may depart from the immediate execution of a client order where, in an individual case, this results in better terms (order handling in a manner that does not disrupt the market).

3.4. Consolidation

It frequently happens that several clients wish to buy or sell the same security on the same day. The key principle to follow is that clients/client orders should be treated in a fair and equal manner and that client interests come first. In reality, this results in orders being executed in the order in which they are received. However, where it is not disadvantageous in general to the client for orders to be consolidated, we reserve the right to execute several or-ders together. Consolidation can be either advantageous or disadvantageous for a particular order.

4. Weiterleitung von Aufträgen In bestimmten Fällen werden wir den Auftrag des Kunden nicht selbst ausführen, sondern ihn an ein anderes Finan-zdienstleistungsunternehmen zur Ausführung weiter-leiten. Der Auftrag des Kunden wird dann nach Massgabe der Vorkehrungen des anderen Finanzdienstleis

5. Fixed-price transactions In the case of fixed-price transactions we do not execute client orders in line with the principles listed above. The contractual agreement obliges us, in return for payment of the agreed fixed sum, simply to deliver to the client the financial instruments ordered and to procure ownership thereof for the client. The same applies where we, in con-nection with a public or private issue, offer securities for subscription or where we conclude with the client con-tracts for financial instruments (e.g. option transactions) which are not tradable on a stock exchange.

The circumstances in which fixed-price transactions are regularly offered can be gleaned from the list of execu-tion centres. Prior to concluding a fixed-price transaction with the client, we check the appropriateness of the pric-es offered to the client by referring to market data and by comparing the prices offered for similar or comparable products.

6. Regular reviewsWe shall regularly (at least once a year) review the exe-cution policy based on this set of principles to check that it continues to represent the best possible policy for exe-cuting client orders. Should it emerge during the course of such a review that these principles are in need of ad-justment, we shall implement such adjustments accord-ingly. Should the adjustments be of a significant nature, we shall advise our clients accordingly.

5

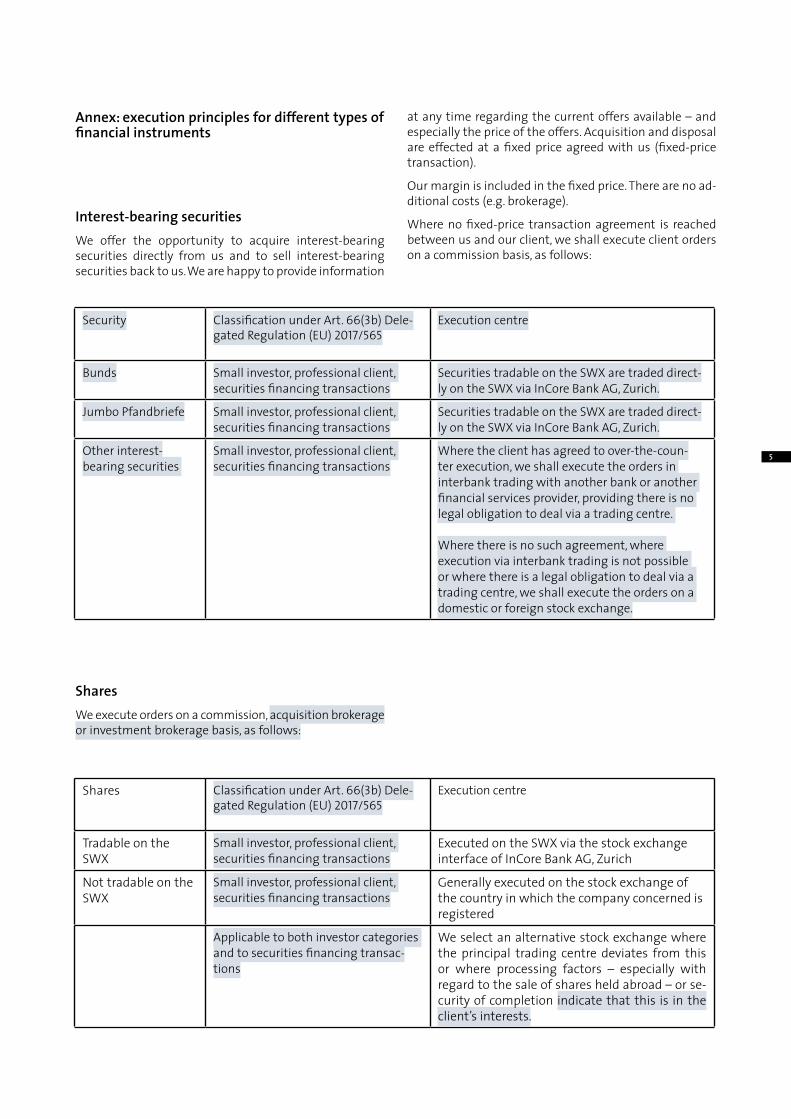

Security Classification under Art. 66(3b) Dele-gated Regulation (EU) 2017/565

Execution centre

Bunds Small investor, professional client, securities financing transactions

Securities tradable on the SWX are traded direct-ly on the SWX via InCore Bank AG, Zurich.

Jumbo Pfandbriefe Small investor, professional client, securities financing transactions

Securities tradable on the SWX are traded direct-ly on the SWX via InCore Bank AG, Zurich.

Other interest- bearing securities

Small investor, professional client, securities financing transactions

Where the client has agreed to over-the-coun-ter execution, we shall execute the orders in interbank trading with another bank or another financial services provider, providing there is no legal obligation to deal via a trading centre.

Where there is no such agreement, where execution via interbank trading is not possible or where there is a legal obligation to deal via a trading centre, we shall execute the orders on a domestic or foreign stock exchange.

Shares Classification under Art. 66(3b) Dele-gated Regulation (EU) 2017/565

Execution centre

Tradable on the SWX

Small investor, professional client, securities financing transactions

Executed on the SWX via the stock exchange interface of InCore Bank AG, Zurich

Not tradable on the SWX

Small investor, professional client, securities financing transactions

Generally executed on the stock exchange of the country in which the company concerned is registered

Applicable to both investor categories and to securities financing transac-tions

We select an alternative stock exchange where the principal trading centre deviates from this or where processing factors – especially with regard to the sale of shares held abroad – or se-curity of completion indicate that this is in the client’s interests.

Annex: execution principles for different types of financial instruments

Interest-bearing securities We offer the opportunity to acquire interest-bearing securities directly from us and to sell interest-bearing securities back to us. We are happy to provide information

at any time regarding the current offers available – and especially the price of the offers. Acquisition and disposal are effected at a fixed price agreed with us (fixed-price transaction).

Our margin is included in the fixed price. There are no ad-ditional costs (e.g. brokerage).

Where no fixed-price transaction agreement is reached between us and our client, we shall execute client orders on a commission basis, as follows:

Shares

We execute orders on a commission, acquisition brokerage or investment brokerage basis, as follows:

6

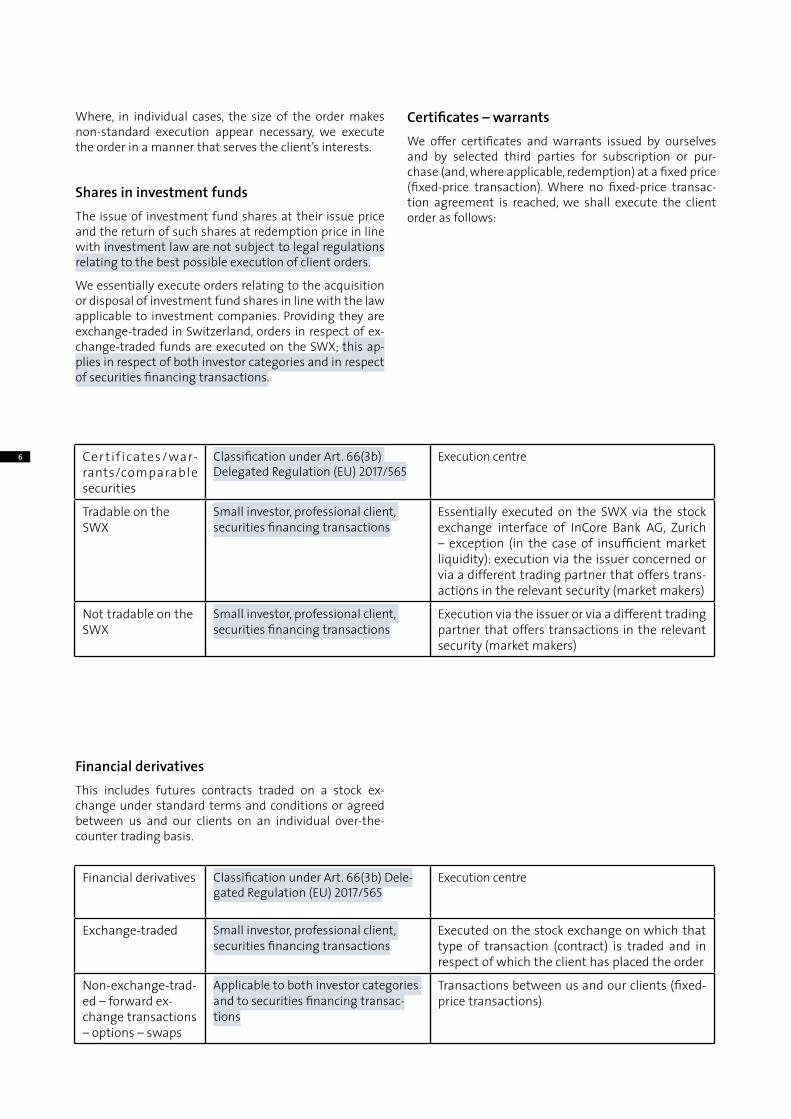

Where, in individual cases, the size of the order makes non-standard execution appear necessary, we execute the order in a manner that serves the client’s interests.

Shares in investment fundsThe issue of investment fund shares at their issue price and the return of such shares at redemption price in line with investment law are not subject to legal regulations relating to the best possible execution of client orders.

We essentially execute orders relating to the acquisition or disposal of investment fund shares in line with the law applicable to investment companies. Providing they are exchange-traded in Switzerland, orders in respect of ex-change-traded funds are executed on the SWX; this ap-plies in respect of both investor categories and in respect of securities financing transactions.

Certificates – warrants We offer certificates and warrants issued by ourselves and by selected third parties for subscription or pur-chase (and, where applicable, redemption) at a fixed price (fixed-price transaction). Where no fixed-price transac-tion agreement is reached, we shall execute the client order as follows:

Financial derivatives This includes futures contracts traded on a stock ex-change under standard terms and conditions or agreed between us and our clients on an individual over-the-counter trading basis.

Cer t if icates/war-rants/comparable securities

Classification under Art. 66(3b) Delegated Regulation (EU) 2017/565

Execution centre

Tradable on the SWX

Small investor, professional client, securities financing transactions

Essentially executed on the SWX via the stock exchange interface of InCore Bank AG, Zurich – exception (in the case of insufficient market liquidity): execution via the issuer concerned or via a different trading partner that offers trans-actions in the relevant security (market makers)

Not tradable on the SWX

Small investor, professional client, securities financing transactions

Execution via the issuer or via a different trading partner that offers transactions in the relevant security (market makers)

Financial derivatives Classification under Art. 66(3b) Dele-gated Regulation (EU) 2017/565

Execution centre

Exchange-traded Small investor, professional client, securities financing transactions

Executed on the stock exchange on which that type of transaction (contract) is traded and in respect of which the client has placed the order

Non-exchange-trad-ed – forward ex-change transactions – options – swaps

Applicable to both investor categories and to securities financing transac-tions

Transactions between us and our clients (fixed-price transactions)

7

Links to trading centre information (cf. also Clause 2.1)

The Bank will publish details on its website (www.bankalpinum.com) regarding the quality of execution at the named electronic execution centres as soon as such information is made available by the execution centres concerned.

List of execution centresA list of the most important execution centres considered by Bank Alpinum AG in connection with the best possible execution of client orders can be found on our website: www.bankalpinum.com. The list is not exhaustive and is continuously updated.

Bank Alpinum AGAustrasse 59 · P.O. Box 15289490 Vaduz · Principality of LiechtensteinTelephone +423 239 62 11 · Fax +423 239 62 [email protected] · www.bankalpinum.com

www.bankalpinum.com

Related Documents