©2011 Langdon & Langdon Financial Services, LLC 1-1 Primer on Income Tax Planning “Taxes are what we pay for a civilized society.” - Justice Oliver Wendell Holmes “There is no such thing as a good tax.” - Sir Winston Churchill 1-2 1-3

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2011 Langdon & Langdon Financial Services, LLC

1-1

Primer on Income Tax Planning

“Taxes are what we pay for a civilized society.”

- Justice Oliver Wendell Holmes

“There is no such thing as a good tax.”

- Sir Winston Churchill

1-2

1-3

©2011 Langdon & Langdon Financial Services, LLC

1-2

Income tax rates beginning at one percent and rising to seven percent for taxpayers with income in excess of $500,000. Less than one percent of the population was subject to the income tax.

The Sales Pitch: Tax the Rich

The Revenue Act of 1913

1-4

Today:

“I want to provide a tax cut for 95% of Americans. If you make less than a quarter of a million dollars a year, you will not see a

single dime of your taxes go up. If you make $200,000 a year or

less, your taxes will go down..”

- Barack Obama, 2008 Presidential Campaign

Have Things Changed ?

1-5

1-6

©2011 Langdon & Langdon Financial Services, LLC

1-3

©2010 Langdon & Langdon Financial Services, LLC. 1-7

Functions of the Income Tax System

Produce Revenue

Management of the Economy effectuate fiscal policy

encourage desired behavior

Social Function redistribution of wealth

Regulatory Function discourage undesirable activities

©2010 Langdon & Langdon Financial Services, LLC. 1-8

Adam Smith’s Criteria for Evaluating Tax Systems

Equality

Convenience

Certainty

Economy

©2010 Langdon & Langdon Financial Services, LLC. 1-9

Tax Structure

Tax Base: amount to which tax rate is applied

Tax Rate: applied to Tax Base to determine tax liability Proportional

Progressive

Regressive

Incidence of Tax: degree to which total tax burden is shared by taxpayers

©2011 Langdon & Langdon Financial Services, LLC

1-4

©2010 Langdon & Langdon Financial Services, LLC. 1-10

Tax Structure

Examples:

Income $10 $20 $30

Proportional Tax $3 (.3) $6 (.3) $9 (.3)

Progressive Tax $3 (.3) $7 (.35) $12 (.4)

Regressive Tax $3 (.3) $5 (.25) $6 (.2)

©2010 Langdon & Langdon Financial Services, LLC. 1-11

Types of Taxes

Transaction (usually state tax)

Estate & Gift

Generation Skipping Transfer

Property (ad valorem)

Income

Employment

Other

Estate Planning

Income Tax

©2010 Langdon & Langdon Financial Services, LLC. 1-12

U.S. Federal Tax System

3 Separate Tax Systems

Income Tax Estate & Gift

Tax

Generation- Skipping Transfer

Tax

©2011 Langdon & Langdon Financial Services, LLC

1-5

Taxable Income Income

Active Portfolio Passive

Wages, Salaries, &

Active Business

Income

Interest,

Dividends,

Capital Gains

Partnerships,

Real Estate

1-13 ©2010 Langdon & Langdon Financial Services, LLC.

3 Essential Tax Principles

Doctrine of Constructive Receipt

Economic Benefit Doctrine

Doctrine of the Fruit & The Tree

1-14 ©2010 Langdon & Langdon Financial Services, LLC.

3-15 ©2008 Langdon & Langdon Financial Services, LLC.

Federal Income Tax Formula

Income (broadly conceived)

Less: Exclusions

Gross income

Less: Deductions for AGI (Above-the line deductions) Adjusted Gross Income (“The Line”)

Less: Itemized or Standard deduction (Below-the line deductions)

Less: Personal and Dependency Exemptions

Taxable Income

Tax on taxable income

Less: Tax credits Tax due (or refund)

1-15 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-6

©2010 Langdon & Langdon Financial Services, LLC. 1-16

Employment Taxes

FICA taxes Paid by both employee and employer

In 2014, Social Security rate is 6.2% on a max of $117,000 of wages.

Medicare rate is 1.45% with no cap

Self-employment tax Rate is 15.3%, base is net self-employment income, and

deduction (FOR AGI) is allowed for 1/2 of self-employment tax

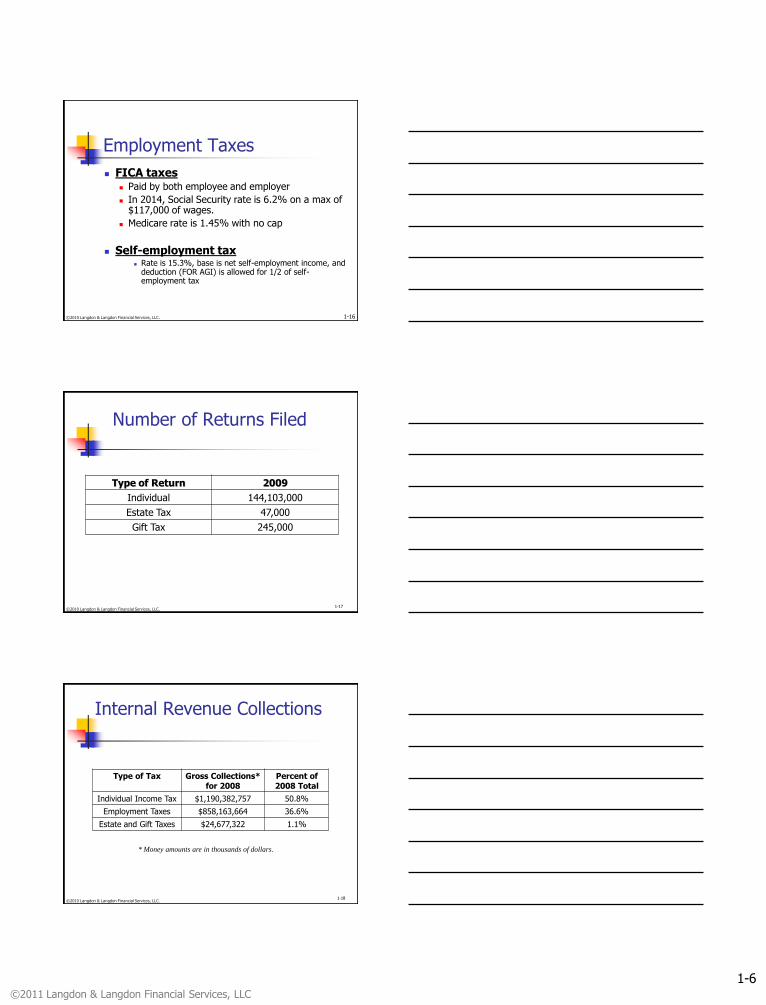

Number of Returns Filed

Type of Return 2009

Individual 144,103,000

Estate Tax 47,000

Gift Tax 245,000

©2010 Langdon & Langdon Financial Services, LLC. 1-17

Internal Revenue Collections

Type of Tax Gross Collections*

for 2008

Percent of

2008 Total

Individual Income Tax $1,190,382,757 50.8%

Employment Taxes $858,163,664 36.6%

Estate and Gift Taxes $24,677,322 1.1%

* Money amounts are in thousands of dollars.

©2010 Langdon & Langdon Financial Services, LLC. 1-18

©2011 Langdon & Langdon Financial Services, LLC

1-7

Working with the Tax Law

1-19 ©2010 Langdon & Langdon Financial Services, LLC.

Sources of Tax Law

Admin Action

Judicial Decisions

Statutory Law

The 16th Amendment to the U.S. Constitution High

Low

Priority

1-20 ©2010 Langdon & Langdon Financial Services, LLC.

Who makes better tax rules…

©2010 Langdon & Langdon Financial Services, LLC. 1-21

The Three Stooges or…..

The Three Wise Men?

©2011 Langdon & Langdon Financial Services, LLC

1-8

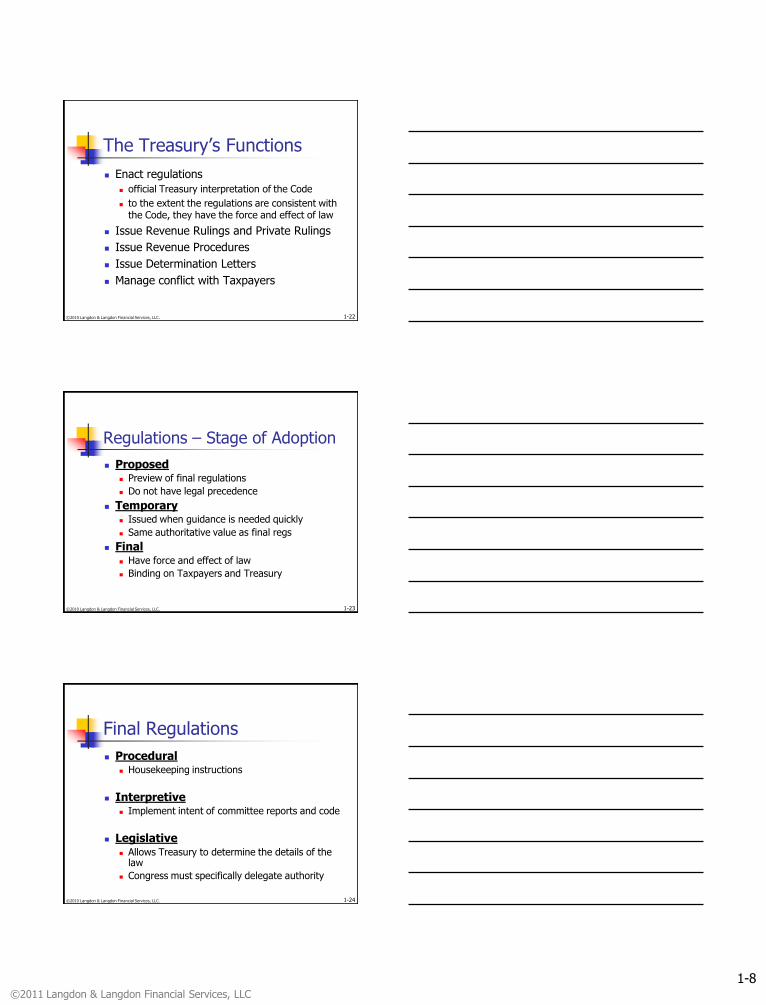

The Treasury’s Functions

Enact regulations

official Treasury interpretation of the Code

to the extent the regulations are consistent with the Code, they have the force and effect of law

Issue Revenue Rulings and Private Rulings

Issue Revenue Procedures

Issue Determination Letters

Manage conflict with Taxpayers

1-22 ©2010 Langdon & Langdon Financial Services, LLC.

Regulations – Stage of Adoption

Proposed Preview of final regulations

Do not have legal precedence

Temporary Issued when guidance is needed quickly

Same authoritative value as final regs

Final Have force and effect of law

Binding on Taxpayers and Treasury

1-23 ©2010 Langdon & Langdon Financial Services, LLC.

Final Regulations

Procedural Housekeeping instructions

Interpretive Implement intent of committee reports and code

Legislative Allows Treasury to determine the details of the

law

Congress must specifically delegate authority

1-24 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-9

Revenue Ruling

facts common to many taxpayers

binding on the IRS

taxpayers can

rely upon the rulings

challenge the rulings in court

courts are not bound by Revenue Rulings

published weekly in the Internal Revenue Bulletin

1-25 ©2010 Langdon & Langdon Financial Services, LLC.

Private Ruling (PLR)

issued at the request of the taxpayer

the IRS is bound by its determination in the ruling

made available to the public after deletion of certain materials

cannot be relied on by other taxpayers as precedent

1-26 ©2010 Langdon & Langdon Financial Services, LLC.

Determination Letters

issued by District Directors for returns filed in their respective districts

must be a completed transaction

issued only if answer is covered specifically by statute

Treasury decision or regulation

ruling opinion or court decision published in the IRB

1-27 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-10

Revenue Procedure

describe internal practices and procedures within the IRS

published in the Internal Revenue Bulletin

generally state changes in techniques and administrative procedures used by the IRS

1-28 ©2010 Langdon & Langdon Financial Services, LLC.

Judicial Sources of Tax Law

Courts

interpret statutory ambiguity

Cannot issue advisory opinions

Need “Case or Controversy”

Court opinions are binding on lower courts, the IRS, and taxpayers

1-29 ©2010 Langdon & Langdon Financial Services, LLC.

Information Available in Basic Tax Research Services

Internal Revenue Code (IRC)

Treasury Regulations (Treas. Reg.)

Practice Aids (offered by RIA publications)

IRS Manual

Court Citations

1-30 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-11

Statute of Limitations

©2010 Langdon & Langdon Financial Services, LLC. 1-31

©2009 Money Education 2-32

Periodicals as a Source of Tax Information

Federal Tax Articles (CCH)

Journal of Taxation

Taxes - The Tax Magazine

Tax Notes

Monthly Digest of Tax Articles

Journal of the Society of Financial Services Professionals

Estate Planning

Trusts & Estates

Journal of Financial Planning

1-33 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-12

Keeping Up with New Developments

CCH & RIA

Accounting Firm Websites

www.TaxAlmanac.com

The Daily Tax Report, published by the Bureau of National Affairs

Database Services

LEXIS and Westlaw

1-34 ©2010 Langdon & Langdon Financial Services, LLC.

3-35 ©2008 Langdon & Langdon Financial Services, LLC.

Basic Tax Planning Principles

1. Receive income in a tax-exempt (excludible) form.

2. Shift income to related taxpayers in lower marginal tax brackets.

3. Receive income that is taxed at favorable capital gains tax rates.

4. Defer Income taxes until later.

1-35 ©2010 Langdon & Langdon Financial Services, LLC.

Basis Rules, Depreciation, & Asset Categorization

1-36 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-13

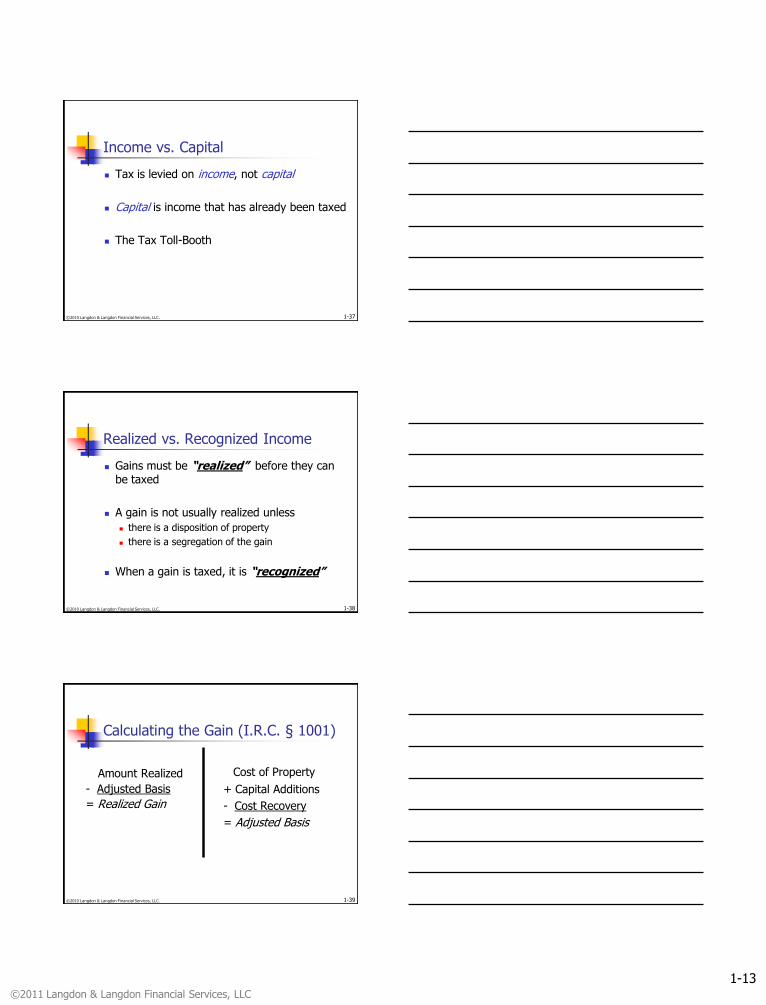

Income vs. Capital

Tax is levied on income, not capital

Capital is income that has already been taxed

The Tax Toll-Booth

1-37 ©2010 Langdon & Langdon Financial Services, LLC.

Realized vs. Recognized Income

Gains must be “realized” before they can be taxed

A gain is not usually realized unless

there is a disposition of property

there is a segregation of the gain

When a gain is taxed, it is “recognized”

1-38 ©2010 Langdon & Langdon Financial Services, LLC.

Calculating the Gain (I.R.C. § 1001)

Amount Realized

- Adjusted Basis

= Realized Gain

Cost of Property

+ Capital Additions

- Cost Recovery

= Adjusted Basis

1-39 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-14

Amount Realized

The sum of money received, plus

the FMV of property received in the exchange, plus

liabilities shed

Results from Sale or other disposition Trade-ins

Casualties

Condemnation

Theft 1-40 ©2010 Langdon & Langdon Financial Services, LLC.

Basis

Purpose Keep track of after-tax dollars (capital) that

is tied up in an investment Allows investor to recoup capital tax-free

upon sale

Uses Determine gain/loss Determine depreciation deductions Determine the amount an investor has “at

risk” under the passive loss rules

1-41 ©2010 Langdon & Langdon Financial Services, LLC.

Determining Basis

Cost Basis

Initial capital used to purchase the investment

Includes

Cash

Cost of property given in exchange

Recourse Debt used for financing

Costs necessary to acquire the asset (sales tax, freight,

installation)

1-42 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-15

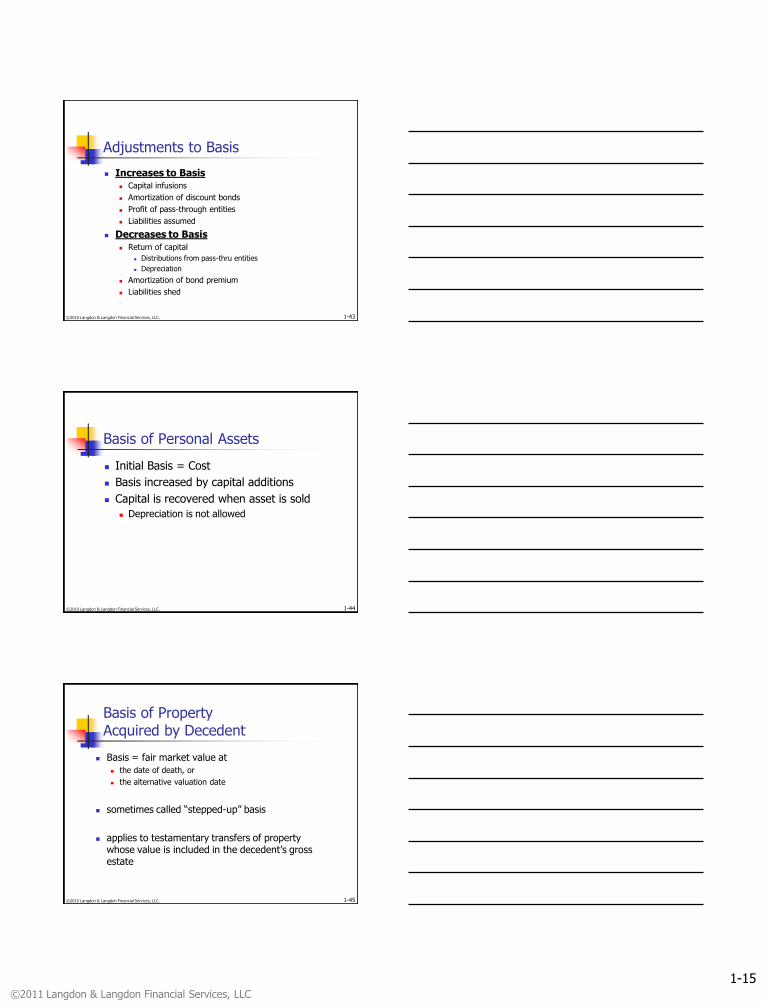

Adjustments to Basis

Increases to Basis

Capital infusions

Amortization of discount bonds

Profit of pass-through entities

Liabilities assumed

Decreases to Basis

Return of capital

Distributions from pass-thru entities

Depreciation

Amortization of bond premium

Liabilities shed

1-43 ©2010 Langdon & Langdon Financial Services, LLC.

Basis of Personal Assets

Initial Basis = Cost

Basis increased by capital additions

Capital is recovered when asset is sold

Depreciation is not allowed

1-44 ©2010 Langdon & Langdon Financial Services, LLC.

Basis of Property Acquired by Decedent

Basis = fair market value at

the date of death, or

the alternative valuation date

sometimes called “stepped-up” basis

applies to testamentary transfers of property whose value is included in the decedent’s gross estate

1-45 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-16

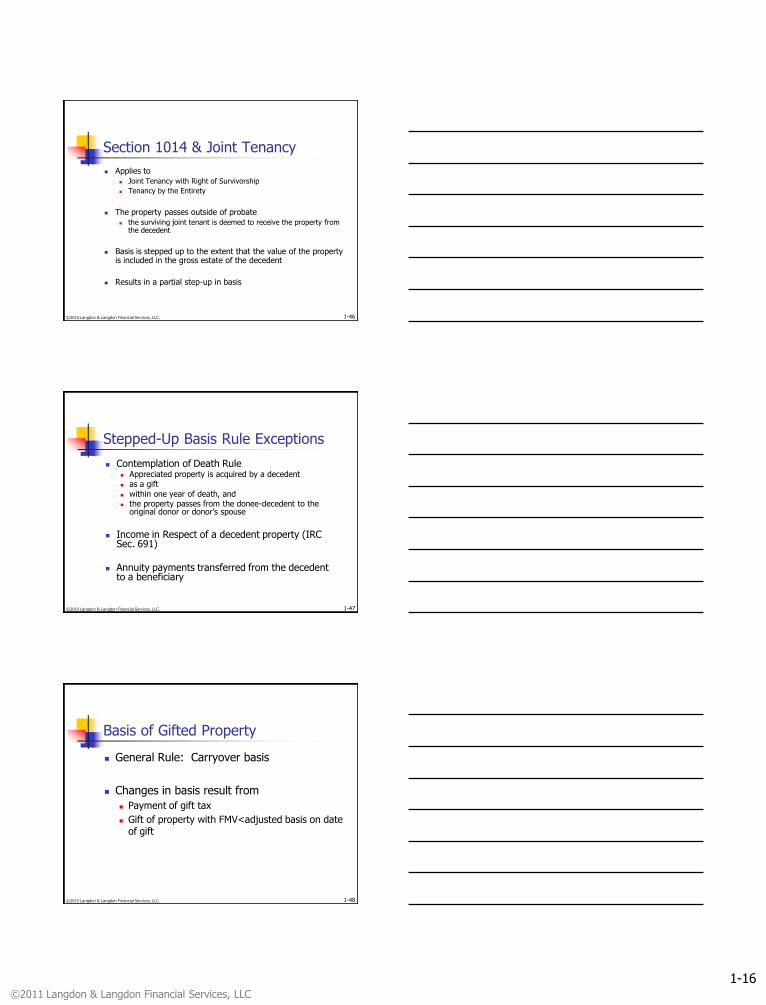

Section 1014 & Joint Tenancy

Applies to

Joint Tenancy with Right of Survivorship

Tenancy by the Entirety

The property passes outside of probate

the surviving joint tenant is deemed to receive the property from the decedent

Basis is stepped up to the extent that the value of the property is included in the gross estate of the decedent

Results in a partial step-up in basis

1-46 ©2010 Langdon & Langdon Financial Services, LLC.

Stepped-Up Basis Rule Exceptions

Contemplation of Death Rule Appreciated property is acquired by a decedent

as a gift

within one year of death, and the property passes from the donee-decedent to the

original donor or donor’s spouse

Income in Respect of a decedent property (IRC

Sec. 691)

Annuity payments transferred from the decedent to a beneficiary

1-47 ©2010 Langdon & Langdon Financial Services, LLC.

Basis of Gifted Property

General Rule: Carryover basis

Changes in basis result from

Payment of gift tax

Gift of property with FMV<adjusted basis on date of gift

1-48 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-17

Impact of Gift Tax on Basis

Donee’s basis is increased by a portion of gift taxes paid by the door if

the donee sells the property

for more than the donor’s original basis

Net Appreciation in Value of Gift

Value of Gift at Transfer x Gift Tax Paid

1-49 ©2010 Langdon & Langdon Financial Services, LLC.

Example

Cathy received a gift from Darren on June 15 of this year that had a FMV of $20,000. Darren’s adjusted basis in the asset was $15,000, and he paid a gift tax on the transfer of $800.

Cathy’s basis in the gifted property is $15,200

Calculation: $15,000 + ($5,000/$20,000 x $800)

1-50 ©2010 Langdon & Langdon Financial Services, LLC.

Gifts of Loss Property

If FMV of gifted property < the donor’s adjusted basis on the date of the gift, a Dual Basis Rule applies

To determine Loss, the adjusted basis of the donee is the lesser of

FMV of the property on the date of gift

the adjusted basis of the transferor

To determine Gain, the basis of the donee is the adjusted basis of the donor (plus an adjustment for gift taxes paid, if applicable)

If the FMV at date of gift < AR < Adjusted basis of transferor, no gain or loss is recognized.

1-51 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-18

Example 10.18

Wally purchased 100 shares of Hyde, Inc. five years ago for $5,000. He just gave those shares to his son, Junior, when the value of the 100 shares was $1,000.

$5,000 Wally’s Adj. Basis

$1,000 FMV at date of Gift

Gain Basis

Loss Basis

No Gain/No Loss Corridor

1-52 ©2010 Langdon & Langdon Financial Services, LLC.

Example 10.18, Continued

Junior sells the shares for $6,000

Gain is $1,000 (Use $5,000 as basis)

Junior sells the shares for $750

Loss is $250 (Use $1,000 as basis)

Junior sells the shares for $3,000

No gain/loss corridor

1-53 ©2010 Langdon & Langdon Financial Services, LLC.

Holding Period For Gifted Property

General Rule:

Holding period in the hands of the donee includes the holding period in the hands of the donor

Exception:

If dual-basis asset is sold for a loss, holding period for donee starts on date of gift

1-54 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-19

Basis & Spousal Transfers

All transfers between spouses & incident to a divorce are treated as gifts.

Basis carries over

Husband and wife are treated as a single economic unit

1-55 ©2010 Langdon & Langdon Financial Services, LLC.

Related Party Transactions

Related Party Spouse, ancestors & descendants, brothers & sisters (of the

whole or half blood)

Sales If a gain results, normal rules apply

If loss results, double basis rule applies Holding period resets

Gifts Gain property – Carryover Basis Loss Property – double basis rule applies

Holding period resets only if loss basis is used

1-56 ©2010 Langdon & Langdon Financial Services, LLC.

Depreciation (Cost Recovery)

Allows taxpayer to recover capital over useful life of asset

May be claimed for assets Used in a trade or business Held for production of income

Capital invested in personal assets is recovered when the asset is sold

1-57 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-20

Taxation of Investment Income

1-58 ©2010 Langdon & Langdon Financial Services, LLC.

Interest & Dividends

Interest

Taxed at ordinary rates when received

EXCEPTION: OID

Dividends

General Rule: taxed at ordinary rates

Qualified Dividends taxed at 15%

1-59 ©2010 Langdon & Langdon Financial Services, LLC.

Capital Gains General Rule: maximum rate of 15% (20% +

surtax of 3.8% for high income taxpayers in 2013) for long-term gains TP in 15% (or lower) bracket - 0%

Exceptions: Collectibles - 28% (28%)

Unrecaptured Sec. 1250 Gain - 25% (25%)

Effective rate may be more than maximum capital gains increase a taxpayer’s AGI

increased AGI may lead to phaseouts

1-60 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-21

Special Rules for Capital Transactions

Sec. 1202

Excludes 50% of gain on small business stock held for 5 years

Aggregate gross assets less than $50 M

C-Corporation

Active conduct of Trade/Profession

Taxable portion subject to 28% capital gains tax

1-61 ©2010 Langdon & Langdon Financial Services, LLC.

Limitation on Capital Losses

Ordinary Portfolio Passive

($3,000)

Income

Lifetime: $3,000 per year

Amounts left over at death are lost

1-62 ©2010 Langdon & Langdon Financial Services, LLC.

Limitation on Passive Losses

Exceptions

Dispose of activity

Meet requirements for $25,000 Loss Deduction

Ordinary Portfolio Passive

($25,000)

Income

1-63 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-22

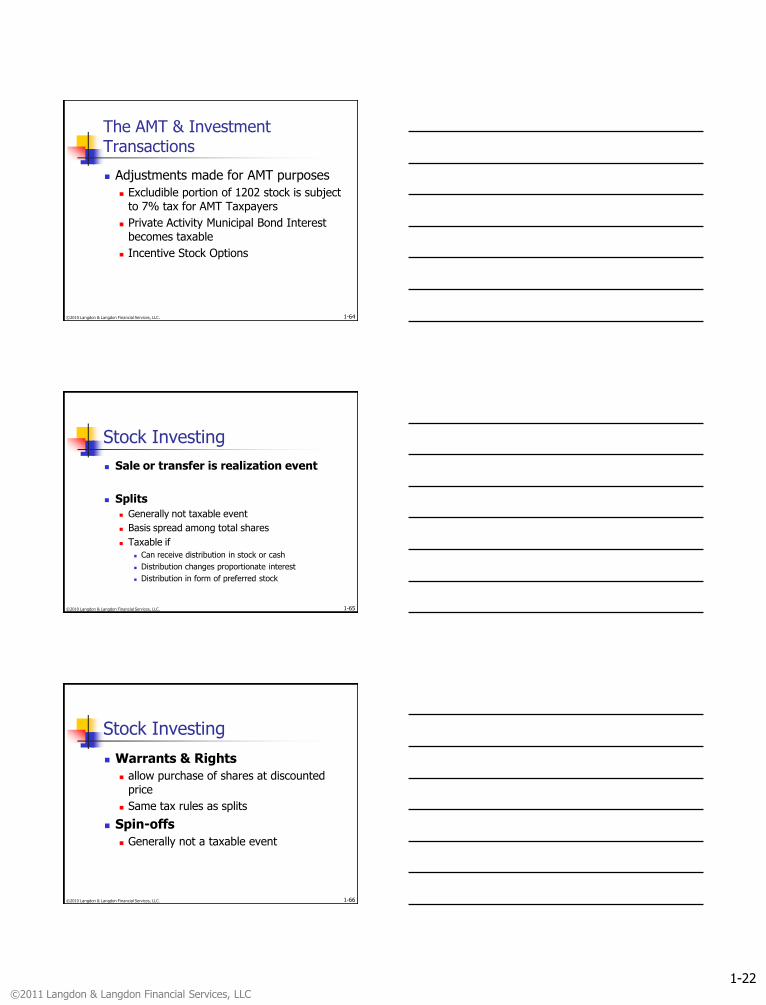

The AMT & Investment Transactions

Adjustments made for AMT purposes

Excludible portion of 1202 stock is subject to 7% tax for AMT Taxpayers

Private Activity Municipal Bond Interest becomes taxable

Incentive Stock Options

1-64 ©2010 Langdon & Langdon Financial Services, LLC.

Stock Investing

Sale or transfer is realization event

Splits

Generally not taxable event

Basis spread among total shares

Taxable if

Can receive distribution in stock or cash

Distribution changes proportionate interest

Distribution in form of preferred stock

1-65 ©2010 Langdon & Langdon Financial Services, LLC.

Stock Investing

Warrants & Rights

allow purchase of shares at discounted price

Same tax rules as splits

Spin-offs

Generally not a taxable event

1-66 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-23

Stock Investing

Short Sales

Used if price expected to go down

Purchase of stock to close transaction is realization event

If gain, purchase date

If loss, settlement date

HP depends on length of time underlying property was held

1-67 ©2010 Langdon & Langdon Financial Services, LLC.

Stock Investing

Short Sales

Special Rules

Gain is ST if on date of original short sale, underlying security was held for 1 year or less

Loss is LT if on the date of the original short sale, substantially similar securities were held for more than one year

1-68 ©2010 Langdon & Langdon Financial Services, LLC.

Stock Investing

Shorting against the box

Formerly used to defer recognition

Treated as constructive sale

Gains are recognized

Losses are deferred

Possible Alternative

Purchase put at the money

1-69 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-24

Stock Investing

Wash Sales (Sec. 1091)

Used to recognize loss without changing economic position

30-day window before & after

Consequences:

No loss recognition

Unrecognized loss added to basis of replacement property

1-70 ©2010 Langdon & Langdon Financial Services, LLC.

Determining Basis of Stock Sales

First-in First-out (FIFO) IRS Approach

Specific Identification Must adequately identify shares

Keep good records

Average Cost Method Tends to lower gain if security increased in value over time

Once elected, must continue to be used for that security

1-71 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of Bonds

Interest (Coupon)

Marginal ordinary income tax rate

Original Issue Discount (OID)

Exception to constructive receipt doctrine

Accrued interest included in income

1-72 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-25

Taxation of Bonds

Market Discount Bonds Investor Election

Amortize discount and increase basis Recognize discount when sold

In either case, treated as interest income

Market Premium Bonds Investor Election (applies to all bonds for the tax year)

Amortize premium over remaining life Do not amortize, and add to basis

If sale results in gain, premium returned tax free If sale results in loss, treated as capital loss

If tax exempt bond, no amortization is permitted, but basis will be reduced by the bond premium

1-73 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of Bonds

Municipal Bonds

Coupon payments are generally exempt

AMT status causes coupon payments to be taxable on all but public purpose municipal bonds

Gain/Loss is subject to tax

1-74 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of Bonds

Government Bonds

Coupon is subject to federal, but not state, taxation

Series EE Bonds for Education

Exempt if

Purchaser was 24 years old

Bond is registered in name of bond owner

MAGI falls below specified limit

1-75 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-26

Taxation of Open-End Mutual Funds

2 Sources of gain

Increase/decrease in value

Capital transaction

Distributions

Interest

Dividends (Qualified or non-qualified)

Long-Term Capital Gains

Short-Term Capital Gains

1-76 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of Closed-End Mutual Funds

Usually purchased in secondary market

Generally capital treatment governs

If elect to be taxed as a regulated investment company, tax rules follow open-end mutual funds

1-77 ©2010 Langdon & Langdon Financial Services, LLC.

Unit Investment Trusts

Similar to mutual funds, but not actively managed

Tend to hold securities that self liquidate over time

Gains/losses follow normal rules

Investment Income

Grantor Trust – all income taxable to owners

Regulated Investment Company – taxed in same manner as open-end mutual fund

1-78 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-27

Taxation of Real Estate

If held for business or rental use, treated as Sec. 1231 asset Depreciation is available

Depreciation recapture calculated on sale

Principal Residence

Sec. 121 Exclusion

Playing monopoly

1031 Exchanges 1-79 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of Real Estate

Tax deductions derive from

Depreciation

Interest on loans

Property tax

1-80 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of REITs

Mutual fund for real estate

Most are Publicly traded

closed-end investment companies

Exempt from tax at entity level if 75% of income comes from real estate

Distributes 90% of income in form of dividends on an annual basis

1-81 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-28

Taxation of Option Contracts

Depends on Long/short position in contract

Type of option held

Manner of disposition

Purchase of an option Not a taxable event

Basis = Cost + Commission

1-82 ©2010 Langdon & Langdon Financial Services, LLC.

Disposition of Long Option Contracts

Sale Calculate gain/loss

Generally STCG (9 month contracts)

LEAPs can be LTCG

Exercise No realization event

Call - Investor’s basis in stock purchased is increased by basis in option contract

Put – sale of underlying stock is taxable event; AR is reduced by basis in the put option

Character determined by HP of stock, not the option

1-83 ©2010 Langdon & Langdon Financial Services, LLC.

Disposition of Long Option Contracts

Expiration

Option premium paid is a capital loss

1-84 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-29

Disposition of Short Option Contracts

Receipt of Premium Not a taxable event

Exercise by purchaser Call – seller adds premium received on sale of

option to AR to determine gain/loss HP determined by length of time stock was held

Put – no immediate taxable event Reduce basis in stock purchased by option premium

received HP begins on the date of exercise

1-85 ©2010 Langdon & Langdon Financial Services, LLC.

Disposition of Short Option Contracts

Expires

Premium is STCG

If position is closed

Recognize STCG/L = Option Premium Received – Option premium paid

1-86 ©2010 Langdon & Langdon Financial Services, LLC.

Employer Stock Options and Stock Plans

Stock Options – The right to buy stock at a specified price for a specified period of time. Agreement must be in writing, and holder has no obligation

to exercise

Option price = FMV at date of grant

Vesting – Right to exercise options only after certain period of time, performance, or occurrence.

Types of Options Incentive Stock Options (ISOs)

Nonqualified Stock Options (NQSOs)

Stock Appreciation Rights (SARs)

1-87 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-30

Incentive Stock Options (ISOs)

statutory Stock Option ties employee benefit to stock price of the

company may provide special taxation may only be granted to employees. aggregate FMV of ISO grants must be less

than $100,000 per year per executive. For ISO special tax treatment, individual must

hold stock two years from date of grant, and one year from date of exercise.

1-88 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of ISOs

Grant Date No taxable income unless exercise price is less than fair

market value at date of grant.

Upon Exercise No regular tax.

AMT adjustment equal to appreciation over the exercise price.

Upon sale of stock Long-term capital gain treatment for stock appreciation over

exercise price.

Negative AMT adjustment.

Employer does not have a tax deduction related to the ISO.

1-89 ©2010 Langdon & Langdon Financial Services, LLC.

Disqualifying Disposition

Selling stock acquired from an ISO before two years from grant date or one year from exercise date.

Loss of favorable tax treatment. Appreciation over exercise price at exercise date =

ordinary income (reported on W-2). Appreciation after exercise date = capital gain

(short/long based on holding period beginning at exercise date).

Employer has a tax deduction equal to the executive’s W-2 income.

1-90 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-31

Cashless Exercise

Very common

Third-party lends cash

Executive repays the lender almost immediately with the proceeds and has W-2 income for the excess value over the exercise price.

A cashless exercise is a disqualifying disposition.

1-91 ©2010 Langdon & Langdon Financial Services, LLC.

Nonqualified Stock Option (NQSO)

Option that does not meet requirements of an ISO.

Ties an employee benefit to the performance of the company stock.

Exercise does not receive favorable tax treatment.

No statutory holding period requirements. Employer’s may place holding period requirements

on the stock.

1-92 ©2010 Langdon & Langdon Financial Services, LLC.

Taxation of NQSOs

Grant Date No taxable income unless exercise price is less

than fair market value at date of grant.

Upon Exercise Executive will have W-2 income for the

appreciation over the exercise price. Employer has income tax deduction for same

amount.

Upon sale of stock Executive will have capital gain/loss with a holding

period beginning at the exercise date.

1-93 ©2010 Langdon & Langdon Financial Services, LLC.

©2011 Langdon & Langdon Financial Services, LLC

1-32

Gifting of ISOs and NQSOs

ISOs

Unexercised ISOs cannot be gifted.

Can only be transferred after exercise date.

NQSO

May be gifted if allowed by employer.

When donee exercises -

Employee will have W-2 income.

Employer will have tax deduction.

Donee’s basis equals W-2 amount.

1-94 ©2010 Langdon & Langdon Financial Services, LLC.

Stock Appreciation Rights (SARs)

Rights that grant the holder cash in an amount equal to the excess of the fair market value of the stock over the exercise price.

Ties an employee benefit to the value of the employer’s stock.

Essentially a cashless exercise without any right to purchase the stock.

No taxation at grant Unless employee elects IRC Section 83(b) – discussed below.

Employee - W-2 income for excess value over exercise price.

Employer – Tax deduction for W-2 amount.

1-95 ©2010 Langdon & Langdon Financial Services, LLC.

Related Documents