Price Risk Management Jim Dunn Penn State University

Price Risk Management Jim Dunn Penn State University.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Price Risk Management

Jim Dunn

Penn State University

A son is helping his father plant some red delicious apple trees and asks, “Why are we planting

these?

The father answers, “I hope that someday someone

might want some.”

Introduction

• Most farmers are in the market for corn and other commodities in some manner

• How much corn will you be buying or selling?

• What price do you expect?• Can you make money at that price?• What is your cost of production?• Have you done anything to lock in that

price?

Risk Management

• What might go wrong?

• Have you made any provisions for that?

• What are they?

• What have you forgotten?

• The “Hidden Bummer Factor”

What price do you expect?

• How do you forecast prices?

• Do you subscribe to a market news service?

• Is there a better way?

What are Futures Contracts?

• A uniform contract for future delivery.

• Everything is specified but the price. Quantity, quality, delivery time, delivery place, penalties & premiums

Role of Futures Markets

• Provide estimate of prices in future

• Transfer risk to those who want it

• Facilitate hedging

• All are important for Risk Management

Provide Estimate of Future Prices

• Can use futures price to estimate local price

• Can use estimates to estimate profitability of crop

• If profitable can forward contract

• Key is Basis

Basis

The difference between the contract price and your local price at the time you expect to close the contract

2000 2002 2004 2006 2008 2010 2012 20140

100

200

300

400

500

600

700

800

900

cts/

bu

ChicagoSE Penn

Corn Price Chicago and SE Pennsylvania

2000-14

Jan Mar May Jul Sep Nov-20

0

20

40

60

80

100

120

140

160

180C

ts/b

u

2008200920102011201220132014

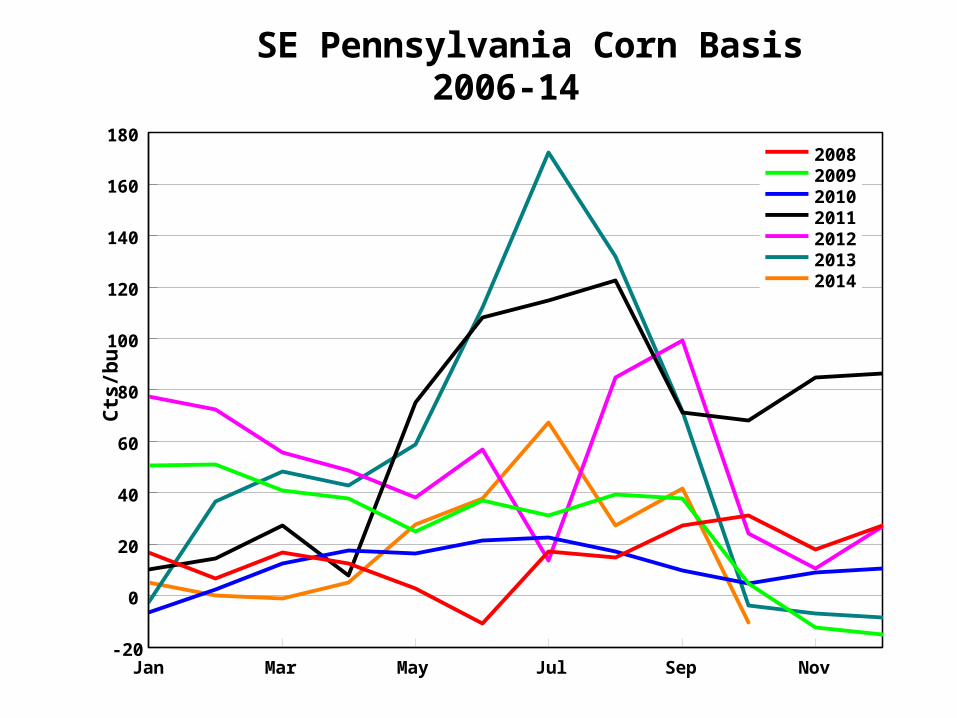

SE Pennsylvania Corn Basis 2006-14

Southeastern PA Basis (2000-14) Month Avg High Low

JAN 27 90 -29FEB 28 81 -4MAR 30 135 -17APR 28 67 -14MAY 35 104 -11JUN 46 197 -24JUL 46 206 -39AUG 50 166 -15SEP 42 141 2OCT 18 73 -39NOV 18 92 -20DEC 23 97 -26

YEAR 34 206 -39

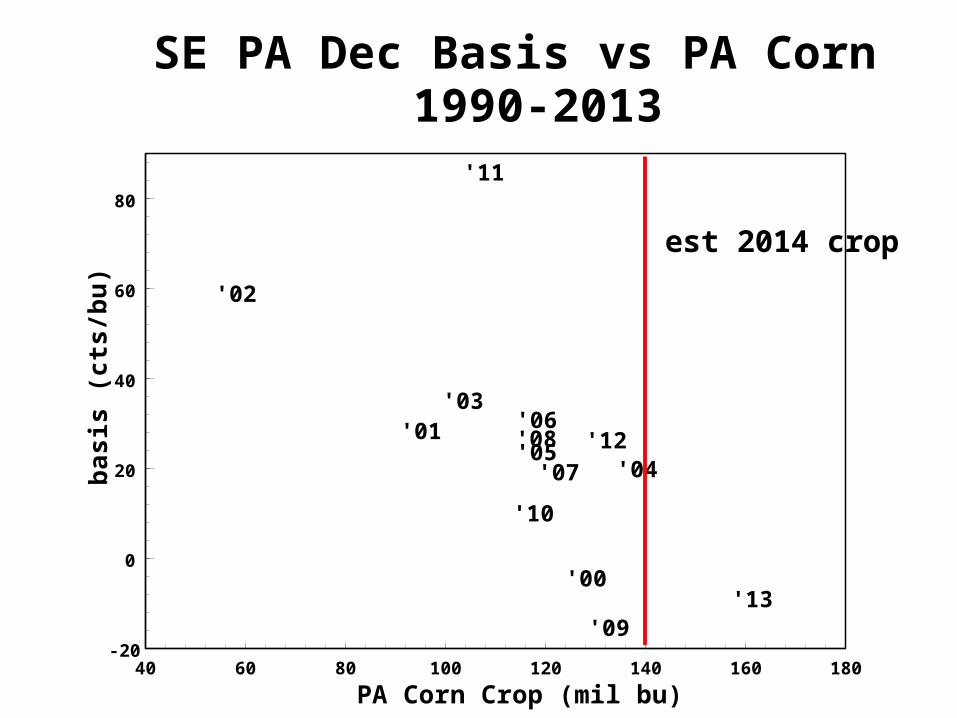

40 60 80 100 120 140 160 180

PA Corn Crop (mil bu)

-20

0

20

40

60

80

bas

is (

cts/

bu

)

'00

'01

'02

'03

'04'05

'06

'07

'08

'09

'10

'11

'12

'13

SE PA Dec Basis vs PA Corn Crop1990-2013

est 2014 crop

Soybean Prices -1995-2004PA and Chicago

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$/bu

SE Pennsylvania Chicago

Soybean Basis -1995-2004Southeast PA

-125-100-75-50-25

0255075

100

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$/bu

Basis

Southeastern Soybean PA basis

Month avg max min

Jan -14 14 -61

Feb -9 19 -63

Mar -11 22 -55

Apr -17 11 -44

May -16 29 -50

Jun -12 34 -50

Jul -17 70 -56

Aug -15 72 -79

Sep -19 50 -75

Oct -30 26 -99

Nov -29 20 -61

Dec -21 23 -65

YEAR -17 72 -99

Transfer risk to those who want it

• Speculators need risk to make money

• Farmers and processors may prefer not to have risk

• Selling corn in advance to speculator reduces risk for farmer

Facilitate hedging

• Hedging using futures markets has low costs

• Liquidity helps with lifting hedge

• Can be used by feed mill to offset risk of direct forward contracts

A Simple Price Risk Management Plan

• When planning check futures prices

• Work out expected profits

• If unprofitable rethink what you will do

• If profitable consider hedging some part

Can you lock in your price?

• Contract locally

• Use futures market

• Options

Contract Locally

• Easiest

• No margin calls

• No basis risk

• Price may be a bit less

• You know who you are dealing with

How to Hedge

• Already face risk in cash market

• By selling a corn contract for December, you are pre-selling corn

• You can do this locally or through futures

• If using futures, see your banker

Hedging with Futures

• For a corn producer

• Sell a futures contract when you want to lock in price

• Buy it back when you want to sell corn

• Sell corn locally

• Price changes in meanwhile should cancel out

• Basis risk remains

Hedging with Futures

• For a corn user

• Buy a futures contract when you want to lock in price

• Sell it back when you want to buy corn

• Buy corn locally

• Price changes in meanwhile should cancel out

• Basis risk remains

Example

• Now• Sell one Dec corn for

$3.67 / bu.• Expect basis to be

$0.23/bu• Commissions are

$0.01• Lock in about $3.79

• December• Buy one Dec. corn

contract $3.25• Sell corn locally $3.45• Net from futures

$3.67– $3.25– $0.01 comm.

$0.41

• Net total $3.86

How this works

• The futures price drives corn prices internationally

• All markets move together, more or less

• Profits or losses in futures offset change in value of corn

• Only uncertainty is value of basis

• In example basis was a a little smaller than average

Margin calls

• Margin - a portion of value of contract as down payment to protect broker

• If corn goes up your contract loses money• But, the corn that you are growing is worth

more• Because you have sold in advance, the

price changes should have no net effect• However, you may need more margin

money - fast

See your Banker First

• Make sure the banker knows difference between hedging and speculating and knows the you know

• Make sure banker knows margin calls don’t hurt your profit outlook

• Make sure you have arranged margin credit beforehand!

What are Futures?

• A uniform contract for future delivery.

• Everything is specified but the price.

• Quantity, quality, delivery time, delivery place, penalties & premiums

Advantages of Futures

• Low transaction costs

• Liquidity

Disadvantages of Futures

• Delivery locations in Midwest• Quantity fixed at a level that may not suit

you• Quality fixed at a level that may not suit

you• Contract expiration fixed at a time that

may not suit you• Lock in price that may be bad, looking

back

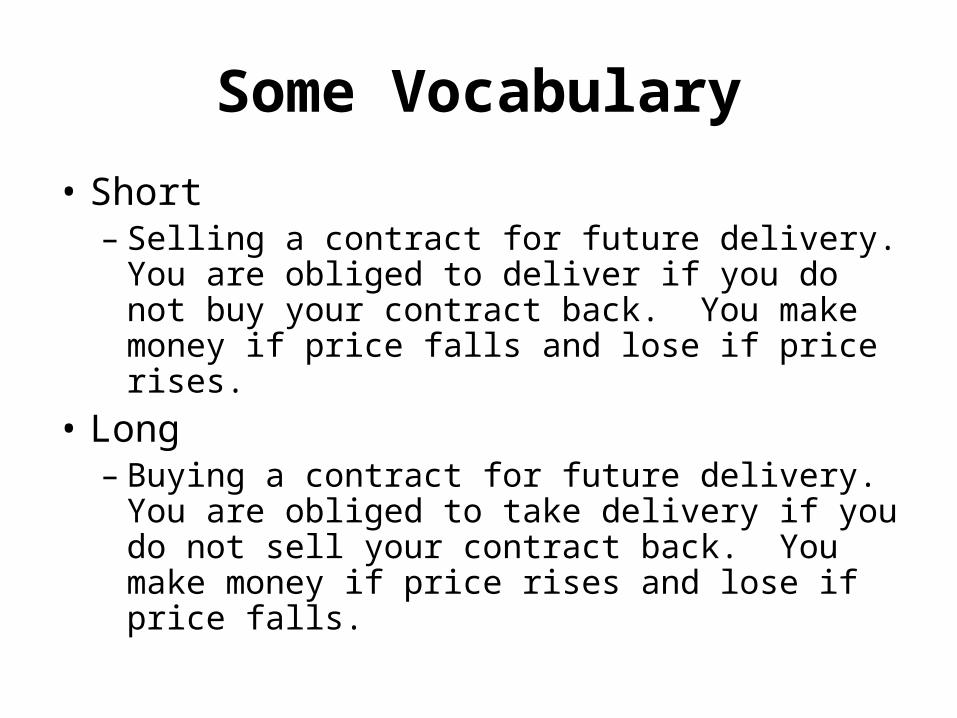

Some Vocabulary

• Short– Selling a contract for future delivery. You are

obliged to deliver if you do not buy your contract back. You make money if price falls and lose if price rises.

• Long– Buying a contract for future delivery. You are

obliged to take delivery if you do not sell your contract back. You make money if price rises and lose if price falls.

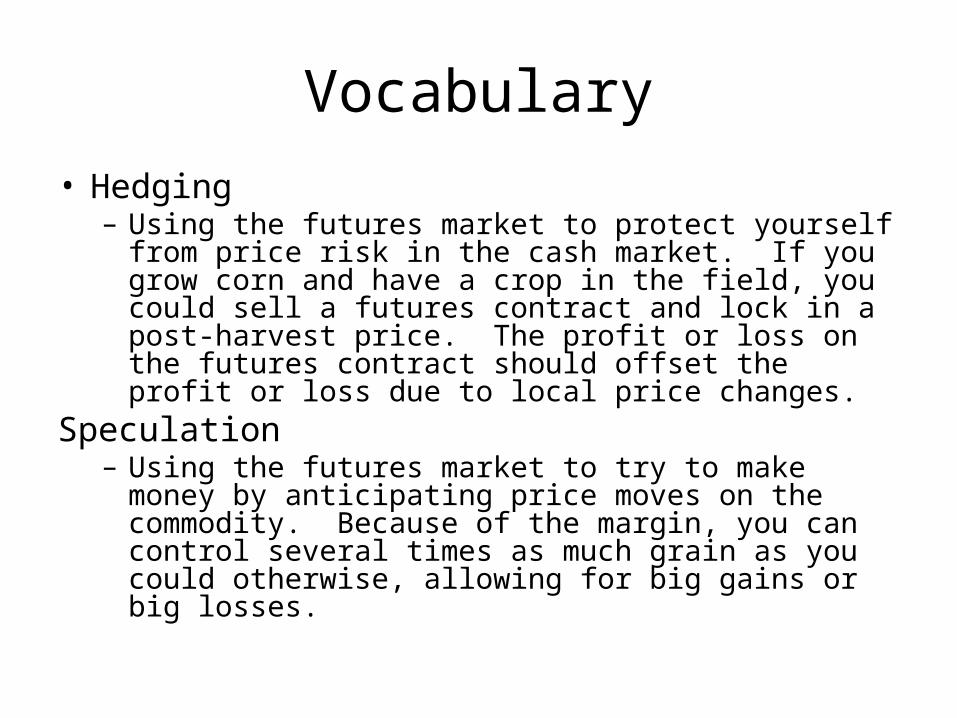

Vocabulary

• Hedging– Using the futures market to protect yourself from price

risk in the cash market. If you grow corn and have a crop in the field, you could sell a futures contract and lock in a post-harvest price. The profit or loss on the futures contract should offset the profit or loss due to local price changes.

Speculation– Using the futures market to try to make money by

anticipating price moves on the commodity. Because of the margin, you can control several times as much grain as you could otherwise, allowing for big gains or big losses.

“There are two times in a man’s life when he should not

speculate: when he can’t afford it and when he can.”

Mark Twain

Options

• Insurance against price risk• Put – insurance against low prices• Call – insurance against high prices• Pretty expensive• Allow you to enjoy favorable price changes but

not suffer from unfavorable price changes• No margin calls• Basis risk remains

Options

• The right, but not the obligation, to either make or take future delivery on a commodity.

Puts

The right to sell a futures contract during a fixed time period for a fixed price. Useful to protect a corn farmer against lower corn prices.

Calls

• The right to buy a futures contract during a fixed time period for a fixed price. Useful to protect a hog farmer against higher corn prices.

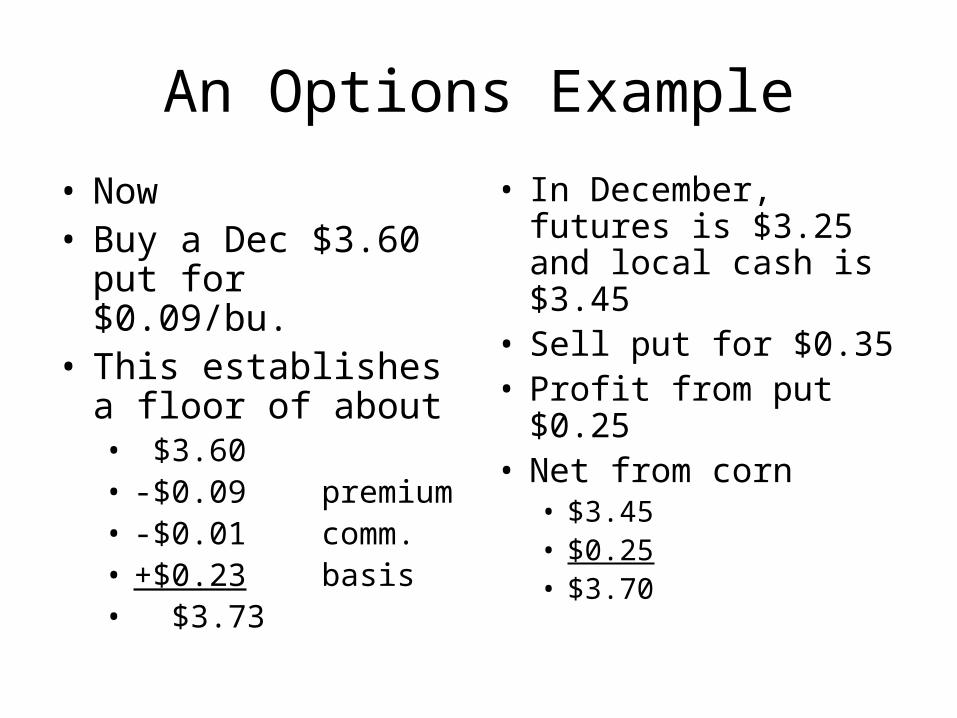

An Options Example

• Now• Buy a Dec $3.60 put

for $0.09/bu.• This establishes a

floor of about • $3.60• -$0.09 premium• -$0.01 comm.• +$0.23 basis• $3.73

• In December, futures is $3.25 and local cash is $3.45

• Sell put for $0.35• Profit from put $0.25• Net from corn

• $3.45• $0.25• $3.70

How this works

• If price falls, floor price is engaged

• If price rises, put becomes worthless

• Only risk is basis value

• Insurance is expensive

Risk Management

• Having no plan is a decision – but not a good one

• Especially if you have debts, or large financial obligations

• You can develop a plan, and institute it, and concentrate on your farming

• Farms go out of business because of high costs, low revenues, and unforeseen events

• Some of this is not understanding costs or risk management well

Related Documents