INDONESIA ECONOMIC QUARTERLY MARCH 2013 Jim Brumby, PREM Sector Manager & Lead Economist Paramadina Public Policy Institute, March 2013 PRESSURES MOUNTING www.worldbank.org/id

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INDONESIA ECONOMIC QUARTERLY MARCH 2013

Jim Brumby, PREM Sector Manager & Lead EconomistParamadina Public Policy Institute, March 2013

PRESSURES MOUNTING

www.worldbank.org/id

MARCH 2013 IEQ LAUNCH PRESENTATION

Steady recent economic growth, but pressures mounting

Strong performance can continue but will require policy progress in key areas

More evidence on the need and scope for progress in these areas

INDONESIA’S ECONOMY CONTINUES TO PERFORM WELL

0

3

6

9

12

15

0

3

6

9

12

15

Dec-2009 Dec-2010 Dec-2011 Dec-2012

Percent Percent

China

IndiaIndonesia

MalaysiaMajor Trading Partners

USA

Source: CEIC; World Bank Global Economic Prospects, January 2013, and East Asia Update, December 2012

Real GDP growth, year-on-year

MOUNTING PRESSURES

1. Investment growth cooling; public infrastructure lagging

2. Real sales and nominal GDP growth: moderating

3. External balances: no relief

4. Fiscal sector: burdened by energy subsidies

5. Poor and vulnerable households: slower pace of improvement

INVESTMENT GROWTH: MODERATING

Source: CEIC; World Bank staff calculations

Year-on-year growth

0

2

4

6

8

10

12

14

-40

-20

0

20

40

60

80

Mar-09 Dec-09 Oct-10 Jul-11 Apr-12 Jan-13

Percent Percent

Capital goods imports (3-month moving average)

Real fixed investment

EXTERNAL BALANCES: STILL UNDER PRESSURE, RECENTLY DUE ESPECIALLY TO OIL & GAS TRADE DEFICIT

Source: CEIC; World Bank staff calculations

-2

-1

0

1

2

3

4

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Non-oil and gas balance Oil and gas balance

USD billion USD billion

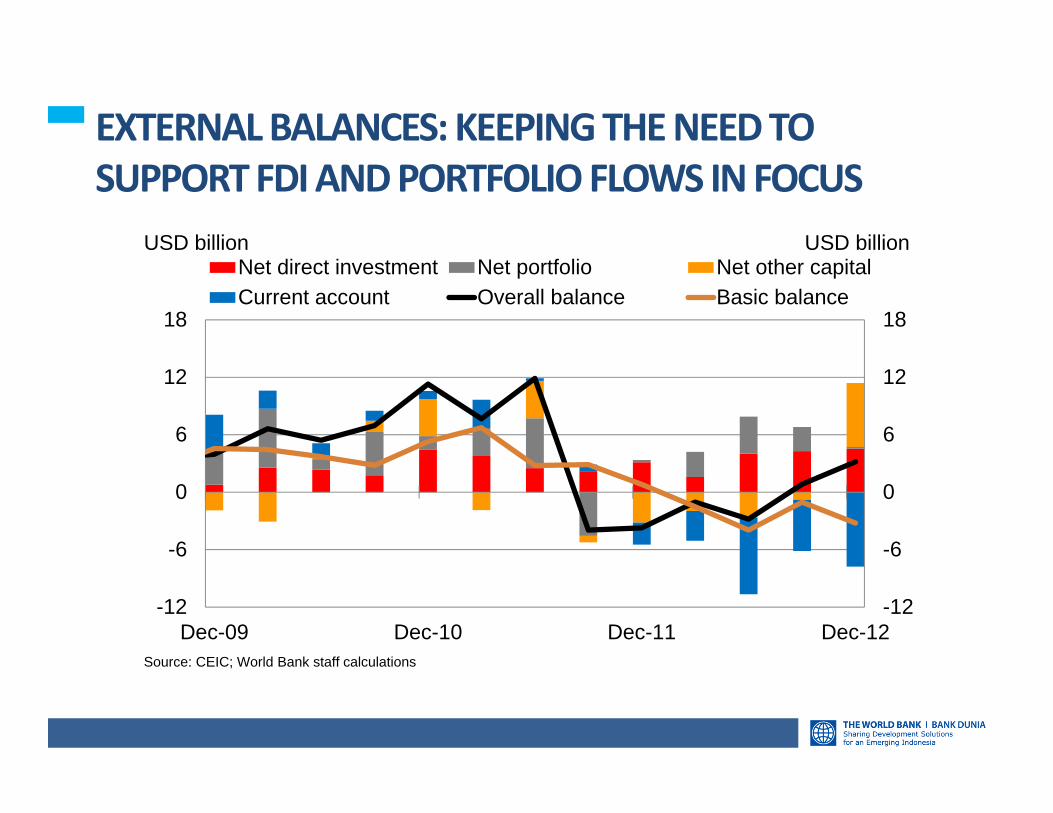

EXTERNAL BALANCES: KEEPING THE NEED TO SUPPORT FDI AND PORTFOLIO FLOWS IN FOCUS

-12

-6

0

6

12

18

-12

-6

0

6

12

18

Dec-09 Dec-10 Dec-11 Dec-12

Net direct investment Net portfolio Net other capitalCurrent account Overall balance Basic balance

USD billion USD billion

Source: CEIC; World Bank staff calculations

GROWTH OUTLOOK: MEASURED REAL FINAL SALES GROWTH DECLINING

0

2

4

6

8

10

0

2

4

6

8

10

Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

Real final sales Real final domestic sales Real GDP

Percent Percent

Note: Real final (domestic) sales = Measured private consumption + government consumption + fixed investment+ net exports (-net exports)Source: CEIC; World Bank staff calculations

Year-on-year growth

GROWTH OUTLOOK: NOMINAL GDP GROWTH MODERATING

0

5

10

15

20

25

30

0

5

10

15

20

25

30

Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

Real GDP Nominal GDP

Percent Percent

Source: CEIC; World Bank staff calculations

Year-on-year growth

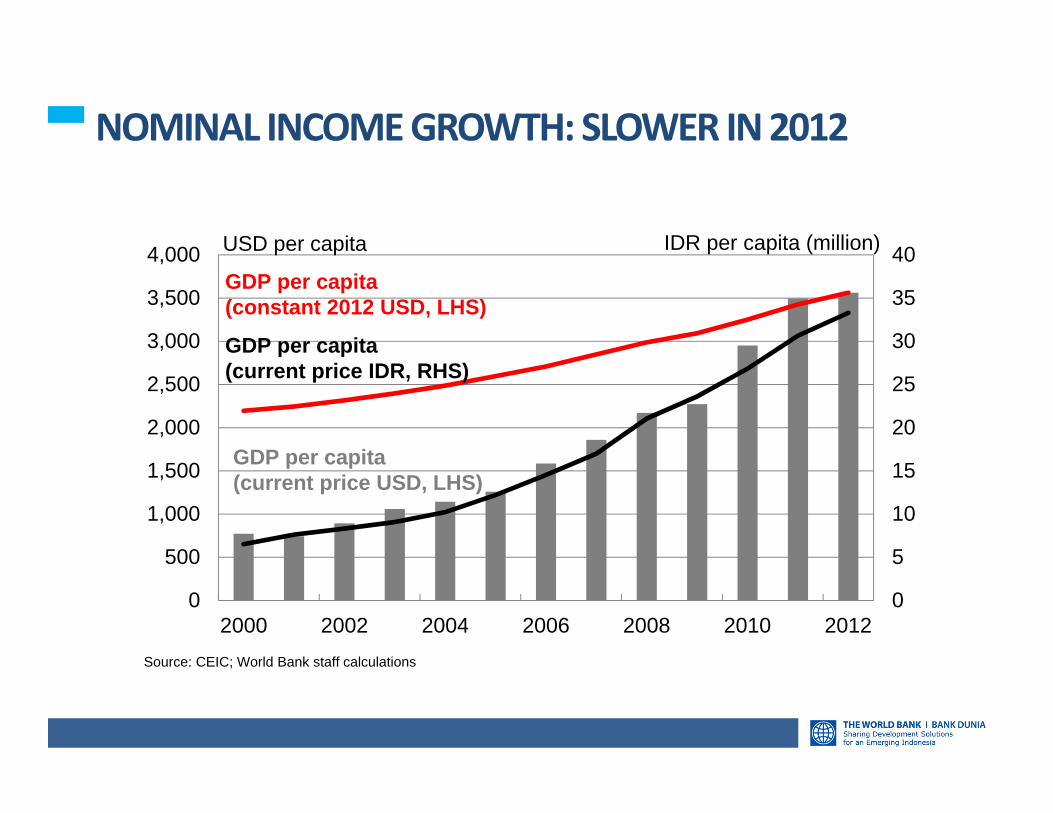

NOMINAL INCOME GROWTH: SLOWER IN 2012

0

5

10

15

20

25

30

35

40

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012

GDP per capita (constant 2012 USD, LHS)

GDP per capita (current price USD, LHS)

GDP per capita (current price IDR, RHS)

USD per capita IDR per capita (million)

Source: CEIC; World Bank staff calculations

INFLATION: FOOD PRICE PRESSURES

Source: CEIC; World Bank staff calculations

0

2

4

6

8

0

20

40

60

80

GreenChili

Red Chili Garlic Onion Foodinflation

exclitems*

Foodinflation

Change in CPI from Dec 2012 toFeb 2013 (LHS)

Change in CPI from Dec 2012 toFeb 2013 (RHS)

Percent Percent

ACHIEVING OFFICIAL POVERTY REDUCTION TARGETS WILL BE A STRETCH

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

0

2

4

6

8

10

12

14

16

18

20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Official Poverty (LHS)

RPJM High TargetRPJM Moderate Target

Annual Change in Poverty

Change in Poverty rate, percentPoverty rate, percent

FISCAL SECTOR: BURDENED BY INEFFICIENT SPENDING

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

Personnel Material Capital Int.Payments

Energysubsidy

Social

2011 Actual Audited 2012 Preliminary Actual 2013 Budget

IDR trillion IDR trillion

Source: MoF; World Bank staff calculations

MARCH 2013 IEQ LAUNCH PRESENTATION

Steady recent economic growth, but pressures mounting

Strong performance can continue but will require policy progress in key areas

More evidence on the need and scope for progress in these areas

NOTWITHSTANDING THE PRESSURES, STRONG PERFORMANCE AND PROGRESS CAN CONTINUE…

Note: CPI is annual average. Government figures for Budget deficit: 2012 is preliminary outturn, 2013 is approved Budget and 2014 is from the 2013 Draft Budget Financial Note Source: Ministry of Finance, BPS, Consensus Forecasts Inc., World Bank staff calculations

2011 2012 2013 2014

Gross domestic product

6.5 6.2 6.2 6.5

Consumer price index 5.2 4.3 5.5 5.2

Budget balance ‐1.2 ‐1.8 ‐1.7 ‐1.4

Major trading partner growth

3.6 3.4 3.7 4.0

…BUT THIS REQUIRES THAT POLICY ADDRESSES MOUNTING PRESSURES

• Investment: Sustain private investment by providing policy

certainty; making ongoing improvements in regulatory framework

Work to meet the public infrastructure investment challenge

Trade and external balances: Focus on competitiveness rather than import

restrictions

Fiscal sector: Fuel subsidy reform

Households: Food: focus on availability; redirect subsidies

Timely responses tend to yield results

MARCH 2013 IEQ LAUNCH PRESENTATION

Steady recent economic growth, but pressures mounting

Strong performance can continue but will require policy progress in key areas

More evidence on the need and scope for progress in these areas

0 25 50 75 100

SUCCESSFUL MANUFACTURES RELY ON IMPORTS

0 25 50 75 100

AgricultureMining

Food prodTCF

Wood&paperChemicals&mi…

Basic metalMachinery

Electric eq.Transport eq.

Other

Domestic goods Domestic servicesForeign goods Foreign services

Percent

Indonesia China

Value-added in manufactured goods exports

Source: OECD and WTO Trade in Value-Added (TiVA) statistics

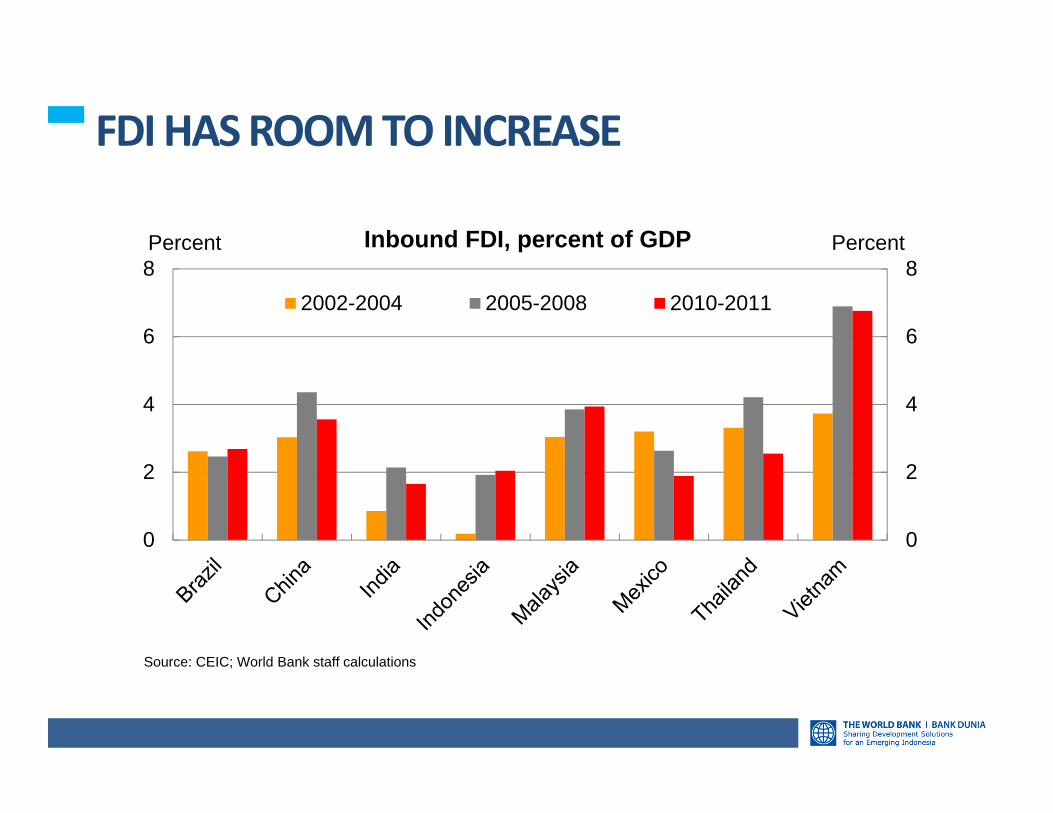

FDIHAS ROOM TO INCREASE

0

2

4

6

8

0

2

4

6

82002-2004 2005-2008 2010-2011

Percent Percent

Source: CEIC; World Bank staff calculations

Inbound FDI, percent of GDP

PUBLIC INFRASTRUCTURE NEEDS A FURTHER BOOST

0

100

200

300

400

500

0

2

4

6

8

10

1995 1997 1999 2001 2003 2005 2007 2009 2011

Percent of GDP IDR trillion

Real spending (2000 prices, RHS)

Infrastructure investment to GDP (LHS)

Note: Real value calculated using investment GDP deflatorSource: Infrastructure investment data as detailed in Box 5 of March 2013 IEQ and World Bank staff calculations

TAP INTO THE POTENTIAL OF FAST URBANIZATION

Source: Indonesia: The Rise of Metropolitan Regions. The World Bank (2012)

Agglomeration areas in Indonesia

15

25

35

45

55

15

25

35

45

555.5 6 6.5 7 7.5 8 8.5 9 9.5

Percent Ln GDP per capita (PPP, 2005 prices)

Indonesia China

India

Philippines

Thailand

Vietnam

Per capita GDP against urbanization rates

SUMMARY: MARCH 2013 IEQ PRESSURES MOUNTING This edition of the IEQ contains analysis on:

Fiscal policy – analysis of the 2012 Budget outturn Trade dynamics – insights from new trade in value‐added data for

Indonesia Urbanization – harnessing the potential of agglomeration areas Infrastructure investment spending – trends and the need for more

Key messages: Steady recent economic performance with base case for this to

continue But there are some mounting pressures and the risks to the economy

are to the downside Timely policy responses tend to yield good results

Related Documents