Natural Gas – a fuel for the future Jan Rune Schøpp, Vice President – Strategy and Analysis Natural Gas, Statoil Press brief ONS, Stavanger 25 August 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Natural Gas – a fuel for the future

Jan Rune Schøpp, Vice President – Strategy and Analysis Natural Gas, Statoil

Press brief ONS, Stavanger 25 August 2010

2

Statoil – building growth from a firm strategy

Maximise the NCS values

Deliver international growth

Build new

energyHarsh environments

Deep water

Heavy oil

Gas value chains

Growth areasA firm strategy

3

Gas increasingly important in Statoil’s production on the Norwegian Continental Shelf

Ambition to maintain NCS production level towards 2020 (mmboed)

Oil production*

* Production: Statoil’s equity production 1990 – 2009

Gas production*

New added production capacity towards 2018

0

200

400

600

800

1000

1200

1990 1993 1996 1999 2002 2005 2008

Sta

rt-u

p 2

014

-2018

Tommeliten Alpha

Astero

Lavrans

Peon

Alfa Sentral

Hild

Luva

Valemon

15/5-2

Dagny/Ermintrude

Marulk (Sanctioned)

Pan Pandora

Ormen Lange Compression

Gudrun (Sanctioned)

Grane C&M

Goliat (Sanctioned)

Note: Bold indicates operatorship / joint operatorship

Sta

rt-u

p 2

012

-2016

4

A unique European gas position

* Statoil entitlement gas and NCS gas marketed on behalf of SDFI sold in EuropeSource other companies Cedigaz 2008

165

71

55 55

Gazprom Statoil* Sonatrach GasTerra

Proximity to markets Access to an integrated and flexible infrastructureA leading marketer of gas (bcm)

Nyhamna

Europipe II

Europipe I

Norpipe

Emden/Dornum

Åsgard transport

Franpipe

Zeebrugge

Zeepipe

St Fergus

VesterledKårstø

Kollsnes

Ormen Lange

Easington

Langeled

Ekofisk

Sleipner

Troll

Dunkerque

Tampen Link

Draupner

Norway

Russia

Algeria

Pipeline

LNG

5

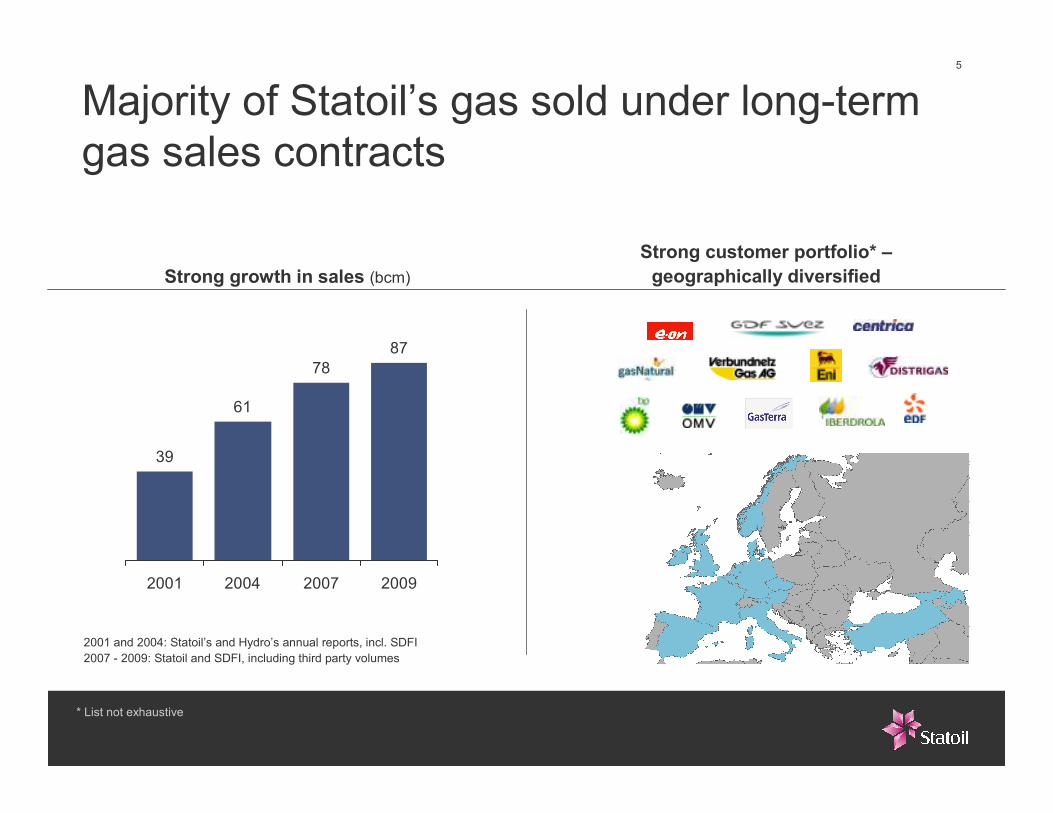

Majority of Statoil’s gas sold under long-term gas sales contracts

2001 and 2004: Statoil’s and Hydro’s annual reports, incl. SDFI

2007 - 2009: Statoil and SDFI, including third party volumes

Strong customer portfolio* –geographically diversifiedStrong growth in sales (bcm)

* List not exhaustive

39

61

78

87

2001 2004 2007 2009

6

Marcellus – US

Developing new gas value chains

Shah Deniz –AzerbaijanAlgeria – North Africa NCS – Norway

7

A new supply corridor to Europe with Shah Deniz in Azerbaijan

- Potential exports phase 2 exceeding 16 bcm/yr

- MoU between Turkey and Azerbaijan represents

a major step forward for the Shah Deniz project

- Statoil’s ownership share 25.5 per cent

- 8 bcm/yr gas export from Shah Deniz phase 1

- Gas sales to Turkey, Georgia and Azerbaijan

Shah Deniz phase 2 –possible new gas corridor to the European market

Shah Deniz – one of Statoil’s most important international gas fields

Italy Greece interconnector (IGI)

NabuccoTrans Adriatic Pipeline (TAP)

Transit pipelinesSouth Caucasus pipeline (SCP)

8

US shale gas production

Gas prices (øre/Sm3)

Gas prices are not low in a historical context

Main drivers in the gas market (bcm)

Gas demand (EU27)

531

565

2008 2009

565

531

2008 2009

LNG supply capacity

268

232

2008 2009

268

232

2008 2009

268

232

2008 2009

63

88

2008 2009

0

100

200

300

2000

2001

2002

2003

2005

2006

2007

2008

2010

2011

2012

2013

2015

NBP HH German border Japan Average

Market’s expectation

Sources: BMWi, Heren, Platts, CERA

9

Robust long term growth in gas demand

Domestic supplies

US (bcm) Europe (bcm) Asia (bcm)

Imports Upside potential

Source: Statoil internal

0

200

400

600

800

1000

2010 2020 2030

0

200

400

600

800

1000

2010 2020 2030

0

200

400

600

800

1000

2010 2020 2030

10

Natural gas – a fuel for the future

Most cost competitive fuel

Available now when old capacity need to be replaced

Source: CERA and Platts

Conclude new sales

Europe

Older than 40 yrs

31 – 40 yrs

21 – 30 yrs

11 – 20 yrs

0 – 10 yrs

New capacity

Source: IEA world energy outlook 2009

$10/MMbtu$11/MMbtu

$15/MMbtu

Old coal plant

emissions

New coal plant

reductions

Gas switch

reduction

Reduce CO2 emissions by 70% compared to old coal-fired plants

New CCGT

emissions

Source: Deutsche Bank

11

The shale gas revolution has increased global gas resources

Source: IEA World Energy Outlook 2009

Global gas resources 2008 (TCM)

Unconventional gas resourcesConventional gas resources

210

OECD

200

Rest of the world

200

Russia / FSU

170

Middle East

12

Summary

− Statoil has a unique gas business

− Natural gas is a fuel for the future: low carbon footprint, cost competitive and

abundant resources

− Statoil has a positive market view going forward

− Window of opportunity to increase the role of gas in the fuel mix for power

generation

Related Documents