Presented to: Institute for Supply Management – Utah Chapter January 12th , 2012 Presented by: Scott Merrill Supply Chain Management: Competitive Advantage

Presented to: Institute for Supply Management – Utah Chapter January 12th, 2012 Presented by: Scott Merrill Supply Chain Management: Competitive Advantage.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presented to: Institute for Supply Management – Utah Chapter

January 12th , 2012Presented by: Scott Merrill

Supply Chain Management:Competitive Advantage

Institute for Supply Management Mission Statement:

ISM-Utah serves as a center of excellence in the development of supply chain management, through three main points:

1.To provide education, certification, and leadership for supply management

2.To expand networking opportunities of supply management

3.To ensure the necessary resources to support this mission

Institute for Supply Management:Objective:

• The objectives of this Association are to foster and promote friendly relations between its members, that they may benefit by the resulting interchange of ideas; to study, develop and encourage more efficient purchasing and supply chain methods; to circulate information that may be of interest or benefit to members, that they may become more familiar with fundamental marketing, producing and manufacturing practices, various products and their use, and dependable source of supply

Business Strategy: Overview

• Business Strategy: Categories– Strategic Analysis: An evaluation of how/where your business is

going

– Strategic Choice: How are you meeting the needs of customers, shareholders, etc.

– Strategic Implementation: Action plans of business improvement and execution

Source: the-business-plan.com/what-is-business-strategy.html

Business Strategy: Definition

• Business strategy is essentially an ongoing process of evaluating how successful an organization is and how it can improve on that success.

Source: the-business-plan.com/what-is-business-strategy.html

• Supply Chains are Certainly not Exempt!– The critical nature of Supply Chains demand buy-in from all

organizational departments in order to experience the most efficient processes and lowest operational expenses

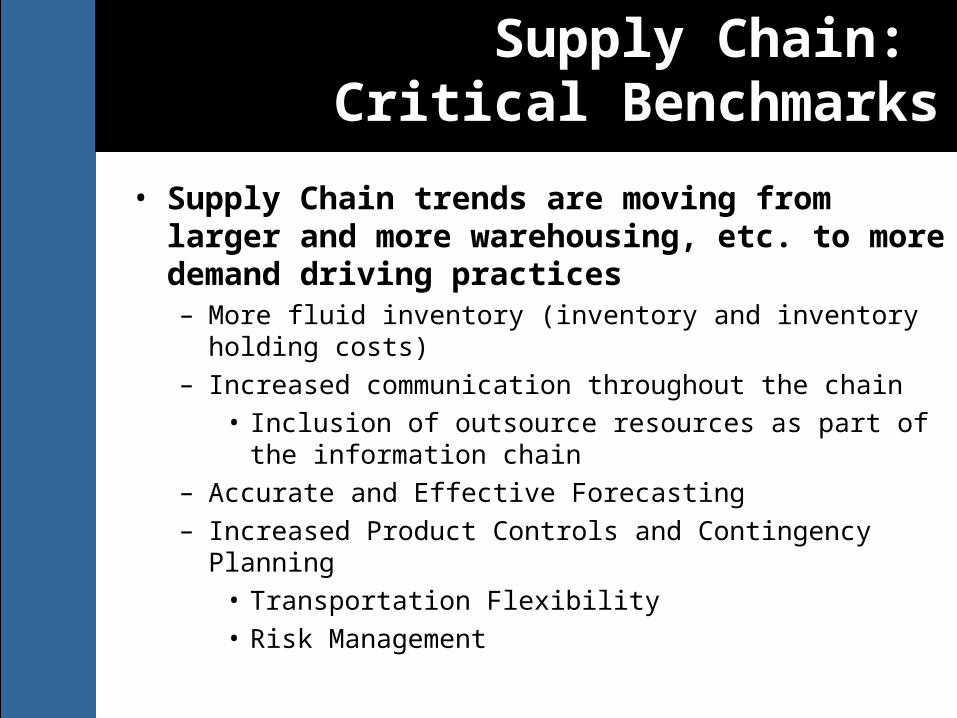

Supply Chain: Critical Benchmarks

• Supply Chain trends are moving from larger and more warehousing, etc. to more demand driving practices– More fluid inventory (inventory and inventory holding costs)

– Increased communication throughout the chain

• Inclusion of outsource resources as part of the information chain

– Accurate and Effective Forecasting

– Increased Product Controls and Contingency Planning

• Transportation Flexibility

• Risk Management

Supply Chain: Critical Change Agents

• Demand Planning

• Globalization

• Increased Competitive and Price Pressure

• Outsourcing

• Shortened and more Complex Product Life Cycles

• Collaboration between Stakeholders

Gross Domestic Product

• Moderate GDP grow for the foreseeable futureChallenges:–Erratic inventory de-stocking and re-stocking practices

• Rapid response to meet demand, Controlled resources to avoid obsolescence

Growth Areas–Non residential fixed investment, equipment and software, export of goods and services

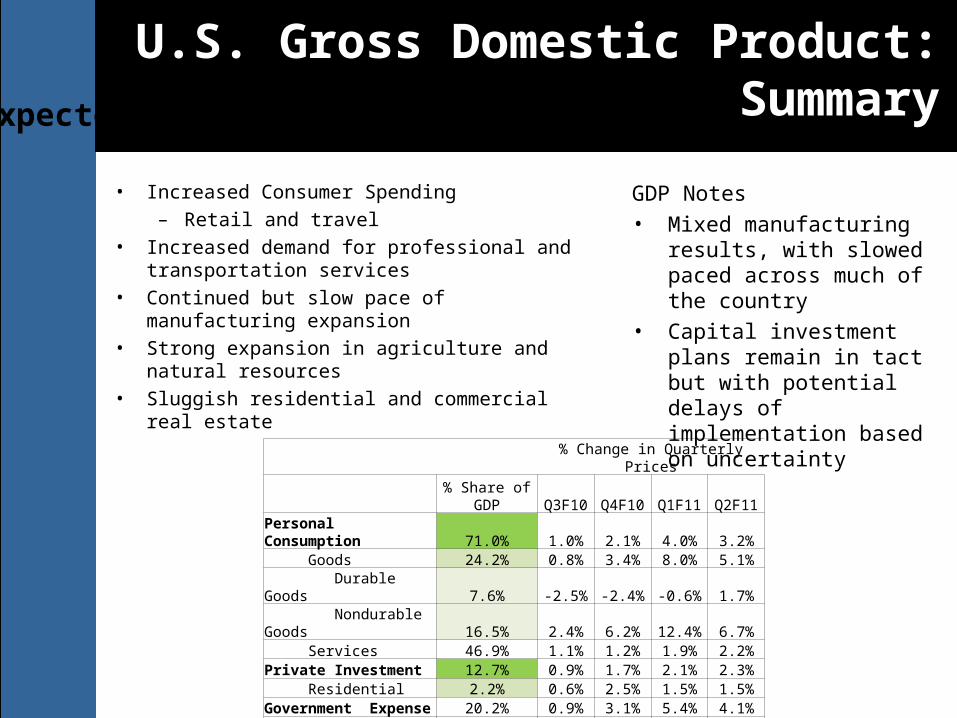

U.S. Gross Domestic Product:Summary

• Increased Consumer Spending– Retail and travel

• Increased demand for professional and transportation services

• Continued but slow pace of manufacturing expansion

• Strong expansion in agriculture and natural resources

• Sluggish residential and commercial real estate

Expected GDP growth rate below 2%

GDP Notes• Mixed manufacturing

results, with slowed paced across much of the country

• Capital investment plans remain in tact but with potential delays of implementation based on uncertainty

% Change in Quarterly Prices

% Share of GDP Q3F10 Q4F10 Q1F11 Q2F11Personal Consumption 71.0% 1.0% 2.1% 4.0% 3.2% Goods 24.2% 0.8% 3.4% 8.0% 5.1% Durable Goods 7.6% -2.5% -2.4% -0.6% 1.7% Nondurable Goods 16.5% 2.4% 6.2% 12.4% 6.7% Services 46.9% 1.1% 1.2% 1.9% 2.2%Private Investment 12.7% 0.9% 1.7% 2.1% 2.3% Residential 2.2% 0.6% 2.5% 1.5% 1.5%Government Expense 20.2% 0.9% 3.1% 5.4% 4.1%Export and Imports -3.9%

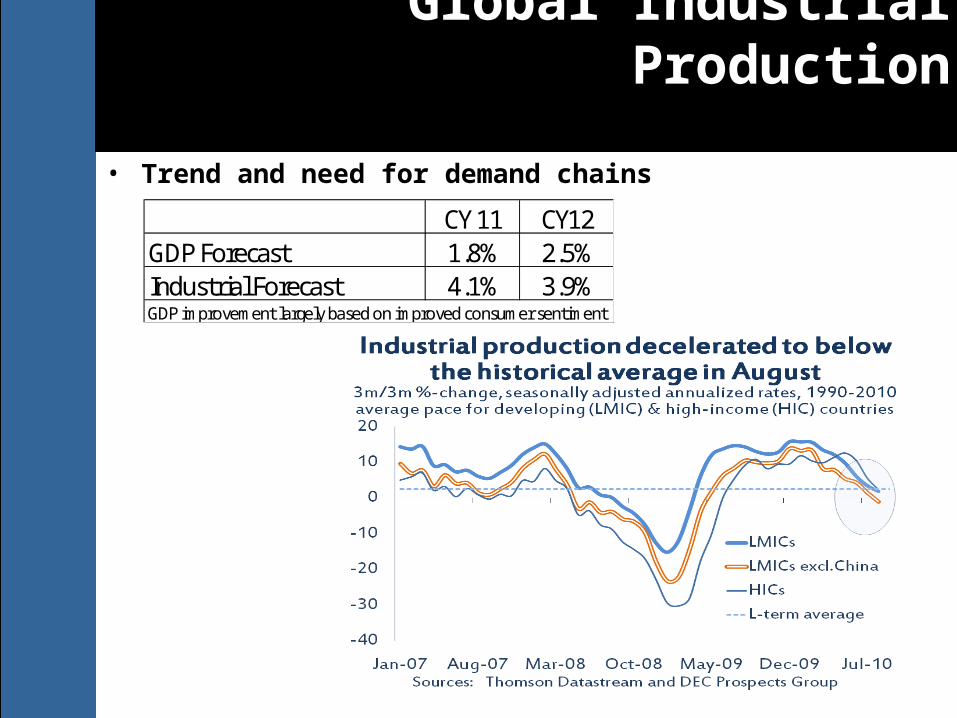

Global Industrial Production

• Trend and need for demand chains

CY 11 CY12GDP Forecast 1.8% 2.5%Industrial Forecast 4.1% 3.9%GDP improvement largely based on improved consumer sentiment

Supply Chain: Improvement Strategies

With Greater Commoditization, Companies are Looking for Improvement in at Least Two Ways:

•#1 Reduce Cost, and Create Greater Efficiency– Sales and Operational Costs

– Transportation Cost Management

– Improve Product Life Cycle

– Improve Sourcing

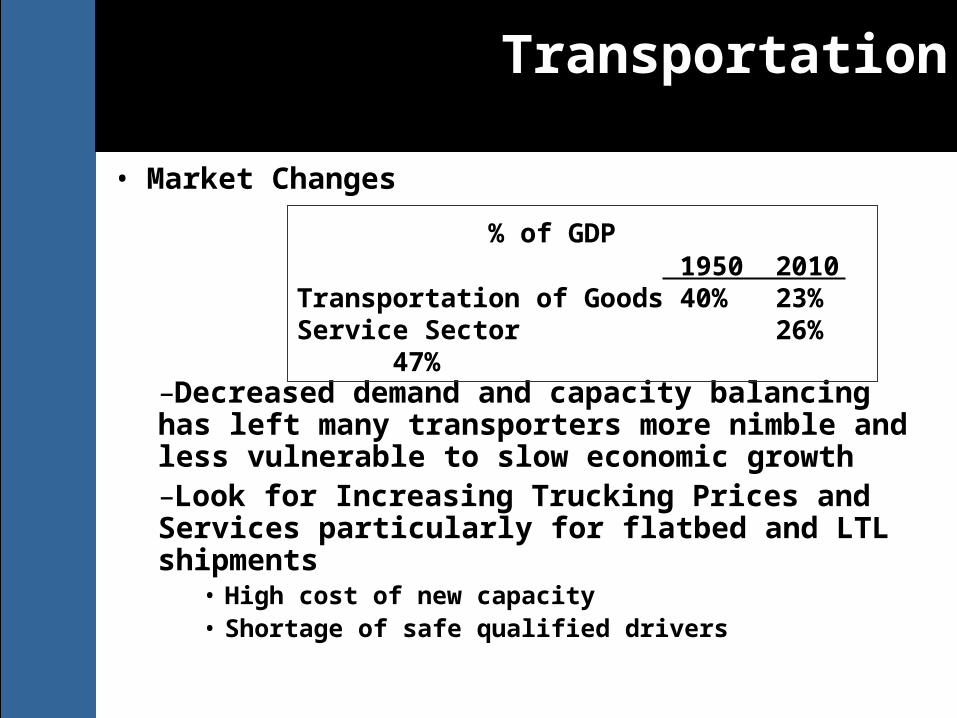

Transportation

• Market Changes

–Decreased demand and capacity balancing has left many transporters more nimble and less vulnerable to slow economic growth–Look for Increasing Trucking Prices and Services particularly for flatbed and LTL shipments

• High cost of new capacity• Shortage of safe qualified drivers

% of GDP1950 2010

Transportation of Goods 40% 23%Service Sector 26% 47%

Supply Chain: Improvement Strategies

With Greater Commoditization, companies are looking for improvement in at least two ways:

•#2 Provide Value-Added Services– Vendor Management Inventory

– Labeling and Packaging Services i.e. Commodity Codes, Global Requirements

– Drop Shipment

– Visibility

•Both Value Strategies can be Supported through a Return on Asset Model

Supply Chain: Improved Visibility

“Better visibility of retailer product availability can reduce overall logistics costs as products move through the value chain to fulfill stock levels and ultimately consumer demand.”

Hitachi Consulting

•Does your Chain create Customer Advantage?– Increased Visibility:

• Increases customer loyalty while meeting expectations

• Decreases operational costs particularly staffing

• Reduces payment time cycle

• Increase channel strength

Create Customer Advantage

Consumer Confidence

• “Worries over making ends meet and the persistently high unemployment rate have weighed on confidence in recent months. . .”

– Copyright, “The Financial Times Limited 2011, Susan Bond

• Consumers are looking for a decent decrease in unemployment

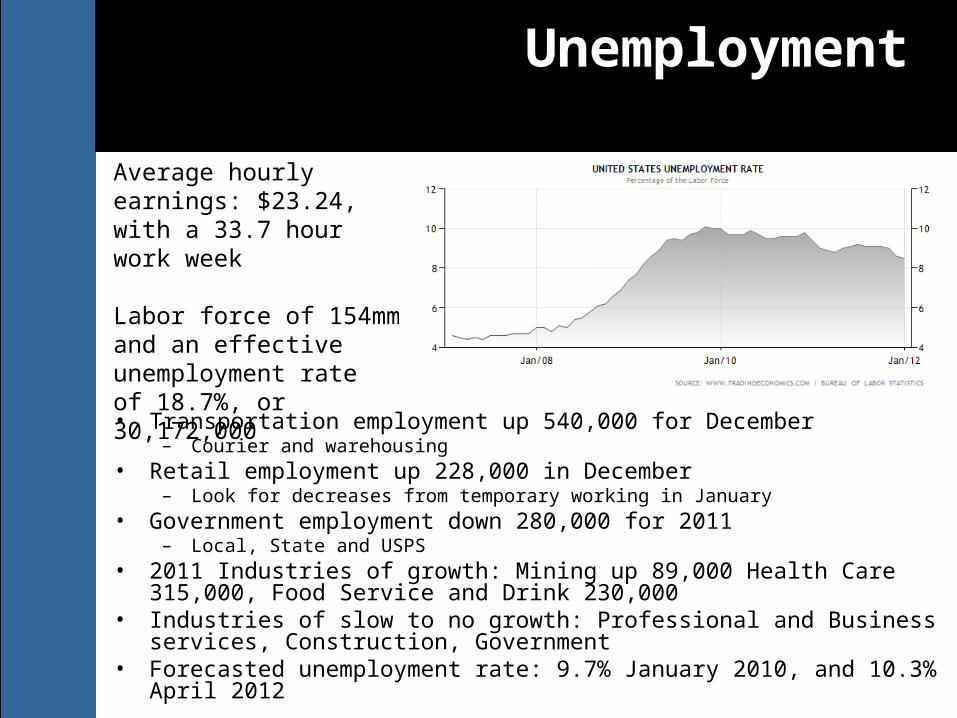

Unemployment:

Positives•200,000 new jobs in December•Unemployment rate of 8.5%

Challenges•5.6mm individuals out of work at least 6 months•3.9mm individuals for a year or more

– Job loss with >8% unemployment = loss of 2.8 years pre-job wages

– Skill deterioration, motivation denigration, negative stigma– Productivity, public finance and social behavior concerns

•Long term decreases in manufacturing jobs, and subsequent fall out of the housing market

Unemployment

• Transportation employment up 540,000 for December– Courier and warehousing

• Retail employment up 228,000 in December– Look for decreases from temporary working in January

• Government employment down 280,000 for 2011– Local, State and USPS

• 2011 Industries of growth: Mining up 89,000 Health Care 315,000, Food Service and Drink 230,000

• Industries of slow to no growth: Professional and Business services, Construction, Government

• Forecasted unemployment rate: 9.7% January 2010, and 10.3% April 2012

Average hourly earnings: $23.24, with a 33.7 hour work week

Labor force of 154mm and an effective unemployment rate of 18.7%, or 30,172,000

Inflation

• 12 Month trends:• Food Up, Energy Down, and all other indexes up• Overall upward inflation trend

• Soft employment, low-to-no upward wage pressure, lost housing equity and related consumer “poor complex” – not a good time for price increases

Current rate of 3.4%

Federal Reserve “desirable rate” is 2%

Short-Term Interest Rates

• Near Zero rates continue through min 2013, or as long as the economy remains weak

• Cash flush banks, financial organizations and corporations press for higher returns with greater risks

• Consumers appear to “hold” on a general scale– Americans overwhelmingly expect to delay by at least 2 months major

purchases and expenditures such as spending on new cars, home repairs, and vacations: Source, Alix Partners, June 3, 2011

HousingSource: WSJ Wednesday 9/21/11

Actual :• Prices have fallen 31.6% since the peak of 2005 equating to $7 Trillion

in lost home equity

• Bank owner foreclosure has restricted new construction and as a by-product, related employment and wages

• I in 5 mortgagees owes more than their home is worth

• Homeowner equity as a percent of home value has fallen to 38.6% from 58.7% in 2005

• Reverse wealth effect: homeowners feel poorer so they reduce consumer spending, the largest GDP component

HousingSource: WSJ Wednesday 9/21/11

Forecast:•Home prices expected to drop 2.5% this year

•Expected average annual increase of 1.1% through 2015

•Reduced Home improvements

– Cash vs. home equity payments

– Lack of confidence that improvements will pay off

Result:•Lost decade with a fraction of increase against large losses – erasing most or all home equity for millions of homeowners

•Depressed housing prices for years

•More than 4 million loan in foreclosure or considered seriously delinquent

•Years to recovery, continued falling prices, eroding equity, the “poor man complex”

Federal Reserve: Stimulus

• Perspective of the Fed– Take further steps as necessary– “Don’t cut spending too quickly . . . to trim the deficit in the long-term.” – European financial strains posed “ongoing risks” to U.S. economic growth– Depressed housing and tight household budgets are factors preventing robust

expansion– Continued sluggish job growth– Little inflationary impact/risk

• Based on the Above– December 13th meeting to leave credit policy unchanged, vote 9:1– Continue monetary easing strategy: operation twist

• Twisting long and short term interest rates closer together• To increase credit and liquidity

• Problem– Lack of demand and confidence, not credit and liquidity– Credit hurdles too high

Federal Reserve: CreditMonetary Policy

• Stimulus:– Quantitative Easing

– Operation Twist

– Remember Quantitative Easing - QE2.• A monetary policy to increase the money supply when interest rates are near 0%.

• Intended to increase loans and spending because of increased liquidity

• The only measurement of success is that things are not as they could have been???

• Actual result; increased cash, stagnant circulation, and future stimulus recoil

• It’s all about employment and wages

• Government debt– Critical action items, No clear course, no one wants to pay the price

• Confidence???

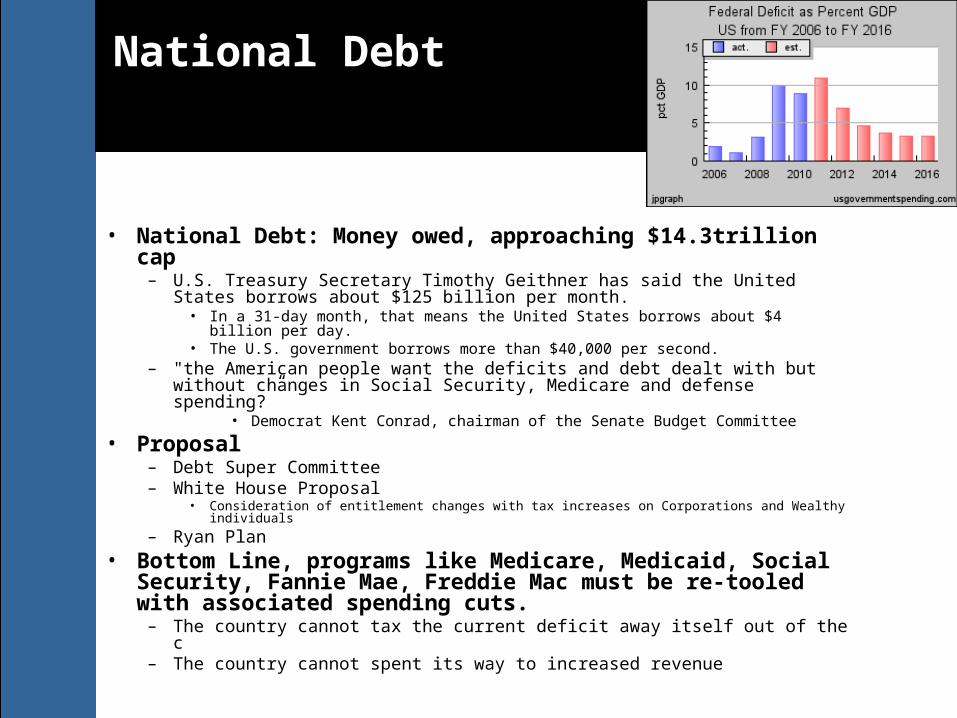

National DebtNational Debt

• National Debt: Money owed, approaching $14.3trillion cap– U.S. Treasury Secretary Timothy Geithner has said the United States

borrows about $125 billion per month.• In a 31-day month, that means the United States borrows about $4 billion per day.• The U.S. government borrows more than $40,000 per second.

– "the American people want the deficits and debt dealt with but without changes in Social Security, Medicare and defense spending?”

• Democrat Kent Conrad, chairman of the Senate Budget Committee

• Proposal– Debt Super Committee– White House Proposal

• Consideration of entitlement changes with tax increases on Corporations and Wealthy individuals

– Ryan Plan

• Bottom Line, programs like Medicare, Medicaid, Social Security, Fannie Mae, Freddie Mac must be re-tooled with associated spending cuts.

– The country cannot tax the current deficit away itself out of the c– The country cannot spent its way to increased revenue

Market Efficiency Theory: Your Supply Chain

• All relevant Information is Available, Considered and “Built-in”

• Likewise, Efficient Supply Chain practices Must Incorporate all Relevant Information in Process

• Efficient Processes Must be Build on:– Information, Open Markets and To/From Market Connectivity

in order to Fundamentally Provide Value– Value is Demonstrated by Quantification

• In Terms of Dollars, what Customer Value does Your Supply Create?

Supply Chain Model:Consideration

• What Are Your Supply Chain Threats?– Accurate: Does your Supply Chain Reflect Your History or

Strategy?• Case Study, Apple Ipod

– Does Your Supply Chain Create Added Custer Value?– Process: Does your Supply Chain Provide Customer Value

by Accomplishing a Customer Based Task?• Flexible: Demand Fluctuation

– Customer, Economics, or Competitive Based• Simplify

– Use Innovation to Reduce Rather Than Complicate Processes - Buried in Systems and Processes

Access - Defined

• Access is a process that enables interaction, contacts and exchanges . . Access indicates Ability

• Access is a Measure of Openness, not Competitiveness • A = F (T, S, I)• A Supply Chain that Generates Access Collapses Time and

Space while Increasing Information, Thereby Conferring Value to its Customers - Visibility

Access – Core CompetencyAccess – Core Competency

• Value Benefits to the Access Generation:– Provides Connection - Individual and Market– Expands Reach, Innovation and Profitability– Offers Increased Choice of What, Where, When and How

• Concluding Questions:– What Markets do you Provide Access To?– What Connections Should you Add?– What Quantifiable Value does your Chain Provide?

Related Documents