Presented by Jason Cheng-Hsien Tsai Professor, Dept. of Risk Management and Insurance Director, Risk and Insurance Research Center National Cheng-Chi University

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presented by Jason Cheng-Hsien Tsai

Professor, Dept. of Risk Management and Insurance

Director, Risk and Insurance Research Center

National Cheng-Chi University

Motivation of Part I

Raise the awareness of Taiwan government

officers about how insurance may mitigate the

damages resulted from typhoons on Taiwan and

its public finances

Implementation

Use simulation analyses to demonstrate how

Taiwan and its public finances would be under the

typhoon risks without and with insurance

Threats of Typhoon Risks on Public

Finances: Analysis Structure Model the dynamics of the typhoon risk losses and

government losses of Taiwan

A Typhoon risk model

Impose hypothetical risk management schemes:

proportion; excess of loss; excess of loss with upper

limits

This framework is in line with the nascent literature that

incorporates the structure of random shocks hitting the

domestic economy to obtain a complete distribution of

probable outcomes for the CAT risk losses, rather than

simply projecting one central scenario.

Modeling Methodologies

Original Intention

Modeling typhoon frequencies first and then

building models upon rainfall, wind speed,

and affecting duration to project severities

This did not work, however.

An Alternative Way

Modeling types of losses resulted from

typhoons directly

Data-Driven Modeling

When long-term data are available, we fit the data with

various statistic distributions using MLE and choose one of

them according to the K-S fitness measure and p-value

Casualties

House Collapses

Agricultural Losses

For the losses that have only short-term data available, we

build regression models upon the above three types of

losses

Transportation Infrastructure Losses

Aqueduct Infrastructure Losses

A Glimpse on the Data

Year CPI

Casualties House Collapses Other Loses (in 1,000 NTD)

Wounded Death & Missing Total and Partial

Losses Agriculture Railway

2,009 1.00 1,557 701 349

2,008 0.99 100 42 83 17,738,667 NA

2,007 1.02 148 16 89 14,117,900 NA

2,006 1.04 6 3 15 1,734,539 NA

2,005 1.05 145 23 169 16,633,380 NA

2,004 1.07 504 49 386 12,045,068 NA

2,003 1.09 5 7 - 3,417,647 NA

2,002 1.09 12 6 - 244,987 NA

2,001 1.09 585 354 2,624 15,819,419 1,144,949

2,000 1.09 178 110 2,159 13,087,291 514,078

Casualties and House Collapses

Data Source: National Fire Agency

Data Duration:1958 ~

Chosen Models:

Generalized Pareto Distribution for Death &

Missing and Wounded

Burr Distribution for House Collapses

Agriculture Loses

Data Source: Agricultural Statistics

Yearbook

Data Duration:1961 ~

Loss Descriptions:

Product losses (including crops, livestock ,

fishery, forestry) and facility losses

Chosen Model:

Generalized Pareto

Transportation Infrastructure Losses

Data Source:

Statistical Report of Taiwan Railways Administration

Statistical Abstract of Transportation and

Communications

Data Duration:

From 1975 to 2001 (Statistical Report)

From 1982 to 2008 (Statistical Abstract)

Regression Model:

Railway Loss = (Death & Missing)*3,133 + 7,250,816

Trans. Inf. Loss = (Railway Loss)*5.978 + 10,601

Aqueduct Infrastructure Losses

Data Source: Water Resource Agency

Data Duration:2001 ~

Facility Descriptions :

Reservoir and Flood Control Facilities

Model:

Aqu. Inf. Loss = (Death & Missing)*25,733 +

Agr. Loss * 0.2523 + 290,850,563

Estimating Public Finance Losses

Death:200,000 NTD

Severe Injury:100,000 NTD

Re-Settlement:20,000 NTD/person; Max. 5

persons / family

Agriculture Subsidy: loss amount

12

Estimating Total Economic Losses

Death:900,000 NTD by the average sum

assured of life insurance in 2008

Injury:6,952 NTD by the average sum

assured of accident and health insurance

House Collapses :4,120,000 NTD / house

(=34.62 pin * 11,921 NTD/pin)

13

Simulation Results

Loss Min. 1st. Qu. Median Mean 3rd. Qu. Max. Std.

Death & Missing Sample 0 13 48 83 100 701 120

Gen. Pareto 0 18 46 87 104 3,670 134

Wounded Sample 0 19 47 247 344 2,055 427

Gen. Pareto 0 49 130 305 311 31,864 813

House Collapse Sample 0 54 864 6,598 3,524 41,057 11,856

Burr 0 175 1,227 7,938 6,126 666,816 23,786

Agriculture Sample 0 1,439,564 3,104,795 5,567,781 7,158,794 23,582,067 6,046,317

Gen. Pareto 510 1,863,861 4,483,056 6,967,801 9,233,682 97,995,040 7,793,143

Railway Sample 0 18,763 64,605 176,107 219,707 1,144,949 259,875

Regression 7,519 71,467 173,306 320,075 381,419 14,286,401 486,846

Transportation Proportion 75,195 714,667 1,733,059 3,200,746 3,814,190 142,864,013 4,868,462

Death & Missing

0

100

200

300

400

500

600

700

1958 1968 1978 1988 1998 2008 2018

Historical Data

80% Possibility(Lower

Bound)

80% Possibility(Upper

Bound)

Mean

Wounded

0

500

1000

1500

2000

1958 1968 1978 1988 1998 2008 2018

Historical Data

80% Possibility(Lower

Bound)80% Possibility(Upper

Bound)Mean

House Collapses

0

5000

10000

15000

20000

25000

30000

35000

40000

1958 1968 1978 1988 1998 2008 2018

"Historical Data"

"80% Possibility(Lower Bound)

"80% Possibility(Upper Bound)

"Mean"

Agriculture Losses

0.00E+00

5.00E+06

1.00E+07

1.50E+07

2.00E+07

2.50E+07

1961 1971 1981 1991 2001 2011 2021

Historical Data

80% Possibility(Lower Bound)

80%Possibility(Upper Bound)

Mean

Transportation Infrastructure Losses

1

2,000,001

4,000,001

6,000,001

8,000,001

10,000,001

12,000,001

1992 1997 2002 2007 2012 2017 2022

Historical Date

80% Possibility(Lower Bound)

80% Possibility(Upper Bound)

mean

Insurance Schemes

Proportional Insurance

Government retain 30% of losses; insurers pay

70%

Proportional with Deductible

Public Finance Losses: 1,200 million NTD

Economic Losses: 50,000 million NTD

20

Simulation Settings

15 years, 50,000 scenarios

Inflation rate: 2% annually

21

Simulated Public Finance Losses (billion NTD)

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Uninsured 10%

Uninsured Mean

Uninsured 99%

Proportion 10%

Proportion Mean

Proportion 99%

Deductible 10%

Deductible Mean

Deductible 99%

22

Public Finance losses w.r.t. the annual

budget of the central government

0.0000%

0.1000%

0.2000%

0.3000%

0.4000%

0.5000%

0.6000%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Uninsured 10%

Uninsured Mean

Uninsured 99%

Proportion 10%

Proportion Mean

Proportion 99%

Deductible 10%

Deductible Mean

Deductible 99%

23

Individual Types of Losses

Death

1%

Severe Injury

1%

Re-Settlement

37%

Agriculture

Subsidy

61%

24

Simulated Economic Losses (billion NTD)

0

1,000

2,000

3,000

4,000

5,000

6,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Uninsured 10%

Uninsured Mean

Uninsured 99%

Proportion 10%

Proportion Mean

Proportion 99%

Deductible 10%

Deductible Mean

Deductible 99%

25

Economic losses w.r.t. the annual

budget of the central government

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Uninsured 10%

Uninsured Mean

Uninsured 99%

Proportion 10%

Proportion Mean

Proportion 99%

Deductible 10%

Deductible Mean

Deductible 99%

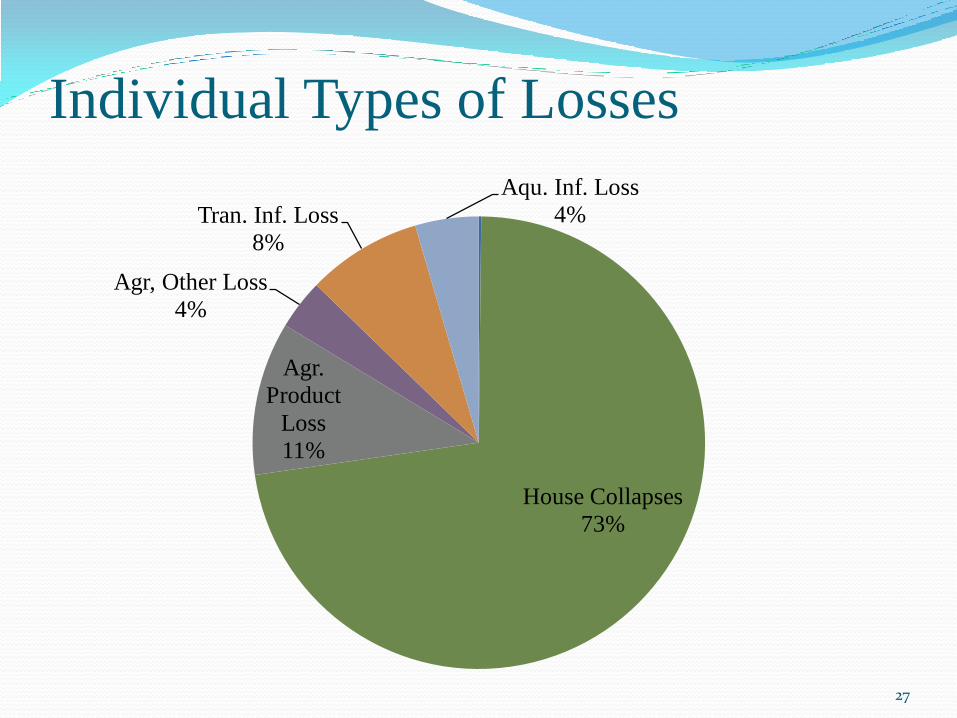

26

Individual Types of Losses

House Collapses

73%

Agr.

Product

Loss

11%

Agr, Other Loss

4%

Tran. Inf. Loss

8%

Aqu. Inf. Loss

4%

27

Motivation of Part II

Using empirical data to examine the typhoon

related risks of government buildings and

estimate the benefits of alternative insurance

schemes

Estimate the risks of total government

properties and study the benefits of employing

the risk management scheme similar to that of

Taiwan Residential Earthquake Insurance Fund

(TREIF)

28

Data and Simulation Estimate the area size used by governments: 350

billion square meters

Assume that the exposures of government

building contents are 5,000 NTD (including

content losses and cleansing costs)

Insurance Premiums

150% * Expected Nominal Losses

The average inflation rate (WPI) in the past 15

years was 1.7%.

29

Insurance Schemes

Proportional Insurance

30% of retention; premiums are about 1.3 billion NTD

Insurance with Deductible of 0.45 billion NTD

Insurance with both deductible and payment limit

Deductible: 0.41 billion NTD; payment limit: 8 billion

NTD according to the 99 percentile of simulated losses

30

Simulation Results of Government

Building Content Losses

0

10

20

30

40

50

60

70

80

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

單位

:億元

Uninsured mean

Uninsured 99%

Uninsured 10%

Proportion mean

Proportion 99%

Proportion 10%

Deductible mean

Deductible 99%

Deductible 10%

Cap & Deductible mean

Cap & Deductible 99%

Cap & Deductible 10%

31

Estimate the total losses of

government properties

Using the ratio of government building content

losses to total losses of government properties

resulted from Typhoon Morakot to estimate the

total losses

32

Risk Management Scheme

Layer 2 (28 billion NTD)

Layer 1

(5 billion NTD) Flood Insurance Fund

Central Government (6.5 billion NTD)

Flood Insurance Fund (7.5 billion NTD)

Reinsurers and/or Capital Markets (9 billion NTD)

Local Insurers (5 billion NTD)

33

Simulation Results

-

100

200

300

400

500

600

700

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

單位

:億元

Uninsured mean

Uninsured 99%

Uninsured 10%

Flood fund mean

Flood fund 99%

Flood fund 10%

34

Related Documents