April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin – Milwaukee

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 21, 2017

Presented by Dr. Rebecca Neumann

for Academic Staff

University of Wisconsin – Milwaukee

Mind your Money, Mind your Future� Goals for today:

� Basic money management skills� Tracking expenses

� Budgeting

� Saving

� Credit� Credit report and credit scores

� Establishing good credit

� Protecting your wealth (insurance)

� How do you make your money grow?� Retirement

� Investing for growth

2

Mind your Money, Mind your Future

� What is financial freedom?

� Being rich?

� Not worrying about money?

� Being able to buy anything you want?

3

Mind your Money, Mind your Future

� Financial freedom

� Ensuring that your net inflows are greater than your net outflows

� This allows you to save and buy what you want.

� Requires making choices!

4

The Role of Budgeting in Your Financial Plan

� What is a budget?

� Plan for income and expenditures!

� The key budgeting decisions for building your financial plan are related to cash flow planning.

� How can I improve my net cash flows in the near future?

� How can I improve my net cash flows in the distant future?

6

Creating a BudgetCash Inflows

� Earned income

� Savings

� Gifts or other

� Note: Gross versus Net income

Cash Outflows

� Rent/Mortgage

� Debt (school, car)

� Fixed Expenses

� Variable Expenses

� Note: fixed versus variable expenses

7

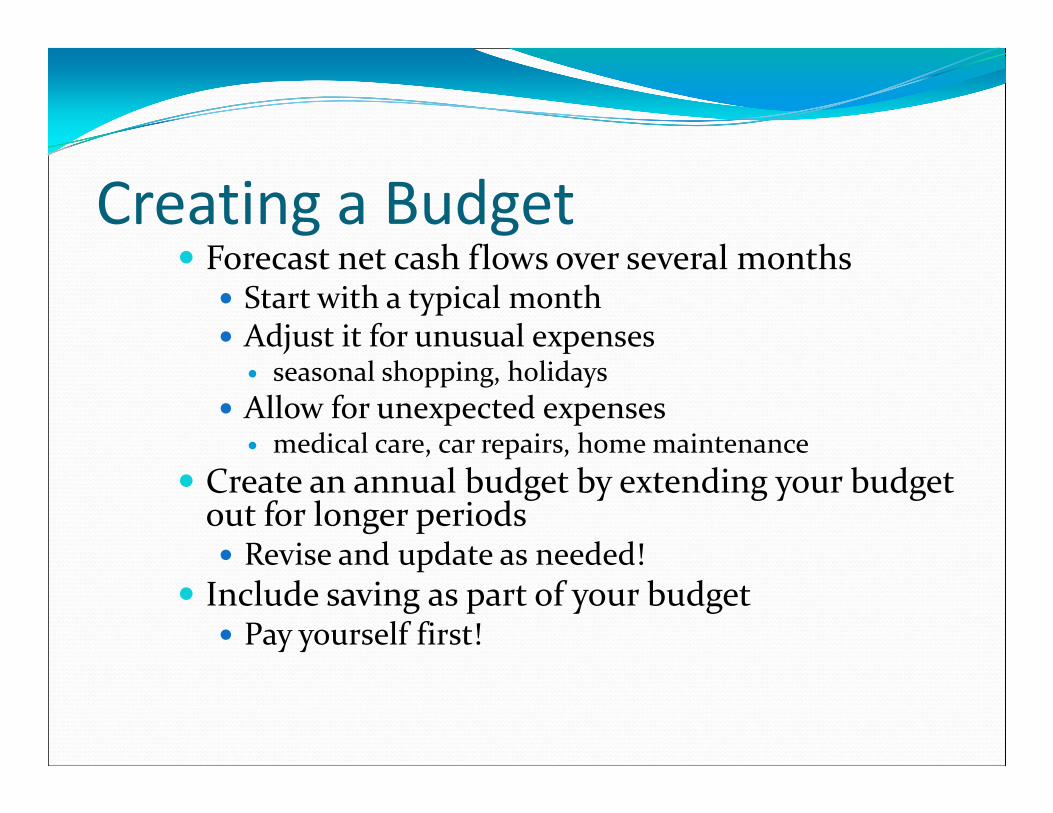

Creating a Budget� Forecast net cash flows over several months

� Start with a typical month� Adjust it for unusual expenses

� seasonal shopping, holidays

� Allow for unexpected expenses� medical care, car repairs, home maintenance

� Create an annual budget by extending your budget out for longer periods� Revise and update as needed!

� Include saving as part of your budget� Pay yourself first!

Budget worksheet

9

May planned May actual June planned June actual July planned July actual

Cash Inflows

Income 1 wages

Income 2 wages/tips

Gifts

Interest, dividends

Alimony, child support

Government payments

Financial Aid

Other

Total Inflows 0 0 0 0 0 0

Cash Outflows

SAVINGS pay yourself first!

Emergency funds

Retirement

Mutual funds

College savings

Stocks and bonds

Fixed

rent or mortgage

electricity

cell phone

internet

cable

water/sewer

other utilities

insurance premiums

tuition, child care, etc

Debt payments

credit card 1

credit card 2

Auto loan

installment loan

Flexible

Groceries, food

food away from home

entertainment

travel

gifts

books

clothes

medical/dental

Total Outflows 0 0 0 0 0 0

Net Cash Flows 0 0 0 0 0 0

Saving� Tips for saving

� Set up a budget

� Pay yourself first

� Direct deposit

� Avoid check cashing stores and payday loans

� Save early – power of compounding

10

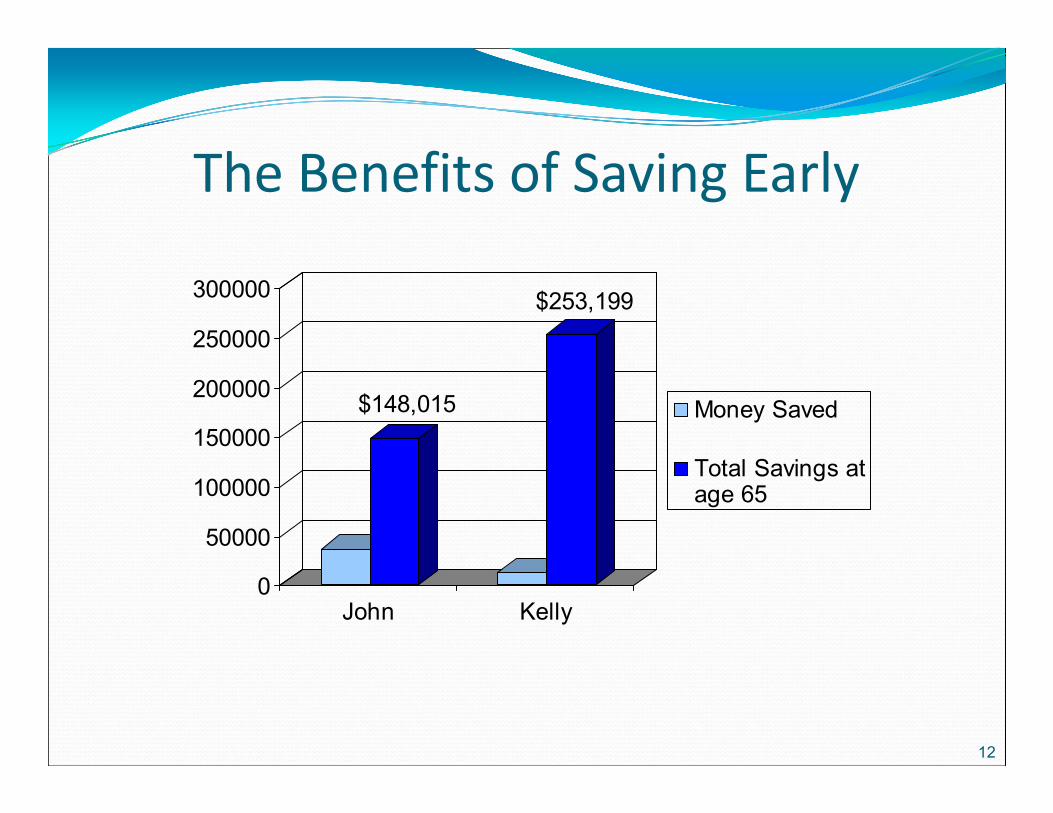

The Benefits of Saving EarlyKelly

� Starts at age 22� Saves $100 per month for 10 years ($12,000)

John � Starts at age 35� Saves $100 per month for 30 years ($36,000)

The interest rate is 8% compounded annually.

Who will have more money at age 65?

11

The Benefits of Saving Early

$148,015

$253,199

0

50000

100000

150000

200000

250000

300000

John Kelly

Money Saved

Total Savings atage 65

12

The Benefits of Saving Early

$148,015

$427,140

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00

400,000.00

450,000.00

John (started atage 35)

Kelly (started atage 22)

MoneySaved

TotalSavings atage 65

13

What if Kelly had continued to save $100 per month until retirement?

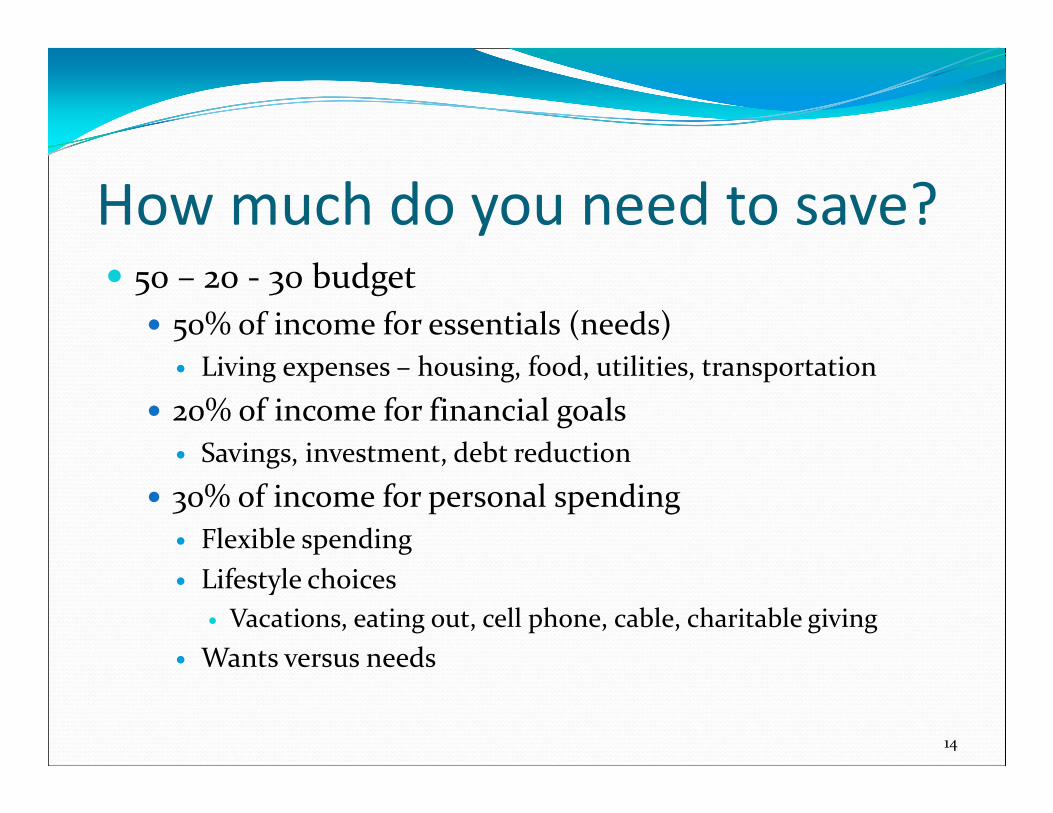

How much do you need to save?� 50 – 20 - 30 budget

� 50% of income for essentials (needs)

� Living expenses – housing, food, utilities, transportation

� 20% of income for financial goals

� Savings, investment, debt reduction

� 30% of income for personal spending

� Flexible spending

� Lifestyle choices

� Vacations, eating out, cell phone, cable, charitable giving

� Wants versus needs

14

Credit� What is it?

� Credit is money that is lent to you.

� You pay it back over time, with interest.

� Credit allows you to buy now and pay later.

� Your ability to get credit is based on your borrowing history.

15

Credit Cards – How they work

When you use a credit card it is like taking out a LOAN

from the issuer of the card.

Item Price APR

Min.Monthly Payment

(3% of Balance)

InterestPaid

How Much

You End Up

Paying

Total Years to Pay Off

TV $500 18% Start at $15 $198 $698 ?

Computer $1,000 18% Start at $30 $698 $1,698 ?

Furniture $2,500 18% Start at $75 $2,198 $4,698 ?13

8

4

Credit Cards – What they cost

17

If only the minimum payment is made:

This is how some people end up…

18

Credit Cards – What they costThe benefit to paying more than the minimum:

OriginalBalance

APRMonthly Payment

Total Years to Pay Off

Total of Payments

$2,500 18%3% of bal.

(start at $75)13 $4,698

$2,500 18% $100 2.5 $3,098

$2,500 18% $2,500 0 $2,500

Credit Card Tips

Avoid carrying a balance.

Don’t use your card for cash advances.

Think before you buy.

Debt Analysis� Not all debt is viewed the same

� Student loans

� Credit card debt

� Mortgages

� Car loans

� Ratios can help you calculate positions for different types of debt and/or different types of cash flow.

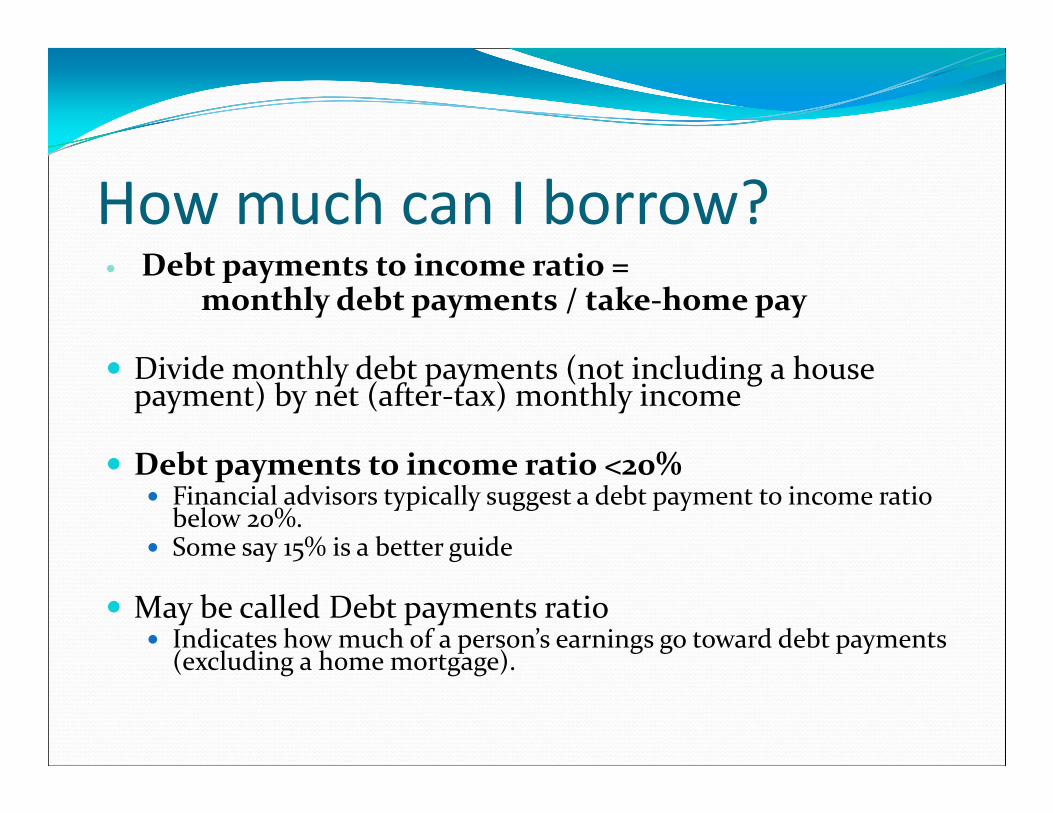

How much can I borrow?� Debt payments to income ratio =

monthly debt payments / take-home pay

� Divide monthly debt payments (not including a house payment) by net (after-tax) monthly income

� Debt payments to income ratio <20%� Financial advisors typically suggest a debt payment to income ratio

below 20%.� Some say 15% is a better guide

� May be called Debt payments ratio� Indicates how much of a person’s earnings go toward debt payments

(excluding a home mortgage).

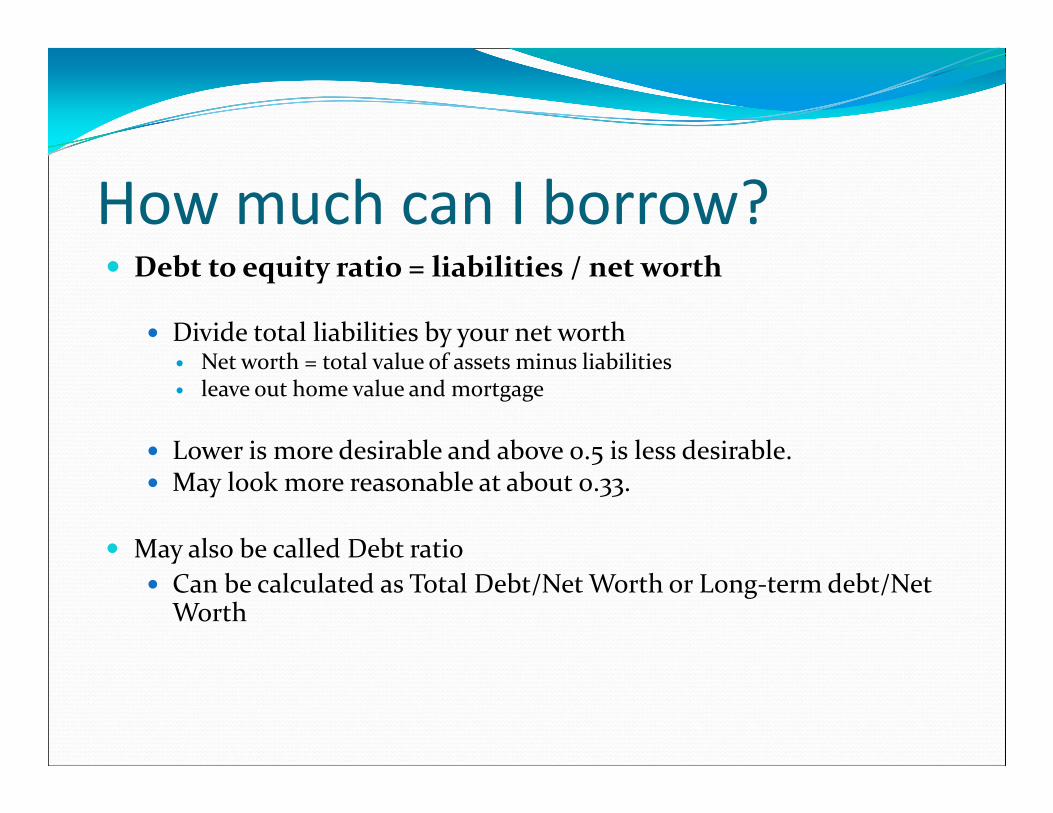

How much can I borrow?� Debt to equity ratio = liabilities / net worth

� Divide total liabilities by your net worth� Net worth = total value of assets minus liabilities� leave out home value and mortgage

� Lower is more desirable and above 0.5 is less desirable. � May look more reasonable at about 0.33.

� May also be called Debt ratio

� Can be calculated as Total Debt/Net Worth or Long-term debt/Net Worth

How much home can I afford?� Front End Ratio = 28%

(Principle + Interest + Taxes+ Insurance)Gross Monthly Income

� “PITI to income” or “housing expenses to income” or “annual income percentage” or “front end ratio”� Basically the total monthly cost of the house (PITI = principal, interest, taxes, and

insurance) relative to gross monthly income (before deductions),

� Back End Ratio = 36%(Principle + Interest+ Taxes+ Insurance + Other Debt Payments)

Gross Monthly Income

� “debt to income” or “debt ratio” or “total annual income debt percentage” or “back end ratio”� Basically all monthly debt payments relative to gross monthly income.

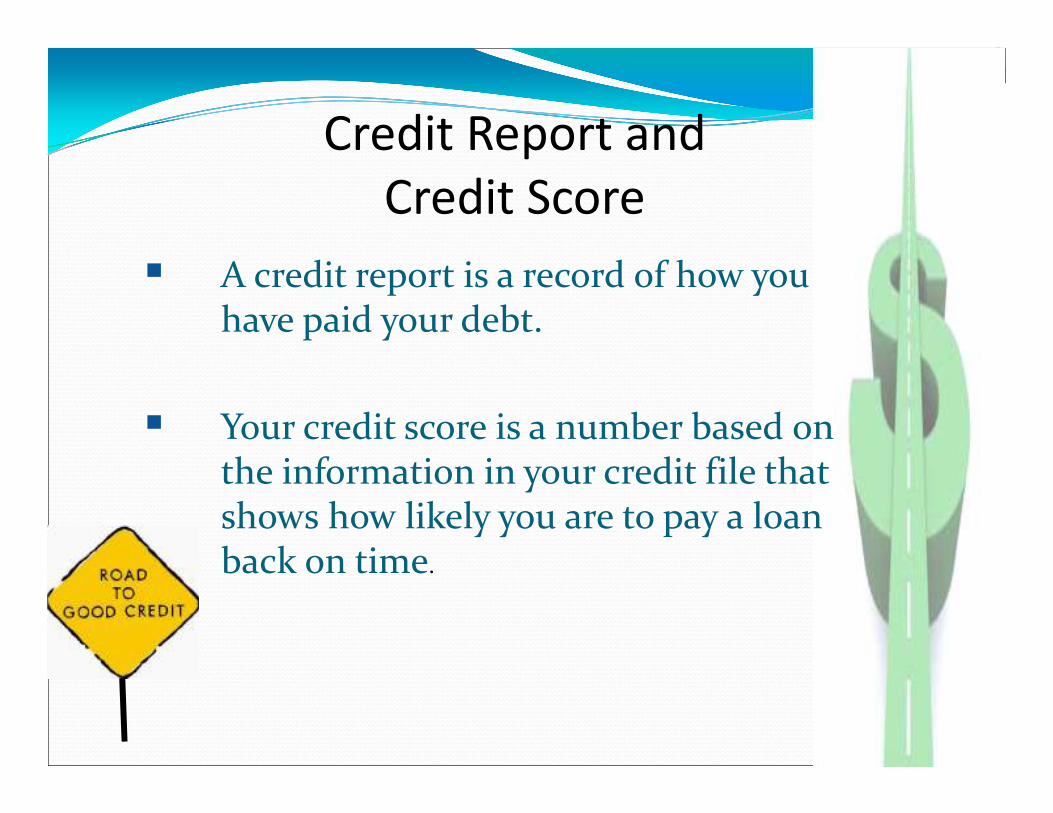

Credit Report and

Credit Score

� A credit report is a record of how you have paid your debt.

� Your credit score is a number based on the information in your credit file that shows how likely you are to pay a loan back on time.

Free Credit Report

www.annualcreditreport.com

� You will need some sort of history to verify. � Credit card or banking info.

� Previous addresses.

� 3 Credit Agencies –� Experian, Transunion, Equifax

� Credit report is free! (Credit score may not be).

What’s In Your Credit Report?

26

Amounts

Owed

Payment

History

Length of

Credit

History

New Credit

Types of

Credit Used

35%15%

10%

10%

30%

Credit score: FICO Score� Payment History 35%

� MOST IMPORTANT!!!!!!

� On time payments, Late payments, bankruptcy

� Amounts Owed 30%

� Proportion of credit line used (suggestions to use <30% of available)

� Number of accounts with balances, total amount owing on accounts

� Length of Credit History 15%

� How long you have been established with credit

� New Credit 10%

� How many applications/requests for credit have you submitted?

� Okay to shop around, but if you seem desperate, that is bad

� Types of Credit Used 10%

� It’s good to have more than one type of credit successfully used

What’s not in your credit score?

Your race, color, religion, national origin, sex and marital status

Your age

Your salary, occupation, title, employer, date employed or employment history

Where you live

Any interest rate being charged on a particular credit card or other account

Any items reported as child/family support obligations or rental agreements

28

29

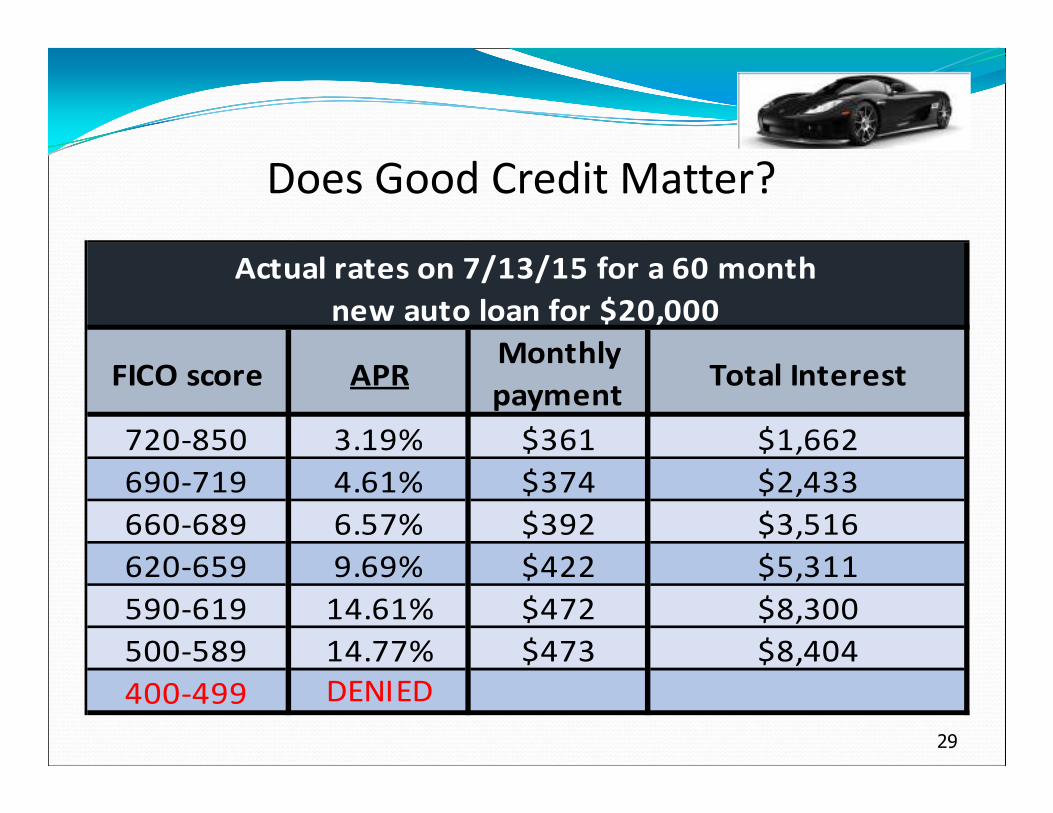

Does Good Credit Matter?

FICO score APRMonthly

paymentTotal Interest

720-850 3.19% $361 $1,662

690-719 4.61% $374 $2,433

660-689 6.57% $392 $3,516

620-659 9.69% $422 $5,311

590-619 14.61% $472 $8,300

500-589 14.77% $473 $8,404

400-499 DENIED

Actual rates on 7/13/15 for a 60 month

new auto loan for $20,000

30

Does Good Credit Matter?

FICO score APRMonthly

paymentTotal Interest

760-850 3.77% $697 $100,757

700-759 3.99% $716 $107,618

680-699 4.17% $713 $113,125

660-679 4.38% $750 $119,901

640-659 4.81% $788 $133,744

620-639 5.35% $838 $151,779

600-620 Denied

Actual rates on 7/13/15 for a 30-year

fixed rate mortgage for $150,000

What will Improve your Credit Report or Score?

� No quick fixes� Most measures are longitudinal

� Consider components of the credit score for possible actions� Consider their weightings� Consider how these are actually measured

What will Improve your Credit Report or Score?� Payment History Tips

� Pay your bills on time every month!� Get help with a debt repayment plan if you need it.

� Amounts Owed� Keep balances low on credit cards and other “revolving credit”.� Pay off debt; do not move it around. Moving it around will not help your score, and if you are taking out

new cards, it may actually hurt.

� Length of Credit History� Opening new accounts will hurt your length of credit history.� Closing unused accounts may impact your credit history – if you’ve had an account open for a while, then

that establishes a longer credit history.

� New Credit� Shop around

� Types of Credit� Apply for and open new credit accounts only as needed.� Having credit cards and installment loans (and making timely payments) will raise your score.� Someone with no credit cards tends to be higher risk than someone who has managed credit cards

responsibly.

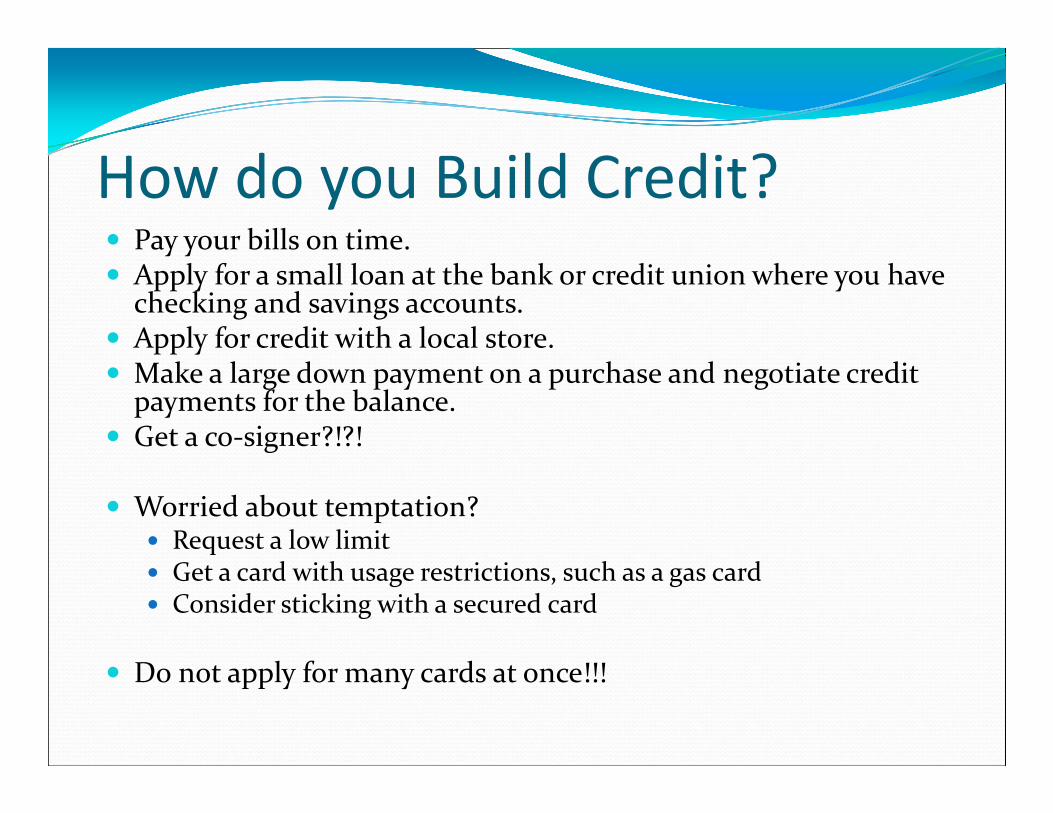

How do you Build Credit?� Pay your bills on time.� Apply for a small loan at the bank or credit union where you have

checking and savings accounts.� Apply for credit with a local store.� Make a large down payment on a purchase and negotiate credit

payments for the balance.� Get a co-signer?!?!

� Worried about temptation?� Request a low limit� Get a card with usage restrictions, such as a gas card� Consider sticking with a secured card

� Do not apply for many cards at once!!!

Important Things to Remember

� No quick fixes

� People who promise a quick fix� Usually some form of debt consolidation

� Does this help?

� Consider the FICO score

� It is important to request and check your own credit report at least once per year.

� If you are denied credit, you may request a free report within 60 days.

Protecting your wealth� Insurance

� Health

� Life

� Disability

� Renters or homeowners

� Automobile insurance

� Check university benefits website.� Remember to enroll spouse/domestic partner and/or

kids if there is a life change. � Check options when this first occurs!

35

How do you make your money grow?

� Savings

� Emergency funds

� For specific uses – travel, home loan deposit, car

� Savings, checking, money market, CDs

� Saving for the future (investing)

� Retirement funds

� Education

� Edvest

� Investment vehicles

� Stocks, bonds, mutual funds

36

What about retirement?� WRS (Wisconsin Retirement System)

� Supplemental� 403b or TSA (Tax-sheltered annuity)

� Wisconsin deferred compensation plan

� IRA, Roth IRA

What about retirement?� Wisconsin Retirement System (WRS):

� Automatically enrolled once eligible

� Work at least 2/3 of full time for one year.

� Employee contribution is 6.8%

� Employer contribution is 6.8%

� Vested after 5 years.

� Also provides disability, separation, and survivor benefits.

� Payout options – formula benefit or money purchase.

� https://www.wisconsin.edu/ohrwd/benefits/ret/

What about retirement?� 403(b) or TSA – tax sheltered annuity

� University’s version of a 401(k)� The funds can be invested in a variety of stocks, bonds,

mutual funds. You then get the earnings in retirement. � If there is a match, contribute at least up to the maximum

amount that your employer will match!� No match at the university.

� https://www.wisconsin.edu/ohrwd/benefits/ret/tsa/

� Wisconsin deferred compensation plan (WDC)� IRA (pre-tax $)� Roth IRA (taxed now but not at withdrawal)

� https://www.wisconsin.edu/ohrwd/benefits/ret/wdc/

Investment Vehicles� Once you’ve got emergency funds set up.

� And you’ve started contributing to retirement funds.

� What else do you use?

� Money Market

� CDs

� Stocks

� Bonds

� Mutual Funds

� Consider risk, return, duration, tax implications

Types of Saving/Investment Products

41

What is it?

Interest

Term

Conditions

+

_

Savings

Bank Account

Variable and Low

No term

Can open with small amount

Low monthly fee,no risk

Low interest

Certificate of Deposit

Bank Account

Fixed, a bit higher

Fixed Term

Need larger amount to open

Higher interest, Compounds daily

Penalty if withdrawn early

Stocks

Shares in a company

Pays dividends

No term

Can be bought and sold in the market at any time

Produces highest return on average

Risk (short-term market fluctuation)

Types of Saving/Investment Products

� Savings accounts � Allow you to withdraw as needed; also called share accounts

at a credit union.

� CDs – certificate of deposit� pays you interest over a specified period of time; penalties for

early withdrawal; usually pays higher interest than a savings account since you lock your funds away for a specific time period.

� Money market funds � a savings account with a minimum balance; usually tied to

changing market interest rates. The fund itself buys short-term money-market assets and then pays out interest on the shares you hold.

Types of Saving/Investment Products� Stocks

� You buy a share of a company; you gain ownership in that company; you then share in the profit of that company via dividends; and you can also gain based on a capital gain (i.e., you can sell your share for a higher price than you paid).

� Corporations issue stock in order to raise funds to invest in physical capital (e.g., new machinery, production processes, new technology, etc…)

� Corporate Bonds� You lend to a company by buying a bond; you earn interest on that bond as a

payment for loaning the funds to the company.� Corporations issue bonds in order to raise funds to invest in physical capital (as

above with stocks).� The bond is the corporation’s written pledge to repay a specified amount of money

with interest.

� Government Bonds� You lend to the government by buying a government bond.� The bond is the written pledge of a government or municipality to repay a specified

sum of money along with interest.� These are often very liquid (trade a lot) and usually have low risk of default.

Financial Assets:

Types of Saving/Investment Products

Mutual Funds � A mutual fund pools money together from a bunch of small investors

to buy stocks, bonds, other financial securities. � You can buy small shares of lots of different stocks and bonds by

purchasing a share in a mutual fund. � Funds can be weighted toward particular types of assets:

� Bonds, Municipal bonds, Balanced funds, Stocks, and Growth funds.

� Funds may focus on a specific investment strategy� Income, growth, income and growth.

� Or have a specific investment objective� Green funds - made up of shares of companies that are green or

environmentally friendly.� Social justice funds - made up of shares of companies that someone has

deemed as socially beneficial.

Financial Assets:

Types of Saving/Investment Products� Diversification

� Spread the risk of loss in a variety of savings and investment options. � “don’t put all your eggs in one basket.”

� Mutual funds offer automatic diversification � Buying one share of the mutual fund gets you a percentage of all the various

companies in which that fund invests. Compare this to buying one share of one company, which doesn’t offer you any diversification (if that stock falls, you lose money).

� You can buy shares in a mutual fund via a bank or other financial institution or directly online.

� Look for no-load funds or check to see that you’re getting something in return for any fees charged.

Setting financial goals� SMART goals

� Specific, significant, stretching

� Measurable, meaningful, motivational

� Attainable, agreed-upon, action-oriented

� Realistic, rewarding

� Time-based, timely

� Talking about finances

� Emotions matter

46

Setting financial goalsSetting financial goals for multiple timeframes (and following through on them)

is an important step on your path to financial freedom.

Timeframe Time Horizon

Dollar Amount Description Action to be taken

Short-Term (0-2 years)

IntermediateTerm (2-5 years)

Longer Term (5+ years)

Example 4 months $200 Save for an upcoming vacation

Put away $50 from the next 4 paychecks

Go do it now!� Start tracking expenses.

� Set up a budget.

� Check your credit report.

� Set a financial goal and take a specific step toward that goal.

� Start saving!

Some Online Resources� Financial planning

� https://www.ubs.com/microsites/ubs-financial-wellness-center/en/home.html

� https://www.mint.com/� https://www.wisconsin.edu/ohrwd/americasaves/� https://www.wisconsin.edu/ohrwd/benefits/download/ret/financial-

wellness-plan.pdf

� Life insurance calculator:� https://web1.lifebenefits.com/sites/lbwem/home/insurance-

basics/insurance-needs-calculator#

� UW System benefits� https://www.wisconsin.edu/ohrwd/benefits/� https://www.wisconsin.edu/ohrwd/benefits/download/summaries/fasl

� UWM benefits links:� http://uwm.edu/hr/home/benefits/current-employee-benefits/� https://uwservice.wisconsin.edu/help/wrs-benefits-statement.php

Some Online Resources

� My page

� Excel versions of the expense tracking worksheet, budget worksheet, balance sheet worksheet.

� Word version of the financial goals worksheet.

� http://people.uwm.edu/rneumann/

Passing on financial skills to the next generation

� Talk about finances!

� Make a Difference – Wisconsin

� http://makeadifferencewisconsin.org/

� Empowers teenagers with financial literacy educational resources and real-world lessons.

� Engaging volunteers, dynamic schools, and generous supporters share a vision of stronger communities built by an investment in “money smart” teens.

Related Documents