Presented by D. Sykes Wilford Chief Investment Officer Bankers Trust Company Private Bank Implications of Changing Sources of Revenues in the Banking Industry Forces of Change in International Banking

Presented by D. Sykes Wilford Chief Investment Officer Bankers Trust Company Private Bank Implications of Changing Sources of Revenues in the Banking Industry.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presented by D. Sykes Wilford

Chief Investment OfficerBankers Trust Company

Private Bank

Implications of Changing Sources of Revenues in theBanking Industry

Forces of Change in International Banking

OBJECTIVES

Examine how managers make investment decisions in banks

Draw conclusions about the structure of those investment decisions under different Accounting systems.

Raise implications for individual bank risks and where they are taken.

Examine how managers react to regulations.

Draw some conclusions about the riskiness of the system.

ASSUMPTIONS

Shares are widely held in portfolios.

Banks operate in a lenders of last resort system.

It is difficult to "take-over" a bank.

The Bank has access to capital.

LENDER OF LAST RESORT

The Moral Hazard Issue

Lenders have a put on the Authorities

BANK FCA

Duration Mismatched

4% Spread

Positive Cash Flowwith any accountingsystem

8%

A L

LOL's

Loans12%

BANK FCA

Duration Mismatched

4% Spread but Negative

Negative Cash Flow

Under MTM probably in default

16%

A L

LOL's

Loans12%

Lenders have no incentive to place controlson managers

Equity holders want to maximize the valuesof their shares

The Government has the Risk

THE FCA PROBLEM

CAPITAL STRUCTURE AS OPTIONS

Equity

Debt

Value of the Firm

Value of the Firm

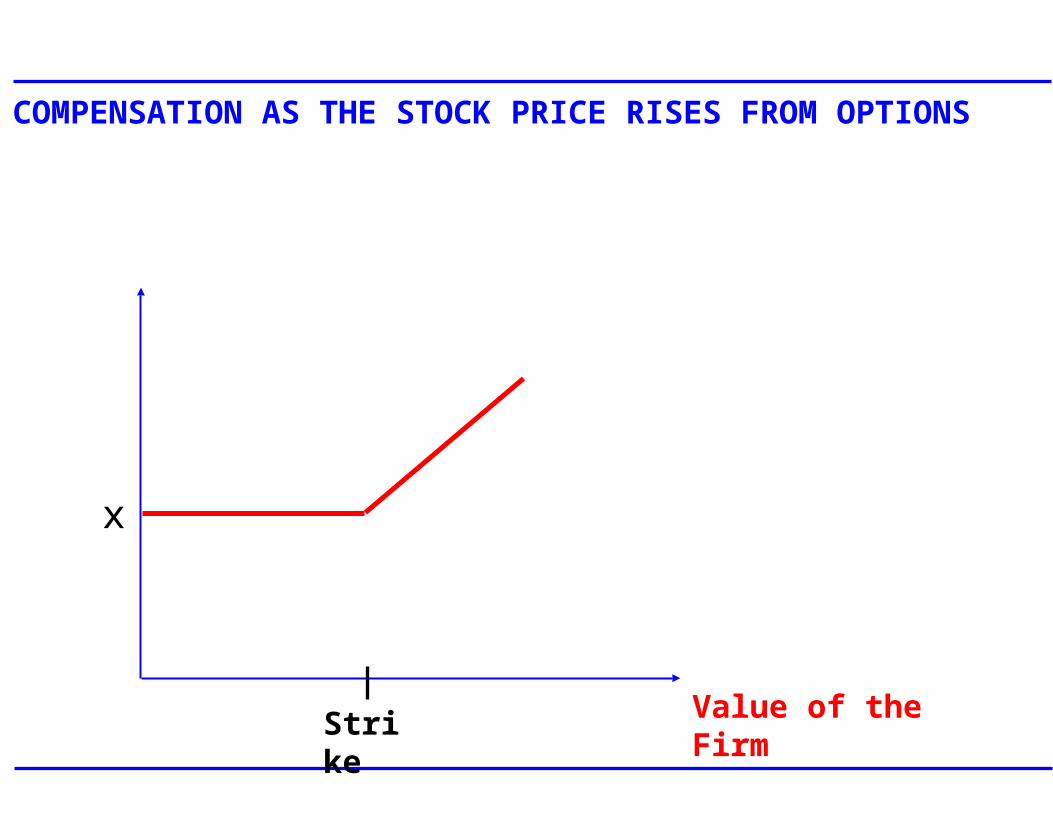

Equity holders maximize their call optionby taking Risk.

This implies the put holders has greater potential Loss.

VALUING THE CALL

Equity Holders

Risk A

Risk B

LENDERS RISK

Does not change under A or B

The Government has written thelenders a Put

Lenders do not monitor Risk

Base Salary

Stock

Stock Options

Accounting Based

MANAGER'S COMPENSATION

Compensation

COMPENSATION AS THE STOCK PRICE RISES FROM OPTIONS

x

Strike Value of the Firm

CHANGE IN COMPENSATION AS THE STOCK PRICE MOVES

Base Salary(-) (+)

Value of the Firm

COMPENSATION FROM ACCOUNTING EARNINGS

Value of the Accounting Earnings

Base

Compensation

ACCOUNTING BASED COMPENSATION

Volatility Implications

Accounting System MTM

Non-MTM

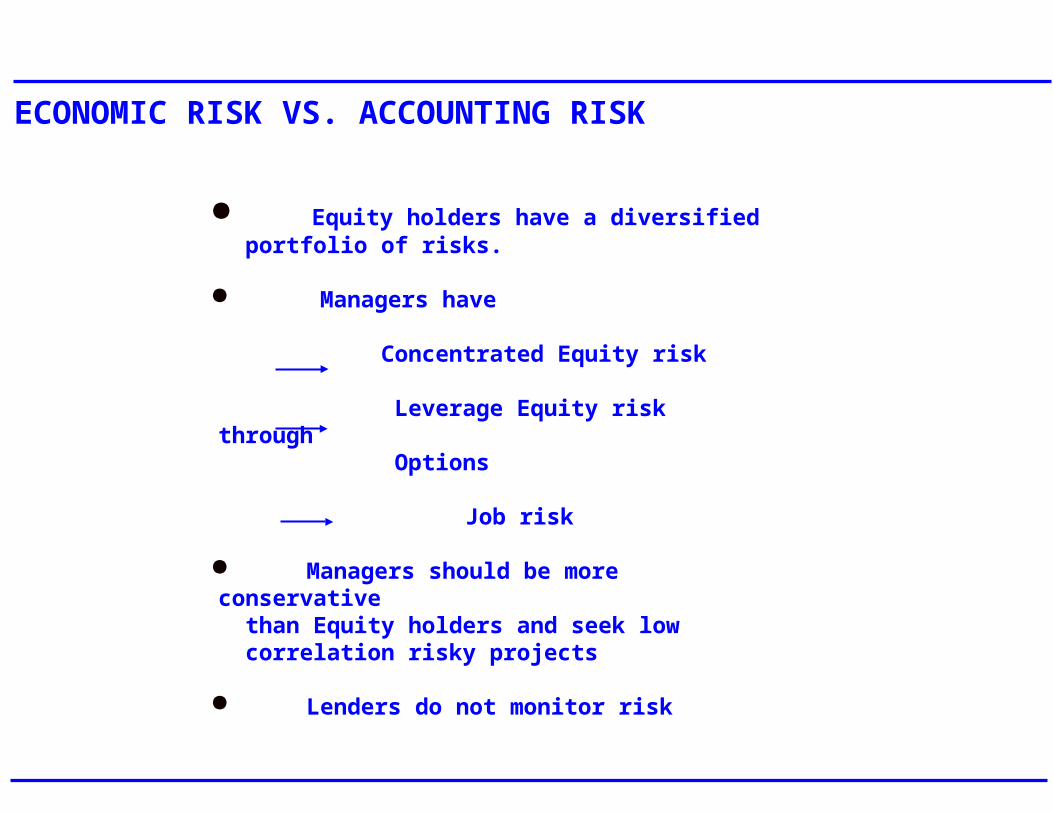

ECONOMIC RISK VS. ACCOUNTING RISK

MTM

Volatility the same for Managers and Shareholders

Accounting Risk based compensation similar to Equity Options

Maximize individual project risk but look at correlation of risks to protect Equity value.

Equity holders have a diversified portfolio of risks.

Managers have

Concentrated Equity risk Leverage Equity risk through Options

Job risk

Managers should be more conservative than Equity holders and seek low correlation risky projects

Lenders do not monitor risk

ECONOMIC RISK VS. ACCOUNTING RISK

EQUITY HOLDERS VERSUS MANAGERS

Riskiness for managers under Non-MTM Accounting

Share holders and Managers incentives differ

Accounting Period Risk

Shareholder Risk

E(R)

MANAGER'S INCENTIVES

Take more economic risk

Push risk into future accounting periods

Take profits to maximize bonuses

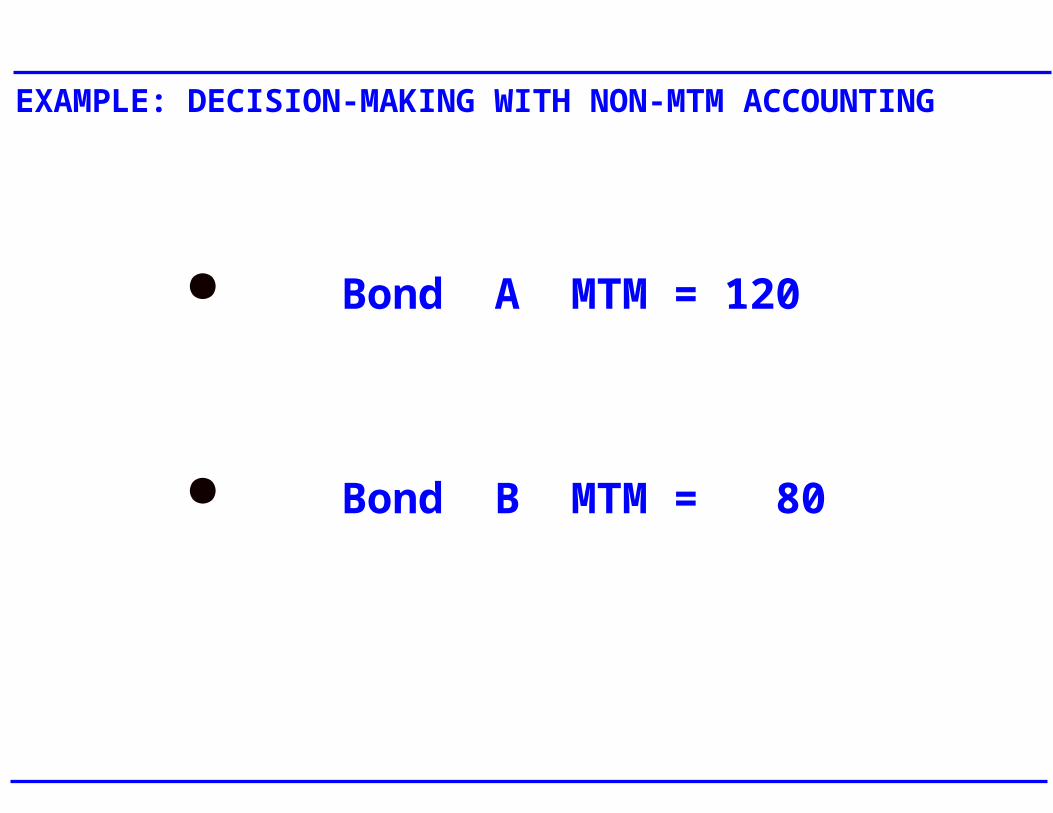

Bond A MTM = 120

Bond B MTM = 80

EXAMPLE: DECISION-MAKING WITH NON-MTM ACCOUNTING

EXAMPLE: DECISION-MAKING WITH NON-MTM ACCOUNTING

Base

Accounting IncomeSell Bond B Sell Bond A

EXAMPLE: DECISION-MAKING WITH NON-MTM ACCOUNTING

Managers own the option on the timing to sell a valuable asset

Managers can leverage their income by moving risk across time

Managers want to maximize the value of this option

Non-MTM accounting dominates

X = Accounting Value Needed to be bonusableY = Level of loan portfolio equal to MTM value

AccountingLoan Value

Accounting Value of LoanPortfolio if income can betaken at manager's discretion

Time

X

t0MTM Value atTime Zero

VALUE OF THE PORTFOLIO INCOME AT ACCOUNTING LEVEL X

MTM ACCOUNTING

Shareholder risk closer to Manager's risk

Managers can diversify risk by choosing low correlation projects

Managers face downside risk

Managers tend to reduce exposures near the end of an accounting period

NON-MTM ACCOUNTING

Managers tend to leverage more to maximize their accounting bonus

Managers can take more concentrated risk The need to diversify risks are reduced

Managers will move risks across accounting dates where possible

Losses will be concentrated in "Bad Years"

REGULATORS MUST BEWARE

Non-MTM accounting and government debt vs. equity

Non-MTM accounting of Debt and MTM accounting of trading activities Inexperienced regulators

Concentrations of Risk

CONCLUSIONS

Managers take new projects to maximize income

Non-MTM projects are superior to MTM projects

Manager increases economic risk when Non-MTM accounting allows near term period risk to be reduced

Managers shift risks across time by selective selling and buying in the investment portfolio with no MTM.

CONCLUSIONS

Managers and Share holders

Have their risks better lined up under MTM accounting

Managers will tend to take less risk thanShareholders under MTM accounting

Managers will desire to diversify risks whenshareholders will not under MTM accounting

Lenders still don't care

CONCLUSIONS

Regulators

Have an incentive to reduce riskiness

May increase concentration of risk throughcertain capital adequacy rules

Often intimidate management by not understandingthe value of diversification

May raise risk by differential accountingprocedures

May promote system risk by imposing measure forcapital adequacy under a system of "Lender of last resort"

Related Documents