The Affordable Care Act / Internal Revenue Service 6055 & 6056 Reporting for Applicable Large Employers

Presented by: Colleen Doherty, SPHR SVP, Compliance & Client Services Eastern Benefits Group [email protected] 508-923-2442 What do I.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Affordable Care Act / Internal Revenue Service6055 & 6056 Reporting for

Applicable Large Employers

2

Presented by:

Colleen Doherty, SPHRSVP, Compliance & Client ServicesEastern Benefits [email protected]

What do I need to know about 6055 & 6056

reporting?

Tony MurphySVP, SalesEastern Benefits [email protected]

So now what do I do?Do I need “a system”?What are my options?

3

WARNING!!

4

5

You might be tempted…

6

Or maybe event take a little nap…

This stuff is really important!

But Don’t!

7

We’ve got an app for that!

EBG Anti-Nap App

Show of hands…

10

INTERNAL REVENUE SERVICE CODE SECTIONS 6055 & 6056

11

6055Health Plan Info

• Applies to all health plan issuers (health insurance carriers) & self-insured health plans

• Tells the IRS which individuals have minimum essential coverage (MEC)

• Required to administer the Individual Mandate

6056ALE Offer of Coverage Info

• Applies to all ALEs • Employers must report cost,

coverage (MEC and Minimum Value - MV) & eligibility info for all Full Time Employees

• Separate statements for each Full Time employee

• Required to administer the Employer Mandate

Health Plan Issuer Employer

12

Minimum Value (MV) PlansMinimum Essential Coverage (MEC)

Minimum Value (MV) Plan

Health plan is expected to pay out on average at least 60% of claims.

Minimum Essential Coverage (MEC)

Virtually any health insurance plan that does not consist solely of “excepted benefits”. Does not need to provide minimum value (MV).

Minimum Value(MV)

Minimum Essential Coverage

(MEC)

5 Reporting Forms Released

1095-AHealth Insurance Marketplace Statement

To be used by state and federal Exchanges only.

1094-BTransmittal of Health Coverage Information Returns

1095-BHealth Coverage

To be used by “issuers”.

Health insurance carriers and self insured health plans that are NOT ALEs.

1094-CTransmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns

1095-CEmployer-Provided Health Insurance Offer and Coverage

To be used by all ALEs

13

We have final instructions & forms for 2014

20142015 forms could change.

14

15

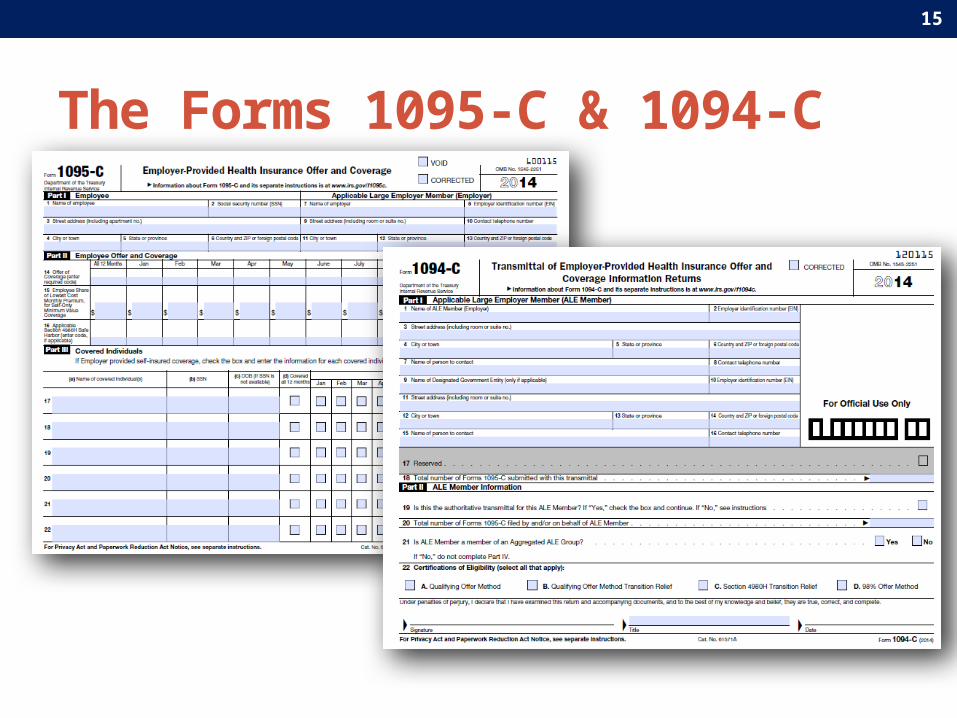

The Forms 1095-C & 1094-C

16

6055 & 6056 Reporting• ALL ALEs ARE REQUIRED TO COMPLETE 6056

REPORTING• ALL ALEs WITH SELF-INSURED PLANS ARE ALSO

REQUIRED TO COMPLETE 6055 REPORTING• 6055 & 6056 combined reporting for ALES with self-insured plans

• Insurance carriers will do 6055 reporting for fully insured plans (EEs will get 2 statements)

• There is no “transition relief” for reporting purposes• Reporting based on full calendar year 2015

17

6055 & 6056 Paper or Electronic Reporting to IRS

PAPER & MAILSmaller Employers Only

(<250 returns)

ELECTRONICRequired for Larger Employers (250+ returns)

Optional for Smaller Employers

Less than 250 returns

18

Reporting Due Dates• Reporting Period is 1/1/2015 – 12/31/2015• All EE reports are due to EEs by 1/31/2016 • All employer reports are due to the IRS:

• End of February 2016 – if you file manually/paper• End of March 2016 for all other ALEs (including smaller employers

that choose to file electronically)

19

Before we get to the forms…

Let’s take a brief look at…

• Employer Shared Responsibility (ESR) Penalties• (also known as “PAY OR PLAY”)

• ESR Transition Relief• Full Time Employees

20

EMPLOYER SHARED RESPONSIBILITY (ESR) ASSESSMENTSAKA – Pay or Play Penalties

21

Employer Shared Responsibility Assessments(AKA – Pay or Play Penalties)

4980H(a)Non-Providing Employer Assessment

• ALEs• MEC• 95% of FT EEs (70% 2015)

• $166.67/mo. ($2k annualized)

• All ACA FT EEs (30 hours/week)

• Minus first 80 2015 / Minus first 30 2016+

4980H(b)Providing Employer Assessment

• ALEs• MV (60% actuarial value)

• Affordable (9.5% )

• $250/mo. ($3k annualized)

• Each ACA FT EE that receives subsidized Exchange Coverage

At least one FT employee must obtain coverage via Exchange / Marketplace – and receive premium tax sharing or cost sharing subsidies in order to trigger either penalty.

Penalties are non tax deductible. Gross up by your tax rate.

A B

22

Penalty Amounts Are Subject To Indexing

2014 4980H A Penalty $2,000 / 12 = $166.67 monthly

??? 2015 (4.2% Increase)

2015 4980H A Penalty

$2,000 * 1.042 = $2,184

$173.67 monthly

2014 4980H B Penalty $3,000 / 12 = $250.00 monthly

??? 2015 (4.2% Increase)

2015 4980H B Penalty

$3,000 * 1.042 = $3,126

$260.50 monthly

There is no actual 2014 Penalty.

2015 Penalty Amounts Based on Indexing? Not released by IRS yet.

Waiver Forms Are Crucial To Avoid “A” Penalties!

24

TRANSITION RELIEFDelayed Penalty Assessments – for Some ALEs

But not delayed reporting!

RELIEF

ACA

RELIEF

RELIEF

RELIEF

25

Transition Relief From Penalty Start Date of January 1, 2015 – For Some Employers

A. Medium Size Employers*

B. Non-Calendar Year Plans*

C. Individual Employees*

Delay for some!* But…

only if transition relief conditions

are met.

26

ESR Assessment Transition Relief for Medium Size Employers (50-99) 2015Employer may qualify for relief from potential penalty assessments in 2015 if…

Limited Workforce Size

Using the same rules to determine ALE status – employer has at least 50 but fewer than 100 employees (including full time equivalent employees) on business days during 2014.

Maintenance of Workforce and Aggregate Hours of Service

During the period beginning on February 9, 2014, and ending on December 31, 2014, the employer does not reduce the size of its workforce or the overall hours of service of its employees in order to satisfy the workforce size condition (50 to 99 employees).

Maintenance of Previously Offered Health Coverage

During the coverage maintenance period the employer does not eliminate or materially reduce the health coverage or employer contribution, if any, it offered as of February 9, 2014. The “coverage maintenance period” means the period beginning on February 9, 2014, and ending on the last day of the plan year that begins in 2015.

Certification of Eligibility for Transition Relief

Must certify on IRS Form 1094-C that it meets the eligibility requirements listed above.

27

ESR Assessment Transition Relief for Non-Calendar Year Plans

All Employees Test

• The non-calendar year plan(s) covered at least one-quarter of the large employer’s employees as of any date in the 12 months ending on Feb. 9, 2014; or

• At least one-third of the large employer’s employees were offered coverage under the non-calendar year plan(s) during the most recent open enrollment period before Feb. 9, 2014.

ACA Full Time Employees Test

• The non-calendar year plan(s) covered at least one-third of the large employer’s full-time employees as of any date in the 12 months ending on Feb. 9, 2014; or

• At least one-half of the large employer’s full-time employees were offered coverage under the non-calendar year plan or plans during the most recent open enrollment period before Feb. 9, 2014.

If your plan meets either of these condition tests – ESR assessments will not begin until the start of your plan year – rather than 1/1.Note – plan year means your 5500 filing plan year.

OR

28

An easier way to look at this…

Non-Calendar Year Transition ReliefDid you…? All Employees Full Time Employees

Cover:as of any date in the 12

months prior toFeb. 9, 2014

1/4 1/3

Offer to:during the most recent open enrollment period

before Feb. 9, 2014. 1/3 1/2

29

ESR Assessment Transition Relief for Individual EmployeesBased on Pre 2015 Eligibility Rules• For Non Calendar Year Plans (aka Fiscal Year Plans)• Regardless of hire date• Would the employee have been eligible for coverage based on your

plan eligibility rules that were in effect on February 9, 2014?• If so, transition relief applies for that employee• Assessments, if any, would begin as of plan year date for that specific

employee.

30

Affordable & Minimum Value

In addition to the rules previously discussed…

In order to take advantage of transitional relief for a delay in any applicable penalties – the coverage offered as of the first day of the plan year in 2015 must be both affordable and meet minimum value requirements.

Affordable:Meets one of 3 possible EE

affordability Safe Harbors: W-2, Rate of Pay or FPL

Minimum ValuePlan expected to pay out at least

60% of claim costs incurred

31

You must know how to accurately identify your ACA

full time employees!

FT = 130 per month

(30 hours per week on average)

Variable Hour Employees!!

YOU NEED TO KNOW WHO YOUR ACA FULL TIME EMPLOYEES ARE

130 HOURS / MONTH

30 HOURS / WEEK

Seasonal, Part Time, Per Diem, Variable Hour, Temporary…Look Back Measurement Periods?

In order to accurately file with the IRS – you need to properly identify who your FT employees are. You also need to know this for your own

ESR assessment planning purposes.

Be sure to carefully look at All Non-Eligible Employees• All employers should especially careful to verify ACA full

time status for employees that are not offered eligibility in the employer sponsored health plan.

Failure to offer coverage to an employee that

should be deemed full time under the ACA can result in

large penalties for an employer!

Measurement Periods(Initial & Standard)

Initial PeriodsStrictly for newly hired employees when an employer cannot reasonably determine full time status at date of hire (i.e., seasonal & variable hour ee’s).

• Initial Look Back / Measurement Period

• Initial Administrative Period

• Initial Stability Period

Standard PeriodsFor “Ongoing Employees”

• Standard Look Back / Measurement Period

• Standard Administrative Period

• Standard Stability Period

New Hires All Ongoing Employees

Measurement (aka Look Back) Period

Under the look-back period safe harbor method, an employer will determine each employee’s full-time status by looking back at a defined period of not less than 3 but not more than 12 consecutive calendar months, as chosen by the employer to determine whether during the measurement period the employee averaged at least 30 hours of service per week.

Test & Plan For Look Back PeriodsBill Field's Seaside Bar & Grill

First Name 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 523

Mo. Avg.

6 Mo. Avg.

9 Mo. Avg.

12 Mo. Avg.

Anton 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40Lenny 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40Meaghan 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40Germaine 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40Tyree 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40 40Darin 20 24 28 35 35 35 20 20 35 35 35 20 20 0 0 20 20 20 20 20 20 20 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 26.9 25.6 26.2Jade 40 40 16 16 16 16 16 16 0 16 16 16 16 32 32 16 16 16 16 16 16 16 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 16 16 16 16 16 16 16 16 16 16 16 16 16 16 24.9 25.2 23.5Jasper 40 40 16 16 16 16 16 16 24 16 16 16 16 32 32 16 16 16 16 16 16 16 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 16 16 16 16 16 16 16 16 16 16 16 16 16 16 24.9 25.2 24Kraig 20 24 28 35 35 35 20 20 35 35 35 20 20 0 0 20 20 20 20 20 20 20 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 26.9 25.6 26.2

Antione 28 21 21 28 28 21 35 35 35 35 28 28 35 35 35 35 28 28 28 35 21 28 40 40 40 40 40 40 40 40 40 40 40 40 40 28 28 28 28 28 21 21 21 21 21 21 21 21 21 21 21 21 21.6 28.9 30.4 30.1

Dorian 20 24 28 35 35 35 20 20 35 35 35 20 20 0 0 20 20 20 20 20 20 20 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 26.9 25.6 26.2Nikolas 56 40 16 16 16 16 16 16 0 16 16 16 16 32 32 16 16 16 16 16 16 16 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 16 16 16 16 16 16 16 16 16 16 32 40 56 19.3 28 27.3 25.4Randal 56 40 16 16 16 16 16 16 0 16 16 16 16 32 32 16 16 16 16 16 16 16 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 16 16 16 16 16 16 16 16 16 16 16 16 56 16 26.5 26.3 24.6

Sebastian 20 24 28 35 35 35 20 20 35 35 35 20 20 0 0 20 20 20 20 20 20 20 40 40 40 40 40 40 40 40 40 40 40 40 40 20 20 20 20 32 32 32 32 32 32 32 20 20 20 20 20 20 27 30.2 27.8 27.8

January 1 - March 31 April 1 - June 30 July 1 - September 30 October 1 - December 31

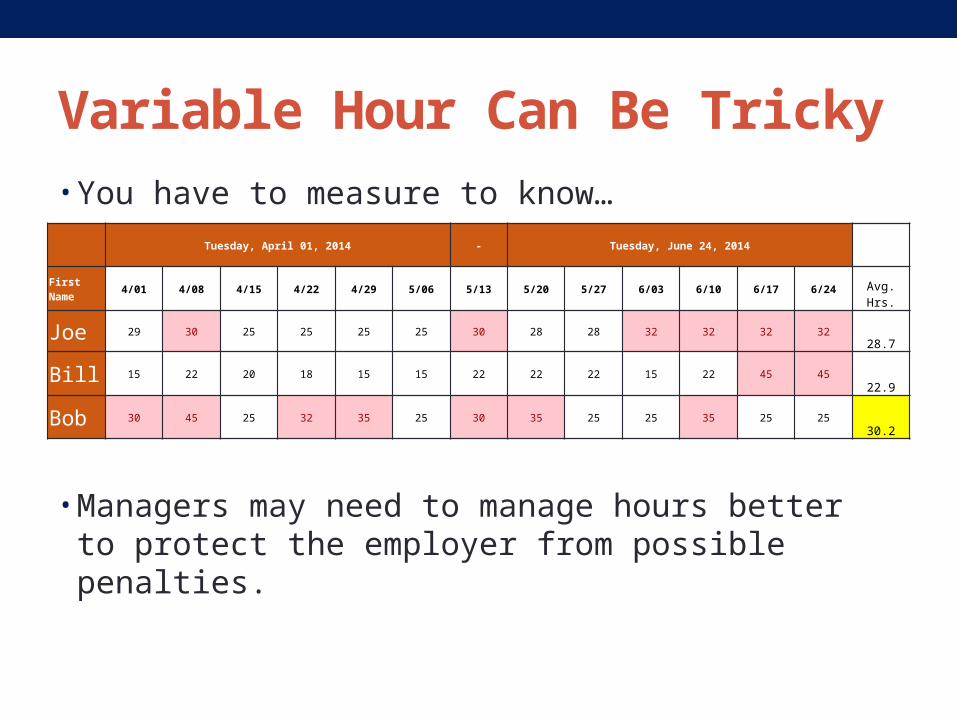

Variable Hour Can Be Tricky• You have to measure to know…

• Managers may need to manage hours better to protect the employer from possible penalties.

Tuesday, April 01, 2014 - Tuesday, June 24, 2014

First Name 4/01 4/08 4/15 4/22 4/29 5/06 5/13 5/20 5/27 6/03 6/10 6/17 6/24

Avg. Hrs.

Joe 29 30 25 25 25 25 30 28 28 32 32 32 3228.7

Bill 15 22 20 18 15 15 22 22 22 15 22 45 4522.9

Bob 30 45 25 32 35 25 30 35 25 25 35 25 2530.2

An Employer Must Consider…• Working Hours: Each hour for which the employee is paid, or

entitled to payment, for the performance of duties for the employer; and

• Non-working Hours: Each hour for which an employee is paid, or entitled to payment, by the employer on account of a period of time during which no duties are performed due to vacation, holiday, illness, incapacity (including disability), layoff, jury duty, military leave or leave of absence.

Think of this as hours worked – and / or paid when determining eligibility in the measurement period.

Rehired Employees and Employees Returning from Leave

For an employee who is treated as a continuing employee, the measurement and stability periods that would have applied to the employee had he or she not experienced the break in service would continue to apply upon the employee’s resumption of service.

Rule of Parity for Rehires & EEs returning from leave

• EEs with breaks of 13+ weeks can be treated as new• Except teachers = 26 weeks before can treat as new

• EEs with breaks of <13 weeks - may use “Rule of Parity”

“Special Unpaid Leave”FMLA Leave, USERRA Leave and Jury Duty

Under the averaging method, the employer either:

• Determines the average hours of service per week for the employee during the measurement period excluding the special unpaid leave period and uses that average as the average for the entire measurement period; or

• Treats employees as credited with hours of service for special unpaid leave at a rate equal to the average weekly rate at which the employee was credited with hours of service during the weeks in the measurement period that are not special unpaid leave.

Your tracking system must have a way to account for these types of unpaid / non-working hours!

Note on “Seasonal”Seasonal Worker vs. Seasonal Employee

Terminology:

• The term Seasonal Workers is used for determining ALE status.

• The term Seasonal Employees is used for FT Employee status during the look back period. • An employee who is hired into a position for which the customary annual

employment is six months or less. The period of employment should begin each calendar year in approximately the same part of the year, such as summer or winter. In certain unusual instances, the employee can still be considered a seasonal employee even if the seasonal employment is extended in a particular year beyond its customary duration (regardless of whether the customary duration is six months or is less than six months). ACA Seasonal employees do not subject an employer to ESR assessments.

Administrative & Stability Periods

Administrative Periods• Up to 3 Months following MP to determine FT status and make offer

of coverage• Only 1 Month Admin Period allowed if using 12 Month Measurement

Period.

Stability Periods• Follows measurement and admin period• Period during which EE is eligible for coverage• Must be at least 6 Months long and match your measurement period.• Employers choosing measurement periods of less than 6 months

would still have to offer a stability period of 6 months.

Measurement Period Examples

2014 2015 2016 2017J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Ex: start MP on 7/1/14 Measurement Admin StabilityNext MP starts on 1/1/15 Measurement Admin Stability

Next MP starts on 7/1/15 Measurement Admin StabilityNext MP starts on 1/1/16 Measurement Admin Stability

6-3-66 Month Look Back Measurement Period3 Month Administrative Period6 Month Stability Period

Non-Calendar Year Example

Measurement Period Examples6-2-6 (6 month look back period, 2 month admin period, 6 month stability period)

2014 2015 2016 2017J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Ex: start MP on 7/1/14 Measurement Admin StabilityNext MP starts on 1/1/2015 Measurement Admin Stability

Next MP starts on 7/1/2015 Measurement Admin StabilityNext MP starts on 1/1/2016 Measurement Admin Stability

6-1-6 (6 month look back period, 1 month admin period, 6 month stability period)

2014 2015 2016 2017J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Ex: start MP on 7/1/14 Measurement A StabilityNext MP starts on 1/1/15 Measurement A Stability

Next MP starts on 7/1/15 Measurement A StabilityNext MP starts on 1/1/16 Measurement A Stability

Non-Calendar Year Example

Measurement Period Examples12-1-1212 Month Look Back Measurement Period1 Month Administrative Period12 Month Stability Period

2014 2015 2016 2017J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Measurement A StabilityNext MP starts 1/1/15 Measurement A Stability

The ACA has a rule that says a FT EE cannot wait more than 13 months to be offered coverage. So an employer using a 12 Month Measurement Period – could NOT use a 3 Month

Administrative Period.

Non-Calendar Year Example

2014 2015 2016J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Meas Admin StabilityMeas Admin Stability

Meas Admin StabilityMeas Admin Stability

Meas Admin StabilityMeas Admin Stability

Meas Admin Stability

Measurement Period Examples

3-3-6Measurement Periods of less than 6 months are generally not recommended due to administrative burden and complexity.

EBG typically recommends 6 or 12 Month measurement

periods.

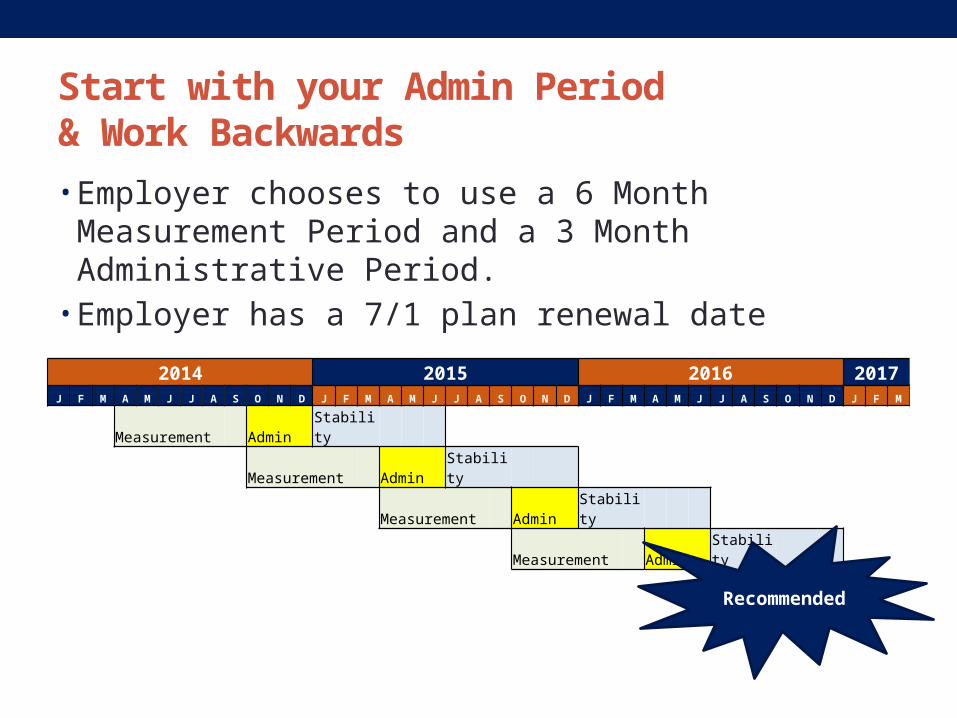

Start with your Admin Period & Work Backwards• Employer chooses to use a 6 Month Measurement Period

and a 3 Month Administrative Period.• Employer has a 7/1 plan renewal date

2014 2015 2016 2017J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Measurement Admin Stability Measurement Admin Stability

Measurement Admin Stability Measurement Admin Stability

Recommended

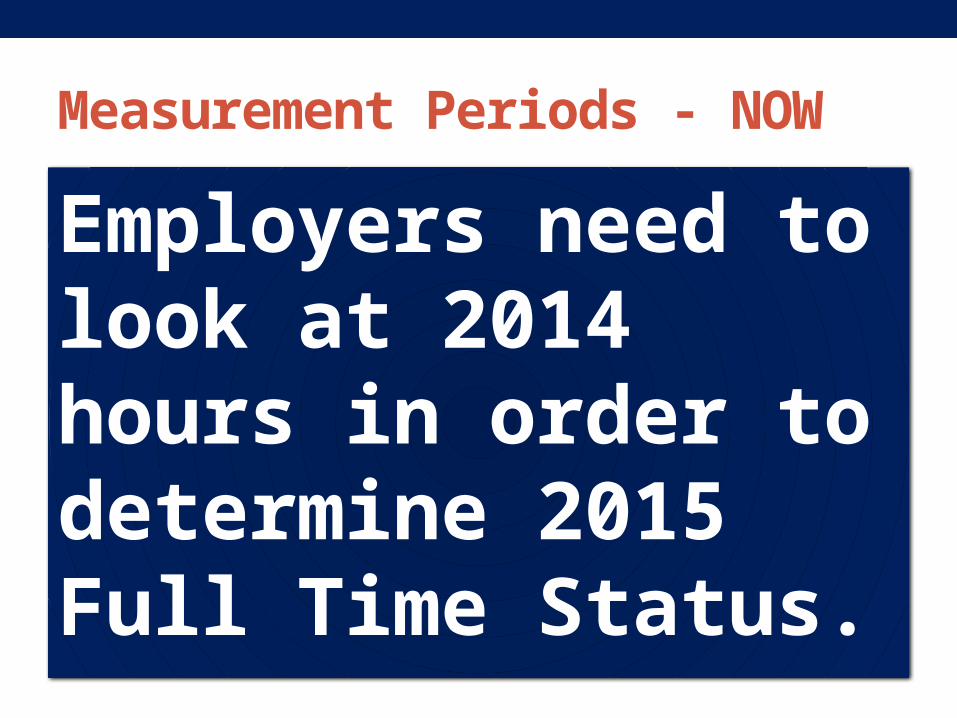

Measurement Periods - NOW

Employers need to look at 2014 hours in order to determine 2015 Full Time Status.

Look Back Transition Relief

Employers that intend to utilize the look-back measurement method for determining full-time

status for 2015 will need to begin their measurement periods in 2014 to have

corresponding stability periods in 2015.

The IRS recognizes that employers that intend to adopt a 12-month measurement period and a

12-month stability period will face time constraints.

Special Rule…

Solely for purposes of stability periods beginning in 2015, employers may adopt a shorter transition measurement period that:

• Is less than 12 months, but not less than 6 months long; and• Begins no later than July 1, 2014, and ends no earlier than 90 days

before the first day of the first plan year beginning on or after Jan. 1, 2015.

This will be helpful to employers with non-calendar year plans that wish to use a 12 Month Measurement Period.

Or, for a calendar year with no administrative period.

51

NOW LET’S GET TO THE FORMS

1095-CPart I

Lines 1 – 13

Basic Employer & Employee Information

Part II (6056 Info)

Lines 14 – 16

Offer, Coverage & Cost Information

Part III (6055 Info)

Lines 17 – 22

Covered Individuals Information (Part III is for self-insured plans only)

52

Goes to each person that was employed as FT for at least 1 month during the calendar year.

Self-Insured ALEs also have to report on ANYONE covered under the plan during the year.

53

54

1095-C – Part I

Basic Info

55

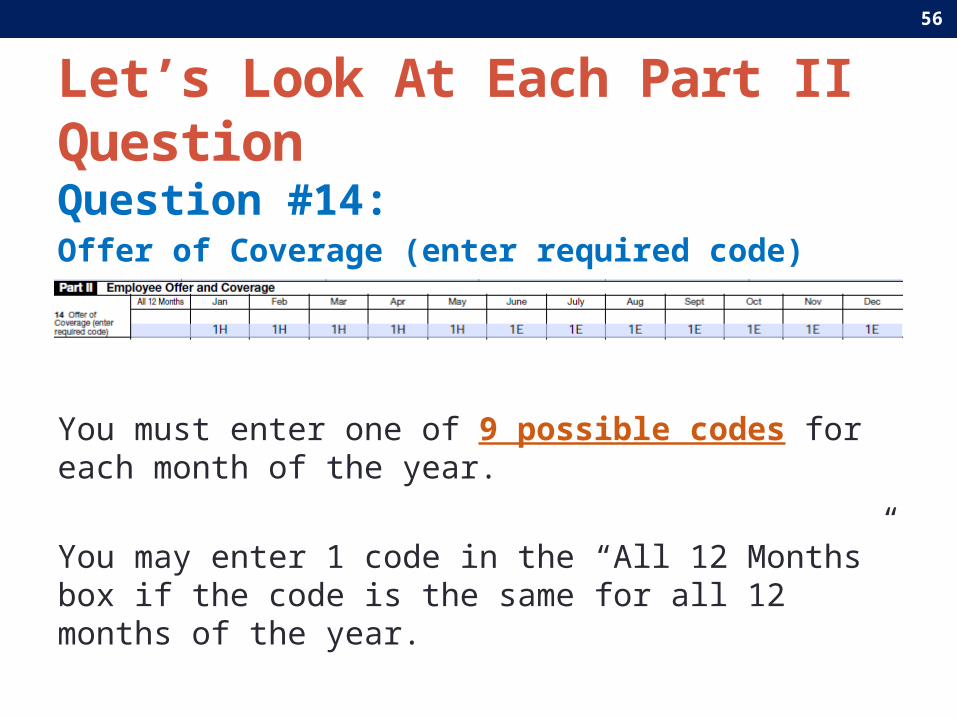

1095-C Part II

3 Questions – 2 sets of “Indicator Codes”

Data will likely be different for many employees.

56

Let’s Look At Each Part II Question

Question #14: Offer of Coverage (enter required code)

You must enter one of 9 possible codes for each month of the year.

You may enter 1 code in the “All 12 Months” box if the code is the same for all 12 months of the year.

9 Possible Codes for Line 14 (1A – 1I)

1. 1A. Qualifying Offer: Minimum essential coverage providing minimum value offered to full-time employee with employee contribution for self-only coverage equal to or less than 9.5%mainland single federal poverty line and at least minimum essential coverage offered to spouse and dependent(s).

2. 1B. Minimum essential coverage providing minimum value offered to employee only.

3. 1C. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to dependent(s) (not spouse).

4. 1D. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to spouse (not dependent(s)).

5. 1E. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to dependent(s) and spouse.

6. 1F. Minimum essential coverage NOT providing minimum value offered to employee, or employee and spouse or dependent(s), or employee, spouse and dependents.

7. 1G. Offer of coverage to employee who was not a full-time employee for any month of the calendar year and who enrolled in self-insured coverage for one or more months of the calendar year.

8. 1H. No offer of coverage (employee not offered any health coverage or employee offered coverage that is not minimum essential coverage).

9. 1I. Qualifying Offer Transition Relief 2015: Employee (and spouse or dependents) received no offer of coverage, received an offer that is not a qualifying offer, or received a qualifying offer for less than 12 months.

57

58

1A – Qualifying Offer

Minimum essential coverage providing minimum value offered to full-time employee with employee contribution for self-only coverage equal to or less than 9.5%mainland single federal poverty line (FPL) and at least minimum essential coverage offered to spouse and dependent(s).

In order to meet the mainland FPL affordability test the employee’s monthly cost of coverage for the employer’s lowest cost MV/MEC plan can be no more than $93.17 per month in 2015.

1B, 1C & 1D1B. Minimum essential coverage providing minimum value offered to employee only.

1C. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to dependent(s) (not spouse).

59

1D. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to spouse (not dependent(s)).

60

1E – MV/MEC Offer of Coverage

Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to dependent(s) and spouse.

For most employers that offer coverage – this will be the most common code used.

1F, 1G & 1H1F. Minimum essential coverage NOT providing minimum value offered to employee, or employee and spouse or dependent(s), or employee, spouse and dependents

1G. Offer of coverage to employee who was not a full-time employee for any month of the calendar year and who enrolled in self-insured coverage for one or more months of the calendar year.

(Example: COBRA or PT eligible EE)

61

1H. No offer of coverage (employee not offered any health coverage or employee offered coverage that is not minimum essential coverage).

This code may be used often – especially during a new FT EE’s waiting period and first year of employment.

62

1I – Qualifying Offer Trans. Relief

1I. Qualifying Offer Transition Relief 2015: Employee (and spouse or dependents) received no offer of coverage, received an offer that is not a qualifying offer, or received a qualifying offer for less than 12 months.

We’ll cover this a bit later in the program.

Not likely to be used by many employers.

63

Let’s Look At Each Part II Question

Question #15: Employee Share of Lowest Cost Monthly premium for Self-Only Minimum Value Coverage

You may enter 1 amount in the “All 12 Months” box if the EE cost is the same for all 12 months of the year.

Leave blank for months in which no offer of coverage is made.

64

Let’s Look At Each Part II Question

Question #16: Applicable Section 4980H Safe Harbor

(enter code if applicable)

You may enter one of 9 possible codes for each month of the year – only if applicable.

You may enter 1 code in the “All 12 Months” box if the code is the same for all 12 months of the year.

Leave blank if no safe harbor code applies.

1.2A. Employee not employed during the month.

2.2B. Employee not a full-time employee.

3.2C. Employee enrolled in coverage offered. *

4.2D. Employee in a section 4980H(b) Limited Non-Assessment Period.

5.2E. Multiemployer interim rule relief. *

6.2F. Section 4980H affordability Form W-2 safe harbor.

7.2G. Section 4980H affordability federal poverty line safe harbor.

8.2H. Section 4980H affordability rate of pay safe harbor.

9.2I. Non-calendar year transition relief applies to this employee.

* Takes precedence over other applicable codes.

9 Possible Codes for Line 16 (2A – 2I)

65

66

Q #16: Ordering Rules

It is possible that more than one rule is applicable. The IRS has issued “ordering rules” to tell us which code should take precedent over another.

2CEmployee enrolled in coverage

offered. Even if other safe harbors apply during that month –

if the EE is enrolled in the employer’s plan – use 2C.

2EMultiemployer interim rule relief. If the employee is covered under a collective bargaining agreement and the employer contributes to a

multiemployer plan – use 2E.

67

Part III – Self Insured Employers OnlyCovered Individuals (Dependents)

• 1095-C Part III is for employers with self insured coverage only!• Need to add info for any covered dependents.• Name, SSN & Months Covered.

(If SSN is not available a DOB may be used after at least 1 initial + 2 documented attempts to get the SSN.)

Now you’re done with the employee’s 1095-C!

6055 Reporting – Don’t forget non-EEs!!!!

68

LET’S LOOK AT SOME COMPLETED SAMPLE FORMS 1095-C

69

SIMPLE – PLAIN VANILLA

Example #1

John has been an executive at XYZ Co. for 5 years. He makes a very good salary. His plan is affordable based on his salary. He covers himself and his dependents for the entire calendar year.

70

IF XYZ Co. had a fully insured group health plan – Part III

would be left blank.

71

1E – Employee was offered coverage for the

entire yearEE Cost for Self Only Coverage

Lowest MV/MEC2C – EE enrolled in plan

for entire year

Self-Insured Plan Dependents

Covered

72

A LITTLE MORE COMPLEX

Example #2

George is a full time college student . He works 30 hours per week (nights/weekends) at XYZ Co. He earns $9 per hour and was hired on March 15, 2015. He’s eligible for XYZ’s insurance but opts not to take it. The insurance is not affordable to him based on his earnings. No affordability safe harbors apply.

73

74

1H – Employee was hired on 3/15/2015 and was NOT offered

coverage until 1st of month following 60 days after DOH (6/1)

1E – EE and dependents (if any) offered coverage on June 1 after EE completes waiting

period.

EE Cost for Self-Only coverage inserted only in months where

coverage was offered.

2A - Employee not employed during the month

2D - Employee in a section 4980H(b) Limited Non-Assessment Period. Blank - EE did not enroll in

coverage and there are no affordability safe harbors

because EE makes $9/hr.

75

UNION EMPLOYEE COVERED BY A MULTIEMPLOYER PLAN

Example #3

Homer belongs to the Local 123 (union). He started to work at Springfield Nuclear on 7/1/2015. Homer is eligible for – and participates in – Local 123’s multiemployer health plan. Springfield Nuclear is required to contribute towards the cost of Homer’s coverage under a collective bargaining agreement. (Springfield offers a fully insured group health plan to its other non-union employees.)

76

77

1H. No offer of coverage (employee not offered any health coverage or employee offered coverage that is not minimum essential coverage).

1E. Minimum essential coverage providing minimum value offered to employee and at least minimum essential coverage offered to dependent(s) and spouse.

2A. Employee not employed during the month.

2E. Multiemployer interim rule relief.

78

Multiemployer Plans (Unions)Important Note

If an employer contributes to a multiemployer plan as part of a collective bargaining agreement for a FT employee:

The multiemployer plan administrator will be responsible for 6055 reporting via Form 1095-B. The employer must still file Form 1095-C and complete Parts I & II only for the employee

The employer may claim to make an offer of coverage and use Code 2E provided that:• the multiemployer plan offers dependent coverage;• the multiemployer plan provides minimum value coverage; and• the coverage is affordable.

79

In order for an employer to use Code 2E for union employees…

The employer must have certification from the multiemployer plan administrator that its plan meets:

MEC

MV

Covers Dependents

Is Affordable

80

1094-CThe ALE “Transmittal Form” for 1095-C

TransmittalForm

81

1094-C Transmittal Form – 3 pages

82

83

84

85

NOW LET’S TRY COMPLETING THE 1094-CThe transmittal form

86

Mary H.R. Executive January 28, 2016

350

87

Q: 22 – Certifications of Eligibility

Qualifying Offer Method

Qualifying Offer Transition Relief

Section 4980(H) Transition Relief(Codes A & B if applicable)

98% Offer Method

88

Alternative MethodsQuestionable Convenience?

RARE BIRD

REPORTING BASED ON CERTIFICATION OF QUALIFYING OFFERS

Applies with respect to an ALE that certifies on its transmittal form that it offered certain coverage (a qualifying offer) to one or more of its full-time employees. A “qualifying offer” occurs when, for all months during the year in which the employee was a full-time employee with respect to whom an employer shared responsibility penalty could apply, the ALE:

Offers MEC providing minimum value at an employee cost for self-only coverage of less than 9.5 percent of the mainland single federal poverty line to one or more of its full-time employees; and

Offers MEC to the employee’s spouses and dependents.

For employees who received a qualifying offer for all 12 months of the calendar year, the ALE will be treated as complying with Section 6056 if it takes the following two steps:

1. Report simplified Section 6056 return information with respect to those employees. The ALE will file Form 1095-C with the IRS, providing only the employee’s name, SSN and address, and indicating (using the Qualifying Offer code 1A) that a qualifying offer was made for all 12 months of the calendar year. The ALE also will not report the dollar amount for any month for the employee’s share of the lowest cost monthly premium for self-only coverage providing minimum value offered to that employee. An employer may not, for any month, use code 1A and also report this dollar amount.

2. Provide a simplified employee statement in lieu of a copy of the Form 1095-C to each full-time employee who received a qualifying offer for all 12 months. This statement must include the employer’s name, address and EIN, and must inform the employee that the employee (and his or her spouse and dependents, if any) received a qualifying offer for all 12 months of the calendar year, and therefore are generally ineligible for a premium tax credit for all of those 12 months. In addition, this statement must direct the employee to see IRS Publication 974, Premium Tax Credit (PTC) (currently in draft form), for more information on eligibility for the premium tax credit.

However, an employer may not provide a simplified employee statement in lieu of a copy of the Form 1095-C for any full-time employee who enrolled in self-insured coverage, regardless of whether the employee received a qualifying offer for all 12 months. The employer must furnish the information reporting enrollment in the self-insured coverage reported on Form 1095-C, Part III. For these employees, the employer may furnish a copy of Form 1095-C as filed with the IRS (with or without the statement described above).

For each employee who received a qualifying offer for fewer than 12 months, the ALE will use the general reporting method. However, the ALE may use code 1A to report for months in which a qualifying offer was received.

QUALIFYING OFFER METHOD TRANSITION RELIEF FOR 2015

The final rule also includes transition relief in 2015 for ALEs that certify on the transmittal that they have made a qualifying offer to at least 95 percent of their full-time employees (and their spouses and dependents).

Generally, employers will have to use the general method of reporting for any employees that did not receive a qualifying offer for all 12 months. However, solely for 2015, ALEs that have made a qualifying offer to at least 95 percent of their full-time employees (and their spouses and dependents) will be treated as complying with Section 6056 if they take the two simplified steps listed above. However, in this case, employers will use either:

The Qualifying Offer code 1A for any months for which the employee received a qualifying offer; or

The Qualifying Offer Method Transition Relief code 1I for any months for which the employee did not receive a qualifying offer.

An employer may not, for any month, use code 1A or code 1I and also report the dollar amount for the employee’s share of the lowest cost monthly premium for self-only coverage providing minimum value.

In addition, the simplified employee statement will vary based on whether the employee received a qualifying offer for all, some or no months of the calendar year.

If the qualifying offer applied to an employee for all 12 months of the calendar year, the statement will inform the employee that the employee (and the employee’s spouse and dependents, if any) will not be eligible to claim a premium tax credit for any of the 12 calendar months.

If the qualifying offer did not apply to an employee for all 12 months, the statement will inform the employee that the employee (and his or her spouse and dependents) may be eligible to claim a premium tax credit for one or more of the 12 calendar months. The statement must also include a name and telephone number that the employee can contact for further information regarding the offer of coverage.

91REPORTING BASED ON CERTIFICATION OF 98 PERCENT OFFERS

This alternative method applies with respect to an ALE that certifies on its transmittal form that it:

Offered MEC that is affordable and provides minimum value to at least 98 percent of its full-time employees on whom it reports in its Section 6056 return; and

Offered MEC to those employees’ dependents.

For this purpose, coverage is treated as affordable if the cost of employee-only coverage satisfies any applicable affordability safe harbor under the employer shared responsibility final regulations.

This alternative method allows eligible ALEs to provide Section 6056 reporting without determining whether each employee offered coverage is a full-time employee or specifying the number of the employer’s full-time employees. Under this alternative method, the employer does not have to provide its full-time employee count on Form 1094-C.

This alternative method is designed to ensure that the employer has offered coverage to “substantially all” of its full-time employees, and therefore is not subject to an employer shared responsibility penalty, without having to know which reported employees are full-time and which are part-time.

Although this alternative method allows reporting without identifying or specifying the number of full-time employees, it does not exempt the employer from any penalties that might apply for failure to report with respect to any full-time employee. Thus, reporting is still required under the normal rules for all full-time employees, including those not offered coverage.

92

Call your trusted advisor first

If you plan on using any of the alternative reporting methods:• Broker• Attorney• Tax Professional• Consultant

CD Opinion: The “simplification” rules are so convoluted that they will not be worthwhile (or applicable) for most employers. I see the possibility for many errors and only recommend the general reporting method at this time.

93

94

Indicator Codes for Form 1094-C

Codes for Section 4980H Transition Relief Indicator -- Form 1094-C Part III, Column (e)

A 50-99 Transition Relief

(ALEs with fewer than 100 full-time employees)

B 100 or more Transition Relief

(ALEs with 100 or more full-time employees)

95

For Controlled Groups & Affiliated Service Groups.

(I.e., Multiple Companies sharing

common ownership.)

96

VOLUNTARY FILING FOR 2014File in 2015 for Calendar Year 2014

97

Voluntary 2014 Filing

Employers that wish to file voluntarily for 2014 may do so in 2015 just to check out the system.

May be a good way to test your own systems of tracking and reporting.

Unfortunately – electronic filing system is not ready yet.

Are you ready?

98

6055 & 6056 IRS REPORTING PENALTIES

99

PenaltiesFailure to Report or Correct Information 6055 & 6056

$30 - $100 per failure (i.e., per employee return)

Under section 6724(d), as amended by the Affordable Care Act, an applicable large employer that fails to comply with the filing and statement furnishing requirements of section 6056 may be subject to penalties for failure to file a correct information return (section 6721) and failure to furnish correct payee statements (section 6722).

However, these penalties may be waived if the failure is due to reasonable cause and not to willful neglect (section 6724). http://www.law.cornell.edu/uscode/text/26/6721

http://www.irs.gov/irb/2014-13_IRB/ar08.html

Always consult a tax professional!

The Future of Obamacare

Will it be repealed?

101

Supreme Court Decision - June

102

TRACKING & REPORTING:YOUR OPTIONS FOR 6055 &

6056 COMPLIANCE

103

You Are Probably Thinking…

1. What information will I need?

2. Do I have all the information and where can I get it?

3. Will I need a system or can I manage this myself?

4. How much time will time will this take?1. HR

2. Payroll

3. Management

4. IT

5. I better start this now.

104

What information will I need? …

Hours of Service

Eligibility

Offer of Coverage Contributions

Wages

Safe Harbor Employee Enrollment

Spousal & Dependent Enrollment

Spousal & Dependent

Social

105

Do I have all this information? …

Where can I gather this information? …

• Most employers have some but not all of this information• Data will come from Multiple Resources

106

Source of Data

Excel / Manual

Spreadsheet

Payroll Company Reports

HRIS / Benefits Admin System

TPA / Insurance

Carrier Reports

One system or maybe a combination of all 4?

107

Insurance Carriers

Options for Employer Reporting

108

Spreadsheet / Mail Merge

Payroll ACA

HRIS / Benefits Administration System

Stand Alone Software

Options for Employer Reporting

109

Can you track and report without purchasing a new ACA reporting system?Yes. It may be time consuming but it can be done.• Depending upon the size and complexity of your workforce• Resources – time, money & knowledge

Manual System

110

OPTION 1MANUAL SPREADSHEET TRACKING

111-

-Smaller employer

-Low turnover

-No Variable Hour

-Inexpensive

-No system required

-Manual Process

-Coordinate data source

-Proper use of codes

-Time Consuming

-Must Maintain Data

-No alerts

EMPLOYER TYPE ADVANTAGES

DISADVANTAGES DISADVANTAGES

112

I think I may need a system• Not all systems are created equal

• Does your technology partner have the resources• When will they be ready• Can they track old data• Is the data being tracked correctly

• Protected Leave and Paid/Not Worked• FMLA, Jury Duty, Military, Paid Sick Time, Holiday

• Consider your goals for a system• ACA Reporting only• Measuring Eligibility and Affordability• Engage employees• Streamline and automate benefit enrollment process• Employer owns data• Carrier agnostic

113

OPTION 2PAYROLL VENDOR

114

-

-Mid to Large employer

-Full Time and/or Variable Hour

-Centralized Data

-Utilizes Existing infrastructure

-Measures Eligibility

-Measure Affordability

-Call to action alerts

-May require system upgrade and 90 to 120 day implementation

-Additional cost

-Import additional data sets

EMPLOYER TYPE ADVANTAGES

ADVANTAGES DISADVANTAGES

115

OPTION 3HRIS OR BENEFITS ADMIN PLATFORM

116

-

-Mid to Large employer

-Full Time and/or Variable Hour

-Automated web enrollment

-Connects HR, Payroll & Carrier

-Measures Eligibility

-Measure Affordability

-Call to Action Alerts

-Increased Employee Engagement and Self-Service

-Payroll Agnostic System

-90 to 120 day implementation

-Additional costs may apply

-Integration of multiple systems

EMPLOYER TYPE ADVANTAGES

ADVANTAGES DISADVANTAGES

117

OPTION 4STAND ALONE SOFTWARE PROGRAM

118

-

-Large employer 1,000+

-Full Time and/or Variable Hour

-Scrubs data and identifies gaps

-Connects fractured data

-Measures Eligibility

-Measure Affordability

-Call to Action Alerts

-Lengthy implementation

-Significant costs

-Mono-line product

EMPLOYER TYPE ADVANTAGES

ADVANTAGES DISADVANTAGES

119

RESOURCESAVAILABLE FROM

EASTERN BENEFITS GROUP

120

Proprietary Document

Eastern Payroll Concierge

Benefit Administration

Stand Alone Software(Tango, HealthyFX, Equifax)

121

Electronic Filing: IRS Publication 5165 UNDER DEVELOPMENT

Affordable Care Act (ACA) Information Returns (AIR)

AIR Guide (IRS Publication 5165)

for Software Developers and Transmitters

122

THINGS TO DO

123

Questions to Ask Your VendorsWill our Payroll / HRIS / Benefits Admin System be able to…

• Capture all required data for 6056 (& 6055 if self-insured) reporting?• Produce completed Forms 1094-C & 1095-C?• Track and calculate hours to determine who is / is not a full time employee? • Apply look back measurement, administrative & stability periods?• Notify you if someone becomes FT?• Measure and report on plan affordability for all 3 employee affordability safe harbor methods?• Accurately apply transitional relief rules?• Mail 1095-Cs to employee homes?• File 1094-C & 1095-C with IRS?

How much will it cost? When will it be ready?

Can we integrate / feed data from multiple systems if necessary?

What new fields will be added to our system(s) and when/how do I put this data into our system?

How much lead time do we need to prepare?

How much of our own estimated labor time will be required to comply with these new reporting requirements?

124

Need more help? Half Day ACA Reporting Workshops

• ATTEND A HALF DAY COMPLIMENTARY WORKSHOP• HANDS-ON / INTERACTIVE• LEARN HOW OTHER EMPLOYERS ARE HANDLING ACA• 8 ATTENDEES MAXIMUM PER SESSION• EBG WAKEFIELD, MA OFFICE

These are pilot program sessions. More sessions may be offered in other locations in May & June.

Date Morning 8:30 – 12:30 Afternoon 1:00 – 5:00

Tue., 4/28/2015 Session 1 Session 2

Wed., 4/29/2015 Session 3 Session 4

Thu., 4/30/2015 Session 5 Session 6

125

ACHCA Members Only

If there is enough interest…

We would be happy to conduct workshops specifically for ACHCA members.

Contact Tony Murphy

781-581-4212

126

QUESTIONS?Colleen Doherty, SPHR

SVP, Compliance & Client Services

Eastern Benefits Group

508-923-2442

?Tony Murphy

SVP, Sales

Eastern Benefits Group

781-581-4212

127

Thank you!

Related Documents